draft - wikileaks commercial diligence... · ・there is a significant opportunity from increasing...

TRANSCRIPT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Value chain analysis

Section Page

Executive Summary 1

Value chain analysis overview 4

Value chain analysis ① 6

Value chain analysis ② 9

Value chain analysis ③ 13

Key Opportunities & Threats 17

Comparative Research 19

1

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

SummarySummary

2

We have focused our review of Red on analysis of the value chain and comparison to leading competitors in the provision of Korean TV programming in Japan. Overall, there appears to be a number of opportunities to further develop the business.

Sales

Development of revenues from CATV (J:COM), where there is low penetration

・ As there are over 44,000 CATV operators in Japan, there is a considerable long-tail to the market which is yet to be fully exploited. However, there would be significant costs in addressing smaller players in the market, in addition to which Red has already signed agreements with leading MSOs (multiple system operators).

・There is a significant opportunity from increasing penetration from the leading CATV provider, J:COM, if Red is to expand sales from CATV to levels consistent with its satellite revenue stream.

・Red was previously able to differentiate its service by providing programs only to Satellite and CATV, however, there is a long-term threat from OTT distribution which may collapse the value chain for Korean TV programming, and may affect Red’s competitive advantage.

Platform switching

・Red’s customer base is weighted towards female consumers who are aged over 40, in common with other Korean programming TV channels. This bias reflects viewing habits of KNTV’s core customer demographic, who typically watch such programs during the evening as part of their daily routine. While this pattern is expected to continue, in the long run there may be disruption to viewing patterns and habits from new technology, in particular watching content directly over the Internet (OTT) provided by global and Japanese media players. The company should carefully calibrate its response to changes in viewing habits.

Cost

Content costs

General operating cost reductions・Based on our understanding of the market and competitors to Red, the company enjoys comparatively good

profitability. As a largely fixed cost business, there may be opportunities for further cost improvement and rationalization as the business develops, although we understand no plans are currently in place.

・ Further, as part of a larger organization there may be long-term opportunity to benefit from cost synergies.

・The price of Korean content is expected to be stable by local management, who have forecast a stable growth of around 3% in their projections. However, as imported material there is exposure to exchange rate risk.

・ Were the company to focus on alternative product content, which we understand may be a possibility, there is opportunity to counter the risk of price increases of drama through alternative content purchasing.

Challenge Commentary

Customer base

・We understand the present customer base of the business is heavily weighted towards female consumers who are over 40, where the company enjoys a strong position.

・While in the short term the business may continue to grow through increasing its penetration rate on CATV, were Red to focus on achieving further growth it may need to consider targeting these alternative customer groupings. In particular, as younger consumers are increasingly watching content through smart phones, the existing drama content format may not be suitable to their tastes or viewing habits. DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

SummarySummary

3

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Korean broadcast contentin Japan market projections (paid )

Projection of subscription numbers byplatform [satellite(CS/BS)/CATV/IPTV] in Japan

Ssatellite/CATV/IPTV/OTT market projections(paid video)

(10,000 people)

Smartphone video market projections in Japan

0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015 2016

(1,000 dollars)

(100 million yen) (100 million yen)

01,0002,0003,0004,0005,0006,0007,0008,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

(e)

2011

(e)

2012

(e)

2013

(e)

2014

(e)

2015

(e)

satellite

CATV

IPTV

0

2,000

4,000

6,000

8,000

10,000

12,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

(e)

2011

(e)

2012

(e)

2013

(e)

2014

(e)

2015

(e)

OTT

IPTV

CATV

satelliteDRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Value chain analysis

Section Page

Summary 2

Value chain analysis overview 4

Value chain analysis ① 6

Value chain analysis ② 9

Value chain analysis ③ 13

Key Opportunities & Threats 17

Comparative Research 19

4

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Value chain analysisValue chain analysis overview

5

We consider there are three principal changes taking place in the Korean TV programming market, as set out below.

satellite(CS)

Broadcast receiver

cable

FTTH

satellite(CS)

CATV

IPTV

1. Growth in Korean broadcast content 2. Maturation of key broadcast platforms 3. Changes to consumer viewing habits

It is expected that the growth of Korean broadcastcontent media will continue, reflecting continuing interest in Asia in Korean music and youth culture. There is a risk, however, contents costs continue to rise, which would impact future profitability

Satellite and CATV markets are largely mature in Japan. By contrast, IPTV and OTT broadcast market are growing, although they continue to be small and with limited use by Red’s core users (female, older than 40).

Viewer figures have fallen in recent years, which has been coupled to an increase in penetration rates of connected devices, which may in the long-term shift viewing habits towards new delivery platforms. At present this trend is likely to be observed largely among younger consumers.

Program adaptation Platform ConsumerContent holder DevicesN/W

Red

Multi-Device

Channel audience

Multi-Network

TV

STB

Parabolic antenna

3G3G WiMAXWiMAXLTELTE FTTHFTTH

InternetSmart phoneSmart phone tablettablet

PCPC Smart TVSmart TV

1

2

3

satellite(BS)satellite(BS)

TV

Movie

Label

Animation

Publisher

Talent agency

・・・・

Digital terrestrialTerrestrial TV

Not channel audience

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Value chain analysis ①

6

Section Page

Summary 2

Value chain analysis overview 4

Value chain analysis ① 6

Value chain analysis ② 9

Value chain analysis ③ 13

Key Opportunities & Threats 17

Comparative Research 19

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Value chain analysis ①Summary of Korean broad cast contents market in Japan and buying cost

7

The Korean broadcast market has enjoyed strong historical growth which is expected to continue for the foreseeable future. However, there is a risk that future content costs reduces Red’s future profitability.

・The price for broadcasting rights to a Korean TV drama program (of about one hour )is approximately USD 100 thousand, and is approximately 20-30% more expensive than 3-4 years ago. Prices are now broadly comparable with the cost of Japanese content.

・At the moment, Red benefits from a comparatively weak Korean Won in importing underlying content from South Korea, which may expose the company to inflation and exchange risk. We note that South Korea continues to enjoy strong GDP growth of 4%, which is likely to result in a long-term appreciation of the currency. We set out below currency forecasts from Economist Intelligence Unit:

・In 2015 the market for Korean broadcast content in Japan is projected to be 34 billion yen, with an assumed average growth rate of 7.1% from 2005 to 2015.* Assumed exchange rate of 1 dollar =90 yen.

Korean broadcast contents market projections in Japan (paid video)

Broadcast content costs

・We understand that leading competitors to Red are able to purchase content at approximately 10-15% of viewing fees, compared to around 33% for Red in 2011. While this in part reflects a differing product mix, including some Japanese TV programs/mobile content, this may suggest future cost increases in drama content may be able to be offset by changes in program mix, if this is consistent with consumer tastes and preferences.

※ Preliminary analysis based on following assumptions:1. Export value of Korean broadcast contents from Korea to Japan (JETRO)2. From 2009 to 2015, assumption that last-year’s growth rate continue3. 81% of export value is paid contents4. Red’s ratios of Revenues/Program costs from 2009 to 2015

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000(1,000 dollars)

11.0 11.5 12.0 12.5 13.0 13.5 14.0 14.5 15.0

2011 2012 2013 2014 2015 2016

(KRW/Yen)(KRW/Yen)

・We understand that competitors to Red have enjoyed revenue growth rates of around 5% per annum.

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Value chain analysis ①Channels broadcasting Korean contents in Japan

8

81% of Korean drama aired in Japan is broadcasted on pay-channels, with Red broadcasting almost one quarter of Korean dramas aired in Japan.

Number of Korean Dramas aired (by Channel)

Regional Stations: TVK, Saitama TV, Chiba TVSource: WOW! Korea

Regional Stations, 7

Nippon TV, 5TBS, 4

TV Asahi, 4

NHK, 3TV Tokyo, 3

Tokyo MX, 2

Pay Channels,

119

Breakdown of Pay Channels

Red, 28

KBS World, 26

Mnet Japan, 17

LaLa TV, 11

Home drama

channel, 9

Eisei Gekijo, 9

So-net, 8

tbs Channel, 4

Monthly charge (including consumption tax)

3,150

525

1,890

735 630

0500

1,0001,5002,0002,5003,0003,500

KNTV LaLa TV Mnet KBS World AsianDramatic TV

So-net

JPY

Red

Charges for SkyperfecTV

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Value chain analysis ②

9

Section Page

Summary 2

Value chain analysis overview 4

Value chain analysis ① 6

Value chain analysis ② 9

Value chain analysis ③ 13

Key Opportunities & Threats 17

Comparative Research 19

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

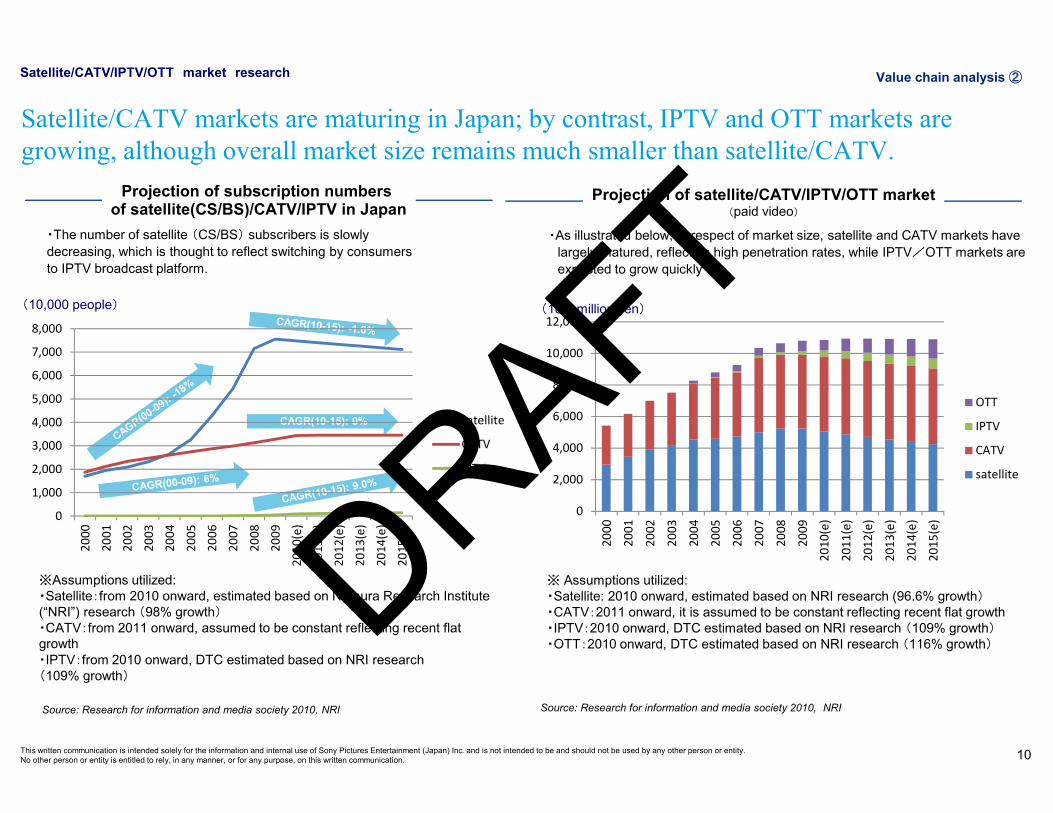

Value chain analysis ②Satellite/CATV/IPTV/OTT market research

10

Satellite/CATV markets are maturing in Japan; by contrast, IPTV and OTT markets are growing, although overall market size remains much smaller than satellite/CATV.

※Assumptions utilized:・Satellite:from 2010 onward, estimated based on Nomura Research Institute (“NRI”) research (98% growth)・CATV:from 2011 onward, assumed to be constant reflecting recent flat growth・IPTV:from 2010 onward, DTC estimated based on NRI research (109% growth)

Projection of subscription numbers of satellite(CS/BS)/CATV/IPTV in Japan

・The number of satellite (CS/BS) subscribers is slowly decreasing, which is thought to reflect switching by consumers to IPTV broadcast platform.

Projection of satellite/CATV/IPTV/OTT market(paid video)

・As illustrated below, in respect of market size, satellite and CATV markets have largely matured, reflecting high penetration rates, while IPTV/OTT markets are expected to grow quickly

Source: Research for information and media society 2010, NRI

※ Assumptions utilized:・Satellite: 2010 onward, estimated based on NRI research (96.6% growth)・CATV:2011 onward, it is assumed to be constant reflecting recent flat growth・IPTV:2010 onward, DTC estimated based on NRI research (109% growth)・OTT:2010 onward, DTC estimated based on NRI research (116% growth)

CAGR(10-15): 0%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

(e)

2011

(e)

2012

(e)

2013

(e)

2014

(e)

2015

(e)

satellite

CATV

IPTV

0

2,000

4,000

6,000

8,000

10,000

12,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

(e)

2011

(e)

2012

(e)

2013

(e)

2014

(e)

2015

(e)

OTT

IPTV

CATV

satellite

(10,000 people) (100 million yen)

Source: Research for information and media society 2010, NRI

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Value chain analysis ②Penetration rate

11

In respect of opportunity to increase penetration rates, the companies with whom Red has already concluded service agreements comprise a substantial portion of the overall addressable market where there may be profit potential.

totalnum

bersof

subscribersofsatellite/C

ATV

/IPTVm

arket

Penetration rate

The number of CATV companies in Japan is approximately 44,000. reflecting a long-tail of smaller, regional players.

We understand from interviews with management that they will continue to focus on expansion of service coverage to include smaller regional operators.

As Red expands its service coverage it will be crucial to ensure that subscriber numbers of J:COM, the largest CATV player in Japan, continue to improve. While the viewer share for J:COM is approximately 0.5%, there may be opportunity to increase towards the levels seen on the Sky perfectTV of over 3%.

Consideration

2007 2008 2009 2010 2011satellite Sky perfecTV 368 371 369 373 379 CATV J:COM 265 317 327 343 366

JCN 50 59 68 77 86 CNCI 30 30 29 30 30 ITSCOM N/A N/A N/A N/A 71 K-CAT 7 10 21 36 52

IPTV Hikari TV(IPTV) 12 28 50 70 90 sum 732 815 864 929 1,074

satellite 5,434 7,154 7,556 7,480 7,406 CATV 2,986 3,130 3,281 3,439 3,449 IPTV 23 46 80 90 106 sum 8,437 10,307 10,883 11,010 10,961

Potential penetration rate (all)

9% 8% 8% 8% 10%

Potential penetration rate (satellite)

7% 5% 5% 5% 5%

Potential penetration rate (CATV)

12% 13% 14% 14% 18%

Potential penetration rate (IPTV)

52% 61% 63% 78% 85%

・The penetration rate of satellite providers with whom Red has established relations over total satellite viewers is relatively low, reflecting lower channel availability. The total satellite TV market is dominated by the services provided by NHK, the national broadcaster of Japan. Due to further increase in number of channels on satellite TV, further penetration growth for Red is thought unlikely.

・The penetration rate of CATV is higher than the overall average across all broadcast platforms, as Red has developed business relationship with the top player J:COM. Nevertheless, there are many regional players.

(10,000 people)

Source: Research for information and media society 2010, NRI

totalnum

bersof

subscribersof

Red’s

major

satellite/CATV/IPTV

partner

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Value chain analysis ②OTT players

12

With the expansion of smart phone devices, new entrants into the OTT market, including large global media brands, new players and , may erode the competitive advantage of established players such as Red over time.

Main player in broadcasting

Main playerin OTT delivery

Strategic Consideration

OTT market overview by market participant group

Terrestrial TV

Global brand

New players

Telecoms Carriers/Physi

cal Stores

presentpaid broadcast

Retain existing customersStrategy of starting contents distribution from 2011 through not only existing pay-

TV platforms, but also internet/mobile devices to retain market share.

Obtain new customersThey may be able to leverage their global brands and customer base;

longer term, there may be also potential to drive down costs/create

original content

Additional value for existing customer

With existing media assets, they have started to enter OTT market, and improve customer satisfaction.

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Value chain analysis ②

13

Section Page

Summary 2

Value chain analysis overview 4

Value chain analysis ① 6

Value chain analysis ② 9

Value chain analysis ③ 13

Key Opportunities & Threats 17

Comparative Research 19

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Value chain analysis ③Impact of Smart Phones

14

3:21

3:28

3:36

3:43

3:50

3:57

2004 2005 2006 2007 2008 2009 2010

・Overall, average TV viewing figures are reducing, although it is difficult to ascertain the effect on niche channels such as Red. Recently, the substantial increase in smart phone sales may provide an alternative delivery platform.

Source. ROA

TV viewing time / Sales of smart phones/ smart TV Smartphone ownership by gender/age

Source:. Nikkei

As a result of a reduction in typical time spent watching TV, and increased penetration of smart phones, particularly for younger consumers, may create favorable conditions for new delivery platforms such as OTT, which may be less suitable for traditional TV content.

Source Video Research Interactive [research in 6/2011]

・At present, smart phone ownership is highest amongst young consumers; as smart phone ownership extends into older age groups, this will also include Red’s core audience.

0 2 4 6 8 10 12 14

total

men total

15-19

20's

30's

40's

50's

60's

female total

15-19

20's

30's

40's

50's

60's

(10,000 units)

(minutes)(%)

Smartphones

SmartTVs

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

0

0.2

0.4

0.6

0.8

1

1.2

0100200300400500600700

2011 2012 2013 2014 2015 2016

video market

decline rate of unitprice

Value chain analysis ③

Service name Fee Start date OS Distribution form

980yen/month 8/2011 iOS/Android Streaming

new:400 yenold:300~350yen

10/2011 Android Download

525yen/month 11/2011 Android Download

Flat/monthPPV

12/2011 iOS/Android Streaming

350yen/month1,000yen/month

12/2011 iOS/Android Streaming

Expansion of smartphone video market

15

The market of movie distribution services through smart phone is expected to have 10M pay-users, a total JPY 60 billion market in 2016, however, the extent of the market opportunity for Red is at yet unclear, given its current customer base.

Smartphone video market in Japan projections・The market size in 2016 is projected to be 60 billion yen

・This market size is smaller than satellite/CATV market size (each of which has a market size of c.400billion yen)

・In line with market expansion, there may be a decrease in unit price

Number of users in smartphone video market

ref:each HP

※decline rate is based on2011.

Source: MM Research Institute

・Number of paid subscribers in 2016 is projected to 10million.

・Including free user, number of users is about 40million.(10,000 people)

(100 million yen)

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2011 2012 2013 2014 2015 2016

free audience paid audience

Ref. MM research Institute

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Value chain analysis ③Viewer Analysis

16

The core audience of Korean TV programming is typically female aged over 40, with a peak time of viewing after 10pm; Korean programming is a core reason for watching pay TV.

Viewing HabitsInterest in Korean TV content

Terrestrial

Broadcasting satellite, free

Communications satellite, pay-TV

NHK-satellite

Broadcasting satellite, pay-TV

8%

10%

10%

6%

9%

6%

22%

19%

20%

14%

14%

11%

20%

25%

17%

19%

22%

27%

51%

47%

53%

61%

54%

56%

<=60

>60

>50

>40

>30

>20

AgeFemale

3%

3%

2%

4%

6%

4%

14%

15%

10%

8%

7%

4%

21%

21%

17%

18%

8%

10%

61%

61%

71%

71%

79%

82%

<=60

>60

>50

>40

>30

>20

I'm a fan of it Like Interested Not interested

AgeMale

The audience watch pay-TV when they want to watch• Old foreign movies: 74%• Old Japanese movies: 73%• Latest foreign dramas: 66%• Latest Korean movies : 65%• Latest Korean dramas : 61%• Rebroadcasted Korean dramas : 60%• Latest Japanese movies : 60%

Reasons for watching Pay TV in Japan

Source: Ministry of Public Management, Home Affairs, Post & Telecoms

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Key Opportunities & Threats

17

Section Page

Summary 2

Value chain analysis overview 4

Value chain analysis ① 6

Value chain analysis ② 9

Value chain analysis ③ 13

Key Opportunities & Threats 17

Comparative Research 19

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Key Opportunities & ThreatsSummary

18

Based on the analysis performed, key opportunities and threats center on future program costs, expansion of non-satellite revenues and a long-term threat of changes in viewing preferences.

■Opportunity・The market for OTT delivered content via smartphone is estimated

to be around 60 billion yen in 2015, a reasonable opportunity. This market is focused at present on younger consumers in the 20s-30s demographic, outside of Red’s existing core customer base.

■Threat・In the long-term, while viewing habits are sticky, new broadcast

platforms may result in switching of Red’s core customer base.

■Opportunity・The satellite and CATV markets are mature, and the core base of

existing users is expected to remain steady over the medium term, providing stability to the business.

■Threat・In the long term, a dependence on satellite and cable may result in

Red missing revenue opportunities as user growth may be limited. The profitability of the established business model of providing drama content through cable and satellite may also be at long-term threat from increases in drama content costs.

■Opportunity・KNTV is well-placed to benefit from the continued interest in Korean culture, fashion and food, and from increased supply of a variety of content suitable for localization in Japan.

■Threat・Risk of increased program costs in the future reflecting currency appreciation and local wage and price inflation.

Although there is expected to be continued market growth for Korean programming content, there is a risk of increased programming costs

Viewer figures have fallen in recent years, which has been coupled to an increase in penetration rates of connected devices, which may in the long-term shift viewing habits towards new delivery platforms. At present this trend is likely to be observed largely among younger consumers.

Value chain shifts Opportunity/Threat Valuation Implications

Management expectations forprogramming costs may betowards the lower end of areasonable bound; future inflationin programming costs may behigher to reflect inflation andexchange rate risk.

The core markets of Red aremature; there is opportunity forRed to increase its penetration inthese established platforms,although there is uncertainty overhow quickly this may be achieved.

There is a broader long-termthreat to pay-TV industry thatmay need to be reflected indiscount rate risk factors applied

There is potential for furtherrevenue growth in new areas,where management have atpresent conservatively assumedflat growth.

The risk of longer term changesto viewing habits is difficult toestimate, and may be bestreflected in discount rate.

While the satellite and CATV markets have largely matured, IPTV market and OTT market are growing. However, both markets are currently focused on a different demographic to Red, which we understand is focused on female viewers aged over 40.

1. Growth in Korean broadcast content

2. Maturation of key broadcast platforms

3. Change of viewing style of consumer DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

Appendix

19

Section Page

Summary 2

Value chain analysis overview 4

Value chain analysis ① 6

Value chain analysis ② 9

Value chain analysis ③ 13

Key Opportunities & Threats 17

Appendix 19

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

RedViewer Analysis

20

Most of Red’s revenue is derived from subscription revenue from Satellite TV, and Cable TV subscribers; as with many Japanese broadcasters, advertising revenue is relatively low.

2,123

483

IPTVCable(J:COM, K-CAT etc..)BS/CS (SkyperfecTV)

2,1792,563 2,692

2,408

2,824 2,848

0

500

1,000

1,500

2,000

2,500

3,000

09/12 10/12 11/12

Subscription Production contents Advertising

Incentive Broadcasting Other

(million yen) Revenue Breakdown

Revenue Breakdown

Source: Red Management, audited financial statements

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

AppendixSmartphone video habits

21

・”Free video” remains the largest group of users, in reflecting the continuing difficulty to monetize content delivered through new media.・The ate of paid video service users is currently 14.5%, which may suggest some profit potential, particularly for niche areas where Red is currently focused.

Service category of smartphone video viewing Smartphone video viewing times

The main user segment for smart phone video services still relates to free content, with a typical viewing time of 1-5 minutes.

Source: goo Research (6/2011 survey)

・Viewing times of 1 -5 minutes remains the largest group within viewers of video delivered via smart phones.・By contrast, longer viewing times of 30 minutes, which may be more suited to longer drama content is a relatively small proportion of the overall total.

Source: Nikkei Consumer Watcher (8/2011 survey)

0 10 20 30 40 50 60

free video

One Seg

TV tel

paid video

video downoaded on PC

other

a few seconds

10 - 30 seconds

30 - 60seconds

1- 5 minutes

5 - 10 minutes

10 - 30 minutes

30 - minutes

40.4%22.6%

18%10.2%

4.3%2.9%

1.5%(%)

DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

AppendixViewer Analysis

22

“Winter Sonata” in 2003 became the first big hit in Japan for Korean drama, triggering the “Korean Wave”, as audiences became interested in other Korean drama series. Likewise Korean music is also popular, although tends to be focused on a younger demographic.

Date Name Media Ranking(weekly) Rate Theme Players2004/8/21 Winter Sonata NHK 3 23.4% Romance Bae Yong Joon2005/12/24 Chan gum no chikai NHK - 9.9% History/Romance I Yeong-ae2010/3/24 Kareinaru Isan Fuji Media Holdings 9 9.7% Family/Romance Hang Hyo Joo2010/4/21 Iris TBS - 10.1% Romance Lee Byung Hun

Korean TV series with high audience market share

CD singles by Korean artists in the top 100 ranking 2011

2009 2010 2011Rank Artist Rank Artist Rank Artist

30 Tohoshinki 26 Tohoshinki 16 Tohoshinki32 Tohoshinki 28 XIAH Junsu 25 KARA49 Tohoshinki 49 Shojo jidai 26 KARA

29 Jang Gunsuk41 Tohoshinki46 Shojo jidai

3 songs / top 50 3 songs / top 50 6 songs / top 50

•Winter Sonata opened the wayfor Korean contents to Japanesemarket.•The drama became popularespecially among the middle andold aged women, and made asensation of Korean wavecoming after.DRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

AppendixComparative Research

23

We have compared Red’s operating model to competitors focused on Korean contents programming in Japan, and note some key business model attributes.

........

Target consumer age group: 30s

Acquisition ofyounger consumers

in the future

Subscriber Revenues Non-Subscriber Revenues

n Major broadcast content

Ø Korean dramaØ MusicØ Foreign drama

n Future possibilities

Ø Enhanced original programming

nProgram sales in greater Asia

nBusiness development and events related to program production e.g. fashion shows

nApparel sales

nExpansion and usage of membership organization

nMobile broadcast business e.g. BeeTV/NTT DoCoMo

nExpansion of Web-enabled services, tie-ups to websites targeting specific demographics e.g. OzmallDRAFT

This written communication is intended solely for the information and internal use of Sony Pictures Entertainment (Japan) Inc. and is not intended to be and should not be used by any other person or entity. No other person or entity is entitled to rely, in any manner, or for any purpose, on this written communication.

AppendixComparative Research

24

The number of UU (monthly unique users) who visit the website of Red is more than any other competitors, which may suggest opportunity to start OTT distribution services.

Comparison to PV/UU

PV/UU

UU(thousands)

Comparison to number of sessions

PV/sessions numbers

Sessions numbers /UU

Ref. Google ad plannerRef. Google ad planner

*PV:page view*UU:monthly Unique Users

*PV:page view*UU:monthly Unique Users

DRAFT