developing a computer simulation based approach to

TRANSCRIPT

Developing a Computer Simulation Based Approach to Simulate Potency of Islamic Voluntary Sector to Alleviate the Poverty in

Indonesia Using System Dynamics Methodology

Dian Masyita ([email protected] and [email protected] ) The Faculty of Economics, Padjadjaran University, Bandung, Indonesia

Submitted to First International Conference on Inclusive Islamic Financial Sector Development:

Enhancing Islamic Financial Services for Micro and Medium Sized Enterprises (MMEs), Brunei, 17th – 19th April 2007

Abstract

This research tries to find out the potency of Islamic Voluntary Sector as financial instrument to alleviate the poverty in Indonesia. This research also tries to offer a computer simulation based approach design of the cash waqf fund management system and zakah fund as a part of Islamic Voluntary Sector in a system dynamics model. Using the system dynamics methodology, we try to know the structure of the cash waqf funds management system and simulate the behaviour of cash waqf and zakah fund.

Zakah and Cash Waqf fund are expected to become the alternative instruments for the poverty alleviation programs in Indonesia. These programs require huge amount of fund that cannot be provided thoroughly by the government. Therefore, development of the voluntary sector for such a program is inevitable. In the Islamic sosio-economic concept, there are some sources of social fund that are economically and politically free of charge, namely cash waqf and zakah, infaq and shodaqah. In this research we focus in Cash Waqf Management and Zakah fund. In these concepts, Nadzir collects the fund from Waqif and invest the money in the real sector (mainly Small & Medium-sized Ventures) and in any syariah-based investment opportunities and Amil also collects the fund from Muzzaki. Amil will distribute all of Zakah fund for Mustahiq and Nadzir will then allocate all profits and returns gained from the investments to any poverty alleviation programs to enhance the quality of poor people’s life, such as free education and health service, cheap basic food, etc.

Not just like Amil, who is allowed to distribute all of zakah fund, Nadzir is obliged to maintain the amount of fund in such a way that it does not go below the initial amount. Therefore, Nadzir not only should be highly capable, but also needs a financial institution, which has been proven to be experienced, highly capable and effective in helping Micro and SMEs development efforts, since such a microfinancing program is considered as the most vital portfolio in the poverty alleviation program. Therefore, it’s necessary to design an instrument which is able to control the cash waqf management.

Keywords: the cash waqf fund, zakah fund, portfolio investment, microfinance, poverty alleviation, system dynamics

1. Preface

Since the Indonesian poverty rate has been still discouraging, development the Islamic voluntary sector is a must in a country that has almost ninety percent Moslim. Based on the Indonesian Statistics Central Bureau (BPS)’s data, there are about 40 million Indonesian people who are under the poverty line. Indonesia has come into debt trap made by the Indonesian government and the private sectors. Large amount of debt has weakened Indonesian economy for the past ten years. Meanwhile, the government has been confronted with the deficit budget almost every year since 1997, which means that the government may find it difficult to cover its routine expenditures. Those regular balance sheet items require so large amount of fund that government cannot provide adequate fund for other strategic needs, such as good education, appropriate health, poverty, and Micro & SME’s development. Mismanagement of debts is the largest of all factors that make Indonesia go into crisis. Consequently, all of citizens and their offsprings have to carry the heavy burden of that debt.

2. Problem Identification

The potential sources of fund to the necessity of sufficient fund for public needs are a special endowment fund, cash waqf, and zakah from people’s donation. People donate their money as cash waqf by purchasing cash waqf certificate. The gathered fund will be then invested in various investment portfolio and the profit of which can be spent for the above mentioned public necessities. The gained profit will also be used for funding poverty alleviation programs, while the principal of funds will be reinvested in various highly profitable investment opportunities. Waqif donates his/her money as waqf fund to Mauquf’alaih (a person who is entitled to get benefit from waqf fund) through Nadzir (a person/an institution being in charge for managing waqf fund and distributing returns of waqf investment). Only gains of the invested waqf fund will be delivered to Mauquf’alaih. The principal of funds keep being invested in potential investment opportunities. In relation to its role as waqf fund investment manager, Nadzir on behalf of Waqf Institution may allocate some waqf funds to financial portfolio and finance Micro & SMEs’ businesses on the basis of profit-loss sharing system. The larger the investment returns, the more fund can be allocated to poverty alleviation program. In some countries1, waqf fund management has reduced poverty effectively and enhanced people’s welfare, by providing additional fund for education & health development programs, cheap houses & public facilities development programs, and so forth. On the other hand, Muzzakki (person who are obliged to pay zakah because they have wealth or properties that are subject to zakah) donates his/her money as zakah fund to Mustahiq (rightful recipient of

1Mannan, M.A.Abdul, Cash Waqf Certificate- an Innovation in Islamic Financial Instrument: Global Opportunities for Developing Social Capital Market in the 21stCentury Voluntary Sector Banking”, Presentation at the Third Harvard University Forum on Islamic Finance, October 1, 1999

2

zakah because they are included as one of those mentioned in Al-Quran as the recipient of zakah) through Zakah Management Institution.

3. Objectives of Research

This research is expected to be able to find out the potency of the Islamic Voluntary Sector, expecially cash waqf and zakah, to alleviate the poverty in Indonesia. This research also tries to offer a computer simulation based approach of the cash waqf fund investment management system and the distribution of zakah fund in a system dynamics model. Using the system dynamics methodology, we try to study the structure of cash waqf management and zakah distribution system and then simulate the behaviour of them.

4. Research Metodology

This research used system dynamics methodology to capture dynamic

phenomenon of a system, in which variables change simultaneously as time moves. The field of system dynamics began in 1956 at the Massachusetts Institute of Technology, Cambridge, MA, USA. Since that time, the concept of dynamics behavior and feedback systems have enhanced the understanding of social, economic, management and physical systems2.

For the research purposes, some of previously researches support it. One of them is a survey on possible implementation of cash waqf in Jakarta and West Java (Masyita, 2001). The survey concluded that most people did not trust any existing government institution to manage cash waqf fund and control its investment activities, especially because cash waqf management will involve large amount of endowment funds. Most of them also recommend that if a special purpose institution is established to manage cash waqf fund, it has to be highly capable of detecting any potential dishonesty and assessing performance of cash waqf fund manager, i.e. nadzir. Therefore, it’s necessary to design an instrument which is able to control the cash waqf management.

Based on the survey’s result, using exclusively designed computer program then simulated some scenarios of cash waqf implemention to formulate some policy concepts applicable in Indonesia. The computer program was designed to help the policy makers (1) estimate cash waqf potential in alleviating poverty in Indonesia, (2) supervise performance of nadzir or waqf fund management institution, and (3) identify appropriate policies conducive to poverty alleviation programs (Masyita, 2005).

For cash waqf data purposes, since there was no similar study preceding the research, some assumptions were applied. The ability of three national TV corporations (RCTI, SCTV, and Indosiar) to collect donation amounting IDR 2 billions in two nights in 2000 and the other charity programs to collect donation in 2001-2005 were used as an assumption basis of amount of fund could be gathered by cash waqf management institution. This research also used data supplied by

2 Forrester, Jay.W. (1968), “Principle of System.”Wright-Allen Press, Inc

3

Biro Pusat Statistik Republik of Indonesia (National Beaurau for Statistics), BKKBN Republic of Indonesia (National Coordinating Agency for Family Planning) and Islamic Financial Institution. For zakah fund data purposes, the potency of zakah fund in Indonesia is obtained from some zakah institution historical data and predictions.

5. Limitation of Research

This research put more emphasived on financial management expecially for raising, investing of cash waqf fund and distributing of zakah fund. The duties of Nazir, as a cash waqf fund manager, are to increase the cash waqf funds and invest those funds in profitable portfolios. On the other hand, the duties of Amil, as a zakah fund manager, are to increase the zakah fund and distribute these funds to the appropriate Mustahiq. As we know, the poverty alleviation problems are complicated. However, they need multi and interdiscipline knowledge to formulate and figure out the solutions. With this research we want to try to make an early design of poverty alleviation program in the financial viewpoint using system dynamics modeling.

4

9

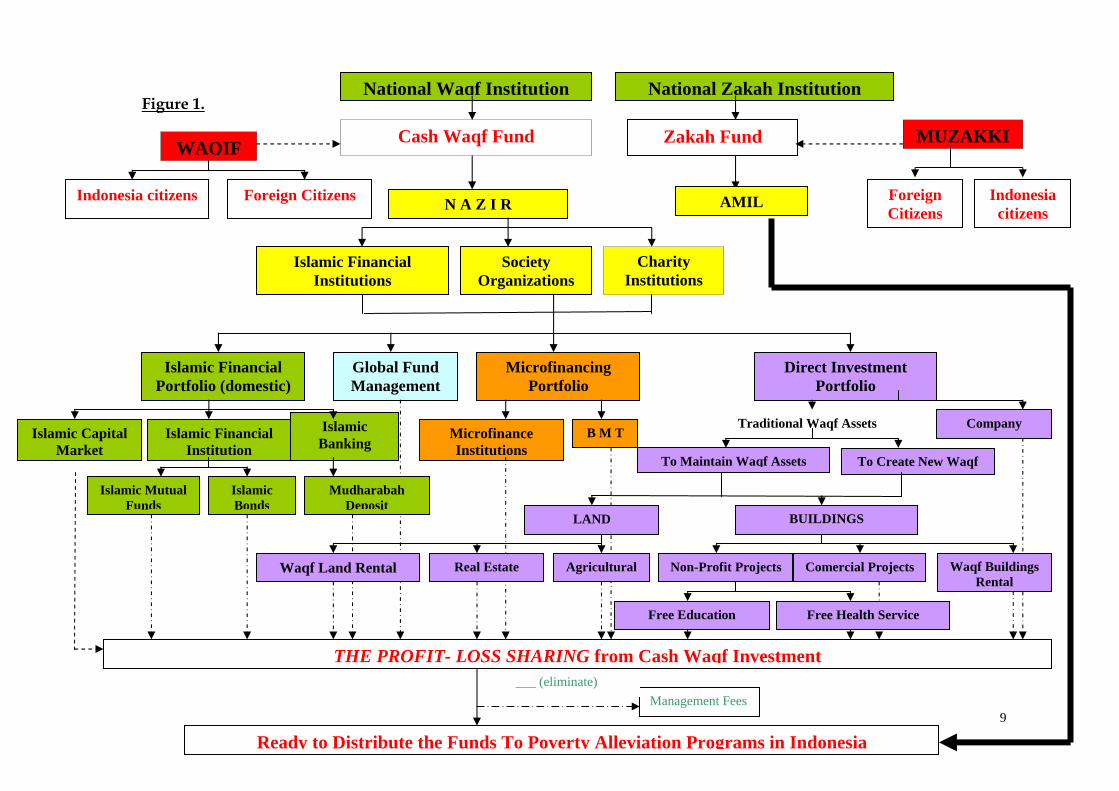

Figure 1.

National Waqf Institution

N A Z I R

Islamic Financial Institutions

Society Organizations

Charity Institutions

Cash Waqf Fund WAQIF Zakah Fund

Microfinancing Portfolio

Islamic Mutual Funds

Microfinance Institutions

Direct Investment Portfolio

Islamic Financial Portfolio (domestic)

Company B M T Islamic Capital

MarketIslamic Financial

InstitutionIslamic

Banking

Islamic Bonds

To Create New Waqf To Maintain Waqf Assets

Traditional Waqf Assets

BUILDINGS

Non-Profit Projects Comercial Projects

Free Education

Management Fees

Ready to Distribute the Funds To Poverty Alleviation Programs in Indonesia

LAND

Agricultural

Free Health Service

Waqf Buildings Rental

___ (eliminate)

THE PROFIT- LOSS SHARING from Cash Waqf Investment

Indonesia citizens Foreign Citizens

National Zakah Institution

MUZAKKI

Indonesia citizens

Foreign Citizens

AMIL

Global Fund Management

Mudharabah Deposit

Waqf Land Rental Real Estate

Figure 2.Figure 2.

Ready to Distribute the Funds To Poverty Alleviation Programs in Indonesia Microfinancing Portfolio

Poor Family Rehabilitation

Health & Sanitation

Establishing health care

programs for the poor

Supplying pure drinking water

Natural Disaster (Tsunami, Flood,Volcanics)

Social Fasilities & Services

Educational & Culture

Improving the condition of poor living below the poverty line

Public Utilities Services

To Alleviate the Poverty in Indonesia

Supporting local culture, art & heritages

Social Infrastructure

Religion Fasilities

To promote self-sufficient & dignity for the poor

Rehabilitating physically handicapped

Free Education (i.e. free tuitition fee, books free

of cost, scholarships etc)

Supporting any projects in the

area of education, research,

religious, etc)

Increasing The Standard of Life of Indonesian Citizens

10

6. General Description of System Conceptualization The system conceptualization involves establishing model boundary,

identifying causal relationships and policy framework3. In this research the model boundary includes all relevant factors that are considered important in the problem context. The model comprises seven interrelated components in the voluntary sector management as shown as Figure 3.

THE POORTHE RICH

CASH WAQFFUNDS

INVESTMENTPORTFOLIOS

+INVESTMENT

PROFITS

AVAILABLE FUNDSFOR THE POVERTY

PROGRAMS+

+

-+

+

(-) loop 1

(+) loop 2

+ (+) loop 3

-

ZAKAH FUNDS+

+

Figure 3. A Macro-view of Model

As depicted in the above causal loop, the model links among the rich, cash waqf fund, zakah fund investment portfolios, investment profits, available funds for the poverty programs and the poor.

A general system of cash waqf model, derived from a macro-view of model above, consists of six sectors i.e: 1). The cash waqf & zakah fund raising sectors (the rich links to the collected-cash waqf funds), 2) The Islamic financial portfolios sectors, 3) The global fund management sectors, 4) The direct investment in large and medium scale enterprises, 5) The microfinance sectors. (number 2,3,4,5 are investment portfolios which link to investment profits) 6) The distribution sectors of the profits of cash waqf investment. (Investment profits link to the poor through the poverty programs). The Interrelationship among variables can be seen in Figure 4. 3 Sushil (1993), System Dynamics “A Practical Approach for Managerial Problems”,Wiley Eastern Limited.

11

Figure 4. The Interrelationship among Variables in the General System

Islamic FinancialPortfolio

MicrofinancePortfolio

The Profits ofMicrofinance

The risk ofmicrofinance

Microfinance PolicyScheme

Bad debts ofmicrofinance

Unemploymentrate

Technical Assistancesfor the poor

+-

-

-

-

+

-

+-

-

IndonesianPopulation

birth rate+

the richthe poor

death ratecash waqf growth

cash inflow ofcash waqf

Collected Cash WaqfFunds

Average Period toCollect Funds

InvestmentFunds

-

++

+

+

+

DirectInvestmentPortfolios

+

+

The Profits of cashwaqf investment

Management Feesfor the Nazir

The funds for thepoverty alleviation

programs-+

+

++

+

-

+

Islamic CapitalMarket

Islamic Banking

Islamic MutualFunds

Dividens capital gains

MudharabahDeposits

NAV's MutualFunds

+

+

+

++

+

+

Islamic Bond+

rate of return

+

Profits of IslamicFinancial Investment

+ + ++

+

Risk of IslamicFinancial Investment

-

+++

+

Invest to company To maintain theexisting waqf assets

To make a newwaqf assets

+ +

+

Dividen or CapitalGains

+Waqf landproductivity

To maintain newassets

Agriculture

Real Estate

+

+

++

Business Risk

SocialProjects

CommercialProjects

Free Education

Free-charge HealthServices

Waqf LandRental

+

++

+

+

The Profits of DirectInvestment

+

++

+

+++ +

+-

+

+

The povertyallevationprograms

-

+

+Global Fund

Mgt+

ForeignWaqif

+

+

+

+

Multiplier Effects ofMicrofinance towards

Family's Welfare

-

+

+

+

Zakah Funds+

12

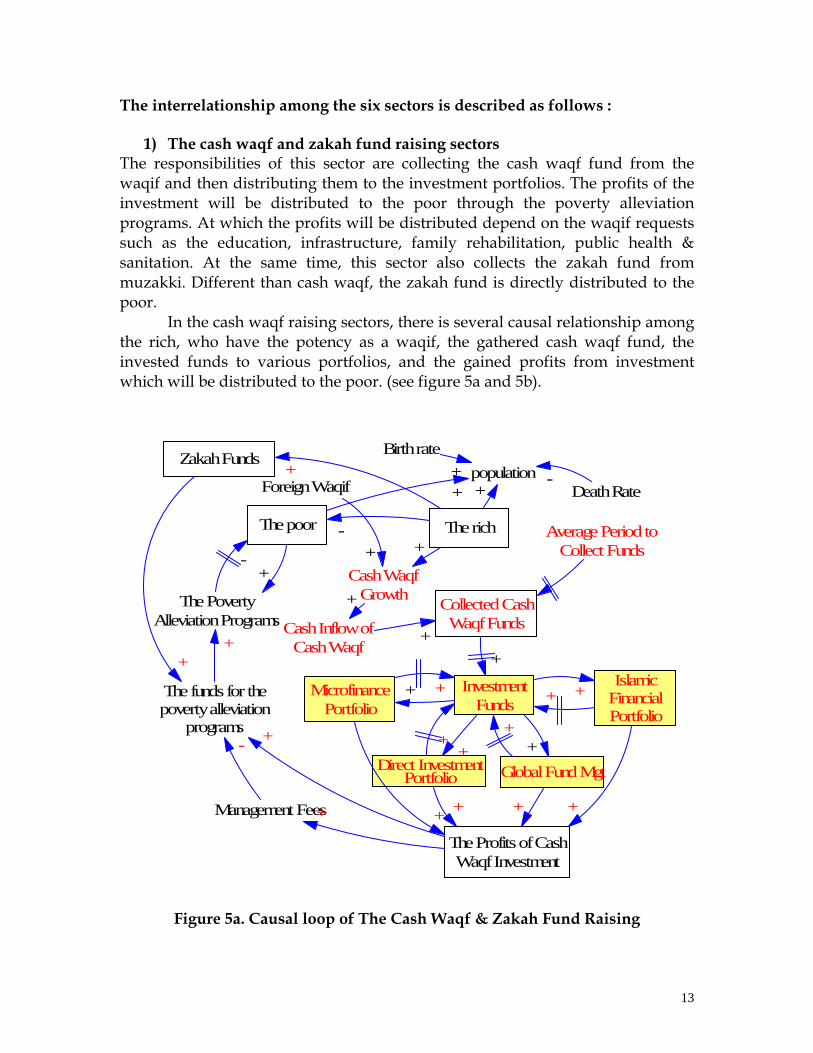

The interrelationship among the six sectors is described as follows :

1) The cash waqf and zakah fund raising sectors The responsibilities of this sector are collecting the cash waqf fund from the waqif and then distributing them to the investment portfolios. The profits of the investment will be distributed to the poor through the poverty alleviation programs. At which the profits will be distributed depend on the waqif requests such as the education, infrastructure, family rehabilitation, public health & sanitation. At the same time, this sector also collects the zakah fund from muzakki. Different than cash waqf, the zakah fund is directly distributed to the poor. In the cash waqf raising sectors, there is several causal relationship among the rich, who have the potency as a waqif, the gathered cash waqf fund, the invested funds to various portfolios, and the gained profits from investment which will be distributed to the poor. (see figure 5a and 5b).

populationBirth rate

Cash WaqfGrowth

MicrofinancePortfolio

+

The richThe poor

Death Rate

Cash Inflow ofCash Waqf

Collected CashWaqf Funds

Average Period toCollect Funds

InvestmentFunds

-

+

++

+

+

+ +

-

The PovertyAlleviation Programs

-+

Global Fund Mgt+

Foreign Waqif

Zakah Funds

+

IslamicFinancialPortfolio

Direct InvestmentPortfolio

+

+

The Profits of CashWaqf Investment

+ + + +esManagement Fe+

+

+

++

+The funds for thepoverty alleviation

programs-

+

+

+

Figure 5a. Causal loop of The Cash Waqf & Zakah Fund Raising

13

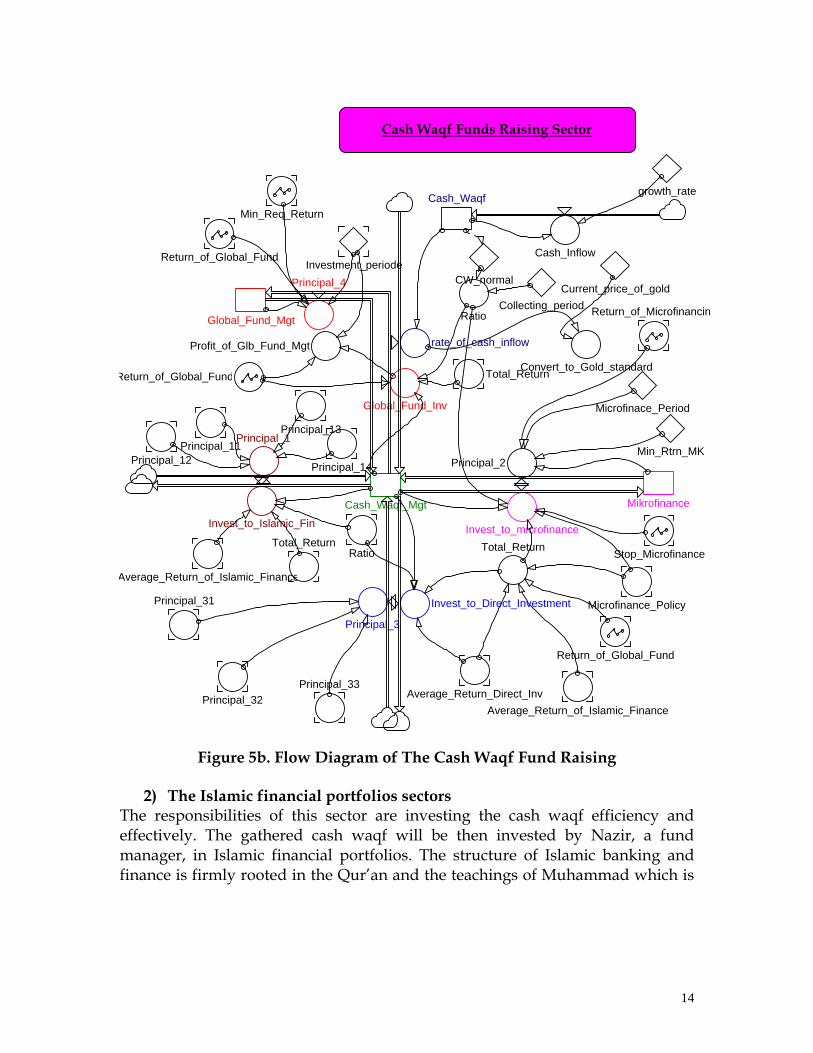

Cash Waqf Funds Raising Sector

Principal_32

Total_Return

growth_rateCash_WaqfMin_Req_Return

Cash_InflowReturn_of_Global_FundInvestment_periode

CW_normalPrincipal_4 Current_price_of_goldCollecting_period

Principal_3

Principal_1Principal_11

Principal_12 Principal_14

Principal_13

Principal_33

Principal_31

Ratio

Global_Fund_Inv

Invest_to_Islamic_Fin

Convert_to_Gold_standard

Cash_Waqf_Mgt Mikrofinance

Global_Fund_Mgt

Return_of_Global_Fund

Total_Return

Invest_to_Direct_Investment

Invest_to_microfinance

Ratio Return_of_Microfinancin

rate_of_cash_inflowProfit_of_Glb_Fund_Mgt

Return_of_Global_Fund

Microfinace_Period

Min_Rtrn_MKPrincipal_2

Total_ReturnStop_Microfinance

Average_Return_of_Islamic_Finance

Microfinance_Policy

Average_Return_Direct_InvAverage_Return_of_Islamic_Finance

Figure 5b. Flow Diagram of The Cash Waqf Fund Raising

2) The Islamic financial portfolios sectors

The responsibilities of this sector are investing the cash waqf efficiency and effectively. The gathered cash waqf will be then invested by Nazir, a fund manager, in Islamic financial portfolios. The structure of Islamic banking and finance is firmly rooted in the Qur’an and the teachings of Muhammad which is

14

called a Islamic Law4. Islamic Law has derived from revealed text a web of interrelated norms prohibiting interest-taking and undue speculative practices.

Generally, these portfolios are divided into four kinds i.e a). Islamic mutual funds, b). Islamic Capital Market, c). Islamic Banking Products (Mudharaba Deposits), d) Islamic Bonds (sukuk). All of them are issued by Indonesian financial institutions.

The gained profits will be distributed to meet the poor’s basic needs and increase the quality of the poor’s life. Meanwhile, the principal keep being invested in potential investment opportunities. (see Figure 6a and 6b).

The richThe poor

Cash Waqf growthCash Waqf

InflowsCollected Cash

Waqf Fund

average period tocollect the funds

Investment funds

Islamic FinancialPortfolio

+ +

++

+

The profits of cashwaqf investments

Management Fees

The funds for thepoverty alleviation

programs-

+

+

+

-

Islamic CapitalMarket

Islamic Banking Islamic MutualFunds

Dividen Capital gain

MudharabahDeposits

NAV of MutualFunds

++ +

++

+ +IslamicBonds

+

rate of return+

The Profits of IslamicFinancial Investments

++ + +

+

Risk of IslamicFinance Investment

-

+

+

+

+

The povertyalleviation programs

-

+

+ -

Figure 6a. Causal loop of The Islamic Financial Portfolios

4 Frank E.Vogel and Samuel L.Hayes III (1998), Islamic Law and Finance “religion, risk and return.” Published by Kluwer Law International.

15

Islamic Financial Portfolio Sector

Investment_periode

Return_Islamic_Finance

Invest_to_Islamic_Fin

Principal_14

Invest_to_Islamic_Fin

Principal_12

Islamic_Mutual_Funds

Invest_to_Mutual_Funds

Min_Req_ReturnReturn_Islamic_Mutual_Fund

Profit_of_Islamic_Bonds

Return_of_Islamic_Bonds

Invest_to_Islamic_Bond

Islamic_Bonds

Principal_13

rn_Islamic_Finance Min_Req_Return

Invest_to_JII

Islamic_Capital_Market

Profit_of_Islamic_Cap_Mrkt

Invest_to_Mudharabah_Deposits

Principal_11Return_Islamic_Finance

Profit_of_Islamic_Mutual_Funds

Investment_periodeInvest_to_Islamic_Fin

Return_of_Deposit

Profit_of_Islamic_Deposits

Profit_of_Islamic_Bonds

Mudarabah_Deposits

Profit_of_Islamic_Finance

Investment_periode

Average_Return_of_Islamic_Finance

Profit_of_Islamic_Deposits

Return_of_Islamic_Stocks

Return_Islamic_Finance

Return_of_Islamic_Bonds Profit_of_Islamic_Mutual_FundsReturn_of_Islamic_Bonds

Return_Islamic_Mutual_Fund

Return_of_Deposit

Return_of_Islamic_Stocks

Min_Req_Return

Figure 6b. Flow Diagram of of The Islamic Financial Portfolios

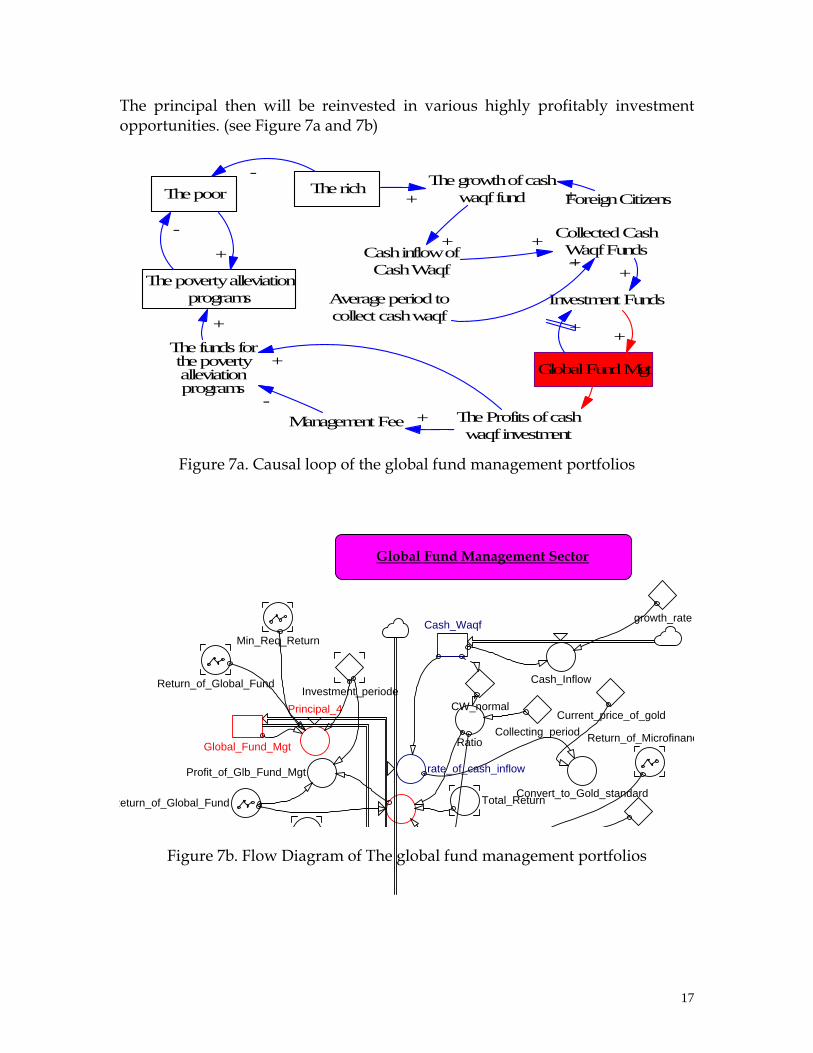

3) The global fund management sectors The responsibilities of this sector are to invest the cash waqf fund in the global financial portfolios as known a global funds management such as Amanah Fund, Lariba Fund, Islamic Indices, etc. A fund manager should choose the portfolios not only high return but also safety. The better Nazir choose the investment portfolios, the higher profits will be gained and the more funds will be acquaired by the poor.

16

The principal then will be reinvested in various highly profitably investment opportunities. (see Figure 7a and 7b)

The richThe poorThe growth of cash

waqf fund

Cash inflow ofCash Waqf

Collected CashWaqf Funds

Average period tocollect cash waqf

Investment Funds

+ ++

+

The Profits of cashwaqf investment

Management Fee

The funds forthe povertyalleviationprograms

-

+

+

+

-

The poverty alleviationprograms

-

+

+

Global Fund Mgt

+

Foreign Citizens+

+

Figure 7a. Causal loop of the global fund management portfolios

Global Fund Management Sector

Total_Return

Principal_4Investment_periode

CW_normal

Convert_to_Gold_standard

growth_rateCash_WaqfMin_Req_Return

Cash_InflowReturn_of_Global_Fund

Current_price_of_goldCollecting_period

Global_Fund_Mgt Ratio

rate_of_cash_inflowProfit_of_Glb_Fund_Mgt

Return_of_Global_Fund

Return_of_Microfinanc

Figure 7b. Flow Diagram of The global fund management portfolios

17

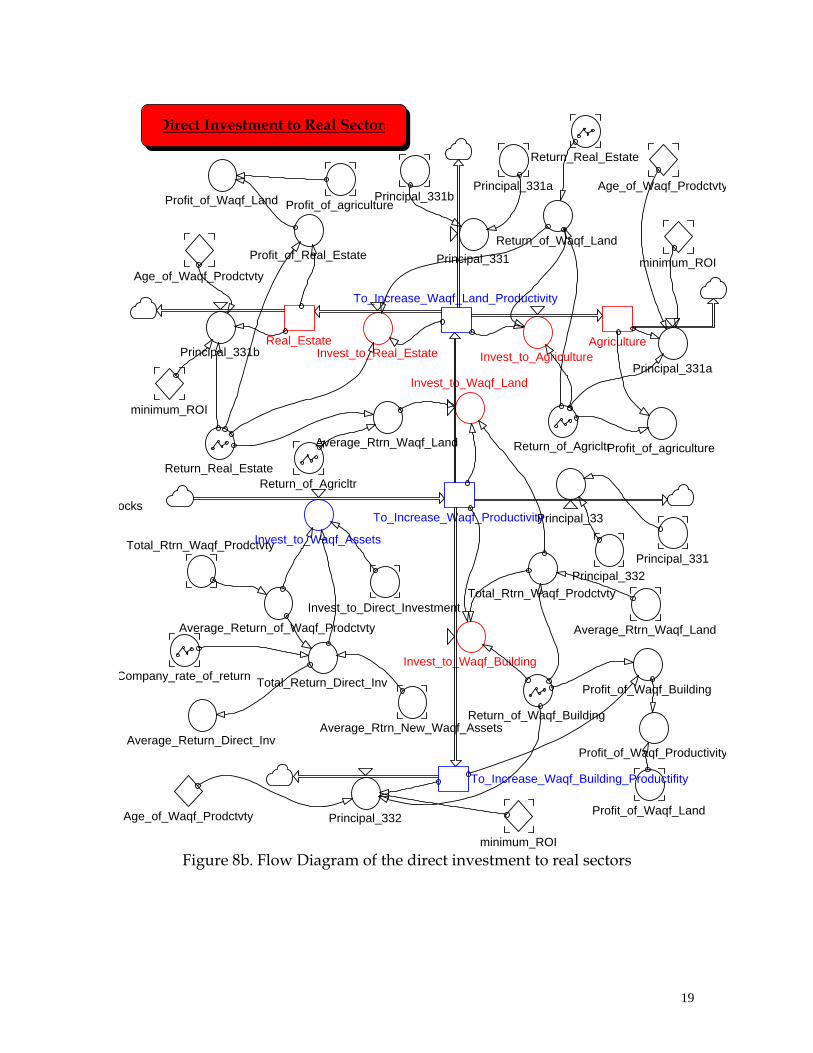

4) The direct investment in large and medium scale enterprises A cash waqf fund manager, Nazir, allocates the gathered funds to the big companies in the forms of stocks which the gained profits are dividends or capital gains. The nature of this sector is the long term. The other forms of direct investment are building the new waqf buildings and maintaining the existings waqf assets either for social projects or the commercial projects. (See Figure 8a and 8b.)

The richThe poor

Cash Waqf growth

Cash Waqf InflowCollected Cash

Waqf Fund

Average Period toCollect Funds Investment Funds

+ +

+ +

Direct InvestmentPortfolio

The Profits of CashWaqf Investment

Management fees

The funds for povertyalleviation programs

-+

+

+

-

Invest tocompany To maintain the

existings waqf assetsTo make the new

waqf assets

+ ++

dividen or capitalgains

+Waqf LandProductifity

To maintain waqfbuldings

Agriculture

Real Estate

++

++

Business Risks

SocialProjectsCommercial

Projects

Free EducationFree-Charge

Healthy Services

Waqf Landrental

+

++

++

The Profits of DirectInvestment

+

++

++ + + +

+-

+

+

The poverty alleviationprograms

-

+

+

Foreign Waqif+

+

Figure 8a. Causal loop of the direct investment to real sectors

18

Direct Investment to Real Sectors

Figure 8b. Flow Diagram of the direct investment to real sectors

Invest_to_Agriculture

Invest_to_Waqf_Assets

Principal_33

Principal_331b

Principal_331

Invest_to_Real_Estate

ocksTo_Increase_Waqf_Productivity

Average_Rtrn_Waqf_Land

Return_Real_Estate

Return_of_AgricltrProfit_of_agriculture

Invest_to_Waqf_Land

AgricultureReal_Estate

minimum_ROI

Age_of_Waqf_Prodctvty

Profit_of_Waqf_Land

Profit_of_Real_Estate

Profit_of_agriculturePrincipal_331b

Return_of_Waqf_Land

Principal_331a

Return_Real_Estate

Principal_331a Age_of_Waqf_Prodctvty

minimum_ROI

To_Increase_Waqf_Land_Productivity

Return_of_Agricltr

Invest_to_Direct_Investment

Total_Rtrn_Waqf_ProdctvtyPrincipal_331

Principal_332Total_Rtrn_Waqf_Prodctvty

Average_Return_of_Waqf_Prodctvty Average_Rtrn_Waqf_Land

Invest_to_Waqf_Building

Principal_332

To_Increase_Waqf_Building_Productifity

Age_of_Waqf_Prodctvty

minimum_ROI

Return_of_Waqf_BuildingAverage_Rtrn_New_Waqf_Assets

Total_Return_Direct_InvCompany_rate_of_returnProfit_of_Waqf_Building

Average_Return_Direct_InvProfit_of_Waqf_Productivity

Profit_of_Waqf_Land

19

Figure 8b. (continue…) Flow Diagram of the direct investment to real sectors

Principal_322

Invest_to_Company

Build_New_Waqf_Assets

Invest_to_new_waqf

Invest_to_build_Comrcl_Projects

Principal_32

Total_Return_Direct_Inv

Total_Rtrn_New_Waqf_Assets

Company

Total_Return_Direct_Inv

Waqf_Land_Growth Decrease_of_Waqf_Land

Age_of_Waqf_Prodctvty

Average_Rtrn_New_Waqf_Assets

Invest_to_Direct_Investment

Commercial_Projects

Commercial_Projects_investment_Perio

erage_Rtrn_New_Waqf_AssetsPrincipal_321

Total_Rtrn_New_Waqf_Assets

Principal_322

Invest_to_Social_Projects

Profit_of_Commercial_ProjectsRtrn_Commercial_Projects

minimum_ROI

Rtrn_Commercial_ProjectsCommercial_Projects_investment_

Principal_321

Company_rate_of_return

minimum_ROI

Company_Profits_

Company_rate_of_return

Time_to_Direct_inv

Invest_to_Direct_InvestmentPrincipal_31

Waqf_Land_Devaluation

he_number_of_Waqif

Fraction_of_year

Profit_of_Waqf_Land_Rental

Rental_Price

Profit_of_Direct_InvestmentProfit_of_Waqf_Land_Rental

Profit_of_Commercial_ProjectsCompany_Profits_

Profit_of_Waqf_Productivity

Time_to_invest_in_Direct_Investment

Waqf_Land_Availability

Social_Projects

n_Commercial_Projects

Adjust_to_Social_Projects

Social_Projects_PolicyReturn_Social_Projects

20

5) The Microfinance Sectors

The microfinancing programs, which used the loss-profit sharing, are one of the most important sectors for poverty alleviation. Most of funds collected through cash waqf certificate issues will be allocated as loan for microenterprises. This microcredit program should particularly be aimed at helping poor people initiate their business and enhance their quality of life, accordingly. Nevertheless, merely supplying them with capital is not sufficient, since most of them do not have adequate knowledge and skill to choose and to run a business that is suitable to their condition. Consequently, relevant business technical assistance and spiritual treatment is needed to help them survive5.

Family’s business activities have significantly influenced economy of a community, particularly in developing countries. Big manufacturing companies indeed dominate mass production processes, both for goods and services, but most of enterprises are initiated by family. In addition, family’s consumption behaviour also affects production and marketing activities, as well as other business activities. Government’s programs for family business empowerment has to do with informal sector development efforts, as most of family businesses are operated in non formal format and business system. Family businesses, which absorb the largest number of employee, are also found mostly in small and medium scale. In most developing economies, these small and medium enterprises (SMEs) have limited access to formal financing practices, as well as to adequate government’s technical assistance. (see figure 9a and 9b)

5 Muljawan, Dadang and Masyita, Dian et al. (2006), “The Pilot Project of Linkage Program for Sharia Financial Institution in Indonesia”. Bank of Indonesia report.

21

MicrofinancingPortfolio

The profit ofmicrofinance

Risk ofMicrofinance

Microfinance PolicyScheme

Bad debt ofmicrofinance

UnemploymentrateTechnical

Assistances

+-

+

-

-

+

-+ -

-

Investment funds

+

The profits of cashwaqf investment

Management Fees

The funds for povertyalleviation programs

-+

+

+

Multiplier Effects ofMicrofinance towards

family's welfare

The povertyalleviation programs

+

The poor

-+

+

-

The rich+ Collected

Cash WaqfFund

+

-

+

+

Figure 9a. Causal loop of The Microfinancing Sectors

Microfinance Portofolio Sectors

Mikrofinance microcreditProfit_of_Microfinance

Indonesian_population Stop_Microfinance

Microfinace_PeriodReturn_of_Microfinancing

Pra_welfare_people

Microfinance_Policy

Policy_ratios

Figure 9b. Flow Diagram of The Microfinancing Sectors

6) The profits of cash waqf investment & zakaf fund distribution sectors The gained profits from the various portfolios will be distributed to the poor through the poverty alleviation programs such as basic needs, health services, sanitations, education, natural disasters victims, etc. The principal of cash waqf will be reinvented to various portfolio opportunities. On the other hand, the zakah fund collected by Amil is directly distributed to the poor through the poverty alleviation programs such as basic needs and natural disasters vistims. (see figure 10a and 10b).

22

The richThe poorCash Waqf

Growth

Cash Waqf Inflow

Collected CashWaqf Funds

Average period tocollect the cash waqf

Investment funds

+

++

+

The Profit of cashwaqf investment

Management fee

The funds for thepoverty alleviation

programs

-+

+

+

-

The PovertyAlleviation Programs

-

+

+Foreign Waqif

+

+

To meet the poorneeds

+

Living CostHealthy Cost

Education cost

The familyrehabilitation cost

Natural DisasterVictims Cost Infrastucture

Recovery cost

Quality of Life++

++++

-

+

Zakah Funds

+

Figure 10a. Causal Loop of the cash waqf profits & zakah fund distribution sectors

23

Zakah Funds & Profits of Cash Waqf Distribution

Cost_4 needs_rate_4

needs_rate_6

Cost_2

Cost_3

Cost_5

Cost_6

Healthy_needs

Rehabilitation_needs

Profit_of_Glb_Fund_Mgt

Profit_of_Microfinance Living_cost Healthy_costNatural_Disaster_CostProfit_of_Direct_Investment

Infstructure_CostProfit_of_Islamic_Finance

Daily_needsFamily_Rehbiittion_Cost

Education_cost

Total_available_fund_for_poor

Cost_1 Needs__ratio_2

Needs_ratio_3

Needs_ratio_4

Needs__ratio_5

allocation_ratio_3

allocation_ratio_4

allocation_ratio_5

Enter_to_pra_welfare

CProfit_of_Cash_Waqf_Investment

oPotency_of_ZakahPra_welfare_people

the_poor

Waqf_Zakah Std

Enter_to_pra_welfareNeeds_ratio_1

allocation_ratio_1Inflation

available_fund_for_healthy

available_fund_for_education

available_fund_for_rehbltation

available_fund_for_infrastrctr

allocation_ratio_2

needs_rate_2

needs_rate_1

needs_rate_3

Education_needs

Disaster_needs

Infrastructure_needs

allocation_rate_6

Needs_ratio_6

Living_needsavailable_fund_for_living

Living_cost available_rate_1

Healthy_cost available_rate_2

Education_cost available_rate_3

Family_Rehbiittion_Costavailable_rate_4

needs_rate_5

available_fund_for_disasteravailable_rate_5Natural_Disaster_Cost

Infstructure_Cost available_rate_6

Waqf_ZakahEnter_to_pra_welfareInflation

Figure 10b. Flow Diagram of the cash waqf profits & zakah fund distribution sectors

24

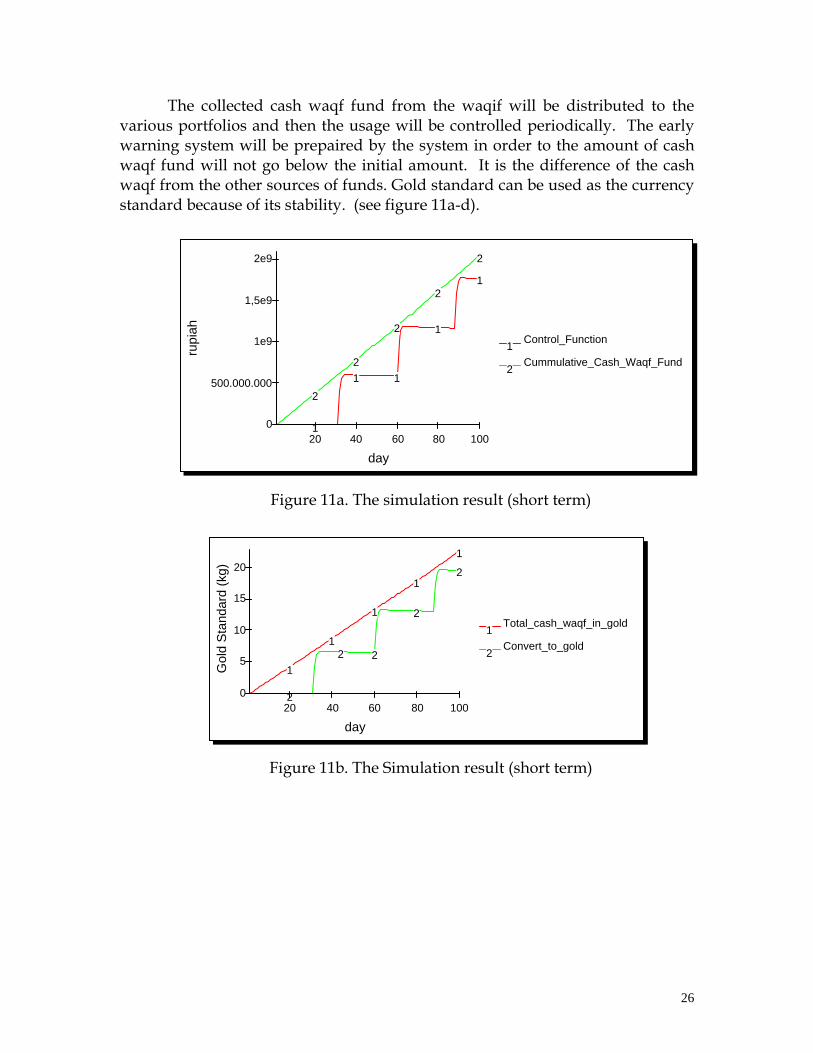

7. The Cash Waqf Management Control

Since the zakat is considered as the buffer against the poverty, all of the

zakat fund will be directly distributed to the poor. Therefore, Amil (a person or body or organization that are specialized in managing zakah, infaq, and shadaqah) is allowed to spend all of the zakah funds to the mustahiq. Contrary to zakah, the cash waqf fund must be maintained in such a way that it does not go below the initial amount.

The survey concluded that most people did not trust any existing government institutions to manage cash waqf fund and control cash waqf investment activities, especially because cash waqf management will involve large amount of endowment funds6. Most of them also recommend that if a special purpose institution is established to manage cash waqf fund, it has to be highly capable of detecting any potential dishonesty and assessing performance of cash waqf fund manager, i.e. nadzir. Therefore, it’s necessary to design an instrument which is able to control the cash waqf management. This model tries to design a control tools which is able to detect the human error in decision making either mismanagement or dishonesty quickly. (see figure 11.)

The Control Function for Fund Management

rate_of_cash_inflow

Profits_Mobilization

Current_price_of_goldConvert_to_gold

Control_Function

Global_Fund_Mgt

Commercial_Projects

Mudarabah_Deposits

Company

Mikrofinance

Real_Estate

To_Increase_Waqf_Building_Productifity

Social_Projects

Islamic_Capital_Market

Agriculture

Islamic_Mutual_Funds

Islamic_Bonds

Cummulative_Cash_Waqf_Fun

available_fund_for_living

available_fund_for_healthy

available_fund_for_education

available_fund_for_disaster

available_fund_for_rehbltation

Total_cash_waqf_in_gold

available_fund_for_infrastrctr

Figure. 11 Flow Diagram of The Control Function for Fund Management

6 Masyita, Dian (2001), Preliminary Implementation Model Design of Cash Waqf Certificate as Alternative Instrument for Poverty Alleviation in Indonesia using System Dynamics Methodologi, Thesis, ITB

25

The collected cash waqf fund from the waqif will be distributed to the various portfolios and then the usage will be controlled periodically. The early warning system will be prepaired by the system in order to the amount of cash waqf fund will not go below the initial amount. It is the difference of the cash waqf from the other sources of funds. Gold standard can be used as the currency standard because of its stability. (see figure 11a-d).

day

rupi

ah

Control_Function1Cummulative_Cash_Waqf_Fund2

20 40 60 80 1000

500.000.000

1e9

1,5e9

2e9

1

212

1

2 1

21

2

Figure 11a. The simulation result (short term)

day

Gol

d St

anda

rd (k

g)

Total_cash_waqf_in_gold1Convert_to_gold2

20 40 60 80 1000

5

10

15

20

1

2

12

1

2

1

2

1

2

Figure 11b. The Simulation result (short term)

26

day

rupi

ah

Cummulative_Cash_Waqf_Fund1Control_Function2

5.000 10.000 15.0000

5e14

1e15

1 2 1 2

Figure 11c The Simulation Result (long term)

day

gold

sta

ndar

d (k

g)

Convert_to_gold1Total_cash_waqf_in_gold2

5.000 15.0000

5.000.000

10.000.000

1 2 1 2

Figure 11d The Simulation Result (long term)

The waqif and public can control or monitor the cash flow of cash waqf

investment. If mismanagement and dishonesty occurred, the simulation result could demonstrate the deviation. (see figure 11e-f)

day

rupi

ah

Control_Function1Cummulative_Cash_Waqf_Fund2

20 40 60 80 1000

1e9

2e9

3e9

4e9

5e9

1

21

2

1

2

1

2

1

2

day

gold

sta

ndar

d (k

g)

Total_cash_waqf_in_gold1

Convert_to_gold2

20 40 60 80 1000

10

20

30

40

50

1

2

1

2

1

2

1

2

1

2

Figure 11e. The Simulation Result (short term)

27

day

rupi

ah Control_Function1Cummulative_Cash_Waqf_Fund2

2.000 6.000 10.0000

2e13

4e13

6e13

1 2 1 2 12 1

2

day

gold

sta

ndar

d (k

g)Total_cash_waqf_in_gold1Convert_to_gold2

2.000 10.0000

300.000

600.000

1 2 1 21 2

1

2

Figure 11f. The Simulation Result (long term)

8. The Potency of Cash Waqf & Zakah Fund for the Poverty Alleviation Programs It can be concluded from the system that the larger the amount of cash

waqf collected, the larger the amount of fund can be invested in highly cost-effective profit sharing-based portfolios, and the larger the amount of return can be distributed to poor people. The more fund allocated to finance microbusiness, the sooner poverty in Indonesia can be alleviated. (see Figure 12).

According to the result of some researches, the potency of zakah fund in Indonesia is approximately Rp 19,3 trillion/year7. In this model the potency of zakah fund, combined with the profit of cash waqf investment, will become the sources of fund for the poverty alleviation programs in Indonesia.

7 CSCR Research (2006), “Islamic Philanthropy and Social Development in Contemporary Indonesia” , University Islam Negeri (UIN) Syarif Hidayatullah, Jakarta

28

Indonesian_population

The Potency of Cash Waqf &Zakah for The Poverty

death_rate

Birth_rate3

death_rate2

birth_rate

death_rate3

birth_rate2

Multiplier_EffectsDaily_needsthe_poor

Waqf_Zakah

alleviation_1

alleviation The_poor_decreasePra_welfare_people

Average_of_Microfinacing

the_welfare_increase

lifetime_expectancyPopulation_growth

Microcredit_for_a_powelfare

Multiplier_effect

oIndonesian_population

the_rich

Average_period_to_become_welfare

Figure 12. Flow Diagram of The Potency of Cash Waqf & Zakah Fund for The Poverty Alleviation

9. The Simulation Result

In a system dynamics modeling process, the initial value and unit variables/parameter are the most important components to build the mathematical equations for the level, rate and auxiliary equation. In this research, the initial value and unit variables/parameter for the flow diagram shown in table 1 are as follows:

Tabel 1 Initial Value and Main Variable Parameter

Variables Initial Value and Parameter Measurement Estimation Methods8

Growth_rate of cash waqf 0.0007 /day Q Cash_Waqf 50.000.000 Rupiah/ray Q Cash_Waqf_Mgt 0 Rupiah Q Collecting_period (cash waqf) 30 Days Q Potency of Zakah Fund 40 billion – 50 billion rupiah/day Current_price_of_gold 90.000.000 rupiah/kg S Population_growth 0.0000419444444 /day S the_rich 49.405.842 Person S

8 note : P = derived from primary data S = derived from secondary data Q = derived from qualitatif information C = predicted by researcher based on another parameter

29

the_poor 37.027.472 Person S Pra_welfare_people 128.842.686 Person S Average_period_to_become_welfare 1800 Day Q lifetime_expectancy 23881.95 Day S Inflation 7.32%-12%/year (graph) /day S Adjust_to_Social_Projects 10%-40%/year (graph) /day Q Company_rate_of_return 15%-18% year (graph) /day S Min_Req_Return 5%-8%/ year (graph) /day Q Rental_Price (waqf land) 200.000 – 1.000.000 Rp/hectare/day Q Return_Islamic_Mutual_Fund -8% - 30%/year (graph) /day S Return_of_Agricltr 25%- 32%/year (graph) /day Q Return_of_Deposito 4%-18% /year (graph) /day S Return_of_Global_Fund 7%-33% /year (graph) /day S Return_of_Islamic_Bonds 12%-17% /year (graph) /day S Return_of_Islamic_Stocks -8% - 45%/year (graph) /day S Return_of_Microfinancing 0%- 15% /year (graph) /day S Return_of_Waqf_Building 10%-30% /year (graph) /day Q Return_Real_Estate 25%-31%/year (graph) /day Q Rtrn_Commercial_Prjcts 36% / year /day Q minimum_ROI 25%/year /day Q Age_of_Waqf_Prodctvty 7200 /day Q Investment_periode (Islamic Finance) 360 /day Q Time_to_Direct_inv (company) 1080 /day Q Microcredit_for_a_poor 5.000.000 rupiah/person Q Microfinace_Period 360 Day Q Multiplier_effect (pra welfare) 4.5 person/family S Multiplier_Effects (the poor) 5.8 person/family S Min_Rtrn_MK 3% / year /day S Comcl_Projets_inv_Periode 10800 Day S Waqf_Land_Availability 500000 Hectare Q Education_cost 2000 Rp/person/day S Family_Rehbilitation_Cost 2000 Rp/person/day S Healthy_cost 1000 Rp/person/day S Infstructure_Cost 1000 Rp/person/day S Living_cost 7496.733333 Rp/person/day S Natural_Disaster_Cost 1000 Rp/person/day Q Build_New_Waqf_Assets 0 Rupiah Q Needs_ratio_1 (living cost) 0.513 - Q Needs__ratio_2 ( healthy) 0.4143 - Q Needs_ratio_3 (education) 0.513 - Q Needs_ratio_4 (rehabilitation) 0.33 - Q Needs__ratio_5 (disasters) 0.10 - Q Needs_ratio_6 (infrastructure) 1 - Q allocation_ratio_1 (living cost) 0.15 - Q allocation_ratio_2 (healthy) 0.2 - Q allocation_ratio_3 (education) 0.3 - Q allocation_ratio_4 (rehabilitasi) 0.2 - Q allocation_ratio_5 (disaster) 0.1 - Q allocation_ratio_6 (infrastruktur) 0.05 - Q

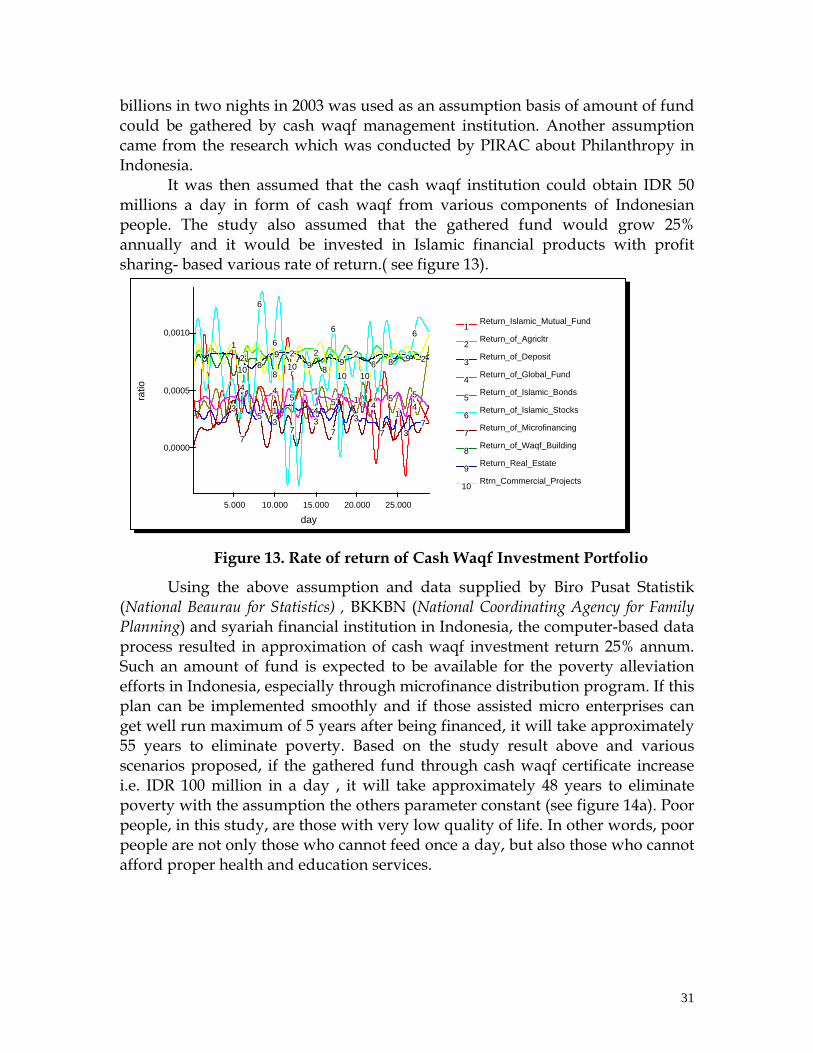

Since there has been no similar study preceding the research, some assumption were applied. The ability of five national TV corporations (RCTI, SCTV, Indosiar, MetroTV and Lativi) to collect donation amounting IDR 3

30

billions in two nights in 2003 was used as an assumption basis of amount of fund could be gathered by cash waqf management institution. Another assumption came from the research which was conducted by PIRAC about Philanthropy in Indonesia.

It was then assumed that the cash waqf institution could obtain IDR 50 millions a day in form of cash waqf from various components of Indonesian people. The study also assumed that the gathered fund would grow 25% annually and it would be invested in Islamic financial products with profit sharing- based various rate of return.( see figure 13).

day

ratio

Return_Islamic_Mutual_Fund1Return_of_Agricltr2Return_of_Deposit3Return_of_Global_Fund4Return_of_Islamic_Bonds5Return_of_Islamic_Stocks6Return_of_Microfinancing7Return_of_Waqf_Building8Return_Real_Estate9Rtrn_Commercial_Projects10

5.000 10.000 15.000 20.000 25.000

0,0000

0,0005

0,00101

2

3

4

5

6

7

89

10

1

2

3

45

6

7

8910

1

2

34

5

6

7

8910

1

2

34

5

6

7

8 9

10

1

2

3

45

6

7

Figure 13. Rate of return of Cash Waqf Investment Portfolio

Using the above assumption and data supplied by Biro Pusat Statistik (National Beaurau for Statistics) , BKKBN (National Coordinating Agency for Family Planning) and syariah financial institution in Indonesia, the computer-based data process resulted in approximation of cash waqf investment return 25% annum. Such an amount of fund is expected to be available for the poverty alleviation efforts in Indonesia, especially through microfinance distribution program. If this plan can be implemented smoothly and if those assisted micro enterprises can get well run maximum of 5 years after being financed, it will take approximately 55 years to eliminate poverty. Based on the study result above and various scenarios proposed, if the gathered fund through cash waqf certificate increase i.e. IDR 100 million in a day , it will take approximately 48 years to eliminate poverty with the assumption the others parameter constant (see figure 14a). Poor people, in this study, are those with very low quality of life. In other words, poor people are not only those who cannot feed once a day, but also those who cannot afford proper health and education services.

31

days

the_poor1the_poor2the_rich3the_rich4Pra_welfare_people5Pra_welfare_people6

0 5,000 10,000 15,000 20,000 25,0000

50,000,000

100,000,000

150,000,000

200,000,000

1 23 4

5 6

1 23 4

5 6

1 23 4

5 6

1 23 4

5 6

12

34

5

6

1

3

Figure 14a. The Simulation Result (based on IDR 50 million a day for line 1-3-5

and IDR 100 million a day for line 2-4-6) Based on various scenarios, if the cash waqf fund combined zakat fund

simultantly are used for poverty alleviation program, it will able to make the great siginificant impact to the poor. It will consume less time to alleviate poverty. (see figure 14b)

days

peo

ple

Pra_welfare_people1Pra_welfare_people2Pra_welfare_people3Pra_welfare_people4the_rich5the_rich6the_rich7the_rich8the_poor9the_poor10the_poor11the_poor12

0 5,000 10,000 15,000 20,000 25,000 30,0000

50,000,000

100,000,000

150,000,000

200,000,000

12

3

4

5 6 7 8

910

11

12

12

3

4

5 6 7 8

910

11

12

12

3

4

5 6 7 8

910

11

12

12

3

4

5 6 7 8

910

11

12

1

2

3

4

5

6

7

8

9 10 1112

5 6 7 8

9 10 11 12

5

9

Figure 14b.The Simulation Result (based on the combination of cash waqf and zakah fund

simultantly)

32

10. Closing Based on the above study result and various scenarios proposed, zakaf fund

as a buffer against poverty and cash waqf fund as a motor of economy must jointly implemented for poverty alleviation program in Indonesia. Some microfinance management strategies were then carefully formulated to ensure the achievement of poverty alleviation goals on the other side.

Most of funds collected through cash waqf certificate issues will be allocated as loan for microenterprises. This microfinance program should particularly be aimed at helping poor people initiate their business and enhance their quality of life, accordingly. At the same time zakaf fund will protect them from the poverty trap. Nevertheless, merely supplying them with capital is not sufficient, since most of them do not have adequate knowledge and skill to choose and to run a business that is suitable to their condition. Consequently, relevant business technical assistance and spiritual treatment are needed to help them survive. Hence, the integration and strong commitment among Board of Indonesian Waqf (BWI), BAZNAS, Microfinance Institutions, Business Technical Assistance Provider, government and citizens for the poverty alleviation program are the most important agenda.

List of References 1. Forrester, Jay.W, “Principle of System.” Wright-Allen Press,Inc, 1968 2. Frank E.Vogel and Samuel L.Hayes III, Islamic Law and Finance “religion,

risk and return.” Published by Kluwer Law International, 1998 3. Mannan, M.A.Abdul, Cash Waqf Certificate- an Innovation in Islamic Financial

Instrument: Global Opportunities for Developing Social Capital Market in the 21stCentury Voluntary Sector Banking”, Presentation at the Third Harvard University Forum on Islamic Finance, October 1, 1999

4. Mannan, M.A.Abdul, Global Mobilization and Creation of Cash Waqf Fund for Human and Social Capital Infrastrukture for the Islamic Ummah, Social Investment Bank Publication Series no. 5, 1999.

5. Mannan, M.A.Abdul, Lesson of Experience of Social Investment Bank in Family Empowerment Micro-credit for Poverty Allevation: A Paradigm shift in Micro-financ”, Social Investment Bank Publication Series no. 10, 1999.

6. Masyita, Dian, Preliminary Implementation Model Design of Cash Waqf Certificate as Alternative Instrument for Poverty Alleviation in Indonesia using System Dynamics Methodologi, Thesis, ITB, 2001

7. Mulyawan, Dadang and Masyita, Dian et al. “The Pilot Project of Linkage Program for Sharia Financial Institution in Indonesia”. Bank of Indonesia report, 2006.

8. Sushil, System Dynamics- A Practical Approach for Managerial Problems, Wiley Eastern Limited, India, 1993

33

34