The New Normal

ASC 20103 May 2010

Maria B. DwightGerontological Services, Inc.

Los Angeles, [email protected]

"Senior (military) officers say the power point program does come in handy when the goal is not imparting information, as in briefings for reporters.

The news media sessions often last 25 minutes, with 5 minutes left at the end for questions from anyone still awake. Those types of PowerPoint presentations are known as “hypnotizing chickens.”

- New York Times, April 26, 2010

An Aside

THE NEW NORMAL … MORE FUN THAN THE OLD NORMAL?

Are we having fun yet?

Are depression babies enjoying the double whammy?

Introduction:

The purpose of this day is to initiate conversation and dialogue around the post 2008 environment of California and its older population.

We will look at the multi-faceted issues and opportunities that will affect ASC members and their future viability and growth.

Are you going to be part of the problem or part of the solution?

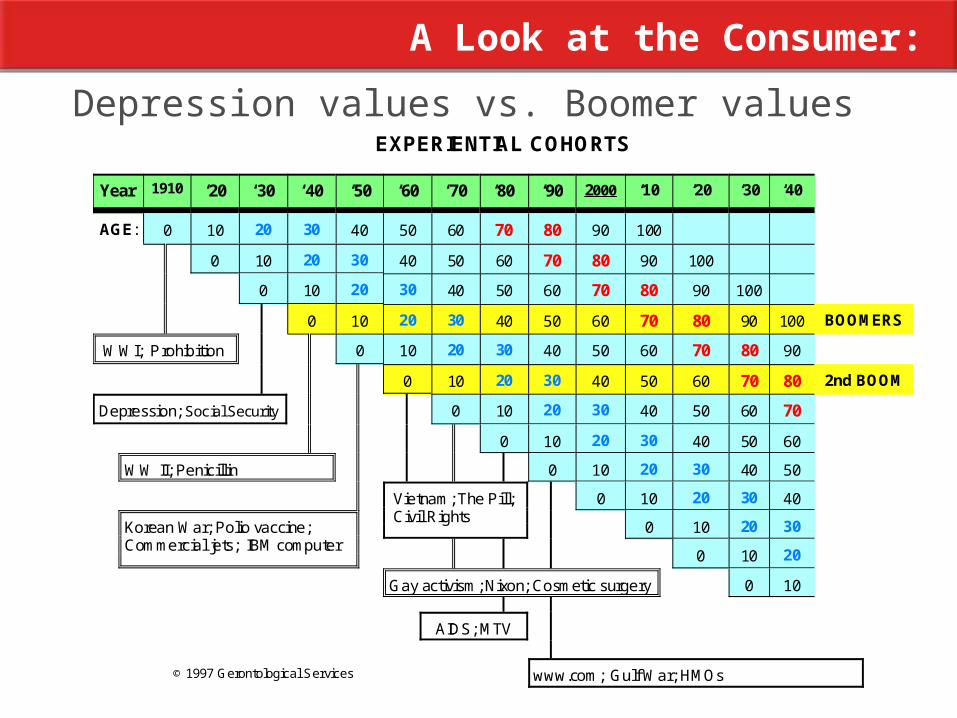

A Look at the Consumer:

Depression values vs. Boomer valuesEXPERIENTIAL COHORTS

Year 1910 ‘20 ‘30 ‘40 ‘50 ‘60 ‘70 ‘80 ‘90 2000 ‘10 ‘20 ‘30 ‘40

AGE: 0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100

0 10 20 30 40 50 60 70 80 90 100 BOOMERS

WWI; Prohibition 0 10 20 30 40 50 60 70 80 90

0 10 20 30 40 50 60 70 80 2nd BOOM

Depression; Social Security 0 10 20 30 40 50 60 70

0 10 20 30 40 50 60

WW II; Penicillin 0 10 20 30 40 50

Vietnam; The Pill; Civil Rights

0 10 20 30 40

Korean War; Polio vaccine;Commercial jets; IBM computer

0 10 20 30

0 10 20

Gay activism; Nixon; Cosmetic surgery 0 10

AIDS; MTV

© 1997 Gerontological Services www.com; Gulf War; HMOs

Drivers of the “new normal”

Value driven (quality and durability)

Experience instead of stuff

Vulnerability to income loss

Vulnerability to asset erosion

Wealth transfer to younger generations

Ratings of Types of Opportunities by AgeIn-Movers, Incomes $50K+

How important is it to you to have access to opportunities for:

Under Age 65

Ages 65-74 Ages 75+

Physical recreation

Very important 86% 79% 66%

Social recreation

Very important 78% 74% 65%

Intellectual growth

Very important 83% 75% 63%

Cultural recreation

Very important 80% 71% 58%

Volunteering

Very important 57% 46% 35%

Spiritual growth

Very important 51% 48% 37%

Depression demographic vs. Boomer demographics

Depression demographic vs. Boomer demographics

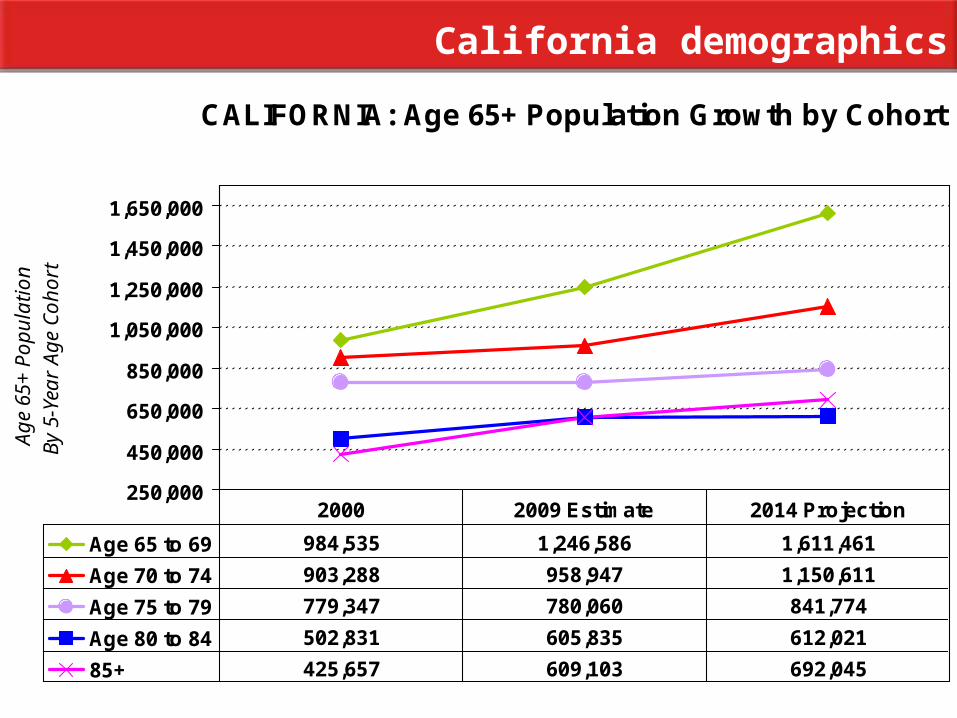

California demographics

CALIFORNIA: Age 65+ Population Growth by Cohort

250,000

450,000

650,000

850,000

1,050,000

1,250,000

1,450,000

1,650,000

Ag

e 6

5+

Po

pu

latio

nB

y 5

-Ye

ar

Ag

e C

oh

ort

Age 65 to 69 984,535 1,246,586 1,611,461

Age 70 to 74 903,288 958,947 1,150,611

Age 75 to 79 779,347 780,060 841,774

Age 80 to 84 502,831 605,835 612,021

85+ 425,657 609,103 692,045

2000 2009 Estimate 2014 Projection

Age 75+ Population Growth by State

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

Ag

e 7

5+

Po

pu

latio

n

2000 1,707,835 87,154 303,998

2009 Estimate 1,994,998 127,873 413,402

2014 Projection 2,145,840 155,802 468,885

California Nevada Arizona

California demographics

Age 75+ Population Annual Growth by State

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Ag

e 7

5+

Po

pu

latio

nA

nn

ua

l Gro

wth

2000 - 2009 1.90% 5.20% 4.00%

2009 - 2014 1.50% 4.40% 2.70%

California Nevada Arizona

California demographics

Age 75+ Higher Income Households by State*

0

50,000

100,000

150,000

200,000

250,000

Ag

e 7

5+

Ho

use

ho

lds

With

Hig

he

r In

com

es

2000 ($57K+) 215,007 9,154 31,286

2009 Esitmated ($75K+) 233,040 12,773 37,223

2014 Projected ($85K+) 234,456 14,547 40,473

California Nevada Arizona

* Adjusted dollars: assumes a consistent 2.8% annual increase in GDP from 2000 to 2014.

California demographics

Age 75+ Higher Income Households, % of Total*

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Ag

e 7

5+

Hig

he

r In

com

eH

ou

seh

old

s, %

of T

ota

l

2000 ($57K+) 20.5% 17.2% 16.0%

2009 Esitmated ($75K+) 20.0% 16.7% 14.4%

2014 Projected ($85K+) 19.2% 15.8% 13.8%

California Nevada Arizona

* Adjusted dollars: assumes a consistent 2.8% annual increase in GDP from 2000 to 2014.

California demographics

Age 75+ Population Growth in Selected Markets

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Ag

e 7

5+

Po

pu

latio

n

2000 35,860 16,641 34,882 50,288

2009 Estimate 41,420 18,523 41,396 56,904

2014 Projection 43,220 19,676 42,436 59,677

Alhambra Marin Oceanside San Francisco

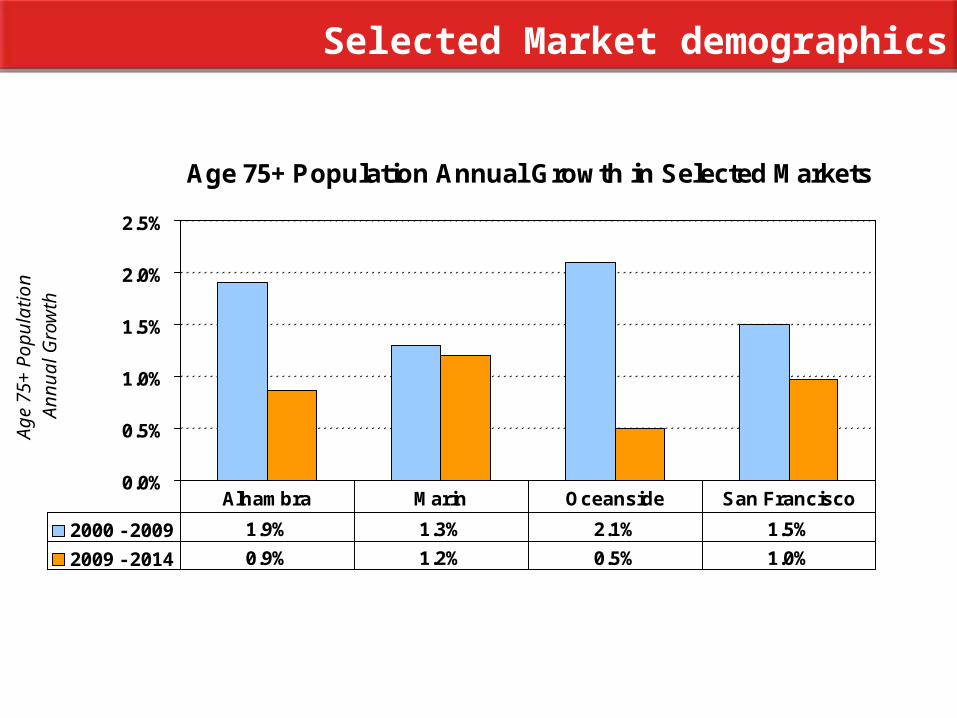

Selected Market demographics

Age 75+ Population Annual Growth in Selected Markets

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Ag

e 7

5+

Po

pu

latio

nA

nn

ua

l Gro

wth

2000 - 2009 1.9% 1.3% 2.1% 1.5%

2009 - 2014 0.9% 1.2% 0.5% 1.0%

Alhambra Marin Oceanside San Francisco

Selected Market demographics

Age 75+ Higher Income Households in Selected Markets*

0

2,000

4,000

6,000

8,000

10,000

Ag

e 7

5+

Ho

use

ho

lds

With

Hig

he

r In

com

es

2000 ($57K+) 3,339 3,449 5,078 8,075

2009 Esitmated ($75K+) 3,251 3,617 6,376 8,338

2014 Projected ($85K+) 2,997 3,753 6,139 8,591

Alhambra Marin Oceanside San Francisco

* Adjusted dollars: assumes a consistent 2.8% annual increase in GDP from 2000 to 2014.

Selected Market demographics

Age 75+ Higher Income Households, % of Total*

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Ag

e 7

5+

Hig

he

r In

com

eH

ou

seh

old

s, %

of T

ota

l

2000 ($57K+) 17.0% 31.7% 24.0% 25.5%

2009 Esitmated ($75K+) 15.4% 30.9% 24.5% 25.2%

2014 Projected ($85K+) 14.0% 30.5% 23.0% 25.3%

Alhambra Marin Oceanside San Francisco

* Adjusted dollars: assumes a consistent 2.8% annual increase in GDP from 2000 to 2014.

Selected Market demographics

Changing Ethnicity

Age 65+ Anglo Population Growth in Selected Markets

0

20,000

40,000

60,000

80,000

Ag

e 6

5+

An

glo

Po

pu

latio

n

2000 38,949 31,349 62,003 51,647

2009 Estimate 37,540 36,100 66,974 54,473

2014 Projection 39,079 40,999 74,113 61,489

Alhambra Marin Oceanside San Francisco

Age 65+ Anglo Pop. Annual Growth in Selected Markets

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Ag

e 6

5+

An

glo

Po

pu

latio

nA

nn

ua

l Gro

wth

2000 - 2009 -0.4% 1.7% 0.9% 0.6%

2009 - 2014 1.1% 2.7% 2.1% 2.6%

Alhambra Marin Oceanside San Francisco

Age 65+ Anglo Population as Percent of Total

0%

20%

40%

60%

80%

100%

Ag

e 6

5+

An

glo

Po

pu

latio

na

s P

erc

en

t of T

ota

l

2000 51% 94% 92% 50%

2009 Esitmated 44% 91% 88% 49%

2014 Projected 41% 89% 87% 49%

Alhambra Marin Oceanside San Francisco

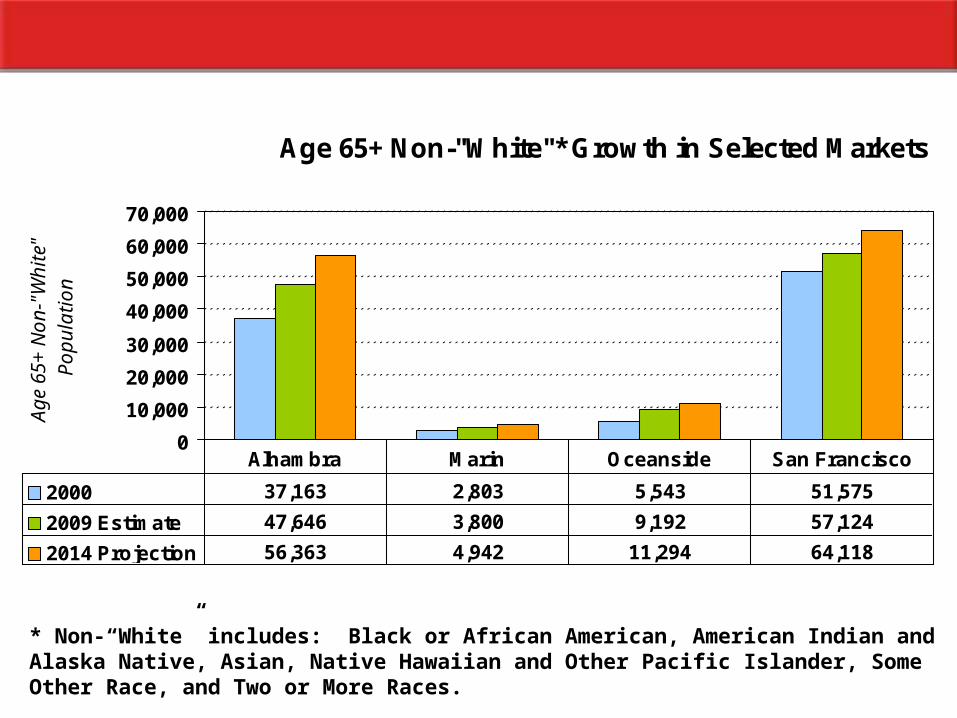

Age 65+ Non-"White"* Growth in Selected Markets

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Ag

e 6

5+

No

n-"

Wh

ite"

Po

pu

latio

n

2000 37,163 2,803 5,543 51,575

2009 Estimate 47,646 3,800 9,192 57,124

2014 Projection 56,363 4,942 11,294 64,118

Alhambra Marin Oceanside San Francisco

* Non-“White” includes: Black or African American, American Indian and Alaska Native, Asian, Native Hawaiian and Other Pacific Islander, Some Other Race, and Two or More Races.

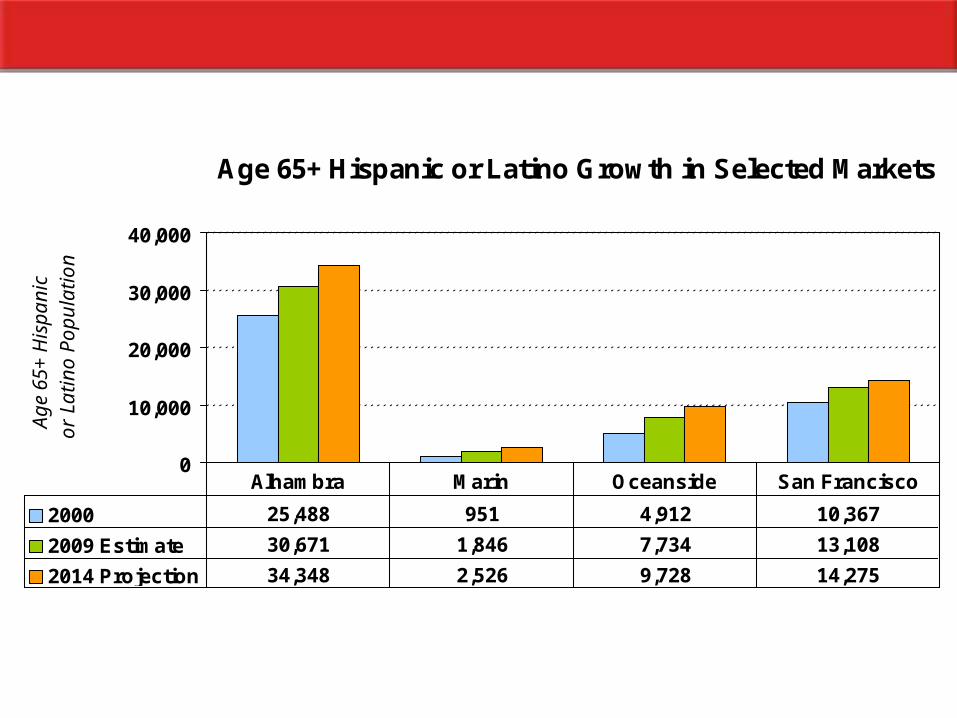

Age 65+ Hispanic or Latino Growth in Selected Markets

0

10,000

20,000

30,000

40,000

Ag

e 6

5+

His

pa

nic

or

La

tino

Po

pu

latio

n

2000 25,488 951 4,912 10,367

2009 Estimate 30,671 1,846 7,734 13,108

2014 Projection 34,348 2,526 9,728 14,275

Alhambra Marin Oceanside San Francisco

Age 65+ Non-"White"* Growth by State

0

500,000

1,000,000

1,500,000

2,000,000

Ag

e 6

5+

No

n-"

Wh

ite"

Po

pu

latio

n

2000 805,166 25,223 52,818

2009 Estimate 1,185,454 54,093 99,603

2014 Projection 1,470,447 79,755 130,844

California Nevada Arizona

* Non-“White” includes: Black or African American, American Indian and Alaska Native, Asian, Native Hawaiian and Other Pacific Islander, Some Other Race, and Two or More Races.

Age 65+ Hispanic or Latino Growth by State

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Ag

e 6

5+

His

pa

nic

or

La

tino

Po

pu

latio

n

2000 472,769 12,173 55,504

2009 Estimate 758,218 31,157 102,500

2014 Projection 964,113 48,209 136,919

California Nevada Arizona

Exciting Opportunities:

Niche marketsPent up demandAvailable and expanded professional pool

New productsNew locationsTechnology