d iamond o ffshore (do) october 24, 2013 1 michael derenzo jason chan paddy gu caleb pierson

TRANSCRIPT

DIAMOND OFFSHORE (DO)October 24, 2013

1

Michael DeRenzoJason ChanPaddy GuCaleb Pierson

AGENDA• Introduction• Company Overview• Macroeconomic Outlook• Relevant Stock Market Prospects• Financial Analysis• Valuation• Recommendation

2

DIAMOND OFFSHORE IN RCMP

3

• February 2008: Purchased 100 shares at $122.82 per share• November 2008: Purchased 50 shares at $72.96 per share• April 2009: Sold a Sep. $80 call at $5.85; Bought a Sep. $60 put

at $4.78• September 2009: Sold 100 shares at $76.25 vs. exercise

adjusted strike on short call• October 2010: Purchased 100 shares at $68.02 per share• Current share price: $63.23 • Accounts for 2.4878% of total portfolio value

COMPANY OVERVIEW

4

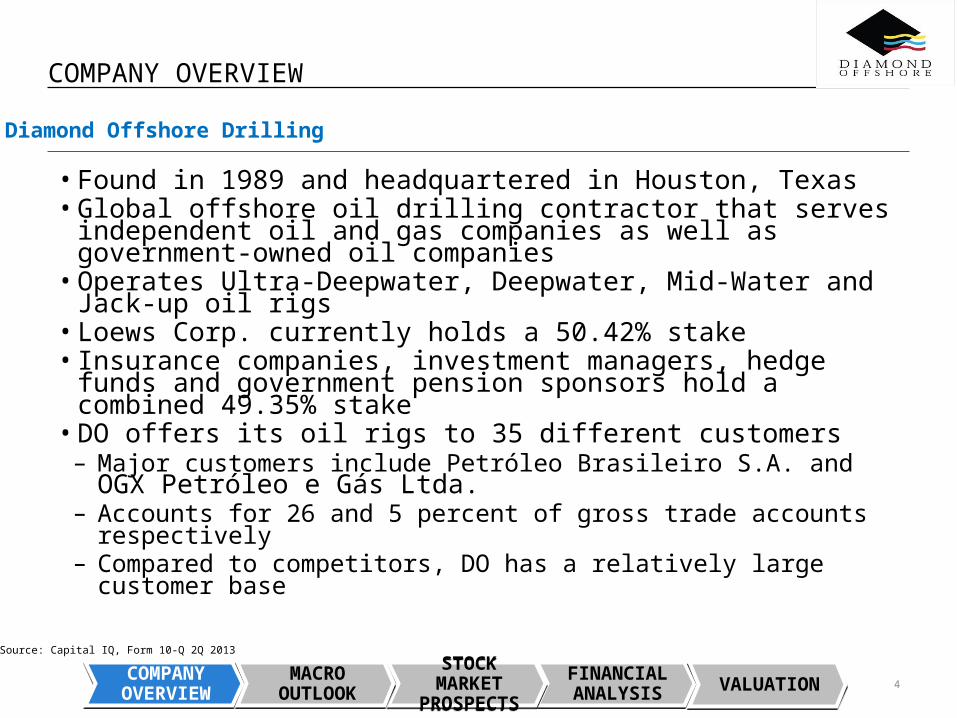

Diamond Offshore Drilling

• Found in 1989 and headquartered in Houston, Texas• Global offshore oil drilling contractor that serves independent

oil and gas companies as well as government-owned oil companies• Operates Ultra-Deepwater, Deepwater, Mid-Water and Jack-up

oil rigs• Loews Corp. currently holds a 50.42% stake• Insurance companies, investment managers, hedge funds and

government pension sponsors hold a combined 49.35% stake• DO offers its oil rigs to 35 different customers– Major customers include Petróleo Brasileiro S.A. and OGX

Petróleo e Gás Ltda.– Accounts for 26 and 5 percent of gross trade accounts respectively– Compared to competitors, DO has a relatively large customer base

Source: Capital IQ, Form 10-Q 2Q 2013

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

COMPANY OVERVIEW

5

Management’s Outlook

• Key factors that impact DO’s rigs operating results– Regulatory surveys and planned downtime

– 7 rigs will undergo surveys during second half of 2013– In total the 7 rigs will be out of service for approximately 670 days

– Physical damage on rigs– Construction and capital upgrade projects• All of these factors impact the revenue earning days for each of

the oil rigs, ultimately lowering the overall utilization rates and average daily revenue• Ultra-Deepwater and Deepwater Floater markets consists of

highest utilization rates– This will result in overall increased competition within these

markets

Source: Form 10-Q 2Q 2013

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

BREAKDOWN OF OIL RIGS BY OCEAN DEPTH

6FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

Source: Diamond Offshore, 2012. DiamondOffsore: Investors:Annual Reports and Proxy Statements. 2012. 21 Feb. 2013http://investor.diamondoffshore.com/phoenix.zhtml?c=78110&p=irol-reportsandproxy

COMPANY OVERVIEW

7

- Source: IHS, . N.p.. Web. 29 Oct 2013. <http://www.ihs.com/products/oil-gas-information/drilling-data/weekly-rig-count.asp&xgt;.

DO Oil Rigs Ultra-Deepwater Deepwater Mid-Water Jack-ups

Revenue Earning Days (2013) 1,198 873 2,099 918

Utilization (2013) 83% 97% 64% 72%

Average Daily Revenue (2013) $350,000 $399,200 $266,500 $86,800

Breakdown Of DO Oil Rigs

• DO recently increased total rig count to 45 – 38 floaters (Ultra-Deepwater, Deepwater, Mid-Water) and 7 Jack-ups– The newest rig is expected to be completed by Q1 2016 and has been contracted for use

in Q3 2016• As of 10/18/2013 global supply of oil rigs hit 814– Marketed utilization rate of 95.1%

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

8

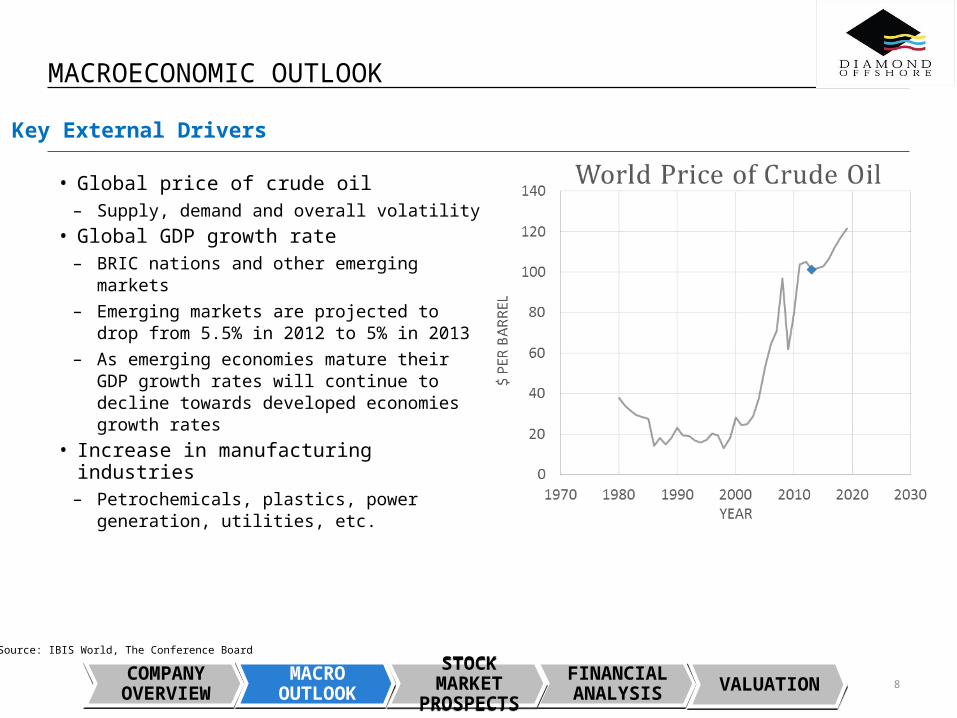

Key External Drivers

Source: IBIS World, The Conference Board

• Global price of crude oil– Supply, demand and overall volatility

• Global GDP growth rate– BRIC nations and other emerging markets– Emerging markets are projected to drop

from 5.5% in 2012 to 5% in 2013– As emerging economies mature their GDP

growth rates will continue to decline towards developed economies growth rates

• Increase in manufacturing industries– Petrochemicals, plastics, power generation,

utilities, etc.

MACROECONOMIC OUTLOOK

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

9

PROJECTED GLOBAL SUPPLY & DEMAND OF OIL

Source: . N.p.. Web. 29 Oct 2013. <http://www.eia.gov/forecasts/ieo/more_highlights.cfm

• Liquid fuels still remain the largest energy source– Liquid share of world energy consumption expected to fall from 34% (2010) to 28% (2040)

Global Oil Production Global Oil Demand

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

INDUSTRY OVERVIEW

10

Volatile prices prevail

BRIC demand

Deep-water Horizon

Oil and Gas consumption is expected to expand moderately as global economic growth continues

Environmental concerns associated with deep-sea oil and gas drilling

Rising operating costs through compliance monitoring and longer lead times

Industry's revenue is forecast to grow at an annualized rate of 2.5% in the five years to 2018 to $5.1 trillion

Ability to accommodate environmental requirements

Downstream ownership links

Output is sold under contract - incorporate long-term sales contracts

Control cost structure

Keys To Success

Industry TrendsCurrent Performance

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

INDUSTRY LIFE CYCLE

Mature•Industry contribution to US economy average at 1.4% per year•Lag the global economy’s GDP •Technological change tend to be incremental•Merger activity is ongoing

11

Intr

od

uct

ion

Gro

wth

Mat

uri

ty

Dec

lin

e

TimeT

ota

l In

du

stry

R

eve

nu

e

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

Source: IBIS World

PORTER’S FIVE FORCES

12

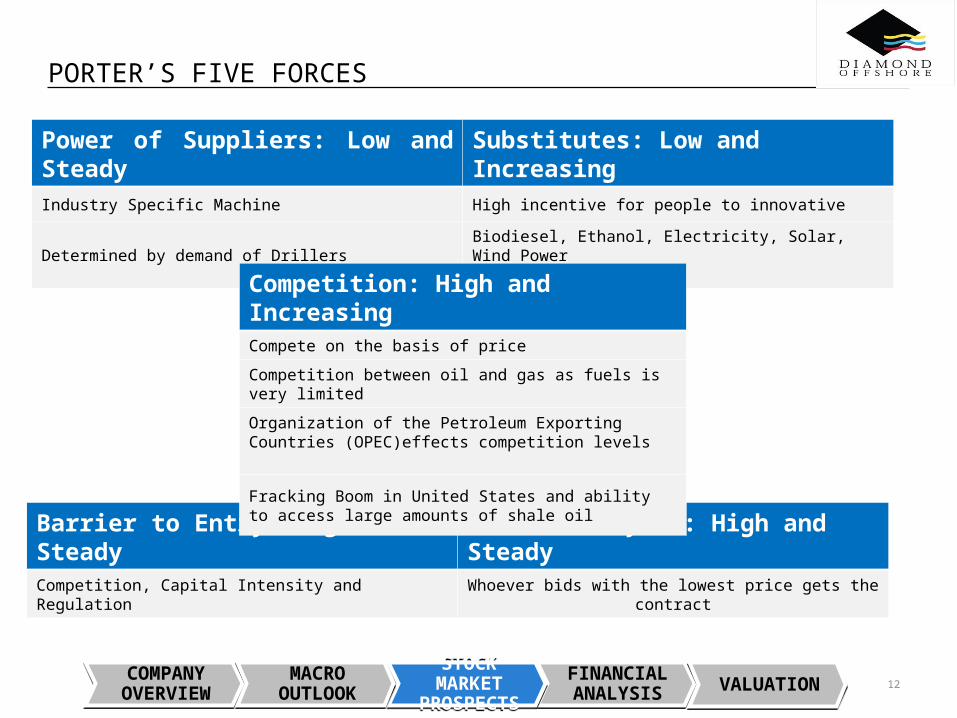

Power of Suppliers: Low and Steady Substitutes: Low and IncreasingIndustry Specific Machine High incentive for people to innovative

Determined by demand of Drillers Biodiesel, Ethanol, Electricity, Solar, Wind Power

Barrier to Entry: High and Steady Power of Buyers: High and SteadyCompetition, Capital Intensity and Regulation Whoever bids with the lowest price gets the contract

Competition: High and IncreasingCompete on the basis of price

Competition between oil and gas as fuels is very limited

Organization of the Petroleum Exporting Countries (OPEC)effects competition levels

Fracking Boom in United States and ability to access large amounts of shale oil

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

13

INDUSTRY ANALYSIS – OIL & GAS EXPLORATION & DRILLING

Revenue Revenue Growth

Source: U.S. Energy Information Administration (EIA)." U.S. Energy Information Administration (EIA). N.p., n.d. Web. 29 Oct. 2013.

• Expected revenue: $4.5 Trillions in 2013• Up from $4.2 trillion in 2008• Annualized growth rate of 1.3% from 2008 to 2013. • Revenue is expected to grow 3.0% in 2013 • Industry performance did experience significant pitfalls• Profit has fluctuated according to oil and gas prices.

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

DRILLING DAY RATES & UTILIZATION PERCENTAGES

14

Mid-Water Oil Rigs Deepwater & Ultra-Deepwater Oil Rigs

• IHS Petrodata Day Rate Indices track drilling fleet day rates and utilization percentages

• Day rates for Mid-Water Oil Rigs reached the highest level in October since the index’s inception in 1994

Source: "Day Rate Index | IHS." IHS Home Page. N.p., n.d. Web. 29 Oct. 2013.

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

UNDERSTANDING MARKET POWER

15

Strengths Weaknesses- Majority of fleet is in

sector with highest utilization rate

- Have five new ultra deep rigs becoming available soon

- Highly dependent on cash flow from a volatile emerging market

- Rely on a relatively small number of customers

Opportunities Threats- New technology allows for

deeper water exploration- Market does not have a

dominant company

- Volatility of crude oil prices

- Decline in GDP growth rates in emerging markets

- High incentives towards alternative energy

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

FINANCIAL ANALYSIS - RATIOS

16

DO, Financial Analysis

Liquidity Ratios2008 2009 2010 2011 2012

Current Ratio 2.88 4.17 2.98

4.66

4.39

Quick Ratio 2.88 4.17 2.98

4.66

4.39

Cash Ratio 1.45 1.88 1.72

2.89

3.06

Profitability Ratios2008 2009 2010 2011 2012

Operating Profit Margin 52.41% 42.89% 37.79% 32.22% 39.68%Net Margin 37.90% 28.75% 28.97% 24.12% 25.52%ROA 27.87% 15.25% 14.31% 10.35% 10.32%ROE (Book Value) 41.10% 26.32% 24.93% 16.63% 16.31%

Solvency Ratios2008 2009 2010 2011 2012

Debt/Assets 0.12 0.24 0.22 0.21

0.21

Debt/Equity 0.18 0.41 0.39 0.35

0.33

Interest Coverage 189.20 38.36 15.72

17.17 20.82

Activity Ratios2008 2009 2010 2011 2012

A/R Turnover 6.17 4.59 5.45 5.89

5.98

Days Sales Outstanding 59.20 79.51

66.96 61.95

61.07

Fixed Asset Turnover 1.04 0.82 0.78

0.71

0.61

Total Asset Turnover 0.72 0.58 0.49 0.48

0.41

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

FINANCIAL ANALYSIS – DUPONT

DuPont Analysis2008 2009 2010 2011 2012

Tax Burden 70.95% 73.66% 71.52% 81.62% 78.48%

Interest Burden 96.69% 98.17% 93.73% 93.93% 95.40%

Operating Profit Margin 52.41% 42.89% 37.79% 32.22% 39.68%

Asset Turnover 72.1% 57.97% 49.40% 47.71% 41.28%

Leverage 1.47 1.73

1.74

1.61 1.58

ROE 38.06% 31.02% 21.80% 18.94% 19.38%

17FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

RECENT STOCK PERFORMANCE

18

20 & 200 Day Moving Average Stock Chart

• DO’s stock price has been well below the 200 day moving average since the end of July, 2013

• Currently the stock price is hovering right around the 20 day moving average and looks as if it may fall below the 20 day moving average in the near future

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

Source: Yahoo Finance

VALUATION – UTILIZATION RATES

Utilization Rates - DOHistorical figures Forecast Figures2010A 2011A 2012A 2013P 2014P 2015P 2016P 2017P

Average Utilization Rates: Ultra-Deepwater 66% 82% 85% 85% 85% 84% 84% 83%

Deepwater 74% 94% 88% 88% 88% 87% 87% 86%

Mid-Water 79% 72% 68% 64% 64% 64% 63% 62%

Jack-Ups 61% 47% 53% 50% 50% 49% 48% 47%

Average Dayrates:

Ultra-Deepwater 358.40 342.90 354.90 365.55 376.51 387.81 399.44 411.43

Deepwater 401.90 416.50 368.80 379.86 391.26 403.00 415.09 427.54

Mid-Water 281.00 269.60 263.60 271.51 279.65 288.04 296.68 305.58

Jack-Ups 87.70 81.90 90.20 92.91 95.69 98.56 101.52 104.57

Number of Rigs

Ultra-Deepwater 9 11 12 12 12 12 13 13

Deepwater 5 6 7 7 7 7 7 8

Mid-Water 19 19 18 18 18 18 18 18

Jack-Ups 13 13 7 7 5 5 4 4

Total 46 49 44 44 42 42 42 43

19

Total Revenue ($ in millions) Ultra-Deepwater 777.05 1,128.93 1,321.29 1,440.99 1,500.71 1,562.71 1,762.68 1,835.09

Deepwater 542.77 857.41 829.21 873.50 899.70 936.99 965.10 1,148.54

Mid-Water 1,539.50 1,346.17 1,177.66 1,141.64 1,194.26 1,230.09 1,305.97 1,365.23

Jack-Ups 253.84 182.65 122.14 118.69 87.32 89.94 74.11 76.33

Total Contract Drilling Revenue 3,113.16 3,515.15 3,450.31 3,574.81 3,681.99 3,819.73 4,107.87 4,425.19

VALUATION – WACC

WACC Calculation

Capital Structure

Debt-to-Total Capitalization 24.2%Equity-to-Total Capitalization 75.8%

Cost of Debt

Cost of Debt 5.9%

Tax Rate 30.0%

After-tax Cost of Debt 4.1%

Cost of Equity

Risk-free Rate(1) 2.7%

Market Risk Premium 6.8%

Levered Beta 1.30

Cost of Equity 11.5%

WACC 9.7%

(1) Interpolated yield on 10-year U.S. Treasury

(2) Sourced from Capital

20

Comparable Companies Unlevered Beta

Market Market Debt/ Marginal Unlevered

Company Levered Beta Value of Debt Value of Equity Equity Tax Rate Beta

Transocean Ltd. (NYSE:RIG) 1.42 $12,459.0 $16,297.8 68.9% 30.0% 0.96

Ensco plc (NYSE:ESV) 1.33 $4,845.9 $12,802.0 39.0% 30.0% 1.04

Noble Corp. (NYSE:NE) 1.50 $4,634.4 $9,521.0 59.9% 30.0% 1.06

Rowan Companies plc (NYSE:RDC) 1.50 $2,009.6 $8,778.0 42.7% 30.0% 1.15

Atwood Oceanics, Inc. (NYSE:ATW) 1.59 $838.3 $4,512.0 63.9% 30.0% 1.10

Mean 1.47 0.55 1.06

Median 1.50 0.60 1.06

Relevered Beta

Mean Target Target

Unlevered Debt/ Marginal Relevered

Beta Equity Tax Rate Beta

Relevered Beta 1.06 31.9% 30.0% 1.30

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

CAPEX PROJECTIONS

21

Comparable Companies Capital Expenditures (2008) Capital Expenditures (2009) Capital Expenditures (2010) Capital Expenditures (2011) Capital Expenditures (2012) Average Growth Rate

Transocean Ltd. (NYSE:RIG) ($2,208.00) ($3,041.00) ($1,349.00) ($974.00) ($1,303.00)

Growth Rate(%) 37.73% -55.64% -27.80% 33.78% -2.98%

Ensco plc (NYSE:ESV) ($764.20) ($857.20) ($875.30) ($729.00) ($1,802.20)

Growth Rate(%) 12.17% 2.11% -16.71% 147.22% 36.20%

Noble Corp. (NYSE:NE) ($1,123.69) ($1,495.06) ($1,266.83) ($2,540.19) ($1,790.89)

Growth Rate(%) 33.05% -15.27% 100.52% -29.50% 22.20%

Rowan Companies plc (NYSE:RDC) ($829.16) ($566.38) ($490.56) ($1,517.67) ($685.26)

Growth Rate(%) -31.69% -13.39% 209.38% -54.85% 27.36%

Atwood Oceanics, Inc. (NYSE:ATW) ($328.25) ($430.47) ($187.09) ($514.86) ($785.08)

Growth Rate(%) 31.14% -56.54% 175.19% 52.49% 50.57%

Average Growth Rate: 26.67%

DO’s Capex growth rate based off of the average historical Capex of the Comparable Companies from FY2008 – FY2012

VALUATION – DCF

22FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

Discounted Cash Flows - DO

Historical Figures Forecast Figures

2008A 2009A 2010A 2011A 2012A 2013P 2014P 2015P 2016P 2017P

EBIT 2,011,491.00 1,998,154.00 1,472,111.00 1,309,995.00 991,731.00 1,526,725.89 1,464,752.29 1,476,298.42 1,510,323.77 1,574,801.63

Less: Income Taxes (536,499.00) (492,212.00) (380,559.00) (216,729.00) (197,604.00) (406,119.86) (389,762.17) (360,214.94) (376,172.27) (416,173.42)

Plus: D&A 287,417.00 346,446.00 393,177.00 398,612.00 392,913.00 533,312.47 731,495.82 926,146.86 1,262,794.12 1,713,025.32

Less: CapEx (666,857.00) (412,444.00) (434,262.00) (774,756.00) (702,041.00) (888,854.11) (1,125,378.19) (1,424,841.32) (1,803,991.60) (2,284,033.77)Less: Change in Working Capital: (311,884.00) 160,661.00 (458,810.00) (80,338.00) (28,580.73) 3,522.25 (109,542.07) 81,011.82 10,566.76

Unlevered FCF 687,507.87 559,091.60 284,703.68 293,660.48 (7,343.07)

Terminal Value = 19,385,911.52

Present Value of Cash Flows 693,032.98 611,792.63 470,924.54 556,161.01 481,175.11 PV of Terminal Value = 10,521,896.10

Discount Rate: 13.0%

EV = 11,941,596.76

3.3% premium added due to business risks involved

VALUATION – DCF

23

Terminal Value Assumption

Terminal Multiple 8.0x

Terminal Value 19,385,911.52

Calculation of Implied Share Price

Implied Enterprise Value $ 11,941,597

Less: Debt $ 1,496,066

Plus: Cash $ 1,485,590

Implied Market Cap $ 11,931,121

Implied Share Price $ 85.81

EBITDA Exit Multiple

EV/EBITDA Weighted

Transocean Ltd. (NYSE:RIG) 8.6x 20.0%

Ensco plc (NYSE:ESV) 7.7x 55.0%

Noble Corp. (NYSE:NE) 9.0x 5.0%

Rowan Companies plc (NYSE:RDC) 9.6x 10.0%

Atwood Oceanics, Inc. (NYSE:ATW) 8.9x 10.0%

Weighted Average: 8.0x

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

VALUATION – COMPARABLES COMPANY ANALYSIS

24

Multiples Weight Implied DO Share Price

Price/Book Value 20% $ 41.37

Forward TEV/Sales 20% $ 85.76

Forward TEV/EBITDA 25% $ 36.35

Forward P/E 25% $ 58.28

DCF 10% $ 85.81

DO Implied Stock Price $ 57.66

Comparables - DOEnterprise

Value / Price / Growth Rates Profitability

CY 2012 CY 2013 CY 2014 LT

Equity Debt/ Enterprise EPS EPS EPS EPS 1 Year Margins

Value Equity Value Rev. EBITDA BV Actual (1) Est. (1) Est. (1) Growth (1) Rev. EBITDA EBITDA NI

Transocean Ltd. (NYSE:RIG) $ 16,298 68.9% $ 23,722 2.5x 8.6x 1.0x 10.1x 11.5x 8.7x 22.8% 3.1% -1.5% 29.5% 7.5%

Ensco plc (NYSE:ESV) $ 12,802 39.0% $ 17,127 3.7x 7.7x 1.0x 10.0x 8.6x 7.5x 16.1% 16.1% 14.8% 48.5% 26.9%

Noble Corp. (NYSE:NE) $ 9,521 59.9% $ 15,399 4.1x 9.0x 1.2x 16.8x 12.9x 8.4x 20.3% 19.7% 29.5% 47.1% 18.7%

Diamond Offshore Drilling, Inc. (NYSE:DO) $ 8,778 31.9% $ 9,055 3.1x 6.6x 1.9x 12.6x 13.3x 10.0x 17.6% -0.7% -5.0% 46.9% 24.0%

Rowan Companies plc (NYSE:RDC) $ 4,512 42.7% $ 55,159 3.6x 9.6x 1.0x 18.2x 16.7x 10.2x 21.6% 14.0% 9.6% 37.8% 15.4%

Atwood Oceanics, Inc. (NYSE:ATW) $ 3,462 63.9% $ 4,581 4.6x 8.9x 1.7x 10.8x 10.3x 8.4x 23.5% 34.8% 39.7% 51.6% 33.6%

Mean 3.7x 8.8x 1.2x 13.2x 12.0x 8.6x 0.2x 0.2x 0.2x 0.4x 0.2xMedian 3.7x 8.9x 1.0x 10.8x 11.5x 8.4x 0.2x 0.2x 0.1x 0.5x 0.2x

High 4.6x 9.6x 1.7x 18.2x 16.7x 10.2x 0.2x 0.3x 0.4x 0.5x 0.3xLow 2.5x 7.7x 1.0x 10.0x 8.6x 7.5x 0.2x 0.0x 0.0x 0.3x 0.1x

FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

COMPARABLES STOCK CHART

25FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

• From the start of the year (2013), DO’s stock price has been one of the lowest (Jan – May) and the lowest (May – Dec) among its competitors.

Source: Yahoo Finance

DECISION DRIVERS

• Strengths– Positioned to take advantage of deep water and ultra-deep water opportunities

with forthcoming drillships and semisubmersibles– Deepwater and ultra-deep water are the areas with the highest current utilization

rate• Concerns– Slow down in emerging market GDP growth – Alternative sources of energy and oil– Large forthcoming capital expenditures for fleet maintenance/upgrade– Stock performance vs. comparables show poor performance– Highly competitive and cyclical industry

26FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

RECOMMENDATION

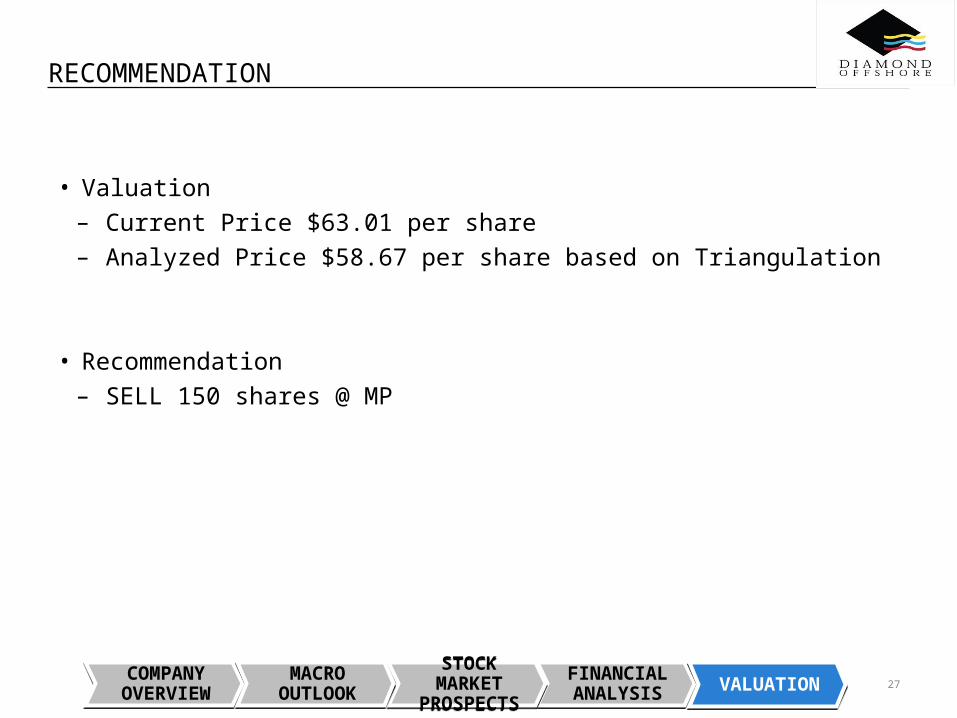

• Valuation– Current Price $63.01 per share– Analyzed Price $58.67 per share based on Triangulation

• Recommendation– SELL 150 shares @ MP

27FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

COMPANY OVERVIEWCOMPANY OVERVIEW

STOCK MARKET

PROSPECTS

STOCK MARKET

PROSPECTS

MACRO OUTLOOK

MACRO OUTLOOK VALUATIONVALUATION

QUESTIONS?

28