demand - mrbeem4+demand+ppt.pdfa. substitutes like coke and pepsi b. compliments like pb and j,...

TRANSCRIPT

Demand Chapter 4

The Way it Works

• What is demand?

– The “want” to purchase goods or services

• Demand is willingness and ability to purchase a good or service at a given RANGE of prices.

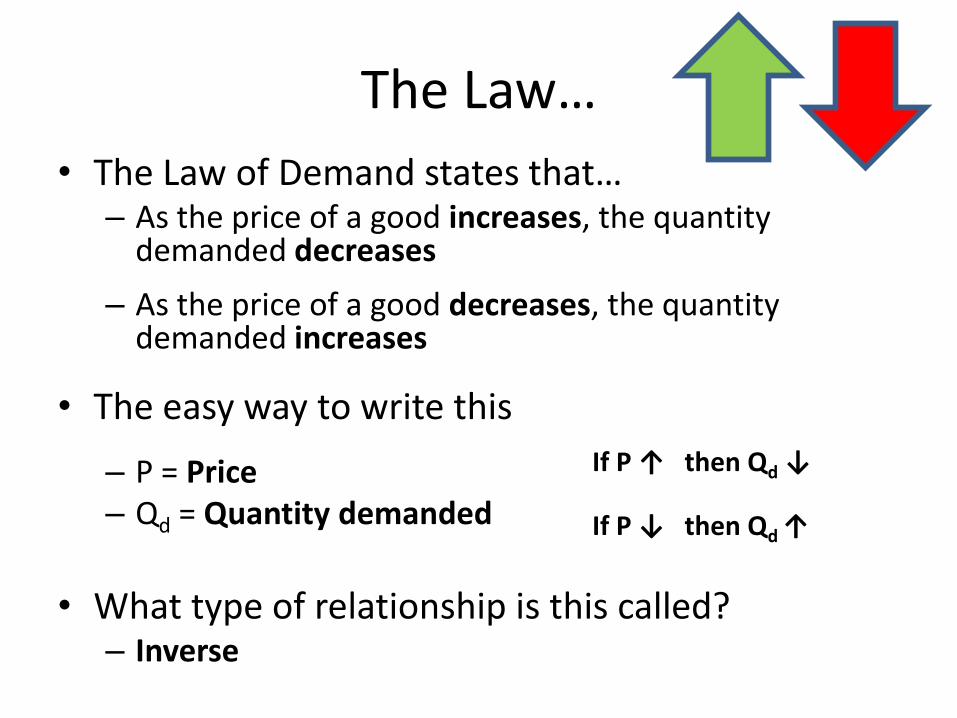

The Law…

• The Law of Demand states that… – As the price of a good increases, the quantity

demanded decreases

– As the price of a good decreases, the quantity demanded increases

• The easy way to write this

– P = Price – Qd = Quantity demanded

• What type of relationship is this called?

– Inverse

If P ↑ then Qd ↓

If P ↓ then Qd ↑

What’s the Difference?

• What is the difference between demand and quantity demanded?

– Demand is simply the willingness and ability to buy something

– Demand is the curve or line

– Quantity demanded is the # of units purchased at a specific price

– Quantity demanded is the dot or point on the line

What’s the Difference?

– Demand is the curve or line

– Quantity demanded is the dot or point on the line

– At $3, the quantity demanded is 2.

How Much You Consume…

• Law of Diminishing Marginal Utility states… – As a person consumes additional units of a good, eventually the

utility gained from each additional unit of the good decreases.

– In economic terms, utility is another word for satisfaction or • Ex. Cheeseburgers at Culvers make me

• The more utility (satisfaction) you receive from a good the… – Higher the price people are willing to pay for it

• The less utility (satisfaction) you receive from a good the… – Lower the price people are willing to pay for it

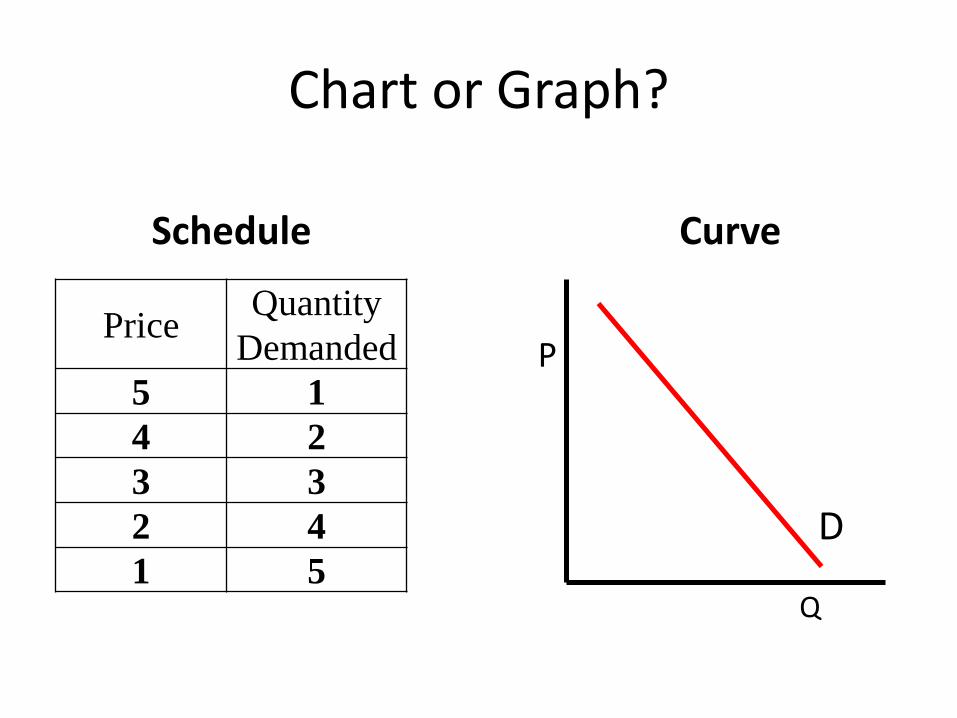

Chart or Graph?

• A demand schedule is the numerical representation of the Law of Demand

• A demand curve is the graphical representation of the Law of Demand

Chart or Graph?

Price Quantity

Demanded

5 1

4 2

3 3

2 4

1 5

P

Q

Schedule Curve

D

Shifting the Curve…

• When demand increases, the demand curve SHIFTS to the right!

D 1

P

Q

D 2

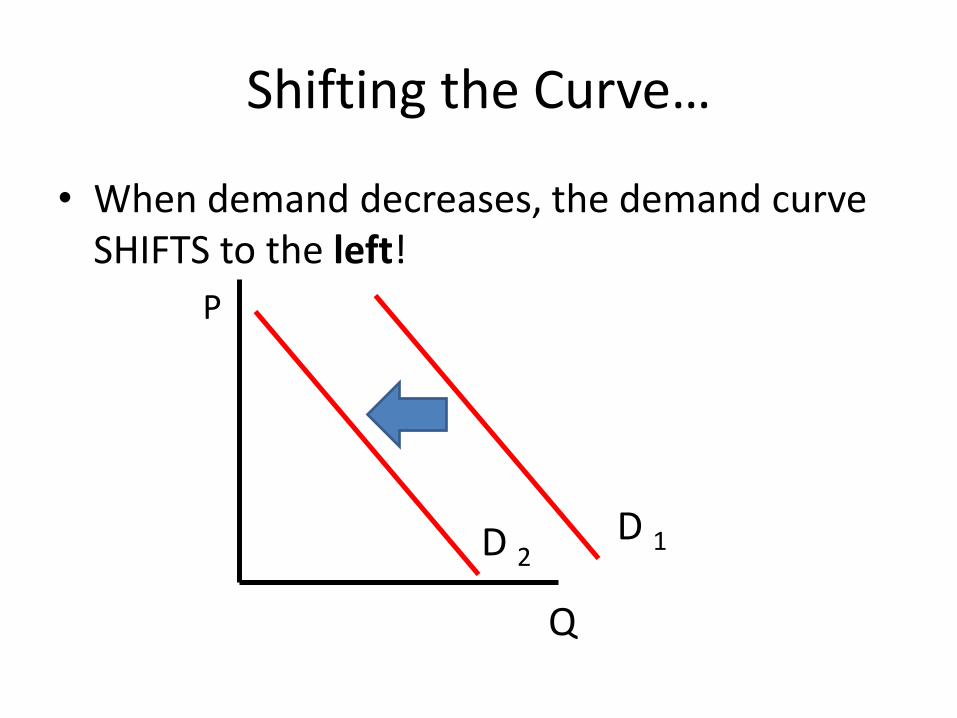

Shifting the Curve…

• When demand decreases, the demand curve SHIFTS to the left!

D 1

P

Q

D 2

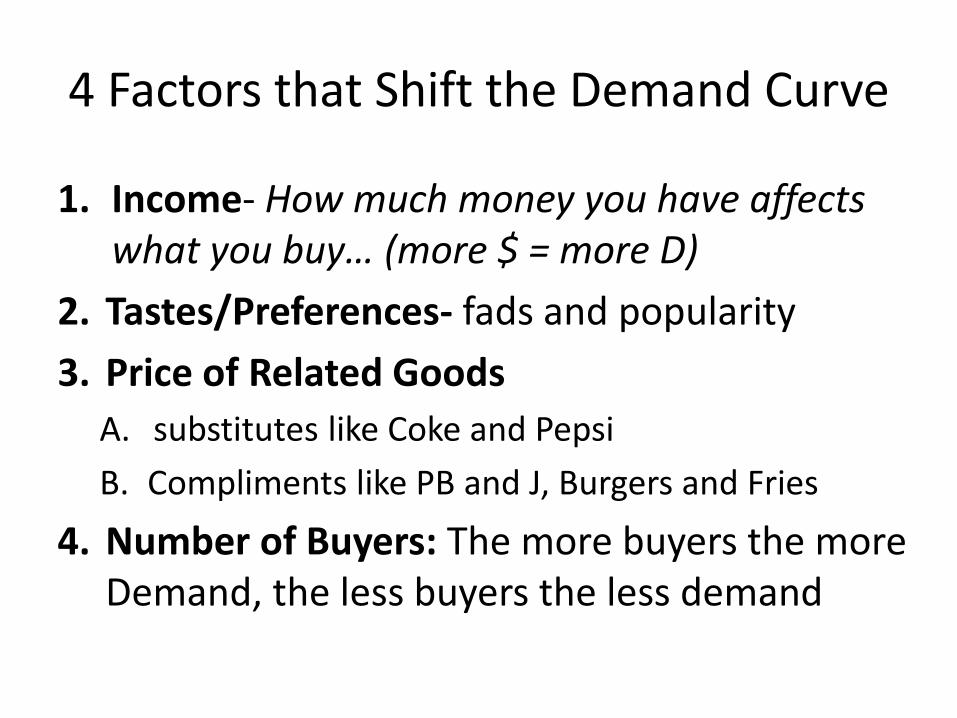

4 Factors that Shift the Demand Curve

1. Income- How much money you have affects what you buy… (more $ = more D)

2. Tastes/Preferences- fads and popularity

3. Price of Related Goods

A. substitutes like Coke and Pepsi

B. Compliments like PB and J, Burgers and Fries

4. Number of Buyers: The more buyers the more Demand, the less buyers the less demand

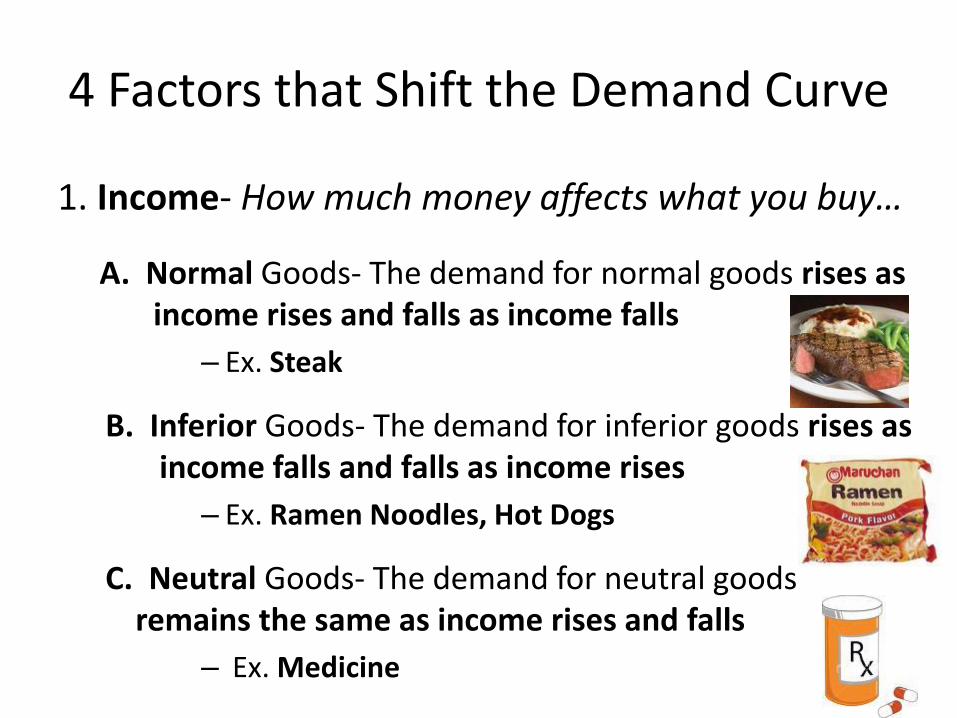

4 Factors that Shift the Demand Curve

1. Income- How much money affects what you buy…

A. Normal Goods- The demand for normal goods rises as income rises and falls as income falls

– Ex. Steak

B. Inferior Goods- The demand for inferior goods rises as income falls and falls as income rises

– Ex. Ramen Noodles, Hot Dogs

C. Neutral Goods- The demand for neutral goods remains the same as income rises and falls

– Ex. Medicine

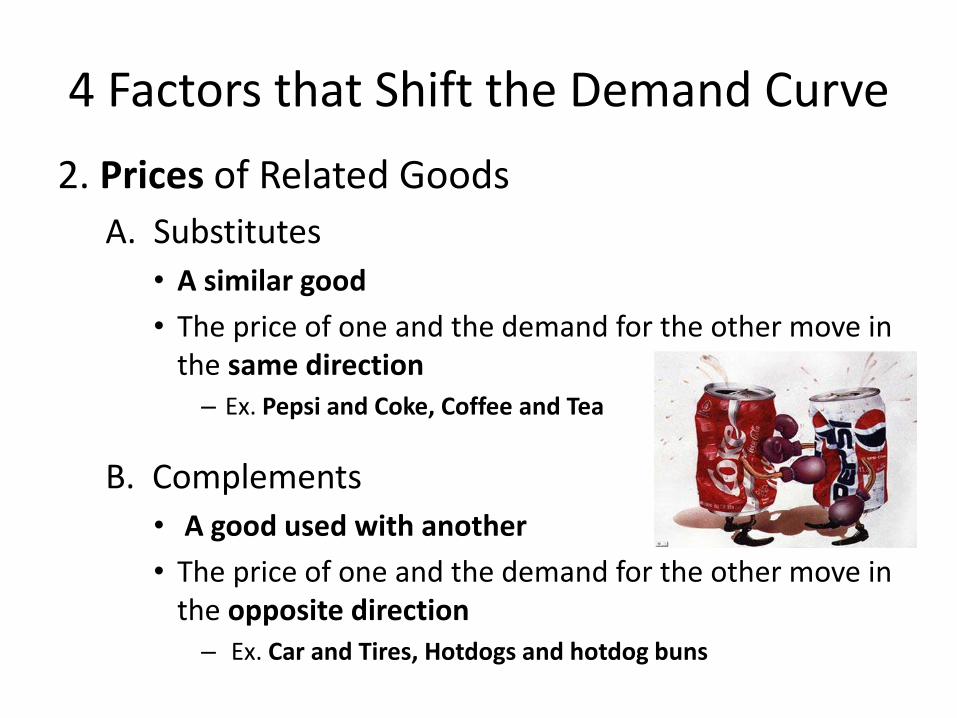

4 Factors that Shift the Demand Curve

2. Prices of Related Goods

A. Substitutes

• A similar good

• The price of one and the demand for the other move in the same direction – Ex. Pepsi and Coke, Coffee and Tea

B. Complements

• A good used with another

• The price of one and the demand for the other move in the opposite direction – Ex. Car and Tires, Hotdogs and hotdog buns

4 Factors that Shift the Demand Curve

3. Preferences

– Demand changes as preference’s change

• Ex. Clothing

4. Number of Buyers

– As the number of buyers increase, the demand for a good increases

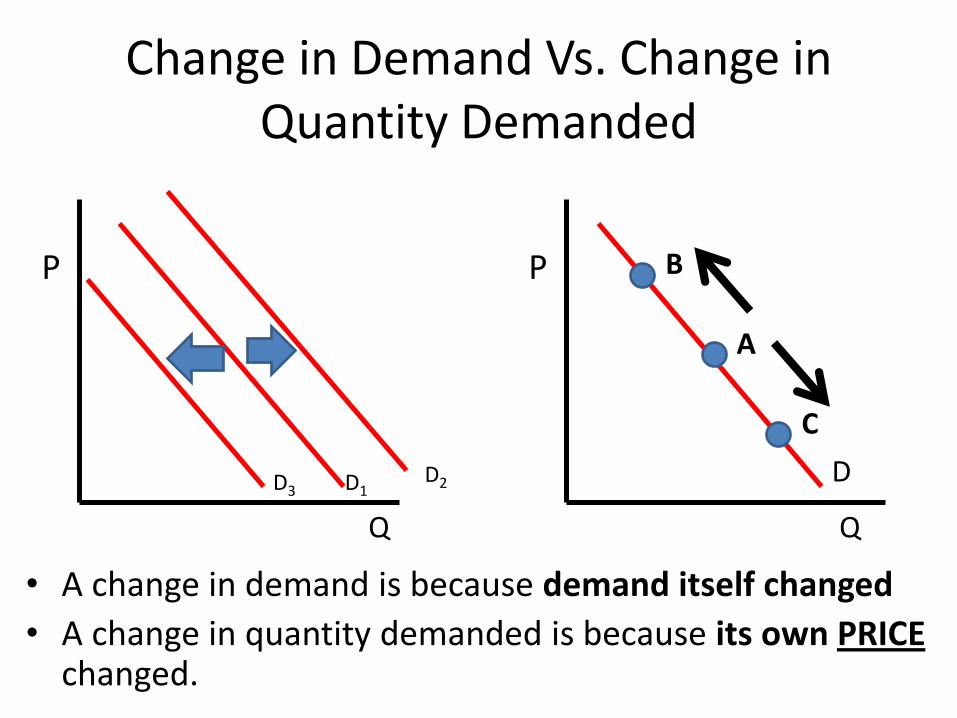

Change in Demand Vs. Change in Quantity Demanded

• A change in demand is because demand itself changed

• A change in quantity demanded is because its own PRICE changed.

P

Q

P

Q

A

B

C

D D2 D1 D3

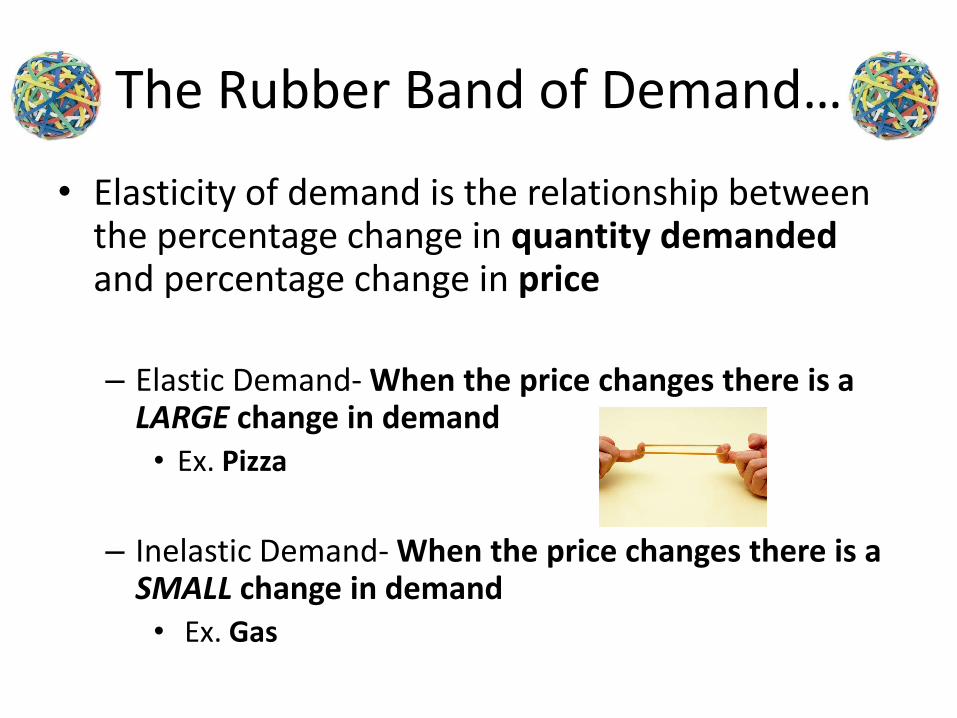

The Rubber Band of Demand…

• Elasticity of demand is the relationship between the percentage change in quantity demanded and percentage change in price

– Elastic Demand- When the price changes there is a LARGE change in demand • Ex. Pizza

– Inelastic Demand- When the price changes there is a SMALL change in demand • Ex. Gas

4 Determinants of Elasticity

1. Number of Substitutes

– If a good has many substitutes, then consumers will choose another type of good when price rises

• Lots of substitutes = Elastic

– Ex. Cereal

• Few or no close substitutes = Inelastic

– Ex. Diamonds

4 Determinants of Elasticity

2. Luxuries vs. Necessities

– If a good is a luxury and the price rises, then consumers will buy less of it

• Luxury = Elastic

• Ex. BMW

– If a good is a necessity and the price rises, then consumers will continue to buy it

• Necessity = Inelastic

• Ex. Gas

4 Determinants of Elasticity

3. Percentage of Income Spent on a Good

– The higher the percentage of one’s income that is spent on a good the more elastic demand for that good will be

• Ex. Cigarettes

4 Determinants of Elasticity

4. Time

– As time increases consumers have more chance to change their purchases

**Ex. Demand for gas in the short run is inelastic because there is no alternative, but in the long run it could be elastic because consumers can purchase new cars

• Ex. Smaller or Hybrid