d&o fiduciary duties in the zone of...

TRANSCRIPT

Presenting a live 90‐minute webinar with interactive Q&A

D&O Fiduciary Duties in the Zone of InsolvencyAvoiding and Defending Fiduciary Duty Claims and Maximizing D&O Insurance Coverage

T d ’ f l f

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, JULY 30, 2013

Today’s faculty features:

Ian E. Roberts, Senior Associate, BakerBotts, Dallas

Felton Parrish, Partner, Winston & Strawn, Charlotte, N.C.

Alexander D. Hardiman, Shareholder, Anderson Kill & Olick, New YorkAlexander D. Hardiman, Shareholder, Anderson Kill & Olick, New York

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Tips for Optimal Quality

S d Q litSound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-888-450-9970 and enter your PIN when prompted Otherwise please send us a chat or e mail when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of attendees at your locationattendees at your location

• Click the SEND button beside the box

If you have purchased Strafford CLE processing services, you must confirm your participation by completing and submitting an Official Record of Attendance (CLE Form).

You may obtain your CLE form by going to the program page and selecting the appropriate form in the PROGRAM MATERIALS box at the top right corner.

If you'd like to purchase CLE credit processing, it is available for a fee. For additional information about CLE credit processing, go to our website or call us at 1-800-926-7926 ext. 35.

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Director and Officer Dutiesin and around Insolvencyin and around Insolvency

Baker Botts L.L.P.Ian E. Roberts214 953 6719214.953.6719

© 2013

Fiduciary Duties in General

Directors Owe Fiduciary Duties in Different Contexts

The Solvent Company

The Insolvent Company The Insolvent Company

The Insolvent Company in Bankruptcy

The Solvent Company in Bankruptcy

6

The Solvent Company

General Rules

Governed by state law Governed by state law Some states allow certain duties to be limited in chartering documents

See Del. Code Ann. tit 6, § 18-1101(c) (limited liability companies); tit 8, § 102(b)(7) (corporations)

Directors of a solvent company owe fiduciary duties exclusively for the benefit of company's residual risk bearers—shareholders Therefore, actions taken by directors are expected to benefit shareholders

See Prod. Res. Group, LLC v. NCT Group, Inc., 863 A.2d 772, 787 (Del. Ch. 2004)

Typically no duties owed to creditors other than those granted in agreementsTypically no duties owed to creditors other than those granted in agreements Courts believe creditors are capable of protecting themselves and are further

protected by fraudulent conveyance law and bankruptcy law Prod. Res. Group, LLC v. NCT Group, Inc., 863 A.2d 772, 787 (Del. Ch. 2004)

7

The Solvent Company (cont'd)

Business Judgment Rule—courts will not second guess a business judgment so long as a minimum level of care was exercised

Directors are presumed to have acted on an informed, independent, good faith basis and with the honest belief that the action was in the best interest of company See, e.g., Solomon v. Armstrong, 747 A.2d 1098, 1111 (Del. Ch. 1999)

However, this presumption can be rebutted See, e.g., Angelo, Gordon & Co., L.P. v. Allied Riser Commc'n Corp., 805 A.2d 221, 229 (Del. Ch. 2002)

If a party demonstrates that there was neither a business decision, nor disinterestedness and independence, nor due care, nor good faith was present, the burden of proof shifts to the defendant to show the entire fairness of a transactionMills Acquisition Co. v. Macmillan, Inc., 559 A.2d 1261, 1287 (Del.1989)

A heightened standard of review may also apply to specific contexts such as sale of control, defensive actions and decisions affecting stockholder voting rights

Policy underpinnings—courts should not second guess a rational business decision, even if decision proves to be unwise in hindsight

Duty of Loyalty Directors must hold the best interest of corporation above any personal interests

Directors must not self-deal, must not usurp corporate opportunities, must avoid fli t f i t t d t ti t di l

8

conflicts of interest, and at times must disclose

The Solvent Company (cont'd)

Duty of Care Two components:

1. directors must act on an informed basis after due consideration; and

2. directors must act with due care in the discharge of their dutiesSee Cede & Co. v. Technicolor, Inc., 634 A.2d 345, 367 (Del. 1993)

Stated differently, a director must exercise informed business judgment with due care d i d f ithand in good faith

Directors can rely on corporate records as well as information, statements, and opinions of officers, employees, committees, and third-party professionals. See Del. Code Ann. tit. 8, § 141(e)

Directors are protected in doing so if they rely in good faith (i.e., there are no "red flags"), the professional was selected with due care and the opinion is within the expertise of theprofessional was selected with due care, and the opinion is within the expertise of the professional

General points of guidance: Avoid haste Prepare thoroughly Prepare thoroughly Engage competent advisors Seek and assess relevant information from management Beware of potential biases and observe confidentiality obligations Ask questions and remain actively involved

9

Ask questions and remain actively involved Understand the alternatives

The Insolvent Company

The Insolvency Threshold Under Delaware law, insolvency occurs where:

1. liabilities exceed assets (i.e., balance sheet insolvency) with no reasonable prospect for the business to continue successfully; or

2. there is an inability to pay debts as they mature in the ordinary courseSee, e.g., Prod. Res. Group, LLC v. NCT Group, Inc., 863 A.2d 772, 782 (Del. Ch. 2004)

Fiduciary Duties Upon Insolvency Upon insolvency, directors owe fiduciary duties for the benefit of shareholders

and creditors Creditors in effect become the senior residual risk bearers

Fiduciary duties are owed foremost to the entity itself, whether solvent or insolvent Insolvency makes creditors the principal constituency that may be injured by fiduciary breaches

that diminish the value of the enterprisethat diminish the value of the enterprise

"The transformation of a creditor into a residual owner does not change the nature of the harm in a typical claim for breach of fiduciary duty by corporate directors”In re Adelphia Comm’ns Corp., 323 B.R. 345, 386 n.140 (Bankr. S.D.N.Y. 2005)

"duty to" vs. "duty for the benefit of"—there is no shift

10

The Insolvent Company (cont'd)

Scope of Duties Owed

Th f d t l till l di t t i i f d b i The fundamentals still apply—directors must exercise informed business judgment in good faith in the best interest of enterprise

During insolvency the exercise of that judgment must include a consideration of the interest of creditorsof the interest of creditors How does a particular course of action distribute risk and reward between

creditors and equity?

As the corporation's continued existence appears unlikely, acting in the bestAs the corporation s continued existence appears unlikely, acting in the best interest of corporation may require a course of action that benefits creditors more than equity However, just because a course of action benefits one constituency more than

another does not mean it is violative of a fiduciary dutyanother does not mean it is violative of a fiduciary duty

11

The Insolvent Company (cont'd)

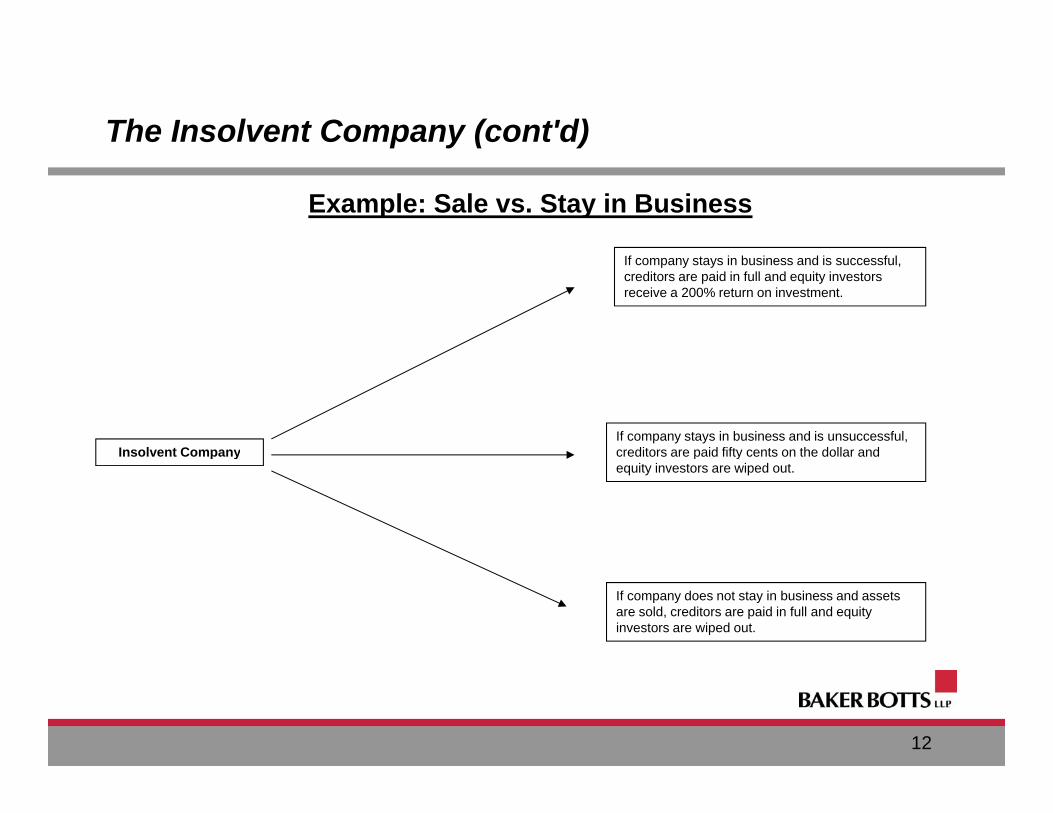

Example: Sale vs. Stay in Business

If company stays in business and is successful, creditors are paid in full and equity investors receive a 200% return on investment.

Insolvent CompanyIf company stays in business and is unsuccessful, creditors are paid fifty cents on the dollar and p y p yequity investors are wiped out.

If company does not stay in business and assets are sold, creditors are paid in full and equity investors are wiped out.

12

The Zone of Insolvency

"Zone of Insolvency"

U t i t t h th dit h h d i ht b f Uncertainty as to whether creditors have enhanced rights before the point of insolvency

Credit Lyonnais suggested that the expansion of duties to creditors can occur in the "vicinity of insolvency " which was unsettling and controversialoccur in the vicinity of insolvency, which was unsettling and controversial Credit Lyonnais Bank Nederland, N.V. v. Pathe Commc'ns Corp., 1991 WL 277613, *34 (Del. Ch. Dec. 30, 1991)

Vicinity standard is inherently vague

13

The Zone of Insolvency (cont'd)

Doubts About the "Zone"

D l S C t d i i i Gh ll t th t th t Delaware Supreme Court decision in Gheewalla suggests that the court may ultimately establish a bright line (e.g., insolvency)N. Am. Catholic Educ. Programming Found., Inc. v. Gheewalla, 930 A.2d 92 (Del. Ch. 2006)

However, commentators and courts have disagreed over whether duties expand for the benefit of creditors prior to insolvency

Fifth Circuit's Torch decision, which applied Delaware law, may suggest that the "zone" remains a viable theoryTorch Liq idating Tr st Stockstill 561 F 3d 377 385 86 (5th Cir 2009)Torch Liquidating Trust v. Stockstill, 561 F.3d 377, 385-86 (5th Cir. 2009)

Southern District of New York has rejected “zone of insolvency” theory under NY Law: “creating a pre-insolvency duty of care to creditors would distort—and potentiallycreating a pre insolvency duty of care to creditors would distort and potentially

conflict with—the incentive structure for corporate managers that the law of fiduciary duties has been erected to create”RSL Comm’ns PLC v. Bildrici, 649 F.Supp.2d 184, 206 (S.D.N.Y. 2009)

14

Case Law Update

In re Trinsum Group, Inc., Reaffirms enforcement of 102(b)(7) provisions in bankruptcy

Di ti i h B id t Distinguishes BridgeportIn re Trinsum Group, Inc., 466 B.R. 596 (Bankr. S.D.N.Y. 2012)

In re TOUSA, Inc. Reaffirmed that subsidiary directors owe duties to insolvent subsidiary's creditors

Court found that parent company's directors could be liable for aiding and abetting breaches of fiduciary duties by subsidiary directors

Court found that parent company's directors could be liable for directing insolvent Court found that parent company s directors could be liable for directing insolvent subsidiaries to use their assets for sole benefit of parent companyOfficial Comm. of Unsecured Creditors v. Technical Olympic (In re TOUSA, Inc.), 437 B.R. 447 (Bankr. S.D. Fla. 2010)

CML V LLC v. BaxD l S C t h ld th t th D l LLC A t d i d i ti t di t Delaware Supreme Court held that the Delaware LLC Act denies derivative standing to creditors of an insolvent limited liability company CML V, LLC v. Bax, 28 A.3d 1037 (Del. 2011)

15

Case Law Update (cont'd)

Auriga Capital Corp. v. Gatz Prop., LLC (Auriga I and II) In Auriga I, Delaware Chancery Court held that, unless eliminated or limited in the LLC g , y ,

agreement, manager owes fiduciary duties of loyalty and care to the LLC and its members by defaultAuriga Capital Corp. v. Gatz Prop., LLC, 40 A.3d 839 (Del. Ch. 2012) (Auriga I)

In Auriga II, Delaware Supreme Court affirmed liability based on terms of the LLCIn Auriga II, Delaware Supreme Court affirmed liability based on terms of the LLC agreement, but held it was "improvident and unnecessary" dictum for Chancery Court to rule on whether the Act imposes default duties. Encourages Delaware Assembly to weigh inGatz Prop., LLC, v. Auriga Capital Corp., 59 A.3d 1206 (Del. 2012) (Auriga II)

Feeley, AK-Feel, LLC v. NHAOCG, LLC Managing member owed fiduciary duties by default under the Act and traditional law

and equity There is no default fiduciary duty for non-managing, non-controlling member of an LLC

(depending on facts and circumstances of the case)Feeley, AK-Feel, LLC v. NHAOCG, LLC, 62 A.3d 649 (Del. Ch. 2012)

16

The Insolvent Company in Bankruptcy

Duties Owed to Estate Directors of a chapter 11 debtor owe fiduciary obligations to bankruptcy estate for benefit

of all constituencies as their interests may appear from time to timeof all constituencies, as their interests may appear from time to timeSee Commodity Futures Trading Comm'n v. Weintraub, 471 U.S. 343, 355 (1985)

Balancing duties Interests of estate's constituencies are often conflicting and adversarial

A debtor simply cannot serve all interests all of the time A debtor simply cannot serve all interests all of the time

Satisfying Duties Preserve and maximize value of debtor's assets

Exercise due care in making business decisions

When conflicts arise, negotiate honestly and in good faith in support of position determined to be in estate's best interest

Inherent conflict among constituencies can exist because of judicial supervision and theInherent conflict among constituencies can exist because of judicial supervision and the rights of parties in interest in the bankruptcy process

17

The Insolvent Company in Bankruptcy (cont'd)

Interaction Between State-law and Bankruptcy-based Duties Although state law fiduciary duties continue to apply in bankruptcy, the Bankruptcy g y pp y p y p y

Code preempts and supplements them to some extent

Section 541 impacts who has standing to assert claims for breach

Transactions outside ordinary course are governed by section 363

Incurring debt is governed by section 364

Creditor and equity committee structure under sections 1102 and 1103

Creditors and equity given right to vote on reorganization plans under sections 1124 and 1126

Trustee or examiner can be appointed under section 1104Trustee or examiner can be appointed under section 1104See Nat'l Convenience Stores Inc. v. Shields (In re Schepps Food Stores, Inc.), 160 B.R. 792 (Bankr. S.D. Tex. 1993)

Preemption especially applicable where state law actions or claims would delay or frustrate reorganization policy of Bankruptcy Code However, a fiduciary duty action that does not impede the bankruptcy proceedings may be , y y p p y p g y

allowed (e.g., action seeking to compel annual meeting for election of directors)See Lionel Corp. v. Comm. of Equity Security Holders (In re Lionel Corp.), 30 B.R. 327 (Bankr. S.D.N.Y. 1983)

18

The Insolvent Company in Bankruptcy (cont'd)

Example: The Conflicted Director What if a director owns substantial equity in debtor and board is faced with restructuring

transaction that pits interests of equity against interests of estate as a whole?

Duty of loyalty is implicated—director should abstain and allow decision to be deliberated upon and made by independent directors

As plan proponent, debtor may elevate its interests above those of a particular constituency Example: cram down

So long as debtor and its management avoid self-dealing and seek to act in estate's best interest, they may pursue a course of action that disfavors a particular constituency

Challenges to a chapter 11 debtor's discharge of fiduciary duties may arise in connection with the exercise of business judgment in a transaction outside ordinaryconnection with the exercise of business judgment in a transaction outside ordinary courseSee, e.g., In re Chrysler LLC, 405 B.R. 84, 105 (Bankr. S.D.N.Y. 2009)

19

The Insolvent Company in Bankruptcy (cont'd)

Types of Suits Under state law and depending on the alleged wrong and relief at stake, a breach of

fiduciary duty may give rise to either:fiduciary duty may give rise to either:1. a direct (or "individual") cause of action or

2. a derivative action

Standing to Pursue SuitStanding to Pursue Suit In bankruptcy, an estate is created that includes all legal or equitable interests of the

debtor in property as of the commencement of the case, including all causes of action See 11 U.S.C. § 541; In re Educators Group Health Trust, 25 F.3d 1281, 1283 (5th Cir. 1994)

If a claim is derivative under state law, it becomes estate property and only the debtor in possession may exercise control over such asset Including claims based on post-petition conduct

Any direct cause of action of a creditor is not property of the estate Any party in interest may seek the appointment of a trustee or examinery y y

11 U.S.C. § 1104

In some circumstances, a bankruptcy court may grant creditors standing to pursue a cause of action on behalf of the estateSee e.g., In La. World Exposition v. Fed. Ins. Co., 858 F.2d 233, 247 (5th Cir. 1988)

20

The Solvent Company in Bankruptcy

Can a chapter 11 debtor be solvent? Debtor may be balance sheet solvent, which would implicate interests of equity

Impact of Solvency Directors' duties continue to be amorphous Whereas outside of bankruptcy duties benefit only shareholders, in bankruptcy duties are

owed to estate as a whole Each constituency has standing to weigh in and protect its interest

Exclusivity and Plan Proposal Debtor's exclusive period to file a plan

11 U.S.C. § 1121(b)

Debtor's ability to cram down is inconsistent with the duty of loyalty to dissenting class, but consistent with its duties to the estate11 U.S.C. § 1129(b)

Bankruptcy Code does not distinguish debtors on the basis of solvency for purposes of plan proposal and confirmation, as it does in other contexts

Exclusivity is balanced with protections for creditors and equity, such as the right to vote and the requirements of cram down

21

Final Thoughts: Issue Spotting

Aiding and abetting Your client need not be the fiduciary

Overlapping boards Wearing multiple hats can invite trouble The wholly-owned subsidiary rule does not apply when the subsidiary becomes

insolvent.

Spin transactions can be problematic (promoter liability, fraudulent transfers and actual independence of new board).

LLC Agreements Do your documents fully eliminate duties? Is an amendment avoidable as an actual

intent fraudulent transfer? Exculpation under the LLC Agreement does not apply once the company is a debtor-in-

possession

Privilege D&O deemed joint clients for purposes of attorney-client privilege, but in a derivative

action that can be overcome under the "fiduciary duty exception." In some situations, separate counsel may be necessary.

22

See In re Teleglobe Com's Corp., 493 F.3d 345, 385 (3d Cir. 2007) and 392 B.R. 561 (Bankr. D. Del. 2008)

Strategies to Avoid and Defend AgainstStrategies to Avoid and Defend AgainstStrategies to Avoid and Defend Against Strategies to Avoid and Defend Against Breach of Fiduciary Duty Claims in Breach of Fiduciary Duty Claims in

Distressed SituationsDistressed SituationsJuly 30, 2013

Felton E ParrishFelton E. ParrishWinston & Strawn LLP100 North Tryon StreetCharlotte, NC 28202

(704) 350-7820

© 2013 Winston & Strawn LLP

(704) 350 [email protected]

Types of ClaimsTypes of Claimsypyp

• Claims typically fall into one of two categories:• Approval of transaction that should not have been approved

• Merger or acquisition• Declaration of dividend• Financing• Spinoff• Actions with subsidiaries

• guarantees or provision of collateral • dividends

• Failure to monitorFi t i t t f it i li ith l• First arose in context of monitoring compliance with law

• Does it apply to monitoring business risk?• In re Citigroup Inc. Shareholder Derivative Litigation, 964 A.2d 106 (Del. Ch.

2009) suggests that answer is no.

© 2013 Winston & Strawn LLP

• Deepening Insolvency?

24

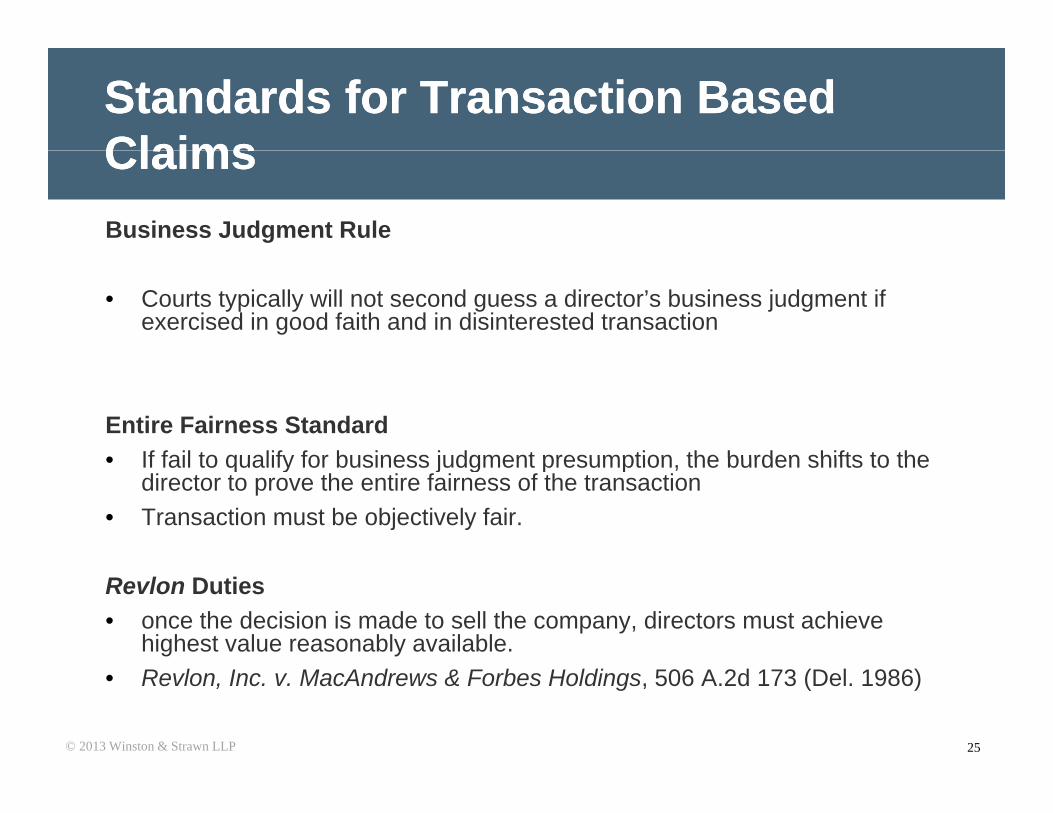

Standards for Transaction Based Standards for Transaction Based ClaimsClaimsClaimsClaimsBusiness Judgment Rule

• Courts typically will not second guess a director’s business judgment if exercised in good faith and in disinterested transaction

Entire Fairness Standard• If fail to qualify for business judgment presumption the burden shifts to the• If fail to qualify for business judgment presumption, the burden shifts to the

director to prove the entire fairness of the transaction• Transaction must be objectively fair.

Revlon Duties• once the decision is made to sell the company, directors must achieve

highest value reasonably available.

© 2013 Winston & Strawn LLP

• Revlon, Inc. v. MacAndrews & Forbes Holdings, 506 A.2d 173 (Del. 1986)

25

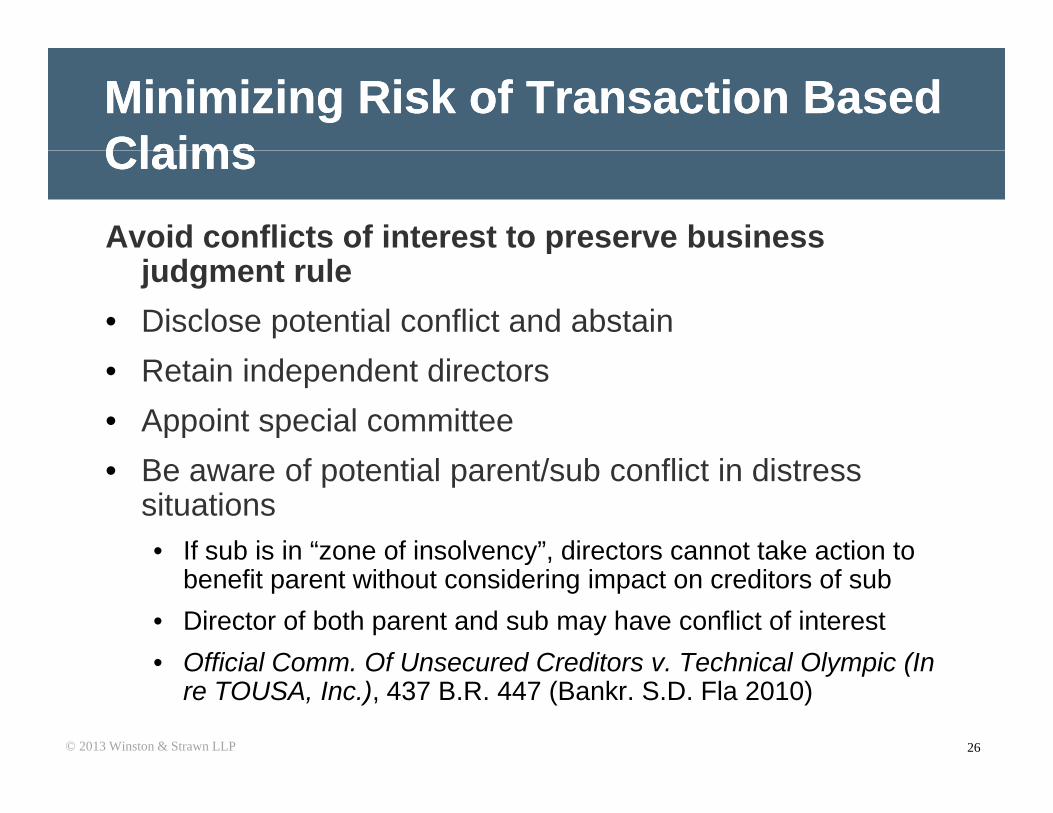

Minimizing Risk of Transaction Based Minimizing Risk of Transaction Based ClaimsClaimsClaimsClaimsAvoid conflicts of interest to preserve business p

judgment rule • Disclose potential conflict and abstain• Retain independent directors• Appoint special committee

f / f• Be aware of potential parent/sub conflict in distress situations• If sub is in “zone of insolvency”, directors cannot take action to y ,

benefit parent without considering impact on creditors of sub• Director of both parent and sub may have conflict of interest• Official Comm Of Unsecured Creditors v Technical Olympic (In

© 2013 Winston & Strawn LLP

• Official Comm. Of Unsecured Creditors v. Technical Olympic (In re TOUSA, Inc.), 437 B.R. 447 (Bankr. S.D. Fla 2010)

26

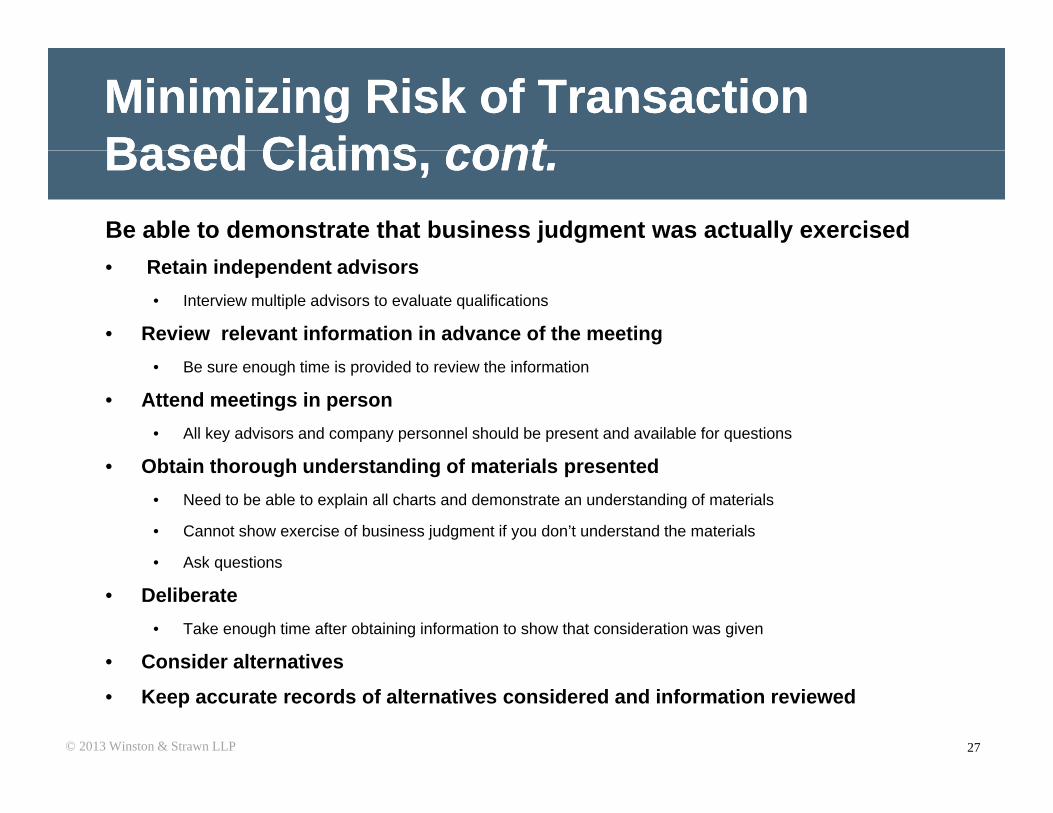

Minimizing Risk of Transaction Minimizing Risk of Transaction BasedBased ClaimsClaims contcontBased Based Claims, Claims, contcont..Be able to demonstrate that business judgment was actually exercised• Retain independent advisors

• Interview multiple advisors to evaluate qualifications

• Review relevant information in advance of the meeting• Be sure enough time is provided to review the information

• Attend meetings in person• All key advisors and company personnel should be present and available for questions

• Obtain thorough understanding of materials presented• Need to be able to explain all charts and demonstrate an understanding of materials

• Cannot show exercise of business judgment if you don’t understand the materials

• Ask questions• Ask questions

• Deliberate• Take enough time after obtaining information to show that consideration was given

• Consider alternatives

© 2013 Winston & Strawn LLP

• Consider alternatives

• Keep accurate records of alternatives considered and information reviewed

27

Standards for Failure to Monitor Standards for Failure to Monitor ClaimsClaimsClaims Claims

Duty of Care or Duty of Loyalty?

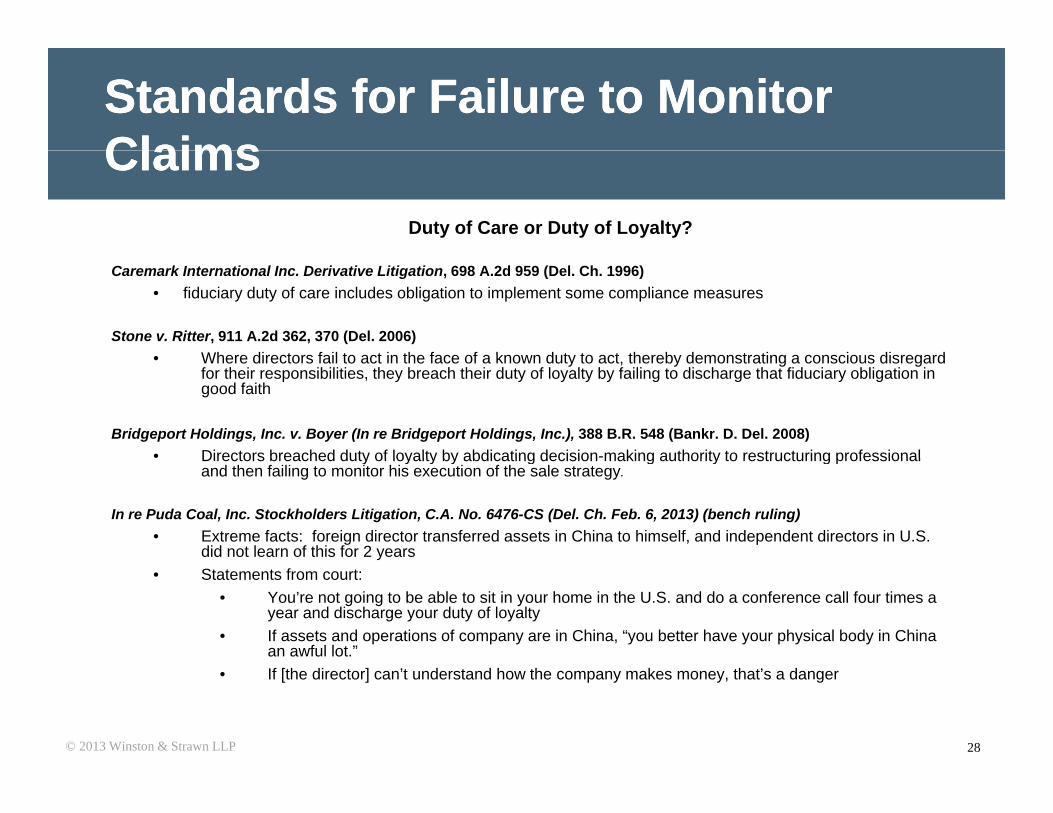

Caremark International Inc. Derivative Litigation, 698 A.2d 959 (Del. Ch. 1996)• fiduciary duty of care includes obligation to implement some compliance measures

Stone v. Ritter, 911 A.2d 362, 370 (Del. 2006)Where directors fail to act in the face of a known duty to act thereby demonstrating a conscious disregard• Where directors fail to act in the face of a known duty to act, thereby demonstrating a conscious disregard for their responsibilities, they breach their duty of loyalty by failing to discharge that fiduciary obligation in good faith

Bridgeport Holdings, Inc. v. Boyer (In re Bridgeport Holdings, Inc.), 388 B.R. 548 (Bankr. D. Del. 2008)• Directors breached duty of loyalty by abdicating decision-making authority to restructuring professionalDirectors breached duty of loyalty by abdicating decision making authority to restructuring professional

and then failing to monitor his execution of the sale strategy.

In re Puda Coal, Inc. Stockholders Litigation, C.A. No. 6476-CS (Del. Ch. Feb. 6, 2013) (bench ruling)• Extreme facts: foreign director transferred assets in China to himself, and independent directors in U.S.

did not learn of this for 2 years• Statements from court:

• You’re not going to be able to sit in your home in the U.S. and do a conference call four times a year and discharge your duty of loyalty

• If assets and operations of company are in China, “you better have your physical body in China an awful lot.”

© 2013 Winston & Strawn LLP

• If [the director] can’t understand how the company makes money, that’s a danger

28

Minimizing Risk of Failure to Monitor Minimizing Risk of Failure to Monitor ClaimsClaimsClaimsClaims• Understand the business and industry

• Implement appropriate monitoring and reporting systems

• Stay informed

• Obtain and review financial reports

• Read articles and analyst reports

• Be on the lookout for “red flags”

• Change in cash flowg

• Increased leverage

• Declining market share

• Key customer in distressKey customer in distress

• Change in marketplace – e.g., competitor with new product

© 2013 Winston & Strawn LLP 29

Deepening InsolvencyDeepening Insolvencyp g yp g y

General Theory:General Theory:• Directors should be responsible for loss of value that

resulted from efforts to prolong company’s existencep g p y

Cause of Action or Measure of Damages?• Trenwick Am Litig Trust v Ernst & Young LLP 906• Trenwick Am. Litig. Trust v. Ernst & Young, LLP, 906

A.2d 168 (Del. Ch. 2006) (no separate cause of action for deepening insolvency).

• Miller v. McCown De Leeuw & Co. (In re The Brown Schools), 386 B.R. 37 (Bankr. D. Del. 2008) (deepening insolvency may still be used as measure

© 2013 Winston & Strawn LLP

(deepening insolvency may still be used as measure of damages).

30

Exculpation Exculpation pp

State laws allow for corporate charters to limit orState laws allow for corporate charters to limit oreliminate liability subject to exceptions

• Delaware GCL § 102(b)(7)

• Model Business Corporation Act § 2.02(b)(4)

© 2013 Winston & Strawn LLP 31

Exceptions to ExculpationExceptions to Exculpationp pp p

Delaware GCL § 102(b)(7)Delaware GCL § 102(b)(7)

No exculpation for:B h f d f l l (b)(7)(i)• Breach of duty of loyalty (b)(7)(i)

• Acts or omissions not in good faith (b)(7)(ii)

• Willful or negligent conduct in paying dividends (b)(7)(iii)

• Transaction from which director obtained improperpersonal benefit (b)(7)(iv)personal benefit (b)(7)(iv)

© 2013 Winston & Strawn LLP 32

Exceptions to Exceptions to Exculpation, cont.Exculpation, cont.pp pp

Model Business Corporation Act § 2.02(b)(4)Model Business Corporation Act § 2.02(b)(4)

• Exceptions more limited than those provided inDGCLDGCL

• No exculpation for:• Amount of financial benefit received by director to which

director is not entitled (b)(4)(A)

• Intentional infliction of harm to the corporation (b)(4)(B)• Intentional infliction of harm to the corporation (b)(4)(B)

• Unlawful distributions (b)(4)(C)

I t ti l i l ti f i i l l (b)(4)(D)

© 2013 Winston & Strawn LLP

• Intentional violation of criminal law (b)(4)(D)

33

Key Points on ExculpationKey Points on Exculpationy py p

In Delaware, no exculpation for breach of duty of loyaltyIn Delaware, no exculpation for breach of duty of loyalty

• Very significant if failure to monitor is viewed as breachof duty of loyaltyof duty of loyalty

• If complaint successfully alleges both breach of duty andbreach of loyalty claims cannot use exculpation provisionbreach of loyalty claims, cannot use exculpation provisionto obtain dismissal

• Alidina v Internet com Corp 2002 WL 31584292 (Del Ch• Alidina v. Internet.com Corp., 2002 WL 31584292 (Del. Ch.Nov. 6, 2002)

• Bridgeport Holdings Inc. Liquidating Trust v. Boyer (In re

© 2013 Winston & Strawn LLP

Bridgeport Holdings Inc. Liquidating Trust v. Boyer (In reBridgeport Holdings Inc.), 388 B.R. 548 (Bankr. D. Del. 2008)

34

IndemnificationIndemnification

Company can agree to indemnify directors subject to certainCompany can agree to indemnify directors subject to certainconditions

DGCL § 145 allows for indemnification if

• Director acted in good faith; and

• Director reasonably believed thaty• Conduct was in or not opposed to best interest of the corporation; and

• In case of criminal proceeding, had no reasonable case to believe thatsuch conduct was unlawfulsuch conduct was unlawful

MBCA has similar standards

© 2013 Winston & Strawn LLP 35

Bankruptcy IssuesBankruptcy Issues

StandingStanding• Once company files for bankruptcy, any derivative

l i th t ld b t d b h lf f thclaims that could be asserted on behalf of thecompany become property of the bankruptcy estate

• Thornton v. Bernard Tech., Inc., 2009 WL 426179(Bankr. D. Del. Feb. 20, 2009)

• In re The 1031 Tax Group, LLC, 397 B.R. 670, 680-81(Bankr. S.D.N.Y. 2008) (holding that breach offiduciary duty and negligence claims are derivative

© 2013 Winston & Strawn LLP

and belong to the trustee)

36

Bankruptcy IssuesBankruptcy Issuesp yp y

Automatic StayAutomatic Stay

• Automatic stay provided by section 362 of the BankruptcyCode only covers the debtorCode only covers the debtor

• Courts may use equitable powers of section 105 to extendtstay.

• Lomas Fin. Corp. v. Northern Trust Co. (In re Lomas Fin Corp.),117 B R 64 (S D N Y 1990) remanded on other grounds 932 F 2d117 B.R. 64 (S.D.N.Y. 1990), remanded on other grounds, 932 F.2d147 (2d Cir. 1991)

• Need to show that debtor would be harmed if litigation continued

© 2013 Winston & Strawn LLP

gagainst officers or directors

37

Bankruptcy IssuesBankruptcy Issuesp yp y

Releases• Plan of reorganization can provide for release of claims against

directors and officers• Debtor can release claims it holds against third parties if proper

exercise of business judgmentexercise of business judgment• In re Spansion, Inc., 426 B.R. 179 (Bankr. D. Del. 2010)

• Non-consensual releases by third partiesC t i l d t ll d i ll Ci it• Controversial and not allowed in all Circuits

• Prohibited in Fifth, Ninth and Tenth Circuits. • In re Zale Corp., 62 F.3d 746 (5th Cir. 1995); In re Lowenschuss, 67 F.3d 1394 (9th Cir.

1995); In re Western Real Estate Fund, 922 F. 2d 592 (10th Cir. 1990).

Even where allowed may be difficult to obtain• Even where allowed, may be difficult to obtain• In re Metromedia Fiber Network Inc., 416 F.3d 136, 143 (2d Cir. 2005) (release appropriate

only in “truly unusual circumstances”)

• Consensual Releases by third parties

© 2013 Winston & Strawn LLP

• Third parties can consent to a release by voting in favor of a plan• See, e.g., In re Monroe Well Service, Inc., 80 B.R. 324, 334-35 (Bankr. E.D. Pa. 1987).

38

D&O INSURANCE ISSUES IN THE CONTEXT OF BANKRUPTCY:

Strategies and Pitfalls on the RoadStrategies and Pitfalls on the Road to Maximizing Coverage

Strafford Publications TeleconferenceJuly 30, 2013

Alexander D. Hardiman, [email protected]@andersonkill.com

(212) 278-1588

39 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

OVERVIEWOVERVIEW• Who does D&O Coverage Belong to?

– Debtor Entity– D&Os– Both

• Accessing Coverage and theAccessing Coverage and the Bankruptcy Stay– Section 302(c) Stay and Policy ProceedsSection 302(c) Stay and Policy Proceeds

• Key D&O Policy Provisions to Maximize Coverage

40 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Coverage

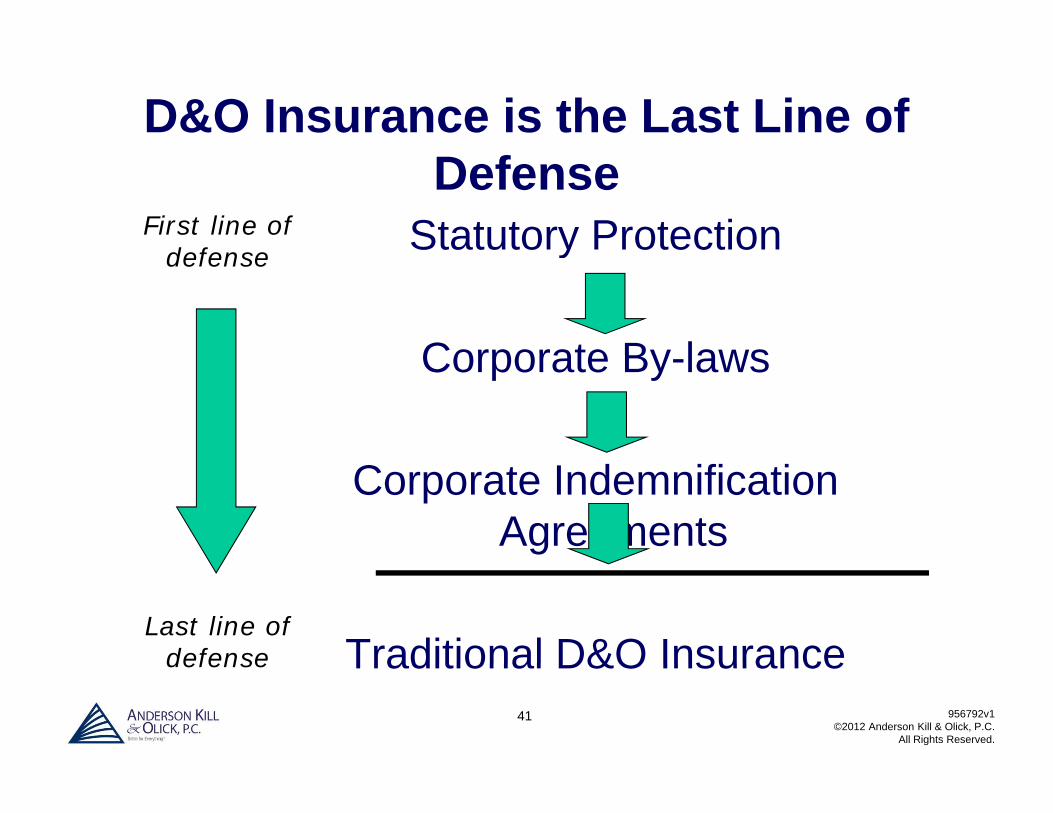

D&O Insurance is the Last Line of Defense

Statutory ProtectionFirst line of defense y

Corporate By laws

defense

Corporate By-laws

Corporate Indemnification Agreements

Traditional D&O InsuranceLast line of

defense

41 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Traditional D&O Insurancedefense

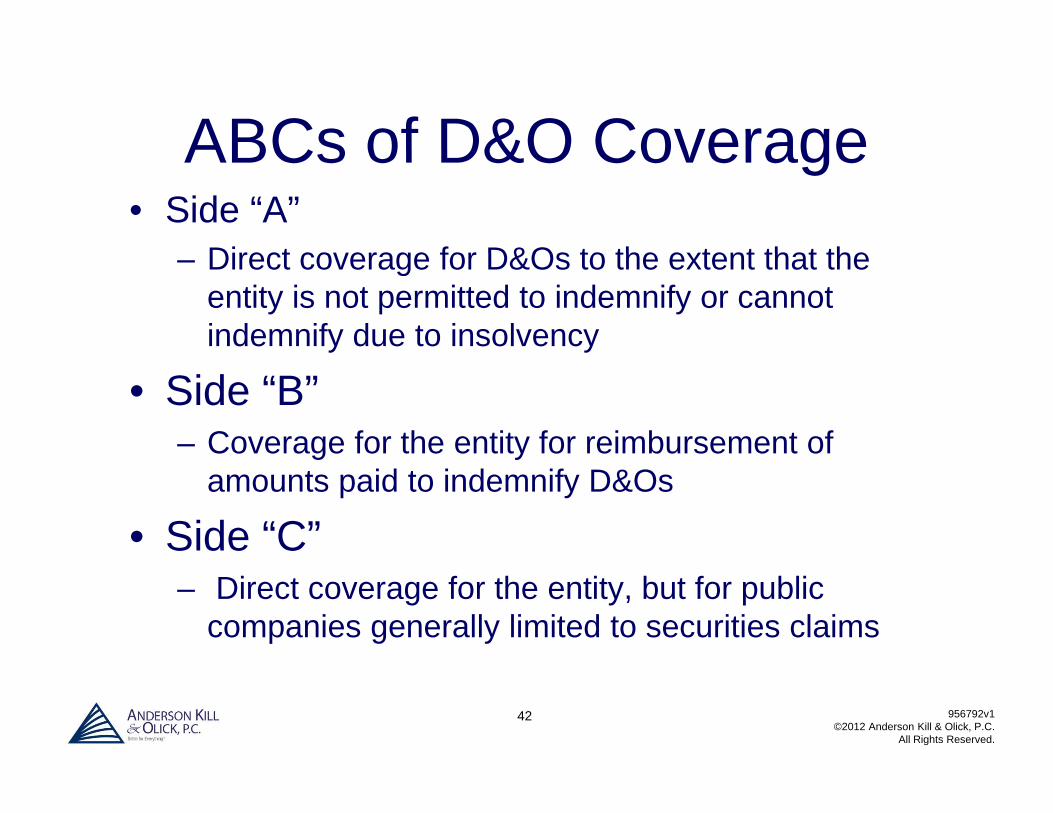

ABCs of D&O CoverageABCs of D&O Coverage• Side “A”

Direct coverage for D&Os to the extent that the– Direct coverage for D&Os to the extent that the entity is not permitted to indemnify or cannot indemnify due to insolvency

• Side “B”– Coverage for the entity for reimbursement of g y

amounts paid to indemnify D&Os

• Side “C”– Direct coverage for the entity, but for public

companies generally limited to securities claims

42 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

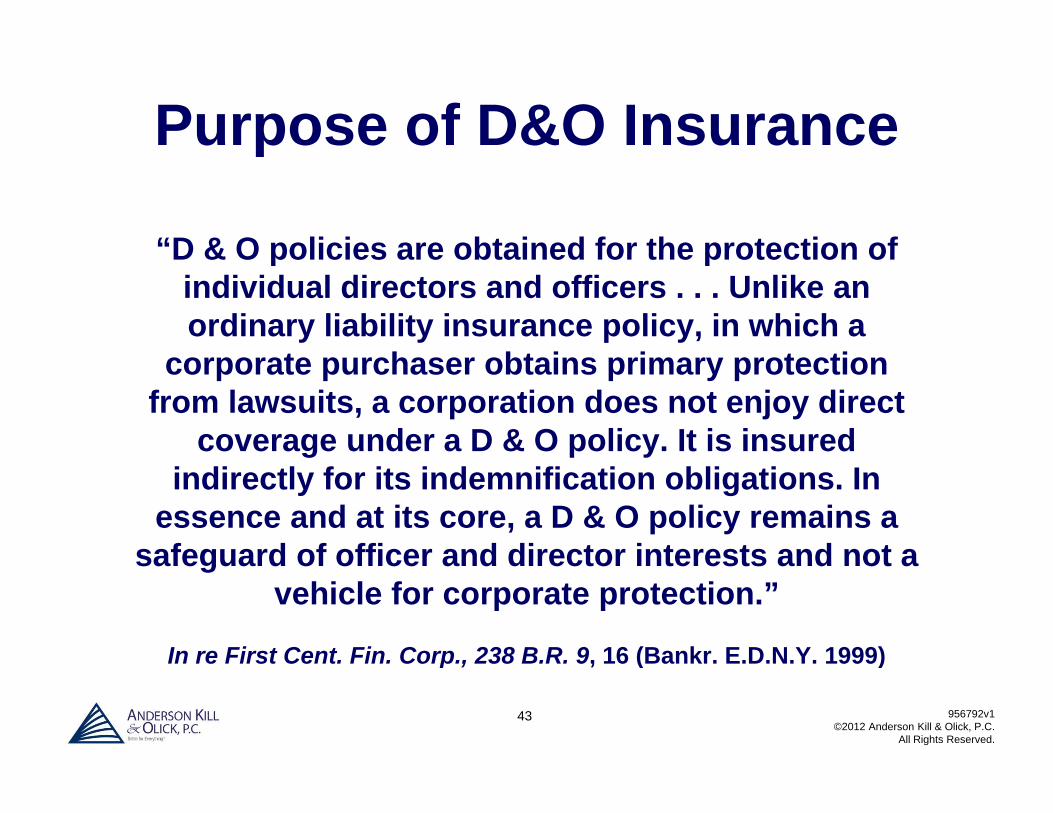

Purpose of D&O Insurancep

“D & O policies are obtained for the protection ofD & O policies are obtained for the protection of individual directors and officers . . . Unlike an ordinary liability insurance policy, in which a

t h bt i i t ticorporate purchaser obtains primary protection from lawsuits, a corporation does not enjoy direct

coverage under a D & O policy. It is insured indirectly for its indemnification obligations. In

essence and at its core, a D & O policy remains a safeguard of officer and director interests and not asafeguard of officer and director interests and not a

vehicle for corporate protection.”

In re First Cent. Fin. Corp., 238 B.R. 9, 16 (Bankr. E.D.N.Y. 1999)

43 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

In re First Cent. Fin. Corp., 238 B.R. 9, 16 (Bankr. E.D.N.Y. 1999)

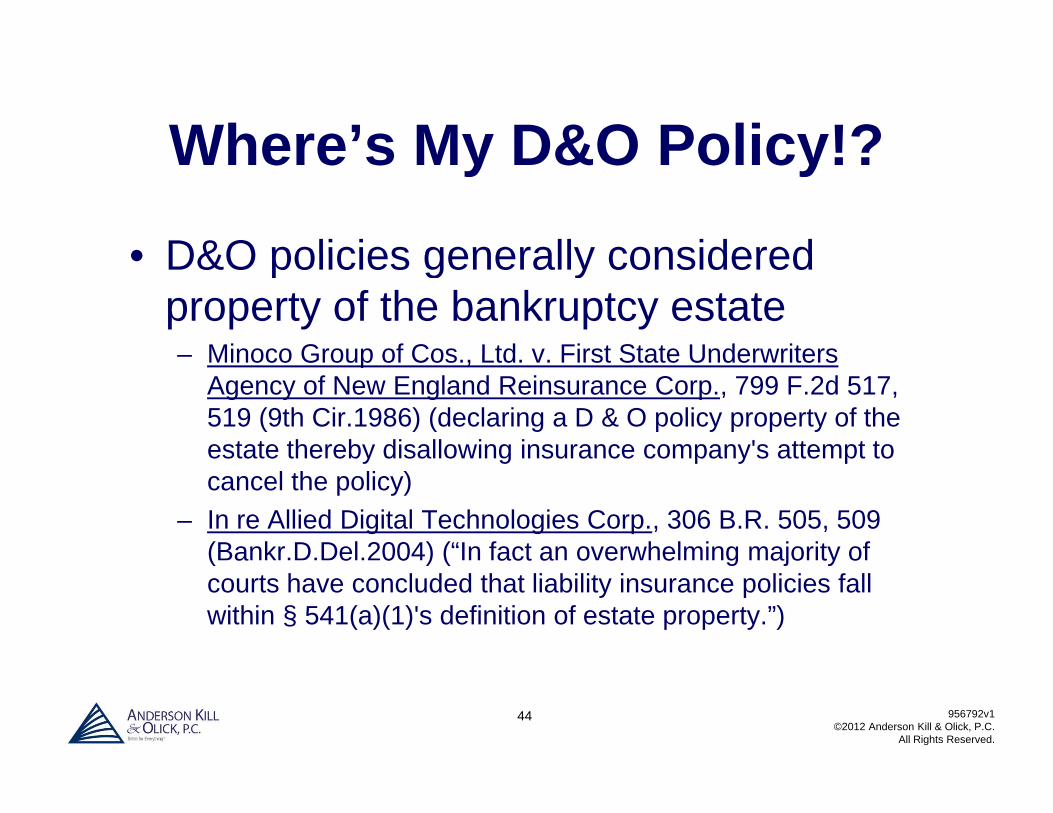

Where’s My D&O Policy!?Where s My D&O Policy!?

• D&O policies generally considered• D&O policies generally considered property of the bankruptcy estate– Minoco Group of Cos Ltd v First State Underwriters– Minoco Group of Cos., Ltd. v. First State Underwriters

Agency of New England Reinsurance Corp., 799 F.2d 517, 519 (9th Cir.1986) (declaring a D & O policy property of the estate thereby disallowing insurance company's attempt toestate thereby disallowing insurance company s attempt to cancel the policy)

– In re Allied Digital Technologies Corp., 306 B.R. 505, 509 (Bankr.D.Del.2004) (“In fact an overwhelming majority of ( a e 00 ) ( act a o e e g ajo ty ocourts have concluded that liability insurance policies fall within § 541(a)(1)'s definition of estate property.”)

44 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

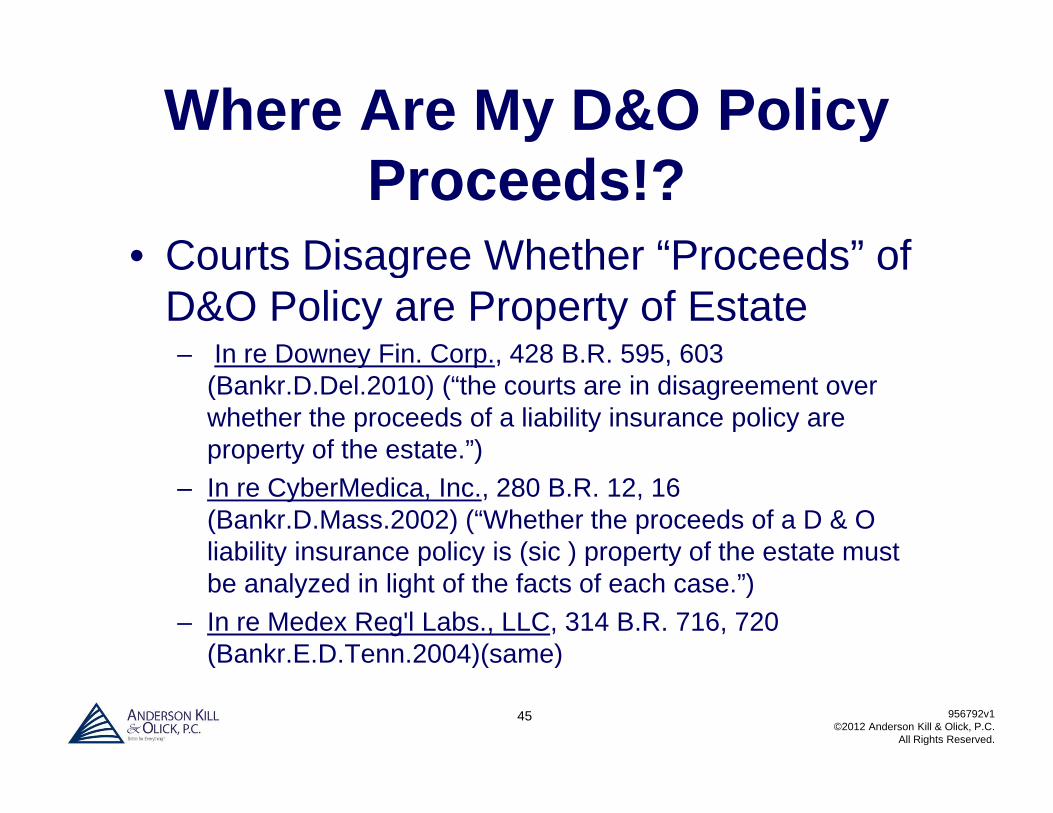

Where Are My D&O Policy Proceeds!?

• Courts Disagree Whether “Proceeds” of• Courts Disagree Whether Proceeds of D&O Policy are Property of Estate– In re Downey Fin Corp 428 B R 595 603– In re Downey Fin. Corp., 428 B.R. 595, 603

(Bankr.D.Del.2010) (“the courts are in disagreement over whether the proceeds of a liability insurance policy are property of the estate.”)property of the estate. )

– In re CyberMedica, Inc., 280 B.R. 12, 16 (Bankr.D.Mass.2002) (“Whether the proceeds of a D & O liability insurance policy is (sic ) property of the estate must ab ty su a ce po cy s (s c ) p ope ty o t e estate ustbe analyzed in light of the facts of each case.”)

– In re Medex Reg'l Labs., LLC, 314 B.R. 716, 720 (Bankr.E.D.Tenn.2004)(same)

45 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

( )( )

Where Are My D&O Policy Proceeds!?

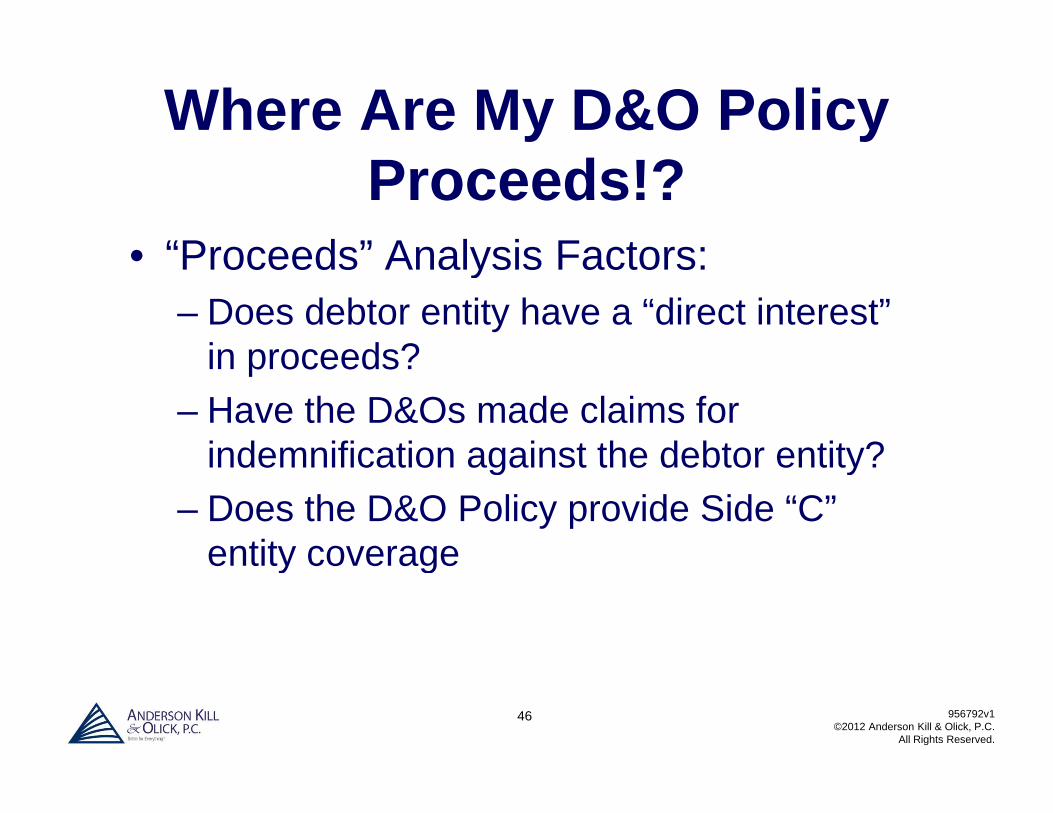

• “Proceeds” Analysis Factors:• Proceeds Analysis Factors:– Does debtor entity have a “direct interest”

in proceeds?in proceeds?– Have the D&Os made claims for

indemnification against the debtor entity?indemnification against the debtor entity?– Does the D&O Policy provide Side “C”

entity coverageentity coverage

46 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Where Are My D&O Policy Proceeds!?

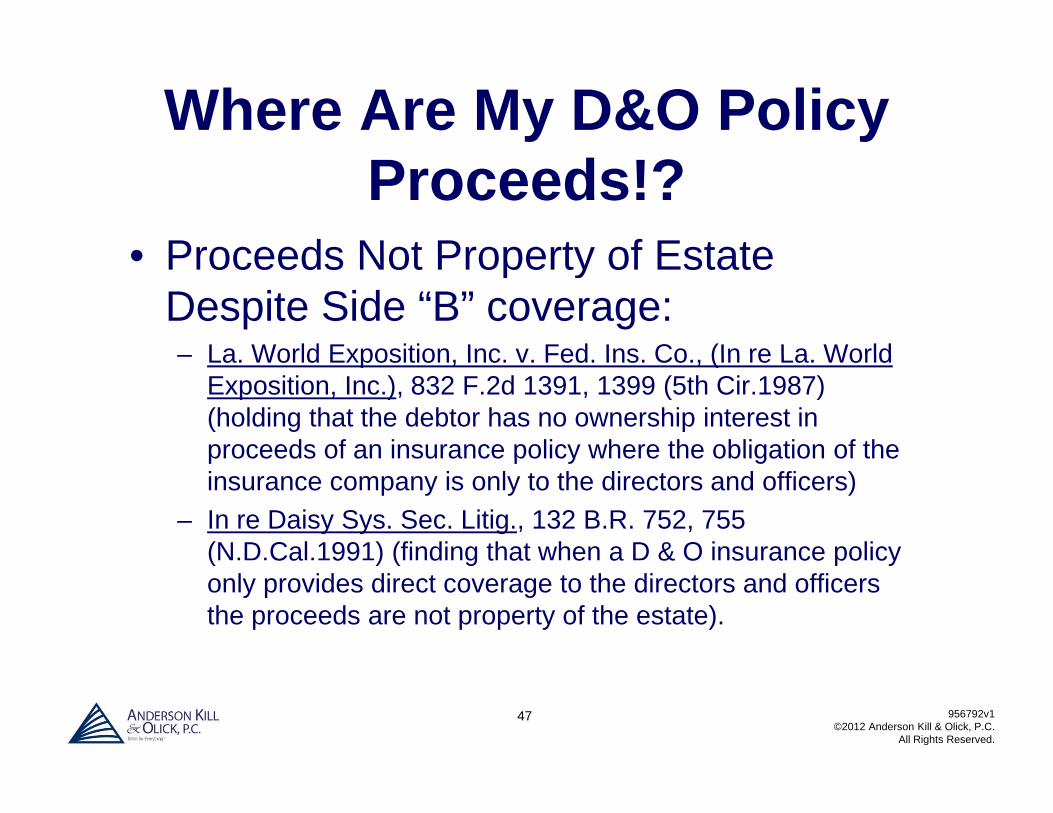

• Proceeds Not Property of Estate• Proceeds Not Property of Estate Despite Side “B” coverage:– La World Exposition Inc v Fed Ins Co (In re La World– La. World Exposition, Inc. v. Fed. Ins. Co., (In re La. World

Exposition, Inc.), 832 F.2d 1391, 1399 (5th Cir.1987) (holding that the debtor has no ownership interest in proceeds of an insurance policy where the obligation of theproceeds of an insurance policy where the obligation of the insurance company is only to the directors and officers)

– In re Daisy Sys. Sec. Litig., 132 B.R. 752, 755 (N.D.Cal.1991) (finding that when a D & O insurance policy ( Ca 99 ) ( d g t at e a & O su a ce po cyonly provides direct coverage to the directors and officers the proceeds are not property of the estate).

47 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Where Are My D&O Policy Proceeds!?

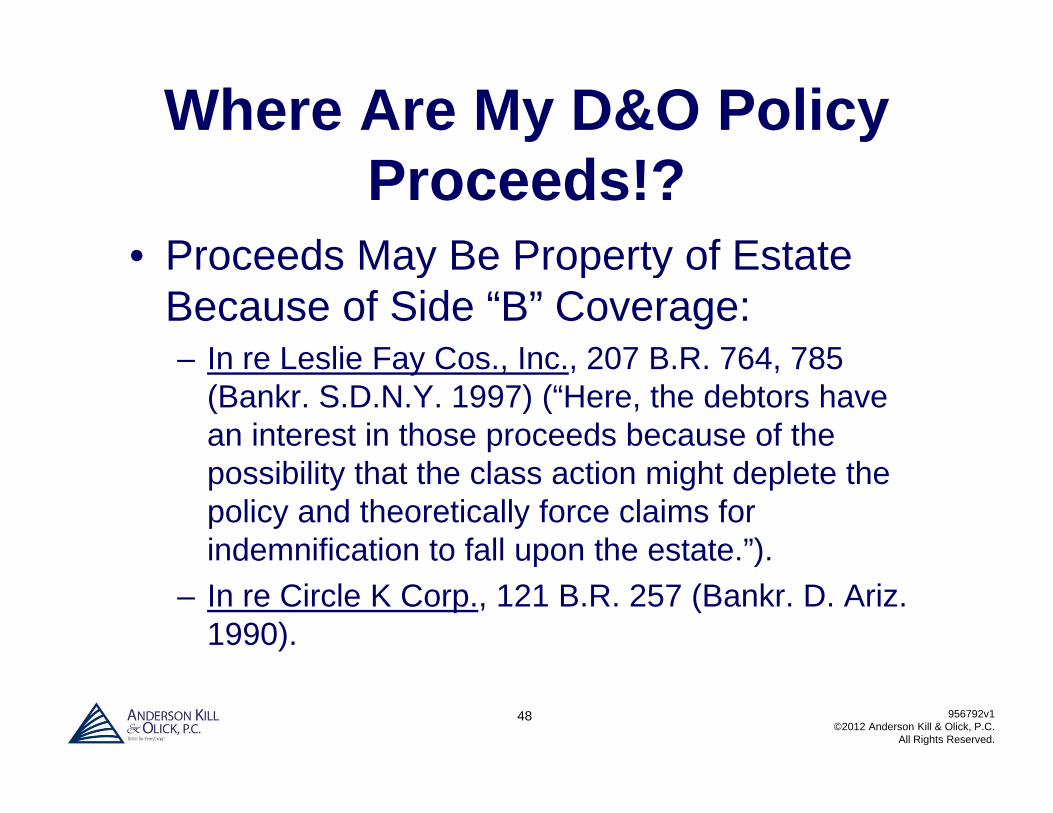

• Proceeds May Be Property of Estate• Proceeds May Be Property of Estate Because of Side “B” Coverage:

In re Leslie Fay Cos Inc 207 B R 764 785– In re Leslie Fay Cos., Inc., 207 B.R. 764, 785 (Bankr. S.D.N.Y. 1997) (“Here, the debtors have an interest in those proceeds because of the possibility that the class action might deplete the policy and theoretically force claims for indemnification to fall upon the estate.”).de cat o to a upo t e estate )

– In re Circle K Corp., 121 B.R. 257 (Bankr. D. Ariz. 1990).

48 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Where Are My D&O Policy Proceeds!?

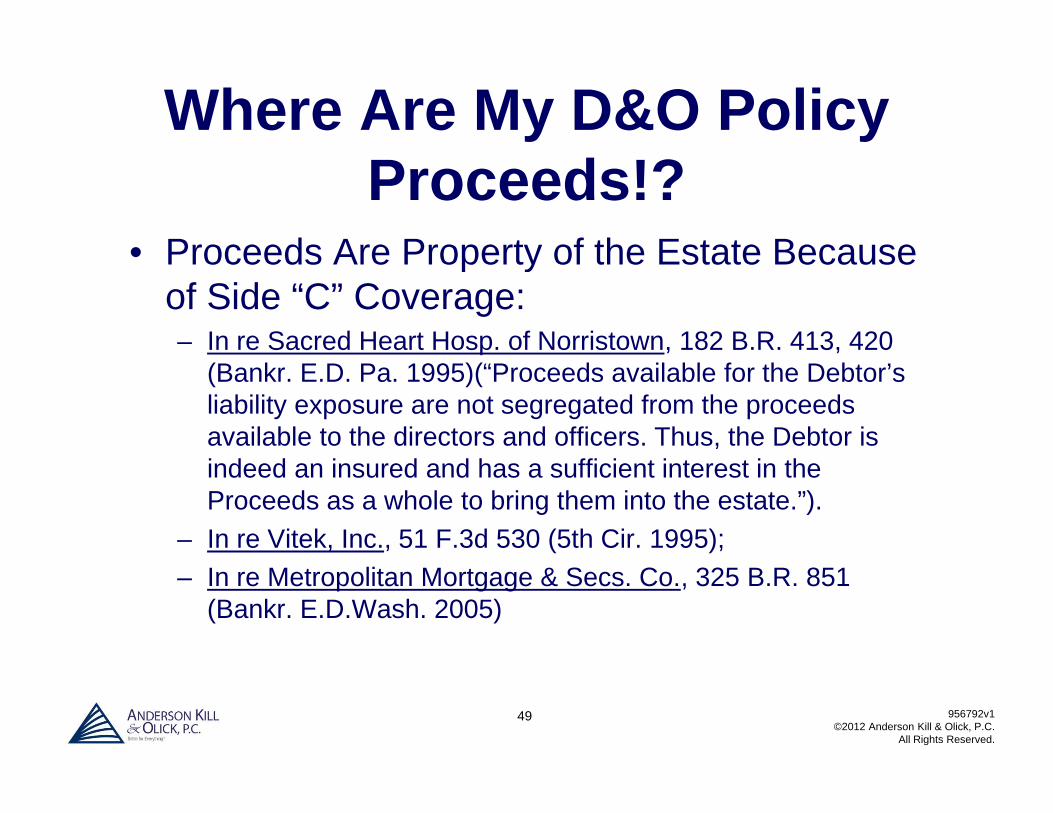

• Proceeds Are Property of the Estate Because• Proceeds Are Property of the Estate Because of Side “C” Coverage:– In re Sacred Heart Hosp. of Norristown, 182 B.R. 413, 420

(Bankr. E.D. Pa. 1995)(“Proceeds available for the Debtor’s liability exposure are not segregated from the proceeds available to the directors and officers. Thus, the Debtor is indeed an insured and has a sufficient interest in the Proceeds as a whole to bring them into the estate.”).

– In re Vitek, Inc., 51 F.3d 530 (5th Cir. 1995); – In re Metropolitan Mortgage & Secs. Co., 325 B.R. 851

(Bankr. E.D.Wash. 2005)

49 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Where Are My D&O Policy Proceeds!?

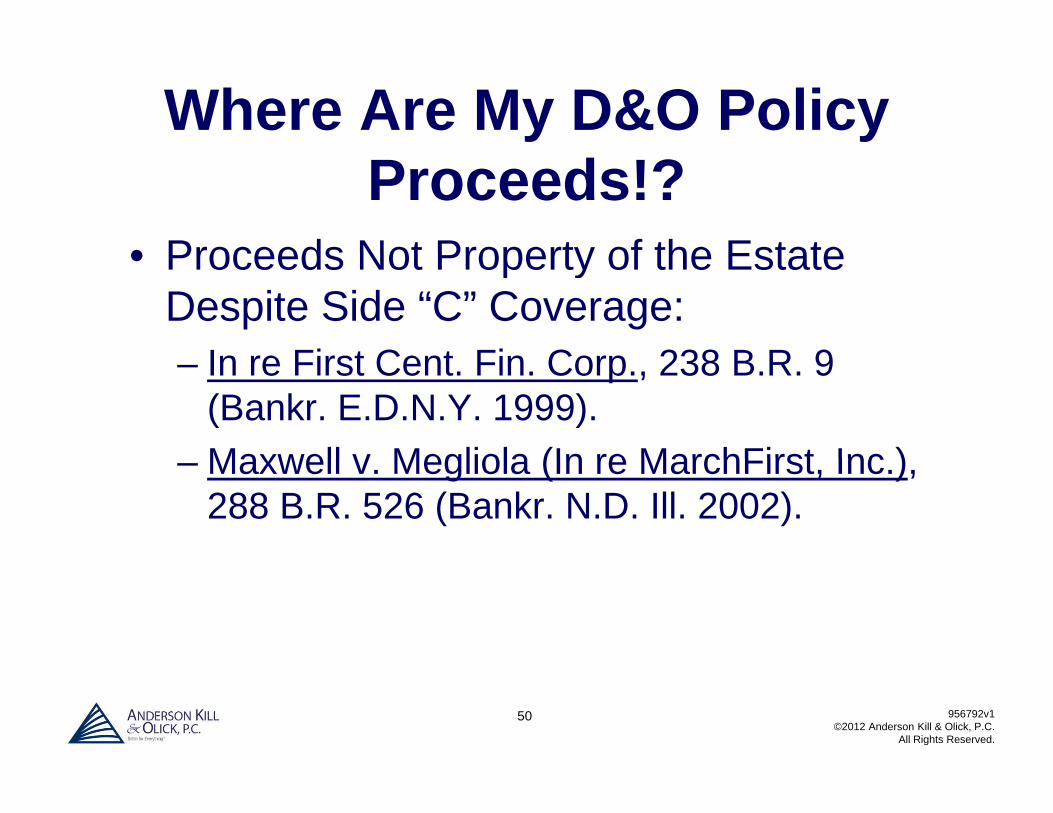

• Proceeds Not Property of the Estate• Proceeds Not Property of the Estate Despite Side “C” Coverage:

I Fi t C t Fi C 238 B R 9– In re First Cent. Fin. Corp., 238 B.R. 9 (Bankr. E.D.N.Y. 1999).Maxwell v Megliola (In re MarchFirst Inc )– Maxwell v. Megliola (In re MarchFirst, Inc.), 288 B.R. 526 (Bankr. N.D. Ill. 2002).

50 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Two “Proceeds” Case Studies

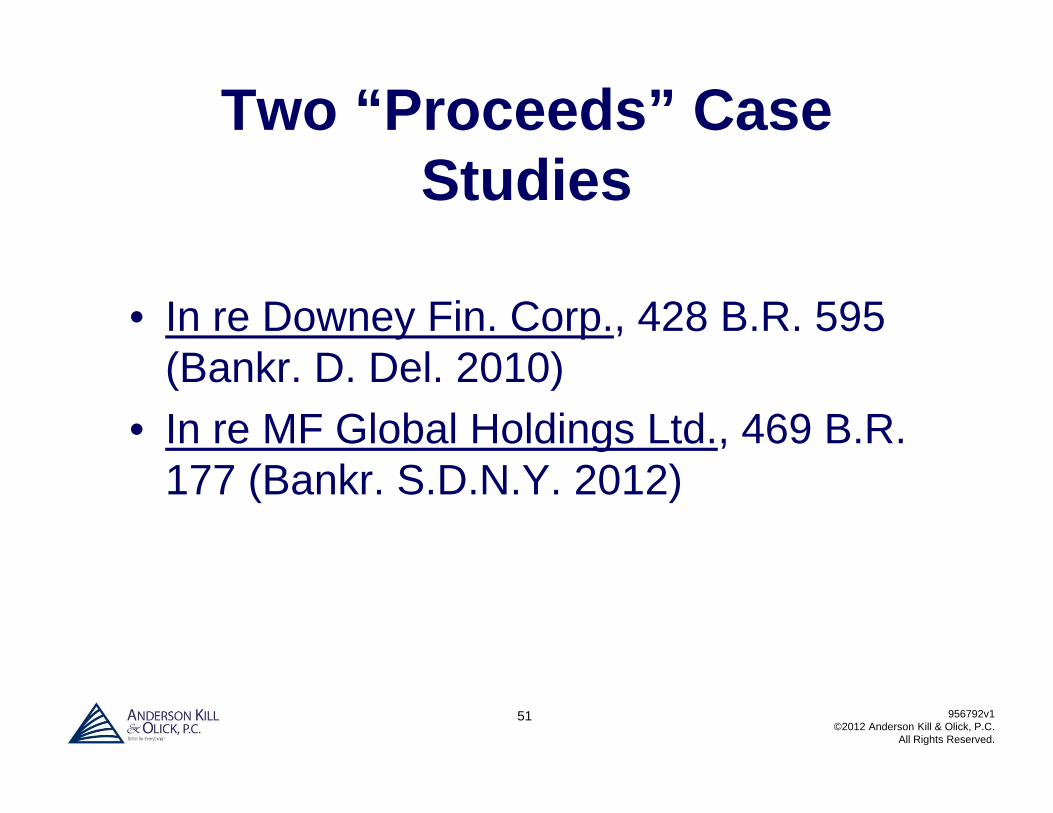

• In re Downey Fin. Corp., 428 B.R. 595 (B k D D l 2010)(Bankr. D. Del. 2010)

• In re MF Global Holdings Ltd., 469 B.R. 177 (Bankr. S.D.N.Y. 2012)

51 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

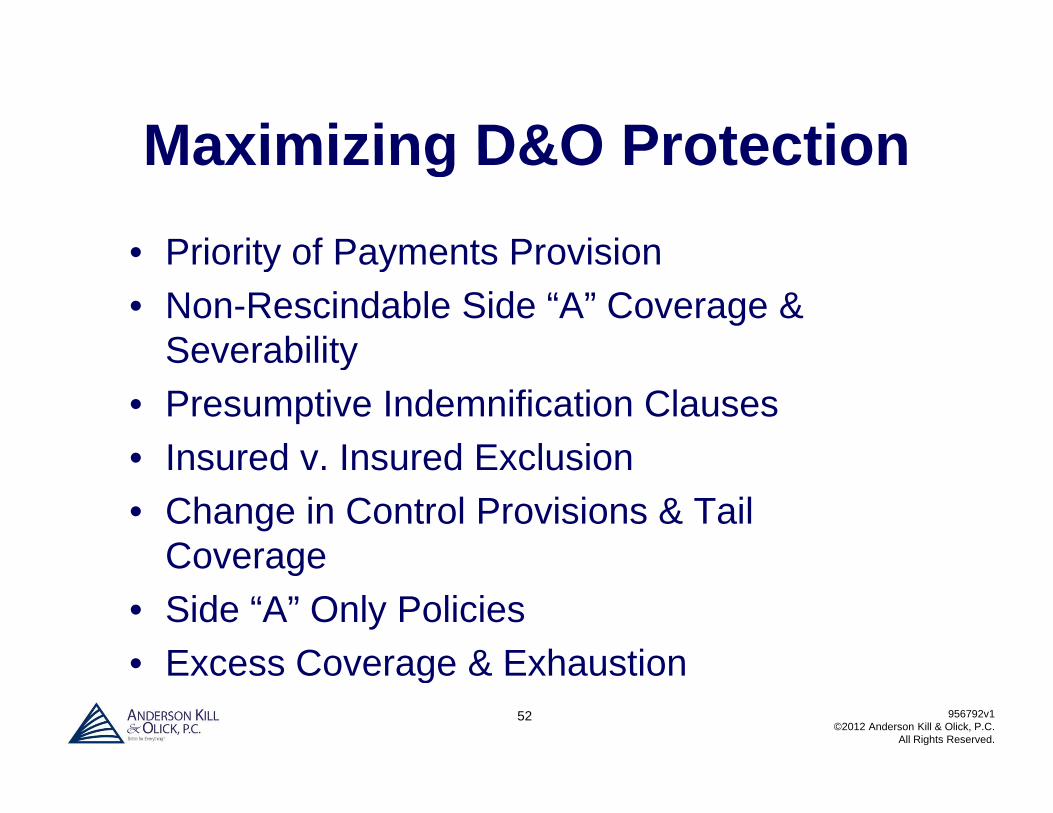

Maximizing D&O ProtectionMaximizing D&O Protection• Priority of Payments Provision• Priority of Payments Provision• Non-Rescindable Side “A” Coverage &

SeverabilitySeverability• Presumptive Indemnification Clauses • Insured v Insured Exclusion• Insured v. Insured Exclusion• Change in Control Provisions & Tail

CoverageCoverage• Side “A” Only Policies• Excess Coverage & Exhaustion

52 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

• Excess Coverage & Exhaustion

Maximizing D&O ProtectionMaximizing D&O Protection

• Priority of Payments Provision• Priority of Payments Provision– Side “A” payments have priority over Side

“B” or Side “C” paymentsB or Side C payments– Assists or may be determinative in

overcoming policy “proceeds” issueovercoming policy proceeds issue– Limits uncertainty over D&O defense cost

fundingfunding

53 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Maximizing D&O ProtectionMaximizing D&O Protection

• Non Rescindable Side “A” Coverage:• Non Rescindable Side A Coverage:– Attempts by insurer to void or rescind

coverage based on fraud orcoverage based on fraud or misrepresentation

– Non Rescindable Side “A” Endorsement– Non Rescindable Side A Endorsement bars rescission

– Severability provisions also limit theSeverability provisions also limit the imputation of knowledge between insureds for rescission / voiding of coverage

54 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Maximizing D&O ProtectionMaximizing D&O Protection

• Presumptive Indemnification Clauses :• Presumptive Indemnification Clauses :– Indemnification of D&O by entity is

“presumed” (i e if entity is required orpresumed (i.e. if entity is required or permitted to indemnify) then retention applicable to Side “B” appliesapplicable to Side B applies

– Include provision stating that presumptive indemnification is inapplicable in the event ppof “financial insolvency or “financial impairment”

55 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Maximizing D&O ProtectionMaximizing D&O Protection

• Insured v Insured Exclusion (I v I)• Insured v. Insured Exclusion (I. v. I)– Excludes coverage for claims of entity

against D&Os and vice versaagainst D&Os and vice-versa– Most I v. I exclusions contain carve out for

bankruptcy related claims but oftenbankruptcy related claims but often concern coverage for claims by receiver, liquidator, chap 7 trusteeq , p

– Ensure that carve-out is provided claims by DIPs, chap 11 trustee, creditors etc.

56 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Maximizing D&O ProtectionMaximizing D&O Protection

• Change in Control Provisions & Tail• Change in Control Provisions & Tail Coverage:– Change in management control as a result of 50%+ change– Change in management control as a result of 50%+ change

of control on board of directors or sale of all or substantially all of assets

– Change in control as a result of pre-packs asset sales– Change in control as a result of pre-packs, asset sales, reorganizations

– Coverage terminates for claims arising out of post-change of control wrongful actscontrol wrongful acts

– Tail Coverage provides additional time to report claims arising out of pre-policy termination wrongful acts

57 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Maximizing D&O ProtectionMaximizing D&O Protection

• Side “A” Only Policies:• Side A Only Policies:– Side “A” Excess: Triggered when all underlying

Side “A” coverage has been exhaustedSide A coverage has been exhausted– Side “A” Excess “DIC”: Triggered when all

underlying coverage has been exhausted and “d d ” h d l i i f t“drops down” when underlying insurer refuses to pay or is insolvent

– Side “A” “IDL” – Side “A” coverage forSide A IDL Side A coverage for independent directors

58 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.

Maximizing D&O ProtectionMaximizing D&O Protection

• Excess Coverage & Exhaustion:• Excess Coverage & Exhaustion:– Underlying coverage must be exhausted

before excess is triggeredbefore excess is triggered– Ensure that excess policies provide for

exhaustion of the underlying limits by theexhaustion of the underlying limits by the policyholder to avoid forfeiture of coverage arguments by excess insurers in the event g yof settlements with underlying insurers

59 956792v1©2012 Anderson Kill & Olick, P.C.

All Rights Reserved.