detlef borghardt, ceo - saf-holland · detlef borghardt, ceo. 2 ... based on top 7 european truck...

TRANSCRIPT

Design

the future

December 09, 2015

Capital Markets Day 2015

“Strategy 2020: Megatrends and Organizational

Structure”

Detlef Borghardt, CEO

2

SAF-HOLLAND in brief 3

Megatrends – Which global trends will be driving our future? 9

Strategy 2020 – How we will benefit 15

Strategy 2020 – Where do we stand? Organizational structure and reporting 21

1

2

3

4

Agenda

3

SAF-HOLLAND: Europe’s largest listed commercial vehicle supplier

• One of the leading global producers and

suppliers of key systems and components for

the trailer, truck, bus, and recreational vehicle

industries

• 29 subsidiaries including 18 manufacturing

facilities on six continents

• ~3,400 employees

• Approx. 9,000 Aftermarket spare parts and

service stations around the world

Axle systems

Landing gear

Kingpins

Fifth wheels

Suspensions

General information Components and systems

1) Please refer to page 37 for detailed information on EBIT adjustments.

4

2014

SAF-HOLLAND

Market Position

Market shares

Europe North America

Europe North America SAF-HOLLAND Σ Top 3 SAF-HOLLAND Σ Top 3

Axles # 1 # 3 39% 89% 8% 90%

Suspensions # 1 # 2 36% 90% 15% 84%

Kingpins # 2 # 1 12% 89%1) 69% 87%1)

Landing gears # 3 # 1 6% 89% 39% 78%1)

Fifth wheel # 2 # 1 23%2) 96% 51% 100%

Truck suspensions n/a # 2 0% 90%3) 6%4) 38%

Service points # 1 # 1 Approx. 9,000 Aftermarket spare parts and service stations

Strong market position in oligopolistic marketsT

rail

er

Syste

ms

Po

were

d V

eh

icle

Syste

ms

Aft

er-

mark

et

Source: L.E.K. Consulting, April 2015

1) Top 2 players 2) Based on top 7 European truck OEMs (Mercedes Benz, VOLVO, MAN, DAF, SCANIA, Renault, IVECO) 3) Predominantly captive market 4) Commercial market share excluding sales to U.S. Defence Dept.

Among the TOP 2 players in almost every product area; Significant growth potential in the North

American market in trailer axles and suspensions as well as truck suspensions to be exploited

5

An international player: 90% of sales originate from Europe and the US

Core sales regions

Production sites

CanadaWoodstock

Norwich

USAHolland

Muskegon

Warrenton South

Warrenton North

Wylie

Dumas

BrazilJaguariuna

IndiaSriperambadur Taluk

AustraliaMelton

ChinaXiamen

Bautou

GermanyBessenbach/Keilberg

Bessenbach/Frauengrund

Singen

South AfricaJohannesburg

United Arab EmiratesDubai

6

Going Global: Truck & Trailer

7

Going Global: Truck & Trailer

8

Going Global: Truck & Trailer

9

Going Global: Truck & Trailer

10

SAF-HOLLAND in brief 3

Megatrends – Which global trends will be driving our future? 9

Strategy 2020 – How we will benefit 15

Strategy 2020 – Where do we stand? Organizational structure and reporting 21

1

2

3

4

Agenda

11

Proposition 1

Understanding and drawing on the global megatrends is the key to maximizing

SAF-HOLLAND’s growth potential

Propositions for SAF-HOLLAND

Mega-Trends significantly affect the truck&trailer markets

Proposition 2

We found the right key drivers (mega-trends) for our business

Proposition 3

In 2030, there will be significantly more:

PEOPLE, MONEY, and ROADS

12

13

14

15

16

17

17

Population and active consumers per region

People

Source: United Nations, Department of Economic and Social Affairs, Population Division. World Population

Despite current slowdowns in the emerging markets, the mid-term trends will prevail

The number of active consumers will e.g. in NEXT-11 and MINT will outgrow the EU/US by far

“We found the right key drivers (mega-trends) for our business.“

18

Money

• Beside the number of people, the MONEY spend for goods which are transported in trucks on

roads is obviously important

• How does the income per capita develop on a global scale?

Source: Gapminder – a fact-based worldview, www.gapminder.org

• The most important consumer group is the so-called “middle class”

• Middle Class is defined as all those living in households with daily per capita incomes of between USD

10 and USD 100 in purchasing power parity (PPP) terms

“We found the right key drivers (mega-trends) for our business.“

19

The right drivers for SAF-HOLLAND’s business

PeopleMoney

Trucks/

Trailers

Goods

Roads

The demand for SAF-HOLLAND products, is and will be driven by people, who have the money

to buy goods that are transported in trucks on roads.

20

SAF-HOLLAND in brief 3

Megatrends – Which global trends will be driving our future? 9

Strategy 2020 – How we will benefit 15

Strategy 2020 – Where do we stand? Organizational structure and reporting 21

1

2

3

4

Agenda

21

SAF-HOLLAND extrapolated regional sales split

Source: CIA World Factbook

RegionActual 2014 MTP 2020 Trend 2030

Core markets

(Europe & North

America)

~90% ~70% ~50%

Emerging

Markets/ RoW~10% ~30% ~50%

ΣΣ 100% 100% 100%

SAF-HOLLAND will exploit the opportunities of the global megatrends by organic growth in

addition to complementary external growth by joint ventures, acquisitions or cooperations;

By 2020 approx. 30% of sales are supposed to originate from today’s RoW area

22

Megatrends provide sustainable mid- and long-term growth perspectives and

business opportunities: 64 individual business plans to drive growth

SAF-HOLLAND will focus on its core competencies: “We will stick with where we

are really good at”

Expand our product portfolio and applications into new markets beyond the

current core regions Europe and North America

Take advantage of leading technological position and outstanding global brand

reputation when it comes to regional cooperations and applications

In the price-sensitive emerging markets the developing premium and techno-

logical mid-market segments will be addressed

Product innovation: Ramp-up of new products, e.g. INTRA-S/R

Above all: Strengthen the Aftermarket focusing on Europe and North America

and simultaneously developing new regions: Share in total Group sales at least

25%

Highlights

1

2

3

7

6

5

4

23

Strategy 2020: Mid-term sales targets

960

≥ 1,035

1,250

0

300

600

900

1200

1500

2014 Actual 2015e 2020 MT

Organic growth is expected to produce €1,250 mn in sales by 2020.

On top, joint ventures, acquisitions and cooperations with local partners will contribute e.g. in the NEXT-11

and MINT countries enabling a faster market entry or expansion of the existing market position

Sales in €mn

1,500

24

SAF-HOLLAND in brief 3

Megatrends – Which global trends will be driving our future? 9

Strategy 2020 – How we will benefit 15

Strategy 2020 – Where do we stand? Organizational structure and reporting 21

1

2

3

4

Agenda

25

Current structure: Business units

Aftermarket

Business Unit

Powered Vehicle Systems

Business Unit

Trailer Systems

Business Unit

• Axle systems

• Landing gears

• Kingpins and coupling products

• Suspensions

Sales FY 2014:

€544.4mn (56.7% of group sales)

• Fifth wheels

• Suspensions (Truck, Bus & RV)

• Tag axles

Sales FY 2014:

€169.5mn (17.7% of group sales)

• Global aftermarket and

service network

Sales FY 2014:

€245.8mn (25.6% of group sales)

26

New structure implementing Strategy 2020: by Region/ Business Area

APAC/ChinaAmericasEMEA/India

Sales FY 2014:

€ 530mn (55.2% of group sales)

Sales FY 2014:

€ 380mn (39.6% of group sales)

Sales FY 2014:

€ 50mn (5.2% of group sales)

• All product groups • All product groups • All product groups

27

Current organizational structure

Detlef Borghardt,

CEO

Wilfried Trepels,

CFO

Mike Kamsickas,

President Powered

Vehicle Systems

Business Unit

Steffen Schewerda,

President Trailer

Systems

Business Unit

Alexander Geis,

President Aftermarket

Business Unit

28

New organizational structure step 1

Detlef Borghardt,

CEO

Detlef Borghardt (temp. double responsibilty)

President APAC/China

Steffen Schewerda

President AmericasAlexander Geis

President EMEA/India

Wilfried Trepels,

CFO

Mike Kamsickas

COO

29

New organizational structure step 2

Detlef Borghardt,

CEO

Steffen Schewerda

President Americas

Alexander Geis

President Europe

Wilfried Trepels,

CFO

Mike Kamsickas

COO

Tbd

President APAC

Tbd

Tbd

President Mid-

East/Africa/India

Tbd

Tbd

President China

Tbd

Design

the future

December 09, 2015

Capital Markets Day 2015

Mike Kamsickas, President Powered Vehicle Systems

Business Unit

31

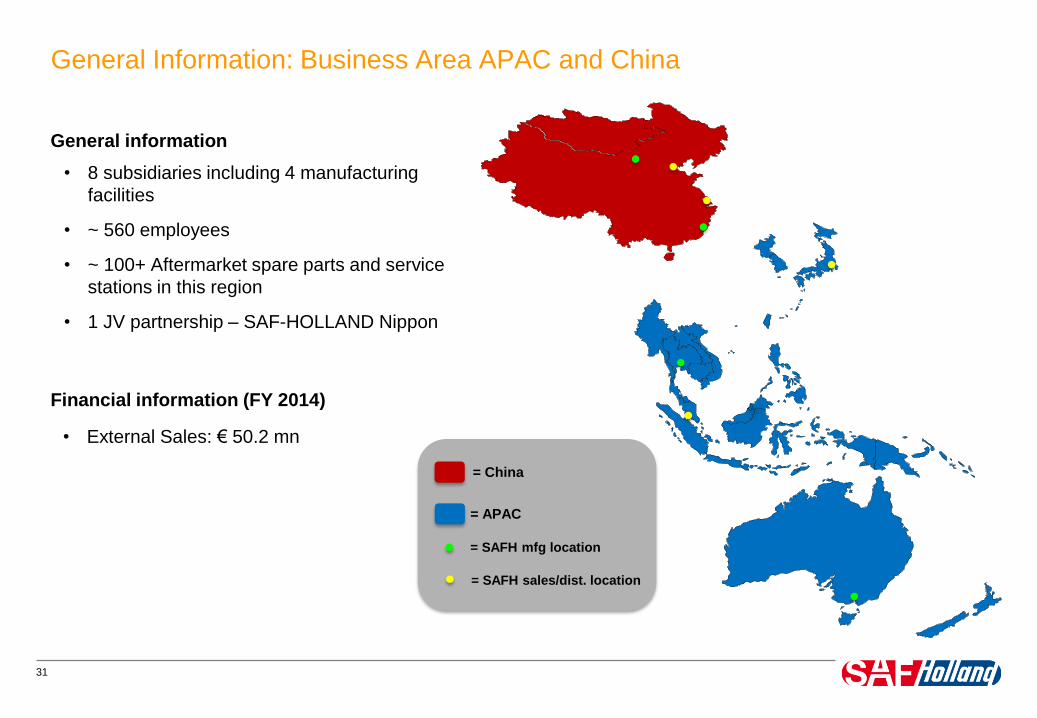

General Information: Business Area APAC and China

• 8 subsidiaries including 4 manufacturing

facilities

• ~ 560 employees

• ~ 100+ Aftermarket spare parts and service

stations in this region

• 1 JV partnership – SAF-HOLLAND Nippon

• External Sales: € 50.2 mn

General information

Financial information (FY 2014)

= China

= APAC

= SAFH mfg location

= SAFH sales/dist. location

32

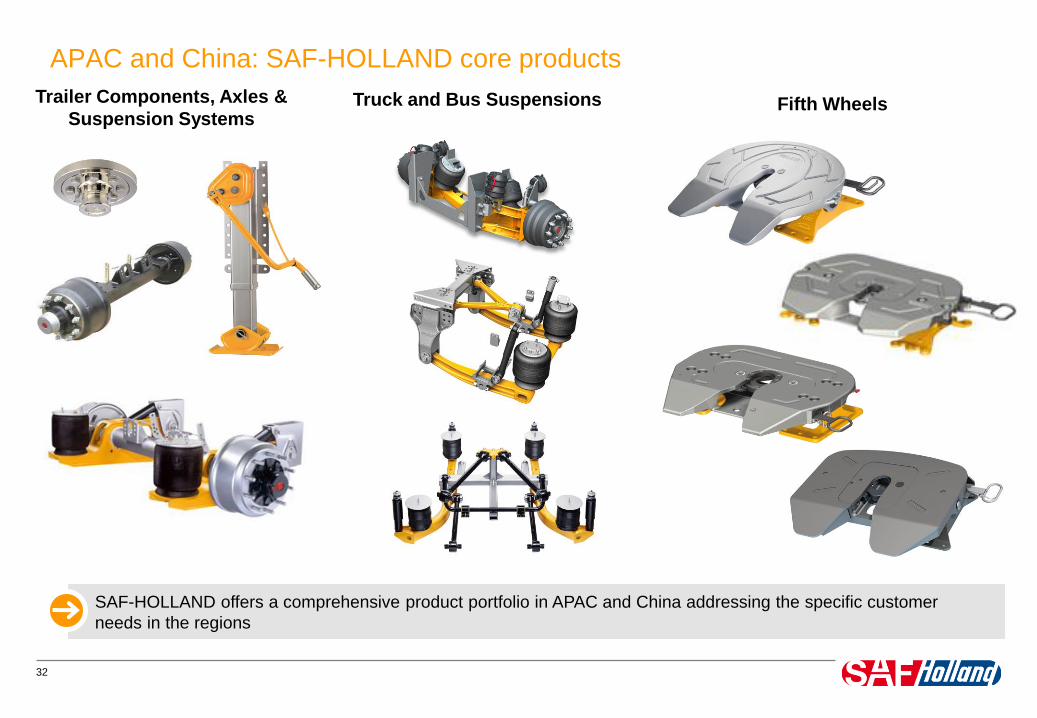

Trailer Components, Axles &

Suspension Systems

SAF-HOLLAND offers a comprehensive product portfolio in APAC and China addressing the specific customer

needs in the regions

Fifth Wheels

APAC and China: SAF-HOLLAND core products

Truck and Bus Suspensions

33

APAC and China: Key OE (customers) producing trucks and trailers

SAF-HOLLAND offers its innovative products to major OE´s in the truck and trailer industry active in APAC and China

34

Focus on major fleets and industry (infrastructure, logistics, specialty, heavy duty, port, etc.)

APAC and China: End customer base of transport companies using trucks & trailers

35

858,60 862,50 881,50

11.612.0

14.1

0

5

10

15

20

-

200,0

400,0

600,0

800,0

1000,0

2014 2015e 2020e

Population in mn Real GDP per capita in K USD

Macroeconomic drivers/ mega trend in the APAC & China region

Population and Real GDP per capita for APAC*

Source: ERS International Macroeconomic Data Set 2014, United Nations, Department of Economic and Social Affairs, Population Division (2015),

World Population Prospects: The 2015 Revision.

ASEAN countries: Indonesia, Malaysia, Thailand, Laos, Cambodia, Vietnam, Myanmar, Brunei, Philippines, and Singapore

1,402 1,405 1,421

7.37.9

10.9

0

5

10

15

20

-

500,0

1000,0

1500,0

2014 2015e 2020e

Population in mn Real GDP per capita in K USD

Population and Real GDP per capita for China

Population growth projections are moderate; however, strong GDP growth will strengthen the economies of

APAC, including China. Specifically, the countries of the ASEAN community are poised for significant

economic growth

* excludes China

1,500

1,000

0

1,000

0

36

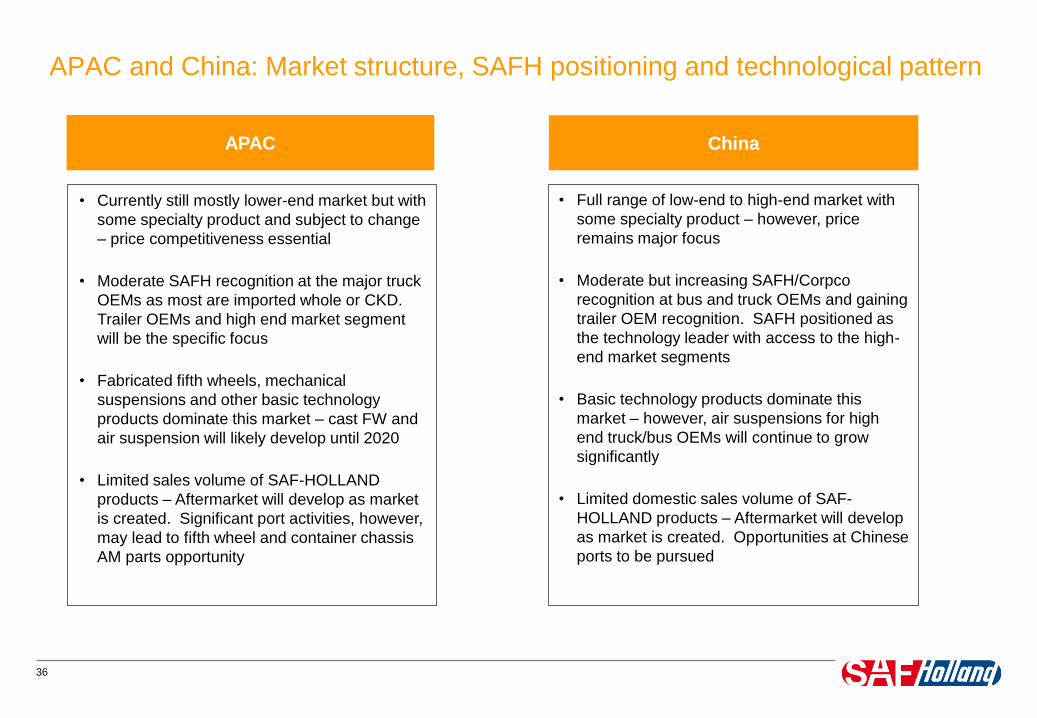

APAC and China: Market structure, SAFH positioning and technological pattern

ChinaAPAC

• Currently still mostly lower-end market but with

some specialty product and subject to change

– price competitiveness essential

• Moderate SAFH recognition at the major truck

OEMs as most are imported whole or CKD.

Trailer OEMs and high end market segment

will be the specific focus

• Fabricated fifth wheels, mechanical

suspensions and other basic technology

products dominate this market – cast FW and

air suspension will likely develop until 2020

• Limited sales volume of SAF-HOLLAND

products – Aftermarket will develop as market

is created. Significant port activities, however,

may lead to fifth wheel and container chassis

AM parts opportunity

• Full range of low-end to high-end market with

some specialty product – however, price

remains major focus

• Moderate but increasing SAFH/Corpco

recognition at bus and truck OEMs and gaining

trailer OEM recognition. SAFH positioned as

the technology leader with access to the high-

end market segments

• Basic technology products dominate this

market – however, air suspensions for high

end truck/bus OEMs will continue to grow

significantly

• Limited domestic sales volume of SAF-

HOLLAND products – Aftermarket will develop

as market is created. Opportunities at Chinese

ports to be pursued

37

APAC: Opportunities and measures

ChinaAPAC

• Content on imported OEM truck and bus

market and development of OEM trailer

and large fleet/industry markets

• Trailer axles, fifth wheels, and truck/bus

suspensions will be the main growth

drivers over the next years

• High end axles, fifth wheel, and truck and

bus suspensions with superior life cycle

characteristics will be a key success factor

• The Aftermarket will grow after the

development of OEMs and with market

growth

• Continued development of bus and truck

market (Corpco), as well as competitive

products for medium segment (axles, FW,

LG, etc.)

• Demonstrated preference for SAFH

product in many high end segments – with

continued work on lower end product

offering

• Truck, bus and trailer suspensions, as well

as competitive FW, axles, and LG provide

significant growth opportunity

• Aftermarket will develop with market share

• Additional M&A activities will increase

sales growth and SAFH development in

the region

38

APAC and China: Strategies for growing the business

China Truck/bus suspensions and FWs for

high end OEMs, mechanical and air

trailer suspensions and axles for all

segments

APAC Maintain the HD market; grow trailer

axles and mechanical suspensions;

increase OEM truck product “pull”

activities (fifth wheels, suspensions)

Significant growth potential in trailer axle, air and mechanical suspensions, and fifth wheels in all market segments

39

50

120

0

200

FY2014 Target 2020

Sales in €mn Summary

• China economy slowing, but still very strong and significant

opportunity for SAFH product

• APAC markets will see significant growth in economies,

export, and infrastructure with growing opportunities for

SAFH product

• Investment will be necessary in personnel as market is

extremely diverse; development of local technical

competence and manufacturing will be necessary

• Technological know-how and brand reputation a key asset

and competitive edge for mid-market and premium market

segments

• Additional product requirements (features, options, etc.)

will be identified and targeted according to group strategy

2020 figures for both APAC and China

Ambitious growth is possible as APAC becomes one of the fastest developing market segments in the world;

China will sustain its high level of growth

APAC and China: Business performance and sales targets 2020

40

Highlights APAC and China

China: Recent award of JMC/Ford truck suspension important reference contract to SAF-

HOLLAND Corpco 1

2China: Shift from export driven economy to a more consumption driven economy requires

continuous development of local manufacturing and domestic customer relationships

3China: Upscaling to high end products for both domestic consumption and export (to compete with

global OEMs)

4 APAC: Road freight in the region is expected to grow at 8.3% annually through 2019

5APAC: There will be additional manufacturing shift from China to lower cost APAC countries and

our presence and product offering will be required

6 Thailand: Award of ISUZU fifth wheel business expected in early 2016

Design

the future

December 09, 2015

Capital Markets Day 2015

Alexander Geis, President Aftermarket Business Unit

42

General Information: Business Area EMEA & India

• 16 subsidiaries including 6 manufacturing

facilities

• ~1,270 employees

• 3,300+ Aftermarket spare parts and service

stations in this region

• 7 main product groups for 3 segments

– Fifth wheels, Trilex wheel systems, Tag

axles and Suspensions for Trucks

– Axles systems, Suspensions, King pins, Ball

races, Landing gears, Trilex wheel systems

for Trailers

– Suspensions for Buses

General information

Axle systems &

suspensionsLanding gear

Kingpins

Fifth wheels

Suspensions

Key components and systems in the region

Spare parts

Trilex wheel

systems

Ball races

• Sales: € 530mn

Financial information (FY 2014)

43

Trailer Axles and

Suspension Systems

SAF-HOLLAND offers a comprising product portfolio in Europe addressing the specific customer needs in

this region; Opportunities on the product side to drive growth are emerging markets and new product

generations

Truck and Bus

SuspensionsFifth Wheels

Europe: SAF-HOLLAND core products

44

Trailer Axles and

Suspension Systems

SAF-HOLLAND offers a comprising product portfolio in MEA addressing the specific customer needs in this

region; Opportunities on the product side to drive growth are emerging markets and new product

generations

Truck and Bus

SuspensionsFifth Wheels

Middle East & India: SAF-HOLLAND core products

Trilex Wheel Systems

Trailer Brake and

EBS Systems

Trailer Lighting

Systems

45

EMEA & India: Key OE (customers) producing trucks and trailers

SAF-HOLLAND offers its innovative products to major OE´s in the truck and trailer industry in EMEA

Focus on fleets: SAF-HOLLAND end customer base includes a manifold of major forwarding agents and

fleets in EMEA

EMEA: End customer base of transport companies using trucks & trailers

46

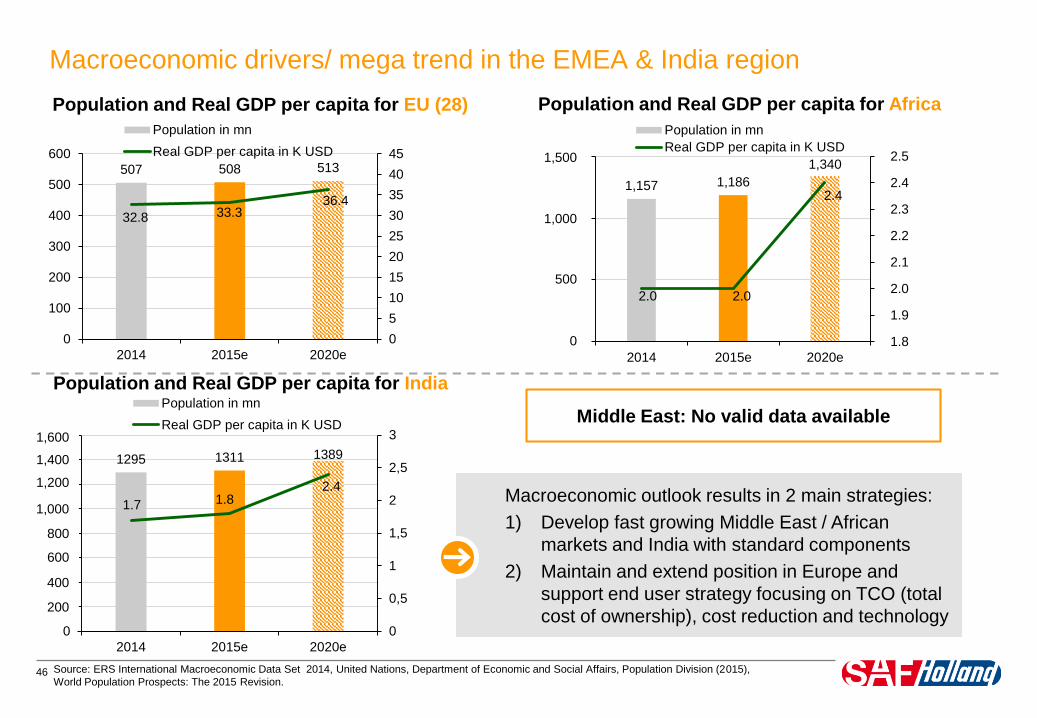

507 508 513

32.8 33.336.4

0

5

10

15

20

25

30

35

40

45

0

100

200

300

400

500

600

2014 2015e 2020e

Population in mn

Real GDP per capita in K USD

Macroeconomic drivers/ mega trend in the EMEA & India region

Population and Real GDP per capita for EU (28)

Source: ERS International Macroeconomic Data Set 2014, United Nations, Department of Economic and Social Affairs, Population Division (2015),

World Population Prospects: The 2015 Revision.

1,157 1,186

1,340

2.0 2.0

2.4

1,8

1,9

2

2,1

2,2

2,3

2,4

2,5

00

500

1.000

1.500

2014 2015e 2020e

Population in mn

Real GDP per capita in K USD

Population and Real GDP per capita for Africa

Macroeconomic outlook results in 2 main strategies:

1) Develop fast growing Middle East / African

markets and India with standard components

2) Maintain and extend position in Europe and

support end user strategy focusing on TCO (total

cost of ownership), cost reduction and technology

1295 1311 1389

1.7 1.82.4

0

0,5

1

1,5

2

2,5

3

0

200

400

600

800

1000

1200

1400

1600

2014 2015e 2020e

Population in mn

Real GDP per capita in K USD

Population and Real GDP per capita for India

Middle East: No valid data available

2.5

2.4

2.3

2.2

2.1

2.0

1.9

1.80

500

1,000

1,500

1,600

1,400

1,200

1,000

800

600

400

200

47

Heavy investments in road infrastructure will occur predominantly in the emerging markets: Russia, India,

Turkey and Nigeria as part of BRIC/MINT are just the most popular examples

Source: CIA World Factbook

8.000.000

9.000.000

10.000.000

11.000.000

12.000.000

13.000.000

14.000.000

15.000.000

0

5.000.000

10.000.000

15.000.000

20.000.000

25.000.000

30.000.000

35.000.000

2005 2010 2012 2015

G7 BRICS+MINT TOTAL

TOTAL km worldwide km G7/BRICS/MINT

+24.5%

+56.8%

+4.0%

Road Network

48

EMEA & India: Market structure, SAFH positioning and technological pattern

Middle East, Africa & IndiaEurope

• Market structure

Developing and growing OEMs

CKD productions for trucks

Gain in local competence as India´s industry

grows

Fast growing populations which lead to an

increase in demand of public and commercial

transport

Old fleets

• SAF-HOLLAND positioning

Premium segment in quality and technology

Entry of market for bus air suspensions

• Technological pattern

Air suspension only for high end applications -

tankers / reefers

Biggest portion is currently mechanical

suspension and drum brake

Presently low end markets

• Aftermarket Unstructured; clear potential for A2 brands and

3rd party products

• Market structure

Mature and well developed market

Big 7 Truck OEMs

Trailer builders with captive axle products

Competition sensitivity and market shares

• SAF-HOLLAND positioning

Technology leader

Focus on TCO

USP: End user approach

• Technological pattern

Air suspension dominating

Disc brake as standard for Truck and Trailer

• Aftermarket

Well developed network with educated

dealers and service stations

OEM population reaching plateau

Increase of A2 and 3rd party product sales

49

EMEA & India: Action plans and measures

Middle East, Africa & IndiaEurope

• Basic axle and mechanical suspension

development to serve standard applications

• Strengthen local FW business as production of

CKD picking up again

• Maintain and strengthen leading position in the

premium segment

• Positioning as complete system supplier for the

local truck / bus and trailer manufacturers

• Expansion of truck and bus suspension business

• Implementation of European end-user strategy

• Expand sales network in Africa

• Further growth of A2 and 3rd party product range

• Focus on smaller OEMs (Truck, Trailer, Bus)

• Introduction of cost reduced INTRA S suspension

• Product to market initiatives of innovations such as

FW32.14W, SAF Direct, galvanized axle, new bus

suspensions, etc.

• Material cost and SG&A: work on detailed plans for

2016/2017

• Finished plant consolidation in Europe and further

investigation of business processes – make or buy

• First impacts to be realized 2016/2017

50

EMEA & India: Risks and Opportunities

EMEA & India

RISKS

• Crisis in Russia / Ukraine / Syria has a significant impact on business including currency issues

• Captive axles of biggest trailer builders – counter measures: introduction of INTRA S & targeting small and

mid-size trailer builders

• Cost pressure – counter measures already implemented

OPPORTUNITIES

• Iranian market to be opened soon

• New customers in small and mid-size segment (Truck, Trailer & Bus)

• End user work in Europe rolled out – additional fleet sales people

• Innovations for Truck and Trailer builders

• Supply of MAN with Fifth wheels starting in 2016

51

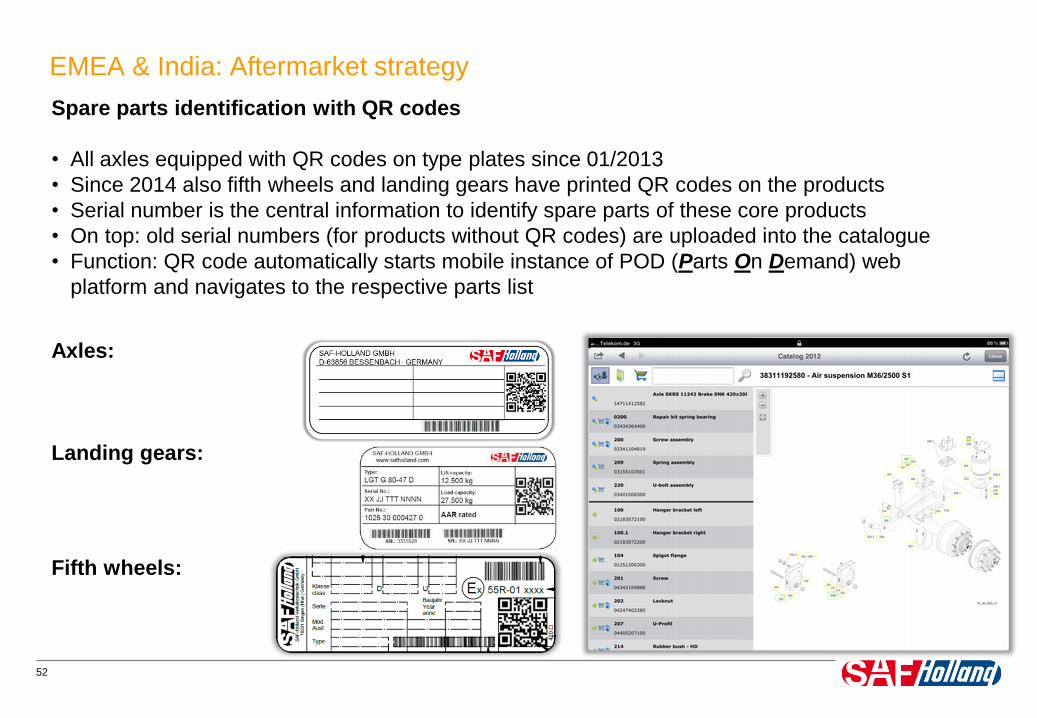

EMEA & India: Aftermarket strategy

Central warehouse

Subsidiaries

Representatives

Sales offices

4

2

3

Overview• 2 Central warehouses for feeding regional

warehouses and reps / direct shipments

• 11 subsidiaries with local warehouses

• 12 representatives with own warehouses

Regional expansionNew regional sales office since October 2015

in Nairobi, Kenia covering “green belt”

countries in Central Africa

Possible new sales office in Morocco/Tunisia

to serve Western Maghreb states and

Western Africa

Re-evaluate structures and setup of subsidiary

in South Africa and work on neighboring

countries like Namibia, Botswana, Zimbabwe,

Mozambique

Stabilize and grow Russia, Ukraine, Belarus

and Stan countries: add new sales partners

and service stations. A2 brand has significant

sales potential

1

2

3

1

4

52

EMEA & India: Aftermarket strategy

Spare parts identification with QR codes

• All axles equipped with QR codes on type plates since 01/2013

• Since 2014 also fifth wheels and landing gears have printed QR codes on the products

• Serial number is the central information to identify spare parts of these core products

• On top: old serial numbers (for products without QR codes) are uploaded into the catalogue

• Function: QR code automatically starts mobile instance of POD (Parts On Demand) web

platform and navigates to the respective parts list

Axles:

Landing gears:

Fifth wheels:

53

SAF-HOLLAND for Fleets App

• Workshop: GPS based Official Service partner search

• Parts dealer: GPS based Original Parts

dealer search

• QR Code scanner

• POD Shop: mobile version of online shop

• Fleet Connect: access and functions

of accounts

Plans for Version 2.0 (2016 / 2017)

• Additional languages

• Additional functions like training registrations

• Videos and repair instructions

• News channels

EMEA & India: Aftermarket strategy

54

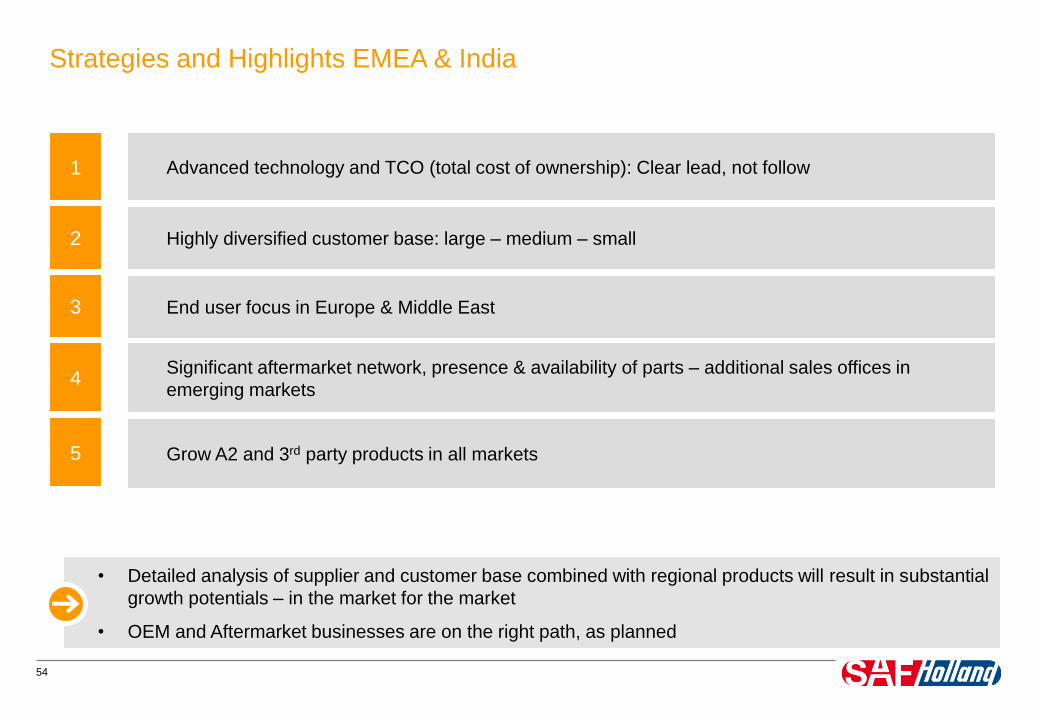

Strategies and Highlights EMEA & India

Advanced technology and TCO (total cost of ownership): Clear lead, not follow1

2 Highly diversified customer base: large – medium – small

3 End user focus in Europe & Middle East

4Significant aftermarket network, presence & availability of parts – additional sales offices in

emerging markets

5 Grow A2 and 3rd party products in all markets

• Detailed analysis of supplier and customer base combined with regional products will result in substantial

growth potentials – in the market for the market

• OEM and Aftermarket businesses are on the right path, as planned

55

Sales in €mn Summary

• Solid market share development in Europe

• Moderate investments in Europe and Middle East

• Strong growth in MEA

• To follow the growth path SAF-HOLLAND Middle East

has to play a more important role in the organization –

will be fully supported by central functions

• Re-started Indian market penetration with fully owned

subsidiary

• Sales target for the region is € 603mn in 2020

• Sales development based on a stable European environment and continuous growth in MEA / India

EMEA & India: Business performance and sales targets 2020

530

603

300

350

400

450

500

550

600

650

FY2014 Target 2020

Design

the future

December 09, 2015

Capital Markets Day 2015

Steffen Schewerda, President Trailer Systems

Business Unit

57

General Information: Business Area AMERICAS

• 4 subsidiaries including 9 manufacturing facilities

• ~ 1,450 employees

• ~ 5,600 Aftermarket service stations in this region

Axle systems &

suspensions

Landing gear

Kingpins

Fifth wheels

Suspensions

• Sales: € 380mn

General information Key components and systems in the region

Financial information (FY 2014)

Spare parts

58

Trailer Axles and

Suspension Systems

SAF-HOLLAND offers a comprising product portfolio in the AMERICAS addressing the specific customer

needs in this region; Opportunities on the product side to drive growth are given especially with suspensions

Truck and Bus

SuspensionsFifth Wheels

AMERICAS: SAF-HOLLAND core products

59

AMERICAS: Key OE (customers) producing trucks and trailers

SAF-HOLLAND offers its innovative products to major OE´s in the truck and trailer industry active in

AMERICAS

60

Focus on the fleets: SAF-HOLLAND end customer base includes a manifold of major forwarding agents and

fleets in AMERICAS

AMERICAS: End customer base of transport companies using trucks & trailers

61

361 362 375

56.2

56.9

63.6

51

53

55

57

59

61

63

65

0

100

200

300

400

500

600

2014 2015e 2020e

Population in mn Real GDP per capita in K USD

Macroeconomic drivers/ mega trend in the AMERICAS region

Population and Real GDP per capita for NA

Source: ERS International Macroeconomic Data Set 2014, United Nations, Department of Economic and Social Affairs, Population Division (2015),

World Population Prospects: The 2015 Revision.

630 631 659

6.7 6.8

8.1

0

1

2

3

4

5

6

7

8

9

0

500

1000

1500

2014 2015e 2020e

Population in mn Real GDP per capita in K USD

Population and Real GDP per capita for Latin America

Growth projections are moderate. However, with 64 K USD per capita, North America is also in 2020 one of

the strongest economies in the world. Latin America will grow >20% over the next 5 years

62

AMERICAS: Market structure, SAFH positioning and technological pattern

Latin AmericaNorth America

• Premium-market segment with clear

focus on the end user

• SAF-HOLLAND well positioned with

brand, products and service

• Trend towards more technically

sophisticated products (e.g. Disc

Brakes) is visible but will require time

• Due to high number of component

suppliers and fleet specifications,

aftermarket business is very diverse

• Low to Mid-market segment more

focused on price. At present small

premium-market segment

• SAFH positioned as the a technology

leader with access to the premium-

market segment

• Core technology. Initial price is more

important than life cycle cost

• Due to the currently low sales volume of

SAF-HOLLAND, the Aftermarket will

develop when population in the market

is installed

63

AMERCIAS: Opportunities and measures

Latin AmericaNorth America

• Beside well established product lines

(e.g. Fifth wheels, Landing gears),

strong growth potential lies especially in

the axle and suspension product line

• Truck suspensions and Trailer axles and

suspensions will be the mayor growth

drivers over the next years

• Introduction of new technology and

providing the fleets with value added

products will be one of the key success

factors

• The Aftermarket will increase even

further, based on growing field

population and recent record

registrations

• Two directional approach: Nurture the

premium-market segment, but also

develop competitive products for the

mid-market segment

• Customers will clearly prefer SAF-

HOLLAND over other brands if the

commercial package is attractive

• Truck, Bus and Trailer suspensions

provide significant growth opportunity

• Aftermarket will develop further with OE

market share

64

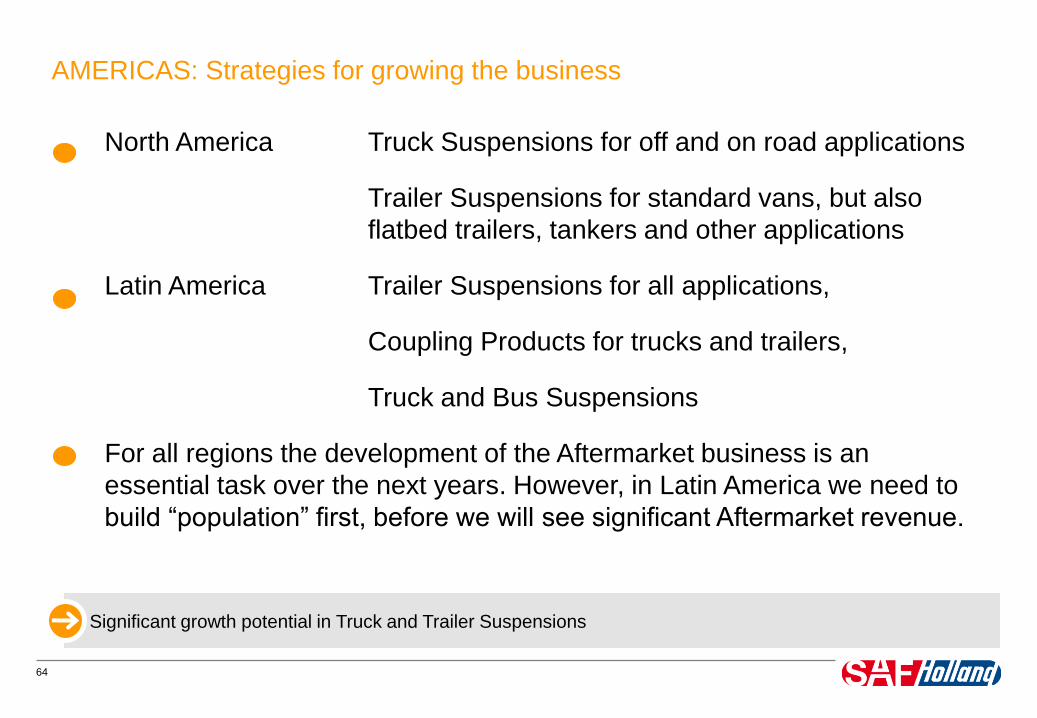

AMERICAS: Strategies for growing the business

North America Truck Suspensions for off and on road applications

Trailer Suspensions for standard vans, but also

flatbed trailers, tankers and other applications

Latin America Trailer Suspensions for all applications,

Coupling Products for trucks and trailers,

Truck and Bus Suspensions

For all regions the development of the Aftermarket business is an

essential task over the next years. However, in Latin America we need to

build “population” first, before we will see significant Aftermarket revenue.

Significant growth potential in Truck and Trailer Suspensions

65

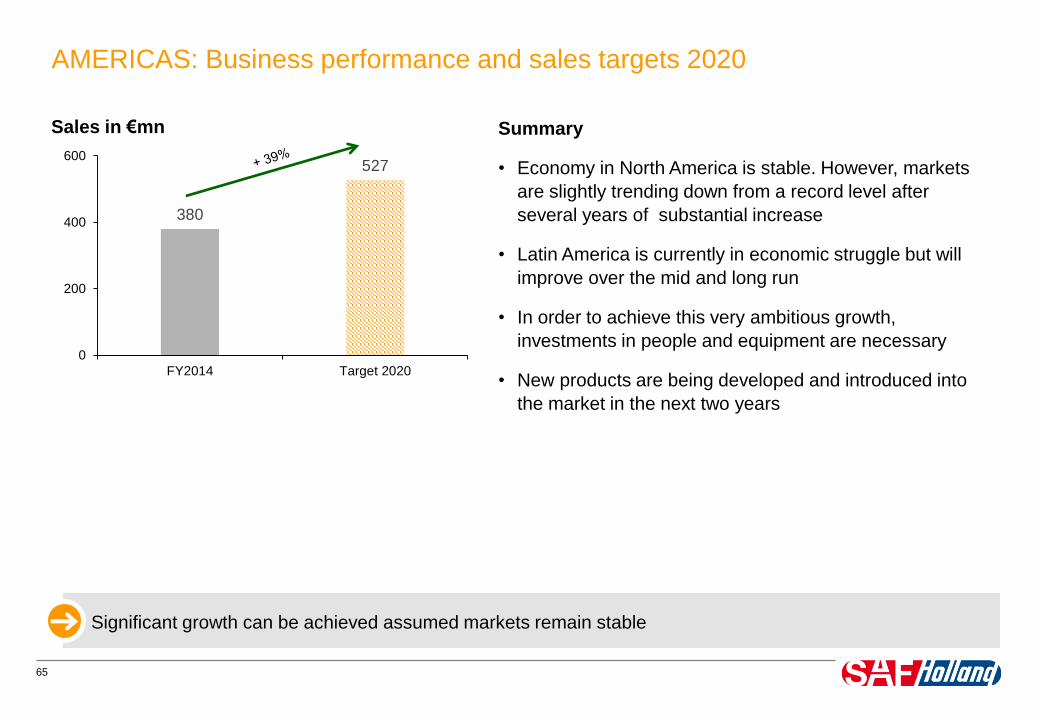

380

527

0

200

400

600

FY2014 Target 2020

Sales in €mn Summary

• Economy in North America is stable. However, markets

are slightly trending down from a record level after

several years of substantial increase

• Latin America is currently in economic struggle but will

improve over the mid and long run

• In order to achieve this very ambitious growth,

investments in people and equipment are necessary

• New products are being developed and introduced into

the market in the next two years

Significant growth can be achieved assumed markets remain stable

AMERICAS: Business performance and sales targets 2020

Challenges in the

Transportation Industry

SAF-HOLLAND Highlights in R&D

Engineering

Mike Kamsickas, President Powered Vehicle Systems Business

UnitDecember 09, 2015

67

Cost

Efficiency

Product

Efficiency

Technology

Innovation

Product

Quality

OEM

How to influence the success of our customers?

Tra

nsp

ort

Eff

icie

ncy

Total Cost of

Ownership

Flexibility /

Multipurpose

Use

Safety

Requirements /

Legislation

Ecological

Requirements /

Legislation

End User / Fleet

68

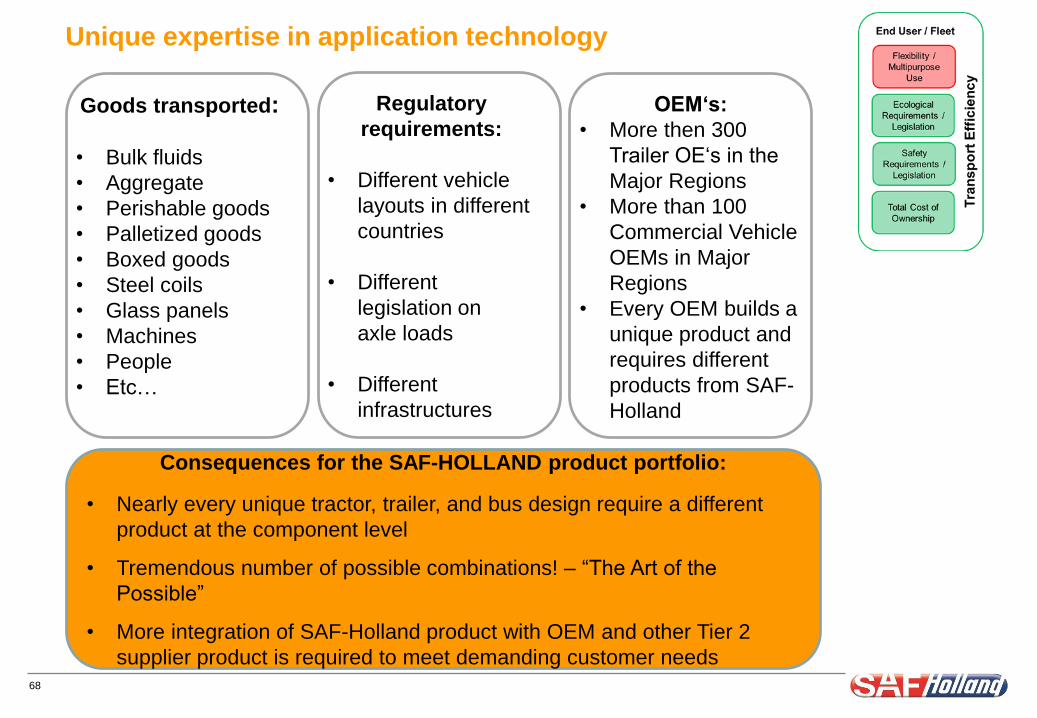

Unique expertise in application technology

Regulatory

requirements:

• Different vehicle

layouts in different

countries

• Different

legislation on

axle loads

• Different

infrastructures

OEM‘s:

• More then 300

Trailer OE‘s in the

Major Regions

• More than 100

Commercial Vehicle

OEMs in Major

Regions

• Every OEM builds a

unique product and

requires different

products from SAF-

Holland

Goods transported:

• Bulk fluids

• Aggregate

• Perishable goods

• Palletized goods

• Boxed goods

• Steel coils

• Glass panels

• Machines

• People

• Etc…

Consequences for the SAF-HOLLAND product portfolio:

• Nearly every unique tractor, trailer, and bus design require a different

product at the component level

• Tremendous number of possible combinations! – “The Art of the

Possible”

• More integration of SAF-Holland product with OEM and other Tier 2

supplier product is required to meet demanding customer needs

69

It’s all about cutting CO2, and cost per mile

IAA 2014: Discussion Forum:

Creating transparency in truck fuel consumption

Wissmann also praised the EU for its plan to create

transparency in truck fuel consumption. “It’s a good idea to

require the disclosure of CO2-values instead of imposing strict

limits as the trucking industry is already calculating on a tight

budget.”

12/2014 :Fact-finding studies in support of the development

of an EU strategy for freight transport logistics

LOT 3: Introduction of a standardized carbon footprint

methodology:

“To harmonize carbon foot printing and to allow

benchmarking of transport . . .

The European Commission has taken the initiative to contributing

to the development of harmonized carbon foot printing standards

for passenger and freight transport.“

3/2015: MISSION OF THE DIRECTORATE-GENERAL FOR

MOBILITY AND TRANSPORT

“developing an agenda for innovation: promoting research

and the development and roll-out of a new generation of

sustainable transport technologies and systems particularly for

integrated traffic management and low-carbon transport,

including in urban areas”

General drive to CO2-based

legislation on OEMs but even

more emphasis on efficiency by

fleet and end users.

70

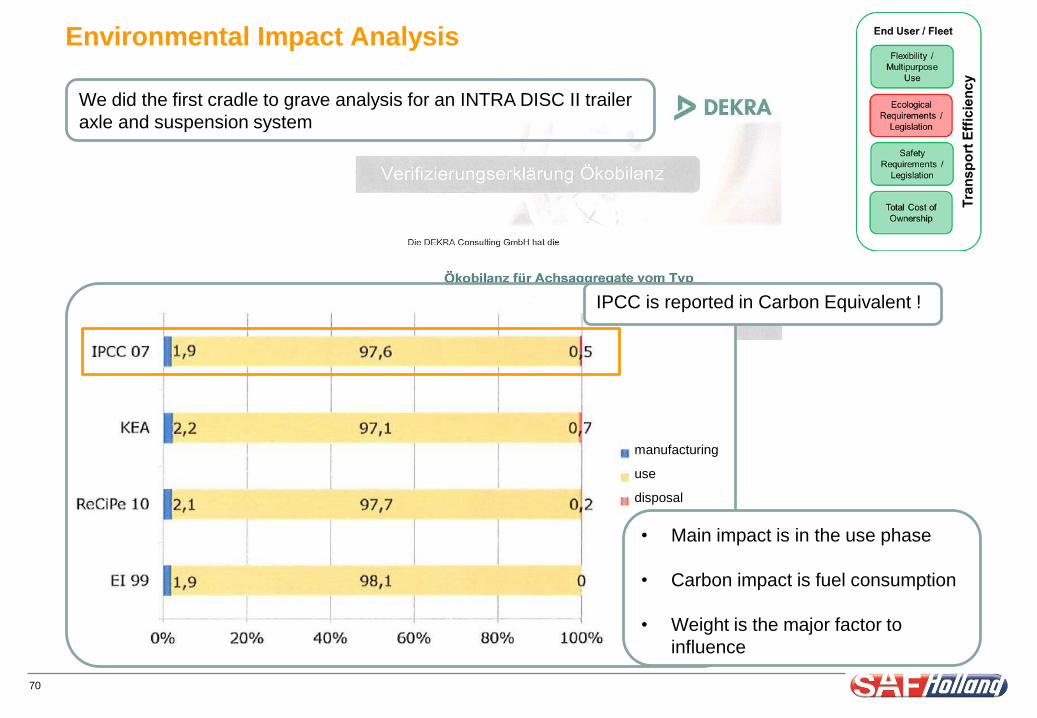

Environmental Impact Analysis

manufacturing

use

disposal

We did the first cradle to grave analysis for an INTRA DISC II trailer

axle and suspension system

IPCC is reported in Carbon Equivalent !

• Main impact is in the use phase

• Carbon impact is fuel consumption

• Weight is the major factor to

influence

71

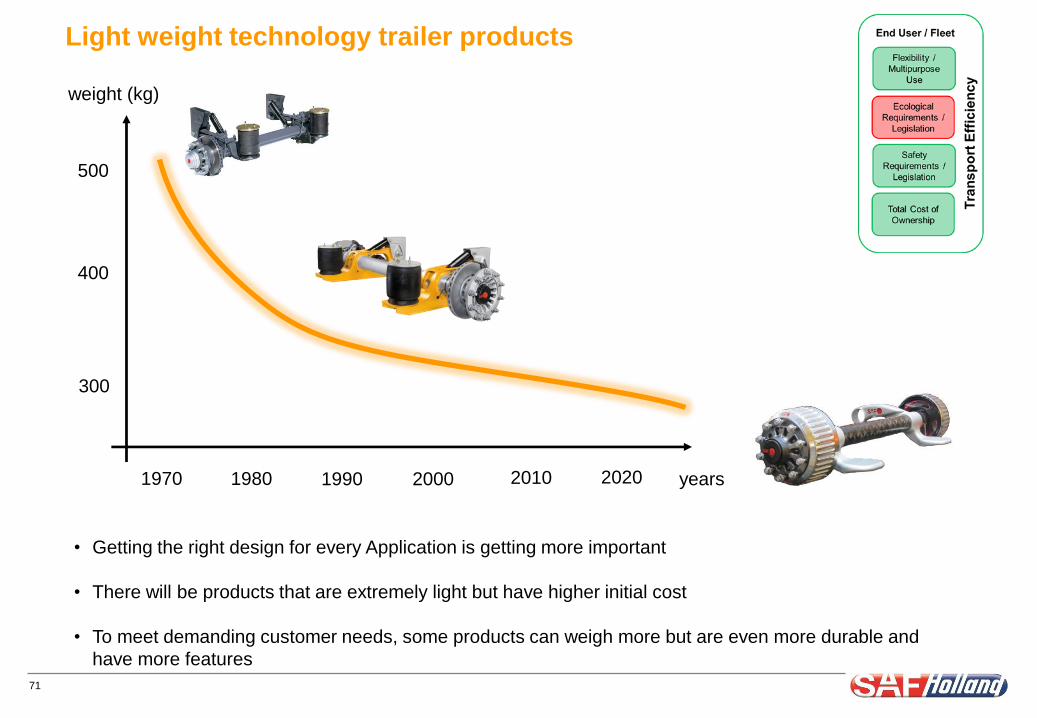

Light weight technology trailer products

• Getting the right design for every Application is getting more important

• There will be products that are extremely light but have higher initial cost

• To meet demanding customer needs, some products can weigh more but are even more durable and

have more features

weight (kg)

500

400

300

1970 1990 2000 years2010 20201980

72

Electric Drivetrain Bus Suspension

• Electric Bus is a high growth market in China and APAC – driven by heavy government subsidies!

• This application requires additional space for batteries, while maintaining suspension performance and roll

stability

• Rear Air Spring positioning allows more space for batteries near the rear wheels.

• New “J Beam” design versus traditional C-Beam allows the bus manufacturer the extra space they need,

with no compromise in ride comfort and performance

73

Light weight technology truck suspension products

• A lot of collaboration with OEMs is necessary to integrate products into new applications.

• OEMs expecting higher levels of DVP&R

• More integration of SAF-Holland products into chassis and axles is necessary for weight reduction

weight (kg)

725

500

300

1970 1990 2000 years2010 20201980

Coming Soon!

74

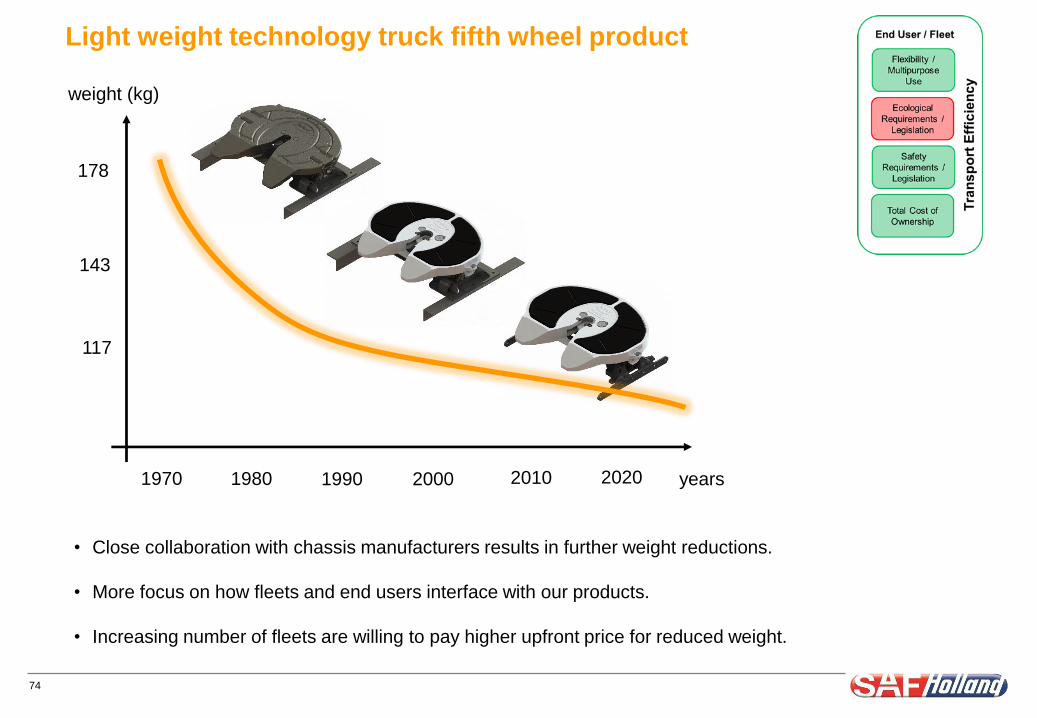

Light weight technology truck fifth wheel product

• Close collaboration with chassis manufacturers results in further weight reductions.

• More focus on how fleets and end users interface with our products.

• Increasing number of fleets are willing to pay higher upfront price for reduced weight.

weight (kg)

178

143

117

1970 1990 2000 years2010 20201980

75

Light weight technology – What’s next?

- 64 kg

per axle

starting at 410 kg system weight…

76

Advantages for End Users

• Weight saving compared to existing solution

Can carry higher loads

Reduction of fuel consumption

CO2-reduction

Advanced driving behavior and safety

Higher resale value

• Optimized field service / maintenance

Maintenance free sealed unit

Use of standard disc brake / brake chambers

Reduction of maintenance times

XXX

Advantages for the OEM

• Component reduction (camshaft, slack,..)

Reduced vehicle weight

Increased freedom of design for the vehicle

manufacturer

• Use of standard disc brake / brake chambers

Brake chambers can already be assembled

Simplified parts logistics

Reduced vehicle assembly effort

SAF Direct: CO2 reduction and TCO

compliment each other

77

Thank you for your attention

Design

the future

December 09, 2015

Capital Markets Day 2015

Wilfried Trepels, CFO

79

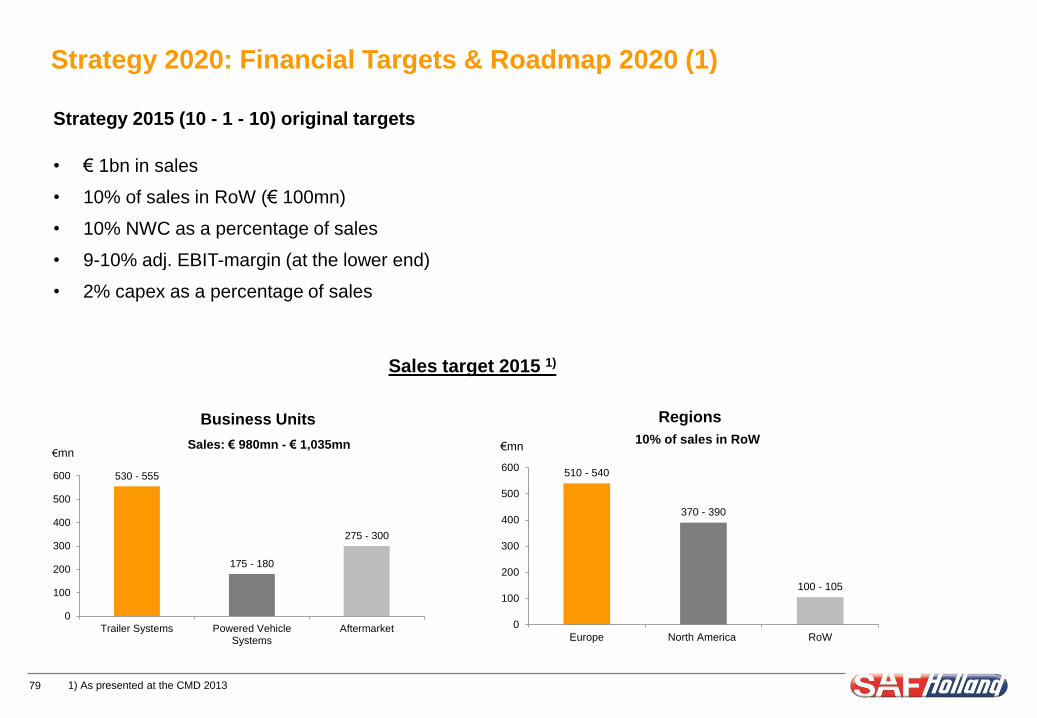

Strategy 2020: Financial Targets & Roadmap 2020 (1)

Strategy 2015 (10 - 1 - 10) original targets

• € 1bn in sales

• 10% of sales in RoW (€ 100mn)

• 10% NWC as a percentage of sales

• 9-10% adj. EBIT-margin (at the lower end)

• 2% capex as a percentage of sales

Business Units Regions

1) As presented at the CMD 2013

510 - 540

370 - 390

100 - 105

0

100

200

300

400

500

600

Europe North America RoW

10% of sales in RoW€mn

Sales target 2015 1)

530 - 555

175 - 180

275 - 300

0

100

200

300

400

500

600

Trailer Systems Powered VehicleSystems

Aftermarket

Sales: € 980mn - € 1,035mn€mn

80

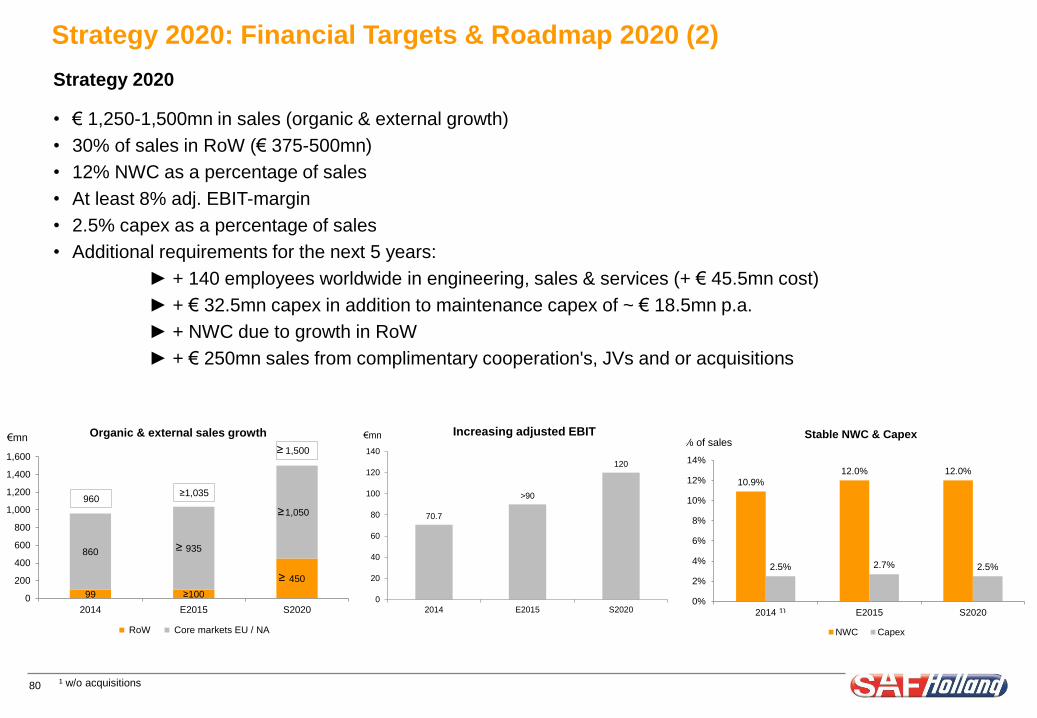

Strategy 2020: Financial Targets & Roadmap 2020 (2)

Strategy 2020

• € 1,250-1,500mn in sales (organic & external growth)

• 30% of sales in RoW (€ 375-500mn)

• 12% NWC as a percentage of sales

• At least 8% adj. EBIT-margin

• 2.5% capex as a percentage of sales

• Additional requirements for the next 5 years:

► + 140 employees worldwide in engineering, sales & services (+ € 45.5mn cost)

► + € 32.5mn capex in addition to maintenance capex of ~ € 18.5mn p.a.

► + NWC due to growth in RoW

► + € 250mn sales from complimentary cooperation's, JVs and or acquisitions

¹ w/o acquisitions

99 ≥100

450

860 935

1,050

0

200

400

600

800

1,000

1,200

1,400

1,600

2014 E2015 S2020

RoW Core markets EU / NA

Organic & external sales growth

≥1,035960

€mn

1,500

70.7

>90

120

0

20

40

60

80

100

120

140

2014 E2015 S2020

€mn€mnIncreasing adjusted EBIT

10.9%

12.0% 12.0%

2.5% 2.7% 2.5%

0%

2%

4%

6%

8%

10%

12%

14%

2014 E2015 S2020

NWC Capex

€mn% of salesStable NWC & Capex

1)

≥

≥

≥

≥

Increasing adjusted EBIT

81

Strategy 2020: Financial Targets & Roadmap 2020 (3)

Strategy 2020

64 Business plans (8 product lines x 8 regions)

• 3 main product areas of growth:

- Trailer Axles & Suspensions

- AM spare parts & service network

- Truck & Bus Suspensions

• 3 main regions:

- Europe & Middle East / Africa/ India

- North America, Mexico & Brazil

- China & APAC

483

240

51

653

333

132

0

100

200

300

400

500

600

700

800

TA&S AMSP T&BS

2014 S2020

€mn€mn€mn€mn€mn3 main product areas (~80% of growth = € 1.1 bn)

+35%

+39%

+159%

530

380

50

603

527

120

0

100

200

300

400

500

600

700

EU / MEA NA / MEX / BRA CH / APAC

2014 S2020

€mn

+39%

+140%

3 main regions

+14%

82

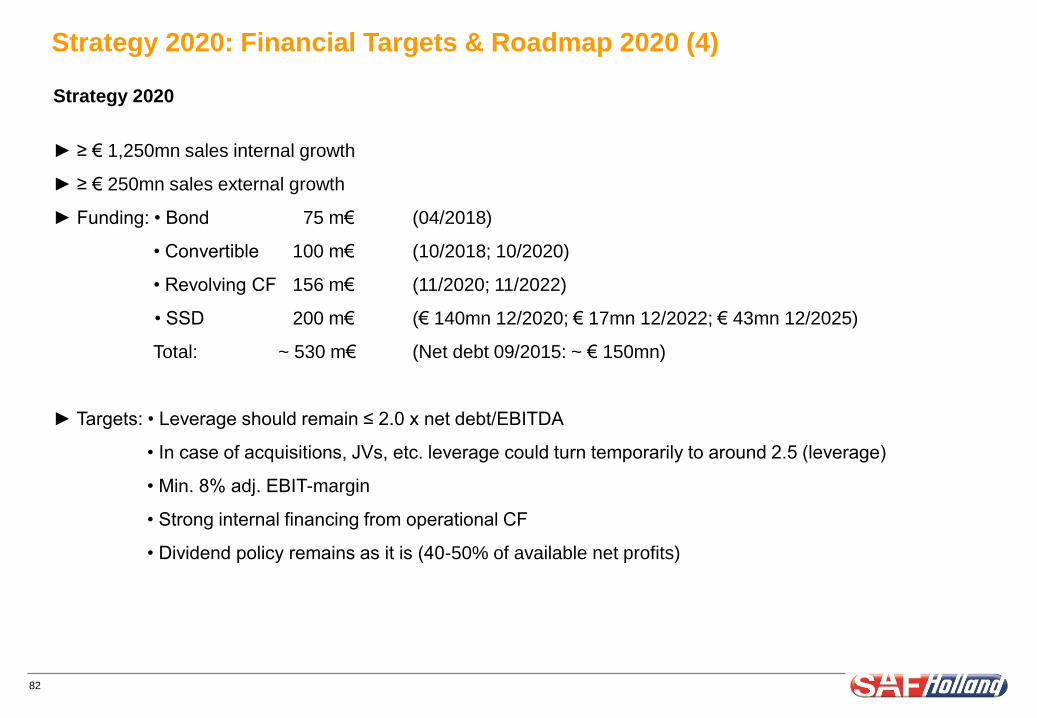

Strategy 2020: Financial Targets & Roadmap 2020 (4)

Strategy 2020

► ≥ € 1,250mn sales internal growth

► ≥ € 250mn sales external growth

► Funding: • Bond 75 m€ (04/2018)

• Convertible 100 m€ (10/2018; 10/2020)

• Revolving CF 156 m€ (11/2020; 11/2022)

• SSD 200 m€ (€ 140mn 12/2020; € 17mn 12/2022; € 43mn 12/2025)

Total: ~ 530 m€ (Net debt 09/2015: ~ € 150mn)

► Targets: • Leverage should remain ≤ 2.0 x net debt/EBITDA

• In case of acquisitions, JVs, etc. leverage could turn temporarily to around 2.5 (leverage)

• Min. 8% adj. EBIT-margin

• Strong internal financing from operational CF

• Dividend policy remains as it is (40-50% of available net profits)

83

Building on a strong year 2015, from today’s perspective 2016 will become another solid year with stable

operational performance laying the basis for the implementation of the growth strategy 2020.

Actual 2015 versus Strategy 2020

Markets:

• Anticipating a retraction of the US market peaking off from record levels

• Growth in Western Europe curtailed by continuous weakness in Russia

• Flattish markets in Brazil and Australia due to political situation and insufficient prices of raw materials

• Sale of non-core Aerway product line

Balancing measures to match these effects:

• Market share gains

• New products (e.g. Intra S/R)

• Expansion of vocational segments

• Further efficiency improvements

Strategy 2020: Financial Targets & Roadmap 2020 (5)

84

Disclaimer

By attending the meeting where this presentation is made, or by reading the presentation slides, you agree to be bound by the following limitations: The information in

this document has been prepared by SAF-HOLLAND S.A. ("SAF-HOLLAND") for use at a road show presentation by SAF-HOLLAND and does not constitute a

recommendation regarding securities of SAF-HOLLAND.

No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the

information, or opinions contained herein. Neither SAF-HOLLAND nor any of SAF-HOLLAND's advisors or representatives shall have any responsibility or liability

whatsoever (for negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with this

document. The information set out herein may be subject to updating, completion, revision, verification and amendment and such information may change

materially.

This presentation is based on the economic, regulatory, market and other conditions as in effect on the date hereof. It should be understood that subsequent

developments may affect the information contained in this document, which neither SAF-HOLLAND nor its advisors are under an obligation to update, revise or

affirm.

The distribution of this presentation in certain jurisdictions may be restricted by law. Persons into whose possession this presentation comes are required to inform

them-selves about and to observe any such restrictions. In particular, this presentation may not be distributed into the United States, Australia, Japan or Canada.

This presentation contains statements concerning the expected future business of SAF-HOLLAND, expected growth prospects and other opportunities for an increase

in value of the company as well as other financial data and certain third-party market data. These forward-looking statements are based on management's current

expectations, estimates and projections and on third-party market data, respectively. They are subject to a number of assumptions and involve known and unknown

risks, uncertainties and other factors that may cause actual results and developments to differ materially from any future results and developments expressed or

implied by such forward-looking statements. Neither SAF-HOLLAND nor its advisors has any obligation to periodically update or release any revisions to the

forward-looking statements contained in this presentation to reflect events or circumstances after the date of this presentation.

This presentation constitutes neither an offer to sell nor a solicitation to buy any securities in the United States, Germany or any other jurisdiction. Neither this

presentation nor anything contained herein shall form the basis of, or be relied on in connection with, any offer or commitment whatsoever.

In particular, this presentation does not constitute an offer to sell or a solicitation of an offer to buy any securities of SAF-HOLLAND in the United States. Securities of

SAF-HOLLAND may not be offered or sold in the United States of America absent registration or an exemption from registration under the U.S. Securities Act of

1933, as amended. SAF-HOLLAND does not intend to conduct a public offering or any placement of securities in the United States.

85

Investor Relations

SAF-HOLLAND GmbH

Stephan Haas

Hauptstraße 26

63856 Bessenbach

Phone +49 6095 301-617

Telefax +49 6095 301-102

Mobile +49 170 306 64 97

www.safholland.com