dry bulk freight market: prospects for recovery

TRANSCRIPT

May 2013

Whilst care and attention has been taken to ensure that the information contained is accurate, it

is supplied without guarantee. SSY Consultancy & Research can accept no responsibility for any

errors or omissions or consequences arising therefrom.

Dry Bulk Freight Market:

Prospects For Recovery

Platts 9th Steel Markets Europe Conference

London 24 May 2013

freight story in the year to date

• capes experience major seasonal plunge in earnings for fourth consecutive year due to reduced cargo availability and re-acceleration in newbuilding deliveries

• panamax spot earnings briefly reach 10-month high as congestion exaggerates Latin America grain effect

• soft start to the year for geared vessels before seasonal upswing re-establishes supras as highest earning sector in year to date

• uneven shift in sentiment

May 2013

capesize iron ore spot rates to China:

monthly averages

0

10

20

30

40

50

60

70

80

90

100Jan

-03

Ju

l-03

Jan

-04

Ju

l-0

4

Jan

-05

Ju

l-05

Jan

-06

Ju

l-06

Jan

-07

Ju

l-07

Jan

-08

Ju

l-08

Jan

-09

Ju

l-09

Jan

-10

Ju

l-10

Jan

-11

Ju

l-1

1

Jan

-12

Ju

l-12

Jan

-13

$/t

W.Australia

Brazil

May 2013

freight’s share of delivered iron ore prices

to China

May 2013

0

10

20

30

40

50

60

70

Ja

n-0

6

Ap

r-0

6

Ju

l-0

6

Oct

-06

Ja

n-0

7

Ap

r-0

7

Ju

l-0

7

Oct

-07

Ja

n-0

8

Ap

r-0

8

Ju

l-0

8

Oct

-08

Ja

n-0

9

Ap

r-0

9

Ju

l-0

9

Oct

-09

Ja

n-1

0

Ap

r-1

0

Ju

l-1

0

Oct

-10

Ja

n-1

1

Ap

r-1

1

Ju

l-1

1

Oct

-11

Ja

n-1

2

Ap

r-1

2

Ju

l-1

2

Oct

-12

Ja

n-1

3

Ap

r-1

3

% S

ha

re

Australia Avg 2006-13

Brazil Avg 2006-13

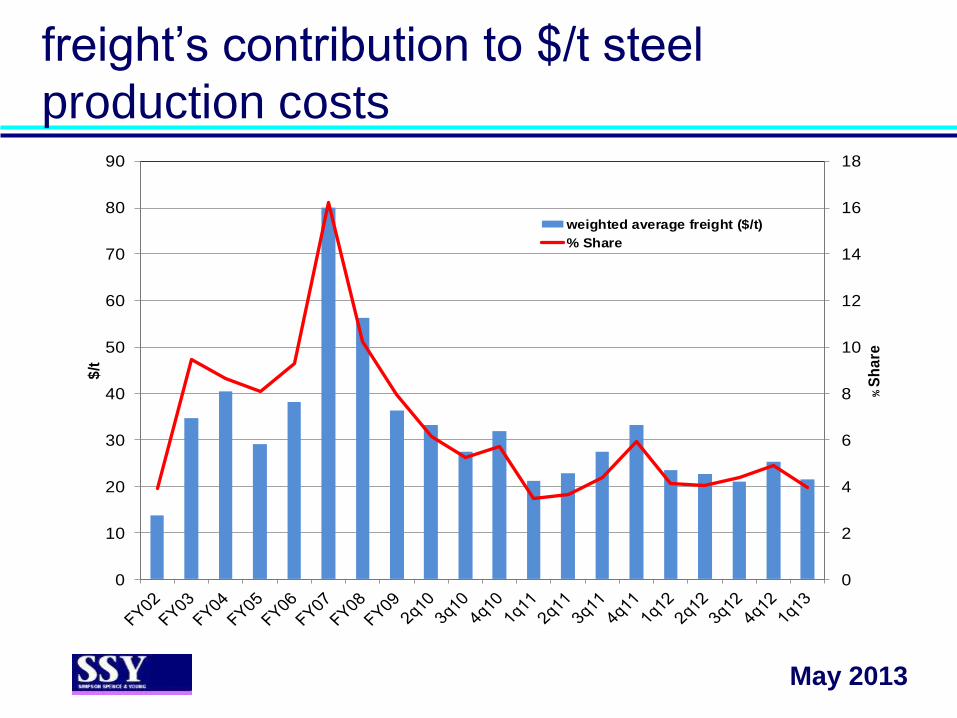

freight’s contribution to $/t steel

production costs

May 2013

0

2

4

6

8

10

12

14

16

18

0

10

20

30

40

50

60

70

80

90

% S

ha

re

$/t

weighted average freight ($/t)

% Share

4

6

8

10

12

14

16

18

20

Jan

-09

Ju

l-09

Jan

-10

Ju

l-10

Jan

-11

Ju

l-11

Jan

-12

Ju

l-12

Jan

-13

Ju

l-13

Jan

-14

Ju

l-14

Jan

-15

Ju

l-15

$/t

Actual FFA (23 May 13)

W.Australia-China capesize iron ore rates

May 2013

does freight have any more surprises for

the steel and iron ore industry?

• dry bulk market overwhelmed by excess newbuilding deliveries…

• but positive Chinese-led trade growth continues

• with planned influx of additional iron ore export capacity planned adding to upside for dry bulk trade

• depressed freight rates have triggered supply-side responses - slower steaming, record scrapping and reduced newbuilding orderbook

• port congestion remains a feature of the iron ore trades and potential source for future volatility

May 2013

quarterly dry bulk carrier deliveries by size

0

4

8

12

16

20

24

28

32

361q

08

2q

08

3q

08

4q

08

1q

09

2q

09

3q

09

4q

09

1q

10

2q

10

3q

10

4q

10

1q

11

2q

11

3q

11

4q

11

1q

12

2q

12

3q

12

4q

12

1q

13

2q

13(f

)

3q

13(f

)

4q

13(f

)

Md

wt

Capesize Panamax

Handymax Handy

May 2013

panamax has highest net fleet growth in

year to date

0

2

4

6

8

10

12

Handysize Handymax Panamax Capesize

MD

wt

Additions

Deletions

0.1 Mdwt

+0.1%

2.8 Mdwt

+1.9%

7.0 Mdwt

+2.5%

6.8 Mdwt

+4.1%

May 2013

New size range changes:

Handymax=40-64,999dwt Panamax=65-99,999dwt

SSY capesize iron ore port congestion

index for China

May 2013

0

2

4

6

8

10

12

14

16

18Ja

n-0

8

Ma

r-0

8

Ma

y-0

8

Ju

l-0

8

Se

p-0

8

No

v-0

8

Ja

n-0

9

Ma

r-0

9

Ma

y-0

9

Ju

l-0

9

Se

p-0

9

No

v-0

9

Ja

n-1

0

Ma

r-1

0

Ma

y-1

0

Ju

l-1

0

Se

p-1

0

No

v-1

0

Ja

n-1

1

Ma

r-1

1

Ma

y-1

1

Ju

l-1

1

Se

p-1

1

No

v-1

1

Ja

n-1

2

Ma

r-1

2

Ma

y-1

2

Ju

l-1

2

Se

p-1

2

No

v-1

2

Ja

n-1

3

Ma

r-1

3

Ma

y-1

3

We

igh

ted

ave

rag

e d

ela

ys

(d

ays

)

60 Capes =

4% of fleet

87 Capes =

10% of fleet

44 Capes = 3% of fleet

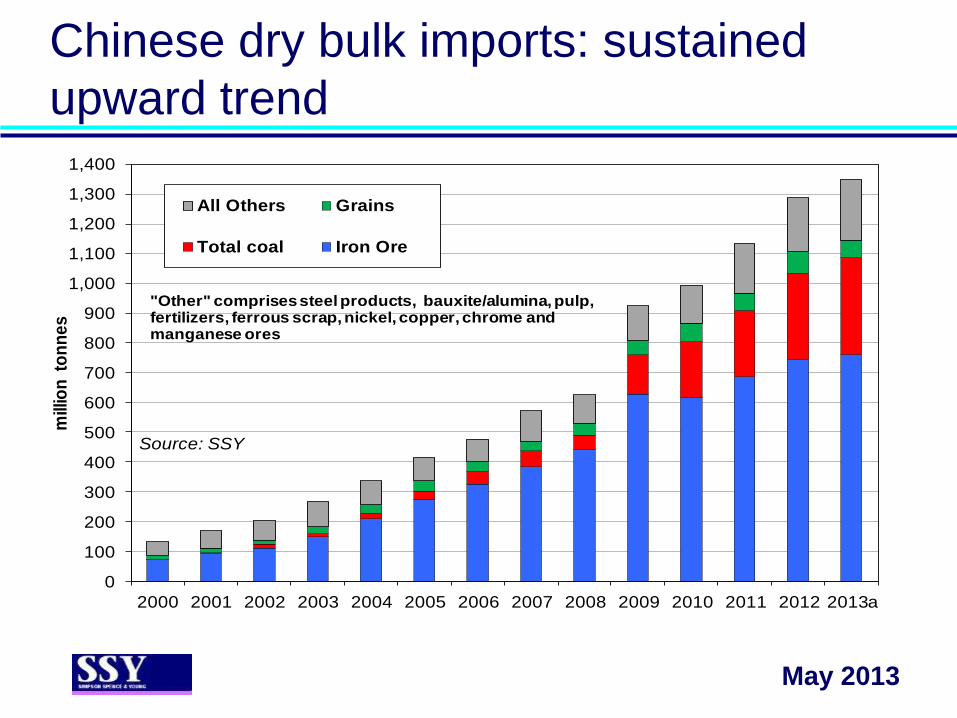

Chinese dry bulk imports: sustained

upward trend

May 2013

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013a

mill

ion

to

nn

es

All Others Grains

Total coal Iron Ore

Source: SSY

"Other" comprises steel products, bauxite/alumina, pulp, fertilizers, ferrous scrap, nickel, copper, chrome and manganese ores

Brazilian iron ore exports & Capesize

earnings

May 2013

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

60.0

65.0

70.0

75.0

80.0

85.0

90.0

95.0

100.0

1q10 2q10 3q10 4q10 1q11 2q11 3q11 4q11 1q12 2q12 3q12 4q12 1q13

$/D

ay

Millio

n to

nn

es

Exports Average TC Earnings

tonne-mile demand growth fails to match

expansion in iron ore trade volumes

May 2013

80

100

120

140

160

180

200

220

240

260

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Ind

ex

(2

00

0 =

10

0)

Cargoes Tonne-miles

is fleet supply growth finally coming

under control?

• dry bulk carrier demolition set a new annual record of

34 Mdwt in 2012 and ship scrap prices remain at

relatively firm levels

• falling asset values are expanding the demolition pool

beyond 25+ years for Panamaxes, as well as Capes

• newbuilding orderbook has fallen to a 5 year low with

financing of new orders a constraining factor

• …but with shipbuilding prices at lowest since 2003 and

yards marketing eco-designs, more Capesize

newbuilding contracts are emerging

May 2013

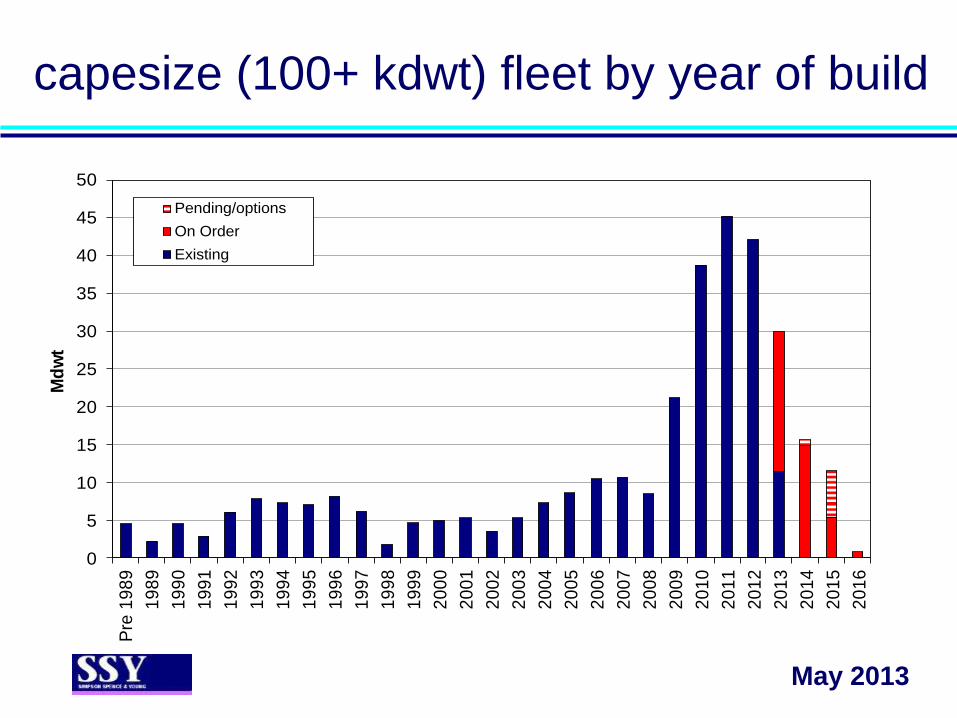

capesize (100+ kdwt) fleet by year of build

May 2013

0

5

10

15

20

25

30

35

40

45

50

Pre

19

89

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Md

wt

Pending/options

On Order

Existing

panamax (65-99 kdwt) fleet by year of

build

May 2013

0

5

10

15

20

25

30

35

Pre

19

89

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Md

wt

On Order Existing

dry bulk carrier demolition

May 2013

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0Ja

n-0

9

Ma

r-0

9

Ma

y-0

9

Ju

l-0

9

Se

p-0

9

No

v-0

9

Ja

n-1

0

Ma

r-1

0

Ma

y-1

0

Ju

l-1

0

Se

p-1

0

No

v-1

0

Ja

n-1

1

Ma

r-1

1

Ma

y-1

1

Ju

l-1

1

Se

p-1

1

No

v-1

1

Ja

n-1

2

Ma

r-1

2

Ma

y-1

2

Ju

l-1

2

Se

p-1

2

No

v-1

2

Ja

n-1

3

Ma

r-1

3

Millio

n D

wt

Monthly volume 3 month average

scrapping potential & tonnage on order

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

Handysize Handymax Panamax Capesize

MD

wt

On Order

25+ years

20+ years

15+years

May 2013

New size range changes:

Handymax=40-64,999dwt Panamax=65-99,999dwt

projected net fleet change in 2013

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Handysize Handymax Panamax Capesize

MD

wt

Additions

Deletions

0.0 Mdwt

0.0%

4.1 Mdwt

+2.8%

10.6 Mdwt +3.8% 16.9Mdwt

+10.3%

May 2013

New size range changes:

Handymax=40-64,999dwt Panamax=65-99,999dwt

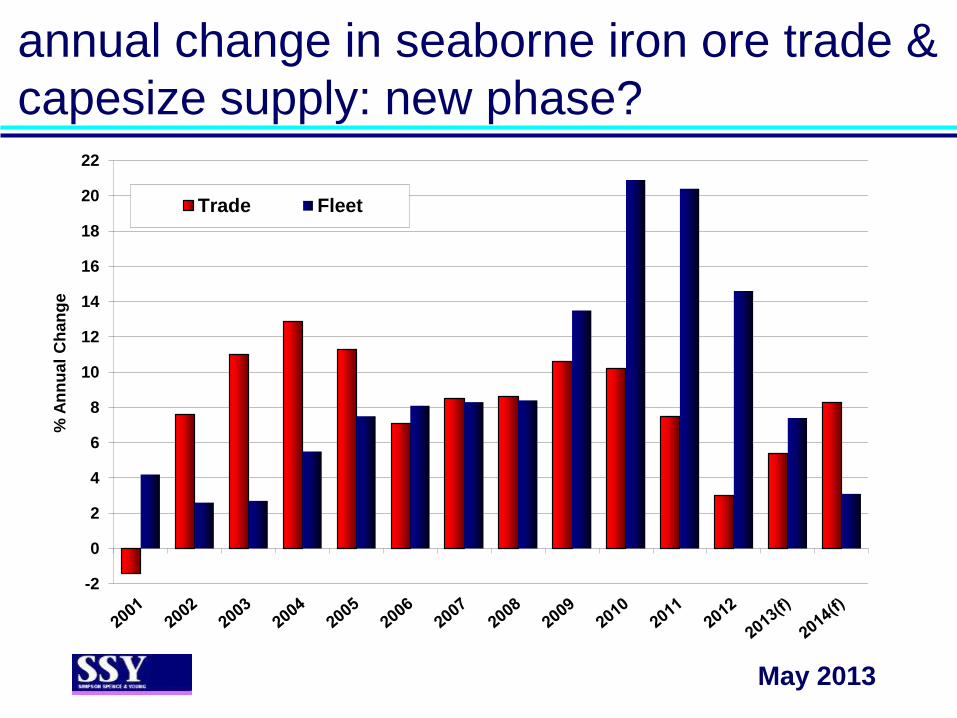

annual change in seaborne iron ore trade &

capesize supply: new phase?

-2

0

2

4

6

8

10

12

14

16

18

20

22

% A

nn

ua

l C

ha

ng

e

Trade Fleet

May 2013

conclusions

• by 4q13 rate of growth in seaborne iron ore trade set

to outpace increases in dry bulk fleet supply,

reversing trend of last 5 years

• prospect for divergence in relative rates of supply-

side growth to widen in 2014, adding to potential

freight rate volatility and raising freight’s share of

delivered iron ore prices

• but only if (1) record scrapping, (2) slower deliveries

and (3) sustained trade growth (requiring increased

cargo availability, as well as end-user demand)

May 2013

SSY LONDON TEL: +44 207 977 7404

SINGAPORE TEL: +65 6854 7122

email: [email protected]

web: ssyonline.com

May 2013