direct and indirect taxationjnujprdistance.com/assets/lms/lms jnu/b.com/sem iv... · iv/jnu ole...

TRANSCRIPT

Direct and Indirect Taxation

This book is a part of the course by Jaipur National University, Jaipur.This book contains the course content for Direct and Indirect Taxation.

JNU, JaipurFirst Edition 2013

The content in the book is copyright of JNU. All rights reserved.No part of the content may in any form or by any electronic, mechanical, photocopying, recording, or any other means be reproduced, stored in a retrieval system or be broadcast or transmitted without the prior permission of the publisher.

JNU makes reasonable endeavours to ensure content is current and accurate. JNU reserves the right to alter the content whenever the need arises, and to vary it at any time without prior notice.

I/JNU OLE

Index

ContentI. ...................................................................... II

List of FigureII. .......................................................VIII

List of TablesIII. ..........................................................IX

AbbreviationsIV. ......................................................... X

Case StudyV. .............................................................. 122

BibliographyVI. ........................................................ 128

Self Assessment AnswersVII. ................................... 131

Book at a Glance

II/JNU OLE

Contents

Chapter I ....................................................................................................................................................... 1Direct and Indirect Taxes ............................................................................................................................ 1Aim ................................................................................................................................................................ 1Objectives ...................................................................................................................................................... 1Learning outcome .......................................................................................................................................... 11.1 Introduction .............................................................................................................................................. 21.2 Direct Tax in India ................................................................................................................................... 4 1.2.1 Direct Tax in Pre-1922 Era ...................................................................................................... 4 1.2.2 Direct Tax in Post 1922 Era ..................................................................................................... 51.3 Indirect Tax in India ............................................................................................................................... 10 1.3.1 Indirect Taxes during Pre-Reform Era ................................................................................... 10 1.3.2 Indirect Taxes in Post-Reform Era ......................................................................................... 101.4 Highlights of the Direct and Indirect Taxes ............................................................................................111.5 Tax Penalties ...........................................................................................................................................11Summary ..................................................................................................................................................... 12References ................................................................................................................................................... 12Recommended Reading ............................................................................................................................. 12Self Assessment ........................................................................................................................................... 13

Chapter II ................................................................................................................................................... 15Income Tax .................................................................................................................................................. 15Aim .............................................................................................................................................................. 15Objectives .................................................................................................................................................... 15Learning outcome ........................................................................................................................................ 152.1 Income Tax ............................................................................................................................................. 162.2 History of Income Tax in India .............................................................................................................. 16 2.2.1 Income Tax Reforms up to 1991 ............................................................................................ 16 2.2.2 Income Tax Reforms from 1991 Till Today ........................................................................... 162.3 Deficiencies in the Indian Income Tax System ...................................................................................... 172.4 The Elements/Sources of Income Tax Law ........................................................................................... 172.5 Rates of Income-Tax for Assessment Year 2012-13 .............................................................................. 18 2.5.1 Other Assessees ..................................................................................................................... 192.6 Definition of Assessee ............................................................................................................................ 202.7 Heads of Income [Sec. 14] ..................................................................................................................... 25Summary ..................................................................................................................................................... 27References ................................................................................................................................................... 27Recommended Reading ............................................................................................................................. 27Self Assessment ........................................................................................................................................... 28

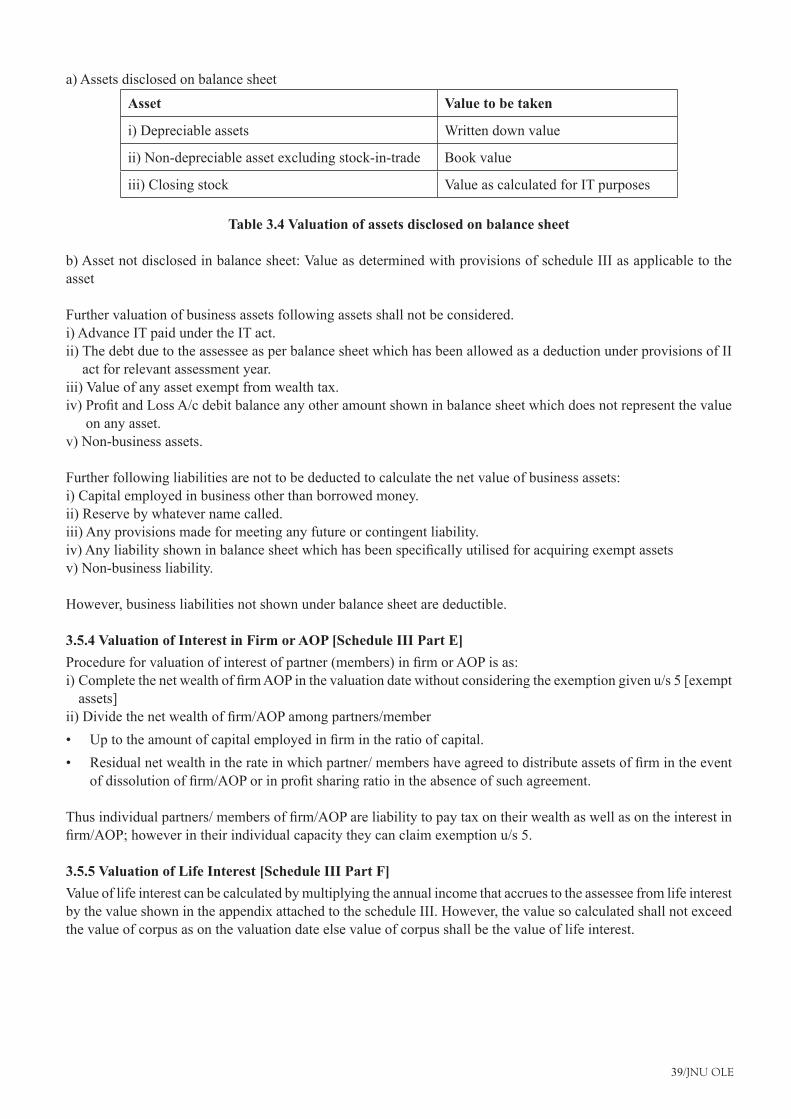

Chapter III .................................................................................................................................................. 30Wealth Tax .................................................................................................................................................. 30Aim .............................................................................................................................................................. 30Objectives .................................................................................................................................................... 30Learning outcome ........................................................................................................................................ 303.1 Introduction ............................................................................................................................................ 313.2 Chargeability .......................................................................................................................................... 313.3 Definitions and Concepts ....................................................................................................................... 31 3.3.1 Assessment Year (A.Y.) [Sec2 (D)] ........................................................................................ 31 3.3.2 Valuation Date [Sec.2 (q)]...................................................................................................... 31 3.3.3 Incidence of Tax ..................................................................................................................... 31 3.3.4 Net Wealth.............................................................................................................................. 32 3.3.5 Assets [Sec.2 (ea)] .................................................................................................................. 32 3.3.6 Deemed Assets [Sec. 4] ......................................................................................................... 33

III/JNU OLE

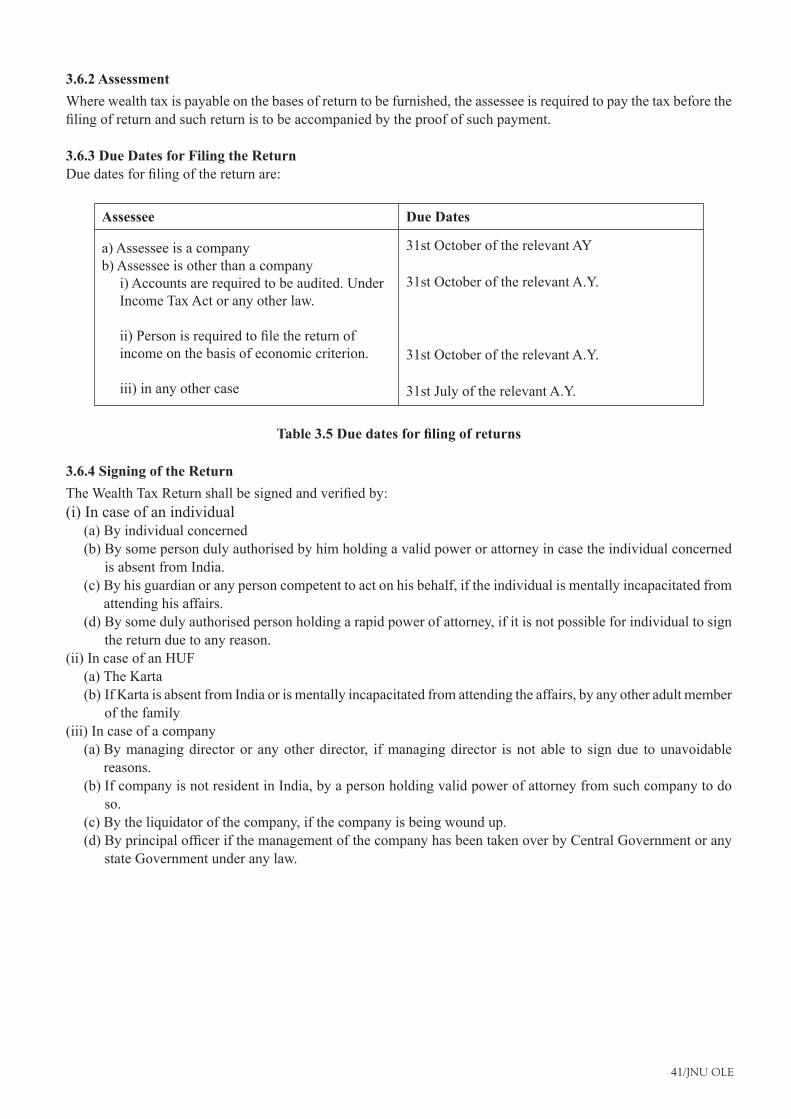

3.3.7 Exempt Assets [Sec 5] ........................................................................................................... 35 3.3.8 Debt Owed ............................................................................................................................. 363.4 Computation of Net Wealth and Wealth Tax .......................................................................................... 363.5 Valuation of Assets ................................................................................................................................. 37 3.5.1 Valuation of a Building .......................................................................................................... 37 3.5.2 Valuation of Self-residential House [Sec.7 (2)] ..................................................................... 38 3.5.3 Valuation of Business Assets [Schedule III Part D] ............................................................... 38 3.5.4 Valuation of Interest in Firm or AOP [Schedule III Part E] ................................................... 39 3.5.5 Valuation of Life Interest [Schedule III Part F] ..................................................................... 39 3.5.6 Valuation of Jewellery [Schedule III Part G] ......................................................................... 40 3.5.7 Valuation of Other Assets [Schedule III Part H] .................................................................... 40 3.5.8 Valuation by Valuation Officer (V.O.) [sec.16A] ................................................................... 403.6 Procedure for Assessment ...................................................................................................................... 40 3.6.1 Wealth Tax Return (Voluntary /Revised) ............................................................................... 40 3.6.2 Assessment ............................................................................................................................. 41 3.6.3 Due Dates for Filing the Return ............................................................................................. 41 3.6.4 Signing of the Return ............................................................................................................. 41Summary ..................................................................................................................................................... 42References ................................................................................................................................................... 42Recommended Reading ............................................................................................................................. 42Self Assessment .......................................................................................................................................... 43

Chapter IV .................................................................................................................................................. 45Gift Tax ....................................................................................................................................................... 45Aim .............................................................................................................................................................. 45Objectives .................................................................................................................................................... 45Learning outcome ........................................................................................................................................ 454.1 Introduction ............................................................................................................................................ 46 4.1.1 Some Important Definitions ................................................................................................... 464.2 Charge of Gift-Tax and Gifts Subject to Such Charge ........................................................................... 46 4.2.1 Charge of Gift-Tax ................................................................................................................. 46 4.2.2 Gifts to Include Certain Transfers .......................................................................................... 46 4.2.3 Exemptions in Respect of Certain Gifts ................................................................................ 47 4.2.4 Value of Gifts, Determined .................................................................................................... 484.3 Gift-Tax Authorities ............................................................................................................................... 48 4.3.1 Gift-tax Officers ..................................................................................................................... 48 4.3.2 Appellate Assistant Commissioners of Gift Tax .................................................................... 49 4.3.3 Commissioners of Gift Tax .................................................................................................... 49 4.3.4 Inspecting Assistant Commissioners of Gift Tax ................................................................... 49 4.3.5 Gift-tax Officers to be Subordinate to the Commissioner of Gift-tax

and the Inspecting Assistant Commissioner of Gift-tax ........................................................ 49 4.3.6 Gift Tax Authorities to Follow Orders of the Board .............................................................. 494.4 Assessment ............................................................................................................................................. 49 4.4.1 Return of Gifts ....................................................................................................................... 49 4.4.2 Return After Due Date and Amendment of Return ................................................................ 50 4.4.3 Assessment ............................................................................................................................. 50 4.4.4 Gift Escaping Assessment ...................................................................................................... 50 4.4.5 Penalty for Default and Concealment .................................................................................... 50 4.4.6 Rebate on Advance Payments ................................................................................................ 514.5 Liability to Assessment in Special Cases ............................................................................................... 51 4.5.1 Tax of Deceased Person Payable by Legal Representative.................................................... 51 4.5.2 Assessment after Partition of a Hindu Undivided Family ..................................................... 52 4.5.3 Liability in Case of a Discontinued Firm or an Association of Persons ................................ 524.6 Appeals, Revisions and References ....................................................................................................... 52 4.6.1 Appeal to the Appellate Assistant Commissioner from Orders of Gift Tax Officers ............. 52

IV/JNU OLE

4.6.2 Appeal to the Appellate Tribunal ........................................................................................... 53 4.6.3 Powers of Commissioner to Revise Orders of Subordinate Authorities ................................ 54 4.6.4 Appeal to the Appellate Tribunal from Orders of Enhancement by Commissioner .............. 54 4.6.5 Reference to High Court ........................................................................................................ 55 4.6.6 Hearing by High Court .......................................................................................................... 55 4.6.7 Appeal to Supreme Court ....................................................................................................... 564.7 Payment and Recovery of Gift-Tax ....................................................................................................... 56 4.7.1 Gift Tax Payable .................................................................................................................... 56 4.7.2 Gift Tax to be Charged on the Property Gifted ...................................................................... 56 4.7.3 Notice of Demand .................................................................................................................. 56 4.7.4 Recovery of Tax and Penalties ............................................................................................... 56 4.7.5 Mode of Recovery ................................................................................................................. 564.8 Miscellaneous ........................................................................................................................................ 57 4.8.1 Rectification of Mistakes ....................................................................................................... 57 4.8.2 Prosecution ............................................................................................................................. 57 4.8.3 Power to Take Evidence on Oath ........................................................................................... 57 4.8.4 Power to Call for Information ................................................................................................ 58 4.8.5 Effect of Transfer of Authorities on Pending Proceedings .................................................... 58 4.8.6 Computation of Period of Limitation ..................................................................................... 58 4.8.7 Service of Notice ................................................................................................................... 58 4.8.8 Prohibition of Disclosure of Information ............................................................................... 58 4.8.9 Bar of Suits in Civil Court ..................................................................................................... 58 4.8.10 Appearance before Gift-tax Authorities by Authorised Representatives ............................. 59 4.8.11 Agreement for Avoidance or Relief of Double Taxation with Respect to Gift Tax ............. 59 4.8.12 Act Not to Apply in Certain Cases ....................................................................................... 59 4.8.13 Power to Make Rules ........................................................................................................... 594.9 The Schedule .......................................................................................................................................... 60 4.9 1 Rates of Gift-Tax.................................................................................................................... 60Summary ..................................................................................................................................................... 61References ................................................................................................................................................... 61Recommended Reading ............................................................................................................................. 62Self Assessment ........................................................................................................................................... 63

Chapter V .................................................................................................................................................... 65Custom Duties ............................................................................................................................................ 65Aim .............................................................................................................................................................. 65Objectives .................................................................................................................................................... 65Learning outcome ........................................................................................................................................ 655.1 Introduction ............................................................................................................................................ 665.2 An Overview of Customs Law ............................................................................................................... 66 5.2.1 Meaning of Customs Duty ..................................................................................................... 66 5.2.2 Development of Customs Law .............................................................................................. 66 5.2.3 Scope and Coverage of Customs Law ................................................................................... 66 5.2.4 Objects of Customs Duty ....................................................................................................... 675.3 Nature of Customs Duty ........................................................................................................................ 67 5.3.1 Taxable Event ......................................................................................................................... 67 5.3.2 Territorial Water of India ....................................................................................................... 67 5.3.3 Indian Customs Water ............................................................................................................ 68 5.3.4 Types of Customs Duties ....................................................................................................... 68 5.3.5 Rate of Duty Applicable ........................................................................................................ 695.4 Definitions and Concepts ....................................................................................................................... 705.5 Classification and Valuation................................................................................................................... 72 5.5.1 Classification of Goods .......................................................................................................... 72 5.5.2 Valuation of Goods ................................................................................................................ 72

V/JNU OLE

Summary ..................................................................................................................................................... 76References ................................................................................................................................................... 76Recommended Reading ............................................................................................................................. 77Self Assessment ........................................................................................................................................... 78

Chapter VI .................................................................................................................................................. 80Central Excise Duty ................................................................................................................................... 80Aim .............................................................................................................................................................. 80Objectives .................................................................................................................................................... 80Learning outcome ........................................................................................................................................ 806.1 Introduction ............................................................................................................................................ 816.2 Nature of Excise Duty ............................................................................................................................ 81 6.2.1 Taxable Event ......................................................................................................................... 81 6.2.2 Rates of Excise Duty .............................................................................................................. 826.3 Chargeability of Excise Duty ................................................................................................................. 826.4 Definitions and Concepts ....................................................................................................................... 82 6.4.1 Factory ................................................................................................................................... 82 6.4.2 Goods ..................................................................................................................................... 82 6.4.3 Manufacture or Production .................................................................................................... 83 6.4.4 Manufacturer .......................................................................................................................... 836.5 Classification of Goods .......................................................................................................................... 83 6.5.1 Scheme of Classification ....................................................................................................... 83 6.5.2 Trade Parlance Theory ........................................................................................................... 846.6 Valuation of Goods................................................................................................................................. 846.7 Registration of Goods ............................................................................................................................ 856.8 Clearance of Goods ................................................................................................................................ 866.9 Duty Payment Provisions ....................................................................................................................... 866.10 Excise Duty Set Off Provisions ........................................................................................................... 87Summary ..................................................................................................................................................... 89References ................................................................................................................................................... 89Recommended Reading ............................................................................................................................. 90Self Assessment ........................................................................................................................................... 91

Chapter VII ................................................................................................................................................ 93Sales Tax ...................................................................................................................................................... 93Aim .............................................................................................................................................................. 93Objectives .................................................................................................................................................... 93Learning outcome ........................................................................................................................................ 937.1 Introduction ............................................................................................................................................ 947.2 Features of Central Sales Tax Act .......................................................................................................... 947.3 Important Definitions ............................................................................................................................. 957.4 Levy and Collection of Tax and Penalties ............................................................................................. 977.5 Principles for Determining Place of Sale or Purchase ........................................................................... 98 7.5.1 In The Course of Interstate Trade .......................................................................................... 98 7.5.2 Sale or Purchase of Goods Outside a State ............................................................................ 99 7.5.3 Sale or Purchase of Goods in the Course of Import and Export [Section 5] ........................ 997.6 Liability to Tax on Inter-state Sales ..................................................................................................... 100 7.6.1 Rates of Tax ......................................................................................................................... 100 7.6.2 Determination of Turnover .................................................................................................. 100 7.6.3 Collection of Tax [Section 9 A] ........................................................................................... 1007.7 Registration of Dealers ........................................................................................................................ 101 7.7.1 Compulsory Registration [Section 7 (1)] ............................................................................. 101 7.7.2 Voluntary Registration [Section 7 (2)] ................................................................................. 101 7.7.3 Procedure for Registration ................................................................................................... 101

VI/JNU OLE

7.7.4 Amendment of Certificate of Registration ........................................................................... 102 7.7.5 Cancellation of Certificate of Registration .......................................................................... 102Summary ................................................................................................................................................... 103References ................................................................................................................................................. 103Recommended Reading ........................................................................................................................... 103Self Assessment ......................................................................................................................................... 104

Chapter VIII ............................................................................................................................................. 106Service Tax ................................................................................................................................................ 106Aim ............................................................................................................................................................ 106Objectives .................................................................................................................................................. 106Learning outcome ...................................................................................................................................... 1068.1 Introduction .......................................................................................................................................... 1078.2 Basics of Service Tax ........................................................................................................................... 107 8.2.1 Nature of Levy of Service Tax ............................................................................................. 108 8.2.2 Taxable Service .................................................................................................................... 108 8.2.3 Service Tax is Destination-based Consumption Tax ........................................................... 108 8.2.4 Service Implies Existence of Two Parties ............................................................................ 108 8.2.5 Cenvat Credit ....................................................................................................................... 108 8.2.6 Rate of Service Tax .............................................................................................................. 108 8.2.7 Service Tax, Education Cess and SAH Education Cess to be Shown Separately in Invoice 109 8.2.8 Taxable Event in Service Tax ............................................................................................... 109 8.2.9 Person Liable to Pay Service Tax ........................................................................................ 109 8.2.10 Services Provided to Non-resident .................................................................................... 109 8.2.11 Services of Insurance Agents ............................................................................................. 109 8.2.12 Consignor/Consignee Paying Freight, in case of GTA Services ........................................ 109 8.2.13 Services of Agents of Mutual Fund ................................................................................... 109 8.2.14 Body Corporate or Firm Located in India Receiving Sponsorship Service ...................... 109 8.2.15 Cenvat Credit of Tax Paid .................................................................................................. 109 8.2.16 Large Taxpayer Unit (LTU) ................................................................................................110 8.2.17 Service on Sub-contract Basis ............................................................................................1108.3 Exemptions from Service Tax ...............................................................................................................110 8.3.1 Small Service Providers ........................................................................................................110 8.3.2 Export of Services .................................................................................................................110 8.3.3 Services to UN Agencies .....................................................................................................110 8.3.4 Services Provided within SEZ .............................................................................................110 8.3.5 Services provided to foreign diplomatic missions, family members of

diplomatic missions, etc. ......................................................................................................110 8.3.6 Services provided by RBI exempt .......................................................................................110 8.3.7 General Exemption to Small Service Providers ...................................................................110 8.3.8 Specific Exemptions .............................................................................................................111 8.3.9 Services Provided to EOU ....................................................................................................113 8.3.10 No Service Tax on Service Provided in J&K ......................................................................1138.4 Classification of Service .......................................................................................................................113 8.4.1 Principles of Classification ...................................................................................................113 8.4.2 Service which has been Specifically Excluded in Definition of

One Service Cannot be Covered Under Another Head .........................................................113 8.4.3 Introduction of New Heading Means Earlier it was not Taxable ..........................................1138.5 Procedures to be Followed for the Administration of Service Tax .......................................................114 8.5.1 Registration Under Service Tax ............................................................................................114 8.5.2 Registration Number (STC Code) ........................................................................................114 8.5.3 Premises Code .......................................................................................................................114 8.5.4 Changes to be Informed in Form ST-1within 30 days .........................................................114 8.5.5 Cancellation/Surrender of Registration ................................................................................114 8.5.6 Centralised Registration ........................................................................................................114

VII/JNU OLE

8.6 Invoice by Service Provider ..................................................................................................................115 8.6.1 Details Required to be Shown in Invoice/Bill/Challan .........................................................115 8.6.2 Education Cess and SAH Education Cess to be Shown Separately .....................................115 8.6.3 Invoice in Case of Continuous Service ................................................................................115 8.6.4 Rounding Up of Tax in Each Invoice not Required ..............................................................116 8.6.5 Advance Payment from Customers ......................................................................................116 8.6.6 Payment of Tax .....................................................................................................................116 8.6.7 Exception in March ..............................................................................................................116 8.6.8 Payment of Tax on Amounts Actually Received .................................................................116 8.6.9 Self Adjustment of Excess Tax Paid in Earlier Period ..........................................................116 8.6.10 Self Adjustment Only in Case of Reasons like Calculation Mistake,

Exact Amount Not Known, etc. ..........................................................................................116 8.6.11 Adjustment upto Rs 2,00,000 Only Permissible ................................................................116 8.6.12 Adjustment in Subsequent Month/Quarter ........................................................................117 8.6.13 Inform Details of Adjustment within 15 Days ...................................................................117 8.6.14 Adjustment in Case of Service Tax on Renting of Immovable Property ............................117 8.6.15 Assessees Having Centralised Registration ........................................................................117 8.6.16 Adjustment If Service Not Provided Partly or Fully ...........................................................1178.7 Payment of Service Tax ........................................................................................................................117 8.7.1 Payment from Cenvat Credit Plus/GAR-7 ............................................................................117 8.7.2 Account Code .......................................................................................................................117 8.7.3 Presentation of Cheque on or Before Due Date is Sufficient ..............................................117 8.7.4 If Last Date is a Holiday .......................................................................................................118 8.7.5 Electronic Accounting System in Excise and Service Tax (EASIEST) ...............................118 8.7.6 Mandatory e-payment if Annual Service Tax Payment Exceeds Rs 50 lakhs ......................118 8.7.7 Mandatory Interest for Late Payment of Service Tax ..........................................................118Summary ....................................................................................................................................................119References ..................................................................................................................................................119Recommended Reading ............................................................................................................................119Self Assessment ......................................................................................................................................... 120

VIII/JNU OLE

List of Figure

Fig. 1.1 Classification of taxes ....................................................................................................................... 4

IX/JNU OLE

List of Tables

Table 1.1 Proposed income tax rates and slabs .............................................................................................. 9Table 2.1 The first schedule of Finance Act ................................................................................................. 18Table 2.2 Income-tax rates for individuals, HUF, AOP/BOI or artificial juridical person .......................... 18Table 2.3 Income-tax rates for a woman resident in India below sixty years .............................................. 19Table 2.4 Income-tax rates for a resident senior citizen (60 years) ............................................................. 19Table 2.5 Income-tax rates for a resident senior citizen (80 years) ............................................................. 19Table 2.6 Income-tax rates applicable to other assessees ............................................................................ 20Table 2.7 Heads of income ........................................................................................................................... 26Table 3.1 Incidence of tax ............................................................................................................................ 31Table 3.2 Computation of net wealth ........................................................................................................... 36Table 3.3 Adjustment for un-built area ........................................................................................................ 38Table 3.4 Valuation of assets disclosed on balance sheet ............................................................................ 39Table 3.5 Due dates for filing of returns ...................................................................................................... 41Table 7.1 Important definitions .................................................................................................................... 97Table 8.1 Taxable services and partial abatement available .......................................................................112

X/JNU OLE

Abbreviations

AOP - Association of PersonsAWB - Airway BillAY - Assessment YearBL - Bill of LadingBTP - Bio-Technology ParkCA - Customs ActCBDT - Central Board of Direct TaxesCBE&C - Central Board of Excise and CustomsCEA - Central Excise ActCEGAT - Customs, Excise & Gold (Control) Appellate TribunalCESTAT - Custom Excise & Service Tax Appellate TribunalCETA - Central Excise Tariff ActCOI - Constitution of IndiaCST - Central Sales TaxCTA - Customs Tariff ActCVD - Countervailing DutyDDT - Dividend Distribution TaxDGFT - Director General of Foreign TradeDTC - Direct Tax CodeEASIEST - Electronic Accounting System in Excise and Service TaxECC - Excise Control CodeEHTP - Electronics Hardware Technology ParkELSS - Equity Linked Savings SchemeEOU - Export Oriented UnitFDI - Foreign Direct InvestmentGDP - Gross Domestic ProductGMR - Gross Maintainable RentGTA - Goods Transport AgencyHSN - Harmonised System of NomenclatureHUF - Hindu Undivided FamilyLR - Lorry ReceiptLTA - Leave Travel AllowanceLTU - Large Taxpayer UnitMODVAT - ModifiedVATMRP - Maximum Retail PriceNCCD - National Calamity Contingent DutyNMR - Net Maintainable RentNPS - New Pension SchemeNSC - NationalSavingsCertificatesPAN - Permanent Account NumberPFY - Polyester Filament YarnPLA - Personal Ledger AccountPY - Previous YearRR - Railway ReceiptSSI - Small Scale IndustrySTC - Service Tax CodeSTP - Software Technology ParkSTT - Securities Transaction TaxTDS - Tax Deducted at SourceTF - Task ForceULIP - Unit Linked Insurance PlansVAT - Value Added TaxWTO - World Trade Organisation

1/JNU OLE

Chapter I

Direct and Indirect Taxes

Aim

The aim of this chapter is to:

introduce the concept of tax•

explicate direct tax in India•

elucidate indirect tax in India•

Objectives

The objectives of this chapter are to:

enlist the characteristics of direct tax code•

explicate direct tax pre and post 1922•

explain direct tax code•

Learning outcome

At the end of this chapter, you will be able to:

identify the merits and demerits of direct and indirect taxes•

understand the history of tax•

determine the highlights of direct and indirect taxes•

Direct and Indirect Taxation

2/JNU OLE

1.1 IntroductionIt is a matter of general belief that taxes on income and wealth are of recent origin, but there is enough evidence to show that taxes on income in some form or the other were levied even in primitive and ancient communities. The origin of the word ‘Tax’ is from ‘Taxation’, which means an estimate. These were levied either on the sale and purchase of merchandise or livestock and were collected in a haphazard manner from time to time. Nearly 2000 years ago, there went out a decree from Caesar Augustus that the entire world should be taxed. In Greece, Germany and Roman Empires, taxes were levied sometime on the basis of turnover and sometimes on occupations. For many centuries, revenue from taxes went to the Monarch. In Northern England, taxes were levied on land and on moveable property, such as the Saladin Title in 1188. Later on, these were supplemented by introduction of poll taxes and indirect taxes known as, ‘Ancient Customs’ which were duties on wool, leather and hides. These levies and taxes in various forms and on various commodities and professions were imposed to meet the needs of the governments, to meet their military and civil expenditures , to ensure safety to the subjects and also to meet the common needs of the citizens like maintenance of roads, administration of justice and such other functions of the State.

A tax is a legally compulsory payment levied by the government on the persons or companies to meet the expenditure incurredonconferringcommonbenefitsuponthepeopleofacountry.Inotherwords,ataxcanalsobedescribedas a compulsory levy, where those who are taxed have to pay the sums irrespective of any corresponding return of services or goods by the government.

Ataxmaybedefinedasa“pecuniaryburdenlaiduponindividualsorpropertyownerstosupportthegovernment,apaymentexactedbythelegislativeauthority.”Atax“isnotavoluntarypaymentordonation,butanenforcedcontribution, exacted pursuant to legislative authority.” Taxes consist of direct taxes and indirect taxes, and may be paid in money or as its labour equivalent (often but not always unpaid labour). India has a well developed taxation structure. The tax system in India is mainly a three tier system which is based between the Central, State Governments and the local government organisations. In most cases, these local bodies include the local councils and the municipalities. According to the Constitution of India, the government has the right to levy taxes on individuals and organisations. However, the constitution states that no one has the right to levy or charge taxes except the authority of law. Whatever tax is being charged has to be backed by the law passed by the legislature or the parliament. Article 246 (seventh schedule) of the Indian Constitution, distributes legislative powers including taxation, between the Parliament and the State Legislature. Schedule VII enumerates these subject matters with the use of three lists:

List - I entailing the areas on which only the parliament is competent to makes laws•List - II entailing the areas on which only the state legislature can make laws and•List - III listing the areas on which both the Parliament and the State Legislature can make laws upon •concurrently

Separate heads of taxation are provided under lists I and II of Seventh Schedule of Indian Constitution. There is no head of taxation in the Concurrent List (Union and the States have no concurrent power of taxation). Any tax levied by the government which is not backed by law or is beyond the powers of the legislating authority may be struck down as unconstitutional. The thirteen heads List-I of Seventh Schedule of Constitution of India covered under Union taxation, on which Parliament enacts the taxation law, are as under:

Taxes on income other than agricultural income•Duties of customs including export duties•Duties of excise on tobacco and other goods manufactured or produced in India except:•

alcoholic liquor for human consumption, and �opium, Indian hemp and other narcotic drugs and narcotics, but including medicinal and toilet preparations �containing alcohol or any substance included in Corporation Tax

Taxes on capital value of assets, exclusive of agricultural land, of individuals and companies, taxes on capital •of companiesEstate duty in respect of property other than agricultural land•Duties in respect of succession to property other than agricultural land•

3/JNU OLE

Terminal taxes on goods or passengers, carried by railway, sea or air; taxes on railway fares and freight•Taxes other than stamp duties on transactions in stock exchanges and futures markets•Taxes on the sale or purchase of newspapers and on advertisements published therein•Taxes on sale or purchase of goods other than newspapers, where such sale or purchase takes place in the course •of inter-state trade or commerceTaxes on the consignment of goods in the course of inter-state trade or commerce•All residuary types of taxes not listed in any of the three lists of Seventh Schedule of Indian Constitution•

The nineteen heads List-II of Seventh Schedule of the Indian Constitution covered under state taxation, on which state legislative enacts the taxation law, are as under:

Land revenue, including the assessment and collection of revenue, the maintenance of land records, survey for •revenue purposes and records of rights, and alienation of revenuesTaxes on agricultural income•Duties in respect of succession to agricultural income•Estate duty in respect of agricultural income•Taxes on lands and buildings•Taxes on mineral rights•Duties of excise for following goods manufactured or produced within the State are:•

alcoholic liquors for human consumption �opium, Indian hemp and other narcotic drugs and narcotics �

Taxes on entry of goods into a local area for consumption, use or sale therein•Taxes on the consumption or sale of electricity•Taxes on the sale or purchase of goods other than newspapers•Taxes on advertisements other than advertisements published in newspapers and advertisements broadcast by •radio or televisionTaxes on goods and passengers carried by roads or on inland waterways•Taxes on vehicles suitable for use on roads•Taxes on animals and boats•Tolls•Taxes on profession, trades, callings and employments•Capitation taxes•Taxes on luxuries, including taxes on entertainments, amusements, betting and gambling•Stamp duty•

Provisions have been made by 73rd Constitutional Amendment, enforced from 24th April, 1993, to levy taxes by the panchayat. A State may by law authorise a panchayat to levy, collect and appropriate taxes, duties, tolls etc. Similarly, the provisions have been made by 74th Constitutional Amendment, enforced from 1st June, 1993, to levy the taxes by the Municipalities. A State Legislature may by law authorise a Municipality to levy, collect and appropriate taxes, duties, tolls, etc.

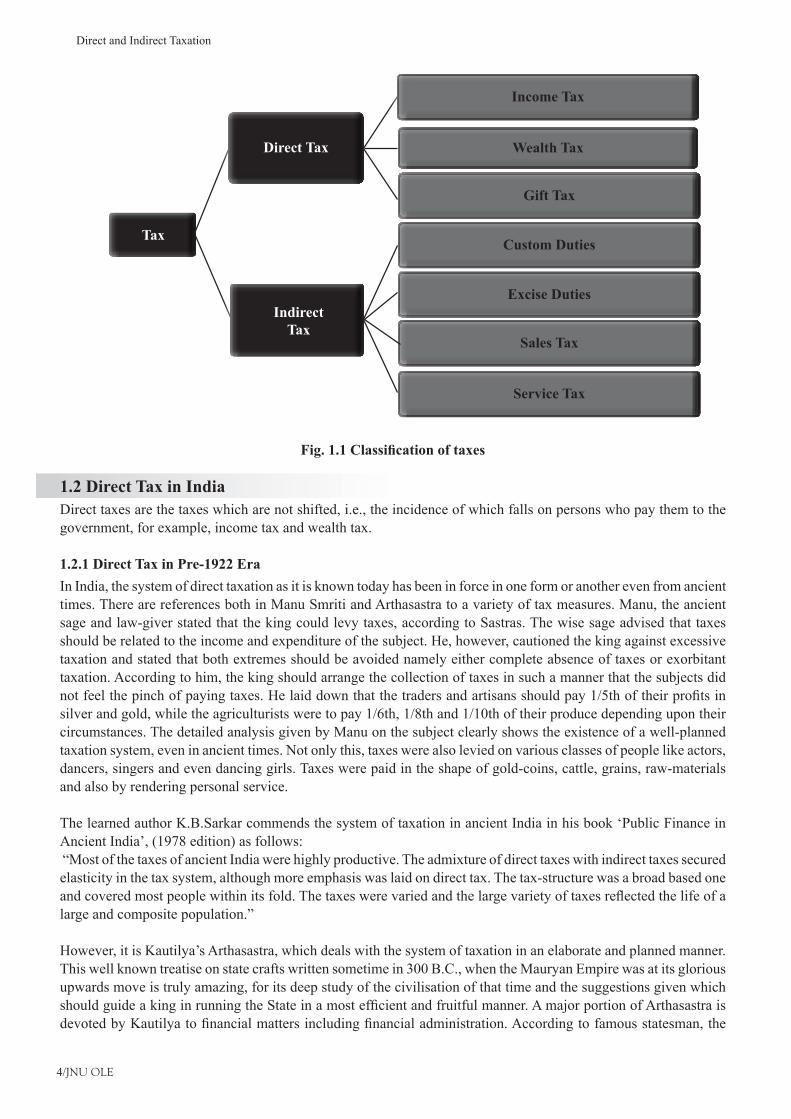

Taxesaremainlyclassifiedinto:Direct tax•Indirect tax•

Direct and Indirect Taxation

4/JNU OLE

Tax

Wealth Tax

Gift Tax

Custom Duties

Excise Duties

Sales Tax

Service Tax

Direct Tax

IndirectTax

Income Tax

Fig. 1.1 Classification of taxes

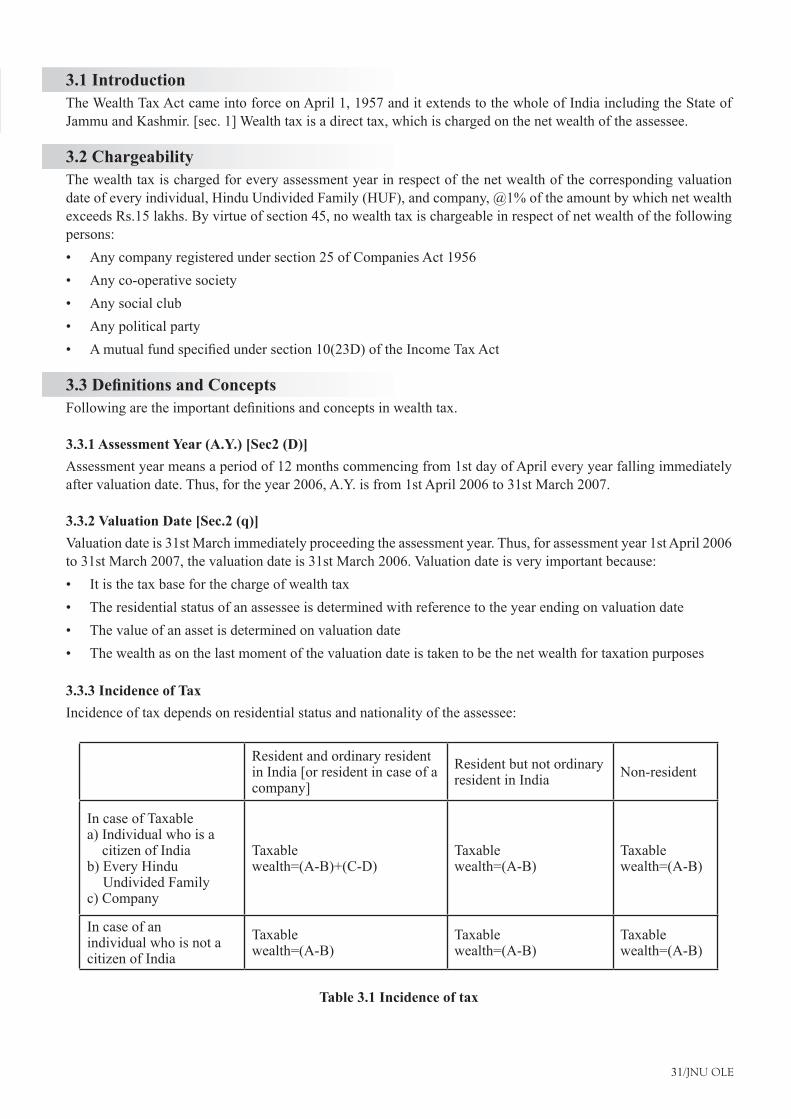

1.2 Direct Tax in IndiaDirect taxes are the taxes which are not shifted, i.e., the incidence of which falls on persons who pay them to the government, for example, income tax and wealth tax.

1.2.1 Direct Tax in Pre-1922 EraIn India, the system of direct taxation as it is known today has been in force in one form or another even from ancient times. There are references both in Manu Smriti and Arthasastra to a variety of tax measures. Manu, the ancient sage and law-giver stated that the king could levy taxes, according to Sastras. The wise sage advised that taxes should be related to the income and expenditure of the subject. He, however, cautioned the king against excessive taxation and stated that both extremes should be avoided namely either complete absence of taxes or exorbitant taxation. According to him, the king should arrange the collection of taxes in such a manner that the subjects did notfeelthepinchofpayingtaxes.Helaiddownthatthetradersandartisansshouldpay1/5thoftheirprofitsinsilver and gold, while the agriculturists were to pay 1/6th, 1/8th and 1/10th of their produce depending upon their circumstances. The detailed analysis given by Manu on the subject clearly shows the existence of a well-planned taxation system, even in ancient times. Not only this, taxes were also levied on various classes of people like actors, dancers, singers and even dancing girls. Taxes were paid in the shape of gold-coins, cattle, grains, raw-materials and also by rendering personal service.

The learned author K.B.Sarkar commends the system of taxation in ancient India in his book ‘Public Finance in Ancient India’, (1978 edition) as follows:“MostofthetaxesofancientIndiawerehighlyproductive.Theadmixtureofdirecttaxeswithindirecttaxessecuredelasticity in the tax system, although more emphasis was laid on direct tax. The tax-structure was a broad based one andcoveredmostpeoplewithinitsfold.Thetaxeswerevariedandthelargevarietyoftaxesreflectedthelifeofalarge and composite population.”

However, it is Kautilya’s Arthasastra, which deals with the system of taxation in an elaborate and planned manner. This well known treatise on state crafts written sometime in 300 B.C., when the Mauryan Empire was at its glorious upwards move is truly amazing, for its deep study of the civilisation of that time and the suggestions given which shouldguideakinginrunningtheStateinamostefficientandfruitfulmanner.AmajorportionofArthasastraisdevotedbyKautilyatofinancialmattersincludingfinancialadministration.Accordingtofamousstatesman,the

5/JNU OLE

Mauryan system, so far as it applied to agriculture, was a sort of state landlordism and the collection of land revenue formed an important source of revenue to the State. The State not only collected a part of the agricultural produce which was normally one sixth but also levied water rates, octroi duties, tolls and customs duties. Taxes were also collected on forest produce as well as from mining of metals, etc.

Kautilya’sArthasastrawasthefirstauthoritativetextonpublicfinance,administrationandthefiscallawsinthiscountry.Hisconceptoftaxrevenueandtheon-taxrevenuewasauniquecontributioninthefieldoftaxadministration.It was he, who gave the tax revenues its due importance in the running of the State and its far-reaching contribution to the prosperity and stability of the empire. It lays down in precise terms the art of state craft, including economic andfinancialadministration.

1.2.2 Direct Tax in Post 1922 EraTherapidchangesinadministrationofdirecttaxes,duringthelastdecades,reflectthehistoryofsocio-economicthinking in India. From 1922 to the present day changes in direct tax laws have been so rapid that except in the bare outlines, the traces of the I.T. Act, 1922 can hardly be seen in the 1961 Act as it stands amended to date. It was but natural, in these circumstances that the set up of the department should not only expand, but undergo structural changes as well.

Changes in administrative set up since the inception of the departmentThe organisational history of the Income-tax Department starts in the year 1922. The Income-tax Act, 1922, gave, forthefirsttime,aspecificnomenclaturetovariousIncome-taxauthorities.Thefoundationofapropersystemof administration was thus laid. In 1924, Central Board of Revenue Act constituted the board as a statutory body with functional responsibilities for the administration of the Income-tax Act. Commissioners of income tax were appointedseparatelyforeachprovinceandassistantcommissionersandincometaxofficerswereprovidedundertheir control. The amendments to the Income Tax Act, in 1939, made two vital structural changes:

Appellatefunctionswereseparatedfromadministrativefunctions;aclassofofficers,knownasappellateassistant•commissioners, thus came into existence. A central charge was created in Bombay. In 1940, with a view to exercising effective control over the progress •andinspectionoftheworkofIncome-taxDepartmentthroughoutIndia,theveryfirstattachedofficeoftheBoard, called Directorate of Inspection (Income Tax) was created. As a result of separation of executive and judicial functions, in 1941, the Appellate Tribunal came into existence. In the same year, a central charge was created in Calcutta also.

WorldWarIIbroughtunusualprofitstobusinessmen.During1940to1947,ExcessProfitsTaxandBusinessProfitsTax were introduced and their administration handed over to the Department (These were later repealed in 1946 and 1949 respectively). In 1951, the 1st Voluntary Disclosure Scheme was brought in. It was during this period, in 1946,thatafew,Group‘A’officersweredirectlyrecruited.Lateronin1953,theGroup‘A’Servicewasformallyconstituted as the ‘Indian Revenue Service’.

This era was characterised by considerable emphasis on development of investigation techniques. In 1947, Taxation on Income (Investigation) Commission was set up which was declared ultra vires by the Supreme Court in 1956 but the necessity of deep investigation had by then been realised. In 1952, the Directorate of Inspection (Investigation) was set up. It was in this year that a new cadre known as Inspectors of Income Tax was created. The increase in ‘largeincome’casesnecessitatedcheckingoftheworkdonebydepartmentalofficers.Thusin1954,theInternalAudit Scheme was introduced in the Income-tax Department.

Asindicatedearlier,in1946,forthefirsttimeafew,Group‘A’officerswererecruitedinthedepartment.Trainingthem was important. The new recruits were sent to Bombay and Calcutta where they were trained, though not in an organised manner. In 1957, I.R.S. (Direct Taxes) Staff College started functioning in Nagpur. Today, this attached officeoftheBoardfunctionsunderaDirector-General.ItiscalledtheNationalAcademyofDirectTaxes.By1963,the I.T. department, burdened with the administration of several other Acts like W.T., G.T., E.D., etc., had expanded to such an extent that it was considered necessary to put it under a separate Board. Consequently, the Central Board of Revenue Act, 1963 was passed. The Central Board of Direct Taxes was constituted, under this Act.

Direct and Indirect Taxation

6/JNU OLE

The developing nature of the economy of the country brought with it both steep rates of taxes and black incomes. In 1965, the Voluntary Disclosure Scheme was brought in followed by the 1975 Disclosure Scheme. Finally, the need for a permanent settlement mechanism resulted in the creation of the Settlement Commission.

A very important administrative change occurred during this period. The recovery of arrears of tax which till 1970 wasthefunctionofStateauthoritieswaspassedontothedepartmentalofficers.AwholenewwingofOfficers-TaxRecoveryOfficerswascreatedandanewcadreofpostofTaxRecoveryCommissionerswasintroducedw.e.f.1-1-1972.

In order to improve the quality of work, in 1977, a new cadre known as IAC (Assessment) and in 1978 another cadreknownasCIT(Appeals)werecreated.TheCommissioners’cadrewasfurtherreorganisedandfivepostsofChief Commissioners (Administration) were created in 1981.

Tax reformsCertain important policy and administrative reforms carried out over the past few years are as follows:

The policy reforms include:•Lowering of rates �Withdrawals/reduction of major incentives �Introduction of measures for presumptive taxation �Simplificationoftaxlaws,particularlyrelatingtocapitalgains �Widening the tax base �

The administrative reforms include:•computerisationinvolvingallotmentofauniqueidentificationnumbertotaxpayerswhichisemergingas �auniquebusinessidentificationnumberrealignment of the available human resources with the changed business needs of the organisation �

ComputerisationComputerisation in the income tax department started with the setting up of the Directorate of Income Tax (Systems) in1981.Initially,computerisationofprocessingofchallanswastakenup.Forthis,3computercentreswerefirstsetup in 1984-85 in metropolitan cities using SN-73 systems. This was later extended to 33 major cities by 1989. The computerised activities were subsequently extended to allotment of PAN under the old series, allotment of TAN, and pay roll accounting. These computer centres used batch process with dumb terminals for data entry.

In 1993, a working group was set up by the government to recommend computerisation of the department. Based on the report of the working group a comprehensive computerisation plan was approved by the government in October, 1993. In pursuance of this, Regional Computer Centres (RCC) were set up in Delhi, Mumbai, and Chennai in 1994-95 withRS6000/59HServers.PCswerefirstprovidedtoofficersinthesecitiesinphases.Theplaninvolvednetworkingof all users on LAN/WAN. Network with leased data circuits were accordingly set up in Delhi, Mumbai and Chennai in Phase-I during 1995-96. A National Computer Centre (NCC) was set up at Delhi in 1996-97. Integrated application software were developed and deployed during 1997-99. Thereafter, Rs 6000 type mid range servers were provided in the other 33 computer centres in various major cities in 1996-97. These were connected to the National Computer Centrethroughleasedlines.PCswereprovidedtoofficersofdifferentleveluptoITOsinstagesbetween1997and1999.InphaseII,officesin57citieswerebroughtonthenetworkandlinkedtoRCCsandNCC.

7/JNU OLE

Restructuring of the Income-tax Department The restructuring of the Income-tax Department was approved by the cabinet in its meeting held on 31-8-2000 to achieve the following objectives:

Increase in effectiveness and productivity•Increase in revenue collection•Improvement in services to tax payers•Reduction in expenditure by downsizing the workforce•Improved career prospects at all levels•Induction of information technology•Standardisation of work norms•

The aforementioned objectives have been sought to be achieved by the department through a multi-pronged strategy of:

re-designing business processes through functionalisation•increasingthenumberofofficerstorationalisethespanofcontrolforbettersupervision,controlandmanagement•of workload and to improve tax-payer servicesre-orient, re-train and re-deploy the workforce with appropriate incentives in the form of career advancement•

Merits of direct taxesMerits of direct tax are as follows:

Imposed according to the ability of the person to pay. (termed as progressive taxation)•Revenue is income elastic as progressive character revenue increases faster than the increase in income.•Create better civic consciousness.•Serves the purpose of transference of income from the rich to the poor.•

Demerits of direct taxesDemerits of direct tax are as follows:

Theabilitytopayisdifficulttodetermine;onlyaroughideacanbeformed.•Because of undeclared sources of income or evasion, the actual payment may not be strictly according to pay.•Necessitate proper maintenance of accounts which some of the tax payers may not be able to do.•Cumbersome assessment procedure requiring expert assistance.•

Direct Tax CodeThe Direct Tax Code seeks to consolidate and amend the law relating to all direct taxes, namely, income-tax, dividend distributiontax,fringebenefittaxandwealth-tax,soastoestablishaneconomicallyefficient,effectiveandequitabledirect tax system which will facilitate voluntary compliance and help increase the tax-GDP ratio. Another objective is to reduce the scope for disputes and minimise litigation.

It is designed to provide stability in the tax regime as it is based on well accepted principles of taxation and best internationalpractices.Itwilleventuallypavethewayforasingleunifiedtaxpayerreportingsystem.ThenewDirect Tax Code (DTC) is said to replace the existing Income Tax Act of 1961 in India. DTC bill was tabled in parliamenton30thAugust,2010.Therearebigchangesnowinmonsoonsessionandthereisnowmuchlessbenefitsascomparedtowhatwereintheoriginalproposal.Duringthebudget2010presentation,thefinanceministerMr.Pranab Mukherjee reiterated his commitment to bringing into fore the new Direct Tax Code (DTC) into force from 1stofApril,2011,butsamecouldnotbefulfilled.

Direct and Indirect Taxation

8/JNU OLE

Some of the provisions of the code are as follows: Single code for direct taxes: All the direct taxes have been brought under a single code and compliance procedures •unified.Thiswilleventuallypavethewayforasingleunifiedtaxpayerreportingsystem.Use of simple language: With the expansion of the economy, the number of taxpayers can be expected to •increasesignificantly.Thebulkofthesetaxpayerswillbesmall,payingmoderateamountsoftax.Therefore,it is necessary to keep the cost of compliance low by facilitating voluntary compliance by them. This is sought to be achieved, inter alia, by using simple language in drafting so as to convey, with clarity, the intent, scope and amplitude of the provision of law. Each sub-section is a short sentence intended to convey only one point. All directions and mandates, to the extent possible, have been conveyed in active voice. Similarly, the provisos and explanations have been eliminated since they are incomprehensible to non-experts. The various conditions embedded in a provision have also been nested. More importantly, keeping in view the fact that a tax law is essentially a commercial law, extensive use of formulae and tables has been made.Reducing the scope for litigation: Wherever possible, attempt is made to avoid ambiguity in the provisions that •invariably gives rise to rival interpretations. The objective is that the tax administrator and the tax payer are adidemontheprovisionsofthelawandtheassessmentresultsinafinalitytothetaxliabilityofthetaxpayer.To further this objective, power has also been delegated to the Central Government/Board to avoid protracted litigation on procedural issues.Flexibility: The structure of the statute has been developed in a manner which is capable of accommodating •the changes in the structure of a growing economy without resorting to frequent amendments. Therefore, to the extentpossible,theessentialandgeneralprincipleshavebeenreflectedinthestatuteandthemattersofdetailare contained in the rules/schedules.Ensurethatthelawcanbereflectedinaform:Formosttaxpayers,particularlythesmallandmarginalcategory,•thetaxlawiswhatisreflectedintheform.Therefore,thestructureofthetaxlawhasbeendesigned,sothatitis capable of being logically reproduced in a form.Consolidation of provisions: In order to enable a better understanding of tax legislation, provisions relating •todefinitions,incentives,procedureandratesoftaxeshavebeenconsolidated.Further,thevariousprovisionshave also been rearranged to make it consistent with the general scheme of the Act.Elimination of regulatory functions: Traditionally, the taxing statute has also been used as a regulatory tool. •However, with regulatory authorities being established in various sectors of the economy, the regulatory function ofthetaxingstatutehasbeenwithdrawn.Thishassignificantlycontributedtothesimplificationexercise.Providing stability: At present, the rates of taxes are stipulated in the Finance Act of the relevant year. Therefore, •there is a certain degree of uncertainty and instability in the prevailing rates of taxes. Under the Code, all rates of taxes are proposed to be prescribed in the First to the Fourth Schedule to the Code itself thereby obviating the need for an annual Finance Bill. The changes in the rates, if any, will be done through appropriate amendments to the Schedule brought before Parliament in the form of an Amendment Bill.

Characteristics of Direct Tax Code (DTC)The following are the characteristics of Direct Tax Code:

Removal of most of the tax saving schemes: DTC removes most of the categories of exempted income. •Unit Linked Insurance Plans (ULIPs), Equity Mutual Funds (ELSS), Term deposits, NSC (National Savings certificates),Long-terminfrastructuresbonds,houseloanprincipalrepayment,stampdutyandregistrationfeesonpurchaseofhousepropertywilllosetaxbenefits.New tax saving schemes: Tax saving based investment limit remains Rs. 1,00,000 but another Rs. 50,000 has •been added just for pure life insurance (Sum insured is at least 20 times the premium paid) , health insurance, mediclaims policies and tuition fees of children. The one lakh investment can now only be done in provident fund, superannuation fund, gratuity fund and new pension scheme (NPS).

9/JNU OLE

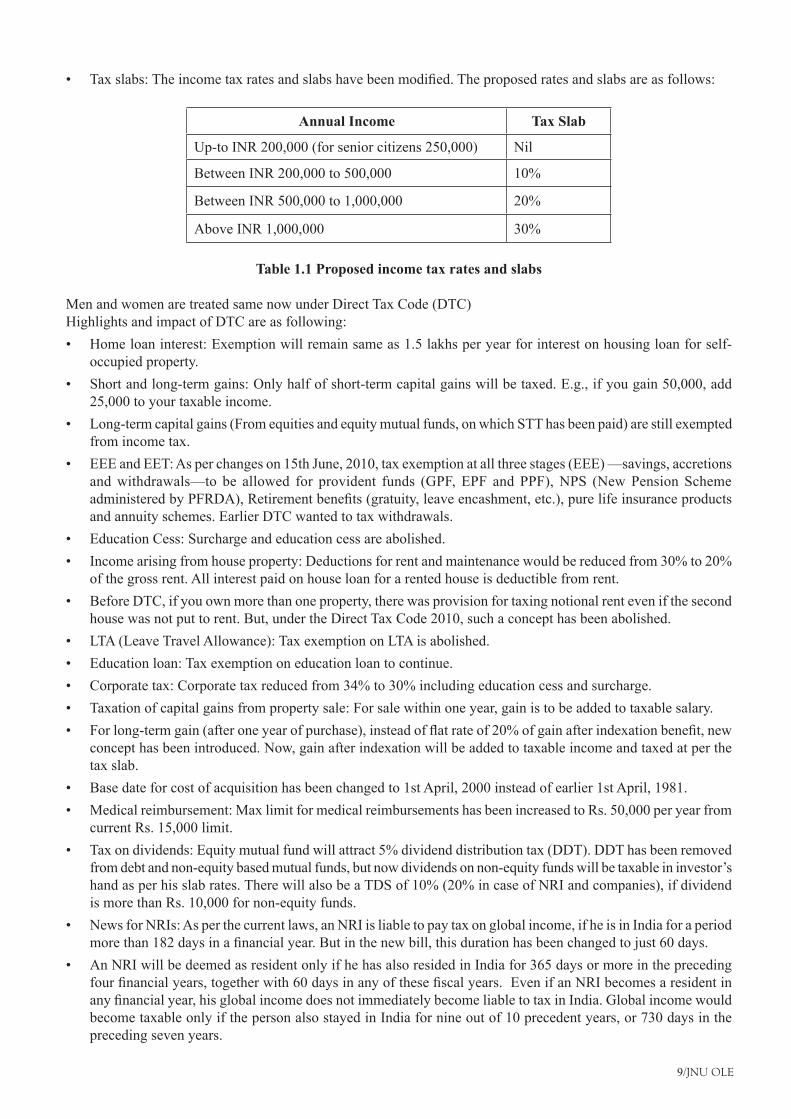

Taxslabs:Theincometaxratesandslabshavebeenmodified.Theproposedratesandslabsareasfollows:•

Annual Income Tax Slab

Up-to INR 200,000 (for senior citizens 250,000) Nil

Between INR 200,000 to 500,000 10%

Between INR 500,000 to 1,000,000 20%

Above INR 1,000,000 30%

Table 1.1 Proposed income tax rates and slabs

Men and women are treated same now under Direct Tax Code (DTC)Highlights and impact of DTC are as following:

Home loan interest: Exemption will remain same as 1.5 lakhs per year for interest on housing loan for self-•occupied property.Short and long-term gains: Only half of short-term capital gains will be taxed. E.g., if you gain 50,000, add •25,000 to your taxable income.Long-term capital gains (From equities and equity mutual funds, on which STT has been paid) are still exempted •from income tax.EEE and EET: As per changes on 15th June, 2010, tax exemption at all three stages (EEE) —savings, accretions •and withdrawals—to be allowed for provident funds (GPF, EPF and PPF), NPS (New Pension Scheme administeredbyPFRDA),Retirementbenefits(gratuity,leaveencashment,etc.),purelifeinsuranceproductsand annuity schemes. Earlier DTC wanted to tax withdrawals.Education Cess: Surcharge and education cess are abolished.•Income arising from house property: Deductions for rent and maintenance would be reduced from 30% to 20% •of the gross rent. All interest paid on house loan for a rented house is deductible from rent.Before DTC, if you own more than one property, there was provision for taxing notional rent even if the second •house was not put to rent. But, under the Direct Tax Code 2010, such a concept has been abolished.LTA (Leave Travel Allowance): Tax exemption on LTA is abolished.•Education loan: Tax exemption on education loan to continue.•Corporate tax: Corporate tax reduced from 34% to 30% including education cess and surcharge.•Taxation of capital gains from property sale: For sale within one year, gain is to be added to taxable salary.•Forlong-termgain(afteroneyearofpurchase),insteadofflatrateof20%ofgainafterindexationbenefit,new•concept has been introduced. Now, gain after indexation will be added to taxable income and taxed at per the tax slab.Base date for cost of acquisition has been changed to 1st April, 2000 instead of earlier 1st April, 1981.•Medical reimbursement: Max limit for medical reimbursements has been increased to Rs. 50,000 per year from •current Rs. 15,000 limit.Tax on dividends: Equity mutual fund will attract 5% dividend distribution tax (DDT). DDT has been removed •from debt and non-equity based mutual funds, but now dividends on non-equity funds will be taxable in investor’s hand as per his slab rates. There will also be a TDS of 10% (20% in case of NRI and companies), if dividend is more than Rs. 10,000 for non-equity funds.News for NRIs: As per the current laws, an NRI is liable to pay tax on global income, if he is in India for a period •morethan182daysinafinancialyear.Butinthenewbill,thisdurationhasbeenchangedtojust60days.An NRI will be deemed as resident only if he has also resided in India for 365 days or more in the preceding •fourfinancialyears,togetherwith60daysinanyofthesefiscalyears.EvenifanNRIbecomesaresidentinanyfinancialyear,hisglobalincomedoesnotimmediatelybecomeliabletotaxinIndia.Globalincomewouldbecome taxable only if the person also stayed in India for nine out of 10 precedent years, or 730 days in the preceding seven years.

Direct and Indirect Taxation

10/JNU OLE

1.3 Indirect Tax in IndiaThe indirect tax in India constitutes a group of tax laws and regulations. The indirect taxes in India are enforced upondifferentactivities includingmanufacturing, tradingand imports. Indirect taxes influenceall thebusinesslines in India. Charge levied by the State on consumption, expenditure, privilege, or right but not on income or property. The indirect tax system in India has undergone extensive reforms for more than two decades. One of the most important reasons for recent tax reforms in many developing and transitional economies has been to evolve a tax system to meet the requirements of international competition

Indirect taxes are those whose burden can be shifted to others, so that those who pay these taxes to the government do not bear the whole burden, but pass it on wholly or partly to others. Indirect taxes are levied on production and sale of commodities and services and small or a large part of the burden of indirect taxes are passed on to the consumers. Excise duties on the product of commodities, sales tax, service tax, customs duty, tax on rail or bus fare are some examples of indirect taxes.

1.3.1 Indirect Taxes during Pre-Reform EraThe indirect tax structure was extremely irrational between the reforms. The Constitution gives the permission to levy a multitude of indirect taxes. But the most important ones are customs and excise duties charged by the Central Government and sales tax excepting inter state sales tax to be charged by the State Government. The indirect taxes levied by the center like customs, excise and central sales tax and the major indirect taxes levied by the states and civic bodies like passenger and goods tax, electricity duty and octroi when taken together did not present a rational system.

1.3.2 Indirect Taxes in Post-Reform EraEven post reforms, the indirect tax regime in India is still in the early stages of growth. Both the Central and State Governments charge a multitude of indirect taxes. The Central Government charges tax on goods at the point of import (Customs Duty), manufacture (Excise Duty), interstate sales (Central Sales Tax or CST) and on provision of services (Service Tax). The state governments charge tax on goods sold within the state (Sales Tax/Value Added Tax or VAT), and on the goods that enter the state (Entry Tax).

In the present scenario, corporate would have to analyse the tax cost involved in a transaction, have enough backup documentation to support their tax positions and keep looking for ways for tax maximisation.

Merits of indirect taxesMerits of indirect taxes are as follows:

Indirect taxes are usually hidden in the prices of goods and services being transacted and, therefore their presence •is not felt so much.If the indirect taxes are properly administered, the chances of tax evasion are less.•Indirect taxes are a powerful tool in moulding the production and investment activities of the economy, i.e., •they can guide the economy in its resource allocation.

Demerits of indirect taxesDemerits of indirect taxes are as follows:

It is claimed and very rightly that these taxes negate the principle of ability- to-pay and are therefore unjust to •the poor. Since one of the objectives is to collect enough revenue, they spread over to cover the items, which are purchased generally by the poor. This makes them regressive in effect.If indirect taxes are heavily imposed on the luxury items then this will only help partially because taxing the •luxuries alone will not yield adequate revenue for the State.Direct taxes take away a part of the purchasing power of the taxpayer and that has the effect of reducing demand •and prices. On the other hand, indirect taxes are added to the sale prices of the taxed goods without touching thepurchasingpowerinthefirstplace.

Theresultisthatintheircaseinflationaryforcesarefedthroughhigherprices,highercostsandwagesandagainhigher prices.

11/JNU OLE

1.4 Highlights of the Direct and Indirect TaxesThe highlights of direct and indirect tax are as follows: