distilleries company of sri lanka plc | annual report 2014

TRANSCRIPT

Distilleries C

ompany of Sri Lanka PLC

| Annual Report 2014 / 15

www.dcslgroup.com

110, Norris Canal Road, Colombo 10, Sri Lanka.Tel. +94 11 5507000 / 2695295-7

Fax: +94 11 2696360 Distilleries Company of Sri Lanka PLC l Annual Report 2014 / 15

DCSL is a legendary company with a heritage of over a hundred years; years we spent fine tuning and refining our classic range of arracks. Over the last two decades, we have diversified our business to include key growth sectors such as plantations, telecommunication, insurance, finance, textiles, power generation, leisure, logistics and media.

Today, as the market leader in the beverage industry, we continue to improve and expand our range of products to suit the changing tastes of consumers, while retaining the traditional flavour of pure coconut arrack.

We are proud of our reputation for quality and excellence, and we pledge to build on our distinguished history to create a distinctive future for the company and its stakeholders.

A distinguished

A distinctive

history.future.

Dist i l ler ies Company of Sr i Lanka PLC2

Contents

3 Highlights of the Year

4 Financial Highlights

6 A Diversified Portfolio of Business Operations

12 Historical Perspectives

14 The Story of Arrack

16 What’s behind Our Continuing Success?

22 Chairman’s Message

26 Board of Directors

30 Group Management

32 DCSL Management

34 Management Discussion & Analysis

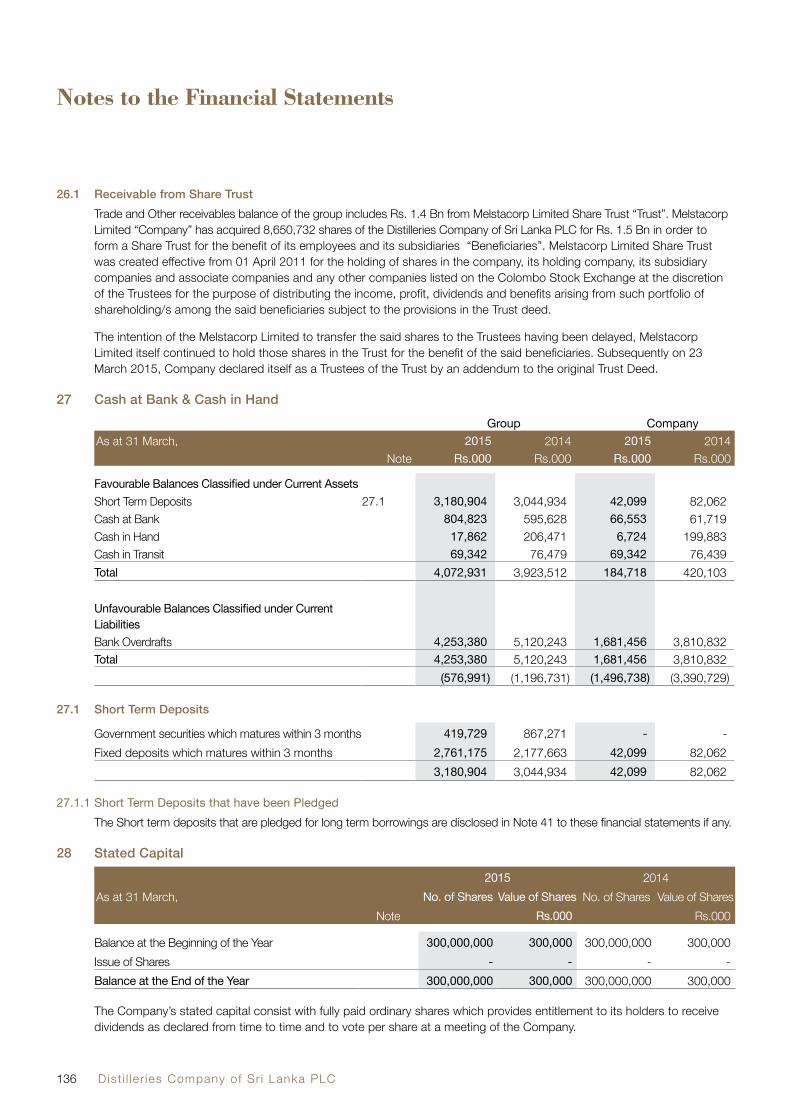

43 Sustainability Report

55 Corporate Governance

67 Enterprise Risk Management

71 Audit Committee Report

73 Remuneration Committee Report

74 Annual Report of the Board of Directors

78 Statement of Directors Responsibility

79 Independent Auditors’ Report

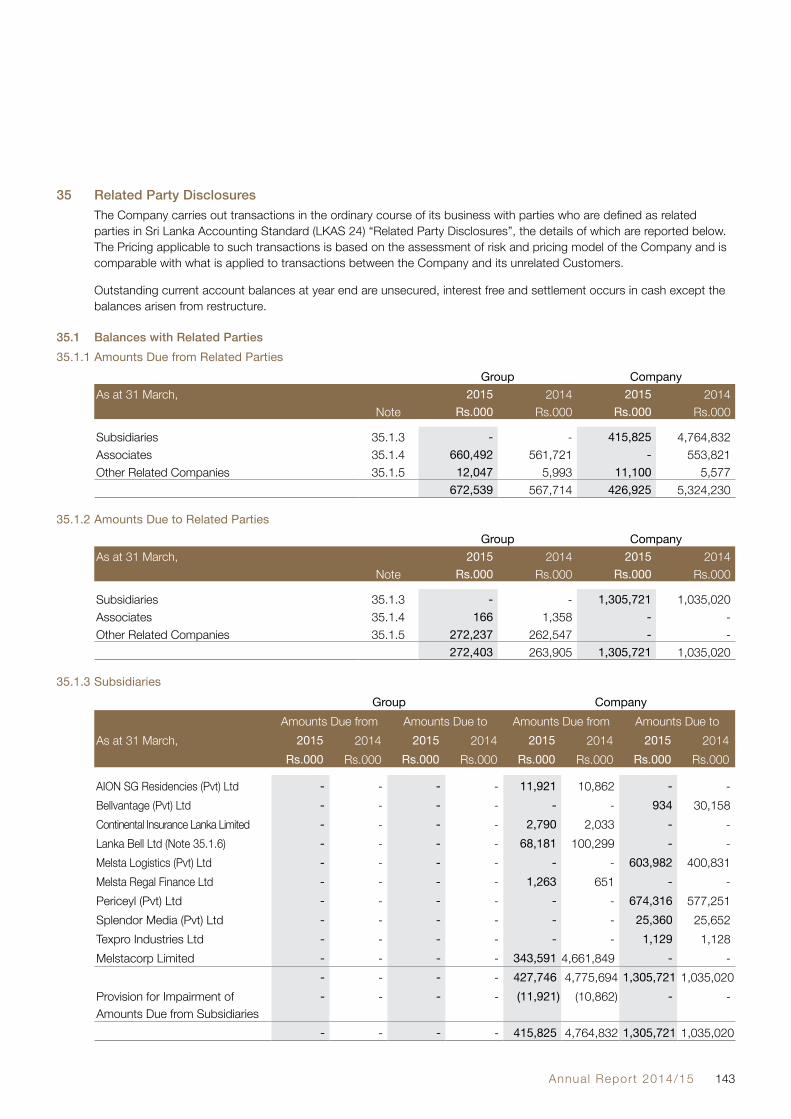

Scan the QR code with your smart deviceto view this report online.

80 Statement of Profit or Loss and Other Comprehensive Income

81 Statement of Financial Position

82 Statement of Changes in Equity

85 Statement of Cash Flows

86 Notes to the Financial Statements

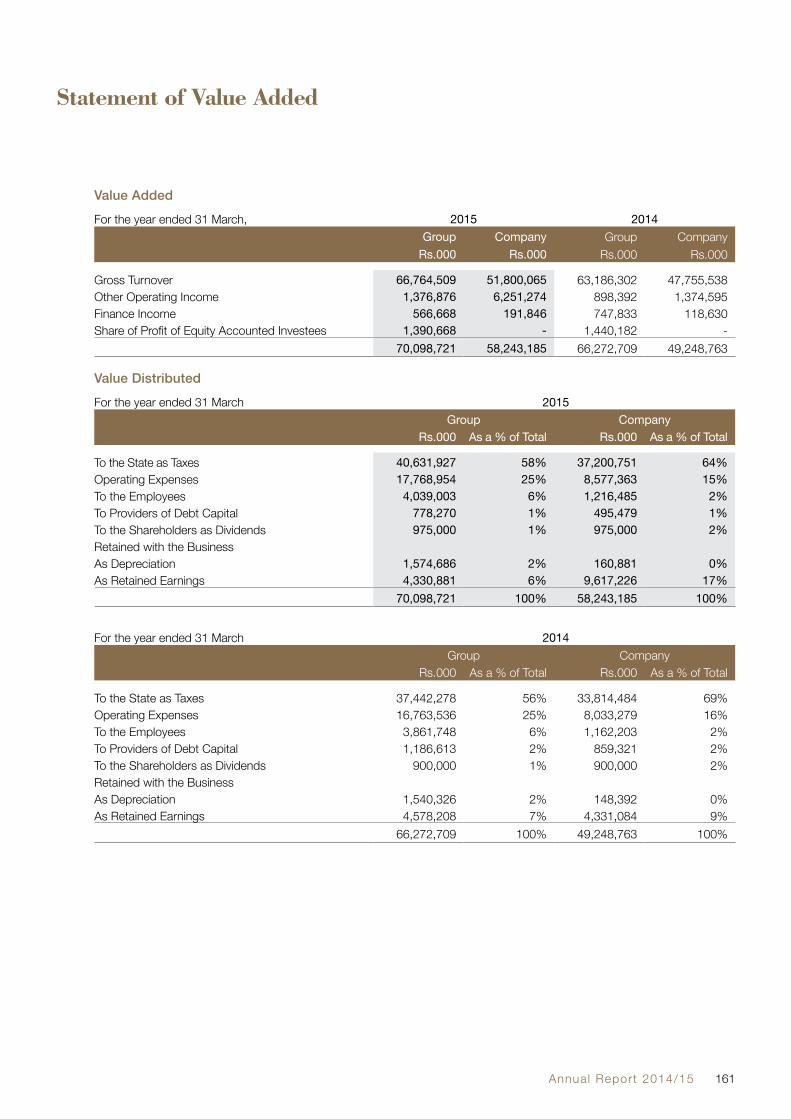

161 Statement of Value Added

162 Details of Real Estate

163 Shareholder Information

165 Ten Year Summary

166 DCSL Management Team

167 Group Directory

173 Notice of Meeting

175 Form of Proxy

177 Attendance Slip

Annual Report 2014/15 3

HighlightsOf The Year

May2014

November 2014

March 2015

November 2014

July 2014

December2014

July2014

Continental Insurance Lanka was assigned ‘A-(lka)’ / Stable by Fitch.

Melsta Regal won the bronze in SLIRTAD People Development Award 2014.

Fitch Rating reaffirmed DCSL a national long term Rating of AAA (lka) / stable outlook - the best & highest entity credit rating for a corporate in Sri Lanka.

DCSL was ranked No. 06 in the Business Today ‘Top Twenty Five’. This was the 16th consecutive year DCSL was listed among corporate heavy weights in the rankings.

Melsta Regal Finance was reaffirmedA+ (lka) / Stable by Fitch, thus signifying a very high credit rating for a finance company.

Melsta Regal Finance opened its Branch in Negombo.

DCSL’s ultra modern state-of-the-art fully automated plant in Seeduwa was declared open by his Excellency Dr. Jürgen Morhard the Ambassador of the Federal Republic of Germany to Sri Lanka

May2014

November 2014

March 2015

November 2014

July 2014

December2014

July2014

Dist i l ler ies Company of Sr i Lanka PLC4

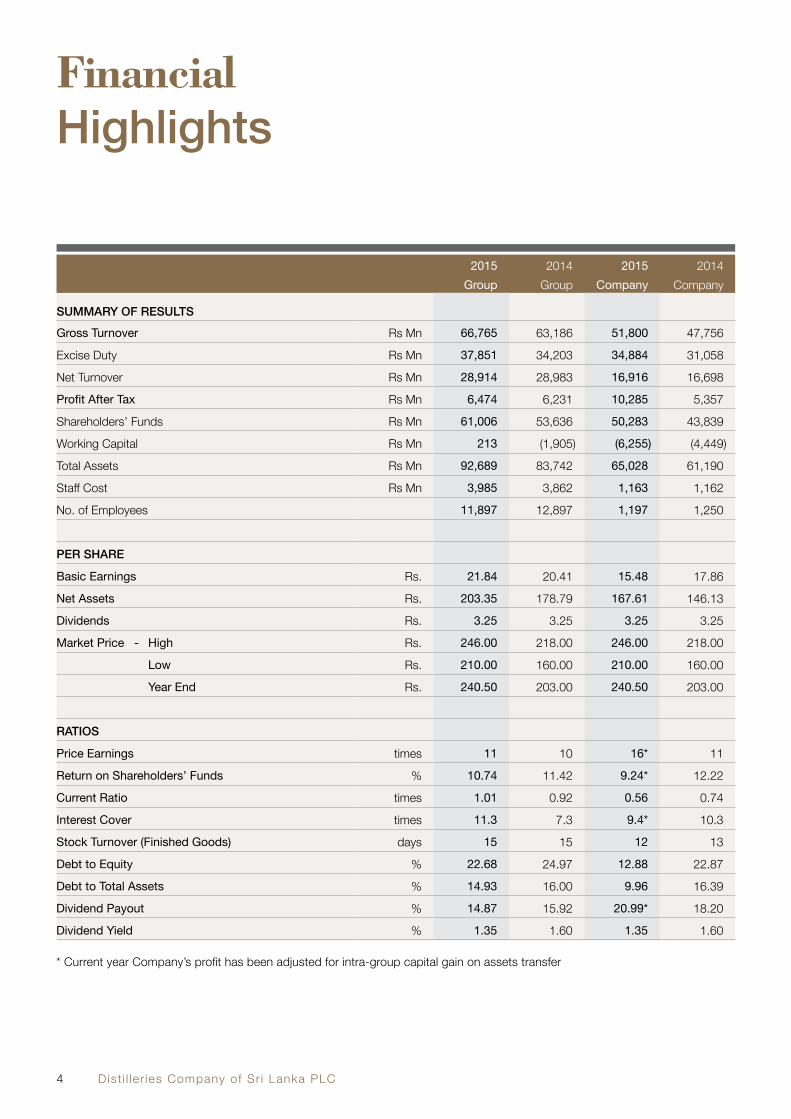

FinancialHighlights

2015 2014 2015 2014Group Group Company Company

SUMMARY OF RESULTS

Gross Turnover Rs Mn 66,765 63,186 51,800 47,756

Excise Duty Rs Mn 37,851 34,203 34,884 31,058

Net Turnover Rs Mn 28,914 28,983 16,916 16,698

Profit After Tax Rs Mn 6,474 6,231 10,285 5,357

Shareholders’ Funds Rs Mn 61,006 53,636 50,283 43,839

Working Capital Rs Mn 213 (1,905) (6,255) (4,449)

Total Assets Rs Mn 92,689 83,742 65,028 61,190

Staff Cost Rs Mn 3,985 3,862 1,163 1,162

No. of Employees 11,897 12,897 1,197 1,250

PER SHARE

Basic Earnings Rs. 21.84 20.41 15.48 17.86

Net Assets Rs. 203.35 178.79 167.61 146.13

Dividends Rs. 3.25 3.25 3.25 3.25

Market Price - High Rs. 246.00 218.00 246.00 218.00

Low Rs. 210.00 160.00 210.00 160.00

Year End Rs. 240.50 203.00 240.50 203.00

RATIOS

Price Earnings times 11 10 16* 11

Return on Shareholders’ Funds % 10.74 11.42 9.24* 12.22

Current Ratio times 1.01 0.92 0.56 0.74

Interest Cover times 11.3 7.3 9.4* 10.3

Stock Turnover (Finished Goods) days 15 15 12 13

Debt to Equity % 22.68 24.97 12.88 22.87

Debt to Total Assets % 14.93 16.00 9.96 16.39

Dividend Payout % 14.87 15.92 20.99* 18.20

Dividend Yield % 1.35 1.60 1.35 1.60

* Current year Company’s profit has been adjusted for intra-group capital gain on assets transfer

Annual Report 2014/15 5

46,451 63,125 65,790 63,186 66,765(Rs. Mn)Gross Turnover - Group

2010/11 2011/12 2012/13 2013/14 2014/15

8,337 6,052 5,258 6,231 6,474(Rs. Mn)Profit After Tax - Group

2010/11 2011/12 2012/13 2013/14 2014/15

59,616 73,355 78,547 83,742 92,689Total Assets - Group(Rs. Mn)

2010/11 2011/12 2012/13 2013/14 2014/15

29,004 39,076 39,850 37,466 41,106Taxes Paid - Group(Rs. Mn)

2010/11 2011/12 2012/13 2013/14 2014/15

Dist i l ler ies Company of Sr i Lanka PLC6

A Diversified Portfolio ofBusiness Operations

Beverages

Plantations

Distillation, Manufactureand Distribution of Liquor Products

Cultivation & Processing of Tea & Rubber

Annual Report 2014/15 7

Telecommunication

InsuranceGeneral Insurance Services - Property, Motor, Marine, General Accident

Voice, Data, Broadband, Hardware, Software andNetworking Solutions

Dist i l ler ies Company of Sr i Lanka PLC8

A Diversified Portfolio ofBusiness Operations

Power GenerationHydro Power Generation

Financial ServicesVariety of innovative Financial Solutions under one roof.

Bogo Power (Pvt) Ltd.

Annual Report 2014/15 9

LogisticsAutomobile Servicing and Logistics

TextilesDyeing and Printing Fabric

Dist i l ler ies Company of Sr i Lanka PLC10

MediaMedia Buying & Creative Services

BPO ServicesBPO, KPO & Call Centre Services

A Diversified Portfolio ofBusiness Operations

Annual Report 2014/15 11

LeisureHotels & Hospitality

BeveragesWines & Spirits

Dist i l ler ies Company of Sr i Lanka PLC12

HistoricalPerspectiveTouching lives for over a century…Present in Sri Lanka for over a century, The Distilleries Company of Sri Lanka PLC (DCSL), is one of the most profitable and well respected corporate entities in the country. Its proud tradition, rich heritage and proven credentials have made the Company a beacon of inspiration for others. Over the past 100 years, our corporate DNA has been strengthened with our values of experience, maturity, innovation, resilience and the determination to succeed.

DCSL’s roots can be traced back to 1913, when the Excise Department of Ceylon, which was initially created as the enforcement authority to distribute and sell liquor products in Sri Lanka, branched out into the distillation and manufacture of liquor products. In 1974, the State Distilleries Corporation was incorporated by statute, to take over this venture, while the Excise Department realigned its operations as a monitoring body. Thus, DCSL has the distinction of being the pioneer distiller in Sri Lanka.

In 1989, under a government policy decision, the State Distilleries Corporation was converted into a limited company. This transfer of ownership took place at the Colombo Stock Exchange (CSE) in 1992, making it the largest transaction in the history of the CSE.

Under its new private management, the Company entered an era of modernisation that witnessed upgrading of machinery and equipment and the introduction of modern management systems and processes. Plant and machinery were upgraded to modern international standards and new technology developed by world renowned experts was introduced. Large investments have also been made in Research and Development (R&D) and in upgrading laboratories.

Annual Report 2014/15 13

These improvements have equipped the Company with top of the line facilities enabling it to produce beverages of international standard. Furthermore, storage facilities and product distribution systems have been upgraded to modern standards with fully computerised systems. A fleet of modern vehicles ensures that customers in even the remotest areas are able to enjoy the best DCSL products delivered island wide. These improvements contributed towards higher production efficiencies across the supply chain. Our people are regularly trained in the best international practices in locations famed for high quality alcohol, such as France, Scotland and Ireland.

Over the years, we have not only grown to become Sri Lanka’s largest distiller, but have been recognised as a leading corporate with the highest quality standards. Despite these achievements and our strong position of business leadership, we continue to look for ways to improve and grow. Since 1992, the Company has not only expanded production, but has also diversified into other non-alcohol related activities.

Today, we are present in all parts of the country, operating under the principle of providing the highest standard of products and services for the people of Sri Lanka, imbued with a vision of uplifting the quality of life of our people. We aim to expand our presence into international markets to render our brand an internationally recognised one.

The newly installed ultra modern state-of-the-art fully automated plant (pictured below) will ensure that only products of the highest quality reach the consumer.

Dist i l ler ies Company of Sr i Lanka PLC14

The Storyof Arrack

The Sri Lankan flavour that lingers on…

The pristine ambrosia-like qualities of Sri Lanka’s unique coconut arrack can be traced back thousands of centuries earlier, finding mention in early literature - “…liquor drawn from the coconut flower”. This delectable beverage is steeped in legend and tradition, making it one of the most prised offerings from Sri Lanka to the world.

The Sri Lankan coconut arrack is believed to be one of the purest, naturally derived alcoholic beverages in the world distilled through a natural fermentation process. Sri Lanka has perfected the technique of making coconut arrack through the years. Today, it has acquired the perfect balance for the discerning palate and coconut arrack reigns as the alcoholic beverage of choice in the country.

The initial step in the process of making coconut arrack is toddy tapping, an age-old vocation which is lovingly passed down from father to son. Toddy Tapping is as much an intricate art as it is a science. Toddy tappers manually extract the toddy from coconut trees which are coupled and girdled by deftly rappelling from tree to tree. Coconut sap or toddy

is obtained by tapping the unopened coconut flower for its nectar. Thereafter, the toddy is collected in earthenware pots. This toddy when fresh contains much sugar, but yeasts, microscopic vegetable organisms soon find their way into it, act on the sugar present and produce alcohol. This process of converting the sugar into alcohol is called fermentation. After a minute filtration process, this liquor is poured into massive casks made of Halmilla wood and are gently transported to our factories for distillation.

The process of distillation comprises of two stages; continuous distillation (patent still distillation) and pot distillation. This distillation process is usually completed within 24 hours. The purified spirit comes out with the distinctive flavour of arrack, ready to be savoured.

The contents of the wooden vats are mixed artfully every fortnight for better aeration and to increase contact with the wood. Herbs and spices from ancient recipes are also added at particular stages, to enhance flavour and mellow the liquor during the crucial maturation process. The maturation process is completed after flavour enhancing and smoothening while ageing in the wooden vats.

Annual Report 2014/15 15

“Sri Lankan coconut arrack, acknowledged as one of the purest alcoholic beverages in the world is extracted by an all-natural fermentation process.”

Finally, spirits of different ages and flavours are blended to create the various DCSL brands, all under the careful supervision of an experienced connoisseur and Master Blender. As the largest coconut arrack distillery in Sri Lanka, possibly even in the world, this golden brew remains our pride and flagship product.

“This delectable beverage is steeped in legend and tradition, making it one of the most prised offerings from Sri Lanka to the world.”

“This delectable beverage is steeped in legend and tradition, making it one of the most prised offerings from Sri Lanka to the world.”

Dist i l ler ies Company of Sr i Lanka PLC16

What’s behindOur ContinuingSuccess?

A 100% coconut spirit, refined, aged and matured in Halmilla vats - giving a woody & natural vanilla flavour

Superior blend of mellow 100% coconut arrack full of character and a distinctive flavour stemming from the traditional process of maturing

Twice distilledin pot stills andmatured slowly inHalmilla vats givinga remarkable tasteand aroma

A blend of coconut spirits and imported neutral spirits bringing herbal flavours with a distinctively rich taste and smooth aroma

Tradition Served with Pride

A blend of 100% aged coconut spirits, well-matured in Halmilla vats to give a taste of oak

Annual Report 2014/15 17

A 100% coconut spirit, matured in Halmilla vats, producing a woody character and exceptional smoothness

A 100% pure coconut spirit, which brings out the full-bodied taste and aroma of desiccated coconut with a subtle sweetness. Best served as a cocktail mixer

Crystal clear and an absolutely pure blend of coconut arrack and neutral spirits giving a tint of fresh lime with a slight burning sensation on your tongue

Finest blend of matured coconut arrack and neutral spirits giving a rich and smooth flavour

A blend of coconut and imported neutral spirits bringing a distinctively rich and smooth flavour

Dist i l ler ies Company of Sr i Lanka PLC18

What’s behindOur ContinuingSuccess?

Exceptional selection of spirits blended to create a great rum, matching international standards

A combination of scotch and fine spirits to produce a rich blend of whisky

Unique premium blended arrack, smooth on the palate with pleasant aromas

Premium blend of malts and fine spirits to produce this classic whisky

Unique variety of imported spirits that combines together to produce an international standard vodka

World Class Blends, Distinctly Sri Lankan

Annual Report 2014/15 19

Flavour of apple with fine imported spirits which provides a rich apple aroma with a smooth apple flavour on the palate

Aged fine French brandy blended with fine spirits matured in vats to enhance the smooth characters of a superior brandy

A blend of finest French brandy merged with fine spirits to bring out a unique flavour that is incomparable

Fine spirits blended with a rich recipe flavoured with lemon

Flavour of mango with fine imported spirits that combines tempting aromas and flavours of rich mango

Dist i l ler ies Company of Sr i Lanka PLC20

GRAND CHAIS DE FRANCE

Founded in 1979, our family company “Les Grand Chais de France” has built its reputation upon the simple motto… “Des Hommes, des terriors, une passion” As the owners of over 30 domains and chateaux in some of the greatest French appellations, as well as being an influential player in the Bordeaux market for Grand Crus Classe, we hope that our customers will benefit from our 20 years experience in wines and spirits

ALBERT BICHOT

“THE EPIC STORY” OF A GREAT HOUSEFrom 1350, the Bichot family was established in Burgundy, with a deer as a symbol. It was only in the XIXth century that the family ventured into the wine business, when Bernard Bichot found in 1831, a wine brokerage. The family heritage has been passed down from father to son until now. Since 1996, Albéric Bichot has represented the 6th generation to run the House.

SOMERTON

The Somerton range reflects the bright fruit flavours that are the hallmark of Australia’s sunny climate regions at incredible value for money.

NAPOLÉON 1875

French traditional brandy is made from the finest wine eaux-de-vie, rigorously selected by the master and aged for a minimum of 12 months in oak casks, until perfectly matured. Its beautiful amber colour, unique woody bouquet, full and soft palate and communicative warmth at the finish, are all thanks to the oak ageing. Can be drunk as an aperitif or after-dinner.

WINCARNIS - TONIC WINE

First produced in 1887, Wincarnis Tonic Wine is a natural tonic, incorporating an unique infusion of herbs and spices. It is also rich in vitamins, especially energy-giving Vitamins. Usually enjoyed straight, Wincarnis Tonic Wine can also be mixed with gin to make a ‘Gin and Win’.

What’s behindOur ContinuingSuccess?Premium Brands from Around the World

Annual Report 2014/15 21

AGAVITA – TEQUILA

Tequila Blanco, or white Tequila, is a Mexican spirit that can be served as a shot or mixed in cocktails. Even though it is colourless, it gives a slight taste of mint and peppery.

CAPE DREAMS

“OUR STORY”The name Cape Dreams reflects our personal aspiration to build an internationally recognised brand whilst making a difference. Our objective is to develop and grow Cape Dreams into a brand synonymous with wines of superb quality, offering an enhanced palate experience aimed at both emerging and established wine markets. Like the Rainbow, Cape Dreams is for the world to share.

MUD HOUSE

Our founders set sail to travel the world; only to fall in love with New Zealand. After planting vines they used the local earth to build their home. Two decades on, we continue to celebrate the spirit of striking out and breaking boundaries. Wherever you are in the world look out for our distinctive wines and celebrate your taste for adventure.

TERRA ANDINABy Sur Andina

From the magnificence of the Andes to the cool waters of the Pacific, Terra Andina use modern and innovative winemaking skills to craft premium wines. Terra Andina is an innovator within the Chilean wine industry. Blending grapes from different valleys with different climates and soil conditions, for its full advantage of richness and diversity of Chile’s different wine growing regions. Fresh and innovative winery free of taboos, Terra Andina is focused on making quality wines to capture full potential of Chilean viticulture.

DOÑA PAULA - LOS CARDOS

Doña Paula is among the main Argentinean wineries that export premium wines; 97% of production is exported to more than 60 countries and the international press has assigned our wines at very high ratings.

Dist i l ler ies Company of Sr i Lanka PLC22

Chairman’sMessageI am pleased to share with you, our valued shareholders, the company’s annual report and audited financial statements for the year ended 31st March 2015.

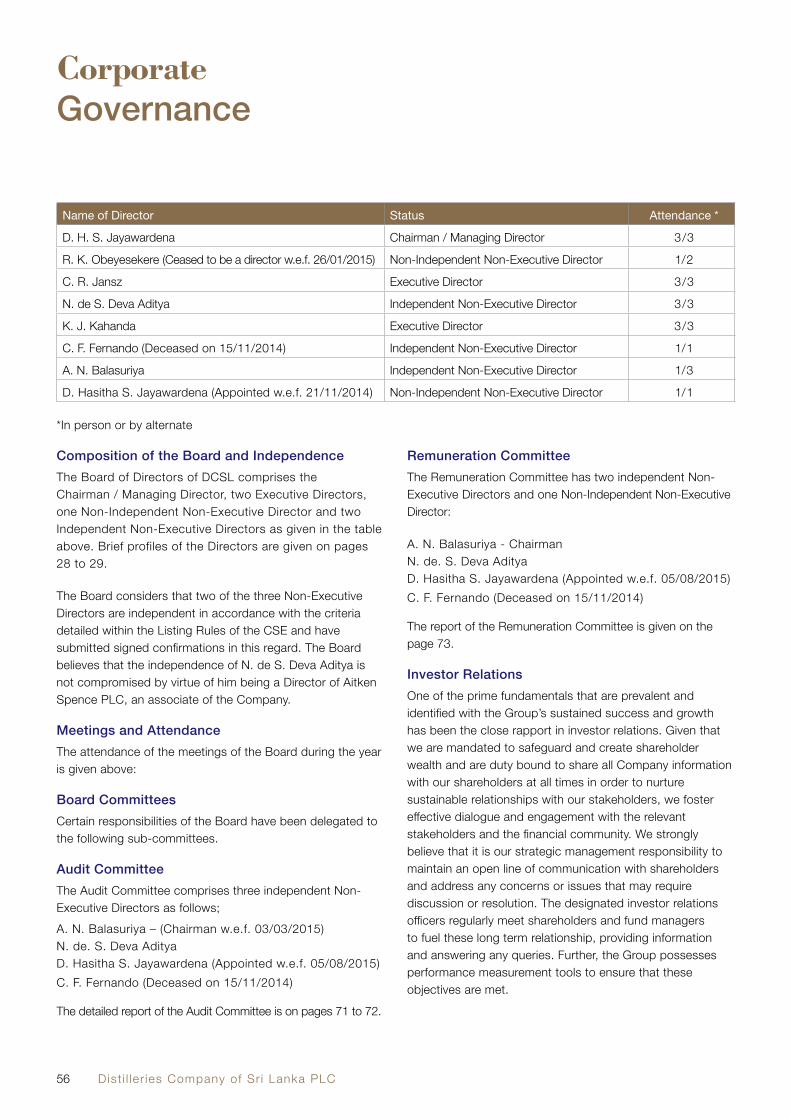

During this period, your company continued its pursuit of growth and expansion. In the face of persisting unfair practices favouring a few unscrupulous elements, we continue to operate in an industry which has not offered a level playing field in years. With the determination and hard work of our staff, we have managed to deliver value to our shareholders and other stakeholders without compromising on our credo of fair play and ethical operations.

Although key indicators of the economy were favourable for growth, due to these reasons your company was unable to maximise the potential we know we can deliver.

Macro Economic ClimateDespite an uncertain global economy and rising geo political tension in the Middle-East, Sri Lanka exhibited a strong performance against key economic indicators. GDP growth rate maintained its steady momentum, making ours one of the few economies displaying consistent growth in the region. All sectors of the economy performed strongly except for agriculture, which was adversely impacted by erratic weather patterns. Meanwhile, the regulators continued to ease monetary policy, resulting in low interest rates and record low inflation levels during the period. Sri Lanka’s economic growth forecast for the next year seems optimistic, alongside a favourable uptick in the global economy as well.

Group Financial Performance During the financial year under consideration, Gross Revenue of the Group was Rs. 66.8 Bn, while the Group Profit after Tax for the year was Rs. 6.5 Bn. The Group contributed Rs. 41.1 Bn in taxes to the national exchequer during this financial year.

Persistent Obstacles in our PathAs the market leader in our segment and a company in existence for over 100 years, DCSL’s credentials as a responsible corporate citizen are beyond question. However, we are sorry to witness the continuation of unfair and illegal practices in the industry, taking place under the very nose of the enforcement authorities despite our repeated efforts to bring these to their notice. Although all our representations to authorities seem to be falling on deaf ears, we will continue to spotlight these negative practices which are harming the industry and preventing it from achieving the status of an industry that is a key contributor to the state revenue.

DCSL adheres to all the laws and tenets imposed on the alcoholic beverage business and is one of the largest tax payers in the country. However, when it comes to some others in the industry, the opposite holds true. Malpractices such as non-invoiced and tax unpaid alcohol abound, negating the rules and regulations on which a legitimate alcoholic beverage businesses is based. Although this business might be looked at negatively by certain socio-religious quarters, it is a legitimate industry, licensed by the state. However, some unscrupulous elements bring infamy and allegations of corruption to the industry, due to their illegal practices, which impact legitimate businesses such as ours, which pay all taxes in accordance with the laws of the land. What is perplexing is the fact that the state refuses to intervene, despite losing millions of rupees in excise taxes due to these players who evade such taxes through various devious means.

A new breed of unscrupulous traders has emerged in the recent past. With the help of law makers, they import ethanol under the guise of other products and thereby flood the market. Law makers also became producers, and sadly, the department tasked with policing the industry also helps such people to produce tax unpaid liquor. Licenses were granted to a few law makers to import ethanol under the guise of eau de cologne which leaked into the market, while DCSL maintained its quality and price. These imports went into unlawful hands and the market was flooded with low retail price products which could not have been possible had all the legitimate duties been paid.

The industry as a whole is highly regulated and as a legitimate entity, we comply with all the rules and regulations laid down by the National Authority on Tobacco and Alcohol (NATA) Act. The act mandates that companies will not advertise or promote their products in any form and in any medium; that they will not directly or indirectly lure young people into alcoholism; and never, under any circumstance, target children. However, most of the players in the industry openly flout the NATA Act by indulging in various barely disguised advertising and promotional activities while authorities repeatedly turn a Nelsonian eye to such illegal practices.

Rs. 41 BnTaxes paid

11,897Employees

Annual Report 2014/15 23

D. H. S. JayawardenaChairman / Managing Director

Dist i l ler ies Company of Sr i Lanka PLC24

Chairman’sMessageA unique and traditional Sri Lankan industry which has been passed down generation to generation over the centuries is today an endangered industry. This sorry state of affairs is the direct result of the proliferation of illegal, artificial toddy manufacturers, who feed the illegal alcoholic beverage business by producing cheap artificial toddy, unfit for human consumption. As a result, traditional toddy suppliers, who are unable to compete with such low cost artificial toddy, are finding that their rich legacy is becoming unsustainable. Amidst the barren wasteland of illegal practices and disregard for tradition, DCSL remains the only company producing 100% natural coconut arrack using 100% pure coconut toddy distilled at our own distilleries, providing consumers a 100% natural product. DCSL has strengthened procedures by appointing qualified personnel to inspect every barrel of toddy, in order to detect any form of adulteration and extraneous matter in the toddy. We are single-handedly nurturing the traditional toddy tapping custom although only a handful of such genuine tappers remain in existence. Even though we lack trained toddy tappers, the Department of Excise is not focusing on this issue to help the industry and to ensure the production of genuine coconut toddy.

All around us we see that the rest of the toddy market is transforming into an artificial one, where vast quantities of sugar, ammonia, yeast, salt, rotten potatoes, sugar syrup and remnants of toddy sludge are being used in the manufacture of artificial toddy. The addition of these unhealthy and artificial ingredients renders the natural form of fermentation extinct, putting consumers at risk. This is a calamity in the industry and it is high time that the generations old Excise Ordinance is evaluated and modified to meet the challenges of the present day.

While one may overlook the responses from the Government bodies, it is not possible for responsible corporate citizens in the country to remain silent and watch the open transgression of the law by those who should be protecting and upholding the law. The enactment of Excise Notification 926, whereby a transferor could transfer a FL(4) license to a transferee for Rs. 1,500,000/- and Rs. 200,000/- for other types of licenses, opened the flood gates for unprincipled manufacturers who embraced this unfortunate regulation and obtained licenses in the names of their kith and kin, thereby finding a channel to dispose of their non-invoiced, tax unpaid liquor with ease. It is pathetic to observe that although the conditions of the manufacturing license indicate that a manufacturer is prohibited from holding any interest in the retail sale of liquor, this condition is blatantly violated under the very noses of the excise authorities. Some manufacturers have taken over 233 retail licenses out of a total of 1000, approximately 23%, which indicates how rampant corruption has spread like a disease in the sector. It has come to light

that some unscrupulous manufacturers are planning to purchase the remaining retail licenses at exorbitant prices which will further impact state revenue from excise earnings. It is disheartening to note that although this industry provides the state with enormous revenue, the Government does little or nothing to prevent such abuses.

It is observed that in the North and East tax unpaid and non invoiced liquor is largely available in the market, at prices 30% to 40% less than a product on which all taxes have been paid. Such businesses are carried out with the help of the officers of the state acting on behalf of these criminal parties instead of defending state laws. DCSL has brought these issues to the notice of the regulator who turns a blind eye and is yet to take any measured steps to bring wrongdoers to book.

In the recent past, a shocking disclosure surfaced-when perusing the price list of some players. The wholesale price of a 750ml bottle of Extra Special Arrack is Rs. 688/- . This is not credible when the excise duty component alone is Rs. 658/- leaving only Rs. 29/- to cover the cost of spirits, label, bottle, cap, labour, transport, overheads and profit. Obviously these products have not been declared for excise duties and eventually find their way to the retail liquor shops run by these unscrupulous manufacturers, depriving billions of rupees of revenue to state coffers. In addition to this fraud, in order to maximise their profit, these parties channel such products to the market offering very attractive incentives to licensees.

Considering that we have successfully sustained our operations for over 100 years, your company remains invested in and upbeat about the prospects for the alcoholic beverage sector. During this year, our Rs. 6 Bn investment in a state-of-the-art blending and bottling plant has resulted in improved capacity, modern packaging and presentation and greater prevention of the possibility of adulteration of our products. This ultra modern plant has fully automated manufacturing operations resulting in higher productivity and greater efficiency at reduced cost to meet current demand.

DCSL complies with stringent quality controls along its product chain. The company has installed advanced R&D capability in modern fully-equipped laboratories to ensure that its products are at the cutting edge of the industry. We continue to enjoy Fitch Ratings assigned long term rating of AAA (lka) with a stable outlook, the highest possible credit rating, which places your company amongst the few exclusive corporates in Sri Lanka who enjoy such ratings. Our fully-owned subsidiary, Periceyl, is working tirelessly to provide customers with the trendiest portfolio of brands, both local and foreign.

Annual Report 2014/15 25

Diversified PerformanceWith regard to other Group business interests, our telecommunication arm Lanka Bell recorded a loss due to challenges experienced in the sector. However, Lanka Bell has a positive EBITDA despite many companies reporting negative growth. We have already taken initiatives to break-even and have established foreign collaboration to enhance the product. We are buoyed by future prospects for the business as we have acquired 4G LTE technology, which will propel the company to the forefront of the country’s data revolution. I expect the company to make a positive contribution to Group revenue in the future by becoming a front runner in the data sector.

Meanwhile, Balangoda Plantations experienced a drop in revenue to Rs. 3 Bn and had an adverse effect on the profitability contributing to a pre-tax loss of Rs. 106 Mn against a backdrop of wage increases and drop in revenue. We are glad to state that our hydro power project, Bogo Power, which was commissioned in December 2011, is now yielding encouraging results for the Group. DCSL Group is also encouraged by the progressive results achieved by our key associate company, Aitken Spence during the financial year.

In July 2014, the Group increased its investment in Continental Insurance to Rs. 750 Mn Established as one of the most innovative and dynamic insurance companies in Sri Lanka, Continental Insurance holds great potential for the future and its (A-) Fitch rating reflects the financial stability of the Company. The insurance industry is a fiercely contested space. However, companies that can position themselves perfectly have much potential for growth.

Melsta Regal Finance embarked on its second year of operations with a focus on penetrating the market with innovative financial solutions. Melsta Regal, A+(lka) rated finance house, achieved noteworthy milestones in terms of asset size and achieved a balance sheet size of Rs 5 Bn and earned pre-tax profit of Rs. 100 Mn during the year.

The uncertainties surrounding the status of our subsidiary, Pelwatte Sugar Industries continues to weigh upon the Group. Following the occupation of the factory by state officials, the ownership of this property remains unresolved. The Group has not changed its position, advocated since the occurrence of this unfortunate incident, of being the legal owner of the property and as such we have communicated our views to the Treasury. However, as a precautionary measure, the Group has also lodged an official claim with the Compensation Tribunal appointed by the State. We hope that some clarity regarding this untoward situation would be forthcoming during the new financial year, after the General Election.

With regard to Sri Lanka Insurance Corporation Ltd. (SLIC), even after a lapse of 6 years, we still await the payment of profit earned during DCSL Group’s tenure at the helm of SLIC. We are hopeful that the profit earned, which has to be paid to us as per the Supreme Court directive, will be reimbursed to us as early as possible.

DCSL has complied with the Listing Rules of the Colombo Stock Exchange and the Code of Best Practices on Corporate Governance issued by the Securities and Exchange Commission and the Institute of Chartered Accountants of Sri Lanka. We are committed to the furtherance of best Corporate Governance principles. The measures taken in this regard are set out in the Corporate Governance Report.

AppreciationI take this opportunity to thank the Board of Directors for their unstinted support and the management and staff for their single-minded pursuit of profitability for the Group against all odds.

During the year, the Board was deeply saddened at the passing away of our fellow director Mr. C. F. Fernando who was the chairman of the Audit Committee too. His tenure on the Board was of much value to the Company.

We also lost a valued team member with the demise of Maj. Gen. Siri Peiris (Retd.), Head of Southern Region who was with us over 15 years and who performed a wonderful job to keep the DCSL flag flying despite the stiff competition from the illegal operators.

I would also like to thank our valued shareholders for placing their confidence in the Group. Our strength lies in the loyalty shown by our customer base and other stakeholders, who continue to inspire us to retain our position as one of the most valuable and respected corporate entities in the country.

D. H. S. Jayawardena Chairman / Managing Director

25 August 2015

Dist i l ler ies Company of Sr i Lanka PLC26

Board ofDirectors

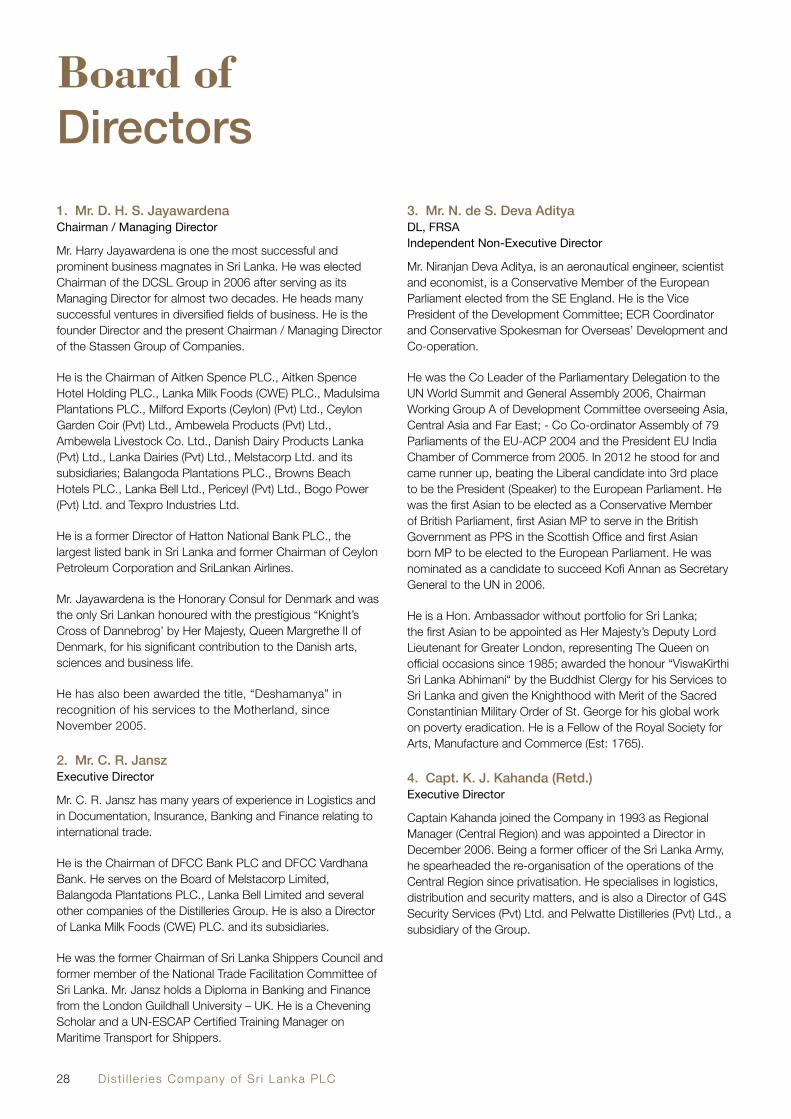

1. Mr. D. H. S. Jayawardena Chairman / Managing Director

2. Mr. C. R. Jansz Executive Director

3. Mr. N. de S. Deva Aditya DL, FRSA Independent Non-Executive Director

4. Capt. K. J. Kahanda (Retd.) Executive Director

1.

3.

2.

4.

1. Mr. D. H. S. Jayawardena Chairman / Managing Director

2. Mr. C. R. Jansz Executive Director

3. Mr. N. de S. Deva Aditya DL, FRSA Independent Non-Executive Director

4. Capt. K. J. Kahanda (Retd.) Executive Director

Annual Report 2014/15 27

5. Dr. Naomal Balasuriya MBBS [Sri Lanka], MBA [Sri.J], CIM [UK], MCGP

[SL], MSLIM, MIMSL Independent Non-Executive Director

6. Mr. D. Hasitha S. Jayawardena BBA (Hons) (UK) Non-Independent Non-Executive Director

7. Ms. V. J. Senaratne Attorney-At-Law, Notary Public, Solicitor (Eng.& Wales) Alternate Director to K. J. Kahanda / Company

Secretary and Chief Legal Officer

8. Mr. Amitha Gooneratne FCA (SL), FCA (Eng. & Wales) Alternate Director to N. de S. Deva Aditya

5.

7. 8.

6.

5. Dr. Naomal Balasuriya MBBS [Sri Lanka], MBA [Sri.J], CIM [UK], MCGP

[SL], MSLIM, MIMSL Independent Non-Executive Director

6. Mr. D. Hasitha S. Jayawardena BBA (Hons) (UK) Non-Independent Non-Executive Director

7. Ms. V. J. Senaratne Attorney-At-Law, Notary Public, Solicitor (Eng.& Wales) Alternate Director to K. J. Kahanda / Company

Secretary and Chief Legal Officer

8. Mr. Amitha Gooneratne FCA (SL), FCA (Eng. & Wales) Alternate Director to N. de S. Deva Aditya

Dist i l ler ies Company of Sr i Lanka PLC28

Board ofDirectors1. Mr. D. H. S. Jayawardena Chairman / Managing Director

Mr. Harry Jayawardena is one the most successful and prominent business magnates in Sri Lanka. He was elected Chairman of the DCSL Group in 2006 after serving as its Managing Director for almost two decades. He heads many successful ventures in diversified fields of business. He is the founder Director and the present Chairman / Managing Director of the Stassen Group of Companies.

He is the Chairman of Aitken Spence PLC., Aitken Spence Hotel Holding PLC., Lanka Milk Foods (CWE) PLC., Madulsima Plantations PLC., Milford Exports (Ceylon) (Pvt) Ltd., Ceylon Garden Coir (Pvt) Ltd., Ambewela Products (Pvt) Ltd., Ambewela Livestock Co. Ltd., Danish Dairy Products Lanka (Pvt) Ltd., Lanka Dairies (Pvt) Ltd., Melstacorp Ltd. and its subsidiaries; Balangoda Plantations PLC., Browns Beach Hotels PLC., Lanka Bell Ltd., Periceyl (Pvt) Ltd., Bogo Power (Pvt) Ltd. and Texpro Industries Ltd.

He is a former Director of Hatton National Bank PLC., the largest listed bank in Sri Lanka and former Chairman of Ceylon Petroleum Corporation and SriLankan Airlines.

Mr. Jayawardena is the Honorary Consul for Denmark and was the only Sri Lankan honoured with the prestigious “Knight’s Cross of Dannebrog’ by Her Majesty, Queen Margrethe II of Denmark, for his significant contribution to the Danish arts, sciences and business life.

He has also been awarded the title, “Deshamanya” in recognition of his services to the Motherland, since November 2005.

2. Mr. C. R. Jansz Executive Director

Mr. C. R. Jansz has many years of experience in Logistics and in Documentation, Insurance, Banking and Finance relating to international trade.

He is the Chairman of DFCC Bank PLC and DFCC Vardhana Bank. He serves on the Board of Melstacorp Limited, Balangoda Plantations PLC., Lanka Bell Limited and several other companies of the Distilleries Group. He is also a Director of Lanka Milk Foods (CWE) PLC. and its subsidiaries.

He was the former Chairman of Sri Lanka Shippers Council and former member of the National Trade Facilitation Committee of Sri Lanka. Mr. Jansz holds a Diploma in Banking and Finance from the London Guildhall University – UK. He is a Chevening Scholar and a UN-ESCAP Certified Training Manager on Maritime Transport for Shippers.

3. Mr. N. de S. Deva Aditya DL, FRSA Independent Non-Executive Director

Mr. Niranjan Deva Aditya, is an aeronautical engineer, scientist and economist, is a Conservative Member of the European Parliament elected from the SE England. He is the Vice President of the Development Committee; ECR Coordinator and Conservative Spokesman for Overseas’ Development and Co-operation.

He was the Co Leader of the Parliamentary Delegation to the UN World Summit and General Assembly 2006, Chairman Working Group A of Development Committee overseeing Asia, Central Asia and Far East; - Co Co-ordinator Assembly of 79 Parliaments of the EU-ACP 2004 and the President EU India Chamber of Commerce from 2005. In 2012 he stood for and came runner up, beating the Liberal candidate into 3rd place to be the President (Speaker) to the European Parliament. He was the first Asian to be elected as a Conservative Member of British Parliament, first Asian MP to serve in the British Government as PPS in the Scottish Office and first Asian born MP to be elected to the European Parliament. He was nominated as a candidate to succeed Kofi Annan as Secretary General to the UN in 2006.

He is a Hon. Ambassador without portfolio for Sri Lanka; the first Asian to be appointed as Her Majesty’s Deputy Lord Lieutenant for Greater London, representing The Queen on official occasions since 1985; awarded the honour “ViswaKirthi Sri Lanka Abhimani“ by the Buddhist Clergy for his Services to Sri Lanka and given the Knighthood with Merit of the Sacred Constantinian Military Order of St. George for his global work on poverty eradication. He is a Fellow of the Royal Society for Arts, Manufacture and Commerce (Est: 1765).

4. Capt. K. J. Kahanda (Retd.) Executive Director

Captain Kahanda joined the Company in 1993 as Regional Manager (Central Region) and was appointed a Director in December 2006. Being a former officer of the Sri Lanka Army, he spearheaded the re-organisation of the operations of the Central Region since privatisation. He specialises in logistics, distribution and security matters, and is also a Director of G4S Security Services (Pvt) Ltd. and Pelwatte Distilleries (Pvt) Ltd., a subsidiary of the Group.

Annual Report 2014/15 29

5. Dr. Naomal Balasuriya MBBS [Sri Lanka], MBA [Sri.J], CIM [UK], MCGP [SL], MSLIM, MIMSL Independent Non-Executive Director

Dr. Naomal Balasuriya, a medical doctor turned-entrepreneur is internationally sought after as a life changing motivational speaker. His professional expertise ranges from medicine, military, management, marketing, mentoring to motivational speaking. He holds both the Master of Business Administration (MBA) and CIM (UK) qualifications. Having worked in the government sector, private sector and the Sri Lanka Air Force as a medical doctor, he now leads his entrepreneurial training company, Success Factory. He is also a Director of Melstacorp Ltd., a subsidiary of the Group.

6. Mr. D. Hasitha S. JayawardenaBBA (Hons) (UK)Non-Independent Non-Executive Director

Mr. Hasitha Jayawardena holds a Bachelor’s Degree in Business Administration BBA (Hons) from the University of Kent in the United Kingdom.

Mr. Jayawardena joined Stassen Group in February 2013. He is a Director of Stassen Exports (Pvt) Ltd., Milford Exports (Ceylon) (Pvt) Ltd., Stassen International (Pvt) Ltd., Stassen Natural Foods (Pvt) Ltd., Ceylon Garden Coir (Pvt). Ltd., Milford Developers (Pvt) Ltd., Stassen Foods (Pvt) Ltd., C. B. D. Exports (Pvt) Ltd., Zahra Exports (Pvt) Ltd. and Mcsen Range (Private) Ltd. He was appointed to the Board of Meltsacorp Ltd. in January 2015 and Periceyl (Pvt) Ltd. in April 2015.

Mr. Jayawardena has also worked as an Intern at the Clinton Global Initiative programme (CGI) in New York in 2007.

7. Ms. V. J. Senaratne Attorney-At-Law, Notary Public, Solicitor (Eng.& Wales) Alternate Director to K. J. Kahanda / Company Secretary and Chief Legal Officer

Ms. Senaratne was appointed as the Company Secretary in 1993. She was admitted to the Bar in 1977 and was enrolled as a Solicitor (England & Wales) in June 1990. She also holds the position as Company Secretary of Periceyl (Pvt) Ltd

She also currently serves as a director on the Board of Paradise Resort Pasikudah (Private) Limited, Amethyst Leisure Limited, DFCC Bank PLC and as an alternate Director of MelstaCorp Limited and Distilleries Company of Sri Lanka PLC.

8. Mr. Amitha Gooneratne FCA (SL), FCA (Eng. & Wales)Alternate Director to N. de S. Deva Aditya

Mr. Amitha Gooneratne has held several senior positions at Commercial Bank of Ceylon PLC and served as the Managing Director from 1996 to April 2012. He is a Fellow member of the Institute of Chartered Accountants, United Kingdom and Wales and a Fellow member of the Institute of Chartered Accountants, Sri Lanka. He was the Founder Chairman of the Financial Ombudsman Sri Lanka (Guarantee) Ltd., and former Chairman of the Sri Lanka Banks’ Association (Guarantee) Ltd. He was also the Managing Director of Commercial Development Company PLC, a Public Quoted Company listed in the CSE and was the Chairman of Commercial Insurance Brokers (Pvt.) Limited. He was also nominated to the Board of SriLankan Airlines during 2002–2004 by the Government of Sri Lanka.

On his retirement, Mr. Gooneratne, assumed duties as Managing Director of Melstacorp Limited, which is the strategic investment arm of the Distilleries Company of Sri Lanka PLC. He is the Chairman of Melsta Regal Finance Limited, Melsta Logistics (Pvt.) Limited and Bellvantage (Pvt.) Limited; Board Member of Periceyl (Pvt.) Limited, Balangoda Plantation PLC, Lanka Bell Limited, Telecom Frontier (Pvt.) Limited, Bell Solutions (Pvt.) Limited, Timpex (Pvt.) Limited Texpro Industries Limited, Bogo Power Limited., Continental Insurance Limited and Browns Beach Hotel PLC., which are subsidiary companies of Melstacorp Limited.

He is an independent Director of Lanka IOC, Textured Jersey and Commercial Development Company Limited.

He is also the Alternate Director to Mr N. de S. Deva Aditiya on the Board of Distilleries Company of Sri Lanka and Aitken Spence PLC.

Dist i l ler ies Company of Sr i Lanka PLC30

GroupManagement

1. Amitha Gooneratne: Managing Director - Melstacorp Ltd. / Chairman - Melsta Regal Finance Ltd., Melsta Logistics (Pvt) Ltd., Bellvantage (Pvt) Ltd., Melsta Tower (Pvt) Ltd. / Director - Continental Insurance Lanka Ltd., Periceyl (Pvt) Ltd., Lanka Bell Ltd., Texpro Industries Ltd., Bogo Power (Pvt) Ltd.

2. Capt. Jagath Kahanda (Retd.): Managing Director - Pelwatte Sugar Distilleries (Pvt) Ltd. / Director - Distilleries Company of Sri Lanka PLC, Melstacorp Ltd., Pelwatte Sugar Industries PLC, Melsta Properties (Pvt) Ltd., Milford Holdings (Pvt) Ltd.

3. Ms. Stasshani Jayawardena: Chairperson - Splendor Media, Director - Aitken Spence PLC

4. Maximus R. Peries: CEO - Distilleries Company of Sri Lanka PLC / Director - Pelwatte Sugar Industries PLC, Lanka Bell Ltd., Melsta Logistics (Pvt) Ltd., Melsta Tower (Pvt) Ltd.

5. Lalith Obeyesekere: Director / CEO - Balangoda Plantations PLC, Madulsima Plantations PLC

6. Capt. Ranjith Wettewa SLN (Retd.): Director - Pelwatte Sugar Industries PLC

7. Asoka Abeyewardene: Director - Continental Insurance Lanka Ltd.

8. Senaka Amarathunga: Director / General Manager - Periceyl (Pvt) Ltd.

1.

4.

7.

2.

5.

8.

3.

6.

Annual Report 2014/15 31

9. Dinal Peiris: Managing Director - Texpro Industries Ltd.

10. Chaminda De Silva: Managing Director - Continental Insurance Lanka Ltd.

11. Dr. Prasad Samarasinghe: Managing Director - Lanka Bell Ltd.

12. Janaka Abeysinghe: Director - Melsta Logistics (Pvt) Ltd.

13. Nishaman Karunapala: Director / CEO - Melsta Regal Finance Ltd.

14. Palitha Rodrigo: Managing Director - Melsta Technologies (Pvt) Ltd.

15. Ms. Farzana Sulaiman: Chief Operating Officer - Bellvantage (Pvt) Ltd.

9.

12.

15.

10.

13.

11.

14.

Dist i l ler ies Company of Sr i Lanka PLC32

DCSLManagement

Left to RightBrig. Aruna Wijewickrama (Retd.) : Head of Central Region

Lalith Ratnayake : Head of Inventory Management

Nimal Nagahawatte : Head of Finance

Ms. V. J. Senaratne : Company Secretary & Chief Legal Officer

Col. Ranjith Rupasinghe (Retd.) : Head of Extra Special Heritage Arena

S. Rajanathan : Head of Procurement

Annual Report 2014/15 33

Left to RightMaj. Roshan Cabraal (Retd.) : Head of Northern Region

Maj. Gen. Jagath Rambukpotha (Retd.) : Head of Southern Region

Ms. Gayathri Chakravarthy : Head of Human Resources

Maximus R. Peries : Chief Executive Officer

Premasiri Liyanaarachchi : Chief Internal Auditor

Roshanth Kumar Perera : Head of Transport & Logistics

Capt. Ranjith Wettewa SLN (Retd.) : Head of Uva Region

Dist i l ler ies Company of Sr i Lanka PLC34

ManagementDiscussion & AnalysisThe DCSL Group epitomises one of Sri Lanka’s reputed diversified conglomerates, holding a portfolio encompassing beverages, plantations, telecommunication, insurance, finance, power generation, textiles, leisure, logistics and media and creative services. The group is synonymous with dynamism and professionalism, and has carved a unique niche for itself in the sectors in which it operates. Having long established its credentials as a respected corporate entity over a period of a century, DCSL embodies state-of-the-art systems and processes led by an inspired and distinguished senior management board and a professional team of employees dedicated to deliver maximum value to shareholders and other valued stakeholders.

Group Overview Our flagship company, which is engaged in the alcohol beverage sector, was impacted by a host of challenges which carried over from the preceding year, providing neither relief nor a level playing field in which to operate. The illegal practices rampant in the industry succeeded in yet again adversely affecting the overall performance of the Group. The beverage sector represents the majority of the Group’s revenue and profitability while DCSL remains as the dominant market leader in the industry.

In order to offer superior products, DCSL has invested in a state-of-the-art fully automated blending and bottling plant to enhance efficiency and quality. DCSL remains committed and strongly believes that such high value investments will ensure the sustainability of its operations.

In order to offer superior products, DCSL has invested in a state-of-the-art fully automated blending and bottling plant to enhance efficiency and quality. DCSL remains committed and strongly believes that such high value investments will ensure the sustainability of its operations.

Melstacorp Group of Companies, under which falls the other diversified sectors of the Group, succeeded in expanding its sphere of influence and in creating a distinct identity for itself. Our focused efforts to build the Melstacorp brand yielded positive results, with greater

brand awareness and recall amongst key stakeholders. While heightened brand equity and an increased presence were achieved during the year, recent investments are yet to yield commensurate returns. Melsta Regal Finance Limited, during its second year of operations, achieved several financial milestones while steadily consolidating its presence as one of the newest and most dynamic players in the financial services sector.

Buoyed by the infusion of capital in mid 2014, our insurance venture, Continental Insurance, recorded its highest-ever profitability in the financial year under consideration, supported by establishing a wider geographical reach.

Unfortunately, the expropriation of Pelwatte Sugar Industries PLC (PSIP), under the Revival of Under-Performing Enterprises and Under-Utilised Assets Act (Act) in November 2011, was an issue that remained unresolved during the financial year under review. Despite being listed as an ‘under-utilised asset’ under the Act, we remain emphatic that we are the legal owners of PSIP. We remain hopeful that this issue will be resolved in a transparent manner at the earliest instance.

Furthermore, despite a lapse of six years, we have still not been reimbursed the profit earned during the DCSL Group’s tenure at the helm of Sri Lanka Insurance Corporation Ltd., (SLIC). We are hopeful that the profit earned, which is rightfully ours, will be paid soon, as per the Supreme Court directive.

The Group’s gross revenue recorded Rs. 66.8 Bn in the current year. The Group’s profit before tax was Rs. 9.7 Bn and a profit after tax of Rs. 6.5 Bn. The contribution to total revenue from the alcoholic beverage sector was Rs. 57 Bn and continues to be the largest contributor to the

Annual Report 2014/15 35

bottom line. The Group’s plantations business, contributed a revenue of Rs. 3 Bn, with telecommunication at Rs. 3.4 Bn and diversified businesses at Rs. 3.4 Bn. Share of associate investees contributed Rs. 1.4 Bn to the Group’s profitability. The Group’s total assets increased to Rs. 92.7 Bn from Rs. 83.7 Bn and the net assets per share rose to Rs. 203.35 from Rs. 178.80. DCSL’s share price gained by 18% during the year, reaching Rs. 240.00 as at end of March 2015.

The DCSL Group strived hard to generate social and economic gains in order to make a significant contribution to the prosperity of the country. As a market leader in the beverage sector and one of the most valued corporate entities in the county, we consider it our responsibility to deliver sustainability across all our operations, while ensuring that our activities have a favourable impact on social, environmental and economic pillars.

Beverage Sector DCSL sustained its status as the Flagship Company and highest revenue generator for the Group in the year under review. The challenges faced in the preceding year persisted despite aggressive lobbying efforts on our part to ensure a level playing field.

The fact that DCSL continues to maintain market leader status despite operating in such a challenging eco system in the legal alcohol industry is a reflection of the loyal customer base and brand loyalty we have succeeded in generating. Despite the infusion of cheaper priced alcohol in the market, DCSL consumers uphold their trust in DCSL brands. Considering that the excise duty component is over 65%, it is impossible for legal producers to retain competitiveness in such markets.

Gross Turnover - Group(Rs. Mn)

56,9932015 2014

Beverage Sector3,002 Plantations Sector3,372 Telecommunication Sector3,398

66,765

53,1373,1723,6343,244

63,186Diversified Sector

Profit Before Tax - Group(Rs. Mn)

8,3982015 2014

Beverage Sector(106) Plantations Sector(692) Telecommunication Sector

737

9,728

8,027130

(639)536

9,494

Diversified Sector1,391 1,440 Share of Associate Companies Profit

Dist i l ler ies Company of Sr i Lanka PLC36

ManagementDiscussion & Analysis

Further, a high tax regime and escalating cost of living serve to render consumers no choice but to opt for cheaper products, despite their dubious quality.

It must be duly noted that we adhere strictly to the NATA Act which prohibits advertising and promoting alcoholic brands. The fact that DCSL has sustained and grown its market share despite these severe restrictions is a reflection of the superior quality of our products which are appreciated by discerning consumers. Therefore, our ongoing success can be attributed to our management skills and consumer loyalty.

Unfortunately, unscrupulous operators do not pursue the same sustainable goals as DCSL does, since they focus on earning high profits with a short term view of the business, resulting in a high social cost. In contrast, the DCSL Group pays all taxes as per the laws of the land, making the Group one of the largest contributors to state coffers.

In October 2014, the beverage sector experienced a significant change in the tax structure in October 2014, wherein the Value Added Tax and Nation Building Tax

component were added to the excise duty. As a result, Value Added Tax on purchases became unrecoverable and added to the cost. Further, customs duty on imported products was increased and taxes such as cess for bulk spirit/finished goods were increased substantially.

During the current financial year, both DCSL and Periceyl continued to maintain profitability despite the challenges posed to the legal alcohol business in the country as a result of a skewed playing field. Gross turnover of DCSL was recorded at Rs. 51.8 Bn. DCSL recorded profit after tax of Rs. 4.7 Bn (adjusted for intra-group capital gain on structuring of investments and properties) as against profit after tax of Rs. 5.4 Bn in the previous year. The beverage sector contributed Rs. 41 Bn to the State by way of taxes.

Periceyl (Pvt) Ltd., achieved greater brand building success during the year, sustaining its profitability. Its brands - Black Opal Arrack, Franklin Brandy, Galerie Brandy and Tillsider Whisky - performed convincingly. Further, Periceyl introduced

new agency lines from Australia (Somerton wines), South Africa (Cape Dreams wines), New Zealand (Riverby and Mudhouse wines), Spain (Viejo Marchante wines) and Scotland (Queens Seal Whisky) and hopes to expand its spirit portfolio in the near future.

However, the year proved to be a challenging one in more ways than one, with some of the local manufacturers distributing finished products, mainly Arrack, at a lower price. Such products were supplied to retailers at a lesser cost and these same products were offered by the manufacturers with a larger margin to retailers, which encouraged the retailers to sell the products over DCSL/Periceyl products

Artificial toddy being supplied at a cheaper price has also created a difficult situation for manufacturers such as DCSL/Periceyl, who are using 100% genuine coconut toddy to

2013/14

53,13756,993

2014/15

Gross TurnoverBeverage Sector(Rs. Mn)

2013/14

8,0278,398

2014/15

Profit Before TaxBeverage Sector(Rs. Mn)

92.7 BnTotal Assets (Rs)

61.0 BnShare Holders’

Funds (Rs.)

Group

21.84Earnings per Share (Rs.)

203.35Net Assets per

Share (Rs.)

Group

Annual Report 2014/15 37

produce coconut spirits. 100% Coconut Old Arrack is a flagship product which is endemic to Sri Lanka and is similar to Scotch whisky in Scotland and Cognac in France. However, due to the weak monitoring framework in the country to crack down artificial toddy suppliers, the country will lose the edge for authentic 100% Coconut Arrack.

Future Outlook Despite the challenges in the sector, we remain optimistic about the prospects for the beverage industry and for DCSL to further secure even greater market share in the future. Our massive investment in the ultra-modern blending and bottling factory will enhance our capacity and ensure that DCSL products can be accessed across the length and breadth of the country. DCSL is reputed for its innovation and our R & D team perseveres in innovating new products to ensure that our products evolve and change with the times. Periceyl remains in constant pursuit of new and emerging opportunities emanating from the country’s leisure and tourism sectors. In conclusion, we remain hopeful that the relevant authorities will exert greater control to curb the illegal liquor industry for the benefit of consumer.

Melstacorp Limited Melstacorp holds 19 direct and indirect subsidiaries and two associate companies under its wing as a result of our Group restructuring plan put into effect during the previous year. Under the new arrangement, DCSL’s shareholdings of subsidiaries and associates were realigned to Melstacorp Limited, enabling Melstacorp to provide greater focus and attention to the diversified investments of the DCSL Group.

In a bid to ingrain the Group philosophy, a series of measures were taken to infuse Group culture and strengthen the shared services framework. Some of the key areas of the shared services such as treasury, finance, audit and control and human resources, were put in place. Our efforts to strengthen shared services and build a common brand under the ‘Melsta’ umbrella will be sustained into the future.

Melstacorp is striving to combine the Group companies’ synergies in a manner that will drive optimum resource utilisation and financial benefits. We have envisioned that Melstacorp will emerge as a diversified conglomerate, enhancing the contribution from the non-alcohol sector whilst reducing the Group’s dependence on the alcohol sector.

Dist i l ler ies Company of Sr i Lanka PLC38

ManagementDiscussion & Analysis

Plantations Sector The 2014 financial year proved to be a challenging one for the plantations sector as adverse weather conditions and labour wage increases accelerate cost of production which in turn served to erode profitability in the sector. Balangoda Plantations (BPL) recorded a pre tax loss of Rs. 106 Mn. The turnover of the company decreased from Rs. 3.2 billion in 2013 to Rs. 3.0 billion in 2014, reflecting a drop of 6.25%. The tea industry as a whole experienced an unfavourable year, posting a decline of 2.20 Mn Kgs in output. The shortfall is mainly due to the deficit shown by the medium grown sector, notwithstanding the positive crops recorded from both high and low grown sectors.

The decline in the rubber segment experienced in the previous year continued in the year under review as well. The BPL’s rubber production decreased by 18% to 98 Mn Kgs over the previous year due to adverse weather conditions which disrupted harvesting. Rubber prices continued to fall in 2014 due to built up stocks and slow growth in emerging markets. BPL sustained its momentum in replanting programmes in tea and rubber in order to position the company on a stronger platform for future growth. The company also invested in selected factories to reduce cost of production and to improve efficiency.

Future Outlook The future for the plantations sector seems challenging due to a variety of factors, such as a slow global growth impacting export markets, geo-political tensions in export markets and the drop in world tea and rubber prices. Locally, the sector remains vulnerable to inclement weather patterns as it does to wage increases which push the cost of production to a non viable extent. Extension of the fertilizer subsidy and its availability will further play an

important role in an industry beset by aging bushes and depleted soils. We are optimistic that the authorities will resolve some of the issues facing the plantation industry such that Sri Lanka’s tea and rubber exports remain competitive in the global arena. BPL is leveraging on a slew of strategic measures to improve its positioning by exercising greater cost controls and enhancing output. We believe that our adoption of sustainable practices will strengthen us in the long term.

Telecommunication Sector Despite the rise of operational costs during the year, the Group’s telecommunication arm, Lanka Bell, was able to sustain a reasonable EBITDA margin in line with the industry.

Lanka Bell is now equipped with the latest in technology to propel itself to the forefront of the industry. The launch of 4G positions the company as one of only two leaders in the sector, thereby ensuring it takes a quantum leap into the future of wireless telephony and connectivity in its tradition of pioneering technology such as introducing CDMA technology to Sri Lanka in 2005.

2013/14

3,172 3,002

2014/15

Gross TurnoverPlantations Sector(Rs. Mn)

2013/14

130

(106)

2014/15

Profit / (Loss)Before Tax Plantations Sector(Rs. Mn)

Annual Report 2014/15 39

Lanka Bell operates its 4G LTE network on a bandwidth of 25 MHz in the 2.3 GHz spectrum called the LTE Band number 40 which is the most sought after band in the Asian region. LTE technology offers faster data rates to customers and is the current trend and future of the ICT (Information and Communication Technology) industry.

Lanka Bell offers an attractive portfolio of value-added high speed broadband and voice services at competitive rates, which makes it a preferred telecom service partner for customers. The strong reputation for customer care and technical expertise of Lanka Bell staff is pushing the company to reach the pinnacle.

Future Outlook Lanka Bell is now well poised for greater growth in the year ahead, leveraging on the latest technologies, greater cost control measures and a technically adept team. Growth in data usage over the year has been encouraging and we believe that the data industry will witness rapid expansion in the years ahead. Hence, we intend to strengthen our presence in this segment further. The adoption of new technology at an early stage, gives us a first mover status and we will build on this further. Lanka Bell is determined to pursue a leadership position in the data market as we are one of only two operators in the country to have a 4G-LTE Network.

Diversified Sector InsuranceContinental Insurance (CILL) recorded its highest growth in gross written premium of 30% since beginning its operations five years ago. CILL has increased its market share to 3.5% in the General Insurance Sector and established itself as one of Sri Lanka’s fast growing Insurance companies. CILL was very successful in securing business during 2014 including that of major power plants,

international cricket stadiums, local and international hotel chains, aviation and major conglomerates in the country.

CILL has expanded its branch network to 37 branches strategically located around the country, offering easier access to its array of solutions. New branches were opened in Wattala, Dambulla and Warakapola areas, with further plans of expanding branch network to ensure that our valued customers enjoy hassle-free services. Striving to service communities in need through CSR projects, CILL believes in creating a positive social reformation through our community welfare programmes. The company carried out various CSR projects across the country, serving communities in need.

CILL is the first insurance company to be awarded a Fitch Rating A-(lka) within five years of operation and obtained ISO 9001:2008 (Quality Management Systems) certification in 2013 in its quest for service excellence. CILL’s (A-) Fitch rating reflects the financial stability of the organisation. It further enhances the confidence of the policy holders to entrust business with absolute assurance.

2013/14

3,634 3,372

2014/15

Gross Turnover Telecommunication Sector(Rs. Mn)

2013/14

(639)(692)

2014/15

Profit / (Loss) Before Tax Telecommunication Sector(Rs. Mn)

2013/14

3,244 3,398

2014/15

Gross Turnover Diversified Sector(Rs. Mn)

2013/14

536

737

2014/15

Profit Before Tax Diversified Sector(Rs. Mn)

Dist i l ler ies Company of Sr i Lanka PLC40

CILL offers a diverse product portfolio to its customers encompassing property, motor, marine and general insurance. The company is committed to constantly innovate and update its product portfolio to meet the ever-changing business landscape. The newest addition to the product portfolio is the company’s health insurance plans, which focuses on making quality health care affordable and ensures financial stability even during unforeseen events of sickness.

The company has enhanced its focus on internet and mobile banking in a proactive effort in anticipation of an exponential increase in usage across the country. Further, in order to offer customer convenience through strategic partnerships, CILL has partnered with eZ cash to pay premiums using mobile telephones.

CILL is on a mission to provide reliable, innovative, customer-friendly insurance services through state-of-the-art technology, and focuses continuously on product improvement to ensure customer confidence in the brand’s value proposition, thereby living up to its promise of “Service, Redefined”. Financial Services Melsta Regal Finance Ltd embarked on the second year of operation with a focus on penetrating the market with innovative financial solutions. The company achieved noteworthy milestones in terms of asset size and achieved a balance sheet size of Rs 5 Bn and earned NBT of Rs. 100 Mn.The company was successful in introducing innovative financial solutions such as the 360° trade finance facility, which proved to be a breakthrough product in the financial services arena. This service, which optimises the capacities of the Group, encompasses a wide ranging financial solution including clearing of imports, warehousing, logistics and

financing. The company has a formidable competitive advantage as this product is offered in partnership with the Group Companies, who possess the relevant expertise. The company is recognised in the financial services industry as a Finance Company with the widest product range.Recognising the importance of expanding the Company’s regional footprint, the company laid the initial foundation for its branch network. Its presence was expanded to the key cities of Kurunegala, Kandy, Matara and Negombo. The Company has also chartered an aggressive regional penetration strategy, which will be implemented in the ensuing months.Another key milestone achieved by the Company was when it successfully negotiated and obtained a USD 10 Mn foreign currency funding line. This is a significant achievement given the short span of history of the Company. Fitch Rating (Lanka) Ltd reaffirmed its A+(lka) rating of Melsta Regal Finance Ltd.During the year, Melsta Regal Finance focused on Human Resources (HR) development, which is a critical success factor in the financial services sector. The HR initiatives implemented and practiced by the Company were recognised with a Bronze Award at the SLITAD People Development Awards Ceremony in 2014.

Future Outlook Melsta Regal Finance is laying strong foundations for future growth, expanding its branch network, and widening its portfolio of products and services, backed strongly by a unique brand of customer care which caters to the evolving needs of its customers. In the short period since its establishment, the company has demonstrated its innovative streak by pioneering one-of-a-kind financial solutions and building a customer centric team.

Collision Repair & Logistics The Collision Repair Centre at Melsta Logistics performed well during the year, and enabled the Group to add value for both internal and external clients. The Centre offers state-of-the-art technology, machinery, equipment and unparalleled know-how on treating vehicles based on the manufacturer’s specifications. These specialised facilities have served to create a distinctive niche for Melsta Logistics. The newly-formed logistics operation continues to accrue gains for Melsta Logistics. Melsta Logistics is now focused on expanding this facility beyond the Group, while investing in superior technology to enhance efficiency.

ManagementDiscussion & Analysis

Annual Report 2014/15 41

Textiles During the year under review, sales volumes increased by 30% with significant improvements to gross profit margins arising from better pricing. Significant cost savings were made on energy due to the use of biomass thermic fluid heaters as an alternative to furnace oil to generate hot air.

Demand for high-quality woven fabrics, which had fallen significantly since 2008, is now starting to pick up, especially for high-end export and local consumption. Well-known international and European brands such as Marks & Spencer, Next, George, C&A, Metalan, etc, appear to be buying more garments manufactured in Sri Lanka which is an encouraging sign.

The textile industry is expecting a remarkable improvement in market conditions in the next year with the reinstatement of GSP+ in Sri Lanka. The industry has already witnessed encouraging signs with enquiries from the European buyers as well as the reactivation of the buying offices in the country. Further, Texpro plans to generate our own steam using bio-mass during the second half of this year, which would result in a further reduction in cost.

Future OutlookIn the new financial year, the company’s results should reflect the full effect of the biomass conversion which we expect will reduce the energy cost by over 30%. We are continuing to convert more of the fossil fuel consuming equipment which will further reduce our operating cost, enabling Texpro to become very competitive in pricing with regional players, thereby increasing profitability. We will sustain our strategy to be an efficient, flexible niche market printer and dyer and provide value added services to discerning customers. We are optimistic of the future and expect a good turnaround in performance in the coming year.

Power Generation Bogo Power (Pvt) Ltd was formed to set up a Mini Hydro Plant at Kirkoswald Group, Bogowantalawa. Bogo Power (Pvt) Ltd is registered with the Board of Investment of Sri Lanka (BOI) and has obtained necessary approvals from the Sustainable Energy Authority of Sri Lanka and the Public Utilities Commission of Sri Lanka. A Power Purchase Agreement has been entered into with the Ceylon Electricity Board for the sale of electricity generated for a period of 20 years. The project was fully commissioned in December 2011 and power capacity of the project is 4 MW and the average annual energy that is expected to be generated is 15.2 GWH. During the year 2014/2015, the project delivered 21.2 GWH, thus exceeding the projected value.

Business Process Outsourcing Bellvantage (Pvt) Ltd delivered an excellent year with expansion of its service portfolio. The Contact Centre continues to offer a host of services including call centre, chat, hosting, data entry, and customised voice and service solutions. The current year’s growth focused on the Banking and the Food chain industries, enabling it to be the pioneer in handling multinational brands by capitalising on adopting further efficiencies in these segments. Beyond industry-based efficiencies, the Bellvantage Contact Centre as a whole is optimised by continuous expansion into existing and new accounts offering 24/7 service.

ICT solutions were further enhanced by investing in the world-renowned latest version of the Contact Centre solution, enabling Bellvantage to keep in pace with the latest technology in providing the best services to the clientele by having a competitive edge in the global marketplace. We successfully launched international projects and still continue to be the leader in the market, having the best brands and names managed locally and internationally in the BPO sector.

Dist i l ler ies Company of Sr i Lanka PLC42

Future Outlook Our leisure arm is poised to unveil a signature hospitality experience as denoted by the Heritance brand, and we expect the new property to rapidly accelerate to the forefront of the country’s hospitality market. Overseas tour operators and industry partners have already expressed a keen interest in the property, and we are extremely bullish about the prospects for Heritance Negombo once it commences operations.

Apart from our established competencies, we created a new ICT arm this year, focusing on Contact centre hosting, Customer Relationship Management (CRM), Hardware and software solutions services to face the most demanding of industries to cater to their requirements.

Melsta Technologies (Pvt) Ltd was established in March 2015 with a vision to “Deliver technology solutions people can depend on”. To this end, it is envisaged that Melsta Technologies will play a strategic role and specialise in niche verticals within the fast evolving Information and Communication Technology (ICT) industry. This coupled with the ever-increasing demand for robust ICT solutions within the highly diversified Group, contributed to our strategic decision to establish Melsta Technologies Private Limited.

Since its inception in March 2015, Melsta Technologies has obtained the Oracle Gold Partner Status and has established an Oracle E‐Business Suite (EBS) implementation practice. Additionally, Melsta Technologies offers advisory services on Oracle Licensing, Oracle Premier Support renewal services, implementation services on Oracle Applications and Technologies and Local Support Services.

Leisure Sri Lanka’s tourism industry crossed the 1.5 million tourist mark in 2014 and is strongly moving towards achieving its target of 2.5 million tourists by 2016. A number of high profile global hotel brands are setting up operations in the country, which indicates the prosperous outlook for the industry in the months and years ahead. The Group’s leisure arm is also gearing up to position itself in this rapidly evolving scenario. The erstwhile Browns Beach Hotels PLC is in the process of completing its extensive reconstruction and will soon be re-launched as Heritance Negombo, offering a state-of-the-art luxury experience. Negombo’s rich culture and sandy beaches and its strategic location and proximity to the airport lend it a unique advantage and Heritance Negombo will spearhead the area’s tourism with its luxury signature hospitality.

ManagementDiscussion & Analysis

Media & Creative Services Recent changes in Sri Lanka’s economic landscape have given rise to unprecedented opportunities. This in turn has informed the scope of various business units within the organisation and we are in the process of diversifying our product portfolio to more proactively meet these changes.

By expanding service offering from a media-centric agency to a full-service advertising agency, Splendor Media continues to gain momentum as a tour de force within the local industry. The company’s expansion into a number of brand related activities and recent investment in digital media solutions will help augment Splendor Media’s current core offering, while helping clients leverage on the latest digital media trends and more sophisticated performance media techniques. This in turn, marks an adventurous move towards a brave new frontier, with possible partnerships and collaborations lined up for the immediate future.

Future OutlookSplendor Media remains committed to nurturing a culture of creativity, passion and effectiveness, one that adds real value to the client and their brand, while doing work that remains true to the spirit of free enterprise and contributes positively towards social change.

Annual Report 2014/15 43

SustainabilityReportTouching LivesOur Sustainability Motto in ActionWe understand that, globally, stakeholders at large are demanding that companies they associate with demonstrate non-financial metrics to define sustainability and sustainable operations. Financial profitability as the sole criteria of a company’s success is an outdated concept and outrightly rejected by most right-thinking stakeholders and the organisations they support. More importantly, being an environmentally, economic and socially sustainable organisation is helping companies earn corporate respect and drive customer loyalty, not to mention earning respect from peers and industry. In an era of growing global competition, climate change and diminishing resources, companies that put sustainability as their foremost goal are winning the race.

As one of the oldest, diversified, blue chip conglomerates in existence in Sri Lanka, we are living proof of continuous improvement and sustainable business practices. While we celebrate over-a-century of existence in the year 2015, we consider this an opportunity to strengthen our conceptions of business practices that are environmentally and socially sustainable, while also being financially sustainable, the key requirement of any commercial entity