Auditing the Auditors: An International Analysis of the Effectiveness of National Inspection

Regimes on Audit Quality

Elizabeth Carson

Professor of Accounting

University of New South Wales

Roger Simnett

Scientia Professor of Accounting

University of New South Wales

Ann Vanstraelen

Professor of Accounting and Assurance Services

Maastricht University

3 September 2013

Preliminary draft: Please do not quote without permission of the authors.

We thank Anna Huggins, Ashna Prasad, Shirley Tsau and Lei Zou for research assistance, and

appreciate the comments of participants at workshops at the University of Auckland, the University of

New South Wales, the International Symposium on Audit Research and the Accounting and Finance

Association of Australia and New Zealand Conference. We also acknowledge the financial support of

the Australian Research Council.

2

3

Auditing the Auditors: An International Analysis of the Effectiveness of National Inspection

Regimes on Audit Quality

ABSTRACT: We undertake an examination of the effectiveness of the different forms of

public oversight and independent inspection regimes that have been put in place by the

various national public oversight bodies of the auditing profession. Using a large sample of

companies from 33 countries over the period 2006-2010, we find that audit quality is higher

in countries where independent inspections are in place and are member of IFIAR. In order to

control for potential endogeneity concerns, we then limit our examination to countries that

introduced independent inspection programs during our sample period, and we find that audit

quality is higher in the period after inspections are introduced compared to the pre-inspection

period. Our results, however, do not support an association between the different ways of

organizing public oversight and audit quality. This provides evidence that the existence of

public oversight and independent inspections has an impact on audit quality, but not the

characteristics of the inspection programs. Overall, our study contributes to the emerging

literature on public oversight of the auditing profession.

Keywords: public oversight; audit quality; IFIAR; inspections

Data Availability: The data are available from sources identified in this study.

4

I. INTRODUCTION

In the last decade one of the key reform initiatives directed at improving the

quality of auditing has been the introduction of public oversight over the audit profession.

This is observed at both the national and international levels, and impacts on both the

setting of standards for the auditing profession as well as its continuing regulation. For

example, over the past decade the setting of auditing standards has been more likely to be

undertaken by bodies independent of the audit process (such as the Public Company

Accounting Oversight Board (PCAOB) in the U.S., and the Australian Auditing and

Assurance Standards Board (AUASB), or independent of the profession (for example, the

International Auditing and Assurance Standards Board (IAASB)). The continuing

regulation of the auditing profession has also been increasingly removed from the auditing

profession to independent national public oversight boards (POBs) (for example, the

PCAOB in the U.S. and the Australian Securities and Investments Commission (ASIC) in

Australia).

The U.S. was one of the front-runners in introducing public oversight of the

auditing profession, and the PCAOB model of independent public oversight has formed

the basis of many other national POBs (Franzel 2012). The PCAOB has four main

responsibilities under the Sarbanes-Oxley (2002) Act: (1) to register public accounting

firms; (2) to establish auditing and other professional standards; (3) to conduct and report

on regular inspections of registered public accounting firms; and (4) to conduct

investigations and disciplinary proceedings of the auditing profession where rules or

standards may have been violated. While other countries have followed suit, they have

made different choices with regard to the organization of public oversight. For example,

most countries outside the U.S. have a policy of adopting or converging with standards

5

developed by the IAASB (Simnett and Smith 2005), and the setting of auditing standards

is separated from the body undertaking the inspection program.

Also, while inspection programs have become the key plank of the strategy and

work effort of all national POBs, divergent approaches to these inspection programs have

developed. For example, some countries have elected to have direct inspections by the

independent POB while other countries have chosen for inspections to be undertaken by

professional bodies in the country under the supervision of the POB. Further, the

frequency of inspections of audit firms varies across countries and some countries have a

longer history of public oversight of the auditing profession compared to others.

Internationally, a growing number of independent national audit regulators have

decided to join the international organization, the International Forum of Independent

Audit Regulators (IFIAR). This organization was founded in September 2006 and aims to

promote audit quality, and effective independent audit regulatory activity. IFIAR has a

specific focus on inspections of audit firms, and co-operation regarding the inspection of

international audit networks (IFIAR 2012).

The rationale behind the auditing profession’s moves to POBs is that regulators

and other market participants expect that independent public oversight is a more effective

way to ensure audit quality than self-regulation by the audit profession. Critics are not

convinced, however, and question the adequacy of the expertise, knowledge and skills of

inspectors of independent POBs (e.g,. Glover et al. 2009). This reflects the often raised

concern in relation to public oversight of the auditing profession of the trade-off between

expertise and independence (e.g., DeFond 2010) and the effectiveness of such oversight.

Given the significant amount of resources that is spent on public oversight, its

effectiveness is an important empirical question. There is an emerging literature in the

U.S. addressing this question (e.g. Lennox and Pittman 2010; DeFond and Lennox 2011;

6

Carcello et al. 2011); however to date there has been no international comparison of the

differing national approaches to public oversight, and in particular the inspection

programs, and their association, if any, with resulting audit quality.

In this paper we examine the effectiveness of the inspection programs, and their

different forms, as undertaken by the national POBs. Specifically, we examine whether

inspections (between countries with and without inspection programs) affect audit quality,

and whether there is a difference in audit quality between the pre- and post-inspection

periods (within member country analysis for countries introducing inspections during the

study period). We further examine whether IFIAR membership, first-time inspections,

inspection experience, type of inspection system (direct inspections versus oversight of

the inspection process) and frequency of inspections affect audit quality. We measure

audit quality by the level of abnormal accruals of audit firms’ client companies.

Using a large sample of listed companies from 33 countries during the period

2006-2010, we find that companies domiciled in countries where inspection programs are

in place have significantly lower abnormal total accruals and this holds for both income-

increasing and income-decreasing abnormal accruals. Further, we find that the level of

abnormal accruals (both income-increasing and income-decreasing) of audit firms’ clients

in countries that introduced inspection programs during our sample period is significantly

lower in the post-inspection period compared to the pre-inspection period. This compares

with no change in abnormal accruals over 2006-2010 for clients in those countries that did

not introduce an inspection program. We further find that companies domiciled in IFIAR

member countries have significantly lower abnormal accruals, which is to be attributed to

lower income-decreasing accruals. We do not find much support for differences in audit

quality that could be explained by differences in design of the oversight system within the

group of countries with independent inspections of audit firms in place. Overall, our

7

findings contribute to the emerging literature on public oversight of the auditing

profession. This study is one of the first that compares the benefits, if any, of the

differences in the national regulatory systems at an international level. A better

understanding of the effectiveness of the different types of oversight systems can facilitate

the design of an optimal and potentially harmonized oversight system which would be

congruent with the objectives of IFIAR. Further, our insights may also prove useful for

regulators across the world in their ongoing discussions and decisions regarding mutual

recognition of public oversight across countries.

The remainder of this paper is organized as follows. In Section II, we provide the

relevant background for the study and formulate the hypotheses that we test. In Section

III, we describe the data, descriptive statistics and research design. In Section IV, we

present the results of the study and we conclude in Section V.

II. BACKGROUND AND HYPOTHESES DEVELOPMENT

The Organization of Public Oversight

A number of high-profile corporate financial reporting scandals in which auditors

were implicated, including the collapse of Enron and the role of its auditor Arthur Andersen,

prompted regulators in the U.S. to end self-regulation of the auditing profession. It was

replaced by a system of public oversight of the auditing profession, created by the Sarbanes-

Oxley Act in 2002. Since 2004, all audit firms that issue an audit report for a SEC-reporting

company or substantially participate in the audit are required to be registered with the

PCAOB. One of the primary duties of the PCAOB is to perform periodic independent

inspections of these firms. In reflecting upon the effectiveness of the PCAOB seven years

after inception, Acting Chairman Goelzer (2009) noted, “in evaluating the Board’s work, the

question is not how many inspections have been conducted or how many pages of standards

8

have been written. It is whether investors are better off as a result. While that is not a question

that is likely to be resolved based on anything I might say today, I believe that evidence is

accumulating that they are.”

Goelzer went on to outline the process by which this benefit was achieved: “… we

know from the visibility that we have through the inspections and remediation process, that

the large firms have made important changes to their systems of quality control in response to

PCAOB inspections findings. These have included such things as changes related to partner

evaluation and compensation to place greater emphasis on audit quality and technical skills;

changes to management structures to provide greater separation between the audit quality

function and audit business operations; creation of national- or regional-level positions or

committees to promote and monitor audit quality; and modifications to internal inspection

programs.”

After the creation of the PCAOB in the U.S., other countries around the world have

followed the U.S. example of creating independent POBs by either introducing or expanding

their use of inspection programs of audit firms. The European Commission (EC) introduced

independent oversight over financial reporting and auditing in its revised Eighth Directive of

2006. This was further reinforced in the EC Green Paper Audit Policy (2010) addressing the

need to strengthen the current role of audit supervision to ensure the full independence of the

public oversight systems from the audit profession in all Member States. In the Green Paper,

the EC suggests transforming the current European Group of Auditors’ Oversight Board

(EGAOB)1 into a so-called ‘Lamfalussy Level 3 Committee’ to strengthen cooperation

between national public oversight bodies, ensure an improved and common approach to

1 The European Group of Auditors’ Oversight Board (EGAOB) was founded in December 2005 and is composed

of high-level representatives from the respective public oversight authorities of EU Member States or alternate

representatives from national ministries in the event that such a national oversight system is not yet established.

The role of the EGAOB is to provide technical input into the preparation of possible measures of the EC in

implementing the 8th

EU Directive on statutory audit, and it facilitates the EC’s implementation of the

requirements of external quality assurance for statutory auditors and audit firms auditing public interest entities.

9

inspections of audit firms, and foster convergence in the application of the rules. This

accentuates the EC’s belief that the establishment of an independent oversight board with the

vested power to enforce cooperation among member states will ultimately improve audit

quality and the level of confidence investors place on financial statement reporting, thereby

contributing to financial stability.

In a similar vein, at an international level, the International Forum of Independent

Audit Regulators (IFIAR) was established in September 2006 by 18 independent audit

regulatory organizations (these being the POBs in these countries) around the world. The

mission of IFIAR is to create a platform to share knowledge of the audit market environment

and practical experience regarding independent audit regulatory activity; to promote

collaboration in regulatory activities; and to provide a focal point for contacts with other

international organizations that have an interest in audit quality (IFIAR 2013). While

membership of IFIAR is not mandated by law, the requirements for becoming a member of

IFIAR clearly reinforce the expectation of an improved audit environment and outline how

this can be achieved. IFIAR memberships are strictly confined to regulatory agencies that are:

(1) independent of the audit profession, which means that the majority of the relevant

governing body should be non-practitioners and that the funding of the board should be free

of influence by the profession; and (2) engaged in audit regulatory functions in the public

interest. The latter requirement refers to the responsibility of the POB in each IFIAR member

country to conduct periodic inspections of audit firms undertaking audits of public interest

entities (IFIAR 2012). Since its inception, IFIAR has increased its membership base from the

initial 18 countries in 2006 to 44 countries at the beginning of 2013.

Inspection programs of audit firms are the main technique for improving deficiencies

in audit quality and driving improvements in the audit process. For example, the Financial

Reporting Council (2012 18) in the United Kingdom describes the objectives and process of

10

their inspection program as “to monitor and promote improvements in the quality of auditing.

As part of our work, we monitor firms’ compliance with the regulatory framework for

auditing, including the Auditing Standards, Ethical Standards and Quality Control Standards

for auditors and other requirements under the Audit Regulations…”. ASIC (2012), the

regulator of the auditing profession in Australia, describes the aim of their audit inspection

program as being to “promote high-quality external audits of financial reports of listed and

other public interest entities in Australia. High-quality audits are an important contributor to

financial report quality and market confidence”.

Although considerable resources go into these inspection regimes, very little is known

about how effective they have been. In 2012, IFIAR released their first global survey of

inspection findings (IFIAR 2012). The survey was designed to identify the level of inspection

activity and common inspection findings related to the audits of public companies. The survey

identified that more needs to be done to improve the consistency of performance by auditors,

and confirmed that IFIAR members are noting audit findings in numerous common areas

(inspection themes) including professional skepticism and tone at the top, group audits,

revenue recognition, internal control testing, and engagement quality control review across

the different jurisdictions.

Prior Literature

The increasing prominence of the various national audit regulators undertaking public

oversight responsibilities for this profession was explored by Simnett and Smith (2005). They

compared and contrasted the various structures that have been instigated or proposed by the

leading national and international bodies in relation to public oversight of the auditing

standard-setting process. These POBs had taken on various dimensions of both the auditing

standard-setting responsibility, and the continuing monitoring function, mainly through

11

inspections of the auditors and audit firms. At this time a unique combination was that in the

U.S., the PCAOB had taken on both the law-maker (developing standards) and the law-

enforcer (inspections) aspects of this public oversight.

Despite its potential merits, public oversight of the auditing profession has been

subject to criticism and skepticism. For example, Glover et al. (2009) criticize the PCAOB for

insufficient staff, staff with limited expertise, inadequate transparency of procedures and

inspection outcomes, and slow feedback. Small U.S. audit firms also do not appear to see an

improvement in audit quality or increased public confidence (Daugherty and Tervo 2010).

Thus, as public oversight is contested in some quarters, its effectiveness has become the

subject of academic research.

Prior research on public oversight has mainly focused on the U.S., as the PCAOB is

one of the few public oversight bodies that publicly disclose inspection findings. Early studies

provide descriptive evidence on inspection reports that are issued by the PCAOB and the type

of quality control defects and audit deficiencies that are found (Hermanson et al. 2007;

Hermanson and Houston 2008; Roybark 2009). Subsequently, academic research has looked

into the informational value of PCAOB inspection reports. For example, Dee et al. (2011)

find a negative stock market reaction to PCAOB sanctions imposed upon one of the Big 4

audit firms. The informational value of PCAOB inspection reports has also been addressed by

examining client hiring and firing of audit firms. For example, Lennox and Pittman (2010)

find no changes in audit firm market shares following deficient inspection findings. However,

Daugherty et al. (2011) find that for triennially inspected audit firms, clients are more likely

to dismiss an audit firm with a deficient inspection report and switch to an audit firm with a

clean inspection report. Similarly, Abbott et al. (2013) find that clients with effective audit

committees or high potential agency conflicts are more likely to switch to a successor auditor

without such deficiencies.

12

A number of studies suggest that public oversight bodies are able to discriminate

between various levels of audit quality. For example, Gunny and Zhang (2013) find that

clients of triennially inspected audit firms with deficiencies identified by the PCAOB have

higher levels of abnormal accruals. A similar result is reported by Van Opijnen et al. (2011) in

a Dutch setting. Furthermore, there is some support within individual countries as to the

effectiveness of national public oversight. For example, Carcello et al. (2011) find that

absolute abnormal accruals decrease following PCAOB inspections. Similarly, Fuentes et al.

(2010) find that earnings quality has improved in Spain since the Spanish public oversight

body started its inspections. Knechel et al. (2012) find that audit fees increase in response to

deficient inspection results.

Apart from the exceptions noted above, research on public oversight bodies outside

the U.S. is very limited. The purpose of our study is to compare the effectiveness

internationally of public oversight of the auditing profession and to provide a comparison of

the relative effectiveness of the differing aspects of the organization of the various public

oversight systems.

Development of Hypotheses

This study examines the effectiveness of public oversight of the auditing profession

from an international perspective. In addition, we examine a number of specific choices that

countries have made with regard to the organization of public oversight. First, we look into

countries that have an inspection program in place and compare these with countries without

inspections of audit firms. Secondly, in order to address potential endogeneity concerns, we

consider whether the introduction of inspection processes in countries that introduced

inspection programs during our sample period is followed by an increase in audit quality. In

additional analyses, we look into the choice of a public oversight body of a country to become

13

a member of IFIAR. As discussed above, IFIAR membership is restricted to those public

oversight bodies that meet certain criteria. Further, we examine whether there is any

association between the characteristics of the various inspection regimes and audit quality.

We infer audit quality by examining the accruals properties of audit firms’ client companies.

In line with prior research, we consider that a high quality audit will be more effective at

constraining opportunistic reporting by managers, which is reflected in lower levels of

abnormal accruals (e.g. Carey and Simnett 2006; Francis and Wang 2008). We formulate the

following hypotheses:

Inspections

For the reasons outlined earlier, we expect that companies domiciled in countries that

have independent inspections in place have higher audit quality compared to companies

domiciled in countries that do not perform independent inspections of audit firms. We

therefore hypothesize that:

H1: Companies domiciled in countries where audit firms are subject to independent

inspections are associated with higher audit quality compared to companies domiciled in

countries where audit firms are not subject to independent inspections.

Pre-/post-inspection

We understand that the above analysis could potentially suffer from endogeneity

issues. Thus we examine whether, for the smaller group of countries in which public oversight

was initiated during the sample period, there is a difference in audit quality for pre- versus

post-inspection audits. We expect that the benefits of introducing an inspection process will

result in audit quality being higher in the post-inspection period. This is tested by the

following hypothesis:

H2: Audit quality after the introduction of the inspection process will be higher than

audit quality before the inspection process began.

14

III. DATA, DESCRIPTIVE STATISTICS, AND RESEARCH DESIGN

Sample Selection and Description

To collect data for this study, we use the Worldscope database which provides

financial data covering 91 countries. The initial scope of the sample is to include all 40

member countries of IFIAR as at the end of 20102, and another 51 non-IFIAR member

countries that are covered in Worldscope. However, data for some countries are lacking or

insufficient for this type of international research and are therefore excluded from the sample.

Furthermore, the data is then filtered to only contain samples that do not have any missing

variables that are required to calculate the dependent and independent variables. Through the

process of filtering, several countries whose number of complete observations fell below 50

per year are eliminated. Finally, consistent with prior studies, financial institutions with

Standard Industrial Codes 6000-6999 are excluded from the sample because this industry is

subject to specific accounting requirements that significantly affect the calculation of

discretionary accruals. The final dataset contains a total of 33 countries, seven of which do

not perform independent inspections and eight of which are non-IFIAR members at the end of

2010. Our sample period is 2006-2010, but we also collect data for 2005 for the calculation of

the discretionary accruals of 2006. In total, we have 39,278 firm-year observations over the

period 2006-2010. The year 2006 is an appropriate year to start to undertake this analysis,

because as well as IFIAR coming into existence in this year, it is also after the introduction of

International Financial Reporting Standards (IFRS) for most countries, and it is the year that

the European Commission published its revised EU 8th Directive, requiring member countries

to install public oversight (with an implementation deadline of two years maximum). For the

testing of Hypothesis 2, we restrict the sample to the 11 countries where public oversight and

2 Data collection occurred in 2012; at that time, data was only available up until the end of 2010.

15

inspections started during the period 2007-2010, and use the year 2006 as the baseline where,

by design, no country has an inspection regime in place. Table 1 provides an overview of the

number of firm-year observations per country included in the sample in the period 2006 –

2010 and its inspection regime, IFIAR membership status, and the year inspections by

independent POBs commenced. We gather information on the frequency, experience, and

type of inspection system using the country profile documentation available on the IFIAR

website, the official websites of the POBs and/or through follow up direct contact with these

boards. This information, for listed entities in each country, is summarized in Table 1.

Specification of Empirical Models

To test our hypotheses, we infer audit quality from reduced managerial discretion

resulting in less abnormal accruals, all other things being equal. As commonly used in the

literature, we measure abnormal accruals by means of the performance-adjusted cross-

sectional modified Jones model (Jones 1991; Dechow et al. 1995; Kothari et al. 2005). This

model has also been widely used in the international auditing literature to measure audit

quality (e.g., Kwon et al. 2007; Francis et al. 2013). Specifically, we estimate:

effectsfixedindustryyearcountry

ROAPPEARREVAssets

TA titititi

ti

ti

//

)(1

,4,3,,2

1,

10,

[1]

Where: TAi,t is total accruals in year t (defined as the change in non-cash current assets

minus change in current liabilities excluding current portion of long-term debt, minus

depreciation and amortisation) scaled by lagged total assets; ASSETSi,t-1 is a firm’s total

assets in year t-1; ΔREVi,t is sales in year t less sales in year t-1; ΔARi,t is accounts receivable

in year t less accounts receivable in year t-1; PPEi,t is net property, plant and equipment in

year t; and ROAi,t is return on assets in year t. A company’s unadjusted abnormal accruals are

set equal to the firm-specific residuals estimated from the above model of expected (normal)

accruals.

16

As an alternative measure for abnormal accruals, we use abnormal working capital

accruals based on the expectation model in DeFond and Park (2001). A common argument in

the literature is that non-working capital accruals are less susceptible to manipulation than

working capital accruals (e.g., DeFond and Jiambalvo 1994; Teoh et al. 1998). Specifically,

we calculate abnormal working capital accruals as realized working capital minus expected

working capital, where expected working capital is assumed to be a fixed proportion of sales

(Dechow et al. 1998; DeFond and Park 2001). Or formally:

tititititi SSWCWCAWCA ,1,1,,, *)/( [2]

Where: AWCAt is abnormal working capital accruals in year t; WCt and WCt-1 are non-

cash working capital in year t and year t-1, respectively, where non-cash working capital is

computed as the difference between (current assets minus cash and short-term investments)

and (current liabilities minus short-term debt); and St and St-1 are sales in year t and year t-1.

To test our hypotheses, we use the following model:

EffectsFixedYearEffectsFixedIndustryInterestofVariables

LawofRuleAuditorGrowthPPEMB

LossGrowthePerformancLeverageSizeAWCAorATA

titititi

tititititititi

__

_

10

,9,8,7,6

,5,4,3,2,10,,

[3]

Where:

|ATAi,t| is the absolute value of performance-adjusted abnormal total accruals

measured by modified Jones model in Equation 1; |AWCAi,t| is the absolute value of abnormal

working capital accruals in Equation 2; Sizei,t is the natural logarithm of total assets (in

millions); Leveraget is the ratio of long-term debt to total assets; Performancei,t is the

operating cash flow scaled by total assets; Growthi,t is the percentage of year-to-year growth

in sales; Lossi,t is an indicator variable for loss in the current year; MBi,t is a company’s

market value of equity scaled by book value of equity; PPE_Growthi,t is a company’s one

year growth in gross property, plant and equipment from year t-1 to year t. Auditori,t is an

17

indicator variable for Big N auditors; Rule of Lawi,t is a World Bank Governance Indicator

developed by Kaufmann et al. (2010 4) and represents “capturing perceptions of the extent to

which agents have confidence in and abide by the rules of society, and in particular the

quality of contract enforcement, property rights, the police, and the courts, as well as the

likelihood of crime and violence”; and Industry is a vector of industry indicator variables and

Year is a vector of year indicator variables. The variables of interest are: Inspection, which is

an indicator variable taking the value of 1 when the observation relates to a country where

independent inspections are in place; Post_Inspect, which is an indicator variable taking the

value of 1 when the observation relates to the post-inspection period; IFIAR, which is an

indicator variable taking the value of 1 if the observation relates to a country whose regulator

is a current member of IFIAR; First_time, which is an indicator variable taking the value of 1

when it is the first year that inspections are performed; Ln_exp, which is the natural logarithm

of the number of years of inspection experience; Type_oversight, which represents the type of

oversight system taking the value of 2 in case of direct oversight, 0 in case of oversight

through the profession under supervision of the oversight board, and 1 in case of a

combination; and Freq_Inspect, which is an indicator variable taking the value of 1 in cases

where large audit firms are inspected on an annual basis.

IV. RESULTS

Descriptives

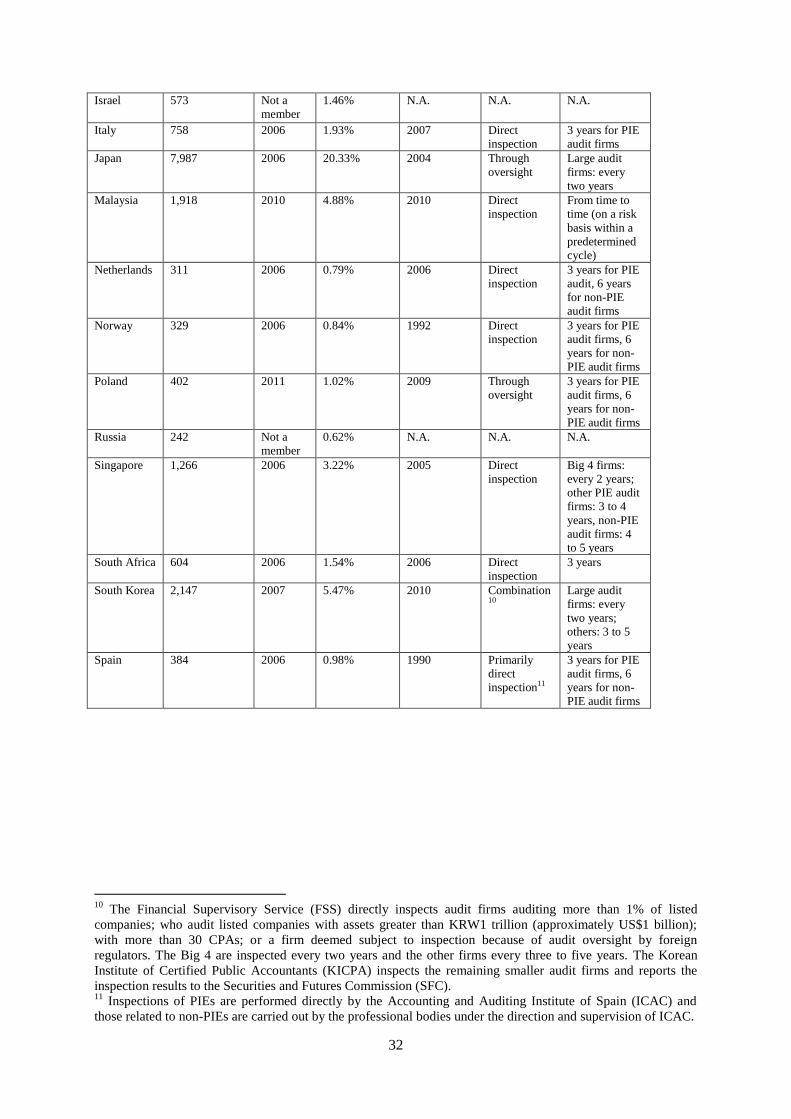

Table 1 presents the 33 countries included in the sample, the number of observations

per country, IFIAR membership and other public oversight features. The most highly

represented countries in the sample in terms of number of observations are Japan (20.33%)

and the U.S. (16.02%). All other countries individually represent less than 7% of the total

sample. To control for the discrepancy in the number of observations and as our focus is at the

18

country-level, we use weighted regressions where we equally weight countries rather than

equal weight client observations, consistent with the approach used by Choi and Wong

(2007). During the sample period (2006-2010), 25 countries (75.75%) are members of

IFIAR.3 There are seven countries (21.2%) in our sample that do not have a public oversight

system in place during the sample period4, and 13 countries (39.39%) that installed a public

oversight system during the sample period. The year when public oversight inspections

started in the countries in our sample ranges from 1978 to 2010. Table 1 further demonstrates

that within the group of countries with a public oversight system in place, there is much

variation in the organization of public oversight. There is variation in the type of oversight

system, which can be direct inspection (16 countries), primarily direct inspection (4

countries), through oversight only (4 countries), or a combination of direct inspections and

oversight (2 countries). Also, the frequency of oversight varies ranges from on demand

(Brazil) or from time to time (Malaysia), to 3 years for PIE audit firms (which is the minimum

requirement for EU countries) up to annually for large audit firms (Australia, Canada,

Germany, Switzerland, Taiwan, Thailand, United Kingdom, and United States).

- INSERT TABLE 1-

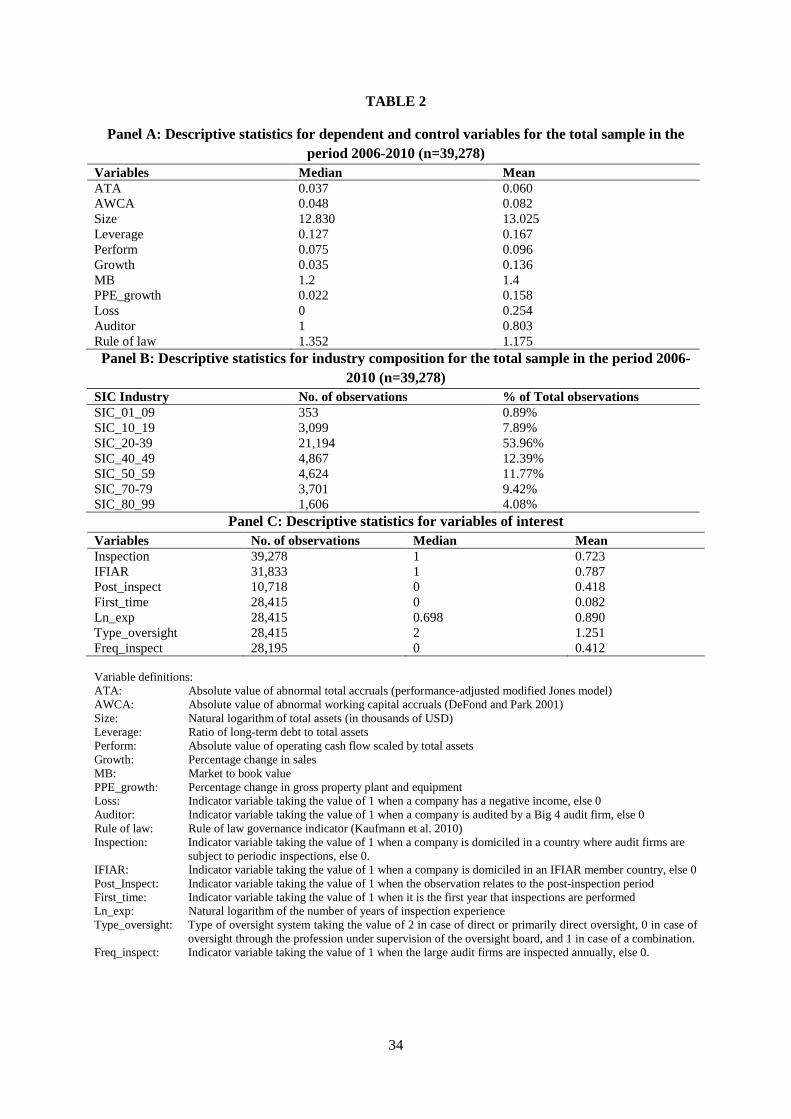

Table 2 presents the descriptive statistics of the dependent and control variables, the

variables of interest, and the distribution across industries. Table 2, Panel A, shows that the

mean (median) abnormal total accruals in absolute value is 0.060 (0.037). The mean (median)

total assets is 3,866 million USD (373 million USD), while the ratio of long-term debt to total

assets has a mean (median) of 16.7% (12.7%). The mean (median) absolute value of operating

3 As can be seen from Table 1, two other countries in our sample joined IFIAR after 2010.

4 It is noted that these seven countries did not have an oversight body in place in 2011, but some of these

countries recently have or are in the process of installing public oversight. Hong Kong, India, Indonesia and

Russia have, or are in the process of establishing, a public oversight system and are considered in the transitional

period for European Union recognition (information as at January 2011); Israel: no public oversight system

(information as at January 2011); China: European Commission declared the oversight system of China to be

equivalent to those of the EU (information as at January 2011); Chile: no public oversight system.

19

cash flow scaled by total assets is 0.096 (0.075). The mean (median) growth rate measured as

the percentage change in sales is 13.6% (3.5%), and the mean (median) growth rate of gross

property plant and equipment is 15.8% (2.2%). The mean (median) market to book value is

1.4 (1.2). In the sample, 25.4% of the observations have a negative income, and 80.3% are

audited by a Big 4 auditor5. The rule of law has a mean (median) value of 1.175 (1.352).

Table 2, Panel B, shows that the majority of the observations (53.96%) relate to the

manufacturing industry (SIC 20-30), followed by 12.39% in the utilities industry (SIC 40-49),

and 11.77% in the wholesale trade industry (SIC 50-59).

Table 2, Panel C, presents the mean (median) values of the variables of interest in the

analyses and the corresponding number of observations. For the testing of Hypothesis 2, we

concentrate on those countries where public oversight was introduced in the period 2007-

2010, and use the year 2006 as the benchmark as, at that stage, no country had public

oversight in place. In total, 11 countries started their inspections in the period 2007-2010,

which corresponds with 10,718 observations of which 58.2% (41.8%) relate to the pre- (post)

inspection period. In the additional analysis, for the testing of IFIAR membership, we focus

on the period 2007-2010, and exclude the year 2006 since IFIAR was founded in September

2006. For this analysis, we have 31,833 observations, 78.7% of which belong to an IFIAR

member country. Our additional analysis of characteristics of inspections uses a sample of

those countries where inspections were in place before or during the sample period, which

represents 28,415 observations. Of these observations, 8.2% relate to a country where

inspections are performed for the first time. The mean (median) years of experience with

inspections is 4.5 (4) years. With regard to the type of oversight system, the median

observation relates to a country where direct or primarily direct inspection is in place. Note

5 We note that the data for the type of auditor are retrieved from Worldscope which only offers static data for this

data item. As we do not have access to earlier versions of Worldscope, we cannot control for changes during the

sample period.

20

that in the analyses we classify primarily direct inspection under direct inspection since our

sample is comprised of listed companies and all listed companies are subject to direct

inspection in those countries where primarily direct inspection applies.

-INSERT TABLE 2-

Multivariate Analysis

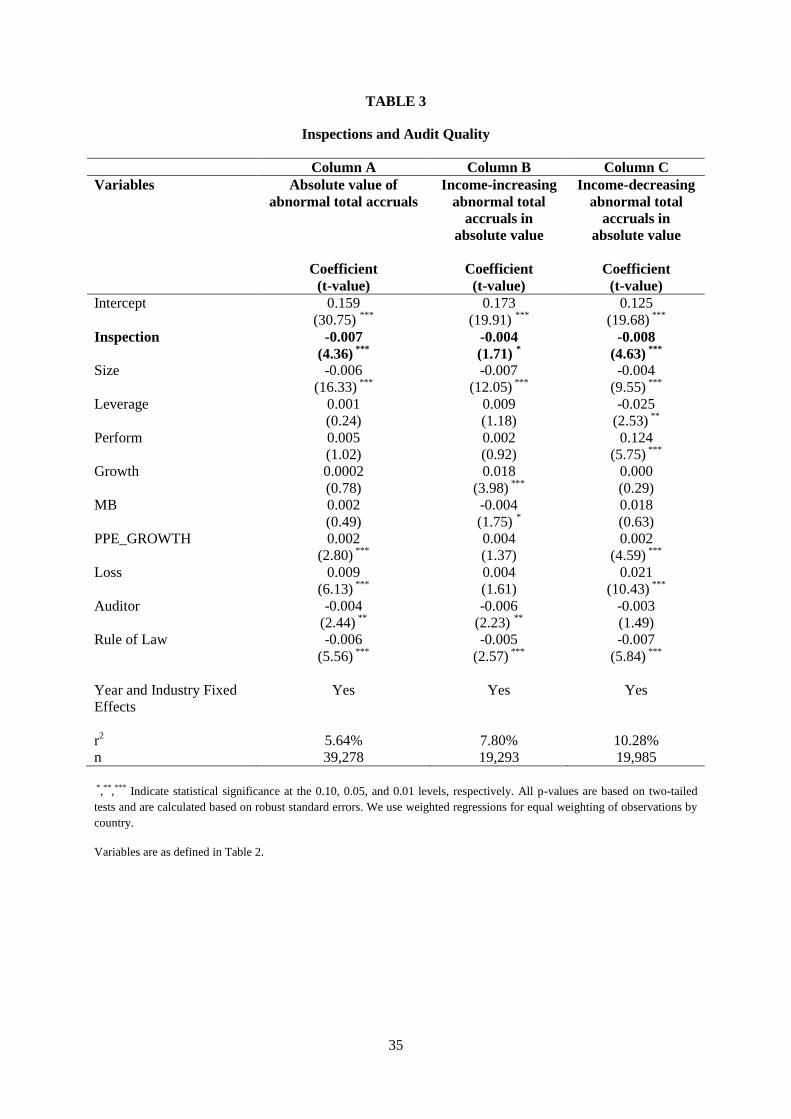

Table 3 presents the results of the testing of Hypothesis 1 on the association between

inspections and audit quality (measured by abnormal total accruals). The results (Column A)

show a significant negative coefficient for the Inspection variable (p<0.01), implying that

companies domiciled in countries with independent inspections have significantly lower

levels of abnormal accruals. This would suggest that audit quality is higher in those countries

as auditors appear to act as a stronger constraint on earnings management. Significant control

variables are size, PPE growth, loss, auditor, and rule of law, all of which are in the expected

direction. We repeat the analysis for income-increasing (Column B) and income-decreasing

(Column C) accruals, and find that inspections are associated with significantly less income-

increasing (p<0.10) and income-decreasing accruals (p<0.01). We repeat these analyses with

abnormal working capital accruals as the dependent variable. The results (not tabulated for

parsimony) are qualitatively similar: inspections are associated with significantly less

abnormal working capital accruals (p<0.01). Similarly, inspections are associated with

significantly less income-increasing abnormal working capital accruals (p<0.05), and

significantly less income-decreasing abnormal working capital accruals (p<0.01).

-INSERT TABLE 3-

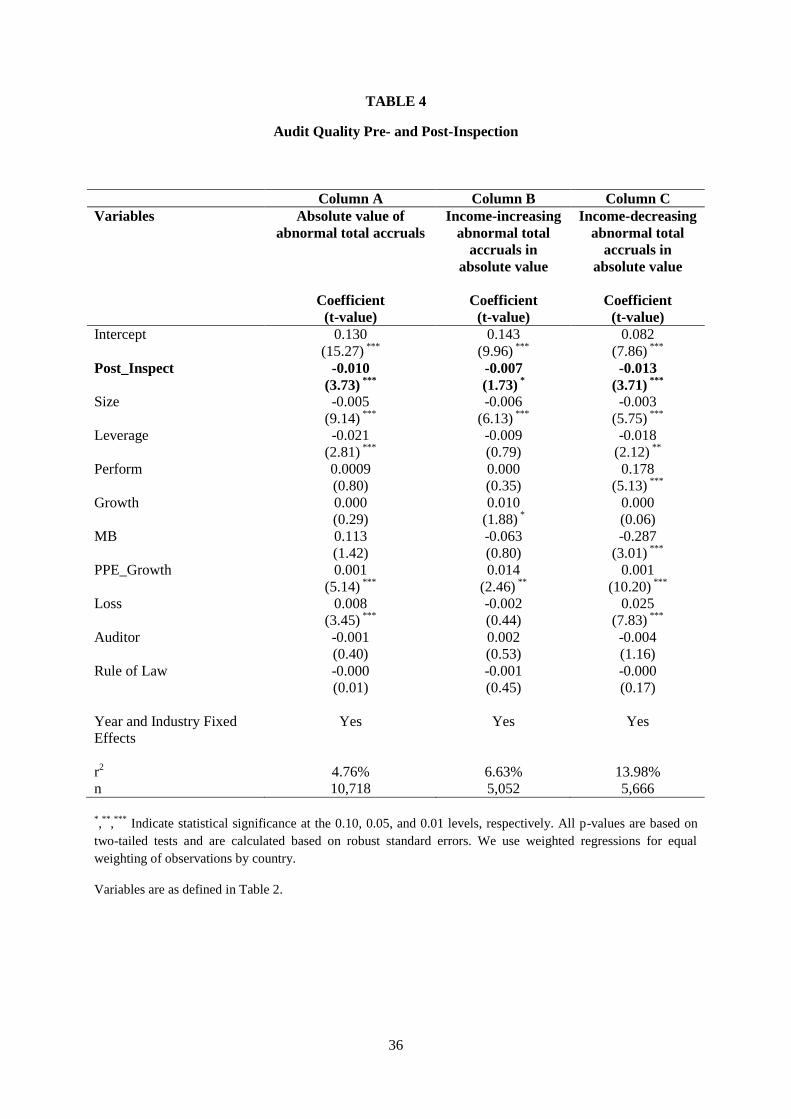

In Table 4, the results of the analysis of Hypothesis 2 relating to audit quality pre- and

post-inspections are presented. The coefficient of the post inspection variable (Column A) is

significantly negative (p<0.01). This implies that the level of abnormal accruals of companies

21

domiciled in countries that installed public oversight during the period 2007-2010 is

significantly lower in the post-inspection regime compared to the pre-inspection regime.

Significant control variables are size, leverage, PPE growth, and loss, all in the expected

directions. This result holds for income-increasing (Column B, p<0.10) and for income-

decreasing accruals (Column C, p<0.01). A univariate t-test shows that the mean value of

absolute abnormal accruals is 0.072 in the pre-inspection regime (n=6,236) and drops to 0.061

in the post-inspection regime (n=4,482) (p<0.01). There is a potential concern that all

environments have experienced an increase in audit quality over this period, and so we

compare these results with companies in our sample from countries in which public oversight

was not installed either before or during the period 2007-2010. For this sample we find a

mean absolute value of abnormal accruals of 0.071 in the benchmark year 2006 (n=1,117),

and 0.073 in the years 2007-2010 (n=5,276), which suggests a slight increase in abnormal

accruals. In a multivariate analysis (not reported), the coefficient of the benchmark year 2006

is not significant. Collectively, this supports the view that the implementation of an inspection

regime has resulted in an increase in audit quality, as over the same period there is no similar

improvement in audit quality where there are no inspection processes in place. We repeat the

analyses of Table 4 with abnormal working capital accruals as the dependent variable.

Untabulated results show that post-inspection these accruals are significantly lower in

absolute value (p<0.01), which is attributed to income-decreasing (p<0.01) abnormal working

capital accruals being significantly lower, while income-increasing abnormal working capital

accruals are negative but not significant. We note that if we run unweighted regressions, we

obtain significant lower abnormal working capital accruals in absolute value (p<0.01), both

for income-increasing (p<0.05) and income-decreasing (p<0.01) abnormal working capital

accruals.

-INSERT TABLE 4-

22

Additional Analyses

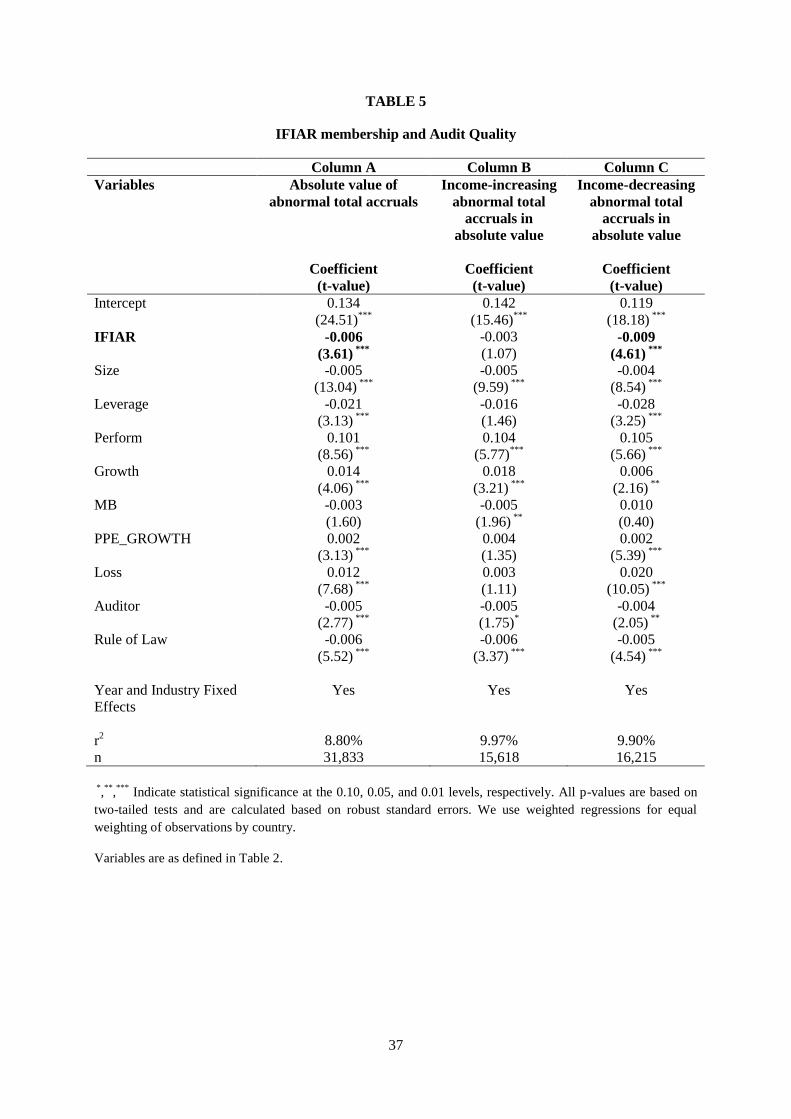

IFIAR Membership

As outlined earlier, IFIAR membership is confined to regulatory agencies that are

independent of the audit profession and conduct periodic independent inspections of audit

firms undertaking audits of public interest entities. Both of these characteristics of a POB

should result in a higher audit quality in that country, and thus we expect that IFIAR

membership has a positive association with audit quality. Since IFIAR was founded in

September 2006, the period of study for this analysis starts in 2007.

Table 5 presents the results of the analysis on the association between IFIAR

membership and audit quality. The results (Column A) show a significant negative coefficient

for IFIAR (p<0.01), implying that companies domiciled in IFIAR member countries have

significantly lower levels of abnormal accruals. This would suggest that audit quality is higher

in those countries as auditors appear to act as a stronger constraint on earnings management.

We repeat the analysis for income-increasing (Column B) and income-decreasing (Column C)

accruals, and find that IFIAR membership is associated both with significantly less income-

decreasing accruals (p<0.01), and negative but insignificant income-increasing abnormal

accruals. We repeat these analyses with abnormal working capital accruals as the dependent

variable. The results (not tabulated for parsimony) are qualitatively similar: IFIAR

membership is associated with significantly less abnormal working capital accruals (p<0.05).

For IFIAR membership, we find a significant negative association with income-decreasing

abnormal working capital accruals (p<0.05), and a negative but insignificant association with

income-increasing abnormal working capital accruals.

-INSERT TABLE 5-

23

Unweighted Regression Analyses

We re-ran the models (untabulated for parsimony) presented in Tables 3 and 5 using

unweighted regressions and subsequently excluding alternatively Japan and the U.S., which

are the dominant countries in the sample. In all cases (full sample, with and without Japan,

with and without the U.S.), we observe a significant negative coefficient for Inspection (as in

Table 3) for the absolute value of abnormal total accruals, income-increasing absolute

abnormal total accruals, and income-decreasing absolute abnormal total accruals.

For IFIAR, we observe a significant negative coefficient for the full sample and

without the U.S. for the absolute value of abnormal total accruals, income-increasing absolute

abnormal total accruals, and income-decreasing absolute abnormal total accruals. Without

Japan, the coefficient for IFIAR is only significantly positive for income-decreasing abnormal

accruals.

Unweighted regressions (untabulated for parsimony) for the models presented in

Table 4 also give a significant negative coefficient for the variable Post_Inspect for the

absolute value of abnormal total accruals, income-increasing absolute total accruals, and

income-decreasing absolute total accruals. Note that Japan and the U.S. are not included in

the sample used for testing of hypothesis 2 as shown in Table 4 and therefore their inclusion

or exclusion will not influence the results reported.

Characteristics of inspection process

In examining the impact of the major characteristics of the inspection process on audit

quality we focus on those countries where independent inspections of audit firms are in place,

and consider a number of choices made by regulators in the design of inspection processes.

Specifically, we consider three major characteristics of the inspection regime, being the

period of time since inspections commenced (outlining the number of years of inspection

24

experience), the type of inspection system, being inspections directly undertaken by the

independent POB or undertaken by professional bodies under the POB’s supervision, and the

frequency of inspections. This allows an examination as to whether variation in the

characteristics of inspection regimes is associated with audit quality.

We examine whether a learning effect arises from the cumulative experience of being

inspected. We also consider the differential impact of the two main types of inspection

systems on audit quality. We consider whether inspections of audit firms directly performed

by inspectors of independent POBs have a stronger association with audit quality compared to

inspections undertaken by a professional body under the supervision of the POB. We argue

that inspection directly undertaken by the POBs will result in a stricter and more rigorous type

of inspection system. The rationale for this analysis is consistent with the reasons why there

has been a move in the last decade from self-regulation by the audit profession to oversight by

independent POBs. In our third additional analysis we consider the frequency of inspections

conducted. We expect that more frequent inspections are associated with higher audit quality.

The reasoning behind this is that the incentives of audit firms to be lenient towards their client

companies may decrease as a function of the likelihood of being caught for malpractice,

which may increase with the frequency of inspections.

The results of these analyses relating to features of inspection regimes and audit

quality are as follows. None of the features that we consider (number of years of inspection

experience, type of oversight system, and frequency of inspections) are significantly

associated with the absolute value of abnormal total accruals. Similarly, none of these features

significantly affects income-increasing abnormal total accruals. We also do not find any

support for a significant association between features of inspection regimes and audit quality

using abnormal working capital accruals, except that direct inspections significantly increase

income-decreasing abnormal working capital accruals (p<0.10).

25

V. CONCLUSION

One of the most profound changes in audit regulation of the past decade has been the

move to independent public oversight of the auditing profession, putting an end to the

traditional model of self-regulation. As the potential merits of public oversight are contested

by some, research on its effectiveness is warranted. Currently, the emerging literature on

public oversight has mainly focused on the U.S., since it is one of the few countries where the

public oversight body publicly discloses inspection findings. The issue is much broader than

the U.S., and the move to independent public oversight bodies has been a world-wide trend,

emphasized by the formation of IFIAR in September 2006, growing to a membership of 44

countries in early 2013. However, apart from a couple of studies relating to individual

countries other than the U.S., to the best of our knowledge, there is no international study on

the effectiveness of independent public oversight which we examine here. In our examination

of the effectiveness of public oversight in its different forms at an international level, we

make use of a large sample of non-financial companies located in 33 countries over the period

2006-2010. We observe that the level of abnormal accruals is significantly lower for

companies domiciled in countries where independent inspections of audit firms are conducted

and in IFIAR member countries. This suggests that audit quality is stronger in countries

where a national independent inspection regime is in place as well as in IFIAR member

countries, where the POB is bound by a number of requirements that are expected to lead to

an improved audit environment.

We further concentrate our analysis on the key plank of the strategy and work effort of

the independent oversight bodies, which is the inspection of audit firms. We find that the level

of abnormal accruals is significantly lower in the period after the introduction of inspections

compared to the pre-inspection regime. This provides evidence that audit quality improves

26

after installing public oversight and conducting inspections. We also consider the various

characteristics of the inspection regimes to identify whether variation in the performance

characteristics of these inspections is associated with audit quality. We do not find much

difference in audit quality that could be explained by different features of the public oversight

system.

Collectively, our results contribute to the emerging literature and debate on public

oversight by providing insights from an international setting. Our findings may prove useful

for regulators in the further development, design and mutual recognition of public oversight

systems. They do suggest that one of the major impacts on audit quality is having an

inspection program, and that the specific characteristics of the inspection programs are less

important.

One of the potential limitations of our study is endogeneity concerns, especially with

regards to the analysis of impact of countries with inspections and IFIAR membership. Our

pre-/post-analysis, where we find that the level of abnormal accruals is significantly lower in

the post-inspection regime compared to the pre-inspection regime, and that this finding does

not hold for audits not subject to inspection regimes over a similar period, helps to alleviate

this concern. However, we cannot categorically attribute the observed improvement in audit

quality directly to the performance of inspections. Although this is the major initiative of the

independent oversight boards aimed at audit quality, it may be that other common factors

associated with the countries that have created independent oversight boards that have

instigated active inspection regimes have also contributed. Alternatively, it may be not that

inspections themselves are improving audit quality but that the expectation of having audit

work subjected to external scrutiny and public disclosure may improve audit practices and

impact audit quality6. A further limitation is that we are restricted to one measure of audit

6 The Consultative Committee of Accountancy Bodies in the United Kingdom conducted a series of interviews

with stakeholders regarding perceptions of the impact of inspections and transparency reports in 2011: “Some

27

quality, discretionary accruals. Other commonly used measures of audit quality are limited to

certain companies (such as the appropriate use of going concern opinions, which are specific

to loss-making companies) or are not available, or comparable, for an international study

(such as financial statement restatements which are a common feature in the U.S. but for

which information is not applicable or available for other countries).

Our study is a first attempt at addressing public oversight of the auditing profession in

an international setting. Future research could attempt to disentangle the impact of inspections

themselves improving audit quality versus the perception that a firm will be inspected that

will impact audit processes and hence audit quality. Further insights could also be gained by

separately analysing the impact of inspection programs on global audit firm networks and

other audit firms. Future research may also look into the effectiveness of public oversight in

an international setting by using other indicators of audit quality, by further exploiting the

different features on the organization and characteristics of public oversight as data become

available, and by further extending the period of study.

investor representatives and regulators saw the potential for the reports to improve audit quality. Most

interviewees, however, did not believe that the governance and transparency reports would improve audit quality

to any significant extent. ... There was a view that the fact that the firm was going to be reviewed was as much a

driver of improvement as the review itself” (emphasis added).

28

REFERENCES

Abbott, L. J., K. Gunny, and T. C. Zhang. 2013. When the PCAOB talks, who listens?

Evidence from client firm reactions to adverse, GAAP-deficient PCAOB inspection

reports. Auditing: A Journal of Practice & Theory 32 (2): 1-31.

Australian Securities and Investments Commission (ASIC). 2012. 12-301MR ASIC's audit

inspection findings for 2011-12. Available at:

http://www.asic.gov.au/asic/asic.nsf/byheadline/12-

301MR+ASICs+audit+inspection+findings+for+2011-12?openDocument.

Carcello, J. V., C. Hollingsworth, and S. Mastrolia. 2011. The effect of PCAOB inspections

on Big 4 audit quality. Research in Accounting Regulation 23 (2): 85-96.

Carey, P., and R. Simnett. 2006. Audit partner tenure and audit quality. The Accounting

Review 81: 653-676.

Choi, J.-H., and T. J. Wong. 2007. Auditors' governance functions and legal environments:

An international investigation. Contemporary Accounting Research 24: 13–46.

Consultative Committee of Accountancy Bodies. 2011. Audit Quality and Transparency, a

Study of the Usage and Impact of Public Reports on Audit Governance: Are they

Providing Appropriate Reassurance on Audit Quality? CCAB Limited: London.

Daugherty, B. and W. Tervo. 2010. PCAOB inspections of smaller CPA firms: The

perspective of inspected firms. Accounting Horizons 24 (2): 189-219.

Daugherty, B., D. Dickins, and W. A. Tervo. 2011. Negative PCAOB inspections of

triennially inspected auditors and involuntary and voluntary client losses. International

Journal of Auditing 15 (3): 231-246.

Dechow, P., R. Sloan, and A. Sweeney. 1995. Detecting earnings management. The

Accounting Review 70: 193-225.

Dechow, P., S. P. Kothari, and R. Watts. 1998. The relation between earnings and cash flows.

Journal of Accounting and Economics 25 (2): 133-168.

Dee, C. C., A. Lulseged, and T. Zhang. 2011. Client stock market reaction to PCAOB

sanctions against a Big Four auditor. Contemporary Accounting Research 28 (1): 263-

291.

DeFond, M. L. 2010. How should the auditors be audited? Comparing the PCAOB

Inspections with the AICPA Peer Reviews. Journal of Accounting and Economics 49

(1-2): 104-108.

DeFond, M. L. and J. Jiambalvo. 1994. Debt covenant violation and manipulation of accruals.

Journal of Accounting and Economics 17(1-2): 145-176.

DeFond, M. L., and C. S. Lennox. 2011. The effect of SOX on small auditor exits and audit

quality. Journal of Accounting and Economics 52: 21-40.

DeFond, M. L. and C. Park. 2001. The reversal of abnormal accruals and the market valuation

of earnings surprises. The Accounting Review 76 (3): 375-404.

European Commission (EC). 2010. Green Paper. Audit Quality: Lessons from the Crisis.

Available at: http://eur-

lex.europa.eu/LexUriServ/LexUriServ.do?uri=COM:2010:0561:FIN:EN:PDF.

29

Financial Reporting Council (FRC). 2012. Audit Quality Inspections: Annual Report 2011-

2012. Available at:

https://www.ifiar.org/IFIAR/media/Documents/General/Members%20Inspection%20Re

ports/Audit-Quality-Inspections-Annual-Report-2011-12.pdf.

Francis, J. R., and D. Wang. 2008. The joint effect of investor protection and Big 4 audits on

earnings quality around the world. Contemporary Accounting Research 25 (1): 157-191.

Francis, J. R., P. Michas, and S. Seavey. 2013. Does audit market concentration harm the

quality of audited earnings? Evidence from audit markets in 42 countries.

Contemporary Accounting Research 30 (1): 325-355.

Franzel, J. M. 2012. Keynote address: Driving change to achieve independent and high

quality audits. Speech delivered at Baruch College Financial Reporting Conference,

May 3. Available at: http://pcaobus.org/News/Speech/Pages/05032012_Baruch.aspx.

Fuentes, C. D., M. Illueca, and M. C. Pucheta-Martinez. 2010. Disciplinary sanctions and

audit quality: Empirical evidence from an external oversight system. Working paper,

available at SSRN.

Glover, S. M., D. F. Prawitt, and M. H. Taylor. 2009. Audit standard setting and inspection

for US public companies: A critical assessment and recommendations for fundamental

change. Accounting Horizons 23: 221-237.

Goelzer D. L. 2009. Seven years of The Public Company Accounting Oversight Board –

What has been accomplished and what remains to be done? Speech delivered at AICPA

Conference, Washington, December 7. Available at:

http://pcaobus.org/News/Speech/Pages/12072009_Goelzer_AICPA_Speech.aspx.

Gunny, K. and T. C. Zhang. 2013. PCAOB inspection reports and audit quality. Journal of

Accounting and Public Policy (forthcoming).

Hermanson, D. R., R. W. Houston, and J. C. Rice. 2007. PCAOB inspections of smaller CPA

firms: Initial evidence from inspection reports. Accounting Horizons 21: 137-152.

Hermanson, D. R., and R. W. Houston. 2008. Quality control defects revealed in smaller

firms’ PCAOB inspection reports. The CPA Journal 78 (12): 36-39.

International Forum of Independent Audit Regulators (IFIAR). 2012. Summary Report of

Inspection Findings 18 December 2012. Available at

https://www.ifiar.org/IFIAR/media/Documents/General/IFIAR-2012-Summary-Report-

of-Members-Inspection-Findings-18-Dec-12-(2).pdf.

International Forum of Independent Audit Regulators (IFIAR). 2013. International Forum of

Independent Audit Regulators (IFIAR) – About Us. Available at:

https://www.ifiar.org/About-Us.aspx.

Jones, J. J. 1991. Earnings management during import relief investigations. Journal of

Accounting Research 29: 193-228.

Kaufmann, D., A. Kraay, and M. Mastruzzi. 2010. The Worldwide Governance Indicators:

Methodology and Analytical Issues. World Bank Policy Research Working Paper No.

5430.

30

Knechel, W. R., M. Offermanns, and A. Vanstraelen. 2012. PCAOB inspections and audit

firm behavior: An analysis of audit fees, audit effort and industry specialization.

Working paper, Maastricht University.

Kothari, S. P., A. J. Leone, and C. E. Wesley. 2005. Performance matched discretionary

accrual measures. Journal of Accounting and Economics 39: 163-197.

Kwon, S. Y., C. Y. Lim, and P. M.-S. Tan. 2007. Legal systems and earnings quality: The

role of auditor industry specialization. Auditing: A Journal of Practice and Theory 26

(2): 25-55.

Lennox, C., and J. Pittman. 2010. Auditing the auditors: Evidence on the recent reforms to the

external monitoring of audit firms. Journal of Accounting and Economics 49 (1-2): 84-

103.

Roybark, H. M. 2009. An analysis of audit deficiencies based on Section 104 inspection

reports issued by the PCAOB during 2004-2007. Journal of Accounting, Ethics and

Public Policy 10(1): 1-81.

Simnett, R., and A. Smith. 2005. Public oversight: An international approach to auditing. In

Ethics and Auditing, edited by T. Campbell and K. Houghton, 45-62. Canberra: ANU

E-Press.

Teoh, S., T. Wong and G. Rao. 1998. Are accruals during initial public offerings

opportunistic? Review of Accounting Studies 3 (1-2): 175-208.

Van Opijnen, M., K. Van de Poel, and A. Vanstraelen. 2011. Public oversight and audit

quality: Evidence from public oversight of audit firms in the Netherlands. Working

paper, available at SSRN.

31

TABLE 1

Observations per Country and Details of Inspection Regimes

Country Number of

Observations

Year of

joining

IFIAR

% of Total

Observations

Year

inspections

commence

Oversight

system

Frequency of

inspections

Australia 912 2006 2.32% 2005 Direct

inspection

Large audit

firms and

significant

smaller firms:

regular

inspections

(approximately

annually)

Belgium 272 2012 0.69% 2007 Through

oversight

3 years for PIE

audit firms, 6

years for non-

PIE audit firms

Brazil 425 2006 1.08% 1978 Combination7

Prior to 2011

on demand

Canada 942 2006 2.40% 2004 Primarily

direct

inspection8

Large audit

firms: annually,

others – 2-3

years

Chile 343 Not a

member

0.87% N.A. N.A. N.A.

China 926 Not a

member

2.36% N.A. N.A. N.A.

Denmark 339 2006 0.86% 2008 Direct

inspection

3 years for PIE

audit firms, 6

years for non-

PIE audit firms

Finland 402 2007 1.02% 2007 Direct

inspection

3 years for PIE

audit firms

France 1,560 2006 3.97% 2003 Primarily

direct

inspection9

3 years for PIE

audit firms, 6

years for non-

PIE audit firms

Germany 1,101 2006 2.80% 2007 Through

oversight

Large audit

firms: annually,

others every 3

years

Greece 369 2010 0.94% 2009 Direct

inspection

3 years for PIE

audit firms

Hong Kong 1,181 Not a

member

3.01% N.A. N.A. N.A.

India 482 Not a

member

1.23% N.A. N.A. N.A.

Indonesia 490 Not a

member

1.25% N.A. N.A. N.A.

7 In 1999, a peer review system with recurring inspections undertaken by the Brazilian professional organization

was implemented. The Brazilian Securities Commission (CVM) retains the ultimate responsibility for this

system and exercises full oversight, remaining empowered to carry out its own direct inspections at any time. 8 The Canadian Public Accountability Board (CPAB) performs most of its own inspections however has entered

into memoranda of understanding with the provincial regulators of public accountants who perform inspections

of some of the smaller audit firms. CPAB’s Director of Interprovincial Affairs reviews the provincial inspection

reports and will supplement a provincial inspection if necessary. 9 A part of the PIE inspections can be delegated to the Compagnie nationale des commissaires aux comptes

(CNCC) under the supervision of the Haut Conseil du Commissariat aux Comptes (H3C). Inspections of

statutory auditors and audit firms of non-PIEs are carried out by the CNCC and Compagnie Régionale des

Commissaires aux Comptes de Paris (CRCC) under the supervision of the H3C.

32

Israel 573 Not a

member

1.46% N.A. N.A. N.A.

Italy 758 2006 1.93% 2007 Direct

inspection

3 years for PIE

audit firms

Japan 7,987 2006 20.33% 2004 Through

oversight

Large audit

firms: every

two years

Malaysia 1,918 2010 4.88% 2010 Direct

inspection

From time to

time (on a risk

basis within a

predetermined

cycle)

Netherlands 311 2006 0.79% 2006 Direct

inspection

3 years for PIE

audit, 6 years

for non-PIE

audit firms

Norway 329 2006 0.84% 1992 Direct

inspection

3 years for PIE

audit firms, 6

years for non-

PIE audit firms

Poland 402 2011 1.02% 2009 Through

oversight

3 years for PIE

audit firms, 6

years for non-

PIE audit firms

Russia 242 Not a

member

0.62% N.A. N.A. N.A.

Singapore 1,266 2006 3.22% 2005 Direct

inspection

Big 4 firms:

every 2 years;

other PIE audit

firms: 3 to 4

years, non-PIE

audit firms: 4

to 5 years

South Africa 604 2006 1.54% 2006 Direct

inspection

3 years

South Korea 2,147 2007 5.47% 2010 Combination10

Large audit

firms: every

two years;

others: 3 to 5

years

Spain 384 2006 0.98% 1990 Primarily

direct

inspection11

3 years for PIE

audit firms, 6

years for non-

PIE audit firms

10

The Financial Supervisory Service (FSS) directly inspects audit firms auditing more than 1% of listed

companies; who audit listed companies with assets greater than KRW1 trillion (approximately US$1 billion);

with more than 30 CPAs; or a firm deemed subject to inspection because of audit oversight by foreign

regulators. The Big 4 are inspected every two years and the other firms every three to five years. The Korean

Institute of Certified Public Accountants (KICPA) inspects the remaining smaller audit firms and reports the

inspection results to the Securities and Futures Commission (SFC). 11

Inspections of PIEs are performed directly by the Accounting and Auditing Institute of Spain (ICAC) and

those related to non-PIEs are carried out by the professional bodies under the direction and supervision of ICAC.

33

Sri Lanka 220 2007 0.56% 2000 Direct

inspection

Annual sample

of all audits

Sweden 601 2006 1.53% 1995 Direct

inspection12

3 years for PIE

audit firms, 6

years for non-

PIE audit firms

Switzerland 509 2007 1.30% 2005 Direct

inspection

PWC, KPMG,

EY: annual

basis; others: 3

years

Taiwan 2,413 2009 6.14% 2009 Direct

inspection

Large audit

firms: every 3

years; others: 6

years

Thailand 597 2010 1.52% 2010 Direct

inspection

Big 4: every

year; others:

every 3 years

United

Kingdom

1,982 2006 5.05% 2004 Primarily

direct

inspection13

Big 4: annual;

other major

firms: 2 years

United

States

6,291 2007 16.02% 2003 Direct

inspection

Large audit

firms: annual;

others: 3 years

Total 39,278 100%

12

For non-PIE audit firms, an oversight role is played by members as inspections are carried out by the

professional institute. 13

The oversight is mostly direct and the U.K. does state “Direct Inspection” in their member form to IFIAR.

Consider the following statement: “There are an estimated further 40 firms with less than 10 public interest

audits, where the Audit Inspection Unit (AIU) of the Financial Reporting Council (FRC) reviews the audit work

of their public interest audits and delegates the independent inspection of the firm to the Monitoring Bodies of

either the Institute of Chartered Accountants in England and Wales (ICAEW) or Institute of Chartered

Accountants in Scotland (ICAS) to undertake the primary review of the firm.”

34

TABLE 2

Panel A: Descriptive statistics for dependent and control variables for the total sample in the

period 2006-2010 (n=39,278)

Variables Median Mean

ATA 0.037 0.060

AWCA 0.048 0.082

Size 12.830 13.025

Leverage 0.127 0.167

Perform 0.075 0.096

Growth 0.035 0.136

MB 1.2 1.4

PPE_growth 0.022 0.158

Loss 0 0.254

Auditor 1 0.803

Rule of law 1.352 1.175

Panel B: Descriptive statistics for industry composition for the total sample in the period 2006-

2010 (n=39,278)

SIC Industry No. of observations % of Total observations

SIC_01_09 353 0.89%

SIC_10_19 3,099 7.89%

SIC_20-39 21,194 53.96%

SIC_40_49 4,867 12.39%

SIC_50_59 4,624 11.77%

SIC_70-79 3,701 9.42%

SIC_80_99 1,606 4.08%

Panel C: Descriptive statistics for variables of interest

Variables No. of observations Median Mean

Inspection 39,278 1 0.723

IFIAR 31,833 1 0.787

Post_inspect 10,718 0 0.418

First_time 28,415 0 0.082

Ln_exp 28,415 0.698 0.890

Type_oversight 28,415 2 1.251

Freq_inspect 28,195 0 0.412

Variable definitions:

ATA: Absolute value of abnormal total accruals (performance-adjusted modified Jones model)

AWCA: Absolute value of abnormal working capital accruals (DeFond and Park 2001)

Size: Natural logarithm of total assets (in thousands of USD)

Leverage: Ratio of long-term debt to total assets

Perform: Absolute value of operating cash flow scaled by total assets

Growth: Percentage change in sales

MB: Market to book value

PPE_growth: Percentage change in gross property plant and equipment

Loss: Indicator variable taking the value of 1 when a company has a negative income, else 0

Auditor: Indicator variable taking the value of 1 when a company is audited by a Big 4 audit firm, else 0

Rule of law: Rule of law governance indicator (Kaufmann et al. 2010)

Inspection: Indicator variable taking the value of 1 when a company is domiciled in a country where audit firms are

subject to periodic inspections, else 0.

IFIAR: Indicator variable taking the value of 1 when a company is domiciled in an IFIAR member country, else 0

Post_Inspect: Indicator variable taking the value of 1 when the observation relates to the post-inspection period

First_time: Indicator variable taking the value of 1 when it is the first year that inspections are performed

Ln_exp: Natural logarithm of the number of years of inspection experience

Type_oversight: Type of oversight system taking the value of 2 in case of direct or primarily direct oversight, 0 in case of

oversight through the profession under supervision of the oversight board, and 1 in case of a combination.

Freq_inspect: Indicator variable taking the value of 1 when the large audit firms are inspected annually, else 0.

35

TABLE 3

Inspections and Audit Quality

Column A Column B Column C

Variables Absolute value of

abnormal total accruals

Income-increasing

abnormal total

accruals in

absolute value

Income-decreasing

abnormal total

accruals in

absolute value

Coefficient

(t-value)

Coefficient

(t-value)

Coefficient

(t-value)

Intercept 0.159

(30.75) ***

0.173

(19.91) ***

0.125

(19.68) ***

Inspection -0.007

(4.36) ***

-0.004

(1.71) *

-0.008

(4.63) ***

Size -0.006

(16.33) ***

-0.007

(12.05) ***

-0.004

(9.55) ***

Leverage 0.001

(0.24)

0.009

(1.18)

-0.025

(2.53) **

Perform 0.005

(1.02)

0.002

(0.92)

0.124

(5.75) ***

Growth 0.0002

(0.78)

0.018

(3.98) ***

0.000

(0.29)

MB 0.002

(0.49)

-0.004

(1.75) *

0.018

(0.63)

PPE_GROWTH 0.002

(2.80) ***

0.004

(1.37)

0.002

(4.59) ***

Loss 0.009

(6.13) ***

0.004

(1.61)

0.021

(10.43) ***

Auditor -0.004

(2.44) **

-0.006

(2.23) **

-0.003

(1.49)

Rule of Law -0.006

(5.56) ***

-0.005

(2.57) ***

-0.007

(5.84) ***

Year and Industry Fixed

Effects

Yes Yes Yes

r2 5.64% 7.80% 10.28%

n 39,278 19,293 19,985

*,**,*** Indicate statistical significance at the 0.10, 0.05, and 0.01 levels, respectively. All p-values are based on two-tailed

tests and are calculated based on robust standard errors. We use weighted regressions for equal weighting of observations by

country.

Variables are as defined in Table 2.

36

TABLE 4

Audit Quality Pre- and Post-Inspection

Column A Column B Column C

Variables Absolute value of

abnormal total accruals

Income-increasing

abnormal total

accruals in

absolute value

Income-decreasing

abnormal total

accruals in

absolute value

Coefficient

(t-value)

Coefficient

(t-value)

Coefficient

(t-value)

Intercept 0.130

(15.27) ***

0.143

(9.96) ***

0.082

(7.86) ***

Post_Inspect -0.010

(3.73) ***

-0.007

(1.73) *

-0.013

(3.71) ***

Size -0.005

(9.14) ***

-0.006

(6.13) ***

-0.003

(5.75) ***

Leverage -0.021

(2.81) ***

-0.009

(0.79)

-0.018

(2.12) **

Perform 0.0009

(0.80)

0.000

(0.35)

0.178

(5.13) ***

Growth 0.000

(0.29)

0.010

(1.88) *

0.000

(0.06)

MB 0.113

(1.42)

-0.063

(0.80)

-0.287

(3.01) ***

PPE_Growth 0.001

(5.14) ***

0.014

(2.46) **

0.001

(10.20) ***

Loss 0.008

(3.45) ***

-0.002

(0.44)

0.025

(7.83) ***

Auditor -0.001

(0.40)

0.002

(0.53)

-0.004

(1.16)

Rule of Law -0.000

(0.01)

-0.001

(0.45)

-0.000

(0.17)

Year and Industry Fixed

Effects

Yes Yes Yes

r2 4.76% 6.63% 13.98%

n 10,718 5,052 5,666

*,**

,***

Indicate statistical significance at the 0.10, 0.05, and 0.01 levels, respectively. All p-values are based on

two-tailed tests and are calculated based on robust standard errors. We use weighted regressions for equal

weighting of observations by country.

Variables are as defined in Table 2.

37

TABLE 5

IFIAR membership and Audit Quality

Column A Column B Column C

Variables Absolute value of

abnormal total accruals

Income-increasing

abnormal total

accruals in

absolute value

Income-decreasing

abnormal total

accruals in

absolute value

Coefficient

(t-value)

Coefficient

(t-value)

Coefficient

(t-value)

Intercept 0.134

(24.51)***

0.142

(15.46)***

0.119

(18.18) ***

IFIAR -0.006

(3.61) ***

-0.003

(1.07)

-0.009

(4.61) ***

Size -0.005

(13.04) ***

-0.005

(9.59) ***

-0.004

(8.54) ***

Leverage -0.021

(3.13) ***

-0.016

(1.46)

-0.028

(3.25) ***

Perform 0.101

(8.56) ***

0.104

(5.77)***

0.105

(5.66) ***

Growth 0.014

(4.06) ***

0.018

(3.21) ***

0.006

(2.16) **

MB -0.003

(1.60)

-0.005

(1.96) **

0.010

(0.40)

PPE_GROWTH 0.002

(3.13) ***

0.004

(1.35)

0.002

(5.39) ***

Loss 0.012

(7.68) ***

0.003

(1.11)

0.020

(10.05) ***

Auditor -0.005

(2.77) ***

-0.005

(1.75)*

-0.004

(2.05) **

Rule of Law -0.006

(5.52) ***

-0.006

(3.37) ***

-0.005

(4.54) ***

Year and Industry Fixed

Effects

Yes Yes Yes

r2 8.80% 9.97% 9.90%

n 31,833 15,618 16,215

*,**

,***

Indicate statistical significance at the 0.10, 0.05, and 0.01 levels, respectively. All p-values are based on

two-tailed tests and are calculated based on robust standard errors. We use weighted regressions for equal

weighting of observations by country.

Variables are as defined in Table 2.