distressed company alert · distressed company alert a division of new generation research, inc....

TRANSCRIPT

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 1

VOLUME 14, NO. 4 | JANUARY 29, 2016

New Generation Research’s weekly newsletter that monitors and reports on companies showing signs of financial distress.

PAGE COMPANY CATEGORY

5 A.M. Castle & Co. Distressed Debt Exchange

6 Extreme Reach, Inc. Low Rating

7 Fairmount Santrol Holdings, Inc. Low Rating 8 GrafTech International Ltd. Low Rating 9 Halcon Resources Corporation Dividend Omission 10 Hidili Industry International Development Ltd. Low Rating 11 Imperial Metals Corporation Low Rating 12 Momentive Performance Materials Inc. Low Rating 13 Mongolian Mining Corporation Low Rating 14 Murphy Oil Corporation Debt at Discount 15 Postmedia Network Inc. Low Rating 16 Spanish Broadcasting System, Inc. Low Rating 17 Talos Energy LLC Low Rating 18 Terrace Energy Corp. Miscellaneous

19 Profile Updates 24 Watch List 26 Bankruptcies

Profile Highlights A.M. Castle & Co.

On January 22, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on A.M. Castle & Co. to CC from CCC+ and its 12.75% senior secured notes were lowered to CC from CCC+. According to Standard & Poor’s, the rating action reflects A.M. Castle’s January 15, 2016 announcement of an exchange offer for its senior secured notes. “We are lowering our corporate credit rating on the company and our issue-level rating on its senior secured debt because we view the related transactions to be distressed,” said Standard & Poor’s credit analyst Patricia Mendonca. “This determination is based on the company’s financial condition, the possibility of default if the exchange is not successful, and that noteholders who do not agree to exchange their notes will be stripped of the original security package.”

Profile Highlights continued on next page…

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 2

Profile Highlights, continued Extreme Reach, Inc.

On January 28, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on Extreme Reach, Inc. to B- from B, its first-lien term loan and revolving facility to B+ from BB- and its second-lien term loan to CCC from CCC+. “The downgrade reflects the risk that the company could violate its leverage covenant by the first quarter of 2017,” said Standard & Poor’s credit analyst Dylan Singh. Standard & Poor’s does not believe the Company will generate enough free cash flow to make the amortization payments, and it will therefore have to draw on its revolving credit facility to make those payments. S&P believes that doing so would likely prevent the Company from reducing leverage in advance of the step downs, resulting in a potential covenant violation. Fairmount Santrol Holdings, Inc.

On January 27, 2016, Moody’s Investors Service downgraded Fairmount Santrol, Inc.’s corporate family rating to Caa1 from B2, its probability of default rating to Caa2-PD from B3-PD and its senior secured credit facility to Caa1 from B2. According to Moody’s, the rating downgrade and negative outlook reflect the expectation that EBITDA and key credit metrics will deteriorate further in 2016 as a result of the persistent weakness in the oil and natural gas industry. Moody’s further states that the negative outlook also considers the Company’s $157 million Term Loan B-1 maturing in 2017. The rapid deterioration in Fairmount’s key end markets has resulted in a 36% decline in adjusted EBITDA for the trailing-twelve months ending September 30, 2015 as compared to year-end 2014. Key credit metrics have also weakened more quickly than previously anticipated.

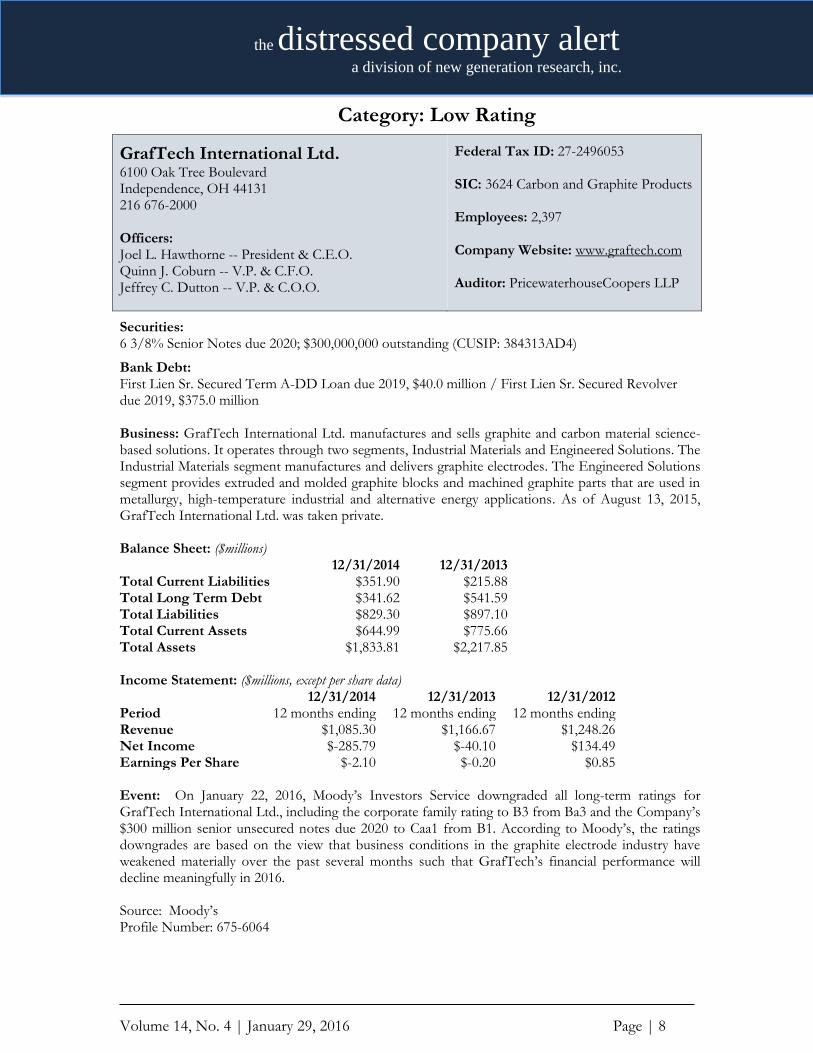

GrafTech International Ltd. On January 22, 2016, Moody’s

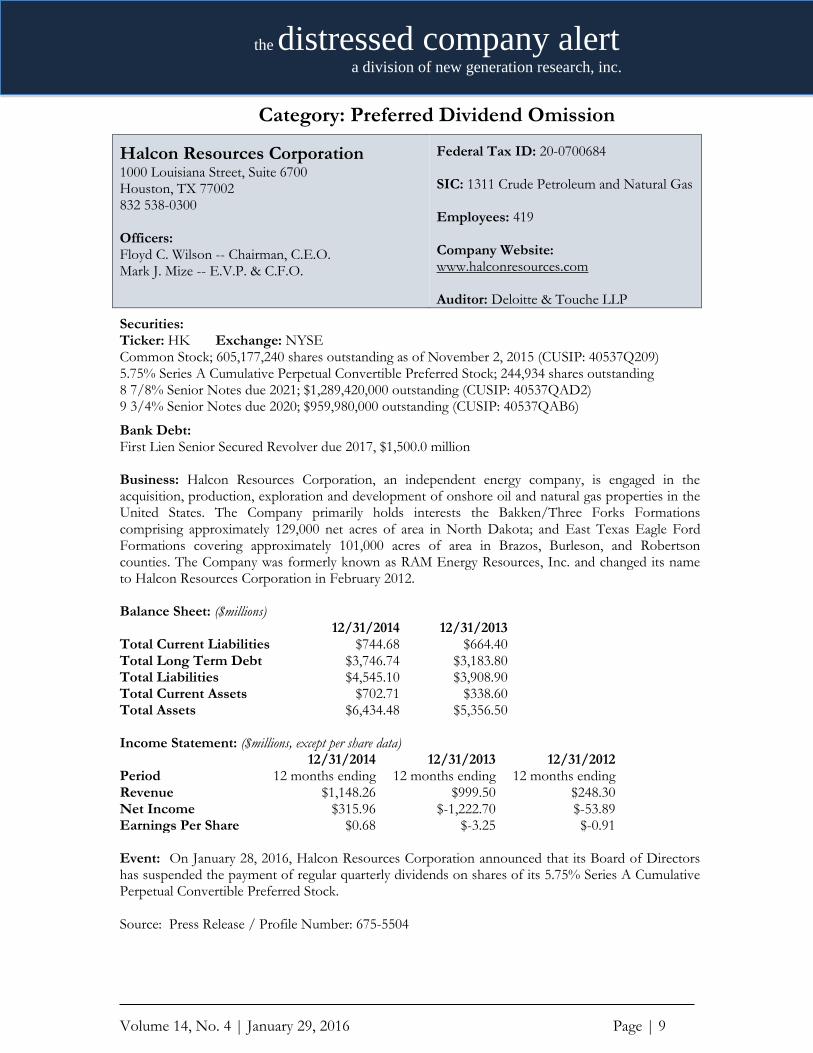

Investors Service downgraded all long-term ratings for GrafTech International Ltd., including the corporate family rating to B3 from Ba3 and the Company’s $300 million senior unsecured notes due 2020 to Caa1 from B1. According to Moody’s, the ratings downgrades are based on the view that business conditions in the graphite electrode industry have weakened materially over the past several months such that GrafTech’s financial performance will decline meaningfully in 2016. Moody’s further states that the negative rating outlook reflects meaningful uncertainty in the graphite electrode industry with no evident catalyst for improvement in the near-term. Moody’s could downgrade the rating if GrafTech does not make the adjustments necessary to put the Company on a deleveraging trajectory and restore adequate near-term liquidity. Halcon Resources Corporation

On January 28, 2016, Halcon Resources Corporation announced that its Board of Directors has suspended the payment of regular quarterly dividends on shares of its 5.75% Series A Cumulative Perpetual Convertible Preferred Stock. This action will preserve liquidity and minimize dilution during this period of extraordinarily weak market conditions. Halcon’s Board of Directors intends to reassess the dividend policy on an ongoing basis.

Profile Highlights continued on next page…

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 3

Profile Highlights, continued Hidili Industry International Development Ltd.

On January 22, 2016, Moody’s Investors Service downgraded Hidili Industry International Development Ltd.’s corporate family rating to C from Caa2. “The downgrade reflects Hidili’s ongoing default situation and lowered expected recovery rate resulting from the distressed coal price environment,” says Dylan Yeo, a Moody’s Analyst. According to Moody’s, Hidili missed the principal payment of $182.8 million and accrued interest of $7.8 million on its outstanding US dollar bond on November 4, 2015 and is in default on some of its bank loans. The Company is currently in talks with creditors to restructure its debt. In Moody’s view, Hidili’s expected recovery rate has declined because the estimated recovery value of its mining assets will be adversely affected by the prolonged weakness in the coking coal market.

Imperial Metals Corporation

On January 27, 2016, Standard & Poor’s Ratings Services lowered its long-term corporate credit rating on Imperial Metals Corporation to CCC from CCC+ and its senior unsecured notes were lowered to CCC- from CCC+. “The downgrade primarily reflects our view that Imperial Metals’ risk of default has increased from our previous expectations, following the sharp deterioration in copper prices,” said Standard & Poor’s credit analyst Jarrett Bilous. According to Standard & Poor’s, the negative outlook mainly reflects the potential for a downgrade within the next 12 months in the event that the Company defaults on its debt obligations, including a distressed exchange, or if S&P believes this to be a virtual certainty.

Momentive Performance Materials Inc. On January 27, 2016, Moody’s

Investors Service downgraded Momentive Performance Materials Inc.’s ratings, including its corporate family rating to Caa1 from B3, its probability of default rating to Caa1-PD from B3-PD, its 3.88% first-lien senior secured notes due 2021 to Caa1 from B3 and its 4.69% second-lien senior secured notes due 2022 to Caa3 from Caa2. “The change in Momentive’s rating to Caa1 from B3 comes following the company’s poor third-quarter 2015 performance, and our expectation that Momentive’s sales and margins will come under increasing pressure due to weakening end-markets for silicones, especially in Asia,” says Anthony Hill, a Moody’s Vice President - Senior Credit Officer. According to Moody’s, Momentive’s Caa1 CFR reflects the Company’s high financial leverage, which Moody’s now expects will be around 7.6x debt/EBITDA (on a Moody’s-adjusted basis) for the fiscal year ended December 2015.

Mongolian Mining Corporation

On January 27, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on Mongolian Mining Corporation (MMC) to CCC- from CCC and its senior unsecured notes were lowered to CCC- from CCC. According to Standard & Poor’s, the downgrade follows MMC’s announcement that it has hired advisors to provide advice on the potential restructuring of the Company’s outstanding notes. S&P believes any transaction or debt exchange would likely be substantially below par value, given that the Company’s unsecured notes currently trade below 30 cents on the dollar. “We believe a default is likely within the next six months barring an agreement with the company’s creditors on a restructuring,” said Standard & Poor’s credit analyst Xavier Jean. “

Profile Highlights continued on next page…

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 4

Profile Highlights, continued Postmedia Network Inc.

On January 22, 2016, Moody’s Investors Service downgraded Postmedia Network Inc.’s corporate family rating to Caa2 from B3, its probability of default rating to Caa2-PD from B3-PD, its first lien notes rating to B1 from Ba3 and its second-lien notes rating to Caa3 from Caa1. “Postmedia’s results following its April 2015 acquisition of the Sun Media assets have been worse than we expected. The downgrade was a result of our lack of confidence that the company will be able to refinance its 2017 and 2018 debt maturities at par,” said Peter Adu, a Moody’s analyst. According to Moody’s, Postmedia’s Caa2 CFR primarily reflects substantial refinancing risk in 2017 and 2018 caused by a combination of high leverage, high business risk from a continuing steep revenue decline from its traditional Canadian newspaper business and weak ability to generate replacement revenue from digital content. Spanish Broadcasting System, Inc.

On January 28, 2016, Moody’s Investors Service downgraded Spanish Broadcasting System, Inc.’s corporate family rating to Caa2 from Caa1, its probability of default rating to Caa3-PD from Caa1-PD, its $275 million senior secured notes due 2017 to Caa2 from Caa1 and its 10 3/4% Series B Preferred Stock to Ca from Caa3. According to Moody’s, the downgrades reflect the need to address restrictions related to its Voting Rights Triggering Event and the heightened potential for payment default given the near term maturity of the Company’s $275 million senior secured notes due April 2017. Moody’s further states that Spanish Broadcasting’s Caa2 CFR and Caa3-PD PDR reflect very high debt+preferred stock-to-EBITDA of 10.4x estimated for LTM December 2015. Also, since the issuance of the 12.5% notes at the beginning of 2012, consolidated revenue and EBITDA fell behind Moody’s initial forecasts, resulting in higher than expected leverage and reduced free cash flow.

Talos Energy LLC On January 25, 2016, Standard &

Poor’s Ratings Services lowered its corporate credit rating on Talos Energy LLC to B- from B and the Company’s senior unsecured notes were lowered to CCC+ from B-. “The downgrade reflects the effect of our reduced oil and natural gas price assumptions on the company’s credit measures and our estimates for higher debt leverage in 2016 and 2017,” said Standard & Poor’s credit analyst Daniel Krauss. According to Standard & Poor’s, the negative outlook reflects the potential that the rating could be lowered within the next year if the Company’s liquidity position were to weaken materially from current levels, or if they viewed the Company’s leverage as unsustainable. Terrace Energy Corp.

On January 27, 2016, Terrace Energy Corp. announced that it will not be making the January 31, 2016 interest payment on its 8% convertible unsecured notes due 2018. Pursuant to the terms of the Indenture, interest payments are payable on a quarterly basis, on the last day of January, April, July and October in each fiscal year. An event of default will occur if the Company fails to make an interest payment within the 15 day cure period provided for in the Indenture, in respect of two consecutive interest payment dates. As such, the Company will not be in default for failing to make the January 31, 2016 payment. Given current market conditions in the oil and gas industry and projected outlook and the Company’s liquidity and other requirements, the Company is reviewing strategic alternatives to preserve liquidity and its ongoing business and may seek to restructure the terms of the Notes.

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 5

Category: Distressed Debt Exchange

A.M. Castle & Co. 1420 Kensington Road, Suite 220 Oak Brook, IL 60523 847 455-7111 Officers: Scott J. Dolan -- President & C.E.O. Patrick R. Anderson -- Interim V.P. & C.F.O.

Federal Tax ID: 36-0879160 SIC: 5051 Metals Service Centers and Offices Employees: 1,667 Company Website: www.amcastle.com Auditor: Deloitte & Touche LLP

Securities: Ticker: CAS Exchange: NYSE Common Stock; 23,558,670 shares outstanding as of February 25, 2015 (CUSIP: 148411101) 12 3/4% 2nd Lien Secured Notes due 2016; $209,900,000 outstanding (CUSIP: 148411AE1) 7% Convertible Senior Notes due 2017; $57,500,000 outstanding (CUSIP: 148411AF8)

Bank Debt: First Lien Sr. Secured ABL Revolver due 2019, $125.0 million Business: A. M. Castle & Co., together with its subsidiaries, operates as a specialty metals and plastics distribution company in the United States, Canada, Mexico, France, the United Kingdom, Spain, China, and Singapore. It operates through two segments, Metals and Plastics. The Metals segment distributes engineered specialty grades and alloys of metals, as well as offers specialized processing services for Fortune 500 companies and medium and smaller sized firms. The Plastics segment stocks and distributes various plastics in forms, such as plate, rod, tube, clear sheet, tape, gaskets and fittings. Balance Sheet: ($millions) 12/31/2014 12/31/2013 Total Current Liabilities $97.50 $101.30 Total Long Term Debt $308.90 $245.00 Total Liabilities $437.70 $369.90 Total Current Assets $389.40 $390.70 Total Assets $588.00 $679.80 Income Statement: ($millions, except per share data) 12/31/2014 12/31/2013 12/31/2012 Period 12 months ending 12 months ending 12 months ending Revenue $979.80 $1,053.10 $1,270.40 Net Income $-134.70 $-34.00 $-9.70 Earnings Per Share $-5.77 $-1.46 $-0.42 Event: On January 22, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on A.M. Castle & Co. to CC from CCC+ and its 12.75% senior secured notes were lowered to CC from CCC+. According to Standard & Poor’s, the rating action reflects A.M. Castle’s January 15, 2016 announcement of an exchange offer for its senior secured notes. Source: S&P / Profile Number: 675-5553

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 6

Category: Low Rating

Extreme Reach, Inc. 75 2nd Avenue, Suite 720 Needham, MA 02494 781 577-2016 Officers: John Roland -- C.E.O. Michael Greiner -- C.F.O. Tim Conley -- C.O.O.

SIC: 7311 Advertising Agencies Employees: 1,000 Company Website: www.extremereach.com

Bank Debt: First Lien Sr. Secured Term B Loan due 2020, $365.0 million / First Lien Sr. Secured Revolver due 2019, $40.0 million / Second Lien Secured Term Loan due 2021, $165.0 million Business: Extreme Reach, Inc. provides video advertising management and distribution solutions that span television (TV), digital and mobile platforms. It offers an enterprise-class cloud-based video platform that enables a single workflow and unified measurement for TV and digital video advertising, including integrated talent and rights management capabilities that automate processes and solve compliance issues for video advertising across various screens. The Company also offers direct response ad distribution and customization services; Source Creative, a source for commercials, such as credits and contact information of key directors, editors, composers and more; and solutions for distributing syndicated content and news programming to broadcast affiliates. Its platform is used by various brands and agencies to manage, monitor and digitally deliver TV advertising; connect to post-production houses and networks of TV media destinations in North America and worldwide; and activate, measure and optimize their video advertising campaigns across screens and devices. The Company has a strategic agreement with Nielsen. Extreme Reach, Inc. was formerly known as Rozzeta, Inc. and changed its name to Extreme Reach, Inc. in November 2008. Financials Not Available Event: On January 28, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on Extreme Reach, Inc. to B- from B, its first-lien term loan and revolving facility to B+ from BB- and its second-lien term loan to CCC from CCC+. “The downgrade reflects the risk that the company could violate its leverage covenant by the first quarter of 2017,” said Standard & Poor’s credit analyst Dylan Singh. Source: S&P Profile Number: 675-6068

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 7

Category: Low Rating

Fairmount Santrol Holdings, Inc. 8834 Mayfield Road Chesterland, OH 44026 800 255-7263 Officers: Jenniffer D. Deckard -- President & C.F.O. Christopher L. Nagel -- E.V.P. & C.F.O.

Federal Tax ID: 34-1831554 SIC: 1446 Industrial Sand Employees: 1,229 Company Website: www.fairmountsantrol.com Auditor: PricewaterhouseCoopers LLP

Securities: Ticker: FMSA Exchange: NYSE Common Stock; 160,929,766 shares outstanding as of March 17, 2015 (CUSIP: 30555Q108)

Bank Debt: First Lien Sr. Secured Term B2 due 2019, $923.8 million / First Lien Sr. Secured Term B1 due 2017, $156.6 million / First Lien Sr. Secured Term B1-EXT due 2019, $161.5 million / First Lien Sr. Secured Revolver due 2018, $100.0 million Business: Fairmount Santrol Holdings Inc., together with its subsidiaries, provides sand-based proppant solutions for exploration and production companies to enhance the productivity of their oil and gas wells. The Company operates in two segments, Proppant Solutions and Industrial & Recreational (I&R) Products. The Company was formerly known as FMSA Holdings Inc. and changed its name to Fairmount Santrol Holdings Inc. in July 2015. Balance Sheet: ($millions) 12/31/2014 12/31/2013 Total Current Liabilities $141.84 $134.39 Total Long Term Debt $1,235.37 $1,246.46 Total Liabilities $1,480.54 $1,448.79 Total Current Assets $460.55 $305.34 Total Assets $1,514.02 $1,283.43 Income Statement: ($millions, except per share data) 12/31/2014 12/31/2013 12/31/2012 Period 12 months ending 12 months ending 12 months ending Revenue $1,356.46 $988.39 $885.19 Net Income $170.62 $104.66 $149.47 Earnings Per Share $1.08 $0.67 $0.96 Event: On January 27, 2016, Moody’s Investors Service downgraded Fairmount Santrol, Inc.’s corporate family rating to Caa1 from B2, its probability of default rating to Caa2-PD from B3-PD and its senior secured credit facility to Caa1 from B2. According to Moody’s, the rating downgrade and negative outlook reflect the expectation that EBITDA and key credit metrics will deteriorate further in 2016 as a result of the persistent weakness in the oil and natural gas industry. Source: Moody’s Profile Number: 675-6063

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 8

Category: Low Rating

GrafTech International Ltd. 6100 Oak Tree Boulevard Independence, OH 44131 216 676-2000 Officers: Joel L. Hawthorne -- President & C.E.O. Quinn J. Coburn -- V.P. & C.F.O. Jeffrey C. Dutton -- V.P. & C.O.O.

Federal Tax ID: 27-2496053 SIC: 3624 Carbon and Graphite Products Employees: 2,397 Company Website: www.graftech.com Auditor: PricewaterhouseCoopers LLP

Securities: 6 3/8% Senior Notes due 2020; $300,000,000 outstanding (CUSIP: 384313AD4)

Bank Debt: First Lien Sr. Secured Term A-DD Loan due 2019, $40.0 million / First Lien Sr. Secured Revolver due 2019, $375.0 million Business: GrafTech International Ltd. manufactures and sells graphite and carbon material science-based solutions. It operates through two segments, Industrial Materials and Engineered Solutions. The Industrial Materials segment manufactures and delivers graphite electrodes. The Engineered Solutions segment provides extruded and molded graphite blocks and machined graphite parts that are used in metallurgy, high-temperature industrial and alternative energy applications. As of August 13, 2015, GrafTech International Ltd. was taken private. Balance Sheet: ($millions) 12/31/2014 12/31/2013 Total Current Liabilities $351.90 $215.88 Total Long Term Debt $341.62 $541.59 Total Liabilities $829.30 $897.10 Total Current Assets $644.99 $775.66 Total Assets $1,833.81 $2,217.85 Income Statement: ($millions, except per share data) 12/31/2014 12/31/2013 12/31/2012 Period 12 months ending 12 months ending 12 months ending Revenue $1,085.30 $1,166.67 $1,248.26 Net Income $-285.79 $-40.10 $134.49 Earnings Per Share $-2.10 $-0.20 $0.85 Event: On January 22, 2016, Moody’s Investors Service downgraded all long-term ratings for GrafTech International Ltd., including the corporate family rating to B3 from Ba3 and the Company’s $300 million senior unsecured notes due 2020 to Caa1 from B1. According to Moody’s, the ratings downgrades are based on the view that business conditions in the graphite electrode industry have weakened materially over the past several months such that GrafTech’s financial performance will decline meaningfully in 2016. Source: Moody’s Profile Number: 675-6064

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 9

Category: Preferred Dividend Omission

Halcon Resources Corporation 1000 Louisiana Street, Suite 6700 Houston, TX 77002 832 538-0300 Officers: Floyd C. Wilson -- Chairman, C.E.O. Mark J. Mize -- E.V.P. & C.F.O.

Federal Tax ID: 20-0700684 SIC: 1311 Crude Petroleum and Natural Gas Employees: 419 Company Website: www.halconresources.com Auditor: Deloitte & Touche LLP

Securities: Ticker: HK Exchange: NYSE Common Stock; 605,177,240 shares outstanding as of November 2, 2015 (CUSIP: 40537Q209) 5.75% Series A Cumulative Perpetual Convertible Preferred Stock; 244,934 shares outstanding 8 7/8% Senior Notes due 2021; $1,289,420,000 outstanding (CUSIP: 40537QAD2) 9 3/4% Senior Notes due 2020; $959,980,000 outstanding (CUSIP: 40537QAB6)

Bank Debt: First Lien Senior Secured Revolver due 2017, $1,500.0 million Business: Halcon Resources Corporation, an independent energy company, is engaged in the acquisition, production, exploration and development of onshore oil and natural gas properties in the United States. The Company primarily holds interests the Bakken/Three Forks Formations comprising approximately 129,000 net acres of area in North Dakota; and East Texas Eagle Ford Formations covering approximately 101,000 acres of area in Brazos, Burleson, and Robertson counties. The Company was formerly known as RAM Energy Resources, Inc. and changed its name to Halcon Resources Corporation in February 2012. Balance Sheet: ($millions) 12/31/2014 12/31/2013 Total Current Liabilities $744.68 $664.40 Total Long Term Debt $3,746.74 $3,183.80 Total Liabilities $4,545.10 $3,908.90 Total Current Assets $702.71 $338.60 Total Assets $6,434.48 $5,356.50 Income Statement: ($millions, except per share data) 12/31/2014 12/31/2013 12/31/2012 Period 12 months ending 12 months ending 12 months ending Revenue $1,148.26 $999.50 $248.30 Net Income $315.96 $-1,222.70 $-53.89 Earnings Per Share $0.68 $-3.25 $-0.91 Event: On January 28, 2016, Halcon Resources Corporation announced that its Board of Directors has suspended the payment of regular quarterly dividends on shares of its 5.75% Series A Cumulative Perpetual Convertible Preferred Stock. Source: Press Release / Profile Number: 675-5504

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 10

Category: Low Rating

Hidili Industry International Development Ltd. 16th Floor Dingli Mansion No 81 Renmin Road Panzhihua, Sichuan Province China 617000 86 81 2335 7888 Officers: Jiankun Sun -- C.E.O. Lai Kuen Chu -- C.F.O.

SIC: 1221 Bituminous Coal and Lignite Surface Mining Employees: 5,153 Company Website: www.hidili.com.cn Auditor: Deloitte Touche Tohmatsu

Securities: Ticker: HIIDY Exchange: OTC Also trades in Hong Kong (1393) Common Stock; 2,045,598,399 shares outstanding as of November 5, 2015 (CUSIP: 42952W109) 8 5/8% Senior Notes due 2015; $182,751,000 outstanding (CUSIP: 42952UAA1) Business: Hidili Industry International Development Limited, an investment holding company, is engaged in the mining, manufacture and sale of clean coal in the Peoples Republic of China. Its Coal Mining segment produces and sells clean coal and its by-products. The Company’s Others segment manufactures and sells alloy pig iron and other producs. It is also involved in the clean coal washing activities. Hidili Industry International Development Limited is a subsidiary of Sanlian Investment Holding Limited. Balance Sheet: (CNYmillions) 12/31/2014 12/31/2013 Total Current Liabilities CNY5,536.00 CNY6,285.10 Total Long Term Debt CNY2,868.10 CNY1,658.50 Total Liabilities CNY8,488.70 CNY8,086.80 Total Current Assets CNY2,088.20 CNY3,283.80 Total Assets CNY14,085.50 CNY15,104.80 Income Statement: (CNYmillions, except per share data) 12/31/2014 12/31/2013 12/31/2012 Period 12 months ending 12 months ending 12 months ending Revenue CNY719.90 CNY729.10 CNY1,923.60 Net Income CNY-142.30 CNY-424.70 CNY-147.40 Earnings Per Share CNY-0.70 CNY-0.21 CNY-0.07 Event: On January 22, 2016, Moody’s Investors Service downgraded Hidili Industry International Development Ltd.’s corporate family rating to C from Caa2. “The downgrade reflects Hidili’s ongoing default situation and lowered expected recovery rate resulting from the distressed coal price environment,” says Dylan Yeo, a Moody’s Analyst. Source: Moody’s Profile Number: 675-5461

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 11

Category: Low Rating

Imperial Metals Corporation 580 Hornby Street, Suite 200 Vancouver, British Columbia Canada V6C 3B6 604 669-8959 Officers: Brian J. Kynoch – President Andre Henry Deepwell -- C.F.O. Don Parsons -- C.O.O.

SIC: 1041 Gold Ores Employees: 877 Company Website: www.imperialmetals.com Auditor: Deloitte & Touche LLP

Securities: Ticker: IPMLF Exchange: OTC Also trades on TSX (III) 7% Senior Notes due 2019; $325,000,000 outstanding (CUSIP: 452892AA0) Common Stock; 81,741,028 shares outstanding as of October 30, 2015 (CUSIP: 452892102)

Bank Debt: First Lien Sr. Secured Revolver due 2016, C$150.0 million / First Lien Sr. Secured Revolver due 2017, $50.0 million / First Lien Sr. Secured Revolver A due 2016, C$50.0 million Business: Imperial Metals Corporation acquires, explores for, develops, mines and produces base and precious metals in Canada. The Company explores for gold, copper, zinc and lead. It operates through Mount Polley, Huckleberry, Red Chris and Sterling segments. The Company primarily holds interests in the Red Chris copper/goldmine in northwest British Columbia; Mount Polley copper/gold mine in central British Columbia; and Huckleberry copper mine in northern British Columbia. Its principal projects also include Sterling goldmine in southwest Nevada, the United States.

Balance Sheet: (C$millions) 12/31/2014 12/31/2013 Total Current Liabilities C$119.90 C$216.80 Total Long Term Debt C$694.30 C$234.00 Total Liabilities C$930.40 C$557.30 Total Current Assets C$63.50 C$54.00 Total Assets C$1,338.40 C$975.50

Income Statement: (C$millions, except per share data) 12/31/2014 12/31/2013 12/31/2012 Period 12 months ending 12 months ending 12 months ending Revenue C$65.00 C$187.80 C$199.40 Net Income C$-70.20 C$41.00 C$32.60 Earnings Per Share C$-0.93 C$0.55 C$0.44

Event: On January 27, 2016, Standard & Poor’s Ratings Services lowered its long-term corporate credit rating on Imperial Metals Corporation to CCC from CCC+ and its senior unsecured notes were lowered to CCC- from CCC+. “The downgrade primarily reflects our view that Imperial Metals’ risk of default has increased from our previous expectations, following the sharp deterioration in copper prices,” said Standard & Poor’s credit analyst Jarrett Bilous. Source: S&P / Profile Number: 675-5735

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 12

Category: Low Rating

Momentive Performance Materials Inc. 260 Hudson River Road Waterford, NY 12188 518 237-3330 Officers: John G. Boss -- C.E.O., President Erick R. Asmussen -- C.F.O.

SIC: 2869 Industrial Organic Chemicals, not Elsewhere Classified Employees: 4,600 Company Website: www.momentive.com

Securities: 3.88% 1st Lien Senior Secured Notes due 2021; $1,100,000,000 outstanding (CUSIP: 60877UBE6) 4.69% 2nd Lien Secured Notes due 2022; $250,000,000 outstanding (CUSIP: 60877UBF3) Business: Momentive Performance Materials Inc., together with its subsidiaries, produces silicones and silicone derivatives and products derived from quartz and specialty ceramics. The Company manufactures, sells and distributes silanes, specialty silicones and urethane additives. It offers fluids for use in textiles, personal care, home care, agriculture and oil and gas applications; silanes and resins for use in tires, additives for coatings, masonry water repellents and protective coatings for plastics and rubber; elastomers for use in healthcare and automotive applications; intermediates including siloxane, silane, and by-product materials used as inputs for other product portfolios; and specialty coatings used in construction, tape and label, adhesives, electronics and automotive markets. The Company also provides room temperature vulcanizers consisting of engineered gels, greases, adhesives, encapsulants and sealants; urethane additives, including polyurethane foam additives and silicone surfactants; consumer sealants used by homeowners, builders and contractors; and construction sealants used in structural glazing, weather-sealing and insulated glass applications. Additionally, it offers fused quartz and ceramic materials for use in semiconductor, lamp tubing, manufacturing, packaging, cosmetic and fiber optic industries. It produces quartz tubing, ingots and crucibles, non-oxide ceramic powders, coatings and solids. Financials Not Available Event: On January 27, 2016, Moody’s Investors Service downgraded Momentive Performance Materials Inc.’s ratings, including its corporate family rating to Caa1 from B3, its probability of default rating to Caa1-PD from B3-PD, its 3.88% first-lien senior secured notes due 2021 to Caa1 from B3 and its 4.69% second-lien senior secured notes due 2022 to Caa3 from Caa2. “The change in Momentive’s rating to Caa1 from B3 comes following the company’s poor third-quarter 2015 performance, and our expectation that Momentive’s sales and margins will come under increasing pressure due to weakening end-markets for silicones, especially in Asia,” says Anthony Hill, a Moody’s Vice President - Senior Credit Officer. Source: Moody’s Profile Number: 675-6065

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 13

Category: Low Rating

Mongolian Mining Corporation Central Tower 16th Floor, Sukhbaatar District Ulaanbaatar, Mongolia 14200 976 7012 2279 Officers: Battsengel Gotov -- C.E.O. Ulemj Baskhuu -- C.F.O. & E.V.P. Samuel Bowles -- C.O.O. & E.V.P.

SIC: 1241 Coal Mining Services Employees: 1,897 Company Website: www.mmc.mn Auditor: KPMG LLP

Securities: Ticker: MOGLF Exchange: OTC Also trades in Hong Kong (975) 8 7/8% Senior Notes due 2017; $600,000,000 outstanding (CUSIP: 60937CAA3) Common Stock; 9,262,591,250 shares outstanding as of December 29, 2014

Bank Debt: First Lien Sr. Secured Term Loan due 2016, $180.0 million / First Lien Sr. Secured Term Loan due 2016, $150.0 million Business: Mongolian Mining Corporation, together with its subsidiaries, engages in the mining, production, transportation, sale and export of coking coal products in Mongolia and China. The Company owns and operates two open-pit coking coal mines comprising the Ukhaa Khudag deposit covering an area of approximately 2,960 hectares located within the Tavan Tolgoi coal formation in Southern Gobi of Mongolia; and the Baruun Naran coking coal deposit covering an area of approximately 4,482 hectares area located in Khankhongor soum of Umnugobi aimag, Mongolia. Balance Sheet: ($millions) 12/31/2014 12/31/2013 Total Current Liabilities $413.00 $433.30 Total Long Term Debt $757.90 $744.40 Total Liabilities $1,286.00 $1,337.90 Total Current Assets $454.40 $449.00 Total Assets $1,682.80 $1,898.90 Income Statement: ($millions, except per share data) 12/31/2014 12/31/2013 12/31/2012 Period 12 months ending 12 months ending 12 months ending Revenue $328.30 $437.30 $474.50 Net Income $-282.80 $-58.10 $-2.50 Earnings Per Share $-0.06 $-0.01 $-0.00 Event: On January 27, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on Mongolian Mining Corporation (MMC) to CCC- from CCC and its US$600 million senior unsecured notes were lowered to CCC- from CCC. According to Standard & Poor’s, the downgrade follows MMC’s announcement that it has hired advisors to provide advice on the potential restructuring of the Company’s outstanding notes. Source: S&P Profile Number: 675-5535

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 14

Category: Debt at Discount

Murphy Oil Corporation 200 Peach Street, P.O. Box 7000 El Dorado, AR 71731 870 862-6411 Officers: Roger W. Jenkins -- President & C.E.O. Kevin G. Fitzgerald -- E.V.P. & C.F.O.

Federal Tax ID: 71-0361522 SIC: 1311 Crude Petroleum and Natural Gas Employees: 1,712 Company Website: www.murphyoilcorp.com Auditor: KPMG LLP

Securities: Ticker: MUR Exchange: NYSE Common Stock; 177,501,534 shares outstanding as of January 31, 2015 (CUSIP: 626717102) 2 1/2% Senior Notes due 2017; $550,000,000 outstanding (CUSIP: 626717AE2) 4% Senior Notes due 2022; $500,000,000 outstanding (CUSIP: 626717AD4) 3.7% Senior Notes due 2022; $600,000,000 outstanding (CUSIP: 626717AF9)

Bank Debt: First Lien Sr. Secured Revolver due 2017, $2,000.0 million / First Lien Sr. Secured Revolver due 2019, $40.0 million / Second Lien Secured Term Loan due 2021, $165.0 million Business: Murphy Oil Corporation operates as an oil and gas exploration and production company worldwide. It explores for and produces crude oil, natural gas and natural gas liquids. The Company was formerly known as Murphy Corporation and changed its name to Murphy Oil Corporation in 1964. Balance Sheet: ($millions) 12/31/2015 12/31/2014 Total Current Liabilities $1,665.80 $3,147.89 Total Long Term Debt $3,040.60 $2,536.24 Total Liabilities $6,168.80 $8,168.90 Total Current Assets $1,448.40 $3,279.15 Total Assets $11,492.10 $16,742.31 Income Statement: ($millions, except per share data) 12/31/2015 12/31/2014 12/31/2013 Period 12 months ending 12 months ending 12 months ending Revenue $2,200.80 $5,476.08 $5,390.09 Net Income $-2,270.80 $905.61 $1,123.47 Earnings Per Share $-13.02 $5.06 $5.98 Event: During the week of January 25, 2016, Murphy Oil Corporation’s 3.7% Senior Notes due 2022 were trading at a level around $58.235. Source: Bloomberg Profile Number: 675-6069

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 15

Category: Low Rating

Postmedia Network Inc. 365 Bloor Street East Toronto, Ontario Canada M4W 3L4 416 383-2300 Officers: Paul Godfrey -- President, C.E.O. Douglas Lamb -- E.V.P., C.F.O.

SIC: 2711 Newspapers: Publishing, or Publishing and Printing Employees: 4,733 Company Website: www.postmedia.com Auditor: PricewaterhouseCoopers LLP

Securities: Ticker: PCDAF Exchange: OTC Also trades on TSX (PNC) Common Stock; 1,040,153 Class C shares outstanding as of August 31, 2015 (CUSIP: 73752W106) 8 1/4% Senior Secured Notes due 2017; $319,050,000 outstanding (CUSIP: 737524AE8) 12 1/2% Secured Notes due 2018; $221,720,000 outstanding (CUSIP: 737524AC2) Business: Postmedia Network Inc. publishes daily and non-daily newspapers in Canada. It engages in the news and information gathering and dissemination operations through various English-language daily and community newspapers, online, digital and mobile platforms. The Company owns and operates 10 daily metropolitan newspapers; the National Post, a daily national newspaper; 2 daily community newspapers; 24 non-daily community newspapers; non-daily shopping guides; and newspaper-related publications. Postmedia Network Inc. is a subsidiary of Postmedia Network Canada Corp. Balance Sheet: ($millions) 08/31/2015 08/31/2014 Total Current Liabilities $169.04 $111.38 Total Long Term Debt $646.34 $743.80 Total Liabilities $963.39 $729.65 Total Current Assets $191.63 $107.54 Total Assets $874.10 $740.59 Income Statement: ($millions, except per share data) 08/31/2015 08/31/2014 08/31/2013 Period 12 months ending 12 months ending 12 months ending Revenue $750.28 $674.26 $751.58 Net Income $-263.41 $-107.46 $-160.23 Earnings Per Share $-1.98 $-2.67 $-3.98 Event: On January 22, 2016, Moody’s Investors Service downgraded Postmedia Network Inc.’s corporate family rating to Caa2 from B3, its probability of default rating to Caa2-PD from B3-PD, its first lien notes rating to B1 from Ba3 and its second-lien notes rating to Caa3 from Caa1. “Postmedia’s results following its April 2015 acquisition of the Sun Media assets have been worse than we expected. The downgrade was a result of our lack of confidence that the company will be able to refinance its 2017 and 2018 debt maturities at par,” said Peter Adu, a Moody’s analyst. Source: Moody’s Profile Number: 675-5403

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 16

Category: Low Rating

Spanish Broadcasting System, Inc. 7007 NW 77th Avenue Miami, FL 33166 305 441-6901 Officers: Raul Alarcon, Jr. -- Chairman, C.E.O. & President Joseph A. Garcia -- S.E.V.P., C.F.O. & C.A.O.

Federal Tax ID: 13-3827791 SIC: 4832 Radio Broadcasting Stations Employees: 439 Company Website: www.spanishbroadcasting.com Auditor: Crowe Horwath LLP

Securities: Ticker: SBSA Exchange: NASDAQ Common Stock; 4,166,991 shares outstanding as of March 21, 2014 (CUSIP: 846425833) Series C Convertible Preferred Stock; 380,000 shares outstanding (CUSIP: 846425783) 12 1/2% Senior Secured Notes due 2017; $275,000,000 outstanding (CUSIP: 846425AN6) Business: Spanish Broadcasting System, Inc. operates as a Spanish-language media and entertainment company in the United States. It operates in two segments, Radio and Television. The Company produces and distributes Spanish-language content, including radio programs, television shows and music and live entertainment. It owns and operates 20 radio stations in the Los Angeles, New York, Puerto Rico, Chicago, Miami and San Francisco markets; AIRE radio networks with over 103 affiliate radio stations; and 3 television stations under the MegaTV brand, as well as has various MegaTV broadcasting outlets under affiliation or programming agreements. Balance Sheet: ($millions) 12/31/2014 12/31/2013 Total Current Liabilities $161.13 $157.52 Total Long Term Debt $276.00 $275.00 Total Liabilities $526.00 $516.20 Total Current Assets $53.31 $56.27 Total Assets $451.81 $461.75 Income Statement: ($millions, except per share data) 12/31/2014 12/31/2013 12/31/2012 Period 12 months ending 12 months ending 12 months ending Revenue $146.28 $153.77 $139.52 Net Income $-19.95 $-88.57 $-1.30 Earnings Per Share $-2.75 $-1.34 $-1.22 Event: On January 28, 2016, Moody’s Investors Service downgraded Spanish Broadcasting System, Inc.’s corporate family rating to Caa2 from Caa1, its probability of default rating to Caa3-PD from Caa1-PD, its $275 million senior secured notes due 2017 to Caa2 from Caa1 and its 10 3/4% Series B Preferred Stock to Ca from Caa3. According to Moody’s, the downgrades and Negative outlook reflect the need to address restrictions related to its Voting Rights Triggering Event and the heightened potential for payment default given the near term maturity of the Company’s $275 million senior secured notes due April 2017. Source: Moody’s / Profile Number: 675-3968

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 17

Category: Low Rating

Talos Energy LLC 500 Dallas Street, Suite 2000 Houston, TX 77002 713 328-3000 Officers: Timothy S. Duncan -- C.E.O. & President Michael Harding -- C.F.O. & S.V.P. Stephen E. Heitzman -- C.O.O. & E.V.P.

SIC: 1382 Oil and Gas Field Exploration Services Employees: 91 Company Website: www.talosenergyllc.com

Bank Debt: First Lien Sr. Secured Revolver due 2019, $500.0 million Business: Talos Energy LLC, an oil and gas company, engages in the exploration, development, and production of oil and natural gas properties in the Gulf of Mexico Shelf and Developed Deepwater. Financials Not Available Event: On January 25, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on Talos Energy LLC to B- from B and the Company’s senior unsecured notes were lowered to CCC+ from B-. “The downgrade reflects the effect of our reduced oil and natural gas price assumptions on the company’s credit measures and our estimates for higher debt leverage in 2016 and 2017,” said Standard & Poor’s credit analyst Daniel Krauss. Source: S&P Profile Number: 675-6066

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 18

Category: Miscellaneous

Terrace Energy Corp. 1030 West Georgia Street, Suite 1012 Vancouver, BC Canada V6E 2Y3 604 282-7897 Officers: William D. Gibbs -- C.E.O. & President Keith R. Godwin -- C.F.O. & V.P. George R. Morris -- C.O.O. & S.V.P.

SIC: 1311 Crude Petroleum and Natural Gas Employees: 9 Company Website: www.terraceenergy.net Auditor: Smythe LLP

Securities: Ticker: TCRRF Exchange: OTC Also trades on TSX (TZR) Common Stock; 87,844,821 shares outstanding as of December 31, 2015 (CUSIP: 88103M102) 8% Convertible Senior Notes due 2018; $38,590,000 outstanding (CUSIP: 88103MAA0) Business: Terrace Energy Corp. engages in the acquisition, exploration and development of unconventional onshore oil and gas properties in the United States. Its principal projects include Olmos Tight Sandstone Development project covering approximately 14,400 gross mineral acres in LaSalle and McMullen counties, Texas; the Maverick County project covering approximately 147,000 gross mineral acres in Maverick and Zavala Counties, Texas; and the Big Wells Project covering approximately 10,130 gross mineral acres in Dimmit and Zavala Counties, Texas. The Company was formerly known as Terrace Resources Inc. and changed its name to Terrace Energy Corp. in June 2011. Balance Sheet: ($millions) 01/31/2015 01/31/2014 Total Current Liabilities $4.57 $1.12 Total Long Term Debt $51.30 $31.29 Total Liabilities $56.34 $32.51 Total Current Assets $30.01 $23.17 Total Assets $73.64 $55.15 Income Statement: ($millions, except per share data) 01/31/2015 01/31/2014 01/31/2013 Period 12 months ending 12 months ending 12 months ending Revenue $6.73 $5.72 $3.42 Net Income $-24.51 $-6.58 $-0.12 Earnings Per Share $-0.30 $-0.10 $0.00 Event: On January 27, 2016, Terrace Energy Corp. announced that it will not be making the January 31, 2016 interest payment on its 8% convertible unsecured notes due 2018. Pursuant to the terms of the Indenture, interest payments are payable on a quarterly basis, on the last day of January, April, July and October in each fiscal year. An event of default will occur if the Company fails to make an interest payment within the 15 day cure period provided for in the Indenture, in respect of two consecutive interest payment dates. As such, the Company will not be in default for failing to make the January 31, 2016 payment. Source: Press Release / Profile Number: 675-6067

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 19

Distressed Company Alert Profile Updates

Verso Corporation – Chapter 11 – January 26, 2016

Verso and 26 affiliated Debtors filed for Chapter 11 protection with the U.S. Bankruptcy Court in the District of Delaware, lead case number 16-10163. The Company, which produces coated papers, including printing papers and specialty papers and high quality market pulp, is represented by Mark D. Collins of Richards, Layton & Finger. "While filing for Chapter 11 protection was a difficult decision, we are pleased that we enter this process with strong creditor support. We have worked together with a broad spectrum of financial creditors to develop a restructuring plan to eliminate $2.4 billion of our outstanding debt and to exit the Chapter 11 process in a short timeframe," said Verso's president and C.E.O., David J. Paterson. The expected agreement on terms for a plan of reorganization is with creditors holding at least a majority in principal amount of most classes of funded debt of Verso and its subsidiaries. Verso anticipates that upon finalizing agreed-upon terms, the plan of reorganization would result in the holders of its funded debt receiving equity of Verso in exchange for their claims. The Company also expects to finalize a debtor-in-possession financing package totaling up to $600 million shortly that, once approved by the Court, will provide the Company with significant operational flexibility to successfully reorganize. Discussing the need for a Chapter 11 filing, Paterson explains: "[S]ince Verso acquired NewPage Holdings Inc. in January 2015, a confluence of external factors, including an accelerated and unprecedented decline in demand…products, a significant increase in foreign imports resulting from a strong U.S. dollar relative to foreign currencies, and Verso's impending financial obligations made it apparent that action was needed." Subsidiary Debtor NewPage emerged from a previous Chapter 11 filing in December 2012.

Previous DCA Event: Miscellaneous 1/16/2016 Previous DCA Event: Low Rating 1/9/2014 Previous DCA Event: Miscellaneous 11/16/2015 Previous DCA Event: Low Rating 11/28/2012 Previous DCA Event: DDE 1/8/2015 Previous DCA Event: Low Rating 5/3/2012 Previous DCA Event: Low Rating 6/25/2014 Previous DCA Event: Audit Concern 4/15/2008

Updates: 7/2/15, 1/16/15, 7/11/14, 3/8/13, 2/8/13, 1/25/13, 12/7/12, 5/8/12 Watch List: 1/16/15

Nuo Therapeutics, Inc. (f/k/a Cytomedix, Inc.) – Chapter 11 – January 26, 2016

Nuo Therapeutics filed for Chapter 11 protection with the U.S. Bankruptcy Court in the District of Delaware, case number 16-10192. The Company, which pioneers leading-edge biodynamic therapies for wound care, is represented by William P. Bowden of Ashby & Geddes. The Company announced that it will request approval of an aggregate of approximately $9 million in debtor-in-possession financing from its pre-bankruptcy lenders: Deerfield Management and certain of its affiliates. The Company will continue to operate its business as a debtor-in-possession during the reorganization and expects that substantially all of its assets will be sold pursuant to a bankruptcy court supervised process under Section 363 of the Bankruptcy Code.

Previous DCA Event: Audit Concern 3/9/2012

For more information on this filing and other bankruptcy filings, go to www.bankruptcydata.com

Profile Updates continued on next page…

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 20

Distressed Company Alert Profile Updates, continued

Aspect Software (Parent), Inc. Previous DCA Event: Low Rating 12/7/2015

On December 7, 2015, Moody’s Investors Service downgraded Aspect Software, Inc.’s corporate family rating to Caa2 from B3, its probability of default rating to Caa2-PD from B3-PD, its 1st lien debt facilities to B3 from B1 and its second lien notes to Caa3 from Caa2. According to Moody’s, the downgrade was driven by challenges the Company is facing in offsetting declines in its legacy product lines, high debt levels and upcoming debt maturities. S&P Lowers Ratings

On January 22, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on Aspect Software, Inc. to CCC- from CCC+, its $445 million first lien term loan and $30 million revolving credit facility to CCC from B- and its second lien notes to CC from CCC. “The downgrade reflects our view that Aspect’s refinancing risk has escalated because a majority of the company’s capital structure comes due in less than six months,” said Standard & Poor’s credit analyst Kenneth Fleming.

Chesapeake Energy Corporation Previous DCA Event: Low Rating 12/22/2015

On December 22, 2015, Standard & Poor’s Ratings Services lowered its corporate credit rating on Chesapeake Energy Corporation to B from BB-, its senior unsecured debt rating to CCC+ from BB-, its senior secured debt to BB- from BB+ and its preferred stock to CCC from B-. “We have reassessed Chesapeake’s business risk and have revised our assessment lower to fair from satisfactory,” said Standard & Poor’s credit analyst Paul Harvey. S&P Lowers Further

On January 25, 2016, Standard & Poor’s Ratings Services lowered its ratings on Chesapeake Energy Corporation, including its corporate credit rating to CCC+ from B and its senior unsecured debt ratings to CCC- from CCC+. “The downgrade reflects the implementation of the recent change in our base case oil and natural gas price assumptions,” said Standard & Poor’s credit analyst Paul Harvey. Based on Standard & Poor’s price assumptions, only limited improvement is expected in the near-term and that Chesapeake will face both a challenging operating environment and weak capital markets as about $2 billion of debt comes due in 2017. Cliffs Natural Resources Inc. Previous DCA Event: Low Rating 1/5/2016

On January 5, 2016, Moody’s Investors Service downgraded Cliffs Natural Resources Inc.’s corporate family and probability of default ratings to Caa1 and Caa1-PD from B1 and B1-PD respectively, as well as its senior secured 1st lien notes to B1 from Ba2, its senior secured 2nd lien notes to B3 from B1 and its senior unsecured notes to Caa2 from B3. According to Moody’s, the downgrade reflects the deterioration in the Company’s debt protection metrics and increase in leverage as a result of continued downward movement in iron ore prices and weak fundamentals in the US steel industry, which are resulting in lower shipment levels. S&P Lowers Ratings / Distressed Debt Exchange

On January 28, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on Cliffs Natural Resources Inc. to CC from B, its second-lien notes to CC from BB- and its senior unsecured notes to CC from B. According to Standard & Poor’s, the rating action reflects Cliffs’ January 27, 2016, announcement of a private debt exchange offer for its second-lien and senior unsecured debt. Standard & Poor’s views the exchange to be distressed, according to its criteria.

Profile Updates continued on next page…

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 21

Distressed Company Alert Profile Updates, continued Consolidated Minerals Limited Previous DCA Event: Profile Update 12/23/2015

On December 23, 2015, Moody’s Investors Service downgraded the corporate family and probability of default ratings of Consolidated Minerals Limited (Consmin) to Caa1 from B3 and to Caa1-PD from B3-PD, respectively. Concurrently, the rating agency downgraded the ratings on the senior secured notes issued by Consmin due 2020 to Caa1 from B3. “Our downgrade reflects the knock on impact on Consmin of a significantly reduced FOB manganese price of $2.42/dmtu in Q3-2015 from $3.83/dmtu in Q3-2014 and that its EBIT generation no longer covers its interest expense,” said Douglas Rowlings, Moody’s Analyst and local market analyst for Consmin. S&P Lowers Ratings

On January 27, 2016, Standard & Poor’s Ratings Services lowered its long-term corporate credit rating on Consolidated Minerals Limited to CCC from CCC+ and its $400 million senior secured notes due 2020 to CCC from CCC+. According to Standard & Poor’s, the rating action follows the Company’s announcement that it will be transitioning its Australian mine into care and maintenance from February 2, 2016. Although this measure is cash-conserving, S&P understands it reflects further deterioration of the market environment. Eclipse Resources Corporation Previous DCA Event: Low Rating 1/19/2016

On January 19, 2016, Moody’s Investors Service downgraded Eclipse Resources Corporation’s corporate family rating to Caa2 from B3, its probability of default rating to Caa2-PD from B3-PD and its senior unsecured notes rating to Caa2 from Caa1. “The downgrade reflects Moody’s expectation that low natural gas prices and significant production curtailments will drive down Eclipse’s cash flow such that it may not cover interest expense,” noted John Thieroff, Moody’s VP -- Senior Analyst. S&P Lowers Ratings

On January 22, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on Eclipse Resources Corporation to CC from B- and its senior unsecured notes due December 2023 to CC from CCC+. “The downgrade follows Eclipse’s announcement that it has launched an exchange offer to existing holders of its $550 million senior unsecured notes for a new issue of 9% senior secured second-lien notes due 2023.” Gibson Brands, Inc. Previous DCA Event: Profile Low Rating 12/22/2015

On December 22, 2015, Moody’s Investors Services downgraded Gibson Brands, Inc.’s ratings, including its corporate family rating to B3 from B2, its probability of default rating to B3-PD from B2-PD and its $375 million senior secured 2nd lien notes due 2018 to Caa1 from B3 following the Company’s very weak quarterly results, pushing credit metrics below Moody’s expectation and putting stress on Gibson’s liquidity profile. “The downgrade reflects Gibson’s weak liquidity position and soft credit metrics,” said Kevin Cassidy, a Moody’s Senior Credit Officer. S&P Lowers Ratings

On January 28, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on Gibson Brands, Inc. to CCC+ from B- and its $375 million senior secured notes due 2018 to CCC+ from B-. “The downgrade reflects our concern that the increase in financial obligations following the agreement made with Philips N.V. for overdue receivables will further pressure the company’s slowly improving cash flow outlook,” said Standard & Poor’s credit analyst Stephanie Harter.

Profile Updates continued on next page…

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 22

Distressed Company Alert Profile Updates, continued Horsehead Holding Corp Previous DCA Event: Profile Update 1/20/2016

On January 20, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on Horsehead Holding Corp. to SD from CCC and affirmed the CCC issue-level rating on the Company’s senior secured notes. “Given our view of the company’s debt level as unsustainable, and ongoing restructuring discussions, we do not expect a payment to be made within the grace period. In accordance with our criteria, we are lowering the corporate credit rating to ‘SD’,” said Standard & Poor’s credit analyst Ryan Gilmore. Moody’s Downgrades

On January 25, 2016, Moody’s Investors Service downgraded the ratings of Horsehead Holding Corp., including its corporate family rating to Ca from Caa2, probability of default rating to Ca-PD from Caa2-PD and senior secured notes to Ca from Caa1. According to Moody’s, the downgrade follows the Company’s announcement that it decided to temporarily idle its zinc smelter in Mooresboro, North Carolina, as well as its previous announcements that it had entered into forbearance agreements with respect to its credit agreements, under which its creditors had agreed to temporarily forebear from their rights related to events of default under the agreements. Rex Energy Corporation Previous DCA Event: Low Rating 1/8/2016

On January 8, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on Rex Energy Corporation to CCC- from B- and its senior unsecured notes to CC from CCC+. According to Standard & Poor’s, the downgrade follows Rex’s announcement that it has scheduled a special meeting of stockholders on January 11, 2016, to gain authorization and approval to negotiate a transaction with Franklin Resources Inc., which may involve the issuance of additional equity or debt securities, or restructuring or refinancing of existing debt, or a combination of these. Moody’s Downgrades

On January 25, 2016, Moody’s Investors Service downgraded Rex Energy Corporation’s corporate family rating to Caa3 from Caa1, its probability of default rating to Caa3-PD from Caa1-PD and its senior unsecured notes to Ca from Caa2. “The ratings downgrade was driven by the continued steep deterioration in the commodity price environment, its impact on the credit metrics of REXX and the increased likelihood of a distressed debt exchange…has significantly elevated the potential for purchases of debt at steep discounts to the face value or other balance sheet restructuring including bankruptcy filing,” commented Sreedhar Kona, Moody’s Senior Analyst. SandRidge Energy, Inc. Previous DCA Event: Dividend Omission 1/8/2016

On January 8, 2016, SandRidge Energy, Inc. announced that its Board of Directors has decided to suspend payment of the $4.25 per share semi-annual dividend on shares of its 8.5% Convertible Perpetual Preferred Stock. The dividend suspension follows the prior suspension of dividend payments on shares of the Company’s 7.0% Convertible Perpetual Preferred Stock announced on September 28, 2015 and reflects the Company’s continued focus on preservation of liquidity, prudent capital allocation and support of long-term enterprise value. Professionals Retained

In Form 8-K field on January 25, 2016, SandRidge Energy, Inc. stated that it has retained Kirkland & Ellis LLP, as legal advisor, and Houlihan Lokey, Inc., as financial advisor, to assist the Company in analyzing and considering financial, transactional and strategic alternatives. No further action or disclosures are anticipated at this time.

Profile Updates continued on next page…

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 23

Distressed Company Alert Profile Updates, continued Seventy Seven Energy Inc. Previous DCA Event: Low Rating 1/14/2016

On January 14, 2016, Standard & Poor’s Ratings Services lowered its corporate credit rating on Seventy Seven Energy Inc. to CCC- from CCC+, its secured notes to CCC+ from B, its unsecured notes to CCC- from CCC+ and its structurally subordinated unsecured notes to C from CCC-. “The downgrade follows Seventy Seven Energy’s announcement that it has hired advisors to explore and identify capital structure opportunities, which we believe could include a debt restructuring or distressed exchange,” said Standard & Poor’s credit analyst Carin Dehne Kiley. Moody’s Downgrades

On January 22, 2016, Moody’s Investors Service downgraded Seventy Seven Energy Inc.’s corporate family rating to Caa3 from Caa1, its probability of default rating to Caa3-PD from Caa1-PD and its senior unsecured notes due 2022 to C from Caa3. “The downgrade reflects the difficulty SSE is likely to face generating sufficient cash flow to cover interest expense in 2016 and 2017, given its high leverage and bleak operating outlook,” said John Thieroff, Moody’s Vice President. “The company’s announcement that it has retained Lazard Freres & Co. LLC to assist in restructuring its debt is a further indication of the company’s untenable capital structure.” The following companies had their ratings affirmed:

Atlas Resource Partners, L.P. – Standard & Poor’s Ratings Services Corporate credit rating affirmed at B- Senior unsecured notes rating affirmed at CCC

Jack Cooper Holdings Corp. – Standard & Poor’s Ratings Services $165 million senior unsecured PIK toggle notes due 2019 affirmed at CCC-

PFS Holding Corporation – Standard & Poor’s Ratings Services Corporate credit rating affirmed at B- First-lien term loan rating affirmed at B- Second-lien term loan rating affirmed at CCC

The following companies had their ratings upgraded:

Headwaters Incorporated – Moody’s Investors Service Corporate family rating upgraded to B1 from B2 Probability of default rating upgraded to B1-PD from B2-PD Sr. Secured Term Loan B due 2022 upgraded to Ba3 from B1 Sr. Unsecured Notes due 2019 upgraded to B3 from Caa1

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 24

Distressed Company Alert Watch List The following companies had their ratings downgraded, but not quite low enough:

Archrock Partners, L.P. (Houston, TX) – Standard & Poor’s Ratings Services Corporate credit rating lowered to B from B+ Senior unsecured notes due 2021 & 2022 lowered to B- from B Senior secured revolving credit facility & term loan lowered to BB- from BB

Capstone Mining Corp. (Canada) – Standard & Poor’s Ratings Services Corporate credit rating lowered to B- from B+

Charlotte Russe Holding, Inc. (San Diego, CA) – Moody’s Investors Service Corporate family rating downgraded to B3 from B2 Probability of default rating downgraded to B3-PD from B2-PD $150 million Senior Secured Term Loan due 2019 downgraded to B3 from B2 $80 million Senior Secured Term Loan due 2019 downgraded to B3 from B2

China South City Holdings Limited (China) – Fitch Ratings Issuer Default Rating downgraded to B from B+ 13.50% senior unsecured bond due 2017 downgraded to B from B+ 8.25% senior unsecured bond due 2019 downgraded to B from B+

CSI Compressco LP (Midland, TX) – Standard & Poor’s Ratings Services Corporate credit rating lowered to B- from B Senior unsecured debt ratings lowered to B- from B

GK Holdings Inc. (Global Knowledge) (Cary, NC) – Standard & Poor’s Ratings Services Corporate credit rating lowered to B from B+ First-lien debt rating lowered to B from B+ Second-lien term loan rating lowered to B- from B

Hydoo International Holding Limited (China) – Fitch Ratings Issuer Default Rating downgraded to B- from B 13.75% senior unsecured bond due 2018 downgraded to B- from B

Koppers Inc. (Pittsburgh, PA) – Standard & Poor’s Ratings Services Corporate credit rating lowered to B from B+ Senior secured debt rating lowered to B+ from BB-

Laredo Petroleum, Inc. (Tulsa, OK) – Standard & Poor’s Ratings Services Corporate credit rating lowered to B from B+ Senior unsecured debt rating lowered to B- from B

Manitowoc Company, Inc., The* – Standard & Poor’s Ratings Services Corporate credit rating lowered to B+ from BB-

Performance Sports Group Ltd. (Exeter, NH) – Standard & Poor’s Ratings Services Corporate credit rating lowered to B- from B $450 million term loan due 2021 lowered to B- from B

Watch List continued on next page…

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 25

Distressed Company Alert Watch List, continued The following companies had their ratings downgraded, but not quite low enough, continued

Pesquera Exalmar S.A.A. (Peru) – Standard & Poor’s Ratings Services Corporate credit rating lowered to B from B+ $200 million senior unsecured notes due 2020 lowered to B from B+

Shiloh Industries, Inc. (Valley City, OH) – Standard & Poor’s Ratings Services Corporate credit rating lowered to B+ from BB-

SRAM LLC (Chicago, IL) – Moody’s Investors Service Corporate family rating downgraded to B2 from B1 Probability of default rating downgraded to B2-PD from B1-PD $715 Million First Lien Term Loan downgraded to B2 from B1 $40 Million First Lien Revolver downgraded to B2 from B1

The following (proposed) bonds were assigned below a “B” rating:

Vizient, Inc. (Irving, TX) – Standard & Poor’s Ratings Services $400 million unsecured notes due 2024 assigned a CCC+ rating

** Please note that we will not have profiles on the above companies until, or unless, they qualify for our criteria, which is defined on the last page of this issue. * Previously profiled in the DCA

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 26

Bankruptcies The data provided below offers a snapshot of Chapter 7 & Chapter 11 filings that have occurred since the prior reporting period for which the petitioning company has sales of at least $1 million. Additional information on companies that have filed for bankruptcy can be found at BankruptcyData.com.

Stelma Properties LLC, New Bern, NC | Bankruptcy Date: 1/22/2016 Callita Irrevocable Trust, Dana Point, CA | Bankruptcy Date: 1/25/2016 American Door Systems Inc, Orlando, FL | Bankruptcy Date: 1/25/2016 A D Die Cutting And Finishing Inc, Massapequa, NY | Bankruptcy Date: 1/27/2016 Sns Buddies Inc, Wilkes-Barre, PA | Bankruptcy Date: 1/28/2016 Comlink LLC, East Lansing, MI | Bankruptcy Date: 1/25/2016 Antero Energy Partners LLC, Dallas, TX | Bankruptcy Date: 1/25/2016 Nuo Therapeutics Inc, Gaithersburg, MD | Bankruptcy Date: 1/26/2016 Paonessa Alfombras Inc, San Juan, PR | Bankruptcy Date: 1/28/2016 D Wilson Electric Inc, Poughkeepsie, NY | Bankruptcy Date: 1/22/2016 Worldwide Transportation Services Inc, Miami, FL | Bankruptcy Date: 1/26/2016 5-7 Mulberry Street Associates LLC, Manchester, NH | Bankruptcy Date: 1/27/2016 Delta Ap LLC, East Hampton, NY | Bankruptcy Date: 1/27/2016

Liquid Holdings Group Inc, Hoboken, NJ | Bankruptcy Date: 1/27/2016 Atkinson Investment Holding Inc, Land O Lakes, FL | Bankruptcy Date: 1/28/2016 Shore Tractor Trailer Training Inc, Bayville, NJ | Bankruptcy Date: 1/28/2016 Greenbrier Whaley Group 2 LLC, Kodak, TN | Bankruptcy Date: 1/28/2016 Great Lakes Comnet Inc, East Lansing, MI | Bankruptcy Date: 1/25/2016 Yellow Cab Cooperative Inc, San Francisco, CA | Bankruptcy Date: 1/22/2016 Wealth Strategies Opportunity Fund LLC, Carson City, NV | Bankruptcy Date: 1/22/2016 5 Star Capital Fund LLC, Mishawaka, IN | Bankruptcy Date: 1/25/2016 Haynes Integrated Technologies LLC, Gulfport, MS | Bankruptcy Date: 1/25/2016 Gildrill Technologies LLC, Houston, TX | Bankruptcy Date: 1/25/2016 Performance Products Inc, San Antonio, TX | Bankruptcy Date: 1/26/2016 Verso Corporation, Memphis, TN | Bankruptcy Date: 1/26/2016

Bankruptcy information is provided by BankruptcyData.com’s Business Bankruptcy Filing Data Service. For information on how you can receive a daily file of business bankruptcies

e-mail [email protected].

the distressed company alert

a division of new generation research, inc.

Volume 14, No. 4 | January 29, 2016 Page | 27

Alert Categories The goal of the Distressed Company Alert newsletter is to alert subscribers of significant recent events reported by U.S. Public Companies indicating possible distress. The Categories Triggering an Alert: Default: A missed interest or principal payment on a debt obligation or the election of a company to not make a payment during or after the grace period. Covenant Violation: A violation of a covenant in an agreement or indenture governing a debt obligation. Audit Concern: A qualification as to the Company’s ability to continue as a going concern is reported by its independent accountants in an annual report. Low Rating: A major ratings agency has downgraded a Company’s publicly traded debt or any other rating to below a “B” rating, indicating vulnerability to default. Debt at Significant Discount: The Company’s public debt trades with a current yield or yield-to-maturity in excess of ten points over long-term Treasury bond rate. Distressed Debt Exchange: A debt exchange where the principal amount or interest rate is significantly reduced because the issuer is having difficulty meeting the original terms. Preferred Dividend Omission: The Company omits a dividend on its preferred stock. Miscellaneous The editors determine a recent event that represents distress or challenges the future prospects of the Company.

DISCLAIMER: Company Profiles in the Distressed Company Alert are selected by the editors because, in their

opinion, the occurrence of such an event or the existence of such a circumstance is a likely indicator of current

or prospective financial or operating difficulty. The inclusion of a profile suggests the possibility of financial

distress or the possibility that the Company may be of interest to workout professionals for some other reason.

Inclusions do not represent analysis of the condition of the Company or a definitive determination that the Company is in difficulty.

ACCURACY & COVERAGE: The information presented has been obtained from sources believed to be reliable, but accuracy cannot be guaranteed. Do not rely on the Distressed Company Alert without independent verification.

Distressed Company Alert is published weekly by New Generation Research, Inc., 1212 Hancock St., Suite LL-15, Quincy, MA 02169 Publisher: George Putnam, III; Editor: Kerry Mastroianni

Subscription Rate: $270.00 for six months or $500.00 per year. For more information, visit www.distressedcompanyalert.com. Other Publications from New Generation Research, Inc. include Bankruptcy Week--a weekly companion newsletter for BankruptcyData.com; The Bankruptcy Yearbook and Almanac--an annual compendium of bankruptcy information; The Turnaround Letter—a monthly investment newsletter. For more information on these publications, e-mail us at [email protected] or call us at (800) 468-3810.