d i n c nigeria ndic annual report and …ndic.gov.ng/files/links/part two.pdf · 2015-02-11 ·...

TRANSCRIPT

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

123

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

SECTION 11THE OPERATING ENVIRONMENTTHE OPERATING ENVIRONMENT

11.1 Introduction

11.2 The Monetary Policy Environment

The environment in which insured deposit-taking financial institutions operated in 2011

was greatly influenced by developments in the domestic and international economies.

These developments, to a large extent, shaped the direction of monetary and fiscal

policies in the country during the year under review. The contractionary monetary

policy, the banking reforms and the slow recovery from the global financial crisis

continued to affect the operations of the banking system during the year under review.

The purchase of non-performing loans of banks by Asset Management Corporation of

Nigeria (AMCON) and subsequent injection of fresh capital into some of the banks led

to improvement in asset quality, liquidity and capitalization of banks. The shareholders'

funds of the banking industry increased by 696.18% from N312.36 billion in 2010 to

N2,486.95 billion in 2011. However, the slow recovery of the capital market continued as

the all-share index further depreciated from its opening figure of 24,770.52 at the

beginning of the year to about 20,763.26 at the end of the year.

The Central Bank of Nigeria (CBN) in its efforts to control money supply and bring down

inflation increased the Monetary Policy Rate (MPR) six times from 6.25% to 12% between

January and December 2011. Similarly, the cash reserve ratio (CRR) and liquidity ratio

were also increased. The reason for the increase of the MPR and other monetary policy

instruments was due to the monetary authorities' commitment to achieving the

objectives of a single digit inflation regime, positive real interest rates, and ensuring

exchange rate stability. It therefore, became imperative for the CBN to embark on tight

monetary policy stance in order to neutralize the effect of increased government

expenditure in the face of dwindling external reserves.

Presented in this section is a review of the operating environment for insured financial

institutions in 2011. The environment was impacted by regulatory, macroeconomic as

well as socio-political events during the year under review.

The objectives of monetary policy in 2011 remained the attainment of internal and

external balances in the form of maintenance of price and exchange rate stability as

well as ensuring an efficient payment system. The CBN adopted various policy

measures aimed at containing growth of monetary aggregates in order to achieve

monetary and price stability. Particular attention was paid to the need to curtail the

inflationary tendencies and specifically ensure that inflation rate was maintained

within the single digit limit. To achieve the aforementioned objectives, the major

monetary policy measures in 2011 included the following:

(a) Liquidity management measures

(b) Interest rate policy

(c) Exchange rate policy

11.3 Regulatory Developments in 2011

(a) Revised Microfinance Policy Regulatory and Supervisory Framework for Nigeria

(b) Granting of New Licences to DMBs

In order to contain the growth of monetary aggregates in the year under review, the

CBN increased the liquidity ratio from 25% to 30% while the Cash Reserve Ratio (CRR)

was increased from 1% to 8% between January and December 2011.

The MPR, being the anchor rate around which all other interest rates revolved, was

increased six times during the year from 6.25% to 12% to curtail inflationary pressures.

The upward reviews of the MPR became imperative given the increased government

spending in 2011, being an election year.

A major development in the foreign exchange market in 2011 was the depreciation of

the Naira by adjusting the target official exchange rate from N150.00/ US $1.00 to

N155.00/ US $1.00 at the WDAS. That, in addition to other measures taken by the CBN to

enhance the efficiency of the foreign exchange market, was in response to pressures

on the Naira especially due to the fall in oil prices and declining external reserves.

During the year under review, various circulars/guidelines were issued by the CBN in

order to guide the operations of insured DMBs and other deposit-taking financial

institutions. The circulars/guidelines included the following:

The revised microfinance policy provided among other things three categories of

microfinance banks (MFB) and stipulated minimum capital requirements for each

category as stated below:

1. Category 1: Unit Microfinance banks - These are MFBs authorised to operate in

one location and with a minimum paid-up capital of N20 million. They are

prohibited from opening branches/cash centres.

2. Category 2: State Microfinance Banks - These are MFBs authorised to operate

within one state or the Federal Capital Territory (FCT), and with a minimum paid-

up capital of N100 million and would be allowed to open branches/cash

centres within the same state, subject to prior approval of the CBN.

3. Category 3: National Microfinance Banks - These are MFBs authorised to

operate in more than one state, including the FCT with a minimum paid-up

capital of N2 billion and would be allowed to have branches in any part of the

country, subject to prior approval of the CBN.

In compliance with its circular BSD/DIR/GEN/UBM/03/025 on the review of Universal

Banks, the CBN during the year under review granted international banking licences to

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

124

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

9 banks, national banking licences to 10 banks and a regional banking licence to one

bank. In addition to this, 4 banks, namely: First Bank Plc, FCMB Plc, UBA Plc and Stanbic

IBTC Plc were permitted to operate as holding companies.

The banks that were granted international banking licences and which were expected

to operate with a minimum regulatory capital of N50 billion were Access Bank Plc,

Diamond Bank Plc, Fidelity Bank Plc, First Bank Plc, First City Monument Bank (FCMB) Plc,

Guaranty Trust Bank Plc, Skye Bank Plc, Zenith Bank Plc and United Bank for Africa Plc.

Those that were granted national banking licences and whose minimum regulatory

capital would be N25 billion were Citibank Ltd, Ecobank Plc, Stanbic IBTC Plc, Standard

Chartered Ltd, Sterling Bank Plc, Unity Bank Plc, Union Bank Plc, Keystone Bank Ltd,

Mainstreet Bank Ltd, and Enterprise Bank Ltd. The regional banking licence whose

regulatory capital would be N10 billion was granted to Wema Bank Plc.

Also banking licence was granted to Jaiz Bank Plc to operate as a national non-interest

banking institution with a regulatory capital of N10 billion.

The CBN, during the year under review, introduced a policy aimed at addressing the

inherent challenges of cash-based economy. The cashless (or cash-lite) policy was

introduced to:

i) Encourage the development of an efficient payment system which w i l l b e

nationally used actively, and recognised internationally;

ii) Enhance the role of the CBN in monetary policy, financial stability and overall

economic activity;

iii) Eliminate the delays in clearing time of cheques, infrastructural bottlenecks,

sharp practices and insider abuses which characterise operations in cash-based

economies, thereby boosting economic development and reducing financial

risks;

iv) Encourage the use of e-payment as an alternative method and therefore cut

operating costs of handling cash, which eats into banks' profits and liquidity;

v) Address the problem of corruption and money laundering;

vi) Facilitate financial inclusion in the country; and

vii) Facilitate the achievement of the vision 20:2020.

The introduction of the policy was expected to demonstrate that the electronic

channels and products were secure, convenient, fast and reliable and would not have

the short comings of cash-based transactions such as bulkiness, slow transaction speed,

revenue leakages, high cost of handling cash and risk of carrying cash.

In order to facilitate the implementation of the policy, the CBN in collaboration with the

Bankers Committee, placed limits on free cash withdrawals and lodgments by

(c) Introduction of Cashless (Cash-lite) Policy

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

125

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

individuals and corporate organizations. Under the policy, a daily cumulative limit of

N150, 000 and N1,000,000 on free cash withdrawals and lodgments by individual and

corporate customers respectively, with DMBs would be imposed with effect from June

1, 2012. Individuals and corporate organizations making cash transactions above the

limits would be charged a penal fee of N100/ thousand and N200/ thousand,

respectively for amounts above the limits.

In addition to the above, third party cheques above N150, 000 would not be eligible for

encashment over the counter. Value for such cheques would be received through the

clearing house. According to the policy, any DMB that did not comply with the law on

the encashment of 3rd party cheques would be liable to a sanction of 10% of the face

value of the cheque or N100, 000 whichever was higher.

Another notable point in the policy was that banks would from that day discontinue

cash in transit lodgment services rendered to merchant- customers. Customers would

be expected to engage the services of the CBN licensed cash-in-transit (CIT) firms to

aid cash movement to and from their banks at mutually agreed terms and conditions.

Contraventions of the policy would attract a fine of N1.0 million per specie movement.

The CBN, during the year under review, granted Jaiz Bank Plc operating licence to

operate as a non-interest bank. StanbicIBTC Bank was also granted approval to

operate a non-interest banking window.

It is instructive to note that a non-interest bank is a bank which transacts banking

business, engages in trading, investment and commercial activities as well as the

provision of financial products and services in accordance with any established non-

interest banking principles.

Non-interest banking and finance models are broadly categorized into two:

1. Non-interest banking and finance based on Islamic commercial jurisprudence.

2. Non-interest banking and finance based on any other established non-interest

principle.

Following the licence to Jaiz Bank and approval to Stanbic IBTC to operate non-interest

banking, the NDIC further fine-tuned its framework for extending deposit insurance

cover to non-interest deposit-taking financial institutions. That was with a view to

creating a level playing field for all operators and engender confidence in the new

banking model.

(d) Granting of approval in principle to Jaiz Bank to operate a Non-Interest Bank

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

126

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

(e) Recapitalisation of the Intervened Banks

BANK CAPITAL INJECTED BOND FACE VALUE

A lot of efforts were put in place to ensure the recapitalization of the intervened banks

in order to meet the September 30, 2011 deadline set by the CBN. It would be recalled

that while Unity Bank Plc was able to meet its capital requirement through Rights Issue,

Wema Bank Plc became fully capitalized through Special Placements.

To ensure the recapitalization of the remaining eight intervened banks before the

deadline, merger arrangements were concluded between Equitorial Trust Bank and

Sterling Bank, Finbank and First City Monument Bank, Intercontinental Bank and Access

Bank and Ecobank and Oceanic Bank. Union Bank was recapitalized by its

shareholders and a core investor, Union Global Partners Ltd (UGPL).

Meanwhile, the financial condition of the other three intervened banks, namely:

Afribank, Springbank, and BankPHB continued to deteriorate while the former owners of

the banks made no effort to recapitalize them on or before the set deadline. Given that

situation and in the interest of depositors and the banking system, the NDIC on August 5,

2011, pursuant to the provisions of Section 39 of the NDIC Act No. 16 of 2006, and after

due consultation with the CBN and the Federal Ministry of Finance, established three

bridge banks for subsequent transfer of assets and liabilities of Afribank Plc, BankPHB Plc,

and Spring Bank Plc. The three bridge banks and the failed banks whose assets were

taken over and liabilities assumed by the bridge banks are listed as follows:

Bridge Bank Bank with Revoked Licence

Mainstreet Bank Limited - Afribank (Nigeria) Plc

Keystone Bank Limited - BankPHB Plc

Enterprise Bank Limited - Spring Bank Plc

The CBN, thereafter, revoked the operating licences of the three banks (i.e. Afribank

(Nigeria) Plc, BankPHB Plc and Spring Bank Plc) on August 5, 2011.

The three bridge banks were subsequently acquired by AMCON by purchase and

assumption transaction. Following the acquisition, AMCON injected fresh capital

through share subscription into the banks to recapitalize them. That brought the

shareholders' fund to positive position and shored up each bank's Capital Adequacy

ratio to 15%. The breakdown of Capital inflow and relative Consideration Bond issued by

AMCON to the banks are detailed in the table below:

₦'Million ₦'Million

MAINSTREET BANK LTD 318,631 433,132

KEYSTONE BANK LIMITED 296,898 403,590

ENTERPRISE BANK LIMITED 121,417 165,049

736,946 1,001,771

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

127

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

With the foregoing development, the number of DMBs fell from 24 to 20 by the end of

December 2011.

A new policy aimed at reforming mortgage/housing finance sector was approved in

November 2011. The policy provided, among other things, two categories of PMBs and

stipulated minimum capital requirements for each category as stated below:

Category 1: State PMBs would be allowed to operate within a state with a minimum

paid-up capital of N2.5 billion.

Category 2: National PMBs would be allowed to operates in all parts of the country with

a minimum paid-up capital of N5 billion.

The policy also provided for the development of uniform underwriting standard for

mortgage loan origination and the establishment of a mortgage refinance/liquidity

company.

The performance of the global financial markets was sluggish during the year under

review. International economic and financial conditions deteriorated as there were no

serious signs of recovery during the year. Most of the advanced economies of America

and Europe remained economically weak as the recession that started earlier in 2010

continued in 2011. Global output growth deteriorated from 5.2% in 2010 to 3.8% in 2011.

The Euro-Zone debt crisis worsened leading to their sovereign credit ratings

downgrades, change of governments and implementation of austerity measures in

seriously affected countries within the zone. As a result, unemployment and inflation

rates remained high leading to large unsustainable fiscal imbalance and low demand.

The development had a direct negative impact on the global financial system stability

and international trade in 2011.

The impact of the weak and sluggish growth of the advanced economies was

relatively contained with minimal negative effects on the Nigerian economy. That was

due to government's commitment to the implementation of the economic

transformation programme aimed at sustaining a favourable macro-economic

performance. Investors' confidence in the economy remained stable during the year

as the sovereign credit rating was within acceptable level which impacted positively

on output. The real GDP growth rate however dropped marginally to 7.36% in 2011 as

against 7.98% in 2010. Although, the growth rate was impressive, rising poverty and

unemployment remained of serious concern during the year under review.

The moderate inflationary pressure witnessed in 2010 continued into 2011 as

government's pursuit of achieving a single digit inflation rate was not realized. Apart

(f) Reform of Primary Mortgage Banks (PMBs)

11.4 The Macro-economic Environment

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

128

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

from the months of August and September when a single digit of 9.4% and 9.3%

respectively, was achieved, all the other months recorded a double digit inflation

figure. For example, inflation rose from 12.1% in January to 12.8% in March before

declining to 10.2%, 10.3% and 10.3% in June, September and December 2011

respectively. The year-on-year headline inflation rate stood at 10.8% in December 2011

compared with 11.8% in December 2010. Similarly, food inflation declined from 12.2% in

January to 11.0% in December and was lower than its level in the preceding 3 years.

Core inflation declined marginally from 12.1% in January to 11.6% and 10.8% in

September and December 2011 respectively. It was 10.9% in December 2010.

The Country's crude oil output increased in 2011 averaging 2.39 million barrels per day

(mbpd) compared to 2.23 million barrels per day recorded in 2010. The higher crude oil

production was facilitated by the relative success of the Federal Government's

Amnesty Programme implementation initiated in 2009 which brought relative peace to

the Niger Delta region. In line with government's commitment to a tighter fiscal stance,

the benchmark price of oil was reduced from US $ 75.0 to US $ 70 per barrel in the third

quarter of the year. However, the average spot price of Nigeria's reference crude, the

Bonny Light, at the International market rose from US $97.96 to US $113.12 in October

2011. The increases in both output and price of oil were expected to boost government

revenue.

The performance of the non-oil activities was satisfactory in 2011. Agriculture and the

Service sectors as well as the recovery in crude oil output recorded significant

improvements especially in the fourth quarter of 2011.

The average exchange rate of the Naira depreciated in all the three segments of the

market. At the WDAS market, the exchange rate opened at N151.62/US $1.00 in

January 2011 but moved up to N154.45/US$ in June 2011 and further to N158.21/US $ in

December 2011. The depreciation of the exchange rate was due to the high demand

for foreign exchange in the market resulting from the import-dependent nature of the

economy compounded by the activities of speculators.

The external reserve position as at end of December 2011 stood at US$ 32.64 billion

compared to US$ 32.34 billion recorded in 2010, indicating a slight increase of US$ 0.30

billion over the 2010 figure. At the 2011 position, the external reserve level could finance

more than six months of imports thus exceeding the six months of import required by the

West African Monetary Zone (WAMZ) arrangement.

The AMCON which commenced operation in 2010, was very visible in the Nigerian

financial system in 2011 as it acquired three DMBs that were established to take over the

assets and assume the liabilities of the failing intervened banks.

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

6

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

129

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

Other activities that AMCON carried out during the year under review included the

completion of the purchase of Eligible Bank Asset, (EBA) from the participating twenty

banks; an addition to second tranches bought in December 2010 and April

respectively. Total EBA's valued at N807.9 billion was purchased from the eligible

financial institutions at a discounted value of N481.9 billion under the latest acquisition.

The AMCON issued 'Series V' Bond face value of N689.2 billion as consideration for the

EBAs purchased. Also, Bond face value of N77 billion (discounted value of N54 billion)

was issued by AMCON as Financial Accommodation to Union Bank of Nigeria. That was

subject to eventual acquisition by the core investor, Union Global Partners Ltd (UGPL)

at agreed terms.

Aggregate domestic credit (net) to the economy in 2011 grew by about 24.57% over

the December 2010 level. Credit to the private sector grew by 24.24% which was higher

than the target growth rate of 23.34% for 2011. However, credit to the Federal

Government stood at 21.65% against the 29.29% target for 2011 due to government's

prudent fiscal operations.

Activities at the money market showed an upward movement in market rates during

the year under review. The average open-buy-back (OBB) rate increased to 15.50% in

December 2011 from 6.22% in January. Similarly, average call rates rose to 14.09% in

December from 6.42% in January 2011. Both lending and deposit rates of deposit

money banks also moved up during the year under review. The maximum lending rate

increased to 23.21% in December from 21.75% in January 2011. The spread between

maximum lending rate and average deposit rate was 20.12% points in December from

19.22% in June.

The Nigerian capital market experienced a decline in its activities during the period

under review. The all-share index (ASI) decreased by 16.18% from 24,770.52 in

December 2010 to 20,763.26 in December, 2011. Similarly, market capitalization also

declined by 19.2% from N6.39 trillion over the same period due partly to the delisting of

the acquired banks and sluggish recovery of the market.

The socio-political scene witnessed a lot of activities during the year under review.

Nigeria conducted the fourth democratic presidential election that ushered in Dr.

Goodluck Ebele Jonathan, (GCFR) and Architect Namadi Sambo as President and

Vice President of the Federal Republic of Nigeria respectively. Also, the fight against

corruption by Economic and Financial Crimes Commission (EFCC) continued under

the new leadership of Mr. Ibrahim Lamorde who replaced Mrs. Farida Waziri. Similar

institutions such as the Independent Corrupt Practices and other Related Offences

Commission (ICPC) and the Code of Conduct Bureau also intensified their fight against

corruption.

11.5 Socio-Political Environment

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

130

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

However, the year witnessed several cases of unrest, bombings and ethno-religious

challenges in various parts of the country. The Federal Government was nevertheless

on top of the situation in its efforts to find a lasting solution through dialogue, economic

measures, enhanced intelligence and other security measures in order to ensure

peace and security of lives and properties and provide a conducive environment for

investment.

Although, the poor state of the nation's infrastructure witnessed a slight improvement in

road and electricity, a lot still needed to be done to improve on the cost of doing

business. The Federal Government continued with the reforms of the power and oil and

gas sectors for improved performance, increased revenue generation and addressing

the issue of corruption in the industry. Data from the National Bureau of Statistics

showed a rise in the unemployment rate to 23.9% in 2011 from 21.4% in 2010. It was

expected that the trend would be reversed by the various job-creation initiatives of the

Federal and State Governments as well as the private sector.

The nation's banking industry witnessed improvement especially in the areas of capital

adequacy and asset quality during the year under review. That development was

largely attributable to the activities of the AMCON through the purchase of non-

performing loans within the industry and the recapitalization of the three acquired

banks.

The efforts towards financial inclusion were heightened in 2011 with the review of the

microfinance policy which aimed at improving the capital base of the microfinance

banks, thereby equipping them to perform their functions better. Also, the

commencement of non-interest banking was expected to bring more depositors on

board as potential depositors who were averse to the interest-bearing products could

now be serviced.

Presented in Table 10.1 are key macro-economic indicators as well as some specific

indicators for the banking industry. The table shows that the total assets for the industry

(inclusive of OBS) recorded an increase of 17.31% from N18.66 trillion in December 2010

to N21.89 trillion in December 2011. The total deposits within the banking industry also

grew by 13.78% from N10.84 trillion in 2010 to N12.33 trillion in 2011. The tight monetary

stance of the CBN took its toll on total loans and leases as the table shows that this item

recorded a marginal increase of 2.04% from N7.17 trillion in 2010 to N7.31 trillion in 2011.

11.6 Review of Banking Industry Performance

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

131

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

Macroeconomic Indicators 2005 2006 2007 2008 2009 2010 2011

GDP (₦’ Trillion at Current Market Prices)

14.57 18.22 22.91 23.84 25.49 29.50 36.53

No.

of Banks

25

25

24

24

24 24 20

Inflation (%)

11.9

8.5

6.6

15.1

12.0 11.8 10.8

Total Deposits

of Banks (N’

Trillion)

2.47

3.41

5.36

8.70

9.99 10.84 12.33

Ratio of Total Bank Deposits

to GDP (%)

16.9

18.9

23.29

33.34

39.19 36.74 33.75

Total Assets

of Banks -

inclusive of

Off-Balance Sheet

Engagement ( OBS) ( N’

Trillion)

5.46

8.14

13.01

19.26

17.52 18.66 21.89

Ratio of Total Assets of Banks

to GDP (%)

37.5 44.7 56.8 66.6 68.7 63.26 59.92

Total Loans and Leases of

Banks (N’ Trillion)

1.83 2.84 4.68 7.41 8.91 7.17 7.31

TABLE 10.1

KEY MACROECONOMIC INDICATORS

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

132

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

SECTION 12

FINANCIAL CONDITIONS OF INSURED DEPOSIT

MONEY BANKS IN 2011

FINANCIAL CONDITIONS OF INSURED DEPOSIT

MONEY BANKS IN 2011

12.0 Introduction

12.1 Capital Adequacy

In 2011, the banking industry recorded significant improvement in the financial

condition and performance of DMBs as revealed by all financial indicators compared

to the previous year's position. One of the major factors that accounted for the

improved performance was the adoption of Mergers and Acquisition (M&A) Strategy

by some banks. The banks that were involved in the M&A were Access Bank Plc, First

City Monument Bank Plc, Ecobank Transnational Incorporated and Sterling Bank Plc

which acquired Intercontinental Bank Plc, Finbank Plc, Oceanic Bank Plc and Equitorial

Trust Bank Limited. Consequently, the number of DMBs reduced from 24 to 20 during the

year.

The banking industry's total assets grew by 17.27%, capital adequacy ratio increased

from 4.06% to 17.71%, asset quality ratio significantly improved as the non-performing

loans to total loans ratio declined from 15.04% to 5.82% due to the purchase of non-

performing loans by the AMCON. Also the average liquidity ratio for the industry rose to

65.69% in 2011 from 51.77% in December 2010.

The banking industry capital position was strong during the year under review. While the

equity capital decreased by about 11.81% from ₦249.71 billion in December 2010 to

₦220.21 billion in 2011, the reserves increased substantially to ₦2,266 billion in 2011 from

₦179.89 billion in 2010. The adjusted shareholders' funds increased to ₦1.93 trillion in

2011 from ₦312.36 billion in 2010. Consequently, the capital adequacy ratio (CAR) of

the DMBs improved from 4.06% in December 2010 to 17.71% in December 2011. It is

noteworthy, that the improvement in the banking industry capital adequacy was

primarily due to the purchase of non-performing loans by AMCON. However, two (2)

DMBs had their capital adequacy ratio below the prudential requirement of 10%. The

average capital adequacy ratio of the two under-capitalized banks was negative

8.31%. Table 12.1 shows some statistics on DMBs capital adequacy as at 31st

December, 2011 with comparative figures as at December 2010

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

133

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

134

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

* Revised Source: Bank Returns

Capital Adequacy Indicators Year

2010* 2011

Total Qualifying Capital (N’ billion) 424.46 1,900.31

Adjusted Shareholders’ Funds (N’ billion) 312.36 1,934.93

Capital to Total Risk Weighted Asset Ratio (%)

4.06 17.71

Number of Banks 24 20

12.2 Asset Quality

The Asset Quality of the banking industry significantly improved during the period under

review. Table 12.2 shows the quality of assets of the industry as at 31st December 2011

relative to December 2010. The performance of asset quality for the period is further

illustrated in charts 12A and 12B.

The industry total loans stood at ₦7.31 trillion in 2011, an increase of 2.04% over the 7.16

trillion reported in 2010. The industry's volume of non-performing loans significantly

decreased by ₦651.70 billion or 60.47% from ₦1.08 trillion in December 2010 to ₦425.96

billion in December 2011. The average non-performing loans to total loan ratio

decreased from 15.04% in December 2010 to 5.82% in December 2011, signifying

improvement in the quality of assets of the banks.

₦

Item

Year

2010*

2011

Total Loans (N, billion)

7, 166.76

7,312.72

Non Performing Loans (N, billion)

1, 077.66

425.96

Ratio of Non Performing Loans to Total Loans (%)

15.04

5.82

Ratio of Non Performing Loans to Shareholder's Funds (%)

250.85

17.13

* Revised Source: Bank Returns

TABLE 12.2

ASSET QUALITY OF INSURED BANKS

TABLE 12.1

INSURED BANKS CAPITAL ADEQUACY

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

135

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

CHART 12A

PROPORTION OF NON PERFORMING LOANS TO TOTAL LOANS

0

2

4

6

8

10

12

14

16

18

20

2010 2011

Adjusted Shareholders’ Funds Non PerformingLoans

0

10

20

30

40

50

60

70

80

2010 2011

Total Loans

CHART 12B

RATIO OF NON PERFORMING LOANS TO SHAREHOLDERS' FUNDS

Top seven (7) DMBs in the banking industry in December 2011 accounted for 68.22% of

total loans as shown in chart 12C.

CHART 12C

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

136

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

12.3 Earnings and Profitability

Total operating income of the industry stood at ₦2.33 trillion in 2011, representing an

increase of 7.90% over the ₦2.16 trillion reported in 2010. Similarly, Total Operating

Expenses increased from ₦932.53 billion in December 2010 to ₦1.79 trillion in December

2011. Consequently, the industry recorded a loss of ₦6.71 billion in December 2011 as

against a profit of ₦607.34 billion recorded in December 2010. A total of nine (9) banks

reported losses at the end of 2011 which resulted in the negative Return on Assets (ROA)

as well as Return on Equity (ROE) and adversely affected the industry performance

during the period under review. The Yield on Earning Assets also dropped to 10.05% as

at December, 2011 from 11.24% as at December 2010. Table 12.3 shows selected

financial indicators of earnings and profitability as at 31st December, 2011.

*Revised

Source: Bank Returns

Indicators

Year

2010*

2011

Profit Before Tax (N, billion)

607.34

-6.71

Net Interest income (N, billion)

824.62

817.14

Non Interest income(N, billion)

462.76

845.65

Interest Expenses (N, billion)

616.31

544.21

Operating Expenses (N, billion)

932.53

1,788.37

Yield on Earning Assets (%)

11.24

10.05

Return on Equity (%) 162.98 (0.28)

Return on Assets (%) 3.91 (0.04)

TABLE 12.3

EARNINGS AND PROFITABILITY INDICATORS

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

137

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

Items

Year

2010* 2011

Average Liquidity Ratio 51.77 65.69

Loans and Advances to Deposit Ratio

59.23

55.95

No of Banks with Less than the 30% minimum Liquidity ratio 1 Nil

TABLE 12.4

LIQUIDITY RATIO OF INSURED BANKS AS AT DECEMEBR 2010

The maturity profile of the industry's assets and liabilities showed a cumulative

mismatch. The mismatch was recorded for all the maturity bands except those

maturing after 365 days. That implied that short-term funds were used to fund long term

investments. Out of total deposits of ₦12.33 trillion, the sum of ₦9.48 trillion or 76.86%

would mature in 30days, ₦1.52 trillion or 12.37% had maturity of between 31 to 90 days

while the remaining ₦1.33 trillion or 10.79% would mature after 91 days. The charts 12D

and 12E illustrate the maturity structure of loans and deposit liabilities as at 31st

December, 2011.

* Revised

Source: Bank Returns

12.4 Liquidity and Funds Management

The banking industry liquidity position was strong in 2011 as the average liquidity ratio

rose from 51.77% in December 2010 to 65.69% in December 2011. All the DMBs met the

minimum liquidity ratio requirement of 30% as at the end of December 2011. Table 12.4

presents the liquidity position of the DMBs for 2010 and 2011.

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

138

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

CHART 12 E

12.5 Sectoral Allocation Of Credit

A review of the Industry Credit Portfolio showed that the eight (8) priority sectors

accounted for 83.53% while other sectors represented 16.47% of the total credits

extended by the DMBs in 2011 as shown in Table 12.5 and the charts 12F and 12G.

CHART 12 D

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

139

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

CHART 12F

DEC 2011 DEC 2010

DETAILS % N'BILLION %

OIL AND GAS

1,529.84

21.03

1,304.34

18.20

MANUFACTURING

1,108.64

15.24

967.10

13.49

GENERAL

854.10

11.74

926.42

12.93

GENERAL COMMERCE

809.20

11.12

710.49

9.91

INFORMATION AND

COMMUNICATION

628.14

8.64

608.43

8.49

GOVERNMENTS

542.93

7.46

439.05

6.13

REAL ESTATE ACTIVITIES

377.33

5.19

481.11

6.71

AGRIC., FORESTRY & FISHINGS 226.13 3.11 154.02 2.15

OTHERS 1,197.44 16.47 1,575.82 21.99

TOTAL 7,273.75 100 7,166.78 100

TABLE 12.5

SECTORAL DISTRIBUTION OF CREDITS OF DMBs IN 2011

N'BILLION

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

140

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

CHART 12G

12.6 Level of Soundness of the DMBs In 2011

The DMBs are usually categorized into five levels of soundness, namely: A-Very Sound;

B-Sound; C-Satisfactory; D-Marginal, and E-Unsound. The Banking Industry

performance and level of soundness during the year ended 31st December, 2011

indicated that five (5) banks were in Category B, thirteen (13) banks in Category C and

two (2) banks were in Category D. There were no banks in Categories A & E as at 31st

December, 2011. The combined Total Assets of the two (2) banks in Category D stood

at ₦560.02 billion or 3.07% of the Industry Total Assets.

SECTION 13BALANCE SHEET STRUCTURE OF DEPOSIT MONEY BANKS IN 2011BALANCE SHEET STRUCTURE OF DEPOSIT MONEY BANKS IN 2011

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

141

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

13.0 Introduction

13.1 Insured Banks' Structure of Assets

The structure of a bank's balance sheet, which is a statement of its assets and liabilities,

reflects the riskiness of its business. It also provides the regulatory authorities a guide as

to which supervisory efforts are necessary to track the health of a bank while providing

the discerning public the information required to take informed decisions in relation to

the bank.

Banks' balance sheet structure in 2011 reflected the volatility in interest rates arising from

increases in the Monetary Policy Rates (MPR). The increases in the MPR from 6.5% to 12%

between January and December 2011, led to increases in lending and other rates.

Consequently, short term investments became more attractive than long term

investments and that led to an increase in short term investments and a reduction in

long term investments.

On the liabilities side of the balance sheet, the impact of the activities of the AMCON

was felt as the purchase of non-performing loans from banks reduced the level of

provisioning they needed to make thereby improving their reserves and by extension

the shareholders' fund. The shareholders' fund was further boosted by the injection of

funds in the three banks acquired by AMCON in August 2011.

This section presents the balance sheet structure of insured DMBs in 2011 compared to

the position in 2010 with particular reference to changes in the structure of assets and

liabilities, shareholders' funds and ownership structure as well as insured banks' deposit

liabilities.

The structure of assets of insured banks (inclusive of Off-Balance Sheet Engagements) is

as presented in Table 13.1. As shown in the table, total assets increased by 17.31

percent from ₦18.66 trillion in 2010 to ₦21.89 trillion in 2011. A cursory look at the structure

of the banks' assets shows that there was a reduction in the proportion of loans and long

term investments in 2011 than in 2010.

As a proportion of Total Assets, most of the asset categories decreased except Cash

and Due from Other Banks as well as short term investments. Cash and Due from Other

Banks comprising vault cash, balances with CBN and balances held with other banks

increased from 10.70% in 2010 to 14.21% in 2011. Also, total short term investments

increased from 6.09% in 2010 to 17.11% in 2011. There was however, no change in the

proportion of Off Balance Sheet Engagements to Total Assets which maintained the

16.83% it recorded in 2010. On the other hand, the following asset categories

decreased: Interbank Placements from 6.22 percent in 2010 to 2.61 percent in 2011;

Other Short Term Funds, comprising money at call and placement with discount

houses, from 1.66 percent in 2010 to 1.63 percent in 2011; Net loans and advances from

32.20 percent in 2010 to 29.14 percent in 2011; Total Investments, comprising

Investments in Federal Government Development Stock, Investments in Preference

Shares and Debentures of other companies and other long term securities, from 18.10

percent in 2010 to 11.64 percent in 2011; Other Assets (net) from 4.57 percent in 2010 to

3.86 percent in 2011; and Net Fixed Assets from 3.63 percent in 2010 to 2.97 percent in

2011.

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

142

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

TABLE 13.1

INSURED BANKS' STRUCTURE OF ASSETS

13.2 INSURED BANKS' STRUCTURE OF LIABILITIES

Table 13.2 presents the structure of liabilities of insured banks in 2011 (compared with

the figures for 2010). During the period under review, there was a quantum leap in the

proportion of Reserves to Total liabilities as it increased from 0.96% in 2010 to 10.35% in

2011. The increase in Reserves was attributable to the purchase of non-performing

loans of DMBs by the AMCON. As a result of that, the amount of provisioning for non-

performing loans reduced. Another liability category that increased, albeit slightly was

Balances with CBN (Current Account) from 0.03 percent in 2010 to 0.30 percent in 2011.

Due to Other Banks also increased from 0.22 percent in 2010 to 0.66 percent in 2011.

The remaining categories of liabilities, when expressed as a proportion of total liabilities

reduced: Total Deposits from 58.07 per cent in 2010 to 56.33 percent in 2011; Interbank

Takings from 4.82 percent in 2010 to 0.78 percent in 2011; Other Liabilities from 12

Assets

Percentage Share as at 31st December

(%)

2010 2011 Cash and Due from other banks 10.70 14.21 Inter-Bank Placements

6.22

2.61

Total Short Term Investments

6.09

17.11

Other Short Term Funds

1.66

1.63 Net Loans and Advances/Leases

32.20

29.14

Total Investment

18.10

11.64 Other Assets(Net)

4.57

3.86

Net Fixed Assets

3.63

2.97

Off-Balance Sheet Engagements

16.83

16.83

Total Assets

100

100

Total Assets (inclusive of OBS) (N’ Billion)

N18,661.27

N21,891.56

Source: Bank Returns

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

143

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

Liabilities

Percentage Shareas at December (%)

2010

2011

Total Deposits

58.07

56.33

Interbank Takings

4.82

0.78

Central Bank (Current Account)

0.03

0.30

Due To Other Banks

0.22

0.66

Total Certificates of Deposits

0.00

0.00

Other Liabilities

12.00

9.60

Long Term Loans

5.72

4.22

Equity Capital

1.34

1.01

Reserves

0.96

10.35

Off-Balance sheet Engagement 16.83 16.83

Total Liabilities 100 100

Total Value of Liabilities Inclusive of Off Balance Sheet Engagements

N18,661.27 N21,891.56

Source: Bank Returns

TABLE 13.2

INSURED BANKS' STRUCTURE OF LIABILITIES IN 2010 & 2011

percent in 2010 to 9.60 percent in 2011; Long term loans from 5.72 per cent in 2010 to

4.22 per cent in 2011; Equity Capital from 1.34 per cent in 2010 to 1.01 percent in 2011.

13.3 INSURED BANKS' SHAREHOLDERS' FUND

There was a significant increase in the shareholders' funds from 312.36 billion in 2010 to

₦1,934.93 billion in 2011. That was largely attributable to the activities of AMCON

through the purchase of non-performing loans from banks.

The resolution of the problem of undercapitalization through the injection of fresh

capital, mergers and acquisitions and the recapitalization of the three banks acquired

by AMCON positively impacted on the banking industry's shareholders' funds. Table

13.3 shows the shareholders' funds of DMBs in 2011 compared to the figures in 2010.

₦

Source: Bank Returns

11

Skye Bank Plc.

90.14

99.64

12

Enterprise Bank plc

(92.40)

11.87

13

Stanbic

IBTC Bank Plc

66.09

70.25

14

Standard Chartered Bank Ltd.

35.92

37.4215

Sterling Bank Plc.

21.68

27.29

16

Union Bank Plc.

(281.49)

54.25

17 United Bank for Africa Plc. 174.69 141.68

18 Unity Bank Plc. 7.43 17.99

19 Wema Bank Plc. (3.49) 11.61

20 Zenith Bank Plc. 290.80 296.04

Total 312.36 1,934.93

S/N

BANKS

SHAREHOLDERS’FUNDS

(N’ BILLION)

2010

SHAREHOLDERS’ FUNDS (N’ BILLION)

2011

1

Access Bank Nig. Plc.

167.61

187.792

Mainstreet Bank plc

(265.27)

35.82

3

Keystone Bank plc

(209.45)

45.24

4

Citibank Nigeria Ltd.

32.17

33.70

5

Diamond Bank Plc.

110.36

91.36

6

Ecobank Plc.

72.28

44.99

7

Fidelity Bank Plc.

128.62

104.88

8 First Bank of Nig. Plc. 312.21 318.789 First City Monument Bank Plc. 127.43 130.34

10 Guaranty Trust Bank Plc. 174.49 173.99

TABLE 13.3

INSURED BANKS' SHAREHOLDERS' FUNDS AS AT DECEMBER 2010 AND 2011

13.4 Ownership Structure

The ownership structure of Nigerian banks in 2011 remained diversified as in the previous

years. Table 13.4 shows that government ownership of shares was below 10% in most of

the banks. As shown in the table, Union Bank, Unity Bank and Wema Bank were the

three banks that had up to 10% government equity ownership. The three banks,

namely: Mainstreet Bank Ltd, Enterprise Bank Ltd and Keystone Bank Ltd acquired by

AMCON had 100% government equity ownership.

Also, the table shows that six out of the twenty banks had some level of foreign

ownership during the period under review. Out of that number, four banks, namely:

Citibank Ltd, Standard Chartered Bank Plc, Stanbic IBTC Plc and Union Bank Plc had

substantial foreign equity holdings in excess of 50% of total equity capital.

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

144

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

145

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

13.5 INSURED BANKS ASSETS BY MARKET SHARE

As in previous years, the oligopolistic tendencies remained in the industry as assets were

concentrated among the larger banks. Out of total assets (excluding OBS) of ₦18.20

trillion as at end of December 2011, the assets of the top five (5) DMBs, amounted to

₦9.59 trillion representing 52.67% of the total assets of all the banks compared to its level

of ₦7.47 trillion or 48.26% of the total assets of the industry in 2010. The table also shows

that the assets of the top ten (10) DMBs stood at ₦14.17 trillion, representing 77.83% of

the total assets of the industry as at the end of December 2011 compared to ₦11.01

trillion, representing 71.08% in 2010. The remaining ten banks had assets to the tune of

₦4.03 trillion, which represented 22.17% of total assets as at the end of December 2011

as against ₦4.48 trillion, representing 22.17 % of total industry assets in 2010. Table 13.5

and Chart 13A present the market share by asset of DMBs in 2011.

S/N

BANKS

OWNERSHIP STRUCTURE (%)

GOVT. PRIVATE

(NIGERIAN)FOREIGN

1 Access Bank Plc 1 99 -

2 Citibank Nig Ltd - 18.1 81.9

3 Diamond Bank Plc - 100 4 Ecobank Plc - 100 5 Enterprise Bank 100 - -

6 Fidelity Bank 100 7 First Bank Plc - 100 -8

First City Monument Bank

100

-

9

Guaranty Trust

-

100

-

10

Keystone Bank

100

-

-

11

Mainstreet Bank

100

-

12

Standard Chartered Bank Nig Ltd

-

-

100

13

Skye Bank Plc

1

50

49

14

Stanbic IBTC Bank

Plc

-

47.31

52.69

15 Sterling Bank Plc 2.55 78.64 18.8

16 United Bank for Africa Plc 2.77 97.23 -

17 Union Bank Plc 19 21 60

18 Unity Bank Plc 35 65 -

19 Wema Bank Plc 10 90 -

20 Zenith Bank Plc 2.8 97.18 -

TABLE 13.4

INSURED BANKS' OWNERSHIP STRUCTURE AS AT DECEMBER 31, 2011

Source: Bank Returns

13.6 Insured Banks' Deposit Liabilities by Type, Market Share and Tenor

Bank deposits usually constitute the largest component of the liability of a bank's

balance sheet. An analysis of the types and sizes of deposits mobilised by banks would

reveal the relative effectiveness of asset/liability management in the financial

institutions. As had been the trend over the years, total deposit liabilities of insured banks

increased from ₦10.84 trillion as at December 2010 to ₦12.33 trillion as at December 31,

2011, representing an increase of 13.75%. Several reasons could account for the

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

146

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

Bank

2010 2011

Assets (N’ Billion)

(%) of Total

Assets ( N’ Billion)

(%)of Total

Top 5 7,471.42 48.26 9,586.8 52.67

Top10 11,005.88 71.08 14,166.77 77.83

All Other Banks 4,478.51 28.92 4,034.70 22.17

TABLE 13.5

SIZE OF ASSETS OF TOP INSURED BANKS

Source: Bank Returns

CHARTS 13A

ANALYSIS OF ASSETS HELD BY INSURED BANKS IN 2011

significant increase in deposit liabilities of insured banks. Amongst these were

improvement in service delivery, innovative and aggressive deposit mobilization by

insured banks, increase in the number of Automated Teller Machines (ATMs) in strategic

locations, the introduction of new products as well as the sanitisation efforts of the

Regulatory Authorities. Table 13.6 and Chart 13B give the analysis of the total deposit

liabilities of insured banks as at December 2011 with comparative figures for 2010.

As shown in Table 13.6 and Chart 13B, savings deposits in insured banks increased by

₦271.16 billion or 16.9%, from ₦1.60 trillion as at December 2010 to ₦1.87 trillion as at

December 2011. A further analysis of the situation in 2011 vis-à-vis 2010 revealed that

savings deposits increased not only in absolute terms but as a proportion of total

deposits. While savings deposits constituted 14.8% of total deposits in 2010, that

category of deposits was 15.16% of total deposits in 2011. Demand deposits of insured

banks amounted to ₦7.63 trillion and accounted for 61.91% of banks' total deposit

liabilities as at December 31, 2011. Demand deposit liabilities increased both in

absolute terms and as a proportion of total deposit. That category of deposits

increased significantly by ₦3.12 trillion or 69.04% from ₦4.52 trillion (41.7%) as at

December 31, 2010 to ₦7.63 trillion (61.91%) as at December 31, 2011. Time/term

deposits in insured banks decreased both in absolute terms and as a proportion of total

deposits. Time/term deposits decreased by ₦1.89 trillion from ₦4.72 trillion in December

2010 to ₦2.83 trillion as at December 2011. As a proportion of total deposits, time/term

deposits also decreased from 43.5% as at the end of 2010 to 22.93% as at the end of

December 2011.

13.6.1 Deposit Liabilities by Type

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

147

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

Type of Deposit

Liabilities

2010

2011

Amount

(=N=’M)

Percentage

of Total (%)

Amount

(=N=’M)

Percentage

of Total (%)

Savings Deposits

1,598,517.25

14.8

1,869,677.19 15.16

Demand

Deposits*

4,515,167.62

41.7

7,632,847.12 61.91

Time/Term

Deposits 4,723,459.18

43.5

2,827,739.47 22.93

TOTAL 10,837,144.06 100.00 12,330,263.78 100.00

TABLE 13.6

COMPOSITION OF TOTAL DEPOSIT LIABILITIES OF INSURED BANKS IN 2010 AND 2011

Source: Bank Returns

* Included in Demand Deposits are Electronic Purse, Domiciliary Accounts and Other Deposits, Certificates and Notes

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

148

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

*Included in Demand Deposits are Electronic Purse, Domiciliary Accounts, and Other

Deposits & Cert. & Notes.

CHART 13B

13.6.2 Deposit Liabilities by Market Share

The market share of deposit of the top five and top ten banks increased during the year

under review. Out of the total deposit liabilities of ₦12.33 trillion in 2011, the deposits of

the top five banks amounted to ₦6.49 trillion or 52.6% of the total deposits as against

46.7% held by the top five banks in 2010. Furthermore, deposit liabilities generated by

the top ten (10) banks stood at ₦9.70 trillion or 78.7% of the total deposit liabilities of all

insured banks as at December 2011 in contrast to 70.1% as at December 2010. The

remaining 15 DMBs held only 47.4% of total industry's deposit as at 31st December, 2011.

Table 13.7 and Chart 13C present the market share of deposit of the top 5 and Top 10

banks in 2011.

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

149

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

Banks

2010 2011

Deposits

(N’Billion)

Percentage of

Total (%)

Deposits

(N’ Billion)

Percentage of

Total (%)

Top Five Banks

5,056.15

46.7

6,486.26

52.6

Top Ten Banks

7,598.82

70.10

9,703.25

78.7

All Other Banks 3,238.32 29.90 2,627.01 21.3

TABLE 13.7

ANALYSIS OF DEPOSIT LIABILITIES HELD BY THE BIG INSURED BANKS

Source: Bank Returns

CHART 13C

13.6.3 Deposit Liabilities by Tenor

The total deposit liabilities of banks by tenor for 2011 and the comparative figures for

2010 are presented in Table 13.8 and Chart 13D. From the table, short-term deposits of

below 30 days increased in absolute terms from ₦8.10 trillion in 2010 to ₦9.48 trillion in

2011, representing an increase of 17.1%. Similarly, as a proportion of total deposits,

short-term deposits of below 30 days increased slightly from 76.30% in December 2010

to 76.86% in 2011. Deposits of between 31 and 90 days increased marginally from

₦1,524.30 billion in 2010 to ₦1,524.72 billion in 2011. However, as a proportion of total

deposits, it recorded a decrease from 14.4% in 2010 to 12.37% in 2011.

Deposits with tenor of between 91 and 180 days increased both in absolute term and as

a percentage of total deposit liabilities from ₦356.45 billion or 3.4% in 2010 to ₦548.80

billion or 4.45% in 2011. Deposits with tenor of between 181 and 365 days increased

marginally from ₦301.32 billion or 2.8% in 2010 to ₦510.29 billion or 4.14% in 2011. Long-

term funds of more than 365 days' duration (one year), however, declined both in

absolute terms and as a percentage of total deposit liabilities from ₦332.31 billion or

3.10% as at December 31, 2010 to ₦270.01 billion or 2.18% as at December 31, 2011.

The analysis of insured banks' deposits by tenor shows that depositors preferred to keep

their funds in short-term deposits with roll-over options, than keeping their funds for a

longer tenor in order to hedge against the volatility of interest rates.

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

150

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

Types of Deposits

2010 2011

Amount (N’M)

Percentage of Total

(%)

Amount ( N’M)

Percentage of Total

(%)

Below 30 Days

8,095,768.03

76.30

9,476,428.75 76.86

Between 31 and 90 Days

1,524,308.78

14.4

1,524,723.04 12.37

Between 91 and 180 Days

356,454.67

3.4

548,806.39 4.45

Between 181 and 365 Days

301,321.54

2.8

510,295.62 4.14

Above 365 Days 332,318.88 3.1 270,009.98 2.18

TOTAL 10,837,144.06 100 12,330,263.78 100

TABLE 13.8

ANALYSIS OF INSURED BANKS' DEPOSITS BY TENOR

CHART 13D

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

151

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

SECTION 14

INSURED BANKS REPORT ON FRAUDS/FORGERIES AND

FIDELITY BOND INSURANCE COVER

INSURED BANKS REPORT ON FRAUDS/FORGERIES AND

FIDELITY BOND INSURANCE COVER

14.0 Introduction

14.1 FRAUDS AND FORGERIES IN INSURED BANKS IN 2011

Sections 35 and 36 of the Nigeria Deposit Insurance Corporation (NDIC) Act No. 16 of

2006 provides for the rendition of monthly returns by all insured deposit money banks

(DMBs) on frauds and forgeries as well as the notification of the NDIC of any dismissal or

termination of staff on the grounds of frauds or financial malpractice.

This section presents the report on cases of frauds and forgeries in the banking industry

in the country in 2011. The section further provides information on the nature of the

cases reported as well as the number and categories of staff involved. The section is

concluded with a report on insured DMBs compliance with fidelity bond insurance

cover during the year under review.

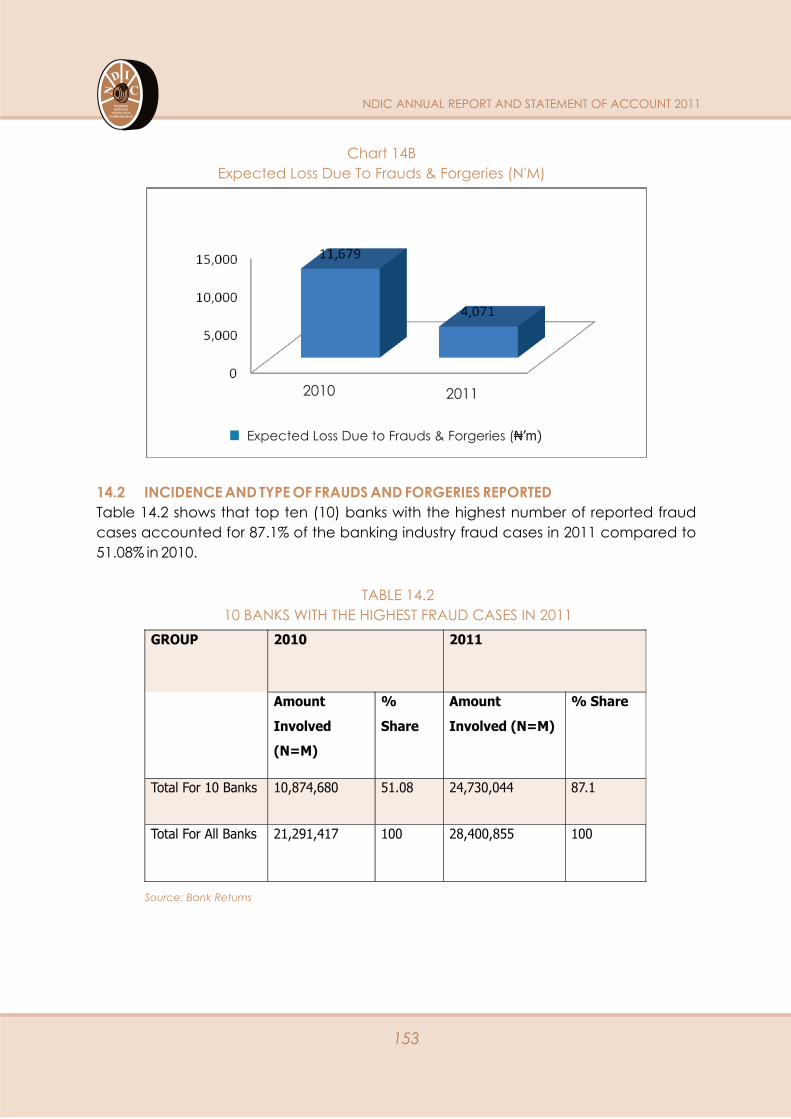

A total of 2,352 fraud cases involving the sum of ₦28.40 billion with

expected/contingent loss of about ₦4.071 billion were reported by DMBs in 2011. That

was an increase of 53.5% in 2011 over the number of reported fraud cases of 1532 in

2010. Although, the amount of frauds and forgeries increased by 33.40% from ₦21.29

billion in 2010 to ₦28.40 billion in 2011, the expected loss decreased by 65% from ₦11.68

billion in 2010 to ₦4.07 billion in 2011. Table 14.1 and Charts 14A and 14B presents returns

of insured banks on frauds and forgeries during the year under review.

Quarter

Year

Total No.

of

Fraud

Cases

(N’m)

Total

Amount

Involved

(N’m)

Total

Expected

Loss (N’m)

Proportion of

Expected Loss

To Amount

Involved (%)

1st 2011 612 2,301 837 36.38

2010

325

4,671

1,757

37.62

2nd

2011

509

3,807

654

17.18

2010

232

4,206

2,767

65.79

3rd

2011

577

2,207

776

35.16

2010

403

8,300

6,438

77.57

TABLE 14.1

RETURNS OF INSURED BANKS ON FRAUDS AND FORGERIES IN 2011

4th 2011 654 20,085 1,805 8.99

2010 572 4.114 717 17.43

Average/Total 2011 2,352 28,400.86 4,071 14.33

2010 1,532 21,291.41 11,679 54.85

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

152

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

Source: Bank Returns

As shown in Table 14.1, the increase of 53.5% in the number of attempted or successful

fraud and forgeries cases as reported in 2011 over the preceding year could be

attributed to rising fraud cases through internet banking and suppression of customer

deposits.

Chart 14A

Amount of Frauds & Forgeries (N'M)

Key

Series-Year

1-2010

2-2011

2010 2011

Amount of Frauds and Forgeries (₦’m)

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

153

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

Chart 14B

Expected Loss Due To Frauds & Forgeries (N'M)

14.2 INCIDENCE AND TYPE OF FRAUDS AND FORGERIES REPORTED

Table 14.2 shows that top ten (10) banks with the highest number of reported fraud

cases accounted for 87.1% of the banking industry fraud cases in 2011 compared to

51.08% in 2010.

GROUP 2010 2011

Amount

Involved

(N=M)

%

Share

Amount

Involved (N=M)

% Share

Total For 10 Banks

10,874,680

51.08

24,730,044

87.1

Total For All Banks

21,291,417

100

28,400,855

100

TABLE 14.2

10 BANKS WITH THE HIGHEST FRAUD CASES IN 2011

Source: Bank Returns

2010 2011

Expected Loss Due to Frauds & Forgeries (₦’m)

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

154

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

A further analysis of the types and nature of the frauds and forgeries committed during

the year under review revealed that ATM Frauds and Fraudulent transfers/withdrawals

accounted for the largest number of perpetrations as had been the case in the

preceding year. There were also rising fraud cases through internet banking and

suppression of customer deposits. The most common cases are listed in Table 14.3.

S/N Nature Of Fraud Frequency

1

ATM Fraud

738

2

Fraudulent Transfer/Withdrawal of Deposit

331

3 Presentation of Forged Cheques 280

4 Outright Theft 240

5 Suppression of Customer Deposit 219

6

Fraudulent Conversion of Cheques

123

7

Non Dispensing Of Money But Registered By

The Electronic Journal

112

8

Internet Fraud

108

TABLE 14.3

TYPE OF FRAUDS AND FORGERIES WITH FREQUENCY

14.3 BANKS' STAFF INVOLVED IN FRAUDS AND FORGERIES

Of the 2,352 fraud cases reported during the year under review, 498 were attributed to

staff/staff participation which showed an increase of 141 from 357 cases reported in

2010. Despite the increase, the losses resulting there from declined by 62.3% from ₦6.43

billion in 2010 to ₦2.42 billion in 2011. The reduction was as a result of better and

improved security and internal control measures put in place by the banks for

transactions involving large sums of money.

Table 14.4 shows the number of staff involved in fraud and forgeries in the past three

years with their respective status.

Source: Bank Returns

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

155

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

Status

2009 2010 2011

Number % Number % Number %

Supervisors & Managers

94

14.32

92

25.77

89

17.87

Officers, Accountants & Executive Assistants

137

20.88

79

22.13

126 25.30

Clerks & Cashiers

200

30.49

115

32.22

163 32.73

Typists, Technicians & Stenographers

64

9.76

23

6.44

7

1.41

Messengers, Drivers, Cleaners, Security Guards & Stewards

11

1.68

15

4.20

35

7.03

Temporary Staff 150 22.87 33 9.24 78 15.66

Total 656 100 357 100 498 100

TABLE 14.4

CATEGORIES OF BANKS' STAFF INVOLVED IN

FRAUDS AND FORGERIES IN 2011

The number of staff involved increased by 39% in 2011 from the preceding year. The

highest number of staff involved in cases of fraud and forgeries during the year under

review was from the clerks and cashier status as had been the case in the preceding

years with the lowest being from the typists, technicians and stenographers.

The causes of frauds could be categorised into two, namely: institutional/endogenous

factors and environmental/exogenous factors. The institutional/endogenous causes

are those that can be attributed to the internal domain of the organisation such as poor

accounting and weak internal control systems, poor management, inexperienced

staff and ineffective supervision of subordinates, uncompetitive remuneration and

perceived sense of inequity in reward, overstretching of staff, disregard of 'Know Your

Customers' (KYC) rules, et cetera. Environmental/exogenous factors are factors that

can be directly traced to the bank's operating environment and they include undue

societal demands, low moral values, slow and tortuous legal process, lack of effective

deterrent or punishment and, at times, reluctance on the part of the individual banks to

report fraud cases due to the negative publicity it could attract for their image.

In view of the extent of frauds and forgeries in the year under review, it is imperative that

all insured banks employ measures to strengthen their operational risk management

frameworks in the areas of internal control and security systems to combat the

incidence of frauds and forgeries. Insured banks should also endeavour to fully comply

with guidelines, rules and regulations on good corporate governance in order to take

14.4 CAUSES OF FRAUDS AND FORGERIES IN INSURED BANKS

Source: Bank Returns

control of the situation. The NDIC would also continue to ensure banks' compliance by

imposing sanctions in case of any breach by any insured bank. Furthermore, insured

banks should also thoroughly screen prospective employees by obtaining status report

from previous employers and relevant agencies while employees should be made to

be aware of the risks in defrauding or attempting to defraud the bank and the action

expected if caught. Insured banks should also endeavour to educate their customers

on the use of ATM and other electronic banking services.

In accordance to Section 33 of the NDIC Act of 2006, all insured banks are expected to

take up fidelity insurance cover which is a measure prescribed for protecting them

against any losses of money or property incurred as a result of fraudulent acts

committed by employees. It insures employers from incurring any losses caused by

dishonest actions of bank's staff and it is intended to cushion/reduce the adverse

impacts of such losses. It is therefore compulsory for all insured banks to take up fidelity

insurance cover as and when due. Table 14.5 presents banks' compliance with the

NDIC's fidelity insurance cover.

14.5 REPORT ON BANKS' FIDELITY BOND INSURANCE COVER

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

156

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

Year (a)

No. Of Banks In

operation

(b)

No. Of Banks

that Complied

(c=b/a)

% of Total

2011

20

18

90

2010

24

24

100

2009 24 23 95.83

Source: Bank Returns

TABLE 14.5

COMPLIANCE STATUS OF INSURED BANKS TO NDIC

FIDELITY INSURANCE COVER REQUIREMENT

As shown in the Table 14.5, two banks, namely: Fidelity Bank Plc and Sterling Bank Plc

failed to render returns on fidelity bond insurance cover in 2011. All DMBs that complied

with the requirement acquired their insurance policies from companies registered with

National Insurance Commission (NAICOM) as required by the NDIC Act.

Further analysis shows that only five out of the eighteen DMBs that complied with the

fidelity bond insurance policy met up with the required 15% paid-up capital implying

that the remaining 13 banks were underinsured due to inadequate fidelity bond

insurance cover during the year under review.

SECTION 15

INSURED BANKS' OFFICES, BRANCHES, BOARD OF DIRECTORS

AND APPROVED EXTERNAL AUDITORS

INSURED BANKS' OFFICES, BRANCHES, BOARD OF DIRECTORS

AND APPROVED EXTERNAL AUDITORS

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

157

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

15.1 Distribution of Insured Banks' Offices and Branches

As at the end of December 2011, there were a total of 5,763 branches/offices operated

by the twenty (20) insured DMBs in the system. That figure was an increase of 189

branches or 3.39% over the 5,574 branches/offices reported in 2010. Table 15.1 shows

the distribution of insured banks' branches/offices in the 36 states of the Federation and

the Federal Capital Territory (FCT), Abuja in 2011.

As evidenced in the table, Lagos State accounted for the highest number of bank

branches/offices with 1,731 branches, about 30.04% of the total. Abuja (FCT) came a

distant second with 397 branches/offices (6.89%), Rivers State came third with 301

branches/offices (5.22%), while Oyo State occupied the fourth position with a total of

234 branches/offices (4.06%). Other leading states during the year under review were

Anambra (233 or 4.04%), Delta (205 or 3.56%), and Edo with (184 or 3.19%).

S/N

States (Including

Abuja)

Number of Branches/Offices

Percentage Share

(%) 1.

Abia 139 2.41

2.

Abuja (FCT) 397 6.89

3.

Adamawa 64 1.11

4.

Akwa-Ibom 110 1.91

5.

Anambra 233

4.04

6.

Bauchi 59

1.02

7.

Bayelsa 36

0.62

8.

Benue 75

1.30

9.

Borno 77

1.34

10.

Cross River 72

1.25

11.

Delta

205

3.56

12.

Ebonyi

42

0.73

13.

Edo

184

3.19

TABLE 15.1

DISTRIBUTION OF INSURED BANKS' OFFICES AND

BRANCHES AS AT 31ST DECEMBER, 2011

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

158

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

14.

Ekiti

78 1.35

15.

Enugu 128 2.22

16.

Gombe 45 0.78

17.

Imo 105 1.82

18.

Jigawa 42 0.73

19.

Kaduna 177 3.07

20.

Kano 184

3.19

21.

Katsina 56

0.97

22.

Kebbi 44

0.76

23.

Kogi 84

1.46

24.

Kwara 78

1.35

25.

Lagos 1,731

30.04

26

Nassarawa

51

0.88

27.

Niger

78

1.35

28.

Ogun

176

3.05

29.

Ondo

117

2.03

30

Osun

103

1.79

31.

Oyo

234

4.06

32.

Plateau

79

1.37

33.

Rivers

301

5.22

34.

Sokoto

58

1.01

35.

Taraba

40

0.69

36.

Yobe

41

0.71

37.

Zamfara

40

0.69

Total

5,763

100

Source: Bank Returns

NDIC ANNUAL REPORT AND STATEMENT OF ACCOUNT 2011

159

N

D I

CNIGERIADEPOSIT

INSURANCECORPORATION

15.2 Head Offices' Addresses and Branches of Insured Banks

15.3 Insured Banks and Their Board of Directors

The distribution of branches per insured bank and Head Office is presented in Table

15.2. As in the past, two (2) banks, namely: First Bank of Nigeria Plc and United Bank for

Africa Plc maintained the first and second positions with the highest number of

branches, while there was a change in the third position from Union Bank Plc to

Ecobank Plc (due to the merger of Ecobank and Oceanic Bank Plc). First Bank of

Nigeria Plc was in the lead with a total of 650 branches, United Bank for Africa Plc was

second with a total of 607 branches, while Ecobank Plc came third with a total of 586

branches. The three banks, as shown in Table 15.2, accounted for 1,843 branches, or

31.98% of the total number of banks' branches/offices in the system. Other leading

banks in terms of branches/offices were Access Bank Plc with 487, Zenith Bank Plc with

393, Union Bank of Nigeria Plc with 382, FCMB with 321, Keystone Bank Ltd and Diamond

Bank Plc with 270 and 250 respectively. Unity Bank Plc had 241, Skye Bank Plc had 238

branches while Mainstreet Bank Ltd had 223.

A sound and responsive corporate governance is critical for the survival of any

organization. The board is a major vehicle for instituting corporate governance. The

board constitutes the highest policy making organ of a bank like in any other

organization as what happens at that level impacts significantly on the operations and

activities of the institution. Insured banks' directors are expected to review policies and

operations of their banks as well as undertake other responsibilities that enable the

banks to operate in a safe and sound manner. Experience has also shown that no

matter how effective regulation is, it does not substitute for the role of an active and

efficient board of directors in banks.

Banking institutions require the highest level of confidence of the members of the public

to survive. An important way of ensuring the survival of banks is for their boards to show

the highest sense of discipline, integrity, steadfastness and tenacity of purpose. Over

the years, the nation's Regulatory/Supervisory Authorities had continually raised issues

bordering on poor corporate governance in some of the banks which could impair

their viability. Regrettably, rather than improve, some of the banks, as revealed by

findings in their on-site examination reports in 2011, continued to exhibit weak

corporate governance practices which manifested in the form of inadequate risk

management framework, ineffective boards' risks management control functions and

regulatory infractions like non-adherence to the Code of Corporate Governance,

among others.

In 2007, the CBN issued Guidelines to all insured banks for the appointment of

Independent Directors. The Guidelines were issued so as to enable banks comply with

Section 5.3.6 of the Code of Corporate Governance for banks operating in Nigeria

effective April 3, 2006. As stated in that Section “at least two (2) non-executive board

members described as Independent Directors (who do not represent any particular

shareholders' interest and hold no special business interest in the bank) should be

appointed by the bank on merit”. In terms of compliance with that requirement, a

review of the nation's banking industry as at the end of year 2011, showed that a few of

the banks were yet to comply with that directive.

The list of insured banks' directors as at 31st December, 2011 is presented in Table 15.2.

As shown in the table, there were 322 directors serving on the boards of the 20 deposit

money banks operating in the system during the year under review.

Auditors play a vital role in the corporate governance process. As a result, the

Regulatory/Supervisory Authorities had continued to strengthen the roles of External

Auditors by encouraging measures that would ensure their independence, through the

regulation of their appointment and disengagement. The statutory reporting

requirements of insured banks' external auditors to the NDIC are stipulated under

Section 54 of the NDIC Act No. 16 of 2006. The CBN's directives and guidelines also

impose basic responsibilities/obligations on banks' external auditors. The external

auditors' reports are expected to lend credence to the banks' financial statements

thereby assisting in promoting confidence and transparency in the banking system.

Approved banks' external auditors are expected to complement the activities of the

Regulatory/Supervisory Authorities in making the banking industry safe and sound.

Their job includes examination of evidence relevant to amounts and disclosures in the

financial statements. It also includes an assessment of the significant estimates and

judgements made by the management and directors in the preparation of the

financial statements; and of whether the accounting policies are appropriate to the

bank's circumstances, consistently applied and adequately disclosed in line with best

practices.

As evidenced in Table 15.2, there were six (6) firms of Chartered Accountants approved

to conduct independent audit of the 20 insured DMBs operating in the system as at

December 31, 2011. KPMG Professional Services, from available statistics, topped the

list with 8 banks on their audit list, followed by PriceWaterhouse Coopers with 6 banks,

while Akintola Williams Deloitte had 4 banks, which were audited either wholly or jointly

with another firm during the year under review.