IATA 2016 KEEPING EUROPE COMPETITIVE IN AN IMPORT ENVIRONMENT

Andrew Bonnington Editorial Director, Strategic Oil Markets Development May 2016

• Jet fuel market weakness explained

• Examining trade flows – new supplies coming online

• Analysing European import infrastructure

• Pipeline networks

• Conclusions

AGENDA

PLATTS – AN INTRODUCTION

Enabling the markets to perform with greater Transparency & Efficiency

Since

PLATTS – AN INTRODUCTION

Editorial and market assessments are conducted with complete Independence & Impartiality

EUROPEAN JET PRICES FALL SHARPLY

0

200

400

600

800

1000

1200

Dec-2013 Apr-2014 Aug-2014 Dec-2014 Apr-2015 Aug-2015 Dec-2015 Apr-2016

$/m

t

Source: Platts

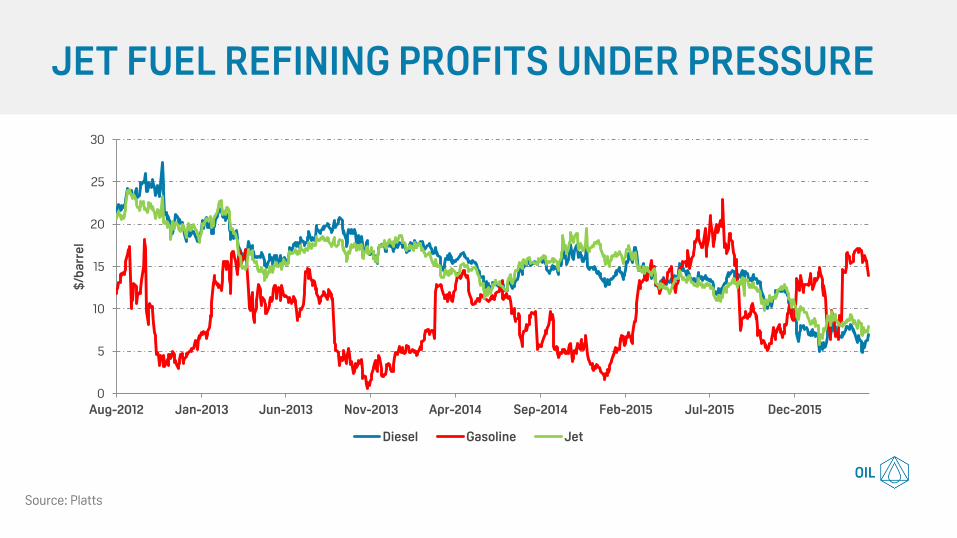

JET FUEL REFINING PROFITS UNDER PRESSURE

0

5

10

15

20

25

30

Aug-2012 Jan-2013 Jun-2013 Nov-2013 Apr-2014 Sep-2014 Feb-2015 Jul-2015 Dec-2015

$/b

arr

el

Diesel Gasoline Jet

Source: Platts

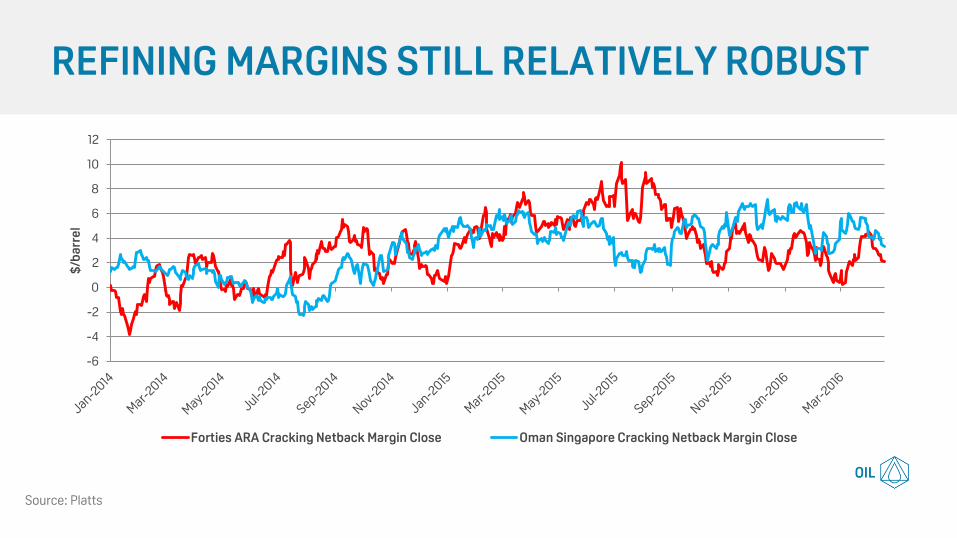

REFINING MARGINS STILL RELATIVELY ROBUST

-6

-4

-2

0

2

4

6

8

10

12

$/b

arr

el

Forties ARA Cracking Netback Margin Close Oman Singapore Cracking Netback Margin Close

Source: Platts

11.09

12.4

9.50

10.00

10.50

11.00

11.50

12.00

12.50

13.00

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

OECD Europe

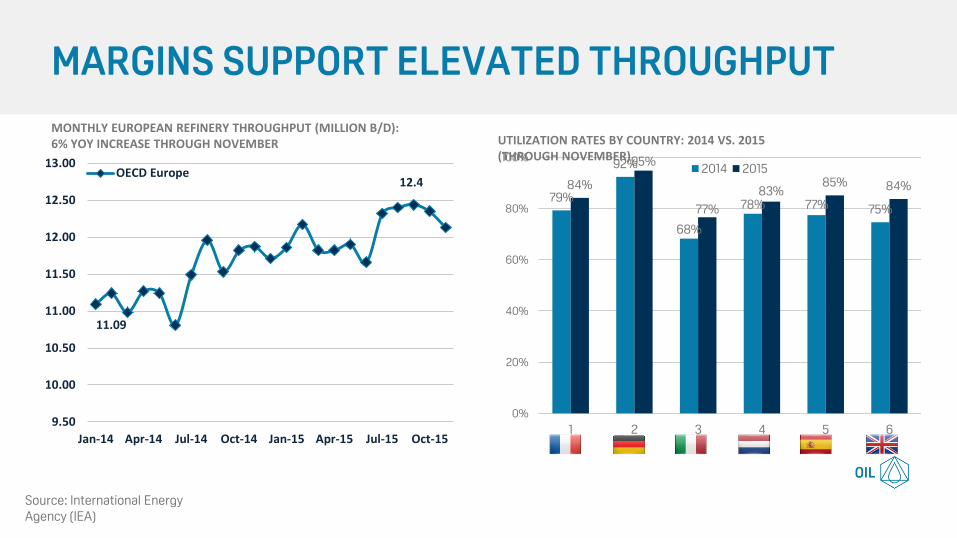

MARGINS SUPPORT ELEVATED THROUGHPUT

MONTHLY EUROPEAN REFINERY THROUGHPUT (MILLION B/D): 6% YOY INCREASE THROUGH NOVEMBER UTILIZATION RATES BY COUNTRY: 2014 VS. 2015

(THROUGH NOVEMBER)

79%

92%

68%

78% 77% 75%

84%

95%

77%

83% 85% 84%

0%

20%

40%

60%

80%

100%

1 2 3 4 5 6

2014 2015

Source: International Energy Agency (IEA)

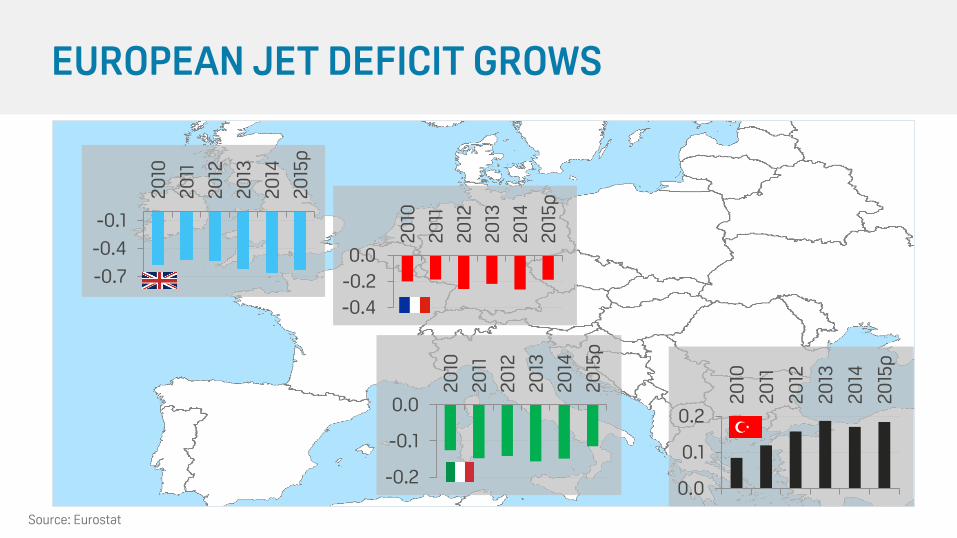

EUROPEAN JET DEFICIT GROWS

-0.7

-0.4

-0.1

20

10

20

11

20

12

20

13

20

14

20

15p

-0.4

-0.2

0.0

20

10

20

11

20

12

20

13

20

14

20

15p

0.0

0.1

0.2

20

10

20

11

20

12

20

13

20

14

20

15p

-0.2

-0.1

0.0

20

10

20

11

20

12

20

13

20

14

20

15p

Source: Eurostat

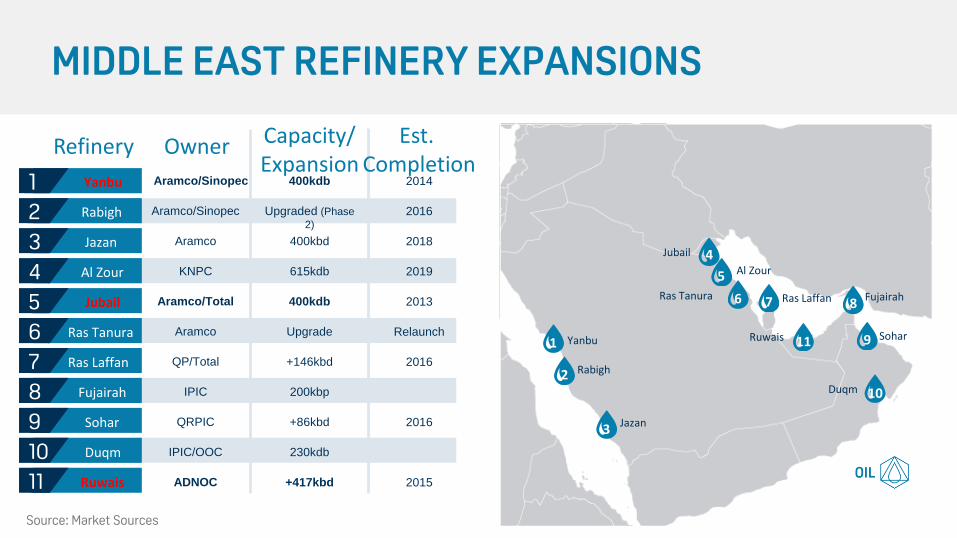

MIDDLE EAST REFINERY EXPANSIONS

Source: Market Sources

Yanbu

Jazan

Rabigh

Duqm

Sohar

Fujairah Ras Laffan

11

Ras Tanura

Jubail

Al Zour

Ruwais 1

2

3

4

5

6 7

11

8

9

10

Refinery

Yanbu

Rabigh

Jazan

Al Zour

Jubail

Ras Tanura

Ras Laffan

Fujairah

Sohar

Duqm

Ruwais

Aramco/Sinopec

Aramco/Sinopec

QP/Total

Aramco

KNPC

Aramco/Total

Aramco

IPIC

QRPIC

IPIC/OOC

ADNOC

400kdb

Upgraded (Phase

2)

+146kbd

400kbd

615kdb

400kdb

Upgrade

200kbp

+86kbd

230kdb

+417kbd

2014

2016

2016

2018

2019

2013

Relaunch

2016

2015

Owner Capacity/ Expansion

Est. Completion

1 2

3

4

5

6

7

8

9

10

11

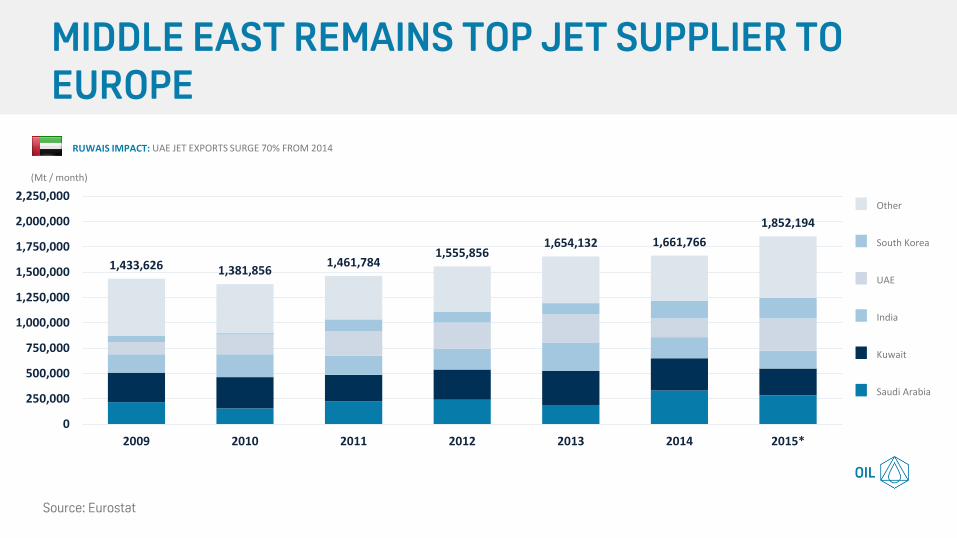

1,433,626 1,381,856 1,461,784

1,555,856 1,654,132 1,661,766

1,852,194

0

250,000

500,000

750,000

1,000,000

1,250,000

1,500,000

1,750,000

2,000,000

2,250,000

2009 2010 2011 2012 2013 2014 2015*

MIDDLE EAST REMAINS TOP JET SUPPLIER TO EUROPE

(Mt / month)

RUWAIS IMPACT: UAE JET EXPORTS SURGE 70% FROM 2014

Source: Eurostat

Saudi Arabia

Kuwait

India

UAE

South Korea

Other

175,629 mt

204,238 mt

264,332 mt

284,283 mt

316,697 mt

EU-28 MONTHLY JET IMPORTS/EXPORTS

Source: Eurostat

TOP 2015 IMPORTERS (MT/MONTH)

UAE

316,697

Kuwait

264,332

Saudi

Arabia

284,283

AG/Far

East flow

USA flow

26,257

Baltic flow

Spain

(165,480)

France

(367,380)

UK

(663,545)

Holland

(269,279)

Italy

(144,346

)

1,852,592 mt

663,545 mt

367,380 mt

262,990 mt

165,480 mt

TOP 2015 EXPORTERS (MT/MONTH)

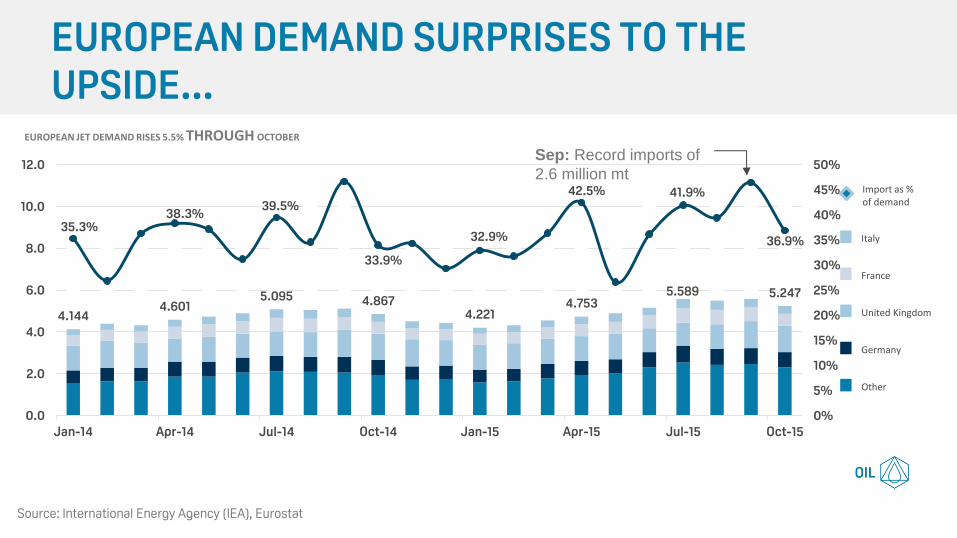

4.144 4.601

5.095 4.867 4.221

4.753 5.589 5.247

35.3% 38.3%

39.5%

33.9%

32.9%

42.5% 41.9%

36.9%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

EUROPEAN DEMAND SURPRISES TO THE UPSIDE...

Source: International Energy Agency (IEA), Eurostat

Sep: Record imports of

2.6 million mt

EUROPEAN JET DEMAND RISES 5.5% THROUGH OCTOBER

Other

Germany

United Kingdom

France

Italy

Import as % of demand

UK NOW HUGELY RELIANT ON IMPORTS

0

2

4

6

8

10

12

14

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Mil

lio

n t

on

ne

s

Imports Domestic Production

Source: UK DECC

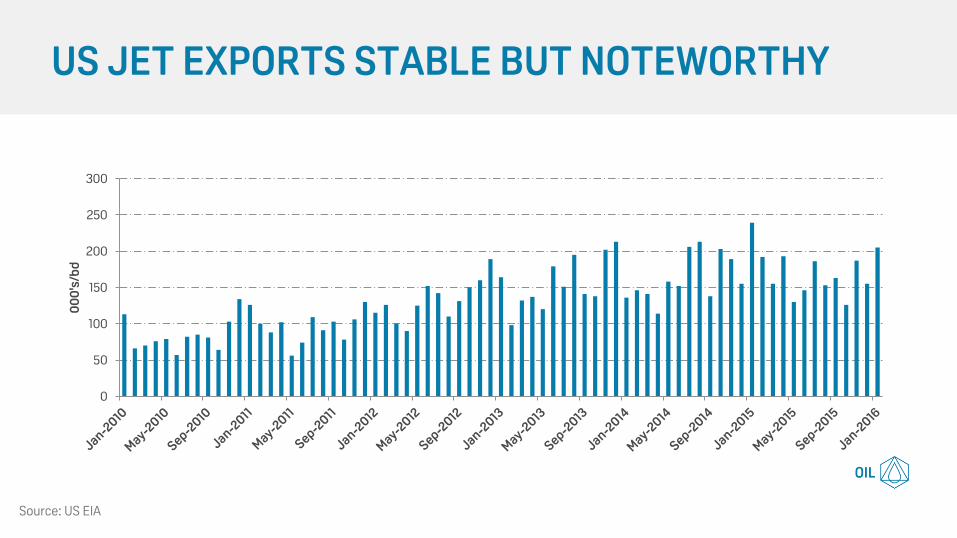

US JET EXPORTS STABLE BUT NOTEWORTHY

0

50

100

150

200

250

300

00

0's

/bd

Source: US EIA

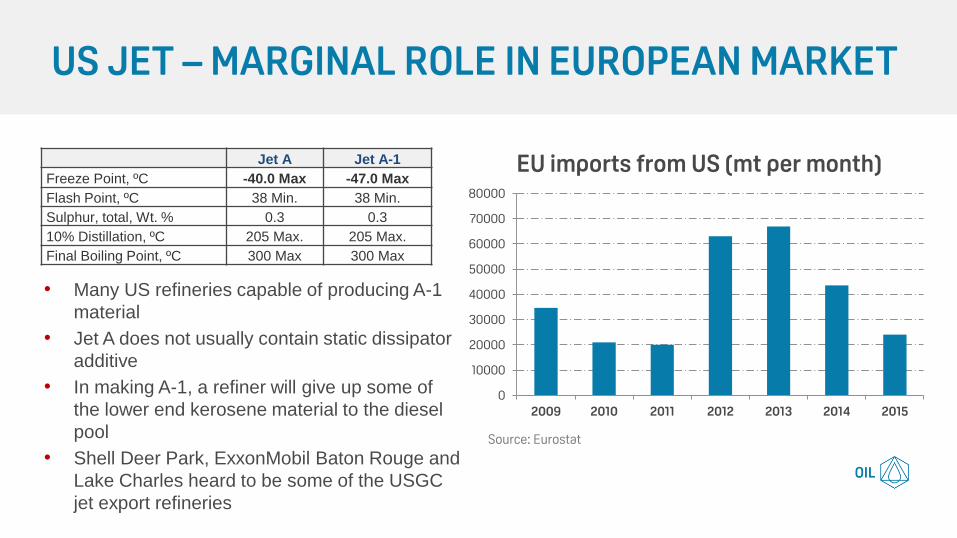

US JET – MARGINAL ROLE IN EUROPEAN MARKET

Jet A Jet A-1

Freeze Point, ºC -40.0 Max -47.0 Max

Flash Point, ºC 38 Min. 38 Min.

Sulphur, total, Wt. % 0.3 0.3

10% Distillation, ºC 205 Max. 205 Max.

Final Boiling Point, ºC 300 Max 300 Max

• Many US refineries capable of producing A-1

material

• Jet A does not usually contain static dissipator

additive

• In making A-1, a refiner will give up some of

the lower end kerosene material to the diesel

pool

• Shell Deer Park, ExxonMobil Baton Rouge and

Lake Charles heard to be some of the USGC

jet export refineries

0

10000

20000

30000

40000

50000

60000

70000

80000

2009 2010 2011 2012 2013 2014 2015

EU imports from US (mt per month)

Source: Eurostat

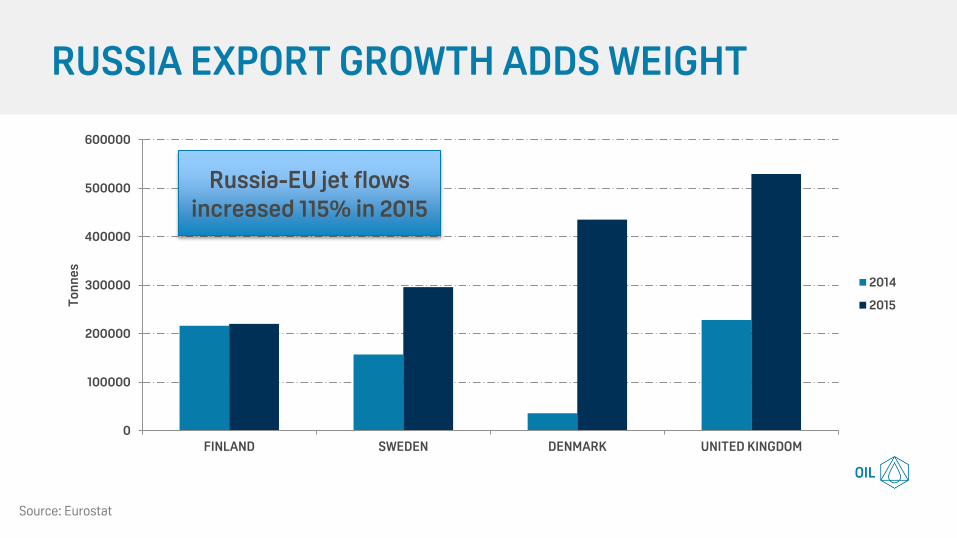

RUSSIA EXPORT GROWTH ADDS WEIGHT

0

100000

200000

300000

400000

500000

600000

FINLAND SWEDEN DENMARK UNITED KINGDOM

To

nn

es

2014

2015

Source: Eurostat

Russia-EU jet flows increased 115% in 2015

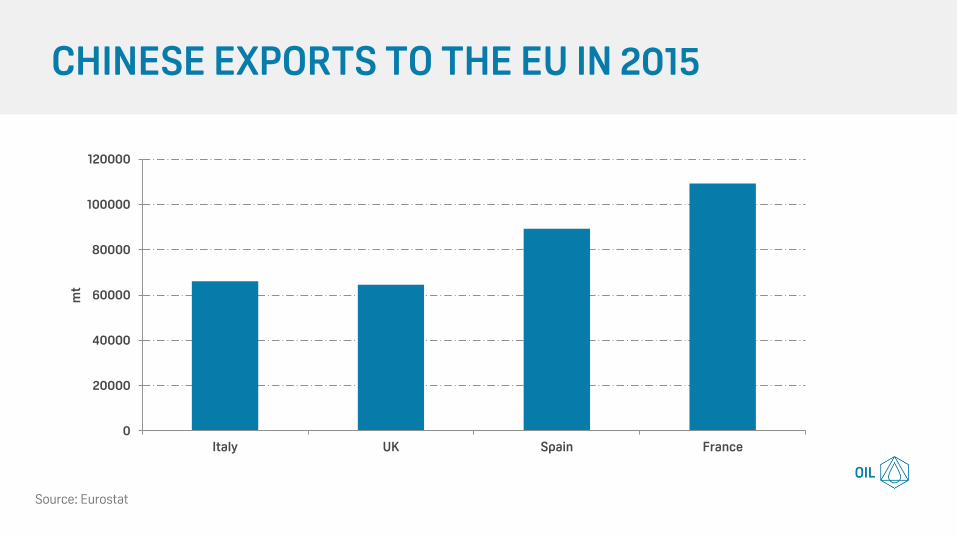

CHINESE EXPORTS TO THE EU IN 2015

0

20000

40000

60000

80000

100000

120000

Italy UK Spain France

mt

Source: Eurostat

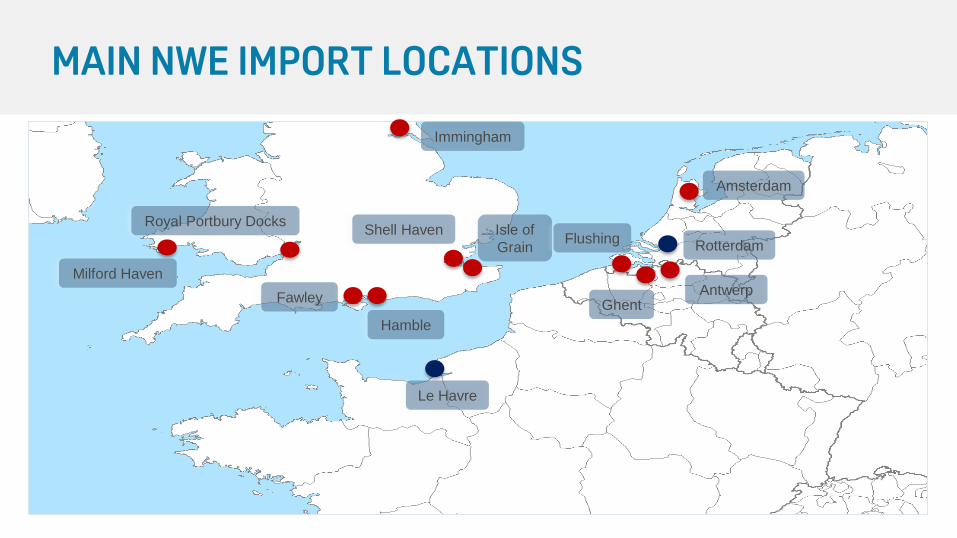

MAIN NWE IMPORT LOCATIONS

Immingham

Shell Haven

Isle of

Grain

Royal Portbury Docks

Hamble

Fawley

Le Havre

Ghent

Rotterdam

Amsterdam

Antwerp

Flushing

Milford Haven

• Puma Energy buying Milford Haven from Murco

• Isle of Grain and Shellhaven

• CLH buying GPSS in UK

• Vitol investment in Antwerp storage

• Floating storage

PORT INFRASTRUCTURE DEVELOPMENTS

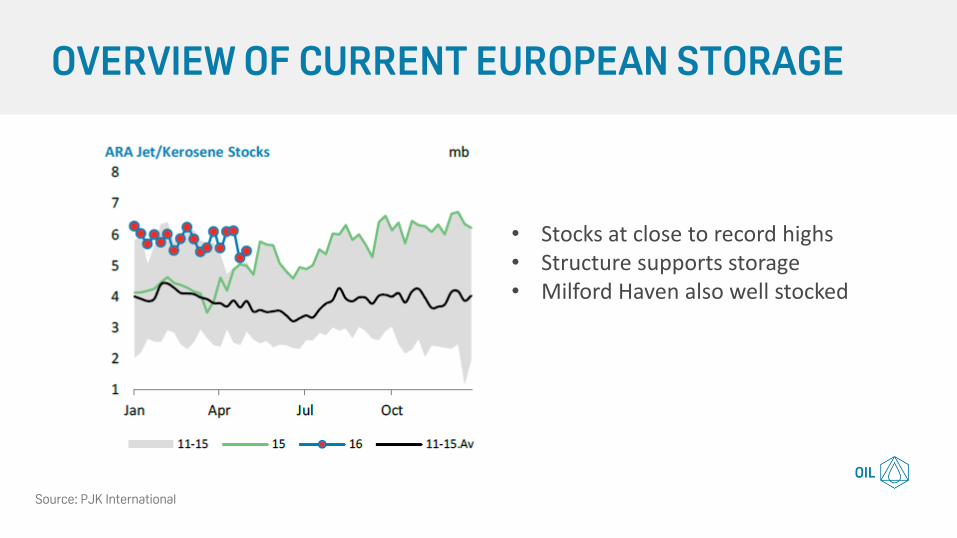

OVERVIEW OF CURRENT EUROPEAN STORAGE

• Stocks at close to record highs • Structure supports storage • Milford Haven also well stocked

Source: PJK International

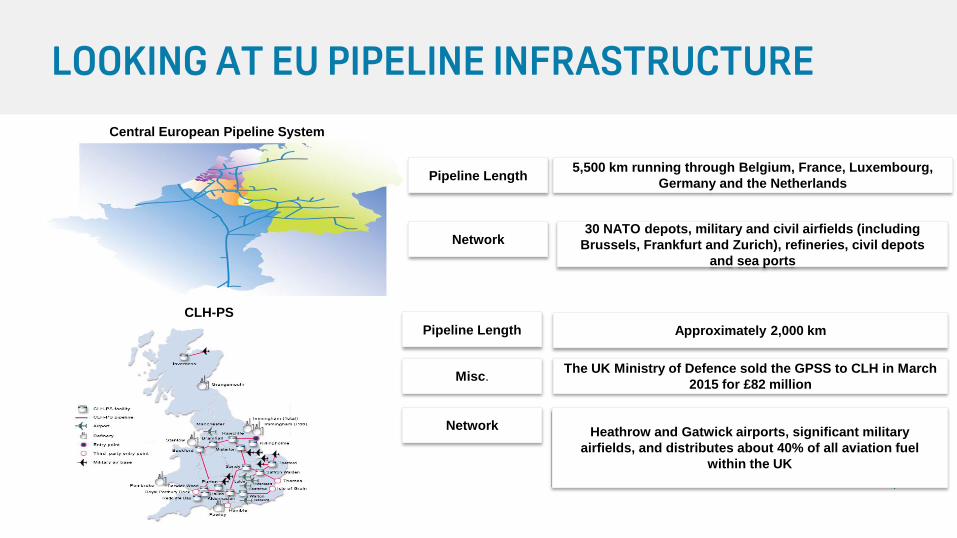

LOOKING AT EU PIPELINE INFRASTRUCTURE

5,500 km running through Belgium, France, Luxembourg,

Germany and the Netherlands Pipeline Length

30 NATO depots, military and civil airfields (including

Brussels, Frankfurt and Zurich), refineries, civil depots

and sea ports

Network

Approximately 2,000 km Pipeline Length

Heathrow and Gatwick airports, significant military

airfields, and distributes about 40% of all aviation fuel

within the UK

Network

The UK Ministry of Defence sold the GPSS to CLH in March

2015 for £82 million Misc.

Central European Pipeline System

CLH-PS

LOOKING AT EU PIPELINE INFRASTRUCTURE

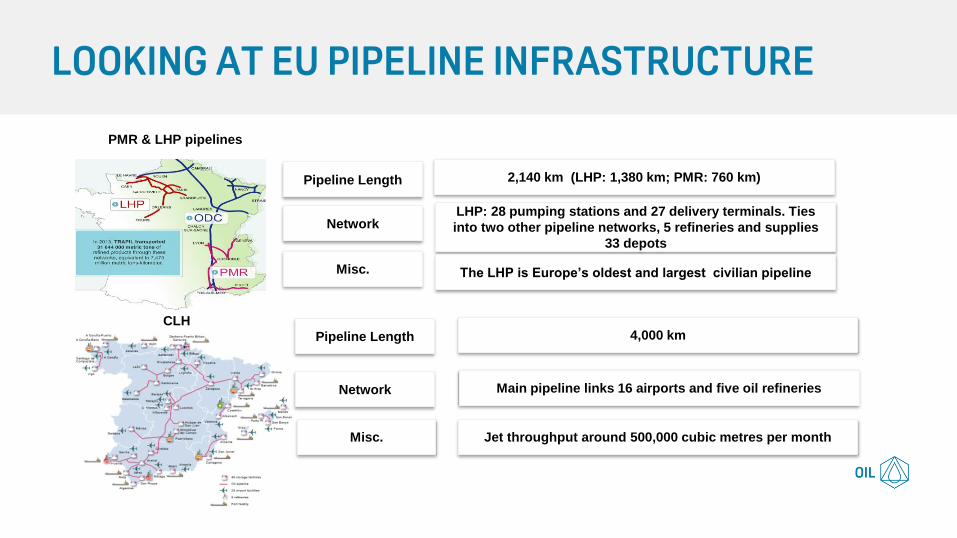

2,140 km (LHP: 1,380 km; PMR: 760 km) Pipeline Length

LHP: 28 pumping stations and 27 delivery terminals. Ties

into two other pipeline networks, 5 refineries and supplies

33 depots

Network

The LHP is Europe’s oldest and largest civilian pipeline Misc.

Pipeline Length 4,000 km

Network Main pipeline links 16 airports and five oil refineries

Misc. Jet throughput around 500,000 cubic metres per month

PMR & LHP pipelines

CLH

• High refinery margins lead to higher domestic output

• Middle East remains largest supply to European market

• New supplies from US, Russia and China providing competition

• Infrastructure investments provide more competition of imports

• Complex pipeline infrastructure serves industry well

CONCLUSIONS