Market Trends and Opportunities for 2014 1:15-2:05 pm

Moderator: Gerard Sansosti, Executive Managing Director, HFF Panelists: Stacey Berger, Executive Vice President, PNC Real Estate/Midland Loan Services Keith Honig, Managing Director, AIG Investments Michael H. Lowe, Co-President and Chief Investment Officer, Lowe Enterprises Lisa Pendergast, Managing Director, Jefferies & Company LLC Mitchell Resnick, Vice President, Multifamily Loan Pricing & Securitization, Freddie Mac

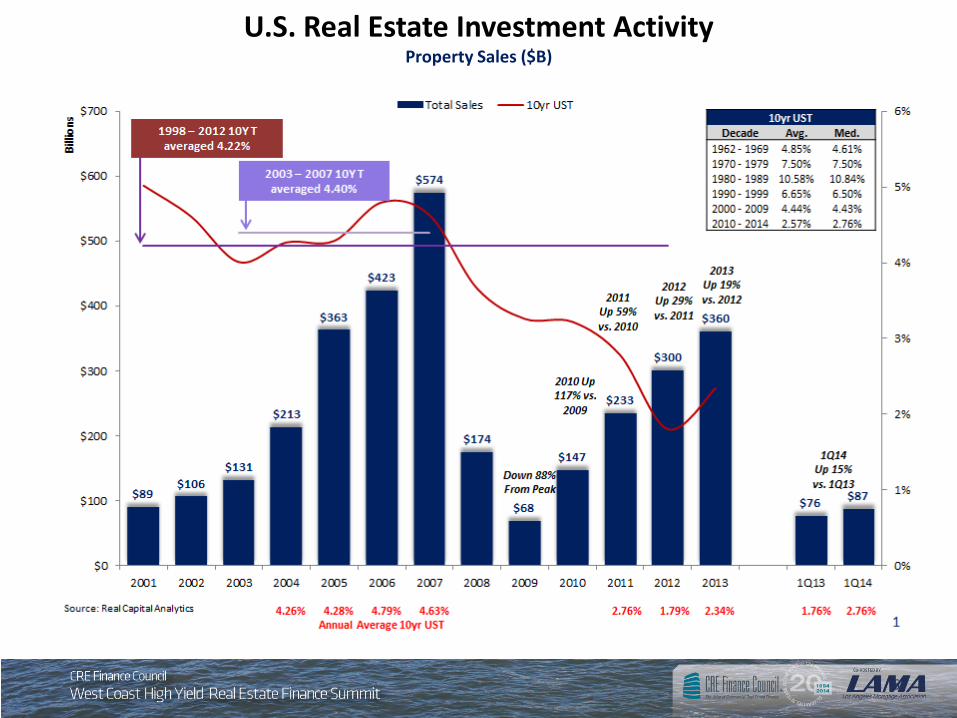

U.S. Real Estate Investment Activity Property Sales ($B)

6

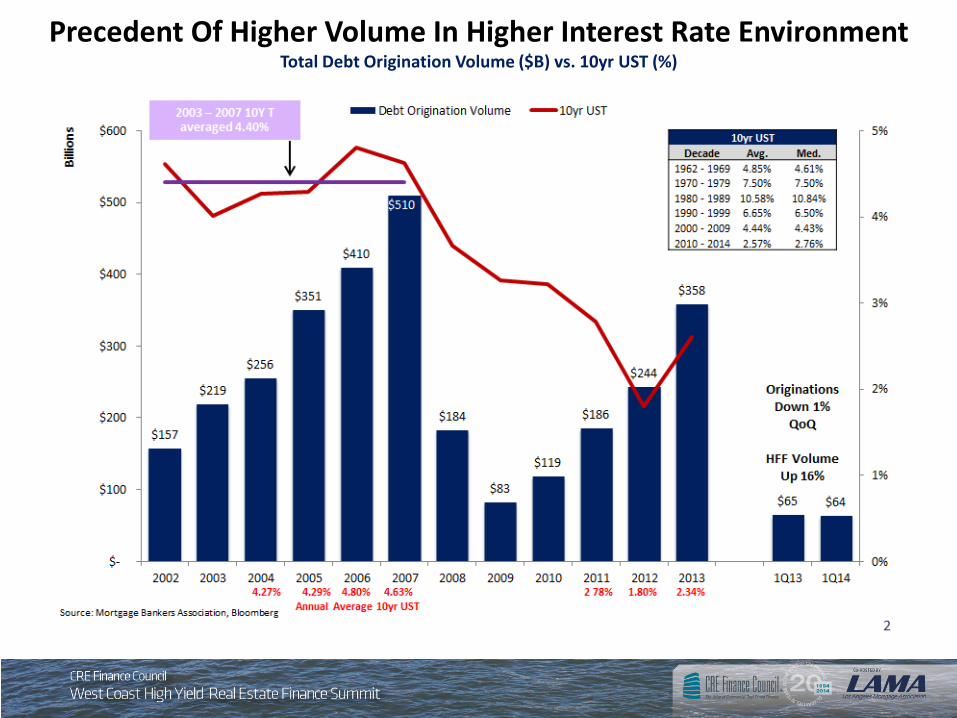

Precedent Of Higher Volume In Higher Interest Rate Environment Total Debt Origination Volume ($B) vs. 10yr UST (%)

Debt Originations Highly Correlated To Transaction Volumes Quarterly Volumes ($B)

8

Source: Mortgage Bankers Association, Real Capital Analytics

9

Debt Origination Volume 2013 Originations Exceed 2005

Source: MBA. Total Debt Origination Volume is for closed loans made by dedicated commercial real estate finance firms and does not double count loans; it can be used as a gauge of the overall volume of lending activity.

$20 $30 $46 $70 $86 $109 $64 $20 $20 $32 $57 $100 $73 $105

$112 $165

$186 $225

$7 $22 $37

$80 $26

$31 $38

$50

$54

$52

$31

$17 $31 $49

$50

$60

$16

$20 $20

$25

$26

$35

$40

$31 $31

$44

$58

$48

$168

$227

$263

$351

$410

$510

$184

$83

$119

$186

$244

$358

$-

$100

$200

$300

$400

$500

$600

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Billi

ons

Commercial Banks Conduits Life InsuranceGSE's (Fannie + Freddie) REITs, Mtg REITs, Investment Funds FHACredit Other Pension Funds

10

Debt Origination Volume Commercial Banks & Conduits Increase Market Share In 2013

Source: MBA. Total Debt Origination Volume is for closed loans made by dedicated commercial real estate finance firms and does not double count loans; it can be used as a gauge of the overall volume of lending activity.

28%

23%

17%

17%

24%

35%

21%

21%

20%

18%

14%

12%

22%

15%

12%

6%

0%

2%

44%

45%

47%

44%

48%

46%

17%

21%

27%

26%

22%

18%

11%

14%

16%

17%

17%

18%

13%

24%

24%

26%

37%

22%

7%

6%

7%

8%

9%

10%

7%

2%

3%

2%

1%

5%

8%

7%

10%

7%

1%

0%

1%

1%

1%

2%

2%

1%

1%

7%

4%

3%

7%

7%

9%

14%

9%

13%

12%

9%

9%

12%

10%

11%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2013

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

Commercial Banks Conduits Life Insurance & Pension Funds

GSE's (Fannie + Freddie) REITs, Mtg REITs, Investment Funds FHA

Credit Other

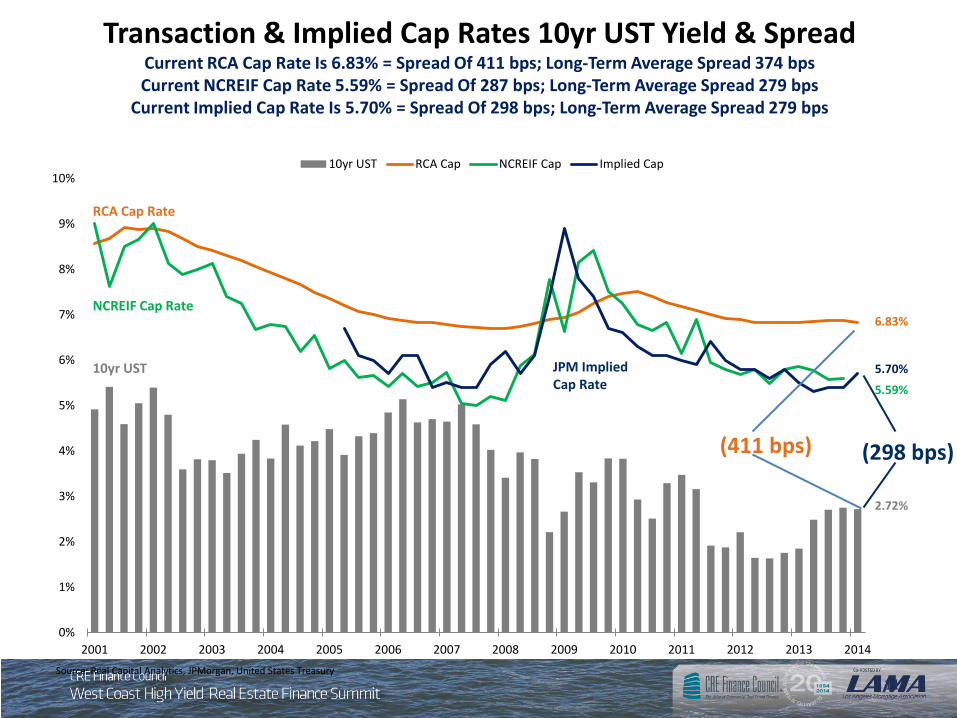

2.72%

6.83%

5.59%

5.70%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

10yr UST RCA Cap NCREIF Cap Implied Cap

11

JPM Implied Cap Rate

RCA Cap Rate

NCREIF Cap Rate

10yr UST

(411 bps) (298 bps)

Transaction & Implied Cap Rates 10yr UST Yield & Spread Current RCA Cap Rate Is 6.83% = Spread Of 411 bps; Long-Term Average Spread 374 bps Current NCREIF Cap Rate 5.59% = Spread Of 287 bps; Long-Term Average Spread 279 bps

Current Implied Cap Rate Is 5.70% = Spread Of 298 bps; Long-Term Average Spread 279 bps

Source: Real Capital Analytics, JPMorgan, United States Treasury

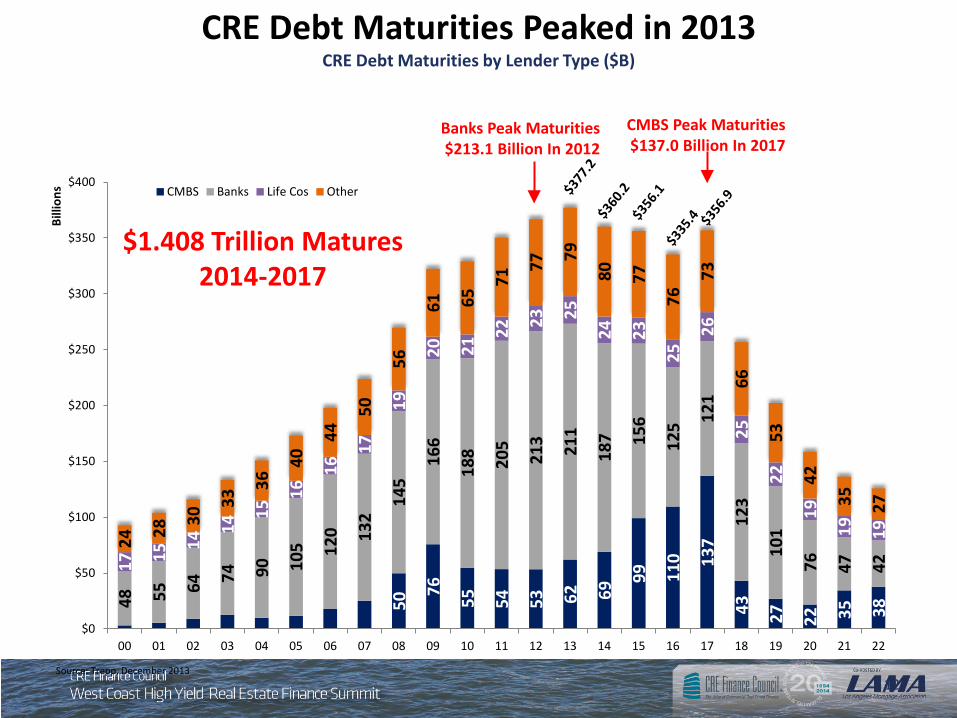

CRE Debt Maturities Peaked in 2013 CRE Debt Maturities by Lender Type ($B)

12

50 76

55

54

53

62

69 99

110 13

7

43

27

22 35

38 48

55 64

74

90

105 12

0 132

145

166

188 205

213 21

1

187 15

6

125 12

1

123

101

76

47

42

17 15

14 14

15 16

16 17

19

20

21 22

23 25

24

23

25 26

25

22

19

19

19

24 28

30 33

36 40

44 50

56

61

65 71

77 79

80

77

76 73

66

53

42

35

27

$0

$50

$100

$150

$200

$250

$300

$350

$400

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22

Billi

ons CMBS Banks Life Cos Other

CMBS Peak Maturities $137.0 Billion In 2017

Banks Peak Maturities $213.1 Billion In 2012

$1.408 Trillion Matures 2014-2017

Source: Trepp, December 2013

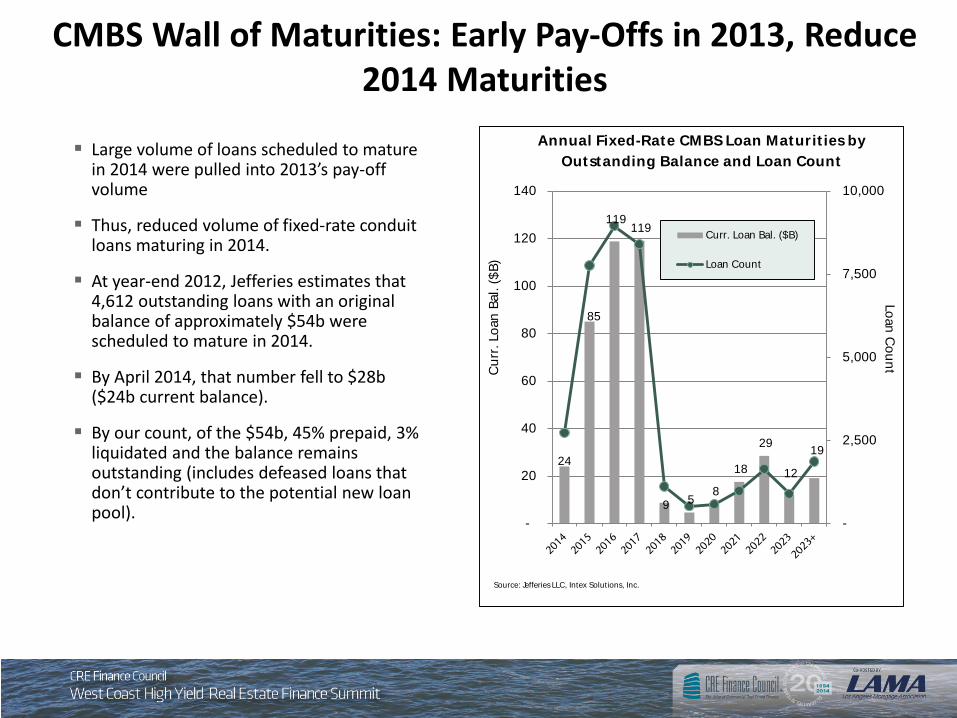

CMBS Wall of Maturities: Early Pay-Offs in 2013, Reduce 2014 Maturities

Large volume of loans scheduled to mature in 2014 were pulled into 2013’s pay-off volume

Thus, reduced volume of fixed-rate conduit loans maturing in 2014.

At year-end 2012, Jefferies estimates that 4,612 outstanding loans with an original balance of approximately $54b were scheduled to mature in 2014.

By April 2014, that number fell to $28b ($24b current balance).

By our count, of the $54b, 45% prepaid, 3% liquidated and the balance remains outstanding (includes defeased loans that don’t contribute to the potential new loan pool).

24

85

119 119

9 5 8

18

29

12

19

-

2,500

5,000

7,500

10,000

-

20

40

60

80

100

120

140

Loan CountCur

r. Lo

an B

al. (

$B)

Annual Fixed-Rate CMBS Loan Maturit ies by Outstanding Balance and Loan Count

Curr. Loan Bal. ($B)

Loan Count

Source: Jefferies LLC, Intex Solutions, Inc.

A CMBS Cycle in Hyper Drive Increase in Conduit Lenders and Growing Debt Capital Sources Elsewhere... As more and more firms take a shot at the origination side of the business, their efforts have not been met

with the demand many thought would exist in early 2014. US. CMBS Issuance Slower Than Projected U.S. CMBS issuance through first 4 months of 2014 totals $24.3b vs. $29.4b for same-period 2013 At the current pace, total U.S. CMBS 2014 issuance will total a projected $65b vs. projections of as

much as $110b and 2013 volume of $81.9b

U.S. Agency CMBS Issuance Follows Suit $22.65 for first four of months of 2013 $15.2b for first four months of 2014

What to Watch for? More investors are willing to pay a premium for better-quality collateral Focus on 2011 and 2012 conduit deals Real money investors staying at the top of the capital stack in deals with aggressively underwritten

collateral Faster money focused on BBB- bonds, pushing spreads to YTD tight of around +315 bps Recent deals experienced increase in credit enhancement to offset more aggressive loans, weaker

assets Investors continuing to focus on Single-Borrower/Single-Asset CMBS. Although 144A, most of these

deals have sufficiently less leverage than their conduit counterparts and assets tend to be trophy quality

A CMBS Cycle in Hyper-Drive: Underwriting Standards Similar to 2005

Conduit / Fusion Fixed-Rate CMBS Comparat ive Analysis2014* 2010 2007 2006 2005

Total Issuance ($B) 18.7 9.2 188.6 161.8 136.4Avg. Deal Size ($B) 1.2 0.8 3.6 2.6 2.2Issuer Debt Yield (%) 10.88 12.86 8.26 9.38 10.32Issuer LTV (%) 65.3 57.9 69.1 68.0 68.7Issuer DSCR 1.69 1.85 1.40 1.47 1.60No. of Loans 65 31 193 188 164No. of Properties 110 74 282 264 228# Properties/# Loans 0 2.38 1.46 1.40 1.39Avg. Loan Size ($M) 18.7 20.4 17.9 14.5 13.9Largest Loan (%) 9.7 15.8 10.0 9.5 8.7Top Ten (%) 0.5 68.8 43.5 41.4 41.4Hotel (%) 13.0 4.7 10.4 10.6 7.2Office (%) 16.5 33.8 27.0 30.3 32.3Retail (%) 29.8 38.8 31.1 31.7 33.2Single-Tenant Exp. (%) 8.5 26.1 11.7 12.4 9.5Avg. AAA Base CE (%) 22.25 18.09 12.00 12.02 12.67Avg. BBB- CE (%) 7.38 6.25 3.12 3.06 3.33% of IO Loans (Partial) 38.4 6.0 30.2 45.2 41.9% of IO Loans (Term) 16.3 7.4 55.8 29.2 21.8Stressed DSCR 1.01 1.36 0.91 1.00 1.05Stressed LTV (%) 105.0 82.6 111.2 100.5 96.4Stressed Debt Yield (%) 9.4 10.9 - - -Cash Flow Hair Cut (%) 5.8 6.0 8.3 5.9 4.2Subordinate Debt (%) 10.1 17.0 54.6 43.7 39.6B-notes (%) 2.2 7.4 8.1 6.9 7.1IG Rated Loans (%) 5.3 33.5 7.0 11.8 13.9Sources: Jefferies LLC, DBRS, Fitch, Kroll, Moody's, Morningstar, S&P. Notes. 2002-2005 IO % = initial and term IO loans combined. *2014 as of 4/30/14.

Rating agency (RA) DSCR ,LTV, and cash

flow haircuts currently resemble 2006 level Unfortunately, the slide continues in

early-2014 2007 RA Stressed DSCR 0.91x vs.

current level of 1.01x 2007 RA Stressed LTV of 111.2%

vs. current level of 104.6% 2007 RA cash flow haircut 5.9% vs.

current level of 5.8%

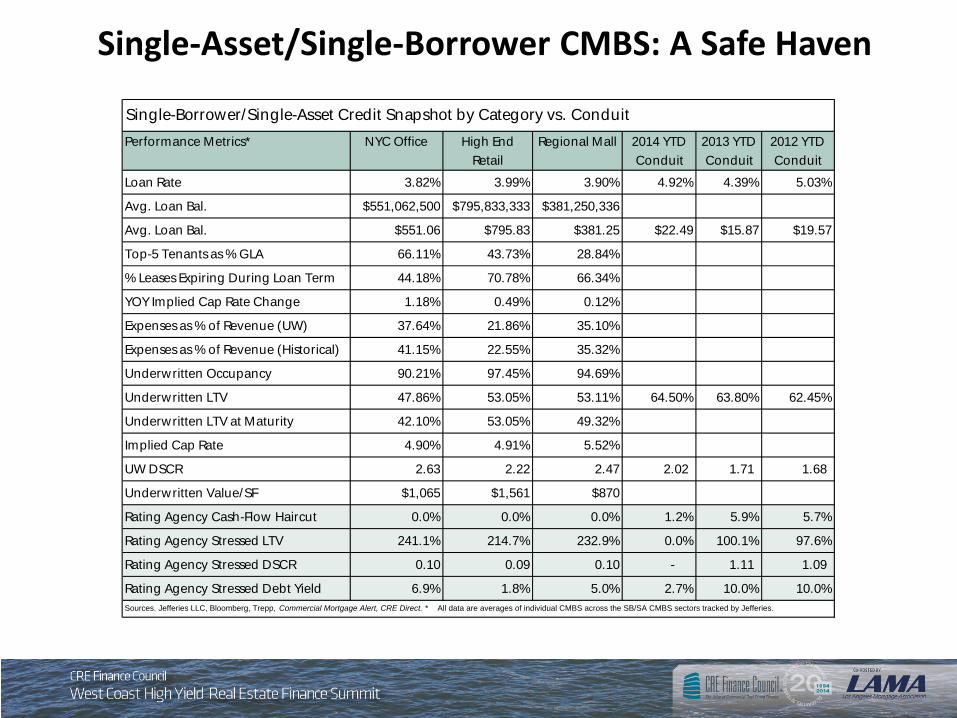

Single-Asset/Single-Borrower CMBS: A Safe Haven

Single-Borrower/Single-Asset Credit Snapshot by Category vs. ConduitPerformance Metrics* NYC Office High End

RetailRegional Mall 2014 YTD

Conduit2013 YTD Conduit

2012 YTD Conduit

Loan Rate 3.82% 3.99% 3.90% 4.92% 4.39% 5.03%

Avg. Loan Bal. $551,062,500 $795,833,333 $381,250,336

Avg. Loan Bal. $551.06 $795.83 $381.25 $22.49 $15.87 $19.57

Top-5 Tenants as % GLA 66.11% 43.73% 28.84%

% Leases Expiring During Loan Term 44.18% 70.78% 66.34%

YOY Implied Cap Rate Change 1.18% 0.49% 0.12%

Expenses as % of Revenue (UW) 37.64% 21.86% 35.10%

Expenses as % of Revenue (Historical) 41.15% 22.55% 35.32%

Underwritten Occupancy 90.21% 97.45% 94.69%

Underwritten LTV 47.86% 53.05% 53.11% 64.50% 63.80% 62.45%

Underwritten LTV at Maturity 42.10% 53.05% 49.32%

Implied Cap Rate 4.90% 4.91% 5.52%

UW DSCR 2.63 2.22 2.47 2.02 1.71 1.68

Underwritten Value/SF $1,065 $1,561 $870

Rating Agency Cash-Flow Haircut 0.0% 0.0% 0.0% 1.2% 5.9% 5.7%

Rating Agency Stressed LTV 241.1% 214.7% 232.9% 0.0% 100.1% 97.6%

Rating Agency Stressed DSCR 0.10 0.09 0.10 - 1.11 1.09

Rating Agency Stressed Debt Yield 6.9% 1.8% 5.0% 2.7% 10.0% 10.0%Sources. Jefferies LLC, Bloomberg, Trepp, Commercial Mortgage Alert, CRE Direct. * All data are averages of individual CMBS across the SB/SA CMBS sectors tracked by Jefferies.

Market Trends and Opportunities for 2014

TOP OF THE STACK REMAINS RELATIVELY UNCHANGED Money managers continue to focus on the short and long part of the curve to meet wide variety of investor

demand Banks have exhibited willingness to pay premium in return for more stable/predictable ASB (amortizing class) and

Front Pay LCF cash flows LCF still attractive to broad investor base ranging from Insurance accounts to Retirement funds as investors

continue to search for money-good assets with sufficient yields further out the curve

CREDIT STACK LOSING SPONSORSHIP As underwriting and structural leverage have increased, many money manager, banks, and insurance companies

have shied away from purchasing A- and BBB- tranches for the fear of these bonds taking losses. Insurance companies are often more comfortable originating a loan in accordance with their own underwriting

standards and holding on their books versus gaining similar yields in purchasing A- and BBB- classes

Tranche Rating WAL (Yrs) Particpant Account TypeA1/A2 AAA 2.5-5 Money ManagerA3 AAA 7 Insurance/Money ManagerASB AAA 7.5 Bank/ Insurance/Money ManagerFront Pay LCF A4 AAA 10 Bank/ Insurance/Money ManagerLCF A5 AAA 10 Money Manager/ Insurance/Retirement-Pension FundAS AAA 10 Insurance/Money ManagerB AA- 10 Money Manager/ InsuranceC A- 10 Money Manager/Hedge FundD BBB- 10 Money Manager/Hedge Fund

New Issue Conduit Capital Stack Investor Analysis