dbm fs_updated 18 nov 15pm

DESCRIPTION

DeloitteTRANSCRIPT

Development Bank of Mongolia International Financial Reporting Standards Interim Financial Statements and Independent Auditor’s Report 30 June 2013

Contents INDEPENDENT AUDITOR’S REPORT INTERIM FINANCIAL STATEMENTS Interim Statement of Financial Position ......................................................................................................... 1 Interim Statement of Comprehensive Income............................................................................................... 2 Interim Statement of Changes in Equity........................................................................................................ 3 Interim Statement of Cash Flows ............................................................................................................. 4 Notes to the Interim Financial Statements

1. CORPORATE INFORMATION AND OPERATING ENVIRONMENT 8

2. FINANCIAL REPORTING FRAMEWORK AND BASIS FOR PREPARATION AND 9

PRESENTATION

3. SIGNIFICANT ACCOUNTING POLICIES 13

4. CRITICAL ACCOUNTING JUDGEMENTS AND KEY SOURCES OF ESTIMATION 21

UNCERTAINTY

5. APPLICATION OF NEW AND REIVISED INTERNATIONAL FINANCIAL 22

REPORTING STANDARDS

6. CASH AND CASH EQUIVALENTS 26

7. BANK DEPOSITS 27

8. LOAN AND ADVANCES 28

9. OTHER ASSETS 32

10. PROPERTY AND EQUIPMENT 33

11. INTANGIBLES ASSETS 34

12. CUSTOMER ACCOUNTS AND OTHER LIABILITIES 35

13. BONDS 35

14. BORROWINGS 36

15. RELATED PARTY TRANSACTIONS 36

16. CONTRIBUTED CAPITAL 38

17. INTEREST INCOME 39

18. INTEREST EXPENSE 39

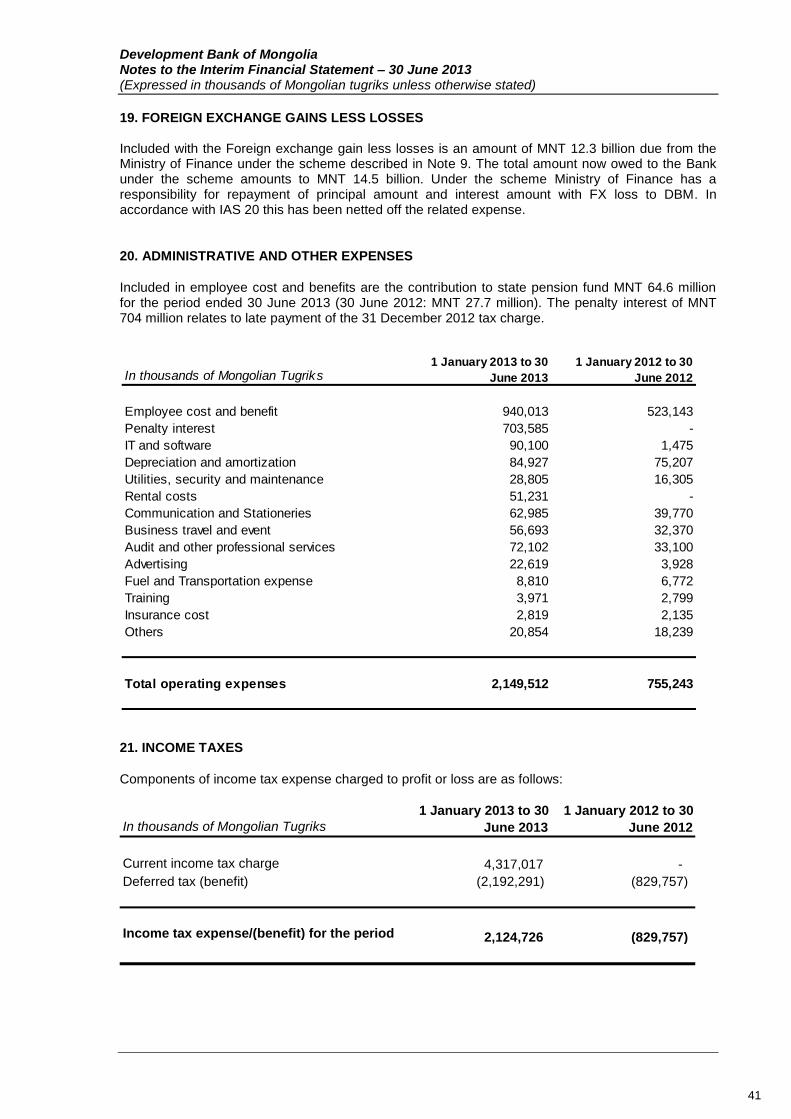

19. FOREIGN EXCHANGE LOSSES LESS GAINS 40

20. ADMINISTRATIVE AND OTHER OPERATING EXPENSES 40

21. INCOME TAXES 40

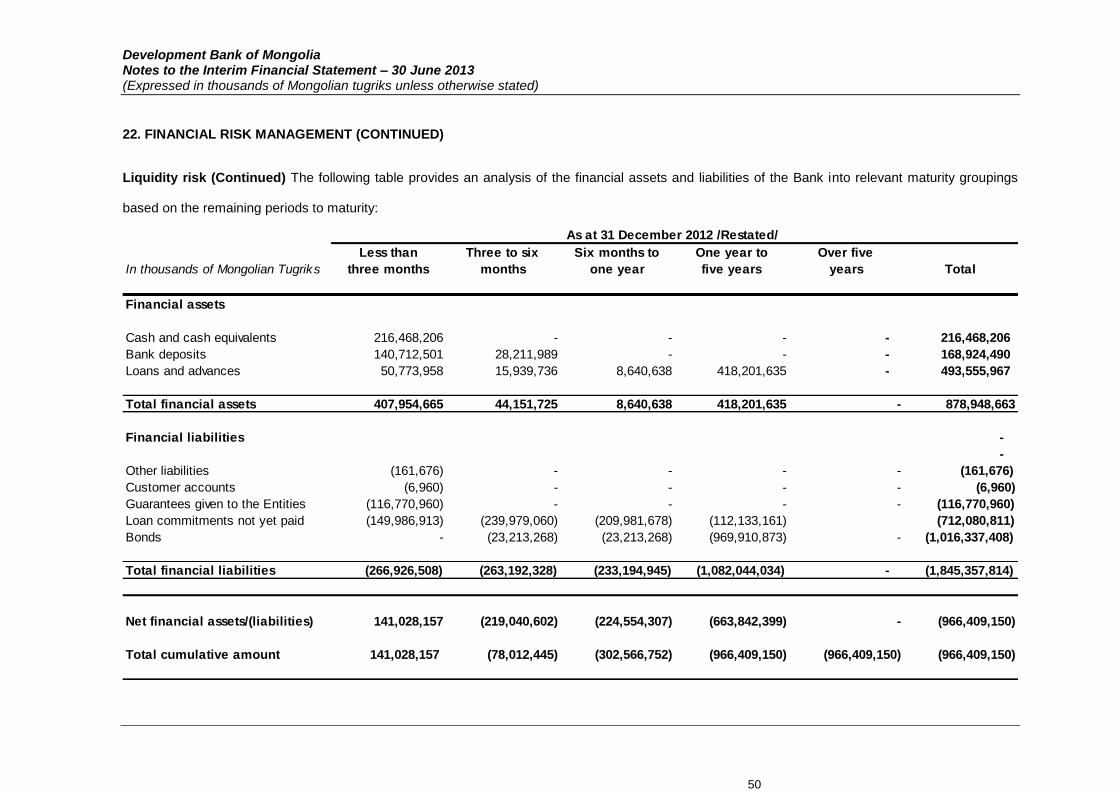

22. FINANCIAL RISK MANAGEMENT 42

23. PRESENTATION OF FINANCIAL INSTRUMENTS BY MEASUREMENT CATEGORY 55

24. FAIR VALUES OF FINANCIAL ASSETS AND LIABILITIES 56

25. COMMITMENTS AND CONTINGENCIES 60

26. SEGMENT REPORTING 61

27. POST BALANCE SHEET EVENTS 62

Development Bank of Mongolia Interim Statement of Financial Position Period ended 30 June 2013

The accompanying notes are an integral part of these financial statements.

Development Bank of Mongolia Interim Statement of Comprehensive Income Period ended 30 June 2013

The accompanying notes are an integral part of these financial statements.

4

Development Bank of Mongolia Interim Statement of Comprehensive Income Period ended 30 June 2013

The accompanying notes are an integral part of these financial statements.

5

In thousands of Mongolian Tugriks Note

1 January 2013

to 30 June 2013

1 January 2012

to 30 June 2012

Interest income 17 40,580,655 600,573

Interest expense 18 (27,655,733) (406,668)

Net interest income 12,924,922 193,905

Net interest income after provision for loan

impairment 12,924,922 193,905

Gains less losses from trading in foreign currencies 770,852 -

Foreign exchange gains less losses 19 (1,966,848) (2,500,419)

Administrative and other operating expenses 20 (2,149,512) (755,243)

Profit/(loss) before tax 9,579,414 (3,061,757)

Income tax (expenses)/benefit 21 (2,124,726) 829,757

Profit/(loss) for the period 7,454,688 (2,232,000)

Total comprehensive income/(loss) for the period 7,454,688 (2,232,000)

Development Bank of Mongolia Interim Statement of Changes in Equity Period ended 30 June 2013

The accompanying notes are an integral part of these financial statements.

In thousands of Mongolian TugriksNote Share capital

Retained

earningsTotal equity

Balance at 1 January 2012 16 49,700,000 (602,190) 49,097,810

Loss for the period - (2,232,000) (2,232,000)

Total comprehensive loss - (2,232,000) (2,232,000)

Balance at 30 June 2012 16 49,700,000 (2,834,190) 46,865,810

Balance at 1 January 2013 16 73,300,000 (6,308,151) 66,991,849

Profit for the period - 7,454,688 7,454,688

Total comprehensive income - 7,454,688 7,454,688

Balance at 30 June 2013 16 73,300,000 1,146,535 74,446,535

Development Bank of Mongolia Interim Statement of Cash Flows Period ended 30 June 2013

The accompanying notes are an integral part of these financial statements.

7

In thousands of Mongolian Tugriks

1 January 2013

to 30 June 2013

1 January 2012

to 30 June 2012

Cash flows from operating activities

Profit / (loss) before tax 9,579,414 (3,061,757)

Adjustments to:

Depreciation, amortization 84,927 75,207

Interest income (40,580,655) (600,573)

Interest expense on borrowings 27,655,733 406,668

FX (gain)/loss -Unrealized 1,638,772 186,086

Other non-cash operating expenses 233,569 114,775

Cash flows from operating activities before changes in

operating assets and liabilities (1,388,240) (2,879,594)

Net (increase)/decrease in loans and advances to customers (616,987,426) (27,225,665)

Net (increase)/decrease in other financial assets 30,917,488 (26,133,092)

Net increase/ (decrease) in other financial liabilities 38,701,826 (1,138,514)

Net cash (used in)/from operating activities before tax and interest received and paid

(548,756,352) (57,376,865)

Income taxes paid (686,593) -

Interest received 22,014,073 391,657

Interest paid on borrowings (24,357,996) (738,049)

Net cash (used in)/from operating activities (551,786,868) (57,723,257)

Development Bank of Mongolia Interim Statement of Cash Flows Period ended 30 June 2013

The accompanying notes are an integral part of these financial statements.

8

In thousands of Mongolian Tugriks

1 January 2013

to 30 June 2013

1 January 2012

to 30 June 2012

Net cash (used in)/from operating activities (551,786,868) (57,723,257)

Cash flows from investing activities

Purchase of property, plant, equipment and intangible assets (297,283) (110,026)

Net cash used in investing activities (297,283) (110,026)

Cash flows from financing activities

Proceeds from borrowings 433,553,076 -

Proceeds from bonds 147,045,342 769,007,622

Net cash from/(used in) financing activities 580,598,418 769,007,622

Effect of exchange rate changes on cash and cash

equivalents 914,183 6,200,770

Net (decrease)/increase in cash and cash equivalents 29,428,450 717,375,109

Cash and cash equivalents at the beginning of the period 216,468,206 75,817,745

Cash and cash equivalents at the end of the period 245,896,656 793,192,854

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

9

1. CORPORATE INFORMATION AND OPERATING ENVIRONMENT

The Development Bank of Mongolia ('the Bank') is a Government-owned, policy-oriented statutory financial institution established on 25 March, 2011 pursuant to Resolution No. 195 dated 20 July 2010 by the Government of Mongolia and under the Development Bank Law passed by Parliament on 10 February 2011. The Bank has been registered as a limited liability company with the Legal Entity Registration Office of the General Authority for State Registration since 25 March 2011 and is the only policy bank in Mongolia. The Bank conducts its business under the direct supervision of the Cabinet, which is the highest institution of Government administration in Mongolia and the Ministry of Economic Development, and is regulated, principally, by the Development Bank Law. The Bank commenced operations in May 2011.

The Government of Mongolia is the Bank's sole shareholder. In May and December 2011, the Government contributed MNT 16.7 billion and MNT 33.0 billion, respectively, in cash to the Bank's capital. In 2012, the Government contributed a further MNT 23.6 billion and as at 30 June 2013, the Bank's share capital was 73.3 billion. The Government has contributed a further MNT 10.0 billion, MNT 5.0 billion and MNT 35.0 billion in July, August and September 2013, respectively, to the Bank’s capital.

In accordance with Article 21.1 of the Development Bank Law, Parliament determines the source of equity financing the Government can provide to the Bank and determines the limits of loan guarantees to be provided by the Government. The Bank is not subject to the rules and regulations issued by the Bank of Mongolia in relation to commercial banks. The Bank's policy is to maintain a strong capital base so as to maintain investor, creditor and market confidence and to sustain future development of the business.

Until July 2013, the executive management of the Bank had been carried out by a joint team from the Bank and the Korean Development Bank. In July 2013, the Management Agreement with the Korean Development Bank was changed to the Advisory Agreement, and the Bank is managed solely by Mongolian nationals appointed by the Government. The Bank had an average of 63 employees during the period ended 30 June 2013 (2012: 43). The Bank's principal place of business is: Max Tower Building 2-3

rd floor, Juulchin Street 4/4 Ulaanbaatar 15170, Mongolia.

These financial statements are presented in Mongolian Tugriks (“MNT”), unless otherwise stated.

These interim financial statements were approved for issue by the Board of Directors of the Bank on 8 November 2013.

Operating Environment of the Bank

Mongolia displays many characteristics of an emerging market including relatively high inflation and

interest rates. After recording steady growth in 2010 and 2011, the Mongolian economy has shown

signs of a slowdown in 2012 that continued to 2013 due to declining global commodities prices,

concerns over slowing growth in China and changes to the Mongolian foreign investment law which

have slowed inbound foreign investment into the country.

The tax and customs legislation in Mongolia is subject to varying interpretations. The future economic

performance of Mongolia is tied to the continuing demand from China and continuing high global

prices for commodities as well as dependent upon the effectiveness of economic, financial and

monetary measures undertaken by the Government together with tax, legal regulatory and political

developments.

The international sovereign debt crisis, stock market volatility and other risks could have a negative

effect on the Mongolian financial and corporate sector.

Management is unable to predict all developments, which could have an impact on the Mongolian

economy, and consequently what effect, if any, they could have on the future financial position of the

Bank. Management believes it is taking all the necessary measures to support the sustainability and

development of the Bank’s business.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

10

2. FINANCIAL REPORTING FRAMEWORK AND BASIS FOR PREPARATION AND PRESENTATION

Statement of Compliance

The interim financial statements of the Bank have been prepared in accordance International Financial Reporting Standards (IFRS), which includes all applicable IFRS, International Accounting Standards (IAS), and interpretations issued by the International Financial Reporting Interpretations Committee (IFRIC) and Standing Interpretations Committee (SIC).

Basis of Preparation and Presentation

These interim financial statements have been prepared in accordance with International Accounting Standard No. 34 Interim Financial Reporting, under the historical cost convention, as modified by the initial recognition of financial instruments based on fair value. The principal accounting policies applied in the preparation of these financial statements are set out below. These policies have been consistently applied to all the periods presented, unless otherwise stated.

Functional Currency These financial statements are presented in Mongolian tugriks ('MNT') the currency of the primary economic environment in which the Bank operates and the Bank’s functional currency.

Amendments of the financial statements after issue.

The Bank’s management has the power to amend the financial statements after issue.

Restatements

The following retrospective restatements have been made in these financial statements:

Accrued Interest Receivable and Accrued Interest Payable. ‘Accrued Interest Receivable’ and ‘Accrued Interest Payable’ were previously reported as separate line items in the Statement of Financial Position for the year ended 31 December 2012, while they are integral to measurement of the related assets and liabilities at amortized cost according to the Bank’s accounting policies. They have therefore been reclassified within ‘Loans and advances’, ‘Bank Deposits’, ‘Cash and cash equivalents’ and ‘Long Term Debt’ in these financial statements. ‘Accrued Interest receivables’ on bank deposits of MNT 2,350 million as at 31 December 2012 has been restated to ‘Bank Deposits’ in the amount of MNT 1,872 million and to ‘Cash and cash equivalents’ in the amount of MNT 478 million. Accrued Interest receivables’ on loans and advances of MNT 6,771 million as at 31 December 2012 has been restated to ‘Loans and advances’. ‘Accrued Interest receivables’ on bank deposits of MNT 108 million as at 1 January 2012 has been restated to ‘Bank Deposits’. ‘Accrued Interest payables’ on bonds of MNT 12,896 million as at 31 December 2012 has been restated to ‘Bonds’. ‘Accrued Interest payables’ on bonds of MNT 102 million as at 1 January 2012 has been restated to ‘Bonds’. This restatement has no impact on the Statement of Comprehensive Income while its impact on the Statement of Financial Position as of 31 December 2012 is presented below.

Unearned Income and Non-Interest income. Management has reconsidered the accounting for ‘Unearned Income’ previously reported within ‘Accounts and Other Liabilities’ and ‘Non-interest income’ which represented loan origination fees. These two items were presented as separate line items in the Statement of Financial Position and the Statement of Comprehensive Income, respectively, for the year ended 31 December 2012. They are reported within ‘Loans and advances’ and ‘Interest Income’ in these financial statements. ‘Other liabilities’ and ‘Loans and advances’ have been reduced by MNT 590 million. This restatement’s impact on the Statement of Comprehensive Income and on the Statement of Financial Position as of 31 December 2012 is presented below.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

11

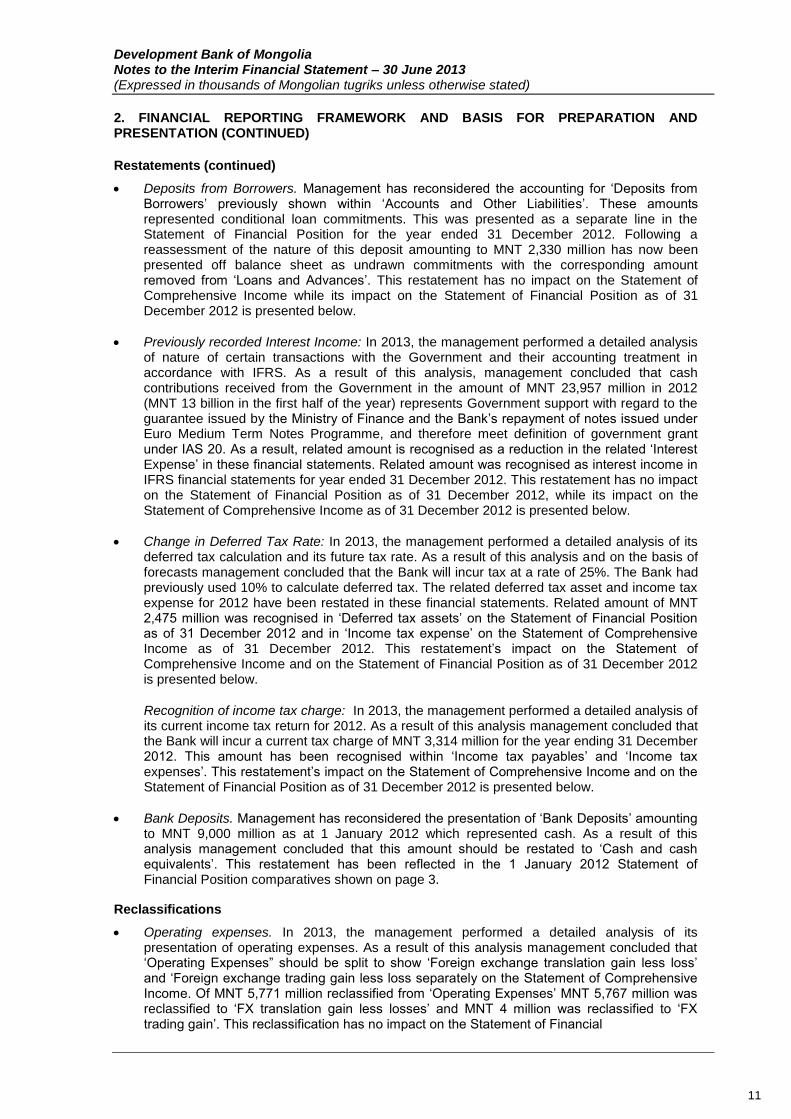

2. FINANCIAL REPORTING FRAMEWORK AND BASIS FOR PREPARATION AND PRESENTATION (CONTINUED)

Restatements (continued)

Deposits from Borrowers. Management has reconsidered the accounting for ‘Deposits from Borrowers’ previously shown within ‘Accounts and Other Liabilities’. These amounts represented conditional loan commitments. This was presented as a separate line in the Statement of Financial Position for the year ended 31 December 2012. Following a reassessment of the nature of this deposit amounting to MNT 2,330 million has now been presented off balance sheet as undrawn commitments with the corresponding amount removed from ‘Loans and Advances’. This restatement has no impact on the Statement of Comprehensive Income while its impact on the Statement of Financial Position as of 31 December 2012 is presented below.

Previously recorded Interest Income: In 2013, the management performed a detailed analysis of nature of certain transactions with the Government and their accounting treatment in accordance with IFRS. As a result of this analysis, management concluded that cash contributions received from the Government in the amount of MNT 23,957 million in 2012 (MNT 13 billion in the first half of the year) represents Government support with regard to the guarantee issued by the Ministry of Finance and the Bank’s repayment of notes issued under Euro Medium Term Notes Programme, and therefore meet definition of government grant under IAS 20. As a result, related amount is recognised as a reduction in the related ‘Interest Expense’ in these financial statements. Related amount was recognised as interest income in IFRS financial statements for year ended 31 December 2012. This restatement has no impact on the Statement of Financial Position as of 31 December 2012, while its impact on the Statement of Comprehensive Income as of 31 December 2012 is presented below.

Change in Deferred Tax Rate: In 2013, the management performed a detailed analysis of its deferred tax calculation and its future tax rate. As a result of this analysis and on the basis of forecasts management concluded that the Bank will incur tax at a rate of 25%. The Bank had previously used 10% to calculate deferred tax. The related deferred tax asset and income tax expense for 2012 have been restated in these financial statements. Related amount of MNT 2,475 million was recognised in ‘Deferred tax assets’ on the Statement of Financial Position as of 31 December 2012 and in ‘Income tax expense’ on the Statement of Comprehensive Income as of 31 December 2012. This restatement’s impact on the Statement of Comprehensive Income and on the Statement of Financial Position as of 31 December 2012 is presented below.

Recognition of income tax charge: In 2013, the management performed a detailed analysis of its current income tax return for 2012. As a result of this analysis management concluded that the Bank will incur a current tax charge of MNT 3,314 million for the year ending 31 December 2012. This amount has been recognised within ‘Income tax payables’ and ‘Income tax expenses’. This restatement’s impact on the Statement of Comprehensive Income and on the Statement of Financial Position as of 31 December 2012 is presented below.

Bank Deposits. Management has reconsidered the presentation of ‘Bank Deposits’ amounting to MNT 9,000 million as at 1 January 2012 which represented cash. As a result of this analysis management concluded that this amount should be restated to ‘Cash and cash equivalents’. This restatement has been reflected in the 1 January 2012 Statement of Financial Position comparatives shown on page 3.

Reclassifications

Operating expenses. In 2013, the management performed a detailed analysis of its presentation of operating expenses. As a result of this analysis management concluded that ‘Operating Expenses” should be split to show ‘Foreign exchange translation gain less loss’ and ‘Foreign exchange trading gain less loss separately on the Statement of Comprehensive Income. Of MNT 5,771 million reclassified from ‘Operating Expenses’ MNT 5,767 million was reclassified to ‘FX translation gain less losses’ and MNT 4 million was reclassified to ‘FX trading gain’. This reclassification has no impact on the Statement of Financial

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

12

In thousands of Mongolian

Tugriks

Year ended

31 December 2012

(as previously

reported

Restatements Note

Year ended

31 December 2012

(restated)

Assets

Cash and cash equivalents 215,990,270 477,936 6 216,468,206

Bank deposits 167,052,000 1,872,490 7 168,924,490

Loans and advances 489,704,568 3,851,399 8 493,555,967

Accrued interest receivables 9,121,272 (9,121,272) 8 -

Intangible assets 726,688 - 11 726,688

Property and equipment 234,558 - 10 234,558

Deferred tax assets 3,465,282 2,475,078 21 5,940,360

Other assets 2,285,515 - 9 2,285,515

Total assets 888,580,153 444,369- 888,135,784

Liabilities

Other liabilities 3,425,135 (2,919,447) 505,688

Customer accounts 6,960 - 12 6,960

Income tax payables - 3,313,560 21 3,313,560

Accrued interest payables 12,896,260 (12,896,260) 13 -

Bonds 804,421,467 12,896,260 13 817,317,727

Total liabilities 820,749,822 394,113 821,143,935

Equity

Share capital 73,300,000 - 16 73,300,000

Retained earnings (5,469,669) (838,482) (6,308,151)

Total equity 67,830,331 (838,482) 66,991,849

Total liabilities and equity 888,580,153 (444,369) 888,135,784

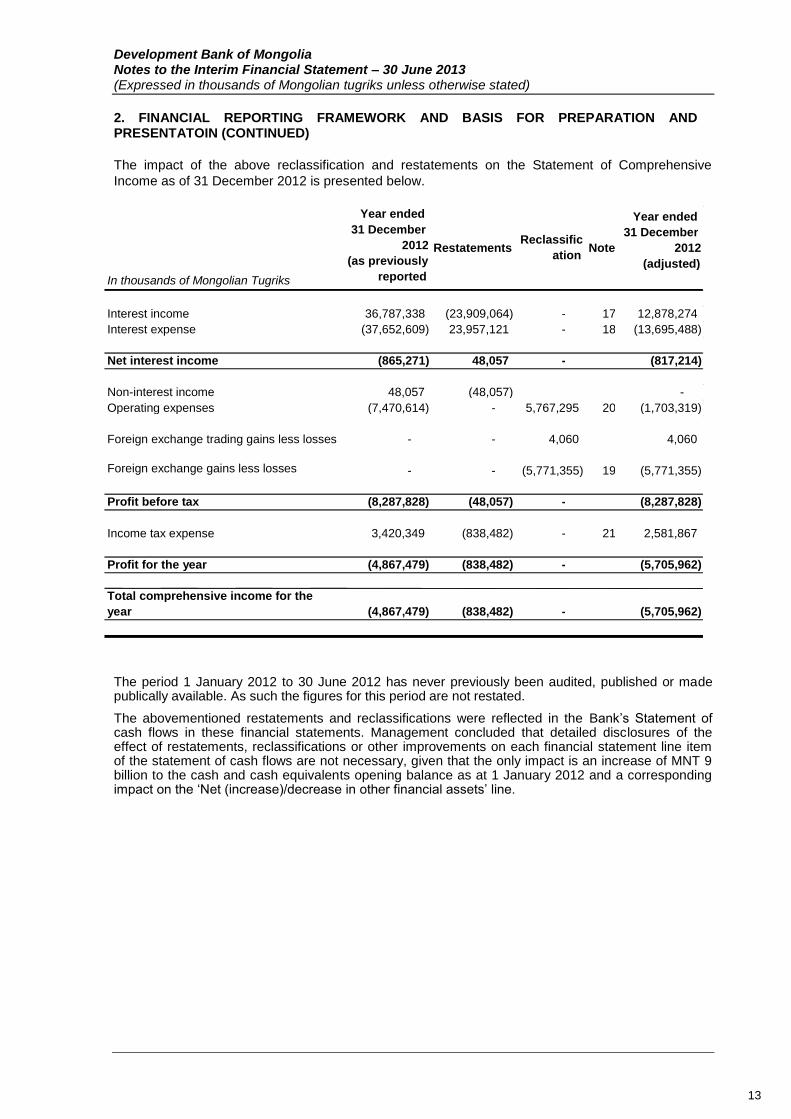

2. FINANCIAL REPORTING FRAMEWORK AND BASIS FOR PREPARATION AND PRESENTATION (CONTINUED) Reclassifications (continued)

Position as of 31 December 2012, while its impact on the Statement of Comprehensive Income as of 31 December 2012 is shown below.

Other Assets and ‘Foreign exchange gain less losses’. In 2013, the management performed a detailed analysis of nature of certain transactions with the Government and their accounting treatment in accordance with IFRS. As a result of this analysis, management concluded that receivables due from the Ministry of Finance, presented within ‘Other Assets”, in the amount of MNT 2,168,468 thousand meets the definition of a government grant under IAS 20. The grant amount is recognised in the related expense to which the grant relates to namely the ‘Foreign exchange gain less losses’ in these financial statements. This was previously treated as an embedded derivative and recorded within ‘Operating Expenses’ in the 31 December 2012 financial statements. This reclassification has no impact on the Statement of Financial Position as of 31 December 2012, and no impact on the Statement of Comprehensive Income as of 31 December 2012.

The reclassifications have no impact on the Statement of Financial Position. The impact of the above restatements on the Statement of Financial Position as of 31 December 2012 is presented below.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

13

In thousands of Mongolian Tugriks

Year ended

31 December

2012

(as previously

reported

Restatements Reclassific

ation Note

Year ended

31 December

2012

(adjusted)

Interest income 36,787,338 (23,909,064) - 17 12,878,274

Interest expense (37,652,609) 23,957,121 - 18 (13,695,488)

Net interest income (865,271) 48,057 - (817,214)

Non-interest income 48,057 (48,057) -

Operating expenses (7,470,614) - 5,767,295 20 (1,703,319)

Foreign exchange trading gains less losses - - 4,060 4,060

Foreign exchange gains less losses - - (5,771,355) 19 (5,771,355)

Profit before tax (8,287,828) (48,057) - (8,287,828)

Income tax expense 3,420,349 (838,482) - 21 2,581,867

Profit for the year (4,867,479) (838,482) - (5,705,962)

Total comprehensive income for the

year (4,867,479) (838,482) - (5,705,962)

2. FINANCIAL REPORTING FRAMEWORK AND BASIS FOR PREPARATION AND PRESENTATOIN (CONTINUED)

The impact of the above reclassification and restatements on the Statement of Comprehensive

Income as of 31 December 2012 is presented below.

The period 1 January 2012 to 30 June 2012 has never previously been audited, published or made publically available. As such the figures for this period are not restated.

The abovementioned restatements and reclassifications were reflected in the Bank’s Statement of cash flows in these financial statements. Management concluded that detailed disclosures of the effect of restatements, reclassifications or other improvements on each financial statement line item of the statement of cash flows are not necessary, given that the only impact is an increase of MNT 9 billion to the cash and cash equivalents opening balance as at 1 January 2012 and a corresponding impact on the ‘Net (increase)/decrease in other financial assets’ line.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

14

3. SIGNIFICANT ACCOUNTING POLICIES

Financial instruments - key measurement terms. Depending on their classification financial instruments are carried at fair value or amortised cost as described below.

Fair value. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The best evidence of fair value is price in an active market. An active market is one in which transactions for the asset or liability take place with sufficient frequency and volume to provide pricing information on an ongoing basis. Fair value of financial instruments traded in an active market is measured as the product of the quoted price for the individual asset or liability and the quantity held by the entity. This is the case even if a market’s normal daily trading volume is not sufficient to absorb the quantity held and placing orders to sell the position in a single transaction might affect the quoted price.

A portfolio of financial derivatives or other financial assets and liabilities that are not traded in an active market is measured at the fair value of a group of financial assets and financial liabilities on the basis of the price that would be received to sell a net long position (i.e. an asset) for a particular risk exposure or paid to transfer a net short position (i.e. a liability) for a particular risk exposure in an orderly transaction between market participants at the measurement date. This is applicable for assets carried at fair value on a recurring basis if the Group: (a) manages the group of financial assets and financial liabilities on the basis of the entity’s net exposure to a particular market risk (or risks) or to the credit risk of a particular counterparty in accordance with the entity’s documented risk management or investment strategy; (b) it provides information on that basis about the group of assets and liabilities to the entity’s key management personnel; and (c) the market risks, including duration of the entity’s exposure to a particular market risk (or risks) arising from the financial assets and financial liabilities is substantially the same.

Valuation techniques such as discounted cash flow models or models based on recent arm’s length transactions or consideration of financial data of the investees are used to measure fair value of certain financial instruments for which external market pricing information is not available. Fair value measurements are analysed by level in the fair value hierarchy as follows: (i) level one are measurements at quoted prices (unadjusted) in active markets for identical assets or liabilities, (ii) level two measurements are valuations techniques with all material inputs observable for the asset or liability, either directly (that is, as prices) or indirectly (that is, derived from prices), and (iii) level three measurements are valuations not based on solely observable market data (that is, the measurement requires significant unobservable inputs). Transfers between levels of the fair value hierarchy are deemed to have occurred at the end of the reporting period.

Transaction costs. Transaction costs are incremental costs that are directly attributable to the acquisition, issue or disposal of a financial instrument. An incremental cost is one that would not have been incurred if the transaction had not taken place. Transaction costs include fees and commissions paid to agents (including employees acting as selling agents), advisors, brokers and dealers, levies by regulatory agencies and securities exchanges, and transfer taxes and duties. Transaction costs do not include debt premiums or discounts, financing costs or internal administrative or holding costs.

Amortised cost. Amortised cost is the amount at which the financial instrument was recognised at initial recognition less any principal repayments, plus accrued interest, and for financial assets less any write-down for incurred impairment losses. Accrued interest includes amortisation of transaction costs deferred at initial recognition and of any premium or discount to maturity amount using the effective interest method. Accrued interest income and accrued interest expense, including both accrued coupon and amortised discount or premium (including fees deferred at origination, if any), are not presented separately and are included in the carrying values of related items in the statement of financial position.

The effective interest method. The effective interest method is a method of allocating interest income or interest expense over the relevant period, so as to achieve a constant periodic rate of interest (effective interest rate) on the carrying amount. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts (excluding future credit losses) through the expected life of the financial instrument or a shorter period, if appropriate, to the net carrying amount of the financial instrument. The effective interest rate discounts cash flows of variable interest instruments to the next interest reprising date, except for the premium or discount which reflects the credit spread over the floating rate specified in the instrument, or other variables that are not reset to

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

15

3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Market rates. Such premiums or discounts are amortised over the whole expected life of the instrument. The present value calculation includes all fees paid or received between parties to the contract that are an integral part of the effective interest rate

Initial recognition of financial instruments. Trading securities, derivatives and other financial instruments at fair value through profit or loss are initially recorded at fair value. All other financial instruments are initially recorded at fair value plus transaction costs. Fair value at initial recognition is best evidenced by the transaction price. A gain or loss on initial recognition is only recorded if there is a difference between fair value and transaction price which can be evidenced by other observable current market transactions in the same instrument or by a valuation technique whose inputs include only data from observable markets.

All purchases and sales of financial assets that require delivery within the time frame established by regulation or market convention (“regular way” purchases and sales) are recorded at trade date, which is the date on which the Bank commits to deliver a financial asset. All other purchases are recognised when the entity becomes a party to the contractual provisions of the instrument.

Derecognition of financial assets. The Bank derecognises financial assets when (a) the assets are redeemed or the rights to cash flows from the assets otherwise expired or (b) the Bank has transferred the rights to the cash flows from the financial assets or entered into a qualifying pass-through arrangement while (i) also transferring substantially all risks and rewards of ownership of the assets or (ii) neither transferring nor retaining substantially all risks and rewards of ownership, but not retaining control. Control is retained if the counterparty does not have the practical ability to sell the asset in its entirety to an unrelated third party without needing to impose restrictions on the sale.

Cash and cash equivalents. Cash and cash equivalents are items which are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. Cash and cash equivalents include all interbank placements with original maturities of less than 90 days. Funds restricted for a period of more than 90 days on origination are excluded from cash and cash equivalents. Cash and cash equivalents are carried at amortised cost.

Loans and advances to customers. Loans and advances to customers are recorded when the Bank advances money to purchase or originate an unquoted non-derivative receivable from a customer due on fixed or determinable dates, and has no intention of trading the receivable. Loans and advances to customers are carried at amortised cost. Bank Deposits. Bank deposit are recorded when the Bank advances money to counterparty banks with no intention of trading the resulting unquoted non-derivative receivable due on fixed or determinable dates. Amounts due from other banks are carried at amortised cost. Impairment of financial assets carried at amortised cost. Impairment losses are recognised in profit or loss for the year when incurred as a result of one or more events (“loss events”) that occurred after the initial recognition of the financial asset and which have an impact on the amount or timing of the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated. The following other principal criteria are also used to determine whether there is objective evidence that an impairment loss has occurred:

- any instalment is overdue and the late payment cannot be attributed to a delay caused by the settlement systems;

- the borrower experiences a significant financial difficulty as evidenced by the borrower’s financial information that the Bank obtains;

- the borrower considers bankruptcy or a financial reorganisation; - there is an adverse change in the payment status of the borrower as a result of changes in

the national or local economic conditions that impact the borrower; or - the value of collateral significantly decreases as a result of deteriorating market conditions.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

16

3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Future cash flows in a group of financial assets that are collectively evaluated for impairment, are estimated on the basis of the contractual cash flows of the assets and the experience of management in respect of the extent to which amounts will become overdue as a result of past loss events and the success of recovery of overdue amounts. Past experience is adjusted on the basis of current observable data to reflect the effects of current conditions that did not affect past periods, and to remove the effects of past conditions that do not exist currently.

If the terms of an impaired financial asset held at amortised cost are renegotiated or otherwise modified because of financial difficulties of the borrower or issuer, impairment is measured using the original effective interest rate before the modification of terms. The renegotiated asset is then derecognized and a new asset is recognized at its fair value only if the risks and rewards of the asset substantially changed. This is normally evidenced by a substantial difference between the present values of the original cash flows and the new expected cash flows.

Impairment losses are always recognised through an allowance account to write down the asset’s carrying amount to the present value of expected cash flows (which exclude future credit losses that have not been incurred) discounted at the original effective interest rate of the asset. The calculation of the present value of the estimated future cash flows of a collateralised financial asset reflects the cash flows that may result from foreclosure less costs for obtaining and selling the collateral, whether or not foreclosure is probable. Allowances are made against the carrying amount of loans and advances that are identified as being potentially impaired, based on regular reviews of outstanding balances, to reduce these loans and advances to their recoverable amount in accordance with Regulations on Asset Classification and provisioning approved by the Executive director of Development Bank of Mongolia.

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognised (such as an improvement in the debtor’s credit rating), the previously recognised impairment loss is reversed by adjusting the allowance account through profit or loss for the year.

Uncollectible assets are written off against the related impairment loss provision after all the necessary procedures to recover the asset have been completed and the amount of the loss has been determined. Subsequent recoveries of amounts previously written off are credited to impairment loss account in profit or loss for the year.

Prepayments. Prepayments represent expenses not yet incurred but already paid in cash. Prepayments are initially recorded as assets and measured at the amount of cash paid. Subsequently, these are charged to profit or loss as they are consumed in operations or expire with the passage of time.

Property and Equipment. Property and equipment are initially measured at cost. At the end of each reporting period, property and equipment are measured at cost less any subsequent accumulated depreciation, amortization and impairment losses. Cost includes expenditure that is directly attributable to the acquisition of the asset.

Purchased software that is integral to the functionality of the related equipment is capitalized as part of that equipment.

When an item of property and equipment is acquired in an exchange for non-monetary asset/s, or a combination of monetary and non-monetary assets, the cost of that item is measured at fair value unless:

- the exchange transaction lacks commercial substance; or - the fair value of neither the asset received nor the asset given up is reliably measurable.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

17

3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Costs of minor repairs and maintenance are expensed when incurred. Costs of replacing major parts or components of premises and equipment items are capitalised, and the replaced part is retired.

Depreciation is computed on the straight-line method, based on the estimated useful lives of the assets as follows:

- IT Equipment 3 years - Furniture and fixture 10 years - Vehicles 10 years

Derecognition of property and equipment. An item of property and equipment is derecognized upon disposal or when no future economic benefits are expected to arise from the continued use of the asset. Gain or loss arising on the disposal or retirement of an asset is determined as the difference between the sales proceeds and the carrying amount of the asset and is recognized in profit or loss. Intangible Assets. Intangible assets that are acquired by the Bank with finite useful lives are initially measured at cost. At the end of each reporting period items of intangible assets acquired are measured at cost less accumulated amortization and accumulated impairment losses. Cost includes purchase price, including import duties and non-refundable purchase taxes, after deducting trade discounts and rebates and any directly attributable cost of preparing the intangible asset for its intended use.

Subsequent expenditure is capitalized only when it increases the future economic benefits embodied

in the specific asset to which it relates. All other expenditure, including expenditure on internally generated goodwill and brands, is recognized in profit or loss as incurred.

Amortization for intangible asset with finite useful life is calculated over the cost of the asset, or other

amount substituted for cost, less its residual value.

Amortization is recognized in profit or loss on a straight-line basis over the estimated useful lives of intangible assets from the date that they are available for use, since this most closely reflects the expected pattern of consumption of the future economic benefits embodied in the asset. The estimated useful lives are as follows:

Software 10 years

Derecognition of intangible assets. An intangible asset is derecognized on disposal, or when no

future economic benefits are expected from use or disposal. Gains or losses arising from derecognition of an intangible asset are measured as the difference between the net disposal proceeds and the carrying amount of the asset and are recognized in profit or loss when the asset is derecognized.

Impairment of Tangible and Intangible Assets. At the end of each reporting period management assesses whether there is any indication of impairment of premises and equipment or intangible assets. If any such indication exists, management estimates the recoverable amount, which is determined as the higher of an asset’s fair value less costs to sell and its value in use. The carrying amount is reduced to the recoverable amount and the impairment loss is recognised in profit or loss for the year. An impairment loss recognised for an asset in prior years is reversed if there has been a change in the estimates used to determine the asset’s value in use or fair value less costs to sell.

Customer accounts. Customer accounts are non-derivative liabilities to individuals, state or corporate customers and are carried at amortised cost.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

18

3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Bonds and Borrowings. Debt securities representing bonds issued are stated at amortised cost. If the Bank purchases its own debt securities in issue, they are removed from the statement of financial position and the difference between the carrying amount of the liability and the consideration paid is included in gains arising from retirement of debt.

Ordinary shares. As at 30 June 2013, the Government of Mongolia had paid in capital contributions

to the Bank, but no share certificates had been issued.

Income tax. Interim period income tax expense is accrued using the effective tax rate that would be applicable to expected total annual earnings, that is, the estimated weighted average annual effective income tax rate applied to the pre-tax income of the interim period.

Deferred income tax. Deferred income tax is provided using the balance sheet liability method for tax loss carry forwards and temporary differences arising between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes. In accordance with the initial recognition exemption, deferred taxes are not recorded for temporary differences on initial recognition of an asset or a liability in a transaction other than a business combination if the transaction, when initially recorded, affects neither accounting nor taxable profit. Deferred tax balances are measured at tax rates enacted or substantively enacted at the end of the reporting period, which are expected to apply to the period when the temporary differences will reverse or the tax loss carry forwards will be utilised.

Deferred tax assets for deductible temporary differences and tax loss carry forwards are recorded only to the extent that it is probable that future taxable profit will be available against which the deductions can be utilised.

Provisions, Contingent Liabilities and Contingent Assets

Provisions. Provisions are recognized when the Bank has a present obligation, either legal or constructive, as a result of a past event, it is probable that the Bank will be required to settle the obligation through an outflow of resources embodying economic benefits, and the amount of the obligation can be estimated reliably.

The amount of the provision recognized is the best estimate of the consideration required to settle the present obligation at the end of each reporting period, taking into account the risks and uncertainties surrounding the obligation. A provision is measured using the cash flows estimated to settle the present obligation; its carrying amount is the present value of those cash flows.

When some or all of the economic benefits required to settle a provision are expected to be recovered from a third party, the receivable is recognized as an asset if it is virtually certain that reimbursement will be received and the amount of the receivable can be measured reliably.

Provisions are reviewed at the end of each reporting period and adjusted to reflect the current best estimate.

If it is no longer probable that a transfer of economic benefits will be required to settle the obligation, the provision is reversed.

Contingent Liabilities and Assets. Contingent liabilities and assets are not recognized because their existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity.

Contingent liabilities are disclosed, unless the possibility of an outflow of resources embodying economic benefits is remote.

Contingent assets are disclosed only an inflow of economic benefits is probable.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

19

3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) Credit related commitments. From time to time, the Bank enters into credit related commitments, including letters of credit and financial guarantees. Financial guarantees represent irrevocable assurances to make payments in the event that a customer cannot meet its obligations to third parties and carry the same credit risk as loans. Financial guarantees and commitments to provide a loan are initially recognized at their fair value, which is normally evidenced by the amount of fees received. This amount is amortized on a straight line basis over the life of the commitment, except for commitments to originate loans if it is probable that the Bank will enter into a specific lending arrangement and does not expect to sell the resulting loan shortly after origination; such loan commitment fees are deferred and included in the carrying value of the loan on initial recognition. At the end of each reporting period, the commitments are measured at the higher of (i) the remaining unamortized balance of the amount at initial recognition and (ii) the best estimate of expenditure required to settle the commitment at the end of each reporting period. In cases where the fees are charged periodically in respect of an outstanding commitment, they are recognized as revenue on a time proportion basis over the respective commitment period.

Employee Benefits

Short-term benefits. The Bank recognizes a liability net of amounts already paid and an expense for services rendered by employees during the reporting period. A liability is also recognized for the amount expected to be paid under short-term cash bonus or profit sharing plans if the Bank has a present legal or constructive obligation to pay this amount as a result of past service provided by the employee, and the obligation can be estimated reliably.

Short-term employee benefit obligations are measured on an undiscounted basis and are expensed as the related service is provided.

Long-term benefits. The Bank has provided funding to a 3rd

party bank in order for it to give its Employees cheaper mortgage and salary loans. The cost of this scheme has initially been booked as a prepayment and will be expensed through the statement of comprehensive income over the life-time of the loan scheme.

Post-employment benefits. The Bank does not have any pension arrangements separate from the state pension system of Mongolia, which requires current contributions by the employer calculated as a percentage of current gross salary payments; such expense is charged to the statement of comprehensive incomes in the period the related salaries and wages are payable.

Offsetting. Financial assets and liabilities are offset and the net amount reported in the statement of financial position only when there is a legally enforceable right to offset the recognised amounts, and there is an intention to either settle on a net basis, or to realise the asset and settle the liability simultaneously.

Income and expense recognition. Interest income and expense are recorded for all debt instruments on an accrual basis using the effective interest method. This method defers, as part of interest income or expense, all fees paid or received between the parties to the contract that are an integral part of the effective interest rate, transaction costs and all other premiums or discounts.

Fees integral to the effective interest rate include origination fees received or paid by the entity relating to the creation or acquisition of a financial asset or issuance of a financial liability, for example fees for evaluating creditworthiness, evaluating and recording guarantees or collateral, negotiating the terms of the instrument and for processing transaction documents. Commitment fees received by the Bank to originate loans at market interest rates are integral to the effective interest rate if it is probable that the Bank will enter into a specific lending arrangement and does not expect to sell the resulting loan shortly after origination. The Bank does not designate loan commitments as financial liabilities at fair value through profit or loss.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

20

3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

When loans and other debt instruments become doubtful of collection, they are written down to the present value of expected cash inflows and interest income is thereafter recorded for the unwinding of the present value discount based on the asset’s effective interest rate which was used to measure the impairment loss.

All other fees, commissions and other income and expense items are generally recorded on an accrual basis by reference to completion of the specific transaction assessed on the basis of the actual service provided as a proportion of the total services to be provided.

Commissions and fees arising from negotiating, or participating in the negotiation of a transaction for a third party, such as the acquisition of loans, shares or other securities or the purchase or sale of businesses, and which are earned on execution of the underlying transaction, are recorded on its completion.

Government Grants. Grants from the government are recognised at their fair value, where there is a reasonable assurance that the grant will be received, and the Bank will comply with all attached conditions. Government grants relating to costs are deferred, and recognised in the Statement of Comprehensive Income over the period necessary to match them with the costs they are intended to compensate. The Bank has opted to recognise its Government Grants as a reduction of the related expense. If part, or all, of a grant becomes repayable to the government, the repayment is first matched against any remaining deferred income set up for that grant. If this is insufficient, the remainder is expensed immediately.

Foreign Currency

Foreign currency transactions. Transactions in currencies other than the MNT are recorded at the rates of exchange prevailing on the dates of the transactions. At the end of each reporting period, monetary assets and liabilities that are denominated in foreign currencies are retranslated at the rates prevailing at the end of the reporting period. Non-monetary assets and liabilities carried at fair value that are denominated in foreign currencies are translated at the rates prevailing at the date the fair value was determined. Gains and losses arising on retranslation are included in profit or loss for the year. Non-monetary assets and liabilities that are measured in terms of historical cost in a foreign currency are not retranslated.

Related Party Transactions

A related party transaction is a transfer of resources, services or obligations between the Bank and a related party, regardless of whether a price is charged.

A person or a close member of that person’s family is related to the Bank if that person:

has control or joint control over the Bank or has significant influence over the Bank or is a member of the key management personnel of the Bank or of a parent of the

Bank

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

21

3. SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

An entity is related to the Bank if any of the following conditions apply:

the entity and the Bank are members of the same group which means that each parent, subsidiary and fellow subsidiary is related to the others;

one entity is an associate or joint venture of the other entity or an associate or joint venture of a member of a group of which the other entity is a member;

both entities are joint ventures of the same third party; one entity is a joint venture of a third entity and the other entity is an associate of

the third entity; the entity is a post-employment benefit plan for the benefit of employees of either

the Bank or an entity related to the Bank; the entity is controlled or jointly controlled by a person who is a related party as

identified above; and A person that has control or joint control over the reporting entity has significant

influence over the entity or is a member of the key management personnel of the entity or of a parent of the entity.

Due to the nature of the Bank and its role as a policy bank almost all loans and transactions are with related parties. The Bank applies the exemption allowed under IAS 24.25.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

22

4. CRITICAL ACCOUNTING JUDGEMENTS AND KEY SOURCES OF ESTIMATION UNCERTAINTY

In the application of the Bank's accounting policies, management is required to make judgments, estimates and assumptions about the carrying amounts of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on the historical experience and other factors that are considered to be relevant. Actual results may differ from these estimates. The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimate is revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both current and future periods.

Key Sources of Estimation Uncertainty. The following are the key assumptions concerning the future and other key sources of estimation uncertainty at the end of each reporting period that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year. Determining the carrying value of employee prepayments. Management has concluded that deposit to State bank of MNT 1 billion receives interest rate below market rate. Based on available information on comparable transactions, management made judgment that the policy rate of the Bank of Mongolia of 10.5% p.a. represents reasonable approximation of market interest rate on MNT funding. As a result, related prepayment was recognized at its fair value at initial recognition of MNT 776,352 thousand. The loss on initial recognition (i.e. the difference between nominal value of this deposit and its fair value) represents salary prepayments in accordance with IFRS requirements. Management has concluded that it is appropriate to recognize the cost of the scheme over the lifetime of the deposit. Refer to Note 9 for details.

Determining the level of loan loss provisioning. The purpose of the Bank is to provide financing to

development projects in the Mongolia. As a result, the projects are often of a social infrastructure

nature and may not have a clearly defined stand-alone profit-oriented cash flow sufficient to

demonstrate a long-term ability to repay the development loan. However, for substantially all loans a

guarantee is provided by the State, and this is considered when assessing whether there is a risk of

loss on any particular loan. Management does not believe any loan impairment assessment is

required on loans where guarantees have been received from the Government. No collective loan

loss provision calculation is performed by the Bank as management assess that given the structure of

the loan portfolio and the guarantees received from Government any loss given default “LGD” on loans would be zero. Given the close involvement of the Government, the Bank and the underlying

projects the Bank finances, management assess that there are no losses incurred but not reported

affecting the Bank. The level of Government guarantees and other collateral guarantees is disclosed

in Note 8. Any changes in the assessment of recoverability of guarantees would impact the profit or

loss of the Bank.

Determining the treatment of Government Grant Schemes. Management has concluded that it is

a recipient of two grant schemes described in Note 18 and Note 19 in the periods 1 January 2012 to

30 June 2012 and 1 January 2013 to 30 June 2013 amounting to MNT 13 billion and MNT 12.3 billion

respectively. Determining whether the transaction falls within the scope of IAS 20 requires

judgement. The definition of government grants includes transfers to an entity, subject to certain

conditions placed on the operating activities of the entity. However, it excludes government

assistance on which cannot be distinguished from normal trading transactions of the entity and transactions which constitute "government participation in the ownership of the entity". Management

have concluded that the two schemes fall within the scope of IAS 20. Management have also

concluded that the receivable due from Government at each reporting date was reasonably assured

to be received.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

23

4. CRITICAL ACCOUNTING JUDGEMENTS AND KEY SOURCES OF ESTIMATION UNCERTAINTY (CONTINUED)

Initial recognition of borrowings and loans at below market rates. During the first half 2013, the Bank has obtained financing directly from the Government of Mongolia. These funds are

denominated in MNT and obtained at an interest rate of 4.9%, which is lower than rates at which the

Bank could source the funds from other lenders at Mongolian market. Based on available information

on comparable transactions, management made judgment that the policy rate of the Bank of

Mongolia represents the best approximation of market interest rate on MNT funding for banks

(10.5%). As a result of such financing, the Bank is able to advance funds to target customers as

determined by the Government, at advantageous rates of approximately 8% p.a. The Bank has little

or no discretionary rights in determining interest rates on issued loans should it continue to wish

receiving cheap financing from the Government. Management has considered whether gains or

losses should arise on initial recognition of such instruments. Management’s judgement is that these

funds and the related lending are at market rates and no initial recognition gains or losses should

arise. In making this judgement management also considers that these instruments are a separate market segment (i.e. the Bank operates in a separate principal market).

Deferred income tax asset recognition. The recognised deferred tax asset represents income

taxes recoverable through future deductions from taxable profits, and is recorded in the statement of

financial position. Deferred income tax assets are recorded to the extent that realisation of the related

tax benefit is probable. The future taxable profits and the amount of tax benefits that are probable in

the future are based on a medium term business plan prepared by management and extrapolated

results thereafter. The business plan is based on management expectations that are believed to be

reasonable under the circumstances taking into account the Bank’s actual profitability during 2013.

Management has concluded that it will be able to recover its deferred tax asset including tax losses

and is likely to incur tax at the rate of 25%.

5. APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS

The following new standards and interpretations became effective for the Group from 1 January 2013:

IFRS 10 “Consolidated Financial Statements” (issued in May 2011 and effective for annual periods beginning on or after 1 January 2013) replaces all of the guidance on control and consolidation in IAS 27 “Consolidated and separate financial statements” and SIC-12 “Consolidation - special purpose entities”. IFRS 10 changes the definition of control so that the same criteria are applied to all entities to determine control. This definition is supported by extensive application guidance. The Standard did not have any material impact on the Bank’s financial statements.

IFRS 11 “Joint Arrangements” (issued in May 2011 and effective for annual periods beginning on or after 1 January 2013) replaces IAS 31 “Interests in Joint Ventures” and SIC-13 “Jointly Controlled Entities—Non-Monetary Contributions by Ventures”. Changes in the definitions have reduced the number of types of joint arrangements to two: joint operations and joint ventures. The existing policy choice of proportionate consolidation for jointly controlled entities has been eliminated. Equity accounting is mandatory for participants in joint ventures. The Standard did not have any material impact on the Bank’s financial statements.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

24

5. APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (CONTINUED)

IFRS 12 “Disclosure of Interests in Other Entities” (issued in May 2011 and effective for annual periods beginning on or after 1 January 2013) applies to entities that have an interest in a subsidiary, a joint arrangement, an associate or an unconsolidated structured entity. It replaces the disclosure requirements previously found in IAS 28 “Investments in associates”. IFRS 12 requires entities to disclose information that helps financial statement readers to evaluate the nature, risks and financial effects associated with the entity’s interests in subsidiaries, associates, joint arrangements and unconsolidated structured entities. To meet these objectives, the new standard requires disclosures in a number of areas, including significant judgments and assumptions made in determining whether an entity controls, jointly controls, or significantly influences its interests in other entities, extended disclosures on share of non-controlling interests in group activities and cash flows, summarized financial information of subsidiaries with material non-controlling interests, and detailed disclosures of interests in unconsolidated structured entities. The Standard did not have any material impact on the Bank’s financial statements.

IFRS 13 “Fair Value Measurement” (issued in May 2011 and effective for annual periods beginning on or after 1 January 2013) improved consistency and reduced complexity by providing a revised definition of fair value, and a single source of fair value measurement and disclosure requirements for use across IFRSs The Standard did not have any material impact on the Bank’s financial statements.

IAS 27 “Separate Financial Statements” (revised in May 2011 and effective for annual periods beginning on or after 1 January 2013) was changed and its objective is now to prescribe the accounting and disclosure requirements for investments in subsidiaries, joint ventures and associates when an entity prepares separate financial statements. The guidance on control and consolidated financial statements was replaced by IFRS 10 “Consolidated Financial Statements”. The Standard did not have any material impact on the Bank’s financial statements.

IAS 28 “Investments in Associates and Joint Ventures” (revised in May 2011 and effective for annual periods beginning on or after 1 January 2013). The amendment of IAS 28 resulted from the Board’s project on joint ventures. When discussing that project, the Board decided to incorporate the accounting for joint ventures using the equity method into IAS 28 because this method is applicable to both joint ventures and associates. With this exception, other guidance remained unchanged. The Standard did not have any material impact on the Bank’s financial statements.

Amendments to IAS 1 “Presentation of Financial Statements” (issued in June 2011, effective for annual

periods beginning on or after 1 July 2013) changed the disclosure of items presented in other comprehensive income. The amendments require entities to separate items presented in other comprehensive income into two groups, based on whether or not they may be reclassified to profit or loss in the future. The suggested title used by IAS 1 has changed to “statement of profit or loss and other comprehensive income”. The amended standard resulted in changed presentation of financial statements, but did not have any impact on measurement of transactions and balances.

Amended IAS 19 “Employee Benefits” (issued in June 2011, effective for periods beginning on or after 1

January 2013) makes significant changes to the recognition and measurement of defined benefit pension expense and termination benefits, and to the disclosures for all employee benefits. The standard requires recognition of all changes in the net defined benefit liability (asset) when they occur, as follows: (i) service cost and net interest in profit or loss; and (ii) remeasurements in other comprehensive income. The Standard did not have any material impact on the Bank’s financial statements.

“Disclosures - Offsetting Financial Assets and Financial Liabilities” - Amendments to IFRS 7 (issued in December 2011 and effective for annual periods beginning on or after 1 January 2013). The amendment requires disclosures that enable users of an entity’s financial statements to evaluate the effect or potential effect of netting arrangements, including rights of set-off. The Standard did not have any material impact on the Bank’s financial statements.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

25

5. APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (CONTINUED)

Improvements to International Financial Reporting Standards (issued in May 2012 and effective for annual periods beginning 1 January 2013). The improvements consist of changes to five standards. IFRS 1 was amended to (i) clarify that an entity that resumes preparing its IFRS financial statements may either repeatedly apply IFRS 1 or apply all IFRSs retrospectively as if it had never stopped applying them, and (ii) to add an exemption from applying IAS 23 “Borrowing costs”, retrospectively by first-time adopters. IAS 1 was amended to clarify that explanatory notes are not required to support the third balance sheet presented at the beginning of the preceding period when it is provided because it was materially impacted by a retrospective restatement, changes in accounting policies or reclassifications for presentation purposes, while explanatory notes will be required when an entity voluntarily decides to provide additional comparative statements. IAS 16 was amended to clarify that servicing equipment that is used for more than one period is classified as property, plant and equipment rather than inventory. IAS 32 was amended to clarify that certain tax consequences of distributions to owners should be accounted for in the income statement as was always required by IAS 12. IAS 34 was amended to bring its requirements in line with IFRS 8. IAS 34 now requires disclosure of a measure of total assets and liabilities for an operating segment only if such information is regularly provided to chief operating decision maker and there has been a material change in those measures since the last annual financial statements. The Standard did not have any material impact on the Bank’s financial statements.

“Transition Guidance Amendments to IFRS 10, IFRS 11 and IFRS 12” (issued in June 2012 and effective for annual periods beginning 1 January 2013). The amendments clarify the transition guidance in IFRS 10 “Consolidated Financial Statements”. Entities adopting IFRS 10 should assess control at the first day of the annual period in which IFRS 10 is adopted, and if the consolidation conclusion under IFRS 10 differs from IAS 27 and SIC 12, the immediately preceding comparative period (that is, year 2012) is restated, unless impracticable. The amendments also provide additional transition relief in IFRS 10, IFRS 11 “Joint Arrangements” and IFRS 12 “Disclosure of Interests in Other Entities”, by limiting the requirement to provide adjusted comparative information only for the immediately preceding comparative period. Further, the amendments remove the requirement to present comparative information for disclosures related to unconsolidated structured entities for periods before IFRS 12 is first applied. The Standard did not have any material impact on the Bank’s financial statements.

Other revised standards and interpretations: IFRIC 20 “Stripping Costs in the Production Phase of a Surface Mine”, considers when and how to account for the benefits arising from the stripping activity in mining industry. The interpretation did not have an impact on the Group’s financial statements. Amendments to IFRS 1 “First-time adoption of International Financial Reporting Standards - Government Loans”, which were issued in March 2012 and are effective for annual periods beginning 1 January 2013, give first-time adopters of IFRSs relief from full retrospective application of accounting requirements for loans from government at below market rates. The amendment is not relevant to the Group.

New Accounting Pronouncements

Certain new standards and interpretations have been issued that are mandatory for the annual periods beginning on or after 1 January 2014 or later, and which the Group has not early adopted.

IFRS 9 “Financial Instruments Part 1: Classification and Measurement”. IFRS 9, issued in November 2009, replaces those parts of IAS 39 relating to the classification and measurement of financial assets. IFRS 9 was further amended in October 2010 to address the classification and measurement of financial liabilities and in December 2011 to (i) change its effective date to annual periods beginning on or after 1 January 2015 and (ii) to add transition disclosures. Key features of the standard are as follows:

Financial assets are required to be classified into two measurement categories: those to be measured subsequently at fair value, and those to be measured subsequently at amortised cost. The decision is to be made at initial recognition. The classification depends on the entity’s business model for managing its financial instruments and the contractual cash flow characteristics of the instrument.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

26

5. APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (CONTINUED)

An instrument is subsequently measured at amortised cost only if it is a debt instrument and both (i) the objective of the entity’s business model is to hold the asset to collect the contractual cash flows, and (ii) the asset’s contractual cash flows represent payments of principal and interest only (that is, it has only “basic loan features”). All other debt instruments are to be measured at fair value through profit or loss.

All equity instruments are to be measured subsequently at fair value. Equity instruments that are held for trading will be measured at fair value through profit or loss. For all other equity investments, an irrevocable election can be made at initial recognition, to recognise unrealised and realised fair value gains and losses through other comprehensive income rather than profit or loss. There is to be no recycling of fair value gains and losses to profit or loss. This election may be made on an instrument-by-instrument basis. Dividends are to be presented in profit or loss, as long as they represent a return on investment.

Most of the requirements in IAS 39 for classification and measurement of financial liabilities were carried forward unchanged to IFRS 9. The key change is that an entity will be required to present the effects of changes in own credit risk of financial liabilities designated at fair value through profit or loss in other comprehensive income.

While adoption of IFRS 9 is mandatory from 1 January 2015, earlier adoption is permitted. The Bank is considering the implications of the standard, the impact on the Bank and the timing of its adoption by the Bank.

“Offsetting Financial Assets and Financial Liabilities” - Amendments to IAS 32 (issued in December 2011 and effective for annual periods beginning on or after 1 January 2014). The amendment added application guidance to IAS 32 to address inconsistencies identified in applying some of the offsetting criteria. This includes clarifying the meaning of ‘currently has a legally enforceable right of set-off’ and that some gross settlement systems may be considered equivalent to net settlement. The Bank is considering the implications of the standard, the impact on the Bank and the timing of its adoption by the Bank.

“Amendments to IFRS 10, IFRS 12 and IAS 27 - Investment entities” (issued on 31 October 2012 and effective for annual periods beginning 1 January 2014). The amendment introduced a definition of an investment entity as an entity that (i) obtains funds from investors for the purpose of providing them with investment management services, (ii) commits to its investors that its business purpose is to invest funds solely for capital appreciation or investment income and (iii) measures and evaluates its investments on a fair value basis. An investment entity will be required to account for its subsidiaries at fair value through profit or loss, and to consolidate only those subsidiaries that provide services that are related to the entity's investment activities. IFRS 12 was amended to introduce new disclosures, including any significant judgements made in determining whether an entity is an investment entity and information about financial or other support to an unconsolidated subsidiary, whether intended or already provided to the subsidiary. The Bank does not expect the amendment to have any impact on its financial statements.

IFRIC 21 – “Levies” (issued on 20 May 2013 and effective for annual periods beginning 1 January 2014). The interpretation clarifies the accounting for an obligation to pay a levy that is not income tax. The obligating event that gives rise to a liability is the event identified by the legislation that triggers the obligation to pay the levy. The fact that an entity is economically compelled to continue operating in a future period, or prepares its financial statements under the going concern assumption, does not create an obligation. The same recognition principles apply in interim and annual financial statements. The application of the interpretation to liabilities arising from emissions trading schemes is optional. The Bank does not expect the amendment to have any impact on its financial statements.

Development Bank of Mongolia Notes to the Interim Financial Statement – 30 June 2013 (Expressed in thousands of Mongolian tugriks unless otherwise stated)

27

5. APPLICATION OF NEW AND REVISED INTERNATIONAL FINANCIAL REPORTING STANDARDS (CONTINUED)

Amendments to IAS 36 – “Recoverable amount disclosures for non-financial assets” (issued in May 2013 and effective for annual periods beginning 1 January 2014; earlier application is permitted if IFRS 13 is applied for the same accounting and comparative period). The amendments remove the requirement to disclose the recoverable amount when a CGU contains goodwill or indefinite lived intangible assets but there has been no impairment. The Bank is currently assessing the impact of the amendments on the disclosures in its financial statements.

Amendments to IAS 39 – “Novation of Derivatives and Continuation of Hedge Accounting” issued in June 2013 and effective for annual periods beginning 1 January 2014).The amendments will allow hedge accounting to continue in a situation where a derivative, which has been designated as a hedging instrument, is novated (i.e parties have agreed to replace their original counterparty with a new one) to effect clearing with a central counterparty as a result of laws or regulation, if specific conditions are met. The Bank does not expect the amendment to have any impact on its financial statements.

Unless otherwise described above, the new standards and interpretations are not expected to affect significantly the Bank’s financial statements.

6. CASH AND CASH EQUIVALENTS

Cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value.

Cash and cash equivalents are not collateralised. All amounts are classified as neither past due nor impaired. The interest on the short term deposit ranges from 7.5%-12.5% p.a. for MNT and 4.8%-7.2% p.a. for USD deposits for the six months of 2013 (in 2012: 4.5%-11.5% p.a.).

Cash at Bank of Mongolia and other banks and short term deposits with local banks with original

maturities of less than three months represent balances with Mongolian banks and the Bank of

Mongolia.