danske invest danish mortgage bond fund

DESCRIPTION

Danske Invest Danish Mortgage Bond Fund. Status and Outlook. 8 February 2011. Return against Competitors. Performance of the Danish Mortgage Bond Fund. Volatility 3,77 Sharpe Ratio 0,77 Ratio of positive returns 67,9%. Duration of segments in the Danish Bond Market. - PowerPoint PPT PresentationTRANSCRIPT

Return on Knowledge

Danske Invest Danish Mortgage Bond FundStatus and Outlook

8 February 2011

2

Return against Competitors

19-04-23

Danish Fixed Income Performance Overview - Mutual Funds

Source: IFR/Bloomberg/DanskeInvestOther funds YTD Perf.* Name 1M 1Y 3Y 5YLuxembourg 1 5,71% Danske Invest - Danish Mortgage Bond -0,2% 5,7% 21,3% 20,3%

2,84% Nordea 1 SICAV - Danish Bond Fund -0,9% 2,8% 16,1% 17,0%

2 4,52% Danske Invest - Danish Bond -0,3% 4,5% 17,2% 19,0%

3,51% Nordea 1 SICAV - Danish Mortgage Bond Fund -0,5% 3,5% 17,3% 19,2%

2010december

Bloomberg / IFROther funds YTD Name AUM ISIN 1M 1Y 3Y 5Y

Luxembourg 3 -0,84% Danske Invest - Danish Mortgage Bond 1147m DKK LU0080347536 -1,2% 3,7% 17,5% 20,1%

-1,00% Nordea 1 SICAV - Danish Bond Fund 146m DKK LU0064319766 -1,4% 1,0% 12,0% 16,8%

2 -0,69% Danske Invest - Danish Bond 361m DKK LU0012089180 -0,9% 2,9% 14,1% 18,5%

-0,63% Nordea 1 SICAV - Danish Mortgage Bond Fund 2756m DKK LU0076315968 -1,1% 1,9% 13,7% 19,1%

4. feb. 2011

3

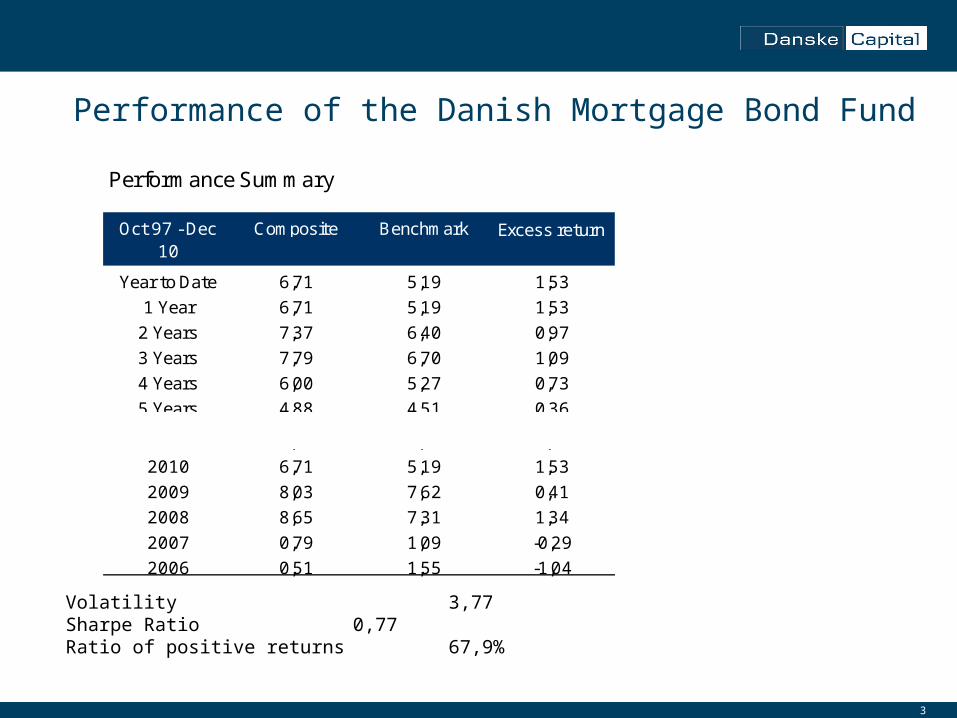

Performance of the Danish Mortgage Bond Fund

Oct 97 - Dec 10

J ahresvolatilität 3,77

Tracking Error (XS) 1,25

Info. Ratio (XS) 0,15

Sharpe Ratio 0,77

Ratio of Positive Return 67,9%

Performance Summary

Composite Rendite (EUR)

Benchmark rendite*

Excess return

Year to Date 6,71 5,19 1,53

1 Year 6,71 5,19 1,53

2 Years 7,37 6,40 0,97

3 Years 7,79 6,70 1,09

4 Years 6,00 5,27 0,73

5 Years 4,88 4,51 0,36Composite Data 6,06 5,87 0,19

2010 6,71 5,19 1,53

Year to Date 2008 2009 8,03 7,62 0,41

Anzahl Konti 1 1 2008 8,65 7,31 1,34

152,45 55,87 2007 0,79 1,09 -0,29

Dispersion N/A N/A 2006 0,51 1,55 -1,04

Oct 97 - Dec 10

-6

-4

-2

0

2

4

6

8

10

Q4 10Q3 09Q2 08Q1 07Q4 05Q3 04Q2 03Q1 02Q4 00Q3 99Q2 98

Quarterly return (pct.)

Nykredits realkreditobligationsindex Composite Oct 97 - Dec 10

J ahresvolatilität 3,77

Tracking Error (XS) 1,25

Info. Ratio (XS) 0,15

Sharpe Ratio 0,77

Ratio of Positive Return 67,9%

Performance Summary

Year to Date 6,71 5,19 1,53

1 Year 6,71 5,19 1,53

2 Years 7,37 6,40 0,97

3 Years 7,79 6,70 1,09

4 Years 6,00 5,27 0,73

5 Years 4,88 4,51 0,36Composite Data 6,06 5,87 0,19

2010 6,71 5,19 1,53

Year to Date 2008 2009 8,03 7,62 0,41

Anzahl Konti 1 1 2008 8,65 7,31 1,34

152,45 55,87 2007 0,79 1,09 -0,29

Dispersion N/A N/A 2006 0,51 1,55 -1,04*Nykredits realkreditobligationsindex

-6

-4

-2

0

2

4

6

8

10

Q4 10Q3 09Q2 08Q1 07Q4 05Q3 04Q2 03Q1 02Q4 00Q3 99Q2 98

Quarterly return (pct.)

Nykredits realkreditobligationsindex Composite

Volatility 3,77Sharpe Ratio 0,77Ratio of positive returns 67,9%

4

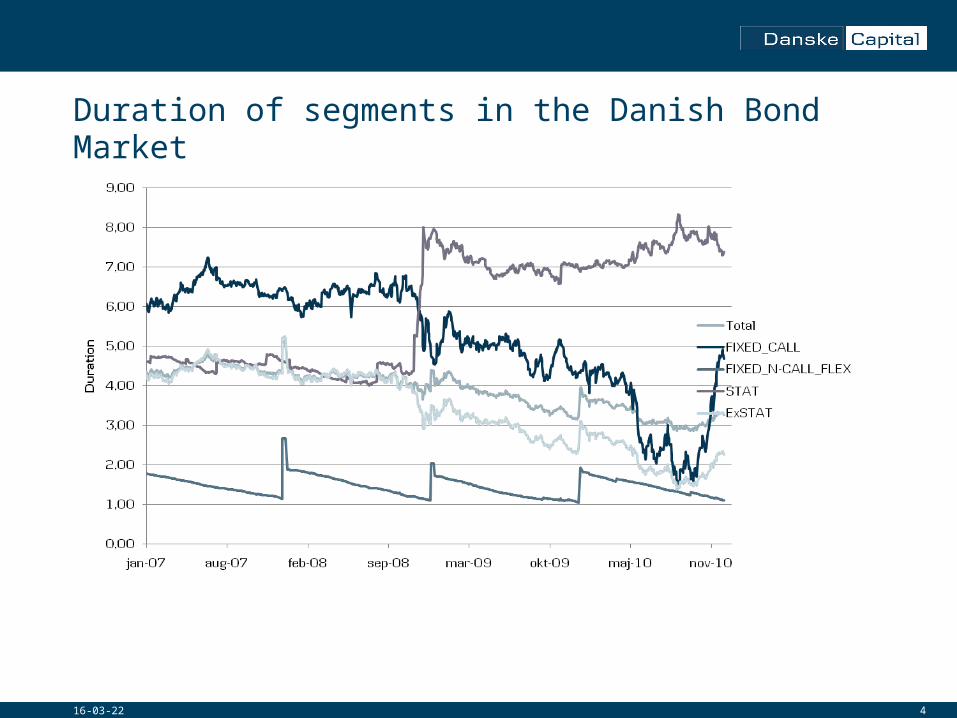

Duration of segments in the Danish Bond Market

19-04-23

5

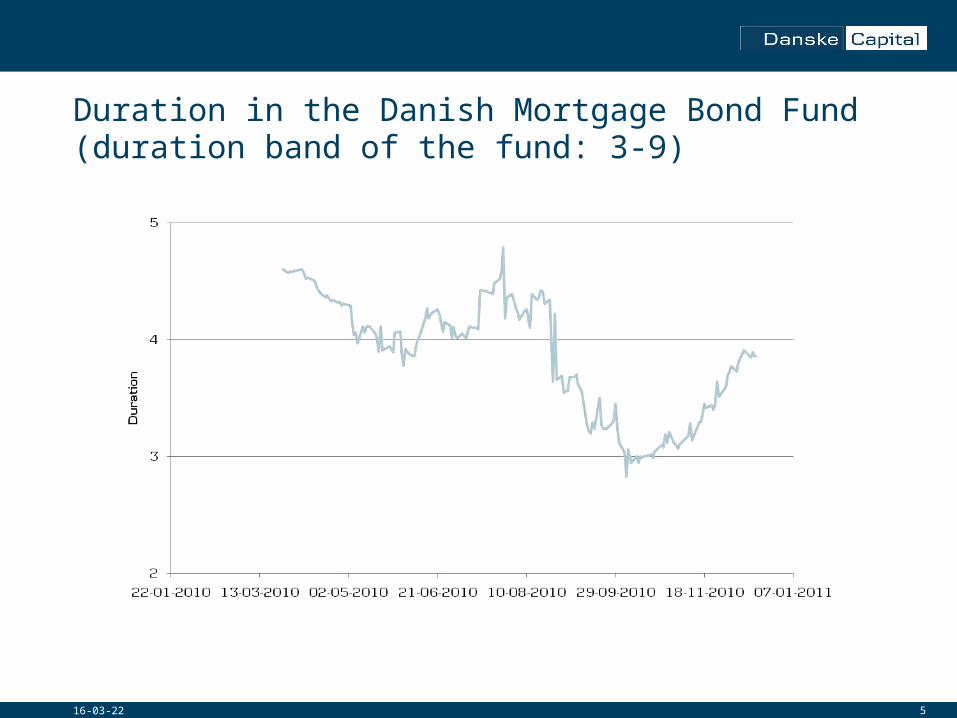

Duration in the Danish Mortgage Bond Fund(duration band of the fund: 3-9)

19-04-23

6

Outlook and Positions going into 2011

Mortgages: overweight• Callable Danish Mortgages with long duration will perform the

most on spread narrowing. Global demand for AAA bonds will keep the segment in a narrow spread to Govies and with a good up-side due to decreasing volatility. Capped Floaters also look interesting, but liquidity in this segment must be kept in mind.

Short Term Rates: Neutral

Duration: Underweight to neutral• We will slightly increase the overall amount of negative

convexity in the portfolio.

Note: We observe demand from EUR-investors and we do not fear supply from pension funds due to Solvency II

7

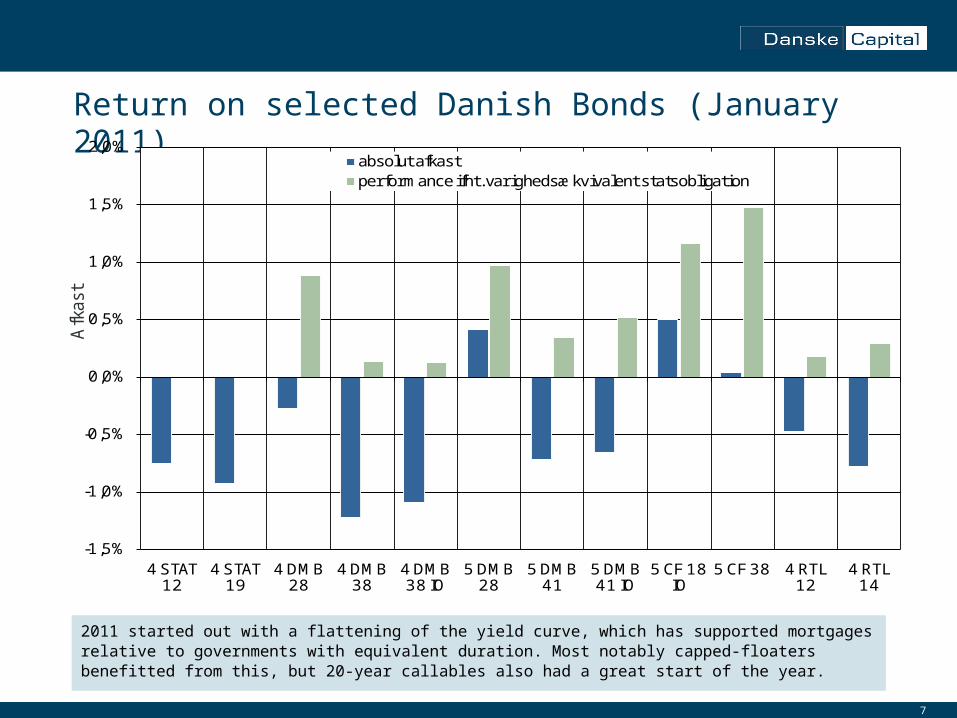

Return on selected Danish Bonds (January 2011)

2011 started out with a flattening of the yield curve, which has supported mortgages relative to governments with equivalent duration. Most notably capped-floaters benefitted from this, but 20-year callables also had a great start of the year.

-1,5%

-1,0%

-0,5%

0,0%

0,5%

1,0%

1,5%

2,0%

4 STAT 12

4 STAT 19

4 DMB 28

4 DMB 38

4 DMB 38 IO

5 DMB 28

5 DMB 41

5 DMB 41 IO

5 CF 18 IO

5 CF 38 4 RTL 12

4 RTL 14

Afk

ast

absolut afkastperformance ifht. varighedsækvivalent statsobligation

8

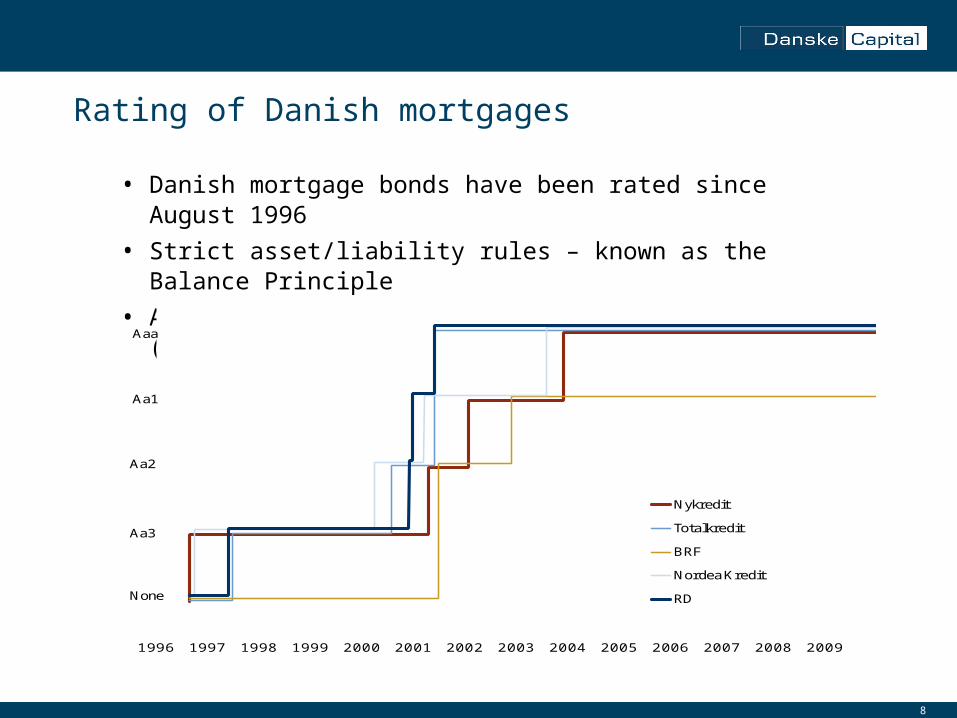

Rating of Danish mortgages

• Danish mortgage bonds have been rated since August 1996

• Strict asset/liability rules – known as the Balance Principle

• All lending is collateralized through property (i.e. Covered bond)

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Nykredit

Totalkredit

BRF

Nordea Kredit

RDNone

Aa3

Aa2

Aa1

Aaa

9

The Danish mortgage system is the best in the world (according to e.g. George Soros, Mexico and EU)• The embedded options

are insurances sold to the borrower!

• The borrower can prepay at par = insurance against falling rates

• The borrower can redeem the loan at market price = insurance against rising rates (every loan is linked directly to a specifik bond)

9

10

21.01.2011

Current Spread on Danish Mortgages

Expected return for German investor: 4,6% p.a.• 3,25% DBR 2020: 3,2%• Option Adjusted Spread: 0,9%• Alpha: 0,5%

Yield spread (bp) 4% DGB 2019 3,25% DBR 20204% Nykredit 2041 140 150

Option premiums 70 70

Option Adjusted Spread 70 80

5% Nykredit 2041 190 200Option premiums 100 100

Option Adjusted Spread 90 100

11

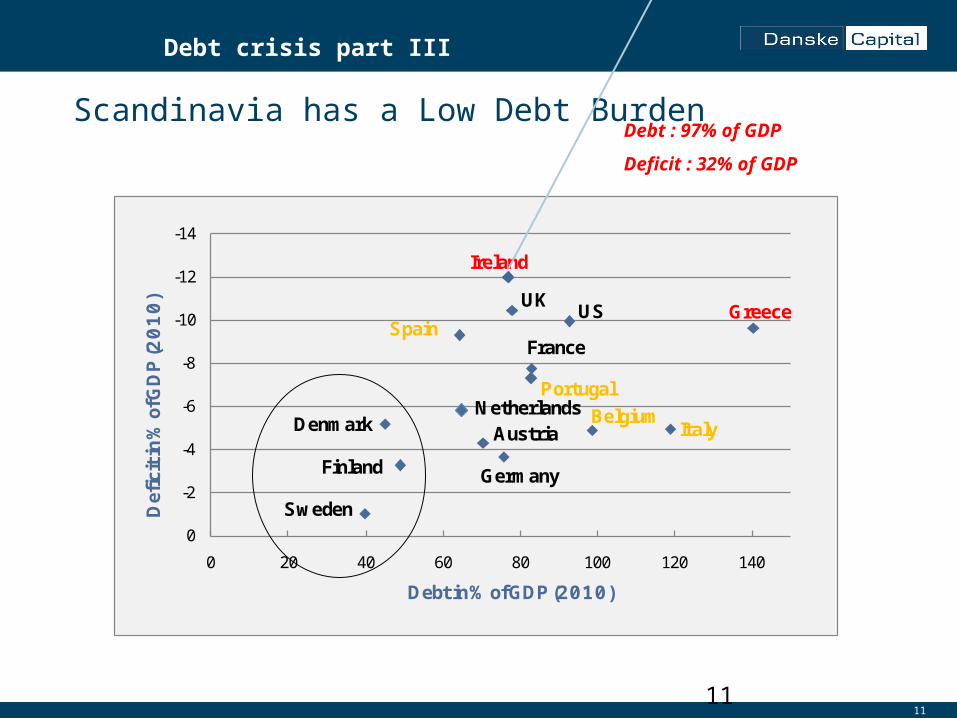

Ireland

SpainGreece

Germany

France

UK

BelgiumItaly

US

NetherlandsDenmark Austria

Finland

Sweden

Portugal

-14

-12

-10

-8

-6

-4

-2

0

0 20 40 60 80 100 120 140

Defi

cit i

n %

of G

DP (2

010)

Debt in% of GDP (2010)

Scandinavia has a Low Debt Burden

11

Debt : 97% of GDP

Deficit : 32% of GDP

Debt crisis part III

12

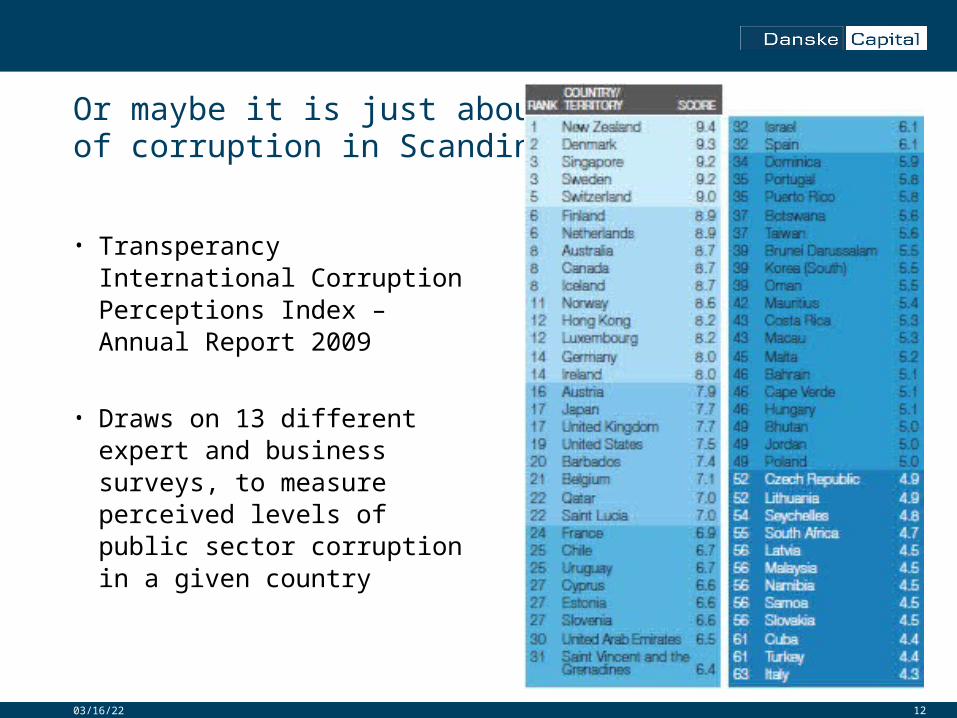

Or maybe it is just about lackof corruption in Scandinavia...

• Transperancy International Corruption Perceptions Index – Annual Report 2009

• Draws on 13 different expert and business surveys, to measure perceived levels of public sector corruption in a given country

04/19/23

13

Disclaimer & Contact information

Danske Capital

Strødamvej 46

DK 2100 Copenhagen

Tel. +45 45 13 96 00

Fax +45 45 14 98 03

http://www.danskecapital.com

This publication has been prepared to be read exclusively in conjunction with the oral presentation provided by Danske Capital. Readers should not replace their own judgement with any information or opinions herein and should contact their investment advisor whenever necessary. Any information or opinions contained herein are not intended for distribution to or use by any person in any jurisdiction or country where such distribution or use would be unlawful and, specifically, are not intended for distribution to or use by any "US Person" within the meaning of the United States Securities Act of 1933, nor any personal customer in the United Kingdom.