domestic attitudes toward debt repayment: public …tomz/working/argsvy-old.pdf · philadelphia...

TRANSCRIPT

Domestic Attitudes Toward Debt Repayment: Public Opinion and Economic Sophistication in Argentina

Michael Tomz Stanford University [email protected]

Version: August 2003

Preliminary Comments Welcome!

Prepared for presentation at the annual meetings of the American Political Science Association, Philadelphia Mariott Hotel, Philadelphia, PA, August 27-31, 2003. I am grateful for financial support from the Center for Latin American Studies at Stanford University, for superb research assistance by Sarah Dix and Diego Miranda, and for fieldwork by the polling firm of Carlos Fara y Asoc., which administered the survey on which this research is based. I thank Bill Clark, Jeff Frieden, Leslie Johns and Kathleen O'Neill for excellent comments, only some of which I have been able to address in the current draft.

1

Abstract This paper offers the first systematic analysis of mass public opinion regarding debt default. The research, which draws on a unique survey of Argentine public opinion, supports two conclusions. First, the preferences of individual Argentines followed a clear pattern that depended on their objective position in the economy and their views about financial flows that a default would disrupt. Other factors equal, those employed in the public sector, those who were unemployed or at risk of losing their jobs, and those who doubted the value of future capital inflows tended to favor default. Second, the effect of economic circumstances was strongest for the most sophisticated portion of the electorate. The paper develops this point by employing several measures of economic sophistication, and recommends that similar measures be incorporated into future research on economic policymaking.

2

1. Introduction

For centuries the international financial system has experienced periodic and traumatic

debt crises. Governments throughout the world – and especially in developing regions – have

failed to pay their foreign creditors in full and on time, and have thus slipped into default on their

external obligations. The most spectacular declaration of financial insolvency involved the

Argentine government, which suspended service on nearly $100 billion in foreign bonds in

January 2002, triggering the largest default in international financial history. But the Argentine

decision, though unprecedented in magnitude, represents only the latest entry in a litany of

defaults by sovereign governments since the 1700s.

Despite the significance of these events, we have only a partial understanding of the

domestic political factors that lead some governments to repay their foreign debts and others to

default. Inspired by the Latin American debt crisis of the 1980s, an important body of literature

explored the effects of business groups and labor unions on debt rescheduling (e.g. Frieden 1988,

1991; Haggard and Kaufman 1992; Kaufman 1988; Nelson 1990), but existing work has devoted

much less attention to the demands of voters. Over the years, those demands have gained

increasing salience as many developing countries have completed the transition from

authoritarianism to democracy. Today, an adequate understanding of debt policy must take the

preferences of the electorate into account.

This paper builds on existing work in two ways. It offers the first systematic analysis of

mass public opinion regarding debt default. The empirical investigation centers on a unique

survey of Argentine public opinion in June 2002. Data from this survey reveal why some voters

favor repayment whereas others oppose it, and help identify the economic and political factors

that affect support for debt service. Second, this paper introduces several individual-level

3

measures of economic sophistication and shows how they interact with objective circumstances

to explain public attitudes toward the foreign debt. The measures could fruitfully be

incorporated into future studies of public attitudes on other economic issues, both domestic and

international.

Analysis of the Argentine survey supports two conclusions. First, the preferences of

individual Argentines followed a clear pattern that depended on their objective position in the

economy and their views about financial flows that a default would disrupt. Other factors equal,

those employed in the public sector, those who were unemployed or at risk of losing their jobs, and

those who doubted the value of future capital inflows tended to favor default. The discovery that

economic circumstances shape attitudes about debt default dovetails with recent work by other

scholars, who show that similar considerations affect preferences about trade policy (Baker 2003;

Mayda and Rodrik 2002; O’Rourke and Sinnott 2001; Scheve and Slaughter 2001) and welfare

spending (Alesina and La Ferrara 2001; Iversen and Soskice 2001; Luttmer 2001).

Second, the effect of economic circumstances is strongest for the most sophisticated

portion of the electorate. Voters in Argentina were not equally capable of understanding how a

policy of debt repayment might affect them personally. Those with a strong knowledge of

economic concepts and events drew the appropriate conclusions, but those with relatively little

command of economics did not recognize the implications. Consequentially, the marginal effect

of each explanatory variable in the analysis increases with the economic sophistication of the

respondent. This finding parallels work in American politics, where researchers have found that

political sophistication conditions attitudes on a wide variety of issues (Althaus 1998; Bartels

1996; Delli Carpini and Keeter 1996; Mondak 2001; Zaller 1992). The evidence in this paper

confirms that such patterns exist in the field of international political economy, as well.

4

The paper proceeds as follows. Section 2 reviews the existing literature and proposes

three sets of hypotheses to explain mass preferences regarding debt. It argues that the attitudes

of individual citizens should depend on their susceptibility to the adjustment costs and

reputational benefits of repayment, and adds that the influence of these variables should be

greatest among the most sophisticated portion of the electorate. Section 3 discusses data and

methods, Section 4 presents the results, and Section 5 concludes the paper.

2. Hypotheses about Public Attitudes toward Debt Repayment

The existing literature on sovereign debt – and on compliance with international

agreements more generally – says little about the preferences of voters and other domestic

groups. In nearly every formal model of debt, for example, an apolitical country weighs the

costs and benefits of honoring its obligations. Default involves some cost: the inability to

borrow in the future, the interruption of international trade, the severing of diplomatic ties, or

even military intervention. Default also brings a benefit: the immediate savings from not having

to transfer interest and principal to creditors. After comparing these costs and benefits, the

welfare maximizer decides whether repayment serves the interests of the country as a whole.

These models provide valuable insight into the problem of sovereign debt, but they tell

only half the story. The way a government treats its foreign creditors depends not only on

strategic interaction at the international level, but also on domestic politics. Politicians and

political parties in the developing world have long disagreed about the wisdom of debt

repayment, and in some cases the issue has assumed center stage in presidential and

congressional campaigns (Tomz 2002). One cannot reconcile this level of domestic

5

disagreement with the notion that debt is a technical and apolitical issue, or that it is highly

consensual because the winners from repayment can compensate the losers.

A handful of studies do consider the domestic politics of debt, and they provide a

foundation for theorizing about the preferences of voters. In one of the first studies along these

lines, Alesina (1988) considered why Germany, France, Italy, Great Britain and the United States

had managed their domestic-currency debt in different ways. He identified three contending

domestic groups: rentiers who held the debt of their own government, businessmen who owned

physical capital and earned profit, and workers who possessed human capital and earned wages.

According to Alesina, debt policy results from a “struggle over income and wealth distribution”

among these three competing groups and their political representatives. Other scholars have

added that democratic institutions affect whose voices get heard and when rentiers enjoy the

upper hand (North and Weingast 1989; Schultz and Weingast 1998; Stastavage 2003).

The aforementioned analyses must be modified for developing countries, however. In

most LDCs, the government cannot raise the money it needs by borrowing from domestic

citizens. Local capital markets are simply too shallow, and in many cases the population is too

poor. Instead, public sector borrowers must turn to multinational banks, foreign bond markets,

and international organizations as sources of funds. Under such conditions, the actor with the

greatest interest in repayment – the rentier – is not a domestic citizen with the right to vote and a

seat in parliament, but a foreigner with little direct influence over the domestic politics of the

borrowing state. This does not mitigate the political controversy surrounding debt repayment,

but it does mean that debates about repaying foreigners will differ fundamentally from debates

about paying citizens at home (Drazen 1998).

6

When debt is owed to foreigners, who – if anyone – prefers to repay it? To help answer

the question, the remainder of this section explains who stands to win and lose from a policy of

repayment. It would be impossible to specify all the ways in which debt service could affect the

distribution of income and wealth. Depending on the circumstances, a decision to pay could

involve changes in fiscal, monetary, and exchange rate policy, each with a myriad of short-term

and long-term consequences. To keep the hypotheses plausible and testable, this paper focuses

on the two most likely channels through which debt repayment hurts some segments of the

population and helps others. The first channel concerns the fiscal adjustment costs that some

citizens must incur to repay the debt; the second involves the reputational benefits that parts of

the population will accrue if the government maintains a good credit record. I consider those

two channels in turn.

2.1 The “Adjustment Channel” and the Costs of Repayment

Repaying the foreign debt affects the welfare of citizens by creating a need for fiscal

adjustment. A government that wants to meet its foreign obligations must acquire and then

transfer funds equal to the interest and principal it owes. Leaders can achieve this objective

during good times by contracting new loans and using the proceeds to service old obligations, a

process called debt rollover. When economic conditions turn sour, however, the supply of

external finance dries up and rollover ceases. At that point, the government can only service its

debts by cutting spending in other areas and/or raising taxes. For these reasons, debt repayment

implies fiscal retrenchment, especially during the economic contractions that accompany debt

crises in the developing world.

7

In recent years, the International Monetary Fund has reinforced the tradeoff between debt

repayment and government programs by demanding fiscal austerity in exchange for a debt

workout. When the economic and political burden of debt repayment becomes too severe,

governments seek to reschedule their debts; they ask international lenders to reduce interest rates,

write off some of the principal, and/or extend interest and maturity dates farther into the future.

With very few exceptions, though, private lenders will not consent to a restructuring unless the

IMF approves, and the IMF will not approve unless the debtor reduces non-debt spending and

increases tax revenues.

The costs of fiscal retrenchment do not fall evenly on society as a whole; instead, they hit

certain groups with special force. The first victims of budget cuts are usually public sector

employees. Even before the Latin American crises of the 1980s, economists at the IMF surveyed

previous episodes and concluded that “the brunt of any downward adjustment of government

expenditure to GDP is most commonly borne by public sector employees….” They noted that

“wage and salary earners in the public sector as a whole generally experience some decline in

their real rate of remuneration, so that their relative income position tends to deteriorate”

(Johnson and Salop 1980, p. 12). Events of the 1980s and 1990s strongly confirmed this pattern.

As country after country tried to meet targets set by the IMF and commercial banks, public

employees lost their jobs, and those who remained on the payroll experienced freezes or cuts in

wages and benefits (Frieden 1989).

The budget cuts required for debt repayment also hurt unemployed and poor citizens.

Programs for these groups usually make up a large component of current spending, and are

therefore likely targets for governments that need to impose austerity quickly (Rodrik 1990). In

theory it may be possible to spare the very poor by pursuing what has come to be known as

8

adjustment with a human face, but in reality unemployment and antipoverty programs tend to fall

onto the chopping block (Haggard and Kaufman 1992, p. 29). Careful empirical research

confirms that IMF programs redistribute income away the unemployed and the working class,

and some call this “the single most consistent effect” of IMF-style policies in the developing

world (Pastor 1987).

In addition to cutting spending, the government could increase taxes. There are clear

limits to this option, though, especially during an economic recession when the tax base is

shrinking and incentives for tax evasion are growing. Consequently, most public austerity

programs focus more on cutting spending than on increasing revenue. Some governments do

elect to raise taxes, of course, but it is difficult to project who will be targeted and the historical

record offers little guidance. We know from decades of experience that budget cuts usually hit

government employees, the unemployed and the poor, but there is no similar regularity in the

incidence of tax hikes. For these reasons, this article focuses on the anticipated effect of budget

cuts and leaves the question of tax policy for future research.

In summary, debt repayment requires budget cuts that reduce the absolute and relative

income of public sector employees, the unemployed and the poor. This leads to the first set of

hypotheses: other factors equal, government employees and the unemployed/poor should be less

inclined to repay the foreign debt than citizens who are personally less vulnerable to fiscal

austerity.

2.2 The “Reputation Channel” and the Benefits of Repayment

If compliance with debt contracts requires fiscal retrenchment, why would voters and

their political representatives ever prefer to pay the foreign debt? Would it not be more

9

advantageous to suspend service or even repudiate the debt, thereby denying any obligation to

repay the money that had been borrowed abroad? A large and important literature in economics

and political science examines these questions. Much of the literature is apolitical in the sense

described previously: it discusses the advantages of debt repayment from the perspective of a

benevolent social planner or the country as a whole, without considering the considerable

heterogeneity in domestic preferences during real crises. Nevertheless, the existing literature can

help us theorize about why some citizens would favor repayment despite the immediate fiscal

cost.

Some argue that governments repay to preserve their reputation in the eyes of

international lenders and thereby gain access to foreign capital in the future (Eaton and Gersovitz

1981; Grossman and van Huyck 1988; Wright 2001). These infusions of foreign capital could

help smooth consumption, support productive investments, and/or provide benefits to political

supporters and other groups within society. Others contend that governments repay to avoid

direct sanctions. They suggest that disgruntled creditors could punish a debtor in a variety of

ways, other than depriving it of future loans. Creditors could, for example, retaliate against the

defaulter by taking it to court, attaching its assets, impeding its trade or applying diplomatic and

military pressure (Bulow and Rogoff 1989).

These two explanations are not mutually exclusive, but the available evidence seems

much more consistent with the reputational story. In a synthetic analysis of sovereign lending

and repayment over the past three centuries, Tomz (2003) finds several striking patterns. When

a country defaults on its external debts, it loses access to international capital markets and almost

never manages to attract new loans until it offers creditors a fair settlement. Moreover, when

defaulters return to the market, they get charged higher interest rates than countries with

10

unblemished records of borrowing and repayment. Over time, a country can rebuild its image by

servicing its debts in full and on time, but the reputational costs of default can linger for decades.

In contrast, researchers have found little empirical support for theories of direct sanctions.

Over the past three centuries, there have been only a handful of cases in which creditors have

taken a sovereign debtor to court, attached its assets, impeded its trade, or imposed diplomatic

and military sanctions in response to a default (English 1996; Tomz 2003). Of course, direct

sanctions may be relevant for some countries and time periods, and they are a worthy topic for

future research. The objective of this paper, however, is to identify the most plausible channels

through which debt repayment affects the welfare of citizens, and to see whether voters take

those pathways into account when formulating attitudes about debt repayment. Consequently,

the empirical analysis focuses on the reputational channel, which is most strongly supported by

data over several hundred years.

This leads to the second set of hypotheses. If the reward for repaying the debt is

continued access to foreign capital, then voters who benefit from capital inflows should support

repayment more strongly than voters who doubt the value of a capital infusion for themselves or

the country as a whole.

2.3 The role of economic sophistication

The previous two sections explained how debt repayment would affect the welfare of

citizens. I have argued that repayment would hurt public employees and the unemployed/poor

but would help those who benefit from capital inflows. Recognizing these connections requires

some degree of economic sophistication, however. Voters must understand the fundamentals of

fiscal policy and budget constraints, including the fact that debt repayment may require cuts in

11

other government programs. They must also know how default would affect the reputation of

the country and its access to foreign capital.

Is the electorate sophisticated enough to draw these connections? At first glance there

may be little grounds for optimism. Much research on public opinion suggests that the average

citizen knows little about domestic politics and is even less informed about world affairs. The

most extensive evidence on this point pertains to the United States, where we might expect the

free flow of information to produce an especially knowledgeable electorate. Shortly after World

War II, however, researchers estimated that 30% of American voters were “unaware of almost

any given event in American foreign policy” and another 45% were aware but unable to frame an

intelligent argument (Kreisberg 1949). Despite the expansion of mass media in the past half

century, research has not altered the conclusion that the average American knows little about

domestic and international politics (Delli Carpini and Keeter 1996; Holsti 1996).

Likewise, the typical citizen has only a limited command of economics. Over the past

few decades, polling firms have administered tests of economic literacy to American citizens.

The tests, which include questions about a broad range of economic concepts and events, are

designed to measure knowledge of microeconomics, macroeconomics, and international trade

and finance. One study conducted by the National Council on Economic Education and the

Gallup Organization in 1992 concluded that US citizens “show widespread ignorance of basic

economics that is necessary for understanding economic events and changes in the national

economy” (Walstad and Larsen 1992). A similar study, commissioned by the Federal Reserve

Bank of Minneapolis, found that US adults gave correct answers to approximately 45 percent of

multiple-choice questions, demonstrating some understanding but ample room for improvement

(Dahl 1998).

12

Notwithstanding these studies, there are at least two reasons for optimism. First, the

mean level of voter sophistication may be low but the variance is fairly high (Converse 2000).

Some voters know almost nothing about politics and economics, but others regularly follow the

news and display impressive powers of reasoning. They correctly anticipate the effects of public

policy, and they form opinions that reflect their own circumstances and fundamental values. In

short, a certain segment of the population knows how to analyze economic policy. Second, the

level of voter sophistication probably varies across issues and over time. International debt

agreements tend to be complex, and under normal conditions voters may not understand the

stakes well enough to form opinions about them. During moments of crisis, though, the decision

to repay or default so profoundly affects the welfare of citizens that it becomes front-page news.

Citizens then have new opportunities to learn about debt and develop attitudes that are rooted in

their own values and circumstances.

Taking advantage of the high variance in voter sophistication, I explore an additional

hypothesis: the economic variables mentioned previously – working in the public sector, being

unemployed/poor, and benefiting from capital inflows – should exert their strongest effect

among respondents with the most knowledge of economic concepts and events.

2.4 Alternative hypotheses

There are three major alternatives to the hypotheses advanced in this paper. The first can

be classified under the heading of “nonattitudes.” As Converse (1964) argued, people often

conjure up random answers to survey questions, rather than admit to not having thought about

the issue. That may well be the case with sovereign debt. If most voters have no genuine views

about whether the debt should be paid but nonetheless offer answers when prompted by the

13

interviewer, we should not be able to predict their responses effectively. In statistical analysis,

we should find no significant relationship between the stated preferences of the voter, on the one

hand, and whether he or she works in the public sector, is unemployed/poor, or looks favorably

on capital inflows.

The second alternative might be dubbed a “non-egoistic” approach to public opinion.

Perhaps voters have genuine views about debt but tend not to base them on economic self-

interest. Instead, they may have the economic welfare of the country in mind or be motivated by

communitarian and nationalist considerations. Mayda and Rodrik (2002) conclude that “non-

economic determinants, in the form of values, identities, and attachments, play a very important

role in explaining the variation in preferences over trade. High degrees of neighborhood

attachment and nationalism/patriotism are associated with protectionist tendencies, while

cosmopolitanism is correlated with pro-trade tendencies.” In a similar way, nationalist

sentiments might lead citizens to prefer default on the foreign debt, regardless of how such a

decision would affect their own economic welfare. Of course, the attitudes of respondents could

depend simultaneously on their self interest and on their views about the collectivity. The more

that non-egoistic considerations come to dominate public opinion, however, the less success we

will have in detecting any relationship between the personal circumstances of the respondent and

their attitudes toward foreign debt.

Finally, it is possible that we have placed our bets on the wrong individual characteristics.

What if citizens have genuine opinions about debt and found them upon egoistic considerations,

but not the ones discussed in this paper? I have identified two plausible pathways – adjustment

and reputation – through which debt repayment could affect the distribution of wealth and

income. But these pathways may not be salient for voters, especially since “individuals and

14

groups occupy a number of positions in the economic structure simultaneously,” and their

“incomes are affected through a variety of channels, including labor and other factor income,

relative prices, and the provision of public services, transfers, and subsidies” (Haggard and

Kaufman 1992, pp. 27-28). Whether the hypotheses proposed in this paper have empirical

support is an open question, to which I now turn.

3. The Data and Statistical Model

The data discussed in this paper come from a specially designed survey of 442 eligible

Argentine voters in July 2002. The sample was drawn from residents of Capital Federal and

Gran Buenos Aires, which together make up 32 percent of the national population.1 On average,

citizens in this part of the country have somewhat higher incomes and levels of education than

people in other parts of the country, so it would be useful in future research to compare the

results of this study with one based on a fully national sample. All interviews were performed

face-to-face in neighborhoods that were selected to match the true demographic and political

profile of the region, as determined by the Argentine census and previous election results.

3.1 Measuring attitudes and economic circumstances

To measure the preferences of citizens regarding debt repayment, interviewers posed the

following question: “The government has borrowed money from international creditors,

including foreign banks and international organizations. I would like to know if you think this

debt should be paid. Do you think Argentina should pay the debt, pay only if favorable

1 Calculated from preliminary results of 2001 Argentine Census, http://www.indec.mecon.ar/censoP2001/

15

conditions can be obtained, or not pay?”2 Approximately 94 percent of subjects offered an

opinion, with an additional 3 percent volunteering that they had not thought about the issue and

the remaining 3 percent saying they did not know. From this point forward, all descriptive

statistics and correlations pertain to the 415 respondents who expressed an opinion about

whether the debt should be paid. Within this group, support for repayment was mixed, with 52

percent preferring to pay only under favorable terms and 19 percent opting not to pay at all.3

If the anticipated costs of adjustment play an important role in mass opinion, the desire to

repay the debt should vary with the economic circumstances of the respondent. In approximately

half the interviews, the respondent was the head of household and main breadwinner in the

family (principal sostén del hogar), while in the other half the respondent was a spouse, young

adult or retiree who depended partly on the head of household but may have had independent

sources of income, as well. I therefore recorded the economic position of the head of household

and the situation of the respondent, and took both into account when constructing measures of

economic circumstances.

As hypothesized in section 2, the attitudes of respondents should depend on the sector

where they typically work. Based on answers to closed-end questions, I created a dummy

variable that measured whether the respondent or the principal breadwinner was working in the

2 El gobierno pidió prestado dinero a acreedores internacionales, incluyendo bancos extranjeros y organizaciones internacionales. Me gustaría conocer si usted opina que esa deuda debe ser pagada. ¿Piensa usted que la Argentina debe pagar la deuda, pagar sólo si se consiguen condiciones favorables, o no pagar? It is possible that this formulation predisposed respondents to prefer default, since the second option (pay only if Argentina can obtain favorable conditions) implied that current conditions were not auspicious. If such a bias existed, though, it probably shifted the entire distribution of responses, which would not necessarily affect the kind of causal analysis in Section Four. To confirm that question wording did not contaminate the results, though, the text of option 2 should be varied in future surveys, perhaps by replacing the word favorables with the phrase “más favorables,” meaning more favorable. 3 The interviewer also challenged respondents with a follow-up question: “Are you sure that this is the best decision in the current situation?” A strong majority (64 percent) claimed to be very sure, and another 26 percent felt somewhat sure of their stand on the issue. This challenge question did not substantially alter the distribution of responses. Among those who were very sure of their response, for example, 50 percent wanted more favorable terms and 24 percent did not want to pay.

16

public sector or had been working there before becoming unemployed or retiring. In

approximately 18 percent of cases, the locus of employment was the public sector.

The perceived costs of adjustment should also depend on whether the respondent was

unemployed or poor. The survey did not contain information about personal and family income,

but it did indicate whether the respondent was unemployed or at risk of losing a job. The

dichotomous unemployment variable takes on a value of one if either the principal breadwinner

or the respondent was unemployed at the time of the interview, or if either had a job but felt

likely to lose it and be without work in the next three months. Given the severe economic strain

in Argentina at the time of the survey, many people reported being unemployed or at high risk of

losing their jobs. The variable was coded one in approximately 48 percent of the cases, with

nearly as many respondents fearing unemployment (21 percent) as actually experiencing it in

their household (27 percent).

The survey included information that could be used to test the reputational pathway, as

well. Specifically, respondents were asked to what extent they agreed with the inflow of foreign

capital into Argentina.4 Attitudes were generally positive, but a sizable minority of around one

quarter of the sample disapproved of capital inflows from the rest of the world.

Finally, the survey included two questions that have been used as measures of

nationalism in previous research (Mayda and Rodrik 2002). Respondents were asked to what

extent they agreed or disagreed with each of the following statements: “I prefer to be an

Argentine citizen over being a citizen of any other country in the world” and “In general terms,

Argentina is a better country than the majority of other countries.” One third of respondents

agreed strongly with both statements, whereas those who disagreed either strongly or somewhat

4 In the analysis for this paper, respondents who answered that they did not know the answers to the reputational or nationalist questions were placed in an intermediate category, resulting in five levels of support, but the conclusions remain the same if cases with missing values are either deleted or are multiply imputed.

17

with both statements comprised only 9 percent of the sample. I constructed an overall measure

of nationalism by adding the scores from both questions (each ranging from 0 to 4) and then

rescaling on the 0-1 interval. Respondents inclined strongly toward the nationalist pole, with a

mean score of 0.73.

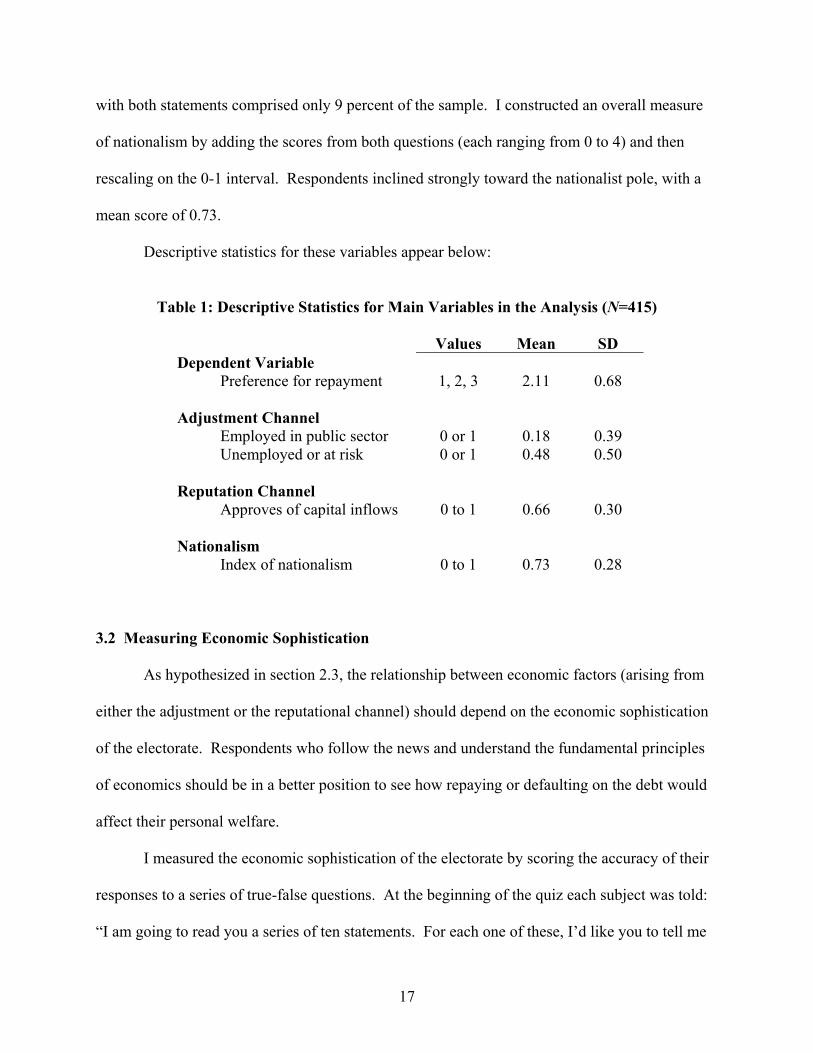

Descriptive statistics for these variables appear below:

Table 1: Descriptive Statistics for Main Variables in the Analysis (N=415)

Values Mean SD Dependent Variable Preference for repayment 1, 2, 3 2.11 0.68 Adjustment Channel Employed in public sector 0 or 1 0.18 0.39 Unemployed or at risk 0 or 1 0.48 0.50 Reputation Channel Approves of capital inflows 0 to 1 0.66 0.30 Nationalism Index of nationalism 0 to 1 0.73 0.28

3.2 Measuring Economic Sophistication

As hypothesized in section 2.3, the relationship between economic factors (arising from

either the adjustment or the reputational channel) should depend on the economic sophistication

of the electorate. Respondents who follow the news and understand the fundamental principles

of economics should be in a better position to see how repaying or defaulting on the debt would

affect their personal welfare.

I measured the economic sophistication of the electorate by scoring the accuracy of their

responses to a series of true-false questions. At the beginning of the quiz each subject was told:

“I am going to read you a series of ten statements. For each one of these, I’d like you to tell me

18

if what is said is true or false. If you don’t know if any of these statements is correct or

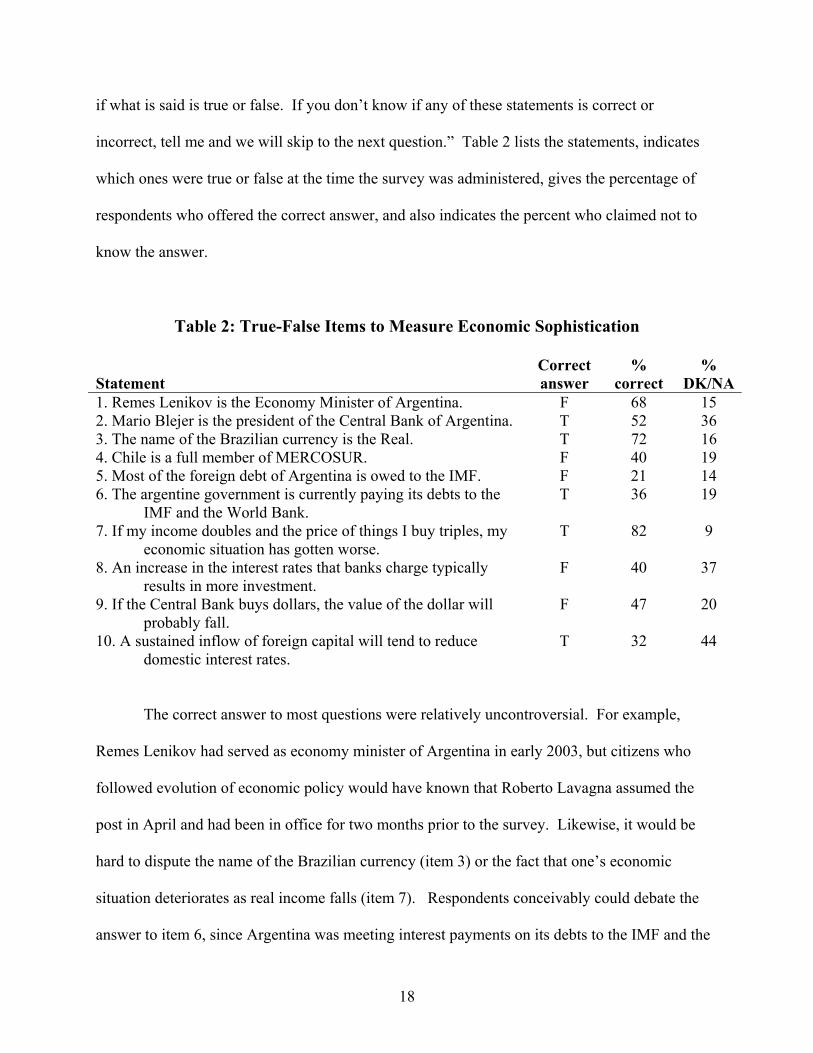

incorrect, tell me and we will skip to the next question.” Table 2 lists the statements, indicates

which ones were true or false at the time the survey was administered, gives the percentage of

respondents who offered the correct answer, and also indicates the percent who claimed not to

know the answer.

Table 2: True-False Items to Measure Economic Sophistication

Statement Correct answer

% correct

% DK/NA

1. Remes Lenikov is the Economy Minister of Argentina. F 68 15 2. Mario Blejer is the president of the Central Bank of Argentina. T 52 36 3. The name of the Brazilian currency is the Real. T 72 16 4. Chile is a full member of MERCOSUR. F 40 19 5. Most of the foreign debt of Argentina is owed to the IMF. F 21 14 6. The argentine government is currently paying its debts to the

IMF and the World Bank. T 36 19

7. If my income doubles and the price of things I buy triples, my economic situation has gotten worse.

T 82 9

8. An increase in the interest rates that banks charge typically results in more investment.

F 40 37

9. If the Central Bank buys dollars, the value of the dollar will probably fall.

F 47 20

10. A sustained inflow of foreign capital will tend to reduce domestic interest rates.

T 32 44

The correct answer to most questions were relatively uncontroversial. For example,

Remes Lenikov had served as economy minister of Argentina in early 2003, but citizens who

followed evolution of economic policy would have known that Roberto Lavagna assumed the

post in April and had been in office for two months prior to the survey. Likewise, it would be

hard to dispute the name of the Brazilian currency (item 3) or the fact that one’s economic

situation deteriorates as real income falls (item 7). Respondents conceivably could debate the

answer to item 6, since Argentina was meeting interest payments on its debts to the IMF and the

19

World Bank but was not repaying the principal, which actually did not come due until later that

year. One could also argue that the term “investment” needed to be more clearly defined in item

8. All the results in this paper are robust to excluding those two items from the test, however.

Table 2 shows that the test contained a good mix of easy and challenging items. The

least difficult stated: “if my income doubles and the price of things I buy triples, my economic

situation has gotten worse.” Approximately 82% of respondents correctly answered that the

statement was true. Another 9% professed not to know or skipped the question, and the

remaining 9% concluded that the statement was actually false! Questions about the name of the

Brazilian currency and the name of the Economy minister also tended to be relatively easy for

this set of respondents, with 72% and 68% giving the correct answer. In contrast, the hardest

question on the test elicited a correct response from only 21% of those who were interviewed.

Table 2 also shows a fair percentage of “don’t know” responses. In the most extreme

case, approximately 44% of voters professed ignorance when asked whether a sustained inflow

of foreign capital tended to reduce domestic interest rates. This was not only the highest

nonresponse rate on the quiz but also the last question in the battery, which makes one wonder

whether voters were getting tired of taking the test. There does not seem to be much evidence of

drop-off, however. Only 9 percent of subjects skipped question 7 and only 20% skipped

question 9. Both those figures are lower than the average non-response rate, which was 23

percent across all the items.

I scored the text by counting the number of correct answers. Two subjects received a

perfect score, while eight gave no correct answers at all. It is fair to ask whether some of these

poor performers got low scores because they refused to be tested, and therefore skipped every

question regardless of whether they knew its veracity. The strong correlation between education

20

and economic sophistication should allay this concern, however. Four subjects did not answer

any questions, and 28 (roughly 7 percent of the sample) skipped at least 7 of 10 items. None of

the subjects in this group had a college degree, however, and 24 of the 28 had not completed

high school. Overall, subjects who skipped a large percentage of questions were considerably

less educated than those who answered most of the items. It is therefore likely that subjects

scored poorly because they did not know the answers, not because they refused to play the game.

Figure 1 shows the distribution of correct responses to the economic sophistication quiz.

The distribution is fairly symmetrical, with 171 respondents getting more than half the items

right and 168 answering less than half correctly. The median and modal response were both 5.

To facilitate analysis I have rescaled the variable on the unit interval, so our measure of

economic sophistication is the proportion of questions that the subject answered correctly. This

variable has a mean of 0.49 and a standard deviation of 0.21.

Figure 1: Distribution of Correct Responses to the Economic Sophistication Quiz

Pro

porti

on o

f Cas

es

Number of Correct Responses0 1 2 3 4 5 6 7 8 9 10

0

.05

.1

.15

.2

3.3 Statistical Model

I used an ordered probit model to estimate how the individual characteristics of voters

affected their attitudes toward debt repayment. In this particular application, the latent variable

21

y* ranges from -∞ to ∞ and measures the voter’s desire to repay the foreign debt. We cannot

observe the precise value of y*, but for each individual i we can infer from the survey whether

yi* is low (respondent said the debt should not be paid), medium (respondent would pay under

favorable conditions), or high (respondent said the debt should be paid). If we designate τ1 as the

threshold between low and medium values, and we let τ2 mark the transition from medium to

high, then we can establish the following mapping between the latent variable yi* and the

observed survey response yi:

≥

<≤

<

=

2*

2*

1

1*

if "debt Pay the"

if "conditionsbetter under only Pay "

if debt" pay thet Don'"

τ

ττ

τ

i

i

i

i

y

y

y

y

For this analysis, the desire to repay, yi*, is modeled as a linear function of the voter’s

sophistication Si, a vector of individual-level economic characteristics Xi, and the interaction of

the two. Rearranging terms, we can express the latent variable as

iiiiiii XSXSSy εωβα ++−+= )1(* .

Bartels (1996) offers an intuitive interpretation for this kind of model. Given that economic

sophistication Si is measured on a scale from 0 to 1, the vector ω measures the effect of

characteristics Xi on yi* for someone with the highest level of economic sophistication, whereas

the vector β quantifies the impact of Xi for a person with almost no understanding of economic

theory and policy. Of course, only a few voters occupy these two extremes. For all other voters,

the model implies that the desire to repay is a weighted average of “high sophistication” and

“low sophistication” effects, with weights given by the voter’s level of economic sophistication.

22

In this model, the parameters to be estimated include the scalar α, the vectors β and ω, and the

thresholds τ1 and τ2.

4. Results

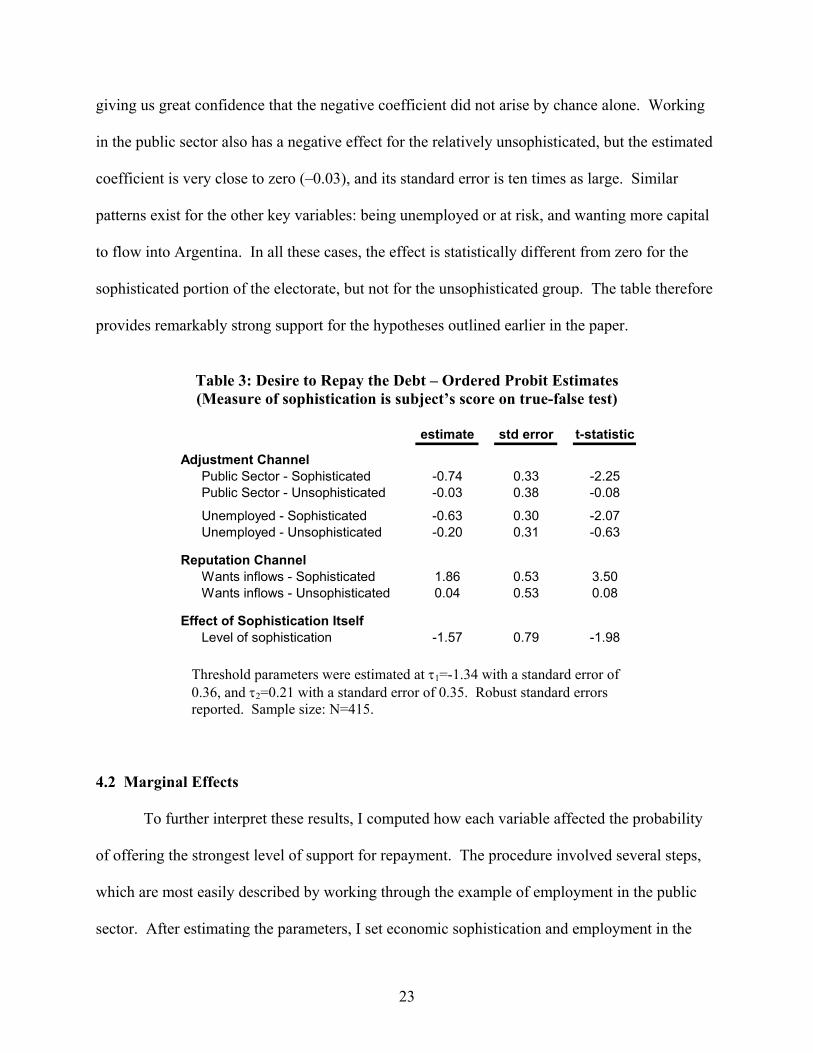

Estimates from the ordered probit model appear in Table 3. The table contains two

parameters for each variable pertaining to the adjustment and reputation channels. One

parameter represents the effect of the variable among the most sophisticated voters; the other

parameter gives the effect among those with the lowest levels of sophistication.

4.1 The Main Results

The table reveals two main patterns. First, all parameter estimates carry the hypothesized

signs. On average, those working in the public sector show less inclination to repay the debt

than those whose locus of employment is the private sector. Similarly, subjects who are

unemployed or perceive themselves at risk of losing a job are less likely to support repayment

than those with more secure employment. Finally, individuals who recognize the benefits of

capital inflows have a much stronger preference for debt repayment than those who doubt the

benefits of capital inflows for themselves and the country as a whole. Interestingly, the level of

economic sophistication also enters the model with a negative sign, implying that the desire to

repay declines as people come to understand more about economic conditions in Argentina.

Second, the table shows that each of the main variables exerts a much stronger impact

among the subpopulation of sophisticated voters than among the set who are relatively

unsophisticated. Compare, for instance, the effect of working in the public sector. When the

respondent has a strong command of economics, being employed in the public sector reduces the

desire to repay by 0.74 on the latent scale. The estimate is more than twice its standard error,

23

giving us great confidence that the negative coefficient did not arise by chance alone. Working

in the public sector also has a negative effect for the relatively unsophisticated, but the estimated

coefficient is very close to zero (–0.03), and its standard error is ten times as large. Similar

patterns exist for the other key variables: being unemployed or at risk, and wanting more capital

to flow into Argentina. In all these cases, the effect is statistically different from zero for the

sophisticated portion of the electorate, but not for the unsophisticated group. The table therefore

provides remarkably strong support for the hypotheses outlined earlier in the paper.

Table 3: Desire to Repay the Debt – Ordered Probit Estimates (Measure of sophistication is subject’s score on true-false test)

estimate std error t-statistic

Adjustment ChannelPublic Sector - Sophisticated -0.74 0.33 -2.25Public Sector - Unsophisticated -0.03 0.38 -0.08

Unemployed - Sophisticated -0.63 0.30 -2.07Unemployed - Unsophisticated -0.20 0.31 -0.63

Reputation ChannelWants inflows - Sophisticated 1.86 0.53 3.50Wants inflows - Unsophisticated 0.04 0.53 0.08

Effect of Sophistication ItselfLevel of sophistication -1.57 0.79 -1.98

Threshold parameters were estimated at τ1=-1.34 with a standard error of 0.36, and τ2=0.21 with a standard error of 0.35. Robust standard errors reported. Sample size: N=415.

4.2 Marginal Effects

To further interpret these results, I computed how each variable affected the probability

of offering the strongest level of support for repayment. The procedure involved several steps,

which are most easily described by working through the example of employment in the public

sector. After estimating the parameters, I set economic sophistication and employment in the

24

public sector equal to 1 and let the unemployment and inflow variables take on their median

values. I then used the parameter estimates in Table 3 to compute the probability that a public

sector employee with the highest level of economic sophistication would prefer to see the debt

repaid. Finally, I reset the public employment variable to 0 and recomputed the probability of

wanting the debt repaid. The effect of being a public sector employee was equal to the first

probability minus the second. By repeating this exercise for different values of economic

sophistication, I obtained the estimated effect across the full range of sophistication scores.

Standard errors and confidence intervals around the effects were computed using the stochastic

simulation techniques proposed by King, Tomz, and Wittenberg (2000).

In theory, public sector employees should be less enthusiastic about debt repayment than

those who work in the private sector. This proves to be true, but the effect grows with the level

of economic sophistication. When the sophistication score is 0, public and private sector

employees are equally likely to say the debt should be paid. As sophistication rises to 0.5,

though, the probability of supporting repayment becomes 13 points lower for public employees

than for private ones. The standard error around this difference is only 5 points, giving us great

confidence that these two types of individuals have different preferences about the foreign debt.

Finally, when economic sophistication reaches its maximum value of 1, the difference in

probabilities between public and private employees grows to nearly 22 points, with a standard

error of 9. Thus, the sector of employment has a large effect on the desire to repay, especially

among those with a good understanding of economic concepts and events. The same conclusion

holds for those who are unemployed or at risk of losing their jobs.

The most powerful variable in the analysis relates to the reputational channel. When

sophistication is at its lowest level, those who strongly favor capital inflows are only slightly

25

more inclined to repay the debt than those who strongly oppose inflows. The estimated

difference in probability is only 2 points, with a standard error nearly nine times as large. At

intermediate levels of sophistication, though, the probability of endorsing repayment is 32 points

higher for those who favor capital inflows, and among the most highly sophisticated voters the

estimated difference is 47 points, with a standard error of 11.

Figure 2: Effects of Main Variables, Conditional on Economic Sophistication (graphs show estimated change in probability and 95% confidence interval)

WORKING IN THE PUBLIC SECTOR

Effe

ct o

n P

roba

bilit

yof

Sup

porti

ng R

epay

men

t

Economic Sophistication0 .1 .2 .3 .4 .5 .6 .7 .8 .9 1

-.4

-.3

-.2

-.1

0

.1

.2

.3

BEING UNEMPLOYED OR AT RISK

Effe

ct o

n P

roba

bilit

yof

Sup

porti

ng R

epay

men

t

Economic Sophistication0 .1 .2 .3 .4 .5 .6 .7 .8 .9 1

-.4

-.3

-.2

-.1

0

.1

.2

STRONGLY FAVOR CAPITAL INFLOWS

Effe

ct o

n P

roba

bilit

yof

Sup

porti

ng R

epay

men

t

Economic Sophistication0 .1 .2 .3 .4 .5 .6 .7 .8 .9 1

-.3-.2-.1

0.1.2.3.4.5.6.7

Figure 2 depicts these effects across the full range of economic sophistication. In each

panel, the central curve gives the estimated change in probability of supporting repayment and

the bordering curves represent 95 percent confidence intervals.

26

4.3 Counterfactual Estimates of Aggregate Opinion

To this point the analysis has focused on individual respondents, but it is interesting to

ask how aggregate opinion would change if the economic circumstances and sophistication of

the citizens were different. In our sample, approximately 29 percent of subjects said that the

foreign debt should be paid. How might public opinion look if all citizens agreed that capital

inflows were beneficial for themselves and the country as a whole? To answer this question I

simulated the distribution of public opinion in an Argentina where all respondents supported

inflows but their exposure to unemployment, participation in the public sector and level of

economic sophistication remained the same. In such a hypothetical world, approximately 38

percent of voters would support an unconditional policy of debt repayment. This is a large

change in public opinion but still leaves a majority in favor of partial or complete default.

Conversely, in a country where all voters strongly doubted the value of capital inflows

but economic circumstances otherwise remained the same, only 13 percent of voters would

prefer to repay the foreign debt. This level of support is less than half of the sample average, but

it is also greater than zero. The data thus suggest that concerns about reputation have a major

effect on public opinion, but a small proportion of the electorate stands ready to repay the foreign

debt for reasons that have little to do with gaining access to future capital. Some may fear the

prospect of direct sanctions; others may feel that the government has moral obligation to repay

the money it borrowed. It would be instructive to explore these two possibilities in future

research.

Finally, the analysis in this paper highlights the effect of economic sophistication. It is

sometimes argued that democracy depends on the presence of a highly informed electorate, one

27

that understands the pros and cons of policy options and can make an informed judgment. How

might Argentine opinion look if all voters were knowledgeable enough to receive a perfect score

on the true-false test? In that case, only 22 percent of voters would support an unconditional

policy of debt repayment. This result strongly contradicts the impression, occasionally cited in

the popular press, that Argentines prefer default because they do not understand economics. On

the contrary, those with the most thorough understanding of economics think default makes

better sense than repayment. The exact reasons for this view remain a topic for future research.

4.4 Other Measures of Economic Sophistication

The main measure of economic sophistication in this paper is the proportion of correct

responses on the true-false test. As it turns out, the results remain very similar when other

measures of economic sophistication are employed.

At the end of the survey, each interviewer was asked to assess the economic

sophistication of the subject on a scale from 0 to 10. No one awarded the minimum or the

maximum scores, perhaps because those numbers represented ideal types that voters could only

approximate. The median score was 5 on a scale from 1 to 9 and the distribution inclined

slightly to the right, resulting in a mean of 5.2. After rescaling on the unit interval, I included the

interviewer assessment in place of the true-false test, and the pattern of results was essentially the

same. Among the least sophisticated voters, neither the adjustment channel nor the reputational

channel had much effect on public opinion. At intermediate and high levels of sophistication,

however, those variables had a striking effect on individual preferences about debt repayment.

The interviewer assessment should not be regarded as a completely independent measure

of sophistication, however. After all, each interviewer had recorded how the respondent

28

answered the true-false questions that appeared earlier in the survey. The polling firm did not

provide interviewers with an answer key for the true-false items, but some interviewers probably

knew the correct responses and may have assigned ratings that reflected how the respondent

performed on the quiz. On the other hand, the survey questions discussed in this paper were part

of an omnibus instrument that included a wide range of items about economic policy. These

questions gave interviewers an additional basis for judging the economic sophistication of the

respondent, above and beyond the results of the economics quiz. The correlation between the

true-false scores and the interviewer assessment was 0.5, suggesting that the two were highly

related but not interchangeable.

Finally, the survey included information about the education of the respondent, which can

be used as an additional measure of economic sophistication. Approximately 29 percent of

subjects had graduated from high school and gone on for postsecondary training, whereas 7

percent had not completed elementary school. Unlike the other measures of sophistication, this

education variable had more of its mass concentrated at low values, such that the median level of

educational attainment (12 years, equivalent to a high school education) exceeded the mean of

10.5. Not surprisingly, this variable performed a bit differently from either the true-false score or

the interviewer assessment. Nevertheless, the overall patterns in the data were the same, as

illustrated by Figure 3.

29

Figure 3: Effects when economic sophistication is measured by interviewer assessment (left column) or years of education (right column)

WORKING IN THE PUBLIC SECTOR

Effe

ct o

n P

roba

bilit

yof

Sup

porti

ng R

epay

men

t

Economic Sophistication0 .1 .2 .3 .4 .5 .6 .7 .8 .9 1

-.4

-.3

-.2

-.1

0

.1

.2

.3

WORKING IN THE PUBLIC SECTOR

Effe

ct o

n P

roba

bilit

yof

Sup

porti

ng R

epay

men

t

Economic Sophistication0 .1 .2 .3 .4 .5 .6 .7 .8 .9 1

-.4

-.3

-.2

-.1

0

.1

.2

.3

BEING UNEMPLOYED OR AT RISK

Effe

ct o

n Pr

obab

ility

of S

uppo

rting

Rep

aym

ent

Economic Sophistication0 .1 .2 .3 .4 .5 .6 .7 .8 .9 1

-.4

-.3

-.2

-.1

0

.1

.2

BEING UNEMPLOYED OR AT RISK

Effe

ct o

n P

roba

bilit

yof

Sup

porti

ng R

epay

men

t

Economic Sophistication0 .1 .2 .3 .4 .5 .6 .7 .8 .9 1

-.4

-.3

-.2

-.1

0

.1

.2

STRONGLY FAVOR CAPITAL INFLOWS

Effe

ct o

n P

roba

bilit

yof

Sup

porti

ng R

epay

men

t

Economic Sophistication0 .1 .2 .3 .4 .5 .6 .7 .8 .9 1

-.6-.5-.4-.3-.2-.1

0.1.2.3.4.5.6.7

STRONGLY FAVOR CAPITAL INFLOWS

Effe

ct o

n P

roba

bilit

yof

Sup

porti

ng R

epay

men

t

Economic Sophistication0 .1 .2 .3 .4 .5 .6 .7 .8 .9 1

-.6-.5-.4-.3-.2-.1

0.1.2.3.4.5.6.7

The impressive performance of the education variable is a promising and important

finding. At a minimum, it suggests that researchers could use the education of the respondent

(available in nearly all public opinion surveys) as a proxy for economic sophistication. This

would allow researchers to examine the interaction between standard political economy variables

and economic sophistication, without incurring the cost of designing new surveys that include

objective tests of economic knowledge. The proxy would not be perfect, and in some

applications a detailed test of economic knowledge may be appropriate, but education could be

30

used to explore a range of interactive effects that until now have not been examined in the

literature.

More generally, the performance of the education variable suggests that sophistication

could be a general trait, one that transcends particular issue domains. A full test of this

conjecture would require a survey that tested knowledge of economics, politics, and other

domains of interest, and then tested for correlations across domains. For now, though, we have

established that economic sophstication (measured directly and with proxy variables such as

education) strongly conditions the attitudes of voters on issues of economic policy.

4.5 Other Sources of Public Opinion

To this point, I have tested the adjustment channel by including dummy variables for

those who work in the pubic sector and those who were unemployed or at risk of losing their

jobs. Due to data limitations, I could not incorporate a separate variable for poverty. Argentine

surveys only rarely include questions about personal or family income, and such data were not

available in the July 2002 survey.

I now extend the analysis by including a proxy variable for poverty: the number and kind

of automobiles, goods and services present in the household. Items were scored according to a

point system developed by the Argentine Marketing Association, and the total was rescaled to

fall between zero and one. As one might expect in a country where more than half the

population falls below the poverty line and inequality is high, the distribution was concentrated

at the lower values but also had a long right tail, leading to a mean score (0.20) nearly twice as

large as the median (0.11).

Table 4 shows that this proxy variable has the anticipated effect on voter preferences.

Other factors equal, those with more household goods are also more inclined to repay the foreign

31

debt, and the effect is more than three times as strong for sophisticated respondents than for

unsophisticated ones. We should exercise some caution when interpreting these estimates, since

the coefficients are small relative to their standard errors, but overall the results point in the

hypothesized direction.

Table 4: Expanded Model of the Desire to Repay

(Measure of sophistication is score on true-false test)

estimate std error t-statistic

Adjustment ChannelPublic Sector - Sophisticated -0.68 0.33 -2.06Public Sector - Unsophisticated -0.11 0.38 -0.31

Unemployed - Sophisticated -0.64 0.31 -2.07Unemployed - Unsophisticated -0.11 0.32 -0.33

HHold Goods - Sophisticated 0.81 0.52 1.54HHold Goods - Unsophisticated 0.29 0.74 0.39

Reputation ChannelWants inflows - Sophisticated 1.97 0.55 3.60Wants inflows - Unsophisticated -0.09 0.54 -0.17

Non-egoistic VariablesNationalism - Sophisticated 1.19 0.55 2.16Nationalism - Unsophisticated -1.50 0.61 -2.47

Effect of Sophistication ItselfLevel of sophistication -4.12 1.24 -3.32

Threshold parameters were estimated at τ1=-2.58 with a standard error of 0.67 and τ2=-1.0 with a standard error of 0.66. Robust standard errors reported. Sample size: N=415.

The other variable that now appears in the analysis is nationalism. As noted in section

2.4, research shows that non-economic determinants, including attachment to country, correlate

with individual attitudes toward free trade. To what extent do nationalist sentiments affect the

desire to repay the debt? Table 4 provides an interesting and somewhat surprising answer.

Among the less sophisticated, nationalism reduces the desire to repay. Among the more

sophisticated, though, the variable has exactly the opposite effect. For the more sophisticated,

pride in country (as measured by those who think Argentina is better than most other countries,

32

and who prefer being Argentine over being citizens of any other country) actually increases the

propensity to repay. Further research is needed to understand how this sophisticated form of

nationalism differs from the unsophisticated variant, and why they have opposing effects on the

desire to repay.

5. Conclusion

Existing research on compliance with international agreements has paid relatively little

attention to the preferences of voters. This has been especially true in the area of international

debt. Most models of debt assume that the borrowing country is governed by a unitary, apolitical

actor that weighs the costs and benefits of default for the country as a whole. These models have

greatly enhanced our understanding of reputation, direct sanctions, and other factors that might

motivate a country to honor its financial commitments, but they have overlooked an important

part of the calculation. The decision to default or repay depends not only on bargaining between

the country and its foreign creditors, but also on the demands of the electorate at home.

This paper has offered the first systematic analysis of voter preferences about debt

default. It has documented the diversity of opinions in the electorate and sought to explain them

as a function of two clusters of variables: the economic circumstances voters face and their level

of economic sophistication. The evidence, based on a unique survey of Argentine voters, shows

that opinion follows a clear pattern. Support for repayment is lowest among citizens who stand

to lose from the fiscal adjustment that would be necessary to avert a default. At the same time,

support is highest among those who believe in the benefits of access to foreign capital. These

results provide a solid foundation for incorporating domestic politics into models of international

debt.

33

The paper has also introduced several measures of economic sophistication and shown

how they interact with objective circumstances to affect the preferences of voters. The findings

suggest two new avenues for research, one theoretical and the other empirical. Many modern

theories in the field of political economy presuppose that voters understand the distributional

implications of public policy and can accurately assess how government decisions affect their

personal welfare. That assumption must now be qualified. Certain segments of the electorate

possess the sophistication to judge economic policy as our current theories suggest, but other

segments lack the education and experience to draw the connections our theories presume. By

incorporating the concept of economic sophistication as a parameter, the next generation of

theories could generate a range of new predictions about how economic policy emerges and

changes in democracies.

The findings of this paper also suggest a new empirical agenda. The use of political

knowledge scales has become increasingly common in research on American politics, but similar

measures have not yet permeated the field of political economy. If the strong interactive effects

in this paper are any guide, the regular use of economic knowledge scales (or of proxies such as

interviewer assessments and education more generally) could advance our understanding of mass

attitudes on a wide range of economic issues, both foreign and domestic.

34

References Alesina, Alberto. 1988. “The End of Large Public Debts.” In High Public Debt: The Italian Experience, edited by Francesco Giavazzi and Luigi Spaventa, 34-79. Cambridge: Cambridge University Press. Alesina, Alberto and Eliana La Ferrara. 2001. “Prefernces for Redistribution I the Land of Opportunities.” NBER Working Paper 8267. Cambridge, MA: National Bureau of Economic Research. Althaus, Scott L. 1998. "Information Effects in Collective Preferences." American Political Science Review 92, no. 3 (September): 545-58. Baker, Andy. 2003. “Why Is Trade Reform so Popular in Latin America? A Consumption-Based Theory of Trade Policy Preferences.” Forthcoming, World Politics. Bartels, Larry M. 1996. “Uninformed Votes: Information Effects in Presidential Elections.” American Journal of Political Science 40, no. 1 (February): 194-230. Bulow, Jeremy, and Kenneth Rogoff. 1989. “A Constant Recontracting Model of Sovereign Debt.” Journal of Political Economy 97, no. 1 (February): 155-78. Converse, Philip. 1964. “The Nature of Belief Systems in Mass Publics,” in Ideology and Discontent, ed. David Apter, pp. 206-61. New York: Free Press. Converse, Philip E. 2000. “Assessing the Capacity of Mass Electorates.” Annual Review of Political Science 3: 331-53. Dahl, David S. 1998. "Why Johnny Can't Choose -- And What Johnny (and Jane) Needs to Know to Understand the Economy." The Region (Federal Reserve Bank of Minneapolis, December. Delli Carpini, Michael X and Scott Keeter. 1996. What Americans Know about Politics and Why It Matters. New Haven: Yale University Press. Drazen, Allan. 1998. "Towards a Political-Economic Theory of Domestic Debt." In The Debt Burden and its Consequences for Monetary Policy: Proceedsings of a Conference held by the International Economic Association at the Deutsche Bundesbank, Frankfurt, Germany, edited by Guillermo A. Calvo and Mervyn King, 159-78. New York: St. Martin's Press. Eaton, Jonathan, and Mark Gersovitz. 1981. “Debt with Potential Repudiation: Theoretical and Empirical Analysis.” Review of Economic Studies 48, no. 2 (April): 289-309. English, William B. 1996. "Understanding the Costs of Sovereign Default: American State Debts in the 1840s." American Economic Review 86, no. 1 (March): 259-75.

35

Frieden, Jeff. 1988. "Classes, Sectors, and Foreign Debt in Latin America." Comparative Politics 21, no. 1 (October): 1-19. Frieden, Jeffry A. 1989. "Winners and Losers in the Latin America Debt Crisis: The Political Implications." In Debt and Democracy in Latin America, edited by Barbara Stallings and Robert Kaufman, 23-37. Boulder: Westview Press. Frieden, Jeffry A. 1991. Debt, Development, and Democracy: Modern Political Economy and Latin America, 1965-1985. Princeton, NJ: Princeton University Press. Grossman, Herschel I., and John B. Van Huyck. 1988. “Sovereign Debt as a Contingent Claim: Excusable Default, Repudiation, and Reputation.” American Economic Review 78, no. 5 (December): 1088-97. Haggard, Stephan, and Robert R. Kaufman. 1992. The Politics of Economic Adjustment: International Constraints, Distributive Conflicts, and the State. Edited by Stephan Haggard and Robert R. Kaufman. Princeton, NJ: Princeton University Press. Holsti, Ole R. 1996. Public Opinion and American Foreign Policy. Ann Arbor: University of Michigan Press. Iversen, Torben and David Soskice. 2001. “An Asset Theory of Social Policy Preferences.” American Political Science Review 95, no. 4 (December): 875-93. Johnson, Omotunde, and Joanne Salop. 1980. “Distributional Aspects of Stabilization Programs in Developing Countries.” IMF Staff Papers 27, no. 1 (March): 1-23. Kaufman, Robert R. 1988. The Politics of Debt in Argentina, Brazil, and Mexico: Economic Stabilization in the 1980s. Berkeley: Institute of International Studies, University of California. King, Gary, Michael Tomz and Jason Wittenberg. 2000. “Making the Most of Statistical Analysis: Improving Interpretation and Presentation.” American Journal of Political Science 44, no. 2 (April): 347-61. Kreisberg, Martin. 1949. “Dark Areas of Ignorance.” In Public Opinion and Foreign Policy, ed. Lester Markel, pp. 49-64. New York: Harper & Bros. Luttmer, Erzo F. P. 2001. “Group Loyalty and the Taste for Redistribution." Journal of Political Economy 109, no. 3 (June): Mayda, Anna Maria, and Dani Rodrik. 2002. “Why Are Some People (and Countries) More Protectionist Than Others?” Mimeo. Cambridge, MA: Department of Economics and John F. Kennedy School of Government, Harvard University. Mondak, Jeffrey J. 2001. "Developing Valid Knowledge Scales." American Journal of Political Science 45, no. 1 (January): 224-38.

36

Nelson, Joan M. 1990. Economic Crisis and Policy Choice, edited by Joan M. Nelson. Princeton, NJ: Princeton University Press. North, Douglass C., and Barry R. Weingast. 1989. "Constitutions and Commitment: The Evolution of Institutions Governing Public Choice in Seventeenth-Century England." Journal of Economic History 49, no. 4 (December): 803-32. O'Rourke, Kevin H., and Richard Sinnott. 2001. "The Determinants of Individual Trade Policy Preferences: International Survey Evidence." In Brookings Trade Forum, edited by Susan M. Collins and Dani Rodrik, 157-206. Washington, DC: Brookings Institution. Pastor, Manuel, Jr. 1987. “The Effects of IMF Programs in the Third World: Debate and Evidence from Latin America.” World Development 15, no. 2: 249-62. Rodrik, Dani. 1990. "The Transfer Problem in Small Open Economies: Exchange Rate and Fiscal Policies for Debt Service." Ricerche Economiche 44, nos. 2-3 (April-September): 231-50. Scheve, Kenneth F., and Matthew J. Slaughter. 2001. "What Determines Individual Trade-Policy Preferences?" Journal of International Economics 54: 267-92. Schultz, Kenneth A., and Barry R. Weingast. 1998. "Limited Governments, Powerful States." In Strategic Politicians, Institutions, and Foreign Policy, edited by Randolph M. Siverson, 15-49. Ann Arbor: University of Michigan Press. Stasavage, David. 2003. Public Debt and the Birth of the Democratic State: France and Great Britain, 1688-1789. New York: Cambridge University Press. Tomz, Michael. 2002. “Democratic Default: Domestic Audiences and Compliance with International Agreements.” Mimeo. Department of Political Science, Stanford University. Tomz, Michael. 2003. Sovereign Debt and International Cooperation. Book manuscript. Department of Political Science, Stanford University. Walstad, William B., and Max Larsen. 1992. A National Survey of American Economic Literacy. Lincoln, Nebraska and Columbia, Maryland: Education Research Divsion, The Gallup Organization. Wright, Mark L. J. 2001. “Reputations and Sovereign Debt.” Cambridge, MA: Department of Economics, M.I.T. Zaller, John. 1992. The Nature and Origins of Mass Opinion. New York: Cambridge University Press.