d&o fiduciary duties in the zone of...

TRANSCRIPT

D&O Fiduciary Duties in the Zone of Insolvency Avoiding and Defending Fiduciary Duty Claims and Maximizing D&O Insurance Coverage

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

THURSDAY, OCTOBER 4, 2012

Presenting a live 90-minute webinar with interactive Q&A

Tony M. Davis, Partner, Baker Botts, Houston

Thomas C. Wolford, Partner, Neal Gerber Eisenberg, Chicago

Alexander D. Hardiman, Shareholder, Anderson Kill & Olick, New York

Sound Quality

If you are listening via your computer speakers, please note that the quality of

your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory and you are listening via your computer

speakers, you may listen via the phone: dial 1-888-450-9970 and enter your

PIN -when prompted. Otherwise, please send us a chat or e-mail

[email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

For CLE purposes, please let us know how many people are listening at your

location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of

attendees at your location

• Click the SEND button beside the box

FOR LIVE EVENT ONLY

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

© 2012

Director and Officer Duties from "Facing

Bankruptcy" to "Filing Bankruptcy"

Baker Botts L.L.P.

Tony M. Davis

(713) 229-1547

Ian Roberts

(214) 953-6719

6

Fiduciary Duties in General

Directors Owe Fiduciary Duties in Different Contexts

The Solvent Company

The Insolvent Company

The Insolvent Company in Bankruptcy

The Solvent Company in Bankruptcy

7

The Solvent Company

General Rules

Governed by state law

Some states allow certain duties to be limited in chartering documents See Del. Code Ann. tit 6, § 18-1101(c) (limited liability companies)

Directors of a solvent company owe fiduciary duties exclusively for the benefit

of company's residual risk bearers -- shareholders

Therefore, actions taken by directors are expected to benefit shareholders See Prod. Res. Group, LLC v. NCT Group, Inc., 863 A.2d 772, 787 (Del. Ch. 2004)

Typically no duties owed to creditors other than those granted in agreements

Courts believe creditors are capable of protecting themselves and are further

protected by fraudulent conveyance law and bankruptcy law Prod. Res. Group, LLC v. NCT Group, Inc., 863 A.2d 772, 787 (Del. Ch. 2004)

8

The Solvent Company (cont'd)

Business Judgment Rule

Courts will not second guess a business judgment so long as a minimum level of care

was exercised

Directors are presumed to have acted on an informed, independent, good faith

basis and with the honest belief that the action was in the best interest of company See, e.g., Solomon v. Armstrong, 747 A.2d 1098, 1111 (Del. Ch. 1999)

However, this presumption can be rebutted See, e.g., Angelo, Gordon & Co., L.P. v. Allied Riser Commc'n Corp., 805 A.2d 221, 229 (Del. Ch. 2002)

If a party demonstrates that there was neither a business decision, nor

disinterestedness and independence, nor due care, nor good faith was present, the

burden of proof shifts to the defendant to show the entire fairness of a transaction.

Mills Acquisition Co. v. Macmillan, Inc., 559 A.2d 1261, 1287 (Del.1989).

Policy underpinnings -- courts should not second guess a rational business decision,

even if decision proves to be unwise in hindsight

Duty of Loyalty Directors must hold the best interest of corporation above any personal interests

Directors must not self-deal, must not usurp corporate opportunities, must avoid

conflicts of interest, and at times must disclose

9

The Solvent Company (cont'd)

Duty of Care

Two components:

1. directors must act on an informed basis after due consideration; and

2. directors must act with due care in the discharge of their duties See Cede & Co. v. Technicolor, Inc., 634 A.2d 345, 367 (Del. 1993)

Stated differently, a director must exercise informed business judgment with due care

and in good faith

Directors can rely on corporate records as well as information, statements, and opinions of

officers, employees, and third-party professionals See Del. Code Ann. tit. 8, § 141(e)

General points of guidance:

Avoid haste

Prepare thoroughly

Engage competent advisors

Seek and assess relevant information from management

Beware of potential biases

Ask questions and remain actively involved

Keep a thorough written record

Understand the alternatives

10

The Insolvent Company

The Insolvency Threshold

Under Delaware law, insolvency occurs where:

1. liabilities exceed assets (i.e., balance sheet insolvency) or

2. there is an inability to pay debts as they mature in the ordinary course See, e.g., Prod. Res. Group, LLC v. NCT Group, Inc., 863 A.2d 772, 782 (Del. Ch. 2004)

Fiduciary Duties Upon Insolvency

Upon insolvency, directors owe fiduciary duties for the benefit of shareholders

and creditors

Creditors in effect become the senior residual risk bearers

Fiduciary duties are owed foremost to the entity itself, whether solvent or insolvent

Insolvency makes creditors the principal constituency that may be injured by fiduciary breaches

that diminish the value of the enterprise

"The transformation of a creditor into a residual owner does not change the nature of the harm

in a typical claim for breach of fiduciary duty by corporate directors” In re Adelphia Comm’ns Corp., 323 B.R. 345, 386 n.140 (Bankr. S.D.N.Y. 2005)

"duty to" vs. "duty for the benefit of" -- there is no shift

11

The Insolvent Company (cont'd)

Scope of Duties Owed

The fundamentals still apply -- directors must exercise informed business

judgment in good faith in the best interest of enterprise

During insolvency the exercise of that judgment must include a consideration

of the interest of creditors

How does a particular course of action distribute risk and reward between

creditors and equity?

As the corporation's continued existence appears unlikely, acting in the best

interest of corporation may require a course of action that benefits creditors

more than equity

However, just because a course of action benefits one constituency more than

another does not mean it is violative of a fiduciary duty

12

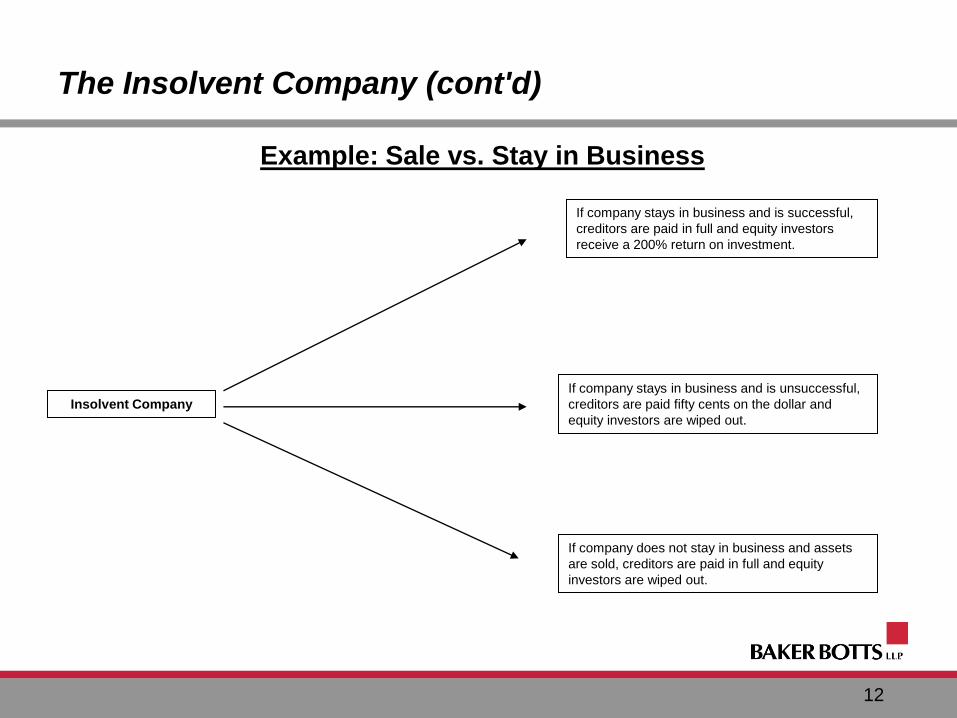

The Insolvent Company (cont'd)

Example: Sale vs. Stay in Business

Insolvent Company

If company stays in business and is successful,

creditors are paid in full and equity investors

receive a 200% return on investment.

If company stays in business and is unsuccessful,

creditors are paid fifty cents on the dollar and

equity investors are wiped out.

If company does not stay in business and assets

are sold, creditors are paid in full and equity

investors are wiped out.

13

The Zone of Insolvency

"Zone of Insolvency"

Uncertainty as to whether creditors have enhanced rights before

the point of insolvency

Credit Lyonnais suggested that the expansion of duties to creditors can

occur in the "vicinity of insolvency," which was unsettling and controversial Credit Lyonnais Bank Nederland, N.V. v. Pathe Commc'ns Corp., 1991 WL 277613, *34 (Del. Ch. Dec. 30, 1991)

Vicinity standard is inherently vague

14

The Zone of Insolvency (cont'd)

Doubts About the "Zone"

Delaware Supreme Court decision in Gheewalla suggests that the court may

ultimately establish a bright line (e.g., insolvency) N. Am. Catholic Educ. Programming Found., Inc. v. Gheewalla, 930 A.2d 92 (Del. Ch. 2006)

However, commentators and courts have disagreed over whether duties

expand for the benefit of creditors prior to insolvency

A recent Fifth Circuit decision, which applied Delaware law, may suggest that

the "zone" remains a viable theory Torch Liquidating Trust v. Stockstill, 561 F.3d 377, 385-86 (5th Cir. 2009)

Southern District of New York has rejected “zone of insolvency” theory under

NY Law:

“creating a pre-insolvency duty of care to creditors would distort—and potentially

conflict with—the incentive structure for corporate managers that the law of

fiduciary duties has been erected to create” RSL Comm’ns PLC v. Bildrici, 649 F.Supp.2d 184, 206 (S.D.N.Y. 2009)

15

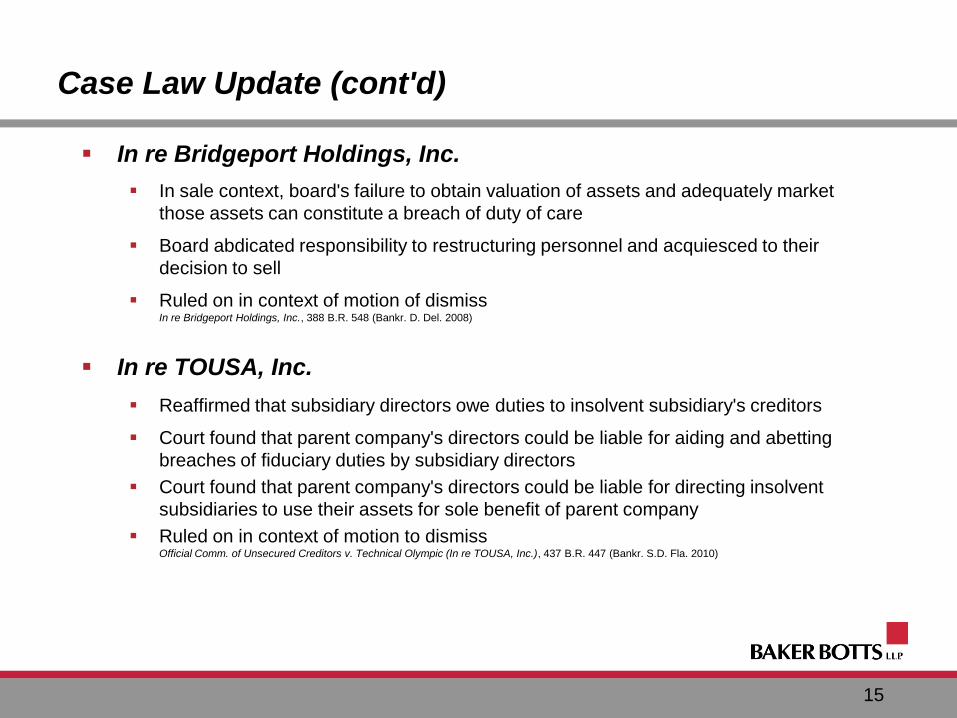

Case Law Update (cont'd)

In re Bridgeport Holdings, Inc.

In sale context, board's failure to obtain valuation of assets and adequately market

those assets can constitute a breach of duty of care

Board abdicated responsibility to restructuring personnel and acquiesced to their

decision to sell

Ruled on in context of motion of dismiss In re Bridgeport Holdings, Inc., 388 B.R. 548 (Bankr. D. Del. 2008)

In re TOUSA, Inc.

Reaffirmed that subsidiary directors owe duties to insolvent subsidiary's creditors

Court found that parent company's directors could be liable for aiding and abetting

breaches of fiduciary duties by subsidiary directors

Court found that parent company's directors could be liable for directing insolvent

subsidiaries to use their assets for sole benefit of parent company

Ruled on in context of motion to dismiss Official Comm. of Unsecured Creditors v. Technical Olympic (In re TOUSA, Inc.), 437 B.R. 447 (Bankr. S.D. Fla. 2010)

16

Case Law Update (cont'd)

Auriga Capital Corp. v. Gatz Prop., LLC Delaware Chancery Court holds that, unless eliminated or limited, the LLC agreement default

principle is that the manager owes fiduciary duties of loyalty and care to the LLC and its

members, including its minority members. Auriga Capital Corp. v. Gatz Prop., LLC, 40 A.3d 839 (Del. Ch. Ct. 2012)

CML V LLC v. Bax Delaware Supreme Court recently held that the Delaware LLC Act denies derivative standing

to creditors of an insolvent limited liability company CML V, LLC v. Bax, --- A.3d ----, 2011 WL 3863132 (Del. Sept. 02, 2011)

Sanford v. Waugh & Co., Inc. Individual creditors of insolvent corporation have no right to assert direct claims for breach of

fiduciary duty against corporation's officers and directors

Individual creditors of insolvent corporation can initiate a derivative claim on behalf of all

creditors for breach of fiduciary duties Sanford v. Waugh & Co., Inc., 2010 WL 5139496, *4-8 (Tenn. Dec. 17, 2010)

17

The Insolvent Company in Bankruptcy

Duties Owed to Estate

Directors of a chapter 11 debtor owe fiduciary obligations to bankruptcy estate for benefit

of all constituencies, as their interests may appear from time to time See Commodity Futures Trading Comm'n v. Weintraub, 471 U.S. 343, 355 (1985)

Balancing duties

Interests of estate's constituencies are often conflicting and adversarial

A debtor simply cannot serve all interests all of the time

Satisfying Duties

Preserve and maximize value of debtor's assets

Exercise due care in making business decisions

When conflicts arise, negotiate honestly and in good faith in support of position

determined to be in estate's best interest

Inherent conflict among constituencies can exist because of judicial supervision and the

rights of parties in interest in the bankruptcy process

18

The Insolvent Company in Bankruptcy (cont'd)

Interaction Between State-law and Bankruptcy-based Duties

Although state law fiduciary duties continue to apply in bankruptcy, the Bankruptcy

Code preempts and supplements them to some extent

Section 541 impacts who has standing to assert claims for breach

Transactions outside ordinary course are governed by section 363

Incurring debt is governed by section 364

Creditor and equity committee structure under sections 1102 and 1103

Creditors and equity given right to vote on reorganization plans under sections 1124 and 1126

Trustee or examiner can be appointed under section 1104 See Nat'l Convenience Stores Inc. v. Shields (In re Schepps Food Stores, Inc.), 160 B.R. 792 (Bankr. S.D. Tex. 1993)

Preemption especially applicable where state law actions or claims would delay or

frustrate reorganization policy of Bankruptcy Code

However, fiduciary duty action that does not impede bankruptcy proceedings may be allowed

(i.e., action seeking to compel annual meeting for election of directors) See Lionel Corp. v. Comm. of Equity Security Holders (In re Lionel Corp.), 30 B.R. 327 (Bankr. S.D.N.Y. 1983)

19

The Insolvent Company in Bankruptcy (cont'd)

Example: The Conflicted Director

What if a director owns substantial equity in debtor and board is faced with restructuring

transaction that pits interests of equity against interests of estate as a whole?

Duty of loyalty is implicated -- director should abstain and allow decision to be

deliberated upon and made by independent directors

As plan proponent, debtor may elevate its interests above those of

a particular constituency

Example: cram down

So long as debtor and its management avoid self-dealing and seek to act in estate's

best interest, they may pursue a course of action that disfavors a particular constituency

Fiduciary duties of a chapter 11 debtor may arise in connection with the exercise of

business judgment in a transaction outside ordinary course See, e.g., In re Chrysler LLC, 405 B.R. 84, 105 (Bankr. S.D.N.Y. 2009)

20

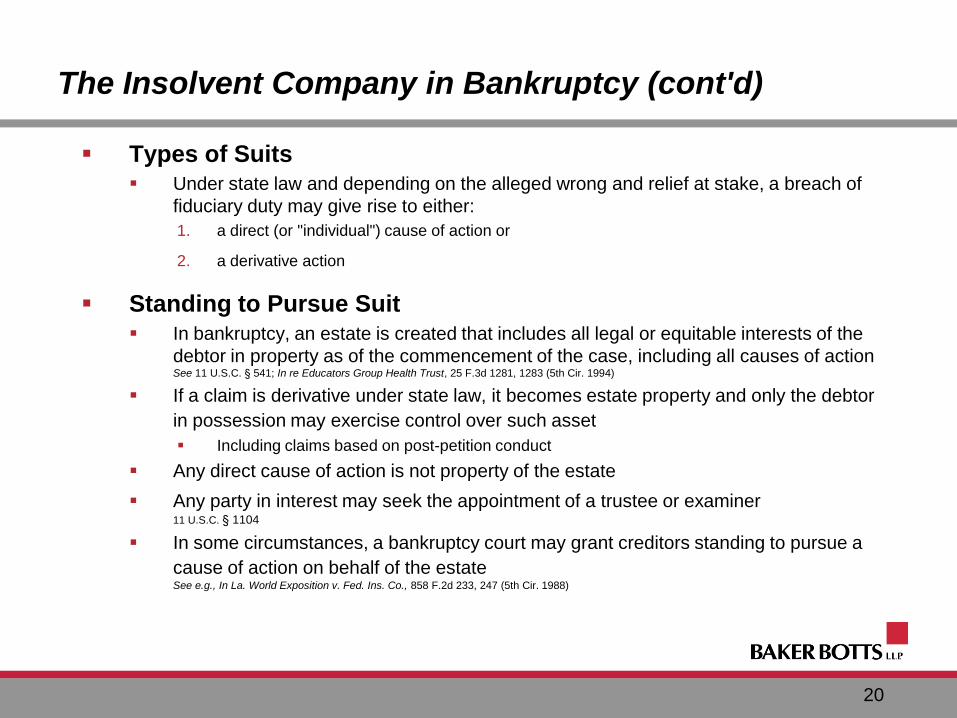

The Insolvent Company in Bankruptcy (cont'd)

Types of Suits Under state law and depending on the alleged wrong and relief at stake, a breach of

fiduciary duty may give rise to either:

1. a direct (or "individual") cause of action or

2. a derivative action

Standing to Pursue Suit

In bankruptcy, an estate is created that includes all legal or equitable interests of the

debtor in property as of the commencement of the case, including all causes of action See 11 U.S.C. § 541; In re Educators Group Health Trust, 25 F.3d 1281, 1283 (5th Cir. 1994)

If a claim is derivative under state law, it becomes estate property and only the debtor

in possession may exercise control over such asset Including claims based on post-petition conduct

Any direct cause of action is not property of the estate

Any party in interest may seek the appointment of a trustee or examiner 11 U.S.C. § 1104

In some circumstances, a bankruptcy court may grant creditors standing to pursue a

cause of action on behalf of the estate See e.g., In La. World Exposition v. Fed. Ins. Co., 858 F.2d 233, 247 (5th Cir. 1988)

21

The Solvent Company in Bankruptcy

Can a chapter 11 debtor be solvent?

Debtor may be balance sheet solvent, which would implicate interests of equity

Impact of Solvency

Directors' duties continue to be amorphous

Whereas outside of bankruptcy duties benefit only shareholders, in bankruptcy duties are

owed to estate as a whole

Each constituency has standing to weigh in and protect its interest

Exclusivity and Plan Proposal

Debtor's exclusive period to file a plan 11 U.S.C. § 1121(b)

Debtor's ability to cram down is inconsistent with the duty of loyalty to dissenting class, but

consistent with its duties to the estate 11 U.S.C. § 1129(b)

Bankruptcy Code does not distinguish debtors on the basis of solvency for purposes of

plan proposal and confirmation, as it does in other contexts

Exclusivity is balanced with protections for creditors and equity, such as the right to vote

and the requirements of cram down

The contents of these slides should not be construed as legal advice or a legal opinion on any specific fact or circumstance. The slides are intended for general purposes only,

and you are urged to consult a lawyer concerning your own situation and any specific legal questions you may have. © Neal, Gerber & Eisenberg LLP 2012

D&O Fiduciary Duties

When a Company Faces Insolvency:

Strategies to Avoid and Defend

Breach of Fiduciary Duty Lawsuits

Thomas C. Wolford Partner Neal, Gerber & Eisenberg LLP (312) 269-8000 www.ngelaw.com

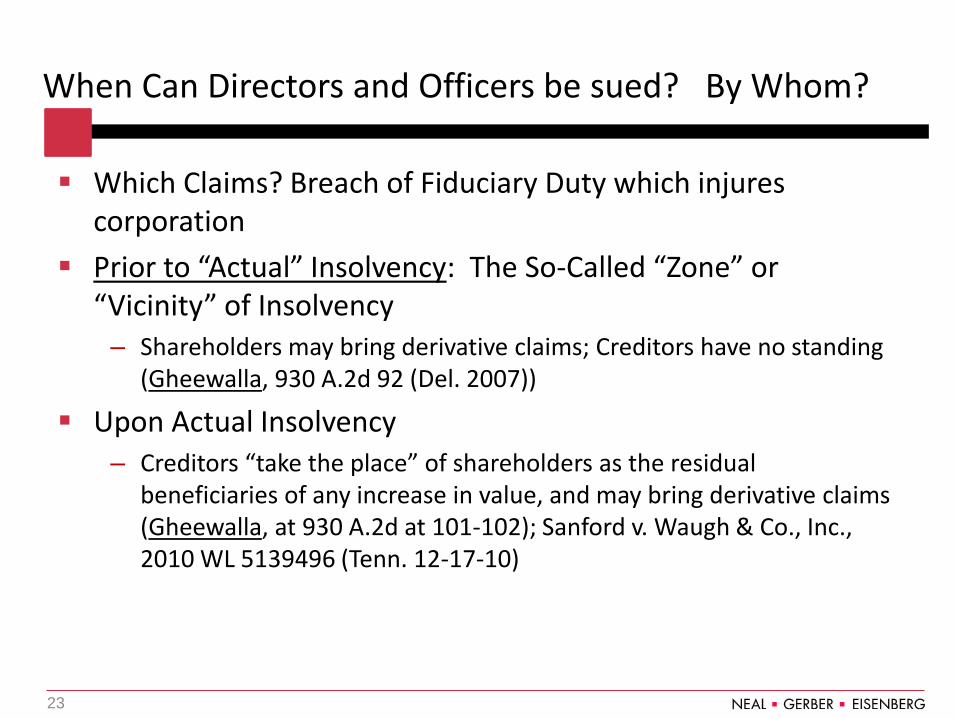

When Can Directors and Officers be sued? By Whom?

Which Claims? Breach of Fiduciary Duty which injures corporation

Prior to “Actual” Insolvency: The So-Called “Zone” or “Vicinity” of Insolvency

– Shareholders may bring derivative claims; Creditors have no standing (Gheewalla, 930 A.2d 92 (Del. 2007))

Upon Actual Insolvency – Creditors “take the place” of shareholders as the residual

beneficiaries of any increase in value, and may bring derivative claims (Gheewalla, at 930 A.2d at 101-102); Sanford v. Waugh & Co., Inc., 2010 WL 5139496 (Tenn. 12-17-10)

23

When can Directors and Officers be sued? By Whom? – cont.

Who can be sued? Both directors and officers

Gantler v. Stephens, 965 A.2d 695 (Del. 2009) (“In the past, we have implied that officers of Delaware corporations, like directors, owe fiduciary duties of care and loyalty, and that the fiduciary duties of officers are the same as those of directors. We now explicitly so hold”)

24

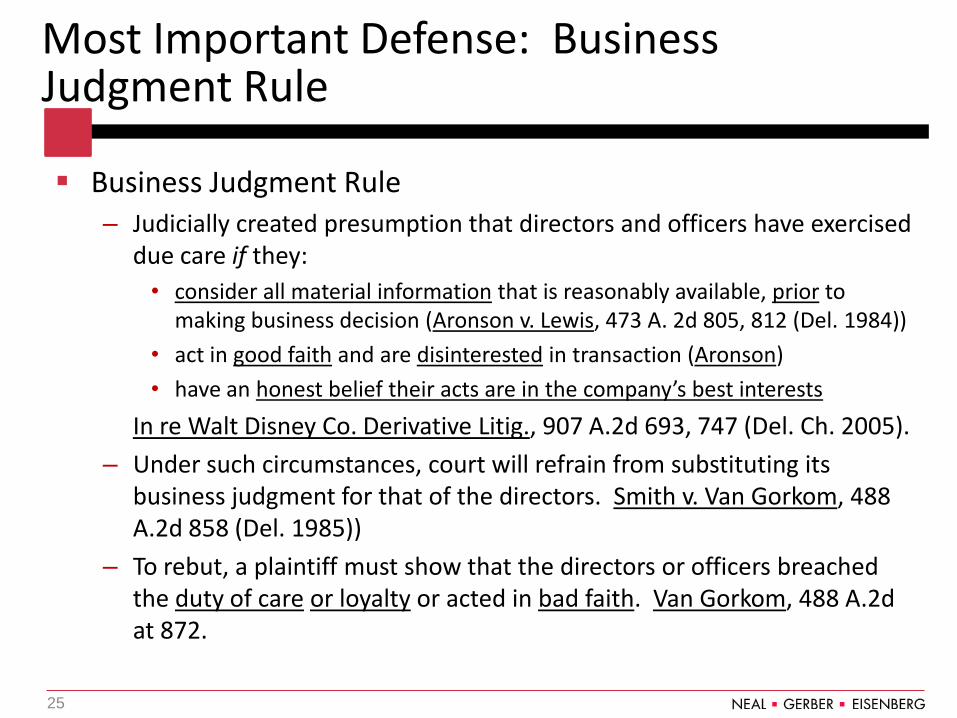

Most Important Defense: Business Judgment Rule

Business Judgment Rule – Judicially created presumption that directors and officers have exercised

due care if they:

• consider all material information that is reasonably available, prior to making business decision (Aronson v. Lewis, 473 A. 2d 805, 812 (Del. 1984))

• act in good faith and are disinterested in transaction (Aronson)

• have an honest belief their acts are in the company’s best interests

In re Walt Disney Co. Derivative Litig., 907 A.2d 693, 747 (Del. Ch. 2005).

– Under such circumstances, court will refrain from substituting its business judgment for that of the directors. Smith v. Van Gorkom, 488 A.2d 858 (Del. 1985))

– To rebut, a plaintiff must show that the directors or officers breached the duty of care or loyalty or acted in bad faith. Van Gorkom, 488 A.2d at 872.

25

Most Important Defense: Business Judgment Rule – cont.

When Business Judgment Rule Unavailable: Entire or “Intrinsic” Fairness Test – Failure to qualify for the business judgment presumption will expose

management to a much less attractive standard, the "intrinsic fairness" or "entire fairness" standard

– Using this standard, the interested director must prove the "entire fairness" of the transaction. Orman v. Cullman, 794 A.2d 5, 23-24 (Del. Ch. 2002)

– Fairness has two components: fair dealing and fair price, each of which will be subject to substantial debate in any given situation. Boyer v. Wilmington Materials, Inc., 754 A.2d 881, 898-99 (Del. Ch. 1999)

26

– Fair dealing implicates the timing, initiation, structure, negotiation, disclosure and approval of the transaction. See Boyer, 754 A.2d at 898.

– Fair price relates to economic and financial considerations of proposed transaction

– Relevant factors include assets involved, market value, earnings, future prospects and other elements that affect intrinsic or inherent value of company's stock

– Subjective good faith will not protect director who engaged in self-dealing or usurpation of corporate opportunity

– A transaction must be objectively fair to satisfy duty of loyalty. See, e.g., Mills Acquisition Co. v. MacMillan, Inc., 559 A.2d 1261, 1280 (Del. 1989)

See Discussion in Report of Examiner, March 9, 2012, In re Dynegy Holdings, LLC, et al., Case No. 11-38111 (CGM) (Bankr. S.D.N.Y.)

Most Important Defense: Business Judgment Rule – cont.

27

Board should be vigilant to detect signals of financial distress, so that directors and officers may take appropriate action as soon as possible – Recurring Losses – Industry Downturn – Significant competitor actions – Technological advances affecting the corporation’s business model or

obsolescence of assets – Strategies that may result in financial distress, such as emphasis on cash

flow to exclusion of profits (or vice versa) – Required amendment of credit terms – Irregular accounting techniques – Covenant Defaults – Insufficient Availability Under Current Revolving Credit Facilities

Strategies to Avoid and Defend

28

To the extent possible, preserve presumption of the business judgment rule

– Avoid transactions involving self-interest – Assess available alternatives; gather available information and educate

yourself; – Fully participate and avoid rash decisions; devote reasonable time to

process – Utilize outside, disinterested professionals – But do Not abdicate decision-making authority to advisors; continue to

supervise them (See Bridgeport Holdings) – Disclose conflicts and recuse yourself (or resign), if necessary – Explore other potential risks

Assume all actions will be analyzed with benefit of hindsight after projected success did not occur

Strategies to Avoid and Defend – cont.

29

Document Your Efforts – Observe corporate formalities

– Address significant matters at a meeting rather than by written consent

– Document board and committee actions in appropriately detailed minutes, which acknowledge the duties during financial distress

– Record a summary of data sought and received

– Record alternatives considered; thoroughly discuss major decisions

– Pursue multiple offers in connection with potential transactions and document efforts

– Exercise diligence – follow up in writing – until satisfactory answers are provided

Strategies to Avoid and Defend – cont.

30

Document Your Efforts – cont. – Obtain independent professional and expert advice prior to making

decisions

• retain advisors have both skills and knowledge necessary to complete assignment successfully

• where appropriate, obtain fairness opinions and/or solvency opinions

• Note: Hiring such advisors and considering a few different options alone

likely will not suffice (See In re Lemington Home for the Aged,

2011 WL 4375676 (3rd Cir. 9/21/11).

Strategies to Avoid and Defend – cont.

31

Consider Interests of All Constituents – Shareholders, Creditors and Value of Enterprise – Assume that company is insolvent

– Listen to the concerns of creditors if insolvency likely

– Treat like creditors alike whenever possible, and do not prefer insiders

Strategies to Avoid and Defend – cont.

32

Typical Scrutinized Transactions – Approving any new business plan

– Refusing to reduce overhead expenses in anticipation of receiving a new round of investment that may or may not materialize

– Approving any sale of a major asset

– Taking on additional debt to finance an acquisition or to otherwise expand operations

– Approving any spin-off

– Collateralizing previously unencumbered assets, especially in an effort to raise cash to meet operational needs in the face of losses

– Approving compensation package for senior executives, including severance payments and other benefits

Strategies to Avoid and Defend – cont.

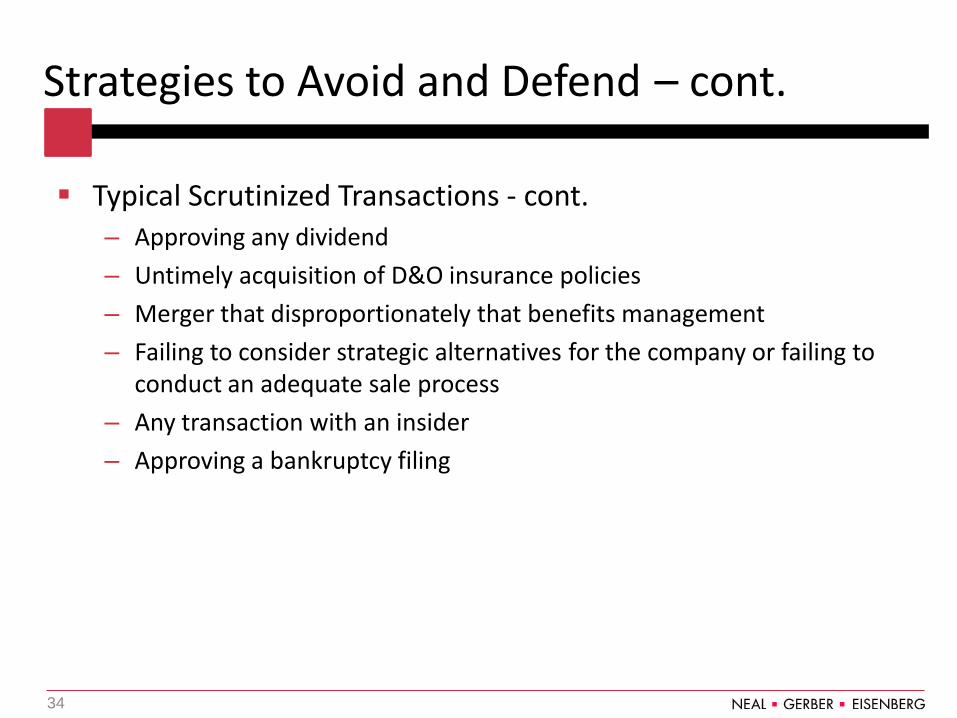

33

Typical Scrutinized Transactions - cont. – Approving any dividend

– Untimely acquisition of D&O insurance policies

– Merger that disproportionately that benefits management

– Failing to consider strategic alternatives for the company or failing to conduct an adequate sale process

– Any transaction with an insider

– Approving a bankruptcy filing

Strategies to Avoid and Defend – cont.

34

Pay particularly close attention to transactions with management and other insiders (and avoid if possible) – Obtain approval by independent directors (See CDX Liquidating

Trust v. Venrock Associates, 640 F. 3d 209 (7th Cir. 2011))

– Obtain advice from independent advisors

– See that any such transaction is fair to the company

Obtain Exculpation and Indemnification

Strategies to Avoid and Defend – cont.

35

Elimination or Limitation of Liability

– Delaware GCL §102(b)(7)

– Certificate of Incorporation may contain a provision limiting or eliminating personal liability of corporate directors for monetary damages for breach of fiduciary duty, but:

• Not for breach of the duty of loyalty ((b)(7)(i))

• Not for acts or omissions not in good faith, involving intentional misconduct, or a knowing violation of law ((b)(7)(ii)) (includes fraud-Zirn v. VLI Corp., 621 A.2d 773 (Del.1993)

• Not for willful or negligent conduct in paying dividends or repurchasing stock ((b)(7)(iii))

• Not for any transaction from which director derived improper personal benefit ((b)(7)(iv))

Exculpation

36

Elimination or Limitation of Liability – cont. – Section 102(b)(7) does not eliminate duty of care, because

injunctive relief still available (Walt Disney Co. Derivative Litigation, 2005 Del. Ch. LEXIS 113)

– Applies only to directors, not officers (McPadden v. Sihu, 2008 Del. Ch. LEXIS 123)

– no retroactive insulation from liability

– Affirmative defense –See Ad Hoc Comm. v. Wolford, 554 F. Supp.2d 538 (D. Del. 2008) (probably will not result in dismissal)

– Contrast Michigan Business Corporation Law, § 450. 1209 – based

on Model Business Corporation Act (narrower exceptions)

Exculpation

37

Indemnification and advancement of expenses

– Delaware GCL §145 • Mandatory indemnification if director or officer is successful (including

partial) (§145(c))

• Third party suits - permitted indemnification if: – acted in good faith;

– reasonably believed to be in best interests of the corporation; and

– no reasonable cause to believe conduct unlawful. (145(a))

• Suits by corporation and derivative suits – indemnification permitted for expenses if director or officer met above standards of conduct; but no indemnification for judgments or settlements or expenses if found liable to the corporation, unless court determines otherwise (§145(b))

• Permitted to advance expenses to current director or officer who provides undertaking to repay if necessary

Indemnification

38

Right to indemnification can not be retroactively eliminated or impaired, unless the relevant indemnification provision provided for it at time of alleged act or omission

Some advantages to contractual indemnity (instead of in certificate of incorporation), but also vulnerable to rejection in bankruptcy

Indemnification Claims can be useful “chip” in negotiations to settle breach of fiduciary duty claims

Indemnification – cont.

39

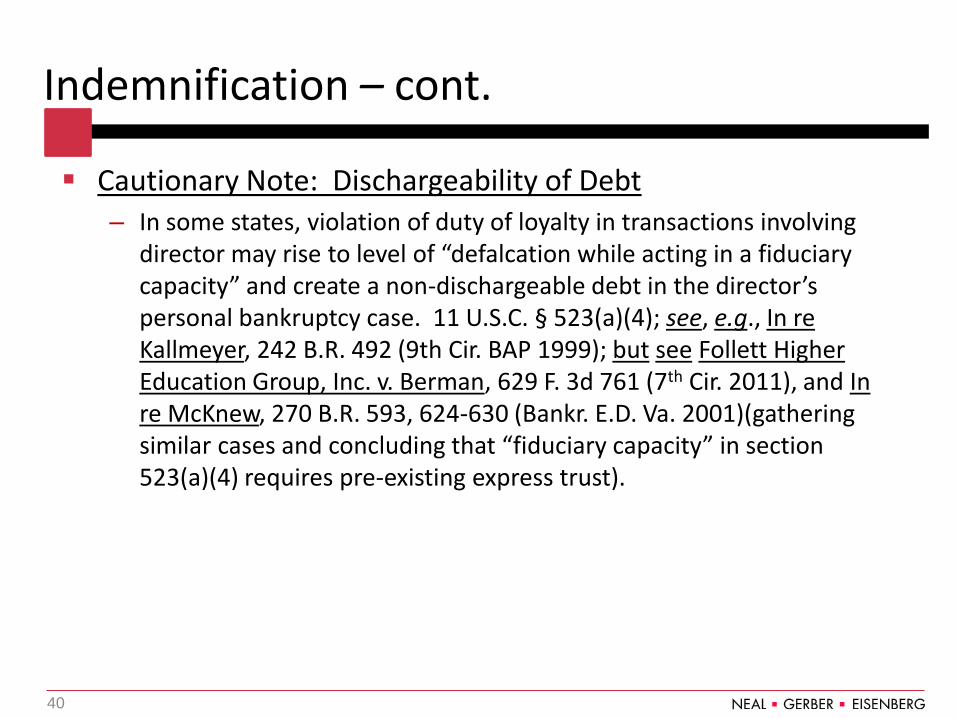

Cautionary Note: Dischargeability of Debt – In some states, violation of duty of loyalty in transactions involving

director may rise to level of “defalcation while acting in a fiduciary capacity” and create a non-dischargeable debt in the director’s personal bankruptcy case. 11 U.S.C. § 523(a)(4); see, e.g., In re Kallmeyer, 242 B.R. 492 (9th Cir. BAP 1999); but see Follett Higher Education Group, Inc. v. Berman, 629 F. 3d 761 (7th Cir. 2011), and In re McKnew, 270 B.R. 593, 624-630 (Bankr. E.D. Va. 2001)(gathering similar cases and concluding that “fiduciary capacity” in section 523(a)(4) requires pre-existing express trust).

Indemnification – cont.

40

Related Strategy to Avoid D&O Litigation: Become a Delaware LLC

Insulation from Exposure to Both LLC Members and Creditors – Members: 6 Del. C. §18-1101(c) permits LLC agreement to restrict or

eliminate any duty (including fiduciary duties) to the LLC or its members or managers, other than implied contractual covenant of good faith and fair dealing.

– Related Westpac LLC et al. v. JER Snowmass LLC et al., 2010 WL 2929708 (Del. Ch. 2010) Defendant member negotiated for consent right with respect to major decisions, which it could withhold to protect its own commercial interests. Held: When a “fiduciary duty’s claim is plainly inconsistent with the contractual bargain struck by the parties to an LLC or alternative entity agreement, the fiduciary duty claim must fall.”

– CML V, LLC v. Bax, et al., 6 A. 3d 238 (Del. Ch. 2010); aff’d 2011 WL 3863132 (Del.). Section 18-1002 of Delaware LLC Act governs standing for derivative actions, and does not grant it to creditors.

41

Insurance

Obtain Appropriate D&O Insurance

42

43 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

D&O INSURANCE ISSUES IN THE

CONTEXT OF BANKRUPTCY:

Strategies and Pitfalls on the Road

to Maximizing Coverage

Strafford Publications Teleconference

October 4, 2012

Alexander D. Hardiman, Esq.

(212) 278-1588

44 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

OVERVIEW

• Who does D&O Coverage Belong to?

– Debtor Entity

– D&Os

– Both

• Accessing Coverage and the

Bankruptcy Stay

– Section 302(c) Stay and Policy Proceeds

• Key D&O Policy Provisions to Maximize

Coverage

45 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

D&O Insurance is the Last Line of

Defense

Statutory Protection

Corporate By-laws

Corporate Indemnification

Agreements

Traditional D&O Insurance

First line of defense

Last line of defense

46 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

ABCs of D&O Coverage • Side “A”

– Direct coverage for D&Os to the extent that the

entity is not permitted to indemnify or cannot

indemnify due to insolvency

• Side “B” – Coverage for the entity for reimbursement of

amounts paid to indemnify D&Os

• Side “C” – Direct coverage for the entity, but for public

companies generally limited to securities claims

47 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Purpose of D&O Insurance

“D & O policies are obtained for the protection of

individual directors and officers . . . Unlike an

ordinary liability insurance policy, in which a

corporate purchaser obtains primary protection

from lawsuits, a corporation does not enjoy direct

coverage under a D & O policy. It is insured

indirectly for its indemnification obligations. In

essence and at its core, a D & O policy remains a

safeguard of officer and director interests and not a

vehicle for corporate protection.”

In re First Cent. Fin. Corp., 238 B.R. 9, 16 (Bankr. E.D.N.Y. 1999)

48 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Where’s My D&O Policy!?

• D&O policies generally considered

property of the bankruptcy estate – Minoco Group of Cos., Ltd. v. First State Underwriters

Agency of New England Reinsurance Corp., 799 F.2d 517,

519 (9th Cir.1986) (declaring a D & O policy property of the

estate thereby disallowing insurance company's attempt to

cancel the policy)

– In re Allied Digital Technologies Corp., 306 B.R. 505, 509

(Bankr.D.Del.2004) (“In fact an overwhelming majority of

courts have concluded that liability insurance policies fall

within § 541(a)(1)'s definition of estate property.”)

49 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

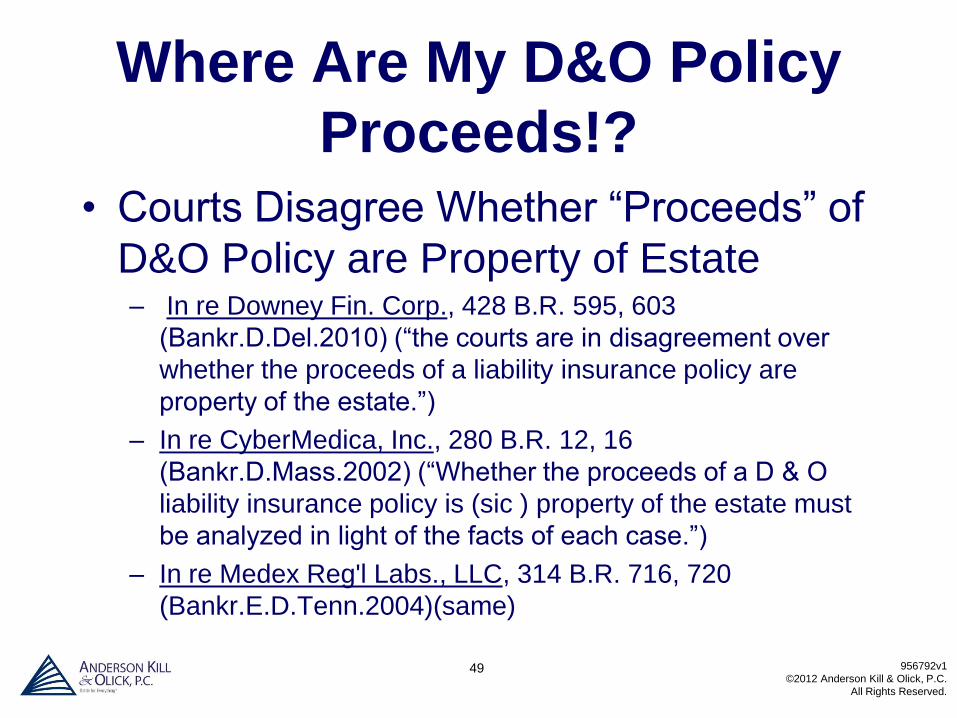

Where Are My D&O Policy

Proceeds!?

• Courts Disagree Whether “Proceeds” of

D&O Policy are Property of Estate – In re Downey Fin. Corp., 428 B.R. 595, 603

(Bankr.D.Del.2010) (“the courts are in disagreement over

whether the proceeds of a liability insurance policy are

property of the estate.”)

– In re CyberMedica, Inc., 280 B.R. 12, 16

(Bankr.D.Mass.2002) (“Whether the proceeds of a D & O

liability insurance policy is (sic ) property of the estate must

be analyzed in light of the facts of each case.”)

– In re Medex Reg'l Labs., LLC, 314 B.R. 716, 720

(Bankr.E.D.Tenn.2004)(same)

50 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Where Are My D&O Policy

Proceeds!?

• “Proceeds” Analysis Factors:

– Does debtor entity have a “direct interest”

in proceeds?

– Have the D&Os made claims for

indemnification against the debtor entity?

– Does the D&O Policy provide Side “C”

entity coverage

51 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Where Are My D&O Policy

Proceeds!?

• Proceeds Not Property of Estate

Despite Side “B” coverage: – La. World Exposition, Inc. v. Fed. Ins. Co., (In re La. World

Exposition, Inc.), 832 F.2d 1391, 1399 (5th Cir.1987)

(holding that the debtor has no ownership interest in

proceeds of an insurance policy where the obligation of the

insurance company is only to the directors and officers)

– In re Daisy Sys. Sec. Litig., 132 B.R. 752, 755

(N.D.Cal.1991) (finding that when a D & O insurance policy

only provides direct coverage to the directors and officers

the proceeds are not property of the estate).

52 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Where Are My D&O Policy

Proceeds!?

• Proceeds May Be Property of Estate

Because of Side “B” Coverage: – In re Leslie Fay Cos., Inc., 207 B.R. 764, 785

(Bankr. S.D.N.Y. 1997) (“Here, the debtors have

an interest in those proceeds because of the

possibility that the class action might deplete the

policy and theoretically force claims for

indemnification to fall upon the estate.”).

– In re Circle K Corp., 121 B.R. 257 (Bankr. D. Ariz.

1990).

53 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Where Are My D&O Policy

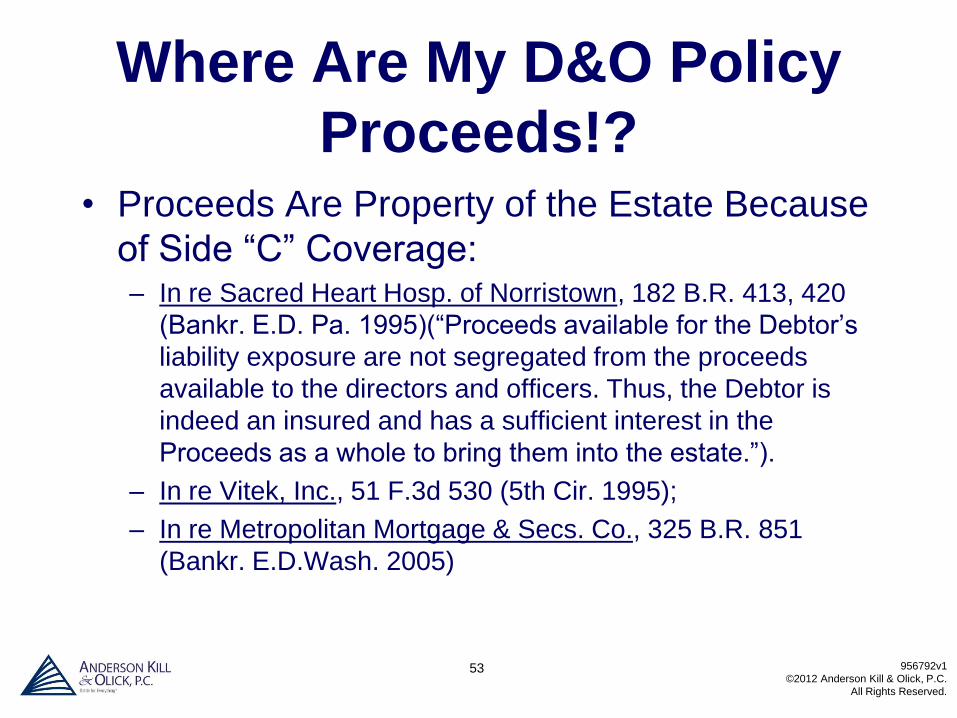

Proceeds!? • Proceeds Are Property of the Estate Because

of Side “C” Coverage: – In re Sacred Heart Hosp. of Norristown, 182 B.R. 413, 420

(Bankr. E.D. Pa. 1995)(“Proceeds available for the Debtor’s

liability exposure are not segregated from the proceeds

available to the directors and officers. Thus, the Debtor is

indeed an insured and has a sufficient interest in the

Proceeds as a whole to bring them into the estate.”).

– In re Vitek, Inc., 51 F.3d 530 (5th Cir. 1995);

– In re Metropolitan Mortgage & Secs. Co., 325 B.R. 851

(Bankr. E.D.Wash. 2005)

54 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Where Are My D&O Policy

Proceeds!?

• Proceeds Not Property of the Estate

Despite Side “C” Coverage:

– In re First Cent. Fin. Corp., 238 B.R. 9

(Bankr. E.D.N.Y. 1999).

– Maxwell v. Megliola (In re MarchFirst, Inc.),

288 B.R. 526 (Bankr. N.D. Ill. 2002).

55 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Two “Proceeds” Case

Studies

• In re Downey Fin. Corp., 428 B.R. 595

(Bankr. D. Del. 2010)

• In re MF Global Holdings Ltd., 469 B.R.

177 (Bankr. S.D.N.Y. 2012)

56 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Maximizing D&O Protection

• Priority of Payments Provision

• Non-Rescindable Side “A” Coverage &

Severability

• Presumptive Indemnification Clauses

• Insured v. Insured Exclusion

• Change in Control Provisions & Tail

Coverage

• Side “A” Only Policies

• Excess Coverage & Exhaustion

57 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Maximizing D&O Protection

• Priority of Payments Provision

– Side “A” payments have priority over Side

“B” or Side “C” payments

– Assists or may be determinative in

overcoming policy “proceeds” issue

– Limits uncertainty over D&O defense cost

funding

58 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

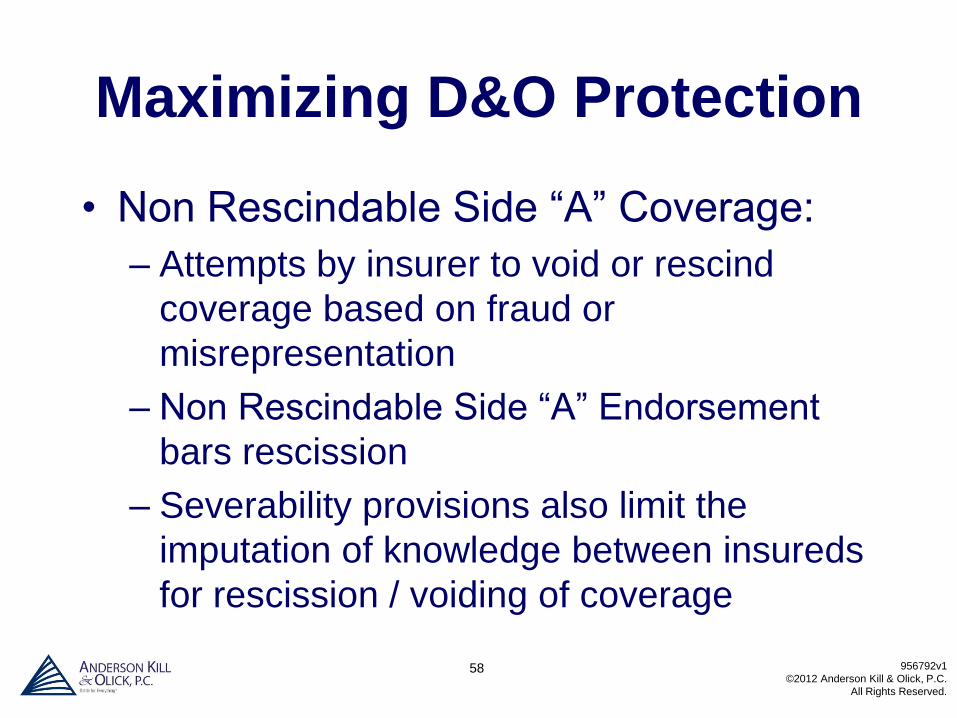

Maximizing D&O Protection

• Non Rescindable Side “A” Coverage:

– Attempts by insurer to void or rescind

coverage based on fraud or

misrepresentation

– Non Rescindable Side “A” Endorsement

bars rescission

– Severability provisions also limit the

imputation of knowledge between insureds

for rescission / voiding of coverage

59 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Maximizing D&O Protection

• Presumptive Indemnification Clauses :

– Indemnification of D&O by entity is

“presumed” (i.e. if entity is required or

permitted to indemnify) then retention

applicable to Side “B” applies

– Include provision stating that presumptive

indemnification is inapplicable in the event

of “financial insolvency or “financial

impairment”

60 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Maximizing D&O Protection

• Insured v. Insured Exclusion (I. v. I)

– Excludes coverage for claims of entity

against D&Os and vice-versa

– Most I v. I exclusions contain carve out for

bankruptcy related claims but often

concern coverage for claims by receiver,

liquidator, chap 7 trustee

– Ensure that carve-out is provided claims by

DIPs, chap 11 trustee, creditors etc.

61 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

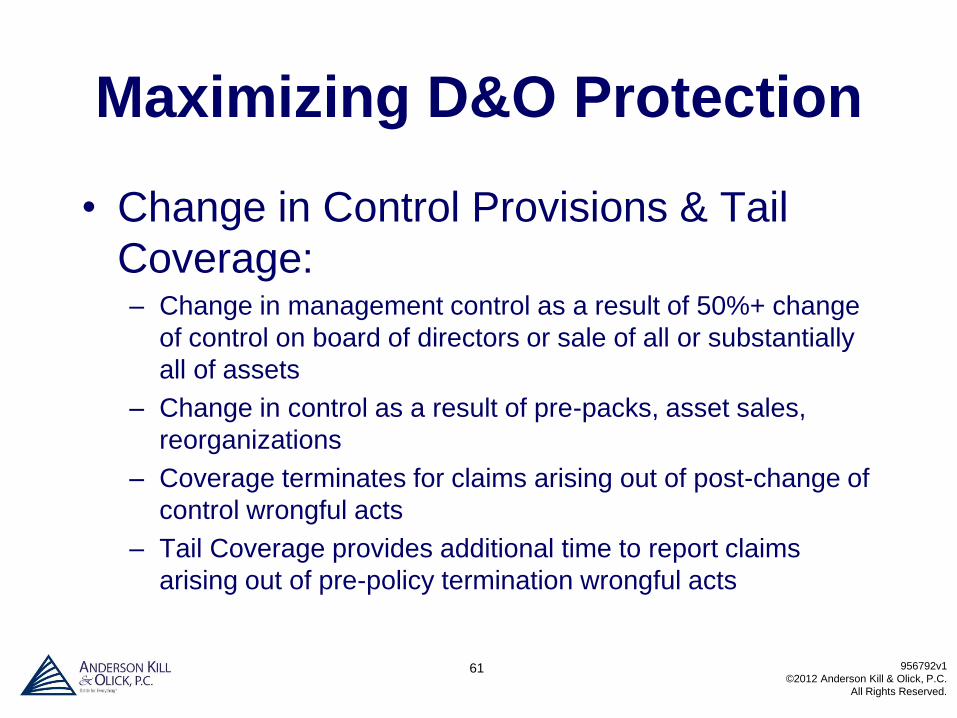

Maximizing D&O Protection

• Change in Control Provisions & Tail

Coverage: – Change in management control as a result of 50%+ change

of control on board of directors or sale of all or substantially

all of assets

– Change in control as a result of pre-packs, asset sales,

reorganizations

– Coverage terminates for claims arising out of post-change of

control wrongful acts

– Tail Coverage provides additional time to report claims

arising out of pre-policy termination wrongful acts

62 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

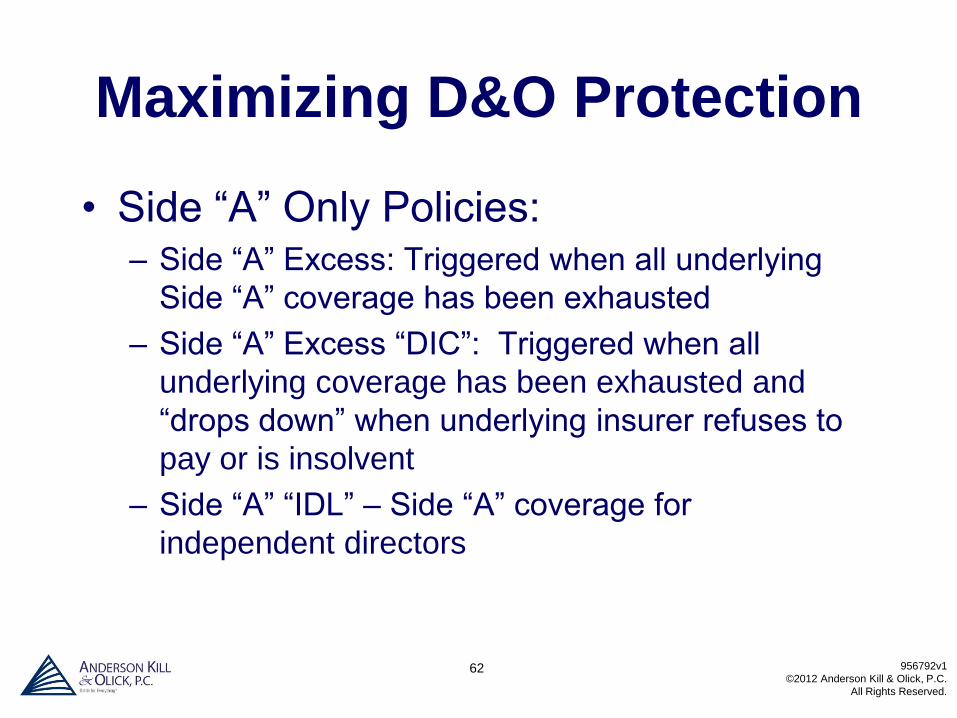

Maximizing D&O Protection

• Side “A” Only Policies: – Side “A” Excess: Triggered when all underlying

Side “A” coverage has been exhausted

– Side “A” Excess “DIC”: Triggered when all

underlying coverage has been exhausted and

“drops down” when underlying insurer refuses to

pay or is insolvent

– Side “A” “IDL” – Side “A” coverage for

independent directors

63 956792v1

©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Maximizing D&O Protection

• Excess Coverage & Exhaustion:

– Underlying coverage must be exhausted

before excess is triggered

– Ensure that excess policies provide for

exhaustion of the underlying limits by the

policyholder to avoid forfeiture of coverage

arguments by excess insurers in the event

of settlements with underlying insurers