digital workshop australia | buchan

DESCRIPTION

1) Digital Media Landscape 2) Digital Media Opportunities 3) Digital Media 6-Step WorkflowTRANSCRIPT

1

Digital Workshop.

Presented to: Buchan – A Wagner Edstrom Partner

Presented by: Damus Chu (on behalf of Pug Life Advertising & IMC Digital)

Presented on: Monday, 26th May 2014

2

Agenda.Digital Media Landscape.

Digital Media Opportunities.

Digital Work-flow.

Question & Answers.

3

Introduction.Living and breathing digital advertising.

4

Past Workshop Feedback.Damus presented the Digital Workshop at the Melbourne SEO Meetup, and it was very well received by a crowd of seasoned SEO professionals. Needless to say,

Damus is well connected with the information that really matters in the digital advertising field, and he conveyed some really astounding data and information to us. The audience was really engaged with his presentation and I

personally consider it to be very important information for business people to take on-board. I highly recommend anyone considering to engage with Damus to do so, and consider it an important opportunity with a highly skilled and talented professional. - Peter Mead - WordPress SEO Consultant

An enjoyable and informative workshop. Excellent coverage of the very fast-moving digital landscape. Chris Burgess – Web & Technology Enthusiasthttp://chrisburgess.com.au/, http://www.linkedin.com/in/chrisburgesscomau

5www.facebook.com/DigitalWorkshopAustralia

Sign-in to Facebook.

6www.surveymonkey.com/s/V6JH8S8

Please Leave Your Feedback.

Or use our FB App

7

Damus | Pug Life Ad Solutions.

Managed over +$20m of advertising investment.

8

Joel | IMC Digital.

Digital Strategy, Social Listening, SEM and Video expert.

9

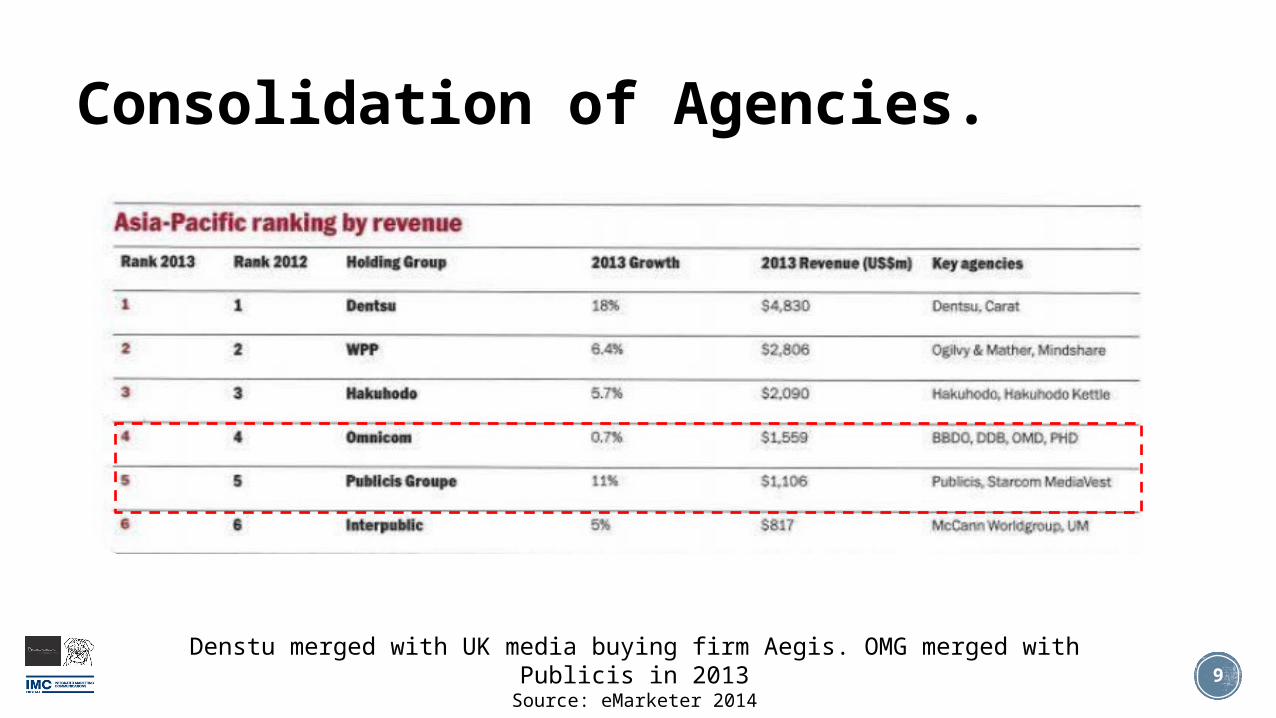

Consolidation of Agencies.

Denstu merged with UK media buying firm Aegis. OMG merged with Publicis in 2013

Source: eMarketer 2014

10

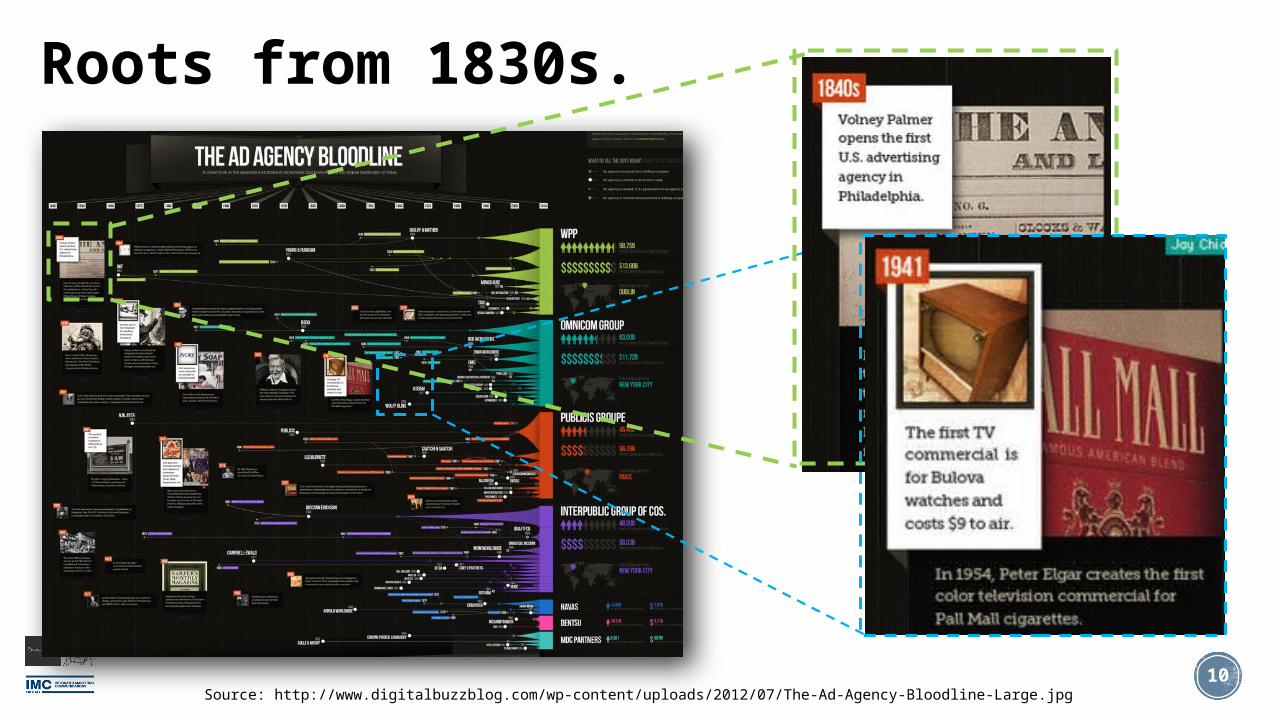

Roots from 1830s.

Source: http://www.digitalbuzzblog.com/wp-content/uploads/2012/07/The-Ad-Agency-Bloodline-Large.jpg

11

Digital Landscape.

Word on Desktop, Video, Mobile & Social.

12

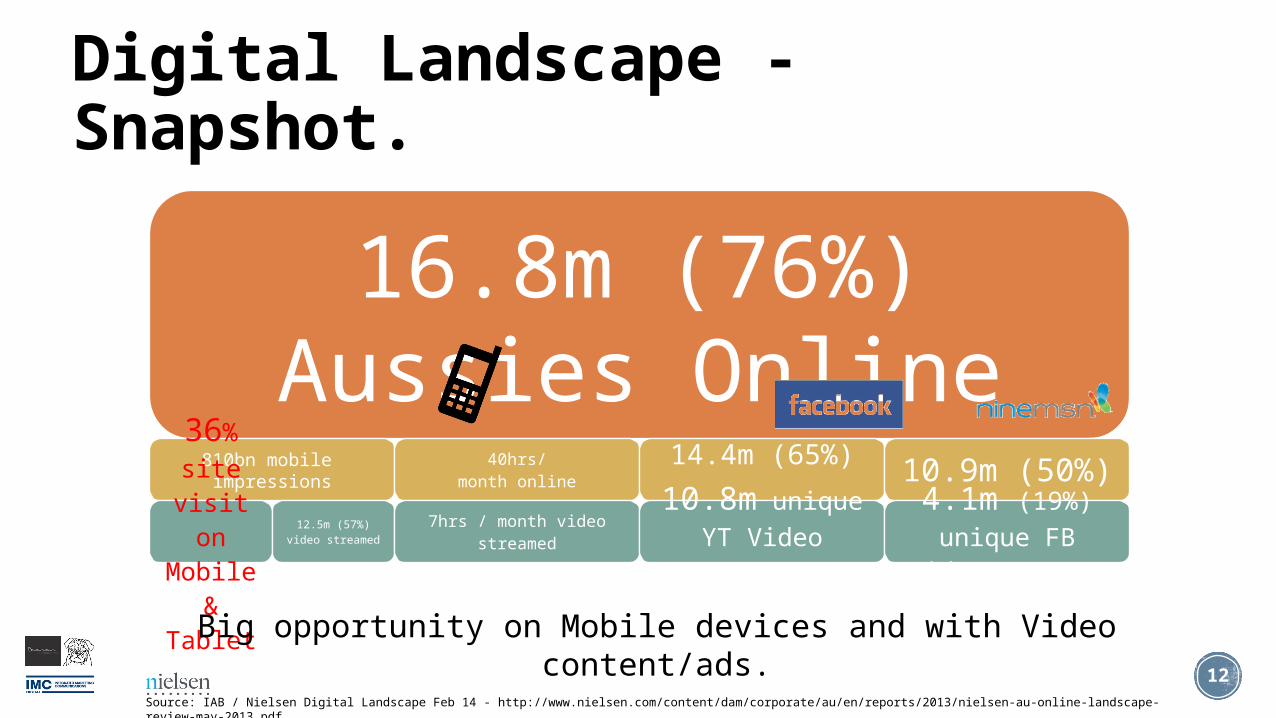

Digital Landscape - Snapshot.

16.8m (76%) Aussies Online

810bn mobile impressions

36% site

visit on Mobile

& Tablet

12.5m (57%) video

streamed

40hrs/month online

7hrs / month video streamed

14.4m (65%)

10.8m unique YT Video streams

10.9m (50%)4.1m (19%)

unique FB Video streams

Big opportunity on Mobile devices and with Video content/ads.

Source: IAB / Nielsen Digital Landscape Feb 14 - http://www.nielsen.com/content/dam/corporate/au/en/reports/2013/nielsen-au-online-landscape-review-may-2013.pdf

13

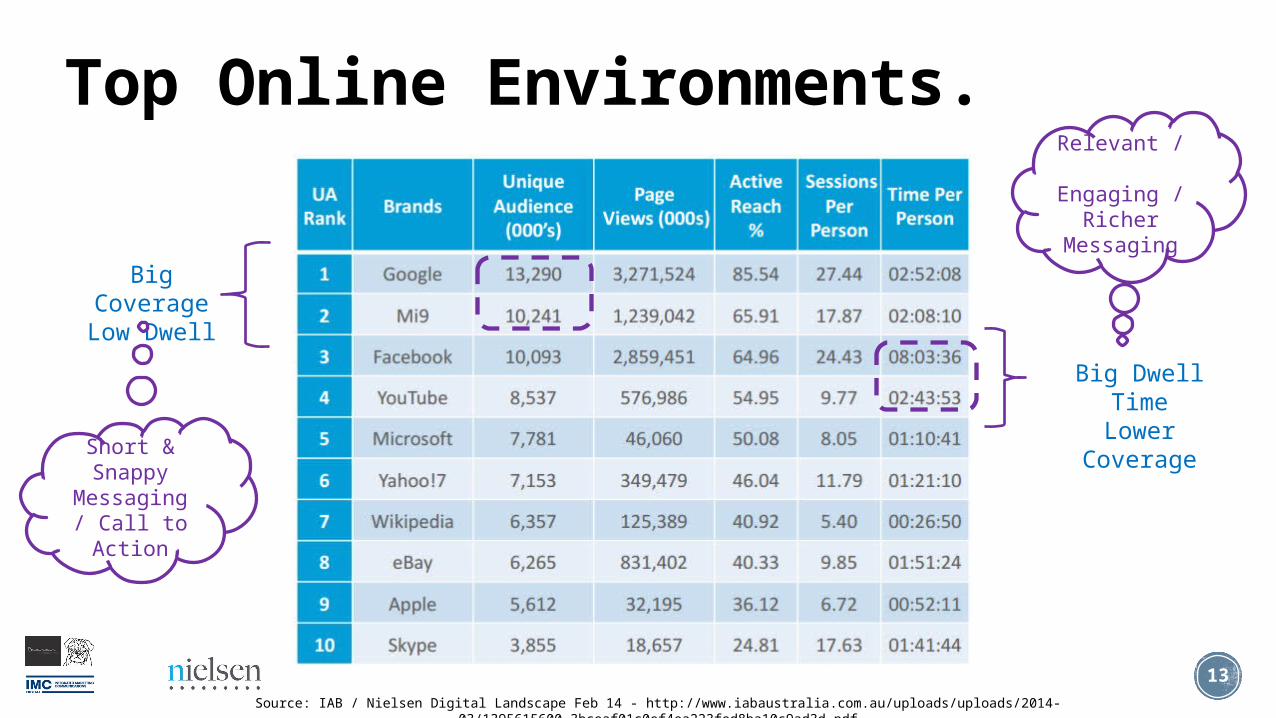

Top Online Environments.

Big CoverageLow Dwell

Big Dwell TimeLower

Coverage

Source: IAB / Nielsen Digital Landscape Feb 14 - http://www.iabaustralia.com.au/uploads/uploads/2014-03/1395615600_3bceaf01c0ef4ea223fed8ba10c9ad3d.pdf

Short & Snappy

Messaging / Call to Action

Relevant / Engaging /

Richer Messaging

14

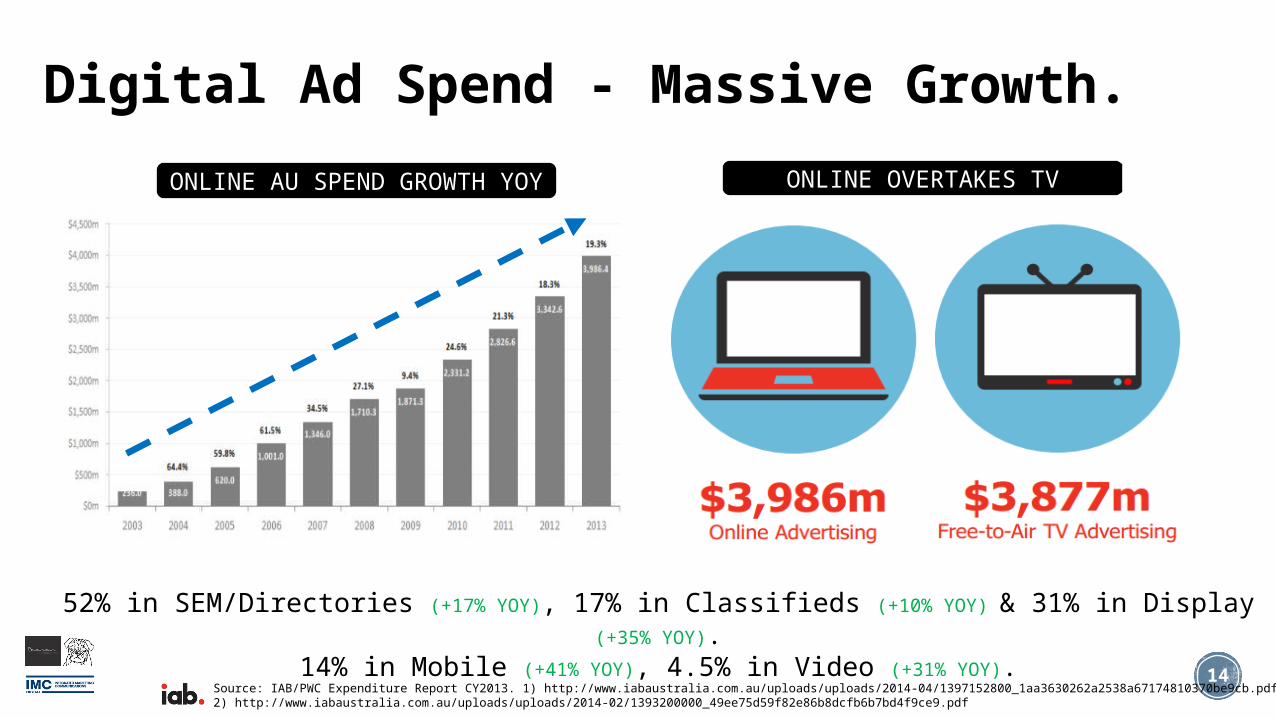

Digital Ad Spend - Massive Growth.

Source: IAB/PWC Expenditure Report CY2013. 1) http://www.iabaustralia.com.au/uploads/uploads/2014-04/1397152800_1aa3630262a2538a67174810370be9cb.pdf2) http://www.iabaustralia.com.au/uploads/uploads/2014-02/1393200000_49ee75d59f82e86b8dcfb6b7bd4f9ce9.pdf

52% in SEM/Directories (+17% YOY), 17% in Classifieds (+10% YOY) & 31% in Display (+35% YOY).14% in Mobile (+41% YOY), 4.5% in Video (+31% YOY).

ONLINE AU SPEND GROWTH YOY

ONLINE OVERTAKES TV

15

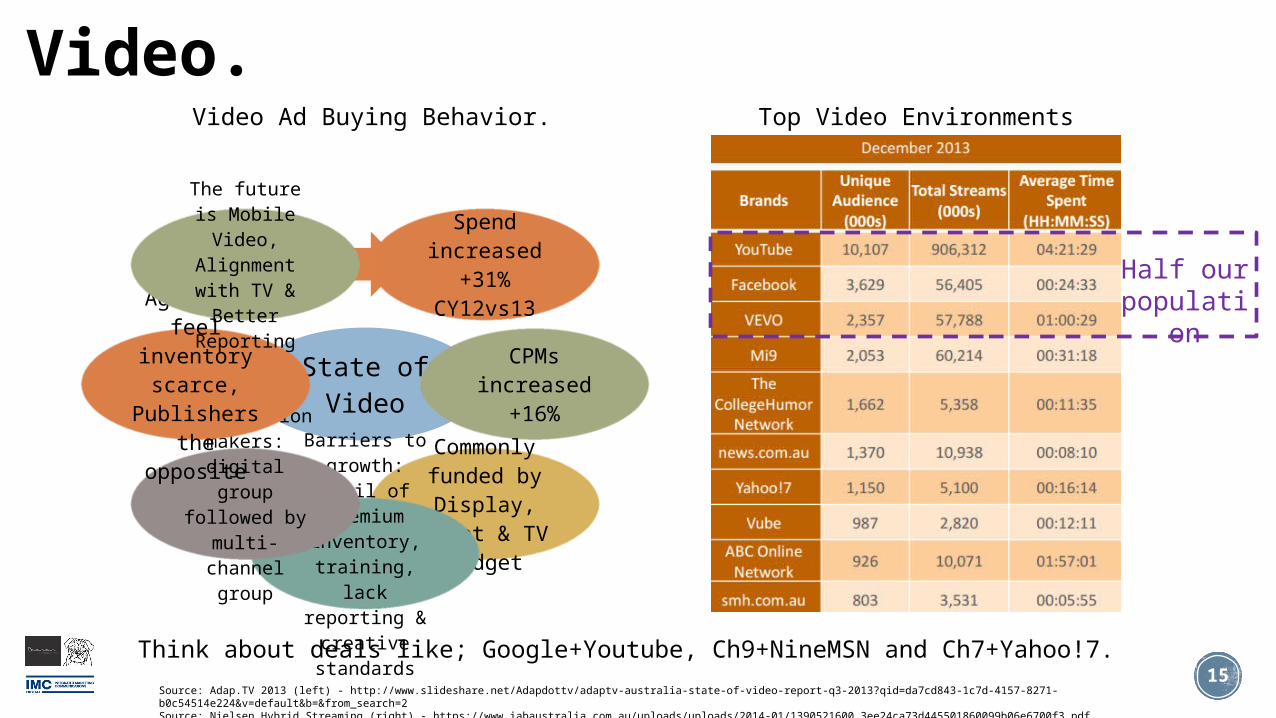

State of Video

Spend increased

+31% CY12vs13

CPMs increased

+16%

Commonly funded by

Display, Print & TV budget

Barriers to growth: avail of premium inventory,

training, lack reporting &

creative standards

Key decision makers: digital group followed

by multi-channel group

Agencies feel inventory scarce,

Publishers the opposite

The future is Mobile Video,

Alignment with TV & Better Reporting

Video.

Source: Adap.TV 2013 (left) - http://www.slideshare.net/Adapdottv/adaptv-australia-state-of-video-report-q3-2013?qid=da7cd843-1c7d-4157-8271-b0c54514e224&v=default&b=&from_search=2Source: Nielsen Hybrid Streaming (right) - https://www.iabaustralia.com.au/uploads/uploads/2014-01/1390521600_3ee24ca73d445501860099b06e6700f3.pdf

Video Ad Buying Behavior. Top Video Environments

Half our populatio

n

Think about deals like; Google+Youtube, Ch9+NineMSN and Ch7+Yahoo!7.

16

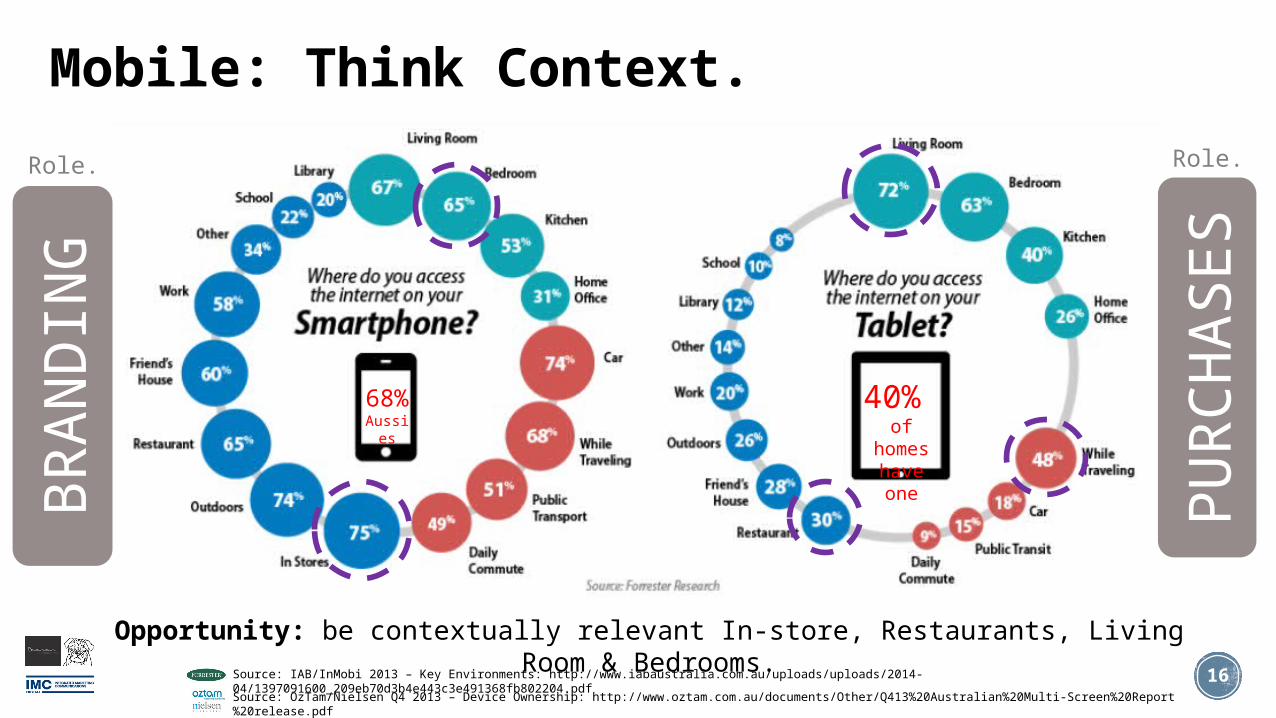

Mobile: Think Context.

Source: IAB/InMobi 2013 – Key Environments: http://www.iabaustralia.com.au/uploads/uploads/2014-04/1397091600_209eb70d3b4e443c3e491368fb802204.pdf

Opportunity: be contextually relevant In-store, Restaurants, Living Room & Bedrooms.

BR

AN

DIN

G

PU

RC

HA

SE

S

Source: OzTam/Nielsen Q4 2013 – Device Ownership: http://www.oztam.com.au/documents/Other/Q413%20Australian%20Multi-Screen%20Report%20release.pdf

40% of

homes have one

68%

Aussies

Role. Role.

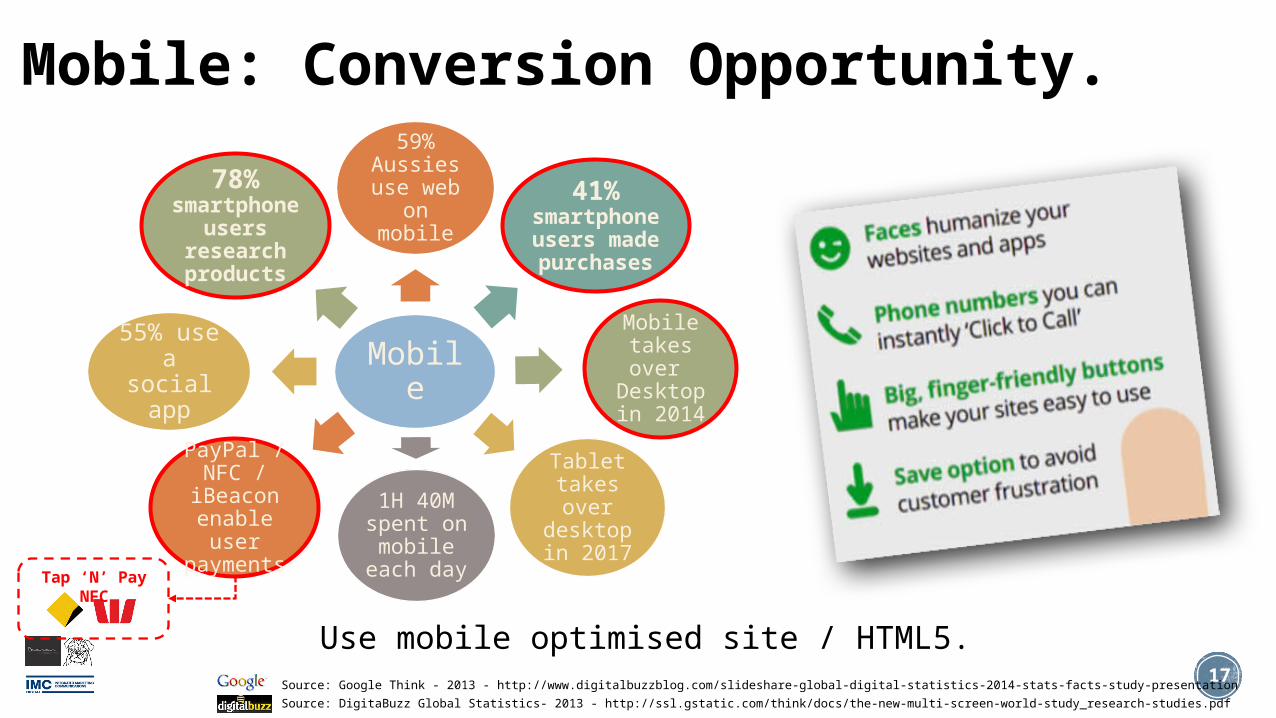

Mobile: Conversion Opportunity.

17

Mobile

59% Aussies use web

on mobile

78% smartphone users research products

55% use a social

app

41% smartphone users

made purchases

1H 40M spent on mobile

each day

PayPal / NFC /

iBeacon enable user

payments

Mobile takes over

Desktop in 2014

Tablet takes over

desktop in 2017

Use mobile optimised site / HTML5.

Tap ‘N’ Pay NFC

Source: Google Think - 2013 - http://www.digitalbuzzblog.com/slideshare-global-digital-statistics-2014-stats-facts-study-presentation

Source: DigitaBuzz Global Statistics- 2013 - http://ssl.gstatic.com/think/docs/the-new-multi-screen-world-study_research-studies.pdf

18

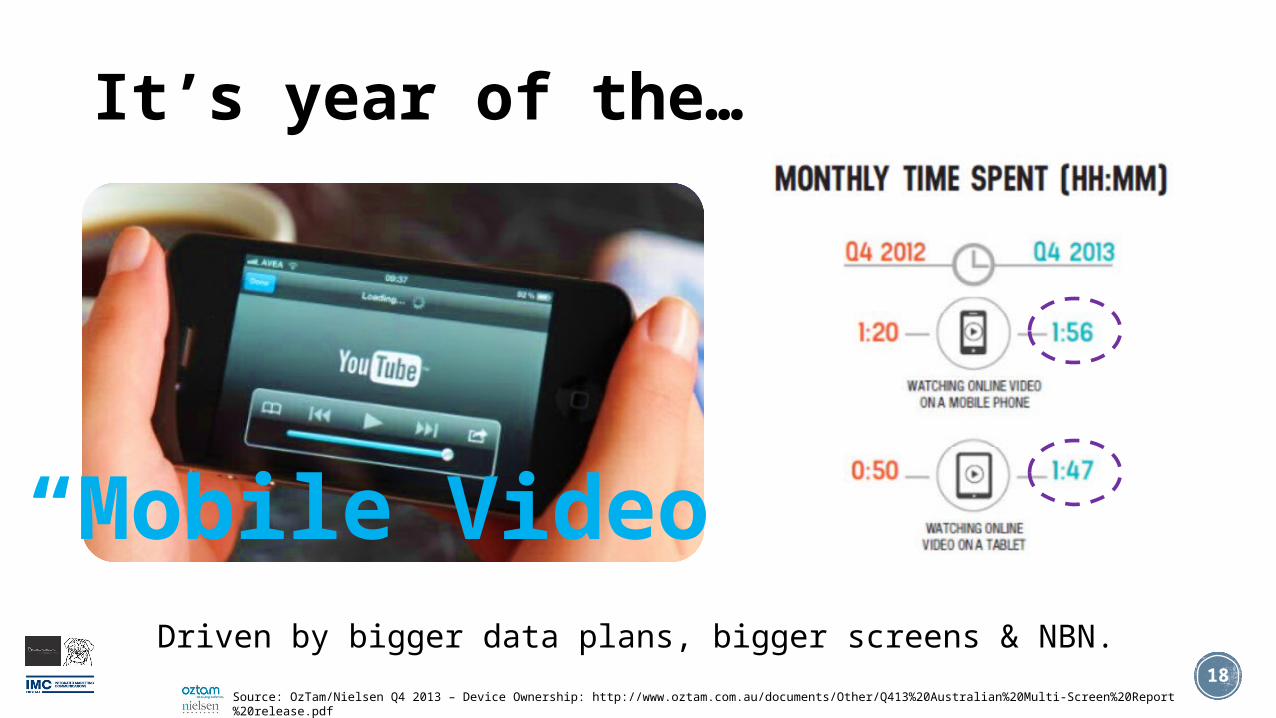

It’s year of the…

Driven by bigger data plans, bigger screens & NBN.

“Mobile Video”

Source: OzTam/Nielsen Q4 2013 – Device Ownership: http://www.oztam.com.au/documents/Other/Q413%20Australian%20Multi-Screen%20Report%20release.pdf

19

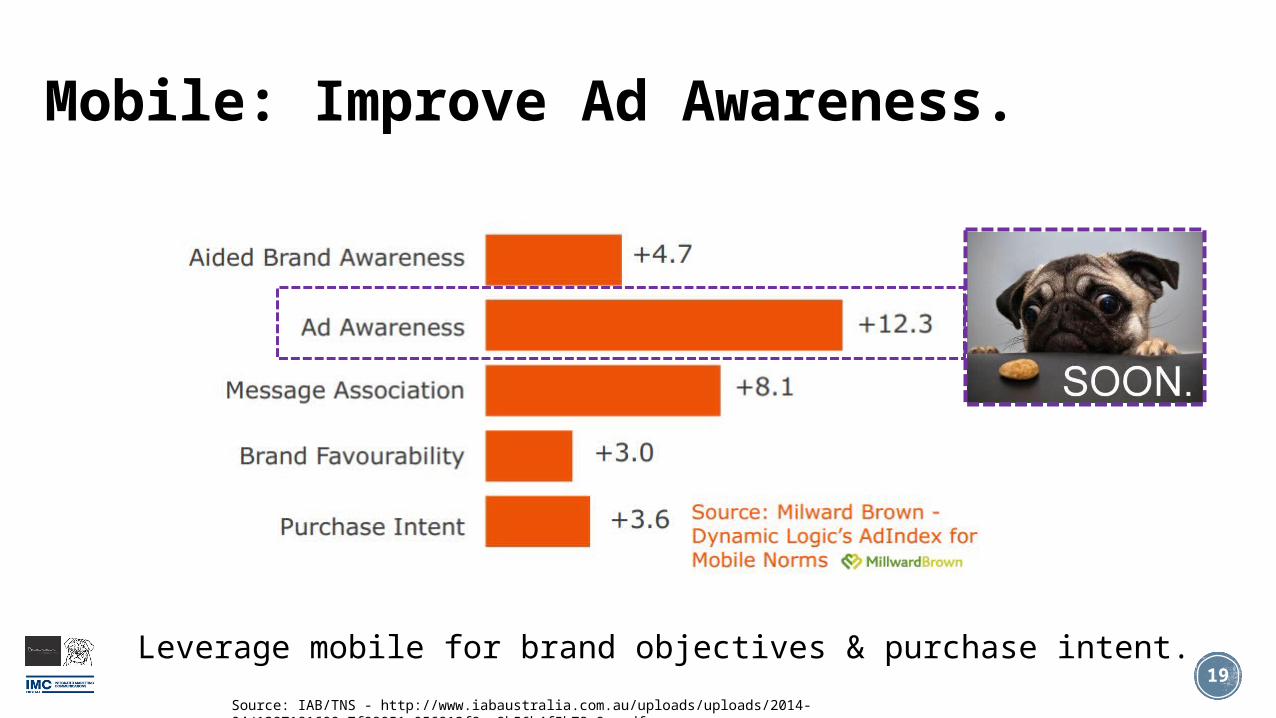

Mobile: Improve Ad Awareness.

Source: IAB/TNS - http://www.iabaustralia.com.au/uploads/uploads/2014-04/1397181600_7f99051e056812f8ca8b56b4f5b78a9c.pdf

Leverage mobile for brand objectives & purchase intent.

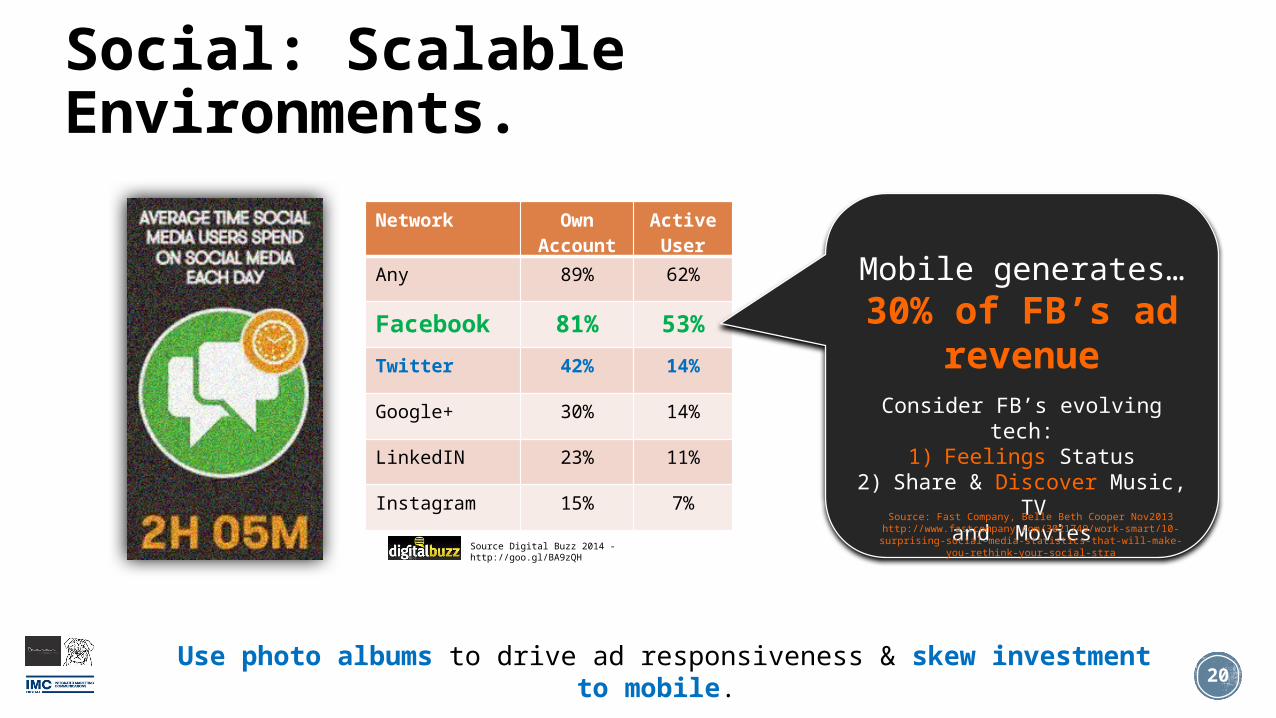

20Use photo albums to drive ad responsiveness & skew investment to

mobile.

Network Own Account

Active User

Any 89% 62%

Facebook 81% 53%

Twitter 42% 14%

Google+ 30% 14%

LinkedIN 23% 11%

Instagram 15% 7%

Source Digital Buzz 2014 - http://goo.gl/BA9zQH

Social: Scalable Environments.

Mobile generates… 30% of FB’s ad

revenueConsider FB’s evolving tech:

1) Feelings Status2) Share & Discover Music, TV

and MoviesSource: Fast Company, Belle Beth Cooper Nov2013

http://www.fastcompany.com/3021749/work-smart/10-surprising-social-media-statistics-that-will-make-you-

rethink-your-social-stra

21

Reasons for digital advertising.

Why businesses should invest in digital presence?

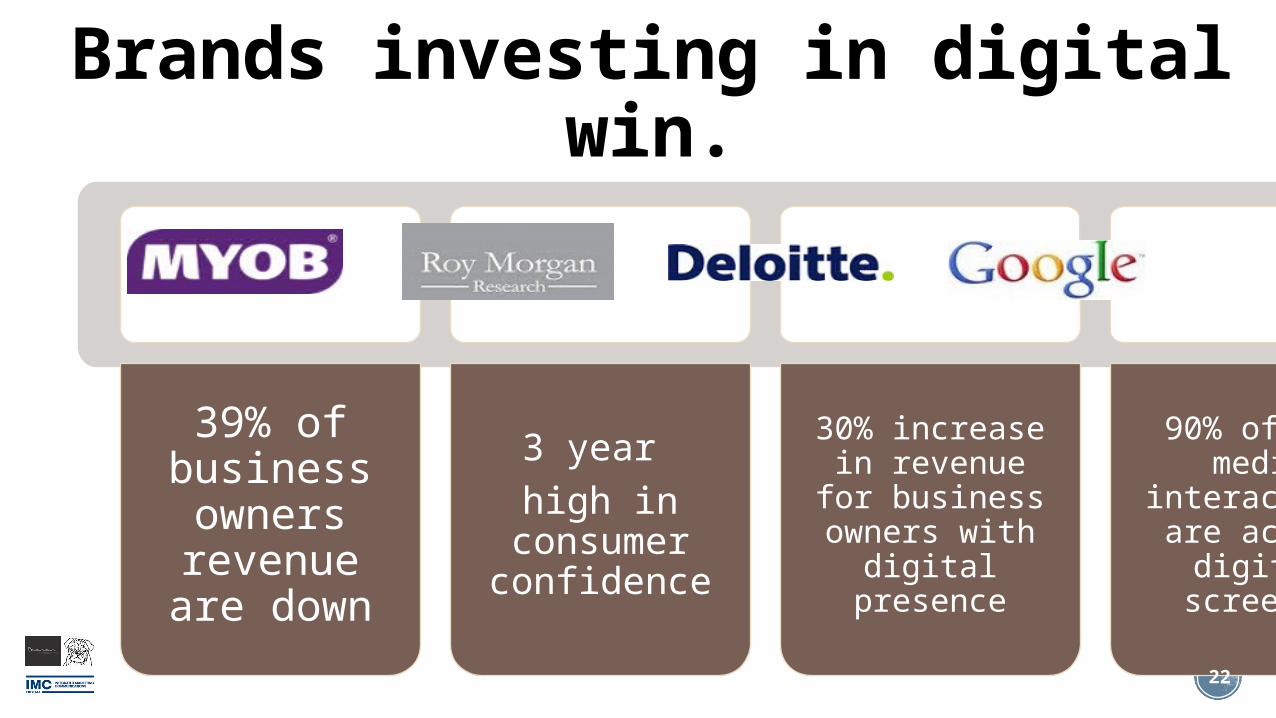

Brands investing in digital win.

39% of business owners revenue are down

3 year high in

consumer confidence

30% increase in revenue for

business owners with

digital presence

90% of all media

interactions are across

digital screens.

22

23

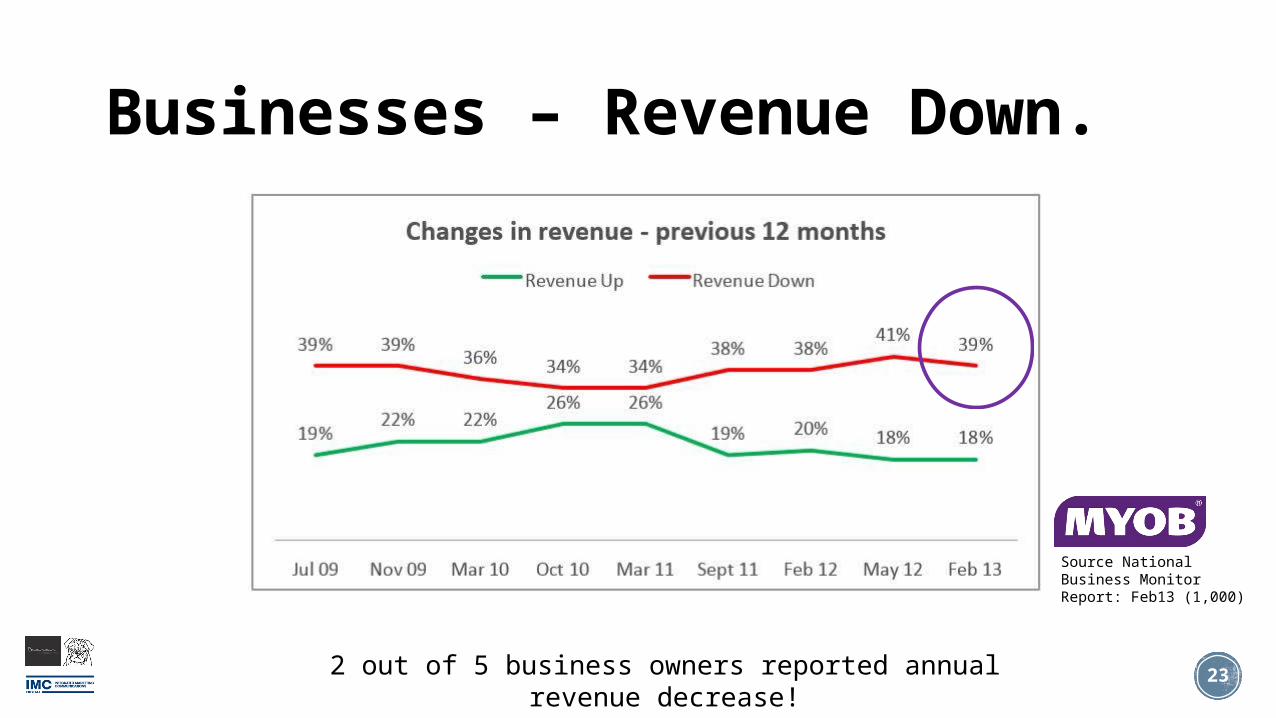

Businesses – Revenue Down.

2 out of 5 business owners reported annual revenue decrease!

Source National Business Monitor Report: Feb13 (1,000)

24

Consumers – Confidence Up.

Source: Roy Morgan - Consumer Confidence Report: Oct13 (53k) http://www.roymorgan.com/~/media/Files/Findings%20PDF/2013/October/5240-Aust-CC-October-15.pdf

25

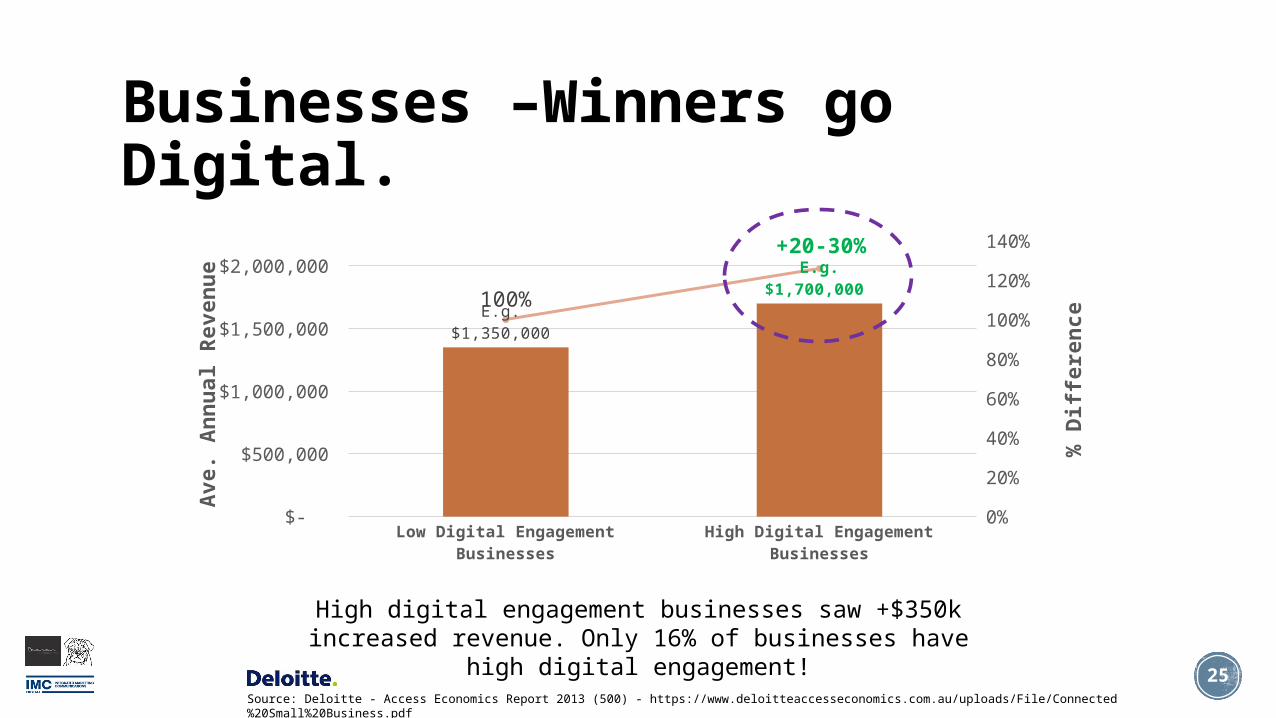

Businesses –Winners go Digital.

Low Digital Engagement Businesses

High Digital Engagement Businesses

$-

$500,000

$1,000,000

$1,500,000

$2,000,000

0%

20%

40%

60%

80%

100%

120%

140%

E.g. $1,350,000

E.g. $1,700,000 100%

+20-30%

Ave.

An

nu

al R

even

ue

% D

iffere

nce

High digital engagement businesses saw +$350k increased revenue. Only 16% of businesses have high digital

engagement!Source: Deloitte - Access Economics Report 2013 (500) - https://www.deloitteaccesseconomics.com.au/uploads/File/Connected%20Small%20Business.pdf

26

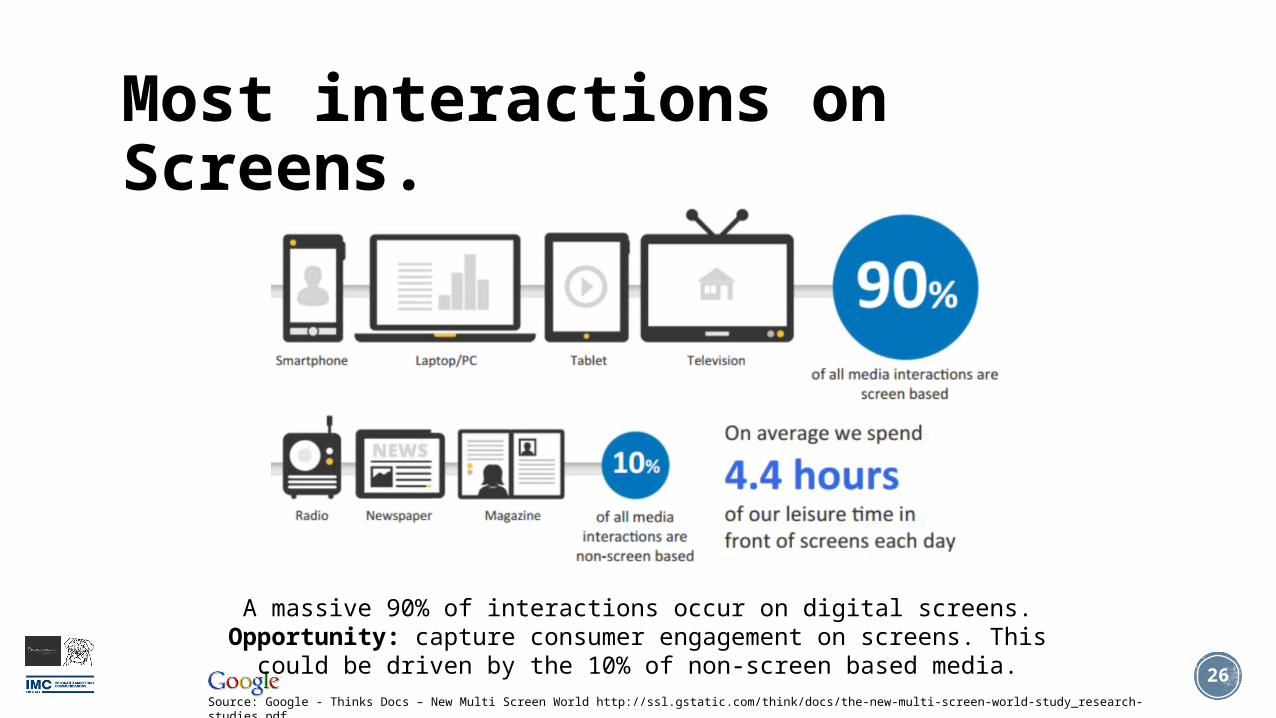

Most interactions on Screens.

A massive 90% of interactions occur on digital screens.Opportunity: capture consumer engagement on screens. This could

be driven by the 10% of non-screen based media.Source: Google - Thinks Docs – New Multi Screen World http://ssl.gstatic.com/think/docs/the-new-multi-screen-world-study_research-studies.pdf

27

Digital Opportunities.

The latest news on key digital media channels.

28

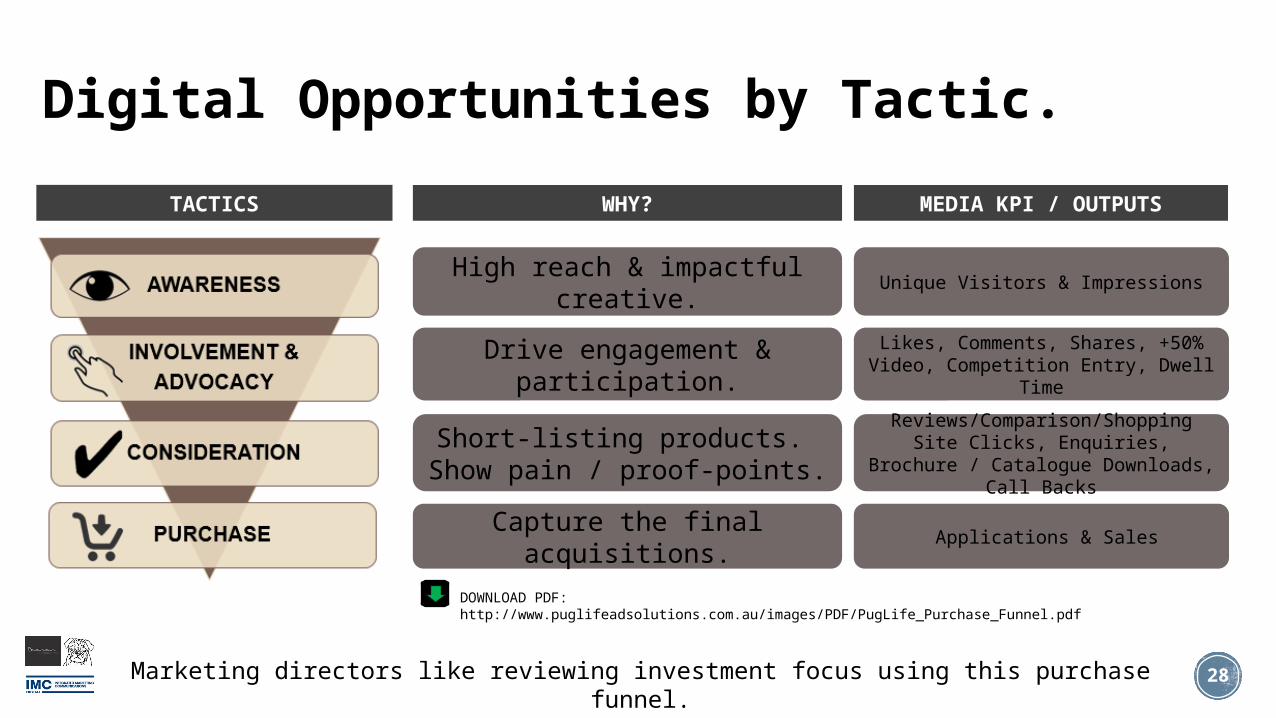

Digital Opportunities by Tactic.

Marketing directors like reviewing investment focus using this purchase funnel.

AWARENESS

INVOLVEMENT & ADVOCACY

CONSIDERATION

PURCHASE

TACTICS

High reach & impactful creative.

Drive engagement & participation.

Short-listing products. Show pain / proof-points.

WHY? MEDIA KPI / OUTPUTS

Capture the final acquisitions.

Unique Visitors & Impressions

Likes, Comments, Shares, +50% Video, Competition Entry, Dwell Time

Reviews/Comparison/Shopping Site Clicks, Enquiries, Brochure / Catalogue

Downloads, Call Backs

Applications & Sales

DOWNLOAD PDF: http://www.puglifeadsolutions.com.au/images/PDF/PugLife_Purchase_Funnel.pdf

29

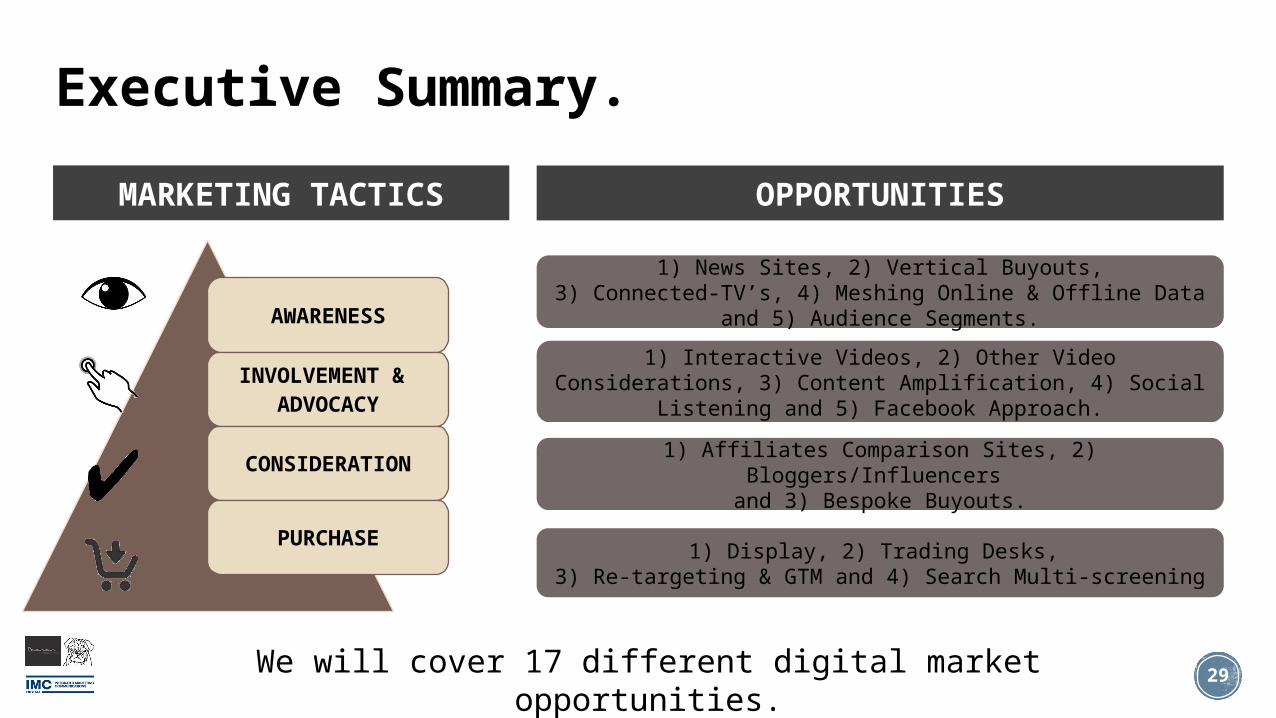

Executive Summary.

We will cover 17 different digital market opportunities.

AWARENESS

INVOLVEMENT & ADVOCACY

CONSIDERATION

PURCHASE

MARKETING TACTICS

1) News Sites, 2) Vertical Buyouts,3) Connected-TV’s, 4) Meshing Online & Offline Data

and 5) Audience Segments.

1) Interactive Videos, 2) Other Video Considerations, 3) Content Amplification, 4) Social Listening and 5) Facebook Approach.

1) Affiliates Comparison Sites, 2) Bloggers/Influencers and 3) Bespoke Buyouts.

OPPORTUNITIES

1) Display, 2) Trading Desks, 3) Re-targeting & GTM and 4) Search Multi-screening

30

Big Scale on Top News Sites.

#12.76m #2

2.75m

#32.45m #4

2.39m

TOP 3 TV PROGRAMS:My Kitchen Rules = 1.766m

The Block = 1.234m9 News = 1.091m

Source: OzTam 26th Wed Feb 2014

Source: Nielsen Online Ratings / Mumbrella January 14 - http://mumbrella.com.au/news-com-au-regains-top-spot-read-website-mail-online-now-eighth-position-206878

31

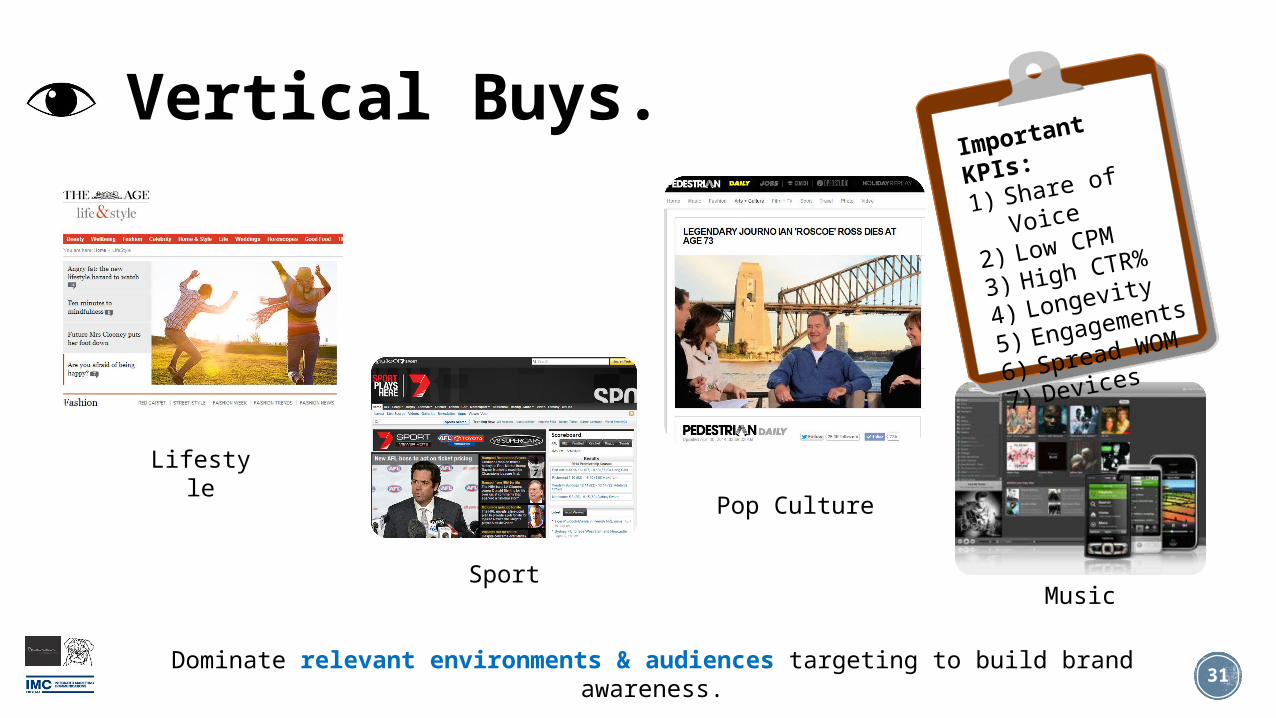

Vertical Buys.

Lifestyle

Sport

Pop Culture

Music

Dominate relevant environments & audiences targeting to build brand awareness.

Important

KPIs:

1) Share of

Voice

2) Low CPM

3) High CTR%

4) Longevity

5) Engagements

6) Spread WOM

7) Devices

32

Innovative Connected TV ads.

Opportunity: brands who want to “first-to-market” should consider this.

- 1 of 3 Australians own a Smart-TV- 300-400k Australians are connect to internet – NBN in

increasing data plans with carrier will see this grow further

- TV shows and movies are most popular- Adconion is the preferred media partner to LG &

Samsung

33

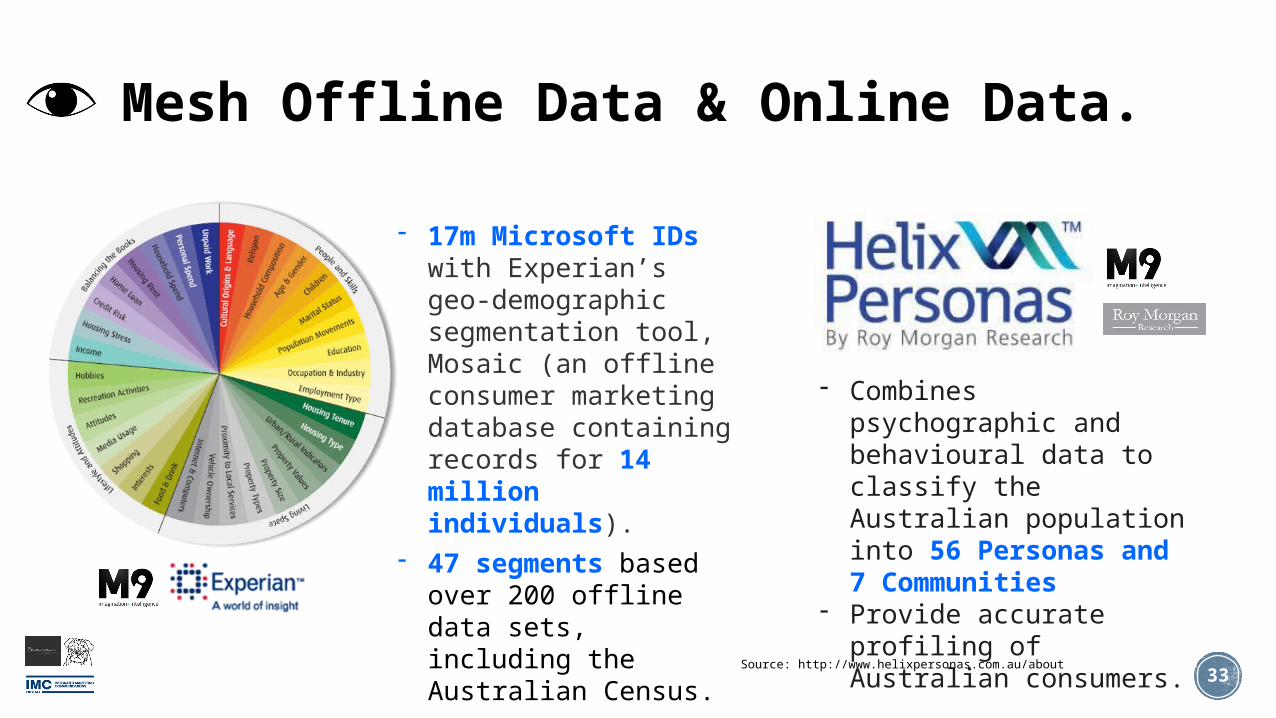

Mesh Offline Data & Online Data.

- 17m Microsoft IDs with Experian’s geo-demographic segmentation tool, Mosaic (an offline consumer marketing database containing records for 14 million individuals).

- 47 segments based over 200 offline data sets, including the Australian Census.

- Combines psychographic and behavioural data to classify the Australian population into 56 Personas and 7 Communities

- Provide accurate profiling of Australian consumers.

Source: http://www.helixpersonas.com.au/about

34

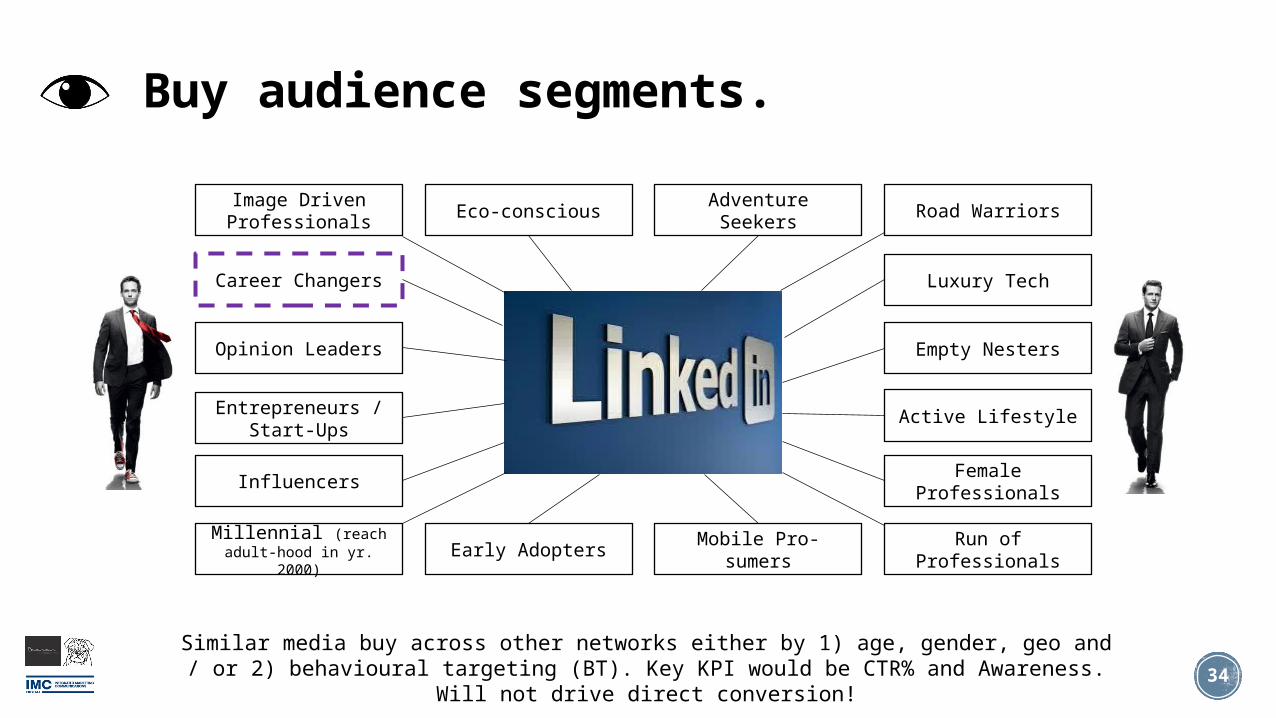

Buy audience segments.

Image Driven Professionals

Career Changers

Opinion Leaders

Entrepreneurs / Start-Ups

Eco-conscious Adventure Seekers

Active Lifestyle

Female Professionals

Run of Professionals

Road Warriors

Influencers

Millennial (reach adult-hood in yr. 2000)

Early Adopters Mobile Pro-sumers

Luxury Tech

Empty Nesters

Similar media buy across other networks either by 1) age, gender, geo and / or 2) behavioural targeting (BT). Key KPI would be CTR% and Awareness. Will not drive direct

conversion!

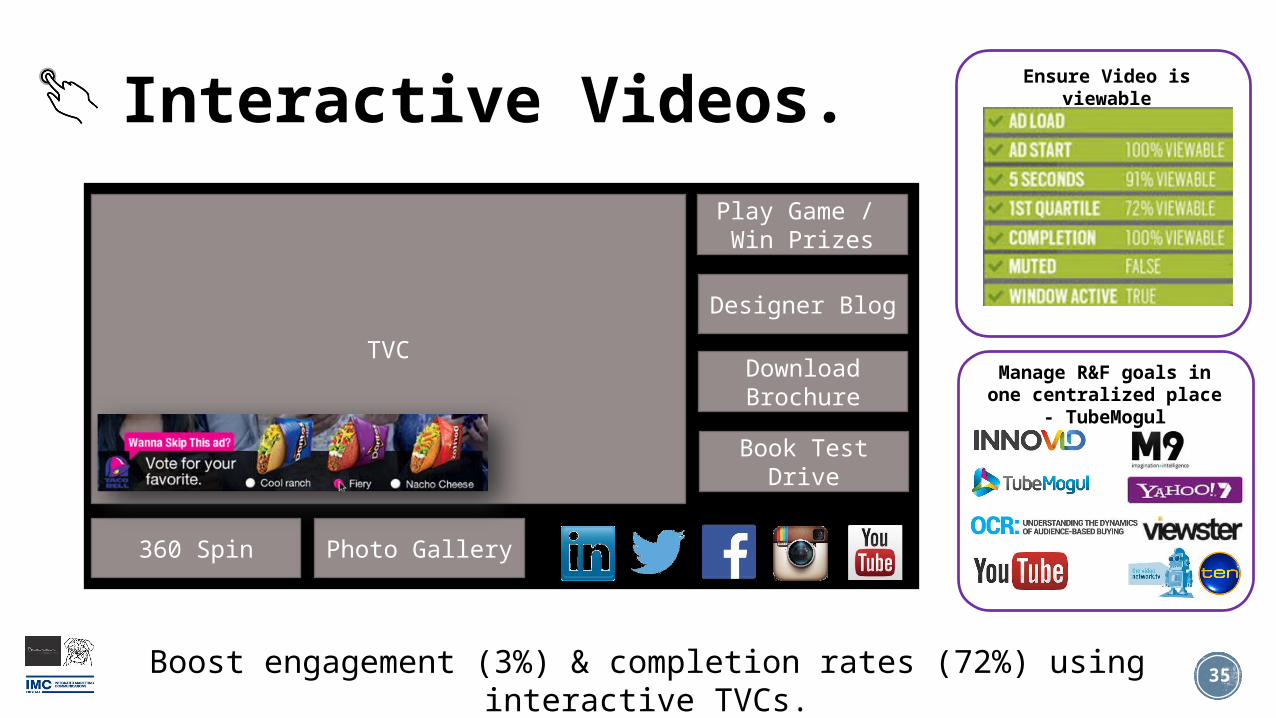

Interactive Videos.

35

360 Spin

TVC

Photo Gallery

Play Game / Win Prizes

Designer Blog

Download Brochure

Book Test Drive

Boost engagement (3%) & completion rates (72%) using interactive TVCs.

(Innovid Benchmarks)

Manage R&F goals in one centralized place - TubeMogul

Ensure Video is viewable

36

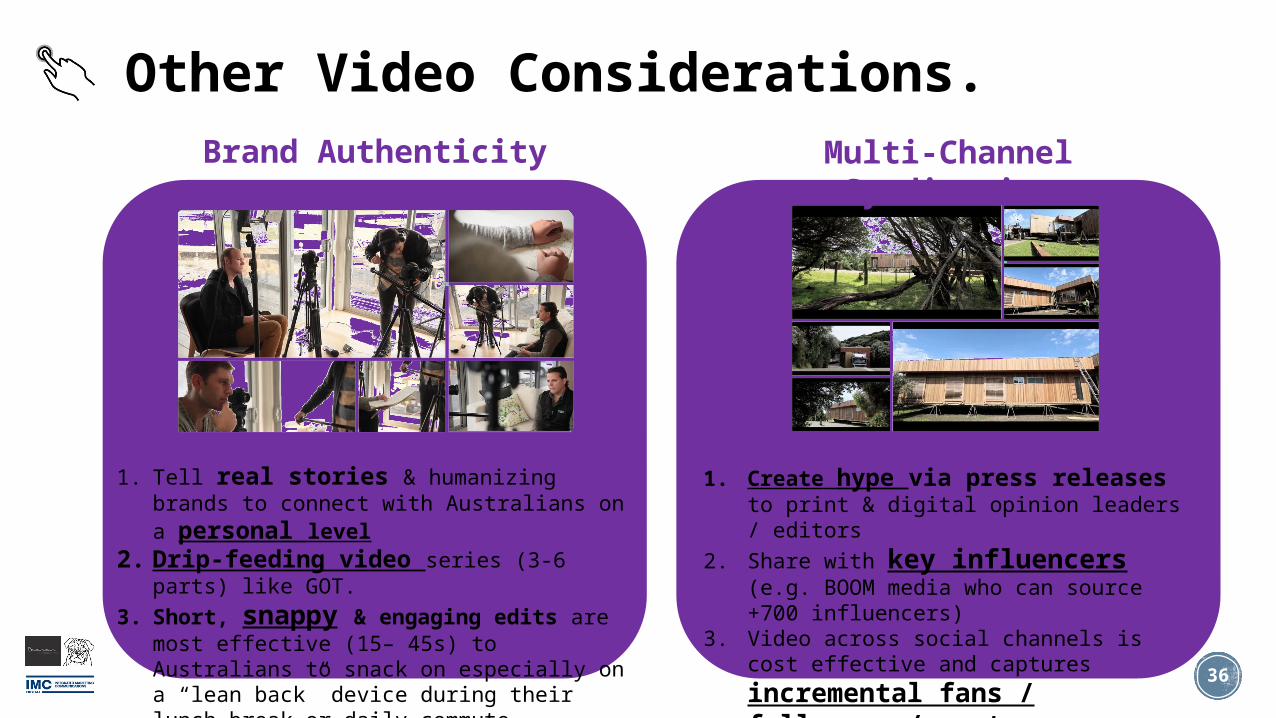

Other Video Considerations.

1. Tell real stories & humanizing brands to connect with Australians on a personal level

2. Drip-feeding video series (3-6 parts) like GOT.

3. Short, snappy & engaging edits are most effective (15– 45s) to Australians to snack on especially on a “lean back” device during their lunch break or daily commute.

1. Create hype via press releases to print & digital opinion leaders / editors

2. Share with key influencers (e.g. BOOM media who can source +700 influencers)

3. Video across social channels is cost effective and captures incremental fans / followers / customers

Brand Authenticity Multi-Channel Syndication

37

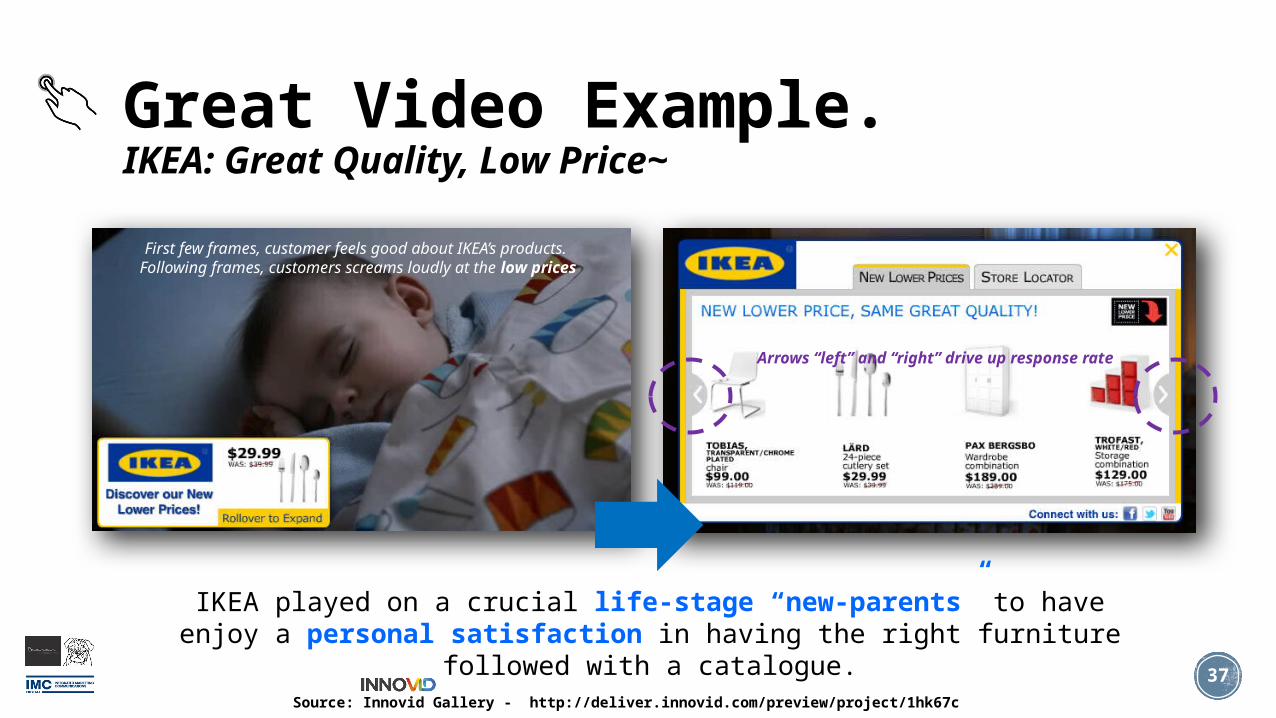

Great Video Example. IKEA: Great Quality, Low Price~

Source: Innovid Gallery - http://deliver.innovid.com/preview/project/1hk67c

First few frames, customer feels good about IKEA’s products. Following frames, customers screams loudly at the low prices

IKEA played on a crucial life-stage “new-parents” to have enjoy a personal satisfaction in having the right furniture followed with a

catalogue.

Arrows “left” and “right” drive up response rate

Content Amplification.

38

Boost positive reviews & articles, and making our ads appear native/organic.

Must be newsworthy – they will subject to approval.

39

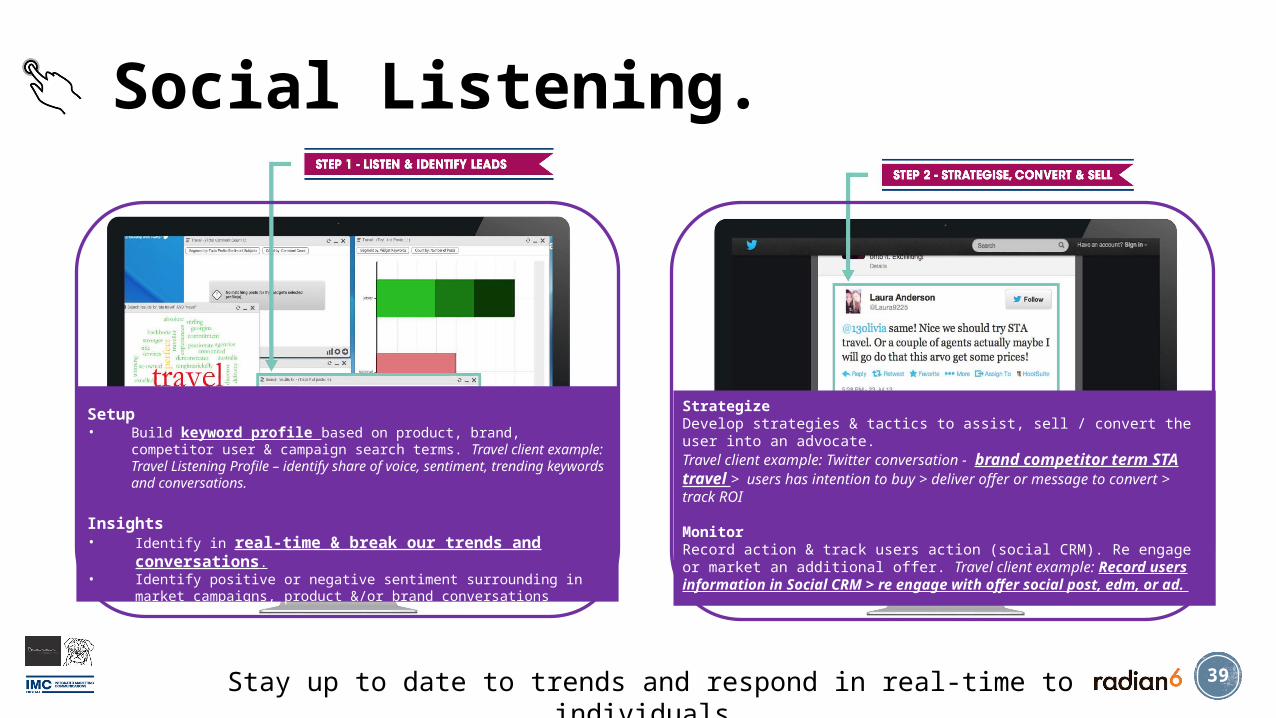

Social Listening.

Setup• Build keyword profile based on product, brand, competitor user

& campaign search terms. Travel client example: Travel Listening Profile – identify share of voice, sentiment, trending keywords and conversations.

Insights• Identify in real-time & break our trends and

conversations.• Identify positive or negative sentiment surrounding in market

campaigns, product &/or brand conversations

StrategizeDevelop strategies & tactics to assist, sell / convert the user into an advocate. Travel client example: Twitter conversation - brand competitor term STA travel > users has intention to buy > deliver offer or message to convert > track ROI

MonitorRecord action & track users action (social CRM). Re engage or market an additional offer. Travel client example: Record users information in Social CRM > re engage with offer social post, edm, or ad.

Stay up to date to trends and respond in real-time to individuals.

40

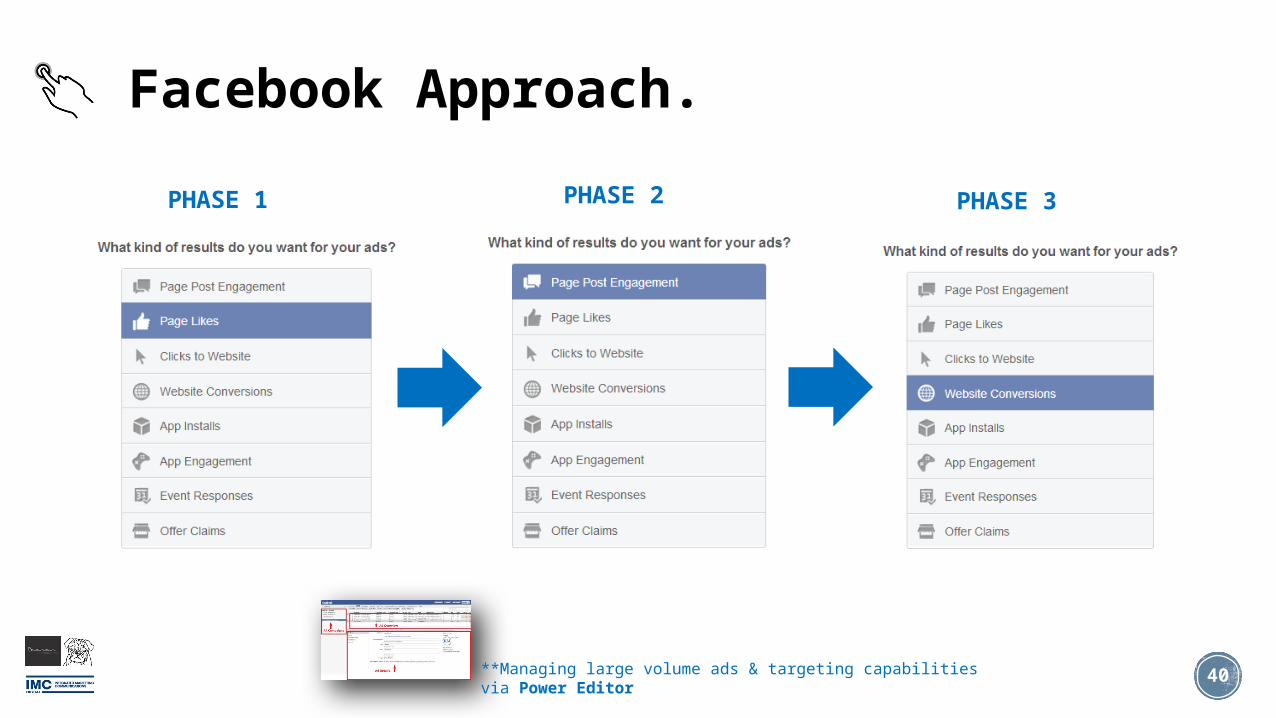

Facebook Approach.

**Managing large volume ads & targeting capabilities via Power Editor

PHASE 1 PHASE 2 PHASE 3

41

Affiliates Comparison Sites.

Drive incremental customer leads and online conversions.DGM manages +3,000 comparison sites.

http://www.dgm-au.com/services/affiliate-marketing/

42

Blogging / Influencers.

Request for product review in exchange for actual product.Consider: Vice, Pedestrian TV, Sound Alliance, NuffNang, KidSpot, StayAtHomeMum, BOOM, etc.

Top Bloggers: 2103 - http://mumbrella.com.au/2013-best-australian-blogger-is-food-blogger-sney-roy-153130

43

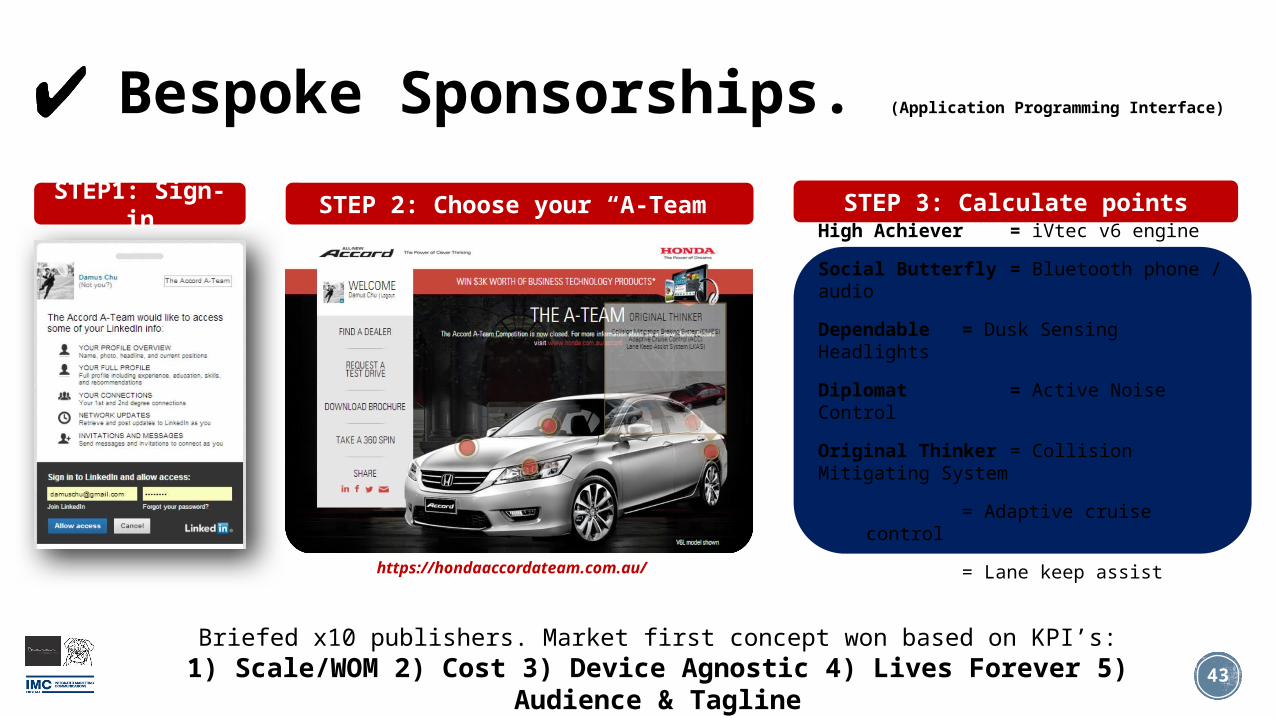

Bespoke Sponsorships. (Application Programming

Interface)

Briefed x10 publishers. Market first concept won based on KPI’s:1) Scale/WOM 2) Cost 3) Device Agnostic 4) Lives Forever 5) Audience

& Tagline

STEP1: Sign-in

STEP 2: Choose your “A-Team”

https://hondaaccordateam.com.au/

High Achiever = iVtec v6 engine

Social Butterfly = Bluetooth phone / audio

Dependable = Dusk Sensing Headlights

Diplomat = Active Noise Control

Original Thinker = Collision Mitigating System

= Adaptive cruise control

= Lane keep assist

STEP 3: Calculate points

44

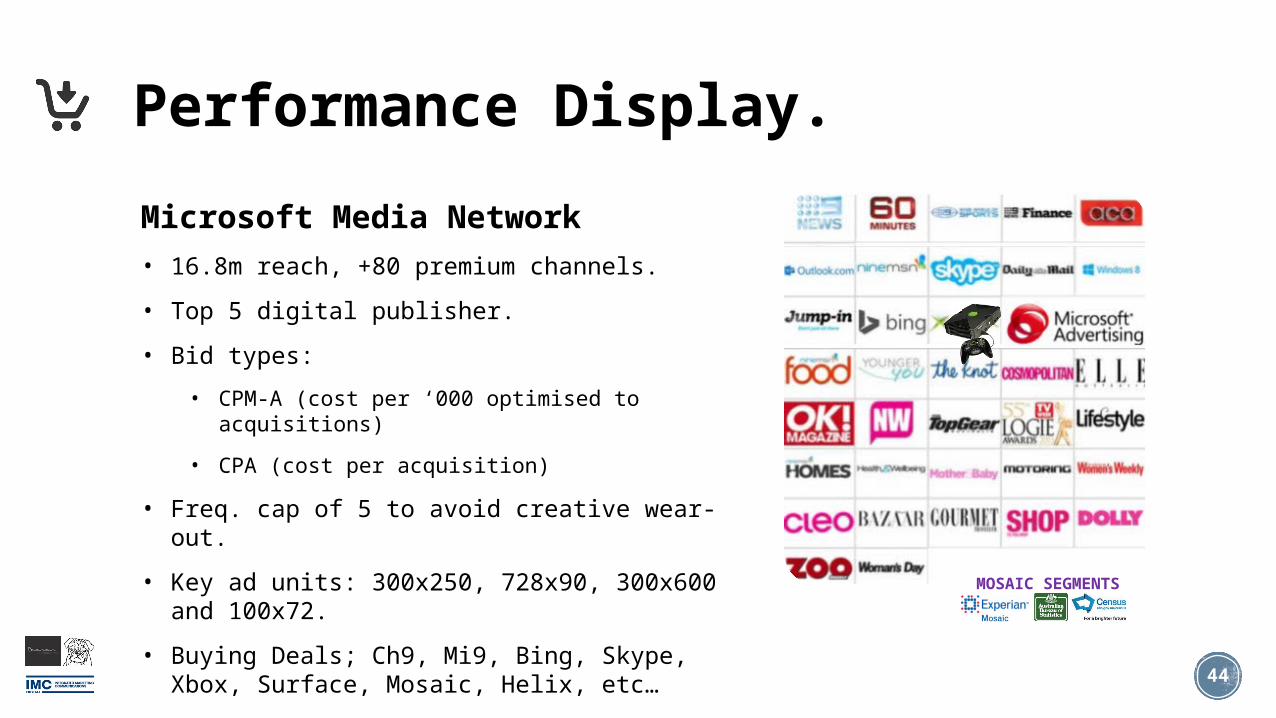

Performance Display.

Microsoft Media Network• 16.8m reach, +80 premium channels.

• Top 5 digital publisher.

• Bid types:

• CPM-A (cost per ‘000 optimised to acquisitions)

• CPA (cost per acquisition)

• Freq. cap of 5 to avoid creative wear-out.

• Key ad units: 300x250, 728x90, 300x600 and 100x72.

• Buying Deals; Ch9, Mi9, Bing, Skype, Xbox, Surface, Mosaic, Helix, etc…

MOSAIC SEGMENTS

45

TRADING DESKS

AD

VER

TIS

ER

S

SUPPLY EXCHANGES

CO

NS

UM

ER

S

DEMAND SIDE PLATFORM

(SOFTWARE)

REAL-TIME BIDDING

The Trading Desk.

SUPPLY SIDE PLATFORM

(SOFTWARE)

Buy remnant inventory for 1) cheap CPM < $5 and 2) re-targeting campaign.

46

Trading Desks Considerations.

Full-time service required to:

Buy and sell ad inventory daily.

Reporting and optimisations daily.

Marketer concerns:

Limited transparency on ad / site performance.

Limited premium ads / buyout opportunities.

No 10% commission rebate. No visibility on margins.Programmatic Buying

47

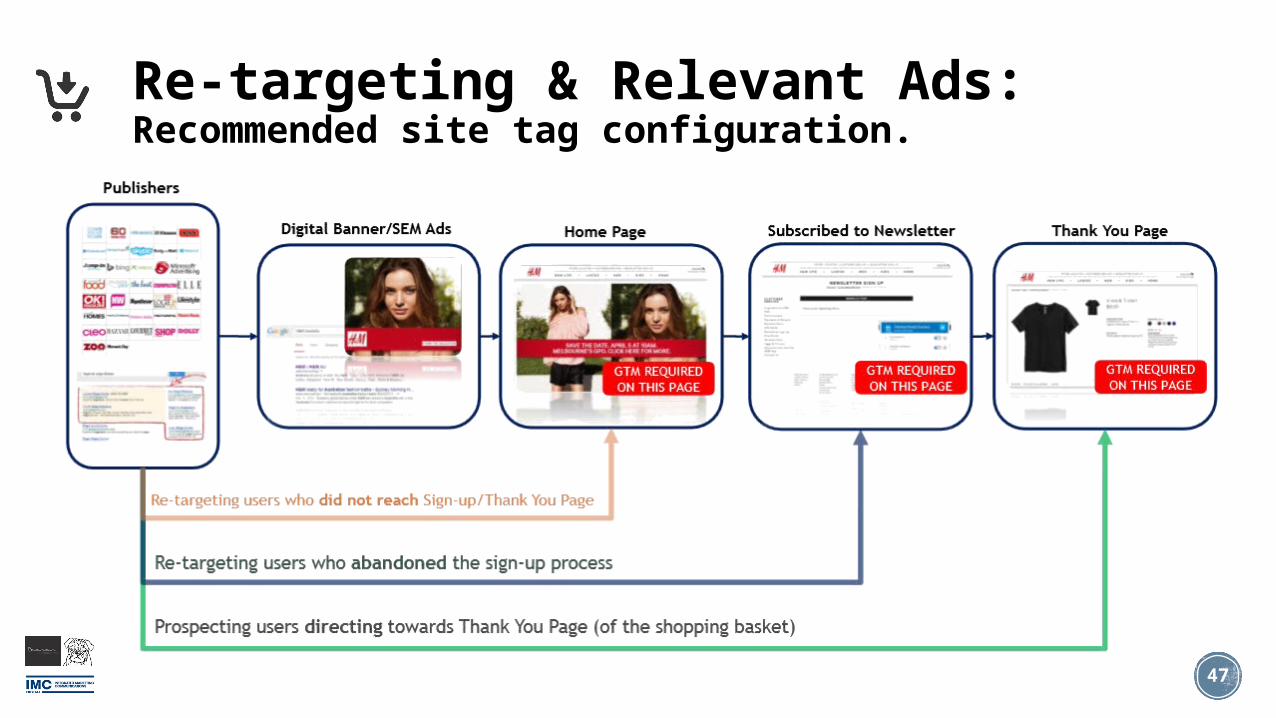

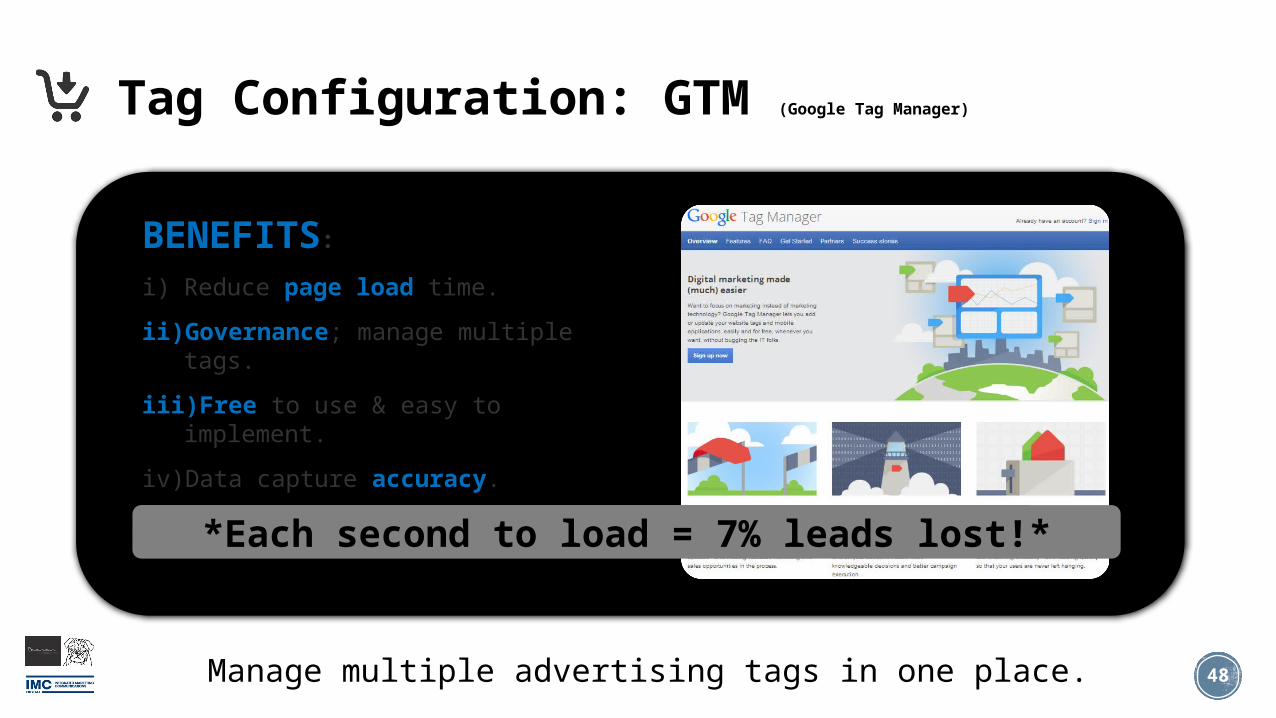

Re-targeting & Relevant Ads:Recommended site tag configuration.

48

Tag Configuration: GTM (Google Tag Manager)

BENEFITS:

i) Reduce page load time.

ii) Governance; manage multiple tags.

iii) Free to use & easy to implement.

iv) Data capture accuracy.

v) Reduce cost to IT.

* source: http://www.tagman.com/mdp-blog/2012/03/just-one-second-delay-in-page-load-can-cause-7-loss-in-customer-conversions/

Manage multiple advertising tags in one place.

*Each second to load = 7% leads lost!*

49

Search: Multi-screens.

Lean Forward Desktop

Lean Back Devices

We can track and optimise across desktop and devices.

Out ‘n’ About

Just saw a TV/Outdoor ad, heard a

radio ad

50

Digital Media Work-flow.

Managing our 6-Step Work-flow.

51

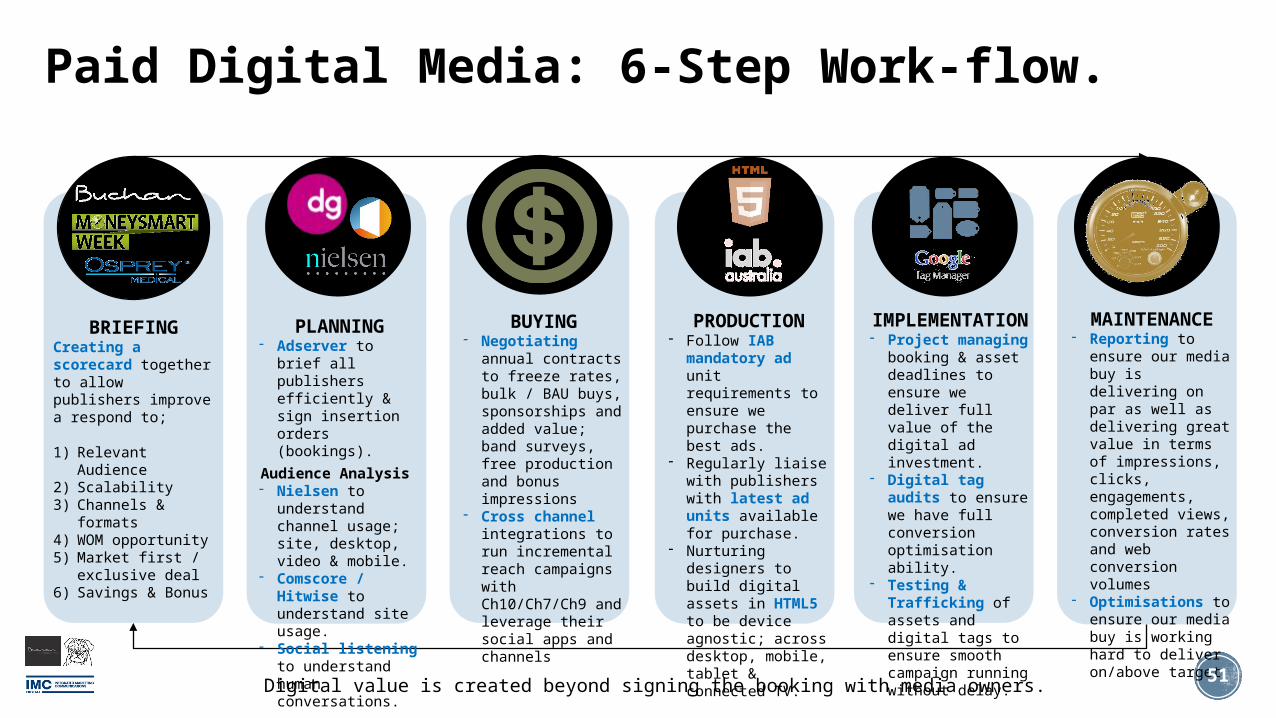

Paid Digital Media: 6-Step Work-flow.

Digital value is created beyond signing the booking with media owners.

BRIEFINGCreating a scorecard together to allow publishers improve a respond to;

1) Relevant Audience

2) Scalability 3) Channels &

formats4) WOM opportunity5) Market first /

exclusive deal6) Savings & Bonus

PLANNING- Adserver to brief

all publishers efficiently & sign insertion orders (bookings).

Audience Analysis - Nielsen to

understand channel usage; site, desktop, video & mobile.

- Comscore / Hitwise to understand site usage.

- Social listening to understand human conversations.

PRODUCTION- Follow IAB

mandatory ad unit requirements to ensure we purchase the best ads.

- Regularly liaise with publishers with latest ad units available for purchase.

- Nurturing designers to build digital assets in HTML5 to be device agnostic; across desktop, mobile, tablet & connected TV.

IMPLEMENTATION

- Project managing booking & asset deadlines to ensure we deliver full value of the digital ad investment.

- Digital tag audits to ensure we have full conversion optimisation ability.

- Testing & Trafficking of assets and digital tags to ensure smooth campaign running without delay.

MAINTENANCE- Reporting to

ensure our media buy is delivering on par as well as delivering great value in terms of impressions, clicks, engagements, completed views, conversion rates and web conversion volumes

- Optimisations to ensure our media buy is working hard to deliver on/above target

BUYING- Negotiating

annual contracts to freeze rates, bulk / BAU buys, sponsorships and added value; band surveys, free production and bonus impressions

- Cross channel integrations to run incremental reach campaigns with Ch10/Ch7/Ch9 and leverage their social apps and channels

52

1. Briefing. THE OPPORTUNITY

COMMUNICATION TONE?

WHAT’S THE OFFER?

TARGET AUDIENCE

WHICH VERTICAL?

***Audience profiling increasingly important as targeting by demographics become a lot more sophisticated with:

- Nielsen Online Campaign Ratings (OCR) using FB profile data

- Roy Morgan Helix Personas using their +50k surveys in Australia to overlay with customer profiles to pull more insights

- Hitwise Experise Mosaics using digital trakcing by site with ABS/Sensis data

DOWNLOAD PDF: http://www.puglifeadsolutions.com.au/images/PDF/PugLife_Media_Brief.pdf

53

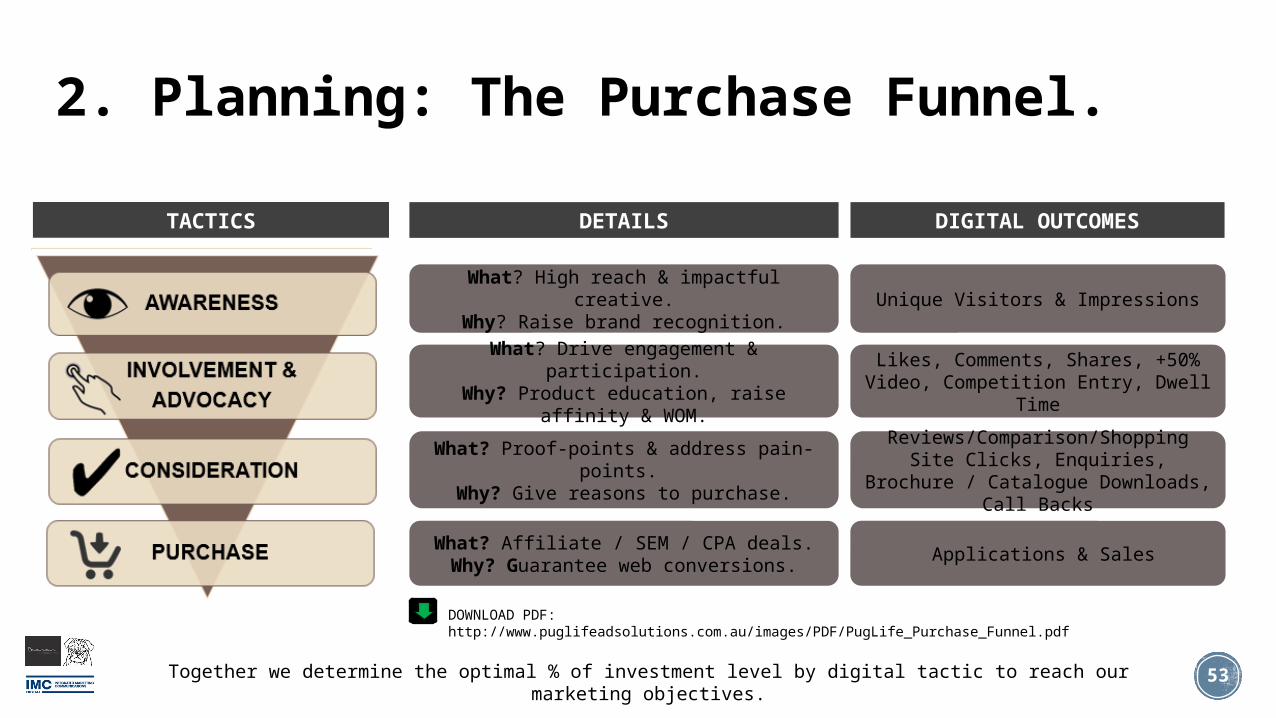

AWARENESS

INVOLVEMENT & ADVOCACY

CONSIDERATION

PURCHASE

TACTICS

What? High reach & impactful creative.Why? Raise brand recognition.

What? Drive engagement & participation.Why? Product education, raise affinity & WOM.

What? Proof-points & address pain-points. Why? Give reasons to purchase.

DETAILS DIGITAL OUTCOMES

What? Affiliate / SEM / CPA deals.Why? Guarantee web conversions.

Unique Visitors & Impressions

Likes, Comments, Shares, +50% Video, Competition Entry, Dwell Time

Reviews/Comparison/Shopping Site Clicks, Enquiries, Brochure / Catalogue

Downloads, Call Backs

Applications & Sales

2. Planning: The Purchase Funnel.

Together we determine the optimal % of investment level by digital tactic to reach our marketing objectives.

DOWNLOAD PDF: http://www.puglifeadsolutions.com.au/images/PDF/PugLife_Purchase_Funnel.pdf

54

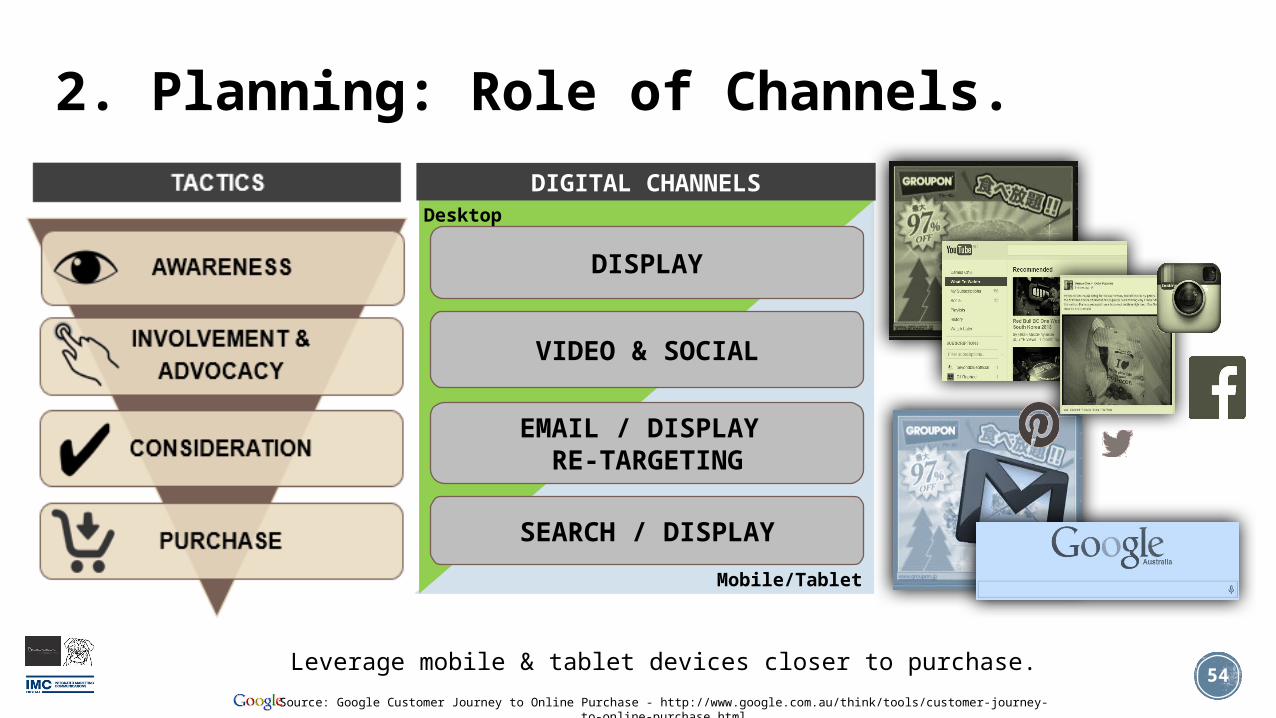

2. Planning: Role of Channels.

DIGITAL CHANNELS

VIDEO & SOCIAL

EMAIL / DISPLAY RE-TARGETING

SEARCH / DISPLAY

DISPLAY

Leverage mobile & tablet devices closer to purchase.

Desktop

Mobile/Tablet

Source: Google Customer Journey to Online Purchase - http://www.google.com.au/think/tools/customer-journey-to-online-purchase.html

55

2. Planning: Media Schedule.

CHANNEL DETAILS- Objective: Awareness- Format:

Display- Publisher: Fairfax- Timing: 1st

Month- Ad Sizes:

Skins, MRC, LB- Specs:

<40kb, SWF v8

FORECASTED ROI- Awareness:

- Impressions / Views- CTR%, CPM, CPC, CPV

- Engage/Connect- Clicks / Fans / CPF- Shares / Comments /

Votes- Brochure / Catalogue

Down/l- Competition Entries

- Convert- Applications / Sales / CPA

FINANCIALS- Gross Value, Discounts,

Bonus - Fees & Nett exc. GST

DOWNLOAD PDF: http://www.puglifeadsolutions.com.au/images/PDF/PugLife_Media_Plan.pdf

Digital plan very accountable, and is approved by client before buying.

56

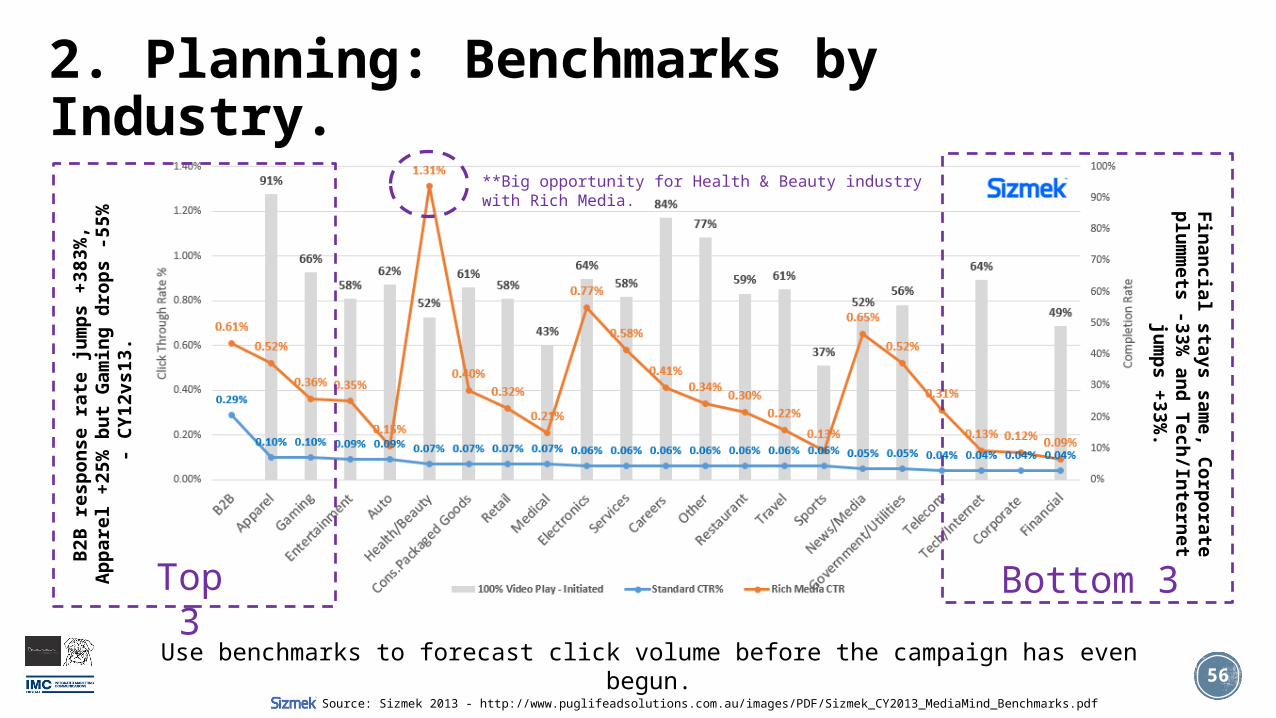

2. Planning: Benchmarks by Industry.

Use benchmarks to forecast click volume before the campaign has even begun.

Top 3 Bottom 3

Source: Sizmek 2013 - http://www.puglifeadsolutions.com.au/images/PDF/Sizmek_CY2013_MediaMind_Benchmarks.pdf

**Big opportunity for Health & Beauty industry with Rich Media.

B2B

resp

on

se r

ate

ju

mp

s +

383%

, A

pp

are

l +

25%

bu

t G

am

ing

dro

ps -

55%

- C

Y12vs13.

Fin

an

cia

l sta

ys s

am

e, C

orp

ora

te

plu

mm

ets

-33%

an

d Te

ch

/Inte

rnet

jum

ps +

33%

.

57

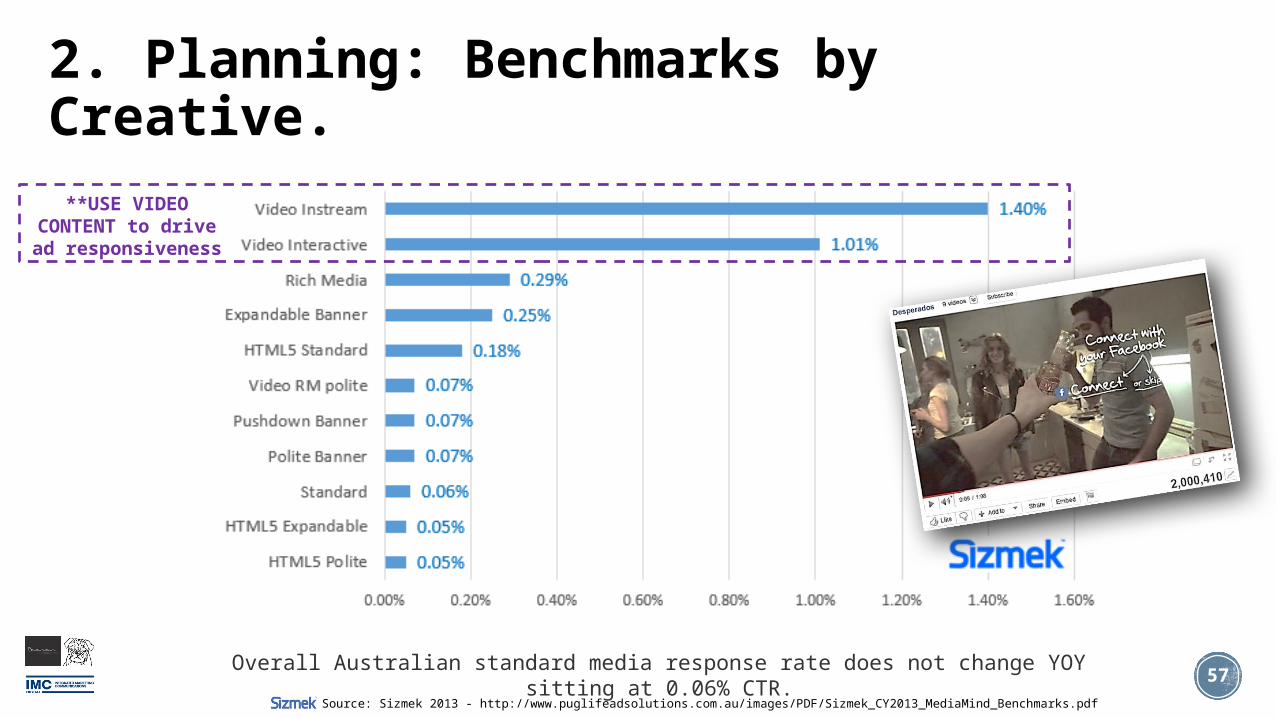

2. Planning: Benchmarks by Creative.

Overall Australian standard media response rate does not change YOY sitting at 0.06% CTR.

**USE VIDEO CONTENT to drive ad responsiveness

Source: Sizmek 2013 - http://www.puglifeadsolutions.com.au/images/PDF/Sizmek_CY2013_MediaMind_Benchmarks.pdf

58

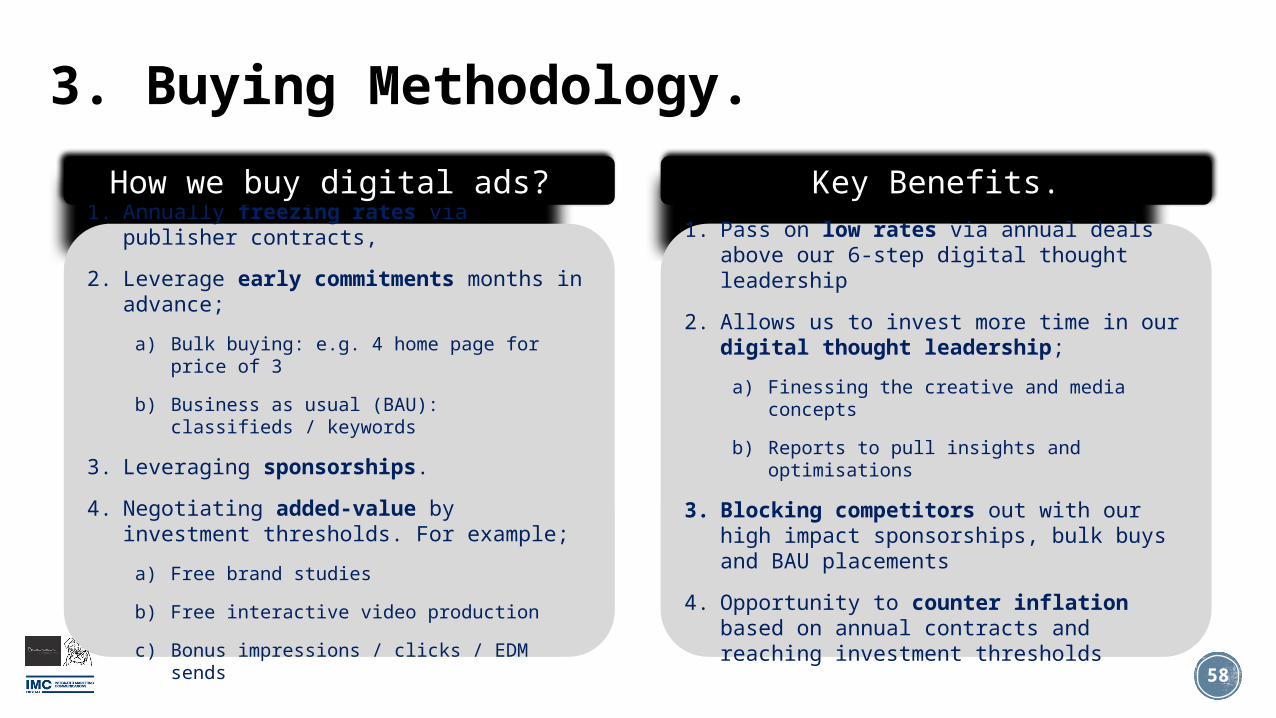

1. Annually freezing rates via publisher contracts,

2. Leverage early commitments months in advance;

a) Bulk buying: e.g. 4 home page for price of 3

b) Business as usual (BAU): classifieds / keywords

3. Leveraging sponsorships.

4. Negotiating added-value by investment thresholds. For example;

a) Free brand studies

b) Free interactive video production

c) Bonus impressions / clicks / EDM sends

1. Pass on low rates via annual deals above our 6-step digital thought leadership

2. Allows us to invest more time in our digital thought leadership;

a) Finessing the creative and media concepts

b) Reports to pull insights and optimisations

3. Blocking competitors out with our high impact sponsorships, bulk buys and BAU placements

4. Opportunity to counter inflation based on annual contracts and reaching investment thresholds

How we buy digital ads? Key Benefits.

3. Buying Methodology.

59

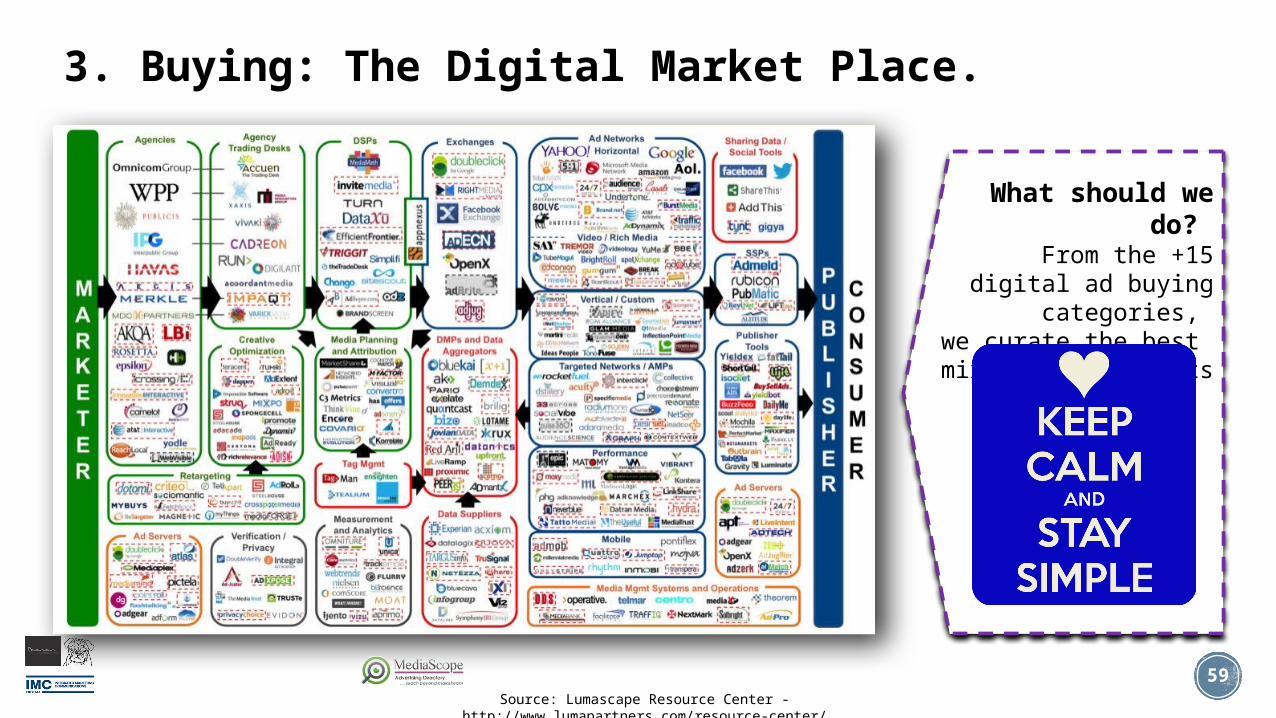

3. Buying: The Digital Market Place.

Source: Lumascape Resource Center - http://www.lumapartners.com/resource-center/

What should we do?

From the +15 digital ad buying categories,

we curate the best mix for our clients

60

4. Production: Standard Ads.

300x250 300x600 160x600

728x90

Recommend referring to IAB as an authority in Australian digital media for best practicesA production schedule is required immediately after media schedule is approved

x4 Mandatory Desktop Display Ad Units

Source: IAB http://goo.gl/QntZA7

61

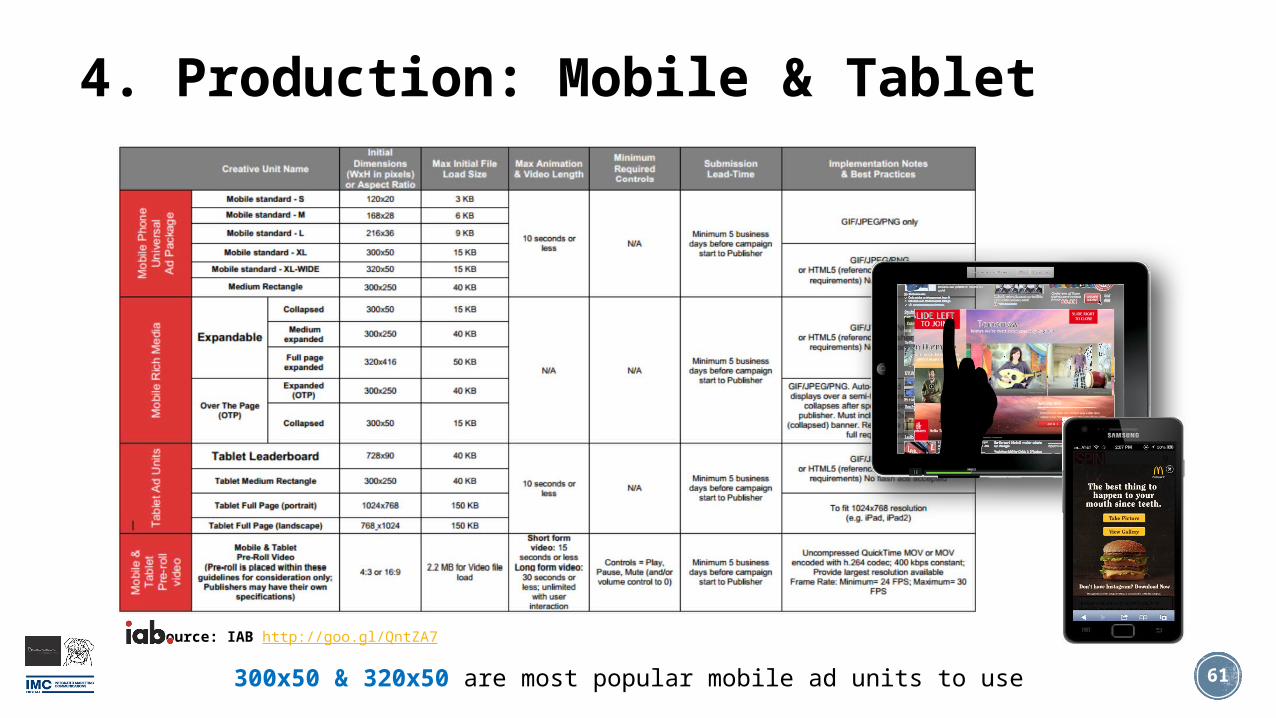

4. Production: Mobile & Tablet

300x50 & 320x50 are most popular mobile ad units to use

Source: IAB http://goo.gl/QntZA7

62

4. Production. HTML5 for Display Banners.

HTML5 becomes an official IAB recommendation.

Benefits:

1. Allows advertisers to deliver creative seamlessly across web pages & devices (i.e. Smart TV > Mobile > Tablet > Desktop)

2. Well established format that can be easily adopted by designers & developers world-wide

3. Rapid testing infrastructure across browsers

Cons:

4. Initial set-up cost is high given the heavy coding required. Adserving costs are higher too.

5. Industry guidelines & best practice still being developed especially for rich media, how to package & optimise files to ensure ad load time is efficient & back up files

Source: IAB HTML5 for Digital Advertising - http://www.iabaustralia.com.au/uploads/uploads/2014-02/1392044400_7c4ec2ec91f443cc900e9339fa7dc5bc.pdf

63

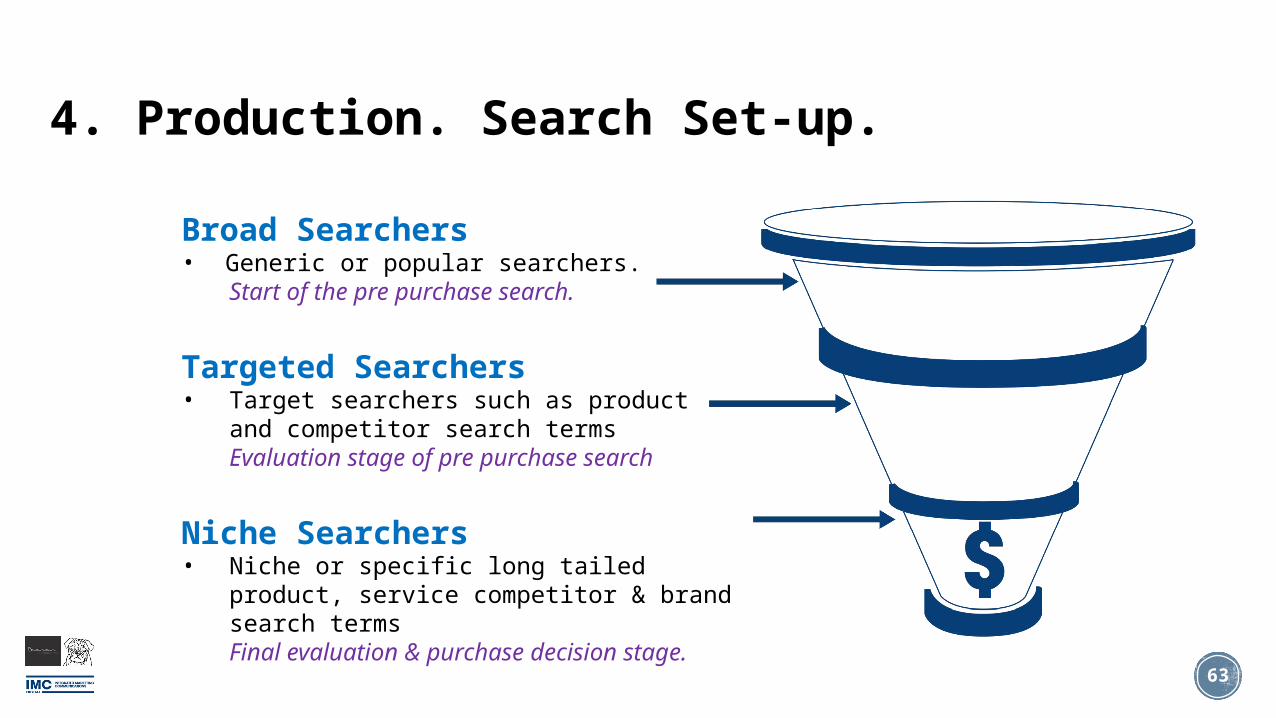

4. Production. Search Set-up.

Broad Searchers• Generic or popular searchers.

Start of the pre purchase search.

Targeted Searchers• Target searchers such as product and

competitor search termsEvaluation stage of pre purchase

search

Niche Searchers• Niche or specific long tailed product,

service competitor & brand search termsFinal evaluation & purchase decision

stage.

64

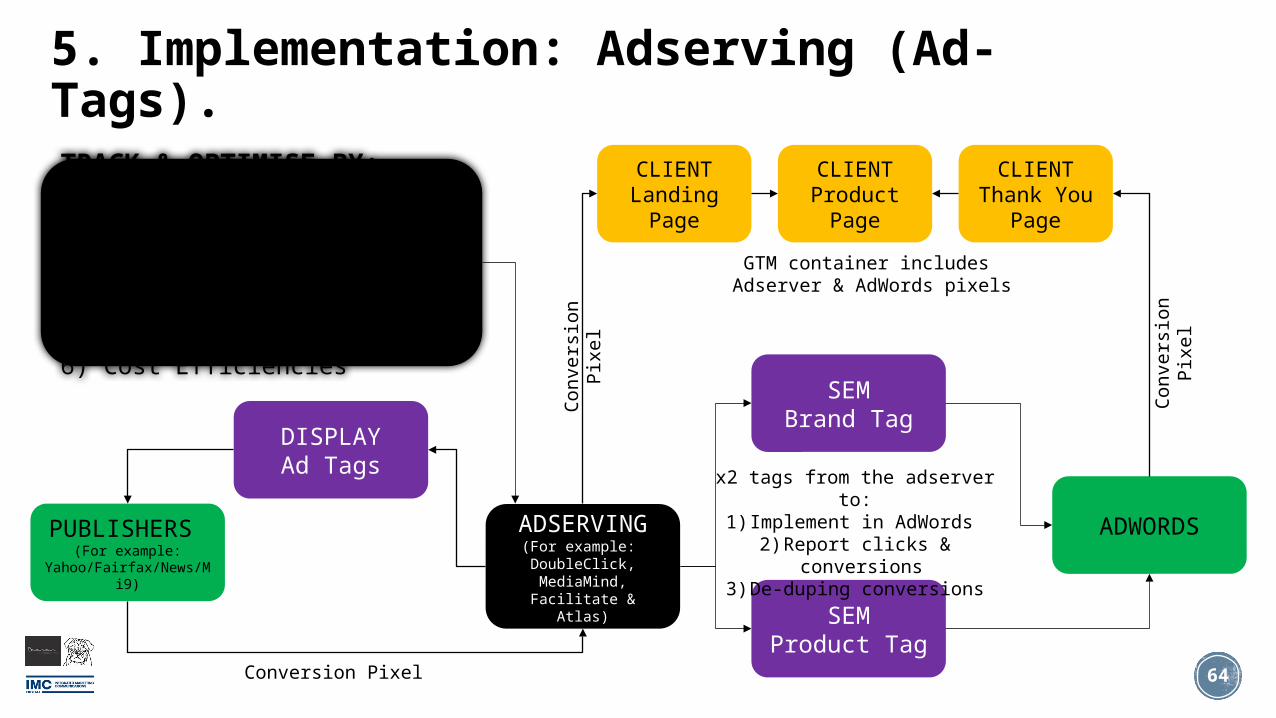

5. Implementation: Adserving (Ad-Tags).

SEMBrand Tag

SEMProduct Tag

ADSERVING(For example: DoubleClick,

MediaMind, Facilitate & Atlas)

ADWORDS

CLIENTLanding

Page

x2 tags from the adserver to:1) Implement in AdWords

2) Report clicks & conversions 3) De-duping conversions

Convers

ion P

ixel

Convers

ion P

ixel

PUBLISHERS (For example:

Yahoo/Fairfax/News/Mi9)

DISPLAYAd Tags

Conversion Pixel

GTM container includes Adserver & AdWords pixels

CLIENT Product

Page

CLIENTThank You

Page

TRACK & OPTIMISE BY:1) Impressions, Clicks, CTR%2) Engagements & Web Conversions4) Dwell Time / Views5) Creative message performance6) Cost Efficiencies

65

5. Implementation: One-Stop-Shop.

Still being refined.

66

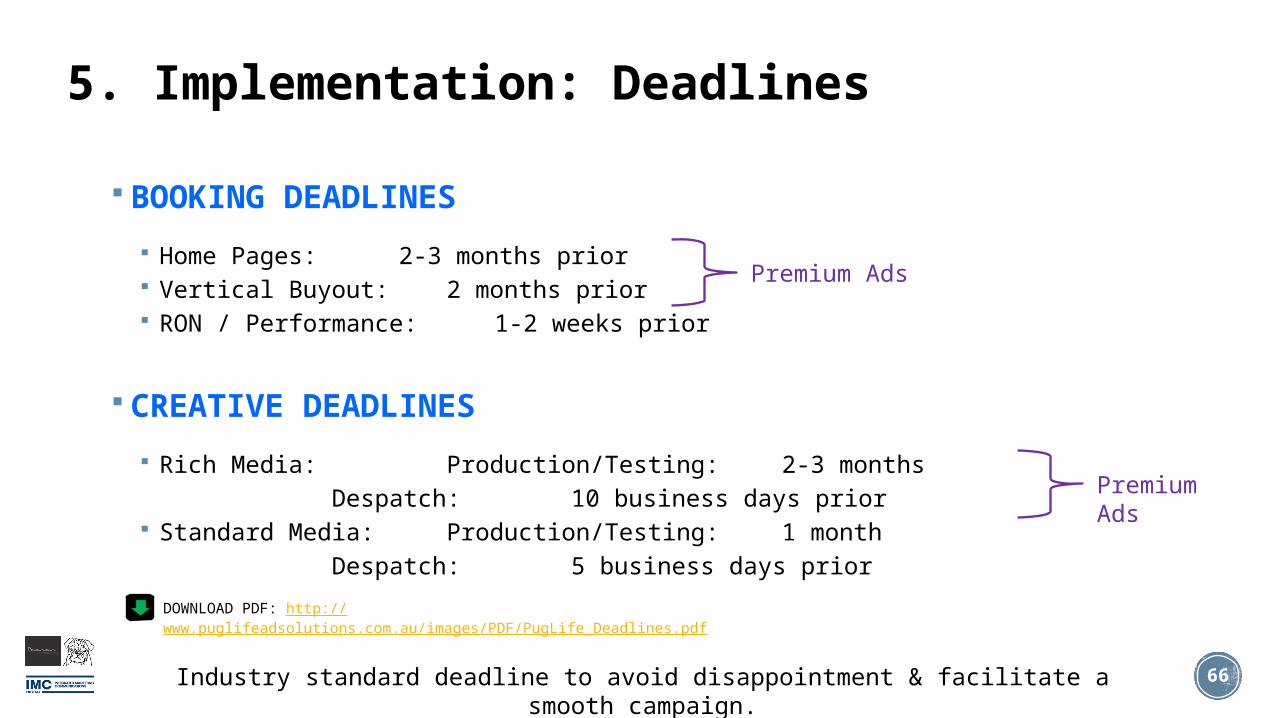

5. Implementation: Deadlines

BOOKING DEADLINES

Home Pages: 2-3 months prior Vertical Buyout: 2 months prior RON / Performance: 1-2 weeks prior

CREATIVE DEADLINES

Rich Media: Production/Testing: 2-3 monthsDespatch: 10 business days prior

Standard Media: Production/Testing: 1 monthDespatch: 5 business days prior

Industry standard deadline to avoid disappointment & facilitate a smooth campaign.

DOWNLOAD PDF: http://www.puglifeadsolutions.com.au/images/PDF/PugLife_Deadlines.pdf

Premium Ads

Premium Ads

67

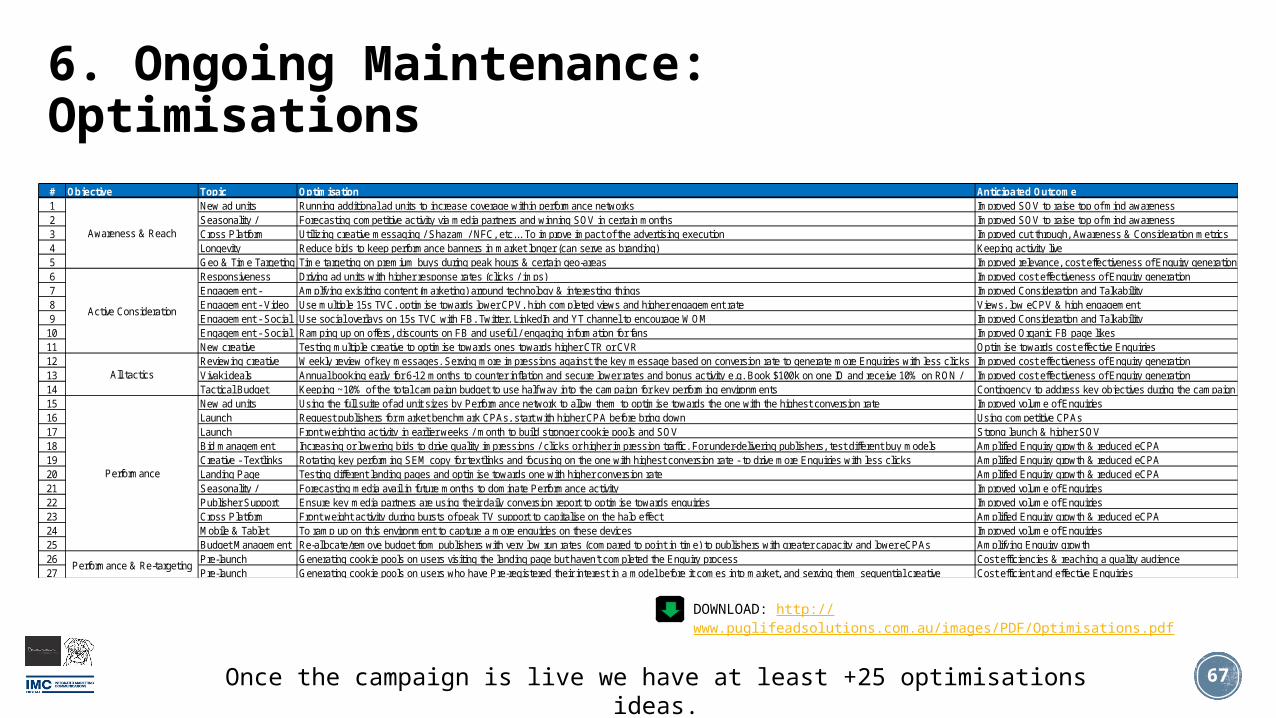

# Objective Topic Optimisation Anticipated Outcome1 New ad units Running additional ad units to increase coverage within performance networks Improved SOV to raise top of mind awareness2 Seasonality / Forecasting competitive activity via media partners and winning SOV in certain months Improved SOV to raise top of mind awareness3 Cross Platform Utilizing creative messaging / Shazam / NFC, etc... To improve impact of the advertising execution Improved cut through, Awareness & Consideration metrics4 Longevity Reduce bids to keep performance banners in market longer (can serve as branding) Keeping activity live5 Geo & Time Targeting Time targeting on premium buys during peak hours & certain geo-areas Improved relevance, cost effectiveness of Enquiry generation6 Responsiveness Driving ad units with higher response rates (clicks / imps) Improved cost effectiveness of Enquiry generation7 Engagement - Amplfying exisiting content (marketing) arround technology & interesting things Improved Consideration and Talkability8 Engagement - Video Use multiple 15s TVC, optimise towards lower CPV, high completed views and higher engagement rate Views, low eCPV & high engagement9 Engagement - Social Use social overlays on 15s TVC with FB, Twitter, LinkedIn and YT channel to encourage WOM Improved Consideration and Talkability

10 Engagement - Social Ramping up on offers, discounts on FB and useful / engaging information for fans Improved Organic FB page likes11 New creative Testing multiple creative to optimise towards ones towards higher CTR or CVR Optimise towards cost effective Enquiries12 Reviewing creative Weekly review of key messages. Serving more impressions against the key message based on conversion rate to generate more Enquiries with less clicks Improved cost effectiveness of Enquiry generation13 Vivaki deals Annual booking early for 6-12 months to counter inflation and secure lower rates and bonus activity e.g. Book $100k on one IO and receive 10% on RON / Improved cost effectiveness of Enquiry generation14 Tactical Budget Keeping ~10% of the total campaign budget to use half way into the campaign for key performing environments Contingency to address key objectives during the campaign15 New ad units Using the full suite of ad unit sizes by Performance network to allow them to optimise towards the one with the highest conversion rate Improved volume of Enquiries16 Launch Request publishers for market benchmark CPAs, start with higher CPA before bring down Using competitive CPAs17 Launch Front weighting activity in earlier weeks / month to build stronger cookie pools and SOV Strong launch & higher SOV18 Bid management Increasing or lowering bids to drive quality impressions / clicks or higher impression traffic. For under-delivering publishers, test different buy models Amplified Enquiry growth & reduced eCPA19 Creative - Textlinks Rotating key performing SEM copy for textlinks and focusing on the one with highest conversion rate - to drive more Enquiries with less clicks Amplified Enquiry growth & reduced eCPA20 Landing Page Testing different landing pages and optimise towards one with higher conversion rate Amplified Enquiry growth & reduced eCPA21 Seasonality / Forecasting media avail in future months to dominate Performance activity Improved volume of Enquiries22 Publisher Support Ensure key media partners are using their daily conversion report to optimise towards enquiries Improved volume of Enquiries23 Cross Platform Front weight activity during bursts of peak TV support to capitalise on the halo effect Amplified Enquiry growth & reduced eCPA24 Mobile & Tablet To ramp up on this environment to capture a more enquiries on these devices Improved volume of Enquiries25 Budget Management Re-allocate/remove budget from publishers with very low run rates (compared to point in time) to publishers with greater capacity and lower eCPAs Amplifying Enquiry growth26 Pre-launch Generating cookie pools on users visiting the landing page but haven't completed the Enquiry process Cost efficiencies & reaching a quality audience27 Pre-launch Generating cookie pools on users who have Pre-registered their interest in a model before it comes into market, and serving them sequential creative Cost efficient and effective Enquiries

Performance & Re-targeting

Performance

All tactics

Active Consideration

Awareness & Reach

6. Ongoing Maintenance: Optimisations

Once the campaign is live we have at least +25 optimisations ideas.

DOWNLOAD: http://www.puglifeadsolutions.com.au/images/PDF/Optimisations.pdf

68

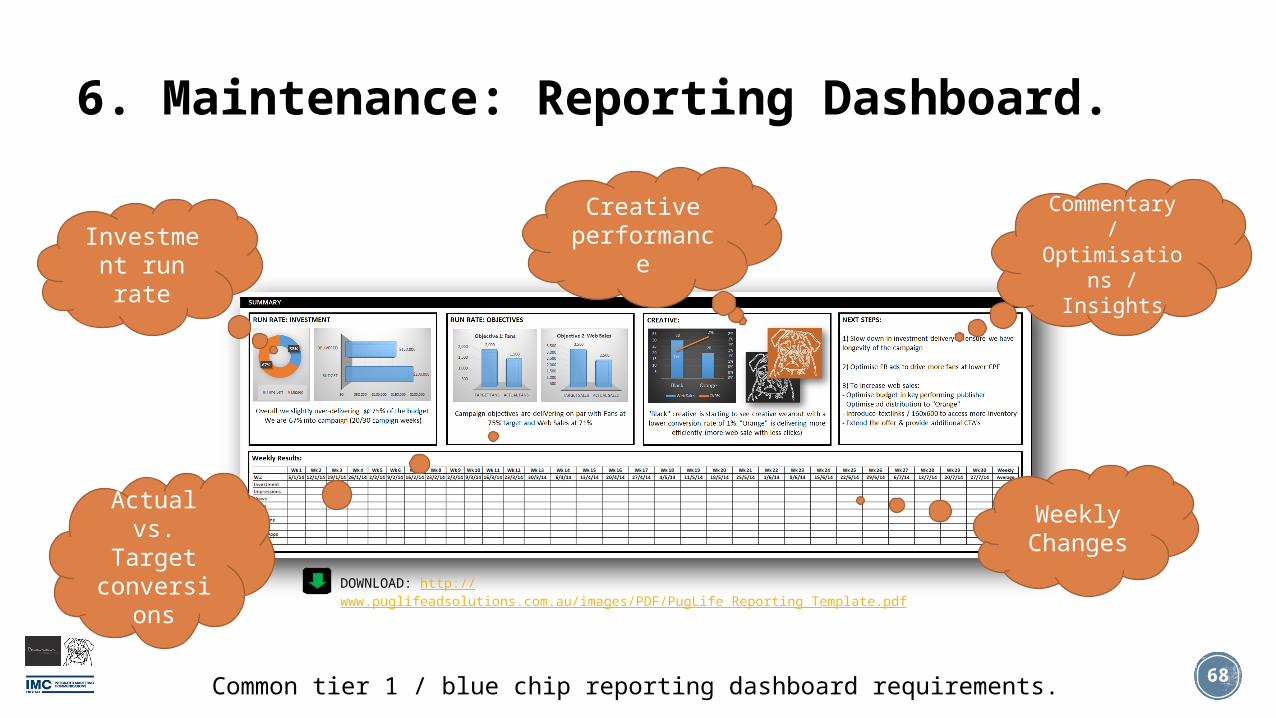

6. Maintenance: Reporting Dashboard.

Common tier 1 / blue chip reporting dashboard requirements.

Investment run rate

Commentary /

Optimisations / Insights

Creative performanc

e

Weekly Changes

Actual vs. Target

conversions

DOWNLOAD: http://www.puglifeadsolutions.com.au/images/PDF/PugLife_Reporting_Template.pdf

69

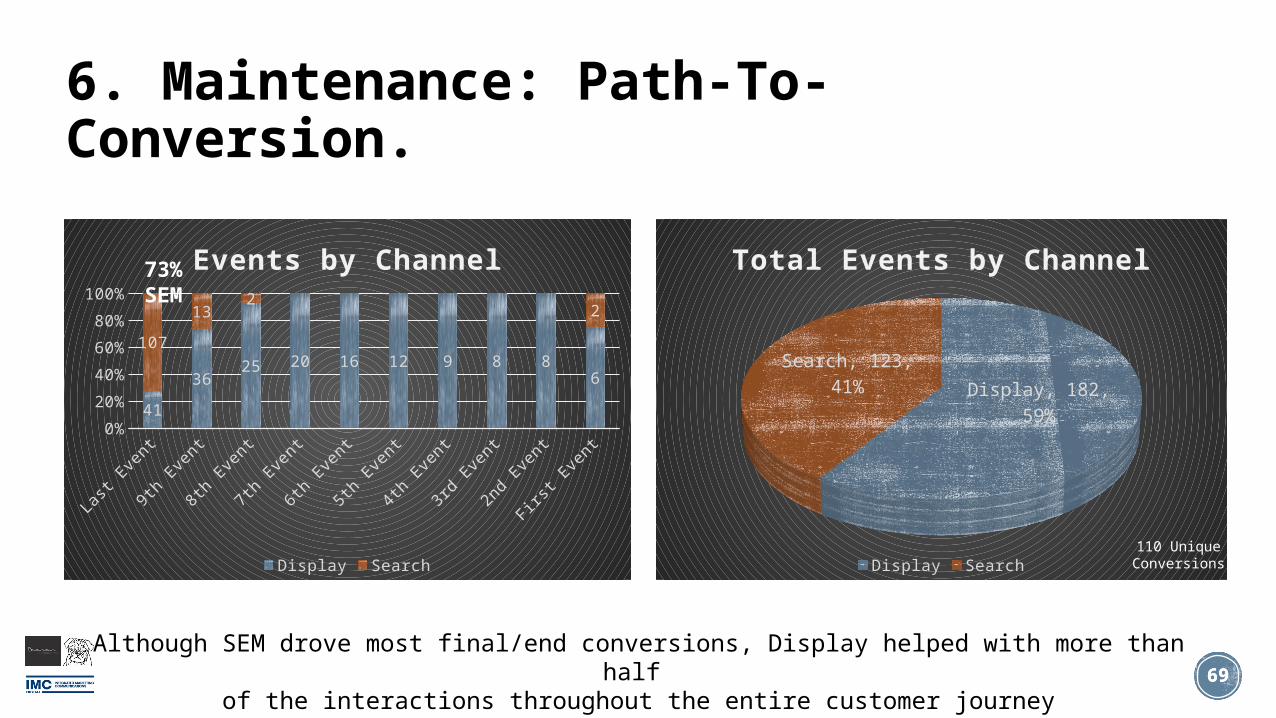

6. Maintenance: Path-To-Conversion.

69

Last Event

9th Event

8th Event

7th Event

6th Event

5th Event

4th Event

3rd Event

2nd Event

First Event

0%10%20%30%40%50%60%70%80%90%

100%

41

3625 20 16 12 9 8 8

6

107

132

2

Events by Channel

Display Search

Display, 182, 59%

Search, 123, 41%

Total Events by Channel

Display Search

73%SEM

110 Unique Conversions

Although SEM drove most final/end conversions, Display helped with more than half of the interactions throughout the entire customer journey

70

Questions & Answers.

THANK YOU!www.facebook.com/DigitalWorkshopAustralia

www.surveymonkey.com/s/V6JH8S8