22

Analyst Meeting2020 Results23 February 2021Ticker: BCPG (SET)

Capturing Thailand Opportunities in midst of COVID-19

Accelerate construction progress of Japan Solar Power Plants in midst of COVID-19

Successful Bond Issuance of USD 1.1 bn to refinance existing loan of Salak-Darajat power plants

PH Tariff Escalation in place granted retroactive adjustment and annual rebase

Successful Capital Raising of THB 10,235 mn

Continuing Asset Optimization

BCPG’s Regional Plan

Acquired Nam San 3B, adding hydro power portfolio to 114 MW

Secured higher tariff with EVN (Vietnam) for 2 hydro power plants

Co-invested 79 km Transmission line from Nam San 3A&3B to sell electricity to VN

Develop 600 MW wind farm to sell electricity cross border to VN

20 MW Solar TH Acquisition District Cooling in CHULA Smart City

Laying a solid 2020 foundation for next stage of growth

5

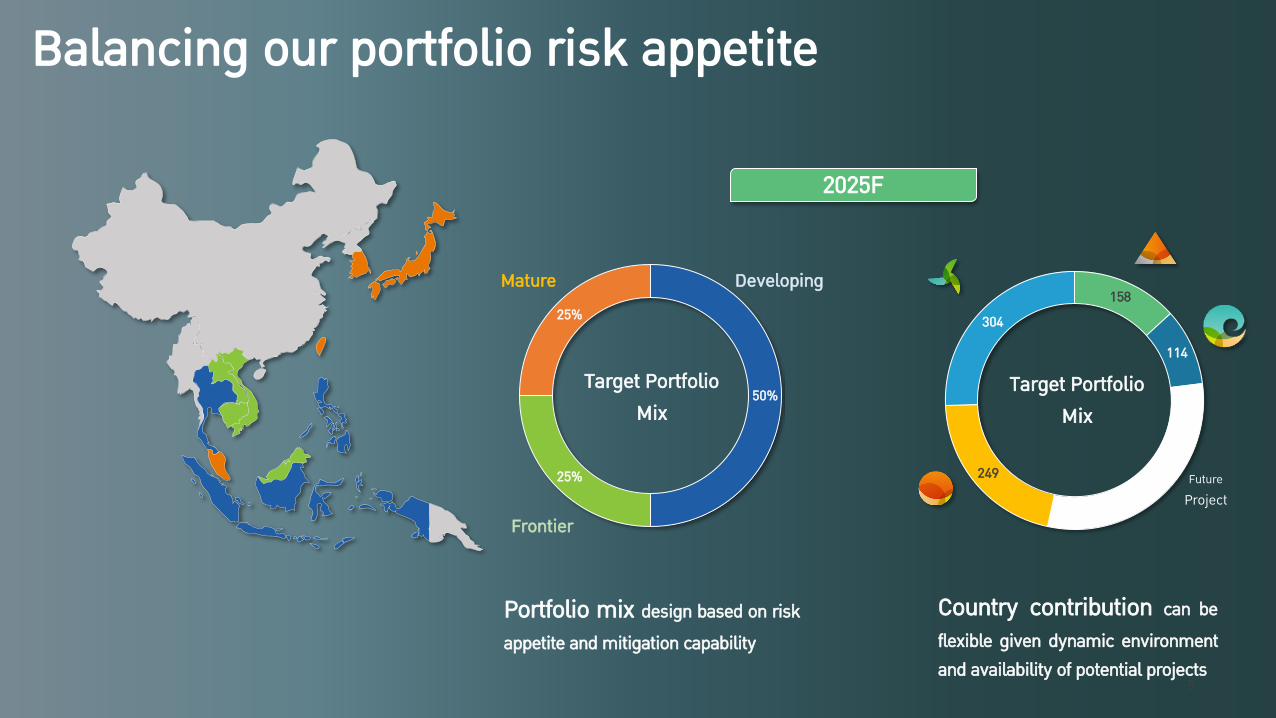

DevelopingMature

Frontier

158

114

249

304

Target PortfolioMix

Future Project

50%

25%

25%

Target PortfolioMix

2025F

Balancing our portfolio risk appetite

Country contribution can be flexible given dynamic environment and availability of potential projects

Portfolio mix design based on risk appetite and mitigation capability

6

Portfolio & Pipelines

Performance & Guidelines

Agenda

Key developments

7

Portfolio & Pipelines

Performance & Guidelines

Agenda

Key developments

8

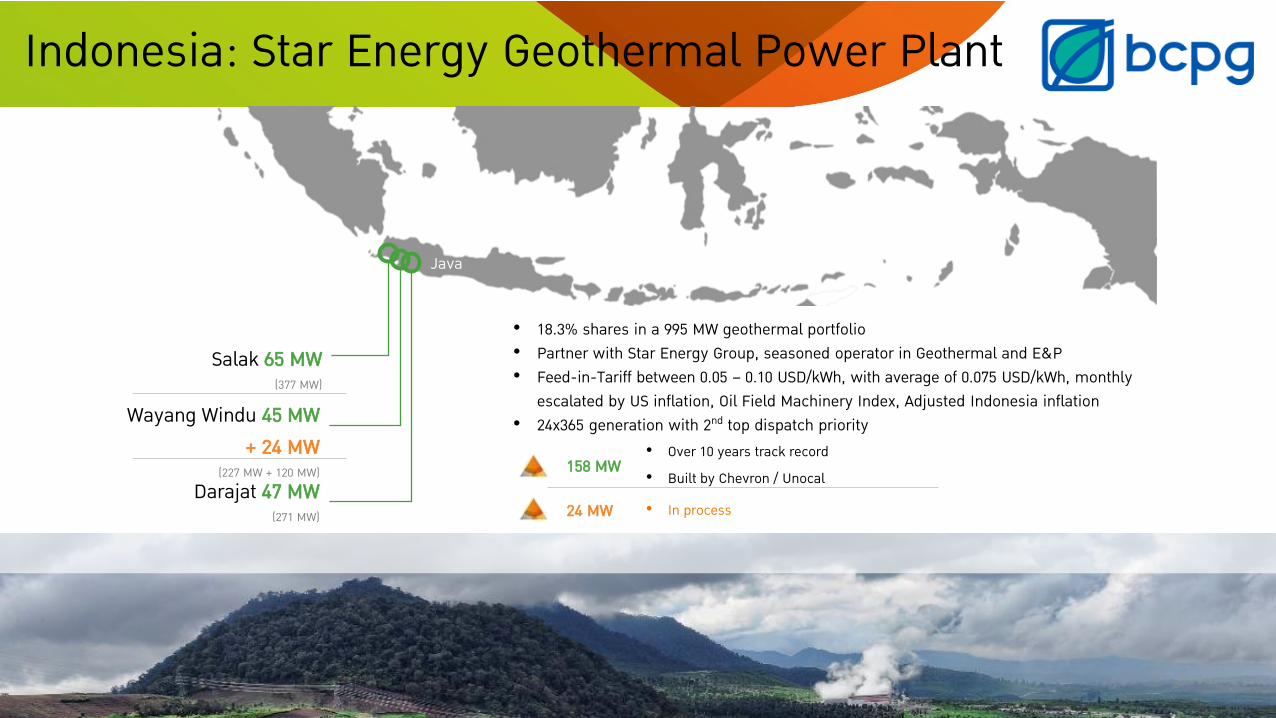

Darajat 47 MW(271 MW)

Salak 65 MW (377 MW)

Wayang Windu 45 MW + 24 MW

(227 MW + 120 MW)

Java

• 18.3% shares in a 995 MW geothermal portfolio• Partner with Star Energy Group, seasoned operator in Geothermal and E&P• Feed-in-Tariff between 0.05 – 0.10 USD/kWh, with average of 0.075 USD/kWh, monthly

escalated by US inflation, Oil Field Machinery Index, Adjusted Indonesia inflation• 24x365 generation with 2nd top dispatch priority

• Over 10 years track record• Built by Chevron / Unocal

158 MW

• In process 24 MW

Indonesia: Star Energy Geothermal Power Plant

Expenses related to refinance

THB -172 mn* Frees up cash dividend to BCPG USD 26 mn or THB 842 mn in 2020. Investment Grade Bond with better conditions e.g. longer tenor, lower interest rate & greater loan amount.The long-term bond have oversubscription of 3.5 times to the issuing amount.Additional cash during 2020-25 to enhance BCPG’s investment ability about THB 10,000 mn.

20202016 2026 2038

PREV

IOUS

REFI

NANC

E

Dividend steam to enhance investment ability.

ID refinancing accelerates dividend payout

Only 5-year tenor left Dividend is restricted until 2023

Free up cash dividend to BCPG

Remark: Above debt is related to Salak and Darajat.*About 35% was non-cash.

Developing: 24.0 MWOperating: 157.5 MW

Hold: 33.3%

Associates

Enhancing investment ability

Bond: Tenor 8.5 & 18 years, avg. rate 4%

Loan: Tenor 10 years, rate 4 - 5%

0200400600800

1,000

2020 2021E 2022E 2023E 2024E 2025E

THB

mn

Additional After Refinance Before Refinance

0

5,000

10,000

15,000

Before Refinance After Refinance

THB

mn

Dividend 2020-25E Investment ability

Gearing up to 4x

10

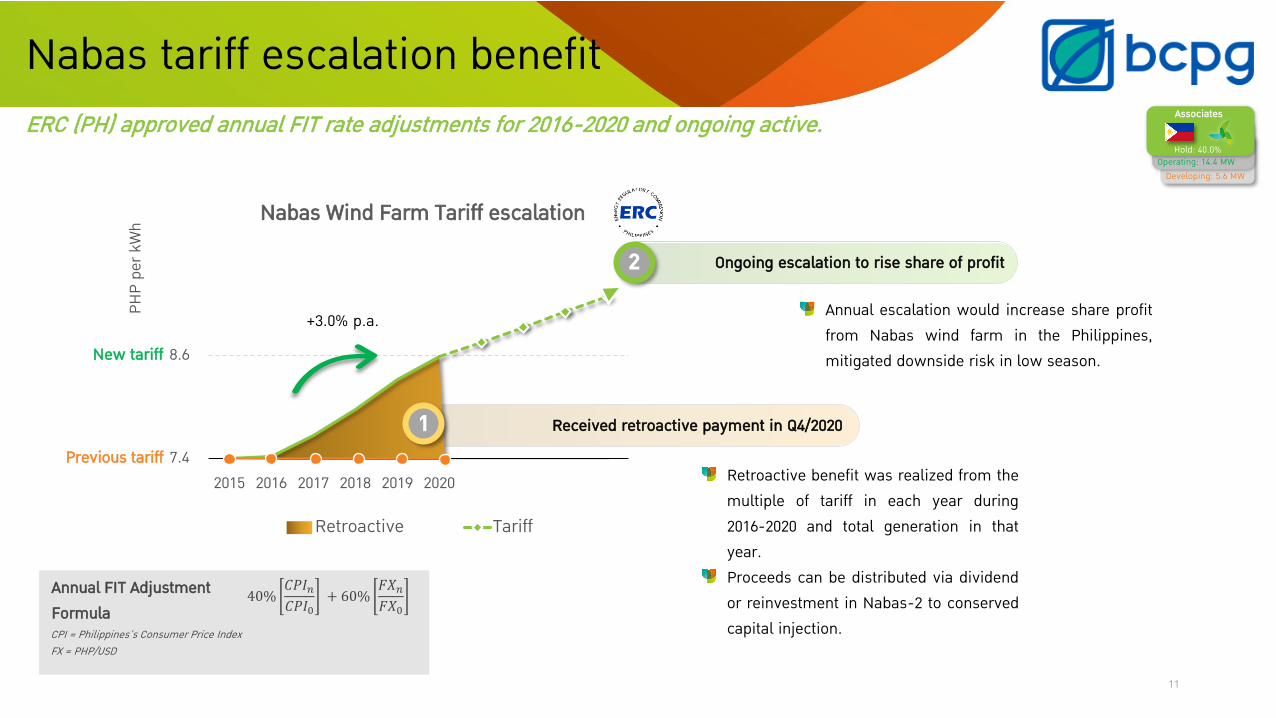

Philippines: Nabas Wind Farm

50 MW Wind Farm

Company PetroWind Energy Inc.

Location Nabas Town, Visayas, Philippines

Investment Up to USD 27.2 mn (THB 925 mn)

Installed Capacity • Phase 1 : Operating 36 MW (Equity of 14.4 MW)• Phase 2 : Developing 14 MW (Equity of 5.6 MW)

Turbine Gamesa G90 (Spain)

COD (Acqusition date) 10 June 2015 (May 2017) for 20 years

Current 2017 - 2020

Capacity Factor * 26% - 37% (Q1 39% - 53%)

FIT Rate 8.60 PHP/kWh since Nov 2020 with retroactive adjustment

*Range capacity factor after acquisition since May 2017

11

Nabas tariff escalation benefit

7.4

8.6

2015 2016 2017 2018 2019 2020

PHP

per k

Wh Nabas Wind Farm Tariff escalation

Retroactive Tariff

ERC (PH) approved annual FIT rate adjustments for 2016-2020 and ongoing active.

40%𝐶𝑃𝐼𝑛𝐶𝑃𝐼0

+ 60%𝐹𝑋𝑛𝐹𝑋0

Annual FIT Adjustment FormulaCPI = Philippines’s Consumer Price IndexFX = PHP/USD

2 Ongoing escalation to rise share of profit

Retroactive benefit was realized from the multiple of tariff in each year during 2016-2020 and total generation in that year.Proceeds can be distributed via dividend or reinvestment in Nabas-2 to conserved capital injection.

1Previous tariff

New tariff

+3.0% p.a.

Developing: 5.6 MWOperating: 14.4 MW

Hold: 40.0%

Associates

Received retroactive payment in Q4/2020

Annual escalation would increase share profit from Nabas wind farm in the Philippines, mitigated downside risk in low season.

12

Nam San 3A Nam San 3B

Type Run-of-the-river

Capacity 69 MW 45 MW

COD1 date 29 Jan 2016 25 Sep 2015

Acquisition date 20 Sep 2019 26 Feb 2020

PPA(Laos)

- Terms: 27 years from COD (2015 – 2042)- Tariff: 6.72 Uscent/kWh (2020)- Take-or-pay: 95%- Currency: 90% USD/10% KIP

PPA(Vietnam)

- Terms: 25 years from COD ([2022] – 2047)- Tariff: 6.95 Uscent/kWh- Take-or-pay: 90%- Currency: 100% USD

Thathom District

3A Powerhouse

3A Dam site

3B Powerhouse

Xiengkhouang, Laos PDR

1Commercial Operation Date

Nam San 3B siteNam San 3A site

3B Dam Site

Nam San 3A & 3BSteppingstone in hydro power plant with large potential collaborations

Developing: 0.0 MWOperating: 114.0 MW

Hold: 100.0%

Subsidiaries

13

220 kV transmission line: Foundation procedure

Transmission line 3A & 3B: LA-VNMilestones tracking to be COD within 2022

1

Substation construction2

Switching station at border379 km Transmission Line

BorderNam San 3A

Nam San 3B

1

23

60% of transmission line foundations are done.

Foundation excavation

Steel bindingFramework installation Concrete pouring

Completion

Land preparation & substation foundation work

14

Development on plan to COD within this year & output remote control to mitigate curtailment

25 MW

20 MWYabukiCOD 4Q21

Chiba 1COD 4Q21

Chiba 2COD 2H22

20 MW

10 MW

S1

S19

S11

TarumizuGotemba

KomaganeCOD 4Q21

Total developing capacity 75.0 MWppa

*Including developing projects

Curtailment impact

No curtailment impact

Projects update in Japan

Chiba 1: Pond development

Yabuki: Site clearing

Developing: 75.0 MWOperating: 14.7 MW

Hold: 100.0%

Subsidiaries

Total operating capacity 14.7 MWppa

15

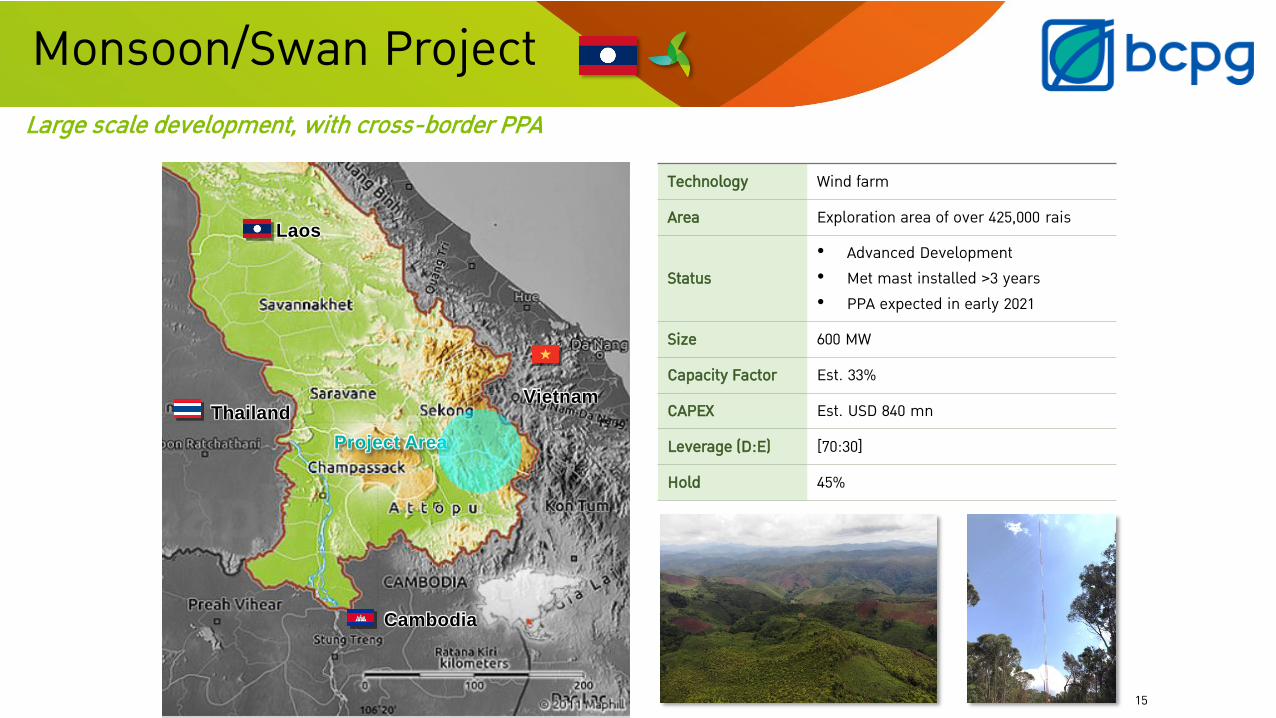

Technology Wind farm

Area Exploration area of over 425,000 rais

Status• Advanced Development• Met mast installed >3 years• PPA expected in early 2021

Size 600 MW

Capacity Factor Est. 33%

CAPEX Est. USD 840 mn

Leverage (D:E) [70:30]

Hold 45%

Thailand

Cambodia

Vietnam

Project Area

Laos

Monsoon/Swan ProjectLarge scale development, with cross-border PPA

16

Lao-VN 600MW Wind Farm milestones

Cross-border milestones: Wind farm

1

2

Project and transmission line construction

Aug-2020

16

34

Financial close

- EPC to be awarded- Financing in place

To b

e CO

D wi

thin

2023

Prime Minister’s Approval

- Acceptance of Grid Study- Tariff Negotiation Range- Project Timeline

- Inclusion of Energy Import into VN’s PDP - Construction of transmission line in VN- COD by 2022- Tariff Ceiling Price

Tariff MOU: Wind Farm✓

✓

PPA to be signed with EVN

17

Portfolio & Pipelines

Performance & Guidelines

Agenda

Key developments

18

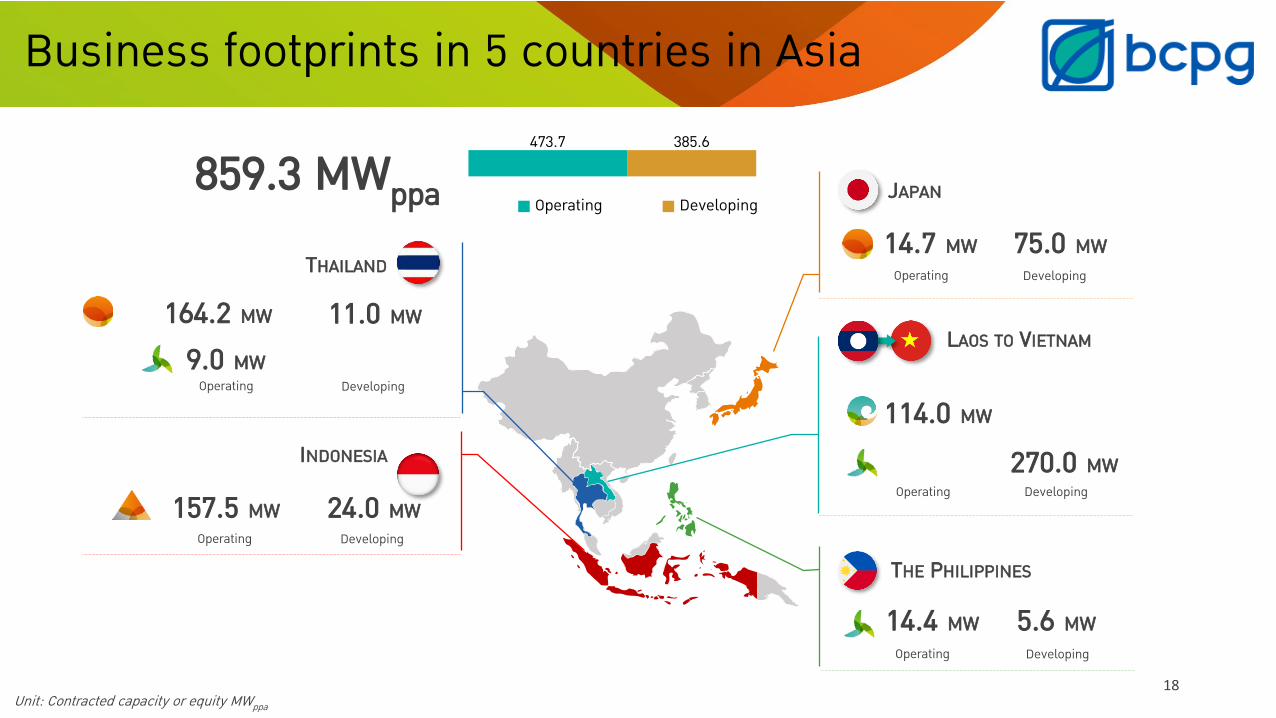

859.3 MWppa

164.2 MW 11.0 MW

THAILAND

Operating Developing

157.5 MW 24.0 MW

INDONESIA

Operating Developing

14.4 MW 5.6 MW

THE PHILIPPINES

Operating Developing

14.7 MW 75.0 MW

JAPAN

Operating Developing

114.0 MW

LAOS TO VIETNAM

Unit: Contracted capacity or equity MWppa

9.0 MW

473.7 385.6

Operating Developing

270.0 MWDevelopingOperating

Business footprints in 5 countries in Asia

19

299.0 MW, 34.7% (275.6 MW under

development)

181.5 MW, 21.1% (24.0 MW under

developing) 267.4 MW, 31.0%

(85.0 MW developing)

114.0 MW, 13.2%

61.0%

2.2%

14.9%

22.0%

Q1 Q2 Q3 Q4

3 hrs 4.1 hrs 4.3 hrs

8.7 hrs

14 hrs

22.5 hrs

Estimated Yearly Power Generation by technology *

Contracted MW by TechnologyY2020 Seasonality by Technology

(Capacity factor %)

859.3 MW

Geothermal (ID)

Hydro (LA)

Wind (PH)

Solar (TH)Solar (JP)

Wind (TH)

Average capacity factor in hours by TechnologyUnit: GWh

Unit: MW

Remarks : * Calculate base on capacity factor (%) & MW at the end of 2020 and subject to holding proportion

> 2,000 GWh / year

Well-diversified portfolio

254

835

1,608 1,651

2,065

2016 2017 2018 2019 2020 2021 202520

…......

Remarks : *Solar equivalent are calculated to be compared with solar power plant in Thailand

Unit: GWh

Current portfolio and pipelines

Current pipeline guarantees a growth of 50% in the next 5 years

Solar Equivalent *

11.0 MW TH75.0 MW JP 5.6 MW PH (Expansion)24.0 MW ID (Expansion)270.0 MW LA

Current pipeline1,450 MW

2,200 MWSolar

Equivalent *

Portfolio growth from existing pipelines

2,100

~3,200

21

Portfolio & Pipelines

Performance & Guidelines

Agenda

Key developments

22

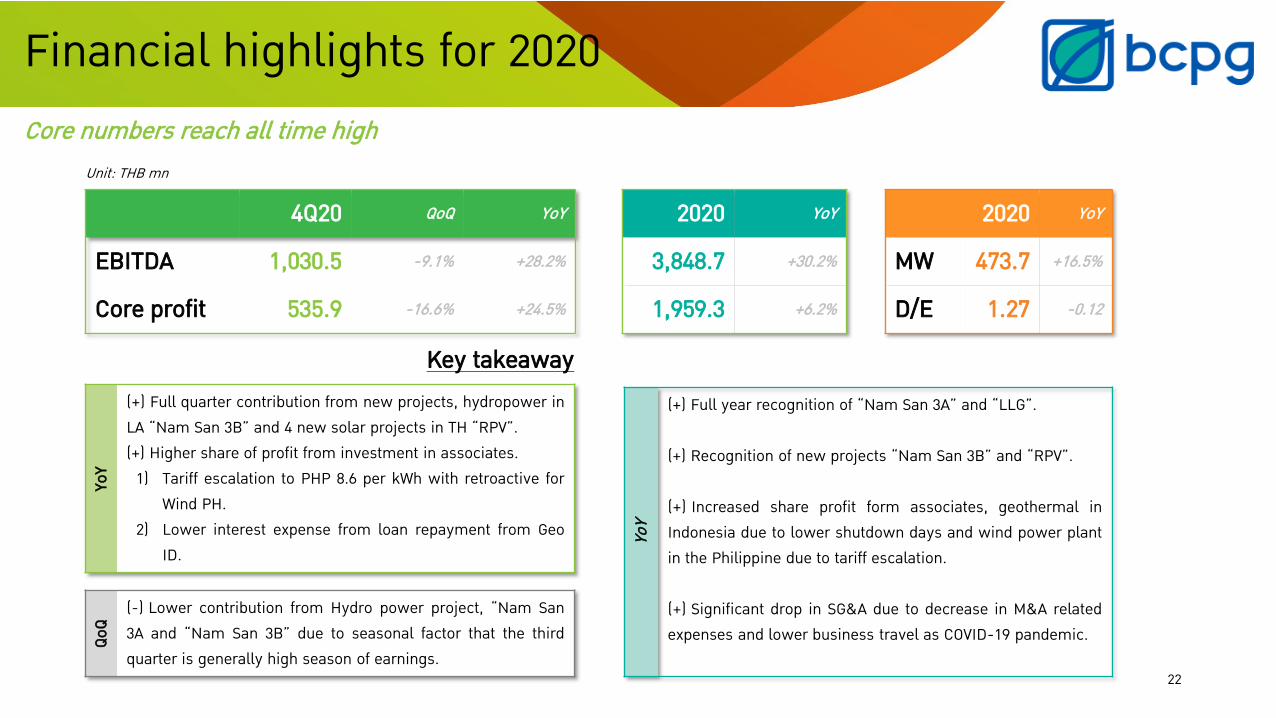

4Q20 QoQ YoY 2020 YoY 2020 YoY

EBITDA 1,030.5 -9.1% +28.2% 3,848.7 +30.2% MW 473.7 +16.5%

Core profit 535.9 -16.6% +24.5% 1,959.3 +6.2% D/E 1.27 -0.12

Unit: THB mn

YoY

(+) Full quarter contribution from new projects, hydropower in LA “Nam San 3B” and 4 new solar projects in TH “RPV”.(+) Higher share of profit from investment in associates.

1) Tariff escalation to PHP 8.6 per kWh with retroactive for Wind PH.

2) Lower interest expense from loan repayment from Geo ID.

QoQ

(-) Lower contribution from Hydro power project, “Nam San 3A and “Nam San 3B” due to seasonal factor that the third quarter is generally high season of earnings.

YoY

(+) Full year recognition of “Nam San 3A” and “LLG”.

(+) Recognition of new projects “Nam San 3B” and “RPV”.

(+) Increased share profit form associates, geothermal in Indonesia due to lower shutdown days and wind power plant in the Philippine due to tariff escalation.

(+) Significant drop in SG&A due to decrease in M&A related expenses and lower business travel as COVID-19 pandemic.

Key takeaway

Financial highlights for 2020Core numbers reach all time high

806.7 777.5 759.1

3,059.7 3,060.4

4Q19 3Q20 4Q20 2019 2020TH (Solar) TH (Wind) TH (Other)

+0.0% YoY-2.4% QoQ

-5.9% YoY

3.2 2.7 3.4

10.0 11.7

14.4%12.2%

15.5% 15.8%13.3%

4Q19 3Q20 4Q20 2019 2020Generation Capacity factor (%)

+16.4% YoY+27.2% QoQ

+6.9% YoY

75.6 73.7 73.5

286.6 290.5

18.2%16.4% 15.5%

17.4% 16.6%

4Q19 3Q20 4Q20 2019 2020Generation Capacity factor (%)

+1.4% YoY-0.3% QoQ

-2.8% YoY

Developing: 0.0 MWOperating: 9.0 MW

Hold: 100.0%

Subsidiaries

Developing: 11.0 MWOperating: 164.2 MW

Hold: 100.0%

Subsidiaries

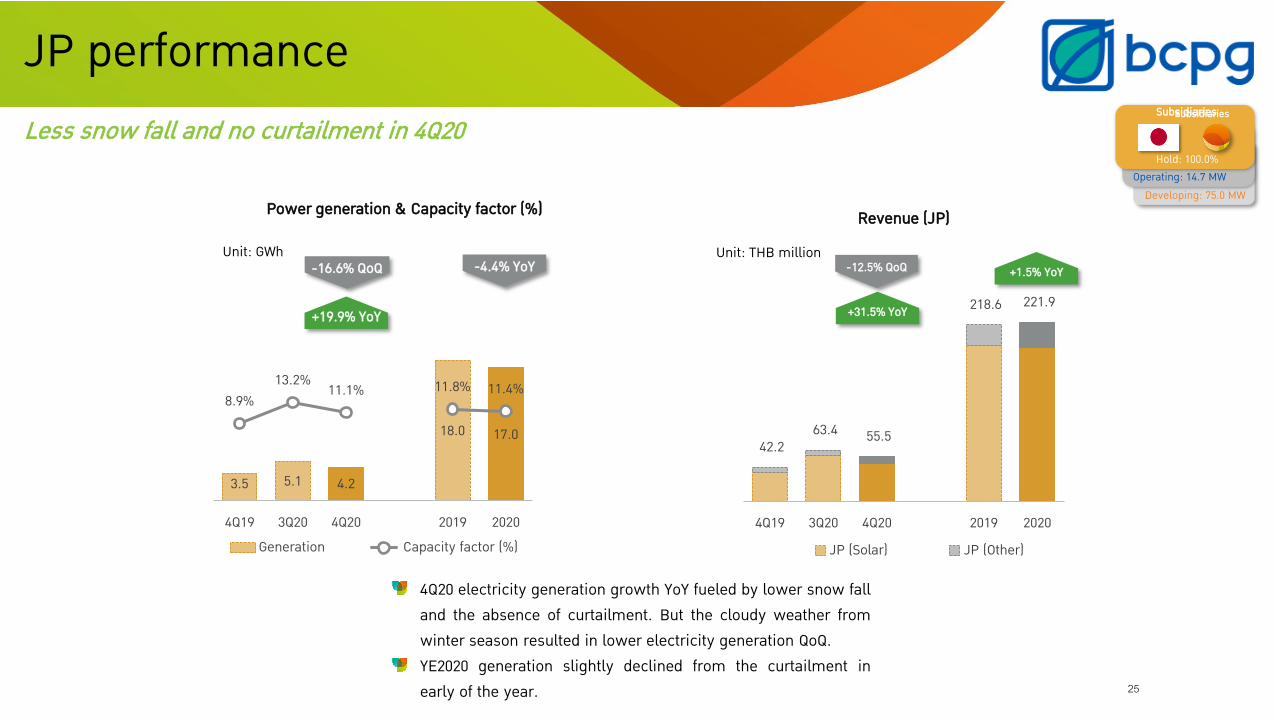

TH performanceWind performance improved from higher wind speed while solar performance improve from newly acquired 20 MW Solar farm

23

Unit: GWh Unit: GWh

Power generation & Capacity factor (%)

In 4Q20, longer than usual of rainy season was impacted to the drop in electricity generationYE2020 generation improvement due to newly acquired 20 MW Solar farm “ RPV”.

Revenue (TH) Unit: THB million

Solar revenue decreased due to longer than usual of rainy season and offset higher revenue of wind power plant.

Wind speed rose YoY from more monsoon and QoQ from high season. YE2020 growth was driven by the full-year operation.

Solar Wind

64.3188.8 157.1

72.0

453.3

42.2%

75.0%62.4%

43.9% 46.4%

4Q19 3Q20 4Q20 2019 2020Generation Capacity factor (%)

+144.2% YoY

+529.2% YoY-16.8% QoQ

132.2

396.9322.2

148.2

948.4

4Q19 3Q20 4Q20 2019 2020

LA (Hydro)

+143.6% YoY

+539.8% YoY-18.8% QoQ

LA Performance

24

Growth from full-year operation of “Nam San 3A” and full quarter operation of “Nam San 3B”

Unit: GWh

4Q20 growth YoY came from full quarter recognition of “Nam San 3B” but seasonal factor impacted to the drop QoQ. YE2020 growth was supported by full-year recognition of “Nam San 3A” and recognition of “Nam San 3B”.

Unit: THB millionRevenue (LA) Power generation & Capacity factor (%)

Developing: 0.0 MWOperating: 114.0 MW

Hold: 100.0%

Subsidiaries

42.2 63.4 55.5

218.6 221.9

4Q19 3Q20 4Q20 2019 2020JP (Solar) JP (Other)

+31.5% YoY

+1.5% YoY-12.5% QoQ

3.5 5.1 4.2

18.0 17.0

8.9%13.2% 11.1% 11.8% 11.4%

4Q19 3Q20 4Q20 2019 2020Generation Capacity factor (%)

-4.4% YoY

+19.9% YoY

-16.6% QoQ

Developing: 75.0 MWOperating: 14.7 MW

Hold: 100.0%

Subsidiaries

JP performance

25

Less snow fall and no curtailment in 4Q20

Unit: THB million

4Q20 electricity generation growth YoY fueled by lower snow fall and the absence of curtailment. But the cloudy weather from winter season resulted in lower electricity generation QoQ.YE2020 generation slightly declined from the curtailment in early of the year.

Unit: GWh

Subsidiaries

Power generation & Capacity factor (%) Revenue (JP)

299.8 319.4 304.6

1,220.4 1,259.1

90.0% 95.9% 91.3% 92.4% 95.0%

4Q19 3Q20 4Q20 2019 2020Generation * Capacity factor (%)

+1.6% YoY

+3.3% YoY-4.6% QoQ

165.7 217.0 189.9

723.0 849.3

4Q19 3Q20 4Q20 2019 2020

+17.5% YoY

+14.6% YoY

-12.5% QoQ

Developing: 24.0 MWOperating: 157.5 MW

Hold: 33.3%

Associates

ID PerformanceGeothermal power plants in Indonesia

26Remark: *Generation based on holding percentage

Share of profit from operation rose from lower shutdown days.

Unit: GWh

Power generation & Capacity factor (%)

Unit: THB million

4Q20 and YE2020 operating results improved YoY from less planned maintenance days. However, net 4Q20 and YE2020 share of profit were pressure by expenses related to refinance scheme.

Amortization (91.4) (94.6) (92.5) (375.0) (378.0)

One-time items (20.0) - (171.5) (20.0) (238.2)*

Net share of profit 54.3 122.4 (74.1) 328.0 233.1*Including Refinance expenses THB171.5 mn, Tax provision THB 23.9 mn and Allowance for account receivable THB 42.8 mn.

Share of profit

27

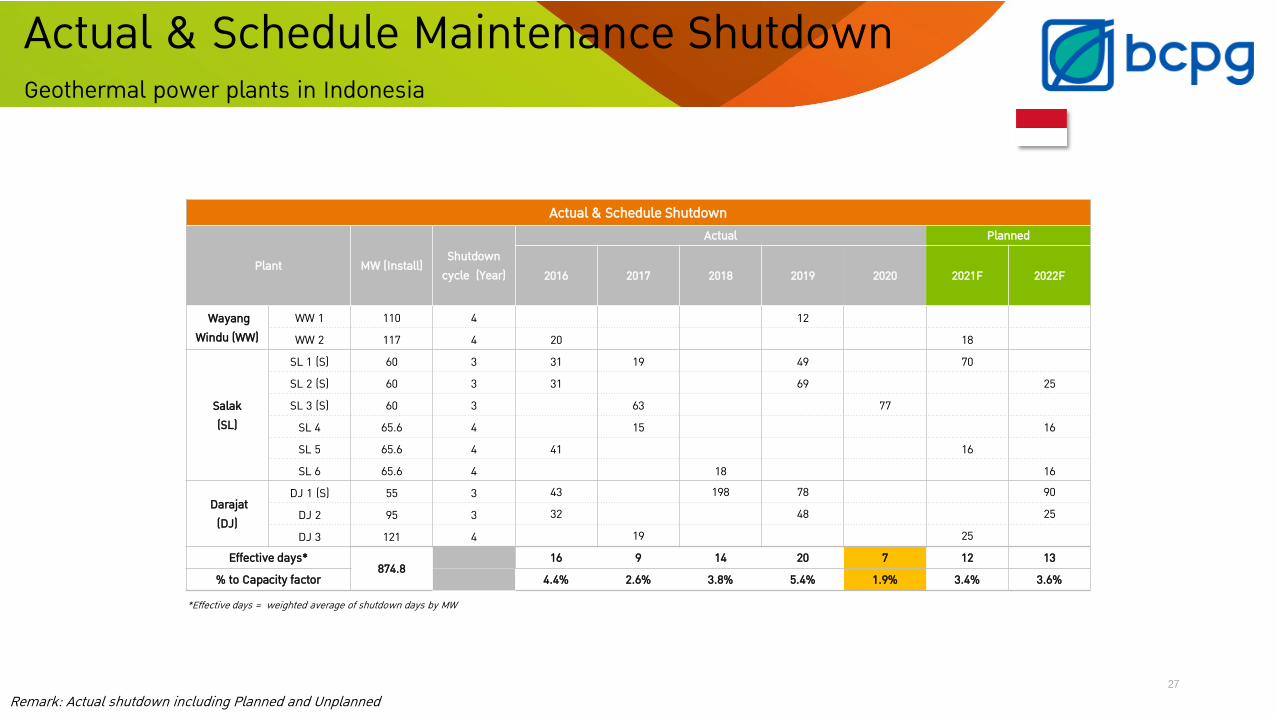

Actual & Schedule Maintenance ShutdownGeothermal power plants in Indonesia

Actual & Schedule Shutdown

Plant MW (Install)Shutdown

cycle (Year)

Actual Planned

2016 2017 2018 2019 2020 2021F 2022F

WayangWindu (WW)

WW 1 110 4 12WW 2 117 4 20 18

Salak (SL)

SL 1 (S) 60 3 31 19 49 70SL 2 (S) 60 3 31 69 25SL 3 (S) 60 3 63 77

SL 4 65.6 4 15 16SL 5 65.6 4 41 16SL 6 65.6 4 18 16

Darajat (DJ)

DJ 1 (S) 55 3 43 198 78 90DJ 2 95 3 32 48 25DJ 3 121 4 19 25

Effective days*874.8

16 9 14 20 7 12 13% to Capacity factor 4.4% 2.6% 3.8% 5.4% 1.9% 3.4% 3.6%

*Effective days = weighted average of shutdown days by MW

Remark: Actual shutdown including Planned and Unplanned

8.2 4.3 8.6

44.733.0

25.7%13.4%

26.9%35.5%

26.1%

4Q19 3Q20 4Q20 2019 2020Generation * Capacity factor (%)

-26.2% YoY+100.6% QoQ

+4.7% YoY 1.1

-13.6

57.4 58.7 69.2

4Q19 3Q20 4Q20 2019 2020

+18.0% YoY

+5,250.5% YoY

+n.a.% QoQ

Developing: 5.6 MWOperating: 14.4 MW

Hold: 40.0%

Associates

PH PerformanceWind power plant in the Philippines

28

Stronger monsoon in 4Q20 and received tariff escalation to PHP 8.6 per kWh.

Remark: *Generation based on holding percentage

Unit: GWh

Amortization (7.8) (8.1) (7.9) (32.0) (32.3)

One-time items - - - - -

Net share of profit (6.7) (21.5) 49.5 26.6 36.9

Higher electricity generation in 4Q20 YoY and QoQ from stronger monsoon. Received price escalation since November 2020 and the retroactive payment for 5 years (2016-2020) of THB 47.8 mn.

Unit: THB million

Power generation & Capacity factor (%) Share of profit

981.2 1,237.9 1,136.8

3,426.6

4,230.7

4Q19 3Q20 4Q20 2019 2020Thailand Japan Lao PDR

+23.5% YoY

+15.9% YoY

-8.2% QoQ

803.81,133.8 1,030.5

2,955.4

3,848.7

4Q19 3Q20 4Q20 2019 2020

+28.2% YoY

+30.2% YoY-9.1% QoQ

Remark: EBITDA from operation including share of profit from associates (after amortization and before one-time items)

Growth is persistent in Revenue and EBITDA

29

EBITDA (Incl. shares of profit)

4Q20 EBTIDA growth followed operating revenue and share of profit from operation. YE2020 EBTIDA growth followed operating revenue, share of profit from operation and lower administrative expenses.

Financial Performance: Revenue & EBITDA

4Q20 YoY growth from the full-quarter contribution of Nam Sam 3B and RPV (newly acquired 20 MW TH Solar). While the drop QoQ from hydropower seasonality. YE2020 growth from the full-year contribution of Nam San 3A and Lomligor as well as the contribution of Nam Sam 3B and RPV (newly acquired 20 MW TH Solar).

Unit: THB millionUnit: THB millionRevenue

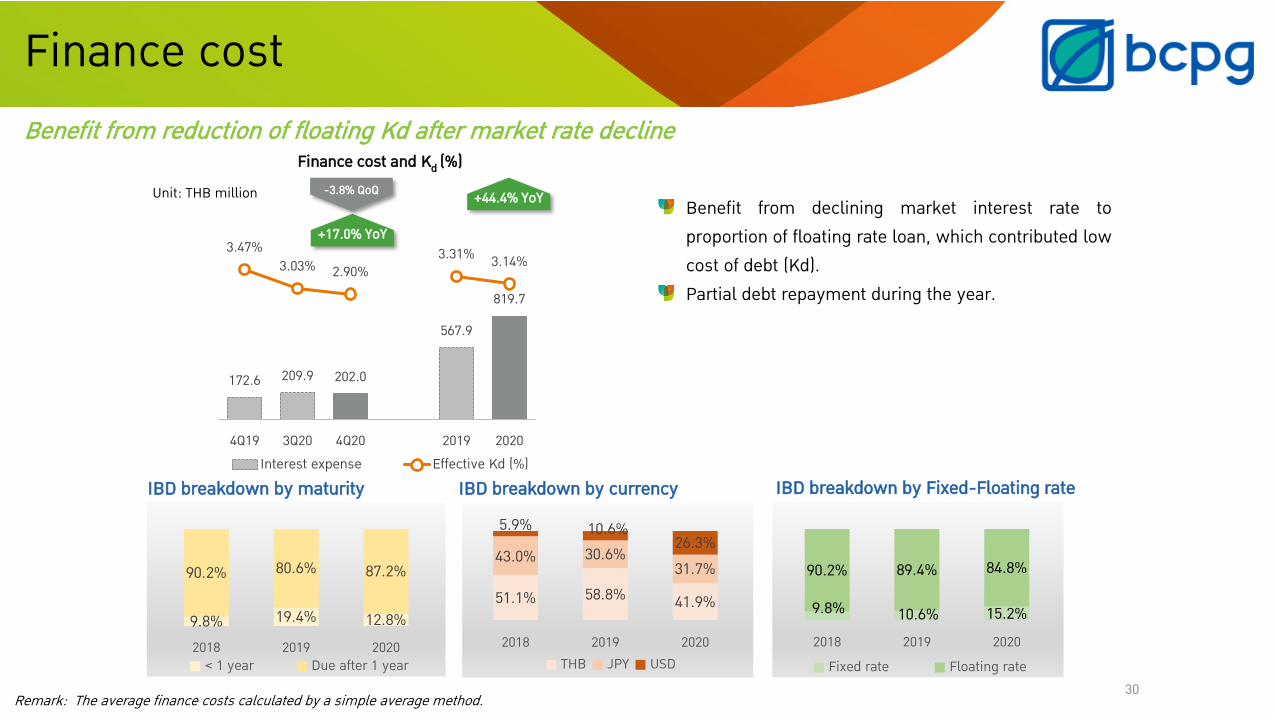

172.6 209.9 202.0

567.9

819.7

3.47%3.03% 2.90%

3.31% 3.14%

4Q19 3Q20 4Q20 2019 2020Interest expense Effective Kd (%)

+44.4% YoY

+17.0% YoY

-3.8% QoQ

30

Unit: THB million

IBD breakdown by maturity IBD breakdown by currency

9.8% 19.4% 12.8%

90.2% 80.6% 87.2%

2018 2019 2020< 1 year Due after 1 year

51.1% 58.8% 41.9%

43.0% 30.6%31.7%

5.9% 10.6%26.3%

2018 2019 2020THB JPY USD

IBD breakdown by Fixed-Floating rate

Benefit from declining market interest rate to proportion of floating rate loan, which contributed low cost of debt (Kd).Partial debt repayment during the year.

9.8% 10.6% 15.2%

90.2% 89.4% 84.8%

2018 2019 2020Fixed rate Floating rate

Finance cost and Kd (%)

Remark: The average finance costs calculated by a simple average method.

Benefit from reduction of floating Kd after market rate decline

Finance cost

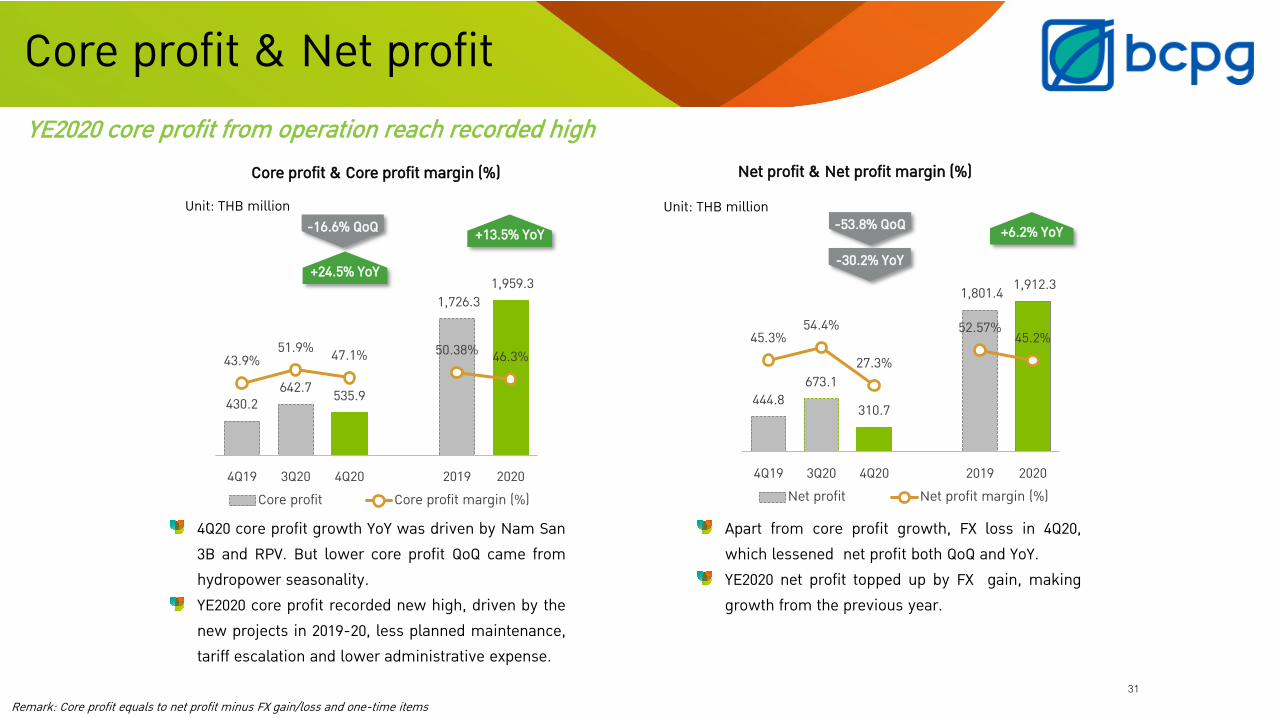

430.2642.7 535.9

1,726.3 1,959.3

43.9%51.9% 47.1% 50.38% 46.3%

4Q19 3Q20 4Q20 2019 2020Core profit Core profit margin (%)

+13.5% YoY

+24.5% YoY

-16.6% QoQ

444.8673.1

310.7

1,801.4 1,912.3

45.3%54.4%

27.3%

52.57% 45.2%

4Q19 3Q20 4Q20 2019 2020Net profit Net profit margin (%)

+6.2% YoY-53.8% QoQ

-30.2% YoY

31

YE2020 core profit from operation reach recorded highCore profit & Core profit margin (%)

Remark: Core profit equals to net profit minus FX gain/loss and one-time items

Unit: THB million

Net profit & Net profit margin (%)

Core profit & Net profit

Unit: THB million

4Q20 core profit growth YoY was driven by Nam San 3B and RPV. But lower core profit QoQ came from hydropower seasonality. YE2020 core profit recorded new high, driven by the new projects in 2019-20, less planned maintenance, tariff escalation and lower administrative expense.

Apart from core profit growth, FX loss in 4Q20, which lessened net profit both QoQ and YoY. YE2020 net profit topped up by FX gain, making growth from the previous year.

32

48.0% 41.9% 44.0%49.3% 53.5%

52.8%31,55837,137

51,220

2018 2019 2020Equity Other Liabilities Interest-bearing debt

1.08 1.39 1.27

2018 2019 2020

D/E Ratio

D/E Ratio Covenant

Covenant = 3.0x

Total assets

ROE (ex-capital raising proceeds) rise

15.1611.74 10.05 12.40

2018 2019 2020 2020(Adjusted)

ROE (%)

Financial position

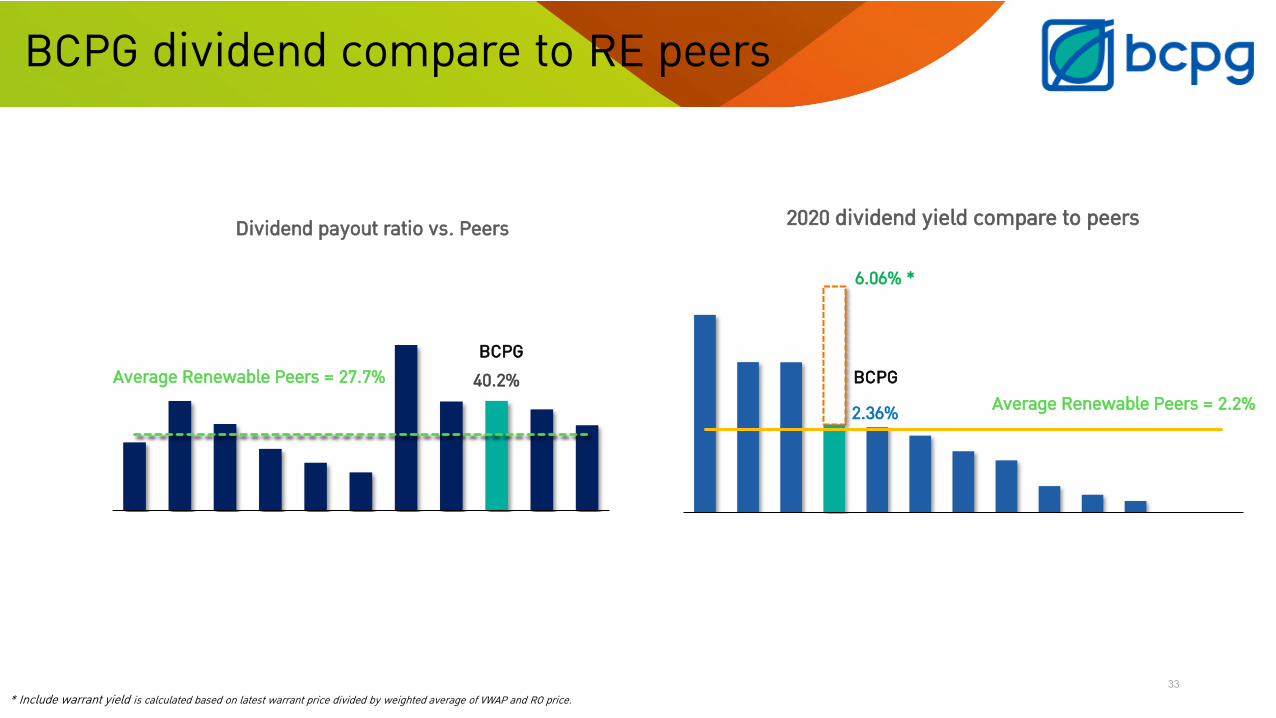

Dividend payment 2020Type Per share (THB) Amount (THB mn)

Interim 0.16 326.7

Annual 0.17 442.1

Total 0.33 768.8

Payout ratio 40.2%

Dividend yield * 2.36%

(+) Warrant yield ** 3.70%

Total yield 6.06%

“For 2020, if excluding proceeds from capital increased which will mostly used in 2021, ROE will be 12.4%.”

Remark: Dividend policy = not less than 40% of the Company’s net profit based on separated yearly Financial Statement* Dividend yield is calculated based on volumed weighted average price (VWAP) / ** While warrant yield is calculated based on latest warrant price divided by weighted average of VWAP and RO price.

On top of dividend yield in this year, warrant yield would be additional return to investors who subscripted right offering shares.

33

BCPG dividend compare to RE peers

40.2%

Dividend payout ratio vs. Peers

Average Renewable Peers = 27.7% BCPG

* Include warrant yield is calculated based on latest warrant price divided by weighted average of VWAP and RO price.

2.36%

6.06% *

2020 dividend yield compare to peers

BCPGAverage Renewable Peers = 2.2%

34

GuidanceActual Plan

2020 2021

EBITDA *

CAPEX THB 6,000 mn THB 18,000 mn

Dividend policy Not less than 40% of the Company’s net profit

Financial covenant Liability/Equity ≤ 3xDSCR ≥ 1.15x

Remark: *Share of profit from associates (after amortization but before one-time items) / For demonstration purposes only

Guideline 2021

>20% 30 - 40%

New acquisitions

>30%

2020 CollectionInvoiced Collected

35

EDL payment still collectable

Remark: Figure for demonstration purpose only

Gradually get paid from EDL since Sep 20

Continuing cash collection stream after Sep 20. We gradually paid currently from Aug 20 invoice. In general, 70% of account receivable collection still can be converted to USD.

A/R THB 592.6 mn

Cash received…

36

Q&A

37

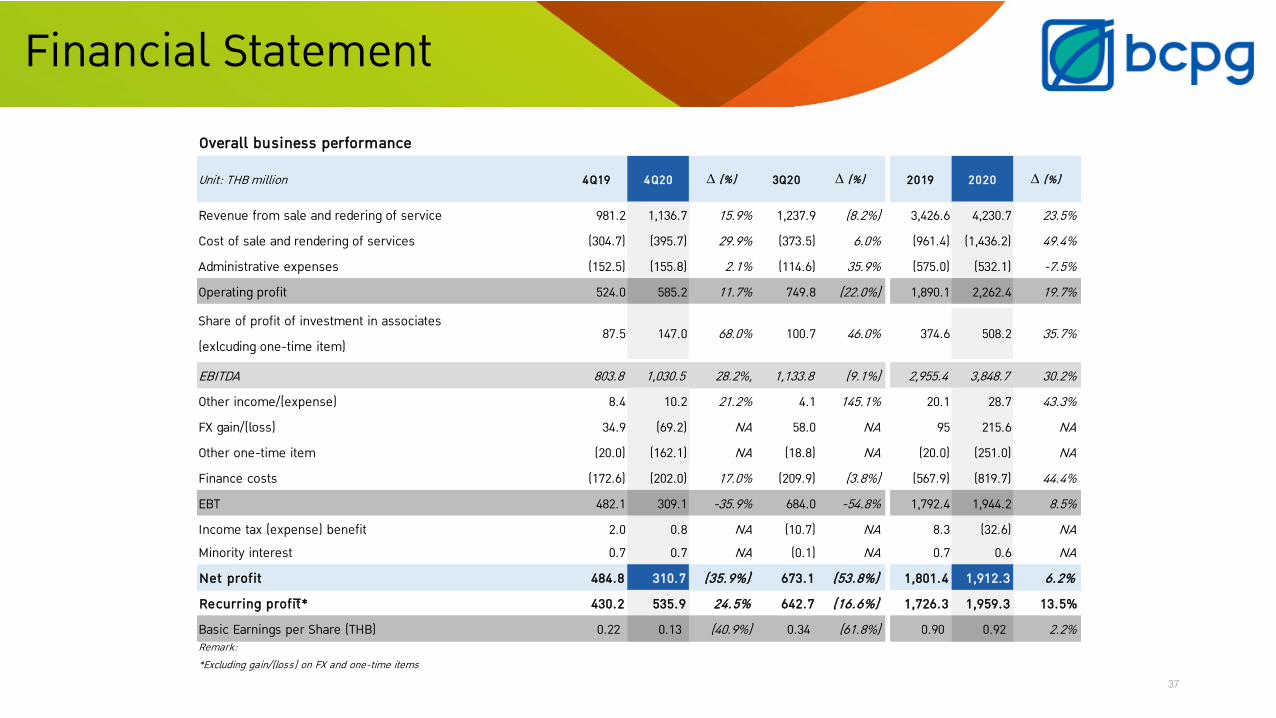

Financial StatementOverall business performance

Unit: THB million 4Q19 4Q20 ∆ (%) 3Q20 ∆ (%) 2019 2020 ∆ (%)

Revenue from sale and redering of service 981.2 1,136.7 15.9% 1,237.9 (8.2%) 3,426.6 4,230.7 23.5%Cost of sale and rendering of services (304.7) (395.7) 29.9% (373.5) 6.0% (961.4) (1,436.2) 49.4%Administrative expenses (152.5) (155.8) 2.1% (114.6) 35.9% (575.0) (532.1) -7.5%Operating profit 524.0 585.2 11.7% 749.8 (22.0%) 1,890.1 2,262.4 19.7%

Share of profit of investment in associates (exlcuding one-time item)

87.5 147.0 68.0% 100.7 46.0% 374.6 508.2 35.7%

EBITDA 803.8 1,030.5 28.2%, 1,133.8 (9.1%) 2,955.4 3,848.7 30.2%Other income/(expense) 8.4 10.2 21.2% 4.1 145.1% 20.1 28.7 43.3%FX gain/(loss) 34.9 (69.2) NA 58.0 NA 95 215.6 NAOther one-time item (20.0) (162.1) NA (18.8) NA (20.0) (251.0) NAFinance costs (172.6) (202.0) 17.0% (209.9) (3.8%) (567.9) (819.7) 44.4%EBT 482.1 309.1 -35.9% 684.0 -54.8% 1,792.4 1,944.2 8.5%Income tax (expense) benefit 2.0 0.8 NA (10.7) NA 8.3 (32.6) NAMinority interest 0.7 0.7 NA (0.1) NA 0.7 0.6 NANet profit 484.8 310.7 (35.9%) 673.1 (53.8%) 1,801.4 1,912.3 6.2%Recurring profitิ * 430.2 535.9 24.5% 642.7 (16.6%) 1,726.3 1,959.3 13.5%Basic Earnings per Share (THB) 0.22 0.13 (40.9%) 0.34 (61.8%) 0.90 0.92 2.2%Remark:*Excluding gain/(loss) on FX and one-time items

38

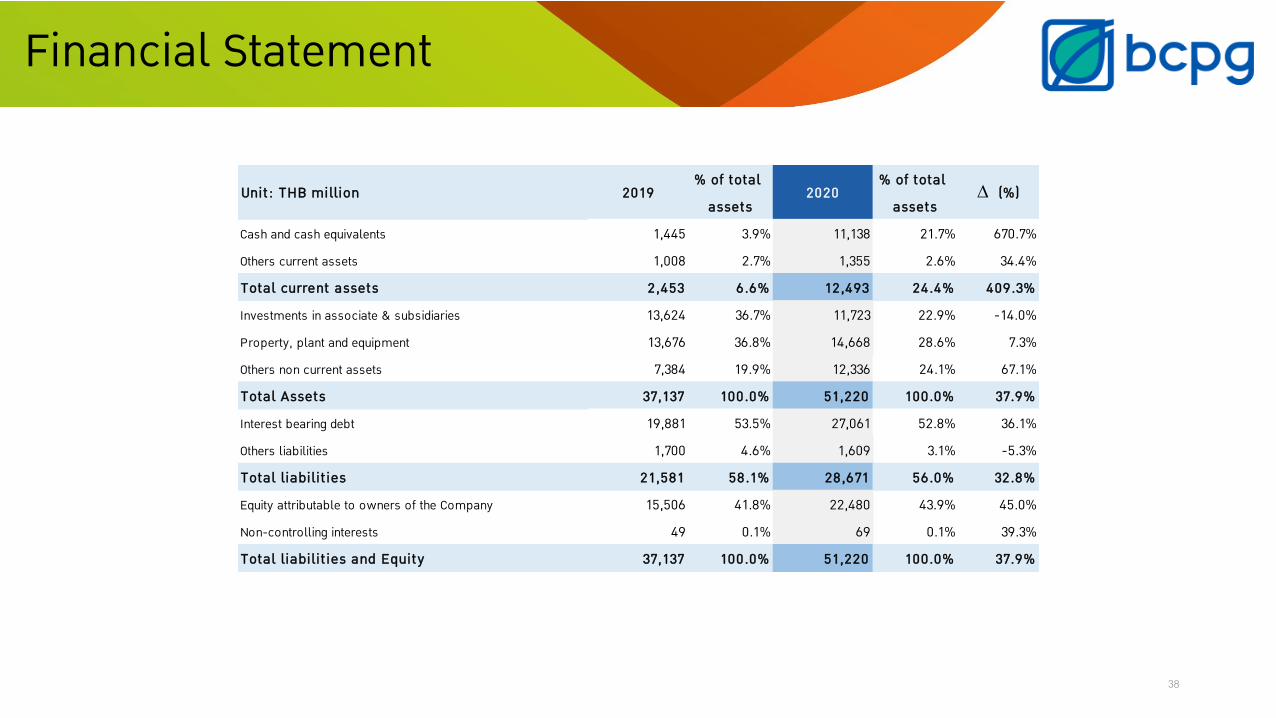

Financial Statement

Unit: THB million 2019% of total

assets2020

% of total assets

∆ (%)

Cash and cash equivalents 1,445 3.9% 11,138 21.7% 670.7%Others current assets 1,008 2.7% 1,355 2.6% 34.4%Total current assets 2,453 6.6% 12,493 24.4% 409.3%Investments in associate & subsidiaries 13,624 36.7% 11,723 22.9% -14.0%Property, plant and equipment 13,676 36.8% 14,668 28.6% 7.3%Others non current assets 7,384 19.9% 12,336 24.1% 67.1%Total Assets 37,137 100.0% 51,220 100.0% 37.9%Interest bearing debt 19,881 53.5% 27,061 52.8% 36.1%Others liabilities 1,700 4.6% 1,609 3.1% -5.3%Total liabilit ies 21,581 58.1% 28,671 56.0% 32.8%Equity attributable to owners of the Company 15,506 41.8% 22,480 43.9% 45.0%Non-controlling interests 49 0.1% 69 0.1% 39.3%Total liabilit ies and Equity 37,137 100.0% 51,220 100.0% 37.9%

39

Financial Statement

Unit: THB million 2019 2020 ∆ YoYNet cash from (used in) operating activities 2,120 3,079 959.4

Net cash from (used in) investing activities (6,001) (5,309) 691.6

Net cash from (repay to) financing activities 2,952 12,068 9,116.6

Net increase in cash and cash equivalents (930) 9,838 10,767.6

Cash and cash equivalents at 1 January 2,425 1,445 (980.1)

Effect of exchange rate changes on balances held in foreign currencies

(50) (145) (94.4)

Cash and cash equivalents at end period 1,445 11,138 9,693.1

CAPEX (5,852) (6,052) (200.0)

Consolidated Statement of Cash Flows

40

No. ProjectLocation

Operating Entity

% of Shareholding

Installed Capacity

(MW)

Contracted Capacity

(MW)Tariff Power Structure Off Taker CODDistrict Province

1 BCPG 1Bang Pa-in Ayutthaya BCPG N.A.

9.5 8

Adder THB 8/kWh

PEA 5/08/11BCPG 2 35.5 30 EGAT 16/07/12

2 BSE-BNN Bumnetnarong Chaiyaphum BSE 99.9 25.0 16

PEA

6/03/133 BSE-BPH Bang Pahan Ayutthaya BSE 99.9 25.0 16 5/04/134 BSE-BRM Prakonechai Buriram BSE-BRM 99.9 12.5 8 19/03/145 BSE-BRM1 Nongkee Buriram BSE-BRM 1 99.9 12.5 8 11/04/146 BSE-CPM1 Bumnetnarong Chaiyaphum BSE-CPM 1 99.9 12.5 8 24/04/147 BSE-NMA Dan Khun Tod NakhonRatchasima BSE-NMA 99.9 12.5 8 10/04/148 BSE-PRI Kabinburi Prachinburi BSE-PRI 99.9 25.0 16 21/04/14

9 Co-op: WSC Wiset Chai Chan Angthong BSE-PRI N.A. 5.0 5.0

FiT: THB 5.66/unit PEA(25 years)

23/12/16

10 Co-op: BPI Bang Pa-in Ayutthaya BSE-PRI N.A. 5.0 5.0 14/03/17

11 Co-op: AYA Phra Nakhon Si Ayutthaya

Ayutthaya BSE - PRI N.A. 2.0 2.0 23/12/16

12 Co-op (WVO)Saraburi Phra Phutthabat Saraburi BCPG N.A. 5.0 5.0

FiT: THB 4.12/unit PEA(25 years)

20/7/18

13 Co-op (WVO)Kanchanaburi Tha Muang Kanchanaburi BCPG N.A. 3.94 3.94 23/7/18

14 Lomligor Pak Panang Nakhon Sri Thammarat LLG 99.9 10.0 8.965 Adder THB 3.5/kWh PEA

(25 years) 11/4/19

15 Private floating solar Bang Pa-in Ayutthaya BCPG N.A. 2.1 2.1 Private PPA BBF 14/11/20

Conventional contracted capacity totaling of 150.0 MW

Conventional solar & wind projects in Thailand

41

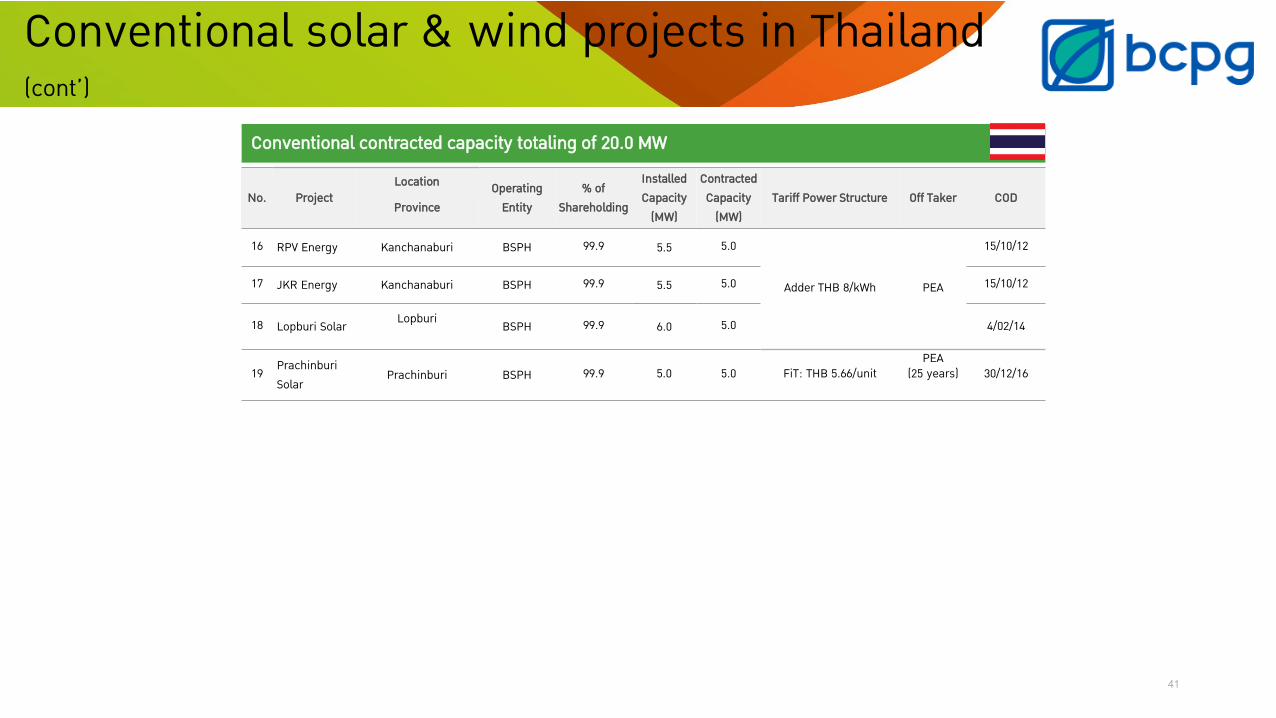

No. ProjectLocation Operating

Entity% of

Shareholding

Installed Capacity

(MW)

Contracted Capacity

(MW)Tariff Power Structure Off Taker COD

Province

16 RPV Energy Kanchanaburi BSPH 99.9 5.5 5.0

Adder THB 8/kWh PEA

15/10/12

17 JKR Energy Kanchanaburi BSPH 99.9 5.5 5.0 15/10/12

18 Lopburi Solar Lopburi BSPH 99.9 6.0 5.0 4/02/14

19 Prachinburi Solar

Prachinburi BSPH 99.9 5.0 5.0 FiT: THB 5.66/unitPEA

(25 years) 30/12/16

Conventional contracted capacity totaling of 20.0 MW

Conventional solar & wind projects in Thailand(cont’)

42

Total contracted capacity in pipeline of 15.2 MW as of 2Q20. COD target by 2021. Potential to be signed is another 17.6 MW

# Type Segment Relation-ship

Project Location Contracted Capacity

Terms (year)

Tariff power structure

Status/ COD

1 Rooftop Industrial Subsidiary Kingboard Uthai, Ayutthaya 0.752 MW 20 Private PPA COD 1/12/2018

2Rooftop Commercial Partner

Habito, T77, Sansiri

Wattana, Bangkok 0.053 MW 25 Private PPA COD 12/1/2019

3Rooftop

Commercial/Residential

Partner T77, Sansiri Wattana, Bangkok 0.376 MW 25 Private PPA COD 1/5/2019

4 Rooftop Commercial/Residential

Partner Escape, Sansiri

Lam Luk Ka, Phathum Thani

0.277 MW25 Private PPA COD 1/2/2020

5 Rooftop Industrial Partner PCF, Sansiri Pak Chong, Nakhon Ratchasima

0.063 MW25 Private PPA COD 1/2/2020

6 Rooftop Mix Others Lots Several cities 1.631 MW 15 – 20 Private PPA 4Q20

7 Rooftop Mix Others Lots Several cities 2.0 MW 15 – 20 Private PPA Under construction

8 Rooftop Commercial Partner (75%)

CMU Mueang, Chiangmai 9.0 MW 20 Private PPA Under construction

Other solar rooftop projects in Thailand

43

Contracted capacity of 14.7 MW

43

No. Project % ofInvestment Location Irradiation

(kWh/m2/year)Installed Capacity

(MW)

Contracted Capacity

(MW)

Feed-in Tariff (FiT)

(JPY/kWh)PPA Period

(Year) Off Taker Status

Operation1 S1

(Natkatsugawa) 100.0 Kagoshima, Japan 1,405 0.9 0.7 40 20

Kyushu Electric Power Company

COD 15/08/14

2 S11 (Takamori ) 100.0 Kumamoto, Japan 1,376 1.3 1.0 40 20 COD 16/02/15

3 S19 (Nojiri) 100.0 Miyazaki, Japan 1,433 1.1 0.9 40 20 COD 24/02/15

4 Tarumizu 100.0 Kagoshima, Japan 1,369 9.7 8.1 40 20 COD 31/08/15

5 Gotemba 100.0 Shizuoka, Japan 1,291 4.4 4.0 32 20 Tokyo Electric Power Company COD 16/04/18

Developing

6 Komagane 100.0 Nagano, Japan 1,472 32.0 25.0 36 20 Chubu Electric Power Company Expect to COD within 4Q21

7 Yabuki 100.0 Fukushima, Japan 1,294 27.9 20.0 36 20 Tohoku Electric Power Company Expect to COD within 4Q21

8 Chiba 1 100.0 Chiba, Japan 1,362 27.0 20.0 36 20 Tokyo Electric Power Company Expect to COD within 4Q21

9 Chiba 2 100.0 Chiba, Japan 1,362 13.0 10.0 32 20 Tokyo Electric Power Company Expect to COD within 2H22

Under development (Exclude from pipeline)10 Nagota 100.0 Kagoshima, Japan 1,448 30.0 24.0 36 20

Wait for Grid11 Isakida 100.0 Kagoshima, Japan 1,463 4.4 3.5 36 20

12 Shimoyunohira 100.0 Oita, Japan 1,330 9.6 8.0 36 20

13 S5 100.0 Kagoshima, Japan 1,371 7.2 6.0 36 20

Sold to IFFNikaho 100.0 Akita, Japan 1,136 13.2 8.8 40 20 Tohoku Electric Power Company COD 15/07/16

Nagi 100.0 Okayama, Japan 1,329 14.4 10.5 36 20 Chugoku Electric Power Company COD 02/03/17

Conventional solar projects in Japan

44

Public

BSE BSE-BRM BSE-BRM1 BSE-CPM1 BSE-NMA BSE-PRI LLG TDED

Thailand

Singapore

99.9% 99.9% 99.9% 99.9% 99.9% 99.9% 99.9% 75.0%

BSEH

100.0%

BCPGI SEGHPL

GreenergyHoldings

GreenergyPower

BCPG Wind

100.0% 100.0% 100.0%The Netherlands

JapanPetrowind

Energy

The Philippines 40.0%HMJ BCPGJ

EPC(1) AM(2) Investment(3) Project Under Development

Operating Projects

Operating Projects

Operating Projects

100.0% 100.0%

100.0% 51.0% 100.0% 100.0% 100.0% 100.0%

100.0%

(1) EPC = Groups of companies doing such business as (1) a turnkey EPC contractor and (2) an operation and maintenance contractor for solar power plants in Japan(2) AM = an Asset Management company rendering operation and maintenance service for the Tiramizu project and its remaining shares of 49.0% are held by a juristic person (3) Investment = companies investing in solar farms in Japan as TK investor

Laos

BCPGIndochina

99.9%

Nam San 3A

100.0%

IEAD

45.0%100.0% 33.33% Hong Kong

Nam San 3B

100.0%

Monsoon

100.0%

Group’s Business Structure

RPV

99.9%

JKRAQU

LS PS

99.9%99.9%

99.9% 99.9%

BSPH

99.9%

CDC

60.0%

45Survey link