providing certainty for your clients’ income needs dial in for audio: 1-877-273-4202 access code:...

TRANSCRIPT

Providing Certainty for Your Clients’ Income Needs

Dial in For Audio: 1-877-273-4202Access Code: 9669134

Identifying the Best Income Riders Available Today

What We Will Accomplish

• Open your awareness about income riders

• Compare the marketplace to identify what are

the best options available

• Review details of the best options

• Share discovery dialogue that works

• Answer your questions

Make the Next 45 Minutes Beneficial

Two Lists

Information without action is like buying a present you never give!

• People to call

• Tasks to do

Be Open-Minded

When presented new information …

how do we come to a conclusion?

Have you ever thought about how you

are thinking?

Don’t allow assumptions to go

unchecked – confirm and verify

What Once Was

Significant changes in the VA space over the

last 5 years?

• Higher fees

• Reduced benefits

• More restrictions on investments

• Fewer carriers

• Lower withdrawal percentages

• No more joint income

What is Now

Significant changes in the Equity Index

Annuity space over the last 5 years

• Income riders are the same or better than VAs offer

• 5% & 6% compounded roll ups

• 7% & 8% simple roll ups

• Income withdrawal percentages from 5% to 6.25%

• Nursing home income enhancements (state specific)

• Joint income available

Paradigm Shift

Here is my story • Allowed incorrect assumptions to draw conclusions

• Income riders comparable• Caps are low so that means that the VA will win out

over time and produce more income later• The spread between VA performance and the EIA

cap is too wide• Conclusion – for future income VAs are better than

EIAs• Put EIAs in a box – clients who wants certainty about

future income and cannot deal with volatility• Case study to do the math and learn what works best.

Director of Annuity Marketing

Over 20 years experience

MBA, FLMI and CRPS

Varied experience … home office,

advanced support and personal

production

Jamie Farmer

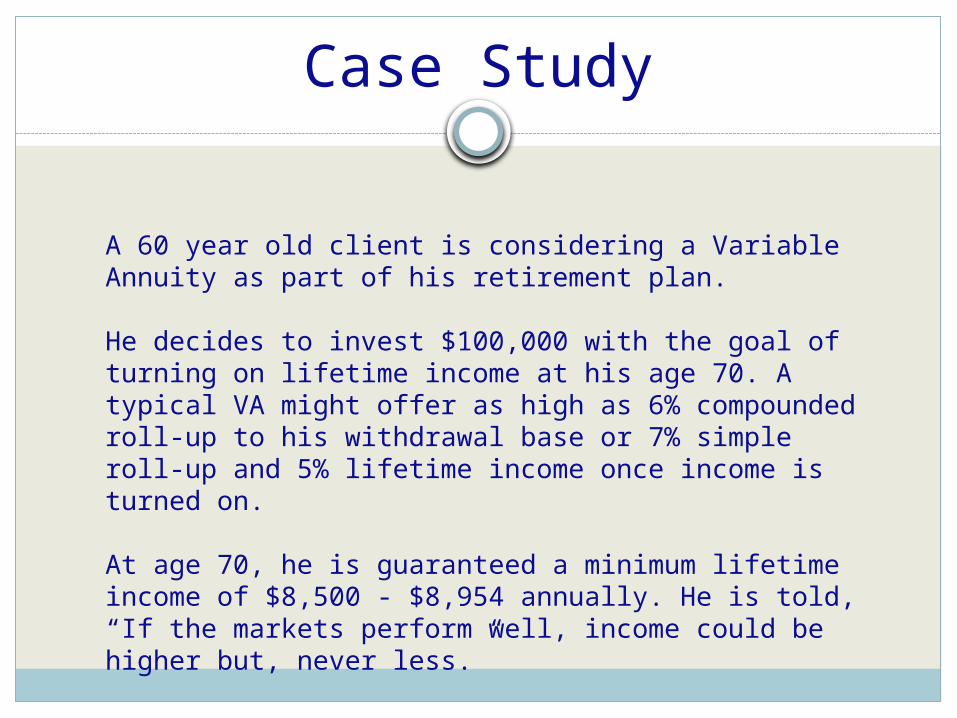

Case Study

A 60 year old client is considering a Variable Annuity as part of his retirement plan.

He decides to invest $100,000 with the goal of turning on lifetime income at his age 70. A typical VA might offer as high as 6% compounded roll-up to his withdrawal base or 7% simple roll-up and 5% lifetime income once income is turned on.

At age 70, he is guaranteed a minimum lifetime income of $8,500 - $8,954 annually. He is told, “If the markets perform well, income could be higher but, never less.”

The EIA Alternative

An alternative to consider is an EIA. The income benefits guaranteed under an EIA usually beat the guarantees offered under a VA.

A typical EIA offers a similar 5% compound roll-up to his withdrawal base or as high as 8% compound but, guaranteed income percentages are generally much higher, ranging from 5.50% - 6.25%.

At age 70, if using an EIA, he is guaranteed a minimum lifetime income of $8,954 - $11,000.

The income guaranteed under an EIA can be as much as 22% higher than the VA!

Under Guarantees - Which is More?

VA = $8,954

EIA = $11,000

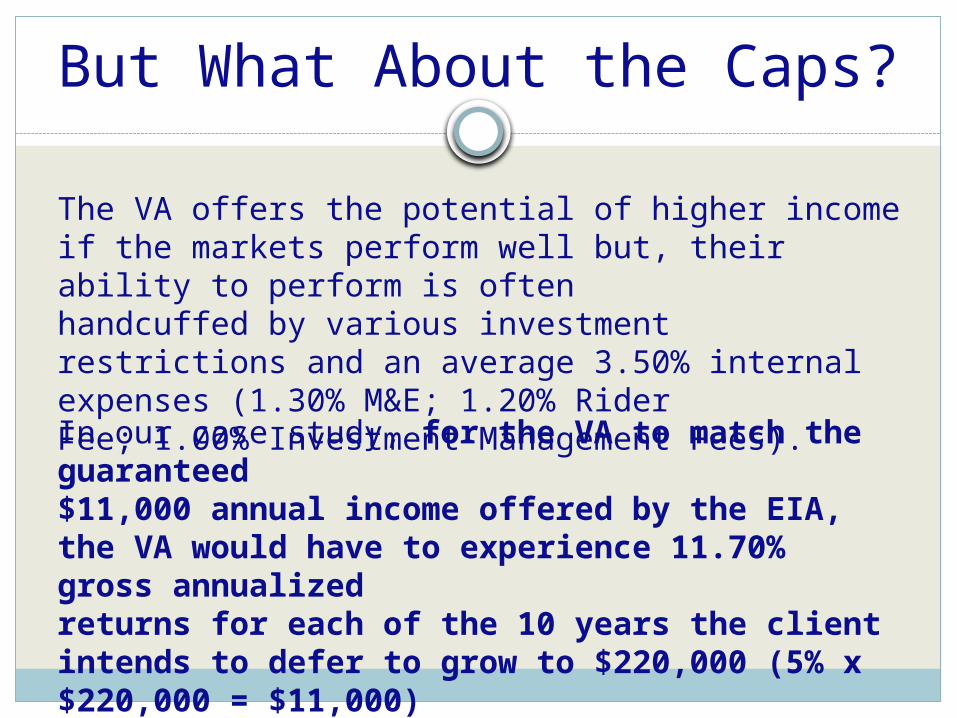

But What About the Caps?

The VA offers the potential of higher income if the markets perform well but, their ability to perform is oftenhandcuffed by various investment restrictions and an average 3.50% internal expenses (1.30% M&E; 1.20% RiderFee; 1.00% Investment Management Fees).

In our case study, for the VA to match the guaranteed$11,000 annual income offered by the EIA, the VA would have to experience 11.70% gross annualizedreturns for each of the 10 years the client intends to defer to grow to $220,000 (5% x $220,000 = $11,000)

Summarize

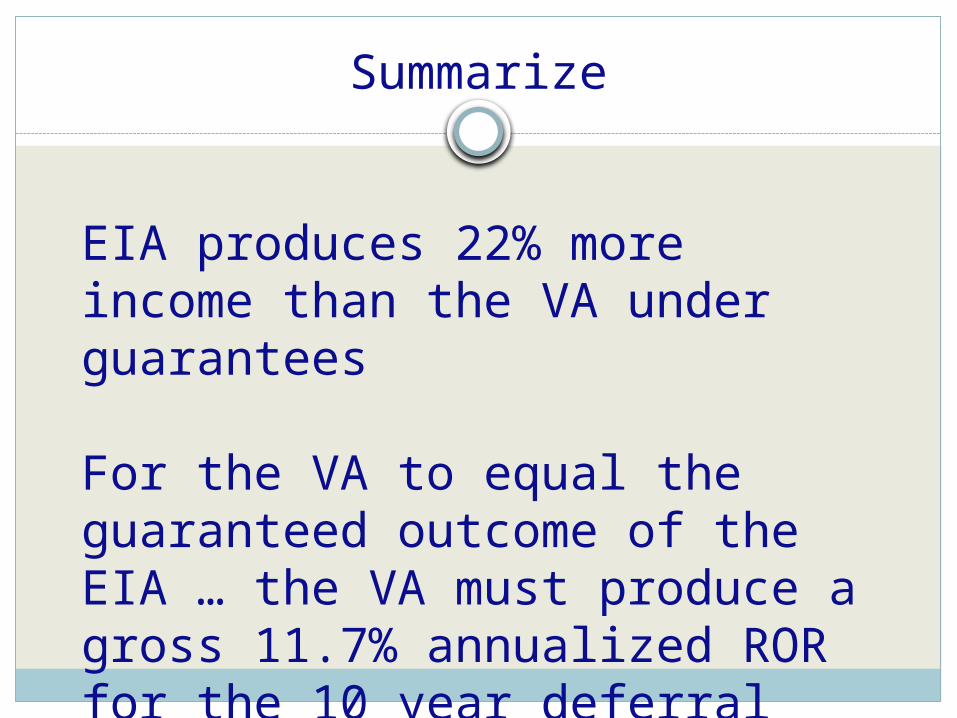

EIA produces 22% more income than the VA under guarantees

For the VA to equal the guaranteed outcome of the EIA … the VA must produce a gross 11.7% annualized ROR for the 10 year deferral

EIA Options to Consider

Income Begins Age 70 Carrier/Product

Premium Bonus Roll-up %

Withdrawal Base with 10 Years Deferral

Single Life Income Percentage Annual Income Nursing Home

Allianz MasterDex X 5.00% 6% Simple $165,000 5.50% $9,075 N/A

American General Choice Index 10 4.00% 7% Simple $200,000 5.50% $11,000 N/A

AVIVA Income Select 6 & 10 0.00% 6% Compound $179,084 5.25% $9,401 $18,802

Genworth SecureLiving 7 & 10 *0.00% 8% Simple $180,000 5.50% $9,900 N/A

ING Secure Index 5 & 7 0.00% 6% Compound $179,084 5.00% $8,954 N/A

ING Secure Index Opportunities Plus 5.00% 6% Compound $188,039 5.00% $9,402 N/A

Lincoln ND 6 & 8 ; OptiChoice 5, 7 & 9 0.00% 5% Compound $162,889 6.25% $10,181 $16,289

Lincoln Opti Point 10 4.00% 5% Compound $169,405 5.85% $9,910 $16,940

Lincoln Opti Point 8 3.00% 5% Compound $167,776 5.85% $9,815 $16,777

North American 0.00% 6.50% Compound $187,714 5.25% $9,855 N/A

Additional Points & EIA Benefits

• VAs still have a place – not to be an argument against • Limited investment options make hurdle harder

• We filter the products to meet your broker dealer’s requirements (10/10/10 guidelines)

• Still must be compliance approved• Caps are moving up … Genworth is approaching 6%• Income now – 5% and more – even for joint life• Seeing more “split” cases• Can’t deny the math – your competition knows about

this• EIA offers ROP• Share the story with clients allow them to choose• A way to lower beta in an AUM portfolio due to ROP

feature and guaranteed future income

What to Ask?

When you think about the income you will be wanting in the future … how much would you like to have guaranteed?

How would you feel if we could smooth out the ups and downs of your portfolio and provide you more certainty about your future income?

How to Access Our Support?

Next Steps

•Call your CORE RM

•Review Lists

•People to call

•Tasks to do

C.O.R.E. is an Independent Marketing Organization distributing life

insurance, annuity, long term care & disability solutions for the independent financial advisor.

We align with you to reduce complexity, optimize outcomes,

enhance relationships, increase profitability and create certainty

for you and your clients.

Who We Are

We are your risk management solutions team

Thank you!

We create certainty through alignment