drb-hicom outperform...2013/01/25 · drb-hicom 25 january 2013 page 2 of 14 kenanga research 1....

TRANSCRIPT

KENANGA RESEARCH Initiating Coverage

25 January 2013

PP7004/02/2013(031762) KENANGA RESEARCH

DRB-Hicom OUTPERFORM Price: RM2.60

Unlocking assets Target Price: RM3.45

We are initiating coverage on DRB-Hicom Bhd (“DRBH”) with an Outperform call, valuing it at RM3.45 based on a sum-of-parts valuation. In our view, the stock is undervalued, underpriced and clearly under-appreciated, trading at just 6.0x FY13 earnings (below its peers’ average of 12.0x) and at the unjustified 36% discount to its FY13E BVPS of RM3.54. However, things could soon turn for the better as management is seriously pursuing to transform this asset and resource-rich group, unlocking earnings, gains and cash. We see new and strong growth potential in its automotive division from Proton, its assembly contract with Volkswagen (VW) and the earnings contribution from the AV8X8 (defense) contract. The group’s Property division too will soon stamp its mark with the kick-start of projects worth a total GDV of RM13.3b. Another potential upside could come from the possible sale of its Shah Alam plant to VW, which may translate into c.70 sen one-off gain. With all the catalysts above, DRBH could well turn out as one of the best winning newsmakers in 2013. OUTPERFORM.

Growth to be driven by a “transformed” automotive…We see strong growth potential in its automotive division mainly from Proton, its assembly contract with Volkswagen (VW) and the earnings contribution from its AV8X8 (defense) contract. The purchase of Proton has positioned DRBH as the country’s single largest automotive group with a market share of 31% for the first nine months of 2012 (9M2011:15%). We view positively the group’s revival plans for Proton, which include increasing sales through the introduction of new models, growing its exports as well as turning around Lotus. Meanwhile, its tie-up with VW is progressing well as the production of the VW marques is well on track. We understand that earnings contribution from the RM7.5b AV8X8 contract will also start coming in from FY14 onwards. To sum it up, all its growth “engines” will be working overtime here for the next two years.

…and a “reinvigorated” property. The group is kick-starting its property projects in 2013/2014 in a massive thrust to get its huge land banks to work for the group. This will clearly showcase management’s serious commitment to transform the group’s assets into earnings and cash. The group has always had a large development land bank with the hot ones now being in Iskandar, Johor and in Glenmarie, Klang Valley. For a start, new launches will total a GDV of RM323m in 2013 before being ramped up to around RM11.0b and RM2.0b in 2014 and 2015 respectively. That means its property EBIT will jump from just RM6m in FY12 to RM32m in FY13 and to RM85m in FY14.

Potential upside from sale of Shah Alam plant or its re-development. It was reported that VW is looking to make Malaysia its manufacturing hub in ASEAN and to do so, it was said to be mulling over the buyout of Proton’s Shah Alam plant for the additional capacity. Should the land sale take place, based on our back-of-the-envelope calculation, this could potentially represent a c.RM0.70 per share revaluation surplus to DRBH (a potential gain on sale of RM1.5b between the reported sale price of RM150 psf and the land cost in the book of just RM10 psf). Apart from just selling the 250-acre land to VW, we believe that another possible scenario is to transfer the land to the group’s property arm for redevelopment (its production activities here could be moved to its under-utilised Tanjung Malim plant), which we reckon would be lucrative as well considering the growing scarcity of prime land bank in the Klang Valley.

OP with an initial target of RM3.45. The stock is clearly mispriced, trading at just 6.0x FY13 EPS (below its peers’ average of 12.0x) and at a 36% discount to its FY13E BVPS of RM3.54. We project earnings to jump 33% YoY in FY13 to 22 sen largely due to the inclusion of Proton results and 45% in FY14 as contribution from its AV8X8 contract starts to kick in. This potential strong earnings rise is still under-recognised by the market for now, but not likely in the future. OUTPERFORM.

Share Price Performance

2.00

2.20

2.40

2.60

2.80

3.00

3.20

3.40

Jan-12 Mar-12 May-12 Jul-12 Sep-12 Nov-12 Jan-13

KLCI 1,635.25 YTD KLCI chg -3.2% YTD stock price chg -4.8%

Stock Information

Bloomberg Ticker DRB MK Equity Market Cap (RM m) 5,026.4 Issued shares 1,933.2

52-week range (H) 3.26

52-week range (L) 2.18

3-mth avg daily vol: 5,595,310

Free Float 34%

Beta 1.2

Major Shareholders

ETIKA STRATEGI SDN B 55.9%

EPF 6.9%

SKAGEN AS 2.8%

Summary Earnings Table FY Mar (RMm) 2012A 2013E 2014E

Turnover 6878.2 14911.9 16706.1 EBIT 474.2 854.5 991.1

PBT 1512.6 1213.0 883.8 Net Profit (NP) 1293.0 858.5 601.7

Core NP 321.5 412.3 601.7 Consensus (NP) - 406.0 534.5 Earnings Revision - - -

EPS (sen) 66.9 44.4 31.1 EPS growth (%) -32.0 28.2 -29.9

DPS (sen) 6.0 8.9 6.2 BVPS (RM) 3.19 3.54 3.79 PER (x) 3.9 5.8 8.3

PBV (x) 0.8 0.7 0.7 Net Gearing (x) 0.4 0.9 0.6

Dividend Yield (%) 2.3 3.4 2.4

The Research Team

[email protected] +603 2713 1373

DRB-Hicom 25 January 2013

Page 2 of 14 KENANGA RESEARCH

1. INVESTMENT MERITS

Growth driven from automotive… We see strong growth potential in its automotive division mainly from Proton, its

assembly contract with Volkswagen (VW) and earnings contribution from its AV8X8 (defense) contract. The inclusion of

Proton has positioned DRBH as the country’s single largest automotive group, gaining a market share of 31% for the first nine months of 2012 (9M2011:15%). We view positively the group’s revival plans for Proton which include increasing sales

through the introduction of new models, growing its exports as well as the turning around of Lotus. Meanwhile, its tie-up with VW is progressing well, as the production of the VW marques is well on track. We understand that earnings

contribution from the RM7.55b AV8X8 contract will start coming in from FY14 onwards.

…and property. Earnings contribution from the property division is expected to increase further (from 1% in FY12) as

the group plans to launch property development projects with a total gross development value (GDV) of RM13.3b between 2013 and 2015. Projects to be launched in 2013 include the cluster house development in Tanjung Malim, Laurel

(Precinct 2B2a), Phase 2B of Laman Glenmarie 2, Phase 3 of Glenmarie Gardens and Glenmarie Villa—for a total GDV of RM323m. Meanwhile 2014 and 2015 will see launches of developments worth RM11b and RM2b, respectively.

Proton acquisition a win-win situation. We view the group’s acquisition of Proton as a win-win situation for both DRBH and Proton. With Proton under its stable, DRBH is now the country’s single largest automotive group with multiple

brand representations, enabling it to rival the strong alliance between Perodua and Toyota Malaysia. DRBH will also be able to leverage on Proton’s strong sales volume and utilise the extra auto manufacturing capacity from the latter’s

underutilised Tanjung Malim plant. On the other hand, Proton will gain from DRBH’s partnerships with renowned automakers.

Volkswagen to increase market share. VW plans to grow its presence in the Malaysian passenger car market as well as in ASEAN. It plans to increase its market share from the current 2% to 10%. It is said that the company is looking to

make Malaysia its manufacturing hub in ASEAN and to do so, is said to be mulling the buyout of Proton’s Shah Alam plant

for its additional capacity. Although we view this as improbable at this juncture, should the land sale take place, based on our back-of-the-envelope calculation, this could potentially add c.RM0.70 per share to DRBH’s fair value (assuming the

asking price of RM150 psf vs. the land cost of RM10 psf).

Redevelopment of the Shah Alam land. DRBH is injecting investments worth RM1.0b in the next five years to bolster

developments at Proton City in Tanjung Malim, Perak, This is to ramp up production at the underutilised Tanjung Malim plant, which may include consolidating the production of the Shah Alam plant with that of Tanjung Malim and assembling

other vehicle makes under the group. We understand that the manufacturing activities in Shah Alam will be gradually phased out, making Tanjung Malim the centre of DRBH’s assembling and manufacturing activities. Apart from selling the

land to VW, we believe that another possible scenario is to transfer the land to the group’s property arm for redevelopment, which we reckon would be lucrative considering the growing scarcity of prime land banks in the Klang

Valley.

Streamlining of operations. DRBH’s acquisition of Proton has increased the group’s borrowings to RM6.3b (+18%) and

its net gearing level to 1.8x (from 0.4x). DRBH is taking measures to divest its non-core assets to pare down the borrowings as well as to streamline its operations. For a start, the group has completed the disposal of Hicom Power (to

Sterling Asia Sdn Bhd, a unit of Malakoff Power Bhd) for RM575m cash. Hicom Power is a wholly-owned subsidiary of DRB-Hicom, whose principal activity is the provision of operation and maintenance (O&M) services for power plants.

DRBH is also looking to sell off a 30% stake in BMMB as well as to dispose off its insurance business (UAL and UAG). The

group is currently in talks with Affin Bank Holdings Bhd to sell off a 30% stake in BMMB in order to comply with Bank Negara Malaysia’s (BNM) guidelines. Meanwhile, the group has also been given the approval by BNM to start preliminary

negotiations with interested parties for the sale of its insurance business. We understand that the group is looking to replace the insurance business with takaful (Islamic insurance). This in turn will enable the group to be syariah-compliant.

Together, these disposals could potentially raise RM976m in cash proceeds for the group (BMMB: RM600m, insurance: RM376m).

Stable income from services segment. The services segment is the group’s second largest division. It has a diverse collection of businesses which include concession-based operations, financial services and trading. These businesses

provide stable recurring income for the group driven mainly by banking (Bank Muamalat) and postal services (Pos Malaysia).

2. SEGMENTAL BREAKDOWN

AUTOMOTIVE

Business overview. DRBH is an exclusive distributor of Audi, Honda, Mahindra, Mitsubishi, Proton, Suzuki as well as Isuzu trucks and pick-ups, HICOM Perkasa light-duty trucks and MODENAS motorbikes. It is also into the manufacturing,

assembly, distribution and sales of military vehicles and special purpose vehicles including the sales of related spare parts and services. In 2010, the group recorded its highest vehicle sales of 74,443 units (+24% YoY; passenger: 75%,

commercial: 25%), representing 12% of the country’s total industry volume of 605,156 units. Honda, its best-selling marque, contributed 60% of the sales. DRBH’s total vehicle sales dropped 15% YoY in 2011 due to the natural disasters

that hit Japan and Thailand, which led to Honda shutting down its operations in both countries.

DRB-Hicom 25 January 2013

Page 3 of 14 KENANGA RESEARCH

The group has eight assembly plants. Four of the plants are for motor vehicles – three at its integrated assembly complex in Pekan and one Honda plant in Melaka. It also has four motorcycle assembly plants, one each for MODENAS,

Honda, Yamaha, and Suzuki. The integrated complex in Pekan, Pahang is designed for passenger, commercial and defence vehicles with an annual capacity of 96,000 vehicles, of which just 18% of the capacity is currently utilised. The plants here

assemble for brands like Mercedes, Suzuki and Isuzu with an output of about 17,000 units p.a. at present.

Assembly contract with Volkswagen. DRBH also assembles Volkswagen (VW) vehicles in Malaysia through its

collaboration with the German automaker. VW aims to expand its market share in ASEAN and plans to position itself to

compete with the Japanese makes i.e. Toyota, Honda and Nissan. We opine that the group can benefit from VW’s plans to establish itself as an assembly hub for VW cars in ASEAN.

Acquisition of Proton. The group completed its acquisition of national carmaker Proton Holdings in last June 2012. We view the acquisition as a win-win situation for both DRBH and Proton. With Proton under its stable, DRBH is now the

country’s single largest automotive group with multiple brand representations, enabling it to rival the strong alliance between Perusahaan Otomobil Kedua Sdn Bhd (Perodua) and Toyota Malaysia. DRBH will be able to leverage on Proton’s

strong sales volume and utilise the extra auto manufacturing capacity at the latter’s underutilised Tanjung Malim plant. On the other hand, Proton will gain from DRBH’s partnerships with renowned automakers.

Proton has two vehicle manufacturing plant—in Tanjung Malim, Perak and Shah Alam, Selangor. Its Tanjung Malim plant has an annual capacity of 150,000 units (two shifts) with a 60% automation level. Currently, the plant produces the Preve,

Persona and Gen 2 at a utilisation rate of 60-70%. Meanwhile, its older plant in Shah Alam includes the original Main Plant and the smaller Multi Vehicle Factory (MVF) with capacities of 150,000 units and 50,000 units respectively. The Main Plant

currently produces the Exora, Inspira and Saga models.

DRB-Hicom’s vehicle sales trend 2005-November 2012

0

4

8

12

16

20

24

28

32

36

20

40

60

80

100

120

140

160

180

2005 2006 2007 2008 2009 2010 2011 11M2012

%'000 units

Passenger Commercial TIV share

Source: MAA, Kenanga Research

Sales breakdown according to marques (passenger cars) Sales breakdown according to marques (commercial)

Honda

17.5 Suzuki

4.4

Mitsubishi

1.7

Audi

0.7

Proton

75.6

Isuzu

55.4

Mitsubishi

43.8

Hicom Perkasa

0.8

Source: Company, Kenanga Research Source: Company, Kenanga Research

DRB-Hicom 25 January 2013

Page 4 of 14 KENANGA RESEARCH

Volkswagen (VW)

On 21 Dec 2010, DRBH entered into a collaboration and licensing agreement with Volkswagen A Gand Volkswagen Group

Malaysia Sdn Bhd to collaborate in the assembly of VW vehicles in Malaysia. Under the agreement, DRBH will assemble

three models i.e. Passat, Jetta and Polo Sedan in its plant in Pekan, Pahang. At the moment, the assembly plant has a production capacity of 80 units per day on a single shift (29k units pa) and this will gradually increase to 40k units pa and

>100k by 2016 and 2018 respectively. Production of the Jetta and Polo Sedan has started in mid-December 2012 with c.1,000 units of the Passat (B series) having been assembled already.

VW is looking to grow its presence in the Malaysian passenger car market as well as in ASEAN. It plans to increase its market share from currently c.2% to 10%. The collaboration with DRBH has enabled VW to leverage on DRBH’s distribution

channels. It is said that the company also planned to have a joint-venture with DRBH for its sales operations.

Proton Holdings

On 16 Mar 2012, Proton Holdings Berhad became a 50.4% subsidiary of the group after the latter acquired Proton’s 42.7%

stake at RM5.50/share bought a 7.7% stake from the market. DRBH also later undertook a mandatory general offer (MGO) for the remaining Proton shares at the same price. The MGO was later completed and Proton shares were then fully

acquired by DRBH in end-June 2012. DRBH’s interest in Proton is seen as a defensive move as 60% of its revenue in its

automotive division comes from Proton—Edaran Otomobil Nasional Berhad (EON), which sells cars for Proton, and the fact that several of its subsidiaries are Tier-1 vendors of auto parts to Proton.

Part of the group’s plans to revive Proton is to increase its local sales by introducing new models (e.g. Perdana replacement) through the sharing of platform with its key auto partners to improve cost efficiency. On 20 Oct 2012, Proton

entered into a collaboration agreement with Honda Motor Co. Ltd to explore opportunities in technology enhancement, new product line-up, platform and facilities sharing. Having a strong and renowned global automotive player like Honda Motor

as a foreign strategic partner will provide Proton and DRBH the opportunity to grow as an Original Equipment Manufacturer. The sharing of platform and facilities will improve Proton’s cost efficiency as well as build up production at its

underutilised plants.

The group also subsequently conducted an internal reorganisation exercise to streamline and consolidate the operations of

Proton Edar Sdn Bhd (Proton’s marketing and distribution arm) and EON. The exercise among others, included the sale, transfer and assignment of EON’s assets and liabilities, and employees to Proton Edar— for a total cash consideration of

RM401m. Going forward, the group may look into reducing the number of Proton Edar and EON’s outlets. Currently, there are c.270 outlets in total, of which 150 is owned by Proton Edar and 80 by EON. We expect the exercise to be beneficial in

the long term as it will bring greater operational efficiency and cost savings as well as providing more integrated services to customers. There are also plans to refurbish and further upgrade the outlets to 3S/4S centers.

Other revival plans include increasing the exports of Proton cars to ASEAN countries, Australia, the UK, China, MENA and Europe. Management is targeting exports of 20,000 units in FY14 (10% of its domestic volume). With these plans in place,

pretax margin at Proton is expected to increase to 5-8% within 3 years.

Lotus

Another key concern for the group is Lotus Group International, which has been dragging Proton’s earnings performance.

For 9MFY12, Lotus recorded an operating loss of RM167m, an increase of 62% YoY as the revenue fell 12% YoY to RM428m. Meanwhile, Proton posted a net loss of RM68m (9MFY11: net profit of RM91m) and a 12% YoY drop in revenue

to RM6.0b.

Lotus has outlined a 5-year turnaround plan which will be done in three phases. The first phase involves the launch of Elise

S and Exige S, which took place recently (8 Jan 2013) together with the official opening of its Malaysian showroom in Selangor. For 2013-14, the company is targeting a production of 3,000-4,000 units, which if sold, will ensure that it breaks

even financially in FY15. For phase two (in FY13-14), Lotus plans to market the Elise S and Exige S in China as well as introduce two new variants for Evora while in FY14-15, it will introduce new variants of the Elise and Exige. Lastly, phase

three will see the launch of its new generation cars—Esprit, Eterne and Elite.

Lotus Elise S and Exige S

Elise S Exige S

Source: MAA, Kenanga Research

DRB-Hicom 25 January 2013

Page 5 of 14 KENANGA RESEARCH

Deftech

On 23 Feb 2011, the Government awarded DRB-HICOM Defence Technologies Sdn Bhd (DEFTECH), the group’s wholly-

owned subsidiary, a seven-year contract worth RM7.55b to design, manufacture and deliver 257 units of 12 variants of 8x8

Armoured Wheeled Vehicles. According to management, production is expected to start in early 2013 and the earnings contribution should start coming in from FY14 onwards.

MODENAS

Syarikat Motosikal dan Enjin Nasional Sdn Bhd (National Motorcycle and Engine Company), or better known as Modenas is

a national motorcycle company producing various small motorcycle models below 200cc targeted for the local market and for export. The company’s technology partner is Kawasaki Heavy Industries. Apart from DRBH, the other shareholders

include Kawasaki, Sojitz, and Khazanah Nasional.

Modenas has 206 dealerships located across Malaysia and is planning to set up seven more. For 9M2012, the company

generated a total domestic sale of 48,000 units. It also exports to countries like Fiji, Greece, Iran, Laos, Singapore and Turkey and is eyeing extend its reach to Indonesia, Philippines, Vietnam and Cambodia.

SERVICES

The services segment is the group’s second largest division. This division has a diverse collection of businesses which include concession-based operations such as solid waste management, vehicle inspection, airport services and power plant

operations and maintenance, as well as financial services and trading companies. These businesses provide a stable

recurring income for the group, driven mainly by banking (Bank Muamalat Malaysia) and postal services (Pos Malaysia).

Bank Muamalat Malaysia Berhad (BMMB)

Bank Muamalat Malaysia Berhad (BMMB) is the second full-fledged Islamic bank established in Malaysia after Bank Islam Malaysia Berhad. On 10 Oct 2007, Bukhary Capital SdnBhd made an offer to DRBH to sell its entire 70% stake in BMMB

for RM1.1b to be satisfied entirely by the issuance of 548.7m new DRBH's shares at RM1.95 per share. The bank’s main business focus is on fee income generation particularly in trade finance, treasury activities, investment banking and

transactional banking as well as in wealth management, Bancatakaful services and Ar-Rahnu business. To comply with Bank Negara Malaysia’s (BNM) guidelines, DRBH needs to pare down its 70% stake in BMMB to 40%. The group is

currently in talks with Affin Bank Holdings Bhd on the potential sale of its 30% stake in BMMB. However, the talks may or may not succeed as we believe the group could be considering proposals from other parties considering its plans to want

to create a mega-Islamic bank. We estimate that a sale will likely raise RM600m in potential cash proceeds for the group (at 1.4x FY12 BV valuation).

Pos Malaysia (POSM)

DRBH completed its acquisition of a 32.2% stake in POSM from Khazanah Nasional Berhad in July 2011. The group plans to leverage on POSM’s extensive network to promote its wide range of products and services especially for its insurance,

logistic and banking businesses. POSM has 700 outlets scattered across not only in the state capitals and major towns but

also in the small towns and rural areas.

POSM is trying to reduce its dependency on the core mail business, which made up 62% of its 15-month (ended 31 Mar

2012) revenue of RM1.48b. It has implemented an aggressive 5-year plan aimed at achieving double digit growth in revenues every year till 2017, significantly improve its current pretax margins of 12%, and explore new merger and

acquisition opportunities. The company is now in the second phase of its transformation plan.

In June 2012, the company formed a strategic partnership with BMMB to offer Islamic pawn broking business (Ar-Rahnu)

at selected POSM outlets. The Ar-Rahnu services is carried out and managed by a 80:20 (POSM: BMMB) JV company known as Pos Ar-Rahnu Sdn Bhd under the brand name of ArRahnu@POS. The offering of ArRahnu@POS would enhance

the product offering at POSM outlets as it provides an alternative to obtain micro credit for the general public and small time entrepreneurs that may have difficulty in obtaining financing from the banks.

Other synergies to be realised by DRBH include the use of POSM courier services by companies under the DRB-Hicom umbrella especially for those in the automotive segment and its airport ground-handling services (Kuala Lumpur Airport

Services (KLAS).

DRB-Hicom 25 January 2013

Page 6 of 14 KENANGA RESEARCH

Uni.Asia Capital

DRBH through its wholly-owned subsidiary, Gadek (M) Bhd has a 51% stake in Uni.Asia Capital SdnBhd, which provides

life and general insurance (motor, business, health, personal and specialised) through Uni.Asia Life Assurance Berhad (UAL) and Uni.Asia General Insurance Berhad (UAG). The United Overseas Bank (M) Bhd (UOB) owns the remaining 49%

of Uni.Asia Capital. Earlier in August 2012, DRBH was given the green light by Bank Negara Malaysia (BNM) to start preliminary negotiations with interested parties for the sale of its insurance business. We understand that the group is

looking to replace the insurance business with takaful (Islamic insurance). This in turn will enable the group to be syariah-compliant. The sale of the insurance business here will likely raise RM376m for the group based on 2.0x FY12 BV

valuation and is expected to be completed by 4QFY13.

PUSPAKOM

PUSPAKOM Sdn Bhd is the country’s only comprehensive national vehicle inspection company. The concession awarded to

the company for the exclusive rights and authority to carry out motor vehicle inspection and testing activities has been recently extended for another 15 years. This followed a new agreement concluded with the Government on 25 Feb 2011

that extended its concession until 31 Aug 2024. Its future plans include the setting up of two new branches to carry out inspection services while eight others will be relocated for operational efficiencies. The company has also set up seven

new hire purchase inspection branches throughout the peninsula and installed additional lanes in five existing branches in order to support this.

Alam Flora

Alam Flora is one of the leading solid waste management companies in Southeast Asia, serving 30% of the Malaysian

population. Alam Flora manages the central and east zones comprising the Federal Territory of Kuala Lumpur, Putrajaya, and Pahang and is set to expand its services to Terengganu and Kelantan by the end of 2012. The company will invest in

research and development and collaborate with local universities to further develop its systems and technologies.

KL Airport Services (KLAS)

KL Airport Services Sdn Bhd (KLAS) is among the group’s star performers. It provides services such as ground handling,

cargo handling, in-flight catering and aircraft maintenance and engineering services. For FY11, KLAS registered a pretax profit of RM21.4m, or 64% above its budget, which was attributed to the increase in ground handling and engineering

activities from new customers secured and increased frequencies from the existing ones. KLAS also benefited from an increase in cargo tonnage and terminal charges and a substantial growth in its customs freight agent business. Going

forward, KLAS is likely to venture into the logistic value chain and expand its business to KLIA2.

PROPERTY, ASSET AND CONSTRUCTION (PAC)

The group through its PAC segment is engaged in the construction of integrated townships, industrial parks and the development of retail, commercial and residential properties. The Property and Infrastructure segment’s operations

include Glenmarie Cove Development Sdn Bhd, HICOM Properties Sdn Bhd, Horsedale Development Berhad, Imatex Sdn Bhd and Rebak Island Marina Berhad.

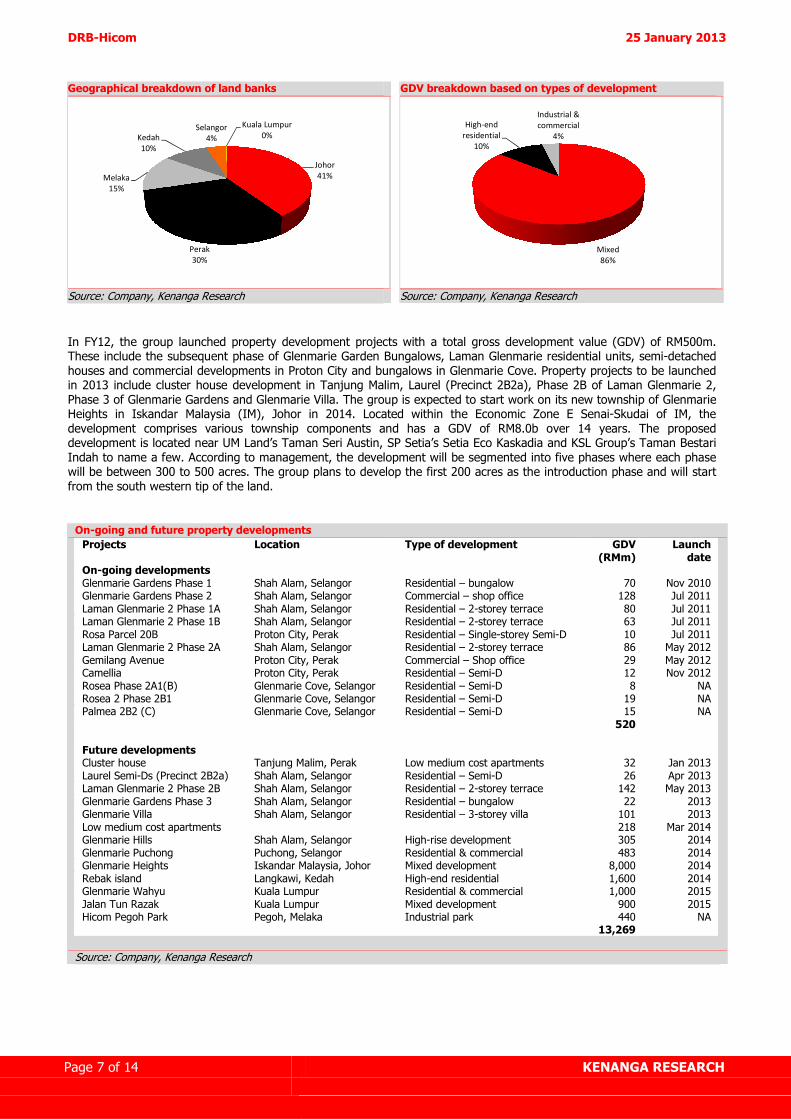

Property

The Group owns a sizable land bank which spans about 3,736 acres (163 million sf) with a total gross development value

of RM21b. Its key land banks are located in Johor (Glenmarie Heights: 1,517 acres), Perak (Proton City: 1,107 acres) and Melaka (Hicom Pegoh Park: 551 acres). A large portion of the group’s property portfolio consist of mixed development

projects (86%) with the balance from high-end residential (10%) and industrial and commercial projects (4%).

DRB-Hicom 25 January 2013

Page 7 of 14 KENANGA RESEARCH

Geographical breakdown of land banks GDV breakdown based on types of development

Johor

41%

Perak

30%

Melaka

15%

Kedah

10%

Selangor

4%

Kuala Lumpur

0%

Mixed

86%

High-end

residential

10%

Industrial &

commercial

4%

Source: Company, Kenanga Research Source: Company, Kenanga Research

In FY12, the group launched property development projects with a total gross development value (GDV) of RM500m. These include the subsequent phase of Glenmarie Garden Bungalows, Laman Glenmarie residential units, semi-detached

houses and commercial developments in Proton City and bungalows in Glenmarie Cove. Property projects to be launched in 2013 include cluster house development in Tanjung Malim, Laurel (Precinct 2B2a), Phase 2B of Laman Glenmarie 2,

Phase 3 of Glenmarie Gardens and Glenmarie Villa. The group is expected to start work on its new township of Glenmarie Heights in Iskandar Malaysia (IM), Johor in 2014. Located within the Economic Zone E Senai-Skudai of IM, the

development comprises various township components and has a GDV of RM8.0b over 14 years. The proposed development is located near UM Land’s Taman Seri Austin, SP Setia’s Setia Eco Kaskadia and KSL Group’s Taman Bestari

Indah to name a few. According to management, the development will be segmented into five phases where each phase will be between 300 to 500 acres. The group plans to develop the first 200 acres as the introduction phase and will start

from the south western tip of the land.

On-going and future property developments

Projects Location Type of development GDV (RMm)

Launch date

On-going developments Glenmarie Gardens Phase 1 Shah Alam, Selangor Residential – bungalow 70 Nov 2010 Glenmarie Gardens Phase 2 Shah Alam, Selangor Commercial – shop office 128 Jul 2011 Laman Glenmarie 2 Phase 1A Shah Alam, Selangor Residential – 2-storey terrace 80 Jul 2011 Laman Glenmarie 2 Phase 1B Shah Alam, Selangor Residential – 2-storey terrace 63 Jul 2011 Rosa Parcel 20B Proton City, Perak Residential – Single-storey Semi-D 10 Jul 2011 Laman Glenmarie 2 Phase 2A Shah Alam, Selangor Residential – 2-storey terrace 86 May 2012 Gemilang Avenue Proton City, Perak Commercial – Shop office 29 May 2012 Camellia Proton City, Perak Residential – Semi-D 12 Nov 2012 Rosea Phase 2A1(B) Glenmarie Cove, Selangor Residential – Semi-D 8 NA Rosea 2 Phase 2B1 Glenmarie Cove, Selangor Residential – Semi-D 19 NA Palmea 2B2 (C) Glenmarie Cove, Selangor Residential – Semi-D 15 NA 520 Future developments Cluster house Tanjung Malim, Perak Low medium cost apartments 32 Jan 2013 Laurel Semi-Ds (Precinct 2B2a) Shah Alam, Selangor Residential – Semi-D 26 Apr 2013 Laman Glenmarie 2 Phase 2B Shah Alam, Selangor Residential – 2-storey terrace 142 May 2013 Glenmarie Gardens Phase 3 Shah Alam, Selangor Residential – bungalow 22 2013 Glenmarie Villa Shah Alam, Selangor Residential – 3-storey villa 101 2013 Low medium cost apartments 218 Mar 2014 Glenmarie Hills Shah Alam, Selangor High-rise development 305 2014 Glenmarie Puchong Puchong, Selangor Residential & commercial 483 2014 Glenmarie Heights Iskandar Malaysia, Johor Mixed development 8,000 2014 Rebak island Langkawi, Kedah High-end residential 1,600 2014 Glenmarie Wahyu Kuala Lumpur Residential & commercial 1,000 2015 Jalan Tun Razak Kuala Lumpur Mixed development 900 2015 Hicom Pegoh Park Pegoh, Melaka Industrial park 440 NA 13,269

Source: Company, Kenanga Research

DRB-Hicom 25 January 2013

Page 8 of 14 KENANGA RESEARCH

Construction

Hicom Builders Sdn Bhd (HBSB) is now the group’s main construction arm following an operational merger and

rationalisation exercise involving Comtrac Sdn Bhd (Comtrac). HBSB will undertake all major construction projects within the group while Comtrac will focus on external projects. HBSB was awarded a contract worth RM855m to lay railway

tracks for the Sungai Buloh-Kajang MY Rapid Transit (SBK MRT) project, which it had jointly bid with Mitsubishi Heavy Industries Ltd, a Japanese multinational engineering, electrical equipment and electronics group. It is understood that the

two would form a joint venture company (JVCo) but the stake allocation had not been disclosed. We reckon that the group’s interest in the JV Co could be less than 50% considering that HBSB is small and the construction arm is mainly

just to complement its property division. The JV could nonetheless serve as a stepping stone for the group’s construction division to acquire the necessary know-how to take up bigger construction projects in the future.

3. EARNINGS OUTLOOK

We project FY13 revenue to grow more than two-fold to RM15.1b from RM6.9b in FY12 mainly due to the inclusion of

Proton Holdings, while revenue growth in FY14 onwards will be underpinned by contribution from the AV8X8 contract and it property division.

Financial highlights for FY13F-15F

FY13F FY14F FY15F Assumptions

Revenue (RMm) 14,912 16,706 18,512

EBITDA (RMm) 1,399 1,605 1,827

Core net profit (RMm) 412 602 742

Core EPS (sen) 21.3 31.1 38.4

DPS (sen) 8.9 6.2 7.7 20% dividend payout

Revenue growth (%) 117 12 11 Revenue to grow more than double in FY13 due to the inclusion of Proton.

EBITDA growth (%) 111 15 14

Adj net profit growth (%) 28 46 23

Revenue breakdown

Automotive 12,152 14,472 15,385 Mainly contributed by Proton sales. AV8X8 contract to start contributing from FY14 onwards.

Services 2,583 1,770 1,907 Assume dilution of 30% stake in BMMB to take place in FY14

PAC 177 464 1,219 Higher revenue growth in FY14-15 to come from launches of property development projects, with total GDV of c.RM13bn.

EBIT breakdown

Automotive 425 507 538

Services 356 244 263

PAC 21 121 333

Others 52 119 38

Source: Kenanga Research

4. VALUATION & RECOMMENDATION

We are valuing DRBH using the sum-of-parts method. We have applied a 12x FY14 PER (PE multiple based on average

peer’s) to its automotive division while its concession-based businesses (Puspakom, Alam Flora and KL Airport Services) and property developments are valued based on the discounted cash flow (DCF) method. BMMB and POSM are valued

based on 1.4x FY12 P/BV and 12x FY14 PER respectively, and its investment properties are valued using book value. These valuations led us to arrive at a SOP/share (target price) of RM3.45, presenting a potential upside of 33% and a

total upside of 36% (inclusive of dividend). Hence, we are assigning an Outperform call on DRBH.

DRB-Hicom 25 January 2013

Page 9 of 14 KENANGA RESEARCH

Sum-of-parts valuation

Divisions Stake Method Value (RMm)

Automotive 100% 12x FY14 PER 4,699.6

Puspakom 100% DCF 210.8

Alam Flora 61% DCF 266.5

KL Airport Services 100% DCF 588.5

Bank Muamalat 70% 1.4x FY12 PBV 1,401.3

Pos Malaysia 32% 12x FY14 PER 553.8

Property

Developments 100% DCF 1,511.7

Investments

Parcels of land in Klang, Selangor 100% BV 122.9

Hicom Pegoh Industrial Park, Melaka 100% BV 412.8

Retail complex - The Verge, Singapore 83% BV 272.3

Menara Uni.Asia 100% BV 58.2

Menara Bumiputera 100% BV 90.5

Factory & land in Gurun, Kedah 100% BV 161.0

Factory & land in Pekan, Pahang 100% BV 128.7

Glenmarie Golf & Country Resort 100% BV 192.3

Rebak Island Resort, Langkawi 60% BV 47.1

Subtotal 10,718.1

Less: Net debt 4,059.2

Total 6,658.9

No. of shares 1,933.2

SOP/share 3.45 Source: Kenanga Research

5. RISKS

Weak economy. The automotive market correlates to the condition of the economy. Slowdown in the economy, rising oil prices and tightening of consumers’ purchasing power will negatively affect auto sales.

Declining consumer sentiments. Buying decisions could be affected by stricter hire purchase policies imposed by the banks. However, according to the Malaysian Automotive Association, car companies have adjusted to the new guidelines

and longer loan processing time.

Unfavorable forex trends. DRBH is exposed to currency risk (i.e. USD and JPY) as it imports auto parts, CKD kits and

CBUs. The weakening of the Ringgit against the US dollar and Japanese Yen may compress its margins.

6. APPENDIX

Brief background. DRB-HICOM Berhad (DRBH) was incorporated as Heavy Industries Corporation of Malaysia Berhad (HICOM) in 1980. HICOM was listed on the Main Board of the Kuala Lumpur Stock Exchange in 1992. It merged with

Diversified Resources Berhad (DRB) in 1996 to form the largest conglomerate in Malaysia. In 2006, the group was acquired by Etika Strategi Sdn Bhd and became one of the three flagships of the AlBukhary Group of Companies.

Business activities. DRBH is principally involved in three main segments: (i) automotive, (ii) services and (iii) property, asset and construction (PAC). In FY12, the automotive segment generated 59% of the total revenue while services and PAC

segments contributed 37% and 4% respectively. However the main, contributor at the operating profit level was the services segment (70%) while automotive only contributed 29% due to its low margins.

DRB-Hicom 25 January 2013

Page 10 of 14 KENANGA RESEARCH

FY12 revenue breakdown FY12 operating breakdown

Automotive59%

Services37%

Property, asset & construction

4%

Automotive29%

Services70%

Property, asset & construction

1%

Source: Company, Kenanga Research Source: Company, Kenanga Research

Organization chart

Note: The list is not exhaustive

Source: Company

DRB-Hicom 25 January 2013

Page 11 of 14 KENANGA RESEARCH

Board of Directors

Name Current appointment Experience

Dato’ Syed Mohamed bin Syed Murtaza

Chairman/Senior Independent Non-Executive Director

Dato’ Syed Mohamad is the Managing Director of Amstrong Auto Parts Sdn Bhd. He also heads Penang Tourists Centre Bhd, MITTAS Bhd, Motorcycle, Scooter Assembly & Distributor Association of Malaysia and the Usains Group of Companies. He is President of both the Federation of Asian Motorcycle Industries and the International Motorcycle Manufacturers Association. His current directorships in companies within the DRB-HICOM Group include HICOM Holdings Bhd, HICOM Bhd and several private limited companies.

Dato’ Sri Haji Mohd Khamil bin Jamil

Group Managing Director His current directorships in companies within the DRB-HICOM Group include Edaran Otomobil Nasional Bhd, HICOM Holdings Bhd, HICOM Bhd, Horsedale Development Bhd, Bank Muamalat Malaysia Bhd, Uni.Asia General Insurance Bhd, Uni.Asia Life Assurance Bhd, Pos Malaysia Bhd and several private limited companies. Dato’ Sri Haji MohdKhamil is a Director of Etika Strategi Sdn Bhd, the holding company of DRB-HICOM Bhd in which he has a 10% shareholding.

Ooi Teik Huat Independent Non-Executive Director Mr Ooi is presently a Director of Meridian Solutions Sdn Bhd and sits on the boards of Tradewinds Plantation Bhd, Tradewinds (M) Bhd, MMC Corporation Bhd, Zelan Bhd, Johor Port Bhd and several private limited companies.

Dato’ Noorrizan bt Shafie Non-Independent Non-Executive Director Dato’ Noorrizan is currently the Under Secretary, Remuneration Policy, Public Money and Management Service Division, Treasury, Ministry of Finance. She started her career in the Civil Service in 1981 and has served in various positions with the Economic Planning Unit in the Prime Minister’s Department, Public Services Department and Ministry of Finance. Dato’ Noorrizan is a Non-Independent Director nominated by the Ministry of Finance. She also sits on the Board of HICOM Holdings Bhd.

Dato’ Ibrahim bin Taib Non-Independent Non-Executive Director Dato’ Ibrahim sits on the Board of Bandar Eco-Setia Sdn Bhd, Iskandar Investment Bhd and KWASA Properties Sdn Bhd. He is a Non-Independent Director nominated by the company’s substantial shareholder, the Employees Provident Fund.

Ong Ie Chong Independent Non-Executive Director Mr Ong was the Executive Chairman of PPB Group Bhd, Managing Director of Central Sugars Refinery Sdn Bhd and a Board member of PPB Oil Palms Bhd and Tradewinds (M) Bhd prior to joining the DRB-HICOM Board. His current directorships in the companies within the DRB-HICOM Group include HICOM Holdings Bhd, HICOM Bhd and several private limited companies.

Tan Sri Marzuki bin Mohd Noor Independent Non-Executive Director His current directorships include being the Chairman of Edaran Otomobil Nasional Bhd and Director of Horsedale Development Bhd, HICOM Holdings Bhd and several private limited companies.

Source: Company

DRB-Hicom 25 January 2013

Page 12 of 14 KENANGA RESEARCH

Income Statement Financial Data & Ratios

FY Mar (RM’m) 2011A 2012A 2013E 2014E 2015E FY Mar (RM’m) 2011A 2012A 2013E 2014E 2015E

Revenue 6,804.1 6,878.2 14,911.9 16,706.1 18,512.2 Growth (%)

EBITDA 586.3 653.4 1,398.9 1,605.3 1,827.0 Turnover 7.8 1.1 116.8 12.0 10.8

Depreciation -145.4 -179.2 -544.5 -614.1 -654.3 EBITDA -16.3 11.4 114.1 14.7 13.8

Operating Profit 440.9 474.2 854.5 991.1 1,172.7 Opg Profit -22.1 7.6 80.2 16.0 18.3

Other Income 0.0 0.0 0.0 0.0 0.0 PBT 6.6 115.6 -19.8 -27.1 21.5

Interest Exp -39.6 -100.9 -377.9 -453.5 -456.3 Core Net Profit -15.0 -19.9 28.2 46.0 23.4

Associate 229.0 167.7 290.3 346.2 357.9

Exceptional Items 71.2 971.5 446.2 0.0 0.0 Profitability (%)

PBT 701.5 1,512.6 1,213.0 883.8 1,074.3 EBITDA Margin 8.6 9.5 9.4 9.6 9.9

Taxation -131.3 -148.0 -230.7 -134.4 -179.1 Operating Margin 6.5 6.9 5.7 5.9 6.3

Minority Interest -97.7 -71.6 -123.9 -147.7 -152.7 PBT Margin 10.3 22.0 8.1 5.3 5.8

Net Profit 472.5 1,293.0 858.5 601.7 742.4 Core Net Margin 6.9 18.8 5.8 3.6 4.0

Core Net Profit 401.3 321.5 412.3 601.7 742.4 Effective Tax Rate 27.8 11.0 25.0 25.0 25.0

ROA 1.7 3.8 2.0 1.4 1.6

Balance Sheet ROE 9.9 23.2 13.2 8.5 9.7

FY Mar (RM’m) 2011A 2012A 2013E 2014E 2015E

Fixed Assets 2,787.3 5,554.6 6,435.1 6,821.0 7,166.6 DuPont Analysis

Intangible Assets 219.0 1,606.0 1,606.0 1,606.0 1,606.0 Net Margin (%) 6.9 18.8 5.8 3.6 4.0

Other FA 11,075.5 16,230.3 16,230.3 16,230.3 16,230.3 Assets Turnover

(x) 4.2 5.8 3.1 2.6 2.6

Inventories 523.5 1,516.8 2,912.4 2,037.2 3,431.7 Leverage Factor (x) 5.7 6.5 6.6 5.8 6.1

Receivables 1,330.6 3,173.1 6,590.9 4,347.9 7,773.5 ROE (%) 9.9 23.2 13.2 8.5 9.7

Other CA 11,009.7 8,700.1 8,700.1 8,700.1 8,700.1

Cash 1,350.3 3,040.3 3,040.3 3,040.3 3,040.3 Leverage

Total Assets 28,295.9 39,821.1 45,515.0 42,782.8 47,948.5 Debt/Asset (x) 0.0 0.1 0.2 0.2 0.2

Debt/Equity (x) 0.3 0.9 1.4 1.0 1.2

Payables 2,058.8 5,961.1 8,304.1 7,637.3 9,976.7 Net Cash/(Debt) 3.9 -

2327.2 -

6376.3 -

4066.4 -

6442.9

ST Borrowings 521.2 1,892.0 5,941.1 3,631.2 6,007.7 Net Debt/Equity

(x) 0.0 0.4 0.9 0.6 0.8

Other ST Liability 16,853.4 19,037.4 17,652.4 17,415.4 17,271.4

LT Borrowings 825.2 3,475.6 3,475.6 3,475.6 3,475.6 Valuations

Other LT Liability 1,905.2 2,161.9 2,161.9 2,161.9 2,161.9 EPS (sen) 24.4 66.9 44.4 31.1 38.4

Minorities Int. 1,242.8 1,151.8 1,131.6 1,131.6 1,131.6 NDPS (sen) 6.0 6.0 8.9 6.2 7.7

Net Assets 8,862.5 12,930.7 13,617.5 14,098.8 14,692.8 BVPS (RM) 2.58 3.19 3.54 3.79 4.10

PER (x) 10.6 3.9 5.8 8.3 6.7

Shareholders' equity 4,980.3 6,161.7 6,848.4 7,329.8 7,923.7 Net Div. Yield (%) 2.3 2.3 3.4 2.4 3.0

Minority interest 1,151.8 1,131.6 1,131.6 1,131.6 1,131.6 PBV (x) 1.0 0.8 0.7 0.7 0.6

Total Equity 6,132.1 7,293.3 7,980.0 8,461.4 9,055.4 EV/EBITDA (x) 7.8 8.4 4.0 3.5 3.1

Cashflow Statement

FY Mar (RM’m) 2011A 2012A 2013E 2014E 2015E

Operating CF 1,622.2 1,622.2 2,367.8 -1,233.8 3,468.7

Investing CF -728.7 -3,854.6 -2,715.0 -1,000.0 -1,000.0

Financing CF -65.2 -87.0 -171.7 -120.3 -148.5

Change In Cash 828.3 -2,319.4 -518.9 -2,354.2 2,320.2

Free CF 1,761.7 1,878.1 3,792.8 -233.8 4,468.7

Source: Kenanga Research

Fwd PER Band Fwd PBV Band

0

1

2

3

4

5

6

7

8

Jan-0

9

Apr

-09

Jul-09

Oct

-09

Jan-1

0

Apr

-10

Jul-10

Oct

-10

Jan-1

1

Apr

-11

Jul-11

Oct

-11

Jan-1

2

Apr

-12

Jul-12

Oct

-12

Jan-1

3

PRICE (RM) PER 2.2 x PER 4.5 x PER 6.9 x PER 9.2 x PER 11.6 x

0

0.5

1

1.5

2

2.5

3

3.5

Jan-0

9

Apr

-09

Jul-09

Oct

-09

Jan-1

0

Apr

-10

Jul-10

Oct

-10

Jan-1

1

Apr

-11

Jul-11

Oct

-11

Jan-1

2

Apr

-12

Jul-12

Oct

-12

Jan-1

3

PRICE (RM) PBV 0.2 x PBV 0.5 x PBV 0.7 x PBV 0.9 x PBV 1.1 x

Source: Kenanga Research

DRB-Hicom 25 January 2013

Page 13 of 14 KENANGA RESEARCH

Malaysian Automobile Sector Comparisons

Price Mkt Cap

PER (x) Est. Div. Yld.

Est. ROE

P/BV Net Profit (RMm) 1 Yr Fwd NP

Growth

2 Yr Fwd NP

Growth

Target Price

Rating NAME

(RM) (RMm) Actual 1 Yr Fwd

2 Yr Fwd

(%) (%) (x) Actual 1 Yr Fwd

2 Yr Fwd

(%) (%) (RM)

DRB-HICOM BHD 2.60 5026.4 3.9 5.9 8.2 3.4 12.5 0.7 1302.0 853.0 615.0 -34.5 -27.9 3.45 Outperform MBM RESOURCES BERHAD 3.51 1371.1 11.3 9.0 7.9 1.3 19.1 1.7 120.9 151.8 172.5 25.6 13.6 3.68 Market Perform TAN CHONG MOTOR HOLDINGS BHD 5.08 3316.3 15.3 20.1 11.3 1.2 9.2 1.9 216.1 165.1 293.3 -23.6 77.6 4.36 Market Perform

Source: Bloomberg, Kenanga Research

Page 14 of 14 KENANGA RESEARCH

Stock Ratings are defined as follows:

Stock Recommendations

OUTPERFORM : A particular stock’s Expected Total Return is MORE than 10% (An approximation to the 5-year annualised Total Return of FBMKLCI of 10.2%)

MARKET PERFORM : A particular stock’s Expected Total Return is WITHIN the range of 3% to 10%

UNDERPERFORM : A particular stock’s Expected Total Return is LESS than 3% (An approximation to the 12-month Fixed Deposit Rate of 3.15% as a proxy to Risk-Free Rate)

Sector Recommendations***

OVERWEIGHT : A particular stock’s Expected Total Return is MORE than 10% (An approximation to the 5-year annualised Total Return of FBMKLCI of 10.2%)

NEUTRAL : A particular stock’s Expected Total Return is WITHIN the range of 3% to 10% UNDERWEIGHT : A particular stock’s Expected Total Return is LESS than 3%

(An approximation to the 12-month Fixed Deposit Rate of 3.15% as a proxy to Risk-Free Rate)

***Sector recommendations are defined based on market capitalisation weighted average expected total return for stocks under our coverage.

This document has been prepared for general circulation based on information obtained from sources believed to be reliable but we do not make any representations as to its accuracy or completeness. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may read this document. This document is for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees. Kenanga Investment Bank Berhad accepts no liability whatsoever for any direct or consequential loss arising from any use of this document or any solicitations of an offer to buy or sell any securities. Kenanga Investment Bank Berhad and its associates, their directors, and/or employees may have positions in, and may effect transactions in securities mentioned herein from time to time in the open market or otherwise, and may receive brokerage fees or act as principal or agent in dealings with respect to these companies.

Published and printed by: KENANGA INVESTMENT BANK BERHAD (15678-H) 8th Floor, Kenanga International, Jalan Sultan Ismail, 50250 Kuala Lumpur, Malaysia Chan Ken Yew Telephone: (603) 2166 6822 Facsimile: (603) 2166 6823 Website: www.kenangaresearch.com Head of Research