croda international plc 2012 preliminary results

TRANSCRIPT

Croda International Plc

2012 Preliminary Results

26 February 2013

Introduction

Steve Foots – Group Chief Executive

Strong performance in tough environment

Sales up 2.3% to £1051.9m

Operating profit up 7.4% to £255.4m

Pre-tax profit up 6.6% to £253.2m

Record ROS, up 1.2% points to 24.3%

Earnings per share up 8.2% to 130p

Dividend increased by 8.2% to 59.5p (payout ratio of 46%)

3

Results confirm the resilience of Croda’s business model and strategy

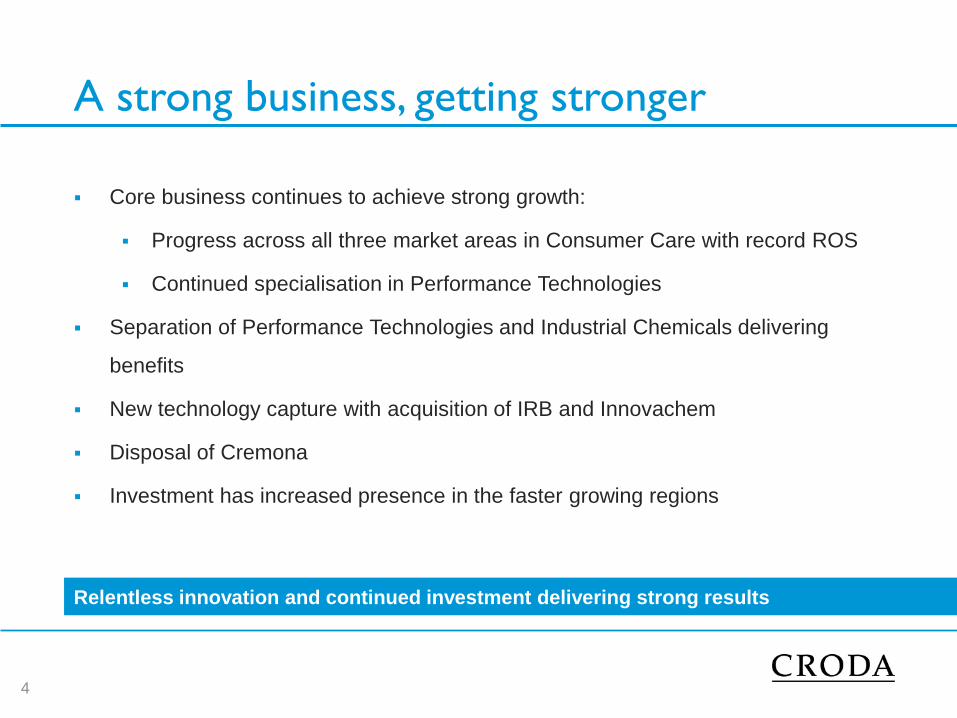

A strong business, getting stronger

Core business continues to achieve strong growth:

Progress across all three market areas in Consumer Care with record ROS

Continued specialisation in Performance Technologies

Separation of Performance Technologies and Industrial Chemicals delivering

benefits

New technology capture with acquisition of IRB and Innovachem

Disposal of Cremona

Investment has increased presence in the faster growing regions

4

Relentless innovation and continued investment delivering strong results

Financial Review

Sean Christie – Group Finance Director

2012 Q4 results

Q4 sales by segment

£m 2012 2011 Growth

Consumer Care 136.3 134.4 +1.4%

Performance Technologies 83.9 81.7 +2.7%

Industrial Chemicals 19.9 18.9 +5.3%

Total turnover 240.1 235.0 +2.2%

Good underlying sales growth in all three segments reduced by currency

translation

7

Sales trends v 2011

8

Q1 Q2 Q3 Q4 Year

Volume -0.7% +2.4% +8.8% +11.7% +5.1%

Price/mix +6.3% +1.0% -5.6% -6.0% -0.7%

Underlying +5.6% +3.4% +3.2% +5.7% +4.4%

Currency -0.2% -2.3% -2.8% -3.7% -2.2%

Acquisition - - +0.1% +0.2% +0.1%

Continuing

sales +5.4% +1.1% +0.5% +2.2% +2.3%

Underlying sales growth steadily improving post Q2

Currency translation headwind increased through 2012

2nd half growth in Industrial Chemicals flatters volumes and weakens mix

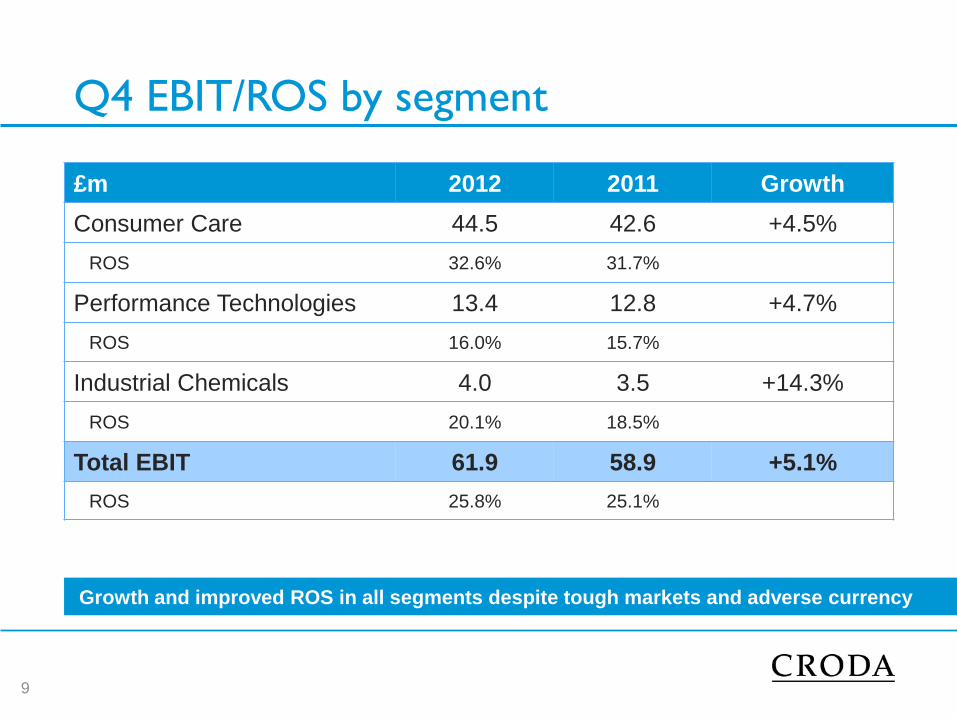

Q4 EBIT/ROS by segment

£m 2012 2011 Growth

Consumer Care 44.5 42.6 +4.5%

ROS 32.6% 31.7%

Performance Technologies 13.4 12.8 +4.7%

ROS 16.0% 15.7%

Industrial Chemicals 4.0 3.5 +14.3%

ROS 20.1% 18.5%

Total EBIT 61.9 58.9 +5.1%

ROS 25.8% 25.1%

9

Growth and improved ROS in all segments despite tough markets and adverse currency

2012 preliminary results

2012 turnover by destination

38%

26%

18%

10%

8%

W. Europe -1%

N. America +5%

Asia +3%

LATAM +4%

Other emergingmarkets* +8%

Good sales growth in Asia

and Latam in high end

products, partially obscured

by our exit from a number of

undifferentiated lines

Strong trading in North

America

Underlying European sales

growth in local currency is

masked by 7% hit on Euro

11

Underlying turnover growth in all regions despite strong 2011 comparatives

* Eastern Europe, Middle East and Africa

UK represents 5% of

total sales

36% of sales

in emerging

markets

Consumer Care

12

£m 2012 2011 Inc

Turnover 586.4 571.4 +2.6%

Operating profit 185.4 171.2 +8.3%

ROS 31.6% 30.0% 0

40

80

120

160

Q1 Q2 Q3 Q4

Sales (£m)

Profit growth in all quarters despite sales

weakness in Q3

All business areas saw underlying sales and

profit growth with Crop Care the strongest

performer 0

10

20

30

40

50

60

Q1 Q2 Q3 Q4

EBIT (£m)

2011

2012

Performance Technologies

13

0

20

40

60

80

100

120

Q1 Q2 Q3 Q4

Sales (£m)

Good progress towards 20% medium

term ROS target despite difficult

European marketplace

Weak European markets (particularly

automotive) reduced profitability in

Lubricants and Coatings and Polymers 0

5

10

15

20

Q1 Q2 Q3 Q4

EBIT (£m)

£m 2012 2011 Inc

Turnover 382.8 373.6 +2.5%

Operating profit 59.7 55.3 +8.0%

ROS 15.6% 14.8%

2011

2012

0

5

10

15

20

25

30

Q1 Q2 Q3 Q4

Sales (£m)

0

1

2

3

4

5

Q1 Q2 Q3 Q4

EBIT (£m)

Industrial Chemicals

14

Limited pricing power so sales, margins

and profit generation can be volatile

Strong H2 performance after weak first

half

£m 2012 2011 Inc

Turnover 82.7 83.0 -0.4%

Operating profit 10.3 11.2 -8.0%

12.5% 13.5%

2011

2012

2012 pre-tax profit up 6.6%

15

Another very strong performance in a difficult market

£m 2012 2011 Growth

Total operating profit 255.4 237.7 +7.4%

ROS 24.3% 23.1%

Financing (2.2) (0.2)

Pre-tax profit 253.2 237.5 +6.6%

Financing

Reduced pension funding credit due to assumption changes

2012 Earnings Per Share up 8.2%

16

£m 2012 2011 Growth

Pre-tax profit 253.2 237.5 +6.6%

Tax rate 30.8% 31.5%

Average number of shares 134.6m 135.3m

Earnings per share 130.0p 120.1p +8.2%

Tax rate reduced to 30.8%

Falling UK tax rates

Average number of shares reduced due to 2011 buyback

Total dividend up 8.2%

17

£m 2012 2011 Growth

Earnings per share 130.0p 120.1p +8.2%

Total dividend 59.5p 55.0p +8.2%

Pay-out ratio 46% 46%

Cover 2.2x 2.2x

Dividend policy:

Total dividend: 40-50% of full year earnings

Total dividend 59.5p

Interim dividend 26.75p

Final dividend 32.75p

Dividend growth exactly in line with earnings growth

So payout ratio and cover unchanged from 2011

Investing in the business

0

10

20

30

40

50

60

70

80

2012 2013 2014 2015

£m

Projected capital investment Estimated depreciation

2012 – 2015

Aiming to spend around twice

depreciation over next few years

>70% of spend in capacity

expansion, new technology and

energy reduction projects

More than doubling investment in

emerging markets (cf 2008 –

2011)

18

Capital expenditure

2012 capital spend £52.3m (2011: £58.3m)

1.6x depreciation versus the medium term target of 2x

Some of shortfall due to project phasing

ROIC improved slightly despite capital spend and M&A

Major spends include

The acrylic polymer plant

Capacity expansion in North America and Singapore

New warehouse and offices in Germany

19

Acquisitions

IRB acquired in July 2012

Cost €7.7m

Based in Italy

Integrated within Sederma

Global leader in plant stem cell technology

Innovachem acquired in December 2012

Cost $2.8m

Based in New Jersey, USA

New and patented product lines for Personal Care

20

Both acquisitions represent exciting niche opportunities in Personal Care

Disposal

Cremona sold November 2012

Final fatty acid/glycerine site acquired with Uniqema in 2006

Turnover in Industrial Chemicals and lower end of Performance

Technologies

Undifferentiated technology, not Croda’s core competence

Treated as discontinued in 2012 accounts

Loss on disposal £11.5m

21

Free cash flow – £181.0m

22

£m 2012 2011

EBITDA 285.0 274.6

Working Capital movement (51.7) (23.7)

Cash from operations 233.3 250.9

Capital expenditure (52.3) (58.3)

Free cash flow 181.0 192.6

3.8% growth in EBITDA

Working capital

High finished goods stock anticipating strong January trading

High raw material stocks ahead of anticipated price increases

High VAT refund due in Germany at year end

Net cash flow

£m 2012 2011

Free cash flow 181.0 192.6

Excess pension contributions (25.2) (17.4)

Share purchases/issues 1.1 (49.4)

Dividends paid (76.8) (67.7)

Interest (8.1) (10.1)

Tax (60.6) (57.7)

M&A 9.1 3.2

Other (mainly restructuring) (1.5) (3.2)

Net cash flow 19.0 (9.7)

Exchange differences 4.4 (1.1)

Change in net debt 23.4 (10.8)

23

Net debt reduced to £207.7m

24

* As per loan covenant calculations, rolling 12 months

£m 2012 2011

Net debt 207.7 231.1

Committed facilities 466.3 477.0

Committed headroom 258.6 245.9

Net debt/EBITDA* 0.7x 0.8x

EBITDA interest cover* 36.8x 33.5x

Main banking facilities run to May 2015

$100m fixed rate loan (5.94%) runs to January 2020

$45m other dollar denominated (floating)

€110m (floating)

Pension deficit decreases by £33.1m pre tax (IAS19 basis)

25

We do not plan to adopt the revised IAS19 rules until 2013, see appendix 3

£m 31 December 2012 31 December 2011

Market value of assets 712.3 647.5

Value of liabilities (878.1) (846.4)

Deficit pre tax (165.8) (198.9)

Deferred tax 44.9 57.3

Deficit post tax (120.9) (141.6)

Changes to certain assumptions and underlying market rates by over £33m pre tax, £20.7m post tax

New deficit reduction schedule for the UK agreed post triennial valuation

2012: £20.4m

2013: £38.4m

£20m (plus inflation) thereafter

Financial KPIs (I)

26

0%

5%

10%

15%

20%

25%

30%

08 09 10 11 12

ROS ROS

Now stands at 24.3%

CC: 31.6% (target: maintain)

PT: 15.6% (target: 20% medium term)

IC: 12.5% (target: maximise profitability)

ROIC

Very high after tax returns maintained

ROIC 23.8%

Far ahead of cost of capital

WACC 6.8%

Capital light business model 0%

5%

10%

15%

20%

25%

08 09 10 11 12

ROIC v

WACC

Financial KPIs (II)

27

-

20

40

60

80

100

120

140

2008 2009 2010 2011 2012

Eps (p)

EPS growth

8.2% growth achieved in 2012

Target 5-10%

Debt ratios

Debt/EBITDA 0.7x (target <3x)

EBITDA interest cover 36.8x (target >4x)

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012

Debt Ratios

x

Strategy Update

Steve Foots – Group Chief Executive

A global leading natural ingredients company

29

Croda helps create multi-million and billion pound brands for its customers

Plant & marine sources Highly trained sales force Flexible manufacturing Valuable intellectual property

Innovation Unmet customer needs Differentiated technologies

Skin Care Oral Care Crop protection Oil & Gas Hair Care Lubricants

Mega trends driving structural growth

30

Positioned well in very attractive growth markets

Beauty and ageing Health and well-being Sustainability

Population growth Disposable income increase Consumer spending growth

Personal Care Health Care Crop Care Lubricants Coatings &

Polymers

Polymer

Additives

Geo

Technologies Home Care

Developments

New niches in adjuvants, skin actives and

drug delivery

Over 50% of growth coming from new

product innovation

Acquisitions: IRB and Innovachem

Looking ahead

Higher brand awareness among emerging

economies

Product quality and safety in use

becoming a key differentiator

Open innovation increasing

Consumer Care

31

£m 2012 2011 Inc

Turnover 586.4 571.4 +2.6%

Operating profit 185.4 171.2 +8.3%

ROS 31.6% 30.0%

Innovation driving growth

Performance Technologies

32

£m 2012 2011 Inc

Turnover 382.8 373.6 +2.5%

Operating profit 59.7 55.3 +8.0%

ROS 15.6% 14.8%

Developments

Robust performance due to improved

speciality portfolio, reducing cyclicality

New niches in oil recovery and green

cleaners

Good growth in our slip additives for

polyolefins

Looking ahead

Asia and Latam set to grow

European demand likely to remain

subdued

Technology acquisition now on agenda

Innovation and margin expansion driving growth

Industrial Chemicals

33

£m 2012 2011 Inc

Turnover 82.7 83.0 -0.4%

Operating profit 10.3 11.2 -8.0%

12.5% 13.5%

Developments

Increasing speciality focus in USA post

distributor exit

Moving from product focus to niche

segment focus

Speciality fatty acid sales driving strong

growth in several markets

Looking ahead

Greater focus on specialities post

Cremona exit

Co-stream demand a function of activity in

Consumer Care and Performance

Technologies

Fast growing niche segments identified

Greater emphasis on specialities driving improvement

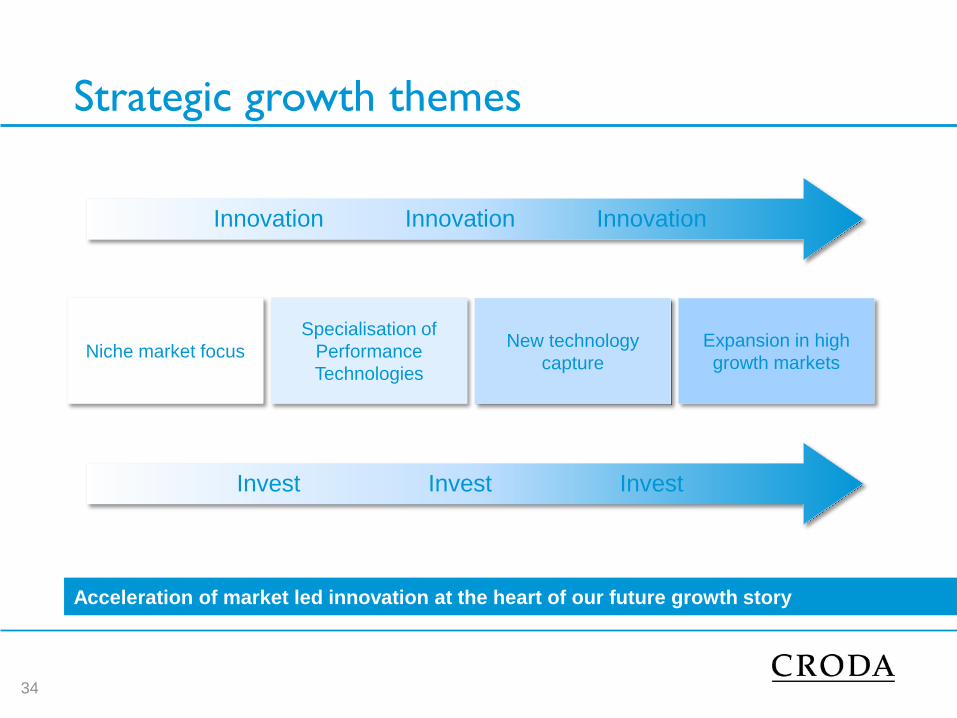

Strategic growth themes

34

Acceleration of market led innovation at the heart of our future growth story

Niche market focus

Specialisation of

Performance

Technologies

New technology

capture

Expansion in high

growth markets

Innovation Innovation Innovation

Invest Invest Invest

Innovation in niche markets – Consumer Care

35

Sustainable actives

Novel performance claims

Based on plant stem cells

from IRB

Market growth exceeding

pharma, high purity needed

Eye drop lubricants and

contact lens solutions

Novel Super Refined™ and

surfactant technologies

Regulation change creating

new niches

Elimination of spray drift to

neighbouring surroundings

In-house proprietary

measuring techniques driving

new product development

Skin creams

Sustainability

Eye care

Sustainability

Spray drift

Sustainability

Powerful sustainability mega trend creating new niches and new opportunities

Innovation in niche markets – Performance Technologies

36

Priplast™ range of 100%

bio-based ingredients

High performance

adhesives for car head-

lamps

Better water repellency

and durability

Replacement for

environmentally hazardous

chemicals

Gas fracking

Inverts polymer emulsions

faster than traditional

surfactants

NatSurf™ range of green

surfactants

Allows lower temperature

washing and reduces

emissions and saves on

energy

Car sealants

Sustainability

Gas fracking

Sustainability

Laundry concentrates

Sustainability

Powerful sustainability mega trend creating new niches and new opportunities

New technology development

Specialisation in Performance Technologies

37

All now supported by dedicated commercial teams placed in all regions of the world

Oil & Gas demulsifiers People

New capacity in Atlas

Point, USA

On stream June 2013,

enabling faster growth in

the Americas

Unique fatty acid platforms

Manufacture planned Q1

2013

Derivatives will serve many

industrial markets

Dedicated global sales

network in place

Continued transfer of skills

from Consumer Care

Asia and Latam teams

strengthened

Globalisation in Performance Technologies

38

Moving manufacturing closer to our customers

Lube esters, Atlas Point

£3.7m, 3.2 kT pa

On stream July 2012

30% sales growth in H2

Lube esters, Brazil

2 kT pa, no spend

needed

On stream H1 2013

Lube esters, Singapore

£1.8m, 4.5 kT pa

On stream Q1 2013 Lubricants

Europe

Overly exposed to Europe

Ester platforms transferred to local

markets

Enabling faster growth

Geo Technologies, Coatings & Polymers

and Home Care to follow in 2013

Very new technologies

New technologies

Technology capture increasing

All six new technologies will contribute this year to our growth story

Acrylic Polymers, Rawcliffe Bridge Biofermentation, Ditton Omega-3 technology, Leek

Polymeric emollients, USA Novel ester platforms, Spain & Singapore

39

IRB, Italy & France

IRB integration

Exceeding expectations already

Customer feedback very positive

Already coded in to new multinational global

formulations

Distributor exit complete

Several new product launches in place for this year

40

Sederma and IRB partnership is progressing smoothly

Leontocell™ Anti-wrinkle

Echingena™ Collagen booster

Shanghai, China

Edison, USA

Expanding in high growth markets – R&D

41

Investment to move Croda closer to our customers and their needs

Formulation support

Customer academy development

More focused new product development

Responsive technical service

Globally coordinated to maximise efficiency

Shiga, Japan

Campinas, Brazil

Regional training centres – Mexico

Ensuring our customers know

how, when and where to use

our products

Continued investment in the education of our customers

10 customer formulating

workshops

5 customer technology events

28% increase in sampling

activity in 2012 from 2011

Non-financial performance

Landfill Waste

2010 2011 2012

Financial Performance

A sustainable business model

43

Non-financial performance now a key differentiator in the eyes of our customers

2010 2011 2012

Water Consumption Energy Consumption

2010 2011 2012

5% 50% 7.5%

Dividend

2010 2011 2012

EPS

2010 2011 2012

Operating Profit

2010 2011 2012

+168% +137% +128%

What would the ideal sustainable manufacturing

business look like?

Croda is as close as any to this model

44

Nature’s raw materials Carbon neutral process Unique performance Biodegradable

Great customer & supplier value

Outlook

Positive start to 2013; expect 2013 to be another year of progress

Trading environment in Europe anticipated to remain challenging

Focus on innovation and technology will enable further growth

On-going investment in facilities and people will underpin progress, especially in

fast growing markets

Continued confidence in Croda’s long term prospects

45

Croda is well positioned to generate sustainable shareholder value

Questions

46

Croda International Plc

2012 Preliminary Results

Appendices

26 February 2013

Appendix 1: Sector sales trends by quarter

Q1 Q2 Q3 Q4 Year

Consumer Care +9.2% +2.5% -2.7% +1.4% +2.6%

Performance Technologies +3.5% +1.2% +2.5% +2.6% +2.5%

Industrial Chemicals -11.1% -7.2% +16.1% +5.3% -0.4%

Continuing sales +5.4% +1.1% +0.5% +2.2% +2.3%

48

2012 v 2011

Appendix I1: 2011 by quarter

£m Q1 Q2 Q3 Q4 Year

Consumer Care 145.7 146.5 144.8 134.4 571.4

Performance Technologies 99.2 100.3 92.4 81.7 373.6

Industrial Chemicals 22.6 23.5 18.0 18.9 83.0

Continuing sales 267.5 270.3 255.2 235.0 1,028.0

Consumer Care 41.8 45.0 41.8 42.6 171.2

Performance Technologies 14.6 14.2 13.7 12.8 55.3

Industrial Chemicals 2.7 3.5 1.5 3.5 11.2

Continuing operating profit 59.1 62.7 57.0 58.9 237.7

Interest (0.2) (0.3) (0.2) 0.5 (0.2)

Continuing pre-tax profit 58.9 62.4 56.8 59.4 237.5

49

Appendix III: 2012 by quarter

£m Q1 Q2 Q3 Q4 Year

Consumer Care 159.1 150.1 140.9 136.3 586.4

Performance Technologies 102.7 101.5 94.7 83.9 382.8

Industrial Chemicals 20.1 21.8 20.9 19.9 82.7

Continuing sales 281.9 273.4 256.5 240.1 1,051.9

Consumer Care 48.2 48.5 44.2 44.5 185.4

Performance Technologies 15.8 17.1 13.4 13.4 59.7

Industrial Chemicals 1.5 2.7 2.1 4.0 10.3

Continuing operating profit 65.5 68.3 59.7 61.9 255.4

Interest (0.7) (0.4) (0.4) (0.7) (2.2)

Continuing pre-tax profit 64.8 67.9 59.3 61.2 253.2

50

Appendix IV: 2012 restated for revised IAS19

standard on pension accounting £m Q1 Q2 Q3 Q4 Year

Consumer Care 48.2 48.5 44.2 44.5 185.4

Performance Technologies 15.8 17.1 13.4 13.4 59.7

Industrial Chemicals 1.5 2.7 2.1 4.0 10.3

Continuing operating profit 65.5 68.3 59.7 61.9 255.4

Interest (0.7) (0.4) (0.4) (0.7) (2.2)

Continuing pre-tax profit 64.8 67.9 59.3 61.2 253.2

Consumer Care 48.1 48.4 44.2 44.4 185.1

Performance Technologies 15.8 17.0 13.3 13.4 59.5

Industrial Chemicals 1.5 2.7 2.1 4.0 10.3

Continuing operating profit 65.4 68.1 59.6 61.8 254.9

Interest (4.3) (4.0) (4.0) (4.3) (16.6)

Continuing pre-tax profit 61.1 64.1 55.6 57.5 238.3

51

In 2013, the revision to IAS19 is expected to be somewhat less onerous, due

to the reduction in the pension deficit.