c.v.o. ca’s news & views vol. 19 no. 12 / june … 2016/fulljune.pdf · to real estate/...

TRANSCRIPT

C.V.O. CA’S NEWS & VIEWS VOL. 19 NO. 12 / JUNE 2016

3

From the desk of ChairmanA Word for The Wise…..

NEWS BULLETINCOMMITEE

ChairmanCA Champak Dedhia

Office BearerCA Ketan Gada

AdvisorCA Ramesh Chheda

ConvenorCA Ameet Chheda

Jt. ConvenorCA Deepesh Chheda

MembersCA Poojan Dedhia

CA Mitul FuriaCA Virav Dedhia

CA Vishesh SangoiCA Tejas GangarCA Kaushik Gada

Sp. InviteesCA Rakesh Vora

C O N T E N T S

ASSOCIATION NEWS

Forth ComingEvents ....................... 4

Events Retrospect ..... 4

Notice of AGM .......... 5

A R T I C L E S

MinimumAlternate TaxRegime ...................... 6

Companies(Auditor's Report)Order, 2016 ............ 12

Levy of ServiceTax on the Servicesprovided byGovernment ora Local Authorityto BusinessEntities Relatingto Real Estate/ConstructionIndustry ................... 20

Digital OfficeProductivity SeriesPart 3:BackupManagement ........... 25

LEGAL UPDATESCentral ExciseUpdates ................... 27

FEMA Updates ........ 29

Success is not the key to happiness. Happiness is the key to success. If you love what you are doing,you will be successful.

True KnowledgeWilliam Blake, a renowned English poet and a mystic writer once said “Knowledge is an eternaldelight”. However cryptic as it may sound, it is very profound in its exact context. Simply put, TrueKnowledge is one that fills us with eternal delight; everlasting bliss that does not beget arrogance ofits attainment.

Look round and what we find is that knowledge in current time is often mistaken for information. Weoften feel insecure, unhappy because we apparently do not possess those super skills of interpretingand assimilating constant barrage of information that is bombarded on us. Preoccupied with effortsin interpreting, we not only feel inadequate but forget the joy that true knowledge brings in our lives.As Eric Berne writes “That moment a little boy is concerned with knowing which is jay and which isa cuckoo, he has lost his joy of hearing them sing”.

It is the lack of True knowledge that deprives us from progressing towards the real purpose of ourlives- which is to attain eternal joy by enlightening ourselves.

What is a True Knowledge?

True Knowledge is wisdom that life in human form is a blessing endowed by the Almighty totranscend beyond ‘Have and have not’. It is a journey which may begin with yearning for ‘ many andmore’ but culminates where there is sheer abundance without possessions. It is something whichgives sense of fulfilment not from physical or intellectual possessions but from enlightenment aboutcosmic laws of universe.

These cosmic laws are:

1. Freedom of choice :Greatest of human freedom is the ability to make choices in life. Realisationthat we are what we have chosen to become can be a life-changing experience. No one can makeus sad or inadequate, unfulfilled and unaccomplished without our consent. Power of knowing thatlife as given is a blank slate where we have choice to determine our roadmap both by thought andaction is the supreme knowledge which is extremely potent.

2. Process of evolution :Knowledge that life is an evolving process brings great serenity in our lives.Nature wants us to learn from our mistakes, not punish us with low self esteem. Every mistake thatwe make, every obstacle that we face is a great lesson for us to move forward in life by knowingwhat ought to have been done. It gives us opportunity to integrate ourselves seamless with theprocess of change that nature desires for our growth and betterment. This knowledge teaches usto flow and not resist.

3. Abundance:The thin line dividing humanity from divinity is a knowledge that everything inuniverse is in abundant supply. The understanding that we mustcultivate is that universe is madeup of energy which is constantly flowing. In order to get more from life we must be prepared togive more. This giving should not originate from compulsion or expectation of receivingsomething in return but out of sheer love and compassion of giving. Giving can be a compliment,help, charity or even a benign smile. When we learn to give, we create space for positive energiesin our lives which in turn creates space for positive magneticforce of attracting like- minded peopleand environment conducive to achieving a true sense of fulfilment and bliss.

German Philosopher Frederic Nietzsche wrote “If you want to be a devotee of truth then enquireinto what seems intangible”. A simple question ‘Who amI?’ led Almighty to his salvation. Why then,not begin the search for True Knowledge right from today? Why not yearn for that treasure which shallbring an eternal delight in our lives.

Let us seek True Knowledge to live a fulfilled life.

Warm Regards,

9th June, 2016. CA Champak K. Dedhia

VOL. 19 NO. 12 / JUNE 2016 C.V.O. CA’S NEWS & VIEWS

4

Compiled by :CA. Ameet ChhedaCA. Deepesh Chheda

ASSOCIATIONNEWS

FORTH COMING EVENTS

STUDY CIRCLE COMMITTEE has organizedstudy circle onDISPUTE RESOLUTION AND INCOMEDECLARATION SCHEME AS NOTIFIEDUNDER FINANCE ACT, 2016.Day & Date : Thursday, 16th June-2016.Venue : D.R.Ghalla Memorial HallTime : 5.30 P.M. to 8.30 P.M.Faculty : CA Nimesh Chotani.

MEMBERS IN INDUSTRY & ASSOCIATESCOMMITTEE has organizedRole of Women CA-Practice / Industry /Entrepreneur and Corridor of Opportunities forWomen CADay & Date : Saturday, 18th June, 2016.

Venue : SNDT College Dome,

Cama Lane, Ghatkopar-(w)

Time : 4.00 P.M. to 7.00 P.M.

Role of Women CA-Practice/ CA Bhavna DoshiIndustry/Entrepreneur Past CCM, ICAI

PANEL DISCUSSIONStatutory Audit, CA AshaInd AS, IFRS RamanathanDirect & International CA Neetu VinayekTaxation Partner, KPMGIndirect Taxation CA Deepali Mehta

Partner, Shah & SavlaInternal Audit, Controls, CA Sumangali Shah,Risk Management VP Internal Controls-

Kohinoor ConstructionsCorporate Laws, SEBI & other CA Neha Gada,regulatory compliances Ex BSE Surveillance HeadOpportunities from ICAI & CA Priti SavlaPanel Moderator RCM-WIRC of ICAI

Programme Committee has organized publicprogramme onREAL ESTATE REGULATION ACT, 2016 &REDEVELOPMENT OF SOCIETYDay & Date: Saturday, 25th June-2016.Venue : King George School Auditorium,

Dadar (CR)Time : 9.00 A.M. to 1.00 P.M.Faculties : Shri Sumit Vadhavkar, Advocate

Shri Dhiren Nandu, Advocate & Solicitor

Do not be embarrassed by your failures, learn from them and start again.

EVENTS RETROSPECTCCA Course Committee had organizedORIENTATION PROGRAMME OFCCA COURSE ( BATCH-3)Day & Date : Saturday, 28th May-2016.Venue : D.R.Ghalla Memorial HallTime : 6.30 P.M. to 7.30 P.M.Attendance : 15 Persons

STUDY CIRCLE COMMITTEE had organizedSTUDY CIRCLES on(A) AUTOMATION IN MVAT &

E-FILING OF NEW MVAT RETURNS.Day & Date : Tuesday, 17th May-2016.Venue : Mysore Auditorium, Matunga.Time : 5.00 P.M. to 8.30 P.M.Faculty : Nitin Shaligram & Team.

Project Director,Dy Comm & Staff )

Attendance : 275

(B) “REPORTING ON INTERNAL FINANCECONTROL (IFC) & CARO” UNDER THECOMPANIES ACT - 2013.Day & Date : Tuesday, 31st May-2016.Venue : D.R.Ghalla Memorial HallTime : 5.30 P.M. to 8.30 P.M.Faculty : Ripan H.Gada

(Asst. Vice President ofEdelweiss Group - ( NBFCs Div).

Chairman : CA Hasmukh Dedhia.Attendance : 50+

Membership & Recreation Committee (MRC) has planned“CVO PICNIC”. Enjoy rejuvenating and exchangingfellowship amongst CVO CA Members and their Family atSHILPI HILL RESORT, SAPUTARA, GUJARAT.

Departure : Sat, 13th Aug 2016 6.00 am

Date of return : Mon, 15th Aug 2016

Venue : Shilpi Hill Resort, Saputara, Gujarat.

Charges : Rs.9,500/- per person- twin sharing basis.Additional person (same room sharing)will be Rs. 5,000/- per person.(Includes transportation to Saputara)

For queries contactCA Ketan Gada 9819748830CA Ameet Chheda 9967564433

For more pictures visit hotel websiteor https://www.makemytrip.com

C.V.O. CA’S NEWS & VIEWS VOL. 19 NO. 12 / JUNE 2016

5Success is simple. Do what’s right, the right way, at the right time.

NOTICE OF ANNUAL GENERAL MEETING

The 34th Annual General Meeting of the Association will be held on Sunday, 26th June 2016 at 3.00 p.m.at Chinchpokli Mahajanwadi's Shri Velji Lakhamshi Napoo Hall, Shri K V O Sthanakwasi Jain Mahajanwadi,Dr. Ambedkar Road, Opp. Voltas, Chinchpokli, Mumbai - 400 012 to transact the following business :

1. To adopt the minutes of the 33rd Annual General Meeting of the Association held on 4th July 2015.

2. To receive and adopt the Audited Balance Sheet as at 31st March, 2016 and Income & Expenditure Account for theyear ended on that date.

3. To receive and adopt the Annual Report of the Managing Committee for the year 2015-2016.

4. To elect 13 (Thirteen) members of the new managing committee for the term 2016-18 and to declare its results.

5. To Appoint the Honorary Auditor of the Association for the year 2016-2017.

6. Distribution of Prizes:

(i) To distributes Late Shri D. R. Ghalla and M/s. Damji Merchant & Co. Prizes.

(ii) To honour the students who have passed both the groups together in first attempt at Intermediate/Finalexamination of C.A., I.C.W.A. and / or C.S. courses and to felicitate students who have passed Final exams ofthe said courses as also merit rank holders in Entrance (CPT) of said courses, results of which have beendeclared during 04th July, 2015 to 25th June 2016

(iii) To present prize to the contributors of the Best Article in the News & Views of the Association for the period July,2015 to June, 2016

7. Any other matters with the permission of the Chair.For C. V. O. Chartered & Cost Accountants' Association

Place : Mumbai CA Nilesh T. DedhiaDate : 03/06/2016 Secretary

NOTES1. In the absence of quorum at the appointed time, the meeting shall be adjourned and such adjourned meeting will be

convened after half an hour at the same place and the business transacted thereat shall be deemed to be in order.

2. The meeting shall be followed by self contributory dinner, charges of which are Rs.100/- per person for the members,their spouse and children above 5 years.

3. Books of Account for F.Y. 2015-2016 shall be available for inspection by members between 20th June, 2016 & 22ndJune, 2016 from 4.00 p.m. to 6.00 p.m. at Association's Office.

4. TENTATIVE PROGRAMME3:00 p.m. to 3:30 p.m. Fellowship over Tea & Coffee3:30 p.m. to 5:45 p.m. Annual General Meeting6:00 p.m. to 9:00 p.m. Entertainment Programme8:00 p.m. to 9:00 p.m. Dinner

(Arrangements for Chouvihar at 6.00 pm)

5. K.V.O. CA's Wives Forum will organise the games and entertainment programme for their members and children from3:00 p.m. to 5:45 p.m. at another banquet hall of the venue.

VOL. 19 NO. 12 / JUNE 2016 C.V.O. CA’S NEWS & VIEWS

6

BACKGROUNDMinimum Alternate Tax (MAT) was effectively

introduced in India by the Finance Act of 1987, videSection 115J of the Income Tax Act, 1961 (Act), to

facilitate the taxation of ‘zero tax companies’. It had

been observed that many companies, despite showing

high profits in their books of accounts and paying

substantial dividends, were paying marginal or no

tax, by taking advantage of various tax concessions

and other incentives, in a manner so as to avoid

paying tax1. MAT was thus envisaged as levying a

minimum tax on such companies by deeming a

certain percentage of their book profits, computed

under the Companies Act, as taxable income. Section

115J was, however, made inoperative from

Assessment Year 1991-922.

The MAT provisions were subsequently reintroduced

in 1996 by the Finance Act (No. 2) of 1996, through

section 115JA; and then by the Finance Act of 2000,

which replaced section 115JA with Section 115JB.

BASIC PROVISIONSection 115JB provides that in case the tax payable

on the total income of a company in respect of any

previous year, computed under the Act, is less than

18.5% of its book profit, such book profit shall be

deemed to be the total income of such company. The

tax payable for the relevant year for such company

shall then be 18.5% of its book profit.Book profit

represents net profit as per profit and loss account

subject to certain additions and deletions specified

therein.

If in any year the company pays liability as per MAT,

then it is entitled to claim credit of MAT paid over

and above the normal tax liability in the subsequent

year(s).The provisions relating to carry forward and

adjustment of MAT credit are given in section

115JAA.

ISSUES AND ANALYSISThere are many issues related to section 115JB,

which have been the matter of contention between

the assessees and the Department. While some of the

issues have been settled by way of amendment in the

Act, the other few issues still remain to be addressed.

MINIMUM ALTERNATE TAX REGIME

Contributed by :CA Tejas Gangara member of the association

he can be reached [email protected]

The key challenges while dealing with MAT along

with certain important aspects of MAT are discussed

as follows:

Q Is withdrawal from ‘provision created in a MAT

year’ allowed as reduction only if such provision

actually suffered MAT in that year?

A The significance of the phrase‘Where this

section is applicable’ is merely to indicate the

general applicability of MAT provisions in the

year of withdrawal and it does not mean that

MAT should actually become payable. In

Circular No. 8 of 2002 dated 27 August 2002

which has explained the purpose of the said

proviso in s.115JB is reproduced below:-

“It also provides that any amount withdrawnfrom a reserve or a provision created on or after1st day of April, 1997, and which is credited tothe profit and loss account shall not be reducedfrom the book profit, unless the book profits in theyear of creation of such reserves or provisionswere increased by the amount transferred to suchreserves or provisions at that time.”

The above extract makes it clear that there is no

pre-condition of MAT liability being triggered in

the year of creation of reserve/provision. In any

case, applicability of section 115JB does not

necessarily mean incurrence of MAT liability. It

only means that the company is required to

compare normal tax and tax on ‘book profit’.

Q. Whether deduction of extra depreciation as

arrears of past years while computing book

profit is allowable?

A. Although, the assessee has an option under the

Companies Act of adopting a straight line

method or written down value method for

claiming depreciation; however, deduction of

extra depreciation as arrears of past years while

computing book profit is not allowable, as has

been held by the Madhya Pradesh High Court in

the case of Gilt Pack Ltd. vs. Union of India

[2007] (163 Taxman 331). While arriving this

conclusion, the High Court followed the

judgement of the Hon’ble Supreme Court in the

case of Karnataka Small Scale Industries

Development Corporation vs. CIT [2002] (AIR

SCW 4926).

1 Circular No. 495, dated 22 September, 1987: [1987] 168 ITR (St.) 87.2 Circular No. 572 dated 3 August, 1990: [1990] 186 ITR (St.) 89

Success means doing the best we can with what we have.Success is the doing, not the getting; in the trying, not the triumph.

C.V.O. CA’S NEWS & VIEWS VOL. 19 NO. 12 / JUNE 2016

7

Q. A taxpayer is liable to pay INR 100mn taxes

under MAT provisions. Against this, INR 80mn

can be availed of by the taxpayer as MAT credit

under section 115JAA in future against its taxes

under the provisions of the Act other than MAT

and is therefore, recognised as an asset in its

financial statements and disclosed in the profit

and loss account as a separate line item.

Therefore, a question arises as to what is the

amount that needs to be adjusted for

determining book profits for the purpose of MAT

(INR 100mn or INR 20mn).

A. As the taxpayer is liable to pay tax under MAT,

in effect the income-tax provision (other than

MAT) for the current year is INR 20mn.

Explanation 1 to section 115JB(2) provides for a

formula to arrive at book profits. Clause (a) to

this explanation provides that “net profit as

shown in Profit and Loss account….as increased

by – (a) the amount of income-tax paid or

payable, and the provision therefore.”

Explanation 2 provides that for purpose of

clause (a) of Explanation 1, the amount of

income-tax shall include certain specified items,

such as tax on distributed profits, interest,

surcharge and cess. This provision does not

specify that MAT credit (under section 115JAA),

that can be availed of in future, should be

factored in while computing “book profit”. Also,

according to Accounting Standards

Interpretation (ASI) 6, MAT is “current tax”.

Hence, it would appear that the adjustment

contemplated would have to be gross amount of

INR 100mn under clause (a). However, this

would lead to an absurd result of requiring to

add back INR 100mn, whereas the net impact to

the profit and loss account on account of taxes is

only INR 20mn. Also, this would result in

effectively having to pay MAT on MAT credit (of

INR 80mn).

It may be noted that clauses (h) and (viii) have

been inserted in the Explanation to section

115JB(2) by the Finance Act, 2008 to provide for

an adjustment on account of deferred tax. The

memorandum explaining the introduction of the

explanation provides as follows:

“As per the Explanation after sub-section (2), theexpression “book profit” means net profit asshown in the profit and loss account prepared inaccordance with the provisions of Part II and IIIof Schedule VI to the Companies Act, 1956 as

increased or reduced by certain adjustments, asspecified in that section. Clause (a) of theaforesaid Explanation, inter-alia, provides forincreasing the book profits by income-tax paid orpayable and the provisions therefore; if debited toprofit and loss account.

The intention behind these add backs is that theitems which mainly appear “below the line” inthe profit and loss account should be added backto arrive at the “book profit” if they appear “abovethe line” in the profit and loss account. Section115JB has not specifically provided for add backof some such “below the line” items like deferredtax, dividend distribution tax, etc. as they werethought to be included in the term “income-tax”.However, there has been some ambiguityregarding add back of these items, if debited toprofit and loss account.

With a view to clarifying the intention, it isproposed to insert a new clause after clause (g) ofthe Explanation 1 as so numbered so as toprovide that the book profit shall be increased bythe amount of deferred tax and the provisiontherefor, if debited to profit and loss account.”

Therefore, it may be possible to adopt a position

that MAT credit is also contemplated to be

adjusted as a “deferred tax” under Explanation

(1)(viii) to section 115JB(2) of the Act, if credited

to the Profit and Loss Account, such that the

objective of items which appear “below the line”

are adjusted to arrive at the “book profit”. Also,

MAT credit may be considered as a “negative”

current tax requiring adjustment to arrive at the

net figure of INR 20mn under clause (a).

Thus, in the example provided above, where the

current year provision is on account of MAT

liability (INR 100mn as MAT, against which a

MAT credit for INR 80mn would be available in

future) the amount debited to the Profit and loss

account on account of income tax would be INR

20mn, in which the case, the adjustment for

current year tax under Explanation (1)(a) to

section 115JB(2) could be INR 20mn, because

effectively the Profit and loss account is debited

by that amount.

Q. Whether comparison of unabsorbed losses and

depreciation should be on year to year basis?

A. There are two views on this as explained below:

View 1: Year to year basis

Action is the foundational key to all success.

VOL. 19 NO. 12 / JUNE 2016 C.V.O. CA’S NEWS & VIEWS

8

Reference is drawn to the Central Board of Direct Taxes (CBDT) Circular 495 dated 22 Sept 1987 (168 ITR

St. 110) to illustrate the position as may emerge if the quantification is done on a year to year basis:

Year Profit Lower of Loss or(excluding Net Book of depreciationdepreciation) Depreciation profit/loss Set off Profit carried forward

1984 (300,000) (100,000) (400,000) (400,000) (100,000)

1985 500,000 (200,000) 300,000 (100,000) 200,000

1986 (1,000,000) (200,000) (1,200,000) - (1,200,000) (200,000)

1987 1,000,000 (200,000) 800,000 (200,000) 600,000

The methodology approved by the Circular can be explained as follows:

z The process of comparison of depreciation or business loss is to be carried out every year.

z In case of loss year, or the successive loss years, the loss component or the depreciation component,

whichever is lower of the respective year is to be carried forward.

z In case of profit year, the lower of the brought forward component will be set of to the extent profit

and losses remaining unabsorbed will be carried forward.

The methodology suggested in the Circular has been largely accepted by the Authority of Advance Ruling

(AAR), New Delhi in the case of RashtriyaIspat Nigam Ltd. In re. [2006](285 ITR 1).

View 2: Consolidated approachThe consolidated figure brought forward business loss at the beginning of the year is traced to two

components: the aggregate unadjusted amount of business loss and the aggregate unadjusted amount of

depreciation comprised in the consolidated loss. The lower of the two is accepted as permissible set off

amount.

Year Profit /(loss) (excluding depreciation) Depreciation Profit/loss after depreciation

1984 (300,000) (100,000) (400,000)

1985 500,000 (200,000) (300,000)

1986 (1,000,000) (200,000) (1,200,000)

Aggregate (800,000) (500,000) (1,300,000)

1987 1,000,000 (200,000) 800,000

As per this approach, for the year 1987, the brought forward loss as per books of account is INR 1,300,000

which comprises of brought forward losses of INR 800,000 and unabsorbed depreciation of INR 500,000.

The lower of the two, being unabsorbed depreciation of INR 500,000is allowed to be set-off. The Mumbai

Tribunal in the case Amline Textiles Ltd vs. ITO [2009](27 SOT 152) upheld the above view.

The method suggested as per CBDT Circular of 1987 may not be the preferred method as it requires

reckoning of carry forward of losses from inception of the Company. It appears that in absence of mandate

in section 115JB, the consolidated review approach appears closer to language of clause (iii) of Explanation

1 of section 115JB in as much as:

z Pursuant to this method, the amount of losses and unabsorbed depreciation will not be different from

the amount brought forward as per books of accounts

z The method did not contemplate, the preparation of parallel set of records of year to year working

which is different from the accounts prepared and presented under the Companies Act.

I cannot give you the formula for success, but I can give you the formula for failure which is: Tryto please everybody.

C.V.O. CA’S NEWS & VIEWS VOL. 19 NO. 12 / JUNE 2016

9

Q. Whether comparison between tax payable as per the regular provisions of the Act and the tax payable as

per section 115JB of the Act is required to be made before or after taking credit for the foreign taxes?

A. The issue can be examined as follows:

Particulars Tax Computation

As per regular As perprovision (INR) MAT (INR)

Foreign sourced income on which tax in foreign country

is paid at 20%

- Eligible for section 10A deduction ….(I) 600 600

- not eligible for section 10A deduction 100 100

Domestic income

- Eligible for section 10A deduction ….(II) 100 100

- Not eligible for section 10A deduction 200 200

Total Income before section 10A deduction 1000 1000

Deduction under section 10A of the Act …(I+II) 700 NIL*

Chargeable Total Income …(III) 300 1000

Tax liability at 30%/18.5% respectively of III above** …(IV) 90 185

Doubly taxed income included in IV above …(V) 100 700

FTC available at 20% /18.5% respectively on doubly taxed

income as per III above …(VI) 20 130

Net Taxable Income after FTC (IV minus VI) …(VII) 70 65

*No deduction under section 10A of the Act is admissible in computation of MAT profit

** Rates presumed

View 1 – Comparison of tax liability should be made at level IV i.e. before claiming credit for foreign taxes

paid. This view proceeds on the basis that foreign tax payment is a mode of discharging tax liability. This

requires comparison to be made between normal tax liability of INR 90 and MAT liability of INR 185. From

INR 185, foreign taxes of INR 130would be deducted and the balance amount of INR 65 would be payable

by the taxpayer. The contents to support this view are:

z Section 115JB of the Act requires comparison between ‘income-tax payable’ as computed under the

regular provisions of the Act and income-tax @18.5% on book profits. The term ‘tax payable’ would

mean the gross liability of tax i.e tax liability before deducting advance tax, tax deduction at source

(TDS) and rebates and relief which may be available.

z Section 91 of the Act, which provides for unilateral relief (in absence of DTAA), provides for

“…deduction from income-tax payable’. Section 91 of the Act requires that the relief for FTC be

computed on the basis of the comparison of the Indian rate of tax with the rate of tax of foreign

country. For the purpose of this section, the Indian rate of tax is determined by dividing the amount

of Indian income-tax (before deduction of any relief) by the total income.

z The provisions of section 234B/234C of the Act also seem to equate FTC as an alternative mode of

discharging a tax liability as an alternative to tax deducted at source.

· The Income-tax Return form clearly indicates that double taxation relief is to be provided after

application of provisions of section 115JB of the Act and not in the process of determination of liability

under this section.

You’ve got to get up every morning with determination if you’re going to go to bed with satisfaction

VOL. 19 NO. 12 / JUNE 2016 C.V.O. CA’S NEWS & VIEWS

10

View 2 – The comparison is made at Level VII.

As per this view, if FTC obliterates the Indian

tax liability, the tax liability as per regular

provisions of INR 70 is payable as it is higher

than the MAT liability of INR 65.

As per section 4 of the Act, the charge of income

tax is subject to the provisions of the Act and

hence, the charge of income-tax is subject to

relief from tax provided under sections 90 and 91

of the Act and MAT payable, after considering

the credit for foreign taxes paid in each of the

computations. On the basis of the foregoing

discussion, View 1 appears to be a better view.

Q. Does the draft rules provide for any guidance for

grant of FTC where MAT is payable

A. The CBDT vide notification dated 18 April 2016

released draft rules on FTC. One of the aspects

considered is in respect of grant of FTC where

tax is payable under the provisions of section

115JB of the Act. The draft rule provides that

the credit of foreign tax shall be allowed against

MAT in the same manner as is allowable against

tax payable under the normal provisions of the

Act. However, the said provision has come with

a rider that where the amount of FTC available

against the tax payable under the provisions of

section 115JB exceeds the amount of tax credit

available against the normal provisions, then

while computing the amount of credit under

section 115JAA in respect of the taxes paid

under section 115JB, as the case may be, such

excess shall be ignored. The said provision is

clarificatory and will obviate taking claim of

excess FTC twice, first, directly upon payment of

taxes when being paid under MAT and second,

indirectly by means of MAT credit against future

tax liabilities.

Q. Whether the taxpayer has choice of selecting the

period for availing MAT credit u/s 115JAA in

view of non-claim of credit in an intervening

period.

A. MAT credit will need to be claimed for the

consecutive assessment years starting from the

year in which the credit becomes allowable. It is

not the option of the taxpayer to pick and choose

the year in which the credit may be claimed

within the overall limitation period of ten years.

This can be supported by following reasons:

z In terms of section 115JAA(1A) / (2A), the

MAT credit is quantified by taking into

account the difference between MAT

liability and normal tax liability. This

necessarily requires comparison between

the tax liabilities for the given assessment

years under the alternative computation

mechanism. By implication, the

quantification is related to the respective

assessment year and is not impacted by the

actual date of payment of tax.

z Proviso to section 115JAA(2A) provides that

there is no interest payable in respect of tax

credit which is allowed under section

115JAA. section 234A to section 234C make

it clear that in determining the quantum of

interest liability, credit allowed to be set off

in accordance with the provisions of section

115JAA needs to be considered.

z The CBDT Circular No 3 of 2006 dated 27

Feb 2006 while explaining the

reintroduction of section 115JAA w.e.f. A.Y.

2006-07 does also make it clear that the

provisions need to be implemented on year

on year basis with clear FIFO application

when a given year has MAT credit available

from more than one year.

Q. Whether the provisions of advance tax are

applicable on companies paying MAT?

A. It has been clarified by Circular No.13/2001

dated 9 September 2001 that provisions of

advance tax are also applicable on the

companies paying MAT and interest under

section 234B/C is levied in case of default by

these companies. This view has been affirmed by

the Honb’le Supreme Court in the case of JCIT

vs. Rolta India Ltd. [2011](196 Taxman 594).

Q. Whether MAT credit is preferred to credit for

advance tax/ TDS payment while working out

interest liability u/s 234B or while granting

interest u/s 244A to the taxpayer on refund of

advance tax paid?

A. It is true that in few cases as also SC ruling in

the case of Tulsyan NEC Ltd [2010](330 ITR

226), Courts have considered MAT credit in

preference to advance tax/ TDS payment while

working out interest liability u/s 234B or while

granting interest u/s 244A to the taxpayer on

refund of advance tax paid. However, in all these

cases Tax Authority had tried to create double

whammy or absurd situation for the taxpayers

wherein inspite of eligible MAT credit being

available for set off, Tax Authority levied

Success is going from failure to failure without losing enthusiasm

C.V.O. CA’S NEWS & VIEWS VOL. 19 NO. 12 / JUNE 2016

11

interest under section 234B or denied grant of

interest under section 244A in such situations

i.e. despite MAT credit standing to the account

of the taxpayer, it’s liability gets increased

instead of getting reduced.

In the case of CIT vs Bharat Aluminium Co. Ltd.

[2007](160 Taxman 388), theDelhi High Court

held that MAT credit is available for adjustment

on the first date of the previous year even before

the instalment of advance tax is due on the

current income. Further, in case of Sami Labs

[2011](ITA No. 231 of 2009), the Karnataka High

Court held that MAT credit is as much as a tax

paid in earlier year and is available by way of

credit to be adjusted in future years.

In light of above and given the fact that there is

no specific provision to set out priority under the

Act, the taxpayer has an option to appropriate

his entitlement i.e. TDS, advance tax, MAT

credit against the liability which it owes in

favour of the tax department.

Q. Whether penalty under section 271(1)(c) is

levied for situations where the income

determined under the general provisions is less

than the income declared for the purpose of MAT

under section 115JB of the Act?

A. In this regard, the CBDT Circular No.25 of 2015

dated 31 December 2015 states the following:

The Delhi High Court in the case of Nalwa Sons

Investment Ltd. [2010] (194 taxman 387) held

that when the tax payable on income computed

under normal procedure is less than the tax

payable under the deeming provisions of section

115JB of the Act, then penalty under section

271(1)(c) of the Act could not be imposed with

reference to additions /disallowances made

under normal provisions.

Subsequently, Explanation 4 to section 271(1) of

the Act have been substituted by Finance Act,

2015 with effect from 1 April 2016, provides the

methodologyfor calculating the amount of tax

sought to be evaded for situations even where

the income determined under the general

provisions is less than the income declared for

the purpose of MAT under section 115JB of the

Act.

Q. Whether MAT is applicable to foreign

companies?

A. Vide Finance Act 2016, Explanation 4 to section

115JB(2) has been introduced (effective from

assessment year 2001-02 to provide for non-

applicability of MAT to a foreign company if-

z It is a resident of a country with which India

has a Double Taxation Avoidance

Agreement (DTAA) and does not have a

permanent establishment in India; or

z It is a resident of a country with which India

does not have a DTAA and the foreign

company is not required to register under

any law applicable to companies.

Q. Whether MAT credit can be transferred to a

buyer by means of slump sale as compared to a

merger

A. Transition of MAT credit to the purchaser by

way of slump sale, inter alia, may not be allowed

on account of following reasons:

z transaction of a slump sale involves

transfer between two private parties which

is distinguishable from merger where there

is direction flowing from the Court order

which may guide one to a different

conclusion.

z MAT credit being in the nature of advance

tax is an asset of the taxpayer and not of the

undertaking. As credit for advance tax is

allowed to the person who makes payment

of the taxes, one may argue that only the

company which has paid tax u/s 115JB is

entitled to carry forward and set off of MAT

credit.

z MAT credit binds the taxpayer and the Tax

Department, a third party cannot

participate in the same.

Our Association’s mouthpiece “News & Views” hasreadership circulation of more than 1250 charteredaccountant and student members.

We have now started accepting advertisement forany vacancy for staff. In case you have any vacancyat your office or at any of your client for qualifiedchartered accountants or students or anyadministrative job, we will publish your requirementin the Journal.

This will be at very nominal cost of Rs. 1,500 forquarter page advertisement per issue. We will betaking advertisement on first cum first serve basis.

Kindly contact CVO CA Office on +91-22-24105987and speak to Vaibhavi for more details.

If you want to make an easy job seem mighty hard, just keep putting off doing it.

VOL. 19 NO. 12 / JUNE 2016 C.V.O. CA’S NEWS & VIEWS

12

COMPANIES (AUDITOR'S REPORT)ORDER, 2016

Contributed by :Dhrumi Dedhiaa student member of the association

she can be reached [email protected]

BackgroundSec 143(11) of the Companies Act, 2013 (‘the Act’) mandates the auditors of certain class of companies to report

on some additional prescribed matters as an annexure to the main audit report. These reporting requirements

have been prescribed under the Companies (Auditor’s Report) Order (CARO), 2016 issued by the Ministry of

Corporate Affairs (MCA) on 29th March, 2016, replacing the existing CARO, 2015, thereby bringing in some

additional reporting requirements, removing a few clauses as well as remolding certain existing provisions.

ApplicabilityCARO 2016, shall apply to financial year commencing on or after 1st April, 2015.

Applicability Non-Applicability

z All private companies which z Banking Company2

are subsidiaries or holding z Insurance Company3

companies of any public z Companies Incorporated with charitable objects4

company irrespective of z Small Company as defined under Sec 2(85)5 of the Act

their capital, borrowings, z One Person Company as defined under Sec 2(62)6 of the Act

turnover etc. z Private Company satisfying all of the following conditions:

z Foreign Company as defined a) Paid Up Capital + Reserves & Surplus < 1 Crore as on

under Sec 2(42)1 of the Act. Balance Sheet date(Previously Rs.50 Lakhs)

b) Borrowings from Bank or Financial Institutions < 1 Crore at

any time during the Financial Year (Previously Rs.25 Lakhs)

c) Revenue < 10 Crore during the financial year

(Previously Turnover Rs.5 Crore)

z CARO, 2016 shall not apply to Consolidated

Financial Statements (CFS)

The scope of applicability of CARO has now been relaxed. The increase in the thresholds will relieve the small

and medium sized entities from the burden of additional reporting. By virtue of this move, many entities that

were previously liable to report under CARO, now might not be covered due to the revised limits.

Reporting Requirements

1. Sec 2(42) of the 2013 Act defines foreign company as ‘any company or body corporate incorporated outside India which

z Has a place of business in India whether by itself or through an agent, physically or through electronic mode and

z Conducts any business activity in India in any other manner’

2. Banking company as defined in clause (c) of section 5 of the Banking Regulation Act, 1949

3. Insurance company as defined under the Insurance Act, 1938

4. Companies licensed to operate under section 8 of the Companies Act,2013

5. As per sec 2(85) a Small Company means a company other than a Public Company, that satisfies both of these conditions:

z Paid-up share capital which does not exceed 50 lac rupees AND

z Turnover of which as per its last profit and loss account does not exceed 2 crore rupees

6. As per sec 2(62), One Person Company means a company which has only one member.

“Happiness is the art of never holding in your mind the memory of any unpleasant thing that has passed.”

C.V.O. CA’S NEWS & VIEWS VOL. 19 NO. 12 / JUNE 2016

13

Additional Reporting

Clause Additional Reporting Points to be taken into consideration

Clause (i)(c) Whether title deeds of z TDRs (Transferable Development Rights), Plant and

Fixed Assets immovable properties are Machinery embedded in land etc., are not considered as

held in the name of the an immovable property.

company. If not, details

to be provided. z The auditor should carry out detailed examination in the

cases where immovable property is transferred as a

result of conversion of partnership firm or LLP into

company or amalgamation of companies, as in such cases

title deeds may be in the name of the erstwhile entity.

Clause (iv) In respect of loans, z Section 185 prohibits advance of any loan to directors,

Loans & investments, guarantees, etc., directly or indirectly.

Investments and security whether

provisions of section z For this purpose, the auditor should carry out the

185 and 186 of the Act, following procedures:

have been complied with. (i) Obtain from the management the details of the

If not, provide the directors or any other person in whom the director

details thereof. is interested. He may also check the details of the

persons covered under this clause from Form

MBP-1 and from the Register maintained u/s 189

of the Act.

(ii) Obtain and check the details of the transactions

carried out with such persons, including of any

guarantee given and security provided.

(iii) Further examine the details to find out whether any

of the transaction is attracting the provisions of

section 185 of the Act.

(iv) In case of transactions that are covered under the

exceptions as provided under section 185, the

auditor should obtain the necessary evidence in

support of such exception

z Sec 186 of the Act governs with giving of loans, and

guarantee or providing any security in connection with

a loan, by a company to any person or other body

corporate and acquiring securities of any other body

corporate by a company. The section also prohibits

a company from making investments through more than

two layers of investment companies.

z For this purpose, the auditor should carry out the

following procedures:

(i) Obtain the details of, loans given to any person or

other body corporate, guarantee given or security

provided in connection with a loan to any other body

corporate or person and securities acquired of any

other body corporate by way of subscription,

purchase or otherwise, made during the year as well

as the outstanding balances as at the beginning of

the year.

“Happiness is the art of never holding in your mind the memory of any unpleasant thing that has passed.”

VOL. 19 NO. 12 / JUNE 2016 C.V.O. CA’S NEWS & VIEWS

14

Clause Additional Reporting Points to be taken into consideration

(ii) Check whether, at any point of time during the year

in case of aforesaid transactions, the company has

exceeded the limit of sixty per cent of its paid-up

share capital, free reserves and securities premium

account or one hundred per cent of its free reserves

(as defined in section 2(43) of the Act and securities

premium account, whichever is more. If it exceeds

the limits specified above, whether prior approval by

means of a special resolution passed at a general

meeting has been obtained.

(iii) Check whether the company has made investments

through more than two layers of investment

companies.

(iv) Check whether the company has disclosed the full

particulars of the loan given, investment made or

guarantee given or security provided in the financial

statement including the purpose for which the same

is proposed to be utilized by the recipient

(v) Check whether the company has passed the board

resolution as prescribed and obtained the prior

approval, wherever required, from the public

financial institution concerned where any term

loan is subsisting.

(vi) Check whether rate of interest is not lower than the

prevailing yield of one year, three year, five year or

ten year government security closest to the tenor of

the loan granted.

(vii) Check if the company is in default in the repayment

of any deposits accepted or in payment of interest

thereon, then the company is not allowed to give any

loan or guarantee or any security or an acquisition

till such default is subsisting.

(viii) Check whether the company has maintained a

register (as per Form MBP-2) in the manner

as prescribed and also check the compliances of

other provisions and relevant rules.

z It may be noted that the aforesaid section is not

applicable in respect of loan made, guarantee given or

security provided by banking company or an insurance

company or a housing finance company in the ordinary

course of its business or a company engaged in the

business of financing of companies or of providing

infrastructural facilities. However, the restriction with

regard to the investment through more than two layers

of investment companies would be applicable for such

companies also. The auditor may ensure compliance

accordingly.

Love yourself first and everything else falls into line.You really have to love yourself to get anything done in this world

C.V.O. CA’S NEWS & VIEWS VOL. 19 NO. 12 / JUNE 2016

15

Clause Additional Reporting Points to be taken into consideration

Clause (xi) Whether managerial z Section 197 of the Act prescribes that the maximum

Managerial remuneration has been ceiling for payment of managerial remuneration by a

Remuneration paid or provided in public company to its directors, including managing

accordance with the director and whole-time director and its manager

requisite approvals which shall not exceed 11% of the net profit of the

mandated by the provisions company in that financial year, computed in

of section 197 read with accordance with section 198 of the Act, except that

Schedule V to the the remuneration of the directors shall not be

Companies Act ? If not, deducted from the gross profits.

state the amount involved

and steps taken by the z It may be noted that section 197 applies only to a

company for securing public company. Thereby, it is not applicable to a

refund of the same Private Company, and, accordingly, reporting under

this clause would not be required.

Clause (xii) Whether the Nidhi § It may be noted that Rule 5(1) of the Nidhi Rules, 2014

Nidhi Company* has complied prescribes the requirements for minimum number

Company with the Net Owned Funds of members, net owned fund etc.

to Deposits in the ratio of § As per this rule every Nidhi shall, within a period of

1: 20 to meet out the one year from the commencement of these rules,

liability and whether the ensure that it has—

Nidhi Company is (i) not less than two hundred members

maintaining ten per cent (ii) net owned funds of ten lakh rupees or more;

unencumbered term (iii) unencumbered term deposits of not less than ten

deposits as specified in per cent of the outstanding deposits as specified in

the Nidhi Rules, 2014 to Rule 14; and

meet out the liability (iv) ratio of net owned funds to deposits of not more

than 1:20.

Clause (xiii) Whether all transactions § The auditor should obtain written representations from

Related Party with the related parties management and, where appropriate, those charged

Transactions are in compliance with with governance that:

sections 177 and 188 (i) They have disclosed to the auditor the identity of

of the Act, where applicable the entity’s related parties and all the related party

and the details have been relationships and transactions of which they are

disclosed in the Financial aware; and

Statements etc., as required (ii) They have appropriately accounted for and disclosed

by the applicable such relationships and transactions in accordance

accounting standards with the requirements of the framework.

Clause (xiv) Whether the company has z It is not necessary to establish a one-to-one relationship

Preferential made any preferential with the amount of fund raised and its utilisation.

Allotment/ allotment or private z It may so happen that the funds raised during the year

Private placement of shares or fully might not have been applied for the stated purpose

Placement or partly convertible during the year, for example, the funds were raised at

debentures during the the fag-end of the year. In such a case, the auditor should

year under review and mention in his audit report that the funds raised during

if so, as to whether the the year has not been utilised. This also implies that the

requirement of section 42 of auditor, while making inquiry in respect of this clause,

the Act have been complied should also consider that the funds raised, which were

* Section 406(1) of the Act defines “Nidhi” to mean a company which has been incorporated as a Nidhi with the object of cultivating the habit of thrift and savingsamongst its members, receiving deposits from, and lending to, its members only, for their mutual benefit, and which complies with such rules as are prescribed bythe Central Government for regulation of such class of companies.

Success does not consist in never making mistakes but in never making the same one a second time.

VOL. 19 NO. 12 / JUNE 2016 C.V.O. CA’S NEWS & VIEWS

16

Clause Additional Reporting Points to be taken into consideration

with and the amount raised raised in the previous accounting period but have been

have been used for the actually utilised during the current accounting period.

purposes for which the

funds were raised. If not,

provide the details in

respect of the amount

involved and nature of

non-compliance

Clause (xv) Whether company has § Section 192 of the Act deals with restriction on certain

Non-cash entered into any non-cash noncash transactions involving directors or persons

transactions transactions with directors connected with them unless it meets the conditions laid

or persons connected with out in the said section.

him and if so, whether the § For reporting on the first leg of the reporting clause,

provisions of sec 192 of the starting point of the auditor’s procedures could be

the Act have been complied obtaining a management representation as to whether

the company has undertaken any non-cash transactions

with the directors or persons connected with the

directors, as envisaged in section 192(1) of the Act.

§ The auditor would need to corroborate the management

representation with sufficient appropriate

audit evidence.

Clause (xvi) Whether the Company is " The auditor is required to examine whether the company

NBFC required to be registered is engaged in the business which attract the

under section 45-IA* requirements of the registration.

of the Reserve Bank of " The registration is required where the financing activity

India (RBI) Act, 1934 and if is a principal business of the company.

so whether the registration " The auditor should report incorporating the following: -

is obtained (i) Whether the registration is required under section

45-IA of the RBI Act, 1934.

(ii) If so, whether it has obtained the registration.

(iii) If the registration not obtained, reasons thereof.

* Sec 45-IA of the RBI Act, 1934 states the requirement to obtain certificate of registration for carrying on the business of a Non-Banking Financial Company (NBFC).

A NBFC is a company registered under the Companies Act, its principal business being that of carrying on Financial activity.

Financial activity as principal business is when a company’s financial assets constitute more than 50 per cent of the total assets and income from financial assets constitutemore than 50 per cent of the gross income.

A company which fulfils both these criteria will need to be registered as NBFC by RBI.

Deleted Clauses

Inventory § Are the procedures of physical verification of inventory followed by the

Clause (ii)(b) & (ii)(c) management reasonable and adequate in relation to the size of the company

and the nature of its business? If not, the inadequacies in such procedures

should be reported

§ Whether the company is maintaining proper records of inventory and

whether any material discrepancies were noticed on physical verification

and if so, whether the same have been properly dealt with in the books of

account

Internal Control Is there an adequate internal control system commensurate with the size of

systemClause (iv) the company and the nature of its business, for the purchase of inventory

and fixed assets and for the sale of goods and services? Whether there is a

continuing failure to correct major weaknesses in internal control system.

I attribute my success to this: I never gave or took any excuse.

C.V.O. CA’S NEWS & VIEWS VOL. 19 NO. 12 / JUNE 2016

17

Statutory Dues Whether the amount required to be transferred to Investor education and

Clause (vi)(c) protection fund (IEPF) in accordance with the relevant provisions of the

Companies Act, 1956 and rules made thereunder has been transferred to

such fund within time.

Accumulated Losses Whether in case of a company which has been registered for a period not

Clause (viii) less than five years, its accumulated losses at the end of the financial

year are not less than 50% of its net worth and whether it has incurred

cash losses in such financial year and in the immediately preceding

financial year

Guarantee for loans taken Whether the company has given any guarantee for loans taken by others

Clause (x) from bank or financial institutions, the terms and conditions whereof are

prejudicial to the interest of the company

Reporting on Internal Financial Control System has now been made a regulatory mandate under the

Companies Act, 2013.Therefore, in order to avoid duplication, certain clauses of CARO requiring to

comment on the Internal Controls of a company have been removed. Moreover, the auditor is now excused

from the obligation to report on timely transfer of amounts to IEPF. However, the Companies (Audit and

Auditors) Rules, 2014 requires the auditor to report on anydelays in transferring the amounts to the said

fund in the Independent Auditor’s report.On one hand, the requirement to comment on whether the terms

and conditions of any guarantee for loans given by the company are prejudicial to its interest has been done

away with and on the other hand an additional responsibilityto report compliance with Sec 185 & 186 of

the Act has been added. Moreover, the compliance burden has reduced by deletion of the clause to comment

on Accumulated Losses

Modified Provisions

Clause Existing Provision Modified Provision Analysis

Clause (iii) Whether the company Whether the company z The limit of Rs.1 Lakh for overdue

Granting has granted any loans, has granted any loans, amount has been removed and

of Loans secured or unsecured secured or unsecured to instead any amount due for more

to companies, firms or companies, firms,Limited than 90 days needs to be

other parties covered Liability Partnerships or reported now.

in the register other parties covered in z Additionally, the auditor is now

maintained under the register maintained required to comment whether the

Sec 189 of the under Sec 189 of terms and conditions of the loans

Companies Act. If so, the Act granted to parties (including LLPs)

(b) If overdue amount (a) Whether the terms covered under Sec 189, are

is more than rupees and conditions of the prejudicial to the interests of the

one lakh, whether grant of such loans are company.

reasonable steps not prejudicial to the z Also the erstwhile provision did not

have been taken company's interest; mention to report the amount

by the company for (c) If the amount is overdue, however, now any amount

recovery of the overdue, state the total overdue more than 90 days needs

principal and interest amount overdue for to be stated and reported.

more thanninety days, z An amount is considered to be

and whether reasonable overdue when the payment has not

steps have been taken by been received on the due date as

the company for recovery per the lending arrangement.

of the principal and z This has enhanced the duty of the

interest. auditor by enhancing the reporting

requirement.

z It may so happen that a party

Follow effective actions with quiet reflection. From the quiet reflection will come even more effective action.

VOL. 19 NO. 12 / JUNE 2016 C.V.O. CA’S NEWS & VIEWS

18

Clause Existing Provision Modified Provision Analysis

listed in the register maintained

under section 189 of the Act might

have taken a loan from a company

and repaid it during the same

financial year. Therefore, while

examining the loans, the auditor

should also take into consideration

the loan transactions that have

been squared-up during the year

and report such transactions under

this clause.

Clause(viii) Whether the company Whether the company z Additional reporting requirement

Default in has defaulted in has defaulted in in case of default in loans and

repayment repayment of dues to repayment of loans or borrowings from Government also

of Loans a financial institution borrowing to a financial to be reported and in case of any

or bank or institution, bank, default in repayment, other than to

Debenture holders? Government or dues to debenture holders, the same needs

If yes, the period and debenture holders? If yes, to be reported lender wise.

amount of default to the period & the amount z Under this clause the auditor is

be reported; of default to be reported required to give lender wise details

(in case of defaults to in case of banks, financial

banks, financial institutions and Government only

institutions, and and not in respect of individual

Government, debenture holders

Lender wise detailsto be provided).

Clause(ix) Whether term loans Whether moneys raised by z The Auditors are now additionally

Applicationwere applied for the way of Initial Public Offer required to report regarding

of term purpose for which (IPO) or Further Public moneys raised by way of IPO or

loans/ the loans were Offer (FPO) (including FPO (including debt Instruments).

Public obtained debt instruments) and z Earlier this reporting requirement

Issue/ term loans were applied was limited only for the purpose of

Follow for the purposes for which term loans. Also, in case the

on offer those are raised. If not, moneys are not applied for the

the details together with specified purpose, the auditors now

delays or default and need to report on the details of

subsequent rectification, default or delay.

if any, as may be z This disclosure requirement was

applicable, be reported already covered for listed

companies under SEBI Regulation.

By making this applicable to

private and unlisted public

companies, a sphere of enhanced

compliance burden is created.

z The auditor should obtain a

representation from the

management as to the complete-

ness of the disclosure with regard

to the end-use of money raised as

well as actual end utilization of

money raised by IPO or FPO

(including debt instruments).

You have to learn the rules of the game. And then you have to play better than anyone else.

C.V.O. CA’S NEWS & VIEWS VOL. 19 NO. 12 / JUNE 2016

19

Clause Existing Provision Modified Provision Analysis

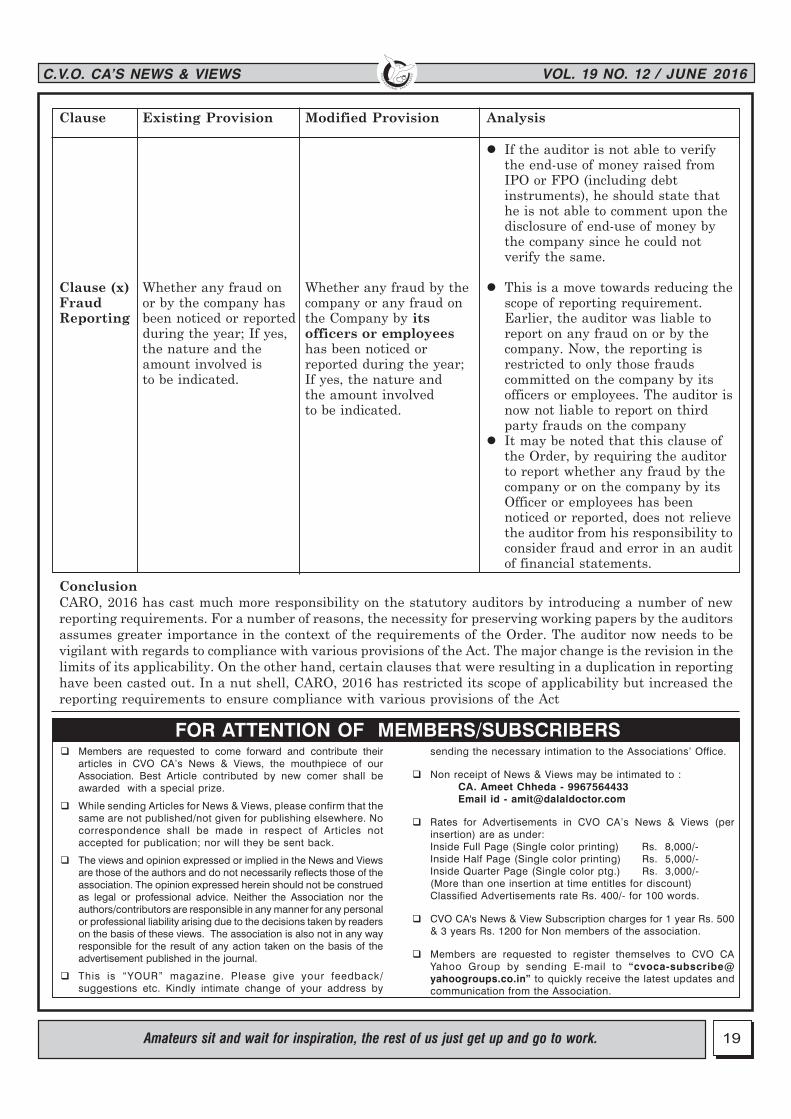

z If the auditor is not able to verify

the end-use of money raised from

IPO or FPO (including debt

instruments), he should state that

he is not able to comment upon the

disclosure of end-use of money by

the company since he could not

verify the same.

Clause (x) Whether any fraud on Whether any fraud by the z This is a move towards reducing the

Fraud or by the company has company or any fraud on scope of reporting requirement.

Reporting been noticed or reported the Company by its Earlier, the auditor was liable to

during the year; If yes, officers or employees report on any fraud on or by the

the nature and the has been noticed or company. Now, the reporting is

amount involved is reported during the year; restricted to only those frauds

to be indicated. If yes, the nature and committed on the company by its

the amount involved officers or employees. The auditor is

to be indicated. now not liable to report on third

party frauds on the company

z It may be noted that this clause of

the Order, by requiring the auditor

to report whether any fraud by the

company or on the company by its

Officer or employees has been

noticed or reported, does not relieve

the auditor from his responsibility to

consider fraud and error in an audit

of financial statements.

ConclusionCARO, 2016 has cast much more responsibility on the statutory auditors by introducing a number of new

reporting requirements. For a number of reasons, the necessity for preserving working papers by the auditors

assumes greater importance in the context of the requirements of the Order. The auditor now needs to be

vigilant with regards to compliance with various provisions of the Act. The major change is the revision in the

limits of its applicability. On the other hand, certain clauses that were resulting in a duplication in reporting

have been casted out. In a nut shell, CARO, 2016 has restricted its scope of applicability but increased the

reporting requirements to ensure compliance with various provisions of the Act

FOR ATTENTION OF MEMBERS/SUBSCRIBERS� Members are requested to come forward and contribute their

articles in CVO CA’s News & Views, the mouthpiece of ourAssociation. Best Article contributed by new comer shall beawarded with a special prize.

� While sending Articles for News & Views, please confirm that thesame are not published/not given for publishing elsewhere. Nocorrespondence shall be made in respect of Articles notaccepted for publication; nor will they be sent back.

� The views and opinion expressed or implied in the News and Viewsare those of the authors and do not necessarily reflects those of theassociation. The opinion expressed herein should not be construedas legal or professional advice. Neither the Association nor theauthors/contributors are responsible in any manner for any personalor professional liability arising due to the decisions taken by readerson the basis of these views. The association is also not in any wayresponsible for the result of any action taken on the basis of theadvertisement published in the journal.

� This is “YOUR” magazine. Please give your feedback/suggestions etc. Kindly intimate change of your address by

sending the necessary intimation to the Associations’ Office.

� Non receipt of News & Views may be intimated to :CA. Ameet Chheda - 9967564433Email id - [email protected]

� Rates for Advertisements in CVO CA’s News & Views (perinsertion) are as under:Inside Full Page (Single color printing) Rs. 8,000/-Inside Half Page (Single color printing) Rs. 5,000/-Inside Quarter Page (Single color ptg.) Rs. 3,000/-(More than one insertion at time entitles for discount)Classified Advertisements rate Rs. 400/- for 100 words.

� CVO CA's News & View Subscription charges for 1 year Rs. 500& 3 years Rs. 1200 for Non members of the association.

� Members are requested to register themselves to CVO CAYahoo Group by sending E-mail to “[email protected]” to quickly receive the latest updates andcommunication from the Association.

Amateurs sit and wait for inspiration, the rest of us just get up and go to work.

VOL. 19 NO. 12 / JUNE 2016 C.V.O. CA’S NEWS & VIEWS

20

LEVY OF SERVICE TAX ON THE SERVICES PROVIDEDBY GOVERNMENT OR A LOCAL AUTHORITY TO

BUSINESS ENTITIES RELATING TO REAL ESTATE/CONSTRUCTION INDUSTRY

Contributed by :CA Jinesh Gadaa member of the association

he can be reached [email protected]

Any service provided by Government or a local

authority to a business entity has been made taxable

w.e.f. 1st April 2016. Post Budget 2016,

representations have been received from several

quarters including business and industry

associations in respect of various aspects pertaining

to the taxation of such services. Accordingly, few

clarifications are issued vide circular No. 192/02/

2016-Service Tax dated 13th April 2016 issued by

Government of India, Ministry of Finance,

Department of Revenue (Tax Research Unit), F.No.

334/8/2016-TRU.

z Services provided by Government or alocal authority to another Government or alocal authority have been exempted vide

Notification No. 25/2012-ST dated 20-06-2012 as

amended by Notification No. 22/2016-ST dated

13-04-2016(Entry 54). However the said

exemption does not cover services specified in

sub-clauses (i), (ii) and (iii) of clause (a) of section

66D of the Finance Act, 1994, the same is

reproduced below:

Section 66 D Negative list of services:The negative list shall comprise of the followingservices, namely:—(a) services by Government or a local authority

excluding the following services to the extentthey are not covered elsewhere -

(i) services by the Department of Posts by wayof speed post, express parcel post, lifeinsurance and agency services provided to aperson other than Government;

(ii) services in relation to an aircraft or a vessel,inside or outside the precincts of a port or anairport; ;

(iii) *transport of goods or passengers; or* exempted for railways w.e.f.02.07.2012 to30.09-2012 vide Notification No 43/2012-ST dated 02.07.2012

z Service Tax on Taxes, cesses or duties are notconsideration for any particular service as suchand hence not leviable to Service Tax. Thesetaxes, cesses or duties include excise duty,customs duty, Service Tax, State VAT, CST,income tax, wealth tax, stamp duty, taxes onprofessions, trades, callings or employment,octroi, entertainment tax, luxury tax andproperty tax.

Service Tax on abovementioned Taxes, cesses or

duties including property tax is rightly

exempted as there is no element of service. By

specifying Property tax under exemption, the

same will act as a major relief to Real Estate/

Construction Industry as due to increase in

rates of Property tax, the said component is very

high in case of development/redevelopment/

reconstruction. Hence controversy to charge

service tax on property tax will not take place.

z Service Tax on fines and penalties :It is clarified that fines and penalty chargeable

by Government or a local authority imposed for

violation of a statute, bye-laws, rules or

regulations are not leviable to Service Tax.

Fines and liquidated damages payable to

Government or a local authority for non-

performance of contract entered into with

Government or local authority have been

exempted vide Notification No. 25/2012-ST

dated 20-06-2012 as amended by Notification

No. 22/2016-ST dated 13-04-2016 (Entry 57).

z Services provided in lieu of fee charged byGovernment or a local authority :It is clarified that any activity undertaken by

Government or a local authority against a

consideration constitutes a service and the

amount charged for performing such activities is

liable to Service Tax. It is immaterial whether

such activities are undertaken as a statutory or

mandatory requirement under the law and

irrespective of whether the amount charged for

such service is laid down in a statute or not. As

long as the payment is made (or fee charged) for

getting a service in return (i.e. as a quid pro quo

for the service received), it has to be regarded as

a consideration for that service and taxable

irrespective of by what name such payment is

called. It is also clarified that Service Tax isleviable on any payment (exceeding Rs.5,000) , in lieu of any permission or licensegranted by the Government or a localauthority.

Above clarification has created havoc in the Real

Estate/Construction Industry because many

permissions or licenses are required to complete

any Real State projects which is granted by the

Government or a local authority, and to acquire

Things may come to those who wait, but only the things left by those who hustle.

C.V.O. CA’S NEWS & VIEWS VOL. 19 NO. 12 / JUNE 2016

21

the same heavy official fees are to be paid to

them. As per above clarification the same will be

covered under service tax net on reverse charge

basis, hence from 01-04-2016 14.5% and from

01-06-2016 after introduction of 0.5% of Krishi

Kalyan Cess 15% service tax has to be paid by

business entities on reverse charge basis as a

result of which cost of Real Estate Developers

will increase tremendously and the said increase

of cost will indirectly be passed on the

consumers. As everybody is knowing that prices

in real estate industry have reached sky high,

now further addition to the same will increase

burden on the lacklustre demand. Buying a flat

for middle class people in Mumbai is like a

dream which will never be fulfilled.

Approval process for Real Estate Projects –Maharashtra (Mumbai) includes following:

a) Ownership Certificate/Extract

b) Building Layout Approval

c) Obtain Intimation of disapproval (IOD)(building permit) from the Building Proposal

office. Scrutiny fees is to be paid along with cost

for IOD varies depending upon whether

construction is of residence or commercial. The

Intimation of disapproval is issued with a list of

no-objection certificates which the applicant

must obtain separately from various

departments & government authorities.

d) Final Clearance to build “CommencementCertificate” (CC) will only be given once the

company obtains all NOCs and meet all IOD

conditions. There are about 40 IOD conditions to

be met by the builder to be eligible for applying

for commencement certificate (CC). Major

NOCs/ IOD conditions are listed below.

i) Non-Agriculture (NA) permission : Granted

by Revenue Department

ii) Obtain NOC from Tree Authority Committee

of Municipal Corporation.

The Tree Authority must ascertain what

trees (if any) will be cut down as a result of

construction. If trees are to be cut down, the

building company will have to plant trees to

replace them.

iii) Obtain NOC from storm water & Drain

Department (Municipal)

iv) Obtain NOC from Sewerage Department

(Municipal)

v) Obtain NOC from the Electric Department

(Municipal):

The electric consultant hired by the

developers works out load requirements,

transformer capacity etc., Load is

sanctioned by power requirements along

with a copy of application submitted for

building plan approval. BEST will assess

whether an electrical sub-station up-grade

is required at this stage.

vi) NOC from the traffic & Co-ordination

Department (Municipal)

vii) Obtain NOC from the Chief Fire Officer

(Municipal): In Mumbai buildings above 24

meters in height requires Chief Fire Officer

(CFO) clearance.

viii) Environment Clearance : The environment

consultant hired by the company prepares

the Environment Impact Assessment

Report which is submitted to the State level

expert Appraisal Committee which refers it

to the State Environment Impact

Assessment Authority (SEIAA).

Approving Authority: Ministry of

Environment/State Environment Impact

Assessment Authority (SEIAA)/ State level

expert Appraisal Committee

ix) NOC if near Coastal area: Approving

Authority: Coastal Zone Management

Authority. Construction is not allowed up to

500 meters from the coast line.

x) Permission for Excavation/ Royalty

payment

xi) Other common facilities Approval (Internal

Infrastructure services)

xi) Road Access Highway/Expressway:

Approving Authority NHAI/PWD

xii) Chief Escalator Installation Approval:

Approving Authority Public Works

Department.

xiii) Electrical substation NOC for all substation

transformers in building (Electric Service

Provider). Approving Authority: Electricity

Distributor Authority

ix) Ancient Monument Approval : Approving

Authority : Archaeological Survey of India

x) Consent to establish & operate: Ministry of

Environment has authorised Pollution

Control Board to monitor the environment

related compliances by the developer which

includes setting up of Sewage Treatment

Plant (STP) etc.

xi) NOC from Airport Authority of India :

Approving Authority : Civil Aviation

Department

e) Submit structural plans approved bystructural engineer to the BMC/Municipal.

The IOD is only an approval of the civil plans.

Spend eighty percent of your time focusing on the opportunities of tomorrow rather than the problems of yesterday

VOL. 19 NO. 12 / JUNE 2016 C.V.O. CA’S NEWS & VIEWS

22

Review of the structural plan is done in parallel

with the NOC process. No approval to this plan

is required from the Municipal Corporation but

copies are required to be submitted.

f) Obtain Occupancy Certificate (OC) fromthe BMC (Municipal)The OC allows the building company to occupy

the building but is not considered the final

document because the building company still

requires the certificate of completion. The

company’s architect must submit a formal letter

stating that construction has been completed

according to the standards set forth in the IOD &

CC.

g) Obtain Building completion certificatefrom the BMC (Municipal)The Building Completion Certificate is

considered to be the ultimate document that the

building company requires to fully occupy the

building and connect it to utilities like water,

power, sewerage connection etc.

Hence based on above one can conclude that

Builder/Developer/Contractor has to obtain n no.

of permissions/licenses granted by the

Government or a local authority. To obtain the

said permissions/licenses builder/developer/

contractor have to pay huge official money on

which now service tax will be applicable from 01-

04-2016 as a result of which now Builder/

Developer/Contractor have to shell out huge

amount of service tax i.e. at present 14.5% and

from 01-06-2016 15% on amount spent by them

for getting above permissions/licenses from

government or a local authority.

“Government” means the Departments of the

Central Government, a State Government and

its Departments and a union territory and its

departments but shall not be include any entity,

whether created by a statute or otherwise, the

accounts of which are not required to be kept in

accordance with article 150 of the Constitution

or the rules made their under

“Local Authority” means-

(a) a Panchayat as referred to in clause (d) of

article 243 of the Constitution;

(b) a Municipality as referred to in clause (e) of

article 243P of the Constitution;

(c) a Municipal Committee and a District

Board, legally entitled to, or entrusted by

the Government With, the control or

management of a municipal or local fund;

(d) a Cantonment Board as defined in section 3

of the Cantonments Act, 2006 (41 of 2006);

(e) a regional council or a district council

constituted under the Sixth Schedule to the

Constitution;

(f) a development board constituted under

article 371 of the Constitution; or

(g) a regional council constituted under article

371A of the Constitution;

M.C.G.M. is covered under local authority but

MHADA is not covered under local authority

definition but it can fall under government

authority which is not included in the said

circular no 192/02/2016-Service tax dated 13-04-

2016. Hence whether one can argue that all

payment in lieu of any permission or license

granted by BMC is not exempt but MHADA is

exempt.

However, Ministry of Finance vide its

notification no. 02/2014 dated 30.01.2014

widened the scope of the definition of the

Governmental Authority. The earlier definition

as provided under the mega Exemption

Notification dated 20.06.2012 was substituted

with the following:

‘(s) “governmental authority” means an

authority or a board or any other body;

i. set up by an Act of Parliament or a State

Legislature; or

ii. established by Government,

with 90% or more participation by way of