derived analytics: the key to more effective...

TRANSCRIPT

DERIVED ANALYTICS: THE KEY TO MORE EFFECTIVE RISK MANAGEMENT AND INVESTINGDENNIS KIRINCICH, MANAGING DIRECTOR, BLACKROCK SOLUTIONS JAYME FAGAS, GLOBAL HEAD OF EVALUATED PRICING, THOMSON REUTERS

JUNE 2013

A THOMSON REUTERS FINANCIAL AND RISK WHITE PAPER

A THOMSON REUTERS FINANCIAL AND RISK WHITE PAPER

Analytics have become an increasingly critical tool in the operating environment of firms around the world, both large and small. Unprecedented monetary policies conducted by the US Federal Reserve (the Fed) have driven down interest rates to lows not seen in decades and flattened the yield curve. In this new normal, and with various interrelated trends increasingly evident across the global financial services industry, fixed-income portfolio and risk managers need sophisticated analytics and modeling capabilities if they are to manage their portfolios successfully and mitigate the risk associated with misaligned portfolios.

THE CHALLENGES1. Search for returnsThe low interest rate environment and stunted global economic growth of recent years have driven industry participants to seek out higher yielding assets. As a consequence, there is a broad-based push into different and more complex asset classes, the risks of which need to be properly understood and managed.

2. Risk managementWith effective risk management becoming such a sensitive topic in the wake of the financial crisis, the portfolio expansion into potentially higher-risk areas is inevitably drawing the scrutiny of regulators and investors. In response, regulators, boards and clients are demanding greater transparency into the underlying portfolio components, and assurance that firms have the ability to assess and manage the risks effectively.

3. Regulatory environmentRisk analytics are an essential component of the drive for increased regulatory oversight and changes in the financial marketplace. Dodd-Frank, Bank Capital Rules and Solvency II require stress testing and macroeconomic scenario analysis, all dependent on accurate market prices, data and analytics.

Unfortunately, supporting an array of complex asset classes can be expensive. To compute the underlying sensitivities for all the different assets and report on them may require several different sophisticated systems, adding to pressure on firms’ already strained cost bases. Yet given the financial and reputational damage that poor risk management can cause, firms can ill afford analytics capabilities that are not up to the task.

The need for sound risk measures is paramount in order to navigate the financial markets and make informed investment decisions.

ANALYTICS: NOW MORE IMPORTANT THAN EVER IN SUPPORTING EFFECTIVE RISK MANAGEMENT AND PROFITABLE INVESTING

SETTING THE STAGE: FED INTERVENTIONThe financial crisis of 2008 has prompted the Fed to respond with a series of major and ongoing monetary policies to stimulate the economy. First, it cut short-term interest rates to an effective rate of zero, which was followed by two rounds of quantitative easing (QE1 and QE2). However, with the economy still showing signs of weakness, the Fed responded from September 2011 through December 2012 with Operation Twist. This involved selling short-dated Treasuries to buy longer-term ones in an effort to bring down long-term interest rates – thereby flattening the yield curve (the “twist”) – and stimulate the economy. The Fed subsequently launched QE3, which will remain in effect until either unemployment drops to 6.5% or inflation rises to 2.5%.

KEY ANALYTICSWith all the quantitative easing from the Fed, the yield-to-worst (YTW) for the Barclays Capital US Aggregate index is at an all-time low, reaching 1.64% as of February 2013.

2

A THOMSON REUTERS FINANCIAL AND RISK WHITE PAPER

MANAGING THE OADIn this environment, the safety cushion for capital preservation is thin. For example, a portfolio with a similar option-adjusted duration (OAD) and yield profile as the Barclays U.S. Aggregate will break even if rates back up by just 35 basis points for the remainder of the year. They start losing capital if rates back up further.

On an absolute basis, managing the OAD will be crucial to meeting capital preservation goals. On an active basis, it is equally important to manage duration risk against the benchmark. Therefore, it is imperative portfolio managers know where the active OAD is positioned on a daily basis to confirm the risk taken is consistent with their investment views.

ADDING KRDs TO THE MIXYet while OAD is a useful and effective risk measure, it does not tell the whole story. Although changes in interest rates are often highly correlated across each point on the curve, the slope and shape can change dramatically over time – as shown by the Fed’s asset purchase program Operation Twist, which has served to flatten the long end of the curve.

Portfolios can achieve a particular OAD with very different sensitivities to the short, intermediate or long end of the yield curve. Therefore, it is important to measure interest rate risk using key rate durations (KRDs), as well as OAD. KRDs quantify an asset or portfolio’s sensitivities to independent shifts along the yield curve at select points (2Y, 5Y, 10Y, 30Y) and thereby help portfolio managers understand their curve positioning.

The example below illustrates the point.

The hypothetical portfolio is overweight at the long end of the curve (10Y/30Y) and underweight at the front end of the curve (2Y/5Y) as measured by KRDs. However, the curve bear steepened where the long-term rates increased faster than short-term rates and was a detractor to performance. So, even though it matched the OAD of the benchmark, the portfolio underperformed by 7 basis points.

ANALYTICS METHODOLOGY: A CLOSER LOOK AT THE MECHANICSEffective Duration: Unlike modified duration, the effective duration (i.e., the Option-Adjusted Duration (OAD)) does not assume cash flows are constant as interest rates change. Instead it measures the sensitivity of market price to parallel shifts in the yield curve, assuming spreads stay constant as the curve shifts. The OAD is computed as follows:

1. Compute the base case spread, adjusting for options with the given market full price (P[0]).

2. Holding the spread constant, compute the price for the security when shifting the yield curve up and down X basis points in parallel. This will derive P[-X] and P[+X].

3. Calculate the effective duration by determining the change in the security’s value by shocking the yield curve as a fraction of the original full price, scale the shock size to normalize to a 100 bps shock, and multiply by 100 to express as a percentage of price. OAD = ((P[-X] – P[+X] / (P[0])) * 100/2X * 100

Key Rate Durations: Key rate durations are based on the notion of partial interest rate shifts, which, when aggregated, approximate a parallel shift in the spot curve. Key rate durations measure the price sensitivity of a security or a portfolio to changes in different parts of the yield curve. The yield curve is divided into four key rate maturity buckets. Positive and negative shifts are independently applied to each of the four spot rates, and using calculations similar to the estimation of effective durations, the partial interest rate durations (i.e., KRDs) are obtained.

A more market intuitive way to view yield curve risk is to consider key Treasury rate durations (KTRDs) instead, which measure changes to par curve instead of spot curve. A KRD is computed by shocking specific parts of the curve as shown in the graph below.

The aggregate sum of KRDs is not “naturally” equal to the OAD, but the model forces the equality by normalizing KRDs to add up to OAD.

In summary, KRDs are a function of:• Discounting (for all bonds) • Indexing (for floating rate securities) • Model optionality (for callable/prepayable securities)

“ Our analytical methodologies for the various asset classes are state of the practice for the industry. We have over 40 financial modelers dedicated to adapting our methods as the markets and industry change.” —Woo Fung Kwong – Head of Analytics within BlackRock Solutions

3

A THOMSON REUTERS FINANCIAL AND RISK WHITE PAPER

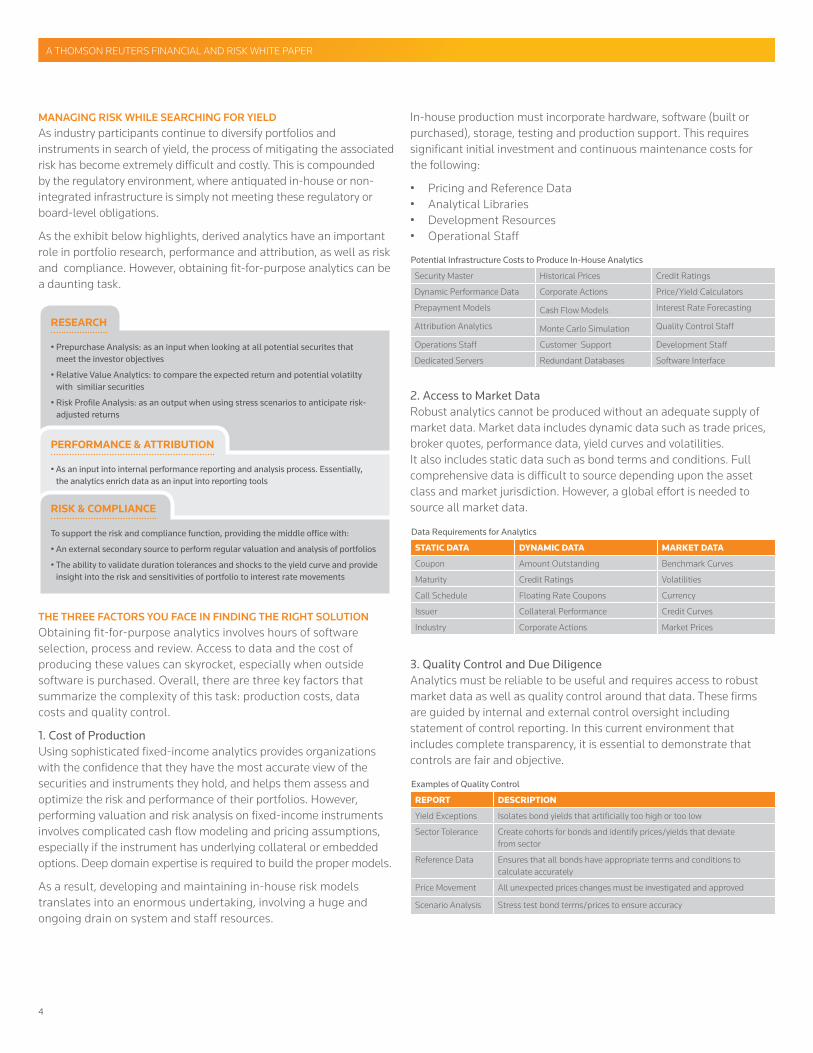

MANAGING RISK WHILE SEARCHING FOR YIELDAs industry participants continue to diversify portfolios and instruments in search of yield, the process of mitigating the associated risk has become extremely difficult and costly. This is compounded by the regulatory environment, where antiquated in-house or non-integrated infrastructure is simply not meeting these regulatory or board-level obligations.

As the exhibit below highlights, derived analytics have an important role in portfolio research, performance and attribution, as well as risk and compliance. However, obtaining fit-for-purpose analytics can be a daunting task.

THE THREE FACTORS YOU FACE IN FINDING THE RIGHT SOLUTION Obtaining fit-for-purpose analytics involves hours of software selection, process and review. Access to data and the cost of producing these values can skyrocket, especially when outside software is purchased. Overall, there are three key factors that summarize the complexity of this task: production costs, data costs and quality control.

1. Cost of ProductionUsing sophisticated fixed-income analytics provides organizations with the confidence that they have the most accurate view of the securities and instruments they hold, and helps them assess and optimize the risk and performance of their portfolios. However, performing valuation and risk analysis on fixed-income instruments involves complicated cash flow modeling and pricing assumptions, especially if the instrument has underlying collateral or embedded options. Deep domain expertise is required to build the proper models.

As a result, developing and maintaining in-house risk models translates into an enormous undertaking, involving a huge and ongoing drain on system and staff resources.

In-house production must incorporate hardware, software (built or purchased), storage, testing and production support. This requires significant initial investment and continuous maintenance costs for the following:

• Pricing and Reference Data• Analytical Libraries• Development Resources• Operational Staff

2. Access to Market DataRobust analytics cannot be produced without an adequate supply of market data. Market data includes dynamic data such as trade prices, broker quotes, performance data, yield curves and volatilities. It also includes static data such as bond terms and conditions. Full comprehensive data is difficult to source depending upon the asset class and market jurisdiction. However, a global effort is needed to source all market data.

3. Quality Control and Due DiligenceAnalytics must be reliable to be useful and requires access to robust market data as well as quality control around that data. These firms are guided by internal and external control oversight including statement of control reporting. In this current environment that includes complete transparency, it is essential to demonstrate that controls are fair and objective.

STATIC DATA DYNAMIC DATA MARKET DATA

Coupon Amount Outstanding Benchmark Curves

Maturity Credit Ratings Volatilities

Call Schedule Floating Rate Coupons Currency

Issuer Collateral Performance Credit Curves

Industry Corporate Actions Market Prices

Data Requirements for Analytics

REPORT DESCRIPTION

Yield Exceptions Isolates bond yields that artificially too high or too low

Sector Tolerance Create cohorts for bonds and identify prices/yields that deviate from sector

Reference Data Ensures that all bonds have appropriate terms and conditions to calculate accurately

Price Movement All unexpected prices changes must be investigated and approved

Scenario Analysis Stress test bond terms/prices to ensure accuracy

Examples of Quality Control

Security Master Historical Prices Credit Ratings

Dynamic Performance Data Corporate Actions Price/Yield Calculators

Prepayment Models Cash Flow Models Interest Rate Forecasting

Attribution Analytics Monte Carlo Simulation Quality Control Staff

Operations Staff Customer Support Development Staff

Dedicated Servers Redundant Databases Software Interface

Potential Infrastructure Costs to Produce In-House Analytics

RESEARCH

• Prepurchase Analysis: as an input when looking at all potential securites that meet the investor objectives

• Relative Value Analytics: to compare the expected return and potential volatilty with similiar securities

• Risk Profile Analysis: as an output when using stress scenarios to anticipate risk-adjusted returns

PERFORMANCE & ATTRIBUTION

• As an input into internal performance reporting and analysis process. Essentially, the analytics enrich data as an input into reporting tools

RISK & COMPLIANCE

To support the risk and compliance function, providing the middle office with:

• An external secondary source to perform regular valuation and analysis of portfolios

• The ability to validate duration tolerances and shocks to the yield curve and provide insight into the risk and sensitivities of portfolio to interest rate movements

4

A THOMSON REUTERS FINANCIAL AND RISK WHITE PAPER

AN EFFICIENT, EFFECTIVE ALTERNATIVE One alternative to the “build” scenario is to take advantage of the expertise and infrastructure investment of a specialist third-party analytics service provider. By accessing superior trending and measurement capabilities, users can improve their research, performance attribution, risk management and compliance processes.

Furthermore, firms no longer have to pay for and support an analytics solution in-house, nor wrestle with manual processes. This translates into lower operating costs, reducing operational complexity, and freeing up staff to focus on the firm’s true core competencies, thereby helping boost profit margins. Even where firms continue to use in-house analytics, a sophisticated third-party capability can serve as a valuable tool for validation purposes, providing compliance and risk teams with a robust and reliable means of checking calculations.

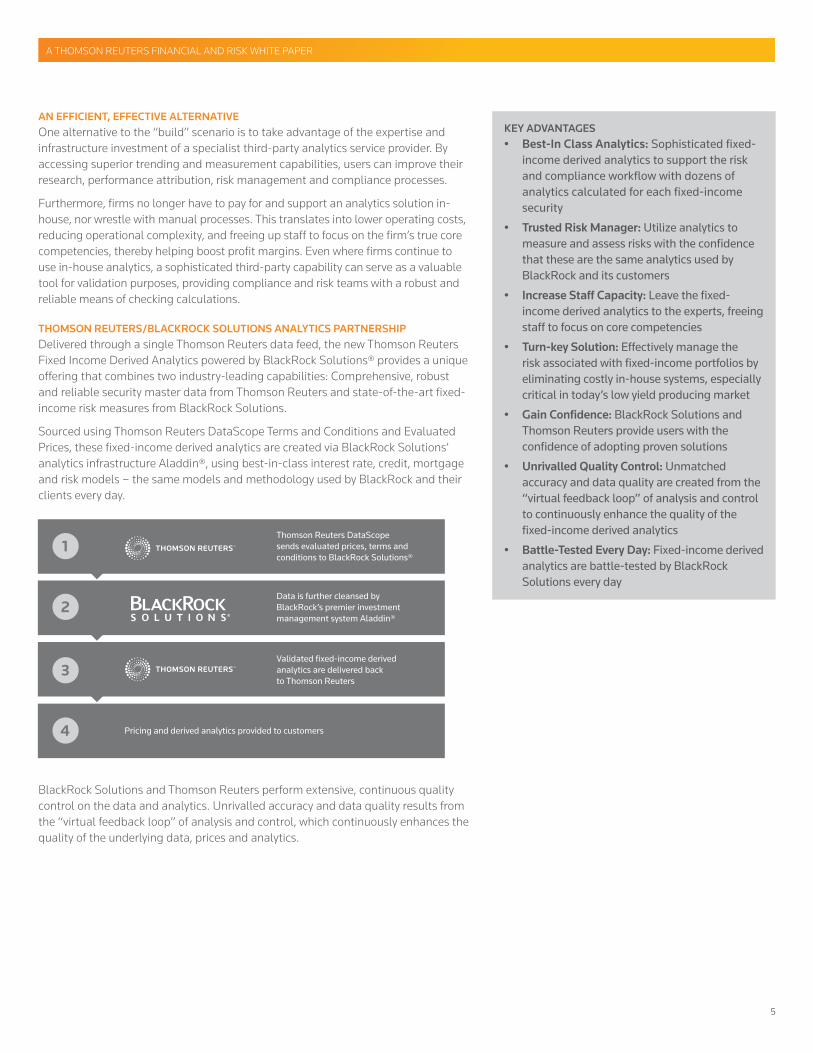

THOMSON REUTERS/BLACKROCK SOLUTIONS ANALYTICS PARTNERSHIP Delivered through a single Thomson Reuters data feed, the new Thomson Reuters Fixed Income Derived Analytics powered by BlackRock Solutions® provides a unique offering that combines two industry-leading capabilities: Comprehensive, robust and reliable security master data from Thomson Reuters and state-of-the-art fixed-income risk measures from BlackRock Solutions.

Sourced using Thomson Reuters DataScope Terms and Conditions and Evaluated Prices, these fixed-income derived analytics are created via BlackRock Solutions’ analytics infrastructure Aladdin®, using best-in-class interest rate, credit, mortgage and risk models – the same models and methodology used by BlackRock and their clients every day.

BlackRock Solutions and Thomson Reuters perform extensive, continuous quality control on the data and analytics. Unrivalled accuracy and data quality results from the “virtual feedback loop” of analysis and control, which continuously enhances the quality of the underlying data, prices and analytics.

KEY ADVANTAGES• Best-In Class Analytics: Sophisticated fixed-

income derived analytics to support the risk and compliance workflow with dozens of analytics calculated for each fixed-income security

• Trusted Risk Manager: Utilize analytics to measure and assess risks with the confidence that these are the same analytics used by BlackRock and its customers

• Increase Staff Capacity: Leave the fixed-income derived analytics to the experts, freeing staff to focus on core competencies

• Turn-key Solution: Effectively manage the risk associated with fixed-income portfolios by eliminating costly in-house systems, especially critical in today’s low yield producing market

• Gain Confidence: BlackRock Solutions and Thomson Reuters provide users with the confidence of adopting proven solutions

• Unrivalled Quality Control: Unmatched accuracy and data quality are created from the “virtual feedback loop” of analysis and control to continuously enhance the quality of the fixed-income derived analytics

• Battle-Tested Every Day: Fixed-income derived analytics are battle-tested by BlackRock Solutions every day

1Thomson Reuters DataScope sends evaluated prices, terms and conditions to BlackRock Solutions®

2

3

Data is further cleansed by BlackRock’s premier investment management system Aladdin®

Validated fixed-income derived analytics are delivered back to Thomson Reuters

4 Pricing and derived analytics provided to customers

5

A THOMSON REUTERS FINANCIAL AND RISK WHITE PAPER

You can obtain more information about these market-leading fixed income derived analytics by speaking to your Thomson Reuters Account Manager, visiting the solutions page on www.prdcommunity.com or emailing [email protected].

ABOUT BLACKROCK SOLUTIONS BlackRock Solutions provides clients with access to the intellectual capital, risk analytics and investment platform used to support BlackRock’s asset management business. By combining sophisticated risk analytics and investment systems with capital markets and business process expertise, BlackRock Solutions helps clients address a variety of risk management and investment process challenges. The BlackRock Solutions’ Aladdin platform is currently used to analyze and process over $13 trillion in assets, liabilities and derivatives as of December 31, 2012. For additional information, please visit the company’s website at www.blackrocksolutions.com.

ABOUT BLACKROCKBlackRock is a leader in investment management, risk management and advisory services for institutional and retail clients worldwide. As of December 31, 2012, BlackRock’s sssets under management was $3.792 trillion. BlackRock offers products that span the risk spectrum to meet clients’ needs, including active, enhanced and index strategies across markets and asset classes. Products are offered in a variety of structures including separate accounts, mutual funds, iShares® (exchange traded funds) and other pooled investment vehicles. BlackRock also offers risk management, advisory and enterprise investment system services to a broad base of institutional investors through BlackRock Solutions. Headquartered in New York City, as of December 31, 2012, the firm has approximately 10,100 employees in 30 countries and a major presence in key global markets, including North and South America, Europe, Asia, Australia and the Middle East and Africa. For additional information, please visit the Company’s website at www.blackrock.com.

ABOUT THOMSON REUTERSThomson Reuters is the world’s leading source of intelligent information for businesses and professionals. We combine industry expertise with innovative technology to deliver critical information to leading decision makers in the financial and risk, legal, tax and accounting, intellectual property and science and media markets, powered by the world’s most trusted news organization. With headquarters in New York and major operations in London and Eagan, Minnesota, Thomson Reuters employs approximately 60,000 people and operates in over 100 countries. Thomson Reuters shares are listed on the Toronto and New York Stock Exchanges.

Visit thomsonreuters.com

For more information, contact your representative or visit us online.

© Thomson Reuters 2013. All rights reserved. 1003236/5-13

ABOUT THE AUTHORSDennis Kirincich Managing Director, BlackRock Solutions

A member of the BlackRock Solutions Relationship Management Client Analytics

Group and head of the Risk Solutions business, Dennis is a senior relationship manager responsible for overseeing client relationships and ensuring delivery of the risk reporting product offering. Specifically, he works with insurance companies, financial institutions, pensions and corporate clients on providing risk transparency and client solutions for multi-asset class investments, liabilities and derivatives.

Jayme Fagas Global Head of Evaluated Pricing, Thomson Reuters

Jayme Fagas is the Global Head of Evaluated Pricing at Thomson Reuters. With Over 25 years in

the financial industry, Ms. Fagas brings significant expertise to the Thomson Reuters team having worked in evaluations, trading and analytics at a number of firms on Wall Street. As a member of the Thomson Reuters Enterprise Content operating committee, Ms. Fagas focuses on managing the evaluated pricing product offering through Thomson Reuters DataScope Select, the strategic data delivery platform for non-streaming content. Ms. Fagas is an active industry participant working closely with mutual funds, hedge funds, asset managers, fund administrators and custodians, to provide solutions that meet the industry’s regulatory and compliance needs.