developments in mortality and longevity risk modeling michael sherris university of new south wales...

TRANSCRIPT

Developments in Mortality and Longevity Risk Modeling

Michael SherrisUniversity of New South Wales

2013 China International Conference on Insurance And Risk Management (CICIRM 2013)

July 17th-20th, 2013Expo Garden Hotel, Kunming, Yunnan ,China

CICIRM 2013

Longevity/Mortality Models

Longevity/Mortality Models Data

Longevity/Mortality Model Risk

Agenda – Model Risks

- Cohort and forward survival curves (financial risk) versus age-period models (demographic/actuarial/survival curve adapted for cohort effects)

- Consistent versus inconsistent mortality curves (dynamics and future survival curves) and parameter stability

- Risk factors and price of risk (explicit versus ad-hoc risk adjustment)

- Heterogeneity – multiple state models with systematic risk versus heterogeneity only (frailty, Markov ageing models)

- Drawing on longevity research at CEPAR, UNSW

Model A Model B

Some of the issues – which would you prefer?

Source: Shao, W., Sherris, M., and Hanewald, K., (2103), Reverse Mortgage Pricing and Capital Requirements Allowing for Idiosyncratic House Price Risk and Longevity Risk.

Males

Model A Model B

Some of the issues – which would you prefer?

Source: Shao, W., Sherris, M., and Hanewald, K., (2103), Reverse Mortgage Pricing and Capital Requirements Allowing for Idiosyncratic House Price Risk and Longevity Risk.

Females

Model A

• Discrete age survival function • Cohort trends – period and

age-to-age variability and trends

• Cohort curve generated by the dynamics

• Multiple risk factors based on age

• Dependence in volatility –principal components

Model B

• Parametric survival function - smoothing of age-to-age variability

• Period trends• Cohort curve read off projected

period curves• Two factors - stochastic

parameters of mortality curve• Dependence – two factors,

from smoothed curve dynamics

Systematic Mortality Model Risk

Importance of cohort and forward survival curves

Source: Alai, D.H. and Sherris, M. (2012), Rethinking Age-Period-Cohort Mortality Trend Models, Article published on line 16 Apr 2012, Scandinavian Actuarial Journal

Model Mortality Surface (age-period and cohort)

Source: C. Blackburn and M. Sherris, (2013), Consistent Dynamic Affine Mortality Models for Longevity Risk Applications, Insurance: Mathematics and Economics, Volume 53, Issue 1, July 2013, Pages 64–73

Quantification of Systematic Longevity Risk

Source: C. Blackburn and M. Sherris, (2013), Consistent Dynamic Affine Mortality Models for Longevity Risk Applications, Insurance: Mathematics and Economics, Volume 53, Issue 1, July 2013, Pages 64–73

Forward survival curves (cohort)

Expected survival curves and pricing

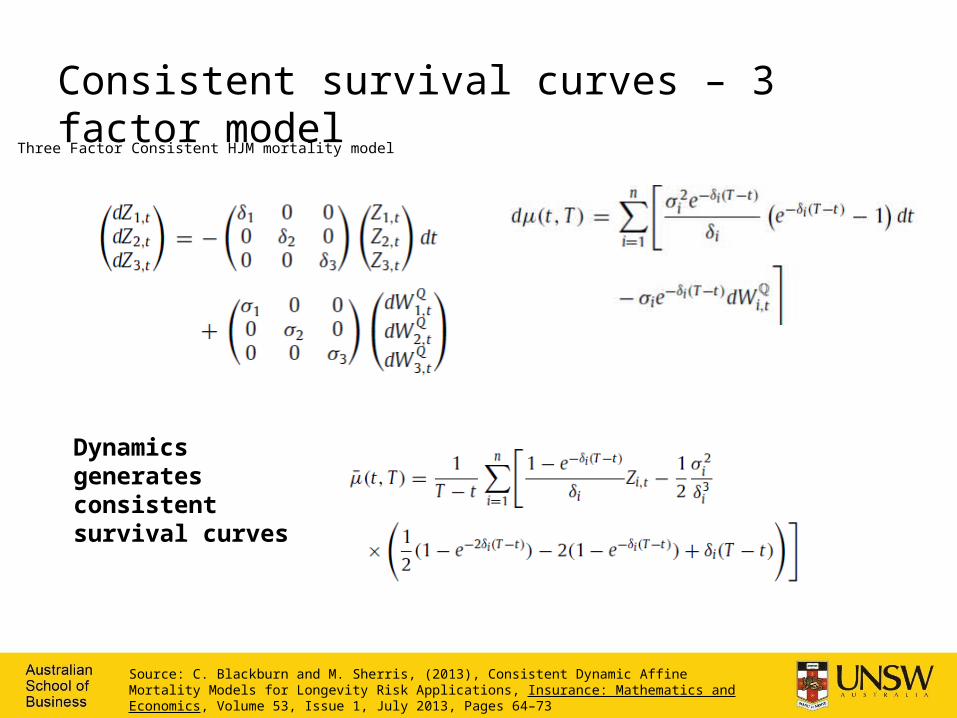

Consistent survival curves – 3 factor model

Three Factor Consistent HJM mortality model

Dynamics generates consistent survival curves

Source: C. Blackburn and M. Sherris, (2013), Consistent Dynamic Affine Mortality Models for Longevity Risk Applications, Insurance: Mathematics and Economics, Volume 53, Issue 1, July 2013, Pages 64–73

Consistent model risk factors – 3 factor estimation stability

Source: C. Blackburn and M. Sherris, (2013), Consistent Dynamic Affine Mortality Models for Longevity Risk Applications, Insurance: Mathematics and Economics, Volume 53, Issue 1, July 2013, Pages 64–73

Refitting model at different time points demonstrates model consistency

How many models used in practice have this property?

Consistent Survivor Curves – 2 versus 3 factor

Source: C. Blackburn and M. Sherris, (2013), Consistent Dynamic Affine Mortality Models for Longevity Risk Applications, Insurance: Mathematics and Economics, Volume 53, Issue 1, July 2013, Pages 64–73

Increase in number of factors explains older age mortality better

Best Estimate Forward Survivor Curve – 2 factors

Removes need for simulations in simulations for ALM, valuation, risk quantification

Price of Risk and Forward Survivor Curve – 2 factors

Price of risk – financial approaches versus actuarial (Wang transform)

Wang transform gives wrong signs and magnitude for prices of risk (offset by other parameters)

Sharpe ratio scales the survivor curve and does not impact risk factor loadings

Price of risk - longevity risk swap pricing

Pricing differences less pronounced than for risk quantification

Price of risk versus volatility parameter risk – survival curve

Source: Fung, M. C., Ignatieva, K. and Sherris, M., (2013), Systematic Mortality Risk: An Analysis of Guaranteed Lifetime Withdrawal Benefits in Variable Annuities

Equity exposure

Mortality risk premium

Source: Fung, M. C., Ignatieva, K. and Sherris, M., (2013), Systematic Mortality Risk: An Analysis of Guaranteed Lifetime Withdrawal Benefits in Variable Annuities

Price of risk versus volatility parameter risk - GLWB

Price of risk and impact on risk based capital

Source: Meyricke, R. and Sherris, M. (2013), Optimal Longevity Risk Management Under Solvency II

Solvency capital costs versus longevity swap for a life annuity

Varying price of risk in Model A

Incentives to hedge shorter terms and retain tail risk with higher prices of risk

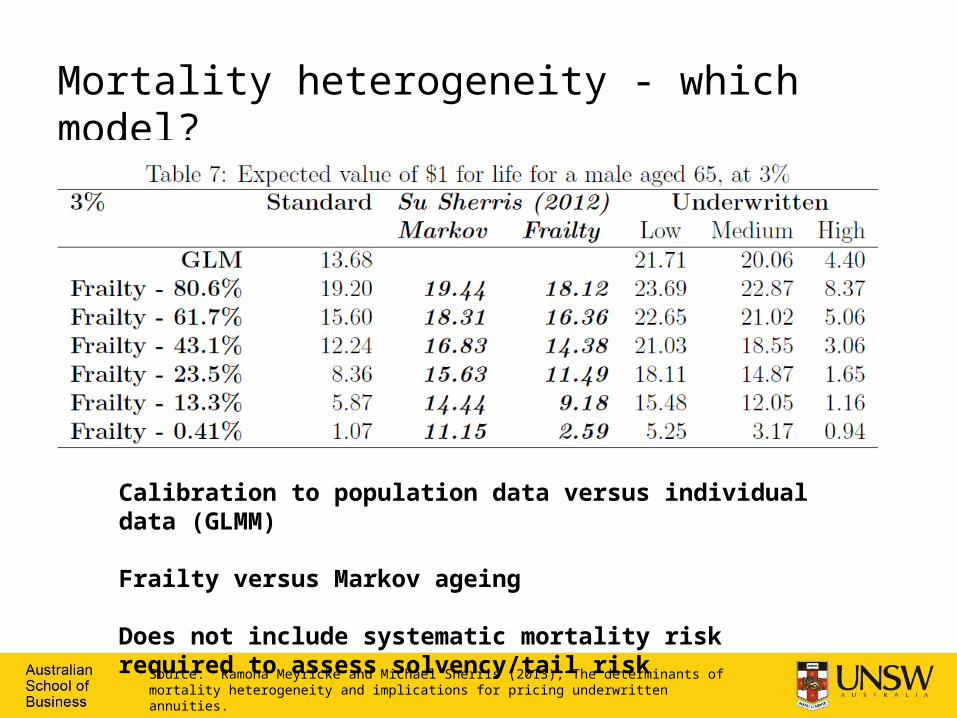

Mortality heterogeneity - which model?

Source: Ramona Meyricke and Michael Sherris (2013), The determinants of mortality heterogeneity and implications for pricing underwritten annuities.

Calibration to population data versus individual data (GLMM)

Frailty versus Markov ageing

Does not include systematic mortality risk required to assess solvency/tail risk

Heterogeneity model risk – longevity tail risk for annuity fund

Mortality model HeterogeneityAnnuity premium

Risk measures at age 110

Mean Stdev 95% VaR

Markov

best health only 16.32 -0.07 386.09 631.73mixed 14.29 -15.86 710.31 1176.89mixed w self selection 14.29

-5872.49 428.07 6566.69

Le Bras

best health only 15.84 4.24 607.33 986.31mixed 14.16 11.56 635.70 1022.46mixed w self selection 14.16

-3105.13 613.12 4109.81

Vaupel

best health only 16.29 -0.88 658.73 1072.07mixed 14.72 -1.61 673.32 1109.78mixed w self selection 14.72

-2610.51 666.36 3694.48

Premium for a life annuity of 1 p.a. and tail risk measures for a pool of 1000 individuals aged 65.

Fixed investment return of 3% p.a.

Effect of adverse selection

Source: Sherris, M. and Zhou, Q. (2013), Model Risk, Mortality Heterogeneity and Implications for Solvency and Tail Risk.

Mortality model

Heterogeneity

Annuity premium

Risk measures at age 110

Mean Stdev 95% VaR

Markov

best health only 13.48 -199.80 4912.11 7843.93state 2 12.54 -198.90 4387.30 7117.17state 3 10.04 -111.25 3192.87 5144.76state 4 6.74 -54.63 1917.96 3131.44state 5 5.00 -35.88 1478.46 2441.54mixed 11.99 -132.34 4420.42 7051.55mixed w self selection 11.99 -14675.61 4112.85 21204.18

Le Bras

best health only 12.95 -109.05 4901.30 7811.46mixed 11.84 -59.61 4283.44 6883.19mixed w self selection 11.84 -7006.90 4244.59 13922.83

Vaupel

best health only 13.14 -141.61 5040.23 8067.82mixed 12.13 -112.90 4476.47 7234.56mixed w self selection 12.13 -5777.86 4397.70 12874.70

Premium for a life annuity of 1 p.a. and tail risk measures for a pool of 1000 individuals aged 65 Results are shown for the different deterministic models of heterogeneity.

Random investment return

Investment risk magnifies longevity risk and impact of selection

Source: Sherris, M. and Zhou, Q. (2013), Model Risk, Mortality Heterogeneity and Implications for Solvency and Tail Risk.

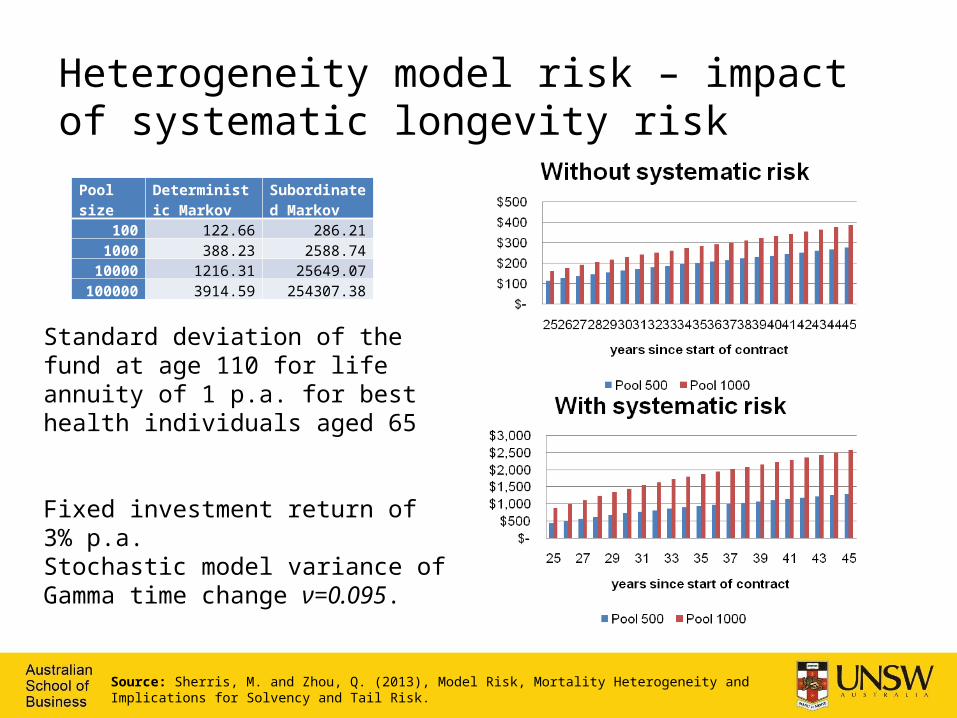

Heterogeneity model risk – investment and longevity tail risk for annuity fund

Pool size

Deterministic Markov

Subordinated Markov

100 122.66 286.211000 388.23 2588.74

10000 1216.31 25649.07100000 3914.59 254307.38

Standard deviation of the fund at age 110 for life annuity of 1 p.a. for best health individuals aged 65

Fixed investment return of 3% p.a.Stochastic model variance of Gamma time change ν=0.095.

Heterogeneity model risk – impact of systematic longevity risk

Source: Sherris, M. and Zhou, Q. (2013), Model Risk, Mortality Heterogeneity and Implications for Solvency and Tail Risk.

Summary – key points

Mortality/longevity risk model developments – key ideas

• Model consistency and parameter stability• Tractability and ease of application• Risk factors and price of risk• Heterogeneity and data

26

Thank you for your attention

Michael Sherris [email protected]

School of Risk and Actuarial StudiesARC Centre of Excellence in Population Ageing Research

University of New South Wales

Acknowledgement: ARC Linkage Grant Project LP0883398 Managing Risk with Insurance and Superannuation as Individuals

Age with industry partners PwC, APRA and the World Bank as well as the support of the Australian Research Council Centre of

Excellence in Population Ageing Research project CE110001029.

ReferencesAlai, D.H. and Sherris, M. (2012), Rethinking Age-Period-Cohort Mortality Trend Models, Article

published on line 16 Apr 2012, Scandinavian Actuarial Journal, DOI: 10.1080/03461238.2012.676563

Su, S. and Sherris, M. (2012), Heterogeneity of Australian Population Mortality and Implications for a Viable Life Annuity Market, Insurance: Mathematics and Economics, 51, 2, 322–332.

Ziveyi, J, Blackburn, C., and Sherris, M. (2013), Pricing European Options on Deferred Annuities, Insurance: Mathematics and Economics, Volume 52, Issue 2, March 2013, 300–311.

Blackburn, C. and Sherris, M., (2013), Consistent Dynamic Affine Mortality Models for Longevity Risk Applications, Insurance: Mathematics and Economics, Volume 53, Issue 1, July 2013, Pages 64–73 http://dx.doi.org/10.1016/j.insmatheco.2013.04.007

Meyricke, R. and Sherris, M. (2013), The determinants of mortality heterogeneity and implications for pricing underwritten annuities, accepted Insurance: Mathematics and Economics, on-line 29 June 2013; http://www.sciencedirect.com/science/article/pii/S0167668713000887

Meyricke, R. and Sherris, M. (2013), Optimal Longevity Risk Management Under Solvency II.

Sherris, M. and Zhou, Q. (2013), Model Risk, Mortality Heterogeneity and Implications for Solvency and Tail Risk.

Fung, M. C., Ignatieva, K. and Sherris, M., (2013), Systematic Mortality Risk: An Analysis of Guaranteed Lifetime Withdrawal Benefits in Variable Annuities.

Shao, W., Sherris, M., and Hanewald, K., (2103), Reverse Mortgage Pricing and Capital Requirements Allowing for Idiosyncratic House Price Risk and Longevity Risk.