does swap-covered interest parity hold in long-term … does swap-covered interest parity hold in...

TRANSCRIPT

PRI Discussion Paper Series (No.17A-06)

Does swap-covered interest parity hold in long-term capital markets

after the financial crisis?

Takahiro Hattori

Researcher, Policy Research Institute, Ministry of Finance

March 2017

Research Department Policy Research Institute, MOF

3-1-1 Kasumigaseki, Chiyoda-ku, Tokyo 100-8940, Japan

TEL 03-3581-4111

The views expressed in this paper are those of the

authors and not those of the Ministry of Finance or

the Policy Research Institute.

1

Does swap-covered interest parity hold in long-term capital

markets after the financial crisis?*

Takahiro Hattori

Ministry of Finance Japan, Hitotsubashi University

This version 2017/3

ABSTRACT

This paper analyzes swap-covered interest parity by comparing US Treasury bonds with

USD denominated foreign assets replicated using cross-currency basis swaps. We find that

the deviations of these yield spreads declined substantially after the financial crisis, which

is in sharp contrast with the variation in the cross-currency basis. The analysis in this paper

also shows the existence of cointegrating relationships between the cross-currency basis

and domestic/foreign swap spreads, and conclude that the US swap spread tightening is

related to the negative currency basis.

JEL classification: E43, F31, G15

Keywords: Covered interest parity, Cross-currency basis swap, Cointegration, Swap spread,

Term structure

* The author would like to express thanks to Hajime Fujiwara, Junko Koeda, Shigeyuki Hamori,

Masazumi Hattori, Makoto Nirei, Tatsuyoshi Okimoto, Toshiaki Watanabe, Tomoyoshi Yabu, Takefumi

Yamazaki and seminar participants at Kyoto University, Waseda University and Ministry of Finance,

Japan. The views expressed in this paper are those of the author and not those of the Ministry of Finance

or the Policy Research Institute. E-mail: [email protected]

2

1.Introduction

The cross-currency basis swap (CCBS) across most USD pairs is receiving attention from

both practitioners and academics. The currency basis was within a few basis points of zero

until the start of the financial crisis, but it has become persistently and systemically

negative after the turmoil. In the academic literature, this persistent negative currency basis

can be considered the deviation from covered interest parity (CIP) and several academic

papers studying this new phenomenon have emerged recently. The general consensus

between practitioners and academics is that the negative currency basis stems from recent

financial regulations.

The negative currency basis is challenging for financial economists as it seems to imply

“arbitrage opportunities”. The analysis in this paper empirically shows that sufficient

arbitrage activity has been widespread in financial markets from USD holders. More

precisely, we directly compare (i) the yield of USD treasuries with (ii) the yield of USD

denominated foreign assets replicated by CCBSs, and conclude that the deviation of these

yields has decreased drastically. This deviation reflects the condition of swap-covered

interest parity, which is proposed by Popper (1993), Terakawa (1995) and Fletcher and

Taylor (1996), among others.

This result seems to contradict previous studies. However, we reconcile our paradoxical

findings with these studies, shedding light on how banking regulation affects asset prices

and investors. There are two mechanisms for rationalizing our results, and the contribution

in this paper also supports previous studies in different ways.

First, this paper explicitly connects the currency basis with swap spreads through the

concept of swap-covered interest parity. In fact, the swap spreads have drastically tightened

and even become negative at longer maturities since the financial crisis. Currently,

academics are studying this anomaly, and one plausible explanation is based on the recent

reform of banking regulations. For example, Jermann (2016) argues that the cost of holding

a bond has increased under post-reform financial regulation, while Klinger and Sundaresan

(2016) focus on the demand for swaps arising from the duration hedging needs of

underfunded pension plans under the balance sheet constraints of swap dealers. In this

3

context, banking regulations are the common driver of the currency basis, and this factor

simultaneously causes the negative currency basis and swap spread tightening, so the

condition of swap-covered interest parity, which links the currency basis with the swap

spreads, has not deteriorated after the financial crisis.

Second, USD denominated foreign bonds enable nonfinancial institutions to enter

currency swap markets. Recently, over-the-counter (OTC) derivative markets have had

higher participation costs such as the agreement of the Credit Support Annex (CSA) and

central clearing. Thus, it is unrealistic for them to enter the OTC market directly. On the

other hand, nonfinancial institutions actually invest in USD denominated bonds through

mutual funds or structured notes, and this implies that they can arbitrage in OTC markets

using USD denominated foreign assets. Because nonfinancial institutions do not have to

abide by banking regulations, their arbitrage activity is not limited. Of course, nonfinancial

institutions are supposed to use CCBS contracts with financial institutions; however, these

financial institutions only play the role of the market maker in this case and they can offset

the regulation cost by hedging and compressing this position. In other words, USD

denominated foreign bonds can be used to avoid banking regulations.

After the financial crisis, there has been increased interest in CIP deviations in the

academic literature. One strand of the literature focuses on deviations during the financial

crisis. Most studies argue that the turmoil prevented arbitrage activity from eliminating the

deviations in CIP (Baba 2009; Baba and Packer 2009; Baba et al., 2008; Baba and Sakurai

2012; Coffey et al. 2009; Griffolli and Ranaldo, 2011; Ivashina et al. 2015). The other

strand of the literature explains the deviations after the financial crisis. Du et al. (2016)

show that the banks’ balance sheets at the end of the quarter have a causal effect on the

forward prices. Borio et al. (2016) and Sushko et al. (2016) construct empirical proxies for

hedging demand and show that these proxies are associated with the CIP deviations. Iida et

al. (2016) find that regulatory reforms, such as a stricter leverage ratio, raise the sensitivity

of CIP deviations to monetary policy. Avdjiev et al. (2016) show that a stronger dollar goes

hand-in-hand with bigger deviations from CIP and contractions of cross-border bank

lending in dollars, caused by the banking regulation.

4

Our paper contributes to the literature by focusing on swap-covered interest parity after

the financial crisis and presents evidence that the deviations from this condition have

decreased substantially, concluding that arbitrage is still effective in international financial

markets. In addition, the analysis in this paper interprets the swap-covered interest parity as

the cointegrating relationship between the cross-currency basis and domestic/foreign

interest rate swap spreads, and empirically show there is an equilibrium relationship among

these variables. Moreover, the estimation results show that the USD swap spread tightening

has been significantly related to the negative cross-currency basis.

The present paper also contributes to a better understanding of the “term structure of the

cross-currency basis”. The equilibrium relationship states that the specific maturity of the

currency basis should be matched with the exact same maturity of the swap spreads, so the

term structure of the currency basis should be driven by the same maturity of the swap

spread curve. Our model can account for about half of the currency basis variations in the

short and middle maturities while the explanatory power increases to around 70–80% in the

longer maturities.

This paper proceeds as follows. Section 2 briefly describes the pricing scheme of USD

denominated foreign assets. Section 3 shows that the deviation from swap-covered interest

parity has decreased after the financial crisis. Section 4 conducts the cointegration analysis.

Section 5 concludes.

2. Swap-covered interest parity and pricing USD denominated bonds

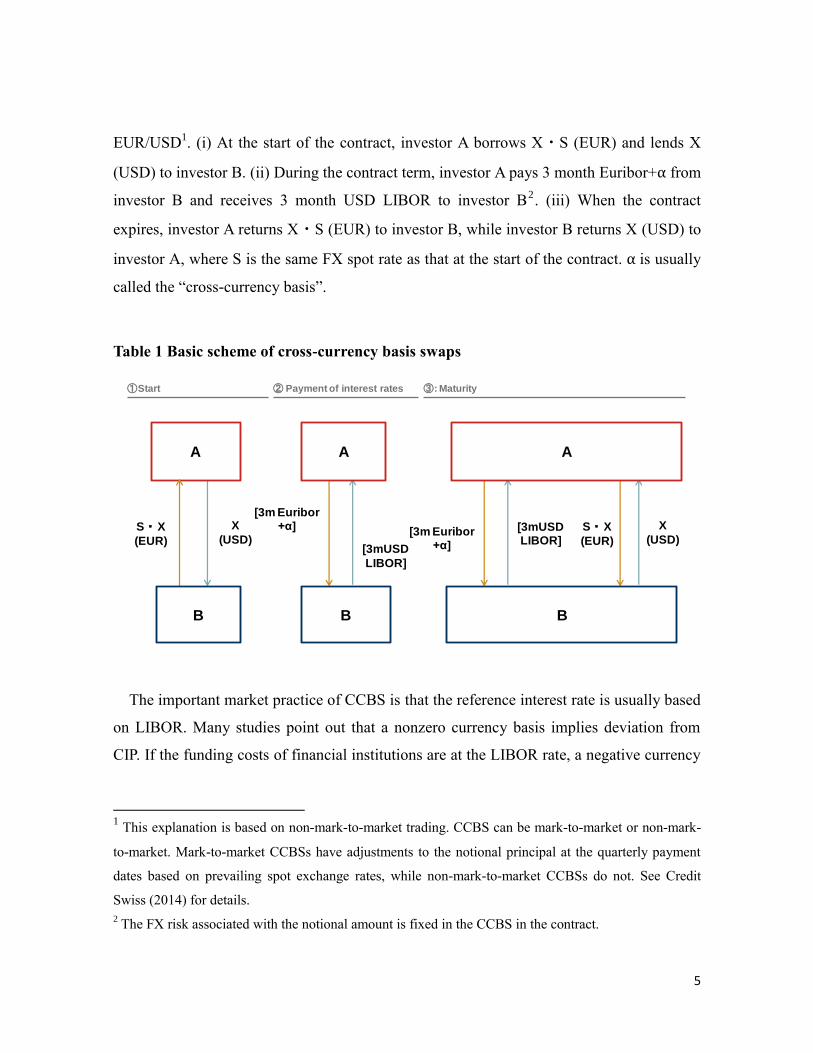

2.1. Cross-currency basis swap and CIP

A CCBS is a financial contract in which one party borrows a currency from another party

and simultaneously lends the same amount, at current spot rates, of a second currency to the

same party (see Baba 2009; Baba and Sakurai 2012). A CCBS is a floating for floating

exchange of interest rate payments in two different currencies. Unlike other basis swaps,

CCBSs also involve the exchange of a notional principal. The floating reference for each

leg is usually based on the three-month LIBOR.

Table 1 illustrates the cash flows when investors A and B contract a CCBS involving

5

EUR/USD1. (i) At the start of the contract, investor A borrows X・S (EUR) and lends X

(USD) to investor B. (ii) During the contract term, investor A pays 3 month Euribor+α from

investor B and receives 3 month USD LIBOR to investor B2. (iii) When the contract

expires, investor A returns X・S (EUR) to investor B, while investor B returns X (USD) to

investor A, where S is the same FX spot rate as that at the start of the contract. α is usually

called the “cross-currency basis”.

Table 1 Basic scheme of cross-currency basis swaps

The important market practice of CCBS is that the reference interest rate is usually based

on LIBOR. Many studies point out that a nonzero currency basis implies deviation from

CIP. If the funding costs of financial institutions are at the LIBOR rate, a negative currency

1 This explanation is based on non-mark-to-market trading. CCBS can be mark-to-market or non-mark-

to-market. Mark-to-market CCBSs have adjustments to the notional principal at the quarterly payment

dates based on prevailing spot exchange rates, while non-mark-to-market CCBSs do not. See Credit

Swiss (2014) for details.

2 The FX risk associated with the notional amount is fixed in the CCBS in the contract.

①Start ③: Maturity② Payment of interest rates

S・X

(EUR)

X

(USD)

[3m Euribor+α]

[3mUSD

LIBOR]

[3mUSD LIBOR]

S・X

(EUR)

X

(USD)[3m Euribor

+α]

B B

AAA

B

6

basis should provide arbitrage opportunities, causing the violation of CIP3. Considering this

context, Du et al. (2016) insist the negative currency basis should be called “LIBOR-based

covered interest parity”. However, after the financial crisis, the funding costs of financial

institutions are higher than the LIBOR rate because of the several additional costs such as

regulation costs. For example, balance sheet regulation such as the leverage ratio requires

additional capital if a financial institution increases the nonrisk asset base of its balance

sheet.

Figure 1 depicts the movement of the currency basis (α) between EUR and USD. Before

the financial crisis, the fluctuations in the currency basis around zero were small. However,

the currency basis deviated substantially and persistently from zero during the global

financial crisis and the European debt crisis. Furthermore, this graph also shows that the

currency basis is persistently negative even after the crisis, and we cannot attribute this

phenomena to the turmoil. Recently, several papers have investigated the negative basis

after the crisis. These papers try to relate this phenomenon to recent banking regulation

(Avdjieve et al. 2016; Borio et al. 2016; Du et al. 2016; Iida et al. 2016; Liao 2016; Sushko

et al. 2016).

Fig. 1 Currnecy Basis (𝛂) of cross-currency basis swaps between EUR and USD

3 See Du et al. (2016) for details.

-100

-80

-60

-40

-20

0

20

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

3year 5year 10year

7

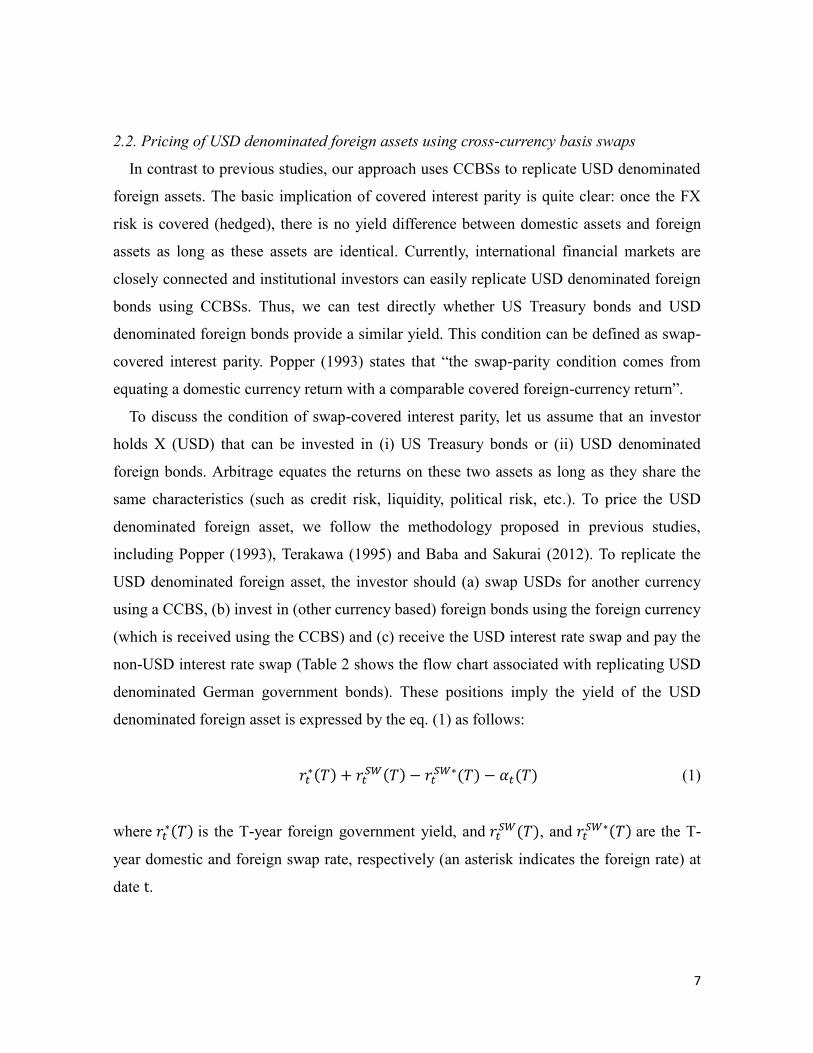

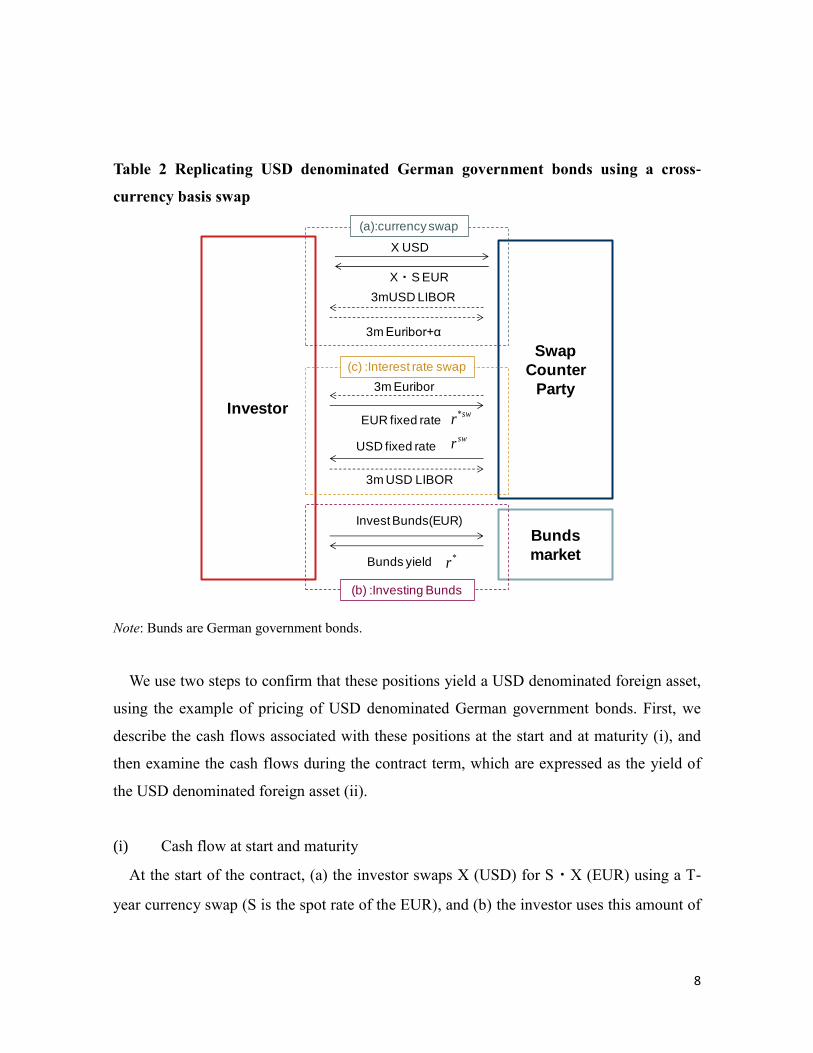

2.2. Pricing of USD denominated foreign assets using cross-currency basis swaps

In contrast to previous studies, our approach uses CCBSs to replicate USD denominated

foreign assets. The basic implication of covered interest parity is quite clear: once the FX

risk is covered (hedged), there is no yield difference between domestic assets and foreign

assets as long as these assets are identical. Currently, international financial markets are

closely connected and institutional investors can easily replicate USD denominated foreign

bonds using CCBSs. Thus, we can test directly whether US Treasury bonds and USD

denominated foreign bonds provide a similar yield. This condition can be defined as swap-

covered interest parity. Popper (1993) states that “the swap-parity condition comes from

equating a domestic currency return with a comparable covered foreign-currency return”.

To discuss the condition of swap-covered interest parity, let us assume that an investor

holds X (USD) that can be invested in (i) US Treasury bonds or (ii) USD denominated

foreign bonds. Arbitrage equates the returns on these two assets as long as they share the

same characteristics (such as credit risk, liquidity, political risk, etc.). To price the USD

denominated foreign asset, we follow the methodology proposed in previous studies,

including Popper (1993), Terakawa (1995) and Baba and Sakurai (2012). To replicate the

USD denominated foreign asset, the investor should (a) swap USDs for another currency

using a CCBS, (b) invest in (other currency based) foreign bonds using the foreign currency

(which is received using the CCBS) and (c) receive the USD interest rate swap and pay the

non-USD interest rate swap (Table 2 shows the flow chart associated with replicating USD

denominated German government bonds). These positions imply the yield of the USD

denominated foreign asset is expressed by the eq. (1) as follows:

𝑟𝑡∗(𝑇) + 𝑟𝑡

𝑆𝑊(𝑇) − 𝑟𝑡𝑆𝑊∗(𝑇) − 𝛼𝑡(𝑇) (1)

where 𝑟𝑡∗(𝑇) is the T-year foreign government yield, and 𝑟𝑡

𝑆𝑊(𝑇), and 𝑟𝑡𝑆𝑊∗(𝑇) are the T-

year domestic and foreign swap rate, respectively (an asterisk indicates the foreign rate) at

date t.

8

Table 2 Replicating USD denominated German government bonds using a cross-

currency basis swap

Note: Bunds are German government bonds.

We use two steps to confirm that these positions yield a USD denominated foreign asset,

using the example of pricing of USD denominated German government bonds. First, we

describe the cash flows associated with these positions at the start and at maturity (i), and

then examine the cash flows during the contract term, which are expressed as the yield of

the USD denominated foreign asset (ii).

(i) Cash flow at start and maturity

At the start of the contract, (a) the investor swaps X (USD) for S・X (EUR) using a T-

year currency swap (S is the spot rate of the EUR), and (b) the investor uses this amount of

Investor

Swap

Counter

Party3m Euribor

EUR fixed rate

Bunds

market

3mUSD LIBOR

3m Euribor+α

(c) :Interest rate swap

X・S EUR

X USD

(a):currency swap

3m USD LIBOR

USD fixed rate

Bunds yield

Invest Bunds(EUR)

swr*

swr

*r

(b) :Investing Bunds

9

cash (S・X) to invest in T-year German government bonds. T-years later, the investor

receives S・X because the T-year bond has reached maturity, and the currency swap

enables the investor to swap S・X (EUR) for X (USD). These cash flows are strictly the

same as a USD denominated bond (the investor invests X (USD) at the start and receives X

(USD) at maturity).

(ii) Cash flow during the contract term

During the contract term of the CCBS, the investor receives [3-month USD LIBOR] and

pays [3-month EUR LIBOR+α(T)] (these cash flows are expressed as [3-month USD

LIBOR – (3-month EUR LIBOR+α(T))]). Because the interest rates exchanged in the

CCBS are floating rates, we convert the floating rates into fixed rates via interest rate swaps

to make this position similar to the fixed income security: the investor receives the T-year

USD interest rate swap (the rate is 𝑟𝑡𝑆𝑊(𝑇)) and pays the T-year EUR interest rate swap

(the rate is 𝑟𝑡𝑆𝑊∗(𝑇))

4. In addition, the investor also earns the yield of German government

bonds (𝑟𝑡∗(𝑇)) by holding them. Thus, these cash flows are expressed in eq. (1).

As described previously, if the quality of the USD foreign bond is the same as the US

Treasury bond, arbitrage equates the returns on these two bonds. In other words, we can

write the swap-covered interest parity condition as follows:

𝑟𝑡(𝑇) = (𝑟𝑡∗(𝑇) + 𝑟𝑡

𝑆𝑊(𝑇) − 𝑟𝑡𝑆𝑊∗(𝑇) − 𝛼𝑡(𝑇)) (2)

Because eq. (2) is not expected to hold perfectly, the deviation from swap-covered

interest parity can be defined as follows:

Deviation = 𝑟𝑡(𝑇) − (𝑟𝑡∗(𝑇) + 𝑟𝑡

𝑆𝑊(𝑇) − 𝑟𝑡𝑆𝑊∗(𝑇) − 𝛼𝑡(𝑇)) (2)’

4 In a CCBS contract, the amount of the future principal payment is fixed at the start of the contract.

Thus, the investor can hedge the FX risk during the contract term.

10

The next section shows that the deviation from this condition has decreased dramatically

after the financial crisis.

2.3. Focus on USD denominated German government bonds

An important premise of swap-covered interest parity is that (i) US Treasury bond and

(ii) USD denominated foreign asset should be identical. For CIP to hold strictly depends on

negligible transaction costs, as well as a lack of political risk, counterparty risk, credit risk

(sovereign risk), liquidity risk and measurement error (Aliber, 1973; Baba and Packer

2009).

As Fong et al. (2010) points out, market liquidity and credit risk are particularly

important in the context of CIP arbitrage. In terms of these points, we compare the yield of

USD denominated German government bonds with the yield of US Treasury bonds. First,

German government bonds are one of the safest assets among the advanced countries in

terms of credit rating and sovereign CDS premium. Second, EUR denominated OTC

derivatives (CCBSs and interest rate swaps) are one of the most liquid OTC derivatives

according to the survey of the Bank for International Settlements (see BIS, 2016). Table 3

shows the turnover of CCBSs and interest rate swaps in 2016/4, with the EUR being the

second most actively traded derivatives after the USD.

2.4. Data description

The empirical analysis performed in this paper uses data including the par rate of US

Treasury bonds and German government bonds, USD and EUR interest rate swaps, and

CCBSs for the EUR/USD pair. The condition of swap-covered interest parity (eq. (2)) is

examined for assets with maturities of three, five and 10 years. We use the prices of CCBSs

and interest rate swaps provided by Bloomberg. We obtain the par rate of US Treasury

bonds from Bloomberg although the par rate of German government bonds is estimated by

the Bundesbank5.

5 The par rate on German government bonds provided by Bloomberg contains many missing values.

11

Table 3 Turnover of cross-currency basis swaps and interest rate swaps (2016/4)

Currency swaps Interest Rate

Swaps All currencies US dollar against

1 USD 73.82 EUR 17.88 USD 898.44

2 EUR 22.29 JPY 17.42 EUR 444.69

3 JPY 18.12 GBP 8.34 GBP 138.06

4 GBP 10.36 AUD 6.74 AUD 104.63

5 AUD 7.05 TRY 4.08 JPY 75.74

6 CAD 4.26 CAD 4.04 CAD 37.86

7 TRY 4.16 CNY 2.53 NZD 25.73

8 ZAR 3.54 SGD 1.71 MXN 25.47

9 CNY 2.62 BRL 1.67 KRW 11.96

10 SGD 1.75 CHF 1.38 SGD 11.86

11 CHF 1.70 NZD 1.21 NOK 11.12

12 BRL 1.70 KRW 1.03 CNY 10.06

13 NZD 1.26 HKD 1.03 CHF 8.91

14 HKD 1.14 SEK 0.60 SEK 8.66

15 KRW 1.05 RUB 0.54 BRL 6.58

16 SEK 0.87 NOK 0.42 INR 5.64

17 NOK 0.59 ZAR 0.32 HKD 5.23

18 RUB 0.55 INR 0.30 CLP 4.19

19 PLN 0.37 PLN 0.26 HUF 3.77

20 INR 0.30 MXN 0.16 MYR 3.12

Note: USD billion. Source: BIS.

We use the pre-CVA (credit value adjustment) value of OTC derivatives (CCBSs and

interest rate swaps), enabling the counterparty risk to be eliminated sufficiently. As Baba

and Sakurai (2012) describes, CCBSs can be viewed as effectively collateralized contracts,

although the collateral does not completely cover all of the counterparty risk. After the

financial crisis, many financial institutions set up CVA desks (see Gregory, 2015) and they

now take account of the counterparty risk by pricing CVAs, which reflect the expected loss

arising from future default by the counterparty. Because of this market practice, the

12

derivative price can be clearly separated into CVA (counterparty risk part) and the

remaining part of the derivative value (pre-CVA value). Thus, after the financial crisis, we

can eliminate counterparty risk as long as we use the pre-CVA value.

We do make one adjustment to the swap rate. The price of CCBSs for the EUR/USD pair

is based on the 3-month Euribor against the 3-month USD LIBOR, although the major

interest reference rate of the EUR swap rate is 6-month Euribor. Thus, we replicate EUR

interest rate swaps linked to the 3-month Euribor using the 3-month/6-month tenor swap

(please see Appendix for details of the tenor swap and the replication).

3. Deviation from swap-covered interest parity: Comparison between US Treasury

bonds and USD denominated German government bonds

3.1. Empirical results

This section compares the deviation from swap covered interest parity before and after

the financial crisis. Figure 2 plots the time series variation of the yield of US Treasury

bonds and USD denominated German government bonds for maturities of three, five and

10 years from 2001/1 to 2016/12. This graph shows each of these yields and their spread.

The behavior of the spread can be summarized as follows. First, the deviations of these

yields decreased persistently from 2001 to 2016. This is partly because the liquidity of

CCBSs has increased (BIS (2016) shows that the turnover of CCBSs increased from 8,139

million USD (2007) to 17,881 million USD (2016) on a daily average basis). Second, the

deviation was much larger during the financial crisis. This suggests that the turmoil

prevented arbitrage activity, and this is consistent with previous studies (see Baba and

Packer 2009; Baba and Sakurai 2012, among others).

Table 4 summarizes the yield deviation between US Treasury bonds and USD

denominated German government bonds, as well as the currency basis (𝛼𝑡) before and after

the financial crisis. As Popper (1993) points out, the mean could be a misleading statistic

because the mean could be deceptively close to zero even if large individual deviations of

opposite signs offset one another in the sample period. Thus, we focus on the mean absolute

deviations (MAD) instead of the mean deviation.

13

Fig. 2 Comparison of the yields of USD based Treasury and USD denominated

German government bonds

Note: USD UST is US Treasury bonds and USD Bunds is USD denominated German government bonds.

The difference is the spread of USD UST and USD Bunds.

-2

-1

0

1

2

3

4

5

6

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Difference

USD UST(3year)

USD Bunds(3year)

-2

-1

0

1

2

3

4

5

6

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Difference

USD UST(5year)

USD Bunds(5year)

-2

-1

0

1

2

3

4

5

6

7

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Difference

USD UST(10year)

USD Bunds(10year)

14

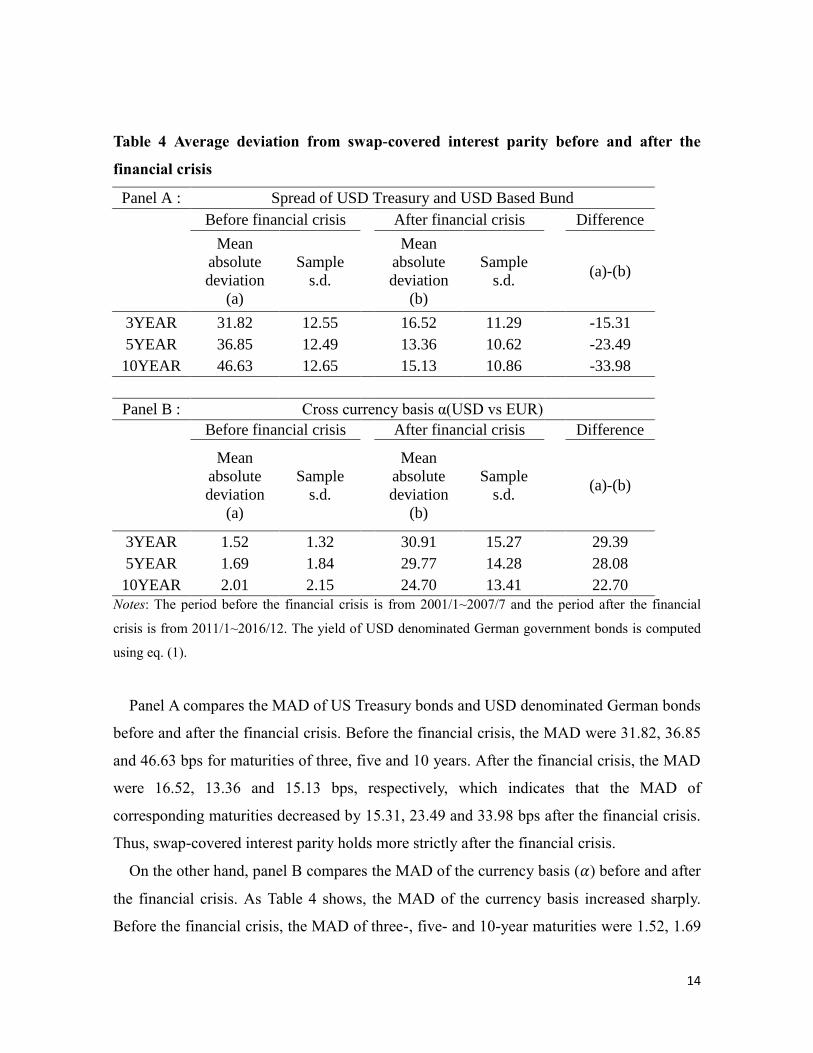

Table 4 Average deviation from swap-covered interest parity before and after the

financial crisis

Panel A : Spread of USD Treasury and USD Based Bund

Before financial crisis After financial crisis Difference

Mean

absolute

deviation

(a)

Sample

s.d.

Mean

absolute

deviation

(b)

Sample

s.d. (a)-(b)

3YEAR 31.82 12.55 16.52 11.29 -15.31

5YEAR 36.85 12.49 13.36 10.62 -23.49

10YEAR 46.63 12.65 15.13 10.86 -33.98

Panel B : Cross currency basis α(USD vs EUR)

Before financial crisis After financial crisis Difference

Mean

absolute

deviation

(a)

Sample

s.d.

Mean

absolute

deviation

(b)

Sample

s.d. (a)-(b)

3YEAR 1.52 1.32 30.91 15.27 29.39

5YEAR 1.69 1.84 29.77 14.28 28.08

10YEAR 2.01 2.15 24.70 13.41 22.70

Notes: The period before the financial crisis is from 2001/1~2007/7 and the period after the financial

crisis is from 2011/1~2016/12. The yield of USD denominated German government bonds is computed

using eq. (1).

Panel A compares the MAD of US Treasury bonds and USD denominated German bonds

before and after the financial crisis. Before the financial crisis, the MAD were 31.82, 36.85

and 46.63 bps for maturities of three, five and 10 years. After the financial crisis, the MAD

were 16.52, 13.36 and 15.13 bps, respectively, which indicates that the MAD of

corresponding maturities decreased by 15.31, 23.49 and 33.98 bps after the financial crisis.

Thus, swap-covered interest parity holds more strictly after the financial crisis.

On the other hand, panel B compares the MAD of the currency basis (𝛼) before and after

the financial crisis. As Table 4 shows, the MAD of the currency basis increased sharply.

Before the financial crisis, the MAD of three-, five- and 10-year maturities were 1.52, 1.69

15

and 2.01 bps, respectively, although the corresponding MAD were 30.91, 29.77 and 24.70

bps after the crisis, indicating the MAD had increased by about 30 bps. This result is in

sharp contrast to the fact that the deviation from swap-covered CIP had decreased

drastically.

3.2. USD denominated foreign bonds as avoidance of regulation costs

Our results indicate that deviations from swap-covered interest parity have decreased

significantly after the financial crisis. This result is in sharp contrast with previous studies

finding that the deviation from CIP persisted after the crisis. However, our results are

consistent with previous studies in regards to how banking regulation affects financial and

nonfinancial institutions.

The regulatory reforms have significantly increased financial institutions’ balance sheet

costs associated with arbitrage. In particular, nonrisk weighted capital requirements, such as

the leverage ratio, require additional equity capital when financial institutions increase their

notional holdings of derivatives. According to standard asset pricing theory, the funding

cost of equity is substantially higher than interest payments such as LIBOR; therefore, the

cost of banking regulation can deviate from LIBOR based CIP when the funding cost is not

equal to LIBOR. In other words, the deviation could disappear if we compute CIP based on

the actual funding cost of the financial institution; but the difficulty is that regulation costs

are not easy to observe.

The advantage of our approach is that nonfinancial companies can invest in USD

denominated German government bonds through mutual funds or structured products. In

other words, we can see the USD denominated bonds can be used to avoid regulation costs,

because nonfinancial institutions, which are not subject to banking regulations, can take

part in OTC derivative markets indirectly. In fact, recent market practices such as the Credit

Support Annex (CSA) have increased the participation cost of OTC derivative markets and,

therefore, nonfinancial institutions are basically unable to participate in CCBS markets

directly (or the participation of nonfinancial institutions in OTC derivative markets is

limited, therefore there is an opportunity to arbitrage away the deviation of LIBOR based

16

CIP).

One possible concern is that the nonfinancial institutions end up making a contract

involving a CCBS with a financial institution through a fund or special purpose company

(SPC) with USD denominated bonds, and this increases the balance sheet cost of the

financial institution. However, financial institutions only play the role of market maker as

long as the nonfinancial institutions invest in USD denominated bonds, and the financial

institutions can hedge this position using an opposite contract that allows them to cancel

out the balance sheet cost by compression. Furthermore, current banking regulations allow

banks to offset their balance sheet cost partially when they hedge their position effectively6.

4. Estimation

4.1. Cointegration analysis of currency basis (𝛼)

This section examines the movement of the currency basis (𝛼𝑡) based on eq. (2), which

can be expressed as follows:

𝛼𝑡(𝑇) = 𝑟𝑡𝑆𝑊(𝑇) − 𝑟𝑡(𝑇) − (𝑟𝑡

𝑆𝑊∗(𝑇) − 𝑟𝑡∗(𝑇)) (3)

This equation shows that the currency basis is determined by (i) the domestic swap

spreads ( 𝑟𝑡𝑆𝑊(𝑇) − 𝑟𝑡(𝑇) ) and (ii) the foreign swap spreads ( 𝑟𝑡

𝑆𝑊∗(𝑇) − 𝑟𝑡∗(𝑇) ). To

examine how 𝛼(𝑇) is empirically related to the swap spreads, we interpret eq. (3) as

follows:

𝛼𝑡(𝑇) = 𝛿 + 𝛽(𝑟𝑡𝑆𝑊(𝑇) − 𝑟𝑡(𝑇)) + 𝛾(𝑟𝑡

𝑆𝑊∗(𝑇) − 𝑟𝑡∗(𝑇)) + 휀𝑡 (4)

where 𝛿 is some constant, 𝛽 and 𝛾 are coefficients reflecting the swap spreads, and 휀𝑡 is an

error term.

If 𝛼𝑡(𝑇), 𝑟𝑡𝑆𝑊(𝑇) − 𝑟𝑡(𝑇), 𝑟𝑡

𝑆𝑊∗(𝑇) − 𝑟𝑡∗(𝑇) are I (1) processes, then (3) implies that

6 See BIS (2014) for details.

17

they are cointegrated. This regression method is similar to the cointegration analysis

commonly used to test purchasing power parity (PPP). In the PPP literature, disturbances

such as transaction costs and taxes should realistically cause deviations from the strong

form of PPP, so the model has been generalized in a parameteric form instead of imposing

unity/zero restrictions on the parameters (see Patel 1990; Cheung and Lai 1993;

MacDonald 1993, among others).

We focus on the “swap spreads” instead of the swap rate or bond yield. This is because

we interpret the swap spreads as a proxy of the balance sheet cost for explaining the

currency basis from eq. (4). The swap spreads have tightened drastically and “negative

swap spreads” emerged in longer maturity bonds after the financial crisis. Figure 3 depicts

the time series of swap spreads. This graph shows that the USD swap spreads tightened

drastically after the financial crisis and 5- and 10-year spreads have become negative,

which is challenging for the standard asset pricing model. On the other hands, EUR swap

spread has been positive and relatively stable especially after 2013. Recent studies have

analyzed the effect of banking regulations on swap spreads and found that balance sheet

costs could cause the negative currency basis spreads (see Jermann 2016; Klinger and

Sundaresan 2016), and this implies the balance sheet cost can have a negative impact on the

swap spreads and the currency basis simultaneously.

We use the same data as used in Section 3, where 𝛼𝑡(𝑇) is the cross-currency basis for

the EUR/USD pair, 𝑟𝑡𝑆𝑊(𝑇) − 𝑟𝑡(𝑇) is the USD swap spreads (the difference between the

USD swap rate and the par rate on US Treasury bonds) and 𝑟𝑡𝑆𝑊∗(𝑇) − 𝑟𝑡

∗(𝑇) is the EUR

swap spreads (the difference between the EUR swap spreads and the par rate of German

government bonds). The maturities are three, five and 10 years (𝑠 = 3,5,10).

Our analysis is from 2011/1 to 2016/12, because we exclude the effect of counterparty

risk (the market practice of pricing CVA has been widespread after the financial crisis as

described in Section 3). The pre CVA value is used to control for counterparty risk.

18

Fig. 3 Time series of swap spreads

USD swap spreads

EUR swap spreads

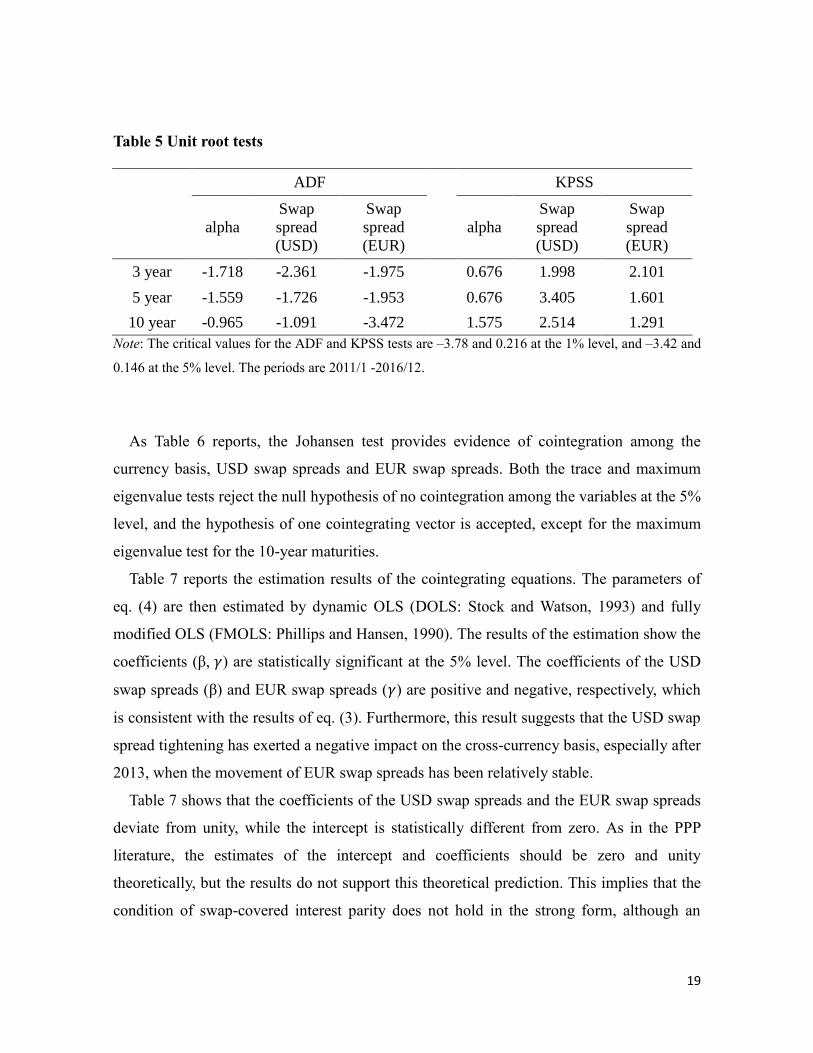

4.2. Estimation results

First, we examine whether the time series of the currency basis and swap spreads are unit

root processes, using the augmented Dickey–Fuller (ADF) and Kwiatkowski, Phillips,

Schmidt, and Shin (1992, KPSS) tests. The results of these unit root tests, reported in Table

5, indicate strong evidence that these series contain unit root processes (except the ADF test

for the 10-year EUR swap spreads).

-30-20-10

0102030405060

11 12 13 14 15 16

3year

5year

10year

(bps)

-20

0

20

40

60

80

100

120

11 12 13 14 15 16

3year

5year

10year

(bps)

19

Table 5 Unit root tests

ADF KPSS

alpha

Swap

spread

(USD)

Swap

spread

(EUR)

alpha

Swap

spread

(USD)

Swap

spread

(EUR)

3 year -1.718 -2.361 -1.975 0.676 1.998 2.101

5 year -1.559 -1.726 -1.953 0.676 3.405 1.601

10 year -0.965 -1.091 -3.472 1.575 2.514 1.291

Note: The critical values for the ADF and KPSS tests are –3.78 and 0.216 at the 1% level, and –3.42 and

0.146 at the 5% level. The periods are 2011/1 -2016/12.

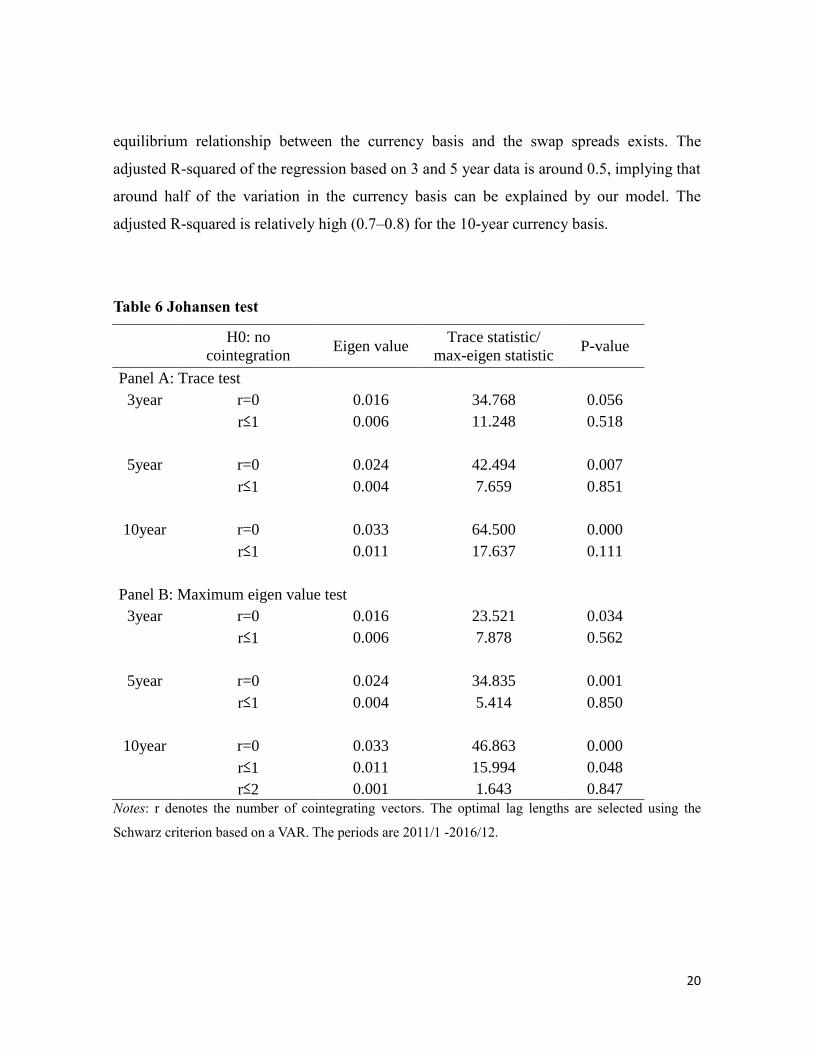

As Table 6 reports, the Johansen test provides evidence of cointegration among the

currency basis, USD swap spreads and EUR swap spreads. Both the trace and maximum

eigenvalue tests reject the null hypothesis of no cointegration among the variables at the 5%

level, and the hypothesis of one cointegrating vector is accepted, except for the maximum

eigenvalue test for the 10-year maturities.

Table 7 reports the estimation results of the cointegrating equations. The parameters of

eq. (4) are then estimated by dynamic OLS (DOLS: Stock and Watson, 1993) and fully

modified OLS (FMOLS: Phillips and Hansen, 1990). The results of the estimation show the

coefficients (β, 𝛾) are statistically significant at the 5% level. The coefficients of the USD

swap spreads (β) and EUR swap spreads (𝛾) are positive and negative, respectively, which

is consistent with the results of eq. (3). Furthermore, this result suggests that the USD swap

spread tightening has exerted a negative impact on the cross-currency basis, especially after

2013, when the movement of EUR swap spreads has been relatively stable.

Table 7 shows that the coefficients of the USD swap spreads and the EUR swap spreads

deviate from unity, while the intercept is statistically different from zero. As in the PPP

literature, the estimates of the intercept and coefficients should be zero and unity

theoretically, but the results do not support this theoretical prediction. This implies that the

condition of swap-covered interest parity does not hold in the strong form, although an

20

equilibrium relationship between the currency basis and the swap spreads exists. The

adjusted R-squared of the regression based on 3 and 5 year data is around 0.5, implying that

around half of the variation in the currency basis can be explained by our model. The

adjusted R-squared is relatively high (0.7–0.8) for the 10-year currency basis.

Table 6 Johansen test

H0: no

cointegration Eigen value

Trace statistic/

max-eigen statistic P-value

Panel A: Trace test

3year r=0 0.016 34.768 0.056

r≤1 0.006 11.248 0.518

5year r=0 0.024 42.494 0.007

r≤1 0.004 7.659 0.851

10year r=0 0.033 64.500 0.000

r≤1 0.011 17.637 0.111

Panel B: Maximum eigen value test

3year r=0 0.016 23.521 0.034

r≤1 0.006 7.878 0.562

5year r=0 0.024 34.835 0.001

r≤1 0.004 5.414 0.850

10year r=0 0.033 46.863 0.000

r≤1 0.011 15.994 0.048

r≤2 0.001 1.643 0.847

Notes: r denotes the number of cointegrating vectors. The optimal lag lengths are selected using the

Schwarz criterion based on a VAR. The periods are 2011/1 -2016/12.

21

Table 7 Dynamic OLS and fully modified OLS estimates

DOLS FMOLS

δ β γ R2 δ β γ R

2

3year

-0.0734 0.5406 -0.9921 0.5336 -0.0827 0.7540 -1.0752 0.4945

(-3.85) (4.17) (-11.95) (-1.49) (2.05) (-4.61)

5year

-0.0600 0.8850 -1.1224 0.5336 -0.0559 0.9769 -1.1734 0.4323

(-3.05) (9.87) (-14.54) (-1.22) (4.72) (-6.74)

10year

-0.1519 0.4706 -0.7857 0.7901 -0.1765 0.5596 -0.6714 0.6914

(-15.74) (9.81) (-17.75) (-8.98) (5.45) (-7.64)

Notes: For the FMOLS estimates, the long-run variance is estimated by a QS kernel and the bandwidth is

chosen using the Andrews procedure. For the DOLS estimates, the Newey and West (1987) technique is

used. The number of leads and lags is selected using the Schwarz criterion for dynamic OLS. The figures

in parentheses are t-statistics. The periods are 2011/1 -2016/12.

5. Conclusion

This paper compares US Treasury bonds and USD denominated German bonds and

shows that the deviation between these yields has decreased drastically. Therefore, the

analysis in this paper concludes that the condition of swap-covered interest parity has been

satisfied more stringently after the financial crisis, although the negative currency basis

seems to contradict the arbitrage-free environment. We reconcile our results with previous

studies and provide two possible reasons for our results. First, the balance sheet cost

simultaneously causes the negative currency basis and swap spread tightening, so the

condition of swap-covered interest parity, which links the currency basis with the swap

spreads, has not deteriorated after the financial crisis. Second, USD denominated foreign

bonds can be used to avoid banking regulations because nonfinancial institutions use

arbitrage in OTC derivative markets through mutual funds or structured notes.

We interpret the condition of swap-covered interest parity as suggesting a cointegrating

relationship. The results show that the equilibrium relationship exists and the negative

currency basis is significantly related to the USD swap spread tightening. The advantage of

22

our approach compared with previous studies is to treat the term structure of the cross-

currency basis explicitly. Our model can account for about half of the currency basis

variations in short and middle maturities, while the explanatory power increases to around

70–80% for longer maturities.

Appendix: Tenor swaps

A tenor swap exchanges two floating rate payments of the same currency based on

different tenor indices (the notional is not exchanged)7. Table A1 shows a typical tenor

swap swapping [3-month LIBOR + 𝜇(𝑇)] and [6-month LIBOR]. We use a tenor swap to

replicate the EUR interest rate linked to the 3-month LIBOR, using EUR interest rate

linked to the 6-month LIBOR. Figure 1A shows the time series of the tenor swap

exchanging 3-month LIBOR with 6-month LIBOR.

According to the arbitrage pricing principle, two floating rates of different tenors should

trade flat in a swap contract because floating rate bonds are always worth the par value at

initiation, regardless of the tenor length (see Chang and Schlogl, 2014). Thus, in this case,

the basis spread should be zero to avoid arbitrage profit. Before the crisis, a small spread (in

general, several basis points) was usually added to the shorter tenor rate. However, the basis

has been wider during and after the crisis

To replicate the T-year interest rate swap linked to 3-month LIBOR using the T-year

interest rate swap linked to 6-month LIBOR, we (1) receive the T-year interest rate linked

to 6-month LIBOR and pay [6-month LIBOR] and (2) pay [3-month LIBOR + 𝜇(𝑇)] and

receive [6-month LIBOR] by means of a tenor swap. Table 2A describes the cash flows of

these positions. We price the T-year swap rate linked to 3-month LIBOR using the

following equation.

𝑟𝑆𝑊,3𝑚(𝑇) = 𝑟𝑆𝑊,6𝑚(𝑇) − 𝜇(𝑇) ⋯ (5)

7 The description of the tenor swap is basically based on Chang and Schlogl (2014).

23

where 𝜇(𝑇) is the basis spread of the T-year tenor swap, and 𝑟𝑆𝑊,3𝑚(𝑇) and 𝑟𝑆𝑊,6𝑚(𝑇) are

the T-year swap rate linked to 3-month LIBOR and 6-month LIBOR, respectively.

We use data for 𝜇(𝑇) from 2003/7/28, and we set 𝜇(𝑇) equal to zero before this date. In

addition, we linearly interpolate for any missing data after this date.

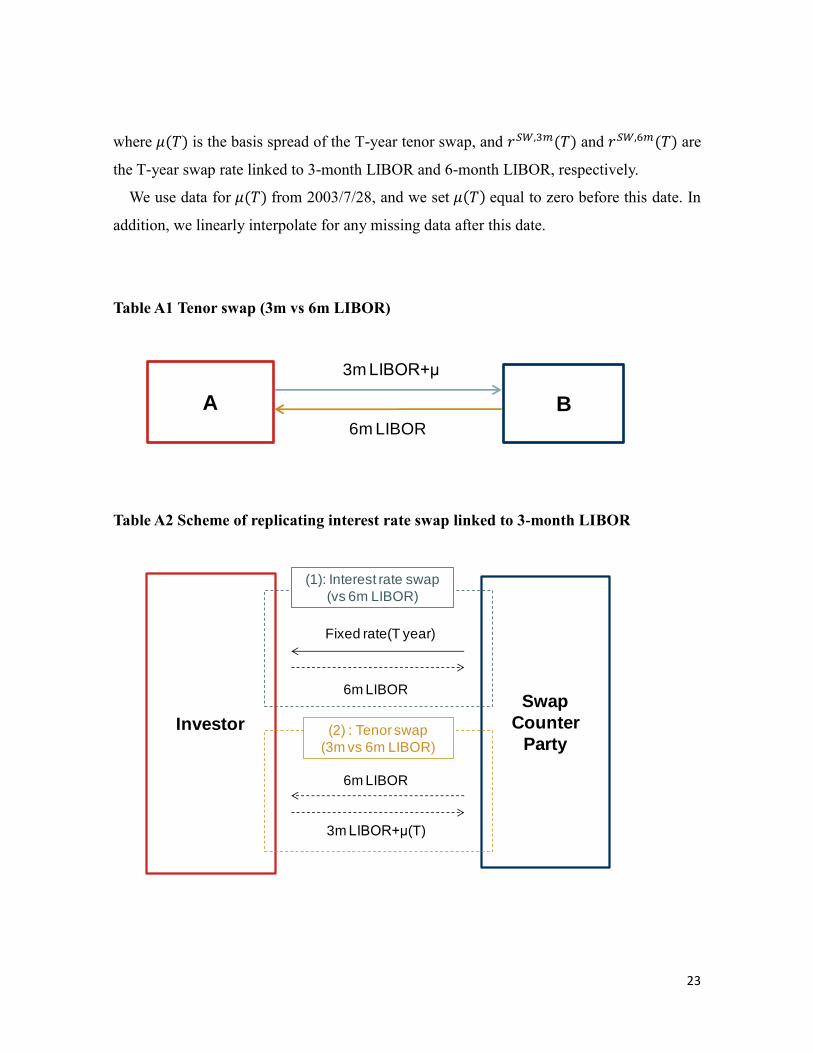

Table A1 Tenor swap (3m vs 6m LIBOR)

Table A2 Scheme of replicating interest rate swap linked to 3-month LIBOR

A

3m LIBOR+μ

6m LIBOR

B

Investor

Swap

Counter

Party

6m LIBOR

(2) : Tenor swap

(3m vs 6m LIBOR)

Fixed rate(T year)

6m LIBOR

(1): Interest rate swap

(vs 6m LIBOR)

3m LIBOR+μ(T)

24

Fig. A1 Time series of 3m vs 6m tenor swaps: EUR

-5

0

5

10

15

20

25

30

03 04 05 06 07 08 09 10 11 12 13 14 15 16

3 year

5year

10 year

(bps)

25

References

Aliber, R. Z., 1973. The interest rate parity theorem: a reinterpretation. Journal of Political

Economy. 81 (6), 1451–1459.

Avdjiev, S., Du, W., Koch, C., Shin, H., 2016. The dollar, bank leverage and the deviation

from covered interest parity. BIS Working Papers No 592.

Baba, N., 2009. Dynamic spillover of money market turmoil from FX swap to cross

currency swap markets: evidence from the 2007 to 2008 turmoil. Journal of Fixed

Income 18, 24–38.

Baba, N., Packer, F., 2009. From turmoil to crisis: dislocation in the FX swap market before

and after the failure of Lehman Brothers. Journal of International Money and

Finance 28, 1350–1374.

Baba, N., Packer, F., Nagano, T., 2008. The spillover of money market turbulence to FX

swap and cross-currency swap markets. BIS Quarterly Review, March, 73–86.

Baba, N., Sakurai, Y., 2012. When and how US dollar shortages evolved into the full crisis?

Evidence from the cross-currency swap market. Journal of Banking and Finance

35(6), 1450–1463.

Bank for International Settlements, 2014. Basel III leverage ratio framework and disclosure

requirements.

Bank for International Settlements, 2016. Triennial Central Bank Survey of Foreign

Exchange and OTC Derivatives Markets in 2016.

Borio, C., McCauley, R., McGuire, P., Susuko, V., 2016. Covered interest parity lost:

understanding the cross-currency basis. BIS Quarterly Review.

Chang, Y., Schlogl, E., 2014. A consistent framework for modelling basis spreads in tenor

swap. Quantitative Finance Research Centre Research Paper 348.

Cheung, Y., Lai, K., 1993. Finite-sample sizes of Johansen’s likelihood ratio tests for

cointegration. Oxford Bulletin of Economics and Statistics 55(3), 313–328.

Coffey, N., Hrung, W. B., Sarkar, A., 2009. Capital constraints, counterparty risk, and

deviations from covered interest rate parity. Federal Reserve Bank of New York

Staff Report 393.

26

Credit Swiss, 2014. Credit Suisse Basis Points: Cross-Currency Basis Swaps.

Du, W., Tepper, A., Verdelhan, A., 2016. Deviations from covered interest rate parity.

Working Paper.

Fletcher, D., Taylor, L.W., 1996. Swap covered interest parity in long-date capital market.

Review of Economics and Statistics 78, 530–538.

Fong, W., Valente, G., Fung, 2010. Covered interest arbitrage profits: The role of liquidity

and credit risk. Journal of Banking and Finance 34(5), 1098–1107.

Gregory, J., 2015. The xVA Challenge: Counterparty Credit Risk, Funding, Collateral, and

Capital, 3rd Edition. Wiley.

Griffolli, M.T., Ranaldo, A. 2011. Limits to Arbitrage during the Crisis: Funding Liquidity

Constraints and Covered Interest Parity. Swiss National Bank Working Papers 2010-

14.

Iida, T., Kimura, T., Sudo, N., 2016. Regulatory reforms and the dollar funding of global

banks: Evidence from the impact of monetary policy divergence. Bank of Japan

Working Paper Series 16-E-14.

Ivashina,V., Scharstein, D.S., Stein, J.C., 2015. Dollar funding and the lending behavior of

global banks. Quarterly Journal of Economics. 130(3), 1241–1281.

Jermann, U. 2016. Negative swap spreads and limited arbitrage. Discussion Paper.

Klingler, S., Sundaresan, S., 2016. An explanation of negative swap spreads: Demand for

duration from underfunded pension plans. Discussion Paper.

Kwiatkowski, D., Phillips, P., Schmidt, O., Shin,Y., 1992. Testing the null hypothesis of

stationarity against the alternative of a unit root: How sure are we that economic

time series have a unit root? Journal of Econometrics 54(1-3), 159–178.

Liao, G., 2016. Credit migration and covered interest rate parity. Discussion Papers.

Harvard Business School.

MacDonald, R., 1993. Long-run purchasing power parity: Is it for real? Review of

Economics and Statistics 75(4), 690–695.

Newey, W.K., West, K.D., 1987. A simple, positive semi-definite, heteroscedasticity and

autocorrelation consistent covariance matrix. Econometrica 55, 703–708.

27

Patel, J., 1990. Purchasing power parity as a long-run relation. Journal of Applied

Econometrics 5(4), 367–379.

Phillips, P.C.B., Hansen, B.E., 1990. Statistical inference in instrumental variables

regression with I(1) processes. The Review of Economic Studies 57, 99–125.

Popper, H., 1993. Long-term covered interest parity: evidence from currency swaps.

Journal of International Money and Finance 12, 439–448.

Stock, J.H., Watson, M.W., 1993. A simple estimator of cointegrating vectors in higher

order integrated systems. Econometrica 61, 783–820.

Sushko, V., Borio, C., McCauley, R., McGuire, P., 2016. The failure of covered interest

parity: FX hedging demand and costly balance sheets. BIS Working Papers No 590.

Terakawa, N., 1995. Currency swaps and long-term covered interest parity. Economics

Letters 49, 181–185.