donald trump as us president – the economic and financial

TRANSCRIPT

Donald Trump as US President – the economic

and financial implications

Follow us on Twitter @Danske_Research

Important disclosures and certifications are contained from page 23 of this report.

9 November 2016

Mikael Olai Milhøj

Senior Analyst

Thomas Harr

Global Head of FICC Research

Arne Lohmann Rasmussen

Chief Analyst, Head of FI Research

Christian Tegllund Blaabjerg

Senior Strategist

Jakob Ekholdt Christensen

Chief Analyst, Head of EM Research

Stefan Mellin

Senior Analyst

Kristoffer Kjær Lomholt

Senior Analyst

Jens Nærvig Pedersen

Senior Analyst

Investment Research www.danskebank.com/CI

11

Key takeaways – macro and politics

22

Key takeaways – market implications

Trump as President

EUR/USDHigher EUR/USD short and medium term. EUR/USD set to rise to 1.13-1.14 in the coming days. Our 12M forecast remains 1.15

EUR/SEKEUR/SEK could reach 10.10-10.20 on a knee-jerk move. The SEK to stay weaker for longer on weaker risk appetite, Riksbank December cut

EUR/NOKNear-term higher towards 9.30-9.40 on negative risk appetite, year-end seasonality, liquidity. Bearish EUR/NOK in 3-12M

EUR/DKKShort and medium term limited impact. Long-term, a more protectionistic US could hit DK's CA and thereby the DKK

vs selective LATAM, Asia and CADPositive for USD.USD/MXN set to reach 21.5 in the days after the election

Global equities Knee-jerk 5-10% sharp fall across markets but sell-off to be short-lived.

Regional US set to outperform eurozone and EM.

Sector performancePositive for industrial and basic materials, Energy and healthcare could rally

Fixed Income US yields

10Y UST yields set to fall around15-20bp and bund yields to fall in days after the election.Medium term, higher UST yields

FX

Equities

A regime shift in US policy but uncertain how

Trump will act as President

44Source: https://www.archives.gov/federal-register/electoral-college/key-dates.html

• At the time of writing, Donald Trump seems to be the new US President.

• The Republicans have retained the power of both the House and the Senate, implying that it will be easier for Donald Trump to get his policies through.

• The electors are due to meet in their state and vote for the President and Vice President on 19 December.

• Congress is due to meet in a joint session to count the electoral votes on 6 January 2017.

• The inauguration of the new President and Vice President is due to take place on 20 January 2017.

Election result

55

• Based on his policy proposals, Donald Trump stands for a significant regime shift in US policy.

• However, we think actual policy changes should be more modest due to likely resistance from Congress, even within the Republican Party. Still, Trump’s room for manoeuvre is larger as the Republican party will also control Congress.

• In the short term, we do not expect growth to be hit by Trump uncertainties through lowerconfidence and hence we expect the economy to continue to grow around 2%.

• Fiscal boost to growth is likely to be offset by a more hawkish Fed.

• In the medium to long term, uncertainty is set to rise but we think the negative effects of more protectionism and tougher immigration policy will dominate the possible positive effects of less regulation, lower taxes and infrastructure spending.

Trump stands for a significant regime shift but actual changes

should be more modest

66

• Trump has promised to ‘at least double’ Clinton’s infrastructurespending, implying at least 0.6% of GDP per year, and suggestedtax cuts of USD3,000bn (1.6% of GDP per year): in sum, fiscaleasing of at least 2.2% of annual GDP.

• Very difficult to estimate the actual effect of Trump’s economicplan but we should expect a much more expansionary fiscalpolicy. We are doubtful he will manage to balance the budget within eight years through dynamic effects as he has suggested.

• We doubt he can get all his economic plan through but the Republican dominance of Congress makes it more likely.

• Using a simple debt model and assuming Trump gets all his policy proposals through (which we, however, do not think will be the case), the US public net debt could increase to above 95% of GDP in 10 years from about 75% today.

• As a result, the US could over the medium- to long-term lose the last two of its ‘AAA’ ratings (has already lost one).

• Less rosy assumptions imply that debt will increase more (slower growth, lower fiscal multiplier, higher rates).

• US public sector needs to reform as projected fiscal path is already unsustainable in the long run.

US government debt set to increase due to higher budget deficit

0

20

40

60

80

100

120

140

160

19

95

19

98

20

01

20

04

20

07

20

10

20

13

20

16

20

19

20

22

20

25

20

28

20

31

20

34

20

37

20

40

20

43

20

46

US public debt,

CBO baseline projection

% of GDP

75

80

85

90

95

100

105

110

115

2017 2019 2021 2023 2025

% of GDP

CBO baseline projection

Fiscal baseline scenario

Fiscal adverse scenario

US public net debt

Source (both charts): CBO, www.donaldjtrump.com, Danske Bank Markets

US government debt set to increase

US public debt to increase significantly in coming decades

77Source: www.donaldjtrump.com,

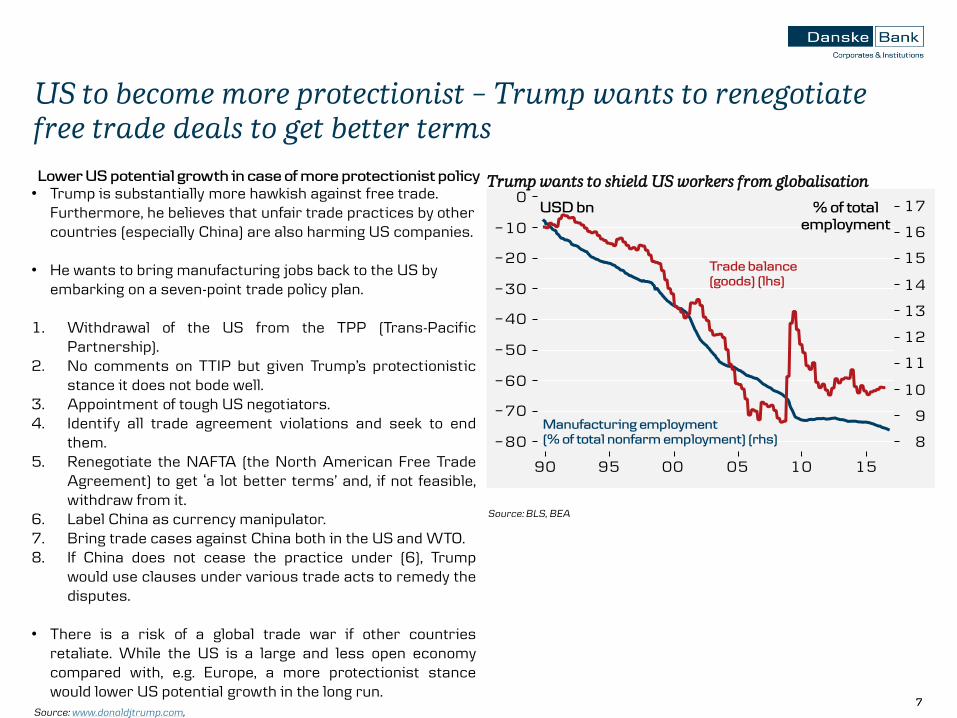

• Trump is substantially more hawkish against free trade. Furthermore, he believes that unfair trade practices by other countries (especially China) are also harming US companies.

• He wants to bring manufacturing jobs back to the US by embarking on a seven-point trade policy plan.

1. Withdrawal of the US from the TPP (Trans-PacificPartnership).

2. No comments on TTIP but given Trump’s protectionisticstance it does not bode well.

3. Appointment of tough US negotiators.4. Identify all trade agreement violations and seek to end

them.5. Renegotiate the NAFTA (the North American Free Trade

Agreement) to get ‘a lot better terms’ and, if not feasible,withdraw from it.

6. Label China as currency manipulator.7. Bring trade cases against China both in the US and WTO.8. If China does not cease the practice under (6), Trump

would use clauses under various trade acts to remedy thedisputes.

• There is a risk of a global trade war if other countriesretaliate. While the US is a large and less open economycompared with, e.g. Europe, a more protectionist stancewould lower US potential growth in the long run.

US to become more protectionist – Trump wants to renegotiate

free trade deals to get better terms

Trump wants to shield US workers from globalisationLower US potential growth in case of more protectionist policy

Source: BLS, BEA

88

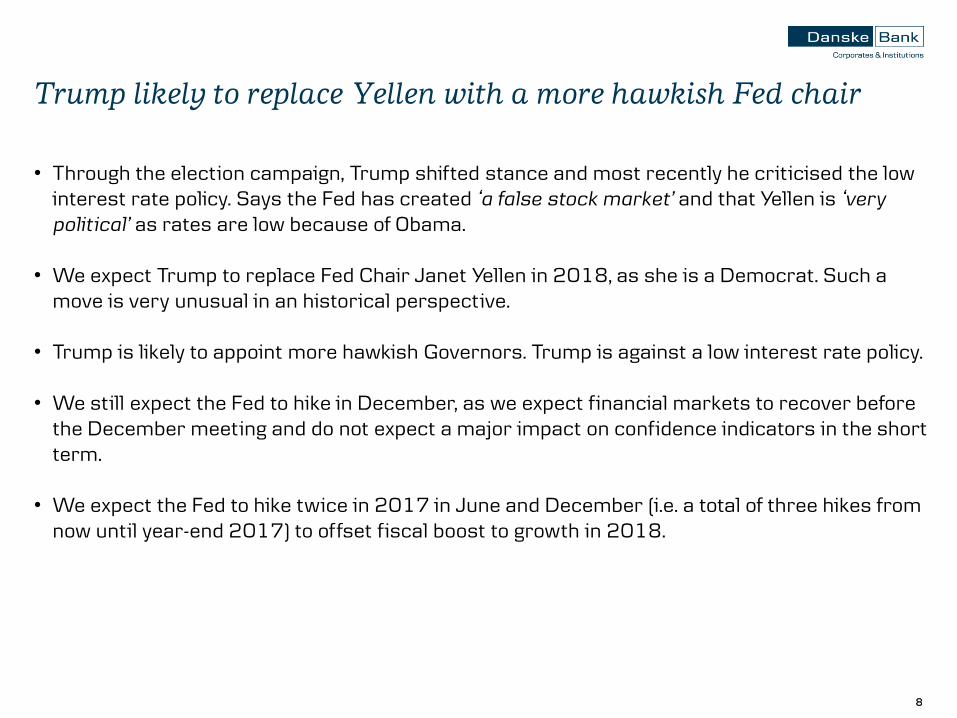

• Through the election campaign, Trump shifted stance and most recently he criticised the low interest rate policy. Says the Fed has created ‘a false stock market’ and that Yellen is ‘very

political’ as rates are low because of Obama.

• We expect Trump to replace Fed Chair Janet Yellen in 2018, as she is a Democrat. Such a move is very unusual in an historical perspective.

• Trump is likely to appoint more hawkish Governors. Trump is against a low interest rate policy.

• We still expect the Fed to hike in December, as we expect financial markets to recover beforethe December meeting and do not expect a major impact on confidence indicators in the short term.

• We expect the Fed to hike twice in 2017 in June and December (i.e. a total of three hikes from now until year-end 2017) to offset fiscal boost to growth in 2018.

Trump likely to replace Yellen with a more hawkish Fed chair

99

Potential regime shift in US foreign policy under Trump

• As Commander in Chief, US President has more power in foreign affairs.

• China is the main enemy, not Russia.

• Improving dialogue with Russia.

• Act as a negotiator in the Syrian conflict and let Russia do the ground job.

• NATO members would be asked to contribute more to NATO if their contributions are below the 2%threshold. This could create possible friction within NATO.

• More sanctions on Iran versus more support of Israel.

Source: Nato

0

0.5

1

1.5

2

2.5

3

3.5

4

2016E

NATO Guideline 2%

Defence expenditures as a share of GDP

(based on 2010 prices and exchange rates)

Trump likely to put pressure on NATO members to contribute 2% in line with NATO guidelines.

1010

• Trump has suggested a much tougher line against illegal immigration. Has said that legalimmigrants are welcome and will receive fair treatment.

• We do not think his plan to build a wall along the Mexico border to prevent illegal immigrantsis realistic.

• However, more realistically, we think he will take measures to reduce illegal immigration and to send home criminal immigrants.

• For national security reasons, he will increase screening of each individual entering thecountry, especially from troubled parts of the world. Has suggested a temporary suspension of immigration entirely from regions where safe and adequate screening cannot occur.

• Immigrants account for a large share of the total labour force and low-skilled immigrantsusually work in low-skilled jobs (manufacturing, transportation, home services). Depending on how much of his policy Trump can get through, a more anti-immigration policy would benegative for potential growth in the long run.

Trump substantially more hawkish versus illegal immigrants

FX – weaker USD versus G10; stronger USD

versus EM

12

EUR/USD – higher short term and in 2017

• EUR/USD has risen above 1.12 on the announcement that Donald Trump will be the next US President. We expect that EUR/USD couldrise a bit further near term to 1.13-1.14.

• Larger fiscal expansions, which can be expected under Trump, have historically tended to drive USD weakness. The exception was Ronald Reagan’s first term in 1981-84, when Fed chairman Paul Volckerraised policy rates sharply, supporting the dollar. We do not expect a sharp rise in real policy rates under Trump’s presidency.

• Fundamentally, the large eurozone-US current account differential and the undervaluation of the EUR should support EUR/USD in 2017.

• However, we expect the Fed to raise interest rates in December and twice in 2017. This, together with political uncertainty shifting back to the eurozone, should mitigate EUR/USD strength in 2017.

• In sum, we forecast EUR/USD to reach 1.15 in 12 months.

9 November 2016

The eurozone-US CA differential is at its widest level in the

history of the eurozone

Source (all charts): Macrobond Financial, Bloomberg, Danske Bank Markets

Danske Bank’s G10 Medium-term Valuation (MEVA) Model

indicates EUR/USD at 1.26 in the medium termFiscal expansions have tended to drive USD weakness

13

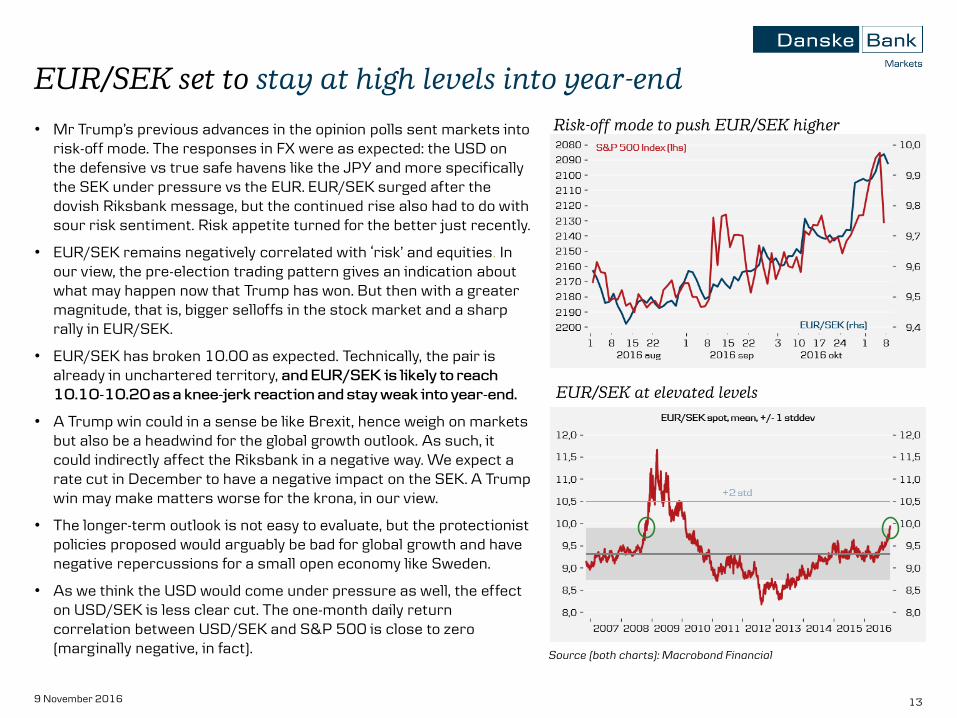

EUR/SEK set to stay at high levels into year-end

• Mr Trump’s previous advances in the opinion polls sent markets into risk-off mode. The responses in FX were as expected: the USD on the defensive vs true safe havens like the JPY and more specifically the SEK under pressure vs the EUR. EUR/SEK surged after the dovish Riksbank message, but the continued rise also had to do with sour risk sentiment. Risk appetite turned for the better just recently.

• EUR/SEK remains negatively correlated with ‘risk’ and equities. In our view, the pre-election trading pattern gives an indication about what may happen now that Trump has won. But then with a greater magnitude, that is, bigger selloffs in the stock market and a sharp rally in EUR/SEK.

• EUR/SEK has broken 10.00 as expected. Technically, the pair is already in unchartered territory, and EUR/SEK is likely to reach

10.10-10.20 as a knee-jerk reaction and stay weak into year-end.

• A Trump win could in a sense be like Brexit, hence weigh on markets but also be a headwind for the global growth outlook. As such, it could indirectly affect the Riksbank in a negative way. We expect a rate cut in December to have a negative impact on the SEK. A Trump win may make matters worse for the krona, in our view.

• The longer-term outlook is not easy to evaluate, but the protectionist policies proposed would arguably be bad for global growth and have negative repercussions for a small open economy like Sweden.

• As we think the USD would come under pressure as well, the effect on USD/SEK is less clear cut. The one-month daily return correlation between USD/SEK and S&P 500 is close to zero (marginally negative, in fact).

9 November 2016

Risk-off mode to push EUR/SEK higher

Source (both charts): Macrobond Financial

EUR/SEK at elevated levels

14

EUR/NOK – higher near term but no game changer

• Deteriorating risk appetite and higher global uncertainty are negatives for the oil price and the NOK short term; especially given the ‘Trump risk’ re-pricing at the beginning of this week.

• However, we see a range of factors limiting the EUR/NOK upside potential. First, markets pricing in a lower probability of a December Fed hike is likely to counter the extent of the risk sell-off. Also, the weaker USD (USD/NOK to move lower) and an adjusting oil supply side would still contribute in lifting the oil price towards our longer-term anchor of USD58/bbl by end-2017. As the US makes up only a limited share of Norwegian exports, more protectionism should primarily hit Norwegian growth indirectly, and as such we do not think the US vote will have any influence on the economic policy outlook in Norway.

• In summary, heightened uncertainty, a lower oil price and year-end

seasonality are likely to send EUR/NOK a little higher near term than

previously projected (9.30-9.40 in 1-2M). For 2017, however, we do not see

the story as much changed and we still expect the long-term fundamentally

overvalued EUR/NOK (and USD/NOK) to move lower, supported by real

rate differentials normalising in the next 12M.

9 November 2016

Oil /risk sentiment set to lift EUR/NOK short term

Year-end seasonality has historically been a NOK negative

Source (all charts): Macrobond, Bloomberg, Danske Bank Markets

US makes up a limited share of Norwegian exports

1515

Source (both charts): Macrobond Financial

• Currently, Denmark holds a current account surplus of 3.5% of GDP versus the US (more than a third of total surplus); hence, strong income flow from the US has been a strong DKK fundamental in recent years.

• Donald Trump’s view on free trade could be a threat to the Danish shipping industry (which makes up a third of Denmark’s total current account surplus). The election of Donald Trump could therefore have a negative impact on Denmark’s external balance, which would create a fundamental headwind for DKK over the long term.

• Note, that Democrat Bernie Sanders has been taking shots at medical sectors in the US, which is a further threat to DKK’s strong fundamentals.

• In the short and medium term, political risk in Europe and high structural savings in Denmark are likely to be more important for DKK and both factors support DKK and our view that EUR/DKK will trade in the low end of the historical trading range on a 12M horizon.

Trump could weaken strong DKK fundamentals

Denmark’s CA with the US is more than 1/3 of total surplus

EUR/DKK set to trade at low end of historical range on 1-12M

Trump could spell trouble for EM

1717

• The possible withdrawal of the US from TPP

and renegotiation of the NAFTA to get ‘a lot

better terms’ (or full withdrawal from it) wouldbe negative for notably Mexico and severalAsian countries.

• Trump could also target China, possibly labelingit as a currency manipulator and bring tradecases against China both in the US and WTO.

• More aggressive trade action by the US couldprompt retaliation by China and other countriesand risk triggering a global trade war.

• On foreign policy, Trump is likely to stir frictions

within Nato. Trump has signalled that he wantsother Nato members to raise their contributionsto 2% of GDP — this could weaken Nato in theshort term, being negative for eastern EuropeanEMs.

Several EMs are vulnerable to more protectionistic US trade

policy…

More aggressive US trade and foreign policies would be negative

for emerging markets

…and global trade would plummet if other countries retaliate

against US trade measures.

Source (both charts): Macrobond Financial

-5

0

5

10

15

20 % of GDPNet exports to the US

1990 2015

TPP

NAFTAUnilateral

1818

• USD/MXN has risen sharply on Trump’s win and we think it may rise further to 21.5 in the next

few days, given its large trade share with the US and Trump’s sharp rhetoric. However, theMexican central bank may hike rates to stabilise the currency. Longer term, the USD/MXN willdepend on how aggressively Trump will be towards trade with Mexico.

• Asian and other Latin American countries and currencies (MYR, VND, KRW and BRL) could alsobe negatively affected to some extent by the Trump victory.

• Other EM regions, notably eastern European EMs, are far less exposed given that their mainexport markets are European countries. However, frictions within Nato could weigh on PLN andHUF.

• Russia and RUB could be a relative winner among EM in the near term. We think that Russiawould benefit from a more positive investor reaction in the short term given Trump’s relativelypositive view, though we see a smaller effect in the longer term given concerns in Congress. ATrump win support our bullish view on RUB.

• China and CNY may be targeted in the short term by the Trump administration, but we do notthink that the US can afford to maintain a hawkish stance in the medium term on China, given theimportance of the Chinese market for the US. Hence, upward pressure on USD/CNY is set topersist over the next 12 months, supporting our current 12M target for the USD/CNY of 7.10.

USD stronger versus most EM currencies

US rates – lower short term; higher medium term

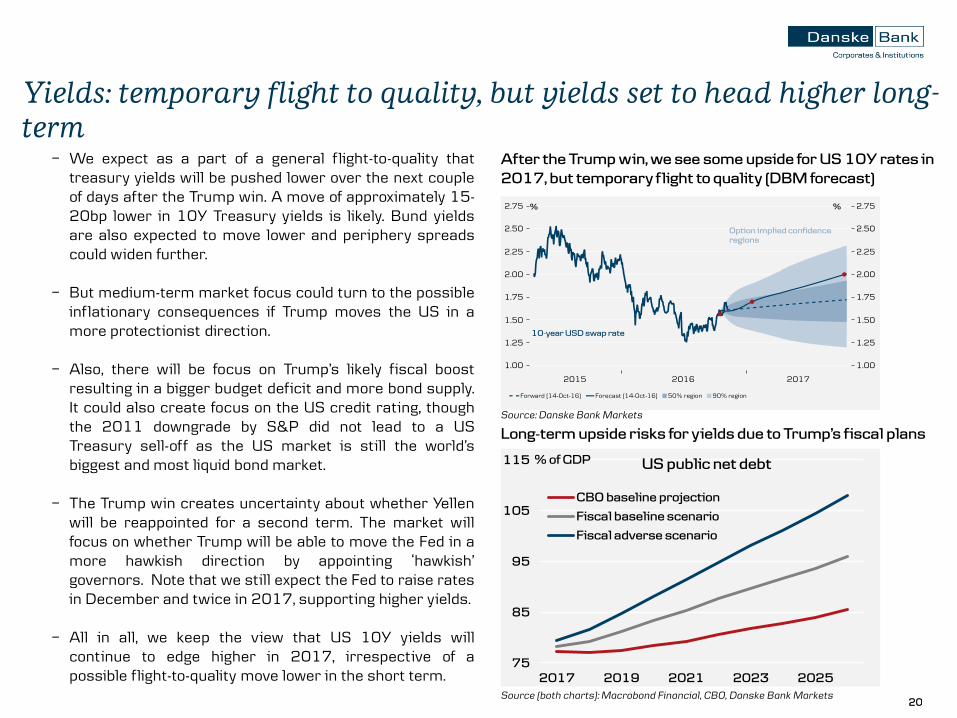

2020

− We expect as a part of a general f light-to-quality thattreasury yields will be pushed lower over the next coupleof days after the Trump win. A move of approximately 15-20bp lower in 10Y Treasury yields is likely. Bund yieldsare also expected to move lower and periphery spreadscould widen further.

− But medium-term market focus could turn to the possibleinf lationary consequences if Trump moves the US in amore protectionist direction.

− Also, there will be focus on Trump’s likely fiscal boostresulting in a bigger budget deficit and more bond supply.It could also create focus on the US credit rating, thoughthe 2011 downgrade by S&P did not lead to a USTreasury sell-off as the US market is still the world’sbiggest and most liquid bond market.

− The Trump win creates uncertainty about whether Yellenwill be reappointed for a second term. The market willfocus on whether Trump will be able to move the Fed in amore hawkish direction by appointing ‘hawkish’governors. Note that we still expect the Fed to raise ratesin December and twice in 2017, supporting higher yields.

− All in all, we keep the view that US 10Y yields willcontinue to edge higher in 2017, irrespective of apossible flight-to-quality move lower in the short term.

After the Trump win, we see some upside for US 10Y rates in

2017, but temporary flight to quality (DBM forecast)

Yields: temporary flight to quality, but yields set to head higher long-

term

Long-term upside risks for yields due to Trump’s fiscal plans

75

85

95

105

115

2017 2019 2021 2023 2025

% of GDP

CBO baseline projection

Fiscal baseline scenario

Fiscal adverse scenario

US public net debt

Source (both charts): Macrobond Financial, CBO, Danske Bank Markets

Source: Danske Bank Markets

Equities – a knee-jerk fall; US to outperform

Europe and EM

Trump wins presidency – Republican congress

Economics

Neutral for growth short-term; moderately negative medium- to long-term. Boost via fiscal policy but countered by protectionism and hawkish immigration policy. Fed forced to premature tightening. Higher EUR/USD short and medium term, but USD to strengthen vs EM and MXN in particular.

Global equities Knee-jerk sharp fall of 5-10% but sell-off to be short-lived

Regional Change to Overweight US. Underweight EU and Nordics.

SectorOverweight Health care, Financials, Industrials, Energy, Basic materials- Underweight Renewables.

Sector NordicsOverweight Health Care, Energy, Industrials. Underweight Renewables, Consumer Staples, Telecom services.

Nordic Shares

Companies likely to benefit: Novo Nordisk, Astra Zeneca, Coloplast, Nordic energy, Volvo, Atlas Copco. Companies likely to suffer: Vestas, Dong, Novozymes, Maersk and DSV.

Trump as President

Eq

uit

ies

23

Disclosures

This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske Bank’). The authors of this presentation are listed on the front page.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in this research report accurately reflect the research analyst’s personal view about the financial instruments and issuers covered by the research report. Each responsible research analyst further certifies that no part of the compensation of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority (UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Finance Society’s rules of ethics and the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-quality research based on research objectivity and independence. These procedures are documented in Danske Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any request that might impair the objectivity and independence of research shall be referred to Research Management and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance or debt capital transactions.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology as well as publicly available statistics for each individual security, issuer and/or country. Documentation can be obtained from the authors on request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including a sensitivity analysis of relevant assumptions, are stated throughout the text.

Date of first publication

See the front page of this research report for the date of first publication.

24

General disclaimerThis research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for informational purposes only. It does not constitute or form part of, and shall under no circumstances be considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant

financial instruments (i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or options, warrants,

rights or other interests with respect to any such financial instruments) (‘Relevant Financial Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that Danske Bank considers to be reliable.

While reasonable care has been taken to ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or

completeness and Danske Bank, its affiliates and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and reflect their judgement as of the date

hereof. These opinions are subject to change and Danske Bank does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report.

This research report is not intended for, and may not be redistributed to, retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior written consent.

Disclaimer related to distribution in the United StatesThis research report was created by Danske Bank A/S and is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer and

subsidiary of Danske Bank A/S, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S. Securities and Exchange Commission. The

research report is intended for distribution in the United States solely to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this research report in connection with distribution in the United States solely to ‘U.S. institutional investors’.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence of research analysts. In addition, the

research analysts of Danske Bank who have prepared this research report are not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial Instrument may do so only by contacting Danske

Markets Inc. directly and should be aware that investing in non-U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and auditing standards of the U.S.

Securities and Exchange Commission.