dial in for audio: 1-877-273-4202 access code: 9669134 taxes matter…renewing the opportunity for...

TRANSCRIPT

Dial in For Audio: 1-877-273-4202Access Code: 9669134

Taxes Matter…Renewing theOpportunity for Tax Free

Income Strategies

Revenue Generation Call #3 for 2013

Today’s Call

The opportunity for tax free accumulation

solutions

Detailed review of the 4 options

Client Profile

Talking points, introductions, objections

Keys to success

Today’s Call

Get the most out of today’s call!

On a clean sheet of paper

1. Clients

2. Your “to do”

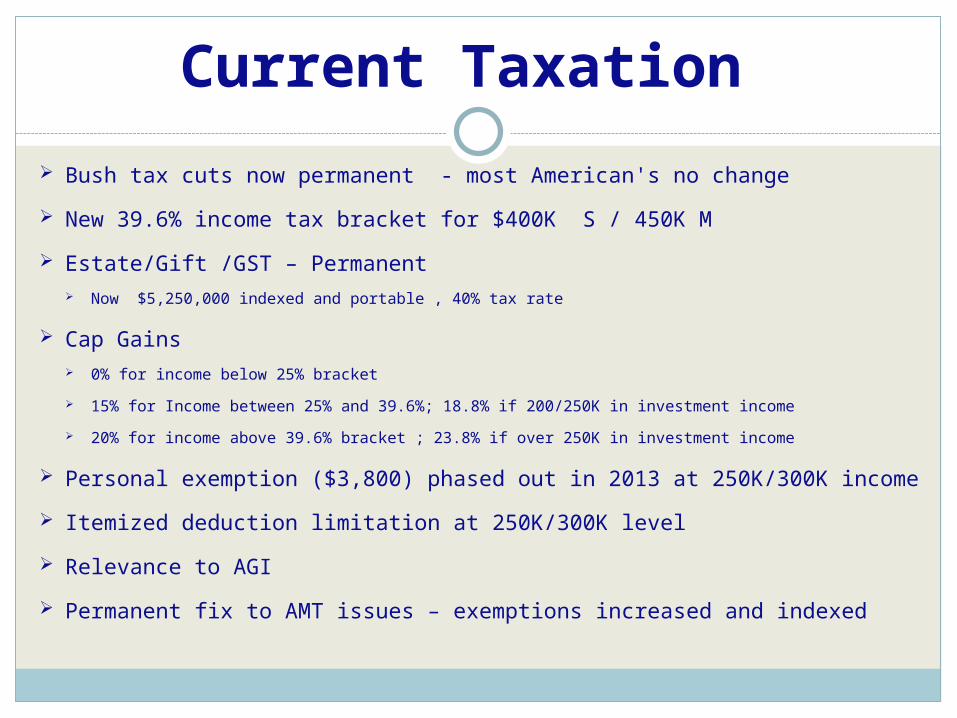

Bush tax cuts now permanent - most American's no change

New 39.6% income tax bracket for $400K S / 450K M

Estate/Gift /GST – Permanent Now $5,250,000 indexed and portable , 40% tax rate

Cap Gains 0% for income below 25% bracket

15% for Income between 25% and 39.6%; 18.8% if 200/250K in investment income

20% for income above 39.6% bracket ; 23.8% if over 250K in investment income

Personal exemption ($3,800) phased out in 2013 at 250K/300K income

Itemized deduction limitation at 250K/300K level

Relevance to AGI

Permanent fix to AMT issues – exemptions increased and indexed

Current Taxation

Remove tax uncertainty for portion of long term investment strategy

Tax deferred growth

Tax free distributions (walks like a Roth, talks like a Roth, call it life insurance)

Self completing accumulation in the event of death (and disability)

Greater flexibility in the future for death benefit planning

Asset protection in many states

Numerous investment strategy options

Why Insurance Accumulation Solutions

Remove tax uncertainty for portion of long term investment strategy

Tax deferred growth

Tax free distributions (walks like a Roth, talks like a Roth, call it life insurance)

Self completing accumulation in the event of death and disability

Greater flexibility in the future for death benefit planning

Asset protection in many states

Numerous investment strategy options

Best Long Term Financial Planning Vehicle

available to the affluent today – Bar none

Why Insurance Accumulation Solutions

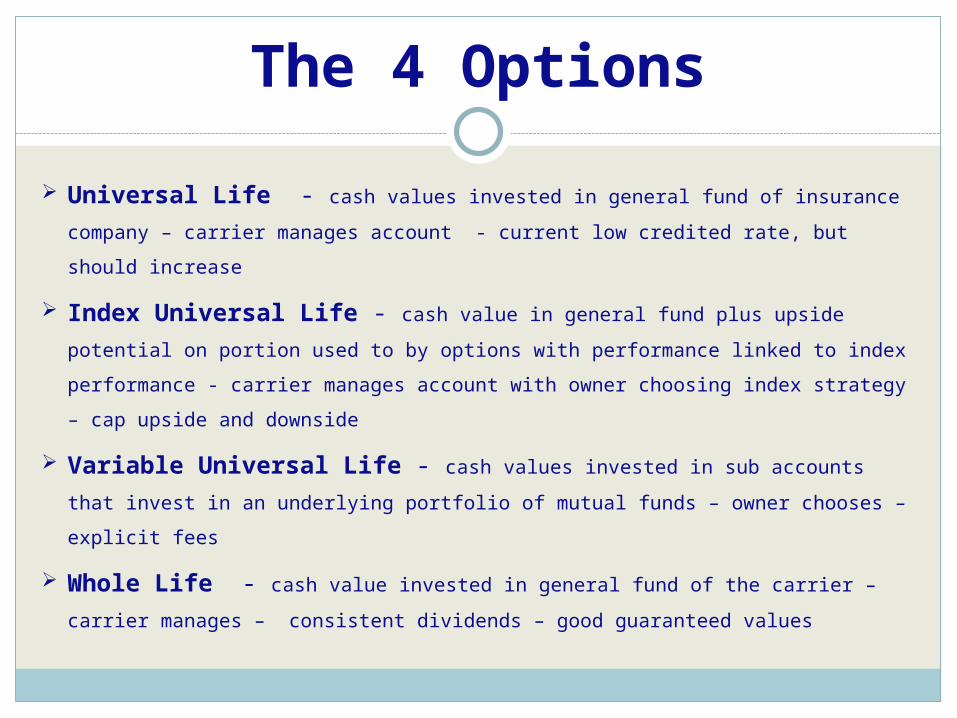

The 4 Options

Universal Life - cash values invested in general fund of insurance company –

carrier manages account - current low credited rate, but should increase

Index Universal Life - cash value in general fund plus upside potential on portion

used to by options with performance linked to index performance - carrier manages

account with owner choosing index strategy – cap upside and downside

Variable Universal Life - cash values invested in sub accounts that invest in an

underlying portfolio of mutual funds – owner chooses – explicit fees

Whole Life - cash value invested in general fund of the carrier – carrier manages –

consistent dividends – good guaranteed values

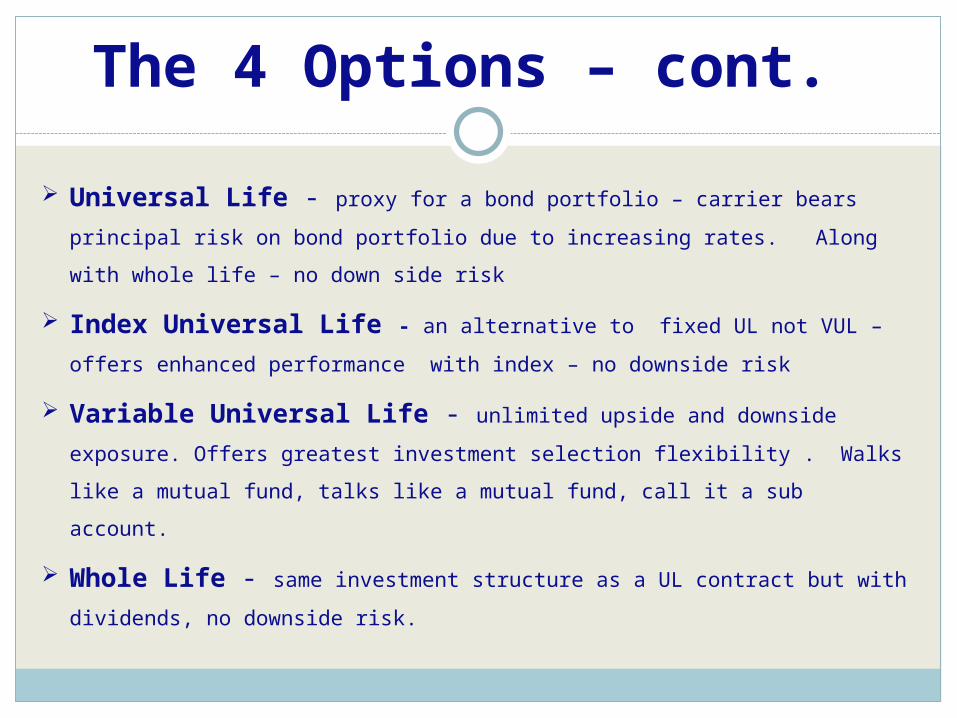

The 4 Options – cont.

Universal Life - proxy for a bond portfolio – carrier bears principal risk on bond

portfolio due to increasing rates. Along with whole life – no down side risk

Index Universal Life - an alternative to fixed UL not VUL – offers enhanced

performance with index – no downside risk

Variable Universal Life - unlimited upside and downside exposure. Offers

greatest investment selection flexibility . Walks like a mutual fund, talks like a mutual

fund, call it a sub account.

Whole Life - same investment structure as a UL contract but with dividends, no

downside risk.

The 4 Options – cont.

Product Flexibility

UL IUL VUL WL

Face Flexible Flexible Flexible Somewhat Flexible Premium Flexible Flexible Flexible No Flexibility

Premium timing Flexible Flexible Flexible No Flexibility

Investment choice None Somewhat Flexible Very Flexible None

CV Accessibility Flexible Flexible Flexible Somewhat Flexible

Loan Mechanism 0 Net 0 Net 0 Net Typical 2% + spread

Basis Tracking GAAP GAAP GAAP Call the carrier

Complexity Low Medium Low Medium

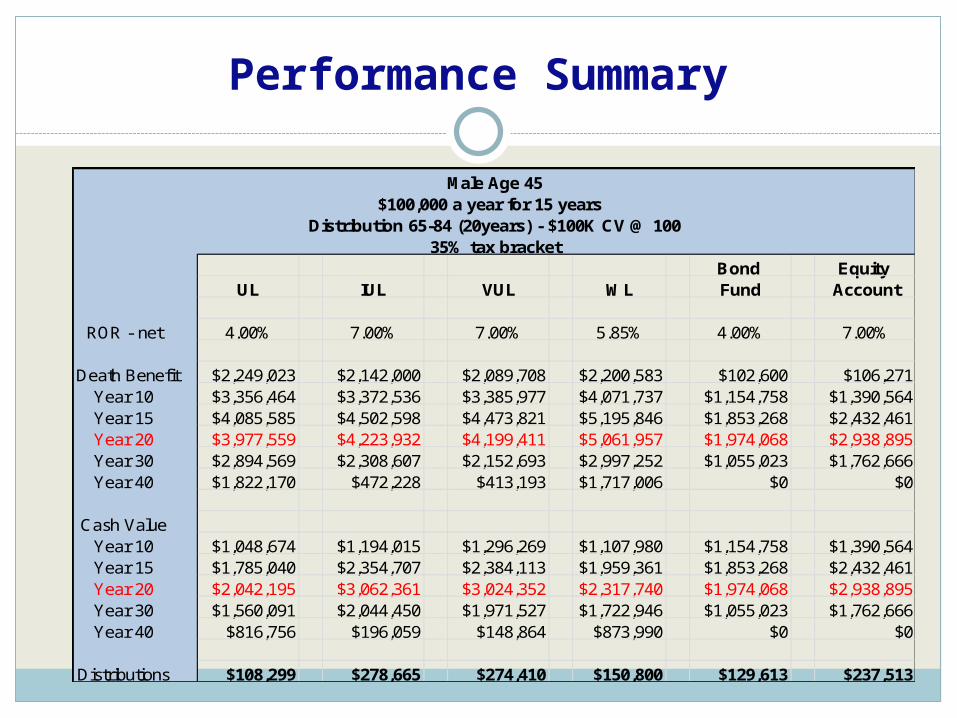

Performance Summary

Male Age 45$100,000 a year for 15 years

Distribution 65-84 (20years) - $100K CV @ 10035% tax bracket

Bond Equity UL IUL VUL WL Fund Account

ROR - net 4.00% 7.00% 7.00% 5.85% 4.00% 7.00%

Death Benefit $2,249,023 $2,142,000 $2,089,708 $2,200,583 $102,600 $106,271Year 10 $3,356,464 $3,372,536 $3,385,977 $4,071,737 $1,154,758 $1,390,564Year 15 $4,085,585 $4,502,598 $4,473,821 $5,195,846 $1,853,268 $2,432,461Year 20 $3,977,559 $4,223,932 $4,199,411 $5,061,957 $1,974,068 $2,938,895Year 30 $2,894,569 $2,308,607 $2,152,693 $2,997,252 $1,055,023 $1,762,666Year 40 $1,822,170 $472,228 $413,193 $1,717,006 $0 $0

Cash ValueYear 10 $1,048,674 $1,194,015 $1,296,269 $1,107,980 $1,154,758 $1,390,564Year 15 $1,785,040 $2,354,707 $2,384,113 $1,959,361 $1,853,268 $2,432,461Year 20 $2,042,195 $3,062,361 $3,024,352 $2,317,740 $1,974,068 $2,938,895Year 30 $1,560,091 $2,044,450 $1,971,527 $1,722,946 $1,055,023 $1,762,666Year 40 $816,756 $196,059 $148,864 $873,990 $0 $0

Distributions $108,299 $278,665 $274,410 $150,800 $129,613 $237,513

Strategies

1. Client asset and income diversification Alternative to after tax investing

Strategies

1. Client asset and income diversification Alternative to after tax investing

2. Executive Roth IRA/401K Look alike Fully discriminatory No funding limits No income phase outs Self fulfilling Asset protected in many states 162 Bonus / REBA Plan

Strategies

3. Spousal Access Trust Allows spouse of grantor access to policy cash values Death benefit outside of estate Spouse or children as trustee

Strategies

3. Spousal Access Trust Allows spouse of grantor access to policy cash values Death benefit outside of estate Spouse or children as trustee

4. Cross Endorsed Buy Sell Agreement funding Cross Purchase structure Individual owns and controls own cash value No back end taxable ownership transfers For business owners that are cash cows Two Birds – succession funding and supplemental retirement

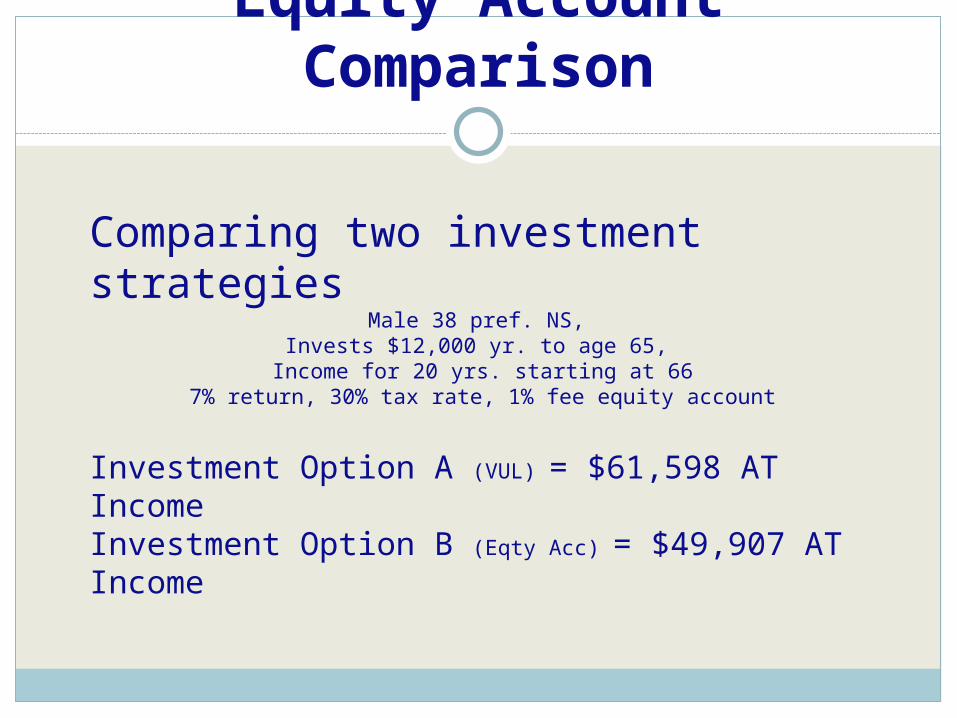

Equity Account Comparison

Comparing two investment strategiesMale 38 pref. NS,

Invests $12,000 yr. to age 65, Income for 20 yrs. starting at 66

7% return, 30% tax rate, 1% fee equity account

Investment Option A (VUL) = $61,598 AT IncomeInvestment Option B (Eqty Acc) = $49,907 AT Income

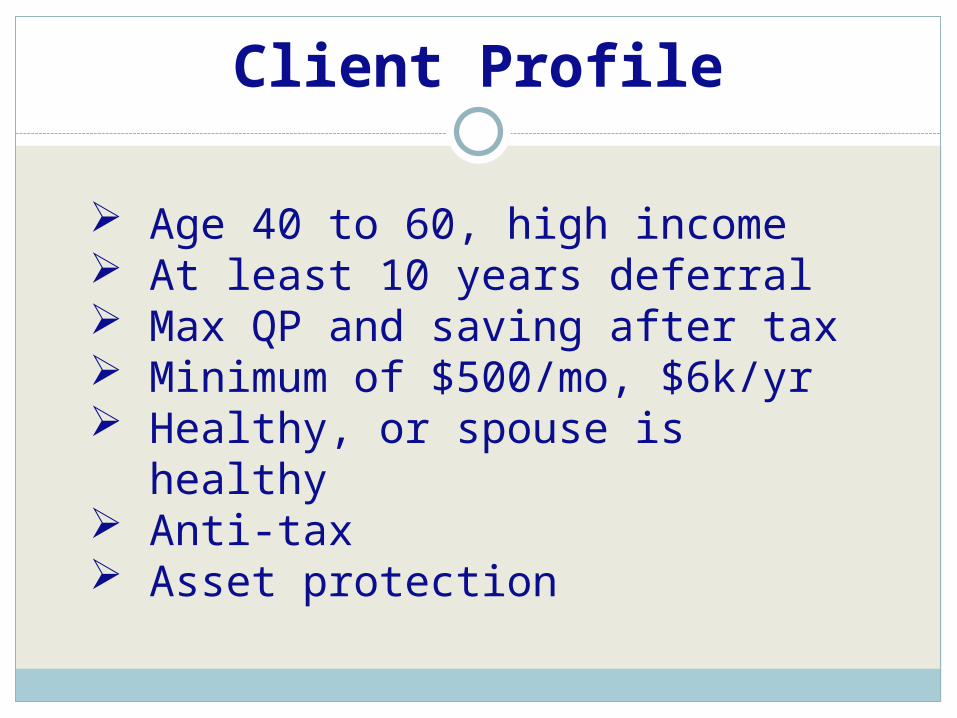

Client Profile

Age 40 to 60, high income At least 10 years deferral Max QP and saving after tax Minimum of $500/mo, $6k/yr Healthy, or spouse is healthy Anti-tax Asset protection

Client Profile cont.

Takes advice Open to new ideas Appreciates having a plan

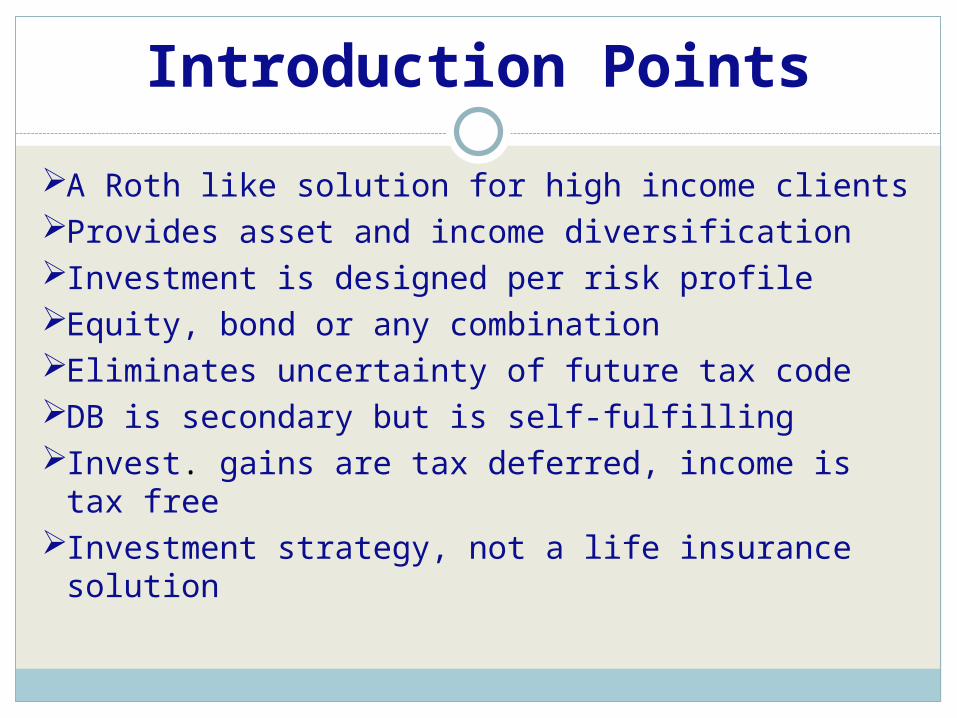

Introduction Points

A Roth like solution for high income clientsProvides asset and income diversificationInvestment is designed per risk profileEquity, bond or any combinationEliminates uncertainty of future tax codeDB is secondary but is self-fulfillingInvest. gains are tax deferred, income is tax freeInvestment strategy, not a life insurance solution

Introduction Conversation

John, I know how you feel about taxes, and of course the recent tax changes just made your load a little heavier. With that in mind I want to briefly share an investment strategy with you that generates tax free income. With this plan your current investment gains are tax deferred, and when it is time for income, you receive that totally tax free. It is similar to the popular ROTH IRA, but because of your income you do not qualify for a ROTH. This solution is ideally suited to high income clients like you, and particularly those now paying a 3% surtax on investment income. I think it is something you will find of value and I would like to review this with you in person. What is the best day this week or next to visit for an hour?

Client Objection

I have always heard that mixing investing and life insurance doesn’t work. Why not just do term and invest the difference?

Response: I understand and I know there are some who are not advocates of this strategy. Two points- first, I am not recommending this as part of your life insurance protection, I don’t believe you need any more life insurance. And second, I am more concerned about the results and not so much how a solution is packaged. And what I mean by that is, for any solution I recommend for you, I focus primarily on what it does, not so much on what it is. What this “does” is provide confidence that you will have tax free income in retirement. How do you feel about tax free income?

Key Factors to Success

You gotta believe Connect to the value, what it does is more important than what it is.

Key Factors to Success

You gotta believe Connect to the value, what it does is more important than what it is.

Understand what is most important to your client Taxes, flexibility, guarantees, risk profile

Key Factors to Success

You gotta believe Connect to the value, what it does is more important than what it is.

Understand what is most important to your client Taxes, flexibility, guarantees, risk profile

Preparation Work with your Relationship Manager

Next Steps

Client List

Contact your Relationship Manager

No RM? Call CORE Case Design800-991-6695

Questions

www.coregroupusa.com

Questions