Download - Home Ownership Cost

Cost to Own

Guide to the real cost of

owning your home

HOME OWNERSHIP COST

Cost to Own

[email protected] 949.769.1599

The OC Housing News ownership cost calculations for family homes ................................................................. 3 A point-‐in-‐time analysis ........................................................................................................................................................................ 3 Asking Price ................................................................................................................................................................................................ 3 Down Payment .......................................................................................................................................................................................... 3 Mortgage Interest Rate .......................................................................................................................................................................... 4 Number of Years ....................................................................................................................................................................................... 4 Mortgage ...................................................................................................................................................................................................... 4 Income Requirement .............................................................................................................................................................................. 5 Monthly Mortgage Payment ................................................................................................................................................................ 5 Property Tax ............................................................................................................................................................................................... 5 Mello Roos & Special Taxes .................................................................................................................................................................. 5 Homeowners Insurance ........................................................................................................................................................................ 6 HOA Dues ..................................................................................................................................................................................................... 6 FHA Mortgage Insurance ....................................................................................................................................................................... 6 Monthly Cash Outlays ............................................................................................................................................................................. 6 Tax Savings .................................................................................................................................................................................................. 6 Principal Amortization ........................................................................................................................................................................... 7 Opportunity Cost ...................................................................................................................................................................................... 7 Maintenance and Reserves ................................................................................................................................................................... 8 Monthly Ownership Cost ....................................................................................................................................................................... 8 Comparable Rental .................................................................................................................................................................................. 8 Added Cost or (Savings) ........................................................................................................................................................................ 8 Furnishing and Move In ......................................................................................................................................................................... 9 Closing Costs ............................................................................................................................................................................................... 9 Down Payment .......................................................................................................................................................................................... 9 Total Cash Costs ........................................................................................................................................................................................ 9 Emergency Cash Reserves ................................................................................................................................................................. 10 Total Savings Needed ........................................................................................................................................................................... 10

How Much a House Really Costs ..................................................................................................................................... 11 Mortgage Payment ................................................................................................................................................................................ 11 Property Taxes ....................................................................................................................................................................................... 12 Homeowners Insurance ..................................................................................................................................................................... 13 Private Mortgage Insurance .............................................................................................................................................................. 13 Special Taxes and Levies .................................................................................................................................................................... 14 Homeowner Association Dues and Fees ..................................................................................................................................... 14 Maintenance and Replacement Reserves ................................................................................................................................... 15 Tax Savings ............................................................................................................................................................................................... 15 Hidden Savings ....................................................................................................................................................................................... 16 Opportunity Cost ................................................................................................................................................................................... 16 Ownership Cost Math .......................................................................................................................................................................... 17

Cost to Own

[email protected] 949.769.1599 Page 3 of 17

The OC Housing News ownership cost calculations for family homes

Below is a concise description of each line item displayed on the MLS property details, why the item is important,

and how it’s calculated.

A POINT-‐IN-‐TIME ANALYSIS

Today is reality; tomorrow is a fantasy. The ownership cost calculation is a snapshot of the cost of ownership at the

time of first payment. It makes no projections for future changes such as home price appreciation. This analysis

purposely does not project future changes for two reasons: First, the costs at the time of first payment are

concrete and knowable. It requires fewer assumptions and no crystal ball. Second, most people who estimate

future appreciation wildly overestimate. Very small changes in rates of appreciation make very large differences

over 10 or more years. Overestimating appreciation always makes owning a property look very desirable

financially. It’s a mistake many people made who bought at the peak of the housing bubble.

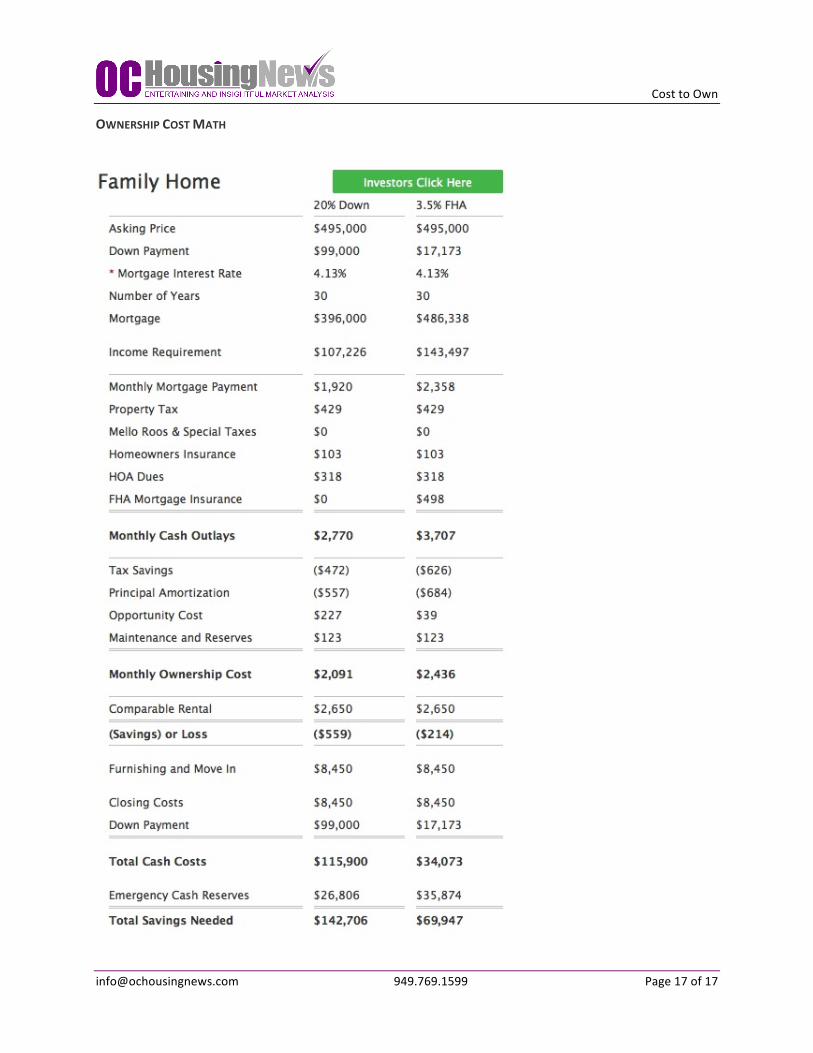

ASKING PRICE

This is the current asking price on the MLS.

DOWN PAYMENT

A conventional loan requires a down payment that is 20% of the purchase price. Down payments will less than 20%

down require private mortgage insurance, a policy paid by the borrower that protects the lender from loss. FHA

down payments are generally 3.5% of the purchase price. The down payment is calculated by multiplying the

asking price by 20% for a conventional loan and 3.5% for an FHA loan.

Cost to Own

[email protected] 949.769.1599 Page 4 of 17

MORTGAGE INTEREST RATE

Mortgage Interest rates are set by lenders competing to offer loans to borrowers who are buying or refinancing

real estate. Mortgage Interest Rates are quoted on many websites, such as Bankrate.com. If the loan is over the

conforming limit, a jumbo premium of 0.35% is added to the market rate. The OC Housing News calculations uses

the interest rate prevailing when the listing first came on the market. The interest rate is periodically updated. The

mortgage interest rate shown is not a quote. It is provided for estimating payments and cost of ownership.

NUMBER OF YEARS

The terms of a loan generally require repayment over time. A mortgage with a fixed repayment schedule is called

an amortizing mortgage, and the period of time over which the mortgage amortizes is called its term. The term of

mortgages is generally 30 years, but 15 year terms are also common, and lenders offer other schedules. The OCHN

calculations assume a 30-‐year fixed-‐rate amortizing mortgage because it is a stable balance between low payments

and reasonable repayment period, and it’s the most common form of home financing.

MORTGAGE

The mortgage balance for a conventional mortgage is the asking price minus the down payment. The mortgage is

80% of the purchase price in these calculations, but buyers executing a move-‐up sale may have larger down

payments and smaller mortgage balances.

The FHA mortgage is not as simple to calculate as a conventional mortgage because the FHA charges a 1.75% up

front fee that gets rolled into the mortgage. The amount borrowed is 96.5% of the purchase price (100% – 3.5%)

plus the 1.75% charge, for a total mortgage balance of 98.25% of the purchase price (96.5% + 1.75%). This is why

the FHA mortgage plus the down payment does not equal the asking price.

Cost to Own

[email protected] 949.769.1599 Page 5 of 17

INCOME REQUIREMENT

The income requirement is based on standards set by Fannie Mae, Freddie Mac, and the Federal Housing

Administration (GSEs and FHA). The monthly cash outlays (described later) multiplied by 12 gives a yearly payment

burden. The yearly payment burden must not exceed 31% of a borrowers income under most circumstances (FHA

often makes exceptions). The formula is as follows: Income Requirement = Monthly Cash Outlays X 12 / 0.31

MONTHLY MORTGAGE PAYMENT

The monthly mortgage payment is determined by lenders using a formula outlined below. It’s based on the

mortgage amount, mortgage interest rate, and loan term (number of years) as described above.

The following formula is used to calculate the fixed monthly payment (P) required to fully amortize a loan of L

dollars over a term of n months at a monthly interest rate of c. [If the quoted rate is 6%, for example, c is .06/12 or

.005].

P = L[c(1 + c)n]/[(1 + c)n -‐ 1]

PROPERTY TAX

Proposition 13 sets property taxes in California are set at 1% of purchase price (assumed asking price).

MELLO ROOS & SPECIAL TAXES

Mello Roos are an example of a special tax levy put on the property by the developer in California. The local

Assessor’s office has this information online, but it is not organized in a way permitting easy download, so it must

be estimated. Not every developer creates a Mello Roos district, so some properties developed since 1985 may

have no Mello Roos. For those properties, the cost of ownership calculations will overstate the true cost.

The calculations on the OCHN estimate as follows:

Cost to Own

[email protected] 949.769.1599 Page 6 of 17

If the year of construction is 2002 or later, Mello Roos = Property Cost Basis × 0.04.

If the year of construction is 1994 or later but earlier than 2002, Mello Roos = Property Cost Basis × 0.02.

If the year of construction is 1985 or later but earlier than 1994, Mello Roos = Property Cost Basis × 0.01.

HOMEOWNERS INSURANCE

Homeowners insurance rates vary widely, but the standard estimation is $25 for each $100,000 in home value.

HOA DUES

The HOA dues is taken straight from the MLS. Sometimes agents input this information incorrectly, but for the

most part, the numbers are accurate.

FHA MORTGAGE INSURANCE

Conventional mortgages with 20% down pay no private mortgage insurance. FHA insures mortgages with as little

as 3.5% down, and the cost of this insurance is 1.3% percentage of the loan balance — it’s higher than property

taxes in California.

MONTHLY CASH OUTLAYS

The monthly cash outlays — also known as PITI — is a standard lender calculation of housing costs. It is the sum of

the costs listed above: payment, property tax, Mello Roos, Insurance, HOAs, and mortgage insurance.

TAX SAVINGS

The tax savings is the most complicated of the calculations. Based on the income requirement, the borrowers

income is compared to both Federal and California tax tables to determine the marginal tax rates for both entities.

To determine the maximum potential tax savings, the marginal tax rate (both Federal and State) is multiplied by

Cost to Own

[email protected] 949.769.1599 Page 7 of 17

the sum of mortgage interest, property taxes, and mortgage insurance (those are deductible expenses). However,

to calculate the actual tax savings the marginal tax rate must be multiplied by the standard deduction, and this

number must be subtracted from the maximum potential tax savings. This adjustment is necessary because in

order to claim the deduction, a tax filer must itemize, and this requires surrendering the standard deduction. This

calculation is so complex because it must be repeated for both State and Federal taxes, and both have different tax

rates, different income thresholds, and different standard deductions.

PRINCIPAL AMORTIZATION

Since part of the mortgage payment is principal, and since this is effectively a forced savings account, the amount

of principal amortization must be backed out because it is not a true cost of ownership.

The payment is calculated by the formula detailed above. The interest on the debt is the outstanding loan balance

multiplied by the interest rate and divided by 12. The interest is subtracted from the payment to ascertain

principal amortization. Over time, principal amortization grows and mortgage interest declines. However, since

this is a point-‐in-‐time analysis, only the amortization of the first payment is counted.

OPPORTUNITY COST

Opportunity cost is perhaps the least understood of the adjustments to ownership cost. When a down payment is

applied to a home purchase, that money came from somewhere. If the buyer would have chosen to rent, that

money could have been invested in any number of safe investment alternatives. The loss of this investment

income is the opportunity cost.

The calculation herein takes the mortgage interest rate, divides it by 3, then adds 1% to it. This generally

approximates the yield on medium-‐term CDs, money-‐market accounts, or Treasuries. For example, at 4.5% interest

rates, the opportunity cost would be 2.5% (4.5% / 3 + 1%).

Cost to Own

[email protected] 949.769.1599 Page 8 of 17

MAINTENANCE AND RESERVES

Real property requires routine maintenance. Further, over time, more expensive items such as roofs or exterior

paint need replacement. Budgeting for the irregular expenses of routine maintenance and the slow depletion of

wear and tear requires establishing a monthly allowance for maintenance and replacement reserves.

The formula used here is asking price times three-‐tenths of one percent divided by twelve (0.003/12).

MONTHLY OWNERSHIP COST

The monthly ownership cost is the monthly cash outlays adjusted for tax savings, principal amortization,

opportunity cost, and maintenance reserves.

COMPARABLE RENTAL

Comparable rental rates are determined by an advanced algorithm for selecting comparable properties. When I

was actively flipping properties in Las Vegas, I evaluated both resale and rental comps on over 1,500 properties. I

developed a series of steps to gradually loosen the various parameters until I obtained a sufficient number of

comparable properties to make a reasonable estimate of value. These algorithms are proprietary. As this is an

automated analysis, there is a degree of error in these estimates, and the actual comparable rental rate may be

significantly higher or lower than the rate shown.

ADDED COST OR (SAVINGS)

The savings or loss is the monthly ownership cost minus the cost of a comparable rental. If this number is negative

(in parenthesis), then the property costs less to own that to rent, which is a good sign. If the number is positive, it

costs more to own than to rent.

Cost to Own

[email protected] 949.769.1599 Page 9 of 17

FURNISHING AND MOVE IN

Furnishing and move in costs vary considerably depending on the tastes of the buyer. There are generally fixed

costs for movers and other service providers, and variable costs for furnishings. In general, people will furnish a

house in proportion to its cost. The following formula is a low-‐cost estimate; most people when moving in to a

family home will spend much more.

The formula used here to estimate is 1% of the asking price plus $3,500.

CLOSING COSTS

The buyer and seller often split certain costs at closing, and some costs are entirely the responsibility of the buyer.

What’s paid by the buyer and what is a split cost varies by local custom. For financed purchases, the buyer must

pay closing costs including loan origination fees and other lender costs.

The formula used here to estimate is 1% of the asking price plus $3,500.

DOWN PAYMENT

The down payment is calculated above. It’s repeated here because it’s part of the calculation of total cash costs.

TOTAL CASH COSTS

The total cash costs is the amount of money a buyer must have available to complete the sale including furnishing

and move in, closing costs, and the down payment. People often forget about closing costs and furnishing cost and

go into debt shortly after the sale to cover these costs.

Cost to Own

[email protected] 949.769.1599 Page 10 of 17

EMERGENCY CASH RESERVES

Though not an actual cost of acquiring the property, financial advisors always recommend having sufficient cash

reserves to cover expenses in case of an emergency. Further, lenders often require liquid cash reserves in addition

to the down payment as a condition to funding. Most borrowers do not reserve much if anything when buying a

home. Almost none have an additional six-‐month’s income like most financial advisors recommend.

The calculation herein only estimates three month’s of income based on the income requirement generated

above.

TOTAL SAVINGS NEEDED

The total amount of savings necessary to have a stress-‐free purchase is the total cash costs plus sufficient

emergency reserves.

Cost to Own

[email protected] 949.769.1599 Page 11 of 17

How Much a House Really Costs

If you are leaning toward owning, it’s important to know how much the property will really cost to own. Most

people make emotional decisions about ownership without a careful examination of the costs. Any analysis is

usually slanted toward justifying a decision they already made. Therefore, the costs tend to be underestimated or

missed entirely, and the benefits are often exaggerated. Getting this right can make the difference between a

happy period of ownership and a soul-‐draining loss of income or even the house itself.

A useful way to look at the total cost of housing is to evaluate the monthly cost of ownership. An ownership cost is

any expenditure required for the possession of property. A working definition is important because there are many

hidden or forgotten costs people overlook. These costs are borne by owners and not by renters. There are 7 costs

to owning a house. Although some of these costs are not paid on a monthly basis, they can be evaluated on a

monthly basis with simple math. These costs are:

• Mortgage Payment • Property Taxes • Homeowners Insurance • Private Mortgage Insurance • Special Taxes and Levies • Homeowners Association Dues or Fees • Maintenance and Replacement Reserves

MORTGAGE PAYMENT

The mortgage payment is the first and most obvious payment because it is the largest. It is also an area where

people take risks to reduce the cost of housing. It was the manipulation of mortgage payments that was the focus

of the lending industry “innovation” that inflated the housing bubble. The relationship between payment and loan

amount is the most important determinant of housing prices. This relationship changes with loan terms such as the

interest rate, but it is also strongly influenced by the type of amortization, if any. Amortizing loans, loans that

require principal repayment in each monthly payment, finance the smallest amount. Interest-‐only loan terms

finance a larger amount than amortizing loans because none of the payment is going toward principal. Negatively

Cost to Own

[email protected] 949.769.1599 Page 12 of 17

amortizing loans finance the largest amount because the monthly payment does not cover the actual interest

expense. Interest-‐only and negatively amortizing loans proved so unstable during the housing bubble, they were

withdrawn from the mortgage market.

By far the best way to determine affordability of a financed home purchase is to compare the cost of ownership to

the cost of a rental. Most markets trade near rental parity levels because financially whichever is lower is generally

the better deal. As rents become

less than the cost of ownership,

many chose to rent, and when

the cost of ownership falls below

the cost of a rental, people chose

to buy.

PROPERTY TAXES

Property taxes have long been a

source of local government tax revenues. Real property cannot be moved out of a government's jurisdiction, and

values can be estimated by an appraisal, so it is a convenient item to tax. In most states, local governments add up

the cost of running the government and divide by the total property value in the jurisdiction to establish a millage

tax rate. California is forced to do things differently by Proposition 13, which effectively limits the appraised value

and total tax revenue from real property. Local governments are forced to find revenue from other sources.

Proposition 13 limits the tax rate to 1% of purchase price with a small inflation multiplier allowing yearly increases.

In California, the first half of regular secured property tax bills are due November 1st, and delinquent after

December 10th; the second half are due February 1st, and delinquent after April 10th each year. If the delinquent

date falls on a Saturday, Sunday, or government holiday, then the due date is the following business day. Often the

lender will compel the borrower to include extra money in the monthly payment to cover property taxes,

homeowners insurance, and private mortgage insurance, and these bills will be paid by the lender when they come

Cost to Own

[email protected] 949.769.1599 Page 13 of 17

due. If these payments are not escrowed by the lender, then the borrower will need to make these payments. The

total yearly property tax bill can be divided by 12 to obtain the monthly cost.

HOMEOWNERS INSURANCE

Homeowners insurance is almost always required by a lender to insure the collateral for the loan. Even if there is

no lender involved, it is always a good idea to carry homeowners insurance. The risk of loss from damage to the

house can be a financial catastrophe without the proper insurance. A standard policy insures the home itself and

the things you keep in it. Homeowners insurance is a package policy. This means that it covers both damage to

your property and your liability or legal responsibility for any injuries and property damage you or members of

your family cause to other people. This includes damage caused by household pets. Damage caused by most

disasters is covered but there are exceptions. The most significant are damage caused by floods, earthquakes and

poor maintenance. You must buy two separate policies for flood and earthquake coverage. Maintenance-‐related

problems are the homeowners' responsibility.

PRIVATE MORTGAGE INSURANCE

Mortgages against real property take priority on a first recorded, first paid basis. This is known as their lien

position. This becomes very important in instances of foreclosure. The first mortgage holder gets paid in full before

the second mortgage holder gets paid and so on through the chain of mortgages on a property. In a foreclosure

situation, subordinate loans are often completely wiped out, and if the loss is great enough, the first mortgage may

be imperiled. Because of this fact, if the purchase money mortgage (1st lien position) exceeds 80% of the value of

the home, the lender will require the borrower to purchase an insurance policy to protect the lender in event of

loss. This policy is of no use or benefit to the borrower as it insures the lender against loss. It is simply an added

cost of ownership. Many of the purchase transactions during the bubble rally had an 80% purchase money

mortgage and a “piggy back” loan of up to 20% to cover the remaining cost. These loan pairs are often referred to

Cost to Own

[email protected] 949.769.1599 Page 14 of 17

as 80/20 loans, and they were used primarily to avoid private mortgage insurance. There were very common

during the bubble.

In the aftermath of the housing crash, many mortgage insurers went out of business due to excessive losses.

Further, the insurance funds maintained by the FHA became dangerously imperiled. As a result, private mortgage

insurance costs rose significantly. Since private mortgage insurance is simply an add-‐on cost of paying the

mortgage, it can be looked on as an additional interest charge. An FHA loan may have a 3.5% interest rate, but

when the FHA insurance premiums are added, the effective interest rate rises to 5% or more. Avoiding the cost of

private mortgage insurance is a strong financial reward to those who can put 20% down.

SPECIAL TAXES AND LEVIES

Several areas have special taxing districts that increase the tax burden beyond the normal property tax bill. Many

states have provisions which allow supplemental property tax situations. The State of California has Mello Roos

fees. A Mello-‐Roos District is an area where a special tax is imposed on those real property owners within a

Community Facilities District. This district is established to obtain public financing through the sale of bonds for the

purpose of financing certain public improvements and services. These services may include streets, water, sewage

and drainage, electricity, infrastructure, schools, parks and police protection to newly developing areas. The taxes

paid are used to make the payments of principal and interest on the bonds.

HOMEOWNER ASSOCIATION DUES AND FEES

Many modern planned communities have homeowners associations formed to maintain privately owned facilities

held for the exclusive use of community residents. These HOAs bill the owners monthly to provide these services.

They have foreclosure powers if the bills are not paid. It is given the authority to enforce the covenants, conditions,

and restrictions (CC&Rs) and to manage the common amenities of the development. It allows the developer to

legally exit responsibility of the community typically by transferring ownership of the association to the

Cost to Own

[email protected] 949.769.1599 Page 15 of 17

homeowners after selling off a predetermined number of lots. Most homeowners' associations are non-‐profit

corporations, and are subject to state statutes that govern non-‐profit corporations and homeowners' associations.

MAINTENANCE AND REPLACEMENT RESERVES

An often-‐overlooked cost of ownership is the cost of routine maintenance and the funding of reserves for major

repairs. For example, a composite shingle roof must be replaced every 20-‐25 years. It may take $100 a month set

aside for 20 years to fund this replacement cost. Also, condominium associations often levy special assessments to

undertake required work for which the reserves are insufficient. In the real world, most people do not set aside

money for these items, which is a mistake. Most will attempt to obtain a Home Equity Line of Credit (HELOC) to

fund the repairs when they are necessary. Of course this assumes a property has appreciated and such financing

will be made available.

TAX SAVINGS

There are two other variables people often consider when evaluating the cost of ownership that is not included in

the prior list: income tax savings and lost down payment interest. When a borrower takes out a home loan, the

interest is tax deductible up to a certain amount. For borrowers in the highest marginal tax bracket, the savings

can be significant, and this can make a dramatic difference in the true cost of ownership. However, this benefit

diminishes over time as the loan is paid off and the interest decreases. Plus, contrary to popular belief, it is never

good financial planning to spend $100 to save $25 in taxes. Also, these benefits are almost universally

overestimated by people considering a home purchase. A renter considering home ownership will need to

remember they will be giving up the standard deduction when they itemize to obtain the Home Mortgage Interest

Deduction (HMID). A "married filing jointly" taxpayer will forgo a $10,700 deduction in 2007. This reduces the net

impact of the HMID. Anecdotally, even those in the highest tax brackets usually do not get more than a 25% tax

savings.

Cost to Own

[email protected] 949.769.1599 Page 16 of 17

HIDDEN SAVINGS

This is the forgotten benefit of a conventionally amortizing loan: forced savings. Most people are not good at

saving. The government recognized this years ago when they started taking money out of peoples salaries to pay

income taxes because they knew people would not do it on their own. People who become homeowners during

their lifetimes often have the equity in their home as their only source of retirement savings other than social

security. To accurately calculate the cost of ownership, this hidden savings amount needs to be deducted from the

total cost of ownership because this money will generally come back to the borrower at the time of sale. Since

taxpayers in the United States get a capital gains exemption up to $250,000, this savings amount does not need to

be adjusted for taxes.

OPPORTUNITY COST

Unless 100% financing is utilized, a cash down payment will generally be withdrawn from an interest bearing

account to purchase a house. The monthly interest that would have accrued if the down payment money was still

in the bank is a cost of ownership. This is perhaps the most overlooked ownership cost. For instance, if you are

putting 20% down on a $500,000 property, you will be taking $100,000 from a bank account where it would have

earned a return. If someone chooses to rent rather than buy, they would earn this interest income. Of course, this

earned income is also taxed, so 75% of this number is the net opportunity cost of a down payment.