credit suisse first boston 2003 asian investment conference stuart grimshaw chief financial officer...

Post on 18-Dec-2015

213 views

TRANSCRIPT

Credit Suisse First Boston2003 Asian Investment Conference

Stuart Grimshaw

Chief Financial Officer

25-28 March 2003

www.commbank.com.au

2

The material that follows is a presentation of general background information about the Bank’s activities current at the date of the presentation, 25 March 2003. It is information given in summary form and does not purport to be complete. It is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. These should be considered, with or without professional advice when deciding if an investment is appropriate.

Disclaimer

3

Speaker’s Notes

Speaker’s notes for this presentation are attached below each slide.

To access them, you may need to save the slides in PowerPoint and view/print in “notes view.”

4

Agenda

Commonwealth Bank in the Current Context

Platforms for Growth

Productivity

Commonwealth Bank in the Current Context

6

Australia’s Economy has been relatively resilient given global conditions

Source: Commonwealth Research

-10

0

10

20

30

Jul-97 Jul-98 Jul-99 Jul-00 Jul-01 Jul-02

-10

0

10

20

30

% %

Housing

Business

Otherpersonal

CREDIT: 3 Month-ended Annual Rates

-3 0 3 6 9

% change

ECONOMIC GROWTH: 2002

ChinaSouth KoreaThailandNew ZealandAustraliaIndonesiaTaiwanCanadaUnited StatesSingaporeHong KongSpainSwedenUnited KingdomNorwayFranceBelgiumItalyGermany

Netherlands

SwitzerlandJapan

7

Domestic housing demand has been strong

Source: Commonwealth Research, Melbourne Institute

-3% -2% -1% 0% 1%

Income (+1%)

Mortgage rate (up 1%)

Unemploymentrate (up 1%)

Investmentreturns (+1%)

House Price Sensitivity (% deviation from baseline)

Income ($'000pa)

5

10

15

20

<30 31-50 51-70 71-100 >100

%Debt Repayment Levels: % household income(Melbourne Institute)

0

20

40

60

Sep-79 Sep-85 Sep-91 Sep-97

Deposit-takinginstitutions

Realestate

Shares

%Wisest Place for New Savings? (Melbourne Institute)

Sep-02

200

250

300

350

400

Jul-99 Jul-00 Jul-01 Jul-02

Quarterly

Monthly

$'000Established House Prices (national)

Jul-03

8

Business confidence has been subdued, but is expected to gain momentum

Source: Commonwealth Research

CAPEX(annual % change)

-30

-15

0

15

30

1988/89 1991/92 1994/95 1997/98 2000/01 2003/04

-30

-15

0

15

30

% %

CBA (f)

INVESTMENT ACTIVITY*(cumulative % contribution, 2001 base yr)

-5 0 5 10

Agriculture

Mining

Manufacturing

Construction

Wholesale

Retail

Transport & storage

Finance & insurance

Prop. & bus. services

Cult. & other services

Gov administration

Health & comm.

Other

* Jan 2003

9

0

1000

2000

3000

4000

5000

6000

7000

Jun-02 Sep-02 Dec-02Industry Commonwealth Bank

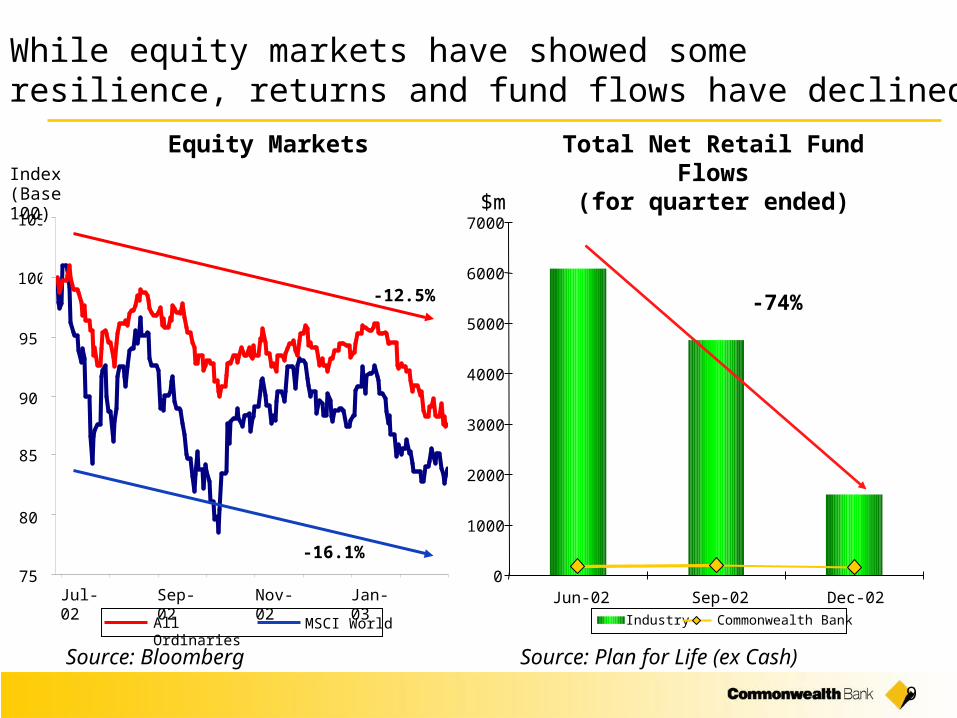

While equity markets have showed some resilience, returns and fund flows have declined

$m

Total Net Retail Fund Flows(for quarter ended)

Source: Plan for Life (ex Cash)

-74%

Equity Markets

Source: Bloomberg

75

80

85

90

95

100

105

Jul-02 Sep-02 Nov-02 Jan-03

-12.5%

-16.1%

All Ordinaries MSCI World

Index (Base 100)

10

Commonwealth Bank’s 1st Half result reflects modest growth in an uncertain environment

Net Profit After Tax (cash basis)*

Comprising: Banking Funds Management Life Insurance

Dec 2002

$1,208m

$1,079m$135m($6m)

Dec 2001

$1,192m

% Change

1%

* ie excluding appraisal value uplift/reduction and goodwill amortisation. Unless otherwise stated the numbers in this presentation refer to the net profit after tax (cash basis) and all comparisons are to the prior comparative period.

$1,092m$186m

$31m

11%(26%)

(117%)

11

4%

5%

6%

7%

8%

9%

10%

11%

Dec 2001 Jun 2002 Dec 2002

0.007

0.008

0.009

0.01

0.011

0.012

Mar-00

Sep-00

Mar-01

Sep-01

Mar-02

Sep-02

0

0.002

0.004

0.006

0.008

0.01

Mar-00

Sep-00

Mar-01

Sep-01

Mar-02

Sep-02

CBA ANZ NAB WBC

The Bank’s credit quality and capital adequacy strengthened during the half

Tier 1 Capital Tier 2 Capital Target Range

9.31%9.80% 9.81%

6.75% 6.78% 7.06%

Capital Adequacy RatiosBad Debt Expense to RWA*

General Provision to RWA

% R

WA

% R

WA

*RWA: risk weighted assets

12

The Bank’s dividend payout ratio remains high relative to peers

Dividends per Share

Dividend Payout Ratio

Dec 2002

69cps

72.7%

95cps

12.39%

52.6%

Dec 2001

68cps

72.6%

94cps

12.43%

54.2%

Change

1c

-

1c

(4bps)

(3%)

Earnings per Share

Return on Equity

Banking Cost to Income Ratio (underlying basis)

…and EPS has improved

For more detail, visit: www.commbank.com.au/shareholder

13

Increasing leveraging from key competitive strengths is important for long term growth

Scale

Brand

Risk Profile

Products and Businesses

Distribution

Innovation

People

Platforms for Growth: Banking

15

%

Customer Share: All Relationships

Source: Research International, December 2002

The Bank is a leading player in the Australian market

1st in Home Lending

1st in Credit Cards

1st in Retail Deposits

1st in Online Broking

Strong in Business Lending

Largest customer base

Most points of access

Best known bank brand

0

10

20

30

40

50

Dec-01 Jun-02 Dec-02

CBA WBC

ANZ NAB

Credit Unions St George

16

Several key trends are shaping the future of the home loan market

Economic Environment

• Interest rates at historical lows - but affordability has weakened• Slowing housing credit demand likely• Historically low credit losses• Property sector attractive compared to other asset classes

Customer Need

• Entrenched fast repayment psyche• First home buying activity brought forward by FHOG* - weaker demand likely •Defined service demands• Wealth creation mindset has fuelled investment loan growth but expect to be tempered by economic uncertainty

Distribution

• Mortgage brokers well established - but facing first slowdown in demand • Continued market consolidation likely• Linkages likely to intensify to financial planners - increased competition

Technology

• Broker groups also investing in front end & CRM** solutions • Centralised back end models utilising straight through processing• Intensification in use of CRM type solutions - owned and rented• Increased use of IVR***/web for customer servicing requests and marketing

Competitive Environment

• Mortgage market a high demand sector • Low credit losses - increasing willingness by some market participants to take on risk • Slowing housing credit demand - propensity for increased poaching/ refinancing offers, including increasing commissions to third parties

***IVR: interactive voice recognition

**CRM: customer relationship management*FHOG: First Home Owner’s Grant

17

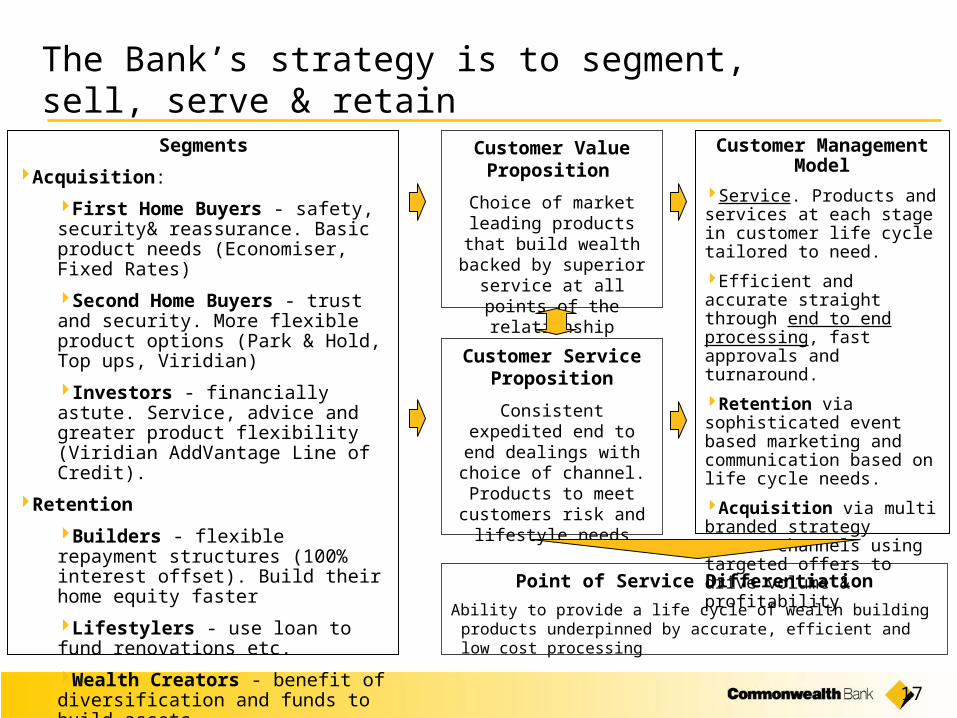

The Bank’s strategy is to segment, sell, serve & retain

Segments

Acquisition:

First Home Buyers - safety, security& reassurance. Basic product needs (Economiser, Fixed Rates)

Second Home Buyers - trust and security. More flexible product options (Park & Hold, Top ups, Viridian)

Investors - financially astute. Service, advice and greater product flexibility (Viridian AddVantage Line of Credit).

Retention

Builders - flexible repayment structures (100% interest offset). Build their home equity faster

Lifestylers - use loan to fund renovations etc.

Wealth Creators - benefit of diversification and funds to build assets

Customer Value Proposition

Choice of market leading products that build wealth

backed by superior service at all points of the

relationship

Customer Management Model

Service. Products and services at each stage in customer life cycle tailored to need.

Efficient and accurate straight through end to end processing, fast approvals and turnaround.

Retention via sophisticated event based marketing and communication based on life cycle needs.

Acquisition via multi branded strategy across channels using targeted offers to drive volume & profitability

Customer Service Proposition

Consistent expedited end to end dealings with choice of channel. Products to meet

customers risk and lifestyle needs

Point of Service Differentiation

Ability to provide a life cycle of wealth building products underpinned by accurate, efficient and low cost processing

18

Share of wallet improving - cross-sell, retention and service initiatives are in train

Basis: If a customer has a relationship (as a main Financial Institution or otherwise) with an Financial Institution, what proportion of their holdings do they keep with that Financial Institution?

Share of Wallet by Financial Institution

Source: Research International, December 2002

4639 39

4738

3036 35

45 42 42 42 40 37 36 34

0

20

40

60

80

100

St GeorgeGroup

CBA Group NAB Group Suncorp WBC Group ING/MercMutual

ANZ Group Bendigo

%

2001

2002

19

Premium Customers: Offering a Differentiated Business Model

BankingPlatform

BrokingPlatform

Borrowing Services

Lending Services

Transactional Banking

Advisory Services

Direct Investment

Indirect Investment

Debt Products

Equity Products

Commercial Adviser

Personal Adviser

InvestmentAdviser

FinancialAdviser

Risk/InsuranceAdviser

Client

Primary Relationship ManagerSecondary Relationship Manager & specialised advice

20

Republic: Providing a comprehensive view of premium customers

Please note information on these data screens have been scrambled for privacy purposes

21

Republic: Providing a comprehensive view of premium customers

Please note information on these data screens have been scrambled for privacy purposes

22

Transforming Business and Corporate Banking

Transformation Agenda Structured In Three Phases

Completed

Status

1. Define and revitalise Business/Corporate Banking

2. Re-organise for success

3. Capture industry leadership

Underway

Parallel implementation with Phase 2

1

2

3

4

5

6

Initiatives

Segment clients and create differentiated business models to improve client service experience

Introduce streamlined credit processes

Lift performance of bottom quartile centres

Better align distribution footprint to client needs

Realise segment specific share targets

Build client service and sales skills

23

No change to credit standards

Owner OccupiedInvestment

$bn

Dec 01 Jun 02 Dec 02

Composition of Housing Portfolio

Consumer Portfolio Commercial Portfolio

Bad debt charge as annualised % of unsecured

lending balances

Bad debt charge as annualised % of secured

lending balances

Dec 01 Jun 02 Dec 02

0

20

40

60

80

100

0.0%

0.4%

0.8%

1.2%

1.6%

2.0%

2.4%

*CBA Equivalent Ratings

29 27 29

15 15 14

36 39 40

171920

0%

20%

40%

60%

80%

100%

AAA/AA* A BBB Other

60%invest.grade

Platforms for Growth: Funds Management

25

The Bank maintains its leadership position in Australian funds under management

Group Funds Under Management by Country of Source

December 2002

Australian Funds Under Management** by Asset ClassDecember 2002

Total Funds Under Management: $95bn

Consisting of: retail $52bnwholesale $38bnretail CMT* $5bn

Australian Funds Under Management: $72bn

Consisting of: retail $39bnwholesale $28bnretail CMT* $5bn

*CMT: cash management trust **Total funds managed in Australia, excluding Colonial First State Property

86%

7% 3% 3% 1%

Australia United Kingdom New Zealand

Hong Kong Singapore

37%

10%4%

1%

47%

1%

Australian shares International sharesListed property Fixed int/mortgages/cashAlternative investments Other

26

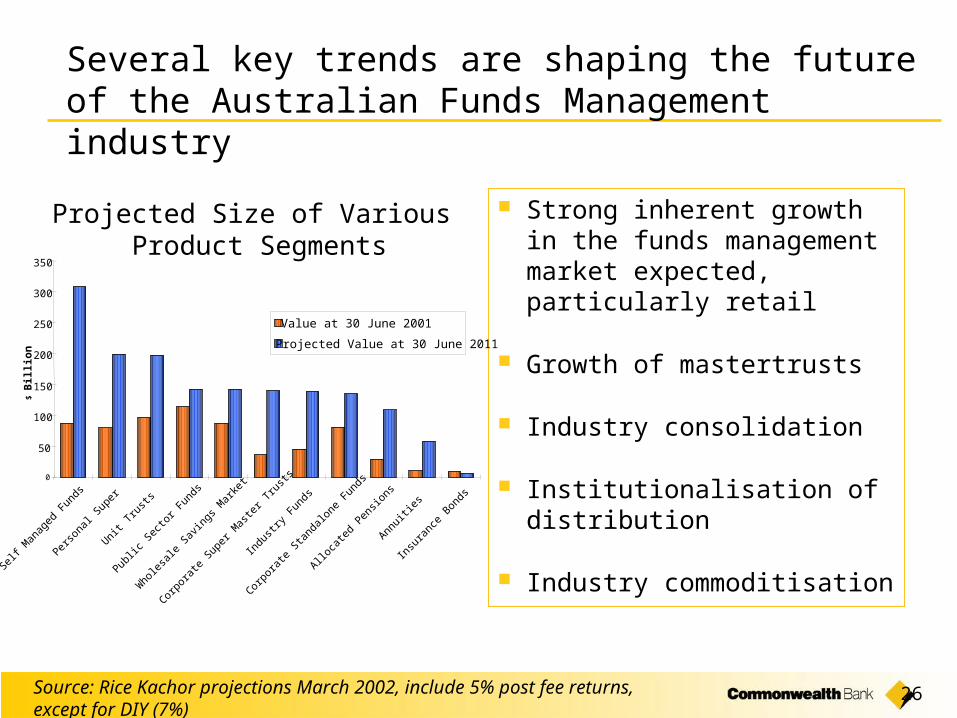

Several key trends are shaping the future of the Australian Funds Management industry

Strong inherent growth in the funds management market expected, particularly retail

Growth of mastertrusts

Industry consolidation

Institutionalisation of distribution

Industry commoditisation

Projected Size of Various Product Segments

Source: Rice Kachor projections March 2002, include 5% post fee returns, except for DIY (7%)

0

50

100

150

200

250

300

350

Self M

anag

ed F

unds

Perso

nal S

uper

Unit T

rust

s

Public

Sec

tor F

unds

Who

lesale

Sav

ings

Mar

ket

Corpo

rate

Sup

er M

aste

r Tru

sts

Indu

stry

Fun

ds

Corpo

rate

Sta

ndalo

ne F

unds

Alloca

ted

Pensio

ns

Annuit

ies

Insu

ranc

e Bon

ds

$ B

illi

on

Value at 30 June 2001

Projected Value at 30 June 2011

27

0

300

600

900

1200

1500

1800

May

-02

Jun-

02

Jul-0

2

Aug-0

2

Sep-0

2

Oct-02

Nov-0

2

Dec-0

2

FirstChoice - Cumulative Flows

FirstChoice has been further enhanced... and other initiatives are underway

$m

• Realise integration benefits, including further rationalisation of legacy systems

• Offer increased style diversification

• Leverage internal distribution opportunities

• Leverage scale to reduce costs

• Grow alternate asset classes

• Increase reputation as manager of international shares

FirstChoice Other Strategic Initiatives

Platforms for Growth: Life Insurance

29

The Bank has a strong presence in life insurance, and a number of opportunities

Source: Tillinghast, December 2002

By Channel

Market Size and Growth Prospects: By Product

$m

2002 2007 projected

2002 2007 projected

Commonwealth Bank Premiums: By Product

By Channel

0

800

1600

2400

3200

4000

4800

Term & Trauma Disability 3rd Party

0

800

1600

2400

3200

4000

4800

Direct Branch 3rd Party

Term & Trauma Disability Group

Direct Branch Other

30

Focus is on distribution, service and risk pricing

Increase internal distribution through PIC’s and BIM’s

Repricing of premiums

Upskilling of call centre staff

Product rationalisation

Systems migration

Productivity

32

Focus is on improving efficiency

...to achieve:

• A better service experience for customers, through greatly improved turnaround times

• Elimination of duplication and inefficiencies

• Annualised benefits of $159m, following an incremental net cost of ~$143m in FY2003

Four productivity initiatives...

Remove back-office functions from branches

Streamline Business Banking processes

Rationalise investment products & systems

Organisational design

Credit Suisse First Boston2003 Asian Investment Conference

Stuart Grimshaw

Chief Financial Officer

25-28 March 2003

www.commbank.com.au

34

9% growth in lending assets

Lending Assets**:

** Excludes securitised housing loan balances $5.9b (Dec 02), $7.0b (Jun 02), $5.7b (Dec 01).

Housing Personal Business & Corporate

$ bi

llion

Bank Acceptances

155 161169

80 86 94

988

55 5554

1213

12

0

50

100

150

200

Dec 2001 Jun 2002 Dec 2002

35

90

92

94

96

98

100

102

104

106

108

Dec-01FUM

Net Flows Investmentreturns

Other Underlying Gandel Winterthur CFS UKPrivate

Business

Dec-02FUM

A number of one offs impacted funds under management

$bn

106

95

98(1)

(5)

(2)

2 (4)

(1)

Underlying reduction of $8bn

One off reduction of net $3bn

36

Risk* GroupUnit Linked

Shareholder Funds in Life Insurance Companies: investment reflect underlying nature of the business

Income

$0.5 billion$2.1 billion

51%49%

Growth

$2.6 billion

74% 26%54% 46%

*Risk includes traditional, investment account, annuities, personal risk and group risk.

37

Dec 2001 Jun 2002 Dec 2002

Charge for Bad & DoubtfulDebts (6 months)

$290m $159m $151m

Charge for Bad & DoubtfulDebts to RWA (annualised)

0.42% 0.23% 0.21%

Gross Impaired Assets (netof interest reserved)

$983m $884m $863m

Specific Provisions $309m $270m $264m

General Provision $1,334m $1,356m $1,327m

General Provision to RWA 0.96% 0.96% 0.92%

Continuing sound asset quality

38

* Includes Colonial

$mill

ion

s

The Bank remains well provisioned

0

300

600

900

1,200

1,500

1,800

2,100

Dec94

Dec95

Dec96

Dec97

Dec98

Dec99

Dec00*

Dec01

Dec02

0

50

100

150

200

250

300

%

General Provision

Specific Provision

Total Provisions/Gross Impaired Assets (axis on right)

39

Arrears in consumer book remain at low levels

Loans Accruing past 90 days or more

30/06/01 31/12/01 30/06/02 31/12/02

$m $m $m $m

Housing Loans 218 168 176 136

Other Loans 90 79 73 75

Total 308 247 249 211

Housing loans arrears rate

30/06/01 31/12/01 30/06/02 31/12/02

Housing Loans accruingbut past 90 days or more $m 218 168 176 136

Housing loan balances $m 73,511 79,745 85,839 93,545

Arrears rate % 0.30% 0.21% 0.21% 0.15%

40

Commercial Portfolio: large exposures are mostly investment grade

Dec 2000

Dec 2001

Dec 2002

Top 20 exposures as a % of Total Committed Exposure

Committed Exposure ($m) 31 December 2002

Top 20 Exposures toCorporates (Committed)

0 200 400 600

BBB

A+

A

AA A

A-

A-

A+

A-

BBB

A+

S&

P R

atin

g o

r E

qu

ival

ent

BBB

A+

A+

BBB

A

BBB

AAA

BBB

A-

AA-

A-

A-

A+

A-

A-

BBB-

BBB

BBB-

A+

A+

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

41

0

500

1000

1500

2000

2500

3000

3500

4000

AAA to A-

BBB+ to BBB-

BB+ to BB-

<B

Credit Exposure - Energy Sector

80%

7%

3%

10%

Australia (73% investment grade)Asia (94% investment grade)North America (58% investment grade)Other (97% investment grade)$3,411m

278

509

1,981

643

$m

42

0

200

400

600

800

1000

1200

1400

1600

AAA to A-

BBB+ to BBB-

BB+ to BB-

<B

Credit Exposure - Telcos Sector

72%

13%

4%

11%

Australia (72% investment grade)Asia (100% investment grade)North America (100% investment grade)Other (64% investment grade)$1,509m

175

186

738

410

$m

43

0

200

400

600

800

1000

1200

AAA to A-

BBB+ to BBB-

BB+ to BB-

<B

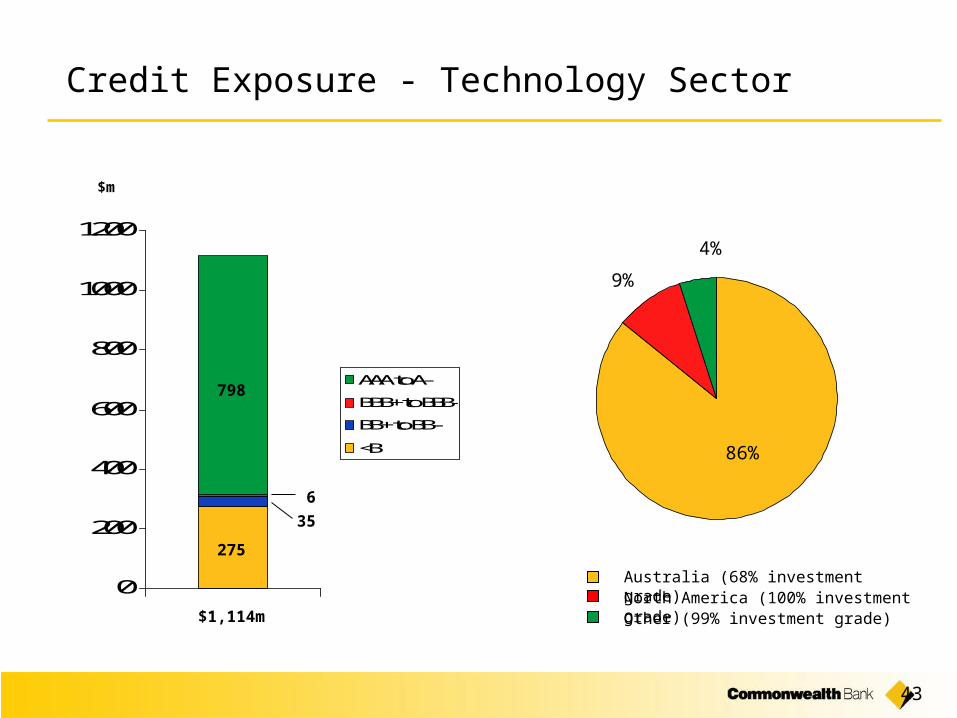

Credit Exposure - Technology Sector

86%

9%

4%

$1,114m

275

35

798

6

$m

Australia (68% investment grade)North America (100% investment grade)Other (99% investment grade)

44

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

AAA to A-

BBB+ to BBB-

BB+ to BB-

<B

Credit Exposure - Agriculture Sector

74%

26%

$7,673m

1,540

5,569

$m

Australia (10% investment grade)New Zealand (3% investment grade)

254

310

45

Group FUM across asset classes

As at 31 December 2002

Listed & Direct Property

16%

International Equities

13%

Australian Equities

27%

Other1%

Fixed Interest & Cash43%