INFORMATION

TECHNOLOGYINDUSTRY

�IN UKRAINE

IMPACT ON ECONOMY

GLOBAL IT MARKETS

IT CONSUMPTION

IT EXPORTS

UKRAINE MARKET

INFOGRAPHIC ATLAS / 2017

© Top Lead LLC. All rights reserved

INTRODUCTION

MEDIA

PRINTED MEDIA MOBILE DATA

FIXED DATA

HARDWARE

SOFTWARE

SERVICES FIXED VOICE

MOBILE VOICE

ТV

RADIO

DIGITAL COMMUNICATIONS

TELECOMIT

ТМТICTWHY WE CREATED THIS REPORT

Information technology (IT) is a tool for the development of a modern economy.IT is capable of accelerating economic development. It can play the same role today as steam engines, the discovery of electricity and the automation of production did in previous epochs.IT is a relatively new and complex industry. Despite its relatively recent appearance, the IT industry has already become the essence of a modern digital economy. It promotes the emergence of new products and services and adds value to existing offers.This report explores the nature of the IT industry and describesits impact on business and the economy. We will also look at the Ukrainian IT market and its place on the global map.

REPORT SCOPE

In traditional market analysis, IT is part of broader technology, media and telecommunications sector (TMT). In this report, we will focus solely on Information and Telecommunications Technology (ICT).It is important to distinguish between the IT industry and the telecommunications industry. We focus on the IT market, but we have not overlooked the telecommunications industry because it plays the same role as roads in the transport industry.In this edition of the report, we have decided not to include the media industry due to a lack of reliable sources and established methodology.

HOW IT MARKET IS ARRANGED

HOW TO READ THIS REPORT

We depicted the IT industry from both global and domestic markets point of view.The latter shows the cost of information technology (in this report, we use the term "IT consumption", based on IDC methodology).This report shows IT consumption in its entirety

or by segment: hardware, software, services.Since we take data on consumption, exports and outsourcing volumes from different sources (IDC, World Bank Group, KPMG), the information may vary in different infographics despite overlapping segmentation.This is due to different methodologies and understandings of the market.

In the first section, we explore information technology, but we show exports generally in terms of ICT due to the lack of specific data for the IT sector.

Report analytical partner: IDC

2

WHY THIS IS IMPORTANT

INDUSTRIAL REVOLUTIONS KEY FACTORS, INSTRUMENTS, CONSEQUENCES AND OPPORTUNITIES

What’s appeared Steam engineRailwaysMechanized productionTransport �

Industrial enterprisesElectric networksMass production of goods��

ElectronicsRobots on productionInformation Technology Industry

INDUSTRIAL CAPITALISM MASS PRODUCTION AUTOMATED MANUFACTURING DIGITAL ECONOMY

Steam energy Electricity Computers and code Information and data

Integral high-performance ecosystem of data collection, analysis and application

PRODUCTIONTOOL

CONVEYER CYBER-PHYSICAL SYSTEMS

0,95 1,3 2,5 6,1

1000 1500

1 2 9

GDP in $ according to PPPper capita (2011 prices)

GDP in $ trillion for PPP (2011 prices)

Key professional ENGINEER MANAGER PROGRAMMER CHIEF DIGITAL OFFICER

Impact of the technology

MAIN ASSET

KEY TECHNOLOGY

Population, billion

The speed of delivery of goodsEfficiency of production

Mass production of goods Automation of productionReduction of the cost of mass production

Increase in the value of intangible assets in relation to material assets

MACHINE COMPUTERS AND ELECTRONICS

MANUFACTURING FACILITIES BRAND INFORMATION

END OF XVIII CENTURY

SECOND HALF OF XIX CENTURY

MIDDLE OF THE XX CENTURY

THE BEGINNING OF THE XXI CENTURY

INDUSTRY 1.0 INDUSTRY 2.0 INDUSTRY 3.0 INDUSTRY 4.0GDP PER CAPITA

POPULATION

Over the past 200 years, the size of the world economy has increased in 110 times. At the same time, GDP per capita has grown only 14 times.

Technology is the primary factor driving economic growth.

The use of electricity created an industrial model for the economy. Computers have promoted the creation of a service economy. Data progress has caused the so-called Industrial Revolution 4.0 and serves as the basis of the digital economy.

SERVICES69%

INDUSTRIES27%

AGRICULTURE4%

3600 10300

63

WORLD GDP2016, $112 trillion for PPP

According to IDC and TOP LEAD. Indicators of economic status and population courtesy of World Bank

4

RESOURCES AND TERRITORY

DIGITAL ECONOMY TECHNOLOGIES KEY TECHNOLOGIES TO INFLUENCE ECONOMY

2018-2020 рр. — estimatedAccording to Atos 2016, CB Insights. 2018-2020 forecast

Advanced Data VisualizationBiometrics

Digital SignageNFC

2018 2019+201720162000

WebRTCIn-memory computingCloud Service Integration

Open Source HardwareIPv6

Insight PlatformsSemantic TechnologiesDeep Learning

Edge computingTrusted DevicesLPWAN

Fabric-Based ComputingVirtual AssistantsContext Broker

BlockchainWearable ComputingNatural User InterfasesWeb-scale computing

Artificial IntelligenceAutonomos VehiclesInternet of Everything3D Printing

Distributed Social NetworksWireless PowerPlastic TransistorsLocation-Based Services NG

Ubiquitous PIM

Self-Adaptive SecurityPrivacy-Enhancing TechnologiesImmercive ExperienceSDx

BiocomputerSwarm Computing5GMemristorsExascale

Smart MachinesAdvanced RoboticsBrain-Computer InterfaseGenetic Engineering

LOW

AVERAGE

LEVEL OF INFLUENCE ON THE ECONOMY

HIGH

ECONOMIC TRANSFORMATION

The digital economy is characterized by a large number of new technologies that increase efficiency by introducing new business models and creating new markets.

This visualization shows the technologies that will have the greatest impact on the economy of the future.

The ranking indicates the level of potential impact on the economy - from minimal to an impact that transforms individual markets and the economy as a whole.

A digital economy is an economy in which virtual (non-physical) assets and transactions have the greatest value.

5

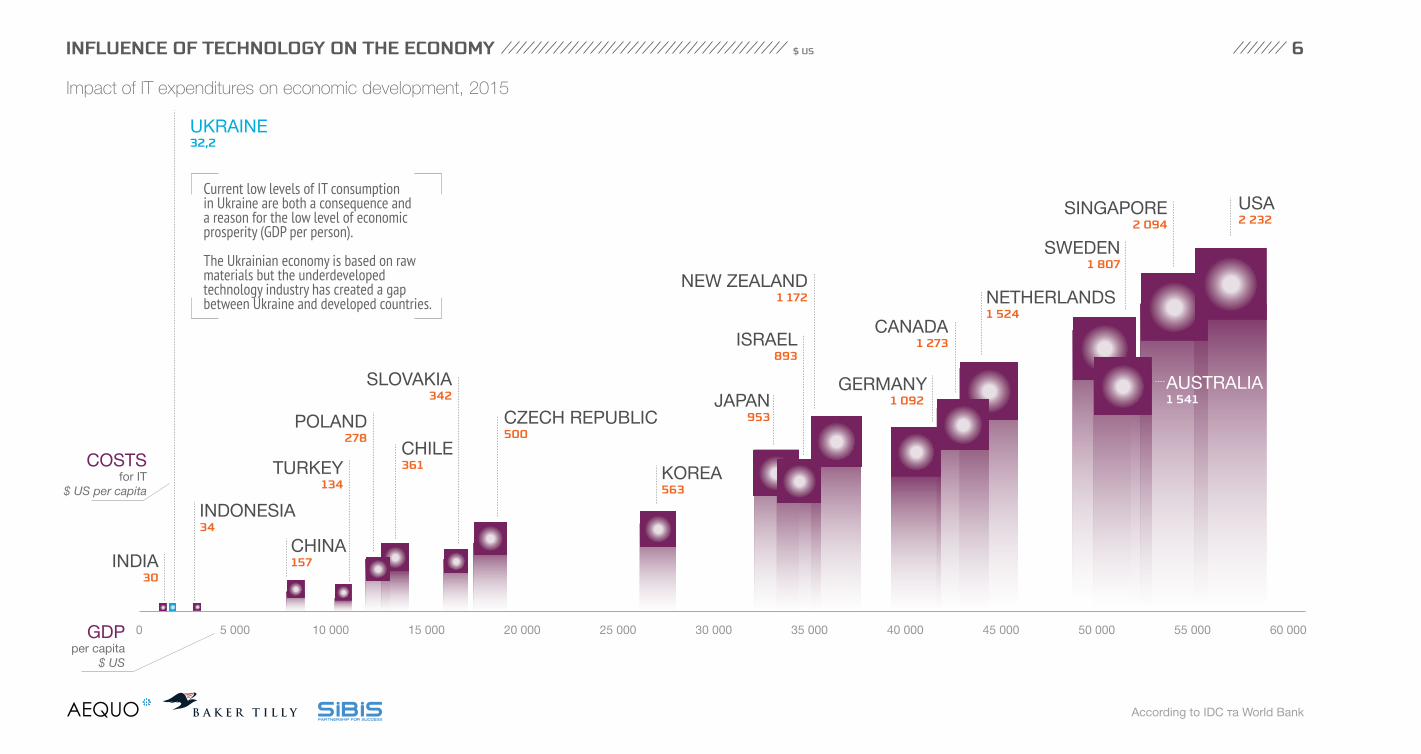

INFLUENCE OF TECHNOLOGY ON THE ECONOMY $ US 6

0 5 000 10 000 15 000 20 000 25 000 30 000 35 000 40 000 45 000 50 000 55 000 60 000

Current low levels of IT consumption in Ukraine are both a consequence and a reason for the low level of economic prosperity (GDP per person).

The Ukrainian economy is based on rawmaterials but the underdeveloped technology industry has created a gap between Ukraine and developed countries.

GDPper capita

$ US

UKRAINE32,2

CHILE361

INDONESIA34

CHINA157

SLOVAKIA342

POLAND278

INDIA30

TURKEY134

COSTSfor ІТ

$ US per capita

According to IDC та World Bank

SINGAPORE2 094

USA2 232

SWEDEN1 807

CANADA1 273

NEW ZEALAND1 172

ISRAEL893

JAPAN953CZECH REPUBLIC

500

GERMANY1 092

AUSTRALIA1 541

NETHERLANDS1 524

KOREA563

Impact of IT expenditures on economic development, 2015

ІТ GLOBAL IT MARKET

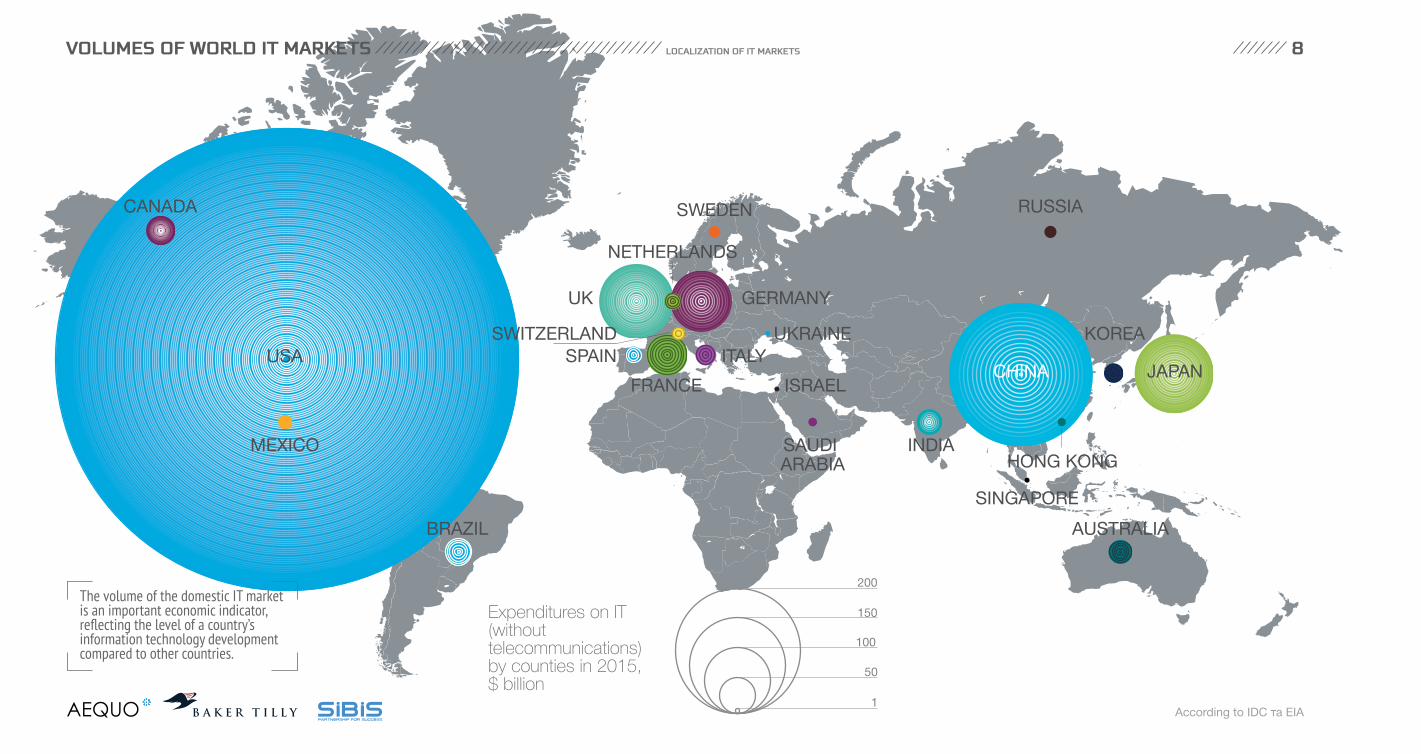

VOLUMES OF WORLD IT MARKETS 8

According to IDC та EIA

LOCALIZATION OF IT MARKETS

USA

MEXICO

CHINA

HONG KONG

SINGAPORE

RUSSIASWEDEN

UK

CANADA

BRAZIL

INDIASAUDI ARABIA

ISRAEL

AUSTRALIA

GERMANY

NETHERLANDS

FRANCE

ITALYSWITZERLAND UKRAINE

SPAINKOREA

JAPAN

Expenditures on IT (without telecommunications) by counties in 2015, $ billion

The volume of the domestic IT marketis an important economic indicator, reflecting the level of a country’s information technology development compared to other countries.

200

150

100

50

1

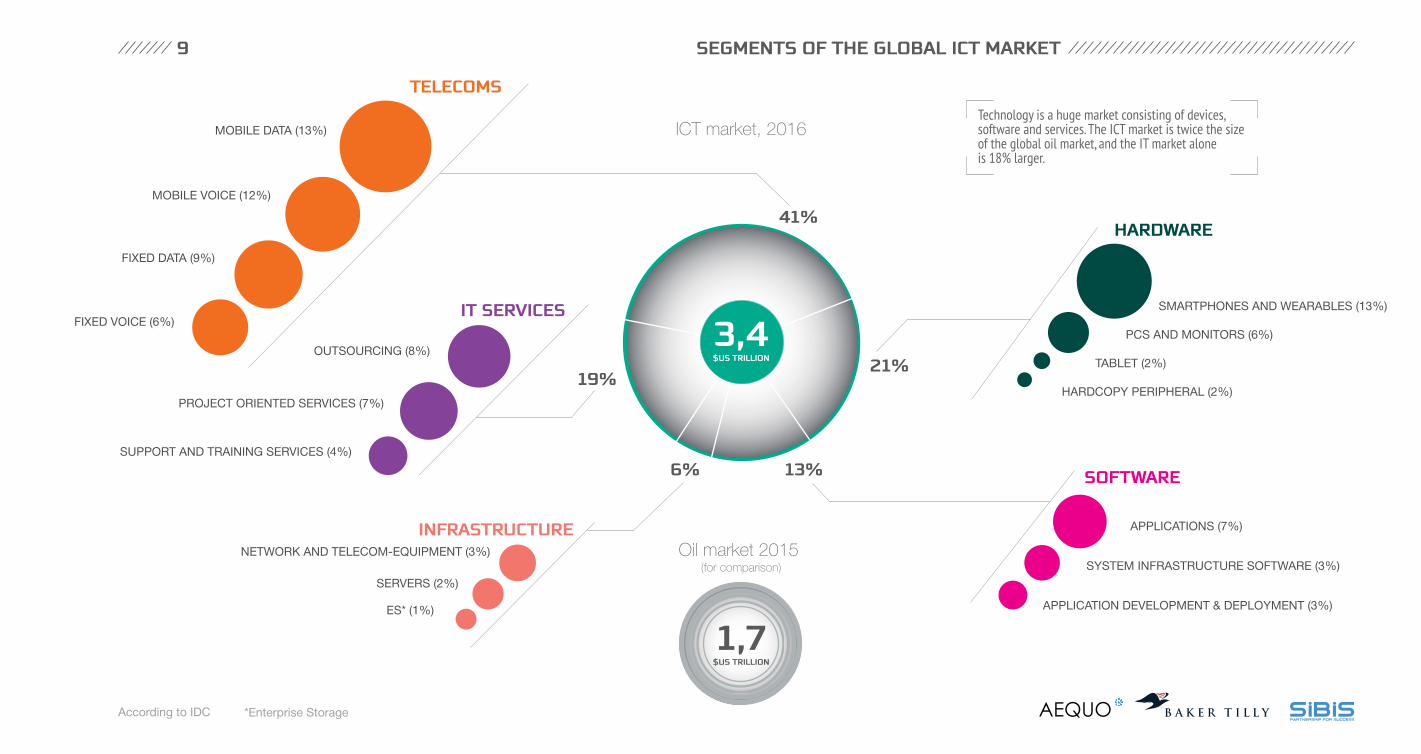

9 SEGMENTS OF THE GLOBAL ICT MARKET

41%

21%

6% 13%

19%

ІТ SERVICES

TELECOMS

HARDWARE

SOFTWARE

INFRASTRUCTURE

MOBILE DATA (13%)

MOBILE VOICE (12%)

FIXED DATA (9%)

FIXED VOICE (6%)

OUTSOURCING (8%)

PROJECT ORIENTED SERVICES (7%)

SUPPORT AND TRAINING SERVICES (4%)

NETWORK AND TELECOM-EQUIPMENT (3%)

SERVERS (2%)

ES* (1%)

SMARTPHONES AND WEARABLES (13%)

PCS AND MONITORS (6%)

TABLET (2%)

HARDCOPY PERIPHERAL (2%)

APPLICATIONS (7%)

SYSTEM INFRASTRUCTURE SOFTWARE (3%)

APPLICATION DEVELOPMENT & DEPLOYMENT (3%)

3,4$US TRILLION

Technology is a huge market consisting of devices, software and services. The ICT market is twice the size of the global oil market, and the IT market alone is 18% larger.

1,7$US TRILLION

Oil market 2015 (for comparison)

ICT market, 2016

*Enterprise Storage According to IDC

UKRAINIAN IT MARKET EXPORTS

ICT SERVICES EXPORTS11

114GERMANY

3,1MOROCCO

0,01LESOTHO

98,1FRANCE

177,8USA

№21 №32 №33 №34 №73

№1 №2 №3 №4 №5

16,3POLAND

3,9COSTA RICA

3,2UKRAINE*

105,1INDIA**

125UK

$ US BILLION

Ukraine in comparison with other countries of the world, $ US billion, 2016

PLACE IN THE WORLD

** information for 2015* Source mobilunity.comAccording to World Bank

12

Dynamics of ICT exports from Ukraine,$ US billion

The structure of IT services exports from Ukraine

19951994 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

0,5 0,4 0,5 0,6 0,3 0,4 0,4 0,3 0,4 0,5 0,7 0,81,1

1,72,3 2,1

3,23,8

4,35,0

4,53,9

3,2

According to World Bank * Source mobilunity.com

UKRINIAN ICT SERVICES EXPORTS

80% of Ukrainian IT exports are to USA

Ukraine is a relatively small player in the IT export market (IT + Telecom).For example, the volume of Polish ICT exports is 5 times higher than Ukrainian.

31% - ICT EXPORT SHAREIN THE EXPORT SERVICES SECTOR IN 2015

EXPORT OF OTHER SERVICES

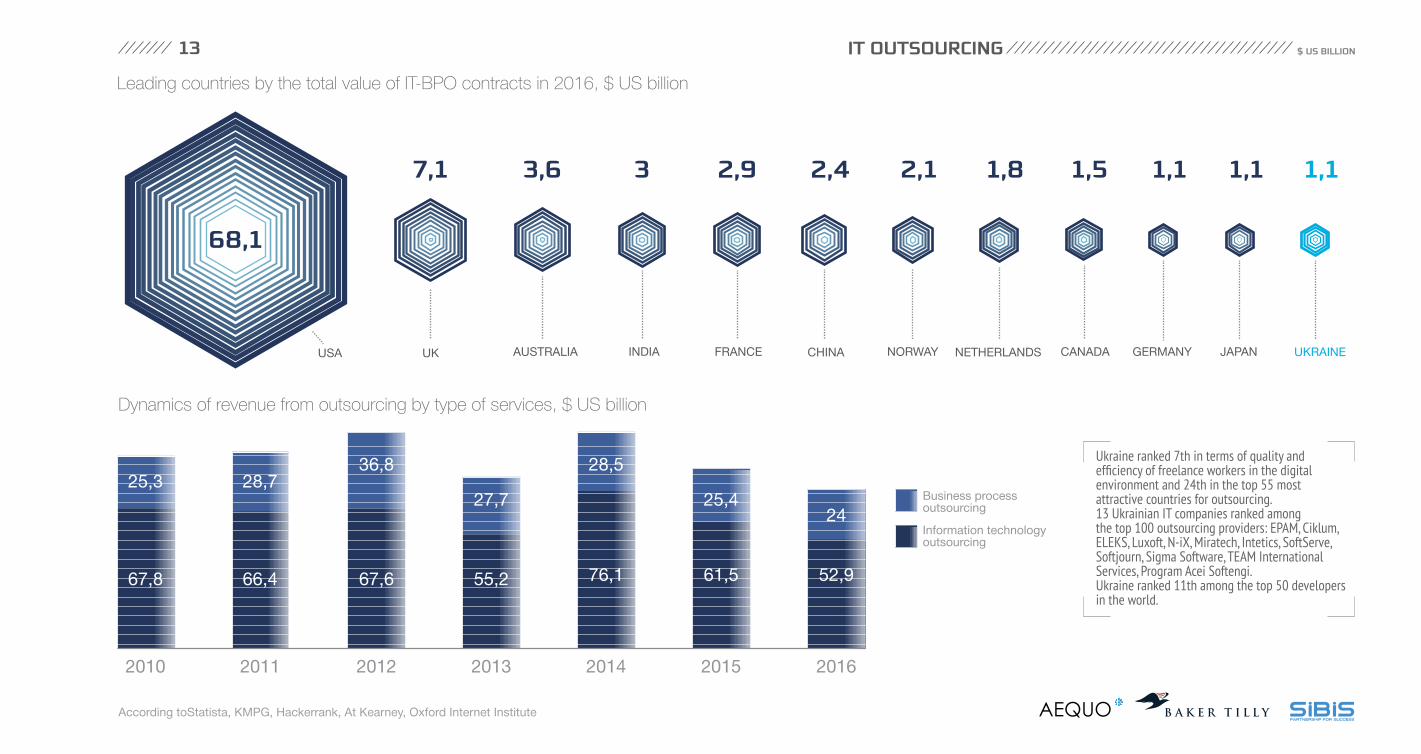

IT OUTSOURCING

13

According toStatista, KMPG, Hackerrank, At Kearney, Oxford Internet Institute

Leading countries by the total value of IT-BPO contracts in 2016, $ US billion

68,1

2,1

NORWAY

1,8

NETHERLANDS

1,5

CANADA

1,1

GERMANY

1,1

UKRAINE

1,1

JAPAN

7,1 3,6

AUSTRALIA

3

INDIA

2,9

FRANCE

2,4

CHINAUSA UK

Ukraine ranked 7th in terms of quality and efficiency of freelance workers in the digital environment and 24th in the top 55 most attractive countries for outsourcing.13 Ukrainian IT companies ranked among the top 100 outsourcing providers: EPAM, Ciklum, ELEKS, Luxoft, N-iX, Miratech, Intetics, SoftServe, Softjourn, Sigma Software, TEAM International Services, Program Acei Softengi.Ukraine ranked 11th among the top 50 developersin the world.

Dynamics of revenue from outsourcing by type of services, $ US billion

$ US BILLION

25,3

67,8 66,4 67,6 55,2 76,1 61,5 52,9

28,736,8 28,5

25,424

27,7

2010 2011 2012 2013 2014 2015 2016

Information technology outsourcing

Business processoutsourcing

DOMESTIC IT MARKETS

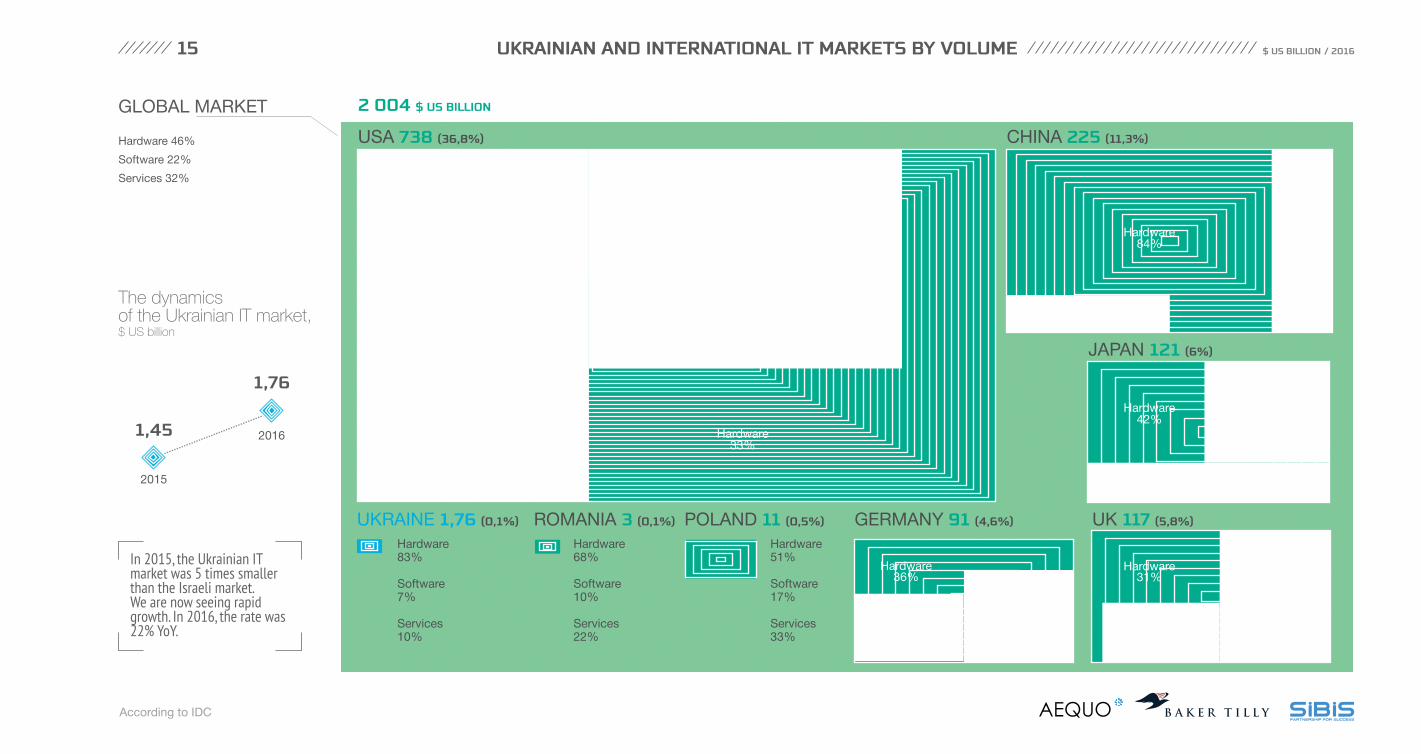

UKRAINIAN AND INTERNATIONAL IT MARKETS BY VOLUME 15 $ US BILLION / 2016

According to IDC

Hardware 46%

Software 22%

Services 32%

GLOBAL MARKET

UKRAINE 1,76 (0,1%)

Hardware33%

Software31%

Services36%

CHINA 225 (11,3%)

Hardware84%

Software6%

Services11%

GERMANY 91 (4,6%)

Hardware36%

Software27%

Services37%

POLAND 11 (0,5%)

Hardware51%

Software17%

Services33%

Hardware68%

Software10%

Services22%

Hardware83%

Software7%

Services10%

ROMANIA 3 (0,1%)

USA 738 (36,8%)

2 004 $ US BILLION

Hardware31%

Software22%

Services46%

UK 117 (5,8%)

Hardware42%

Software20%

Services38%

JAPAN 121 (6%)

2016

2015

1,45

1,76

The dynamics of the Ukrainian IT market, $ US billion

In 2015, the Ukrainian IT market was 5 times smallerthan the Israeli market. We are now seeing rapid growth. In 2016, the rate was22% YoY.

UKRAINE ON THE GLOBAL HARDWARE MARKET $ US BILLION

2006 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018 2019 20202007 2008

....

....

....

....

....

....

....

..

3,4

1,9

3,3

3,5 3,4 3,5

2,0

1,2

1,5

1,7 1,7 1,8

1,84,24,5

647761

927 994

....

....

....

....

....

....

....

..

GLOBALMARKET

$ US billion

UKRAINIANMARKET

$ US billion

DYNAMICSof the Ukrainian

hardware market$ US billion

16

Hawdware is the largest part of Ukrainian IT imports, but its volume is barely noticeable on the global scale.

According to IDC * evaluation 2018-2020 рр. — forecast

(selected years)

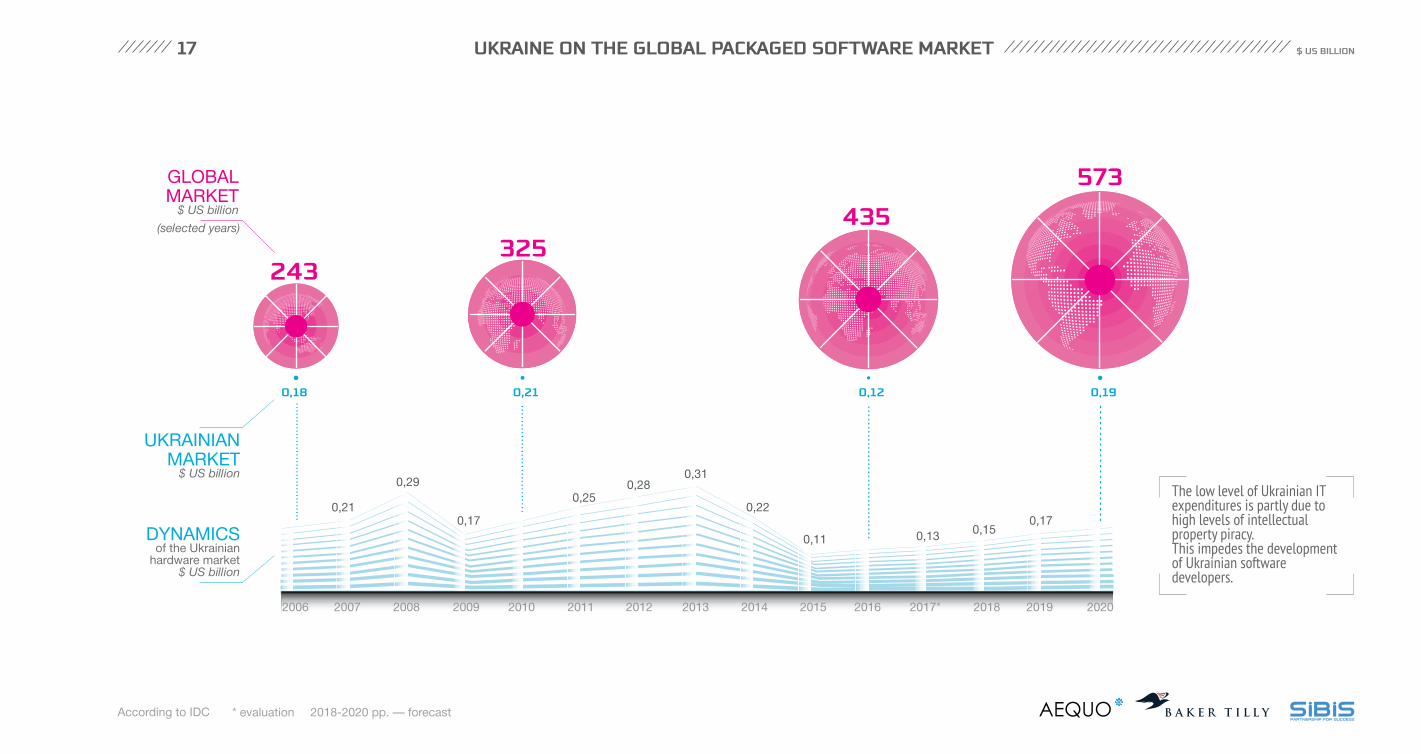

UKRAINE ON THE GLOBAL PACKAGED SOFTWARE MARKET $ US BILLION

2006 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018 2019 20202007 2008

......

......

......

......

......

.....

....

....

....

....

....

....

....

.

.................................

......................

243325

435

573

0,18

0,21

0,29

0,17

0,21

0,250,28

0,31

0,22

0,12

0,13 0,150,17

0,19

GLOBALMARKET

$ US billion

UKRAINIANMARKET

$ US billion

DYNAMICSof the Ukrainian

hardware market$ US billion

The low level of Ukrainian IT expenditures is partly due to high levels of intellectual property piracy.This impedes the development of Ukrainian software developers.

0,11

(selected years)

17

2018-2020 рр. — forecast* evaluationAccording to IDC

2018-2020 рр. — forecast

18

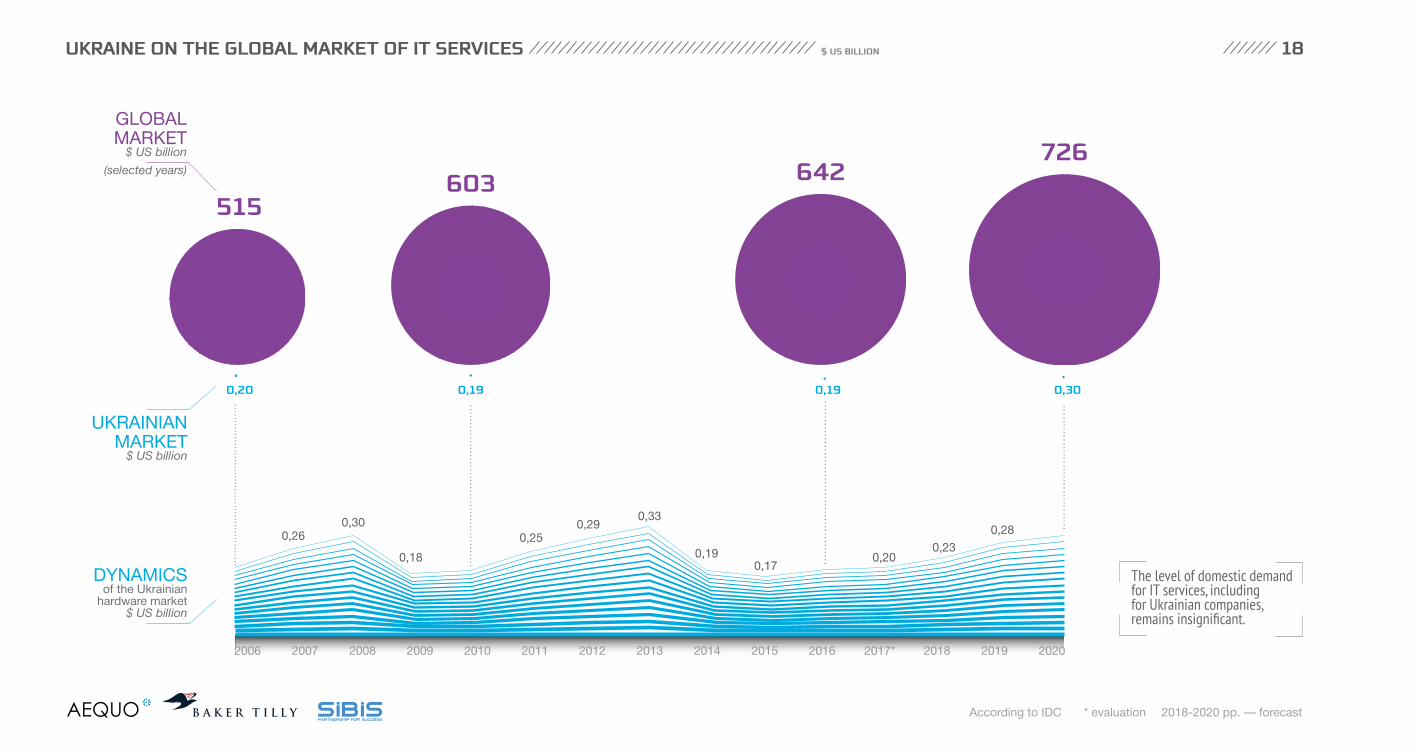

According to IDC * evaluation

The level of domestic demandfor IT services, including for Ukrainian companies, remains insignificant.

UKRAINE ON THE GLOBAL MARKET OF IT SERVICES $ US BILLION

2006 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018 2019 20202007 2008

....

....

....

....

....

....

....

....

....

....

....

....

..

....

....

....

....

....

....

....

....

....

....

....

..

....

....

....

....

....

....

....

....

....

....

....

.

....

....

....

....

....

....

....

....

..

515603 642

726

0,20

0,18

0,19

0,250,29

0,33

0,190,17

0,19

0,200,23

0,28

0,30

0,260,30

GLOBALMARKET

$ US billion

(selected years)

UKRAINIANMARKET

$ US billion

DYNAMICSof the Ukrainian

hardware market$ US billion

DOMESTIC IT MARKETS

Bankingand Financial

Sector9%

Government and education49%

Communications (telecoms)-23%

Others34%

Services (incl. for business)10%

Process Manufacturing(including metallurgy, food

and chemical industry)-4%

Retail and Wholesale-10%

Transportation101%

Discrete Manufacturing (including engineering, electronics, automotive, aircraft construction and shipbuilding)14%Utilities1%

INDUSTRY SHARE OF IT CONSUMPTION AS %

35% 16%

12% 11%

7%6% 6%

3%

3%

2%

Telecom Services

Hardware

Services

Packaged software

1,85

1,46

0,19

0,12

The volume of the Ukrainian ICT market in 2016, $ US billion Structure of IT consumption by industry in Ukraine, 2016

According to IDC

The financial and public sectors are the largest consumers of technologies in Ukraine.

%, DYNAMICS COMPARINGTO THE PREVIOUS YEAR

19

IT MARKET SHARE BY REGION

REGIONAL SHARE OF IT CONSUMPTION

8%

3%6%

6%

6%

5%

5%

4%3%

3%

3%

3%

3%

3%

3%

3%2%

2%2%

2%

2%

2%

2%

2%

17%Kyiv

20

According to IDC

The largest consumers of IT services on the domestic market are the largest industrial regions of Ukraine.

Regional share of IT consumption in b2c segment, %

n.a.17 8 6 5 4 3 2

TELECOM

UKRAINE ON THE GLOBAL TELECOM SERVICES MARKET $ US BILLION

......

......

......

......

......

......

......

....

....

....

....

....

....

....

....

....

....

....

....

....

....

....

...

......

......

......

......

......

......

......

......

......

......

.....

2006 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018 2019 20202007 2008

4,24,4

4,8

3,1

3,8 3,8 3,8

2,8

1,7 1,9 2,1 2,3

3,2 1,9 2,5

1431 1367 1420

1118

22

Due to the fall of the hryvniaand the reduction of tariffs, the profits of Ukrainian telecom operators dropped by around 50% whilethe number of users increased.

GLOBALMARKET

$ US billion

(selected years)

UKRAINIANMARKET

$ US billion

DYNAMICSof the Ukrainian

hardware market$ US billion

2018-2020 рр. — forecastAccording to IDC * evaluation

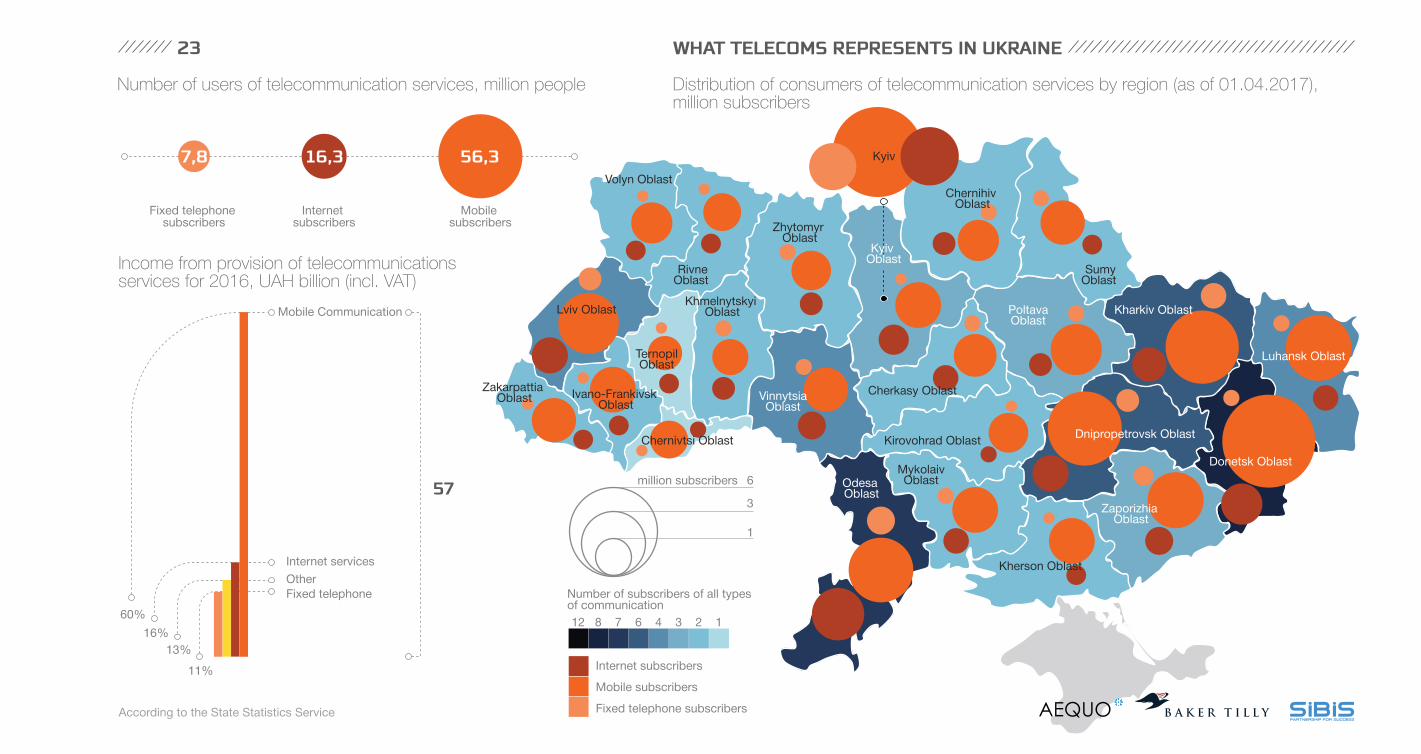

WHAT TELECOMS REPRESENTS IN UKRAINE23

60%

16%

13%

11%

Mobile Communication

Mobile subscribers

Mobile subscribers

Internet subscribers

Internet subscribers

Fixed telephone subscribers

Fixed telephone subscribers

Internet services

OtherFixed telephone

57

Одеська

Number of users of telecommunication services, million people Distribution of consumers of telecommunication services by region (as of 01.04.2017), million subscribers

Income from provision of telecommunications services for 2016, UAH billion (incl. VAT)

7,8 16,3 56,3

3

6million subscribers

Number of subscribers of all types of communication

1

12 8 7 6 4 3 2 1

Vinnytsia Oblast

Zhytomyr Oblast

Zaporizhia Oblast

Kirovohrad Oblast

Mykolaiv Oblast Odesa

Oblast

PoltavaOblast

Rivne Oblast

Kharkiv Oblast

Kherson Oblast

Khmelnytskyi Oblast

Chernihiv Oblast

Donetsk Oblast

Luhansk Oblast

Volyn Oblast

Lviv Oblast

Ternopil Oblast

Ivano-Frankivsk Oblast

Zakarpattia Oblast

Chernivtsi Oblast Dnipropetrovsk Oblast

Sumy Oblast

Cherkasy Oblast

Kyiv Oblast

Kyiv

According to the State Statistics Service

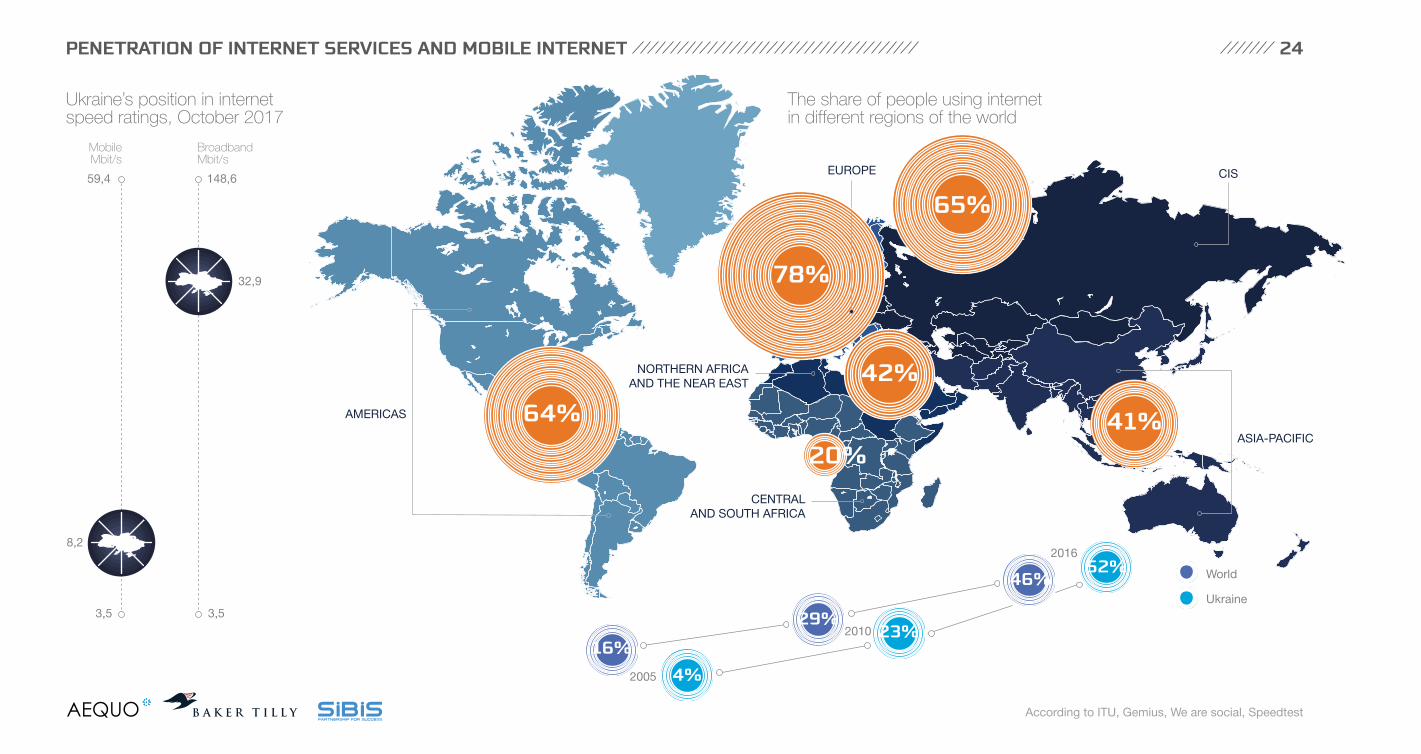

PENETRATION OF INTERNET SERVICES AND MOBILE INTERNET 24

The share of people using internet in different regions of the world

16%4%

29%23%

46%52%

2005

2010

2016

Ukraine

World

64%

78%

20%

42%

41%

65%

3,5

8,2

59,4

110

3,5

32,9

148,6

42

Ukraine’s position in internet speed ratings, October 2017

MobileMbit/s

BroadbandMbit/s

AMERICAS

CENTRALAND SOUTH AFRICA

EUROPE CIS

ASIA-PACIFIC

NORTHERN AFRICAAND THE NEAR EAST

According to ITU, Gemius, We are social, Speedtest

HOW TECHNOLOGIES IMPACT BUSINESS

IMPACT OF TECHNOLOGY ON BUSINESS

Exxon Mobil

General Electric

Citigroup

BP

Apple

Alphabet

Microsoft

Amazon

Technology has changed the market of space launches, market share by companies %

Financial result of the digital transformation

of companies, $ US billion

Sea Launch

Japan

China

Russia

Europe

Other U.S.

SpaceX

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%2010 2011 2012 2013 2014 2015 2016 2017 2018

The use of information technology enabled SpaceX to increase the efficiency of space launches and significantly reduce costs, allowing it to become the market leader within several years and take market share from Russia.

IT companies have overtaken traditional mining and productionsectors and consistently demonstratethe highest financial indicatorsgrowth rates.

According to Fortune, Forbes, Financial Times, PWC, IDC

752

580

508

427

343

261

166

114

363

372

239

233

53

81

281

20

2005 2016

3646

19

17

17

25

22

1 2

0,2

8

9

15

1

0,4

12CAPITALIZATION

NET INCOME

26

SECOND PLATFORM THIRD PLATFORM FOURTH PLATFORM

ТРЕТЯ ПЛАТФОРМА

According to IDC

Low compatibility of systems. Expensive equipment and proprietary software. Minimal opportunities for process automation. Low level of utilization of resources. High dependence on suppliers and vendors. Expensive and poor-quality communication services. Lack of IT development strategy and metrics to assesstheir effectiveness.

Development of system interfaces. Expanding the range of available IT solutions, reducing dependence on vendors.Distribution of automation at different levels.

Improvement of infrastructure utilization, including by means of virtualization and deployment of cloud services.Widespread distribution of available telecommunicationservices, including for mobile users. Binding IT Development Strategy to other business tasks.

Seamless integration of systems. Ability to create any solution in the XaaS / PAYG model.End-to-end automation of processes.High level of utilization of resources.Connectivity combines assets, devices, data and users into a single ecosystem. An unprecedented level of competition and globalization of markets. The DX strategy becomes a prerequisite for survival.

DX means building business around systems and business tools –this is the ability to create competitive services and products in the digital economy. From a technological point of view, the main driver of DX is the ecosystem of the "third platform".

The digital transformation of a business (DX) is the transformation of the company's activities to ensure its efficiency and competitiveness in the digital economy.

The third platform - the stage of the development of information technology, where infrastructure becomes centralized - through the creation of cloud platforms and data centers. The main components of the third platform are mobility (mobile users), big data, social platforms (networks) and cloud technologies.

IT IS SEPARATED FROM BUSINESS PROCESSES2000

IT INTEGRATED INTO BUSINESS PROCESSES2010

IT AND BUSINESS ARE INSEPARABLE2020

DIGITAL TRANSFORMATION: STAGES OF IMPLEMENTATION OF IT IN BUSINESS ACCORDING TO IDC PLATFORMS’ METHODOLOGY 27

THE FUTURE OF DIGITAL TRANSFORMATION

According to IDC

By 2018, half of all major companies will have already earned revenue from DaaS (data as a service), selling raw data, statistics and insights.

During 2018, half of the governments in the world will postpone or cancel implementation of e-gov solutions, such as e-voting platforms, due to risks associated with cyber attacks.

By 2019, ML, AI, and Cognitive will have the highest growth rates in the software development industry.

By 2019, P2P transactions from mobile devices will reach $ 6 trillion.

More than half of the executives of the SMB segment in 2019 will be from the millennials generation.

In 2019, expenditures on digital transformation (DX) in the world will be $1.7 trillion - 42% more than in 2017.

By 2020, the first wave of cyborgization of mankind will begin - systems and products associated with the third platform can be incorporated into the human body.

By 2020, every fifth company entrusts the creation of new content, such as presentations and reports, to machine learning platforms.

In 2020, 60% of CIO will be switched from IT to digital products.

By 2021, 20% of data from sources on open networks will be registered on a public blockchain. corresponding APIs will make that data more accessible and reliable.

At Least 15% of businesses' standard customer experience decisions will be handled by algorithms.

70% of digital advertising and marketing will be augmented or automated using artificial intelligence and machine learning.

90% of organizations will be incorporating cognitive/AI and machine learning into new enterprise apps.

By 2019, 35% of all enterprise applications users in the CEE region will have access to intelligent virtual assistants.

By 2019, AI will handle up to 70% of routine software development.

By 2019, 20% of all corporate mobile applications will have built-in augmented reality (AR) support.

More than 700 EB of unique data will be available in industry clouds for subscriber companies. This is 2.5 times higher than today.

By 2020, half of all new productive assets will be self-sustaining - independently tracking their condition while diagnosing and correcting possible crashes and breakdowns.

In 2020, 90% of organizations and companies will use several cloud platforms at once while more than a third of customers will implement integration and synchronization tools for multi-cloud ecosystem.

Three-quarters of companies will implement cloud-based strategies to support DX infrastructure allowing access to the benefits of the "API economy".

Every month, 180 million people around the world will watch 12 billion hours of virtual reality video.

By 2021, at least 50% of Global GDP will be digitized.

By 2021, 30% of online transactions in CEE region will use biometric authentication.

By 2021, 25% of the world's personal data will be compromised and housed in a data lake analyzed and utilized by consortiums of threat actors.

The use of robotic process automation enhanced by aI capabilities to automate business processes will grow threefold by 2021.

2018 2019 2020 2021

28

PROCESS OF DIGITAL TRANSFORMATION OF BUSINESS

Economic and technical indicators,as well as market trends, confirm: the world has moved to the stage of digital transformation.

The cost of material products,including high-tech, is rapidly decreasing."Virtual" values are increasingly important.

The application of new solutions is noticeable throughout the world, while most highly specialized professions are not able to track the impact of everything that is happening in the overall picture.

The Fourth Industrial Revolution redefines key professions, assets, competitive advantages and opportunities. And its consequences are manifested in all aspects of our lives.

Business and technology are increasingly inseparable. A new reality is rapidly forming while most companies are hopelessly backward.

The transformation trigger was the formation of the ecosystem of new technologies.

11

109

8

7

6

543

21

KPIs and approaches to doing business have changed. The Product Creation Chain and interaction with the market differ significantly from the approaches favored in previous times.

Dependence of "everything from everything". The rapid expansion of the "coverage area" by the technologies of communication, gathering and analysis of data has already plunged us into the "digital universe".

The service model incorporates everything. Customers are no longer buying a "box", which after hard and expensive setting will help them in their work. They expect a ready-made service (model PAYG), which they need here and now.

Everything is determined entirely by the level of understanding and limited by the imagination. Any tools necessary for the implementation of any idea are already available. The only question is how to combine them to get what you need.

Cargo-cults will not work. It makes no sense to blindly imitate and create dummies very similar to popular solutions. A reed crate is not a Boeing competitor.

29

According to IDC

Industry 4.0 involves the active useof big data for forecasting, management and automation, usingthe Internet of things and platformsof artificial intelligence. Service platforms (on which the customer pays only for services, not for the tools that provide them) and cyber-physics systems (CPS) in production, which combine physical assets and information systems, are crucial.

To be ready for the transition to a digital economy, businesses need to be substantially reformed. This means increasing the efficiency and innovation of a business to achieve digital transformation.

DXSTARTS

ECOSYSTEMEMERGES

VIRTUALVALUES

NEWSOLUTIONS CHANGES

ARE EVERYWHERE

NEWKPIS

COPY/PASTE DOES NOT

WORK

DIGITALWORLD

EVERYTHING IS SERVICE

KNOWLEDGE ECONOMY

THINGS CHANGE FAST

According to AEQUO

1. INITIALSTAGE

A. START OF NEGOTIATIONS between the seller and buyers;

B. DRAFTING a non-disclosure agreement,

exclusivity agreement, memorandum of understanding

A. SECURING PERMISSIONS from state bodies (merger clearance);

B. ADVANCE BANK PAYMENT;C. EXECUTION

of other conditions.

3. EXECUTION OF PURCHASE CONTRACT

A. EXECUTION OF SELLER'S NON-COMPETE ARRANGEMENTS;

B. EXECUTION OF ADDITIONAL PAYMENTS WITH

THE SELLER.

5. EXECUTION OF ADDITIONAL OBLIGATIONS

AFTER CLOSING (IF APPLICABLE)

A. LEGAL AUDIT: І. Confirmation of ownership of the object of the deal and verification of existing encumbrances; ІІ. Verification of the availability of all regulatory documents (in particular, license in the field of

telecommunications for telecommunications companies, registration of the operator, telecommuni-cations provider, availability of the license of the provider of the software service, etc.);

ІІІ. Checking the proper registration of relations with the developers of IT products (business entities or hired workers) and transfer of rights to them;

IV. Checking for rights to distribute copyright objects;B. TECHNICAL AUDIT:

І. . revision of the technical condition of the telecommunications network (for telecommunications companies), verification of assets

on the company's balance sheet; ІІ. Revision of IT products (for IT companies).

2. DUE DILIGENCE TO DETERMINE POSSIBLE RISKS

FOR NEW OWNER

4. ACQUISITION OF THE RIGHTS TO AN ASSET

A. EXECUTION OF PAYMENTS;B. TRANSFER OF TITLE

TO THE BUYER; C. APPOINTMENT OF NEW MANAGEMENT.

MAIN STAGES OF M&A TRANSACTIONS IN THE TMT SECTOR 30

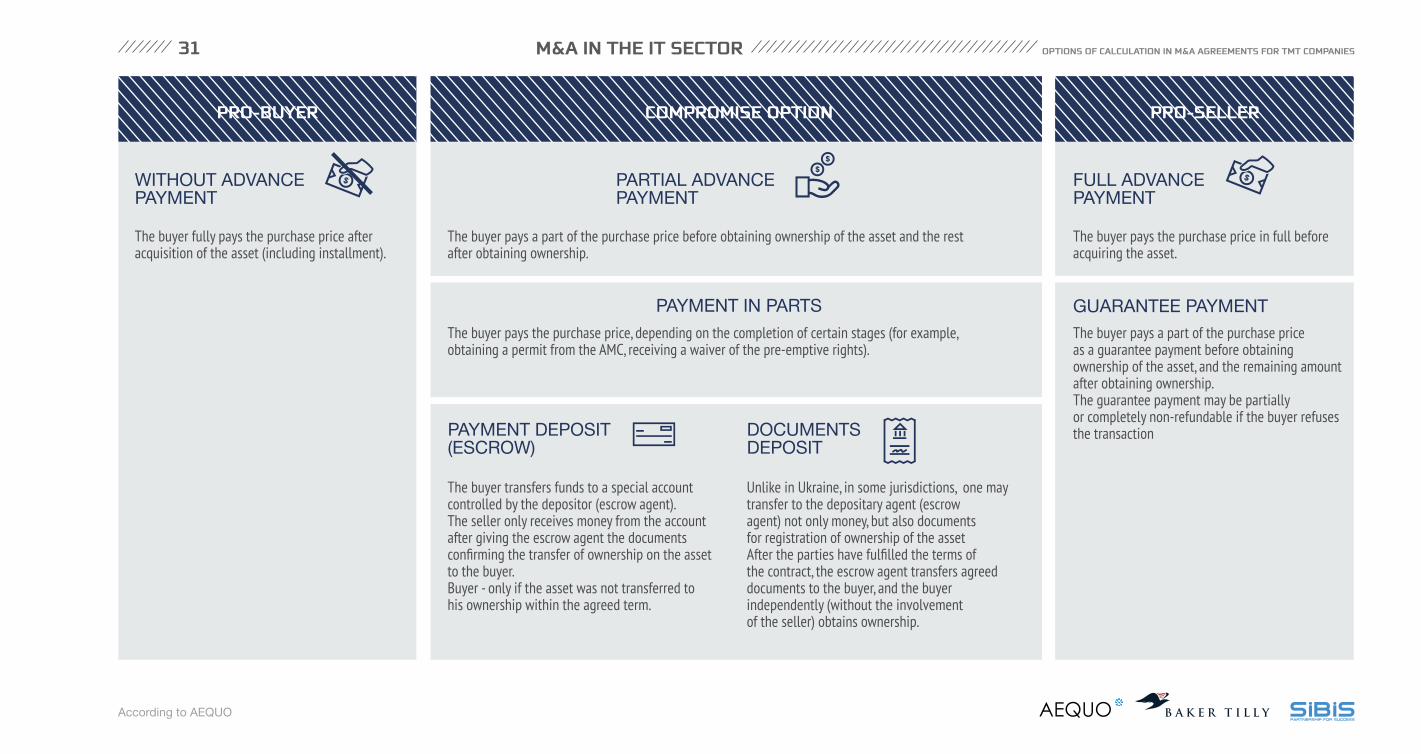

М&A IN THE IT SECTOR

PRO-BUYER COMPROMISE OPTION PRO-SELLER

WITHOUT ADVANCE PAYMENT

PARTIAL ADVANCE PAYMENT

FULL ADVANCE PAYMENT

GUARANTEE PAYMENTPAYMENT IN PARTS

PAYMENT DEPOSIT (ESCROW)

DOCUMENTSDEPOSIT

The buyer fully pays the purchase price after acquisition of the asset (including installment).

The buyer transfers funds to a special account controlled by the depositor (escrow agent). The seller only receives money from the account after giving the escrow agent the documents confirming the transfer of ownership on the asset to the buyer.Buyer - only if the asset was not transferred to his ownership within the agreed term.

Unlike in Ukraine, in some jurisdictions, one maytransfer to the depositary agent (escrowagent) not only money, but also documentsfor registration of ownership of the assetAfter the parties have fulfilled the terms of the contract, the escrow agent transfers agreed documents to the buyer, and the buyer independently (without the involvement of the seller) obtains ownership.

The buyer pays the purchase price in full before acquiring the asset.

The buyer pays a part of the purchase price as a guarantee payment before obtainingownership of the asset, and the remaining amount after obtaining ownership.The guarantee payment may be partially or completely non-refundable if the buyer refusesthe transaction

The buyer pays a part of the purchase price before obtaining ownership of the asset and the rest after obtaining ownership.

The buyer pays the purchase price, depending on the completion of certain stages (for example,obtaining a permit from the AMC, receiving a waiver of the pre-emptive rights).

According to AEQUO

OPTIONS OF CALCULATION IN М&A AGREEMENTS FOR ТМТ COMPANIES

31

VIVID VISUALIZATION for your content marketing:

Content for any stageof the customer journey

toplead.eu

Motion graphicPresentationsResearch

CREATED BY

TOP LEADtoplead.com.ua

Terms of use of this guide: partial reprint of the materials in this guide is possible with a direct hyperlink to the BUSINESSVIEWS page where this guide is located. Use of the full version of this guide and its placing on sites electronically is strictly prohibited. © Top Lead LLC. All rights reserved

AEQUOVector Business Center,st. B. Khmelnitsky 52, Kyiv, Ukraine

aequo.ua

BAKER TILLYAlexander Pochkun, Managing Partner

bakertilly.ua

SI BISIgor Fedchenko, CEO Lyudmila Bilyk-Beregova, CMO

sibis.com.ua

businessviews

businessviews.com.ua

DISCLAIMERThis report is created solely to inform users. We make every effort to ensure that the information provided in the directory is accurate and up-to-date. Despite the fact that this report was carefully prepared by specialists, it can be used to gain a general idea of the subjects discussed herein. It is not recommended to use the information contained in the report as professional advice on any particular issue or for professional assessment. Featured data was collected and prepared for publication in 2017.

For requests for sponsorship and partnership in infographic report projects

Partnership

BusinessViews

ANALITICAL PARTNER

MEDIA PARTNERS: