MBSP 0354MBSP 0354International FinanceInternational Finance

Lecture 5Lecture 5

03 NOV 0903 NOV 09

DEVISING A DEVISING A FOREIGN EXCHANGE FOREIGN EXCHANGE

MANAGEMENT MANAGEMENT STRATEGYSTRATEGY

Objectives of LectureObjectives of Lecture

Introduce the Role of the Introduce the Role of the TreasurerTreasurer

Discuss:Discuss: External FX Management External FX Management StrategiesStrategies

Internal FX Management Internal FX Management StrategiesStrategies

Readings:Readings:

Buckley:Buckley: Chapter 10Chapter 10 Chapter 11Chapter 11 Chapter 32 - 32.3 to 32.5Chapter 32 - 32.3 to 32.5

Centralise or DecentraliseCentralise or Decentralise

Centralise:Centralise: Take Decisions at “Group” LevelTake Decisions at “Group” Level Maybe CheaperMaybe Cheaper Maybe more EfficientMaybe more Efficient

Decentralise:Decentralise: Take Decisions at “Subsidiary Take Decisions at “Subsidiary Company” LevelCompany” Level

Maybe more in Line with Maybe more in Line with Devolved Management Devolved Management ResponsibilityResponsibility

Centralise or DecentraliseCentralise or Decentralise

Responsibility

ControlAccountability

Enter – The TreasurerEnter – The Treasurer

Internal BANKER:Internal BANKER: NOT AccountantNOT Accountant

Job is to Make Best Use of Job is to Make Best Use of Internal and External Banking Internal and External Banking Facilities and TechniquesFacilities and Techniques

Profit Centre or Cost CentreProfit Centre or Cost Centre

The Treasurer – Job DescriptionThe Treasurer – Job Description

Identify Exposure:Identify Exposure: Transaction ExposureTransaction Exposure Translation ExposureTranslation Exposure Commercial / Economic ExposureCommercial / Economic Exposure

Manage ExposureManage Exposure Manage CashManage Cash

Transaction ExposureTransaction Exposure

Arises from Changes in Spot Arises from Changes in Spot RateRate

Affects:Affects: Sales RevenueSales Revenue Cost of SalesCost of Sales OverheadOverhead CostCost

A Threat to the Profit & Loss A Threat to the Profit & Loss AccountAccount

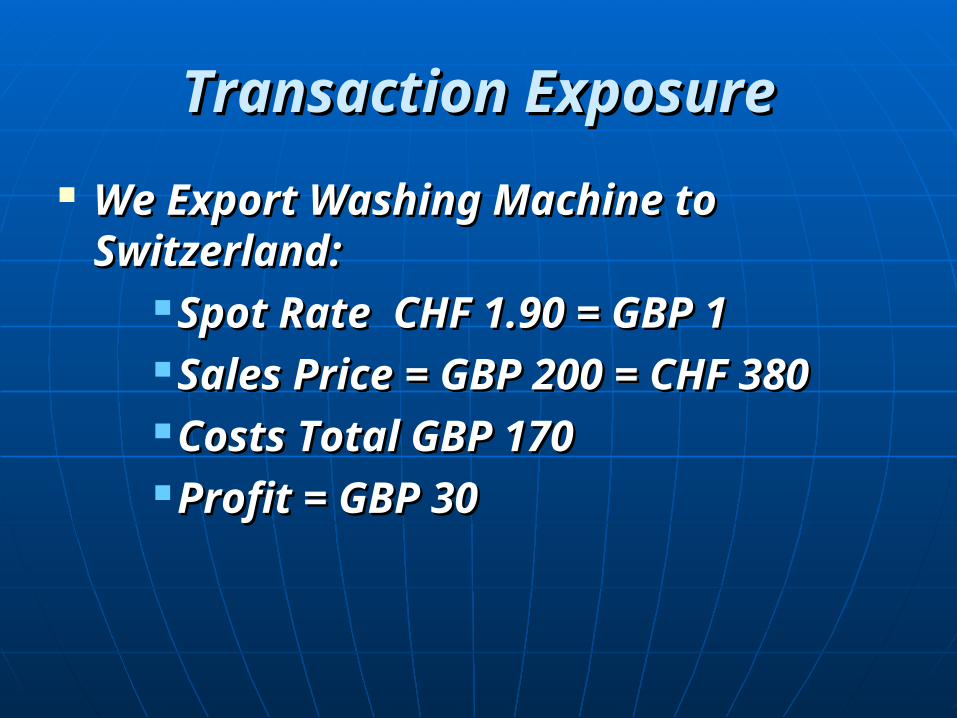

Transaction ExposureTransaction Exposure

We Export Washing Machine to We Export Washing Machine to Switzerland:Switzerland:

Spot Rate CHF 1.90 = GBP 1Spot Rate CHF 1.90 = GBP 1 Sales Price = GBP 200 = CHF Sales Price = GBP 200 = CHF 380380

Costs Total GBP 170Costs Total GBP 170 Profit = GBP 30Profit = GBP 30

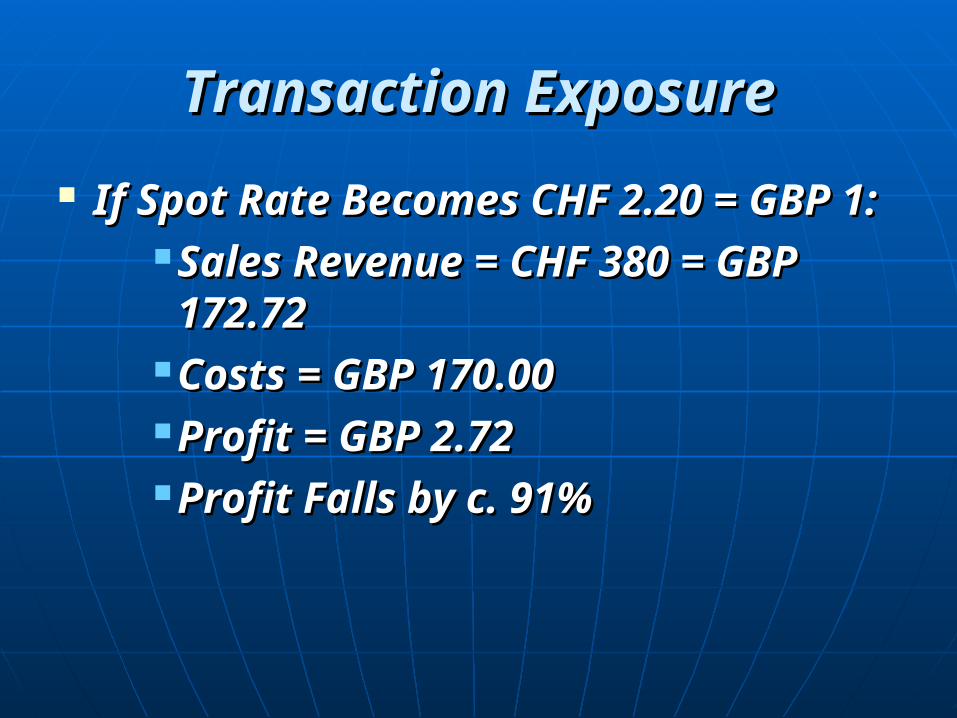

Transaction ExposureTransaction Exposure

If Spot Rate Becomes CHF 2.20 = If Spot Rate Becomes CHF 2.20 = GBP 1:GBP 1:

Sales Revenue = CHF 380 = Sales Revenue = CHF 380 = GBP 172.72GBP 172.72

Costs = GBP 170.00Costs = GBP 170.00 Profit = GBP 2.72Profit = GBP 2.72 Profit Falls by c. 91%Profit Falls by c. 91%

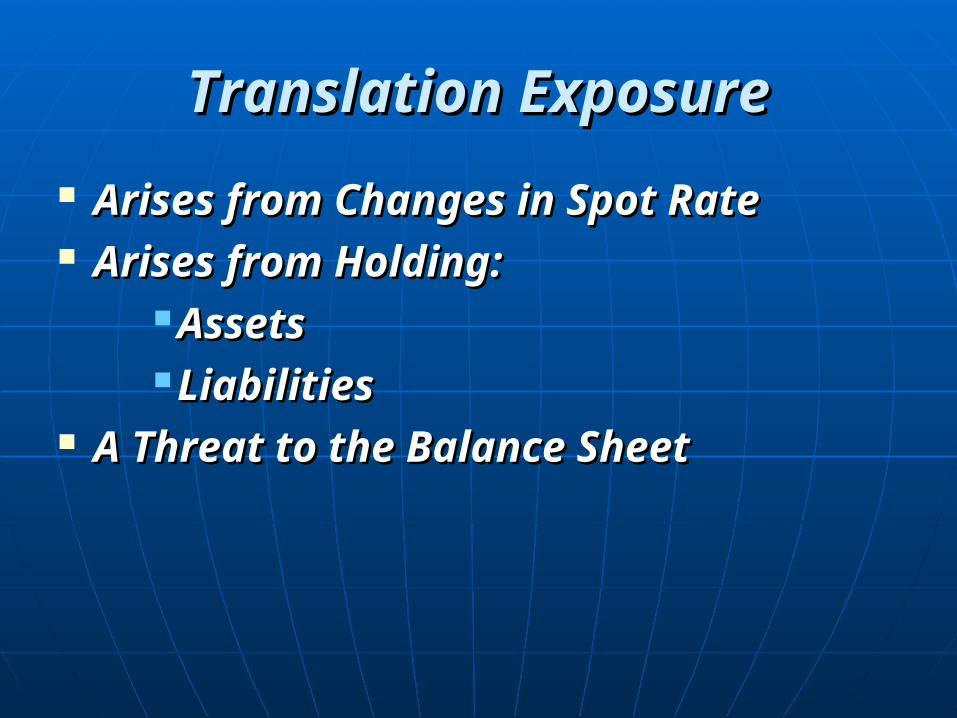

Translation ExposureTranslation Exposure

Arises from Changes in Spot Arises from Changes in Spot RateRate

Arises from Holding:Arises from Holding: AssetsAssets LiabilitiesLiabilities

A Threat to the Balance SheetA Threat to the Balance Sheet

Translation ExposureTranslation Exposure

Purchase Office Block / Service Centre Purchase Office Block / Service Centre for CHF 2,000,000for CHF 2,000,000

Spot Rate CHF 1.90 = GBP 1:Spot Rate CHF 1.90 = GBP 1: Value is GBP 1,052,630Value is GBP 1,052,630

2 years Later:2 years Later: Value is Still CHF 2,000,000Value is Still CHF 2,000,000 Spot Rate is CHF 2.20 = GBP 1Spot Rate is CHF 2.20 = GBP 1 Value is GBP 909,090Value is GBP 909,090 Translation Loss is GBP 143,540Translation Loss is GBP 143,540

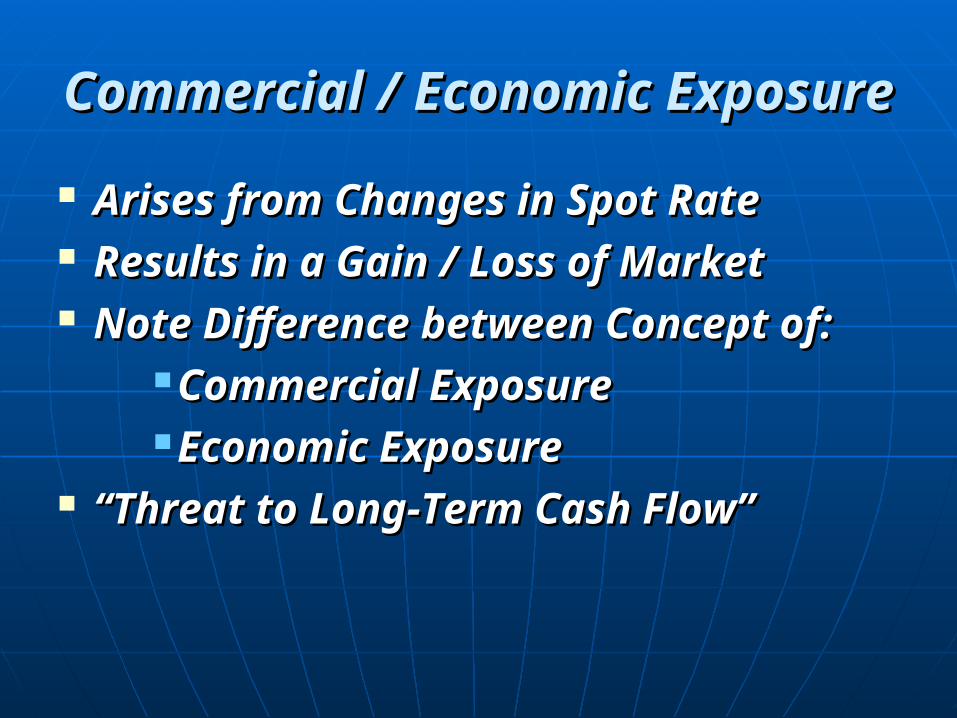

Commercial / Economic Commercial / Economic ExposureExposure

Arises from Changes in Spot RateArises from Changes in Spot Rate Results in a Gain / Loss of MarketResults in a Gain / Loss of Market Note Difference between Concept Note Difference between Concept

of:of: Commercial ExposureCommercial Exposure Economic ExposureEconomic Exposure

““Threat to Long-Term Cash Flow”Threat to Long-Term Cash Flow”

Commercial / Economic Commercial / Economic ExposureExposure

We Export Washing Machine to We Export Washing Machine to Switzerland:Switzerland:

Our Price is GBP 200Our Price is GBP 200 At CHF 1.90 = GBP 1:At CHF 1.90 = GBP 1:

Our Price is CHF 380Our Price is CHF 380 German Competitor Sells at CHF German Competitor Sells at CHF

420420

Commercial / Economic Commercial / Economic ExposureExposure

Spot Rate Changes to CHF 2.25 Spot Rate Changes to CHF 2.25 =GBP 1=GBP 1

EUR / CHF Spot Rate UnchangedEUR / CHF Spot Rate Unchanged Our Price Changes to CHF 450Our Price Changes to CHF 450 German Co’s Price Still CHF 420German Co’s Price Still CHF 420

Internal TechniquesInternal Techniques

NettingNetting MatchingMatching Leading & Lagging BalancesLeading & Lagging Balances Determining Currency of InvoiceDetermining Currency of Invoice

NettingNetting Netting End of Period Balances:Netting End of Period Balances:

Same CurrencySame Currency Parallel CurrencyParallel Currency

Simple Example:Simple Example: A Owes B USD 10,000,000A Owes B USD 10,000,000 B owes A USD 8,000,000B owes A USD 8,000,000

Net Debt is from A to BNet Debt is from A to B Net Debt is USD 2,000,000Net Debt is USD 2,000,000

Real Life Examples much more Real Life Examples much more ComplicatedComplicated

Parallel CurrencyParallel Currency Currencies Closely Linked in their Market Currencies Closely Linked in their Market

PerformancePerformance 2 year Chart - Spot Rate Euro (EUR) v. Danish Krone 2 year Chart - Spot Rate Euro (EUR) v. Danish Krone

(DKK)(DKK)

MatchingMatching

Matching Inflows and Outflows Matching Inflows and Outflows of Same Currencyof Same Currency

Dates of Individual Receipts / Dates of Individual Receipts / Payments AlteredPayments Altered

Simple Example:Simple Example: A is due to Receive EUR 1,000,000 A is due to Receive EUR 1,000,000 on 25 JAN 10on 25 JAN 10

A is due to Pay EUR 1,000,000 on A is due to Pay EUR 1,000,000 on 05 FEB 1005 FEB 10

Leading and LaggingLeading and Lagging

Speeding Up (Leading) Speeding Up (Leading) Settlement of Receipt / PaymentSettlement of Receipt / Payment

Slowing Down (Lagging) Slowing Down (Lagging) Settlement of Receipt / PaymentSettlement of Receipt / Payment

Normally on Inter-Company Normally on Inter-Company Items:Items:

Can Also be on External Items Can Also be on External Items (Risky)(Risky)

Leading and LaggingLeading and Lagging

Useful in Countries with Volatile Useful in Countries with Volatile RatesRates

Some Governments Often Some Governments Often Impose Fixed Payment DatesImpose Fixed Payment Dates

Can also be used for Tax Can also be used for Tax Planning:Planning:

Shifting Revenues / CostsShifting Revenues / Costs

Leading and LaggingLeading and Lagging A (Co. in Ruritanian) has to pay 10 m. A (Co. in Ruritanian) has to pay 10 m.

Ruritanian Pesos (RUP) in one MonthRuritanian Pesos (RUP) in one Month Current Spot Rate RUP 10 = GBP 1Current Spot Rate RUP 10 = GBP 1 Current Value GBP 1,000,000Current Value GBP 1,000,000 Exp. 10% Devaluation of RUP within Exp. 10% Devaluation of RUP within

Month (New Rate RUP 11 = GBP 1)Month (New Rate RUP 11 = GBP 1) Expected Value GBP 909,090Expected Value GBP 909,090 Pay now (Lead) and Save GBP 90,910Pay now (Lead) and Save GBP 90,910

Determining Invoice CurrencyDetermining Invoice Currency

Do not Invoice in Weak Currency:Do not Invoice in Weak Currency: Use Strong CurrencyUse Strong Currency Prices in Russia Quoted in USD Prices in Russia Quoted in USD not Russian Roubles (RUR)not Russian Roubles (RUR)

Could Invoice in Strong Currency Could Invoice in Strong Currency to take Advantage of Currency to take Advantage of Currency GainsGains

External TechniquesExternal Techniques

Forward MarketsForward Markets Currency Futures MarketsCurrency Futures Markets Currency Options MarketsCurrency Options Markets Currency SwapsCurrency Swaps Factoring Foreign Debts:Factoring Foreign Debts:

Selling Invoice to Factor (Bank)Selling Invoice to Factor (Bank)

Back to ExposureBack to Exposure

A Company only has ONE net A Company only has ONE net Exposure per CurrencyExposure per Currency

Treasurer’s Job to Manage thisTreasurer’s Job to Manage this

Cost ControlCost Control

Use Internal Techniques Use Internal Techniques Whenever Possible:Whenever Possible:

Replace External TechniquesReplace External Techniques CheaperCheaper Offsets Cost of TreasurerOffsets Cost of Treasurer Contributes to ProfitContributes to Profit

Information FlowsInformation Flows

Treasurer Needs Information on:Treasurer Needs Information on: Cash Balances:Cash Balances:

In ALL CurrenciesIn ALL Currencies Cash Flows Through TradingCash Flows Through Trading Cash Requirements for Capital Cash Requirements for Capital ExpenditureExpenditure

Information Report CycleInformation Report Cycle

Some Information Needed Daily:Some Information Needed Daily: Cash BalancesCash Balances Cash ExpectedCash Expected Cash RequiredCash Required

Other Reporting Frequencies:Other Reporting Frequencies: Capital Expenditure RequirementsCapital Expenditure Requirements

Behavioural IssuesBehavioural Issues

Responsibility

ControlAccountability

Behavioural IssuesBehavioural Issues

Given Need for:Given Need for: ResponsibilityResponsibility AccountabilityAccountability ControlControl

How do you Exercise Central How do you Exercise Central Control ?Control ?

Behavioural IssuesBehavioural Issues

Answer - PersuasionAnswer - Persuasion Treasurer’s Rates Always BestTreasurer’s Rates Always Best Treasurer’s Costs Always LowestTreasurer’s Costs Always Lowest What is in Company’s Interest is What is in Company’s Interest is

also in Subsidiary’s Interestalso in Subsidiary’s Interest