D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 1

Developing a New Common User Deep Water Port

for SA’s Bulk Mineral Exports

Stewart Lammin

General Manager Flinders Ports

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 2

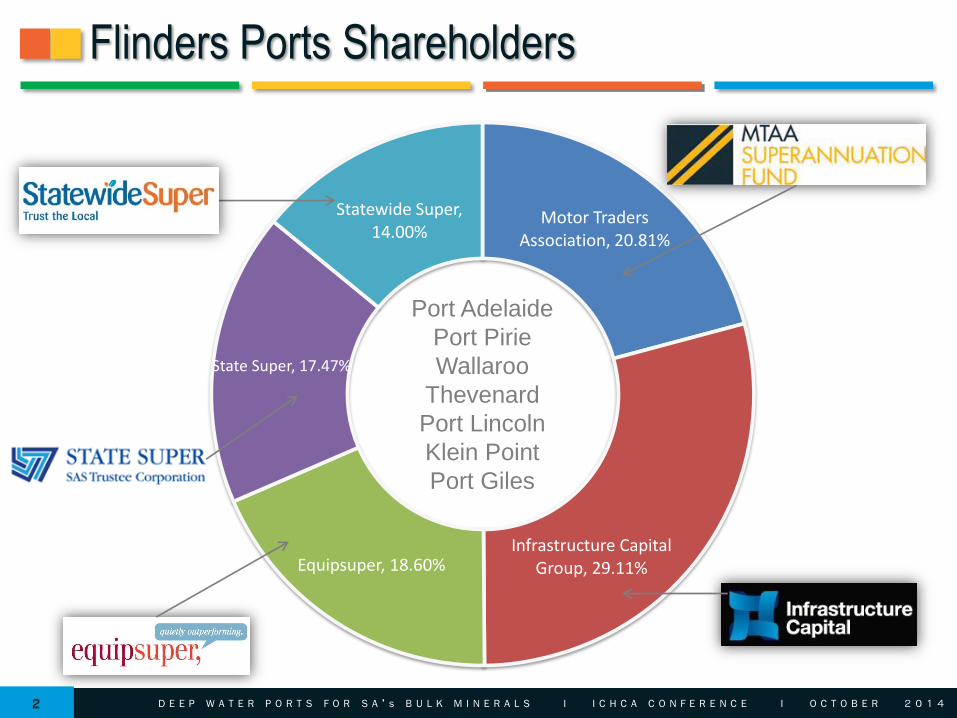

Motor Traders Association, 20.81%

Infrastructure Capital Group, 29.11% Equipsuper, 18.60%

State Super, 17.47%

Statewide Super, 14.00%

Flinders Ports Shareholders

Port Adelaide

Port Pirie

Wallaroo

Thevenard

Port Lincoln

Klein Point

Port Giles

2

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 3

Flinders Holdings Organisational Chart

Flinders Holdings

Flinders Ports Flinders Logistics Flinders ACT

Structure

1

Core Business

2 Owning, managing & operating port related infrastructure and

providing services that facilitate the movement of cargo through

the port logistics chain. “

“

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 4

South Australian Ports

Thevenard

Port Adelaide Port Giles

Klein Point

Ardrossan

Wallaroo

Port Pirie Whyalla

Port Bonython

Port Lincoln

Flinders Ports

Indentured / Old Ports

New Port Proposals

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 5

Flinders Ports Options

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 6

Iron Ore Port Options

Proposed Ports

Operational Ports

Cape Hardy Iron Road - Bulk

Port Spencer Centrex - Bulk

Lucky Bay IronClad - Barge

Port Bonython Flinders Ports - Bulk

Port Lincoln Flinders Ports - Bulk

Whyalla Arrium - Barge Port Pirie

Flinders Ports - Barge

Port Adelaide Flinders Ports -

Containers

Myponie Point Braemar - Bulk

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 7

The State’s Mining Growth

The Opport-

unity

The Challenge

Transporting cargo to

a suitable port and

onto a ship.

• Iron Ore – Low value, large parcels,

prefer deep water.

• Mineral sands, copper concentrates,

zinc – high value, smaller parcels – don’t

require deep water.

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 8

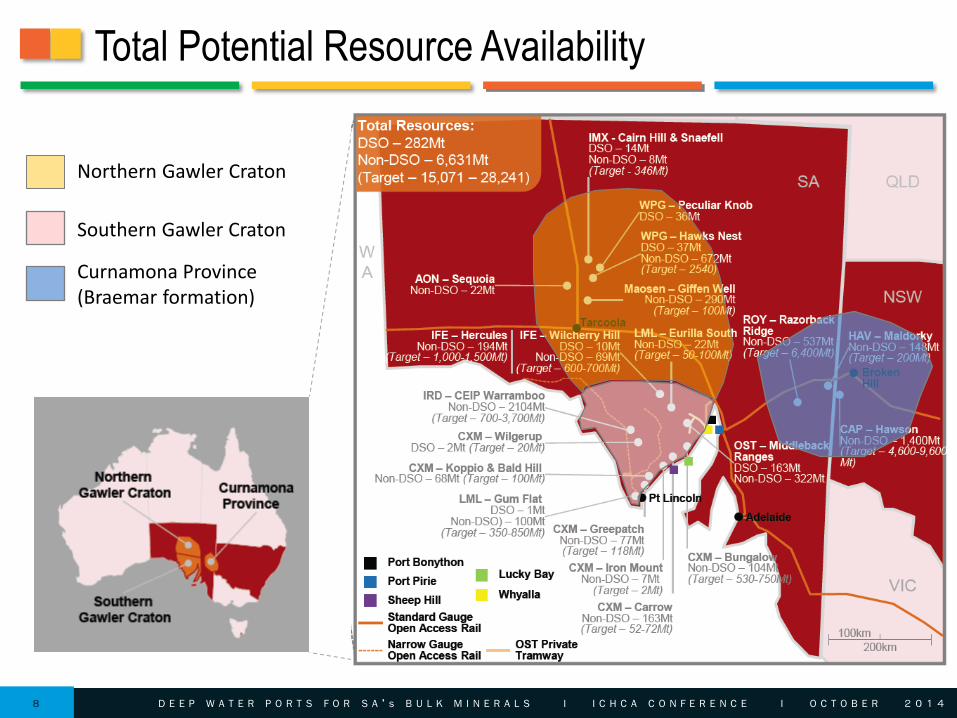

Total Potential Resource Availability

Curnamona Province (Braemar formation)

Southern Gawler Craton

Northern Gawler Craton

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 9

Proposed Iron Ore Production

South Australian Forecast Iron Ore Productions (Mtpa)

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 10

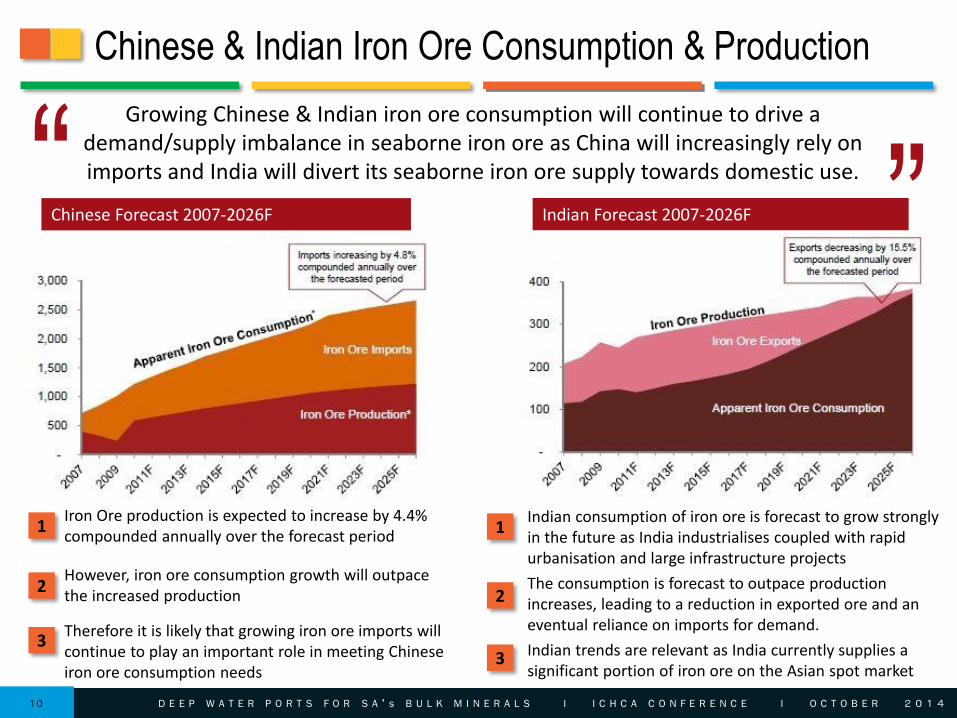

Chinese & Indian Iron Ore Consumption & Production

Growing Chinese & Indian iron ore consumption will continue to drive a demand/supply imbalance in seaborne iron ore as China will increasingly rely on imports and India will divert its seaborne iron ore supply towards domestic use. “

“

Chinese Forecast 2007-2026F Indian Forecast 2007-2026F

1 Iron Ore production is expected to increase by 4.4% compounded annually over the forecast period

1 Indian consumption of iron ore is forecast to grow strongly in the future as India industrialises coupled with rapid urbanisation and large infrastructure projects

2 However, iron ore consumption growth will outpace the increased production

3 Therefore it is likely that growing iron ore imports will continue to play an important role in meeting Chinese iron ore consumption needs

2 The consumption is forecast to outpace production increases, leading to a reduction in exported ore and an eventual reliance on imports for demand.

3 Indian trends are relevant as India currently supplies a significant portion of iron ore on the Asian spot market

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 11

Flinders Ports Strategy – Staged Approach

Almost all iron ore resources in and around South Australia are

likely to be competitive against seaborne iron ore on a landed

cash cost basis into China

Cost Curve

Long Term

Viability

All other necessary economic conditions for the long term

viability of the port appear favourable

Interim

Solutions

Interim port solutions are likely to be necessary Port Adelaide and Port Pirie are likely to be the optimal locations due to:

a) adequate rail/land/port capacity and

b) cost effective CAPEX

Bank-

ability

Bankability Port is currently unlikely due to a) default risk and

b) shipment dates of users

c) Market Conditions

Demand Study Conclusions

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 12

Port Adelaide Outer Harbor

Current channel depth (14.2metres)

Swinging Basin (14.2 metres)

Additional dredging (9.3m current)

or 646,000m3 of spoils to be removed

6

9

8

7

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 13

Port Adelaide Outer Harbor – Berth 7

Concept

• Utilise existing supply chain

• Loading Panamax vessels

• Capacity 2,000,000 mtpa Operation

• Existing rail

• Straddles or ITV’s from stockpile

• Tipplers

• Portainer cranes

IMX iron ores

stockpile

Advantage

• Utilise existing assets

• Minimal CAPEX

• Approvals in place

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 14

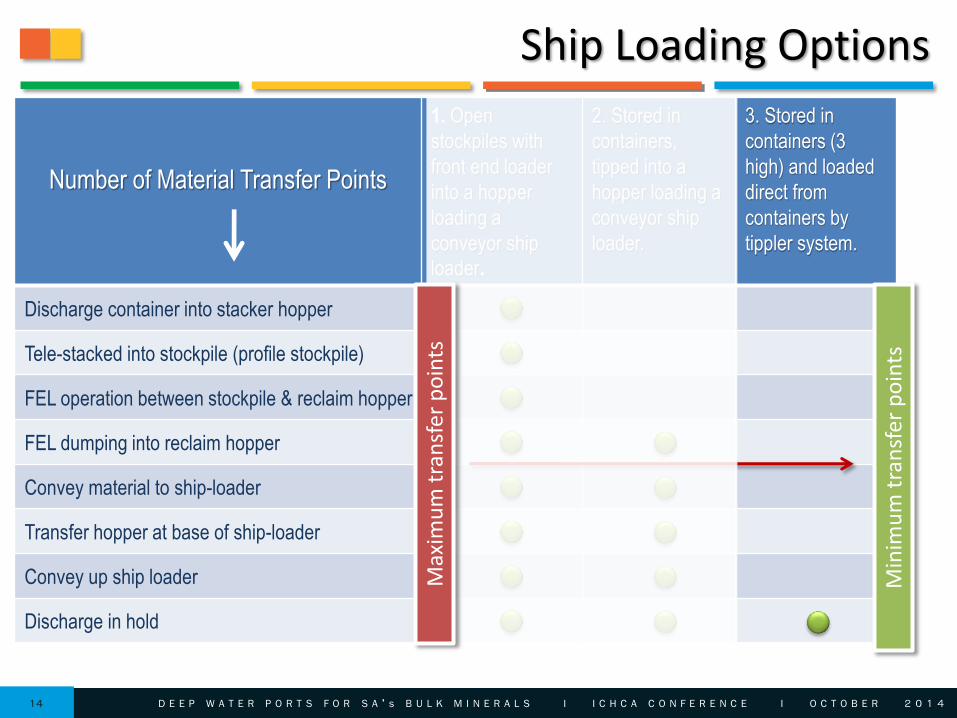

Ship Loading Options

Number of Material Transfer Points

1. Open

stockpiles with

front end loader

into a hopper

loading a

conveyor ship

loader.

2. Stored in

containers,

tipped into a

hopper loading a

conveyor ship

loader.

3. Stored in

containers (3

high) and loaded

direct from

containers by

tippler system.

Discharge container into stacker hopper

Tele-stacked into stockpile (profile stockpile)

FEL operation between stockpile & reclaim hopper

FEL dumping into reclaim hopper

Convey material to ship-loader

Transfer hopper at base of ship-loader

Convey up ship loader

Discharge in hold

Max

imu

m t

ran

sfer

po

ints

Min

imu

m t

ran

sfer

po

ints

FEL = Front End Loader

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 15

Port Pirie

Concept • Brownfield Development

• Transhipment to Capesize vessels

Users • Northern Gawler Craton

• Curnamona

Supply Chain

• Existing rail corridor & assets

• Enclosed sheds

• Conveyed to shiploader

Capacity • 10,000,000mtpa + (1 berth)

• Studies to identify port capacity

Port

• Utilise existing wharf assets

• Option of Berth/s 2/5 or 7

• Ability to pre-load barges

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 16

Port Pirie – Ore Loading Facility

Advantages

Next Steps

Utilising existing rail & port assets

Utilising existing rail and port capacity

Scalable

Shorter timeframe for operational facility

Lower CAPEX alternative

Environmentally responsible

Pre-Feasibility underway • Preferred option/s – community and environment

• High level CAPEX

User Agreements – Carpentaria Exploration

Community & Council support

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 17

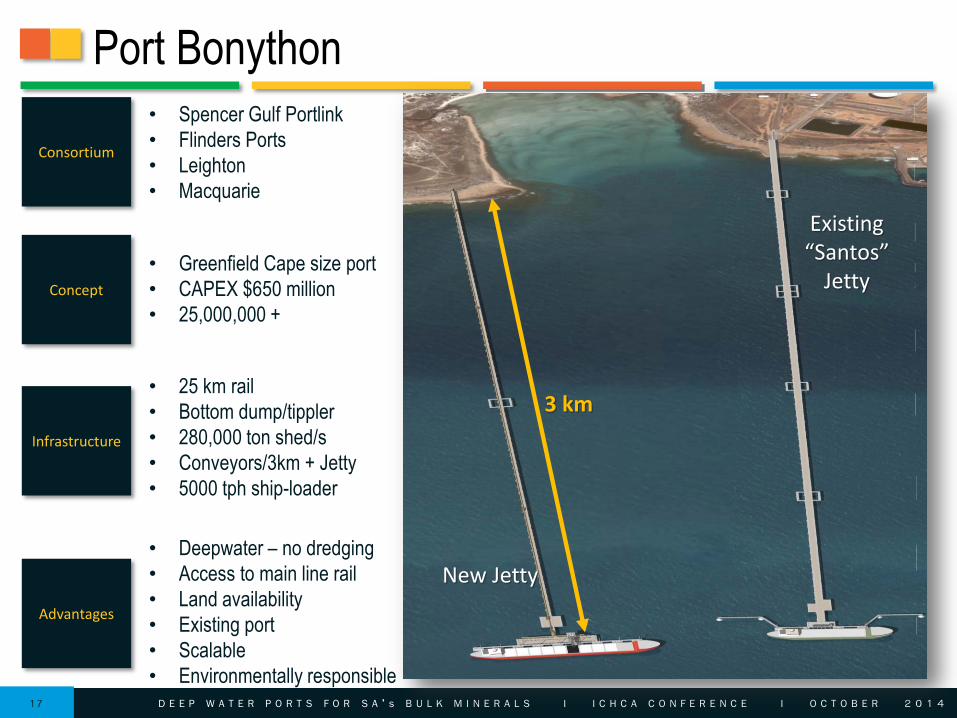

Port Bonython

Advantages

• Deepwater – no dredging

• Access to main line rail

• Land availability

• Existing port

• Scalable

• Environmentally responsible

Existing “Santos”

Jetty

New Jetty

3 km • 25 km rail

• Bottom dump/tippler

• 280,000 ton shed/s

• Conveyors/3km + Jetty

• 5000 tph ship-loader

Infrastructure

• Greenfield Cape size port

• CAPEX $650 million

• 25,000,000 +

Concept

• Spencer Gulf Portlink

• Flinders Ports

• Leighton

• Macquarie

Consortium

D E E P W A T E R P O R T S F O R S A ’ s B U L K M I N E R A L S I I C H C A C O N F E R E N C E I O C T O B E R 2 0 1 4 18

MAY 08: State Government releases EOI

JUN 08 SGPL submit bid

OCT 08 SGPL selected as preferred bidder to move to Phase II – feasibility stage of EOI

MAR 09 Feasibility Report submitted to SA Gov.

NOV 09 Official response received from State Government.

MAY 11 Exclusivity granted to Flinders Ports until 31-Mar-14 via SGPL

AUG 11 ARUP confirmed as SGPL

Environmental Impact Statement Consultants

JUN 11 SGPL submitted its Section 46 Major Project application

FEB 12 SA Gov. confirms approval for project to be developed under Section 46 Status.

EIS - submitted awaiting approval with conditions ILUA/Native Title – Process commenced, to be finalised Engineering – Additional geo-technical Ongoing discussions with Government & industry Binding Agreements Financial close Construction – 36 months.

MAR 10 User Agreements & Government extensions

Next Steps

2008 2009 2010 2011 2012 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2013

SEP 13 EIS submitted – awaiting final approval from State Government

Q1 Q2 Q3 Q4

Port Bonython – Project Timeline to Date