diageo interim results six months ended 31 · pdf fileorganic net sales 4.2% eps...

TRANSCRIPT

1

DIAGEO INTERIM RESULTS SIX MONTHS ENDED 31 DECEMBER 2017

CONSISTENT DELIVERY OF STRONG RESULTS

Four measures of our progress• efficient growth• value creation• credibility and trust• motivated people

Reflecting our ambition to be one of the best performing, most trusted and respected consumer products companies in the world

Delivering through our six priorities with clear goals defined by our performance ambition

2

CONSISTENT DELIVERY OF STRONG RESULTS

Consistent strong cash delivery: Free cash flow £1bn

Organic operating margin expansion 81bps

3

Organic volume 1.8%. Organic net sales 4.2%

Eps pre-exceptionals up 9.4%

Returned £0.8bn to shareholders through share buy-back

Interim dividend up 5%

CONTINUING OUR PERFORMANCE MOMENTUM

4

Organic net sales growth

77

2419

37

81

F14 F15 F16 F17 F18 H1

Organic operating margin improvement (bps)

326

699839

1,084 1,029

F14 H1 F15 H1 F16 H1 F17 H1 F18 H1

Free cash flow (£ million)

0.4%0.0%

2.8%

4.3% 4.2%

F14 F15 F16 F17 F18 H1

CONTINUED SOLID GROWTH IN THE THREE FOCUS AREAS: ORGANIC NET SALES GROWTH

India 2.3%

US Spirits 2.9%

5

Scotch 2.8%

CONTINUED MOMENTUM WHICH REFLECTS:

Consistent broad based growth across the business and the three

focus areas

Continued margin expansion enabled by productivity programme and strong cash flow

6

Delivering our strategy through our six execution priorities

Confidence in delivering our medium term guidance and enables

our long term performance ambition

A SET OF RESULTS THAT DEMONSTRATE CONTINUED PERFORMANCE MOMENTUM

ROIC

Organic net sales growth

Organic operating margin improvement

Free cash flow

Pre-exceptional eps

Total Shareholder Return

Value creation:

Efficient growth:

7

F18 H1

up 77 bps to 16.5%

4.2%

+81bps

£1.0bn

up 9.4% to 67.8p

up 22%

8

Organic growth

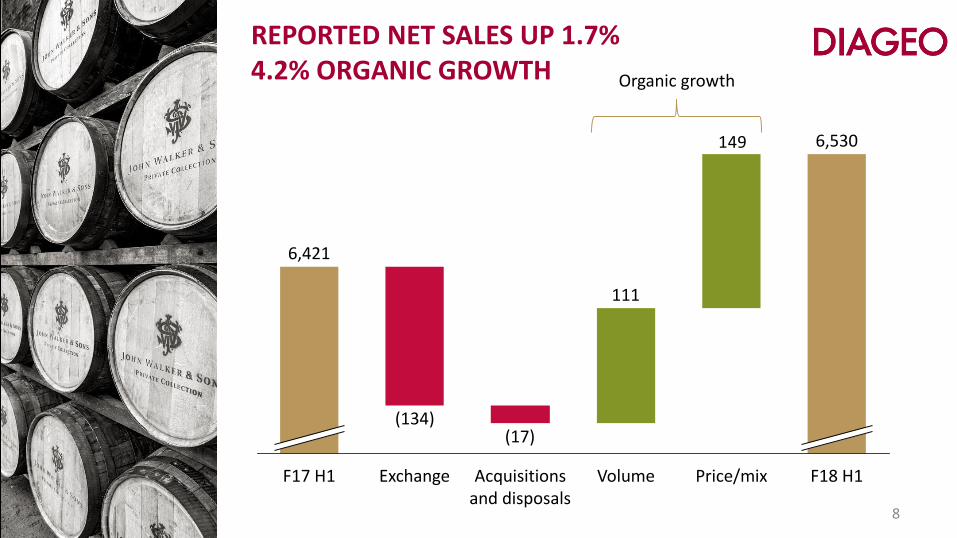

REPORTED NET SALES UP 1.7% 4.2% ORGANIC GROWTH

149 6,530

Price/mixVolumeAcquisitions and disposals

ExchangeF17 H1

6,421

F18 H1

111

(17)(134)

4.2% ORGANIC NET SALES GROWTH

4.2%4.3%

2.8%2.4%

3.2%

1.5%1.8%

1.1%1.3%

F18 H1F17F16

Organic volume growth Organic net sales growthPrice/Mix

9

10

NAM DIAGEO

8.3%

LAC

8.7%

6.9%

2.4%

APAC

(1.5)%

6.8%

4.2%

1.8%

2.5%

0.8%

1.7%4.6%

4.4%

EUROPE & TURKEY

(1.9)% (1.8)%

AFRICA

3.6%

1.7%

ALL REGIONS DELIVERED TOP LINE GROWTH

volume

price/mix

Organic net sales growth

(0.2)%

BROAD BASED ORGANIC GROWTH ACROSS OUR CATEGORIES

Tequila

4%

Gin

16%

IMFL Whisky

43%

BeerLiqueurs

5%

Rum

1%

5%

NAM Whiskey

4%

Vodka

(3)%

Scotch

Organic net sales growth

Category as a % of net sales

27% 11% 9% 7% 6% 5% 4% 3% 15%

11

3%

STRONG PERFORMANCE ACROSS OUR PORTFOLIO

12

Reserve

11%

Local stars

5%

Global giants

5%

Organic net sales growth

6%

Captain Morgan 6%

Smirnoff

Global giants

Guinness 4%

Tanqueray 16%

Baileys

(1)%

Johnnie Walker 7%

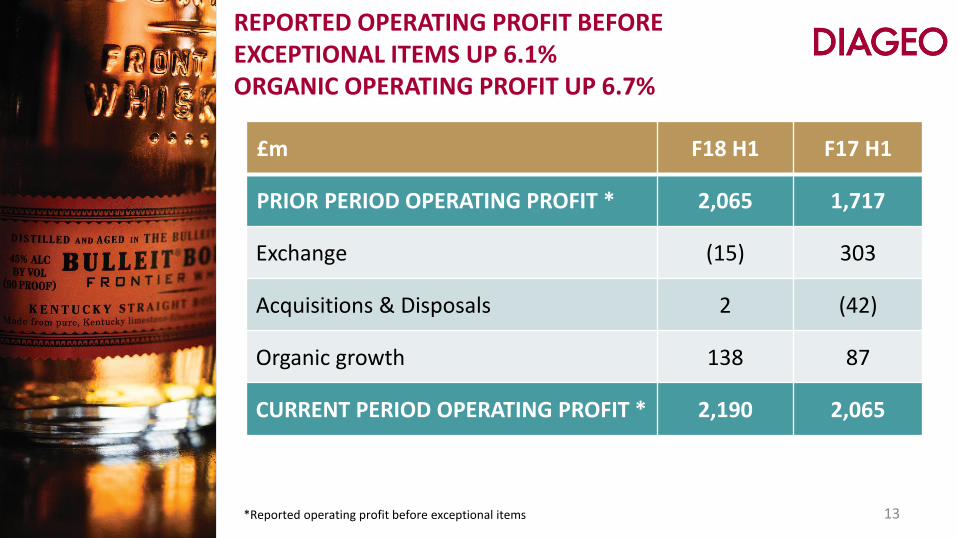

REPORTED OPERATING PROFIT BEFORE EXCEPTIONAL ITEMS UP 6.1% ORGANIC OPERATING PROFIT UP 6.7%

13

£m F18 H1 F17 H1

PRIOR PERIOD OPERATING PROFIT * 2,065 1,717

Exchange (15) 303

Acquisitions & Disposals 2 (42)

Organic growth 138 87

CURRENT PERIOD OPERATING PROFIT * 2,190 2,065

*Reported operating profit before exceptional items

REPORTED OPERATING MARGIN EXCLUDING EXCEPTIONAL ITEMS UP 138 BPSORGANIC OPERATING MARGIN GREW 81 BPS

14

81bps

12bps45bps

F18 H1Organic operating margin

Acquisitions and disposals

ExchangeF17 H1

33.5%

32.2%

ORGANIC OPERATING MARGIN UP 81 BPS

15

F18 H1Other operating

items

MarketingGross marginF17 H1

Movement in organic operating margin

32.8%

33.6%

(44)bps

122bps

3bps

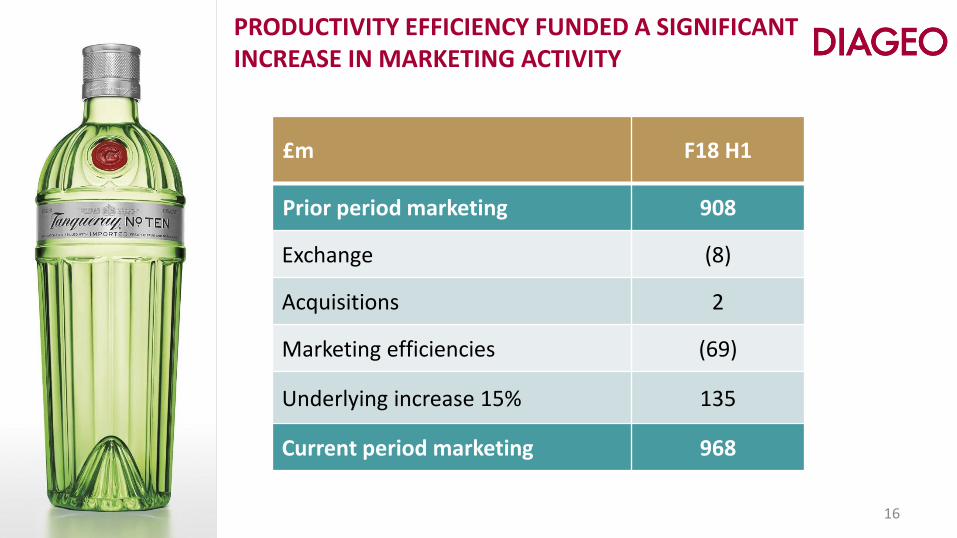

PRODUCTIVITY EFFICIENCY FUNDED A SIGNIFICANT INCREASE IN MARKETING ACTIVITY

16

£m F18 H1

Prior period marketing 908

Exchange (8)

Acquisitions 2

Marketing efficiencies (69)

Underlying increase 15% 135

Current period marketing 968

ORGANIC OPERATING MARGIN UP 81 BPS

17

Movement in organic operating margin

32.8%

33.6%

F17 H1 F18 H1Other operating

items

MarketingGross margin

(44)bps

122bps

3bps

PRODUCTIVITY PROGRAMME ON TRACK TO DELIVER INCREASED GUIDANCE

NET REVENUE MANAGEMENT

MARKETINGGLOBAL SUPPLY

ORGANISATION EFFECTIVENESS

INDIRECTS

F17-F19 GuidanceProductivity target £700m

2/3 reinvestedMargin improvement of 175bps

18

STRONG FREE CASH FLOW DELIVERY

19

86

F18

1,029

Other (iii)InterestTax

(101)

Capex

(17)

Working capital

(37)

Operating profit (ii)

Exchange (i)

(15)

F17

1,084

(i) Exchange on operating profit before exceptional items(ii) Operating profit excluding exchange, depreciation and amortisation, post employment charges and non cash items(iii) Other items include post employment payments, dividends received from associates and joint ventures, and loans and other

investments

218

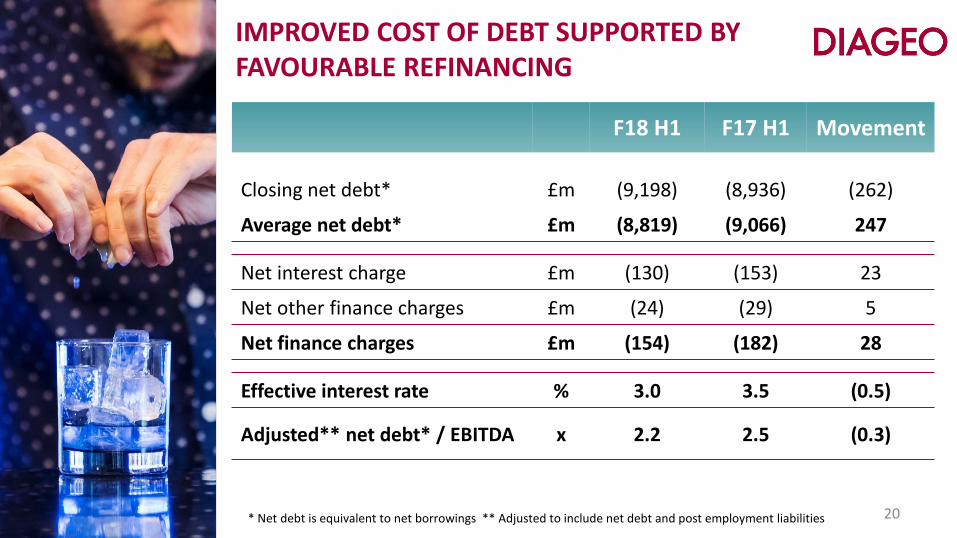

IMPROVED COST OF DEBT SUPPORTED BY FAVOURABLE REFINANCING

F18 H1 F17 H1 Movement

Closing net debt* £m (9,198) (8,936) (262)

Average net debt* £m (8,819) (9,066) 247

Net interest charge £m (130) (153) 23

Net other finance charges £m (24) (29) 5

Net finance charges £m (154) (182) 28

Effective interest rate % 3.0 3.5 (0.5)

Adjusted** net debt* / EBITDA x 2.2 2.5 (0.3)

20* Net debt is equivalent to net borrowings ** Adjusted to include net debt and post employment liabilities

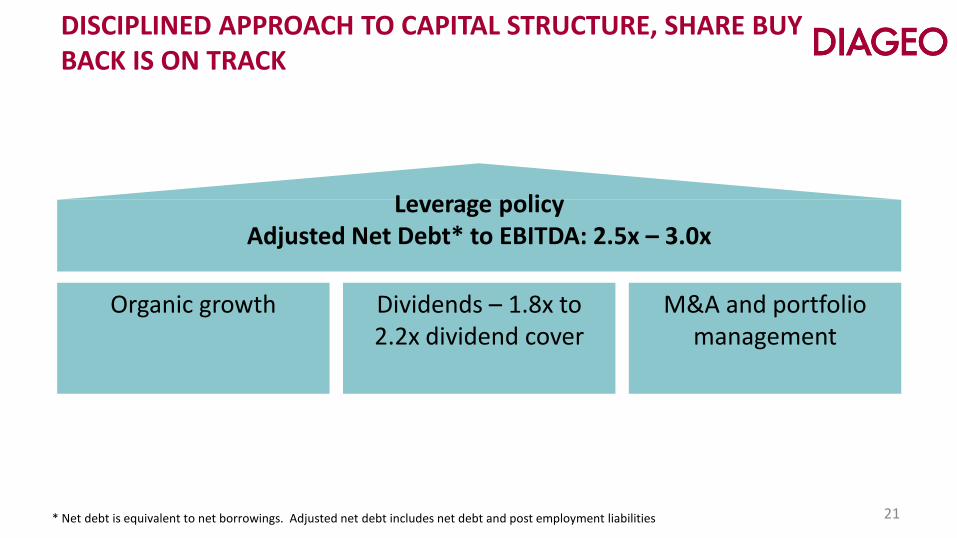

DISCIPLINED APPROACH TO CAPITAL STRUCTURE, SHARE BUY BACK IS ON TRACK

21

Organic growth Dividends – 1.8x to 2.2x dividend cover

M&A and portfolio management

Leverage policyAdjusted Net Debt* to EBITDA: 2.5x – 3.0x

* Net debt is equivalent to net borrowings. Adjusted net debt includes net debt and post employment liabilities

F18 EXCHANGE IMPACT NOW FORECAST TO BE NEGATIVE FOR BOTH OPERATING PROFIT AND NET SALES

22

Translation rate

F17* F18 H1**

F18forecast ***

$/£ 1.27 1.32 1.36

€/£ 1.16 1.12 1.13

* Average rate **Average rate Jul-Dec ***Weighted average rate of F18 H1 and spot rate for H2

Transaction rate

F171 F18 H1 F18 forecast2

$/£ 1.45 1.41 1.37

€/£ 1.22 1.17 1.15

1. Average rate inc. hedging2. 81% of £/$ exposure hedged

59% of €/£ exposure hedged

Exchange rates Total Exchange Impact

£m F17 F18 H1F18

forecast

Net Sales 1,359 (134) (460)

Operatingprofit

447 (15) (60)

Net Interest

(28) 2 8

BASIC EPS INCREASED 36%EPS BEFORE EXCEPTIONAL ITEMS UP 9.4%

23

Pence per share

F17 H1 eps before exceptional items 62.0

Exchange (0.6)

Organic operating profit growth 5.5

Associates and joint ventures (0.1)

Tax (0.3)

Finance charges 1.1

Other 0.2

F18 H1 eps before exceptional items 67.8

A STRONG SET OF RESULTS DELIVERING EFFICIENT GROWTH AND VALUE CREATION

24

ROIC

Organic net sales growth

Organic operating margin improvement

Free cash flow

Pre-exceptional eps

Total Shareholder Return

Value creation:

Efficient growth: F18 H1

up 77 bps to 16.5%

4.2%

81bps

£1.0bn

up 9.4% to 67.8p

up 22%

CONSISTENT DELIVERY OF STRONG RESULTS

Four measures of our progress• efficient growth• value creation• credibility and trust• motivated people

Reflecting our ambition to be one of the best performing, most trusted and respected consumer products companies in the world

Delivering through our six priorities with clear goals defined by our performance ambition

25

Our consumers drink better, not more We contribute to the World Health Organization goal of 10% reduction in harmful

drinking by 2025

Educate 5 million young people, parents and teachers about the dangers of

underage drinking

Reach 200 million people with moderation messages from our brands

Collect 50 million pledges never to drink and drive through #JoinThePact

ALCOHOL IN SOCIETY: DIAGEO’S AMBITIOUS NEW TARGETS

By 2025, we will:

26

The outcome we seek through our Alcohol in Society work:

A CLEAR STRATEGY DELIVERED THROUGH OUR SIX PRIORITIES

1 Keep premium core vibrant

2 Increase participation in mainstream spirits

3 Continue to win in reserve

4 Drive innovation at scale

5 Build advantaged routes to consumer

6 Embed productivity in our culture to drive out costs to invest in growth

27

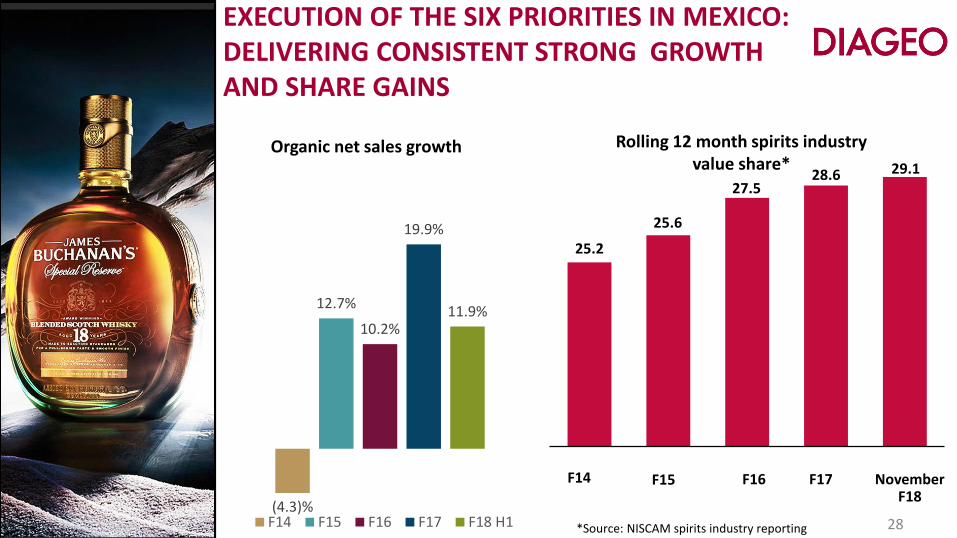

28

Rolling 12 month spirits industry value share*

25.2

25.6

November F18

F15F14

27.5

F16

28.6 29.1

F17

(4.3)%

12.7%

10.2%

19.9%

11.9%

F14 F15 F16 F17 F18 H1

Organic net sales growth

EXECUTION OF THE SIX PRIORITIES IN MEXICO: DELIVERING CONSISTENT STRONG GROWTHAND SHARE GAINS

*Source: NISCAM spirits industry reporting

29

KEEPING PREMIUM CORE VIBRANT WITH PURPOSE DRIVEN MARKETING IN MEXICO

F15-F17 organic net sales CAGR 14%

+ NATIONAL DISTRIBUTION

+ REGIONAL COMMUNICATIONS

+ NATIONAL COMMUNICATIONS

REGIONAL DISTRIBUTION

ACCELERATE

550K cases

Value Share*

F13 F14 F15 F16 F17

5.0 12.3 14.6 21.6 27.9

391K cases

231K cases

128K cases

65K cases

INCREASING PARTICIPATION IN MAINSTREAM SPIRITS: BLACK & WHITE LEADING PRIMARY SCOTCH GROWTH IN MEXICO

*Share of primary scotch category. Source: NISCAM spirits industry reporting

31

CONTINUE TO WIN IN RESERVE WITH THE LEADING LUXURY DRINKS PORTFOLIO IN MEXICO

46.845.2

47.0 47.949.4

Rolling 12 month value share of reserve category*

F14 F15 F16 F17 November F18

*Source: NISCAM spirits industry reporting

32

DRIVING INNOVATION AT SCALE IN MEXICO

33

BUILD ADVANTAGED ROUTES TO CONSUMER: EXPANDING OUR FOOTPRINT IN MEXICO

On Trade

Off Trade

Hotels and Third Space

Expanded distribution from 50 to 75 cities More than doubled called on outlets while increasing

sales force effectiveness

Small dedicated team to increase focus Increased hotel distribution more than 4X Reaching 30 festivals and over 10 million consumers

Created a team 100% focused on execution Increased distribution by 25% Almost doubled called on outlets Automation to track and audit execution

34

Organisational effectiveness and zero based budgeting driving overheads savings

EMBEDDING PRODUCTIVITY TO DRIVE OUT COSTS TO INVEST IN GROWTH

Net revenue management enabling top line growth

Delivered supply savings through footprint optimisation, operational excellence and procurement savings

Marketing efficiencies delivered through rationalising media agencies, reducing cost of point of sale material and non-working spend

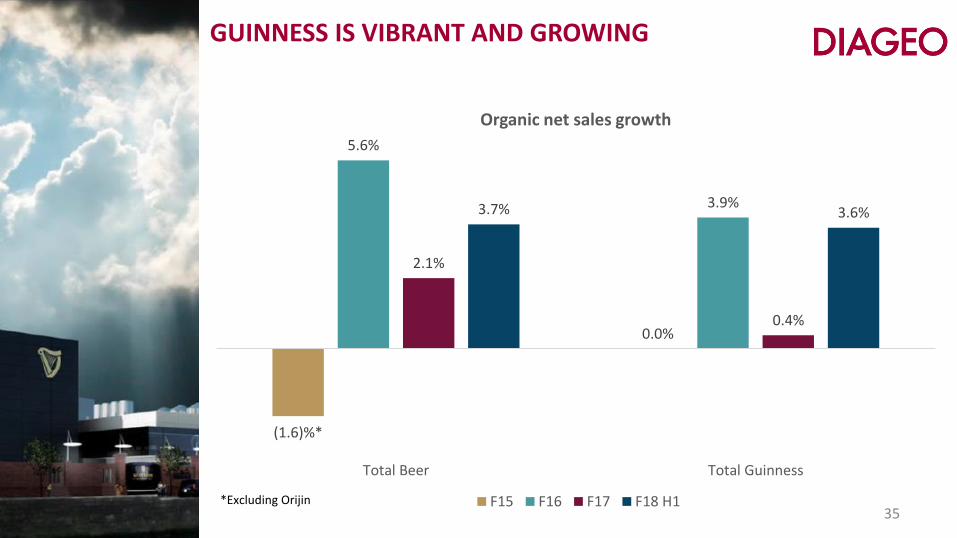

GUINNESS IS VIBRANT AND GROWING

(1.6)%*

0.0%

5.6%

3.9%

2.1%

0.4%

3.7% 3.6%

Total Beer Total Guinness

Organic net sales growth

F15 F16 F17 F18 H1*Excluding Orijin35

GUINNESS IS VIBRANT AND GROWING

GB US

Nigeria/Kenya

Ethiopia 36

CONTINUED SOLID GROWTH IN THE THREE FOCUS AREAS: ORGANIC NET SALES GROWTH

India 2.3%

US Spirits 2.9%

37

Scotch 2.8%

38

F18 FOCUS AREAS: SCOTCH SOLID FIRST HALF PERFORMANCE

0.4% 0.7%

9.6%

6.5%8.8%

(13.5)%

4.7%6.0%

16.2%

2.5%4.8%

(4.5)%

2.8%

6.7%

0.9% 2.5%

7.5%

(14.0)%

Total Scotch Johnnie Walker Buchanan's Scotch Malts Primary Scotch Other

F16 F17 F18 H1

Organic net sales growth

% of Scotchnet sales

57% 9% 12% 11% 11%

39

F18 FOCUS AREAS: SCOTCH RECRUITING WITH JOHNNIE WALKER

INSPIRING STORIES

BLUE LABEL

COMPELLING

DRINKS STRATEGY

GIFTING

THE YEAR WE PAINT THE WORLD JOHNNIE WALKER BLACK

40

F18 FOCUS AREAS: SCOTCHACCELERATING THE FUTURE OF SCOTCH IN CHINA

41

Whisky Boutiques

Liquid on Lips- Whisky Academy Love WhiskySocial Media Platform for

Whisky Enthusiasts

Prestige Scotch

Johnnie Walker Blue Label and The Singleton

F18 FOCUS AREAS: US SPIRITSROBUST FIRST HALF PERFORMANCE

Organic volume and net sales growth

(3.5)%

1.2% 1.5%0.9%

(1.5)%

3.1% 3.4%2.9%

(2.1)%

4.2%

6.1%5.5%

F15* F16 F17 F18 H1

Volume Net sales Net sales excluding Ciroc and Ketel One vodka

42* Excluding Wine

Net sales excluding Cîroc and Ketel One vodka

F18 FOCUS AREAS: US SPIRITSCATEGORY SHARE GAINS CONTINUED FOR ALL KEY BRANDS EXCEPT VODKA

43

10.6%

4.7%

1.5%

7.3%

(1.6)%

(14.4)%

27.8%

11.6%

5.9% 5.3%

1.8%

5.7%

(2.4)%

(8.1)%(2.4)%

34.2%

4.4%

Crown Royal JohnnieWalker

CaptainMorgan

Baileys Smirnoff Cîroc Ketel Onevodka

Don Julio Bulleit Buchanan's

Nielsen and NABCA combined value growth

F17 H2 F18 H1*

Core brands(3.9)%

v

15.0%

F18 H1 category value share change*

11.9%

* Nielsen through 30 December, 2017, NABCA through 30 November, 2017

Cîroc

Improve super premium vodka

Continue double digit growth on reserve*

44

Execute proven plans for our brands in the second half supported

by marketing up-weight

US SPIRITS: STRONG PLANS IN THE SECOND HALF

* Excluding super premium vodka

Robust innovation pipeline for the second half

F18 FOCUS AREAS: INDIAIMPROVED PERFORMANCE AS TOP LINE HEADWINDS SUBSIDE

45

9.5%

11.3%

2.8%

5.7%

Prestige and above brands organic net sales growth

5.3%

4.0%

0.5%

2.3%

India organic net sales growth

F18 FOCUS AREAS: INDIAPRESTIGE AND ABOVE PLANS ARE WORKING

46

PAINTING INDIA JOHNNIE WALKER BLACKContinuing renovation of Prestige and

Above brands

Innovation

Black & White 12 year old

Primary scotch - Black Dog

Royal Challenge Xtra Bold

Captain Morgan Original Rum

COGS• Inputs rate negotiation with suppliers post GST roll-out

• Tramlining and Brand Value Engineering

Marketing• Efficiency in agency and point of sale costs

• Leveraging new tools to improve ROI

Overheads• Additional savings from organisation effectiveness

• Zero based budgeting driving further indirect spend savings

Net Revenue Management

• Price increases implemented across 13 states

• Efficiency in trade spend

• Positive mix from prestige and above brands growth

47

Gross margin improvement

c. 200bps

Overheads reduced 10%

F18 FOCUS AREAS: INDIAMITIGATED GST IMPACT WITH ACCELERATED PRODUCTIVITY AND ADDITIONAL MITIGATION STEPS

EFFECTIVE EXECUTION OF OUR STRATEGYCONSISTENT DELIVERY OF STRONG RESULTS:

Consistent top line growth and margin expansion enabled by productivity programme and strong cash flow

48

Delivering our strategy through our six execution priorities

Creating a more agile, disciplined and high performing organisation

Confidence in delivering our medium term guidance and enables our long term performance ambition

APPENDIX 1: 1/2FORWARD LOOKING STATEMENTS

Exchange rate outlook Using exchange rates £1 = $1.39; £1 = €1.13, the exchange rate movement for the year ending 30 June 2018 is estimated to adversely impact net sales by approximately £460 million and operating profit by approximately £60 million.

Net salesLooking to the full year, our expectations for fiscal 18 remain unchanged. We continue to expect organic net sales growth roughly in line with last year and consistent with our mid-term guidance of mid-single digit top line growth.

Operating marginOn margin, we expect continued progress toward our goal to deliver 175 basis points of improvement for the three years ended June 2019, with more of the margin expansion across both financial years coming through in fiscal 19 as we expect to have less costs to absorb and will get greater benefits from our investments in NRM and marketing catalyst capabilities.

Net finance chargesFor the full year we expect our effective interest rate to remain around 3.0% as we continue to see the benefit from the refinancing with some risk of floating rates rising.

We expect other finance charges for the full year to be roughly in line with fiscal 17.

49

APPENDIX 1: 2/2FORWARD LOOKING STATEMENTS

TaxationOur current expectation is that the tax rate before exceptional items for the year ending 30 June 2018 will be approximately 20%, a 1ppt improvement versus our prior guidance. The decrease between our prior expectation and the estimated tax rate for the year ending 30 June 2018 is principally driven by the headline rate reduction in the United States introduced by the Tax Cuts and Jobs Act enacted on 22 December 2017. As for most multinationals the current tax environment is creating increased levels of uncertainty.

Capital expenditureWe expect our full year Capex spend to be in the range of £500m to £550m.

DividendWe have a progressive dividend policy and we expect to maintain a mid single digit increase until we rebuild dividend cover back to our target range of 1.8 to 2.2x.

Share buy-backIn July 2017, the board approved a share buy-back programme to return up to £1.5bn of capital back to shareholders. We are on track and at the end of December £760m has been utilised to repurchase 29.5m shares with these shares having been cancelled.

50

51

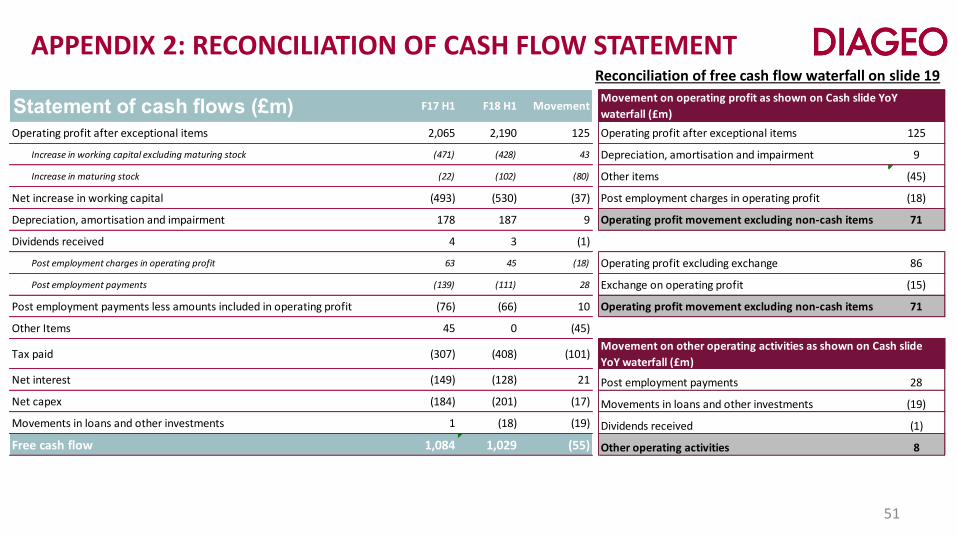

Reconciliation of free cash flow waterfall on slide 19

APPENDIX 2: RECONCILIATION OF CASH FLOW STATEMENT

Statement of cash flows (£m) F17 H1 F18 H1 Movement

Operating profit after exceptional items 2,065 2,190 125 Operating profit after exceptional items 125

Increase in working capital excluding maturing stock (471) (428) 43 Depreciation, amortisation and impairment 9

Increase in maturing stock (22) (102) (80) Other items (45)

Net increase in working capital (493) (530) (37) Post employment charges in operating profit (18)

Depreciation, amortisation and impairment 178 187 9 Operating profit movement excluding non-cash items 71

Dividends received 4 3 (1)

Post employment charges in operating profit 63 45 (18) Operating profit excluding exchange 86

Post employment payments (139) (111) 28 Exchange on operating profit (15)

Post employment payments less amounts included in operating profit (76) (66) 10 Operating profit movement excluding non-cash items 71

Other Items 45 0 (45)

Tax paid (307) (408) (101)

Net interest (149) (128) 21 Post employment payments 28

Net capex (184) (201) (17) Movements in loans and other investments (19)

Movements in loans and other investments 1 (18) (19) Dividends received (1)

Free cash flow 1,084 1,029 (55) Other operating activities 8

Movement on operating profit as shown on Cash slide YoY

waterfall (£m)

Movement on other operating activities as shown on Cash slide

YoY waterfall (£m)

Cautionary statement concerning forward-looking statements

This document contains ‘forward-looking’ statements. These statements can be identified by the fact that they do not relate only to historical or current facts. In particular, forward-looking statements include all statements that express forecasts, expectations, plans, outlook, objectives and projections with respect to future matters, including trends in results of operations, margins, growth rates, overall market trends, the impact of changes in interest or exchange rates, the availability or cost of financing to Diageo, anticipated cost savings or synergies, expected investments, the completion of any strategic transactions and restructuring programmes, anticipated tax rates, changes in the international tax environment, expected cash payments, outcomes of litigation, anticipated deficit reductions in relation to pension schemes and general economic conditions. By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements, including factors that are outside Diageo's control.

These factors include, but are not limited to:

• economic, political, social or other developments in countries and markets in which Diageo operates, which may contribute to a reduction in demand for Diageo’s products, decreased consumer spending, adverse impacts on Diageo’s customer, supplier and/or financial counterparties, or the imposition of import, investment or currency restrictions;

• the negotiating process surrounding, as well as the eventual terms of, the United Kingdom’s exit from the European Union, which could lead to a sustained period of economic and political uncertainty and complexity whilst detailed withdrawal terms and any successor trading arrangements with other countries are negotiated, finalised and implemented, potentially adversely impacting economic conditions in the United Kingdom and Europe more generally as well as Diageo's business operations and financial performance;

• changes in consumer preferences and tastes, including as a result of changes in demographics, evolving social trends (including potential shifts in consumer tastes towards locally produced small batch products), changes in travel, vacation or leisure activity patterns, weather conditions, public health regulations and/or a downturn in economic conditions;

• any litigation or other similar proceedings (including with customs, competition, environmental, anti-corruption and other regulatory authorities), including litigation directed at the drinks and spirits industry generally or at Diageo in particular;

• changes in the international tax environment, including as a result of the OECD Base Erosion and Profit Shifting Initiative and EU anti-tax abuse measures, leading to uncertainty around the application of existing and new tax laws and unexpected tax exposures;

• the effects of climate change, or legal, regulatory or market measures intended to address climate change, on Diageo’s business or operations, including any impact on the cost and supply of water;

• (Continued on following page)52

• (continued from previous page)• changes in the cost of production, including as a result of increases in the cost of commodities, labour and/or energy or as a result of inflation;• legal and regulatory developments, including changes in regulations relating to production, distribution, importation, marketing, advertising, sales, pricing, packaging and

labelling, product liability, labour, compliance and control systems, environmental issues and/or data privacy; • the consequences of any failure by Diageo or its associates to comply with anti-corruption, sanctions, trade restrictions or similar laws and regulations, or any failure of

Diageo’s related internal policies and procedures to comply with applicable law;• the consequences of any failure of internal controls, including those impacting compliance with new accounting and/or disclosure requirements;• Diageo’s ability to maintain its brand image and corporate reputation or to adapt to a changing media environment;• increased competitive product and pricing pressures, including as a result of actions by increasingly consolidated competitors, that could negatively impact Diageo’s market

share, distribution network, costs and/or pricing;• Diageo’s ability to derive the expected benefits from its business strategies, including in relation to expansion in emerging markets, acquisitions and/or disposals, cost saving

and productivity initiatives or inventory forecasting; • contamination, counterfeiting or other circumstances which could harm the level of customer support for Diageo’s brands and adversely impact its sales; • increased costs for, or shortages of, talent, as well as labour strikes or disputes;• any disruption to production facilities, business service centres or information systems, including as a result of cyber-attacks; • fluctuations in exchange rates and/or interest rates, which may impact the value of transactions and assets denominated in other currencies, increase Diageo’s cost of

financing or otherwise adversely affect Diageo’s financial results;• movements in the value of the assets and liabilities related to Diageo’s pension plans;• Diageo’s ability to renew supply, distribution, manufacturing or licence agreements (or related rights) and licences on favourable terms, or at all, when they expire; or• any failure by Diageo to protect its intellectual property rights.

All oral and written forward-looking statements made on or after the date of this document and attributable to Diageo are expressly qualified in their entirety by the above risk factors and by the ‘Risk factors’ section contained in the annual report on Form 20-F for the year ended 30 June 2017 filed with the US Securities and Exchange Commission (SEC). Any forward-looking statements made by or on behalf of Diageo speak only as of the date they are made. Diageo does not undertake to update forward-looking statements to reflect any changes in Diageo's expectations with regard thereto or any changes in events, conditions or circumstances on which any such statement is based. The reader should, however, consult any additional disclosures that Diageo may make in any documents which it publishes and/or files with the SEC. All readers, wherever located, should take note of these disclosures.This document includes names of Diageo's products, which constitute trademarks or trade names which Diageo owns, or which others own and license to Diageo for use. All

rights reserved. © Diageo plc 2018.The information in this document does not constitute an offer to sell or an invitation to buy shares in Diageo plc or an invitation or inducement to engage in any other

investment activities.This document may include information about Diageo’s target debt rating. A security rating is not a recommendation to buy, sell or hold securities and may be subject to

revision or withdrawal at any time by the assigning rating organisation. Each rating should be evaluated independently of any other rating.Past performance cannot be relied upon as a guide to future performance. 53

CELEBRATING LIFE, EVERY DAY, EVERYWHERE

54