Download - 150 +22% -25% 130 +37%

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

01 December 2015

Asia Pacific

Equity Research

Investment Strategy

Asia Pacific Equity Strategy STRATEGY

2016 Outlook: A year of positive returns?

Figure 1: MSCI Asia ex-Japan performance around Fed tightening

70

90

110

130

150

170

190

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

MXASJ

-25%

-14%

-21%

-20%

+22%

+15%

+37%

Source: MSCI. We are assuming Dec 2015 is the first Fed rate hike.

■ Three reasons why 2016 could be a year of positive returns. With MSCI

Asia ex-Japan up just 1% in 2014 and down 10% in 2015, we highlight three

reasons why 2016 could be a year of positive returns. One, Figure 1

highlights that while MSCI Asia ex-Japan has historically corrected in the

run-up to the first Fed tightening in 1994 and 2004 and during the 2013 Fed

taper, MXASJ has historically rallied in the six months after. Two, Figure 2

highlights that MXASJ P/B has dropped to 1.37x. This is the lowest P/B start

since 2008-09. Three, MXASJ ROE appears to be bottoming at 11%.

■ Key risks to our call. With the Fed tightening against a weaker macro

backdrop globally and particularly so in China and 2004 (the episode with

the 37% return for MXASJ) associated with NJA ROE rising from 10% to

15%, the key question is whether these differences are big enough to negate

history. The other risk is whether global policy divergences (Fed tightening

versus ECB and BOJ easing) mean the DXY does not fall as it did in prior

episodes. We believe a modest 10% return though is still likely.

■ Overweight Cheapest 4. While past performance is not necessarily a good

guide to the future, the Cheapest 4 outperformed the Expensive 4 by 7%

YTD in 2015. We continue to Overweight the Cheapest 4, which are Korea,

MSCI China, Taiwan and Singapore.

Research Analysts

Sakthi Siva

65 6212 3027

Kin Nang Chik

Analyst Team (Market Strategy) Asia Pacific

Sakthi Siva

Australia Hasan Tevfik

China / Hong Kong Vincent Chan / Li Chen

India Neelkanth Mishra / Prateek Singh

Indonesia Jahanzeb Naseer

Japan

Daisuke Takato

Malaysia

Tan Ting Min

Pakistan

Farhan Rizvi, CFA / Fahd Niaz, CFA

Philippines

Alvin Arogo

Singapore

Gerald Wong

South Korea

Gil Kim

Taiwan

Chung Hsu

Thailand Dan Fineman

Vietnam Dan Fineman / Chate Benchavitvilai

Analyst Team (Sector) Autos and Auto Components

Jatin Chawla / Bin Wang

Banks

Sanjay Jain

Basic Materials

Trina Chen

Chemicals, and Oil Refining/Marketing

Kenneth Whee

Consumer

Kevin Yin / Arnab Mitra / A-Hyung Cho

Environment

Trina Chen

Gaming

Kenneth Fong

Industrials

Edmond Huang / Tim Ross / MinSeok Sinn / Henry Kwon / Lokesh Garg / Baiding Rong /HaYoung Chung

Insurance

Arjan van Veen

Oil & Gas

Thomas Wong

Technology

Manish Nigam

Telecoms

Colin McCallum

Transportation

Tim Ross / Muzhafar Mukhtar / Christopher Siow

Utilities and Renewable Energy

Dave Dai

01 December 2015

Asia Pacific Equity Strategy 2

Focus charts

Figure 2: MSCI Asia ex-Japan price-to-book

0.5

1.0

1.5

2.0

2.5

3.0

Dec-95 Dec-97 Dec-99 Dec-01 Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

Asia ex-JP - Trailing PB

1.37x now

1.23x in Feb 091.19x in Sep 01

0.94x in Aug 98

1.47x in Jan 141.22x in

Mar 031.28x on

24 Aug

Source: MSCI

Figure 3: Asia ex-Japan ROE

10%

11%

12%

13%

14%

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Asia ex Japan ROE

High 14% Nov 2010

11.0%11.3% Dec 2014

Source: Company data, Credit Suisse estimates

Figure 4: CS country tilts Figure 5: CS sector tilts

Aust / NZ

India

Malaysia

Thailand

Philippines

Indonesia

Japan

Singapore

China

Hong Kong

Taiwan

Korea

-5% -4% -3% -2% -1% 0% 1% 2% 3% 4%

Tilt sizeUnderweight Overweight

Health Care

Industrials

Telcos

Consumer Staples

Materials

Utilities

Energy

Discretionary

Real estate

Information Technology

Financials (ex-Real Est.)

-10% -5% 0% 5% 10% 15%

Tilt sizeUnderweight Overweight

Source: MSCI Source: MSCI

MSCI Asia ex-Japan P/B of

1.37x is the lowest P/B start

since 2008-09

We believe a big driver of

NJA's underperformance

over the past five years has

been slowing ROE; we

believe it is now bottoming

at 11%

01 December 2015

Asia Pacific Equity Strategy 3

Table of contents Top picks: Countries and sectors 4

Country Sections 32 Australia 33 China 36 China A-share Market Strategy 39 Hong Kong 42 India 44 Indonesia 48 Japan 51 Malaysia 54 Pakistan 58 Philippines 62 Singapore 67 South Korea 70 Taiwan 74 Thailand 77 Vietnam 80

Sector Sections 83 Autos and Components 84 Banks 86 Basic Materials 88 Chemicals and Oil Refining/Marketing 90 Consumer 92 Environment 94 Gaming 96 Industrials 98 Insurance 100 Oil & Gas 102 Technology 104 Telecoms 106 Transportation 108 Utilities and renewable energy 110

01 December 2015

Asia Pacific Equity Strategy 4

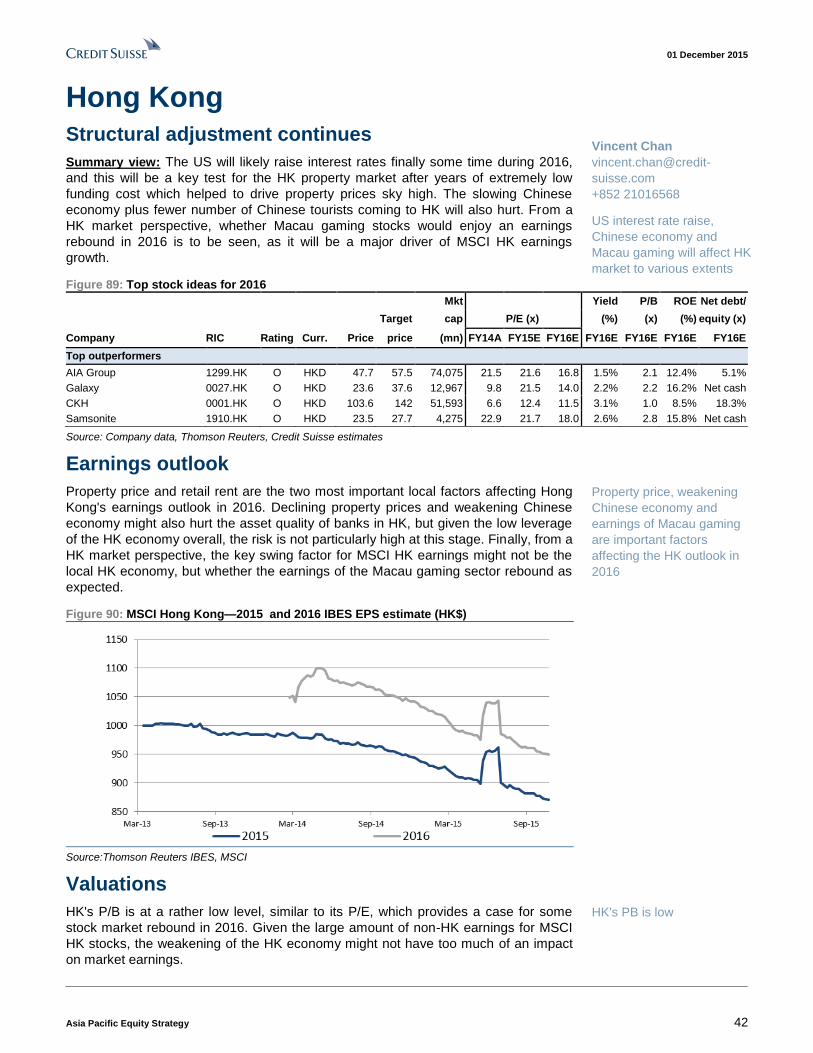

Top picks: Countries and sectors Figure 6: Best Outperform ideas—by country (picked by our country strategists)

Mkt Yield P/B ROE Net debt/

Target cap P/E (x) (%) (x) (%) equity (x)

Company RIC Rating Curr. Price price (mn) FY14A FY15E FY16E FY16E FY16E FY16E FY16E

Australia

Rio Tinto Ord RIO.AX N AUD 47.1 53 61,433 6.8 11.9 20.0 6.3% 1.5 7.5% 33.7% AGL Energy Ord AGL.AX O AUD 16.8 18.4 8,197 15.9 17.4 15.8 4.6% 1.2 7.4% 28.1% Carsales.com Lim Ord CAR.AX O AUD 10.3 11.3 1,792 25.7 24.7 21.8 3.7% 9.6 44.1% 63.3% Lend Lease Group Unt LLC.AX O AUD 12.6 16.6 5,292 8.8 11.8 10.7 4.9% 1.4 13.2% 25.8%

China

China Pacific (H) 2601.HK O HKD 32.3 50 38,141 21.8 13.0 12.6 3.2% 1.7 13.4% Net cash Hikvision 002415.SZ O CNY 36.1 41.6 22,995 31.0 23.1 17.7 1.7% 5.9 33.0% Net cash Goldwind (H) 2208.HK O HKD 13.2 26.3 6,632 16.9 9.5 8.3 6.0% 1.5 18.5% 35.8% Alibaba BABA.N O USD 81.7 98 205,290 44.3 37.5 31.9 0.0% 5.9 18.5% Net cash Geely 0175.HK O HKD 4.2 5.7 4,770 21.3 10.5 7.4 1.6% 1.3 17.5% Net cash Kweichow Moutai 600519.SS O CNY 213.0 270 41,884 15.8 16.1 14.2 2.1% 3.4 24.1% Net cash

China A-share Market Strategy

Midea 000333.SZ O CNY 28.63 41 148,156 11.5 9.8 9.0 4.5% 2.1 25.9% Net cash Wanda Cinema 002739.SZ O CNY 104.81 122 142,405 65.4 95.3 52.8 0.2% 19.0 43.0% Net cash Hengrui Medicine 600276.SS O CNY 50.54 57 119,956 50.2 46.9 40.4 0.3% 8.2 22.4% Net cash GeorTek 002241.SZ O CNY 33.2 41.8 61,479 30.5 36.7 27.9 0.4% 4.5 17.5% Net cash

Hong Kong

AIA Group 1299.HK O HKD 47.7 57.5 74,075 21.5 21.6 16.8 1.5% 2.1 12.4% 5.1% Galaxy 0027.HK O HKD 23.6 37.6 12,967 9.8 21.5 14.0 2.2% 2.2 16.2% Net cash CKH 0001.HK O HKD 103.6 142 51,593 6.6 12.4 11.5 3.1% 1.0 8.5% 18.3% Samsonite 1910.HK O HKD 23.5 27.7 4,275 22.9 21.7 18.0 2.6% 2.8 15.8% Net cash

India

Tech Mahindra TEML.BO O INR 538 700 7,818 20 17 14 1.7% 3 24% -0.3 Hindustan Unilever HLL.BO O INR 811 920 26,420 41 40 34 2.2% 36 113% -1.0 Ultratech Cement ULTC.BO O INR 2,778 3,525 11,470 36 30 19 0.7% 3 18% 0.2 Tata Motors TAMO.BO O INR 401 490 17,424 9 11 8 0.6% 1 20% 0.5

Indonesia

Astra International ASII.JK O IDR 6,175 7,600 18,267 12.8 14.5 12.4 4.1% 2.3 18.6% 40.4% Gudang Garam GGRM.JK O IDR 50,400 61,500 7,086 18.1 18.1 16.1 2.1% 2.4 14.9% 34.6% XL Axiata EXCL.JK O IDR 3,770 5,150 2,351 -35.8 228.2 17.5 3.1% 2.2 12.4% 151.7% Summarecon SMRA.JK O IDR 1,580 1,960 1,666 16.5 17.8 15.0 1.6% 3.0 20.0% 42.6%

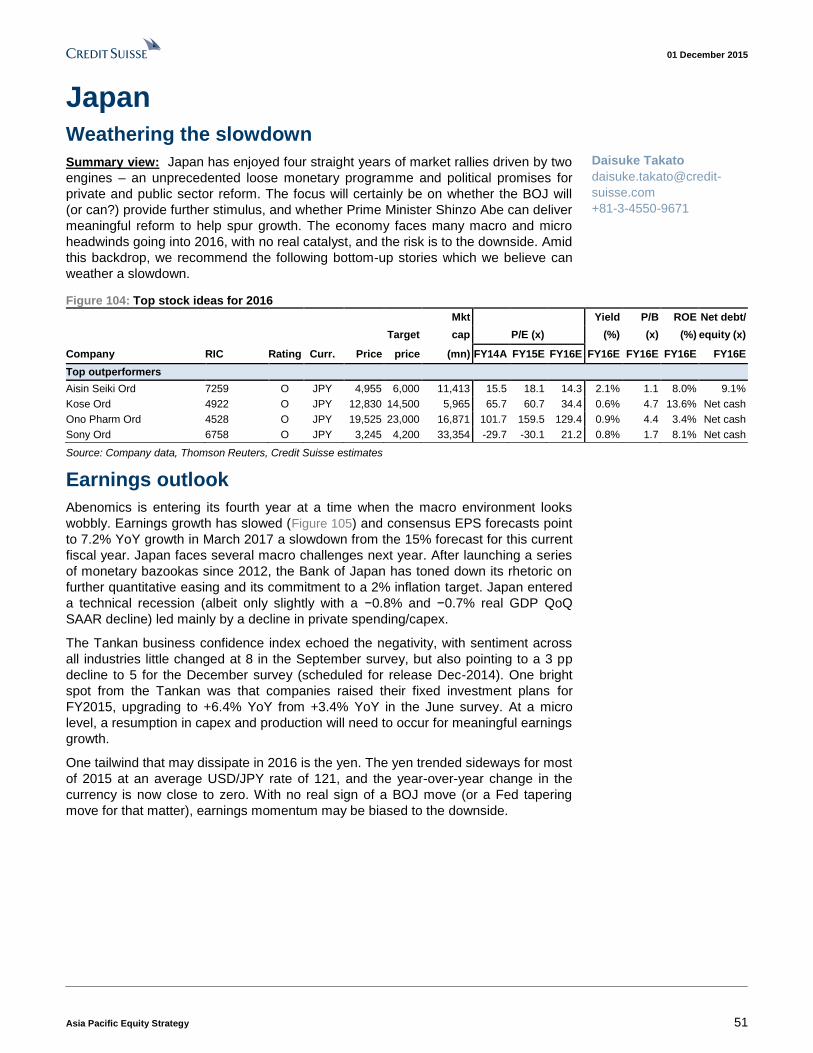

Japan

Aisin Seiki Ord 7259 O JPY 4,955 6,000 11,413 15.5 18.1 14.3 2.1% 1.1 8.0% 9.1% Kose Ord 4922 O JPY 12,830 14,500 5,965 65.7 60.7 34.4 0.6% 4.7 13.6% Net cash Ono Pharm Ord 4528 O JPY 19,525 23,000 16,871 101.7 159.5 129.4 0.9% 4.4 3.4% Net cash Sony Ord 6758 O JPY 3,245 4,200 33,354 -29.7 -30.1 21.2 0.8% 1.7 8.1% Net cash

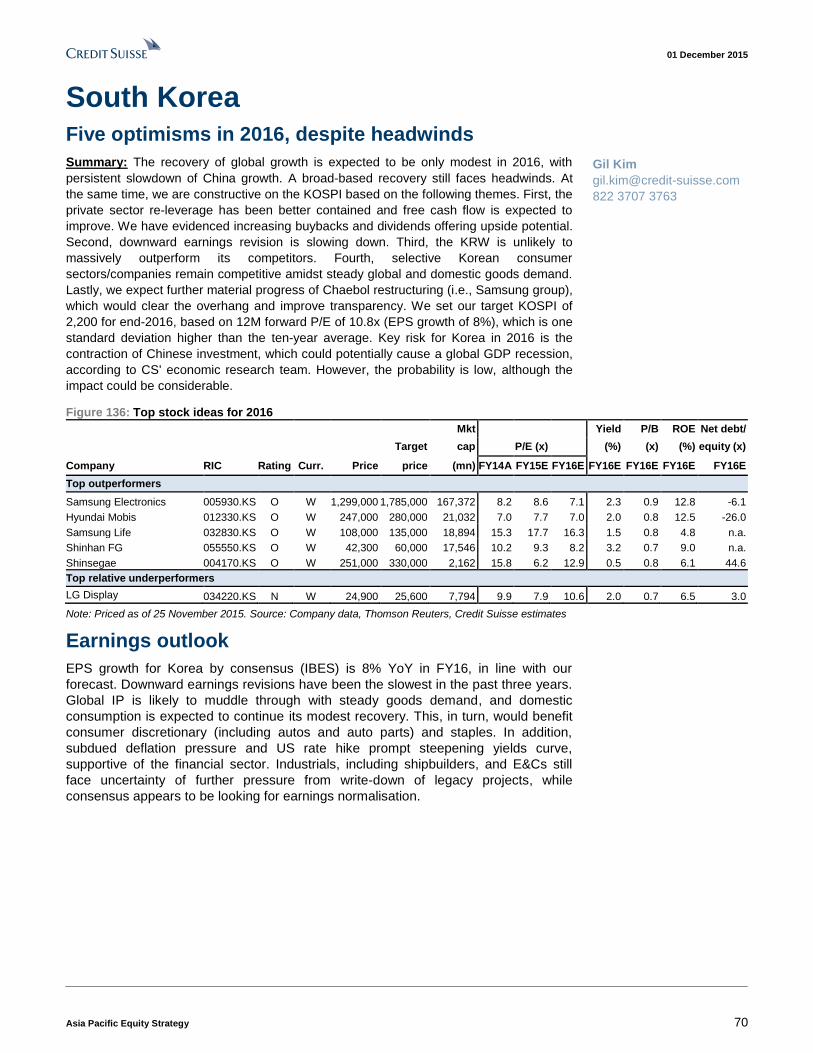

Korea

Sam. Elec. 005930.KS O W 1,299,000 1,785,000 167,372 8.2 8.6 7.1 2.3 0.9 12.8 -6.1 Mobis 012330.KS O W 247,000 280,000 21,032 7.0 7.7 7.0 2.0 0.8 12.5 -26.0 Sam. Life 032830.KS O W 108,000 135,000 18,894 15.3 17.7 16.3 1.5 0.8 4.8 n.a. Shinhan FG 055550.KS O W 42,300 60,000 17,546 10.2 9.3 8.2 3.2 0.7 9.0 n.a. Shinsegae 004170.KS O W 251,000 330,000 2,162 15.8 6.2 12.9 0.5 0.8 6.1 44.6

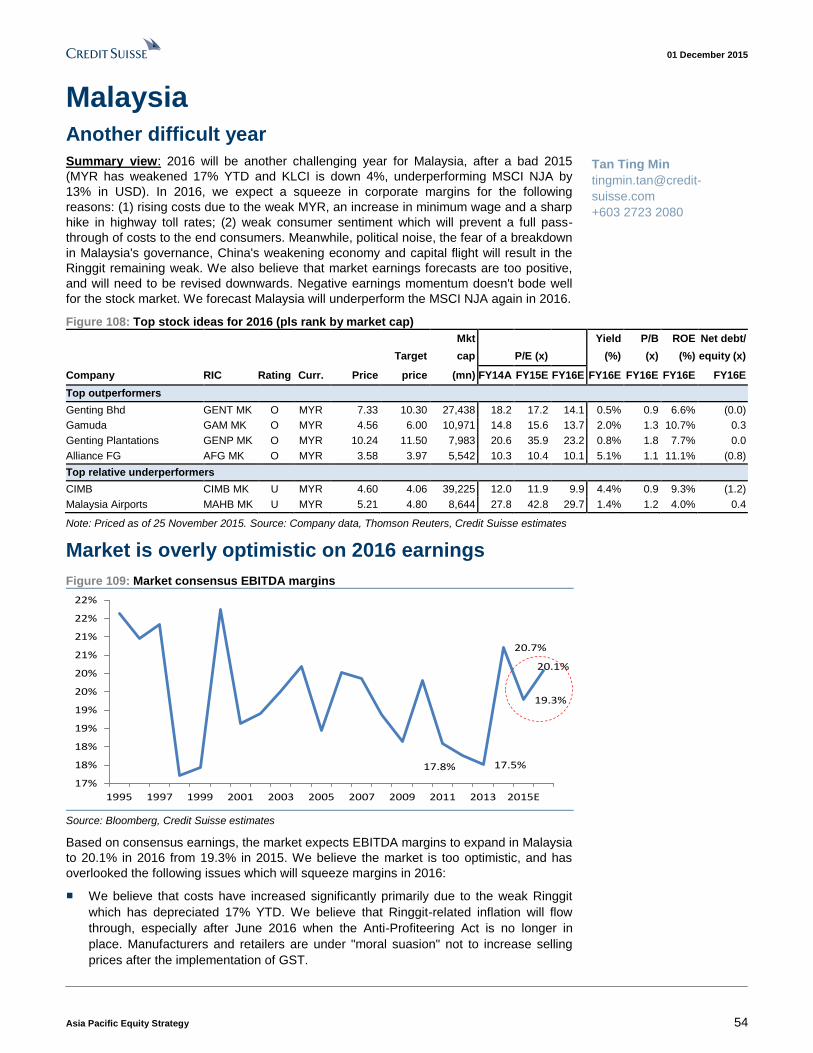

Malaysia

Genting GENT MK O MYR 7.33 10.30 27,438 18.2 17.2 14.1 0.5% 0.9 6.6% (0.0) Gamuda GAM MK O MYR 4.56 6.00 10,971 14.8 15.6 13.7 2.0% 1.3 10.7% 0.3 Gent Plant GENP MK O MYR 10.24 11.50 7,983 20.6 35.9 23.2 0.8% 1.8 7.7% 0.0 Alliance FG AFG MK O MYR 3.58 3.97 5,542 10.3 10.4 10.1 5.1% 1.1 11.1% (0.8)

Pakistan

United Bank Limited UBL.KA O PRs 164 218 1,904 7.9 7.1 1.3 18.0 Pakistan Oilfields PKOL.KA O PRs 310 425 696 8.7 10.2 2.2 21.7 DG Khan Cement DGKH.KA O PRs 136 175 567 7.8 6.9 0.8 11.1 K-Electric KELE.KA O PRs 7.6 10.5 1,993 13.6 8.3 1.3 15.5 Engro Corporation EGCH.KA O PRs 283 368 1,405 8.5 7.2 1.8 24.3

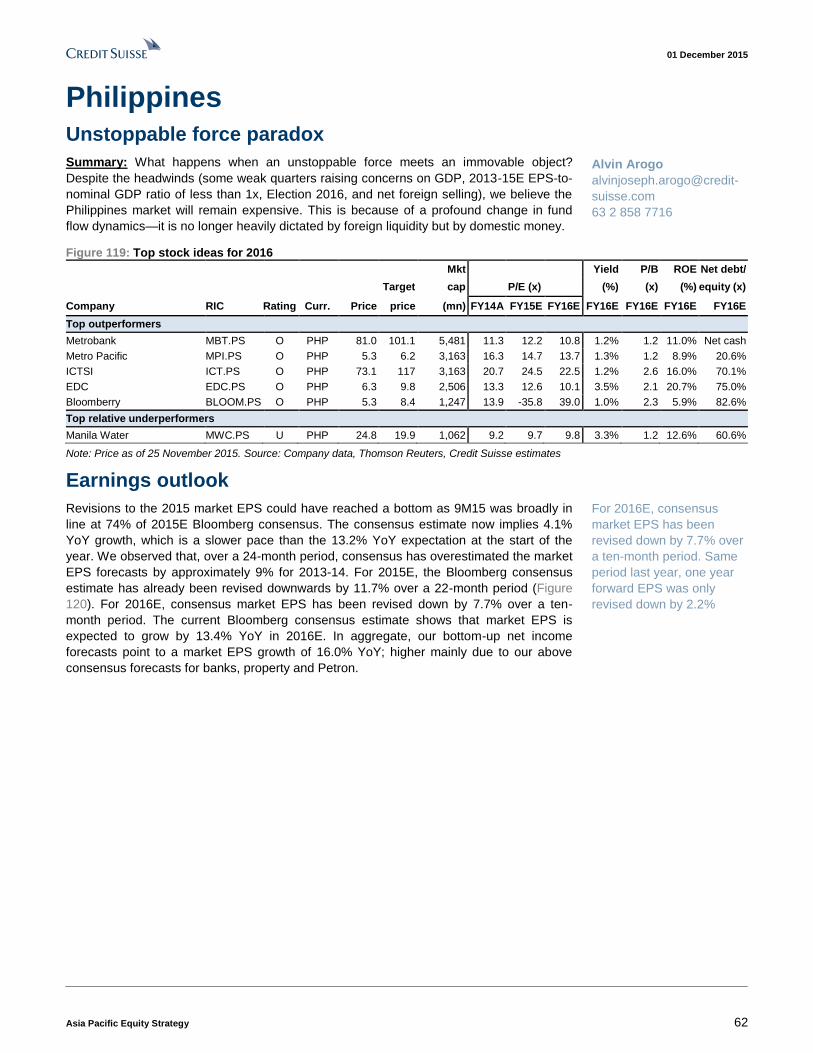

Philippines

Metrobank MBT.PS O PHP 81.0 101.1 5,481 11.3 12.2 10.8 1.2% 1.2 11.0% Net cash Metro Pacific MPI.PS O PHP 5.3 6.211 3,163 16.3 14.7 13.7 1.3% 1.2 8.9% 20.6% ICTSI ICT.PS O PHP 73.1 117 3,163 20.7 24.5 22.5 1.2% 2.6 16.0% 70.1% EDC EDC.PS O PHP 6.3 9.8 2,506 13.3 12.6 10.1 3.5% 2.1 20.7% 75.0% Bloomberry BLOOM.PS O PHP 5.3 8.4 1,247 13.9 -35.8 39.0 1.0% 2.3 5.9% 82.6%

Singapore

CDL CTDM.SI O SGD 7.44 12.00 4,816 14.9 13.4 9.6 2.2 0.7 7.8 19.8 SingTel STEL.SI O SGD 3.80 4.40 43,128 16.6 16.0 15.2 4.8 2.4 16.0 34.1 DBS DBSM.SI O SGD 16.72 22.00 29,931 10.8 9.7 8.7 3.6 0.9 11.6 n.m.

01 December 2015

Asia Pacific Equity Strategy 5

Mkt Yield P/B ROE Net debt/

Target cap P/E (x) (%) (x) (%) equity (x)

Company RIC Rating Curr. Price price (mn) FY14A FY15E FY16E FY16E FY16E FY16E FY16E

Taiwan

SPIL 2325.TW O TWD 45.0 52.0 4,325 12.0 12.2 11.7 6.4 1.22 16.4 3.0 Delta 2308.TW O TWD 158.5 196.0 12,592 18.7 22.5 19.4 3.6 3.60 25.2 0.5 Hon Hai 2317.TW O TWD 84.3 108.0 39,791 9.5 9.0 8.9 5.7 1.91 13.9 -35.1 E.Sun 2884.TW O TWD 19.9 23.0 4,803 11.9 11.0 9.9 2.0 0.45 12.7 n/m Uni-President 1216.TW O TWD 54.2 64.0 9,441 26.6 19.3 16.8 3.6 1.23 18.1 46.6

Thailand

AIS ADVANC.BK O THB 205.0 280 17,087 16.9 15.5 14.5 6.9% 13.0 90.1% 232.7% BTS Group Holdings BTS.BK O THB 9.4 12.2 3,144 54.7 42.3 56.7 7.1% 2.3 4.1% 36.9% Thai Union TU.BK O THB 18.5 22.5 2,475 15.5 17.1 13.7 3.6% 1.8 13.1% 63.7% STECON STEC.BK O THB 24.6 30 1,052 24.7 29.2 24.1 1.9% 3.9 16.0% Net cash C.P. ALL CPALL.BK O THB 48.5 60 12,214 44.6 31.7 25.4 2.8% 10.0 39.2% 358.8%

Vietnam

Vinamilk VNM.HM O VND 125,000 140,000 19.7 17.5 3.3 5.7 32.6

Vingroup VIC.HM O VND 43,400 52,000 23.9 12.2 - 2.2 17.8

Masan Group MSN.HM N VND 70,500 80,000 29.0 21.9 - 1.9 12.3

Note: Priced as of 25 November 2015. Source: Company data, Thomson Reuters, Credit Suisse estimates

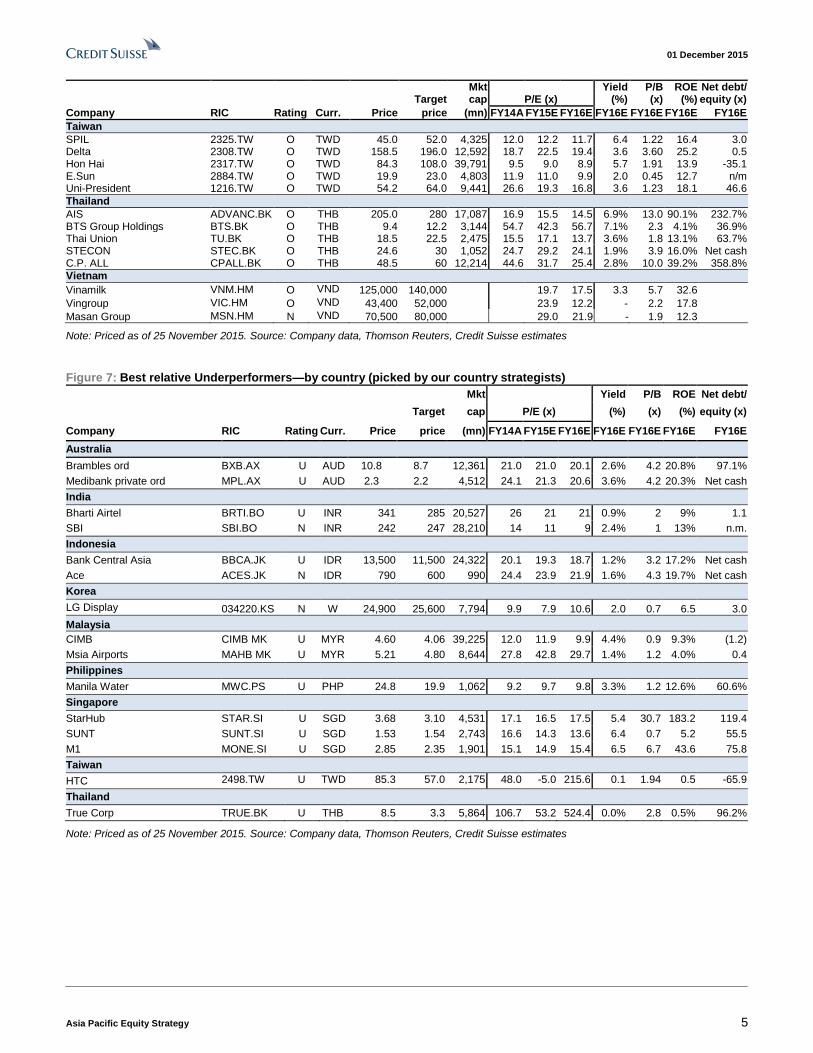

Figure 7: Best relative Underperformers—by country (picked by our country strategists)

Mkt Yield P/B ROE Net debt/

Target cap P/E (x) (%) (x) (%) equity (x)

Company RIC Rating Curr. Price price (mn) FY14A FY15E FY16E FY16E FY16E FY16E FY16E

Australia

Brambles ord BXB.AX U AUD 10.8 8.7 12,361 21.0 21.0 20.1 2.6% 4.2 20.8% 97.1%

Medibank private ord MPL.AX U AUD 2.3 2.2 4,512 24.1 21.3 20.6 3.6% 4.2 20.3% Net cash

India

Bharti Airtel BRTI.BO U INR 341 285 20,527 26 21 21 0.9% 2 9% 1.1

SBI SBI.BO N INR 242 247 28,210 14 11 9 2.4% 1 13% n.m.

Indonesia

Bank Central Asia BBCA.JK U IDR 13,500 11,500 24,322 20.1 19.3 18.7 1.2% 3.2 17.2% Net cash

Ace ACES.JK N IDR 790 600 990 24.4 23.9 21.9 1.6% 4.3 19.7% Net cash

Korea

LG Display 034220.KS N W 24,900 25,600 7,794 9.9 7.9 10.6 2.0 0.7 6.5 3.0

Malaysia

CIMB CIMB MK U MYR 4.60 4.06 39,225 12.0 11.9 9.9 4.4% 0.9 9.3% (1.2)

Msia Airports MAHB MK U MYR 5.21 4.80 8,644 27.8 42.8 29.7 1.4% 1.2 4.0% 0.4

Philippines

Manila Water MWC.PS U PHP 24.8 19.9 1,062 9.2 9.7 9.8 3.3% 1.2 12.6% 60.6%

Singapore

StarHub STAR.SI U SGD 3.68 3.10 4,531 17.1 16.5 17.5 5.4 30.7 183.2 119.4

SUNT SUNT.SI U SGD 1.53 1.54 2,743 16.6 14.3 13.6 6.4 0.7 5.2 55.5

M1 MONE.SI U SGD 2.85 2.35 1,901 15.1 14.9 15.4 6.5 6.7 43.6 75.8

Taiwan

HTC 2498.TW U TWD 85.3 57.0 2,175 48.0 -5.0 215.6 0.1 1.94 0.5 -65.9

Thailand

True Corp TRUE.BK U THB 8.5 3.3 5,864 106.7 53.2 524.4 0.0% 2.8 0.5% 96.2%

Note: Priced as of 25 November 2015. Source: Company data, Thomson Reuters, Credit Suisse estimates

01 December 2015

Asia Pacific Equity Strategy 6

Figure 8: Best Outperform ideas—by sector (picked by our sector heads) Mkt Yield P/B ROE Net debt/

Target cap P/E (x) (%) (x) (%) equity (x)

Company RIC Rating Curr. Price price (mn) FY14A FY15E FY16E FY16E FY16E FY16E FY16E

Autos and Components

Geely 0175.HK O HKD 4.2 5.7 4,770 21.3 10.5 7.4 1.6% 1.3 17.5% Net cash Tata Motors* TAMO.BO O INR 401.1 490 17,449 9.2 11.3 8.3 0.6% 1.5 18.0% 50.6% Maruti Suzuki* MRTI.BO O INR 4,640.5 5,200 21,125 37.8 24.6 17.1 1.1% 4.1 23.8% Net cash Mobis 012330.KS O KRW 247,000 280,000 21,032 7.0 7.7 7.0 2.0% 0.8 11.8% Net cash Astra International ASII.JK O IDR 6175 7,600 18,267 12.8 14.5 12.4 4.1% 2.3 18.6% 40.4%

Banks

HDFC Bank HDBK.BO O INR 1,063.9 1,360 40,414 30.1 25.2 21.5 1.0% 3.7 17.4% Net cash IndusInd Bank INBK.BO O INR 919.6 1,080 8,216 34.2 27.0 21.2 0.8% 3.2 14.1% Net cash SKS SKSM.BO O INR 427.4 520 817 66.0 28.6 20.0 0.0% 4.1 20.5% Net cash SFG 055550.KS O KRW 42,300 60,000 17,546 10.2 9.3 8.2 3.2% 0.6 7.6% Net cash

Basic Materials

Conch 0914.HK O HK$ 21.95 30.00 14,913 8.7 12.5 13.9 3.8 1.3 9.6 4.2 Lee&Man 2314.HK O HK$ 4.62 6.60 2,782 11.4 9.8 8.5 8.5 1.0 12.8 52.9 POSCO 005490.KS O W 171,000 240,000 11,922 21.8 n.a. 9.0 4.7 0.3 3.6 45.5

Chemicals and Oil Refining/Marketing

Lotte Chemical 011170.KS O W 246,500 410,000 7,364 7.2 6.3 1.0 1.0 16.2 15.0 Formosa Plastics 1301.TW O NT$ 76.5 94.0 14,998 16.4 16.3 3.1 2.0 12.9 5.8 Mitsubishi Chem Hldg 4188 O ¥ 830 1,030 9,975 20.0 16.4 1.7 1.2 7.5 71.9

Consumer

JD.com JD.OQ O USD 30 40 41,482 2.2* 1.5* 1.0* 0.0% 6.9 1.1% Net cash Hindustan Unilever HLL.BO O INR 811 920 26,459 45.4 40.7 40.2 1.9% 41.3 102.7% Net cash Amorepacific 090430.KS O KRW 408,500 440,000 20,889 63.0 39.9 30.1 0.3% 5.7 19.0% Net cash Indofood CBP ICBP.JK O IDR 12,600 15,100 5,369 28.2 22.2 18.3 2.2% 4.0 21.8% Net cash

Environment

Dongjiang 0895.HK O HK$ 13.0 23.0 2,615 36.4 28.5 19.0 1.1 3.0 16.7 73.4 BEW 0371.HK O HK$ 6.1 8.0 6,899 29.5 23.7 18.9 2.0 2.8 15.6 115.4 CEI 0257.HK O HK$ 11.8 18.5 6,838 31.1 22.0 15.2 1.9 2.5 17.8 32.8 SIIC SIIC.SI O S$ 0.78 1.50 1,229 24.6 19.3 12.6 0 1.4 11.6 32.0

Gaming

Galaxy 0027.HK O HKD 23.6 37.6 12,967 9.8 21.5 14.0 2.2% 2.2 16.2% Net cash MGM China 2282.HK O HKD 10.3 20 5,031 6.8 11.6 12.1 5.0% 4.3 35.9% 124.5% Kangwon Land 035250.KS O KRW 37,750 54,000 7,065 21.3 17.4 15.2 3.2% 2.6 16.1% Net cash Bloomberry BLOOM.PS O PHP 5.32 8.3 1,247 13.9 -35.8 39.0 1.0% 2.3 5.9% 82.6% Genting Singapore GENS.SI O SGD 0.775 1 6,669 20.6 32.5 22.7 1.3% 1.2 5.4% Net cash Genting Bhd GENT.KL O MYR 7.3 10.3 6,514 18.2 17.2 14.1 0.7% 0.9 6.6% Net cash

Industrials

Goldwind 2208.HK O HKD 13.3 26.3 6.5 17.0 9.6 8.4 5.9 1.6 19.5 35.8 Singapore Air SIAL.SI O SGD 10.47 14.00 8.9 36.3 14.6 12.0 5.0 0.9 8.0 Net cash Voltas VOLT.BO O INR 283.20 345.00 1.4 41.9 27.7 26.9 0.9 4.0 15.6 Net cash Hyundai Mipo 010620.KS O KRW 63,800 90,100 1.1 -2.0 19.1 14.7 0.0 0.7 4.6 125.6 Hyundai Dev 012630.KS O KRW 41,850 70,000 2.7 44.7 12.8 10.0 1.2 1.2 12.2 19.3

Insurance

AMP ORD AMP.AX N AUD 5.7 6.35 12,135 17.5 16.2 15.6 5.1% 2.0 11.9% 145.1% AIA Group 1299.HK O HKD 47.7 57.5 74,075 21.5 21.6 16.8 1.5% 2.1 12.4% 5.1% PICC P&C 2328.HK O HKD 17.3 21.5 33,100 13.4 9.3 10.8 2.3% 1.7 16.0% Net cash

Oil & Gas

CNOOC 0883.HK O HKD 8.75 10.70 50,505 5.4 15.6 12.0 3.3% 0.86 7.2% 21% Reliance Industries RELI.BO O INR 968 1,040 47,183 13.9 13.3 13.1 1.5% 1.32 10.1% 50% PTT PTT.BK O THB 270 321 21,596 13.8 26.3 9.0 4.4% 1.02 11.3% 28%

Technology

Alibaba BABA O USD 81.71 98.00 205,290 37.5 31.9 24.7 0.0 4.9 19.8 (50.7) Baidu Inc BIDU O USD 201.80 210.00 70,934 32.1 37.8 30.9 0.0 5.6 18.2 (73.2) Lenovo Group Ltd 0992.HK O HKD 8.64 11.00 12,384 14.5 (33.4) 10.8 1.9 3.5 32.4 (5.2) Samsung Electronics 005930.KS O KRW 1,299,000 1,785,000 167,372 8.2 8.6 7.1 2.3 0.9 12.1 (6.1) Siliconware Precision 2325.TW O TWD 45.00 52.00 4,315 12.0 12.2 11.7 6.4 1.9 16.1 3.0 Tech Mahindra Limited TEML.BO O INR 537.55 700.00 7,830 20.1 17.4 13.9 1.7 3.0 21.9 (27.8)

Telecoms

Link Net LINK.JK O IDR 3,750 8,450 834 20.4 17.5 11.8 1.7% 2.6 21.7% Net cash China Telecom 0728.HK O HKD 3.9 7.93 40,517 14.6 15.5 11.2 3.6% 0.8 7.4% 36.2% DTAC DTAC.BK O THB 49.0 93 3,253 10.8 19.1 14.9 6.7% 3.6 23.8% 169.1% XL Axiata EXCL.JK O IDR 3,770 5,150 2,351 -35.8 228.2 17.5 3.1% 2.2 12.4% 151.7%

Transportation

JAL 9201.T O JPY 4,371 6,800 12,914 4.6 9.9 8.9 2.8% 1.7 19.5% Net cash AirAsia AIRA.KL O MYR 1.4 1.9 925 7.8 5.0 5.4 3.1% 0.9 16.1% 226.3% SIA SIAL.SI O SGD 10.6 14 9,071 43.3 36.9 14.8 4.3% 1.0 6.7% Net cash

01 December 2015

Asia Pacific Equity Strategy 7

Mkt Yield P/B ROE Net debt/

Target cap P/E (x) (%) (x) (%) equity (x)

Company RIC Rating Curr. Price price (mn) FY14A FY15E FY16E FY16E FY16E FY16E FY16E

Utilities and renewable energy

HNR 0958.HK O HKD 2.3 4.4 2,925 15.5 9.7 6.9 2.9% 0.9 13.7% 309.4% NTPC NTPC.BO O INR 131.2 160 16,296 11.3 12.4 11.9 4.4% 1.3 10.6% 133.4% KEPCO 015760.KS O KRW 49,100 64,000 27,572 6.5 2.6 6.3 2.0% 0.4 7.1% 73.2% EDC EDC.PS O PHP 6.28 9.8 2,506 13.3 12.6 10.1 3.5% 2.1 20.7% 75.0%

Note: Priced as of 25 November 2015. Source: Company data, Thomson Reuters, Credit Suisse estimates

Figure 9: Best relative Underperformers—by sector (picked by our sector heads) Mkt Yield P/B ROE Net debt/

Target cap P/E (x) (%) (x) (%) equity (x)

Company RIC Rating Curr. Price price (mn) FY14A FY15E FY16E FY16E FY16E FY16E FY16E

Autos and Components

Weichai Power (H) 2338.HK U HKD 8.3 6 5,929 5.5 16.3 11.2 4.5% 0.8 7.1% Net cash

Banks

SBI SBI.BO N INR 241.5 247 28,251 15.6 13.8 11.3 1.9% 1.3 10.9% Net cash Maybank MBBM.KL U MYR 8.4 6.8 19,491 11.7 12.7 13.1 5.8% 1.4 10.4% Net cash

Basic Materials

Yanzhou 1171.HK U HK$ 3.63 3.00 2,289 19.2 n.a. n.a. n.a. 0.4 -5.6 135.6 Tata TISC.BO U RS 224.35 180.00 3,320 6.1 n.a. 8.8 3.6 0.7 7.8 238.1

Chemicals and Oil Refining/Marketing

FCFC 1326.TW N NT$ 73.8 76.0 13,322 17.2 16.5 2.9 2.0 12.8 9.2 FPCC 6505.TW N NT$ 77.7 84.0 22,795 17.3 20.9 4.0 2.6 12.7 30.0

Consumer

Sa Sa 0178.HK U HKD 2.81 1.75 1,031 8.6 9.5 18.2 6.4% 3.5 19.8% Net cash Siam Global GLOBAL.BK U THB 10.8 8.8 1,055 53.6 39.6 31.8 0.2% 3.2 10.0% 22.4%

Environment

BJC 600008.SS U Rmb 11.1 8.7 4,203 40.2 38.7 34.1 1.7 3.0 8.9 127.0

Industrials

SEG 2727.HK U HKD 4.81 2.20 19.2 21.0 28.9 25.5 1.2 1.2 4.9 Net cash Evergreen 2603.TW U TWD 13.05 13.00 1.4 -30.9 -21.6 22.9 1.3 0.8 3.6 58.0 BHEL BHEL.BO U INR 173.35 155.00 6.4 29.9 21.2 16.4 1.3 1.1 7.1 Net cash

Insurance

Bangkok Life BLA.BK U THB 54.25 39.25 2,591 34.5 25.3 19.6 1.1% 2.9 15.1% n.a. MEDIBANK PRIVATE ORD MPL.AX U AUD 2.26 2.2 4,512 24.1 21.3 20.6 3.6% 4.2 20.3% Net cash

Oil & Gas

Anton Oil 3337.HK U HKD 0.98 0.80 280 -9.0 -11.2 -12.4 - 1.02 -8.2% 100% Sinopec SSC - H 1033.HK U HKD 2.30 1.90 18,531 11.9 -11.6 -51.0 - 1.22 -2.4% 45%

Technology

LG Electronics Inc 066570.KS N KRW 56,100 46,200 8,031 13.5 23.0 18.4 0.8 0.7 3.6 51.0 MediaTek Inc. 2454.TW N TWD 262.50 250.00 14,480 8.8 14.8 16.7 4.9 1.6 9.7 (63.3) Pegatron 4938.TW N TWD 84.60 93.00 6,776 13.6 9.0 9.0 6.8 1.4 15.6 (36.7) Quanta Computer 2382.TW U TWD 52.00 46.00 6,180 10.6 11.6 11.2 6.7 1.7 14.8 (10.4)

Telecoms

True Corp TRUE.BK U THB 8.5 3.3 5,864 106.7 53.2 524.4 0.0% 2.8 0.5% 96.2% Idea Cellular IDEA.BO U INR 139.9 115 7,587 23.6 15.7 17.2 0.7% 2.0 11.4% 160.1%

Transportation

EMC 2603.TW U TWD 12.6 13.0 1,363 -29.8 -20.9 22.1 1.3% 0.8 3.5% 58.0% Westports WPHB.KL U MYR 4.25 3.75 3,441 28.3 29.4 23.5 3.2% 7.1 30.3% 38.7%

Utilities and renewable energy

CLP 0002.HK U HKD 66 62 21,515 14.9 15.6 15.3 4.2% 1.7 11.4% 63.0% EA EAm.BK U THB 24.4 20 2,551 56.6 33.5 19.1 0.2% 6.9 36.4% 99.2%

Source: Company data, Thomson Reuters, Credit Suisse estimates

01 December 2015

Asia Pacific Equity Strategy 8

2016 Outlook: A year of positive returns?

Three reasons why 2016 could be a year of positive returns. With MSCI Asia ex-Japan

up just 1% in 2014 and down 10% in 2015, we highlight three reasons why 2016 could be

a year of positive returns.

One, Figure 1 highlights that while MSCI Asia ex-Japan has historically corrected in the

run-up to the first Fed tightening in 1994 and 2004 and during the 2013 Fed taper, MXASJ

has historically rallied in the six months after.

Two, Figure 2 highlights that MXASJ P/B has dropped to 1.37x. This is the lowest P/B start

since 2008-09.

Three, MXASJ ROE appears to be bottoming at 11%.

Key risks to our call. With the Fed tightening against a weaker macro backdrop globally

and particularly so in China and 2004 (the episode with the 37% return for MXASJ)

associated with NJA ROE rising from 10% to 15%, the key question is whether these

differences are big enough to negate history. The other risk is whether global policy

divergences (Fed tightening versus ECB and BOJ easing) mean the DXY does not fall as

it did in prior episodes. We believe a modest 10% return though is still likely.

Overweight Cheapest 4. While past performance is not necessarily a good guide to the

future, the Cheapest 4 outperformed the Expensive 4 by 7% YTD in 2015. We continue to

Overweight the Cheapest 4 which are Korea, MSCI China, Taiwan and Singapore. We

also continue to Underweight the Expensive 4, which are the Philippines, India, Indonesia

and Malaysia.

History suggests MXASJ rallies after the first Fed

tightening

While history is not always a good guide to the future, the performance of MXASJ in the

current episode in the lead-up to the first Fed tightening (which we expect in December

2015) appears to suggest history is repeating itself. Figure 1 highlights that MXASJ has

corrected by 20% in the current episode. The 20% correction from the highs is fairly similar

to the corrections ranging from 14% at the Fed taper episode to 21% in the 2004 Fed

tightening and to 25% in the 1994 Fed tightening.

Figure 10: MSCI World performance around Fed tightening

85

90

95

100

105

110

115

120

125

130

135

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

MXWD

-8.2%

-8.7%

-8.8%-8%

+17%

+9%

+18%

Source: MSCI. We are assuming Dec 2015 is the first Fed rate hike.

Three reasons why 2016

could be a year of positive

returns for MSCI Asia ex-

Japan

History suggests MXASJ

rallies after the first Fed

tightening

For MSCI World, corrections

are smaller (than MXASJ) in

the run-up to Fed tightening,

and rallies after the first Fed

tightening are also smaller

01 December 2015

Asia Pacific Equity Strategy 9

Figure 1 also highlights that MXASJ bottomed one month prior to the start of Fed

tightening in the 2004 episode versus one month after the start in the 1994 and 2013

episodes. The rally in MXASJ from those lows to the six months after the first Fed

tightening ranged from 15% in the 2013 episode to 22% in the 1994 episode to 37% in the

2004 episode.

For MSCI World, Figure 6 highlights that the corrections are much smaller than for MXASJ

at around 8% to 9%. Similarly, the rally from the lows to the highs about six months later

also seems to be smaller at between 9% and 18%.

We believe history is supported by valuations, with MXASJ P/B dropping to 1.37x in the

current episode. Figure 7 highlights that the current 1.37x P/B is lower than the lows of

1.47x in the 2013 episode, 1.62x in the 2004 episode and 2.13x in the 1994 episode.

Figure 11: MSCI Asia ex-Japan price-to-book around Fed tightening

1.0

1.5

2.0

2.5

3.0

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

MXASJ - Trailing PB

1.37x nowLow 1.47x

Low 1.62x

Low 2.13x

Source: MSCI. We are assuming Dec 2015 is the first Fed rate hike.

For MSCI World, Figure 8 highlights that the current P/B of 2.07x is right in the middle of

the range of previous Fed tightening episodes.

Figure 12: MSCI World price-to-book around Fed tightening

1.6

1.8

2.0

2.2

2.4

2.6

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

MXWD - Trailing PB

2.07x now

Low 2.32x

Low 2.03x

Low 1.85x

Source: MSCI. We are assuming Dec 2015 is the first Fed rate hike.

We believe history is

supported by valuations with

MXASJ P/B of 1.37x below

the lows seen at the start of

previous rallies

For MSCI World, the current

P/B of 2.07x is right in the

middle of the range seen

during previous Fed

tightening episodes

01 December 2015

Asia Pacific Equity Strategy 10

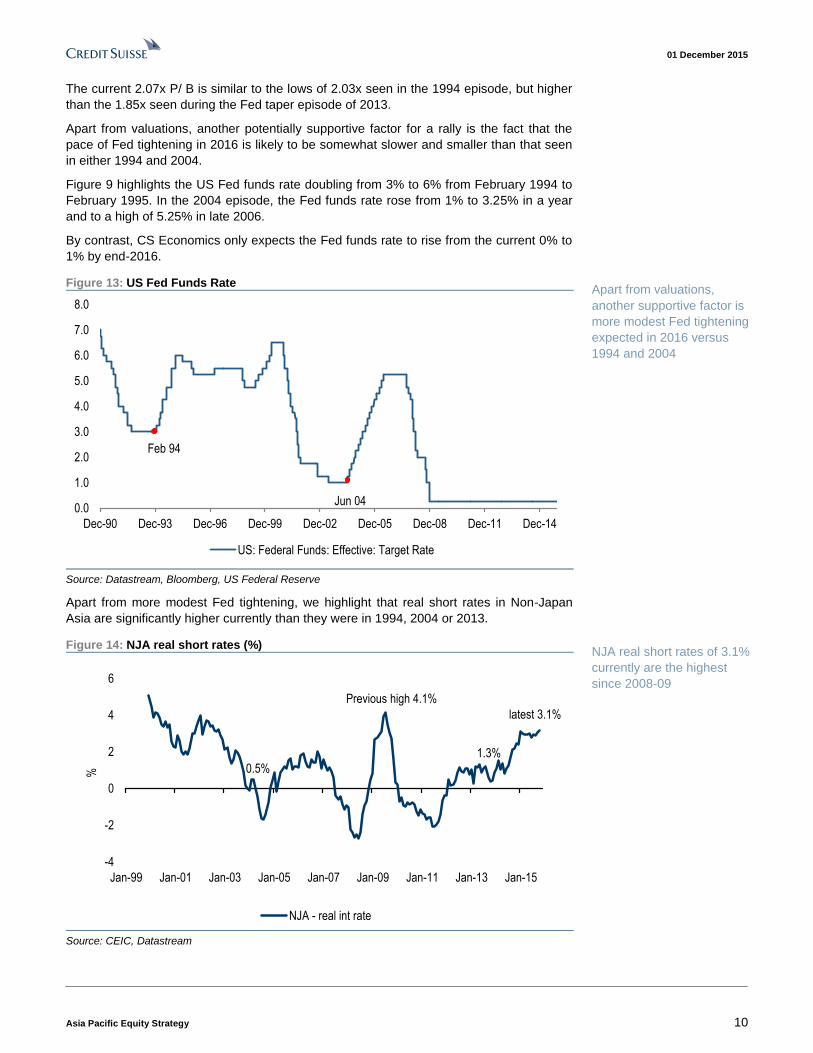

The current 2.07x P/ B is similar to the lows of 2.03x seen in the 1994 episode, but higher

than the 1.85x seen during the Fed taper episode of 2013.

Apart from valuations, another potentially supportive factor for a rally is the fact that the

pace of Fed tightening in 2016 is likely to be somewhat slower and smaller than that seen

in either 1994 and 2004.

Figure 9 highlights the US Fed funds rate doubling from 3% to 6% from February 1994 to

February 1995. In the 2004 episode, the Fed funds rate rose from 1% to 3.25% in a year

and to a high of 5.25% in late 2006.

By contrast, CS Economics only expects the Fed funds rate to rise from the current 0% to

1% by end-2016.

Figure 13: US Fed Funds Rate

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Dec-90 Dec-93 Dec-96 Dec-99 Dec-02 Dec-05 Dec-08 Dec-11 Dec-14

US: Federal Funds: Effective: Target Rate

Feb 94

Jun 04

Source: Datastream, Bloomberg, US Federal Reserve

Apart from more modest Fed tightening, we highlight that real short rates in Non-Japan

Asia are significantly higher currently than they were in 1994, 2004 or 2013.

Figure 14: NJA real short rates (%)

-4

-2

0

2

4

6

Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

%

NJA - real int rate

latest 3.1%

Previous high 4.1%

1.3%

0.5%

Source: CEIC, Datastream

Apart from valuations,

another supportive factor is

more modest Fed tightening

expected in 2016 versus

1994 and 2004

NJA real short rates of 3.1%

currently are the highest

since 2008-09

01 December 2015

Asia Pacific Equity Strategy 11

So we do not expect Asian economies to follow the Fed in tightening. We think the bias

still remains for countries to ease, particularly if forex pressures eases.

Figure 10 highlights that real short rates in NJA (weighted by GDP) are currently 3.1%.

These are the highest real short rates since 2008-09. The current 3.1% compares

favourably with 1.3% in 2013 and just 0.5% in 2004. We use real short rates as a rough

proxy for the stance of monetary policy with higher real short rates suggesting more room

for central banks to cut rates. While India continues to have the highest real short rates if

rates are deflated by the WPI (Wholesale Price Index), China's RRR of 17% still provides

the PBOC with plenty of room to ease policy.

Figure 15: US Fed Funds Rate versus US real GDP growth (YoY %)

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Dec-93 Dec-96 Dec-99 Dec-02 Dec-05 Dec-08 Dec-11 Dec-14

Rea

l GD

P Y

oY%

Fed

fund

s ta

rget

rat

e (%

)

US: Federal Funds: Effective: Target Rate US Real GDP YoY%

4% in 1994

3.8% in 2004

2.2% in 2013

2.6% in 20152.8% in 2016

Source: Consensus Economics, CEIC, Datastream, Bloomberg, US Federal Reserve

While lower price-to-book coupled with significantly higher real short rates in NJA support

our case for a rally in MXASJ once the Fed tightens, there are some differences that may

be considered more negative for Asian returns.

Figure 16: US Fed funds rate versus China real GDP growth (YoY %)

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

15.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Dec-93 Dec-96 Dec-99 Dec-02 Dec-05 Dec-08 Dec-11 Dec-14

Rea

l GD

P Y

oY%

Fed

fund

s ta

rget

rat

e (%

)

US: Federal Funds: Effective: Target Rate China Real GDP YoY%

6.8% in 20156.5% in 2016

7.7% in 2013

10.1% in 2004

13.1% in 1994

Source: Consensus Economics, CEIC, Datastream, Bloomberg, US Federal Reserve

In the past Fed tightening

cycles, US real GDP growth

was stronger than is

expected in 2016E

China's real GDP growth in

2016E much weaker than

1994 and 2004

01 December 2015

Asia Pacific Equity Strategy 12

In past cycles when the Fed was tightening, US and global growth was significantly

stronger and this provided a lot of impetus to Asian exports, growth and ROE more

generally. Figure 11 highlights that US real GDP grew by 4% in 1994 and 3.8% in 2004

when the Fed was tightening back then. This compares with a less robust 2.8% growth

expected in 2016E.

More so than US real GDP growth, Figure 12 highlights the much weaker macro backdrop

from China. Consensus Economics expects China's real GDP growth to be only 6.5% in

2016E versus 7.7% in 2013, 10.1% in 2004 and 13.1% in 1994. As a result of this global

growth divergence, CS Economics expects the ECB and the BOJ as being likely to ease

further rather than following the Fed in tightening as in previous cycles. Please see 2016

Global Outlook report of 12 November for more details. The question then is whether we

are likely to see falls in the DXY (trade-weighted US dollar) as occurred in 1994, 2004 and

2013 after the first Fed tightening, given this policy divergence.

Figure 17: DXY (trade-weighted US dollar) around Fed tightening

85

90

95

100

105

110

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

DXY Index

11% fall in 1994

6% fall in 2013

12% fall in 2004

Source: Bloomberg, Datastream

Figure 13 highlights the 6% to 12% falls in the DXY following the first Fed tightening in 1994,

2004 and 2013, which were about 30% to 40% of the return from MXASJ during the rallies.

Figure 18: NJA ROE around Fed tightening

8

9

10

11

12

13

14

15

16

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

Asia ex-JP - ROE (%)

11%

Source: Company data, Credit Suisse estimates. We are assuming Dec 2015 is the first Fed rate hike.

Historically, the DXY has

fallen after the Fed first

tightens; the question is

whether this time is different

NJA ROE in 2004 very

different to current episode

rising from a low of 10% to a

high of nearly 15%

But current ROE is similar to

2013 and above 1994

01 December 2015

Asia Pacific Equity Strategy 13

We do emphasise though that NJA is more of a commodity importer (with only Malaysia and

Indonesia being exceptions) and that weaker commodity prices, which may follow DXY

strength (if this time is different) actually benefit NJA, compared with Latin America or EMEA.

The next question for investors is whether given the weaker Asia, and particularly China

backdrop, Asian ROEs are lower today than they were in 1994, 2004 and 2013. Figure 14

highlights that only in 2004 was there a significant difference in ROE with NJA ROE rising

from a low of 10% to a high of nearly 15%. In 2013, NJA ROE was around 12.2% when

the Fed started its taper and ROE slowed marginally to 11.8% in the 12 months after. In

the 1994 episode, NJA ROE was lower at around 9% when the Fed started to tighten.

At the country level, it appears that markets that corrected less in the run-up to Fed

tightening like Japan and Taiwan have historically had smaller rallies thereafter and vice

versa. But Figure 18 highlights some differences in the current episode versus prior

episodes such as Taiwan's ROE being significantly higher currently than it was in the prior

three Fed tightening episodes.

Figure 19: MSCI Japan around Fed tightening Figure 20: MSCI Japan P/B around Fed tightening

80

90

100

110

120

130

140

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

MSCI Japan

-24.5%

-5.7%

-18.6% -12%

+36.6%

+24%

+15%

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

MSCI Japan - Trailing PB

1.38x now

1.88x

1.65x

1.23x

Source: MSCI. We are assuming Dec 2015 is the first Fed rate hike. Source: MSCI. We are assuming Dec 2015 is the first Fed rate hike.

Figure 21: MSCI Taiwan around Fed tightening Figure 22: Taiwan ROE around Fed tightening

70

90

110

130

150

170

190

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

MSCI Taiwan

-20%

-11%

-27%-21.5%

+40%

+19%

+11%

4

6

8

10

12

14

16

18

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

Taiwan - ROE (%)

14.4% now

Source: MSCI. We are assuming Dec 2015 is the first Fed rate hike. Source: Company data, Credit Suisse estimates. We are assuming

Dec 2015 is the first Fed rate hike.

Conversely, markets that corrected significantly in the run-up to Fed tightening—like India

and Indonesia—appeared to be associated with stronger rallies post the first Fed

tightening. But Figures 20 and 22 highlight significant differences though between the

current episode and the three others particularly in terms of ROE. For Indonesia ROE, the

current ROE is the second lowest ROE of the four and the episode, which had lower ROE

was associated with a sharp rise in ROE. Similarly, with India, ROE currently is close to

the lowest of the four episodes.

Countries that corrected

less in the run-up to Fed

tightening appeared to have

smaller rallies post the first

Fed tightening

01 December 2015

Asia Pacific Equity Strategy 14

Figure 23: MSCI Indonesia around Fed tightening Figure 24: Indonesia ROE around Fed tightening

60

80

100

120

140

160

180

200

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

MSCI Indonesia

-29.5%

-24%

-35%-23%

+20.7%

+27%

+61%

8

10

12

14

16

18

20

22

24

26

28

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

Indonesia - ROE (%)

18.2% now

Source: MSCI. We are assuming Dec 2015 is the first Fed rate hike. Source: Company data, Credit Suisse estimates.

Figure 25: MSCI India around Fed tightening Figure 26: India ROE around Fed tightening

70

90

110

130

150

170

190

210

230

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

MSCI India

-15.6%

-27%

-29%-18%

+23.3%

+57%

+52%

8

10

12

14

16

18

20

22

24

-9m -6m -3m 0m +3m +6m +9m +12m

Feb-94 Jun-04 May-13 current

India - ROE (%)

14.1% now

Source: MSCI. We are assuming Dec 2015 is the first Fed rate hike. Source: Company data, Credit Suisse estimates.

MXASJ P/B of 1.37x, lowest start since 2008-09

Figure 23 highlights that MXASJ price-to-book has dropped to 1.37x. This is the lowest

start since 2008-09.

Figure 27: MSCI Asia ex-Japan price-to-book

0.5

1.0

1.5

2.0

2.5

3.0

Dec-95 Dec-97 Dec-99 Dec-01 Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

Asia ex-JP - Trailing PB

1.37x now

1.23x in Feb 091.19x in Sep 01

0.94x in Aug 98

1.47x in Jan 141.22x in

Mar 031.28x on

24 Aug

Source: MSCI

If we look at the price-to-book on 31 December in prior years, the current 1.37x compares

favourably with 1.50x in 2014, 1.54x in 2013, 1.63x in 2012, 1.55x in 2011, 2.11x in 2010,

2.1x in 2009 and 1.31x in 2008.

MXASJ P/B of 1.37x is just

10% above GFC lows of

1.23x

01 December 2015

Asia Pacific Equity Strategy 15

The current P/B of 1.37x is about 10% higher than the 1.23x seen at the lows in 2008-09.

Except for 1997-98, P/B at the last three lows was around 1.2x book with 1.19x in the

2001 global recession, 1.22x in the 2003 SARS episode and 1.23x in the 2008-09 GFC.

As we have highlighted previously, we do believe the current episode is very different to

1997-98 with much lower corporate net debt to equity, with forex reserves exceeding

short-term external debt, overall NJA running a current account surplus, lower capex-to-

sales and ROE currently of 11% versus just 1.7% at the 1997-98 lows.

NJA's ROE appears to be bottoming at 11%

As we have highlighted previously, a key driver of NJA's underperformance over the past

five years has been its slowing ROE. Figure 24 highlights that NJA ROE has slowed from

a high of 14% in late 2010 to 11% currently.

Figure 28: Asia ex-Japan ROE

10%

11%

12%

13%

14%

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Asia ex Japan ROE

High 14% Nov 2010

11.0%11.3% Dec 2014

Source: Company data, Credit Suisse estimates

This slowing in NJA ROE has occurred during a period when Japan's ROE has risen from

a low of 3.4% in March 2012 to 8.4% currently.

Figure 29: Japan ROE

-4%

-2%

0%

2%

4%

6%

8%

10%

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

MSCI Japan ROE

8.4%

3.4%

Source: MSCI

NJA ROE has slowed over

the past five years from 14%

in late 2010 to 11%

currently; this, in our view,

has been a key driver of

NJA's underperformance

Particularly as NJA ROE

slowed while Japan's ROE

rose

01 December 2015

Asia Pacific Equity Strategy 16

While Japan's ROE rose, US ROE remained steady at a very high 14%. While this

explains nearly five years of underperformance, the question now for investors is whether

NJA's ROE is finally bottoming.

Figure 30: US ROE

7%

8%

9%

10%

11%

12%

13%

14%

15%

16%

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

MSCI USA ROE

13.8%

Source: MSCI

If we look at the ROE data, ROE has been between 11% and 11.3% for NJA over much of

the past year. We believe our view that ROE is bottoming is also supported by the fact that

Korea's ROE has risen from a low of 7.9% in December 2014 to 9.5% currently. While

Korea's ROE has been rising over much of the past year, the key question is how

sustainable is the pick-up.

Figure 31: Korea ROE

4%

6%

8%

10%

12%

14%

16%

18%

Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12 Dec-14

Korea - ROE

9.5% now

low 7.9%in Dec 14

low 7.6% in 2009

Source: Company data, Credit Suisse estimates

We believe this is sustainable as six of the nine sectors in Korea are associated with rising

ROE. These six sectors are Utilities, Consumer Staples, Materials, Financials, Energy and

Telcos.

NJA's ROE slowed while US

ROE remained stable at a

high 14% plus

Key question now is

whether NJA's ROE is

bottoming supported by the

rise in Korea's ROE

Figure 27 shows Korea's

ROE rising from a low of

7.9% in Dec 2014 to 9.5%

currently

Six of nine sectors

associated with rising ROE

in Korea

01 December 2015

Asia Pacific Equity Strategy 17

Figure 32: Korea utilities ROE Figure 33: Korea staples ROE

-10%

-5%

0%

5%

10%

15%

20%

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Korean Utilities - ROE

14.4% now

6%

8%

10%

12%

14%

16%

18%

20%

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Korean Consumer, Non-cyclical - ROE

12.6% now

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 34: Korea materials ROE Figure 35: Korea energy ROE

0%

5%

10%

15%

20%

25%

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Korean Materials - ROE

5.5% now

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Korean Energy - ROE

8.4% now

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 36: Korea financials ROE Figure 37: Korea telcos ROE

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Korean Financial - ROE

7.0% now

0%

5%

10%

15%

20%

25%

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Korean Telcos - ROE

9.2% now

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

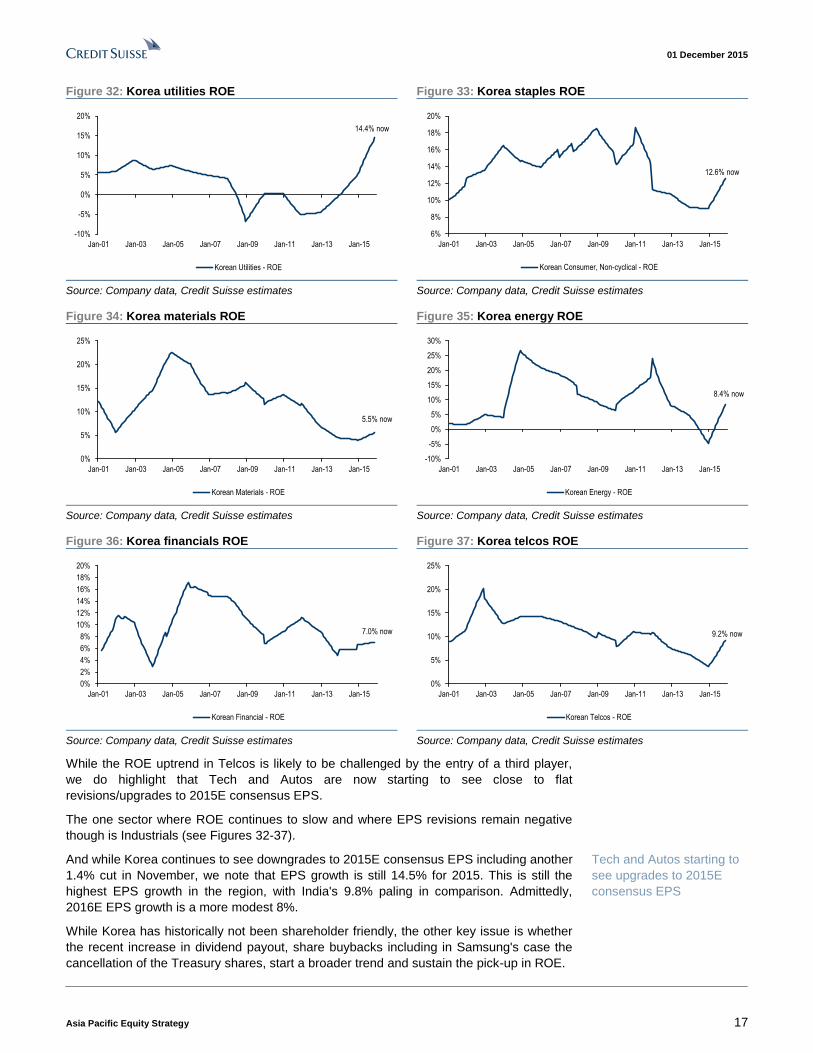

While the ROE uptrend in Telcos is likely to be challenged by the entry of a third player,

we do highlight that Tech and Autos are now starting to see close to flat

revisions/upgrades to 2015E consensus EPS.

The one sector where ROE continues to slow and where EPS revisions remain negative

though is Industrials (see Figures 32-37).

And while Korea continues to see downgrades to 2015E consensus EPS including another

1.4% cut in November, we note that EPS growth is still 14.5% for 2015. This is still the

highest EPS growth in the region, with India's 9.8% paling in comparison. Admittedly,

2016E EPS growth is a more modest 8%.

While Korea has historically not been shareholder friendly, the other key issue is whether

the recent increase in dividend payout, share buybacks including in Samsung's case the

cancellation of the Treasury shares, start a broader trend and sustain the pick-up in ROE.

Tech and Autos starting to

see upgrades to 2015E

consensus EPS

01 December 2015

Asia Pacific Equity Strategy 18

Figure 38: Korea tech ROE Figure 39: Korea consumer cyclicals ROE

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Korean Tech - ROE

12.4% now

0%

2%

4%

6%

8%

10%

12%

14%

16%

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Korean Consumer, Cyclical - ROE

10.3% now

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 40: Korea tech 2015E consensus EPS Figure 41: Kia Motors 2015E consensus EPS

60

65

70

75

80

85

90

95

100

105

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15

Korea Information Technology - EPS 15E

-0.6% in Nov-15

7000

7500

8000

8500

9000

9500

10000

10500

11000

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

Kia Motors - EPS 2015E

Source: IBES Source: IBES

Apart from the breadth of the ROE recovery, we believe Korea's nominal GDP growth of

4% to 4.5% in 2015-16 (up from a low of 3% in 2012) also supports our view that Korea's

ROE rise is sustainable.

Figure 42: Korea ROE versus Korea Nominal GDP Growth (YoY %)

2%

4%

6%

8%

10%

12%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2000 2002 2004 2006 2008 2010 2012 2014 2016E

Nom

inal

GD

P Y

oY%

RO

E (

non-

finan

cial

s)

Korea - ROE Korea - nominal GDP (YoY%)

4-4.5%

Source: Datastream, Consensus Economics, company data, Credit Suisse estimates

Apart from Korea's nominal GDP growth, we believe Consensus Economics forecast that

US nominal GDP growth will rise from 3.6% in 2015E to 4.5% in 2016E supports our view

on the sustainability of Korea's ROE pick-up.

Korea's nominal GDP

growth of 4-4.5% in 2015-16

is up from lows of 3% in

2012

01 December 2015

Asia Pacific Equity Strategy 19

Figure 43: Korea ROE versus US nominal GDP growth (YoY %)

-3%

-1%

1%

3%

5%

7%

9%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2000 2002 2004 2006 2008 2010 2012 2014 2016E

Nom

inal

GD

P Y

oY%

RO

E (

non-

finan

cial

s)

Korea - ROE US nominal GDP (YoY%)

2015E: 3.6%2016E: 4.5%

Source: Datastream, CS Economics, company data, Credit Suisse estimates

While Korea's ROE bottomed in December 2014, Figure 44 highlights that Taiwan's ROE

was the first to bottom at 9% in December 2012. It has since risen from 9% to 12.4%

currently. But the key concern over Taiwan's ROE is whether it is close to peaking, given

high smartphone penetration and downgrades to 2015E consensus EPS, particularly for

Tech over the last six months.

Figure 44: Taiwan ROE

7%

8%

9%

10%

11%

12%

13%

14%

15%

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Taiwan - ROE

High 14% Dec 2010

Low 9% Dec 2012

12.4% now

Source: Company data, Credit Suisse estimates

As with Korea, we believe drivers of Taiwan's ROE are Taiwan's nominal GDP growth and

US nominal GDP growth, and Consensus Economics is forecasting a pick-up in growth

rates for both of these in 2016E.

For Taiwan's nominal GDP growth, Consensus Economics is forecasting a pick-up from

3.4% in 2015E to 3.8% in 2016E. Figure 45 also highlights that the low in Taiwan's

nominal GDP growth was 1.4% in 2011.

Figure 46 highlights the fairly good fit between Taiwan's ROE and US nominal GDP

growth. As highlighted above, Consensus Economics is forecasting a pick-up from 3.6% in

2015E to 4.5% in 2016E.

Korea's ROE rise also

supported by Consensus

Economics suggesting US

nominal GDP growth rises

from 3.6% in 2015E to 4.5%

in 2016E

Apart from Korea, Taiwan's

ROE has also been rising;

but investors are

questioning whether it is

close to peaking

01 December 2015

Asia Pacific Equity Strategy 20

Figure 45: Taiwan ROE versus Taiwan nominal GDP

growth (% YoY)

Figure 46: Taiwan ROE versus US nominal GDP growth

(% YoY)

-4%

-2%

0%

2%

4%

6%

8%

10%

5%

7%

9%

11%

13%

15%

17%

19%

2000 2002 2004 2006 2008 2010 2012 2014 2016E

Nom

inal

GD

P Y

oY%

RO

E (

non-

finan

cial

s)

Taiwan - ROE Taiwan - nominal GDP (YoY%)

1.4% in 2011

3.4% in 2015E3.8% in 2016E

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

5%

7%

9%

11%

13%

15%

17%

19%

2000 2002 2004 2006 2008 2010 2012 2014 2016E

Nom

inal

GD

P Y

oY%

RO

E (

non-

finan

cial

s)

Taiwan - ROE US nominal GDP (YoY%)

3.6% 2015E4.5% 2016E

Source: Datastream, Consensus Economics, Company data, Credit

Suisse estimates

Source: Datastream, Consensus Economics, Company data, Credit

Suisse estimates

Figure 47: Taiwan tech ROE Figure 48: Taiwan non-tech ROE

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Taiwan Tech - ROE

14.3% now

High 14.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Taiwan non-Tech - ROE

10.8% now

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 47 also highlights that Taiwan Tech's ROE appears to have peaked at 14.8% and

has slowed to 14.3% currently. Despite the slowdown in Taiwan Tech ROE, Taiwan's

overall ROE has continued to rise (albeit slowly) as Non-Tech ROE has continued to rise.

Within Non-Tech, five of the seven sectors are associated with rising ROE. The five are

Industrials, Financials, Energy, Materials and Real Estate. The two associated with

slowing ROE are Consumer Staples and Telcos.

Figure 49: Taiwan financials ROE Figure 50: Taiwan industrials ROE

0%

2%

4%

6%

8%

10%

12%

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Taiwan Financial - ROE

11.2% now

-5%

0%

5%

10%

15%

20%

25%

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15

Taiwan Industrial - ROE

10.6% now

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

We believe NJA's ROE is bottoming as ROE in two of the four big markets—namely

Taiwan and Korea—is now rising. But the key question is whether the ROE rise extends

beyond Korea and Taiwan to India and possibly even MSCI China.

5 of 7 non-Tech sectors in

Taiwan are associated with

rising ROE

01 December 2015

Asia Pacific Equity Strategy 21

India's ROE has been stable at around 13.8% over the past few months. And with India

largely a domestically driven story, Figure 51 highlights the good fit between India's ROE

and its nominal GDP growth. While we are not sure whether India's nominal GDP growth

will rebound as strongly as suggested by Consensus Economics (from 11% in 2015E to

16% in 2016E), we believe a rise in India's nominal GDP growth looks likely given falling

commodity prices and rate cuts. If India's ROE does rise in 2016E, then potentially NJA's

ROE could rise for the first time since 2010.

Figure 51: India ROE versus India's nominal GDP growth (YoY %)

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

12%

14%

16%

18%

20%

22%

24%

26%

2000 2002 2004 2006 2008 2010 2012 2014 2016E

Nom

inal

GD

P Y

oY%

RO

E (

non-

finan

cial

s)

India - ROE India - nominal GDP (YoY%)

11.7%11%

16%

Source: Datastream, Consensus Economics, Company data, Credit Suisse estimates

While we do expect India's ROE to rise—from the current 13.8% towards 16%—we

estimate implied ROE though is closer to 19%. The market already appears to be pricing

in a significant ROE recovery.

With Hong Kong-listed China shares, there are few signs, if any, of ROE bottoming. Figure 53

highlights ROE has been sliding from a high of 17.6% in 2010 to just 12.8% currently.

Figure 52: India ROE Figure 53: China (HK-listed) ROE

10%

12%

14%

16%

18%

20%

22%

24%

26%

Mar-02 Mar-04 Mar-06 Mar-08 Mar-10 Mar-12 Mar-14

India - ROE

13.8% now

19.8% in Mar 06

16% in 2009

12%

13%

14%

15%

16%

17%

18%

19%

Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12 Dec-14

China (HK listed) - ROE

High 17.6% in 2010

12.8% now

16% in 2009

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

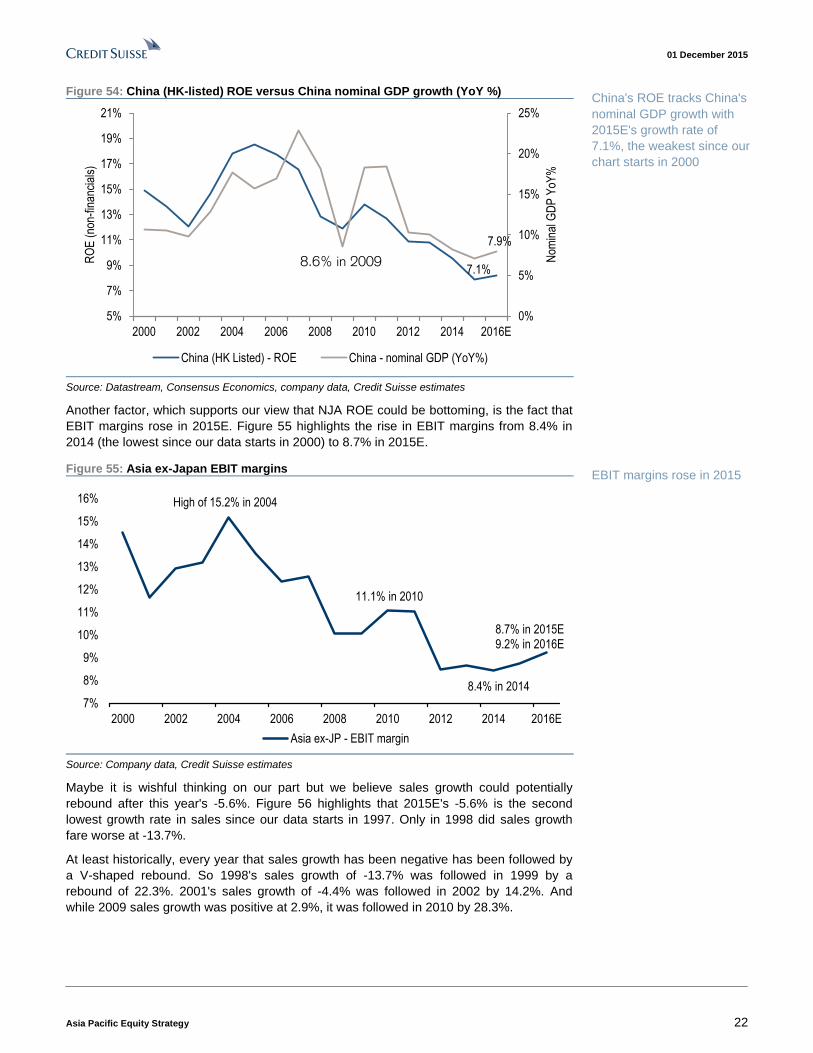

Figure 54 highlights the key reason for the slide in China's ROE is China's nominal GDP

growth in 2015E of just 7.1%. This is the lowest growth rate in China's nominal GDP since

our chart starts in 2000. It is significant that the 2015E growth rate is even lower than

2009's 8.6%. But there do appear to be some signs of stabilisation in nominal GDP

growth—PMI, services sector, property—and Consensus Economics is suggesting a

modest pick to 7.9% in 2016E.

India's ROE tracks India's

nominal GDP growth fairly

well

No signs yet of a bottoming

in China's ROE

01 December 2015

Asia Pacific Equity Strategy 22

Figure 54: China (HK-listed) ROE versus China nominal GDP growth (YoY %)

0%

5%

10%

15%

20%

25%

5%

7%

9%

11%

13%

15%

17%

19%

21%

2000 2002 2004 2006 2008 2010 2012 2014 2016E

Nom

inal

GD

P Y

oY%

RO

E (

non-

finan

cial

s)

China (HK Listed) - ROE China - nominal GDP (YoY%)

7.9%

7.1%8.6% in 2009

Source: Datastream, Consensus Economics, company data, Credit Suisse estimates

Another factor, which supports our view that NJA ROE could be bottoming, is the fact that

EBIT margins rose in 2015E. Figure 55 highlights the rise in EBIT margins from 8.4% in

2014 (the lowest since our data starts in 2000) to 8.7% in 2015E.

Figure 55: Asia ex-Japan EBIT margins

7%

8%

9%

10%

11%

12%

13%

14%

15%

16%

2000 2002 2004 2006 2008 2010 2012 2014 2016E

Asia ex-JP - EBIT margin

High of 15.2% in 2004

11.1% in 2010

8.4% in 2014

8.7% in 2015E 9.2% in 2016E

Source: Company data, Credit Suisse estimates

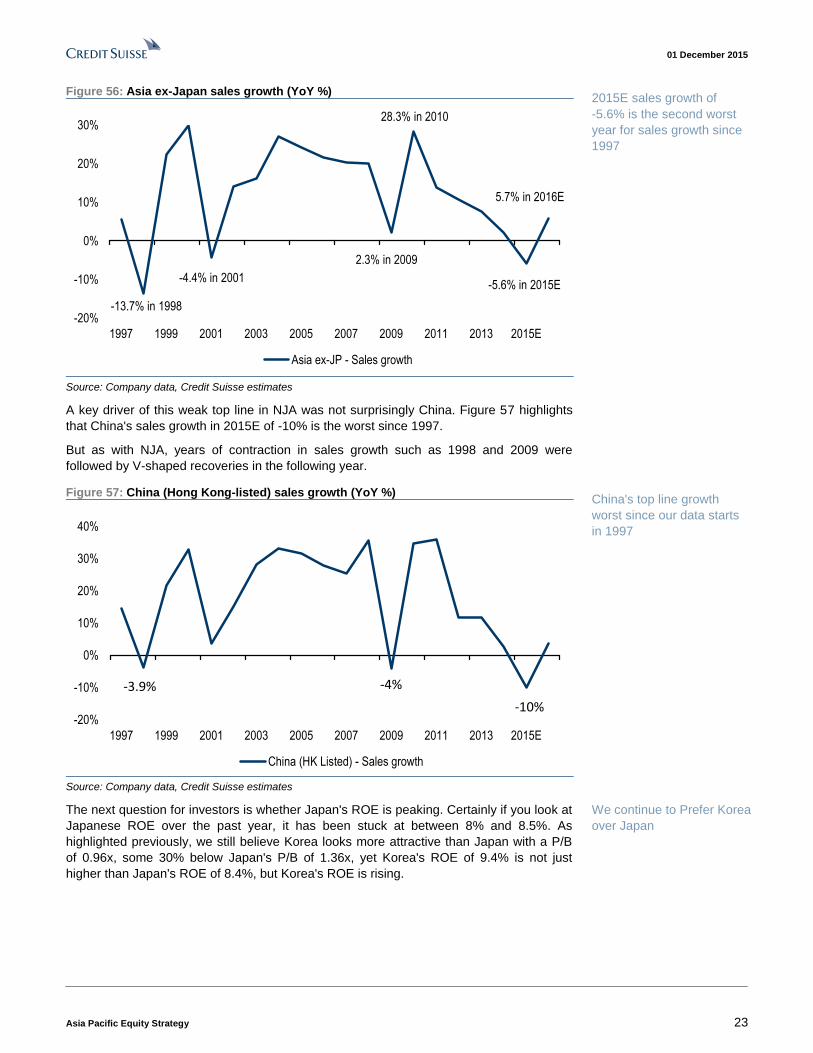

Maybe it is wishful thinking on our part but we believe sales growth could potentially

rebound after this year's -5.6%. Figure 56 highlights that 2015E's -5.6% is the second

lowest growth rate in sales since our data starts in 1997. Only in 1998 did sales growth

fare worse at -13.7%.

At least historically, every year that sales growth has been negative has been followed by

a V-shaped rebound. So 1998's sales growth of -13.7% was followed in 1999 by a

rebound of 22.3%. 2001's sales growth of -4.4% was followed in 2002 by 14.2%. And

while 2009 sales growth was positive at 2.9%, it was followed in 2010 by 28.3%.

China's ROE tracks China's

nominal GDP growth with

2015E's growth rate of

7.1%, the weakest since our

chart starts in 2000

EBIT margins rose in 2015

01 December 2015

Asia Pacific Equity Strategy 23

Figure 56: Asia ex-Japan sales growth (YoY %)

-20%

-10%

0%

10%

20%

30%

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015E

Asia ex-JP - Sales growth

-4.4% in 2001

-13.7% in 1998

2.3% in 2009

28.3% in 2010

-5.6% in 2015E

5.7% in 2016E

Source: Company data, Credit Suisse estimates

A key driver of this weak top line in NJA was not surprisingly China. Figure 57 highlights

that China's sales growth in 2015E of -10% is the worst since 1997.

But as with NJA, years of contraction in sales growth such as 1998 and 2009 were

followed by V-shaped recoveries in the following year.

Figure 57: China (Hong Kong-listed) sales growth (YoY %)

-20%

-10%

0%

10%

20%

30%

40%

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015E

China (HK Listed) - Sales growth

-3.9% -4%

-10%

Source: Company data, Credit Suisse estimates

The next question for investors is whether Japan's ROE is peaking. Certainly if you look at

Japanese ROE over the past year, it has been stuck at between 8% and 8.5%. As

highlighted previously, we still believe Korea looks more attractive than Japan with a P/B

of 0.96x, some 30% below Japan's P/B of 1.36x, yet Korea's ROE of 9.4% is not just

higher than Japan's ROE of 8.4%, but Korea's ROE is rising.

2015E sales growth of

-5.6% is the second worst

year for sales growth since

1997

China's top line growth

worst since our data starts

in 1997

We continue to Prefer Korea

over Japan

01 December 2015

Asia Pacific Equity Strategy 24

Figure 58: Japan versus Korea P/B Figure 59: Japan versus Korea ROE

0.96

1.36

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Dec-95 Dec-98 Dec-01 Dec-04 Dec-07 Dec-10 Dec-13

Korea - PB Japan - PB

9.4%

8.4%

-5%

0%

5%

10%

15%

20%

Dec-95 Dec-98 Dec-01 Dec-04 Dec-07 Dec-10 Dec-13

Korea - ROE Japan - ROE

Source: MSCI, company data, Credit Suisse estimates Source: MSCI, company data, Credit Suisse estimates

While Japan has progressed further in terms of share buybacks and increasing dividend

payouts, we highlight that Korea's dividend yield of 1.41% is not that far below Japan's

dividend yield of 1.87%.

The other key issue is how much of the improvement in Japan's EBIT margin came from

the sharp fall in the Yen as the Yen has now stopped falling. Figure 60 suggests that forex

has definitely played a role in the doubling of Japan's EBIT margins from a low of 4% in

2009 to 8% in 2016E.

The key risk with Overweighting Korea and being Neutral Japan in an Asia-Pacific context

is a further sharp fall in the Yen, particularly if the BOJ embarks on another round of QE.

Perhaps this risk is not that high with Japanese core CPI rising by over 1% recently, and

the BOJ's balance sheet as a share of its GDP is significantly higher than the Fed's (during

QE) and the ECB's.

Figure 60: Japan EBIT margin versus Won/Yen forex rate

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,6004%

5%

5%

6%

6%

7%

7%

8%

8%

9%

2003 2005 2007 2009 2011 2013 2015

KR

W v

s JP

Y (

x100

)

EB

IT m

argi

n

Japan - EBIT margin KRW vs JPY (x100)

Source: Bloomberg, Datastream, company data, Credit Suisse estimates

Cheapest 4 outperformed Expensive 4 by 7% in 2015

While past performance is not necessarily a good guide to future performance, Figure 61

highlights that the Cheapest 4 basket (equally weighted) has outperformed MSCI Asia ex-

Japan (MXASJ) 87% of the time after 12 months.

Forex appears to have

played a role in Japan's

EBIT margins doubling

01 December 2015

Asia Pacific Equity Strategy 25

Figure 61: Cheapest 4- backtest results from 2000

Overweighting cheapest 4 countries 3 months 6 months 12 months

Number of episodes with outperformance 49 46 53

Number of episodes with underperformance 14 16 8

% of episodes with outperformance 78% 74% 87%

Average outperformance 2.2% 3.6% 6.1%

Source: MSCI, Company data, Credit Suisse estimates. We can provide detailed backtest results from

2000 on request.

We do emphasise that it is the basket of the Cheapest 4 that has historically outperformed

and not necessarily all four of the individual countries. We also highlight that undervalued

markets may stay undervalued for longer than we expect but eventually mean-revert and

our highest success rate is after 12 months.

2015 continues this trend of outperformance with Figure 62 highlighting that the Cheapest

4 basket (equally weighted) has so far in 2015 outperformed MXASJ by 4.3%. Three of the

four countries in the Cheapest 4 have outperformed with MSCI Hong Kong outperforming

by 10% while MSCI China and Korea have outperformed by 5% to 8%. Only Australia

within the Cheapest 4 basket has underperformed.

Figure 62: Cheapest 4—backtest results for calendar 2015

Absolute performance Relative performance

Dec-14 3 mths 6 mths since Dec-14 3 mths 6 mths since Dec-14

China -32.9% 8.1% 12.6% -6.0% 4.0% 10.6% 5.0%

Korea -28.6% 4.0% 0.1% -3.4% 0.1% -1.7% 7.9%

Hong Kong 5.7% 5.3% 10.1% -1.4% 1.3% 8.0% 10.1%

Australia 6.0% 1.8% -5.4% -15.7% -2.1% -7.1% -5.9%

Average 4.8% 4.4% -6.6% 0.8% 2.4% 4.3%

Mar-15 3 mths 6 mths since Mar-15 3 mths 6 mths since Mar-15

China -32.0% 4.2% -20.0% -13.0% 6.3% -1.1% 0.9%

Korea -13.4% -3.7% -15.2% -7.1% -1.8% 4.8% 7.8%

Hong Kong 0.4% 4.5% -13.1% -6.4% 6.6% 7.4% 8.6%

Singapore 4.7% -1.5% -21.9% -17.8% 0.5% -3.5% -4.6%

Average 0.8% -17.5% -11.1% 2.9% 1.9% 3.2%

Jun-15 3 mths since Jun-15 3 mths since Jun-15

China -24.2% -23.2% -16.5% -7.0% -5.0%

Korea -19.2% -11.9% -3.5% 6.8% 9.8%

Singapore 3.4% -20.7% -16.5% -4.0% -5.1%

Taiwan 4.5% -18.8% -16.0% -1.6% -4.5%

Average -18.6% -13.1% -1.4% -1.2%

Sep-15 QTD QTD

China -29.5% 8.7% 2.1%

Korea -18.0% 9.5% 2.8%

Hong Kong 0.8% 7.7% 1.1%

Singapore 1.6% 5.2% -1.2%

Average 7.8% 1.2%

Source: MSCI, company data, Credit Suisse estimates

While past performance is

not necessarily a good

guide to the future,

Cheapest 4 has

outperformed MXASJ 87%

of the time after 12 months

Cheapest 4 has

outperformed MXASJ by

4.3% so far in 2015

01 December 2015

Asia Pacific Equity Strategy 26

While the Cheapest 4 has outperformed MXASJ by 4.3% so far in 2015, Figure 63

highlights that the Expensive 4 has underperformed YTD by 2.7%. So the Cheapest 4 has

outperformed the Expensive 4 by 7%.

With the Expensive 4, the bulk of the underperformance YTD has come from one market

Indonesia, though Taiwan has also underperformed YTD.

But in the current quarter, we highlight the 6% to 9% underperformance of the Philippines

and India.

Figure 63: Expensive 4—Backtest results for 2015 YTD

Absolute performance Relative performance

Dec-14 3 mths 6 mths since Dec-14 3 mths 6 mths since Dec-14

Philippines 59.5% 9.2% 3.6% -7.7% 5.1% 1.6% 3.0%

India 48.0% 5.2% 0.9% -9.8% 1.2% -1.0% 0.7%

Indonesia 44.4% 2.0% -13.4% -21.4% -1.9% -15.0% -12.3%

Taiwan 27.3% 3.9% 4.2% -12.5% 0.0% 2.2% -2.3%

Average 5.1% -1.2% -12.9% 1.1% -3.0% -2.7%

Mar-15 3 mths 6 mths since Mar-15 3 mths 6 mths since Mar-15

Philippines 54.7% -5.2% -15.4% -15.5% -3.3% 4.6% -2.0%

Indonesia 45.0% -15.1% -35.8% -23.0% -13.4% -20.6% -10.6%

India 42.8% -4.1% -10.9% -14.2% -2.1% 10.0% -0.4%

Malaysia 21.6% -8.7% -25.8% -20.6% -6.8% -8.3% -7.8%

Average -8.3% -22.0% -18.3% -6.4% -3.6% -5.2%

Jun-15 3 mths since Jun-15 3 mths since Jun-15

Philippines 51.4% -10.7% -10.9% 8.1% 1.3%

India 45.0% -7.2% -10.6% 12.4% 1.7%

Indonesia 20.2% -24.3% -9.2% -8.4% 3.2%

Thailand 13.5% -18.4% -15.5% -1.2% -3.8%

Average -15.2% -11.5% 2.8% 0.6%

Sep-15 QTD QTD

Philippines 55.4% -0.2% -6.3%

India 49.8% -3.6% -9.5%

Malaysia 29.0% 7.1% 0.5%

Australia 16.9% 6.8% 0.3%

Average 2.5% -3.7%

Source: MSCI, company data, Credit Suisse estimates

So our country tilts continue to be largely driven by which markets are in the Cheapest 4

versus the Expensive 4. We continue to Overweight the Cheapest 4 which currently are

Korea, MSCI China, Taiwan and Singapore.

Expensive 4 has

underperformed MXASJ by

2.7% YTD

So Cheapest 4 has

outperformed Expensive 4

by 7% YTD

Cheapest 4 currently are

Korea, MSCI China, Taiwan

and Singapore

01 December 2015

Asia Pacific Equity Strategy 27

Figure 64: Countries ranked on our P/B vs ROE valuation model

-20%

0%

20%

40%

60%K

orea

Chi

na

Sin

gapo

re

Tai

wan

Hon

g K

ong

Tha

iland

Aus

tral

ia

Japa

n

Mal

aysi

a

Indi

a

Indo

nesi

a

Phi

lippi

nes

PB less ROE rel to Asia Pac ex-JP

Source: Company data, Credit Suisse estimates

We also continue to Underweight the Expensive 4, which are the Philippines, India,

Indonesia and Malaysia.

Sector strategy: Will cyclicals follow history in

outperforming defensives post Fed tightening?

While our country strategy is largely following valuations, our sector strategy assumes to

some degree that history repeats itself.

While we do not have MSCI data on the performance of cyclicals versus defensives during

the 1994 and 2004 Fed tightening, Figure 65 highlights that during the Fed taper in 2013,

cyclicals outperformed defensives by 19% from one month after the Fed started to tighten.

Interestingly, the underperformance of cyclicals versus defensives was 12% in the run-up

to the Fed taper in 2013 and is also 12% in the current episode.

Figure 65: MSCI Asia ex-Japan Cyclicals versus Defensives relative price performance

85

90

95

100

105

110

-9m -6m -3m 0m +3m +6m +9m +12m

May-13 current

Asia ex-JP Cyclicals vs Defensives

-12%

+18.6%

-12%+8%

Source: MSCI. We are assuming Dec 2015 is the first rate hike.

After 12%

underperformance in the

run-up to Fed tightening, will

history repeat itself with

cyclicals outperformance

once the Fed moves?

01 December 2015

Asia Pacific Equity Strategy 28

While data at the aggregate cyclicals to defensives level is only available for the 2013

episode, we do have data at the individual cyclicals level for the 2004 Fed tightening

episode. For cyclicals, we use the MSCI definition, which includes Tech, Consumer

Cyclicals, Energy, Materials and Industrials. For defensives, the MSCI definition includes

Consumer Staples, Utilities and Telcos.

Figures 66-69 highlight strong gains in both the 2004 Fed tightening and 2013 Fed taper

episode for cyclical sectors once the Fed starts to tighten. We do emphasise that we

believe 2013 maybe the more relevant comparison as 2004 was associated with strong

and rising Chinese real GDP growth, which we do not currently have.

Figure 66: MSCI Asia ex-Japan tech around Fed

tightening

Figure 67: MSCI Asia ex-Japan consumer cyclicals

around Fed tightening

70

80

90

100

110

120

130

140

150

-9m -6m -3m 0m +3m +6m +9m +12m

Jun-04 May-13 current

MXASJ Info Tech

-31%

-13%

-16.4%

+23%

+35%

70

80

90

100

110

120

130

140

150

-9m -6m -3m 0m +3m +6m +9m +12m

Jun-04 May-13 current

MXASJ Consumer Discretionary

-23%

-11%

-18.4% now

+46%

+26%

Source: MSCI Source: MSCI

Figure 68: Materials around Fed tightening Figure 69: Energy around Fed tightening

70

80

90

100

110

120

130

140

150

160

170

-9m -6m -3m 0m +3m +6m +9m +12m

Jun-04 May-13 current

MXASJ Materials

-28.5%

-25%

-23.7% now

+71%

+22%

70

90

110

130

150

170

190

-9m -6m -3m 0m +3m +6m +9m +12m

Jun-04 May-13 current

MXASJ Energy

-28%

-26%

-29.6%

+59%

+17%

Source: MSCI Source: MSCI

We believe history is supported by valuations with the P/B gap between cyclicals and

defensives still close to 2008 levels.

Figure 70 highlights that the P/B gap between cyclicals and defensives has narrowed from

a low of -0.82x in August 2015 to -0.66x currently. But the current gap of -0.66x is still 90%

of the gap of -0.74x seen at the 2008 lows.

While in 2008, ROE of the cyclicals was 8 pp below defensives, Figure 67 highlights that

the current ROE gap is zero.

We continue to Overweight Tech and Consumer Cyclicals (particularly Korean autos). We

have also reduced our Underweights in Materials and Energy.

Our least favoured defensive sector remains Consumer Staples, which are not only the

most overvalued sector on our P/B vs ROE valuation model but also associated with big

downgrades to 2015E consensus EPS.

We believe 2013 may be the

more relevant episode as

2004 was associated with

strongly rising Chinese real

GDP growth

Cyclicals to defensives P/ B

gap has narrowed from

-0.82x to -0.66x, but this is

still close to the gap seen at

2008 lows

01 December 2015

Asia Pacific Equity Strategy 29

Figure 70: Cyclicals P/B less defensives P/B Figure 71: Cyclicals ROE less defensives ROE

-0.8

-0.6

-0.4

-0.2

0.0

0.2

Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

Asia ex-JP Trailing PB - Cyclicals less Defensives

-0.74 Dec 2008

-0.66x now

-0.82x

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

Dec-03 Dec-05 Dec-07 Dec-09 Dec-11 Dec-13 Dec-15

Asia ex-JP ROE - Cyclicals less Defensives

0.0% now

-8.4%

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

The key risks to our constructive stance on equities are China hard landing/systemic risk.

The other key risks are that history does not repeat itself and even after the Fed tightens,

markets continue to correct. Another risk is that ROE does not bottom as we expect.

While we are Overweight cyclicals, we continue to be cautious on "New" Economy defined

as Macau Gaming and Internet. While Macau Gaming's P/B has derated from a high of

9.3x in February 2014 to just 3.1x, we highlight that even in the month of November 2015E

consensus EPS was downgraded by a further 4.5%.

Figure 72: Macau Gaming P/B Figure 73: Macau Gaming 2015E consensus EPS

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15

Macau gaming - PB

now 3.1x

average: 5.5x

high 9.3x

20

30

40

50

60

70

80

90

100

110

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15

Macau gaming - EPS15E

-67.5% since Apr 14

-4.5% in Nov

Source: Company data, Credit Suisse estimates Source: IBES

While the downgrades are smaller for Internet, Figure 75 highlights a further 1.3% cut to

2015E consensus EPS for China Internet in the month of November. We wonder therefore

how much of the recent rally in Internet stocks has to do with just flows from MSCI

inclusion rather than improving fundamentals.

Figure 74: NJA Internet 2015E consensus EPS Figure 75: China Internet 2015E consensus EPS

70

75

80

85

90

95

100

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15

NJA Internet - EPS15E

-0.1% in Nov

-27%

86

90

94

98

102

106

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15

China Internet - EPS15E

-1.3% in Nov

-19%

Source: IBES Source: IBES

Macau Gaming P/B has de-

rated from a high of 9.3x in

February 2014 to just 3.1x

currently

01 December 2015

Asia Pacific Equity Strategy 30

Figure 76 highlights that ChiNext P/B has now risen from a recent low of 7x back to 9.67x.

This is not that far from the high of 13.4x seen at the height of the bubble in May/June

2015.

Figure 76: Chinext current P/ B versus prior bubbles

0

2

4

6

8

10

12

14

0 6 12 18 24 30 36

Tra

iling

PB

Japan TSE since Jun 88 Nasdaq Comp since Aug 98 China A since Apr 06China H since Apr 2006 China A current China H currentShenzhen SME current Chinext current US listed CN Int current

month

NASDAQ 8x at 2000 highShenzhen SME 5.46xChina A 6.9x 2006-07 high

China H 5.2x at 2007 high

China H 1.01x

China A 2.33x

high 7.03x

high 2.98x

high 1.43x

Chinext 9.67x

high 13.4x

US listed CN Internet 5.30x

high 5.47x

Source: Bloomberg, Datastream, MSCI, company data, Credit Suisse estimates

ChiNext P/B has risen to

9.67x, not far from the

height of the bubble at 13.4x

01 D

ec

em

ber 2

015

Asia

Pacific

Eq

uity

Stra

teg

y

31

CS regional model portfolio

China Hong Kong Korea Taiwan India Aust / NZ Asean Japan Total Rel.

Consumer Great Wall Motor 2.0% Hyundai Motors 2.5%

Fuji Heavy Inds 4.0% 15.0% 1.6%

Discretionary Hyundai Mobis 0.5%

Toyota 4.0%

Aisin Seiki 2.0%

Consumer

LG Household 1.0%

Kose 2.0% 4.0% -2.7%

Staples

KT&G 1.0%

Energy SK Innovation 1.0% FPCC 1.0%

2.0% -0.8%

Financials Bank of China 2.0% BOC Hong Kong 1.9% Shinhan 0.3% Cathay 0.5%

CBA 3.5% DBS 2.5% Sumitomo Mitsui 8.0% 32.2% 8.4%

(ex-Real Est.) Ping An 2.0% Dongbu Insurance 0.5% CTBC 0.5%

ANZ 2.0% Bank BRI 1.0% Dai-ichi Life 7.0%

Fubon 0.5%

Healthcare

0.0% -5.4%

Industrials Goldwind 1.5% CKH Holdings 2.0%

JAL 2.5% 9.0% -4.0%

Sumitomo Elec 3.0%

Information Alibaba 2.0% SEC 3.0% TSMC 4.0% HCL Tech 1.0%

Softbank 4.0% 19.3% 5.2%

Technology Hon Hai 2.3%

Sony 3.0%

Materials

1.0% Hindalco 0.5% Rio 2.0%

3.5% -2.5%

Real estate COLI 2.5% CK Property 4.0%

Mitsui Fudosan 4.0% 10.5% 4.5%

Telcos China Mobile 2.5%

2.5% -3.0%

Utilities Kepco 1.0% AGL Energy 1.0% 2.0% -1.2%

Total 14.5% 7.9% 11.8% 8.8% 1.5%

8.5% 3.5% 43.5% 100.0%

Rel. to MSCI AC APAC 2.0%

2.2%

3.6%

2.4%

-2.7%

-3.8%

-3.6%

-0.1% 0.0%

Source: MSCI, Credit Suisse estimates

01 December 2015

Asia Pacific Equity Strategy 32

Country Sections

01 December 2015

Asia Pacific Equity Strategy 33

Australia Alpha and the lost decade

The Australian economy seems to have already started its lost decade and the future