current austrlian economic trends and 2015 predictions

TRANSCRIPT

MatthewPearce EconomicsReport

ReportontheCurrentEconomicSituationinAustraliaandPredicted

Trendsfor2015

MatthewPearce

ExecutiveSummaryThisreportgivesadetailedanalysisoftheeconomicsituationfacingAustraliaat theendof2014.ByexaminingdatacollectedthroughtheReserveBankofAustraliaandtheAustralianBureauofStatistics, itconsidersthe factors thatcontribute to Gross Domestic Product (GDP) growth of Consumption (C),Investment(I),Government(G)andNetExport(NX)expendituresadheringtotheframework:

GDP(Y/E)=C+I+G+NXIt further suggestswhatGDP growth trends are expectedmoving into 2015andforecastifanymonetarytools(specificallyincashratemovements)canbeemployedtoencouragethisgrowth.Inconsideringall thedevelopmentsmoving into2015, thisreportwillarguethat the Australian economy is currently in a contraction phase of theeconomic cycle, with growth expectations set to be below trend in 2015.However the report concludes thatwhilemonetary policy is a viable tool tohelp grow the economy, at the present moment it is limited inwhat it canachieveoverthenext12monthsinAustralia.Giventhemanyvariablessuchasour already historically low interest rates and the downward trend of thedollar, the best action of the RBA in 2015 is to remain conservative in itsapproachtomonetarypolicyandnotchangethecashrate.Ratherthereportsuggeststhatgiventhealreadyvolatilestateoftheeconomy,aratecutcouldservetohampereconomicgrowthratherthanfacilitateit.

MatthewPearce EconomicsReport

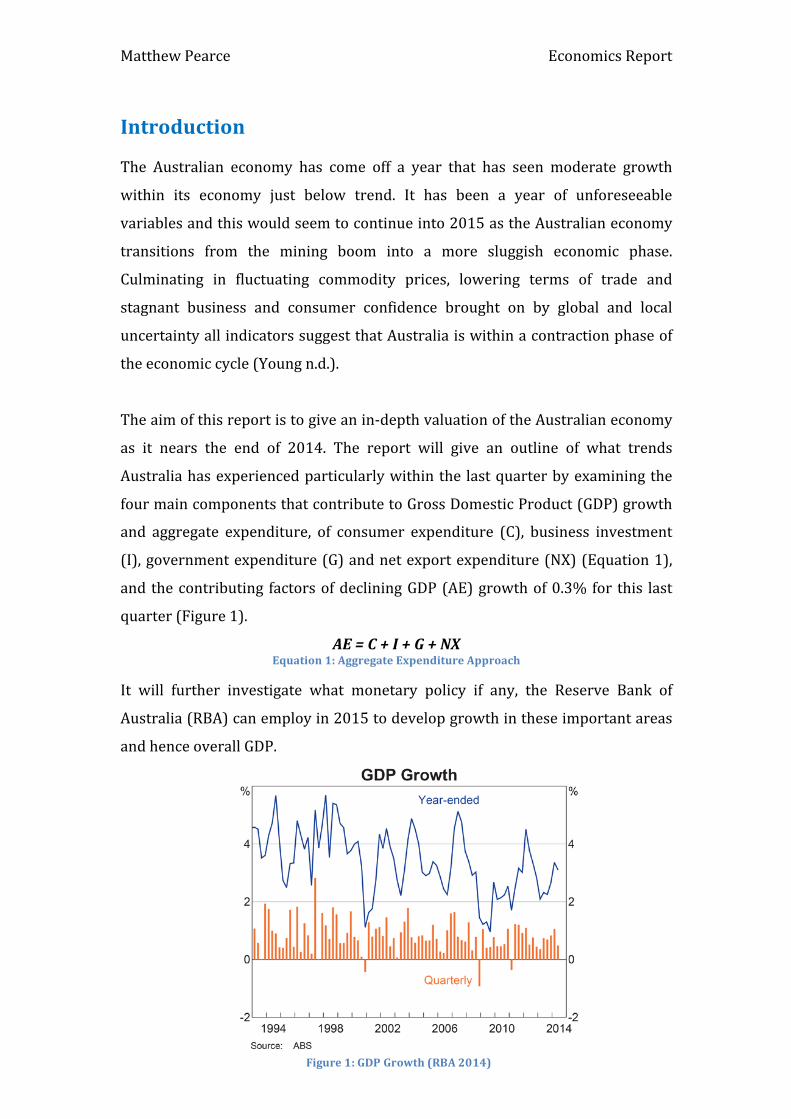

IntroductionThe Australian economy has come off a year that has seen moderate growth

within its economy just below trend. It has been a year of unforeseeable

variablesandthiswouldseemtocontinueinto2015astheAustralianeconomy

transitions from the mining boom into a more sluggish economic phase.

Culminating in fluctuating commodity prices, lowering terms of trade and

stagnant business and consumer confidence brought on by global and local

uncertaintyallindicatorssuggestthatAustraliaiswithinacontractionphaseof

theeconomiccycle(Youngn.d.).

Theaimofthisreportistogiveanin-depthvaluationoftheAustralianeconomy

as it nears the end of 2014. The report will give an outline of what trends

Australiahasexperiencedparticularlywithinthe lastquarterbyexaminingthe

fourmaincomponentsthatcontributetoGrossDomesticProduct(GDP)growth

and aggregate expenditure, of consumer expenditure (C), business investment

(I),governmentexpenditure(G)andnetexportexpenditure(NX)(Equation1),

and thecontributing factorsofdecliningGDP(AE)growthof0.3%for this last

quarter(Figure1).

AE=C+I+G+NXEquation1:AggregateExpenditureApproach

It will further investigate what monetary policy if any, the Reserve Bank of

Australia(RBA)canemployin2015todevelopgrowthintheseimportantareas

andhenceoverallGDP.

Figure1:GDPGrowth(RBA2014)

MatthewPearce EconomicsReport

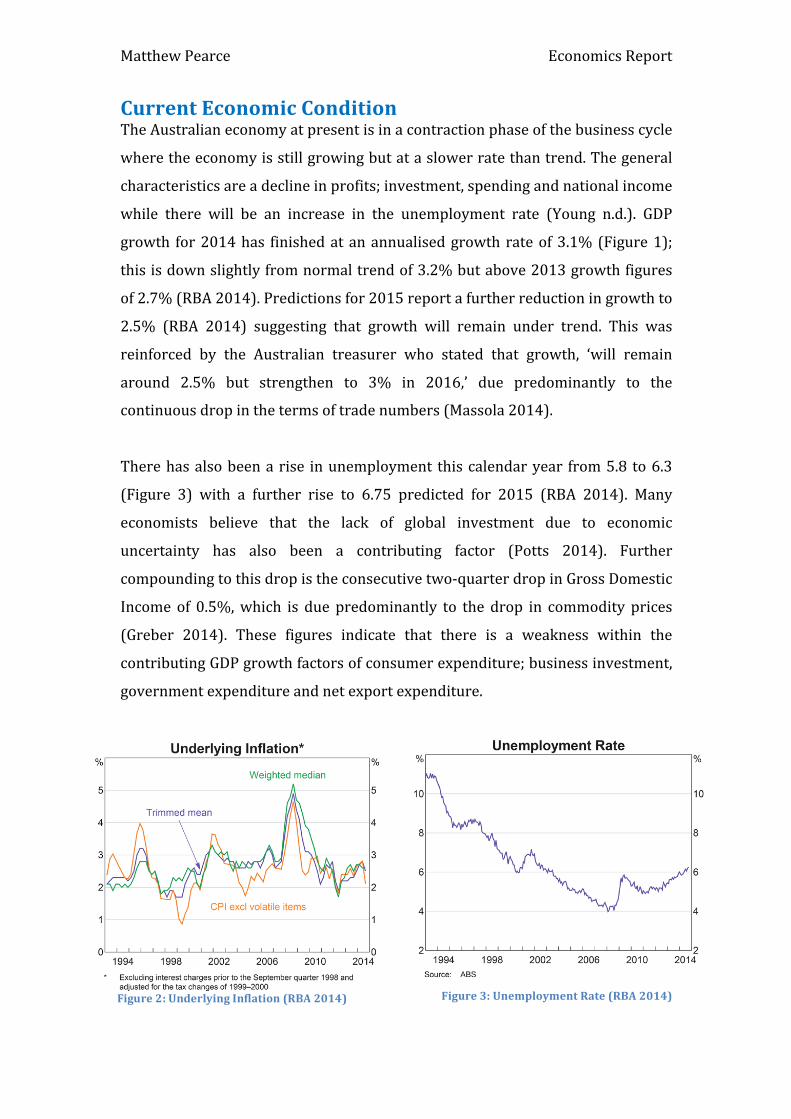

CurrentEconomicConditionTheAustralianeconomyatpresentisinacontractionphaseofthebusinesscycle

wheretheeconomyisstillgrowingbutataslowerratethantrend.Thegeneral

characteristicsareadeclineinprofits;investment,spendingandnationalincome

while there will be an increase in the unemployment rate (Young n.d.). GDP

growth for2014has finishedatanannualisedgrowthrateof3.1%(Figure1);

thisisdownslightlyfromnormaltrendof3.2%butabove2013growthfigures

of2.7%(RBA2014).Predictionsfor2015reportafurtherreductioningrowthto

2.5% (RBA 2014) suggesting that growth will remain under trend. This was

reinforced by the Australian treasurer who stated that growth, ‘will remain

around 2.5% but strengthen to 3% in 2016,’ due predominantly to the

continuousdropinthetermsoftradenumbers(Massola2014).

Therehasalsobeenarise inunemployment thiscalendaryear from5.8 to6.3

(Figure 3) with a further rise to 6.75 predicted for 2015 (RBA 2014). Many

economists believe that the lack of global investment due to economic

uncertainty has also been a contributing factor (Potts 2014). Further

compoundingtothisdropistheconsecutivetwo-quarterdropinGrossDomestic

Income of 0.5%,which is due predominantly to the drop in commodity prices

(Greber 2014). These figures indicate that there is a weakness within the

contributingGDPgrowthfactorsofconsumerexpenditure;businessinvestment,

governmentexpenditureandnetexportexpenditure.

Figure3:UnemploymentRate(RBA2014)Figure2:UnderlyingInflation(RBA2014)

MatthewPearce EconomicsReport

ConsumerExpenditureThis is the amount that consumers spend on durable, non-durable goods and

servicesinagivenperiodtherebycontributingtothegrowthofGDP(Farnham

2010).Thelevelofconsumptionexpenditureisinfluencedbyavarietyoffactors

suchasincome(Y),personaltaxes(Tp),interestrates(r),consumerconfidence

(CC),personalwealth levels(W),availablecredit(CR)andpersonaldebt levels

(D).

C=f(Y,Tp,r,CC,W,CR,D)(+)(-)(-)(+)(+)(+)(-)

Equation2:TheConsumptionFunction

Currently in Australia there has been a significant weakness within some of

these consumer function indicators. The rise in unemployment and weak

demand has led to a fifteen-year slump inwages growth of 2.6% (ABS 2014).

Addedtothisistheloweringofdispensableincome(Yd)dueto‘bracketcreep,’

whereannualinflationarypayrisespusheslowandmiddle-incomeearnersinto

higher tax brackets (Tp) without a real increase in income this is seen by

economist asneither efficientnor equitable (Sloan2014) and leads to a lower

dispensable income level (Yd= Y - Tp). Consumer confidence has also seen its

lowest recordings (Figure 4) since August 2011 with a 5.7% drop in the

Westpac-Melbourne Institute measure of consumer sentiment (‘Consumer

SentimentSlumpsto3yearLow’2014).

Figure4:ConsumerSentiment(RBA2014) Figure5:HouseholdWealth&Liabilities(RBA2014)

However therearepositivesignswithin thehouseholdwealth, creditanddebt

levelindicators.Nethouseholdwealthlevelsareclimbinggraduallytopre-Global

MatthewPearce EconomicsReport

Financial Crisis numbers as a percentage of household disposable income and

are amongst the highest by global standards, while debt is holding steady at

around150%ofdisposableincome(Figure5)whichJohnSuttonoftheBankof

Queensland states as ‘a verymanageable level’ (Potts 2014). Because of these

positivefiguresandafavourablecashrateof2.5%(RBA2014)creditavailability

for the housing and personal sectors is slowly rising as banksmake available,

‘low-interestandno-interest loans’(Potts2014).Overall though, thesepositive

factorshavenotbeenenough tobalance thenegative impact of low consumer

confidence, increased taxation and lowerwage growth creatingwhat Nicholas

MooreofMacquarieBankdescribesasaconsumer‘demanddeficit’(Durie2014,

p. 25).Thiswill in turnhaveanegativeaffecton consumeraggregatedemand

andwillthereforeshifttotheleftinthecomingyear(Graph1).

Graph1:ConsumerAggregateDemandPrediction2015

BusinessInvestmentBusiness investment levels determine how much the private business sector

invests in structures, equipment and technology to improve its capacity to

produce goods and meet consumer demand (Farnham 2010). Like the

consumptionfunctiontherearearangeofinfluencesonhowmuchbusinesswill

investintheseareassuchasincome(Y),interestrates(r),Taxationonbusiness

(Tb),profitexpectations(PR)andCapacityUtilization(CU).

AD1

AD2

SAS

Y

PL

Y1Y2

PL1

PL2

Positives:r,CR,W,D

Negatives:Y,Yp,CC

MatthewPearce EconomicsReport

I=f(Y,r,Tb,PR,CU)(+)(-)(-)(+)(+)

Equation3:TheInvestmentFunction

The lack of consumer demand therefore has had a negative affect on business

income and investment. The significant decline in investment in the mining

sector(Figure6)hascompoundedthisissue(RBA2014)astheindustrymoves

into its production phase. The RBA has also looked to moderate business

spendingwithinthehousinginvestmentmarketbyreducingtheamountofnon-

residentialbuildingapprovals(Figure7)(Greber2014).Consequentlytherehas

beennegativetrendinbusinessinvestmentthroughout2014(Figure8).

Figure8:TotalBusinessInvestment(RBA2014)

To counter the slowing in investment in the housing and mining sectors, the

federalgovernmentandtheRBAwill looktoprovideincreasedincome(Y)and

credittobusinessthroughaplannedcompanytaxcutof1.5%in2015(Tb)and

making available cheap credit (r) for non-mining business investment (Figure

10).Thishas led to an increase inbusiness confidenceandprofit expectations

Figure6:MiningandNon-MiningInvestment(RBA2014)

Figure7:Non-ResidentialBuildingApprovals(RBA2014)

MatthewPearce EconomicsReport

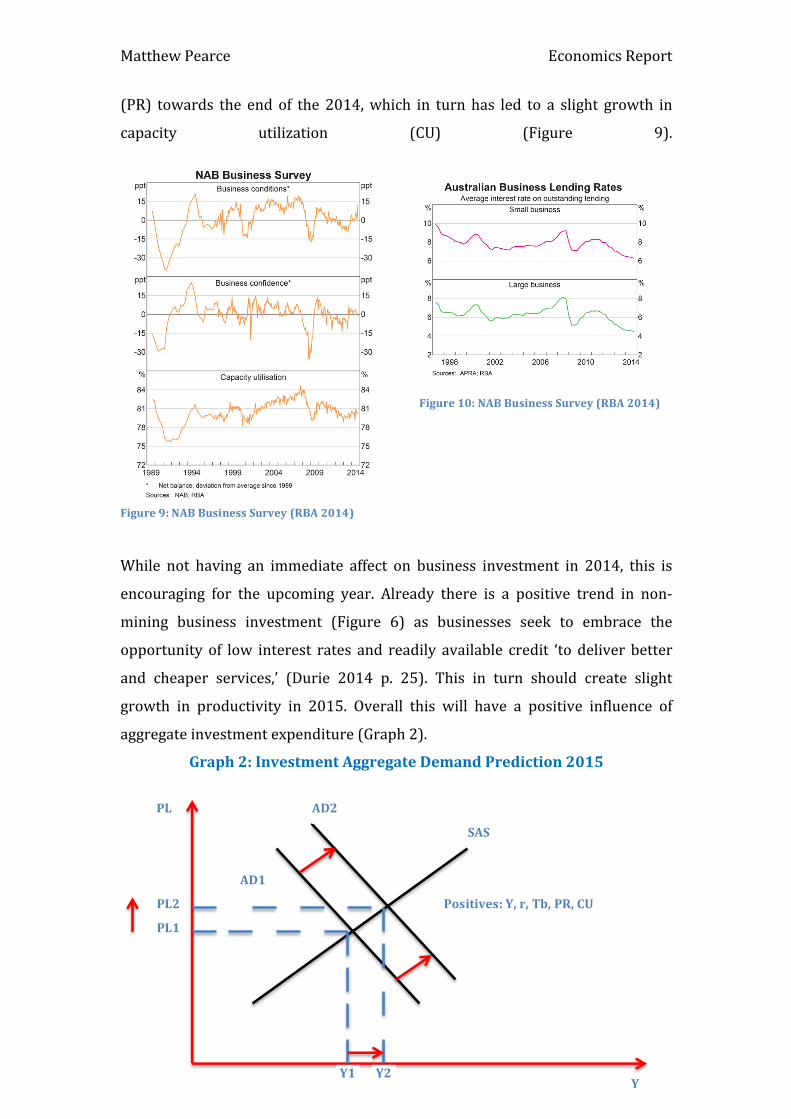

(PR) towards the end of the 2014,which in turn has led to a slight growth in

capacity utilization (CU) (Figure 9).

Figure10:NABBusinessSurvey(RBA2014)

While not having an immediate affect on business investment in 2014, this is

encouraging for the upcoming year. Already there is a positive trend in non-

mining business investment (Figure 6) as businesses seek to embrace the

opportunity of low interest rates and readily available credit ‘to deliver better

and cheaper services,’ (Durie 2014 p. 25). This in turn should create slight

growth in productivity in 2015. Overall this will have a positive influence of

aggregateinvestmentexpenditure(Graph2).

Graph2:InvestmentAggregateDemandPrediction2015

Figure9:NABBusinessSurvey(RBA2014)

AD2

AD1

SAS

Y

PL

Y2Y1

PL2

PL1

Positives:Y,r,Tb,PR,CU

MatthewPearce EconomicsReport

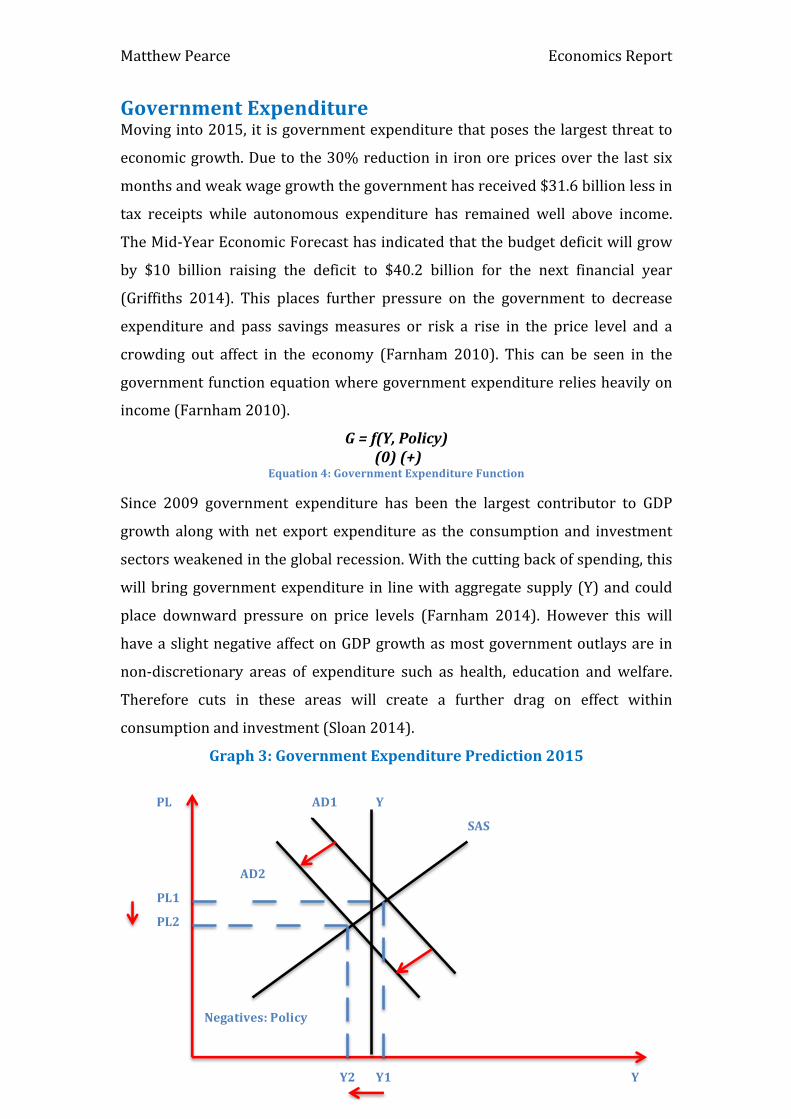

GovernmentExpenditureMovinginto2015,itisgovernmentexpenditurethatposesthelargestthreatto

economicgrowth.Duetothe30%reductionin ironorepricesoverthe lastsix

monthsandweakwagegrowththegovernmenthasreceived$31.6billionlessin

tax receipts while autonomous expenditure has remained well above income.

TheMid-YearEconomicForecasthasindicatedthatthebudgetdeficitwillgrow

by $10 billion raising the deficit to $40.2 billion for the next financial year

(Griffiths 2014). This places further pressure on the government to decrease

expenditure and pass savingsmeasures or risk a rise in the price level and a

crowding out affect in the economy (Farnham 2010). This can be seen in the

governmentfunctionequationwheregovernmentexpenditurereliesheavilyon

income(Farnham2010).

G=f(Y,Policy)(0)(+)

Equation4:GovernmentExpenditureFunction

Since 2009 government expenditure has been the largest contributor to GDP

growth alongwithnet export expenditure as the consumption and investment

sectorsweakenedintheglobalrecession.Withthecuttingbackofspending,this

willbringgovernmentexpenditure in linewithaggregatesupply(Y)andcould

place downward pressure on price levels (Farnham 2014). However this will

haveaslightnegativeaffectonGDPgrowthasmostgovernmentoutlaysare in

non-discretionary areas of expenditure such as health, education andwelfare.

Therefore cuts in these areas will create a further drag on effect within

consumptionandinvestment(Sloan2014).

Graph3:GovernmentExpenditurePrediction2015

AD1Y

AD2

SAS

Y

PL

Y1Y2

PL1

PL2

Negatives:Policy

MatthewPearce EconomicsReport

NetExportExpenditureThefallingpriceswithinthecommoditiesmarketplacesfurtherpressureonnet

export expenditure or termsof trade.Net export expenditure is the difference

between the costs of imports against export revenue (Equation 5). As such

overseas, income (GDP/Y*) and currency exchange (R) is a large factor in the

revenuereceivedfromexports(Farnham2010).

X=f(Y,Y*,R)(0)(+)(-)

Equation5:ExportExpenditure

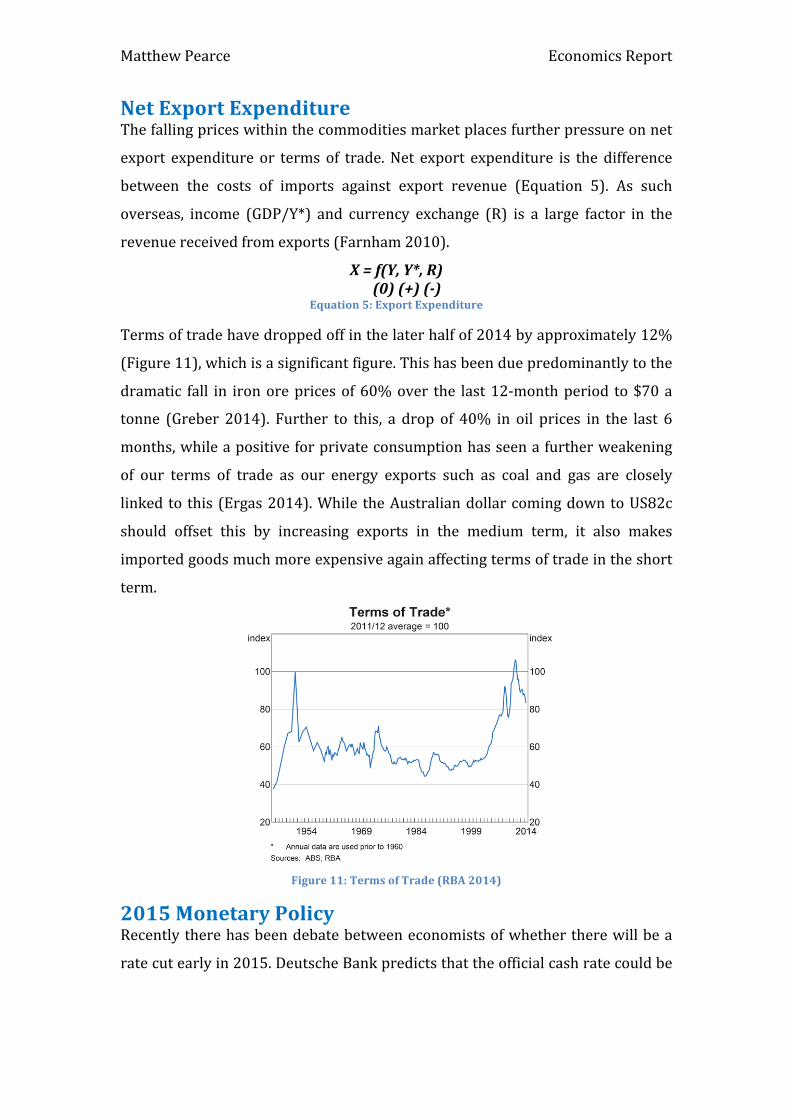

Termsoftradehavedroppedoffinthelaterhalfof2014byapproximately12%

(Figure11),whichisasignificantfigure.Thishasbeenduepredominantlytothe

dramatic fall in ironorepricesof60%over the last12-monthperiod to$70a

tonne (Greber 2014). Further to this, a drop of 40% in oil prices in the last 6

months,whileapositiveforprivateconsumptionhasseenafurtherweakening

of our terms of trade as our energy exports such as coal and gas are closely

linkedto this (Ergas2014).While theAustraliandollarcomingdowntoUS82c

should offset this by increasing exports in the medium term, it also makes

importedgoodsmuchmoreexpensiveagainaffectingtermsoftradeintheshort

term.

Figure11:TermsofTrade(RBA2014)

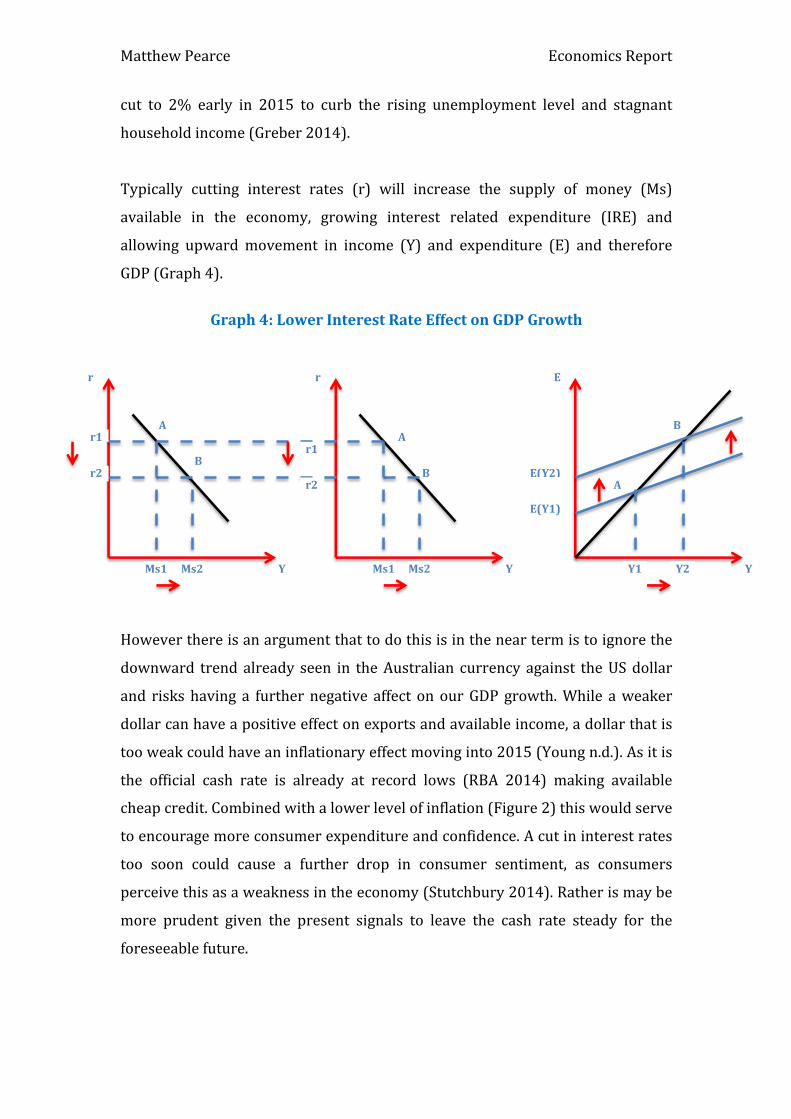

2015MonetaryPolicyRecentlytherehasbeendebatebetweeneconomistsofwhethertherewillbea

ratecutearlyin2015.DeutscheBankpredictsthattheofficialcashratecouldbe

MatthewPearce EconomicsReport

cut to 2% early in 2015 to curb the rising unemployment level and stagnant

householdincome(Greber2014).

Typically cutting interest rates (r) will increase the supply of money (Ms)

available in the economy, growing interest related expenditure (IRE) and

allowing upwardmovement in income (Y) and expenditure (E) and therefore

GDP(Graph4).

Graph4:LowerInterestRateEffectonGDPGrowth

Howeverthereisanargumentthattodothisisintheneartermistoignorethe

downward trendalready seen in theAustralian currency against theUSdollar

and riskshaving a furthernegative affect onourGDPgrowth.While aweaker

dollarcanhaveapositiveeffectonexportsandavailableincome,adollarthatis

tooweakcouldhaveaninflationaryeffectmovinginto2015(Youngn.d.).Asitis

the official cash rate is already at record lows (RBA 2014) making available

cheapcredit.Combinedwithalowerlevelofinflation(Figure2)thiswouldserve

toencouragemoreconsumerexpenditureandconfidence.Acutininterestrates

too soon could cause a further drop in consumer sentiment, as consumers

perceivethisasaweaknessintheeconomy(Stutchbury2014).Ratherismaybe

more prudent given the present signals to leave the cash rate steady for the

foreseeablefuture.

r1

r2

r1

r2

Ms1 Ms2 Ms2Ms1 Y1 Y2

A

B

E(Y2)

E(Y1)

Y

Err

Y Y

AA

BB

MatthewPearce EconomicsReport

This argument is further supportedbyGlennStevens the governorof theRBA

who indicatedonDecember12th that therewouldn’tbeanear termcutas the

dollar is expected to fall to US75c independently. This reflects the downward

pressurethecontinuedgrowthoftheUSeconomyandtheweakeningofenergy

priceshasontheAustraliandollar(Stutchbury2014).Ratherfocusshouldbeon,

‘being more efficient and more productive, and using our labour and capital

resourcesinawaythatgetsmoreoutputperheadovertime,’(Stutchbury2014).

ConclusionOverallwhiletherearesomepositivesignsfor2015withinbusinessnon-mining

investment and a predicted increase in exports due to the lowering dollar.

However thiswillnotbeenough to counter theweaknesswithin consumption

demand and a cut to government expenditure. These two combinedwhile not

takingtheeconomyintorecessionwillkeepgrowthundertrend(Graph4).

Graph4:TotalAD/ASGraph

Whiletheconversationattheendof2014hasbeenaboutrepairing‘confidence’

in the economy, most economists agree that there should be a concerted

emphasisonbuildingcompetivenesswithinourstructuraleconomy.51of76top

Australian CEO’s when interviewed agreed that while the ‘economic base in

AD1

AD2

SAS

Y

PL

Y1Y2

PL1

PL2

LAS

Trend

MatthewPearce EconomicsReport

Australia is sound,’ (Durie 2014) there needs to be more focus on factors

affecting productivity within the economy such as tax reform, budget reform,

infrastructure investment, IR reform and federation reform. This can only be

achieved through government fiscal policy and therefore limits what effect

monetarypolicycanhave.