economic outlook and mortgage market implications

DESCRIPTION

Economic outlook and mortgage market implications. Little recovery in sight Martin Gahbauer Senior Economist. Outline. 3 negative shocks to mortgage transactions “Credit crunch” Economic downturn House price expectations Future prospects for activity. Shock #1: Credit Crunch. - PowerPoint PPT PresentationTRANSCRIPT

Economic outlook and mortgage market

implications

Little recovery in sight

Martin Gahbauer

Senior Economist

Outline

• 3 negative shocks to mortgage transactions

1. “Credit crunch”

2. Economic downturn

3. House price expectations

• Future prospects for activity

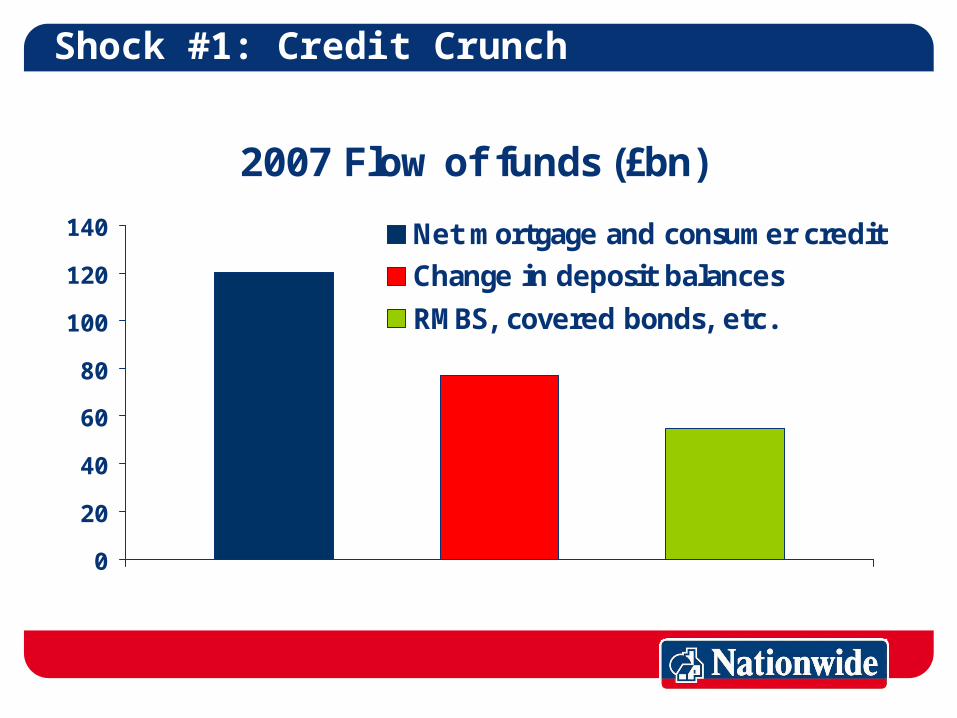

Shock #1: Credit Crunch

2007 Flow of funds (£bn)

0

20

40

60

80

100

120

140 Net mortgage and consumer creditChange in deposit balances

RMBS, covered bonds, etc.

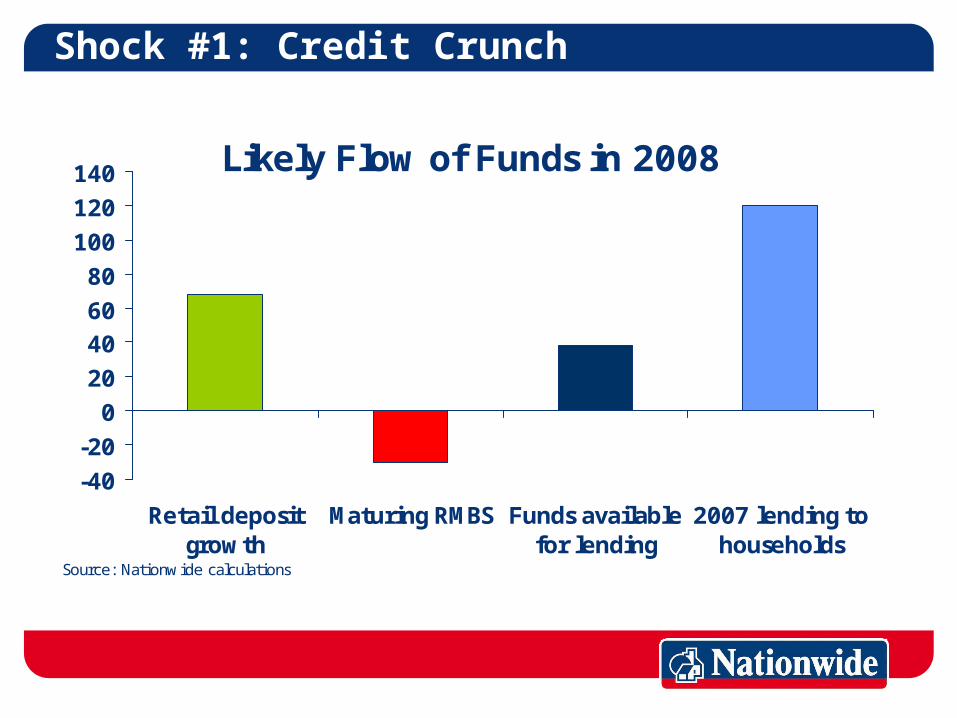

Shock #1: Credit Crunch

Likely Flow of Funds in 2008

-40

-20

0

20

4060

80

100

120

140

Retail depositgrowth

Maturing RMBS Funds availablefor lending

2007 lending tohouseholds

Source: Nationwide calculations

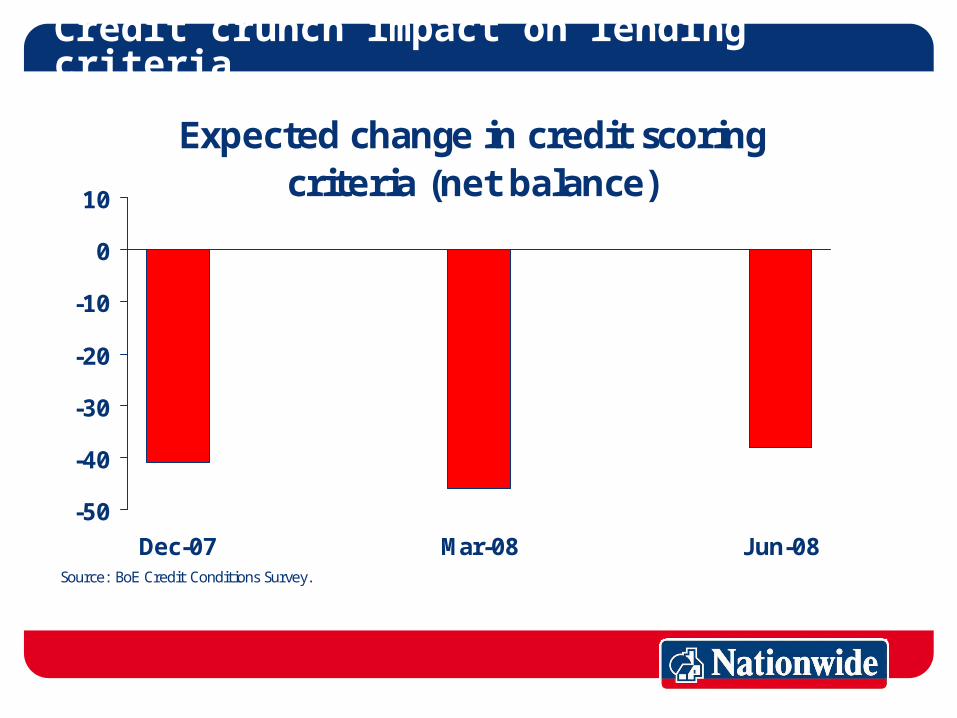

Credit crunch impact on lending criteria

Expected change in credit scoring criteria (net balance)

-50

-40

-30

-20

-10

0

10

Dec-07 Mar-08 Jun-08Source: BoE Credit Conditions Survey.

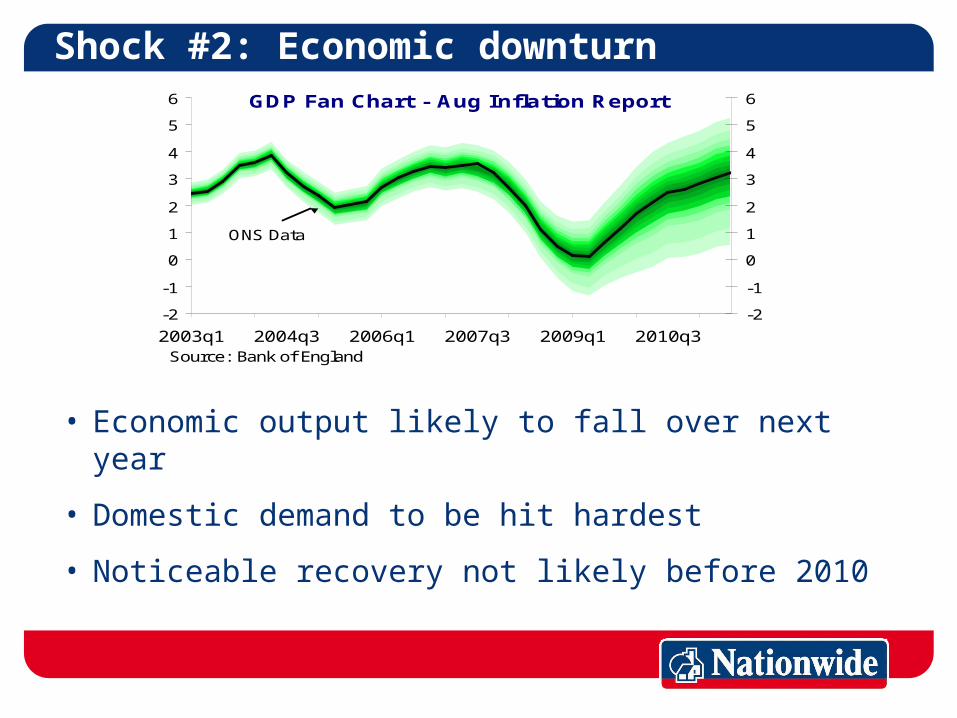

Shock #2: Economic downturn

• Economic output likely to fall over next year

• Domestic demand to be hit hardest

• Noticeable recovery not likely before 2010

GDP Fan Chart - Aug Inflation Report

ONS Data

-2

-1

0

1

2

3

4

5

6

2003q1 2004q3 2006q1 2007q3 2009q1 2010q3Source: Bank of England

-2

-1

0

1

2

3

4

5

6

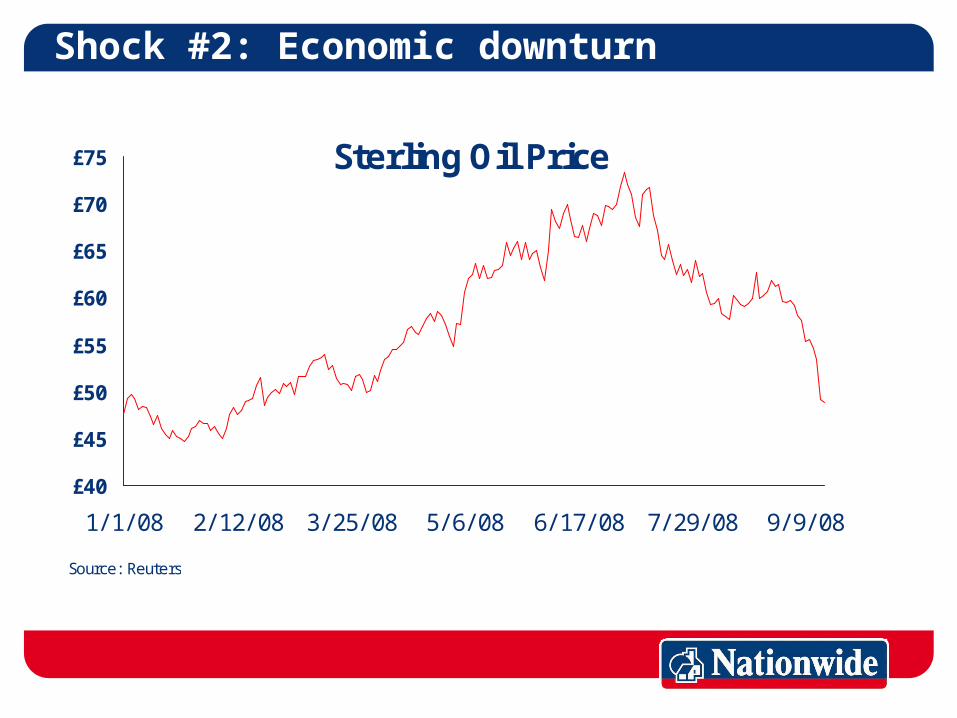

Shock #2: Economic downturn

Sterling Oil Price

£40

£45

£50

£55

£60

£65

£70

£75

1/ 1/ 08 2/ 12/ 08 3/ 25/ 08 5/ 6/ 08 6/ 17/ 08 7/ 29/ 08 9/ 9/ 08

Source: Reuters

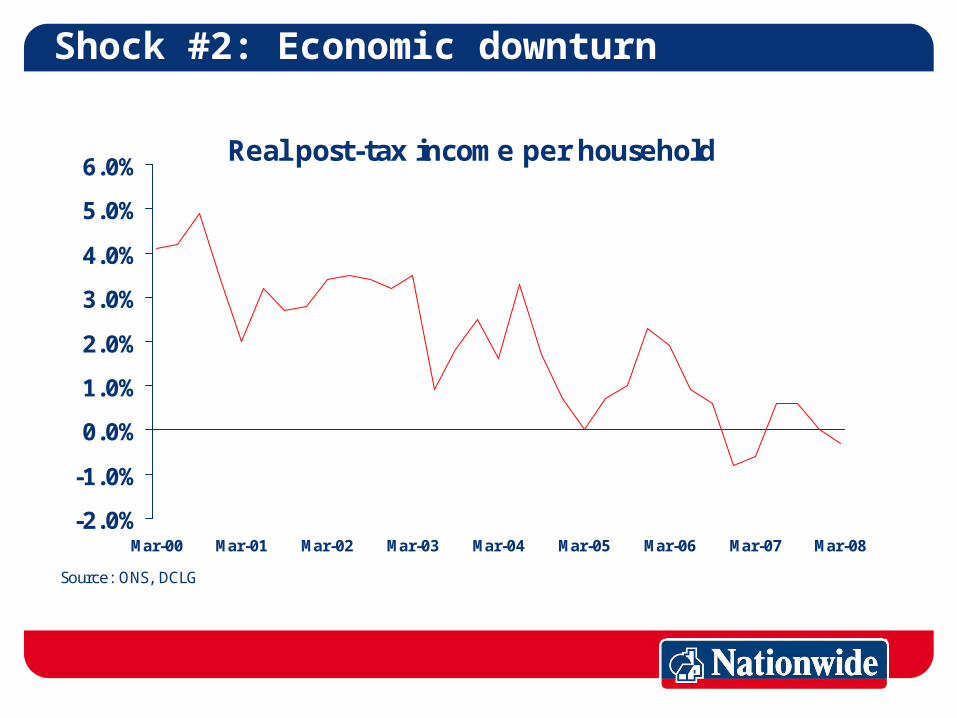

Shock #2: Economic downturn

Real post-tax income per household

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Mar-00 Mar-01 Mar-02 Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08

Source: ONS, DCLG

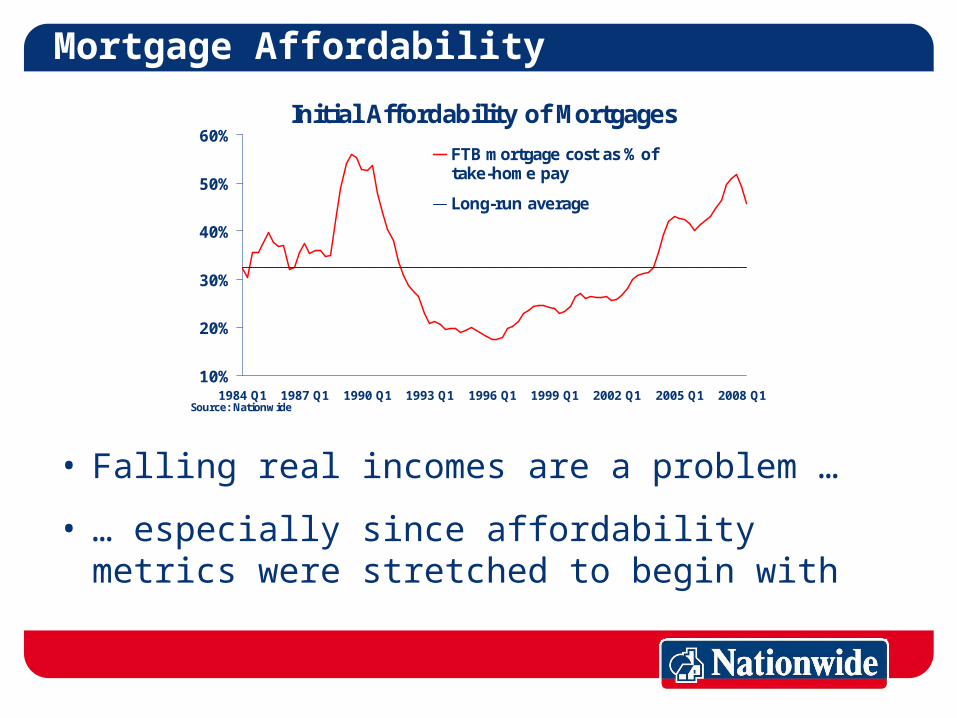

Mortgage Affordability

Initial Affordability of Mortgages

10%

20%

30%

40%

50%

60%

1984 Q1 1987 Q1 1990 Q1 1993 Q1 1996 Q1 1999 Q1 2002 Q1 2005 Q1 2008 Q1Source: Nationwide

FTB mortgage cost as % oftake-home pay

Long-run average

• Falling real incomes are a problem …

• … especially since affordability metrics were stretched to begin with

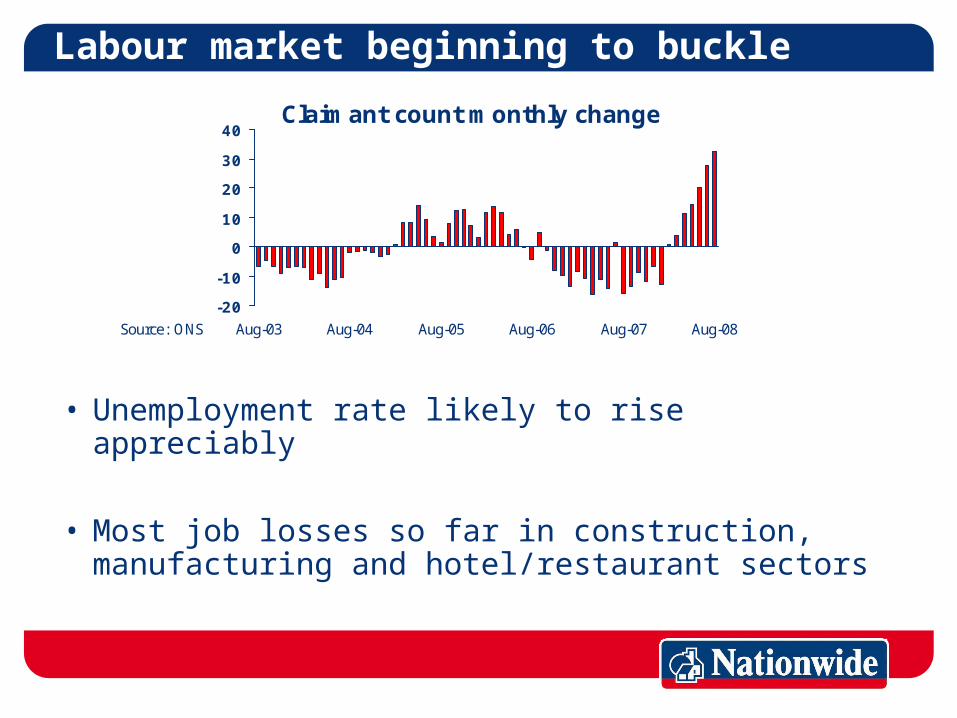

Labour market beginning to buckle

Claimant count monthly change

-20

-10

0

10

20

30

40

Aug-03 Aug-04 Aug-05 Aug-06 Aug-07 Aug-08Source: ONS

• Unemployment rate likely to rise appreciably

• Most job losses so far in construction, manufacturing and hotel/restaurant sectors

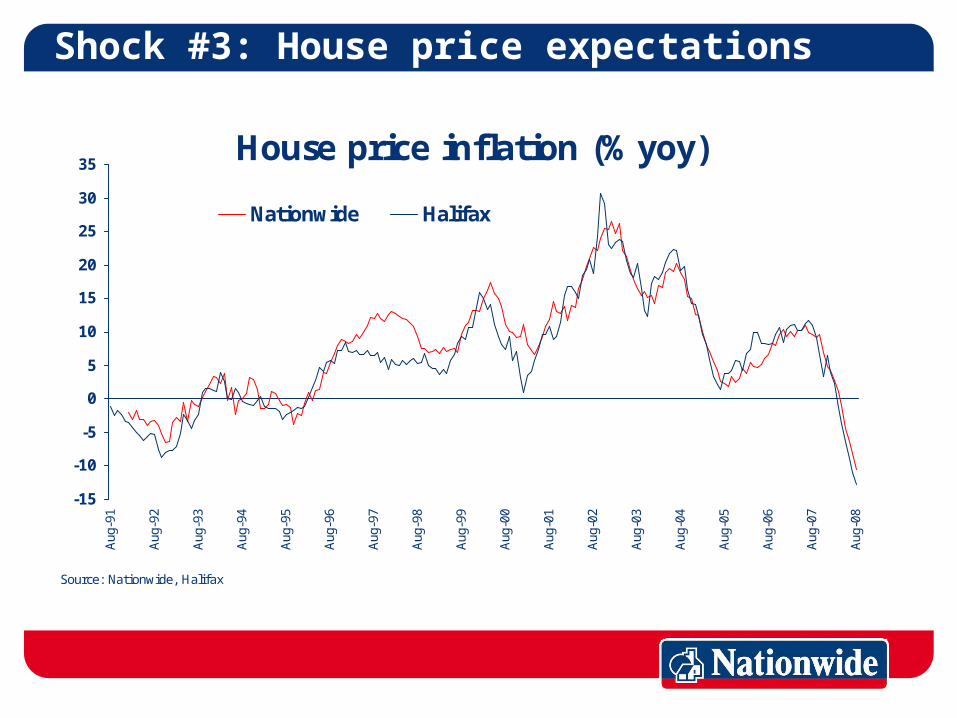

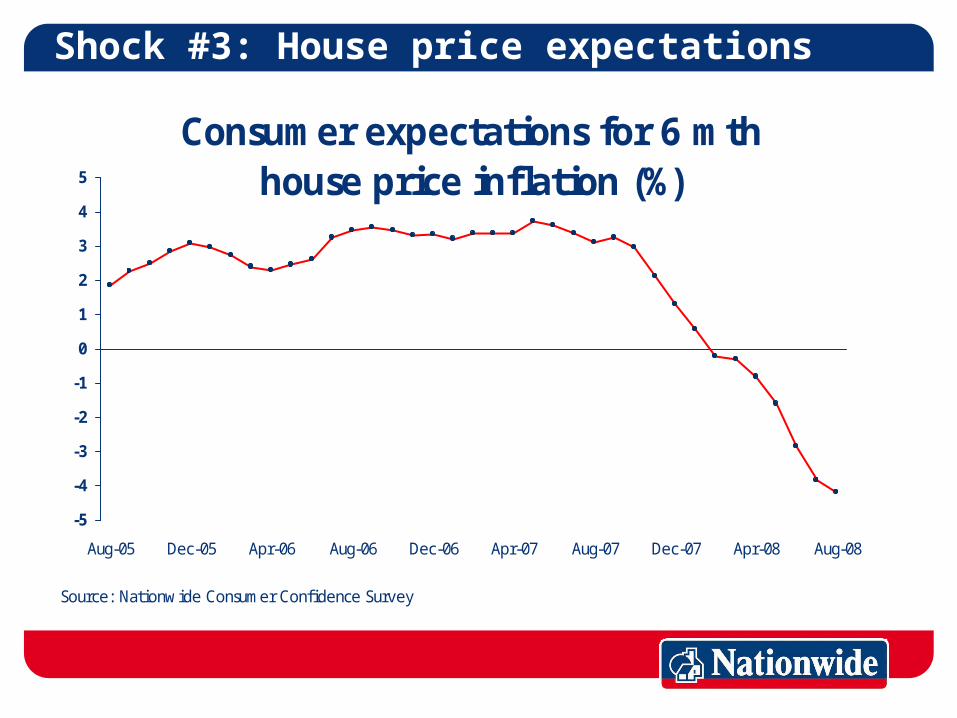

Shock #3: House price expectations

House price inflation (% yoy)

-15

-10

-5

0

5

10

15

20

25

30

35

Aug

-91

Aug

-92

Aug

-93

Aug

-94

Aug

-95

Aug

-96

Aug

-97

Aug

-98

Aug

-99

Aug

-00

Aug

-01

Aug

-02

Aug

-03

Aug

-04

Aug

-05

Aug

-06

Aug

-07

Aug

-08

Source: Nationwide, Halifax

Nationwide Halifax

Shock #3: House price expectations

Consumer expectations for 6 mth house price inflation (%)

-5

-4

-3

-2

-1

0

1

2

3

4

5

Aug-05 Dec-05 Apr-06 Aug-06 Dec-06 Apr-07 Aug-07 Dec-07 Apr-08 Aug-08

Source: Nationwide Consumer Confidence Survey

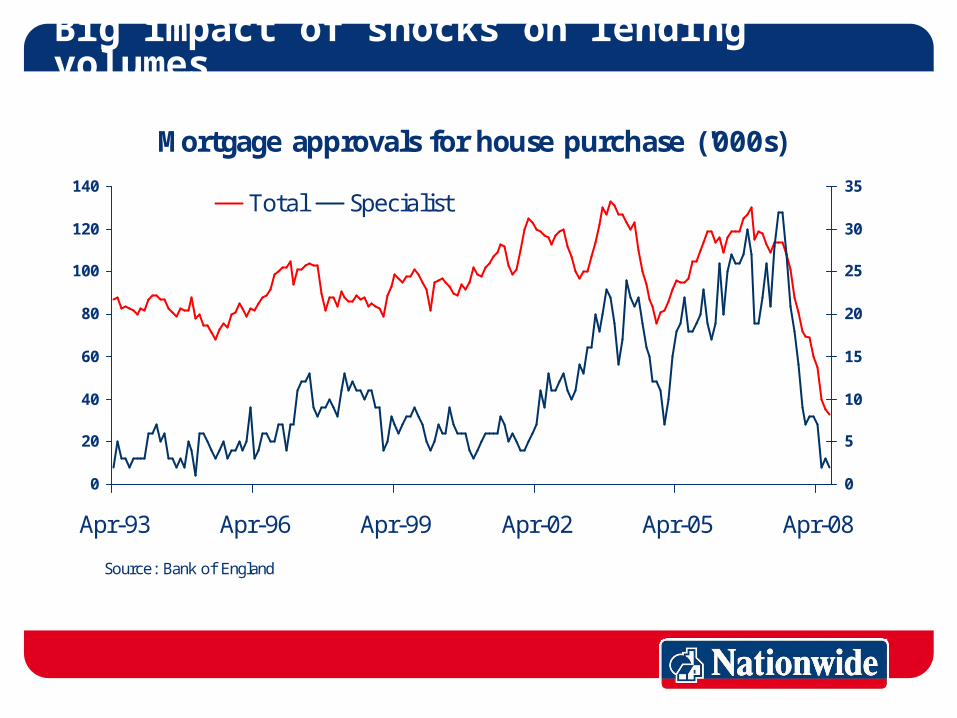

Big impact of shocks on lending volumes

Mortgage approvals for house purchase ('000s)

0

20

40

60

80

100

120

140

Apr-93 Apr-96 Apr-99 Apr-02 Apr-05 Apr-08

Source: Bank of England

0

5

10

15

20

25

30

35Total Specialist

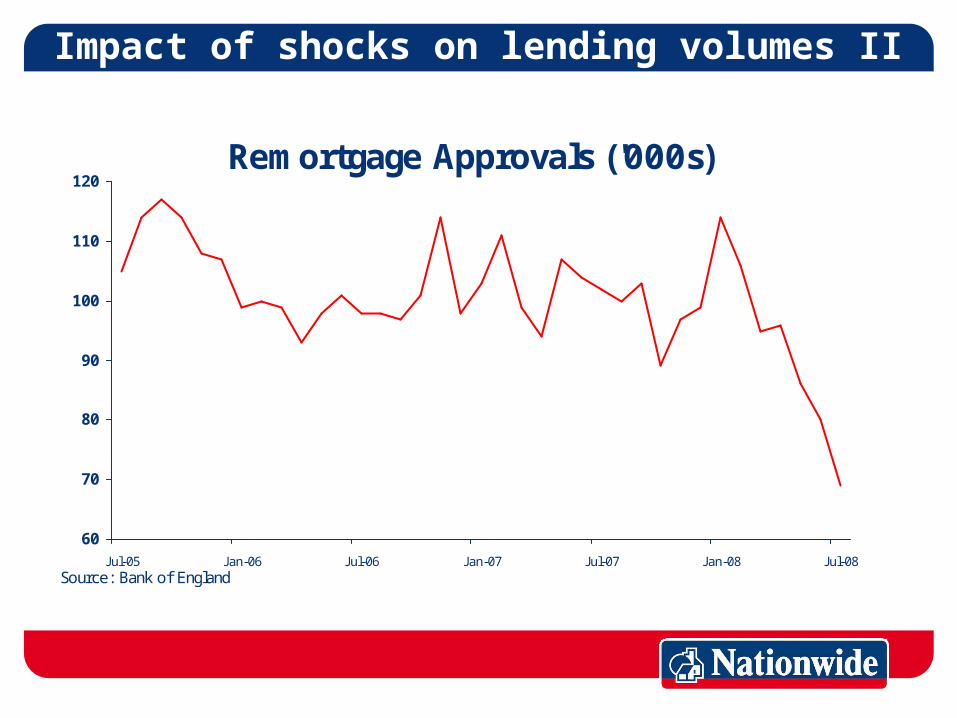

Impact of shocks on lending volumes II

Remortgage Approvals ('000s)

60

70

80

90

100

110

120

J ul-05 J an-06 J ul-06 J an-07 J ul-07 J an-08 J ul-08Source: Bank of England

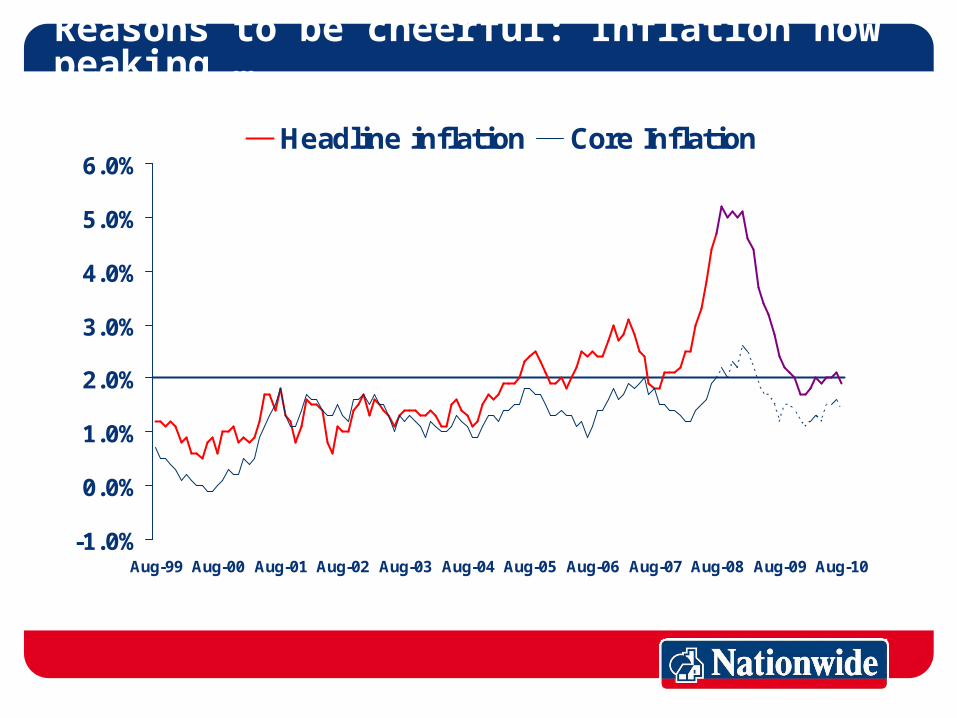

Reasons to be cheerful: Inflation now peaking …

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Aug-99 Aug-00 Aug-01 Aug-02 Aug-03 Aug-04 Aug-05 Aug-06 Aug-07 Aug-08 Aug-09 Aug-10

Headline inflation Core Inflation

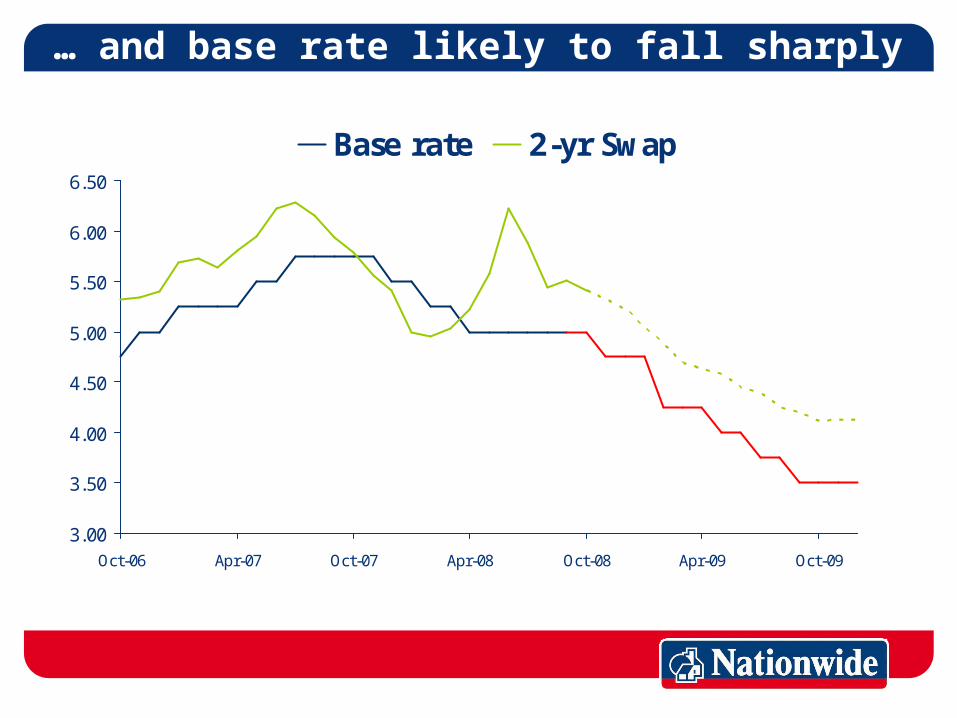

… and base rate likely to fall sharply

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

Oct-06 Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09

Base rate 2-yr Swap

Market will eventually recover

• Valuations will adjust to more affordable level

• Rental yields likely to rise well above “risk-free” rate of return

• US rescue plan may boost investor confidence

• Economy and employment outlook should improve by 2010

• Low activity has been leading to build-up of pent-up demand

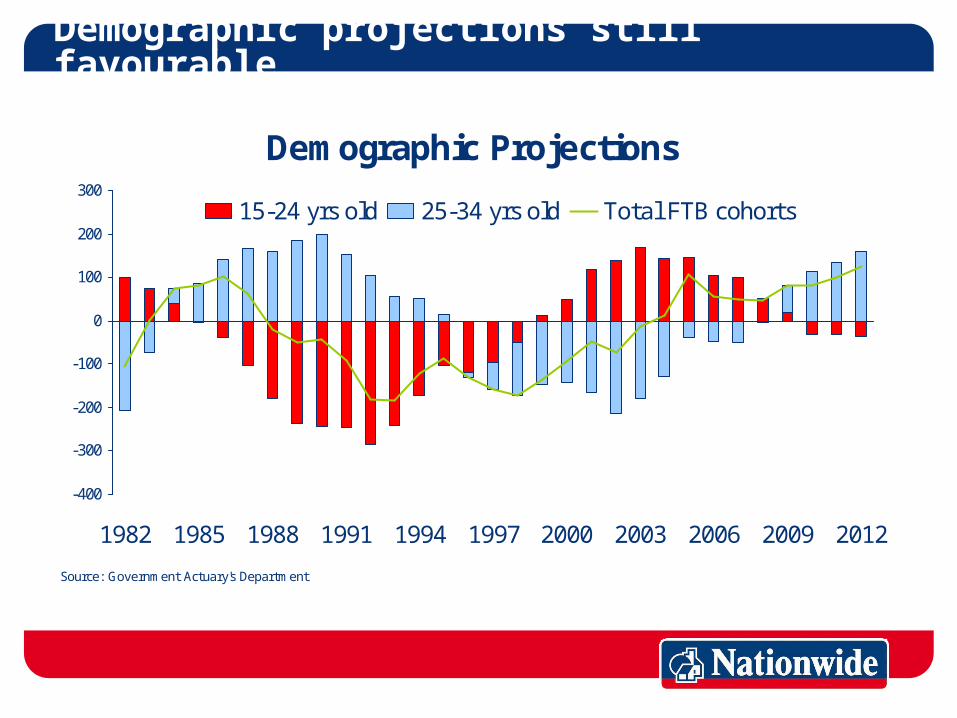

Demographic projections still favourable

Demographic Projections

-400

-300

-200

-100

0

100

200

300

1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

Source: Government Actuary's Department

15-24 yrs old 25-34 yrs old Total FTB cohorts

Specific market dynamics

• House purchase:

Activity should already be in a bottoming out process, albeit at extremely low levels

Expect FTB activity to recover somewhat in 2009

• Re-mortgage:

Deal maturity pipeline to slow in 2009

Some borrowers may not meet criteria

But rate cuts should lead to more attractive deals

Conclusions

• Near-term outlook for transaction volumes remains very difficult

• Adjustment takes time to work through system …

• … but a cyclical recovery will eventually arrive