cross-sectional patterns of mortgage debt during … · cross-sectional patterns of mortgage debt...

TRANSCRIPT

Introduct ion Empincal Strategy Evidence I m pltcations eooo 0 000000000 0000

Cross-Sectional Patterns of Mortgage Debt

During the Housing Boom: Evidence and Implications

Chris Foote, Lara Loewenstein and Paul Willen FRB Boston

FDIC Consumer Credit Symposium

Washington , DC October 28, 2016

0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 1 1 18

Introduction Empincal Strategy Evidence I m pltcations oeoo 0 000000000 0000

Disclaimer

0 - .(!)<;('-

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19, 2016 2 1 18

Introduct ion Empincal Strategy Evidence I m pltcations oeoo 0 000000000 0000

Disclaimer

• I am speaking today as a researcher and as a concerned citizen

0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 2 1 18

Introduct ion Empincal Strategy Evidence I m pltcations oeoo 0 000000000 0000

Disclaimer

• I am speaking today as a researcher and as a concerned citizen

• not as a representative of:

0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 2 1 18

Introduct ion Empincal Strategy Evidence I m pltcations oeoo 0 000000000 0000

Disclaimer

• I am speaking today as a researcher and as a concerned citizen

• not as a representative of:

• The Boston Fed

0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 2 1 18

Introduct ion Empincal Strategy Evidence I m pltcations oeoo 0 000000000 0000

Disclaimer

• I am speaking today as a researcher and as a concerned citizen

• not as a representative of:

• The Boston Fed • or the Federal Reserve System

0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 2 1 18

Introduct ion Empincal Strategy Evidence I m pltcations oeoo 0 000000000 0000

Disclaimer

• I am speaking today as a researcher and as a concerned citizen

• not as a representative of:

• The Boston Fed • or the Federal Reserve System

• When I say "we" , I don't mean Janet and me. 0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 2 1 18

Introduction Empincal Strategy Evidence I m pltcations ooeo 0 000000000 0000

Growth in Debt

10

8

Vl c .Q ·;: 6.....-c

4

Household Mortgage Debt

(~left scale) "\t

2 ~---------------~------·----------~------~--~~ 91 93 95 97 99 01 03 05 07 09 11 13 15

0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 3 1 1s

Introduction Empincal Strategy Evidence I m pltcations ooeo 0 000000000 0000

Growth in Debt

Household Mortgage Debt

(~left scale) "\t

~-------------~----------------~------~--~~ 91 93 95 97 99 01 03 05 07 09 11 13 15

10

8

• Explosion 1n debtVl c .Q ·;:: 6 .....-c

4

2

0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 3 1 1s

c

Introduction Empincal Strategy Evidence I m pltcations ooeo 0 000000000 0000

Growth in Debt

• Ex plosion in debt

·;:: 6 12Vl • Not incom e ..... c ~ .Q

·;:: ..... ~

4 8 ·= "" Persona l income (right sca le---7 )

10

8

Vl c 0

Household Mortgage Debt

(~l eft scale) ')I

- 16

2 4

91 93 95 97 99 01 03 05 07 09 11 13 15

0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 3 1 1s

c

Introduction Empincal Strategy Evidence I m pltcations ooeo 0 000000000 0000

Growth in Debt

• Ex plosion in debt

·;:: 6 12Vl • Not incom e ..... c ~ .Q

2 4

91 93 95 97 99 01 03 05 07 09 11 13 15

0 - .(!)<;('-

10

8

Vl c 0

Household Mortgage Debt

(~l eft scale) ')I

- 16

4

• Why?· ;:: ..... ~

8 ·= "" Persona l income (right sca le---7 )

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 3 1 1s

Introduct ion Empincal Strategy Evidence I m pltcations oooe 0 000000000 0000

Explaining the boom

Credit Ex pansion

• Credit Expansion in early 2000s

0 - .(!)<;('.... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 4 1 1s

Introduct ion Empincal Strategy Evidence I m pltcations oooe 0 000000000 0000

Explaining the boom r,---------------------,~

Constrained Low Inco me

Low Credit Score \..

Credit

Ex pansion

• Credit Expansion in early 2000s

0 - .(!)<;('.... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 4 1 1s

Introduct ion Empincal Strategy Evidence I m pltcations oooe 0 000000000 0000

Explaining the boom r~------------------~~Constrained

Low Inco me Low Credit Score \..

Credit

Ex pansion

Unconstrained High Income

Hig h Credit Score

• Credit Expansion in early 2000s

0 - .(!)<;('.... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 4 1 18

Introduct ion Empincal Strategy Evidence I m pltcations oooe 0 000000000 0000

Explaining the boom r~------------------~~Constrained

Low Inco me Low Credit Score \..

Credit

Ex pansion

Unconstrained High Income

Hig h Credit Score

• Credit Expansion in early 2000s

• He I ped constrained borrowers

0 - .(!)<;('.... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 4 1 18

Introduct ion Empincal Strategy Evidence I m pltcations oooe 0 000000000 0000

Explaining the boom r~------------------,~

Constrained Low Income

Low Credit Score \..

Credit

Expansion

Unconstrained High Income

High Credit Score

• Credit Expansion in early 2000s

• He I ped constrained borrowers

• M argina I borrowers

0 - .(!)<;('.... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 4 1 18

Introduct ion Empincal Strategy Evidence I m pltcations oooe 0 000000000 0000

Explaining the boom r~------------------,~

Constrained

M argina I borrowers Constrained borrowers

Low Income Low Credit Score \..

Credit

Expansion

Unconstrained High Income

High Credit Score

• Credit Expansion in early 2000s

• He I ped constrained borrowers

• •

0 - .(!)<;('.... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 4 1 18

Introduct ion Empincal Strategy Evidence I m pltcations oooe 0 000000000 0000

Explaining the boom r~------------------,~

Constrained Low Income

Low Credit Score \..

Credit

Expansion

Unconstrained High Income

High Credit Score

• Credit Expansion in early 2000s

• He I ped constrained borrowers

• M argina I borrowers • Constrained borrowers • Drive up house prices (also relaxes

constraints) 0 - .(!)<;('....

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 4 1 18

Introduct ion Empincal Strategy Evidence I m pltcations oooe 0 000000000 0000

Explaining the boom r~------------------,~

Constrained Low Income

Low Credit Score \..

Credit

Expansion

Unconstrained High Income

High Credit Score

• Credit Expansion in early 2000s • Unconstrained borrowers?

• He I ped constrained borrowers

• M argina I borrowers • Constrained borrowers • Drive up house prices (also relaxes

constraints) 0 - .(!)<;('....

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 4 1 18

Introduct ion Empincal Strategy Evidence I m pltcations oooe 0 000000000 0000

Explaining the boom r~------------------,~

Constrained Low Income

Low Credit Score \..

Credit

Expansion

Unconstrained High Income

High Credit Score

• Credit Expansion in early 2000s • Unconstrained borrowers?

• He I ped constrained borrowers • Wealth effects?

• M argina I borrowers • Constrained borrowers • Drive up house prices (also relaxes

constraints) 0 - .... .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 4 1 18

Introduct ion Empincal Strategy Evidence I m pltcations oooe 0 000000000 0000

Explaining the boom r,-----------------~~

Constrained Low Income

Low Credit Score \..

tCredit Relati+e ShiftExpansion

I

• Credit Expansion in early 2000s

• He I ped constrained borrowers

• M argina I borrowers • Constrained borrowers • Drive up house prices (also relaxes

constraints)

Unconstrained High Income

High Credit Score

• Unconstrained borrowers?

• Wealth effects?

• Relative balance sheet shift in debt to constrained

.(!)<;('0 - .... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 4 1 1s

Introduction Empincal Strategy Evidence I m pltcations oooe 0 000000000 0000

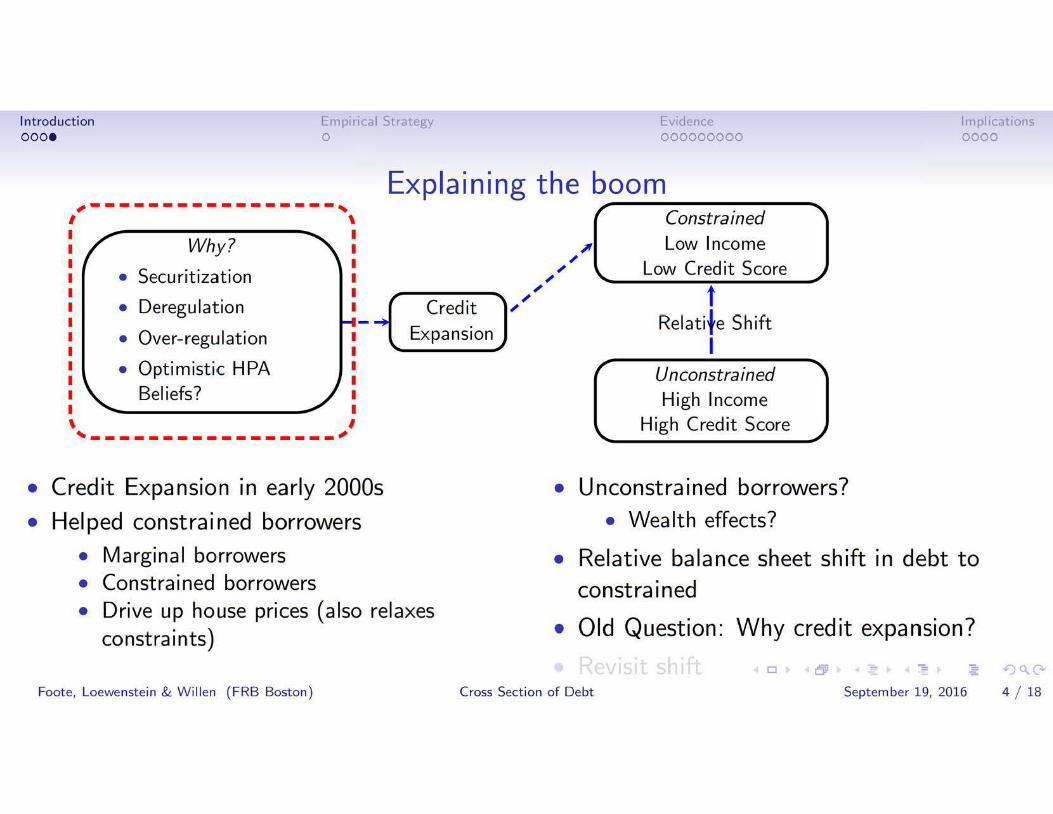

Explaining the boom I ~-----------------,\

Why?

• Securitization

• Deregulation

I I I I I I

I I I I I I

Credit -~

Expansion• Over-regulation

• Optimistic HPA Beliefs?

\ I

~-----------------'

r,-----------------~~Constrained Low Income

Low Credit Score \..

t Relati+e Shift

I Unconstrained High Income

High Credit Score

• Credit Expansion in early 2000s • Unconstrained borrowers?

• He I ped constrained borrowers • Wealth effects?

• M argina I borrowers • Relative balance sheet shift in debt to • Constrained borrowers constrained • Drive up house prices (also relaxes

• Old Question: Why credit expansion? constraints) 0 - .(!)<;('....

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 4 1 1s

Introduction Empincal Strategy Evidence I m pltcations oooe 0 000000000 0000

Explaining the ,Beem ---- -------~ I \

I ~-----------------,\ 1 r Constrained "

Why? I I I

P' Low Income I ~

~~ ~ Low Credit Score ~• Securitization I ~ '---------t~-------' I

Credit ~~• Deregulation I

Relati+e ShiftExpansion• Over-regulation I -~

I I • Optimistic HPA I UnconstrainedI

Beliefs? I High Income I

\ I High Credit Score ~-----------------'

'~---------------' • Credit Expansion in early 2000s • Unconstrained borrowers?

• He I ped constrained borrowers • Wealth effects?

• M argina I borrowers • Relative balance sheet shift in debt to • Constrained borrowers constrained • Drive up house prices (also relaxes

• Old Question: Why credit expansion? constraints)

• Revisit shift 0 - .... .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 4 1 1s

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

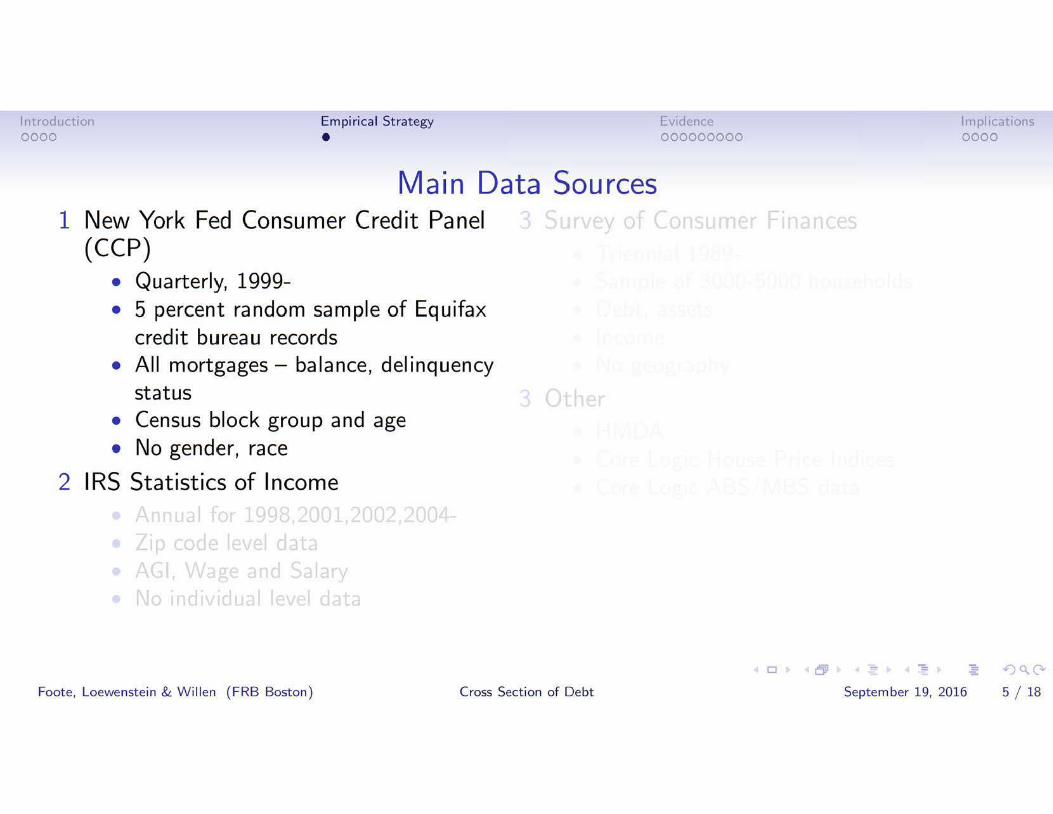

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP)

0 - .(!)<;('.... Foote, Loewenstein & Willen (F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999

0 - .(!)<;('.... Foote, Loewenstein & Willen (F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records

0 - .(!)<;('.... Foote, Loewenstein & Willen (F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status

0 - .(!)<;('.... Foote, Loewenstein & Willen (F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age

0 - .(!)<;('.... Foote, Loewenstein & Willen (FRB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

0 - .(!)<;('.... Foote, Loewenstein & Willen (FRB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me

0 - .(!)<;('.... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004

0 - .(!)<;('.... Foote , Loewe nstein & W illen ( F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004• Zip code level data

0 - .(!)<;('.... Foote , Loewe nstein & W illen ( F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004• Zip code level data • AGI, Wage and Salary

0 - .(!)<;('.... Foote , Loewe nstein & W illen ( F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004• Zip code level data • AGI, Wage and Salary • No individual level data

.(!)<;('0 - .... Foote , Loewe nstein & W illen ( F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel 3 Survey of Consumer Finances

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004• Zip code level data • AGI, Wage and Salary • No individual level data

0 - .(!)<;('.... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

• Triennial 1989

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel 3 Survey of Consumer Finances

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004• Zip code level data • AGI, Wage and Salary • No individual level data

.(!)<;('0 - .... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel 3 Survey of Consumer Finances

(CCP) • Triennial 1989• Quarterly, 1999- • Sample of 3000-5000 households • 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004• Zip code level data • AGI, Wage and Salary • No individual level data

0 - .(!)<;('.... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004• Zip code level data • AGI, Wage and Salary • No individual level data

3 Survey of Consumer Finances

• Triennial 1989• Sample of 3000-5000 households • Debt, assets

0 - .(!)<;('.... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004• Zip code level data • AGI, Wage and Salary • No individual level data

3 Survey of Consumer Finances

• Triennial 1989• Sample of 3000-5000 households • Debt, assets • Income

0 - .(!)<;('.... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004• Zip code level data • AGI, Wage and Salary • No individual level data

3 Survey of Consumer Finances

• Triennial 1989• Sample of 3000-5000 households • Debt, assets • Income • No geography

.(!)<;('0 - .... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004• Zip code level data • AGI, Wage and Salary • No individual level data

3 Survey of Consumer Finances

• Triennial 1989• Sample of 3000-5000 households • Debt, assets • Income • No geography

3 Other

0 - .(!)<;('.... Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004• Zip code level data • AGI, Wage and Salary • No individual level data

3 Survey of Consumer Finances

• Triennial 1989• Sample of 3000-5000 households • Debt, assets • Income • No geography

3 Other • HMDA

0 - .(!)<;('.... Foot e , Loewenstein & Willen (FRB Boston ) Cross Section of Debt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me • Annual for 1998,2001,2002,2004• Zip code level data • AGI, Wage and Salary • No individual level data

3 Survey of Consumer Finances

• Triennial 1989• Sample of 3000-5000 households • Debt, assets • Income • No geography

3 Other • HMDA • Core Logic House Price Indices

.(!)<;('0 - .... Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 s 1 18

Introduction Empirical Strategy Evidence I m pltcations 0000 000000000 0000•

Main Data Sources 1 New York Fed Consumer Credit Panel

(CCP) • Quarterly, 1999• 5 percent random sample of Equifax

credit bureau records • All mortgages- balance, delinquency

status • Census block group and age • No gender, race

2 IRS Statistics of I nco me

• Annual for 1998,2001,2002,2004• Zip code level data • AGI, Wage and Salary • No individual level data

3 Survey of Consumer Finances

• Triennial 1989• Sample of 3000-5000 households • Debt, assets • Income • No geography

3 Other • HMDA • Core Logic House Price Indices • Core Logic ABS / MBS data

.(!)<;('0 - .... Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 s 1 18

Introduction Empincal Strategy Evidence I m pltcations 0000 0 e oooooooo 0000

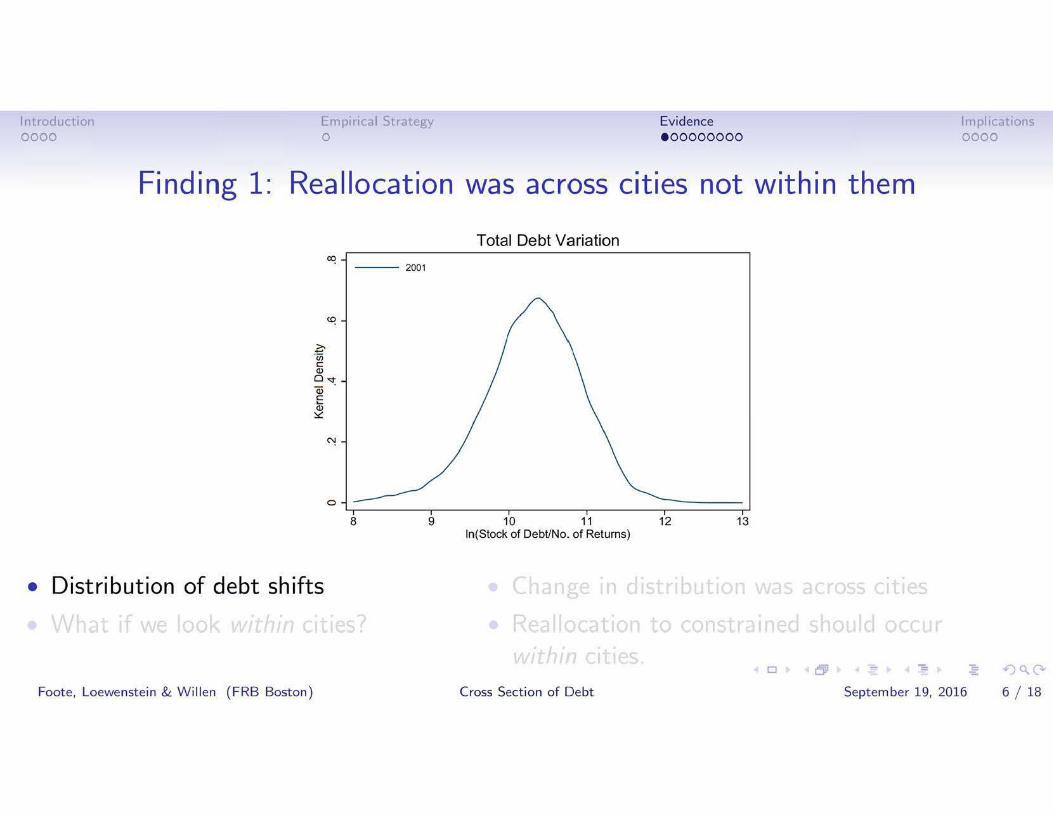

Finding 1 : Reallocation was across cities not within them

Total Debt Variation

-- 2001

0

8 9 10 11 12 13 ln(Stock of Debt/No. of Returns)

• Distribution of debt shifts

0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 6 1 1s

--

Introduction Empincal Strategy Evidence I m pltcations 0000 0 e oooooooo 0000

Finding 1 : Reallocation was across cities not within them

Total Debt Variation

--- 2001

---- - 2006

I

I I

I /

I /

I I

/ ---/ .....

' \ \ \ \ I

I \ I \

I ' \ \

\ \

/ / ' \/

' '/ /

' .... -0

8 9 10 11 12 13 ln(Stock of Debt/No. of Returns)

• Distribution of debt shifts

0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 6 1 1s

0

Introduction Empincal Strategy Evidence I m pltcations 0000 0 e oooooooo 0000

Finding 1: Reallocation was across cities not within them

Within-CBSA Debt Variation

- 2001

- 2 -1 0 In(Stock of DebUNo. of Returns)

2

• Distribution of debt shifts

• What if we look within cities?

0 - .(!)<;('-

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19, 2016 6 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 e oooooooo 0000

Finding 1: Reallocation was across cities not within them

Within-CBSA Debt Variation

--2001

----- 2006

0

- 2 -1 0 In(Stock of DebUNo. of Returns)

• Distribution of debt shifts

• What if we look within cities?

Foote , Loewenstein & W il len (F RB Boston)

2

0

Cross Section of Debt

-September 19, 2016

- .(!)<;('

6 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 e oooooooo 0000

Finding 1: Reallocation was across cities not within them

Within-CBSA Debt Variation Between- CBSA Debt Variation

- 2001

----- 2006

0

- 2 -1 0 In(Stock of DebUNo. of Returns)

• Distribution of debt shifts

• What if we look within cities?

Foote , Loewenstein & W illen (F RB Boston)

-- 2001

<X:!

~ ·u; CD c . Q)

0 Qi c.... a> "<I: ~

~

0

2 8 9 10 11 12 In( Stock of DebUNo. of Returns)

• Change 1n distribution was across cities

0 - .(!)<;('-Cross Section of De bt September 19, 2016 6 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 e oooooooo 0000

Finding 1: Reallocation was across cities not within them

Within-CBSA Debt Variation Between-CBSA Debt Variation

- 2001

----- 2006

0

~ ·ii3~ Q)

0 Qi E Q)"<t ~ -

0

- 2001

--- - 2006

/\

'\ \ /V'\1 I

I \ \ I \ I \ \ I \

\ \ \

\ \

' ' - 2 -1 0 2 8 9 10 11

In( Stock of DebUNo. of Returns) In( Stock of DebUNo. of Returns)

• Distribution of debt shifts • Change 1n distribution was across cities

• What if we look within cities?

0 - .(!)<;('-Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 6 1 1s

12

Introduction Empincal Strategy Evidence I m pltcations 0000 0 e oooooooo 0000

Finding 1: Reallocation was across cities not within them

Within-CBSA Debt Variation Between-CBSA Debt Variation

- 2001

----- 2006

- 2 -1 0 In( Stock of DebUNo. of Returns)

• Distribution of debt shifts

• What if we look within cities?

Foote , Loewenstein & W illen (F RB Boston)

-- 2001

---- - 2006

~ ·ii3~ Q)

0 Qi E Q)"<t ~ -

/\

'\ \ /V'\1 I

I \ \ I \ I \ \ I \

\ \ \

\ \

0 0 ' ' 2 8 9 10 11 12

In( Stock of DebUNo. of Returns)

• Change in distribution was across cities

• Reallocation to constrained should occur within cities.

0 - .(!)<;('-Cross Section of De bt September 19, 2016 6 1 1s

--

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oe ooooooo 0000

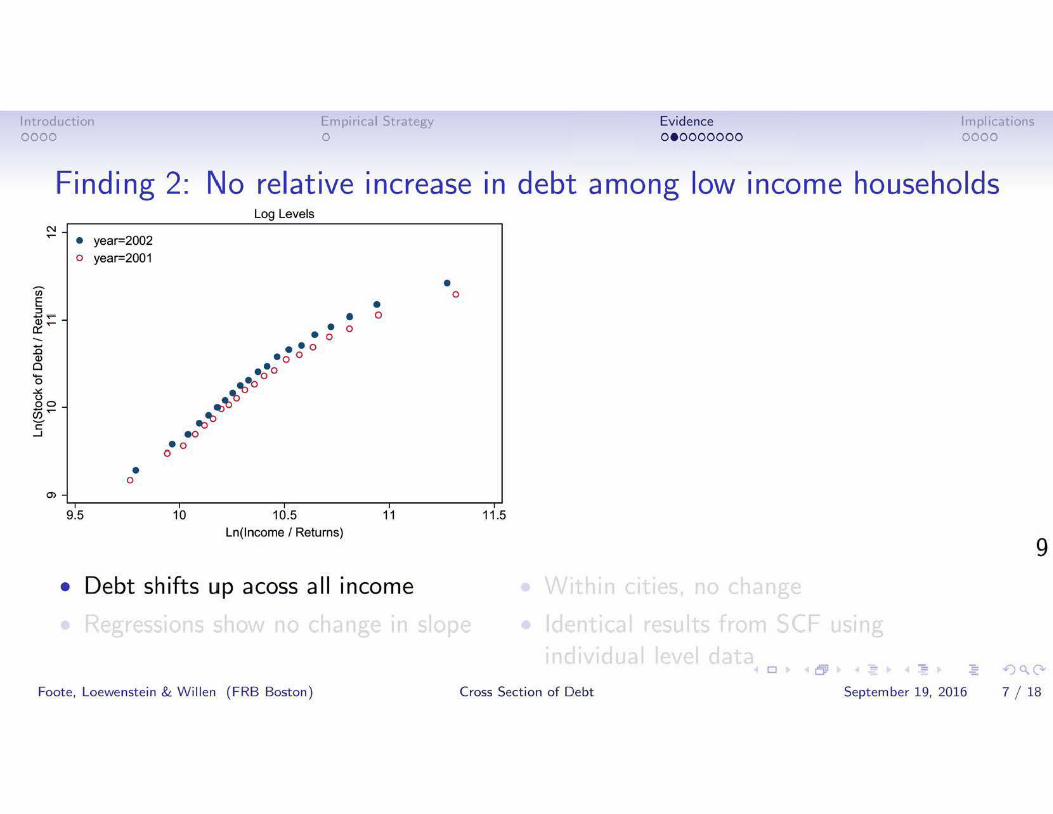

Finding 2: No relative increase in debt among low income households N..-

o year=2001

Log Levels

0

0

0 0

E Q)

0 0 ..ll:: (.)

U500

..c ...J

0 0

0

9.5 10 10.5 11 11 .5 Ln(lncome I Returns)

9

• Debt shifts up acoss all income

0 - .~!)<;('-

Foote , Loewenstein & W illen ( F RB Boston) Cross Section of Debt September 19, 2016 7 1 1s

--

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oe ooooooo 0000

Finding 2: No relative increase in debt among low income households Log Levels

N..-

E Q)

0 0 ..ll:: (.)

U500

..c ...J

Ln(lncome I Returns)

9

• Debt shifts up acoss all income

• year=2002 o year=2001

•0

10 10.5 11

•0

11 .5 9 .5

0 - .~!)<;('-

Foote , Loewenstein & W illen ( F RB Boston) Cross Section of Debt September 19, 2016 7 1 1s

--

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oe ooooooo 0000

Finding 2: No relative increase in debt among low income households Log Levels

N..-• year=2004 o year=2001 •

•• • • 0

0

0 0

E Q)

0 0 ..ll:: (.)

U500

..c ...J

• 0 0

0

9 .5 10 10.5 11 11 .5 Ln(lncome I Returns)

9

• Debt shifts up acoss all income

0 - .~!)<;('-

Foote , Loewenstein & W illen ( F RB Boston) Cross Section of Debt September 19, 2016 7 1 1s

•• •

• •

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oe ooooooo 0000

Finding 2: No relative increase in debt among low income households Log Levels

N..-• year=2005 o year=2001 •

• • 0

0

0 - •• 0 E •• 0 0 Q) • 00 • 0

• 00 • 00..ll::

(.) •• 0 oOU5

00 .. • 0

0c ...J 0

• 0 0

0

9 .5 10 10.5 11 11 .5 Ln(lncome I Returns)

9

• Debt shifts up acoss all income

0 - .~!)<;('-

Foote , Loewenstein & W illen ( F RB Boston) Cross Section of Debt September 19, 2016 7 1 1s

• • • ••

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oe ooooooo 0000

Finding 2: No relative increase in debt among low income households Log Levels

N

• year=2006 • o year=2001 •

0

• 0 • 0

- ••• 0 0E Q) •• 0 0 0 • 000 •• 00..ll:: (.) • 0

• oOU500

..00c

...J • 0 0

0

0

9 .5 10 10.5 11 11 .5 Ln(lncome I Returns)

9

• Debt shifts up acoss all 1ncome

0 - .~!)<;('-

Foote , Loewenstein & W illen ( F RB Boston) Cross Section of Debt September 19, 2016 7 1 1s

--

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oe ooooooo 0000

Finding 2: No relative increase in debt among low income households Log Levels Deviated from CBSA-Year Means

N

(i) c .... ::3 ...... ,.. ~ .....

E Q)

0 0 ..ll:: (.)

U500 ..... c ...J

• o

year=2006 year=2001

• • •• •

• • 0

0

• 0

•

••• •• 0 0

0 0

• 00

• 0

0

•• 00 • 0

• oO 00

0

0

o year=2001 0

0(i)ll)c . 0.... ::3 ...... 0Q)

00:: 0

:i5 L~o ~ 0 ~~-------------!-+------------*""0 0

0

..ll:: 00 (.) 0B oCl)cLO o ...J , ·

0

0 or'

9 .5 10 10.5 11 11.5 -1 -.5 0 .5 1 Ln(lncome I Returns) Ln(lncome I Returns)

9

• Debt shifts up acoss all 1ncome • Within cities, no change

0 - .~!)<;('-Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 7 1 1s

--•• ••

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oe ooooooo 0000

Finding 2: No relative increase in debt among low income households Log Levels Deviated from CBSA-Year Means

N

(i) c .... ::3 ...... ,.. ~ .....

E Q)

0 0 ..ll:: (.)

U500 ..... c ...J

• o

year=2006 year=2001

• • •• •

• • 0

0

• 0

•

••• •• 0 0

0 0

• 00

• 0

0

•• 00 • 0

• oO 00

0

0

(i)ll)c . .... ::3 ...... Q)

0::

• year=2002 0 year==2001 e o

• ~

•• ,. ~·

•

• ~ •

~ -r

1

9 .5 10 10.5 11 11.5 -1 -.5 0 .5 1 Ln(lncome I Returns) Ln(lncome I Returns)

9

• Debt shifts up acoss all 1ncome • With in citi es, no change

0 - .~!)<;('-Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 7 1 1s

--

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oe ooooooo 0000

Finding 2: No relative increase in debt among low income households Log Levels Deviated from CBSA-Year Means

N

(i) c .... ::3 ...... ,.. ~ .....

E Q)

0 0 ..ll:: (.)

U500 ..... c ...J

• o

year=2006 year=2001

• • •• •

• • 0

0

• 0

•

••• •• 0 0

0 0

• 00

• 0

0

•• 00 • 0

• oO 00

0

0

(i)ll)c . .... ::3 ...... Q)

0::

• o

year=2004 year==2001

8 8

8 •

• • •

~·

•••••• ~

i

i-r 1

9 .5 10 10.5 11 11.5 -1 -.5 0 .5 1 Ln(lncome I Returns) Ln (lncome I Returns)

9

• Debt shifts up acoss all 1ncome • Within cities, no change

0 - .~!)<;('-Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 7 1 1s

--

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oe ooooooo 0000

Finding 2: No relative increase in debt among low income households Log Levels Deviated from CBSA-Year Means

N

(i) c .... ::3 ...... ,.. ~ .....

E Q)

0 0 ..ll:: (.)

U500 ..... c ...J

• o

year=2006 year=2001

• • •• •

• • 0

0

• 0

•

••• •• 0 0

0 0

• 00

• 0

0

•• 00 • 0

• oO 00

0

0

(i)ll)c . .... ::3 ...... Q)

0::

• o

year=2005 year==2001 ~

~

~

• @.

•• •

"'.~· ~

8 • ~

0•-r 1

9 .5 10 10.5 11 11.5 -1 -.5 0 .5 1 Ln(lncome I Returns) Ln (lncome I Returns)

9

• Debt shifts up acoss all 1ncome • Within cities, no change

0 - .~!)<;('-Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 7 1 1s

--

• • • ••

•• •• ••

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oe ooooooo 0000

Finding 2: No relative increase in debt among low income households Log Levels Deviated from CBSA-Year Means

• year=2006 0 year==2001 o•

~

~

~

e• ~

t•

• ., ~

~

•0

-1 -.5

• Debt shifts up acoss all 1ncome • With in citi es, no change

N

• year=2006 • o year=2001 •

(i) (i)ll)0c c . .... .... ::3 ::3...... ,.. ......• 0 Q)~ ..... • 0 0::

••• 0 0E Q) •• 0 0 0 • 000 •• 00..ll:: (.) • 0

• oOU500 ..... 00c

...J • 0 0

0

0 -r

1

9 .5 10 10.5 11 11.5 Ln(lncome I Returns)

0 .5 1 Ln(lncome I Returns)

9

0 - .~!)<;('-Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 7 1 1s

•• •• ••

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oe ooooooo 0000

Finding 2: No relative increase in debt among low income households N .....

(i) c .... ::3 ...... ,.. ~ ..... --.c Q)

0-0 ..ll:: (.) 00U5..c ...J

• year=2006 0 year=2001

• 0

Log Levels

• • •••• 0• 0• 0• 00••• 00•• 00 • 0

• oO 00

0 0

• 0

• 0

•

(i)ll)c . .... ::3 ...... Q)

0::

15 ~0-0 ..ll:: (.)

.8 Cl)cLO ...J ,·

Ol

0 or'

9.5 10 10.5 Ln(lncome I Returns)

11 11.5

Deviated from CBSA-Year Means

• year=2006 0 year==2001 o•

~

~

~

e• ~

t•

• ., ~

~

•0

-1 -.5 0 .5 1 Ln (lncome I Returns)

9

• Debt shifts up acoss all income • Within cities, no change

• Regressions show no change in slope

0 - - .(!)<;('

Foote , Loewenstein & W illen ( F RB Boston) Cross Section of D ebt September 19, 2016 7 1 1s

•• •• ••

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oe ooooooo 0000

Finding 2: No relative increase in debt among low income households N .....

(i) c .... ::3 ...... ,.. ~ ..... --.c Q)

0-0 ..ll:: (.) 00U5..c ...J

• year=2006 0 year=2001

• 0

Log Levels

• • •••• 0• 0• 0• 00••• 00•• 00 • 0

• oO 00

0 0

• 0

• 0

•

(i)ll)c . .... ::3 ...... Q)

0::

15 ~0-0 ..ll:: (.)

.8 Cl)cLO ...J ,·

Ol

0 or'

9.5 10 10.5 Ln(lncome I Returns)

11 11.5

Deviated from CBSA-Year Means

• year=2006 0 year==2001 o•

~

~

~

e• ~

t•

• ., ~

~

•0

-1 -.5 0 .5 1 Ln(lncome I Returns)

9

• Debt shifts up acoss all income • Within cities, no change

• Regressions show no change in slope • Identical results f rom SCF using individual level data

.(!)<;('

Foote , Loewenstein & W illen ( F RB Boston) Cross Section of D ebt September 19, 2016 7 1 1s

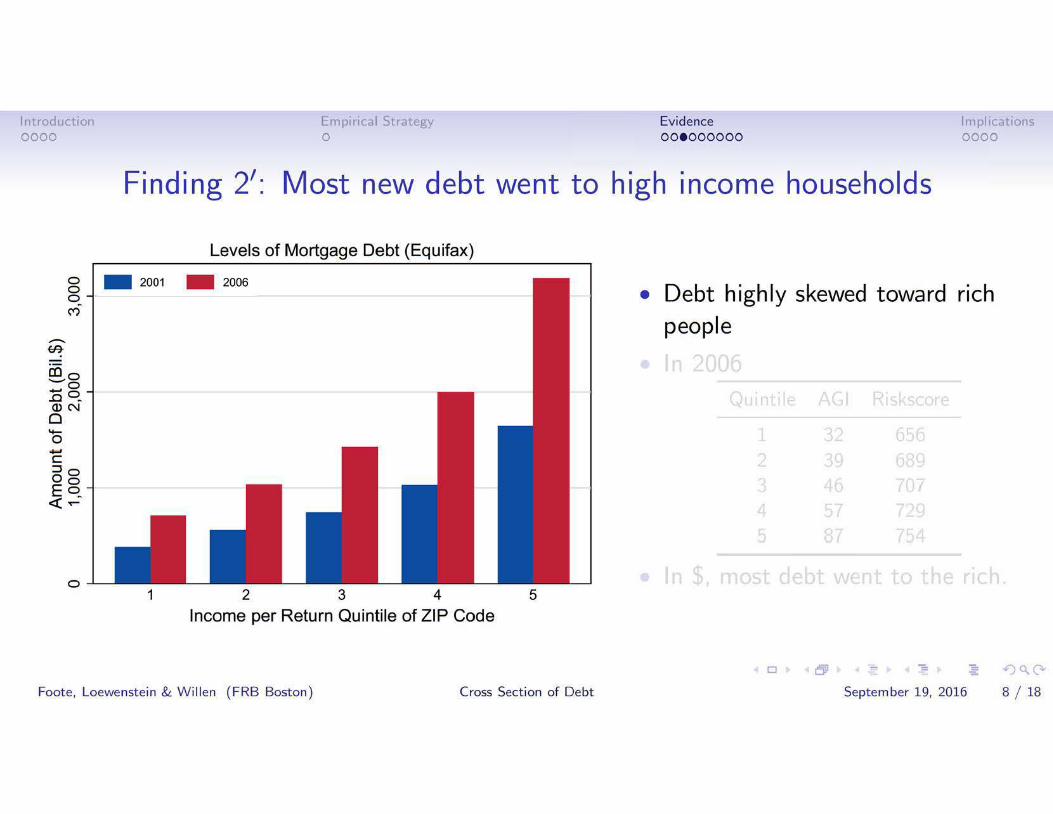

Introduction Empincal Strategy Evidence I m pltcations 0000 0 ooeoooooo 0000

Finding 2': Most new debt went to high income households

Levels of Mortgage Debt (Equifax)

g0 ('()

0 -..,_, c :::JoOoEo <( ~-

0

- 2001 - 2006

1 2 3 4 Income per Return Quintile of ZIP Code

• Debt highly skewed toward rich people

5

0 .(!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19, 2016 8 1 18

Introduction Empincal Strategy Evidence I m pltcations 0000

0 0 0 ('()

fflCO o..._...o ..... o.0 ~ <l>N 0

0 -..,_, c :::JoOo E o <( ~~

0

0 ooeoooooo 0000

Finding 2': Most new debt went to high income households

Levels of Mortgage Debt (Equifax)

- 2001 - 2006

1 2 3 4 5 Income per Return Quintile of ZIP Code

Foote , Loewe nstein & W il len ( F RB Boston) Cross Section of Debt

• Debt highly skewed toward rich people

• In 2006

Q ui ntile AGI Riskscore

1 32 656 2 39 689 3 46 707 4 57 729 5 87 754

0 Oil - .... .(!)<;('

September 19, 2016 8 1 18

Introduction Empincal Strategy Evidence I m pltcations 0000

0 0 0 ('()

fflCO o..._...o .0..... o <l>N

~

0

0 -..,_, c :::JoOo E o <( ~~

0

0 ooeoooooo 0000

Finding 2': Most new debt went to high income households

Levels of Mortgage Debt (Equifax)

- 2001 - 2006

1 2 3 4 5 Income per Return Quintile of ZIP Code

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt

• D ebt highly skewed toward rich peopl e

• In 2006

Q ui ntile AGI Riskscore

1 32 656 2 39 689 3 46 707 4 57 729 5 87 754

• In $, most debt went t o the rich.

0 - .(!)<;('= September 19, 2016 8 1 18

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oooeooooo 0000

Finding 3: Relative changes in originations offset by terminations

0

Binned Scatterplot: Originations

o year=2002 •

-1 -.5 0 .5

Ln(lncome I Returns)

1

• Growth in stock of debt is

l:l. Stock' ,V'

Net flow

== Purchases + Cash-Out

Gross flow in

Curtailment Amortization

Gross flow out

Sales

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt

0 -

September 19, 2016 - .(!)<;('

9 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oooeooooo 0000

Finding 3: Relative changes in originations offset by terminations

Binned Scatterplot: Originations Binned Scatterplot: Terminations -Vl

o

-1 -.5 0 .5 1 -1 -.5 0 .5 1 Ln(lncome I Returns) Ln(lncome I Returns)

• Growth in stock of debt is

l:l. Stock == Purchases + Cash-Out - Curtailment - Amortization - Sales

Net flow Gross flow in Gross flow out 0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 9 1 1s

c '-rl0 :l ...... (])

CX:LI) ........... year=2002 Vl c 0 0 +---------~ ~ ro -~ Ll)E ,·,_ (])

1-ri •

-c· ....J

o year=2002 • 0 •0. 0

•

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oooeooooo 0000

Finding 3: Relative changes in originations offset by terminations

-Vl Binned Scatterplot: Originations Binned Scatterplot: Terminations

o o year=2002 • c '-...-40 ::::l ...... (])

a:::IJ"l .......... . year=2002 Vl c 0 0 +---------~ ~ ro -~ IJ"lE ~· •.... (J)

1-...-t -c~ .....J

0 •0. 0

•

-1 -.5 0 .5 1 -1 -.5 0 .5 1 Ln(lncome I Returns) Ln(lncome I Returns)

• Growth in stock of debt is

Binned Scatterplot: Stock of Debt-V)

c '-...-4 ::::l.... (J)

a:::IJ"l .......... .... ..0 <1Jo0

0 -~Lf") v I

0.... ~...-t c I

.....J

-1 -.5 0 .5 1

Ln(lncome I Returns)

l:l. Stock == Purchases + Cash-Out - Curtailment - Amortization - Sales

Net fl ow Gross f low in Gross flow out 0 - .(!)<;('-

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19, 2016 9 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 ooooeoooo 0000

Finding 4: Relative increase in churn New Purchase Mortgages/ Al l l st mortgages

- 2001

- 2006

• In marginal areas, there was an increase in transactions (Adelino, et al. (2016) , Mian and Sufi (2009, 2016)).

1 2 3 4 5 Income Quintile

0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 10 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 ooooeoooo 0000

Finding 4: Relative increase in churn New Purchase Mortgages/ Al l l st mortgages

- 2001

- 2006

• In marginal areas, there was an increase in transactions (Adelino, et al. (2016) , Mian and Sufi (2009, 2016)).

1 2 3 4 5 Income Quintile

• People bought more homes

0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 10 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 ooooeoooo 0000

Finding 4: Relative increase in churn New Purchase Mortgages/ Al l l st mortgages

- 2001

- 2006

• In marginal areas, there was an increase in transactions (Adelino, et al. (2016) , Mian and Sufi (2009, 2016)).

Income Quintile • People bought more homes

• People a I so sold more homes

1 2 3 4 5

0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 10 1 1s

Introduction Emprncal Strategy Evide nce lmpltcattons 0000 0 ooooeoooo 0000

Finding 4: Relative increase in churn New Purchase Mortgages/All 1st mortgages

- 2001

- 2006

• In marginal areas, there was an increase in transactions (Adeline, et al. (2016) , Mian and Sufi (2009 , 2016)).

1 2 3 4 5 Income Ouintile

• People bought more homes Owner Occupied, Within CBSA

• People a I so sold more homes

• Role of investors

Income per Return Qulntile

- 2001 - 2006

0 1 2 3 4 5

Foote , Loewenst ei n&. Will en (FRB Boston) Cross Section of Debt September 19, 2016 10 / 18

---

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oooooeooo 0000

Finding 5: No influx of "margina l" borrowers

N 0

0

Probability of Acquiring First Mortgage by Within CBSA Credit Score Quintile

t--1 I..... ---- ... -- • Ql

ON COlli ..... . a. 0 0)

...... ... ... ... ... .... ·-·-·-·-·-·- -·-·-·-· ..... .'

- - - · - · - · - · - 0

------------- ... ... ... I'V

-. .. . ... . ... .... . ... . ... . ... ....------------------ 0

2002 2004 2006 2008 2010 2012

---- l - · -- - · - · - 2 - · - · - · 3 -------· 4 -- S (HighestCredit Scores)

• "Ex tensive margin"

0 L5il - .~!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19 , 2016 11 1 18

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oooooeooo 0000

Finding 5: No influx of "marginal" borrowers Probability of Acquiring First Mortgage by Within CBSA Credit Score Quintile

rl

-e rocx:> NOro • :c \0

0

·-.

-

..... --- ... ·-t-1

:c • Ql ON COlli ..... . a. 0 0)

N 0

0

... ... ... ... .... ·-·-·-·-·-·- ·-· ·-· ' .

------------

...... ..... .

- - - · - · - · ·

----------------- ... ... ... -. .. . ... . ... .... . ... . ... . ... ....

0 I'V

0

2002 2004 2006 2008 2010 2012

---- l - · - · - · - · - 2 - · - · - · 3 -------- 4 -- S(HighestCredit Scores)

• "Extensive margin"

• As documented by Bhutta {2015),

probability of first-time homebuying

(mortgageship), actually went down. 0 .(!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19 , 2016 11 1 18

--------

lntroductcon Empincal Strategy Evidence Implications 0000 0 oooooe ooo 0000

Finding 5: No influx of "marginal" borrowers

Within CBSA ~ • 2001 • 2006

, .. ••

,..••• I ·' •

c;o Q) ,. u .... ,Q) c.. ~N c . -I ~ '

I

• ~ . ~~----------~----------~------------~

-.5 0 .5 1 ln(lncome Per Return)

• Fraction of mortgaged households (not

homeownership rate) by income

0

...-l

N ...-l

...-l

"0 ..... roco NO ro • :I: ~

0

'=t o

N 0

0

Probability of Acquiring First Mortgage by Within CBSA Credit Score Quintile

~ ~------~----------------------------~

1-' :I:

• Ql ON (X)QI..., , Q. 0

-

0\

0

... ----- 0

~

----------------- -- --............. - -·- ..... -N

----------- 0

..................

---·-·-·-···... __ _

L---~----~----~----~------~----~~ 2002 2004 2006 2008 2010 2012

--- - 1 - · - · - · - · - 2 - · - · - · 3 - ------- 4 --- 5 (Highest Credit S<ores)

• ,.Extensive margin"

• As documented by Bhutta {2015),

probability of first- time homebuying

(mortgageship) , actually went down . Foote, Loewenstein & Willen ( FRB Boston) Cross Section of Debt September 19, 2016 11 / 18

--------

lntroductcon Empincal Strategy Evidence Implications 0000 0 oooooe ooo 0000

Finding 5: No influx of "marginal" borrowers

Within CBSA ~ • 2001 • 2006

, .. ••

,..••• I ·' •

c;o Q) ,. u .... ,Q) c.. ~N c . -I ~ '

I

• ~ . ~~----------~----------~----------~

-.5 0 .5 1 ln(lncome Per Return)

• Fraction of mortgaged households (not

homeownership rate) by income

• No change 0

...-l

N ...-l

...-l

"0 ..... roco NO ro • :I: ~

0

'=t o

N 0

0

Probability of Acquiring First Mortgage by Within CBSA Credit Score Quintile

~ ~------~----------------------------~

1-' :I:

• Ql ON (X)QI..., , Q. 0

-

0\

0

... - ---- 0

~

----------------- -- --............. - -·- ..... -N

----------- 0

..................

---·-·-·-···... __ _

L---~----~----~----~----~----~--~ 2002 2004 2006 2008 2010 2012

--- - 1 - · - · - · - · - 2 - · - · - · 3 - ------- 4 -- 5 (Highest Credit S<ores)

• ,.Extensive margin"

• As documented by Bhutta {2015),

probability of first- time homebuying

(mortgageship) , actually went down . Foote, Loewenstein & Willen ( FRB Boston) Cross Section of Debt September 19, 2016 11 / 18

0000 Introduction Empincal Strategy Evidence I m pltcations

o750 0 rl

II 500 ("'' rl 0 ("'1250 ~

~ ro ~ 0

0 ooooooeoo 0000

Finding 5': Rea Iity Check

I I

• Credit availability- all time high

MBA Mortgage Credit Availabi lity Index').

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

0 Oil - .(!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19, 2016 12 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 ooooooeoo 0000

Finding 5': Rea Iity Check

o750 0 ~

II 500 01

0 ~

01 250J:: v 'ro ~ 0

I I

MBA Mortgage Credit Availabi lity Index').

NAR First-T ime Homebuyer Qua lifying

Income

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

• Credit availability- all time high

• Income needed for mortgage all time high

50 ~ 4-0

40~ 0 0 c:

30

0 Oil - .(!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19 , 2016 12 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 ooooooeoo 0000

Finding 5': Rea Iity Check

o750 0 ~

II 500 01

0 ~

01 250J:: v ' ro ~ 0

I I

MBA Mortgage Credit Availabi lity Index').

NAR First-T ime Homebuyer Qua lifying

Income

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

• Credit availability- all time high

• Income needed for mortgage all time high

50 ~ • Affordability - all tim e low 4-0

40~ 0 0 c:

30

0 Oil - .(!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19 , 2016 12 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oooooooe o 0000

Finding 6 : No change in distribution of defaults

• In 2009, disproportionate share of default were low income areas.

0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19, 2016 13 1 18

• •

Introduction Empincal Strategy Evidence I m pltcations 0000 0 oooooooe o 0000

Finding 6: No change in distribution of defaults

• In 2009, disproportionate share of default were low income areas.

• Low income areas always have higher defaults!

Across All Zip Cod es ~

0 2001 • 2009• •

1.1"'1 •

~

('f)

• • • • • • I 0

...... 0 •IU'<t 0a:: • •0

.:!::: •0:I 0

0 •IU

..... 1.1"'1Q) • e. or 0 0

0 c 0

01.1"'1 0 ' 0

0

II)

~ ~~----------~----------~----------~ 3 3.5 4 4.5

ln( lncome Per Return) 0 Oil - .(!)<;('

Foote , Loewenstein & W il len ( F RB Boston) Cross Section of Debt September 19 , 2016 13 1 1s

• • • • • • • • • •

Introduction Empincal Strategy Evidence I m pltcations 0000 0 ooooooo e o 0000

Finding 6: No change in distribution of defaults

• In 2009, disproport ionat e share of default were low income areas.

• Low income areas always have higher defaults!

• With CBSA fixed effects

Across All Zip Cod es Dev iated from CBSA-Year Means

0 2001 • 2009•

0

•0 •

0 0

• 30

•0 ~ <II

0 0 eo 0

c 0

0If\ 0 ' 0

0 If\

' ~ ~ ~~----------~------------~----------~

0 200 1 • 2 0 0 9

0

• 0

••0

0 0

•• 0 -·------------------------ ! _.,_i ___________________________ _ ~ ~

•0

•0

3 3.5 4 4.5 -. 5 0 .5 ln( lncome Per Return) ln(lncome Per Return) .(!)<;('

Foote , Loewenstein & W illen ( F RB Boston) Cross Section of D ebt September 19 , 2016 13 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 ooooooooe 0000

Finding 7: Subprime didn't cause a reallocation, it prevented one

Contributions of Mortgage Types to Total Z IP-Level Debt Growth, by Initial Income Group of ZIP Code: 2001-2006

- Subprime - Alt-A - Prime coco0 . 0N • Subprime was skewed t o low...-'"-. 0 0 1ncome areas. Nco ;..:... c,_ ::II{)Q) • 0:::: "-'O:tQ) • a. .OM-Q)

0-.EC\! 0 -..c...~ 0,_ (.90

· G)co..., 0

. ~ -....j =r

0-<:n:r 0

. CD <.ncr-

1 3 5 7 9 11 13 15 17 19 Income per Return Group of ZIP Code in 2001

0 L5il - .(!)<;('

Foote , Loewenstein & Willen (F RB Boston) Cross Section of Debt September 19, 2016 14 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 ooooooooe 0000

Finding 7: Subprime didn't cause a reallocation, it prevented one

Contributions of Mortgage Types to Total Z IP-Level Debt Growth, by Initial Income Group of ZIP Code: 2001-2006

- Subprime - Alt-A - Prime coco0 . 0N • Subprime was skewed t o low...-'"-. 0 0 1nco me areas. Nco ;..:... c,_ ::II{) • Offset a little by Alt-A Q) •

0:::: "-'O:tQ) • a. .OM-Q)

0-.EC\! 0 -..c...~ 0,_ (.90

· G)co..., 0

. ~ -....j =r

0-<:n:r 0

. CD <.ncr-

1 3 5 7 9 11 13 15 17 19 Income per Return Group of ZIP Code in 2001

0 Oil - .(!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19, 2016 14 1 1s

Introduction Empincal Strategy Evidence I m pltcations 0000 0 ooooooooe 0000

Finding 7: Subprime didn't cause a reallocation, it prevented one

Contributions of Mortgage Types to Total ZIP-Level Debt Growth, by Initial Income Group of ZIP Code: 2001-2006

- Subprime - Alt-A - Prime coco0 . 0N • Subprime was skewed to low...-'"-. 0 0 1ncome areas. Nco ;..:... c,_ ::II{) • Offset a little by Alt-AQ) •

0:::: "-'O:tQ) • • If we only had prime, boom a. .OM-Q) would have resulted in big shift0-.EC\! in debt to high income areas . 0 -..c...~ 0,_ (.90

· G)co..., 0

. ~ -....j =r

0-<:n:r 0

. CD <.ncr-

1 3 5 7 9 11 13 15 17 19 Income per Return Group of ZIP Code in 2001

0 Oil - .(!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19 , 2016 14 1 1s

___ ___________

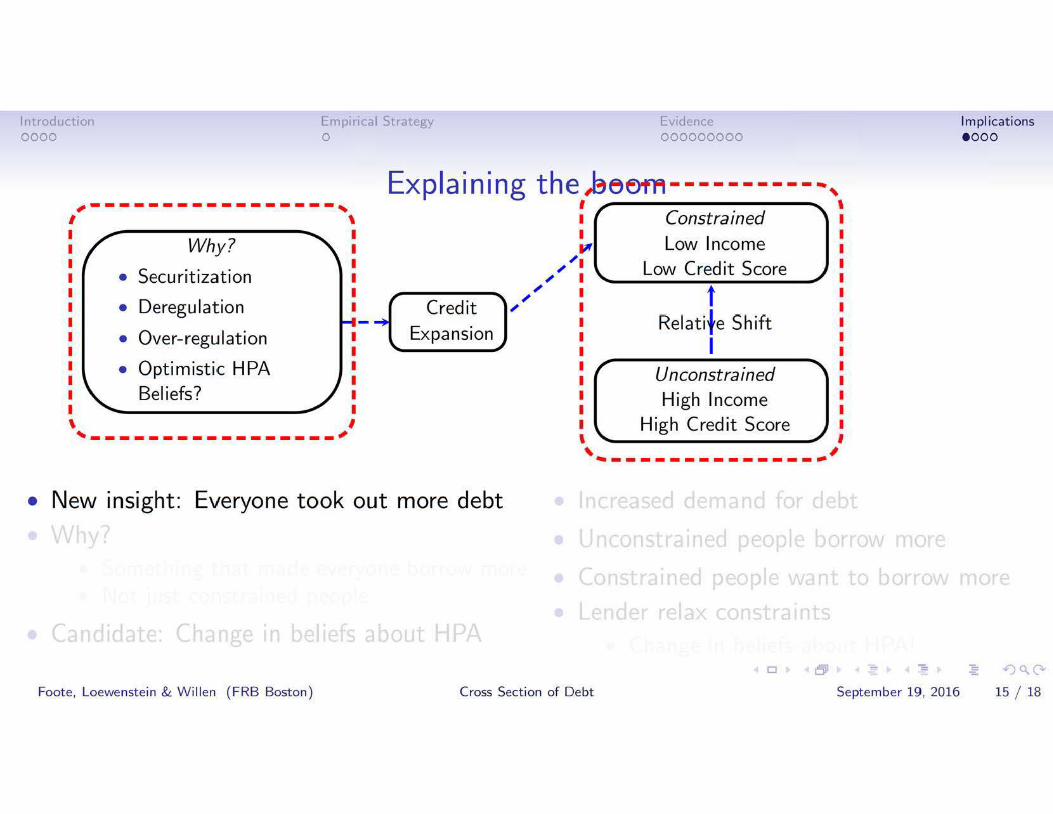

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 eooo

Explaining the ,Beem---- ------ -~ I \ 1 r Constrained " I

Low Income Why? P' ~

Low Credit Score ~ ~ \..• Securitization

~ t~ ~• Deregulation Credit

Relati+e ShiftExpansion• Over-regulation I • Optimistic HPA

,

Unconstrained Beliefs? High Income

\ High Credit Score ~----------------- '

__,

• New insight: Everyone took out more debt

0 L5il - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 1s 1 18

___ ___________

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 eooo

Explaining the ,Beem---- ------ -~

Why?

• Securitization

• Deregulation

,

Credit

Expansion• Over-regulation

• Optimistic HPA Beliefs?

\

~----------------- '

• New insight: Everyone took out more debt

• Why?

I \ 1 r Constrained " I

Low Income P' ~

Low Credit Score ~ ~ \..

~ t~ ~

No Rela~ive Shift

Unconstrained"' High Income

High Credit Score __,

0 L5il - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 1s 1 18

Introduction Empincal Strategy Evidence Impl ications 0000 0

I ~-----------------,

\

Why?

• Securitization

• Deregulation

• Over-regulation

• Optimistic HPA Beliefs?

~-----------------'

• New insight: Everyone took out more debt

• Why? • Something that made everyone borrow more

I I I I I I

I I I I I I

000000000 eooo

---- -------~ \

~~ ~~

~Credit -~

Expansion

I

Explaining the ,Beem I 1 r Constrained " I

Low Income P' ~

~ Low Credit Score ~ '-------~t--------~

No Rela~ive Shift

Unconstrained"' High Income

High Credit Score ,________________,

\

0 L5il - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 1s 1 18

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 eooo

Explaining the ,Beem---- -------~ I \

I ~-----------------,\ 1 r Constrained " I I I I I I

I I I I I I

,

I Low Income Why? P'

~~ ~

~ Low Credit Score ~• Securitization ~~ '-------~t--------~ ~• Deregulation Credit

-~ No Rela~ive ShiftExpansion• Over-regulation

• Optimistic HPA Unconstrained"' Beliefs? High Income

High Credit Score \ I ________________,~-----------------'

• New insight: Everyone took out more debt

• Why? • Something that made everyone borrow more • Not just constrained people

0 L5il - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 1s 1 18

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 eooo

Explaining the ,Beem ---- -------~ I \

I ~-----------------,\ 1 r Constrained " I I I I I I

I I I I I I

_______________,_

I Low Income Why? P'

~~ ~

~ Low Credit Score ~• Securitization ~~ '-------~t--------~

~• Deregulation Credit -~ No Rela~ive ShiftExpansion• Over-regulation

• Optimistic HPA Unconstrained"' Beliefs? High Income

High Credit Score \ I ,~-----------------'

• New insight: Everyone took out more debt

• Why? • Something that made everyone borrow more • Not just constrained people

• Candidate: Change in beliefs about HPA 0 L5il - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 1s 1 18

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 e ooo

Explaining the ,Beem ---- -------~ I \

I ~-----------------,\ 1 r Constrained " I I I I I I

I I I I I I

I Low Income Why? P'

~~ ~

~ Low Credit Score ~• Securitization ~~ '-------~t--------~

~• Deregulation Credit -~ No Rela~ive ShiftExpansion• Over-regulation

• Optimistic HPA Unconstrained"' Beliefs? High Income

\ I High Credit Score ~-----------------'

'~---------------' • New insight: Everyone took out more debt • Increased demand for debt

• Why? • Something that made everyone borrow more • Not just constrained people

• Candidate: Change in beliefs about HPA 0 Oil - .(!)<;('

Foote , Loewenstein & W il len ( F RB Boston) Cross Section of Debt September 19 , 20 16 1s 1 18

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 eooo

Explaining the ,Beem ---- -------~ I \

I ~-----------------,\ 1 r Constrained " I I I I I I

I I I I I I

I Low Income Why? P'

~~ ~

~ Low Credit Score ~• Securitization ~~ '-------~t--------~

~• Deregulation Credit -~ No Rela~ive ShiftExpansion• Over-regulation

• Optimistic HPA Unconstrained"' Beliefs? High Income

\ I High Credit Score ~-----------------'

'~---------------' • New insight: Everyone took out more debt • Increased demand for debt

• Why? • Unconstrained people borrow more • Something that made everyone borrow more • Not just constrained people

• Candidate: Change in beliefs about HPA 0 Oil - .(!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19 , 2016 1s 1 18

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 eooo

Explaining the ,Beem ---- -------~ I \

I ~-----------------,\ 1 r Constrained " I I I I I I

I I I I I I

I Low Income Why? P'

~~ ~

~ Low Credit Score ~• Securitization ~ '---------t~-------'

Credit ~~• Deregulation -~ No Rela~ive ShiftExpansion• Over-regulation

• Optimistic HPA Unconstrained"' Beliefs? High Income

\ I High Credit Score ~-----------------'

'~---------------' • New insight: Everyone took out more debt • Increased demand for debt

• Why? • Unconstrained people borrow more

• Something that made everyone borrow more • Constrained people want to borrow more • Not just constrained people

• Candidate: Change in beliefs about HPA 0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19 , 2016 1s 1 18

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 eooo

Explaining the ,Beem ---- -------~ I \

I ~-----------------,\ 1 r Constrained " I I I I I I

I I I I I I

I Low Income Why? P'

~~ ~

~ Low Credit Score ~• Securitization ~ '---------t~-------'

Credit ~~• Deregulation -~ No Rela~ive ShiftExpansion• Over-regulation

• Optimistic HPA Unconstrained"' Beliefs? High Income

\ I High Credit Score ~-----------------'

'~---------------' • New insight: Everyone took out more debt • Increased demand for debt

• Why? • Unconstrained people borrow more • Something that made everyone borrow more • Constrained people want to borrow more • Not just constrained people

• Lender relax constraints • Candidate: Change in beliefs about HPA

0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19 , 2016 1s 1 18

-----------------

Introduction Empincal Strategy Evidence Impl ications 0000 0

I ~-----------------,\

Why?

• Securitization

• Deregulation

• Over-regulation

• Optimistic HPA Beliefs?

\

000000000 eooo

Explaining the ,Beem ---- -------~

I I I I I I

I I I I I I

-~ Expansion

I

Credit ~~

~-----------------'

• New insight: Everyone took out more debt

• Why? • Something that made everyone borrow more • Not just constrained people

• Candidate: Change in beliefs about HPA

: r Constrained "" I

Low Income P'

~~ ~

~ Low Credit Score ~ ~ '---------t~-------'

No Rela~ive Shift

Unconstrained"' High Income

High Credit Score

'

'

, • Increased demand for debt

• Unconstrained people borrow more

• Constrained people want to borrow more

• Lender relax constraints

• Change in beliefs about HPA! 0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of De bt September 19 , 2016 1s 1 18

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 oeoo

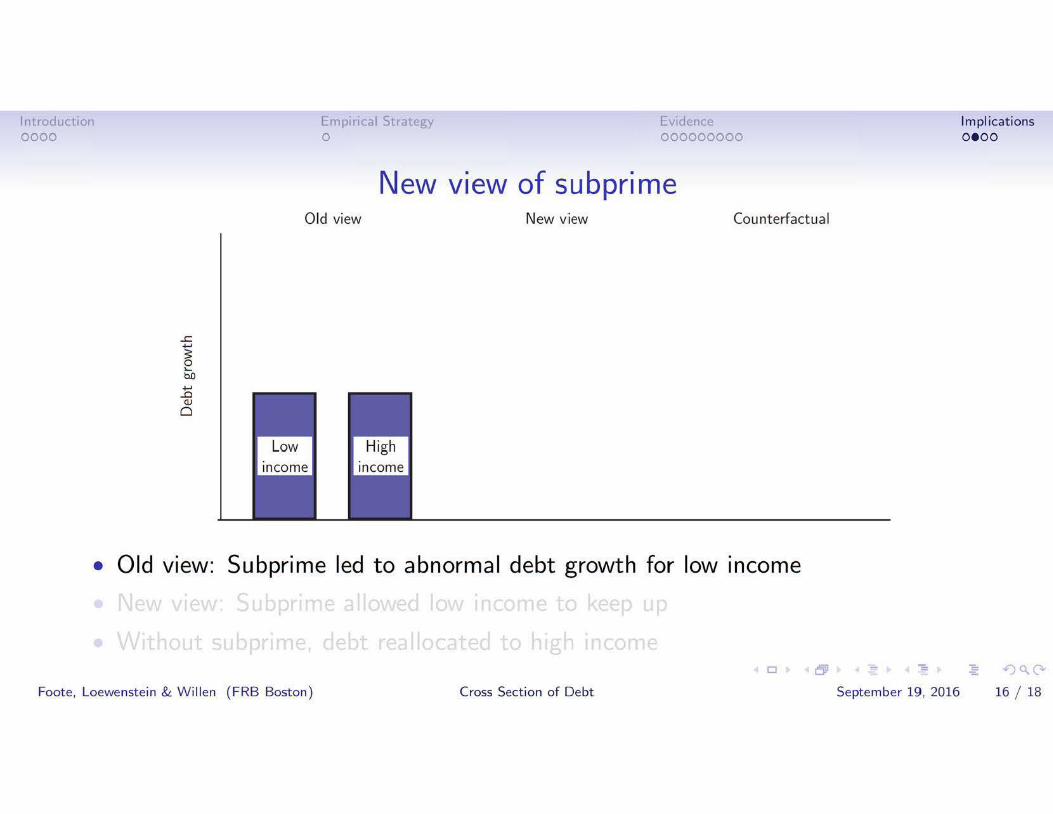

New view of subprime Old view New view Counterfactual

....c ...... g "bD

...... ....0 Q)

0

• Old view: Subprime led to abnormal debt growth for low income

0 Oil - .(!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19 , 2016 16 1 1s

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 oeoo

New view of subprime Old view New view Counterfactual

....c ...... g "bD

...... ....0 Q)

0

• Old view: Subprime led to abnormal debt growth for low income

0 Oil - .(!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19 , 2016 16 1 1s

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 oeoo

New view of subprime Old view New view Counterfactual

....c ...... g "bD

...... ....0 Q)

0

• Old view: Subprime led to abnormal debt growth for low income

0 Oil - .(!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19 , 2016 16 1 1s

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 oeoo

New view of subprime Old view New view Counterfactual

....c ...... g "bD

...... ....0 Q)

0

• Old view: Subprime led to abnormal debt growth for low income

0 Oil - .(!)<;('

Foote , Loewenstein & W il len (F RB Boston) Cross Section of Debt September 19 , 2016 16 1 1s

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 oeoo

New view of subprime Old view New view Counterfactual

....c ...... g "bD

...... ....0 Q)

0

• Old view: Subprime led to abnormal debt growth for low income

0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 16 1 18

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 oeoo

New view of subprime Old view New view Counterfactual

....c ...... g "bD

...... ....0 Q)

0

• Old view: Subprime led to abnormal debt growth for low income

• New view: Subprime allowed low income to keep up

0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 16 1 18

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 oeoo

New view of subprime Old view New view Counterfactual

....c ...... g "bD

...... ....0 Q)

0

• Old view: Subprime led to abnormal debt growth for low income

• New view: Subprime allowed low income to keep up

0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 16 1 18

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 oeoo

New view of subprime Old view New view Counterfactual

....c ...... g "bD

...... ....0 Q)

0

• Old view: Subprime led to abnormal debt growth for low income

• New view: Subprime allowed low income to keep up

• Without subprime, debt reallocated to high income 0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 16 1 18

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 ooe o

Contribution of Non-Prime PLS Lending

Total Debt~

99 00 01 02 03 04 05 06 07 08 09 10 11

• T ota I debt rose a bout 6

trillion

0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 17 1 1s

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 ooe o

Contribution of Non-Prime PLS Lending

~------------

10 I

Total Debt~

---------------------·

• T ota I debt rose a bout 6~:I trillion ~ I fl • Suppose all that had

happened in the boom061

was securitized subpri me

and Alt-A541 --- I ""2001 Debt

99 00 01 02 03 04 05 06 07 08 09 10 11

0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 17 1 1s

Introduction Empincal Strategy Evidence Implications 0000 0 000000000 ooe o

Contribution of Non-Prime PLS Lending

Total Debt~

99 00 01 02 03 04 05 06 07 08 09 10 11

• T ota I debt rose a bout 6

trillion

• Suppose all that had

happened in the boom

was securitized subpri me

and Alt-A

0 Oil - .(!)<;('

Foot e , Loewenstein & Willen (F RB Boston) Cross Section of Debt September 19, 2016 17 1 1s

Introduction Empincal Strategy Evidence Implications 0000 0 000000000 ooe o

Contribution of Non-Prime PLS Lending

Total Debt '\t

2001 Debt+Subprime /+Alt-A

99 00 01 02 03 04 05 06 07 08 09 10 11

• T ota I debt rose a bout 6

trillion

• Suppose all that had

happened in the boom

was securitized subpri me

and Alt-A

0 Oil - .(!)<;('

Foot e , Loewenstein & Willen (F RB Boston) Cross Section of Debt September 19, 2016 17 1 1s

Introduction Empincal Strategy Evidence Impl ications 0000 0 000000000 oooe

The slide you've all been waiting for.. .

0 Oil - .(!)<;('

Foote , Loewenstein & W illen (F RB Boston) Cross Section of Debt September 19 , 2016 18 1 18

Introduction Empincal Strategy Evidence Implications 0000 0 000000000 oooe

The slide you've all been waiting for.. .

• The end .

0 Oil - .(!)<;('

Foot e , Loewenstein & Willen (F RB Boston) Cross Section of Debt September 19, 2016 18 1 18