d9 audit report izicredit georgia eng.pdf

TRANSCRIPT

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 1/20

Microfinance Organization

“Easycred Georgia “LLC

FI NANCIAL STATEM ENTS

F or the year ending D ecember 31, 2014

With

I NDEPENDENT AUDI TORS ’ REPORT

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 2/20

finansuri mar vis jgufi

balanCivaZis q 20177 Tbilisi, saqarTvelotel.: (995) (322) 47 09 00faqsi: (995) (322) 36 33 11el-fosta: [email protected]

FINANCIAL MANAGEMENT GROUP2 str. Balanchivadze0177 Tbilisi, GeorgiaTel.: (995) (322) 47 09 00Fax: (995) (322) 36 33 11E-mail: [email protected]

INDEPENDENT AUDITOR’S REPORT

Report on the financial statements

1. We have audited the accompanying financial statements on pages 4 to 7 of microfinanceorganization “ EasyCred Georgia ” LLC. (hereinafter as – “the Company”), w hich comprise the

balance sheet as of December 31, 2014, the income statement, statement of changes in equityand cash flow statement for the period then ended and a summary of significant accounting

policies and other explanatory notes.

Management’s responsibility for the financial statements

2. Management is responsible for the preparation and fair presentation of these financialstatements in accordance with International Financial Reporting Standards. This responsibilityincludes: designing, implementing and maintaining the internal control relevant to preparationand fair presentation of financial statements that are free from material misstatement, whetherdue to fraud or error; selecting and applying appropriate accounting policies and makingaccounting estimates that are reasonable in the circumstances.

Auditor’s responsibi lity

3. Our responsibility is to express an opinion on these financial statements based on our audit. Weconducted our audit in accordance with International Standards on Auditing. Those standardsrequire that we comply with ethical requirements and plan and perform the audit to obtainreasonable assurance whether the financial statements are free from material misstatement.

4. An audit involves performing procedures to obtain audit evidence about the amounts anddisclosures in the financial statements. The proce dures selected depend on the auditor’s

judgment, including the assessment of the risk of material misstatements of the financialstatements whether due to fraud or error. In making those risk assessments, the auditorconsiders internal control relevant to the Company’s preparation and fair presentation of thefinancial statements in order to design audit procedures that are appropriate in thecircumstances, but not for the purpose of expressing an opinion on the effectiveness of the

Company’s internal contr ol. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well asevaluating the overall presentation of the financial statements.

5. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit.

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 3/20

finansuri mar vis jgufi

balanCivaZis q 20177 Tbilisi, saqarTvelotel.: (995) (322) 47 09 00faqsi: (995) (322) 36 33 11

el-fosta: [email protected]

FINANCIAL MANAGEMENT GROUP2 str. Balanchivadze0177 Tbilisi, GeorgiaTel.: (995) (322) 47 09 00Fax: (995) (322) 36 33 11

E-mail: [email protected]

Opinion

6. In our opinion, the accompanying financial statements give a true and fair view of the financial position of the Company as of December 31, 2014 and of its financial performance and its cashflows for the year then ended in accordance with International Financial Reporting Standards.

Intended use of the report 7. The report is intended solely for the use of company and shall not be made available for others

or used for other purposes unless our prior written consent.

Financial Management Group

Member of HLB International

Tbilisi, GeorgiaOctober 30, 2015

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 4/20

L LC E ASYCRED G EORGIA

Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Page 4 of 20

NOTES 12/31/2013 12/31/2014

ASSETSCash and cash equivalents 4 441,358 310,335Loans to Customers 5 8,746,834 7,962,966Investment in subsidiary 6 310,240 282,652Accounts Receivables 7 1,719 78,490Other Assets 8 53,353 45,826Advances 9 100,980 (2,115)Mortgage property 10 1,383,226 322,930Inventory 11 36,610 27,928Prepaid Income Tax 12 146,407 -Prepaid Tax 12 85,651 528,568Deferred tax assets 12 47,615 -Hotel Project 13 - 4,202,070Fixed Assets 14 1,686,247 1,791,468Intangible Assets 15 9,674 20,696

Total Current Assets 13,049,915 15,571,812

Total Assets 13,049,915 15,571,812

Liabilities

Loans and borrowings 16 6,485,966 9,550,546Interest payable 17 138,310 175,097Accounts Payable 18 2,615 97,309Wages payable 19 244 243Tax payable 20 180,901 189,710Deferred tax liabilities 20 4,097 6,410

Total Liabilities 6,812,133 10,019,316

Capital

Share capital 4,501,721 4,501,721Total Rezervs 19,096 17,331Retained earnings (last yesr) 810,607 784,448Retained earnings 906,357 248,996

Total Capital 6,237,781 5,552,496

Total Capital and Liabilities 13,049,914 15,571,812

Financial statements approved by management

Guram Kandelaki Arsen Demurashvili Director Financial Manager

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 5/20

L LC E ASYCRED G EORGIA

Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Page 5 of 20

Note12 months, 2013year

12 months, 2014year

Interest income 21 2,622,100 2,518,446

Interest expense 21 (775,422) (1,038,639)

Net Interest Income 1,846,678 1,479,807

Other operating income 22 431,859 976,057Gain from exchange rate conversion 22 667,528 574,128

Fee and commission income 22 349,943 370,646

Operating Income 1,449,330 1,920,831

Non Operating Income from Hotel 23 - 1,317

Non operating Income 1,449,330 1,922,148

Loss from exchange rate conversion 24 (533,309) (1,041,503)

Other general administrative expenses 25 (1,696,398) (2,067,515)

Profit before income tax 1,066,302 292,937

Income Tax expense (159,945) (43,940)

Net Income 906,357 248,996

Financial statements approved by management

Guram Kandelaki Arsen Demurashvili Director Financial Manager

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 6/20

L LC E ASYCRED G EORGIA

Financial Statements for the year ended December 31, 2013 Amount expressed in Georgian Lari unless otherwise stated

Page 7 of 20

Cash Flow Statement 31.12.2013 12/31/2014Period Profit/Loss 1,066,302 292,937Depreciation (159,945) (43,940)

Operating cash flows before working capital changes 906,357 248,996

Decrease (increase) in Loans to Customers (1,635,725) 783,869Decrease (increase) in Investment in subsidiary (13,158) 27,588Decrease (increase) in accounts receivables 1,837 (76,771)

Decrease (increase) in other Assets 19,487 7,527Decrease (increase) in Advances (75,417) 103,096Decrease (increase) in mortgage property (932,398) 1,060,296Decrease (increase) in Inventory (36,438) 8,682Decrease (increase) in Income Tax (146,407) 146,407Decrease (increase) in Deferred tax assets (47,615) 47,615Decrease (increase) in Prepaid Tax (85,576) (442,917)Decrease (increase) in hotel project - (4,202,070)Acquisition of fixed assets (837,582) (105,220)Acquisition of intangible assets 29,102 (11,022)Decrease (increase) in Loans and borrowings 2,654,774 3,064,580Decrease (increase) in Interest payable 107,562 36,787Increase (decrease) in accounts payable (101,844) 94,694Decrease (increase) in wages payable (1,656) (1)Increase (decrease) in taxes payable 130,539 8,809

Decrease (increase) in deferred tax liabilities - 2,313

Total cash flows from operating activities (64,157) 803,258

Net cash flows from financing activitiesDecrease (increase) in Share capital 847,720 -Decrease (increase) in reserves (1,765)Correction (2,692) (41,452)Payment of dividends (546,035) (891,065)

Net cash flows from financing activities 298,993 (934,282)

Net increase (decrease) in cash and cash equivalents 234,835 (131,024)

Cash and cash equivalents at the beginning of the period206,523 441,358

Cash and Cash Equivalents at the end of the period441,359 310,335

Financial statements approved by management

Guram Kandelaki Arsen Demurashvili Director Financial Manager

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 7/20

L LC E ASYCRED G EORGIA

Financial Statements for the year ended December 31, 2013 Amount expressed in Georgian Lari unless otherwise stated

Share capital ReservesRetainedearnings

Paymentofdividends Total

Statement of changes inequity for the yearended 31 December2013 3,654,001 19,096 1,359,334 - 5,032,431

Retained earnings 906,357 906,357

Payment of dividends (546,035) (546,035)

Correction (2,692) (2,692)

Increase of Share capital 847,720 847,720Statement of changes inequity for the yearended 31 December2013 4,501,721 19,096 2,262,999 (546,035) 6,237,781

Retained earnings 248,996 248,996

Payment of dividends - (891,065) (891,065)

Correction (41,452) (41,452)

Reduction of reserves (1,765) (1,765)Statement of changes inequity for the yearended 31 December2014 4,501,721 17,331 2,470,543 (1,437,100) 5,552,495

Financial statements approved by management

Guram Kandelaki Arsen Demurashvili Director Chief Accountant

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 8/20

L LC E ASYCRED G EORGIA

Notes to the Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Page 20 of 20

N OTES TO THE F INANCIAL S TATEMENTS

Note 1- GENERAL INFORMATION

Microfi nance organization “ EasyCred Georgia “LLC was founded in November 21, 2008and was registered by Tbilisi tax Inspection with tax payer code: 205267584. The owners of thecompany are: Kakhaber Kakhiani 15 %; Laerti Zubadalashvili 76%; Eliza Daushvili 9%.

Main activities or our company are currency exchange, pawn services, short-term loans,long-term loans, mortgage loans, faster money transfers in Georgia.

Note 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The principal accounting policies applied in the preparation of these financial statementsare set out below. These policies have been consistently applied to the period presented, unlessotherwise stated.

2.1 Basis of presentation

The accompanying financial statements have been prepared in accordance withInternational Financial Reporting Standards (“IFRS”) and Interpretations issued by the InternationalAccounting Standards Board.

The Company maintains its accounting records in accordance with Georgian accounting

and tax legislation. These financial statements have been prepared from those accounting recordsand adjusted as necessary in order to comply with IFRS. The Company’s financial year -end is onDecember 31.

2.2 Foreign currency translation

(a) Functional and presentation currency

Items included in the financial statements of the Company are measured using the currencyof the primary economic environment in which the entity operates (“the functional currency”). Thefinancial statements are presented in Georgian Lari (“GEL”), which is the Company’s functionaland presentation currency.

(c) Foreign currency transactions and balances

Foreign currency transactions are translated into the functional currency using the exchangerates prevailing at the dates of the transactions. Monetary assets and liabilities denominated inforeign currencies at the reporting date are retranslated to the functional currency at the exchangerate at that date. The foreign currency gain or loss on monetary items is the difference betweenamortized cost in the functional currency at the beginning of the year, adjusted for effective interestand payments during the year, and the amortized cost in foreign currency translated at the exchangerate at the end of the year.

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 9/20

L LC E ASYCRED G EORGIA

Notes to the Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Page 10 of 20

Non-monetary assets and liabilities that are measured at fair value in a foreign currency areretranslated to the functional currency at the exchange rate at the date that the fair value wasdetermined. Non-monetary items that are measured based on historical cost in a foreign currencyare translated using the exchange rate at the date of the transaction.

(c) Foreign currency transactions and balances (continued)

Foreign currency is translated at the National Bank of Georgia rate of exchange at the given date(year end for the statements). According to an official information from National Bank of Georgia therate of Exchange of GEL to USD and EUR were:

The Exchange Rates at 12/31/20141.8636 GEL/USD2.2656 GEL / EUR

2.3 Property, plant and equipment

Buildings comprise mainly factories, retail outlets and offices. Buildings are shown at fairvalue, (valuation by external independent values has not yet been provided) less subsequentdepreciation for buildings. Valuations will be performed with sufficient regularity to ensure that thefair value of a revalued asset does not differ materially from its carrying amount. Any accumulateddepreciation at the date of revaluation is eliminated against the gross carrying amount of the asset,and the net amount is restated to the revalued amount of the asset. All other property, plant andequipment is stated at historical cost less depreciation. Historical cost includes expenditure that is

directly attributable to the acquisition of the items. Cost may also include transfers from equity ofany gains/losses on qualifying cash flow hedges of foreign currency purchases of property, plantand equipment.

Subsequent costs are included in the asset’s carrying amount or recognized as a separateasset, as appropriate, only when it is probable that future economic benefits associated with the itemwill flow to the Company and the cost of the item can be measured reliably. The carrying amount ofthe replaced part is derecognized. All other repairs and maintenance are charged to the incomestatement during the financial period in which they are incurred

Depreciation on other assets is calculated using the straight-line method to allocate their costor revalued amounts to their residual values over their estimated useful lives.

The assets’ residu al values and useful lives are reviewed, and adjusted if appropriate, at theend of each reporting period.

An asset’s carrying amount is written down immediately to its recoverable amount if theasset’s carrying amount is greater than its estimated recov erable amount.

Gains and losses on disposals are determined by comparing the proceeds with the carryingamount and are recognized within ‘Other (losses)/gains – net’ in the income statement.

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 10/20

L LC E ASYCRED G EORGIA

Notes to the Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Page 11 of 20

2.4 Intangible assets

(a) Computer software

Costs associated with maintaining computer software programs are recognized as an expenseas incurred.

2.5 Impairment of non-financial assets

Intangible assets that have an indefinite useful life or intangible assets not ready to use arenot subject to amortization and are tested annually for impairment. Assets that are subject toamortization are reviewed for impairment whenever events or changes in circumstances indicatethat the carrying amount may not be recoverable.

An impairment loss is recognized for t he amount by which the asset’s carrying amountexceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value lesscosts of disposal and value in use. For the purposes of assessing impairment, assets are grouped atthe lowest levels for which there are largely independent cash inflows (cash-generating units). Priorimpairments of nonfinancial assets (other than goodwill) are reviewed for possible reversal at eachreporting date.

2.6 Financial assets

2.6.1 Classification

The Company classifies its financial assets in the following categories: at fair value through profit or loss, loans and receivables. The classification depends on the purpose for which thefinancial assets were acquired. Management determines the classification of its financial assets atinitial recognition.

(a) Financial assets at fair value through profit or loss

Financial assets at fair value through profit or loss are financial assets held for trading. Afinancial asset is classified in this category if acquired principally for the purpose of selling in theshort term. Derivatives are also categorized as held for trading unless they are designated as hedges.Assets in this category are classified as current assets if expected to be settled within 12 months,otherwise they are classified as non-current.

(b) Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They are included in current assets, except formaturities greater than 12 months after the end of the reporting period. These are classified as non-current assets. The group’s loans and receivables comprise ‘trade and other receivables’ and ‘cashand cash e quivalents’ in the balance sheet.

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 11/20

L LC E ASYCRED G EORGIA

Notes to the Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Page 12 of 20

2.6.2 Recognition and measurement

Regular purchases and sales of financial assets are recognized on the trade-date – the date onwhich the group commits to purchase or sell the asset. Investments are initially recognized at fairvalue plus transaction costs for all financial assets not carried at fair value through profit or loss.Financial assets carried at fair value through profit or loss are initially recognized at fair value, andtransaction costs are expensed in the income statement. Financial assets are derecognized when therights to receive cash flows from the investments have expired or have been transferred and theCompany has transferred substantially all risks and rewards of ownership. Available-for-salefinancial assets and financial assets at fair value through profit or loss are subsequently carried atfair value. Loans and receivables are subsequently carried at amortized cost using the effectiveinterest method.

2.7 Offsetting financial instruments

Financial assets and liabilities are offset and the net amount reported in the balance sheetwhen there is a legally enforceable right to offset the recognized amounts and there is an intentionto settle on a net basis or realize the asset and settle the liability simultaneously.

2.8 Impairment of financial assets

(a) Assets carried at amortized cost

The Company assesses at the end of each reporting period whether there is objective

evidence that a financial asset or group of financial assets is impaired. A financial asset or a groupof financial assets is impaired and impairment losses are incurred only if there is objective evidenceof impairment as a result of one or more events that occurred after the initial recognition of the asset(a ‘loss event’) and that loss event (or events) has an impact on the estimated future cash flows ofthe financial asset or group of financial assets that can be reliably estimated.

Evidence of impairment may include indications that the debtors or a group of debtors isexperiencing significant financial difficulty, default or delinquency in interest or principal

payments, the probability that they will enter bankruptcy or other financial reorganization, andwhere observable data indicate that there is a measurable decrease in the estimated future cashflows, such as changes in arrears or economic conditions that correlate with defaults.

For loans and receivables category, the amount of the loss is measured as the difference

between the asset’s carrying amount and the present value of estimated future cash flows (excludingfuture credit losses that have not been incurred) discounted at the financial asset’s original effectiveinterest rate. The carrying amount of the asset is reduced and the amount of the loss is recognized inthe consolidated income statement. If a loan or held-to-maturity investment has a variable interestrate, the discount rate for measuring any impairment loss is the current effective interest ratedetermined under the contract. As a practical expedient, the Company may measure impairment onthe basis of an instrument’s fair value using an observable market price.

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognized (such as animprovement in the debtor’s credit rating), the reversal of the previously recognized impairmentloss is recognized in the income statement.

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 12/20

L LC E ASYCRED G EORGIA

Notes to the Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Page 13 of 20

2.9 Trade receivables

Trade receivables are amounts due from customers for merchandise sold or services performed in the ordinary course of business. If collection is expected in one year or less (or in thenormal operating cycle of the business if longer), they are classified as current assets. If not, theyare presented as non-current assets.

Trade receivables are recognized initially at fair value and subsequently measured atamortized cost using the effective interest method, less provision for impairment.

2.10 Cash and cash equivalents

In the statement of cash flows, cash and cash equivalents includes cash in hand, depositsheld at call with banks, other short-term highly liquid investments with original maturities of three

months or less and bank overdrafts. In the consolidated balance sheet, bank overdrafts are shownwithin borrowings in current liabilities.

2.11 Share capital

Where any company purchases the company’ s equity share capital, the consideration paid,including any directly attributable incremental costs (net of income taxes) is deducted from equityattributable to the company’s equity holders until the shares are cancelled.

2.12 Dividends

In accordance with Georgian legislation the Company’s distributable reserves are limited tothe balance of retained earnings as recorded in the Company’s statutory financial stat ements prepared in accordance with IFRSs.

2.14 Borrowings

Borrowings are recognized initially at fair value, net of transaction costs incurred.Borrowings are subsequently carried at amortized cost; any difference between the proceeds (net oftransaction costs) and the redemption value is recognized in the income statement over the period ofthe borrowings using the effective interest method.

Fees paid on the establishment of loan facilities are recognized as transaction costs of the

loan to the extent that it is probable that some or all of the facility will be drawn down. In this case,the fee is deferred until the draw-down occurs. To the extent there is no evidence that it is probablethat some or all of the facility will be drawn down, the fee is capitalized as a pre-payment forliquidity services and amortized over the period of the facility to which it relates.

2.15 Borrowing costs

General and specific borrowing costs directly attributable to the acquisition, construction or production of qualifying assets, which are assets that necessarily take a substantial period of time toget ready for their intended use or sale, are added to the cost of those assets, until such time as theassets are substantially ready for their intended use or sale

All other borrowing costs are recognized in profit or loss in the period in which they are incurred.

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 13/20

L LC E ASYCRED G EORGIA

Notes to the Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Page 14 of 20

2.16 Current Tax

Tax expense comprises current and deferred tax. Current tax and deferred tax is recognizedin profit or loss except to the extent that it relates to a business combination, or items recognized

directly in equity or in other comprehensive income.

Current tax is the expected tax payable or receivable on the taxable income or loss for theyear, using tax rates enacted or substantively enacted at the reporting date, and any adjustment totax payable in respect of previous years. Current tax payable also includes any tax liability arisingfrom the declaration of dividends.

2.17 Profit tax

It is taxable at a rate of 15% in accordance with Georgian regulatory legislation on taxation.Profit tax expense is calculated and accrued for in the financial statements on the basis of

information available at the moment of the preparation of the financial statements, and estimates ofincome tax performed by the management in accordance with Georgian regulatory legislation ontaxation.

Deferred profit tax is provided in full, using the liability method, on temporary differencesarising between the tax bases of assets and liabilities and their carrying amounts in the consolidatedfinancial statements. Deferred income tax is determined using Georgian tax rates (and laws) thathave been enacted or substantially enacted by the balance sheet date and are expected to apply whenthe related deferred profit tax asset is realized or the deferred income tax liability is settled.

Deferred profit tax assets are recognized to the extent that it is probable that future taxable profit will be available against which the temporary differences can be utilized.

According to Georgian legislation, tax losses are carried forward for 5 years.

2.18 Income and expense recognition

Interest income and expense are recognized in profit or loss using the effective interestmethod. Loan origination fees, loan servicing fees and other fees that are considered to be integralto the overall profitability of a loan, together with the related transaction costs, are deferred andamortized to interest income over the estimated life of the financial instrument using the effectiveinterest method. Other fees, commissions and other income and expense items are recognized in

profit or loss when the corresponding service is provided. Payments made under operating leasesare recognized in profit or loss on a straight-line basis over the term of the lease. Lease incentivesreceived are recognized as an integral part of the total lease expense, over the term of the lease.

NOTE 3 - FINANCIAL RISK MANAGEMENT

3.1 Financial risk factors

The group’s activities expose it to a variety of financial risks : market risk (includingcurrency risk, fair value interest rate risk, cash flow interest rate risk and price risk), credit risk andliquidity risk. Risk management is carried out by a financial department.

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 14/20

L LC E ASYCRED G EORGIA

Notes to the Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Page 15 of 20

(a) Credit risk

Credit risk is managed on Company basis, except for credit risk relating to accountsreceivable balances. Credit risk arises from cash and cash equivalents, derivative financial

instruments and deposits with banks and financial institutions, as well as credit exposures towholesale customers, including outstanding receivables and committed transactions. If wholesalecustomers are independently rated, these ratings are used. If there is no independent rating, riskcontrol assesses the credit quality of the customer, taking into account its financial position, pastexperience and other factors. Individual risk limits are set based on internal or external ratings inaccordance with limits set by the board.

(b) Liquidity risk

Cash flow forecasting is performed in the operating entity and aggregated by companyfinance. Company finance monitors rolling forecasts of the Company ’s liquidity requirements toensure it has sufficient cash to meet operational needs while maintaining sufficient headroom on itsundrawn committed borrowing facilities at all times so that the Company does not breach

borrowing limits or covenants (where applicable) on any of its borrowing facilities. Suchforecasting takes into consideration the Company ’s debt financing plans, covenant compliance,compliance with internal balance sheet ratio targets and, if applicable external regulatory or legalrequirements – for example, currency restrictions.

3.2 Capital management

The Company ’s objectives when managing capital are to safeguard the Company ’s ability tocontinue as a going concern in order to provide returns for shareholder and benefits for otherstakeholders and to maintain an optimal capital structure to reduce the cost of capital

In order to maintain or adjust the capital structure, the Company may adjust the amount ofdividends paid to shareholder, return capital to shareholder.

Consistent with others in the industry, the Company monitors capital on the basis of thegearing ratio. This ratio is calculated as net debt divided by total capital. Net debt is calculated astotal borrowings (including ‘current and non -current borrowings’ as shown in the balance sheet)less cash and cash equivalents.

Note 4 -Cash and Cash Equivalents 12/31/2013 12/31/2014Cash in banks 187,152 235,904

Total cash in banks 187,152 235,904

Petty cash 254,207 74,431

Total Cash and Cash Equivalents 254,207 74,431

Total Cash and Cash Equivalents441,358 310,335

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 15/20

L LC E ASYCRED G EORGIA

Notes to the Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Page 16 of 20

Note 5 - Loans to Customers12/31/2013 12/31/2014

Short-Term loans to customers 2,070,970 2,832,387

Gold Pawn 6,084 6,530Short-term Loans to Service industry 72,991 19,864Short-term loans to other industry - -Long-Term loans to customers 5,972,948 4,423,546Long-term Loans to Service industry 141,872 174,542Long-term Loans to Manufacturing industry 67,599 45,181Overdue Debts 395,106 620,886Accrued interest receivable 429,241 626,048Accrued interest receivable from money transfers 1 8Reserve (409,976) (786,026)Total Loans to Customers 8,746,835 7,962,965

Note 6 - Investment in subsidiary12/31/2013 12/31/2014

Investment in subsidiary 310240 282652Total Investment in subsidiary 310,240 282,652

Note 7 - Accounts Receivable12/31/2013 12/31/2014

Accounts Receivable 1718 67129

Other receivable 0 11361Total Accounts Receivable 1,719 78,490

Note 8 - Other Assets12/31/2013 12/31/2014

Money transfers 1 9467Other Assets 21193 30153Money transfers in USD 32153 6206

Total Other Assets 53,347 45,826

Note 9 -Advances

12/31/2013 12/31/2014

Advances of Mortgage property 25413 -2115

Advances to suppliers 75567

Total Advances 100,980 (2,115)

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 16/20

L LC E ASYCRED G EORGIA

Notes to the Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Page 17 of 20

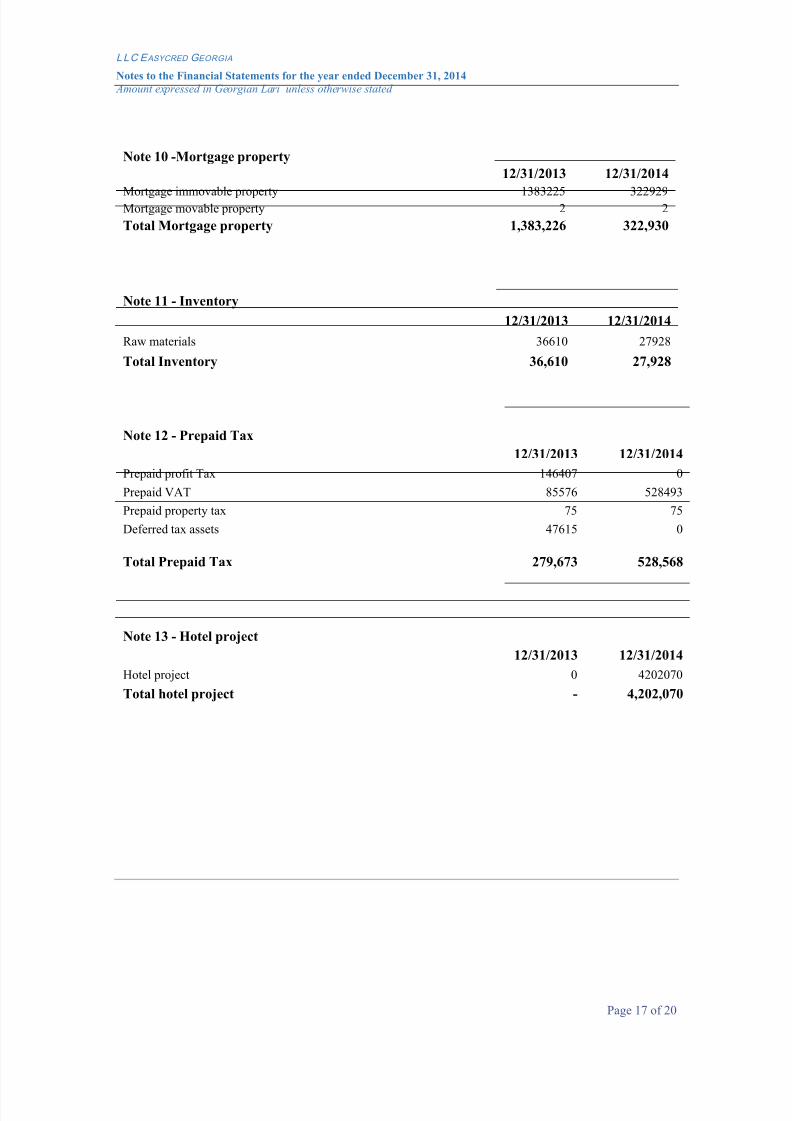

Note 10 -Mortgage property12/31/2013 12/31/2014

Mortgage immovable property 1383225 322929Mortgage movable property 2 2Total Mortgage property 1,383,226 322,930

Note 11 - Inventory12/31/2013 12/31/2014

Raw materials 36610 27928

Total Inventory 36,610 27,928

Note 12 - Prepaid Tax12/31/2013 12/31/2014

Prepaid profit Tax 146407 0

Prepaid VAT 85576 528493Prepaid property tax 75 75

Deferred tax assets 47615 0

Total Prepaid Tax 279,673 528,568

Note 13 - Hotel project12/31/2013 12/31/2014

Hotel project 0 4202070

Total hotel project - 4,202,070

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 17/20

LL C C REDIT S ERVICE +

Notes to the Financial Statements for the year ended December 31, 2013 Amount expressed in Georgian Lari unless otherwise state d

Page 20 of 20

Note 14 - Fixed Assets

Land Buildings Office Supplies,Advertising Materials Furniture Other Fixed

Assets Generator and other

Beginning BalanceBalance 2012 Year 31 December 114,032 657,622 21,694 36,281 19,271 (234)

Additions in 2013 Year 585,314 598,396 9,966 5,600 - -

Write-Offs in 2013 Year - (334,958) (170)

Balance 2013 31 December 699,346 921,059 31,490 41,881 19,271 (234)

Accumulated Depreciation - (22,872) (3,665) (30) -

Balance 2013 Year 31 December 699,346 898,187 31,490 38,216 19,241 (234)

Additions in 2014 Year 1,210,928 2,984,925 174,414 137,977 - 71,422

Write-Offs in 2014 Year (497,212) (3,645,960) (161,682) (122,656) - (1)

Accumulated Depreciation - (11,436) (23,633) (11,867) - -

Balance 2014 31 December 1,413,062 225,717 20,590 41,670 19,241 71,187

Balance 2013 31 December 699,346 898,187 31,490 38,216 19,241 (234)

Balance 2014 31 December 1,413,062 225,717 20,590 41,670 19,241 71,187

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 18/20

L LC C REDIT S ERVICE +

Notes to the Financial Statements for the year ended December 31, 2013 Amount expressed in Georgian Lari unless otherwise stated

Page 20 of 20

Note 15 - Intangible Assets

IntangibleAssets

Beginning BalanceBalance 2012 Year 31 December 38,776Additions in 2013 Year 67,977Write-Offs in 2013 Year (97,079)

Balance 2013 31 December 9,674Accumulated Depreciation -Balance 2013 Year 31 December 9,674Additions in 2014 Year 11,022Accumulated Depreciation -

Balance 2014 31 December 20,696

Residual ValueBalance 2013 31 December 9,674Balance 2014 31 December 20,696

Note 16 - Loans12/31/2013 12/31/2014

Loans from financial institutions 2,973,578 5,129,926

Loans from individuals 3,512,389 4,420,619

Total Loans 6,485,966 9,550,546

Note 17 - Interest payable12/31/2013 12/31/2014

Interest payable from non-bank loans 8,186 5,535

Interest payable from bank loans 26,720 32,102

Interest payable on personal loans 103,405 137,460

Total Interest payable 138,311 175,097

Note 18 - Accounts Payable12/31/2013 12/31/2014

Accounts Payable 0 92420

Liabilities from money transfer 2615 4889

Total Accounts Payable 2,615 97,309

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 19/20

L LC E ASYCRED G EORGIA

Notes to the Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Page 20 of 20

Note 19 -Wages payable

12/31/2013 12/31/2014

Wages payable 240 196Dividends payable 4 47

Wages payable 244 243

Note 20 - Taxes Payable12/31/2013 12/31/2014

Profit tax payable 208316 80849VAT payable -6530 112445Income tax payable -29465 -40488Property tax payable 8998 36817Land tax payable -418 2399Deferred tax liability 4097 4097

Total taxes payable 184,998 196,120

Note 21 -Interest Income and Expenses12/31/2013 12/31/2014

Interest Income

Interest Income from resident bank accounts 1,014 819Interest Income from short-term loans 763,685 740685Interest income from loans to legal entities 30,521 27126Interest income from long-term loans 1,784,010 1681686Interest income from long-term loans to legal entities 42,687 68130Other interest income 182

Total Interest Income 2,622,100 2,518,446

Interest ExpensesInterest expenses on personal loans (434,456) (666,514)

Interest expenses from bank loans (340,966) (372,125)Total Interest Expenses (775,422) (1,038,639)

Net Income 1,846,678 1,479,807

Note 22 -Operating Income

12/31/2013 12/31/2014

Other operating income 431,859 976,057

Gain from exchange rate conversion 667,528 574,128

Fee and commission income 349,943 370,646

Total Operating Income 1,449,330 1,920,831

7/21/2019 D9 Audit Report Izicredit Georgia Eng.pdf

http://slidepdf.com/reader/full/d9-audit-report-izicredit-georgia-engpdf 20/20

L LC E ASYCRED G EORGIA

Notes to the Financial Statements for the year ended December 31, 2014 Amount expressed in Georgian Lari unless otherwise stated

Note 23 -Non Operating Income

12/31/2013 12/31/2014

Non-Operating income from Hotel - 1,317

Total Non-Operating Income - -

Note 24 - Non Operating Loss12/31/2013 12/31/2014

Loss from exchange rate conversion (533,309) 1,041,503

Total Non-Operating Loss (533,309) 1,041,503

Note 24 - Operating Expenses12/31/2013 12/31/2014

Bank commission expense 23 1,364Other commission expense 7,563 9,423Loss from other operations 345,176 -Legal expense 37,988 2,425Insurance expense 9,241 11,052Rent expense 29,412 28,919

Salary expenses 799,979 1,005,277Advertising costs 65,452 18,841Representation expense 11,886 10,477Charity expense 11,677 1,020Business travel - 3,999Depreciation 26,566 60,238Vehicle expenses 22,483 29,337Utilities expense 10,264 16,156Security expense 7,095 42,454Consulting and audit fees 24,730 21,470

Office supplies expense 2,145 5,176

Other administrative expense 284,717 799,886Total Operating Expenses 1,696,398 2,067,515

Note 26 – Profit Tax

Company had gain for the audit period and significantly have accrued profit tax. The Company'smanagement is not aware of any circumstances, which may give rise to a potential material liabilityin this respect.

End of document

* * * * *