de ned bene t division guide - unisuper/media/files/forms and... · 2019-09-30 · de ned bene t...

TRANSCRIPT

Defined Benefit Division and Accumulation 2 Product Disclosure Statement, Part 1 of 2

This Guide, together with the Accumulation 2 Guide, forms the Defined Benefit Division and Accumulation 2 Product Disclosure Statement. Issued 1 October 2019 by UniSuper Limited ABN 54 006 027 121.

Defined Benefit Division Guide/ 1 October 2019 /

2019

FUNDOF THE YEAR2019

About this GuideThis Guide has been prepared and issued by UniSuper Limited. It’s for Defined Benefit Division (DBD) members, and summarises the key features of the product (including significant benefits and characteristics, fees and taxes) as well as key risks.

Information in this Guide may change from time to time. We’ll provide updates of any changes at unisuper.com.au/pds. You can also request a paper or electronic copy of updated information without charge by calling us on 1800 331 685.

UniSuper, ABN 91 385 943 850, MySuper Authorisation Number 91385943850448 is referred to as ‘UniSuper’ or ‘the Fund’. UniSuper Limited, ABN 54 006 027 121, AFSL No. 492806, is referred to as ‘USL’ or the ‘Trustee’. UniSuper Management Pty Ltd, ABN 91 006 961 799, AFSL No. 235907, is referred to as ‘UniSuper Management’ or ‘USM’. USL has delegated administration of UniSuper to USM, which is wholly owned by USL in its capacity as UniSuper’s Trustee. UniSuper Advice is operated by USM, which is licensed to deal in financial products and provide financial advice. UniSuper advisers are employees of USM. They are remunerated by way of a base salary and potential bonuses. External insurance cover is provided to UniSuper through group insurance policies the Trustee has taken out with TAL Life Limited, ABN 70 050 109 450, AFSL No. 237848 (referred to as our ‘Insurer’ throughout this document).

The information in this document is of a general nature only and does not take into account your individual objectives, financial situation or needs. You should consider the appropriateness of the information having regard to your personal circumstances and consider consulting a qualified financial adviser before making an investment decision based on information contained in this Guide. The value of your investments can go up or down and investment returns can be positive or negative. The Trustee does not guarantee the performance of the Fund’s investment options. To the extent that this Guide contains any information which is inconsistent with the UniSuper Trust Deed and Regulations (together, ‘the Trust Deed’) the Trust Deed will prevail.

USM, SuperRatings Pty Ltd and Chant West Pty Ltd have consented to their logo and/or statements being included in this document, in the form and context in which they have been included, and consent has not been withdrawn as at the date of this document.

© UniSuper Limited 2019.

Important information documentsYou should read the following documents together with this Guide and the Accumulation 2 Guide:

> More about the DBD and Accumulation 2

> How we invest your money

> Insurance in your super

> How super is taxed, and

> What happens to your inbuilt benefits if you choose Accumulation 2?.

They’re incorporated by reference into this Guide and italicised when we refer to them. They’re available free of charge at unisuper.com.au/pds or by calling 1800 331 685.

AWARD-WINNING FUNDWith a string of awards and high ratings from Australia’s top ratings and research agencies, SuperRatings and Chant West, we’re one of Australia’s most award-winning super funds.

2019

FUNDOF THE YEAR2019

10MYSUPEROF THE YEAR2019

SuperRatings, a superannuation research company, has awarded UniSuper a Platinum Choice rating for its accumulation products, something only the ‘best value for money’ funds receive. Our accumulation products have also achieved a 10-year Platinum Performance rating. Go to www.superratings.com.au for details of its rating criteria. SuperRatings does not issue, sell, guarantee or underwrite this product. SuperRatings has consented to the inclusion in this document of the references to SuperRatings and the inclusion of its logos in the form and context in which they are included.

In 2019, Chant West awarded UniSuper ‘Super Fund of the Year’, ‘Investments Best Fund’ and ‘Advice Services Best Fund’. Our accumulation products have received a 5 Apples rating. For information about the methodology used, see www.chantwest.com.au. Chant West has consented to the inclusion in this document of the references to Chant West and the inclusion of its logos in the form and context in which they are included.

Contents06 The DBD and your choices

12 How does yoursuper grow?

16 Contributing to super

18 Accessing super

19 Nominating beneficiaries

20 More than just super – inbuilt benefits and insurance

24 How we invest your money

25 Risks of super

26 How super is taxed

29 General information

30 Fees and other costs

Forms Defined Benefit Division/Accumulation 2 changing your default options Reduce my default member contributions Application for insurance at UniSuper

2 1800 331 685UNISUPER.COM.AU

Jargon busterThe super industry is full of terms that can be hard to understand. We’ve tried our best to keep our information straightforward but you might find this jargon buster useful as you read this guide.

JARGON WHAT IT MEANS

Accumulation component

DBD membership has two parts—a ‘defined’ part based on a formula, and an ‘accumulation’ part. Some contributions, like transfers from other super funds, don’t go into ‘defined’ super—they get added to your accumulation component. You can choose how the money in your accumulation component is invested.

Average Contribution Factor (ACF)

This is the time-weighted average of your contribution factors. If you always make default member contributions (7% after tax or 8.25% before tax), your ACF is 100%.

Reducing your default member contributions will generally decrease your ACF. See the definition of ‘Contribution factors’ for more information in the More about the DBD and Accumulation 2 document.

Average Service Factor (ASF)

This refers to how much of your DBD membership has been spent in full-time employment. It’s calculated by averaging all of your Service Fractions over your period of Benefit Service with a UniSuper participating employer. For example, if you always worked full-time with your UniSuper employer(s), your ASF is 100%. However, any breaks in employment will reduce your ASF. Typical breaks in employment include the time between ceasing one job and starting another, periods of leave without pay, periods of part-time work and half contributions. Breaks in employment are calculated in days and include weekends.

Beneficiary The person(s) you nominate to receive your death benefit if you die. To be eligible as a beneficiary when you die, the recipient must be your spouse or child, financially dependent on you, in an interdependent relationship with you or be your legal personal representative.

Benefit Salary The benefit salary is generally the five-year benefit salary. The five-year benefit salary is the average of your annual equivalent full-time salary (not indexed) as a contributing DBD member over your last five years of employment with a UniSuper employer(s), before your benefit is calculated.

If you’ve worked for less than five years, it’s generally averaged over the time you’ve been employed as a contributing DBD member.

Benefit Service Your period of service covers the years and days of your DBD membership. If you’re a contributing member and you die before age 60, your benefit service will also include the period from the date of your death to what would have been your 60th birthday. If you’re a contributing member and you suffer disablement, your benefit service covers the period (years and days) from the date of your disablement up to age 65.

Concessional contribution

This is money added to super before income tax is taken out. It’s taxed at 15%—not at your income tax rate. Examples of concessional contributions are ‘employer contributions’ and ‘salary sacrifice contributions’.

Contribution Money paid into your super that goes towards your retirement savings.

Contributions caps

The maximum amount you can pay into super each year without having to pay extra tax. There are two types of contributions caps – concessional (before tax) and non-concessional (after tax).

3Defined Benefit Division GuideJARGON bUSTER

JARGON WHAT IT MEANS

Defined benefit Super which is calculated using a formula that’s based on the number of hours worked (e.g. full or part time), your salary, your age and your level of contributions.

Employer contributions

Your employer must contribute 9.5% of your before-tax earnings to super. Some employers contribute a higher amount—DBD and Accumulation 2 members generally receive either 14% or 17%.

Inbuilt benefits Similar to insurance cover and provided exclusively to DBD members, inbuilt benefits can provide financial protection against injury, illness or death. They’re self-insured by UniSuper and are different to the insurance provided through our Insurer. The ‘cost’ of inbuilt benefits is already included in the defined benefit formula, meaning there’s no deduction from your account balance to pay for them.

Income protection cover

If you can’t work because of injury or illness, this type of insurance can pay you a regular monthly amount for a period of time. Income protection cover isn’t available to DBD members.

Insurance Can provide financial protection against injury, illness or death. The default insurance cover we provide you when you join UniSuper—and any extra cover you buy through us—is provided by our Insurer, TAL Life Limited.

Investment options

You can choose how your accumulation component is invested. We offer 16 different investment options, each with differing levels of risk and expected returns. There’s also a default option if you don’t choose. You don’t choose investment options for defined benefit super as it’s determined by a formula.

Lump sum When super is withdrawn as a single amount—rather than being transferred into a pension or income stream—we call this a lump sum.

Lump Sum Factor

This is based on your age when we calculate your defined benefit.

MySuper A simple superannuation solution designed to protect members by ensuring certain rules are met in relation to investment strategy, fees and insurance cover.

Non-concessional contributions

This is money added to super after income tax has been taken out. It doesn’t get taxed, because you’ve already paid tax on it (although limits do apply). Also known as ‘personal’ or ‘voluntary’ contributions.

Salary sacrifice contributions

An arrangement between you and your employer where you contribute (‘sacrifice’) some of your before-tax salary into super. Salary sacrifice contributions into super can have tax and income advantages and are generally taxed at 15%.

Default member contributions

This is money you add to your super over and above your employer’s contributions. As a DBD or Accumulation 2 member, the default level is 7% after tax (or 8.25% before tax and with the agreement with your employer) of your salary. You can lower your default member contributions, but this will reduce the amount you have when you retire, as you’ll have contributed less (it may also affect the availability of insurance cover).

Trustee This is a company appointed to make sure the fund operates in accordance with our Trust Deed and with relevant law. Trustees are obliged to act in the best interests of members. Our Trustee is called UniSuper Limited.

4 1800 331 685UNISUPER.COM.AU

Getting started > Read this Guide, the Accumulation 2 Guide and all

the important information documents we refer to throughout them.

> Complete the Defined Benefit Division/Accumulation 2 changing your default options form included with this Guide (also available at unisuper.com.au/pds) and return it to your employer.

> Read the Accumulation 2 Guide—and the Choosing a style of super that suits you fact sheet available at unisuper.com.au/factsheets —to see whether accumulation-style super is more suited to your circumstances. If it is, remember to transfer within your first two years of membership.

We’re here to helpWe’re available on your campus to help with information and general advice about your membership and our range of products. You might find it beneficial to speak to one of our consultants—either on campus or at one of our member centres.

Visit unisuper.com.au/oncampus to book an appointment.

The DefinedBenefit Division

(DBD)

6

As a DbD member > You’ll make a 7% ‘member contribution’ to your

super from your take-home pay. In addition, your employer will make a 14% or 17% contribution.

> You can choose to reduce your member contribution at any time.

> You can also choose whether you’d like to remain a DBD member or permanently transfer to our Accumulation 2 product. You have two years from the date you join to make this decision.

These are important decisions which should not be rushed.

We’re here to help. We can provide you with information to help you make the best choice for your circumstances.

Why is the DbD UniSuper’s default option? UniSuper has been providing defined benefit superannuation to employees in the higher education and research sector since 1983. It’s part of our DNA. Defined benefit funds were, in fact, the standard default option for most corporate super funds until relatively recently. While other funds have moved to an accumulation-style default offering, we continue with a defined benefit offering because, in simple terms, it’s designed to achieve an adequate level of retirement savings—without individual members being exposed to the volatility of investment markets.

This is achieved by the pooling of risks—similar to the principle applying to insurance policies. We’re proud of the fact that, since inception, no member has lost a single cent in accrued benefits due to market downturns. Of course, past performance is no indicator of future performance, but at the date of this PDS, the funding level of the DBD is in a healthy surplus.

Given that the funds managed within the DBD represent a relatively stable source of capital, UniSuper’s investment managers are able to source attractive investment opportunities with a long-term time horizon. Together with the smooth returns generated by risk-pooling, each member’s final payout is linked to their salary (see formula below), enabling them to plan for their retirement with greater certainty. We tend to think of the DBD as a ‘set and forget’ superannuation strategy.

Broadly speaking, the DBD may not suit members anticipating only a short period of employment in higher education. It may also not suit members who are expecting little or no salary growth arising from promotion or reclassification to higher roles during their higher education employment. Later in this section we talk about the suitability of the DBD for different members. You should read this information before choosing your product.

The DBD and your choicesCongratulations—the terms of your employment mean you’re now a member of our Defined Benefit Division (DBD). All eligible employees in the higher education and research sector become DBD members by default. The DBD provides a super benefit that grows based on a formula and isn’t affected by the performance of investment markets.

7Defined Benefit Division GuideTHE DbD AND yOUR cHOIcES

DbD members have an ‘accumulation component’ tooAs a DBD member, your account has two parts: a defined benefit component and an accumulation component. Your defined benefit component and your accumulation component are added to work out your account balance.

WE’RE HERE TO HELP

We’re available on your campus to help with information and general advice about your membership and our range of products. You might find it beneficial to speak to one of our consultants — either on campus or at one of our member centres.Visit unisuper.com.au/oncampus to book an appointment.

Any extra contributions, transfers and investment

returns (which can be positive or negative), less any fees, costs, taxes and

insurance premiums.

What you end up with at retirement

ACCUMULATION COMPONENT

DEFINED BENEFIT

your account balance

8 1800 331 685UNISUPER.COM.AU

X

X

X

X

5-YEARBENEFITSALARY

This is generally your average salary over

the last five years when contributing to the DBD

LUMP SUMFACTOR

This is based on your age when we calculate your

defined benefit

AVERAGECONTRIBUTION

FACTOR

This reflects your level of member contributions to

the DBD

BENEFITSERVICE

This is the length of time you’ve been a DBD

member

AVERAGESERVICE

FRACTION

This reflects your level of full-time, part-time employment and can include allowances

The value of your defined benefit is calculated using the DBD formula.

Your defined benefit

For a full explanation of this formula—plus detailed examples of how it works— visit unisuper.com.au/pds and read the More about the DBD and Accumulation 2 document.

We’re available on your campus to help with information and general advice about your membership and our range of products. You might find it beneficial to speak to one of our

consultants — either on campus or at one of our member centres.

Visit unisuper.com.au/oncampus to book an appointment.

9Defined Benefit Division GuideTHE DbD AND yOUR cHOIcES

your accumulation componentIn addition to the defined benefit part of your super, you’ll have another part called an ‘accumulation component’. This is like the super you might already be used to: > it’s a bit like a bank account > it moves up and down with investment markets,

and > you can choose how to invest it.

If you receive employer contributions at the rate of 17%, then 3% will go into your accumulation component (unless you choose to reduce your default member contributions). Read more about this on page 16.

You can transfer super from your other funds into your accumulation component, so you can have all your super in one place and avoid paying multiple sets of fees.

you receive inbuilt benefits and insurance coverWhen you join the DBD, you automatically receive ‘inbuilt benefits’, which can cover you if you’re temporarily or permanently unable to work, terminally ill, or if you die. They’re calculated based on formulas too, and they’re automatically part of your membership (you can’t opt out of them). A three-year pre-existing condition exclusion (PEC) period applies to inbuilt benefits, which means a benefit may not be payable for any condition (e.g. illness or injury) that existed at the time of joining the DBD for a period of three years.1

If you’re joining UniSuper as a DBD member, you’ll generally also get one unit of insurance cover for death and total and permanent disablement (TPD) on competitive terms through our Insurer (which you can change or opt out of).2 This is called ‘default cover’.

Read the ‘More than just super – inbuilt benefits and insurance’ section on page 20 for more information about how your DBD membership can help protect you when you’re most in need.

Your options when you join the DBDWhen you’re a brand new DBD member, you have two years to decide if the DBD suits you. If it doesn’t, you can choose our ‘Accumulation 2’ product. To find out more about Accumulation 2, and whether it might suit you, read the Accumulation 2 Guide.

1 For more information about inbuilt benefits, including restrictions, what happens if you’re no longer working or have lowered your contribution amounts, visit unisuper.com.au/pds and read the More about the DBD and Accumulation 2 document

2 For more information on the default cover you receive when joining UniSuper, visit unisuper.com.au/pds and read the Insurance in your super document, as well as information on page 20.

ACCUMULATION 2DEFINED BENEFITDIVISION

You have two years to choose which

product to stay with.

10 1800 331 685UNISUPER.COM.AU

There are two styles of superannuation in Australia: defined benefit and defined contribution.

Defined benefit account balances are calculated using a formula, usually incorporating your age, salary and length of membership (amongst other things), whereas defined contribution balances reflect the money added to and taken from your account, as well as the returns on the investment options you select (positive or negative).

DBD members have both of these styles of super. The DB component is a defined benefit, whereas the accumulation component is defined contribution.

If you choose the Accumulation 2 product over the DBD, all of your super will be defined contribution.

What is Accumulation 2? > It’s a bit like a bank account. > It moves up and down with investment markets. > You can choose how to invest it. > You can tailor your insurance cover to meet your

needs.

Read the Accumulation 2 Guide for full details.

The DbD may not be the right option for everyone Broadly speaking, the DBD may suit members intending to pursue a reasonably long career in higher education and/or members who are expecting some salary growth arising from promotion or reclassification to higher roles during their career.

By extension, the DBD may not suit members anticipating only a short period of employment in higher education and/or members who are expecting little or no salary growth arising from promotion or reclassification to higher roles.

These are generalisations about the suitability of the DBD. They may not apply to your individual circumstances. They can be affected by many variables including your age and employment patterns. That’s why it’s important you spend some time considering the resources we provide to help you make your decision. Remember, you can always make an appointment with a member of our team to ask any questions you might have.

There is no standard or default investment option within the superannuation industry, although in defined contribution super, a ‘Balanced’ option (with about 70% in growth assets and 30% in defensive assets) is the most popular.

The main attraction of defined contribution super is that it provides much more flexibility for members who want to change their investment preferences. A cost of this flexibility, however, is exposure to the fluctuations of investment markets.

Another potential positive of defined contribution super over defined benefit super (like our DBD) is the consistent treatment of people of different ages. In other words, regardless of your age or how long you’ve been employed, your return will always be linked to the return of the market.

On the other hand, as with all products that work on the basis of risk-pooling, the final outcome for any individual in the DBD will vary depending on different factors (as shown in the formula above). The practical effect of this is that, while DBD members are able to enjoy a smooth return outcome, the absolute return for some members will be higher or lower than for others.

11Defined Benefit Division GuideTHE DbD AND yOUR cHOIcES

DbD and Accumulation 2 outcomes Your defined benefit grows according to a formula and is not intended to grow in line with investment returns on your contributions. This means your benefit does not decrease every time investment markets experience negative returns.

Depending on your situation, there may be times when your defined benefit is less than the sum of your contributions plus the investment returns which our investment options could have earned (or were targeting) if you were an Accumulation 2 member.

Generally speaking, the younger you are and the shorter the period of time you spend in the DBD, the greater the chance your defined benefit will grow at a rate which is less than the investment

return objective of our Balanced investment option. However, this could also be the case regardless of your age and the time you spend in the DBD.

The rate at which your defined benefit grows, and how this compares to the investment returns available through Accumulation 2 membership, depends on complex interactions between the variables in our defined benefit formula, your personal circumstances, which investment options you would have chosen if you were an Accumulation 2 member and how they perform. These are hard to predict in advance.

HOW DO I WORK OUT WHAT’S bEST FOR ME?

While UniSuper believes the DBD is a good default option to smooth and share risk in a volatile investment environment, all new DBD members should consider whether they should elect to move to Accumulation 2.

We provide valuable materials on our website (visit unisuper.com.au and search ‘your first year with UniSuper’) to help you understand the DBD and consider your circumstances when deciding whether to stay in or opt out of it. We also provide face to face consultations with specially trained UniSuper staff at no additional cost—often at your workplace or in our offices—to help you understand what the DBD and Accumulation 2 can do for you. You can book one of these consultations on our website.

The rate at which your defined benefit grows may or may not be a significant factor in your decision to remain a DBD member. You may prefer to base your decision on the relative certainty that defined benefits can provide (because they’re insulated from the fluctuations of financial markets), the very low risk of losing money and the peace of mind that this provides.

Alternatively, you may prefer defined benefits because of expected growth in your future salary, how long you expect to remain a DBD member, and how old you expect to be when you leave or retire. The insurance benefits available through the DBD may be another factor, especially after taking into account the cost of insurance premiums for Accumulation 2 members.

When thinking about the rate at which your defined benefit grows on your contributions to the DBD, it’s important to bear in mind that if your contributions had instead been made to Accumulation 2, your investment returns would depend on which investment options you’d chosen. Different investment options target different rates of return —some higher, some lower, depending on how aggressive or conservative they are). The actual rate of return depends on conditions in the relevant financial markets and the performance of the securities in which we and our investment managers invest on your behalf. For many investment options, there is a risk of negative returns in some periods.

12

How does your super grow?In the DBD, your super grows through a number of different ways. Here’s an overview.

Through contributionsDifferent types of contributions can go into your super, as illustrated opposite.

DEFAULT MEMbER cONTRIbUTIONSTo give you the best chance at having enough in retirement, as a DBD member you’ll make extra super contributions either on an after-tax basis or—with your employer’s agreement—on a before-tax basis. These are called ‘default member contributions’. They’re over and above the contributions your employer makes and are necessary if you want to maintain your full defined benefit entitlements.

You can lower your default member contributions if you want to, but contributing less will affect the DBD formula by reducing your Average Contribution Factor and your inbuilt death benefit. If you’re a DBD member and reduce your default member contributions you cannot increase your contributions to the DBD fund. However you can make extra super contributions to your accumulation component.

For more information on the impact of reducing your default member contributions, read the More about the DBD and Accumulation 2 document.

For more information about contributions, see page 16.

WE’RE HERE TO HELP

We’re available on your campus to help with information and general advice about your membership and our range of products. You might find it beneficial to speak to one of our consultants — either on campus or at one of our member centres.Visit unisuper.com.au/oncampus to book an appointment.

Contribution types

Employer contributions (equal to 17% or 14% of your salary)

Default member contributions

Other contributions (optional and subject to eligibility)

Co-contributions (subject to eligibility)

THE GOVERNMENT MAKES:

YOUR EMPLOYER MAKES:

YOU MAKE:

13Defined Benefit Division GuideHOW DOES yOUR SUPER GROW?

Through your accumulation componentDBD members can invest their accumulation component in our range of 16 investment options.

Any contributions you make above ‘default member contributions’ and any super you transfer in from other funds will be allocated to your accumulation component.

Simply put, the longer you’re in the DBD, the more time you spend working full-time, the more time you contribute ‘default member contributions’ and the higher your salary when you’re approaching retirement, the better the DBD formula is going to work for you and the greater your retirement income will be.

For information about our investment options—including how they’re invested, the different asset mixes and the different levels of risk associated with them—visit unisuper.com.au/pds and read the How we invest your money document.

For information about part-time work, taking parental or unpaid leave, reducing your default member contributions—and how all this can affect your formula—visit unisuper.com.au/pds and read the More about DBD and Accumulation 2 document.

If you want to know more about Accumulation 2, read the Accumulation 2 Guide.

WHAT DOES IT cOST?We’re committed to providing you with value for money. The fees we charge cover the costs of managing your account and investments. We don’t pay advisers commissions, and we don’t pay shareholder dividends.For information about the fees and costs associated with being a DBD member, read the ‘Fees and other costs’ section on page 30.

The DBDA closer look

16

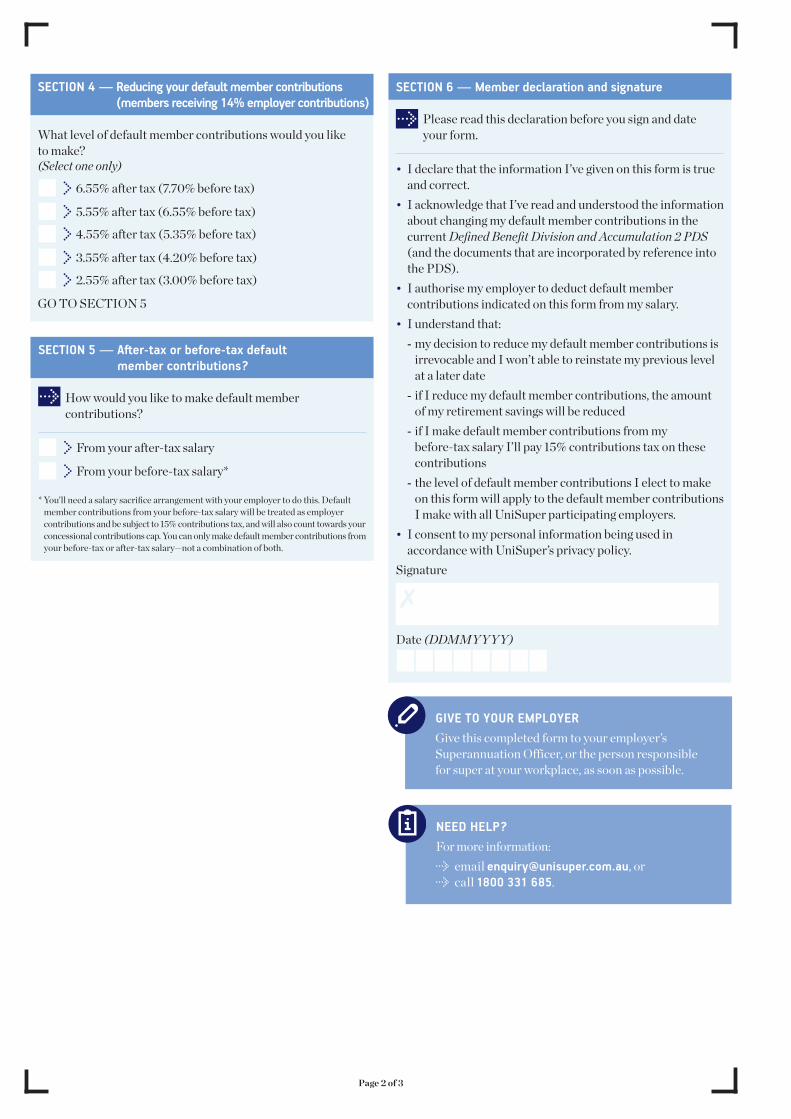

LOWERING yOUR DEFAULT MEMbER cONTRIbUTIONSYou can lower your default member contributions to zero if you receive 17% employer contributions, or to a minimum of 2.55% after tax - or 3% before tax (with agreement of your employer) if you receive 14% employer contributions.3

If you do lower them: > you’ll receive more take-home pay, but you’ll

reduce the size of your super savings over the long term

> your inbuilt death benefit may be lower > you may not have enough funds in your

accumulation component to pay insurance premiums (if you have any insurance cover)

> you may need to satisfy extra criteria to receive default cover through our Insurer

> you can’t increase them at a later date. If you want to make additional member contributions in the future, they’ll be made as voluntary contributions and go into your accumulation component.

Read the More about the DBD and Accumulation 2 document at unisuper.com.au/pds for the available levels of default member contributions and the impacts that reducing them can have on: > your ‘defined’ super and inbuilt benefits, and > your eligibility for default cover.

Employer contributionsAs a DBD member, your employer will be making generous contributions to your super—equal to 14% or 17% of your salary (depending on the terms of your employment).

If you receive 17% employer contributions these are split by: > 14% going to your defined benefit component, and > 3% going to your accumulation component.

Note: > If you lower your default member contributions,

the 3% employer contribution will go to your defined benefit component.

> If you receive 14% employer contributions, this entire contribution will go to your defined benefit component.

> We’re required to deduct a 15% contributions tax from employer and before-tax (salary sacrifice) contributions, and an extra 32% ‘no TFN contributions tax’ if we don’t have your tax file number.

Default member contributionsIn addition to employer contributions, DBD members make ‘default member contributions’. The default level of member contributions for new DBD members is 7% after tax—or 8.25% before tax (and with the agreement of your employer)—of your salary. Your default member contributions (if any) are used to fund your defined benefit component.

Contributing to superHere’s an overview of the ways to contribute to super as a DBD member.

3 The minimum is 3% if your employer agrees to you making default member contributions on a before-tax basis. Your employer will maintain their contribution level.

17Defined Benefit Division GuidecONTRIbUTING TO SUPER

cONTRIbUTING TO THE DbDContributions made to your defined benefit component are first used to meet the 15% contributions tax applicable to employer contributions and any before-tax member contributions. They’re then used for the provision of inbuilt benefits and—along with investment returns after expenses—the payment of retirement and resignation benefits to members. For this reason, you can’t make a direct comparison between these contributions and the balance of your defined benefit component.

Other contributions

VOLUNTARy cONTRIbUTIONSThese are optional contributions made over and above your default member contributions, and go into your accumulation component. Voluntary contributions include salary or after-tax contributions and after-tax lump sum contributions.

If you’re 65 or over and are looking to sell the family home, you may also consider making ‘downsizer’ contributions with the proceeds. Read the More about the DBD and Accumulation 2 document at unisuper.com.au/pds for more information.

GOVERNMENT cO cONTRIbUTIONSIf your total income is $38,564 per year or less for 2019-20, the Government will contribute $0.50 to your account for every dollar of non-concessional (after-tax) contributions you make into super, up to a maximum of $500. This is called a ‘co-contribution’.

Read the More about the DBD and Accumulation 2 document at unisuper.com.au/pds for more information.

contribution limitsThere are limits, called ‘contributions caps’, on how much money can go into your super each financial year and still receive favourable tax treatment. You may pay a higher tax rate on any contributions that exceed the caps.

cONTRIbUTION cAPS (2019-20)

Concessional cap4 Non-concessional cap5

$25,000 $100,000

cONSIDER yOUR NOTIONAL TAXED cONTRIbUTIONSIt’s important to note when considering your contributions caps how notional taxed contributions (NTCs) apply to DBD members. NTCs are the notional amount of contributions—excluding non-concessional (after-tax) contributions—that relate to your defined benefit component. NTCs count towards your concessional contributions cap and are added to the other concessional (before-tax) contributions made to your accumulation component in a financial year.

For more information, read the following fact sheets available at unisuper.com.au/factsheets : > The concessional contributions cap and NTC

rates for DBD members receiving 17% employer contributions

> The concessional contributions cap and NTC rates for DBD members receiving 14% employer contributions.

cONTRIbUTION cAPSExceeding contribution caps may have tax implications. Visit unisuper.com.au/pds and read the How super is taxed document.

4 A 15% tax applies to these contributions. Concessional contributions may be taxed at a higher rate if Division 293 applies. Read the How super is taxed document at unisuper.com.au/pds for more details.

5 An additional lifetime cap called the ‘total super balance’ applies to these contributions. Read the How super is taxed document at unisuper.com.au/pds for more details.

18

WHEN yOU RETIRE OR LEAVE yOUR JObIf you retire, you can access your account balance (calculated using the DBD formula set out in the More about the DBD and Accumulation 2 document at unisuper.com.au/pds ), provided you’ve: > reached your ‘preservation age’, or > are no longer employed for reasons other than

disablement (including being temporarily unable to work due to injury or illness) death, or suffering a terminal medical condition.

It’ll also include your accumulation component (including investment returns, which may be positive or negative), minus any fees, costs, charges and taxes.

bEING TEMPORARILy UNAbLE TO WORK, TOTALLy AND PERMANENTLy DISAbLED (TPD), TERMINALLy ILL, OR DyINGIf you’re temporarily unable to work due to injury or illness, an inbuilt temporary incapacity benefit may be payable if you satisfy the eligibility requirements.

If you’re permanently disabled, an inbuilt disablement benefit and any TPD insurance cover you hold may be payable.

If you become terminally ill, you may be able to receive an inbuilt terminal medical condition benefit (this is equivalent to your inbuilt death benefit). If you have any external insurance cover, a terminal illness benefit may also be payable.

If you die, a death benefit will be payable to your eligible beneficiaries. Any death insurance cover you hold may also be payable to you if you satisfy the terms of the insurance policy.

Note that different eligibility requirements apply for inbuilt benefits and insurance cover provided by our Insurer and each is assessed separately. To understand the differences between insurance and inbuilt benefits and your eligibility, read the ‘More than just super – inbuilt benefits and insurance’ section on page 20 For further details, visit unisuper.com.au/pds and read the More about the DBD and Accumulation 2 and Insurance in your super documents.

You usually can’t access your super until you’ve reached a certain age (called your ‘preservation age’) and retired, but there are some special circumstances (called ‘conditions of release’) where you can withdraw it earlier, including: > retiring permanently from work once you’ve

reached your preservation age > ceasing employment on or after the age of 60 > turning 65 > permanent incapacity > having an account balance of less than $200 when

you terminate employment with an employer who contributed to UniSuper, and

> death.

For information about additional special circumstances and accessing your super, visit unisuper.com.au/pds and read the More about the DBD and Accumulation 2 document.

When can you access your super?Restrictions are imposed under UniSuper’s Trust Deed which limit when you can access your defined benefit component. Generally, you can only withdraw all or part of your defined benefit component if that component consists entirely of unrestricted non-preserved super (meaning super that isn’t subject to a condition of release and can be paid to you on request).

If you withdraw all or part of your defined benefit component, you’ll cease to be a DBD member and generally any remaining defined benefit component will be transferred together with your accumulation component to an Accumulation 1 account. Any future employer and member contributions will be made into the Accumulation 1 account.

Different rules apply to requests to withdraw benefits on the grounds of severe financial hardship or ATO-approved compassionate grounds.

Accessing super There are restrictions on withdrawing your money from super funds.

19

There are many rules around beneficiary nominations, including who you can and can’t nominate, what constitutes a valid nomination and administrative things like how to update or cancel a nomination.

Read the information about beneficiary nominations in the More about the DBD and Accumulation 2 document, available at unisuper.com.au/pds , before making a decision.

You can make two types of beneficiary nominations: > non-binding beneficiary nominations, and > binding death benefit nominations.

For binding death benefit nominations, you can also specify whether your nomination is ‘lapsing’ (it expires after three years) or ‘non-lapsing’ (it doesn’t expire).

Nominating beneficiariesIt’s worth considering who you’d like to leave your super and other benefits to if you die. The people you nominate are called ‘beneficiaries’.

20

When you join the DBD, subject to eligibility, you’re provided with inbuilt benefits as part of your membership. These include benefits for temporary incapacity, terminal medical condition, disablement and death. A three year pre-existing condition (PEC) generally applies from the date inbuilt benefits commence.

If you’re joining UniSuper as a DBD member you’re generally also provided with one unit of default Death and Total and Permanent Disablement (TPD) insurance cover—‘default cover’—through our Insurer. You can apply to increase or cancel this cover at any time.

If you’re receiving 17% employer contributions and are eligible for default cover, you may also be eligible to apply for up to two additional units of Death and/or TPD cover within 180 days of being first eligible to join UniSuper, without having to provide evidence of your health to our Insurer.

If you cancel your default cover, you can always apply again later on. You’ll just need to give us some detailed health information to have our Insurer assess you. Exclusions and/or loadings may apply to the cover you apply for.

WHAT ARE INbUILT bENEFITS?‘Inbuilt benefits’ is the term used to describe benefits payable to DBD members or their beneficiaries in the event of disablement, temporary incapacity, suffering a terminal medical condition and death.Inbuilt benefits are: > calculated based on formulas > self-insured by UniSuper (i.e. not an

external insurance provider) > not an additional cost > part of the DBD so you can’t opt out

of them.You should read the important information about the eligibility requirements of inbuilt benefits before making a decision. Visit unisuper.com.au/pds and read the More about the DBD and Accumulation 2 document.

More than just super – inbuilt benefits and insuranceOne of the great benefits of your DBD membership is being covered if the worst should happen.

21Defined Benefit Division GuideMORE THAN JUST SUPER – INbUILT bENEFITS AND INSURANcE

DBD OR ACCUMULATION 2?Within your first two years as a DBD member you can choose to remain in the DBD or switch to Accumulation 2

YOU JOIN THE DBDAnd you’ll generally receive two types of cover

INBUILT BENEFITSReceive inbuilt benefits for temporary incapacity,

terminal medical condition, disablement and death. You can’t change or opt out of inbuilt benefits.

INSURANCE COVERReceive one unit of default Death and TPD cover

through our external insurer. You can cancel or increase your cover (subject to the approval

of our Insurer).

SWITCH TO ACCUMULATION 2Inbuilt benefits transition to external insurance cover

(‘transitioned cover’), some or all of which may be subject to a pre-existing condition (PEC) exclusion. Any existing external

insurance cover comes with you. Your total cover consists of any existing external cover

plus ‘transitioned cover’.

REMAIN IN THE DBDYou keep your inbuilt benefits

and existing external insurance cover. You can increase (subject to approval by our Insurer) or cancel

your external insurance cover.

An overview of insurance through DbD and Accumulation 2 membership

For detailed information about inbuilt benefits, visit unisuper.com.au/pds and read the More about the DBD and Accumulation 2 document. For information about external insurance cover, visit unisuper.com.au/pds and read the Insurance in your super and What happens to your inbuilt benefits if you choose Accumulation 2? documents.

We’re here to helpWe’re available on your campus to help with information and general advice about your membership and our range of products. You might find it beneficial to speak to one of our consultants — either on campus or at one of our member centres.

Visit unisuper.com.au/oncampus to book an appointment.

22 1800 331 685UNISUPER.COM.AU

MORE INFORMATIONFor detailed information about inbuilt benefits for disablement, temporary incapacity, terminal medical condition and death provided with DBD membership, read the More about the DBD and Accumulation 2 document.For detailed information about external insurance cover through our Insurer (including ‘default cover’), read the Insurance in your super document.

IF yOU bEcOME TEMPORARILy UNAbLE TO WORKProvided you satisfy the relevant requirements, you may be entitled to a monthly payment (known as an inbuilt temporary incapacity benefit) for up to two years. This benefit is calculated using the formula set out in the More about the DBD and Accumulation 2 document at unisuper.com.au/pds

Temporary incapacity is generally a state of health which, in the opinion of the Trustee, leaves you unable to perform your own duties or any other duties for which you’re reasonably qualified by training and experience at your place of employment.

It’s important to note that you’ll need to have been away from work (due to the relevant illness/injury) for 60 days (pro-rata if you work part time) within a period of twelve consecutive months immediately prior to lodging your claim—and exhausted all your sick leave—before qualifying.

For more information about how and when these benefits will be paid, read the Inbuilt disablement benefits for DBD members and Inbuilt temporary incapacity benefits for DBD members fact sheets at unisuper.com.au/factsheets

Types of benefits and insurance available

IF yOU bEcOME PERMANENTLy DISAbLEDIt’s important to note that different criteria apply—and different definitions need to be satisfied—for an inbuilt disablement benefit and a TPD benefit.

Inbuilt disablement benefitProvided you satisfy the relevant requirements, you may be entitled to a monthly payment until you reach age 65—known as an inbuilt disablement benefit—calculated using the formula set out in the More about the DBD and Accumulation 2 document at unisuper.com.au/pds

We’ll consider you ‘disabled’ if you’re permanently incapable of performing duties or engaging in employment for which you’re reasonably qualified by training and experience, where you’ve been absent from work—because of injury or illness—for the waiting period (which is generally sixty working days within a period of 12 consecutive months), prior to ceasing employment.

TPD benefitIf you have insurance cover for TPD you may also be entitled to a one-off payment equal to the level of cover you hold.6

In general terms, ‘total and permanent disablement’ means you’re unlikely—because of illness or injury—to undertake paid work for which you’re reasonably qualified by education, training or experience.

Accumulation componentIf you can show that you’re permanently incapacitated and satisfy criteria set out within super law, you can also access your accumulation component (including investment returns—which may be positive or negative—minus any fees, costs, charges and taxes).

Refer to the definitions section of the Insurance in your super document at unisuper.com.au/pds for the full definitions.

6 Subject to the approval of our Insurer, who pays the one-off payment to UniSuper—we then release it to you, provided you meet a condition of release. Read the Insurance in your super document at unisuper.com.au/pds for more information.

23Defined Benefit Division GuideMORE THAN JUST SUPER – INbUILT bENEFITS AND INSURANcE

‘UNITISED’ AND ‘FIXED’ cOVERBy default, Death and TPD insurance cover is provided as unitised cover, but if you’re under 61, you can convert it to fixed cover if you want to.

‘Unitised cover’ means the cost of each unit stays the same over time, but the amount of cover you get for each unit reduces as you get older.

‘Fixed cover’ means the cost of your cover increases over time, but the amount of insurance you get stays the same until you turn 61.

Some important notes about fixed cover: > You can’t have both fixed and unitised cover (you

either have one or the other). > If you do choose fixed cover, you can’t ever convert

back to unitised cover. > You can’t ‘fix’ your level of inbuilt benefits, as

they’re determined by a formula. > If you’ve already got TPD cover when you convert

to fixed cover, from age 61 your TPD cover will reduce by 10% each year until you’re insured for $0 at age 70.

Find out more about fixed cover and the premiums applicable in the Insurance in your super document at unisuper.com.au/pds

Tailoring your external insurance coverYou can apply: > to increase your cover > for Death and/or TPD cover if you don’t meet the

eligibility criteria for default cover, or now wish to have this cover if you opted out when you first joined.

How to apply: > Log into your account online and go to the

insurance section, or > Complete the application form in the Insurance in

your super document at unisuper.com.au/pds , or > Call 1800 331 685 and we can arrange for you to

complete your application over the phone.

All applications for external insurance cover (excluding additional default cover) are subject to our Insurer’s approval. Note that the Insurer may accept or decline your application, or impose special conditions like restrictions, exclusions and loadings on premiums.

IF yOU bEcOME TERMINALLy ILL OR DIEIf eligible, you’ll be entitled to a one-off payment calculated using the formula set out in the More about the DBD and Accumulation 2 document at unisuper.com.au/pds

If you have external insurance cover for death, an additional one-off payment—equal to the amount of cover you hold—may also be payable (your estate and/or beneficiaries will need to make a separate claim for it).7

You’ll receive an insured terminal illness payment if you’re diagnosed with a terminal illness and satisfy any other applicable criteria. If a terminal illness payment is made and the Death cover is higher, any remaining Death cover is payable on death.

The total benefit payable will also include your accumulation component (including investment returns—which may be positive or negative—minus any fees, costs, charges and taxes).

Transferring to the DBD from our Accumulation 1 or Personal Account product?You may already have external Death and TPD insurance cover. This cover will continue when you join the DBD and include any existing restrictions, loadings and exclusions. Insurance premiums will be deducted from your accumulation component.

When you join the DBD, even though inbuilt benefits are automatically provided, a three-year PEC exclusion is generally applied to your Death and TPD cover.

Any Income Protection cover you hold ceases on joining the DBD.

More information about default coverYou’re generally provided with one default unit of Death and TPD cover upon joining UniSuper, which you can change to Death-only or TPD-only cover, or even cancel altogether if you want to. Significantly, if eligible, you can apply to increase the amount of this default cover by up to two additional units without providing evidence of your health to our Insurer if you apply within 180 days of first being eligible to join UniSuper.

You can do this by completing the appropriate sections of the Defined Benefit Division/Accumulation 2 changing your default option form, or later by: > logging into your account online, or > completing the Changing your insurance cover

form available at unisuper.com.au

7 Subject to the approval of our Insurer, who pays the one-off payment to UniSuper—we then release it to you, provided you meet a condition of release. Read the Insurance in your super document at unisuper.com.au/pds for more information.

24

The DBD’s central investment objective is to maximise the probability of generating sufficient returns to meet its future benefit payments. It’s currently in a very healthy position, as reflected by a vested benefit index (VBI) and an accrued benefit index (ABI) that sit comfortably above 100%.

Ideally this would allow us to adopt a more conservative investment strategy such as holding more bonds. However, yields currently on offer in the bond market are well below the returns required to satisfy our central objective, and expectations are that low yields will persist for some time.

Accordingly, we’re likely to continue our current strategy which entails holding a high proportion of the portfolio in high quality growth assets, although actual asset allocations may deviate within forward allocation ranges depending on prevailing market conditions.

The DBD is backed by a $28 billion8 asset pool invested across a range of asset classes including shares, property, infrastructure, bonds and cash. As a DBD member, most of your contributions are invested in this asset pool. Most DBD members will also have an accumulation component which can be invested in our range of 16 investment options, with the default option being our Balanced option. For more information about our investment options—including how they’re invested, the different asset mixes and the levels of risk associated with them—read the How we invest your money document at unisuper.com.au/pds

While your individual defined benefit isn’t directly affected by the market performance of the pool of assets, the overall health of the DBD will heavily depend on the performance of the portfolio, so an effective investment strategy is crucial.

UniSuper’s Trustee is ultimately responsible for approving the investment strategy of all investment options, including the DBD. The Trustee in turn delegates the responsibility to execute the strategy to UniSuper’s Investment Committee and team of investment professionals.

Currently, the DBD’s asset portfolio is heavily skewed towards quality assets that generate sustainable income streams, with the potential for capital growth that we expect can at least keep pace with inflation.

The following pie chart shows the general asset allocation of the DBD portfolio as at 30 June 2019. The Australian and international shares component is largely comprised of ‘blue-chip’ companies that have a history of paying dividends. The Property component is largely concentrated in high quality retail and commercial assets, and infrastructure including ‘fortress’ assets such as airports.

How we invest your moneyHere’s an overview of how we invest your money as a DBD member.

57% Australian

shares

15% Fixed interest and cash

7% Infrastructure and private equity

8% Property

13% International

shares

DbD ASSET ALLOcATIONAS AT 30 JUNE 2019

8 Approximate as at 30 June 2019.

25

All investments, including super, have some level of risk.

Investment risk is the potential for your accumulation super to rise or fall due to how it is invested.

Different strategies may carry different levels of risk, depending on the assets that make up the strategy. Those assets with the highest potential return over the longer term (such as equities) may also have the highest risk of losing money in the shorter term.

Investment risks associated with your account include the risk of negative returns from a specific investment, risk of underperformance by an investment manager, market risks, risks associated with poor performance by investments in particular markets or countries, currency risk, credit risk, inflation risk, liquidity risk and risks associated with the use of derivatives.

Other risks include potential changes to legislation and taxes that may apply in the future, the risk that events beyond our control may impact our administration, including the ability to process transactions, cyber risk and the risk that our Trust Deed or fees and costs may change.

There’s also a risk that we may discontinue a particular investment option in the future or make changes to the investment strategy or objective of an option. We’d give you advance notification if any investment options were to be discontinued.

When considering your investment in super, it’s important to understand that: > the value of investments will go up and down > the level of investment returns will vary and

future returns may differ from past returns > investment returns are not guaranteed and you

may lose some of your money > super laws may change in the future > the appropriate level of risk for you will depend

on a range of factors including your age, your investment time frame, your other investments and your personal risk tolerance

> you may not contribute enough, or work enough (e.g. full-time or part-time), to produce an adequate retirement benefit.

Defined benefits are supported by a pool of assets into which you and your employer contribute, and which we invest in a diversified portfolio of investments. We’ve designed the DBD so that in the longer term, investment returns are expected to be sufficient to provide for UniSuper’s defined benefits, although this is not guaranteed. Over short periods, the funding position may vary with investment volatility.

There’s also a risk that the defined benefit pool could be insufficient to meet all obligations to DBD members, meaning your defined benefit may be reduced.

The More about the DBD and Accumulation 2 document, available at unisuper.com.au/pds, details these and other significant risks of super for both DBD and Accumulation 2 members.

Risks of superYour super is designed to provide you with an income for retirement. It aims to build your retirement savings in a cost-effective, tax-efficient way. But there are certain risks you should be aware of.

26

Tax on contributionsThis table is an overview of tax on contributions to super. It assumes you’ve provided us with your tax file number (TFN).

MAIN TyPES OF cONTRIbUTIONS

HOW MUcH TAX IS PAID HOW THE TAX IS PAID

Concessional (before-tax) contributions: > Superannuation

Guarantee (SG) employer contributions

> Salary sacrifice contributions made by your employer from your before-tax salary

> Personal contributions where you provide us with a valid form that states your intention to claim a tax deduction, and

> Notional taxed contributions for your defined benefit interest.

15% on contributions up to the concessional (before-tax) contributions cap.*

Where the concessional (before-tax) contributions are paid into your accumulation component the tax is deducted from that account.

Tax on notional taxed contributions is deducted from the defined benefit pool of assets. No charge is deducted directly from your accumulation component.

Contributions which exceed your concessional contributions cap are included in your assessable income and taxed at your marginal tax rate. An excess concessional contributions charge will also apply.

You’ll also be entitled to a 15% tax offset on the excess concessional contribution (because you have already paid tax on this money). The offset is not refundable.

You can release up to 85% of your excess concessional contributions from your accumulation component. Amounts cannot be released from your defined benefit interest.

Any excess concessional contributions not released from super are counted towards your non-concessional (after-tax) contributions cap.

Any excess concessional contributions you release from your super account will no longer count toward your non-concessional contributions cap.

The ATO will provide you with an assessment. The tax is paid ‘out of your pocket’ to the ATO. If you choose to release some of your excess contributions, we pay this to the ATO, who will offset it against any outstanding tax or other Australian Government debts you have before refunding any remaining balance.

How super is taxedSuper can be a tax-effective way to save for retirement because the Government provides tax breaks and incentives. Here’s how tax can affect your super.

* If your income for ‘Division 293 tax’ exceeds $250,000 during an income year, additional tax may apply to your concessionally-taxed contributions. For more details, visit unisuper.com.au/pds and read the How super is taxed document.

27Defined Benefit Division GuideHOW SUPER IS TAXED

MAIN TyPES OF cONTRIbUTIONS

HOW MUcH TAX IS PAID HOW THE TAX IS PAID

Non-concessional (after-tax) contributions: > Personal contributions

that haven’t been claimed as a tax deduction

> Contributions your spouse makes on your behalf. These are treated in the same way as after-tax contributions, provided your spouse doesn’t claim the contribution as a tax-deductible employer contribution and provided you’re not living separately from your spouse

> Excess concessional contributions not released from your super account.

There’s no tax payable on non-concessional contributions made up to your non-concessional contributions cap.

N/A

If you exceed the non-concessional contributions cap, you may choose to release the super contributions in excess of your non-concessional contributions cap plus 85% of any associated earnings. Amounts cannot be released from your defined benefit interest.

The associated earnings released are taxed at your marginal tax rate. You will also be entitled to a 15% tax offset on the associated earnings included in your assessable income (because you’ve already paid contributions tax on this money).

The offset is not refundable.

The ATO will provide you with an assessment.

The funds released are paid from us to the ATO, who will offset it against any outstanding tax or other Australian Government debts you have before refunding any remaining balance.

If you choose not to release your excess non-concessional contributions they will remain in your super account and the excess will be taxed at 47%.

The excess contributions tax is paid out of your nominated super account.

* There’s 15% tax payable by your fund on concessional (before-tax) contributions paid into a super fund. Your super fund usually reduces your super account by your share of this tax.

** An additional lifetime cap—the total super balance—applies to non-concessional (after-tax) contributions. Read the How super is taxed document at unisuper.com.au/pds for more details.

contributions capsThe Government limits the amount of money—contributed by you or on your behalf—that can go into your super each financial year and still receive favourable (‘concessional’) tax treatment.

These ‘caps’ apply regardless of how many employers or super funds you have, and it’s your responsibility to monitor them.

You can exceed the caps, but you might pay more tax.

cONTRIbUTION cAPS (2019-20)

Concessional cap Non-concessional cap$25,000* $100,000**

Tax on transfersIf you transfer your super from one fund to another, there isn’t any tax payable unless the amount contains an untaxed element, e.g. from a public-sector super fund. Any untaxed element transferred to UniSuper is taxed at 15% when we receive it.

Tax on investment earningsInvestment earnings are generally taxed at up to 15%. This tax is deducted from the Fund’s investment earnings before they’re allocated to your account.

28 1800 331 685UNISUPER.COM.AU

Tax on withdrawalsYou may have to pay tax when you withdraw super from us. We’ll normally deduct any tax before paying you. The amount of tax will depend on things like your age and how your benefit is paid.

Your payment will generally be tax free if you’re 60 or older, but it may incur tax if you’re under 60. If you’re under 60 and haven’t provided a TFN, tax at the rate of 47% will generally be payable on the taxable component of a benefit payment made to you.

Regardless of your age, your payment may incur tax if it’s paid in other circumstances (like if you die and a death benefit is paid to a non-dependant for tax purposes).

MORE INFORMATIONVisit unisuper.com.au/tfn and read the important information about providing your TFN. You can also request a copy of that information, free of charge, by calling 1800 331 685.

Don’t pay any more tax than you have to!Your TFN is the unique, confidential number which links all your investments, super and taxation records to your identity. While it’s not compulsory to give us your TFN, if you don’t, any contributions or transfers that would attract tax (such as employer contributions or salary sacrifice contributions) may be taxed at the highest marginal tax rate and your benefit may be reduced.

It’s important for us to have accurate and up-to-date information about you to manage your account efficiently and protect your retirement savings. We use details such as your name, date of birth and also your TFN to: > match contributions and transfers from other

super funds to your account, and > verify your identity if you’re transferring super out

of UniSuper.

You can give us your TFN by logging into your account and going to the ‘Personal details’ page.

29

If you have an enquiry or complaint We hope that you don’t have any complaints about your super, but if you do, please contact us.

We’ll deal with your complaint and respond as quickly as possible. To make a complaint, call 1800 331 685 or write to:

Complaints Officer UniSuper Level 1, 385 Bourke Street Melbourne VIC 3000

Email: [email protected]

If our response to your complaint does not resolve it to your satisfaction, we have not resolved your complaint within 90 days or you would prefer to speak to someone else, then you can complain to the Australian Financial Complaints Authority (AFCA). AFCA provides a fair and independent complaint resolution service that is free to consumers.

You can contact AFCA at:

Australian Financial Complaints Authority GPO Box 3, Melbourne VIC 3001 Phone: 1800 931 678 (free call within Australia) Email: [email protected] Online: www.afca.org.au

It’s important to note there are time limits for lodging certain complaints. This includes complaints about the payment of a death benefit, which you must lodge with AFCA within 28 days of receiving our written decision.

Go to unisuper.com.au/complaints for more information.

How we protect your privacyWe recognise the importance of protecting your personal information and are committed to complying with our privacy law obligations.

We collect your personal information to administer your account, ensure you’re eligible for insurance cover, provide you with UniSuper membership benefits, services and products, verify your identity and improve our products and services. You consent to our collecting sensitive information about you, where collecting that information is reasonably necessary for us to perform one or more of our functions or activities. We usually collect personal and sensitive information directly from you, however, it may also be collected from third parties, such as your employer.

We may also collect this information from you because we’re required or authorised by or under an Australian law or a court/tribunal order to collect that information.

If you don’t provide this information, we may not be able to administer your account, provide you with a product or service or you may be disadvantaged in some other way.

We may disclose your information to any service provider we engage (for example mail-houses, auditors, insurers, actuaries, lawyers and research consultants) to carry out or help us provide your membership benefits, services and products. This includes overseas entities. The countries we may disclose personal information to are Japan, Canada and the United States of America. Where information is transferred overseas, we’ll seek to ensure the recipient of the data has security systems to prevent misuse, loss or unauthorised disclosure in line with Australian laws and standards.

Our Privacy Policy contains information about how you can access any personal information we hold, how to correct your information and how to make a complaint about a breach of the Privacy Act. It’s available at unisuper.com.au or by calling 1800 331 685.

General informationHere we outline some extra important information you should know as a UniSuper member.

30

These fees and costs may be deducted from your account, from the returns on your investment or from the assets of the superannuation entity as a whole.

Other fees, such as activity fees, advice fees for personal advice and insurance fees may also be charged, but these will depend on the nature of the activity, advice or insurance you choose.

Entry and exit fees cannot be charged.

You should read all the information about fees and other costs because it is important to understand their impact on your investment.

Taxes, insurance fees and other costs relating to insurance are set out in this Guide and the More about the DBD and Accumulation 2 document, available at unisuper.com.au/pds

The fees and other costs for the Balanced investment option, and each other investment option offered by UniSuper, are set out on page 33.

Fees and costs

cOMPETITIVE FEES AND NO cOMMISSIONSUniSuper members benefit from the savings we achieve as one of the largest super funds in the country—savings we pass on to you through competitive fees.

We don’t pay commissions, and our advisers don’t receive commissions.

Fees and other costsThis section shows you the fees and other costs you may be charged.

consumer advisory warning

DID yOU KNOW? Small differences in both investment performance and fees and costs can have a substantial impact on your long-term returns.

For example, total annual fees and costs of 2% of your account balance rather than 1% could reduce your final return by up to 20% over a 30-year period (for example, reduce it from $100,000 to 80,000).

You should consider whether features such as superior investment performance or the provision of better member services justify higher fees and costs.

You or your employer, as applicable, may be able to negotiate to pay lower fees.Ask the fund or your financial adviser.1

TO FIND OUT MOREIf you would like to find out more, or see the impact of the fees based on your own circumstances, the Australian Securities and Investments Commission (ASIC) website (www.moneysmart.gov.au) has a superannuation calculator to help you check out different fee options.

1 This text is required by law to be included in all PDSs. However, UniSuper’s fees are set at a competitive level that is consistent with effective management and are not negotiable by members.

31Defined Benefit Division GuideFEES AND OTHER cOSTS

DEFINED bENEFIT DIVISION

Type of fee Amount How and when paidInvestment fee Balanced investment option 0.42%1

per year The investment fee for the investment options your accumulation component is invested in accrues daily and is deducted from the Balanced investment option and any other option(s) you’re invested in (as relevant).1

Administration fee Currently, $221 per year is deducted from the assets of the DBD pool to meet the administration costs associated with your DBD account.*

The costs of administering DBD members are allowed for in the DBD formula and deducted from the defined benefit pool of assets. No charge is deducted directly from your account.

Buy-sell spread Nil. Not applicable.Switching fee The first switch per account in each

financial year is free of charge. All subsequent switches will be charged a fee of $9.85 per switch on the date the switch becomes effective.

If you’re invested in the Balanced investment option before submitting your request, the fee will be deducted in full from this option before the switch is completed.

If you’re not invested in the Balanced investment option, the fee is deducted proportionally from your investment option(s).

For DBD members, the fee will be deducted from the accumulation component.

Advice fees2 for all members investing in the Balanced investment option or any other investment option

Nil. Not applicable.

Other fees and costs2

Indirect cost ratio (ICR)3

Balanced investment option 0.13%1 per year

The ICR for the investment options your accumulation component is invested in accrues daily and is deducted from the Balanced investment option and any other option(s) you’re invested in (as relevant).1

* Government regulations require this fee to be stated here. It is, however, notional only, in that it is not deducted from your account or benefit when paid. It may be indirectly relevant to your final benefit in that it is deducted from the pool of money used to fund all defined benefits and could therefore be a contributing factor if UniSuper were to be unable to cover defined benefits (see ‘Risks of super’ on page 25).

1 The investment fee and ICR shown above are indicative only and are based on the investment fee and ICR for this investment option for the year ended 30 June 2019, including several components which are estimates. The actual amount you’ll be charged in subsequent financial years will depend on the actual fees and costs incurred by the Trustee in managing the investment option. From 1 October 2019, we anticipate that the ICR will decrease by up to 0.02% on the basis that the funding of the Operational Risk Reserve will reduce from 0.03% to 0.01%, although, as the ICR shown is an estimate only, it may increase or decrease depending on the actual fees and costs incurred. The amounts of investment fees and ICRs for other investment options are set out on page 33, and these are paid at the same frequency and in the same manner as the Balanced investment option. For further details, refer to the fees and costs applicable to your investment options on page 33.

2 Further fees and costs such as fees for personal advice and insurance fees may apply. For further information, refer to ‘Additional Explanation of Fees and Costs’ on page 32.

3 The ICR for the defined benefit component is allowed for in the formula used to calculate your defined benefit.

32 1800 331 685UNISUPER.COM.AU

ADDITIONAL EXPLANATION OF FEES AND cOSTS

Investment fees and indirect cost ratio (ICR)The investment fees and ICRs for the year ending 30 June 2019 can be viewed on page 33 or at unisuper.com.au/investment-costs. These costs show the total investment fees and indirect costs attributed to each of our investment options (excluding the fees that are charged directly to your account) as a percentage of the total average net assets of the relevant investment option.

Performance-based feesWe don’t directly deduct any performance-based fees from member accounts. However, some external investment managers may be entitled to receive performance-based fees if they generate strong investment returns. These are included in the investment fees and are indirectly borne by members invested in an option.

To receive performance-based fees, a manager must generate returns which exceed an agreed benchmark (in some cases by a margin or hurdle), in which case the manager is entitled to receive a percentage of the excess returns. The amount that can be recouped by any particular manager in one year is generally capped and fees in excess of the cap are carried forward into future years and can potentially be paid in future years, subject to generating adequate returns. If managers fail to generate excess returns in a year, this typically results in a negative amount being carried forward for future years to offset any performance-based fees which may otherwise become payable in future.

Note that managers generally manage portfolios comprising assets which relate to multiple investment options. It’s not possible to accurately predict the amount of performance-based fees that may be payable in respect of a particular investment option in the next financial year. This will depend on: > the investment returns generated during the year

ahead > which managers generate excess returns within

their portfolios > whether there were negative amounts (or positive

amounts) being carried forward for those managers

> the individual fee arrangements (if any) which had been negotiated with the relevant investment managers

> the size of the portfolios being managed by those managers, and

> the proportion of those portfolios which relate to the relevant investment option.

The table overleaf sets out the estimated investment fees and costs for each option.

33Defined Benefit Division GuideFEES AND OTHER cOSTS

INVESTMENT OPTION FEES AND cOSTS FOR THE yEAR ENDED 30 JUNE 2019

Option Investment Fees (%)1 Indirect Costs (%)1 Total (%)3

Conservative 0.32 0.28 0.60Conservative Balanced 0.34 0.30 0.64Balanced 0.42 0.13 0.55Sustainable Balanced 0.33 0.04 0.37Growth 0.50 0.19 0.69High Growth 0.51 0.16 0.67Sustainable High Growth 0.38 0.04 0.42Cash2 0.14 0.04 0.18Australian Bond2 0.18 0.04 0.21Diversified Credit Income 0.33 0.04 0.36Listed Property4 0.24 0.09 0.33Australian Shares 0.37 0.33 0.70International Shares 0.60 0.04 0.64Global Environmental Opps 0.44 0.04 0.48Australian Equity Income 0.39 0.04 0.42Global Companies in Asia 0.45 0.04 0.48

1 The investment fees and ICRs shown above are indicative only and are based on the investment fees and ICRs for the year ended 30 June 2019, including several components which are estimates. The actual amount you’ll be charged in subsequent financial years will depend on the actual fees and costs incurred by the Trustee in managing the relevant investment option. From 1 October 2019, we anticipate that the ICR will decrease by up to 0.02% on the basis that the funding of the Operational Risk Reserve will reduce from 0.03% to 0.01%, although, as the ICR shown is an estimate only, it may increase or decrease depending on the actual costs incurred.

2 From 1 October 2019, we anticipate that the investment fee for the Cash and Australian Bond options will decrease by up to 0.04%.3 Components may not add to ‘Total’ due to rounding.4 These amounts reflect the fees and costs which we have incurred in managing the Listed Property option, for example, fees and