economic outlook for the west of england lep - amazon s3 us... · growth, with strong economic...

TRANSCRIPT

Economic outlook for the West of

England LEP

Prepared for the

West of England LEP

September 2015

Contents

2

Introduction

Oxford Economics were commissioned by the West of England LEP to produce sector-based employment and GVA

forecasts and scenario analysis for the West of England LEP, four constituent local authorities, South West and UK. This

report provides a summary of these forecasts, and is accompanied by a detailed database of economic, labour market and

demographic variables for each location.

This report has 4 sections:

1. An overview of the current performance and outlook for the UK economy. This provides the context within which the

West of England LEP economy will be operating over the medium to long term;

2. The current demographic and labour market structure of the South West economy, and the outlook to 2036;

3. The current demographic and labour market structure of the local authorities within the West of England LEP economy,

and the outlook to 2036;

4. The current demographic and labour market structure of the West of England LEP economy, and the outlook to 2036;

5. An overview of the scenario assumptions and key results.

The annex to this report provides a technical section setting out data sources and assumptions.

Please contact Oxford Economics for further information:

Kerry Houston [email protected]

Niall Dowds [email protected]

The macroeconomic context

Global environment

A key area for concern is the slowdown in China.

The recent sharp sell-off in equities has increased

concerns about financial stability and growth. And

with the rally before the crash having been so debt-

fuelled there are real risks to consumption and

investment.

Estimates for 2015 suggest Emerging Markets are

forecast to have their worst year since 2001

(excluding 2009), mainly impacted by the strong

dollar. Falling commodity prices, slowing capital

inflows and rising debt burdens in these economies

skew risk growth forecasts downward.

The global economic recovery is firming but the outlook is uncertain; with positive outlooks for the US, UK and

Europe: whilst greater downside risks loom for emerging markets and China . The US emerges as a driver of global

growth, with strong economic momentum underpinned by consumer spending and confidence. Solid growth in

business activity and a buoyant labour market have also helped to support firm growth. Fuelling global growth, the

US will face the threats of a Greek exit which still linger, a slowdown in the Chinese economy and a strong dollar.

The Eurozone emerged again from recession in 2014, as uncertainty started to ease from the continent. Despite the

shock of the Greek crisis, growth will accelerate in 2015 supported by weak oil prices. The pace of the recovery will

remain weak, with Greek insecurity, fiscal tightening and unemployment remaining high. But as the recovery

broadens growth will rise slightly in the medium term.

4

2014 2015 2016 2015-2019 2015-2036

US 2.4 2.3 2.8 2.7 2.5

Japan -0.1 1.0 1.8 1.0 0.7

China 7.4 6.6 6.1 5.9 4.8

Eurozone 0.9 1.5 1.8 1.6 1.3

Germany 1.6 1.9 2.1 1.6 0.9

France 0.2 1.3 1.6 1.5 1.5

Italy -0.4 0.5 1.0 0.9 0.7

Ireland 4.8 3.7 3.8 3.2 2.7

Greece 0.7 -0.7 -0.2 1.0 2.0

Spain 1.4 3.2 2.7 2.5 1.6

UK 3.0 2.6 2.8 2.5 2.3

Brazil 0.1 -1.6 0.3 1.0 2.0

OPEC 2.5 2.0 3.3 3.7 3.7

Source: Oxford Economics

Annual average GDP growth (%)

UK: Growth remaining firm

Following a strong GVA outturn of 3.0% in 2014, we expect the

UK’s pace of growth to ease to 2.6% in 2015 before rebounding

to 3.0% in 2016. The data at the start of this year was

surprisingly soft. Expansion in Q1 was distinctly two-speed, with

a strong performance by the service sector limited by a fall in

manufacturing output, and export demand sapped by the strong

pound.

The preliminary estimate for Q2 is positive with growth

rebounding on the back of stronger business surveys and other

economic indicators. The pick up in Q2 highlights the imbalance

in the economy, a strong performance in the service sector

contrasted with a weak construction and manufacturing data.

After ten consecutive periods of quarterly growth, GDP per head

is estimated to have approximately returned to the pre-crisis

peak. Admittedly, this is a reassuring milestone but it means

living standards are only what they once were seven years ago.

Further out we expect the ‘Summer Budget’ to impact on growth,

with the cutting of in-work benefits weakening consumer

spending. The introduction of a compulsory ‘living-wage’ in 2020

is estimated by the Office for Budget Responsibility (OBR) to

have a moderate impact on employment, but this is highly

uncertain, as firms may respond to higher wages by cutting jobs.

5

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2010 2011 2012 2013 2014 2015

Services Construction Production

UK: Contributions to quarterly GDP growth%pts

Source : Oxford Economics/Haver Analytics

-6

-4

-2

0

2

4

6

2004 2006 2008 2010 2012 2014 2016 2018

% year

Consumer spending

Real disposableincome

Source: Oxford Economics

Forecast

UK: Consumer spending and income

UK: Drivers of growth

Rising household spending in the short-run – CPI inflation is expected to remain broadly flat until latter this year,

when it is expected to approach 1% by the end of the year. Underlying price pressure is expected to remain modest and

we forecast inflation remaining well below the 2% target through 2016. When combined with stronger wage growth, as a

result of a tightening labour market, it should deliver a substantial boost to household spending power. We expect real

consumer spending grow by 3.3% in 2015, easing to 2.8% in 2016. In the medium term beyond 2017 we expect

consumer spending to weaken as the effects of the recent ‘Summer Budget’ take hold. As the deep cuts to in-work

benefits are introduced, the impact will more than offset the boost from the new ‘living wage’, subduing growth in

household incomes.

Strong corporate finances supporting investment – Strong corporate finances have allowed firms to remain

confident, with business investment unaffected by uncertainty surrounding the general election and the Greece bailout.

UK corporate finances are in a secure position, with profitability at their highest levels since the 1990s and cash

reserves are at record levels. The future outlook for business investment remains positive with business surveys

reporting strong investment plans. We expect business investment growth of 5.3% in 2015 and 6.1% in 2016.

Sustained strength in house building – Despite a cooling in the housing market, residential investment grew by 9.6%

in the year to Q1 2015. The existence of government support programmes, such as ‘Help to Buy’ and ‘Shared equity

schemes’, have given builders ample confidence to continue development. This will provide direct support to the

economy, supporting employment and GVA growth, while also alleviating any potential supply side constraints, keeping

house prices in check.

Further austerity –A combination of welfare cuts, tax rises and a slower pace of fiscal consolidation, has allowed the

Chancellor to smooth out the departmental spending ‘rollercoaster’. The planned path of government spending is slightly

higher over the next five years than we had previously anticipated, though fiscal policy will remain a drag on growth.

6

UK: Drivers of growth

Subdued export outlook – Survey data suggest that the 10%

appreciation of sterling against the euro since the start of 2015

has driven a weakening in export order books. Our forecasts

assume that both the US and Eurozone economies strengthen

over the coming two years, providing some support to UK

exports, but we do not expect net trade to make any

meaningful contribution to GDP growth in the short-term.

Low inflation - Our forecast continues to assume that the first

rate hike comes in Q1 2016, as the majority of the MPC are

unlikely to move until inflation has moved decisively away from

zero and the situation in Greece has become clearer.

Subsequent tightening is assumed to come at the very

measured pace of 50bps per year.

Longer-term growth will be underpinned by:

Helpful demographics – the UK is expected to see its

working-age population continue to expand strongly, driven by

natural increases, persistent net inward migration and further

rises in the state pension age.

Leading position in several service sectors – the UK

economy has strong representation in dynamic private

services sectors and is a global leader in the provision of

several parts of financial and business services.

7

0

1

2

3

4

5

6

2004 2006 2008 2010 2012 2014 2016 2018

UK: Interest rates%

Source : Oxford Economics

Bank Rate

10-year gilt yield

Forecast

-16

-12

-8

-4

0

4

8

12

16

2004 2006 2008 2010 2012 2014 2016 2018

World trade Exports (non-fuel goods)

Source: Oxford Economics

Forecast

UK: Exports & world trade

% year

UK: Employment sectoral outlook

UK employment is forecast to rise by an

additional 3.2million jobs by 2036, equivalent to

average annual growth of 0.5%. Employment

growth will be strongest over the next few years

before easing into the longer-term.

Providing the largest absolute increase in jobs

over the forecast period to 2036 are professional

services (890,000 jobs), administration & support

(800,000 jobs) and construction (540,000 jobs).

The majority of sectors are expected to see

employment rise over this period, including the

relatively small but rapidly growing information &

communications sector.

Job shedding will be experienced in a small

number of sectors over the forecast period. The

most significant reduction in absolute terms is

expected in the manufacturing sector, where

more than 630,000 jobs are forecast to be lost

across the UK by 2036.

Austerity measures to be implemented over the next parliament by the Conservative government will lead to job losses

in the public sector. Cuts are expected in public administration and education, with the greatest impact to be felt early in

our forecast period. We forecast stable employment growth in the healthcare sector as political pressure to ‘ring-fence’

front line services will save jobs.

8

000sAnnual

Avg (%)000s

Annual

Avg (%)

Agriculture, forestry and fishing -33 -1.6 -43 -1.0

Mining and quarrying -19 -2.3 -16 -3.4

Manufacturing -285 -1.0 -350 -1.4

Electricity, gas, steam -15 -1.0 -17 -1.5

Water supply; sewerage -13 -0.6 -17 -0.9

Construction 276 1.4 263 1.0

Wholesale and retail trade 204 0.6 72 0.1

Transportation and storage 108 0.7 -7 0.0

Accommodation and food service 147 0.9 59 0.2

Information and communication 176 1.4 109 0.6

Financial and insurance activities -9 0.0 10 0.1

Real estate activities 82 1.4 67 0.9

Professional, scientific and technical 494 2.0 399 1.0

Administrative and support services 468 1.9 331 0.9

Public administration and defence -149 -1.3 -45 -0.3

Education 3 0.1 36 0.1

Human health and social work 199 0.5 257 0.5

Arts, entertainment and recreation 147 1.6 124 1.0

Other service activities 115 1.2 84 0.7

Total 1,895 0.7 1,317 0.3

Source: Oxford Economics

2015-2025 2025-2036

UK: risks to the outlook

There are a number of risks which would impact on our forecast outlook for the UK economy. These include:

Austerity – though the ‘Summer Budget’ eased the pace of austerity a little, the government is still planning to tighten

policy significantly over the period to 2020, with unprotected government departments having been asked to plan for

real terms spending cuts of 25% and 40%. There is a risk that this retrenchment causes GDP growth to slow sharply,

particularly if monetary policy is tightened too aggressively or external demand softens.

Labour market – our forecast assumes that the recovery in activity will be accompanied by a rebound in productivity,

offsetting some of the productivity losses of the past five years. Were the productivity response to be weaker, we would

see stronger employment growth and, potentially, a pick-up in wage pressures in the short term as firms face skills

shortages. However, it would imply weaker prospects for growth over the medium-term.

Housing bubble – with house price growth having cooled in H1 2015, concerns about a housing bubble have receded.

However, a bubble could still develop if demand rebounds strongly and the supply response disappoints.

‘Grexit’ - Miraculously a Greek bailout was agreed and conditions approved by the Greek parliament. But the threat of

‘Grexit’ remains. An exit from the single currency would elevate financial stress across member states as contagion risk

gripped the Eurozone. The resultant slowdown would severely impact on the UK’s economic growth prospects.

US and Eurozone upside surprise - further falls in oil prices could amplify the effects of an upside surprise in the US

and Eurozone economies. The combination of stronger demand from our main trading partners and low inflation

boosting the purchasing power of domestic consumers could be particularly potent for the UK and lead GDP growth to

accelerate towards 4% in 2016-17.

The probability of each of these shocks is relatively low, but each would have put a significant effect on our UK outlook.

Under any scenario where the headline UK growth figure was skewed from the baseline outlook, there would be a notable

impact on the South West region and the West of England LEP.

9

South West

This section summarises the outlook for the South West region, focusing on demographic and labour market

developments, including comparisons with the UK economy.

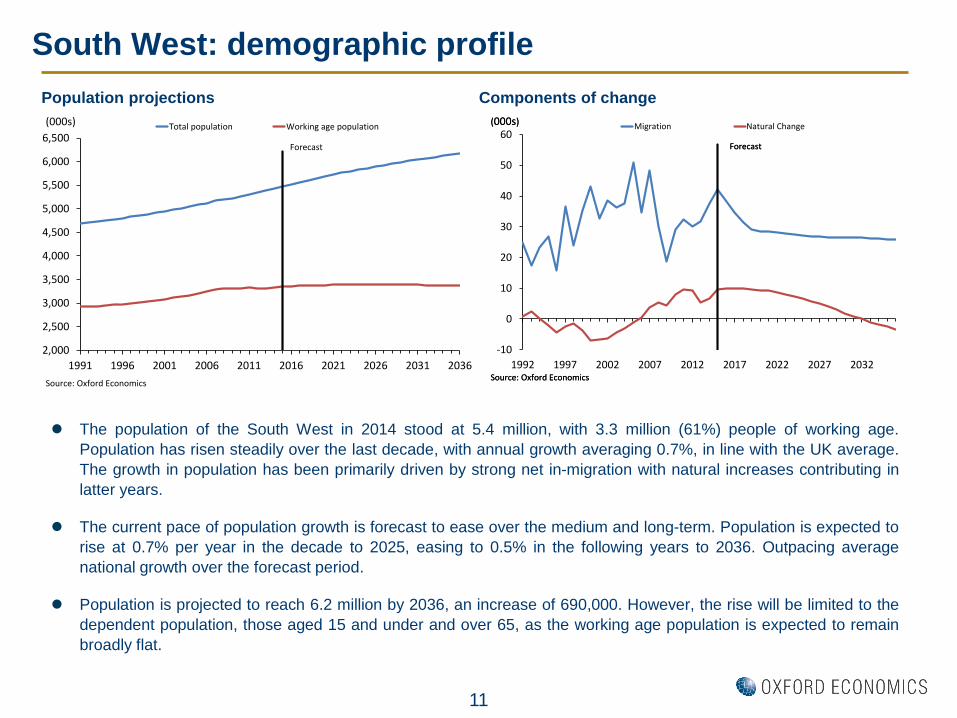

South West: demographic profile

The population of the South West in 2014 stood at 5.4 million, with 3.3 million (61%) people of working age.

Population has risen steadily over the last decade, with annual growth averaging 0.7%, in line with the UK average.

The growth in population has been primarily driven by strong net in-migration with natural increases contributing in

latter years.

The current pace of population growth is forecast to ease over the medium and long-term. Population is expected to

rise at 0.7% per year in the decade to 2025, easing to 0.5% in the following years to 2036. Outpacing average

national growth over the forecast period.

Population is projected to reach 6.2 million by 2036, an increase of 690,000. However, the rise will be limited to the

dependent population, those aged 15 and under and over 65, as the working age population is expected to remain

broadly flat.

Population projections Components of change

11

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

1991 1996 2001 2006 2011 2016 2021 2026 2031 2036

Total population Working age population

Source: Oxford Economics

Forecast

(000s)

-10

0

10

20

30

40

50

60

1992 1997 2002 2007 2012 2017 2022 2027 2032

Migration Natural Change

Source: Oxford Economics

Forecast

(000s)

Source: Oxford Economics

Forecast

(000s)

South West: current structure

Total employment in the South West in 2014 was 2,839,000. Services are the dominant employers in the region,

providing 81% of jobs, marginally below the UK’s breakdown of 83%. The largest sectors in the region are wholesale &

retail, healthcare and education, employing 410,000 (14.5%), 390,000 (13.8%) and 239,000 (8.4%) people respectively.

Relative to the UK, the South West has a high concentration of jobs in accommodation & food, healthcare and

construction. Administration & support and professional services are under-represented in the South West relative to

the UK. The region’s large exposure to the public administration sector, and low relative concentration in administration

& support and professional services, will constrain growth over the forecast period.

Employment structure: South West v UK, 2014 Key indicators: 2014

12

-2.0 -1.0 0.0 1.0 2.0

Accommodation and foodHealthcare

ConstructionPublic admin & defence

Agriculture, forestry and fishingManufacturing

Real estateOther service s

Water supply; sewerageFinancial and insurance

Electricity, gas, steamMining and quarrying

Wholesale & retail tradeArts and entertainment

EducationInformation & communication

Transportation & storageProfessional, scientific &technicalAdministrative & support service

Source: Oxford Economics

UK more dependent

South West more dependent

Percentage point difference

South West UK

Population (000s) 5,423 64,597

Population aged 16-64 (000s) 3,328 41,037

Net migration (000s) 37.5 260.0

Employment (000s) 2,839 33,330

GVA (£m, 2011) 110,389 1,458,027

Consumer expenditure (£m, 2011) 95,685 1,035,160

Resident employment rate (%) 59.8 59.7

Unemployment rate (%) 1.8 3.0

Productivity (£000s/job) 38.9 43.7

Source: Oxford Economics

South West: outlook

The South West has had a historically strong

labour market. Employment growth averaged

1.2% in the years preceding the crisis, ahead of

the UK average of 1.0%. The impact of the

crisis was significant in the South West but

limited in a UK context. Employment growth

weakened since 2008, halving to 0.6% per year,

on par with the UK average. Whilst the South

West’s labour market recovery has been quite

strong relative to other regions, the robust and

sustained rebound of London job market has

driven up the UK average overall.

Total employment in the South West is estimated to increase by 31,000 additional jobs in 2015, equivalent to

growth of 1.1%, this will lag UK growth of 1.4% in the year. Growth will slow in the South West and UK in 2016 to

0.7% and 0.9% respectively. The pace of employment growth will slow in the South West from current rates over

the forecast period. Rising by 0.5% per year in the period to 2025, then slowing to 0.3% in the years 2025 to 2036.

Total jobs in the region are forecast to reach almost 3.1million by 2036, an increase of 210,000 on current levels.

Working age population remaining flat will place a drag on labour market growth in the years ahead, as historically

low unemployment rates restrict the ability of increased labour market participation.

GVA in the South West increased by 2.9% in 2014, its largest expansion since 2007. The pace of acceleration is

expected to ease in the coming years but remain robust, rising by 2.3% in 2015, and 2.7% in 2016.Looking over

the forecast period we see that GVA growth in the South rest will remain solid, however it is expected to

consistently underperform the UK average. The pace of economic growth is forecast to be higher in the coming

decade to 2025, rising on average by 2.5% per year, followed by 2.1% per year thereafter.

Employment performance

13

90

95

100

105

110

115

120

125

130

2000 2005 2010 2015 2020 2025 2030 2035

South West UK

Source: Oxford Economics

Forecast

(Index 2000=100)

South West: sector outlook

Sectorally, construction and professional services are

expected to underpin employment growth over the

forecast period, each adding approximately 50,000

additional jobs. Healthcare and administration & support

will also contribute significantly to job creation, adding

46,000 and 40,000 jobs respectively.

Production industries are expected to experience job

shedding in the period ahead to 2036. The largest

declines are in the manufacturing sector, with the loss of

57,000 jobs predicted by 2036. The fall in employment

is expected due to productivity gains.

Education and public administration are forecast to face

job losses in the years leading to 2020, as the new

government’s austerity policy reduces public sector

spending. Cuts will be deepest in public administration,

with the sector not expected to recover over the forecast

period. However, employment in healthcare is expected

to rise in the period 2015-2036, due to increased

demand owing to the growing elderly population.

Economic activity will be lead by professional services,

with growth expected to average 3.6%. Information &

communications and administration & support are also

forecast to experience high growth rates, rising at 3.5%

and 3.2% per year respectively.

Employment outlook

14

Level

000s 000s 000s

Agriculture, forestry and fishing 55 44 -11 -1.3

Mining and quarrying 4 2 -2 -2.9

Manufacturing 241 183 -57 -1.2

Electricity, gas, steam 9 7 -2 -1.3

Water supply; sewerage 16 14 -2 -0.7

Construction 209 259 50 1.1

Wholesale and retail trade 417 438 21 0.3

Transportation and storage 101 113 12 0.6

Accommodation and food service 238 253 16 0.4

Information and communication 82 92 10 0.6

Financial and insurance activities 95 95 0 0.1

Real estate activities 62 77 15 1.0

Professional, scientific and technical 208 257 49 1.1

Administrative and support services 188 228 40 1.0

Public administration and defence 148 134 -14 -0.5

Education 241 243 3 0.1

Human health and social work 393 439 46 0.5

Arts, entertainment and recreation 78 98 20 1.1

Other service activities 85 103 17 0.9

Total 2,870 3,081 211 0.4

Source: Oxford Economics

20362015Annual

Avg (%)

Change

West of England LEP

This section summarises the outlook for the West of England LEP, focusing on demographic and labour market

developments.

West of England LEP: demographic profile

The population of West of England LEP is currently 1.1 million, accounting for one fifth of the total population in the

South West. The working age population of the LEP stands at 712,000, 64.5% of the total population. Population

growth in the last decade has averaged 0.9%, marginally ahead of the South West and the UK. The LEP has

benefited from strong levels of net inward migration in the past decade, mirroring trends across the South West. The

natural change in population also continued to make a positive contribution to growth.

Population growth is expected to continue at a similar pace, rising by 1.0% in 2015 and 0.9% in 2016. The pace of

population growth is forecast to ease over the medium and long-term. With growth expected to average 0.6% - a

similar rate as the South West. Net migration is expected to be weaker over the forecast, than recently, averaging

2,600 people per year. This reflects a general reduction in net migration into the UK as the one off influence of the

EU enlargement fades and economic growth on the continent improves.

Population projections Components of change

16

500

600

700

800

900

1,000

1,100

1,200

1,300

1991 1996 2001 2006 2011 2016 2021 2026 2031 2036

Total population Working age population

Source: Oxford Economics

Forecast

(000s)

-2

0

2

4

6

8

10

12

14

1992 1997 2002 2007 2012 2017 2022 2027 2032

Migration Natural Change

Source: Oxford Economics

Forecast

(000s)

West of England LEP: current structure

In 2014, 634,000 people were employed in the West of England LEP region. At the same time, 544,000 people living in

the LEP were in employment, signifying net-in commuting to the region. 13,000 residents where registered on the

claimant count measure, equivalent to 1.8%. This is in line with the South West and compares favourably to the national

average.

Services play a dominant role in the West of England, providing 86% of jobs, above the South and UK averages of 81%

and 83% respectively. Healthcare and wholesale & retail contribute the greatest number of jobs to the LEP, employing

89,000 (14.0%) and 86,000 (13.5%) workers respectively, following the trend across the South West. Also providing a

large minority of jobs are professional services and education, employing 58,000 (9.1%) and 57,000 (9.0%) of jobs.

In comparison to the South West, the LEP has a high concentration of jobs in professional services, administration &

support and financial services. Whereas manufacturing, accommodation & food, and agriculture are under-represented

in the LEP.

Employment structure: LEP vs South West, 2014 Key indicators: 2014

17

-2.0 -1.0 0.0 1.0 2.0

Professional, scientific & technicalAdministrative & support service

Financial & insuranceInformation & communication

Transportation & storageEducation

HealthcareWater supply; sewerage

Mining & quarryingReal estate

Electricity, gas, steamArts, entertainment & recreationPublic administration & defence

Other serviceConstruction

Wholesale & retail tradeAgriculture, forestry & fishing

Accommodation & food serviceManufacturing

Source: Oxford Economics

South West more dependent

LEP more dependent

Percentage point difference

West of

England LEPSouth West

Population (000s) 1,105 5,423

Population aged 16-64 (000s) 712 3,328

Net migration (000s) 6.8 37.5

Employment (000s) 634 2,839

GVA (£m, 2011) 27,930 110,389

Consumer expenditure (£m, 2011) 21,112 95,685

Resident employment rate (%) 60.2 59.8

Unemployment rate (%) 1.8 1.8

Productivity (£000s/job) 44.1 38.9

Source: Oxford Economics

West of England LEP: outlook

The West of England LEP has enjoyed strong

employment growth since 2000, despite small

declines in 2006, 2010 and 2012. The LEP had

a strong recovery from the financial crisis with

22,000 additional jobs created since 2008,

equivalent to a 0.8% average annual increase.

The pace of recovery compares favourably with

the South West and UK.

Employment grew by 3.4% in the West of

England economy in 2014, the highest pace of

growth in over a decade. Despite an increase

of 21,000 jobs in the year, the rate of growth

marginally lagged that across the South West.

Job creation in the LEP is set to continue in 2015, with employment estimated to rise by 10,000. This still represents

solid growth of 1.5%, comparing favourably to the South West (1.1%) and the UK (1.4%). In 2016 and 2017,

employment rises will ease to 0.8% and 0.6% respectively, ahead of forecasts for the South West.

The pace of employment growth in the West of England economy will slow over the long run as demographic

developments, most notably a slowdown in the growth of working age population, become less supportive of

employment growth. Nonetheless, employment in the West of England LEP is forecast to reach 697,000 by 2036, an

increase of 54,000 jobs.

The West of England economy grew by 3.3% in 2014, outperforming the South West (2.9%) and the UK (3.0%). The

pace of GVA growth is estimated to grow at 2.7% in 2015, matching UK expansion. We expect the West of England

LEP to outperform the South West over the forecast period, with average annual growth of 2.4%.

Employment performance

18

90

95

100

105

110

115

120

125

130

2000 2005 2010 2015 2020 2025 2030 2035

South West UK West of England LEP

Source: Oxford Economics

Forecast

(Index 2000=100)

West of England LEP: sector outlook

The majority of job creation in the West of England

LEP is forecast within the service sector. The greater

reliance on services, follows a regional and national

trend of increasingly services-orientated economies

that will help deliver growth. Professional services

and administration & support are expected to drive

employment growth between 2015 and 2036, adding

16,000 and 12,000 new jobs respectively. Also

construction and healthcare are forecast to

contribute significantly to employment growth,

creating an additional 9,500 and 9,100 jobs

respectively.

Production industries are forecast to constrain

employment growth in the years ahead to 2036. Job

shedding will be most significant in the

manufacturing sector, with losses numbering 9,700

between 2015 and 2036. The decline in the sector is

consistent with losses experienced in the wider

South West region.

Employment outlook

19

Public administration and education are forecast to face job losses in the years leading to 2020, as government rein in

expenditure to reduce the deficit. Public administration will face the severest losses over the medium term, which will

not be recovered over the remainder of the forecast period. Only a moderate contraction is expected in the education

sector over the next few years, with post 2020 gains reclaiming most losses.

Economic activity in the LEP will be driven by professional services, wholesale & retail, and financial services, as they

make the largest contribution to growth in the period.

Level

000s 000s 000s

Agriculture, forestry and fishing 3.4 2.7 -0.6 -1.3

Mining and quarrying 0.2 0.1 -0.1 -2.8

Manufacturing 42.2 32.5 -9.7 -1.1

Electricity, gas, steam 0.9 0.6 -0.3 -1.6

Water supply; sewerage 4.0 3.4 -0.6 -0.7

Construction 40.6 50.2 9.5 1.1

Wholesale and retail trade 87.4 89.5 2.1 0.2

Transportation and storage 26.5 29.8 3.3 0.6

Accommodation and food service 43.0 45.1 2.0 0.3

Information and communication 27.4 30.6 3.1 0.6

Financial and insurance activities 31.1 31.0 0.0 0.0

Real estate activities 13.0 16.6 3.6 1.1

Professional, scientific and technical 60.1 76.1 16.0 1.3

Administrative and support services 54.6 66.6 12.0 1.1

Public administration and defence 30.8 27.2 -3.7 -0.7

Education 57.2 57.1 -0.1 0.0

Human health and social work 88.5 97.6 9.1 0.4

Arts, entertainment and recreation 15.6 19.7 4.1 1.2

Other service activities 17.0 20.7 3.7 1.0

Total 643.6 697.1 53.5 0.4

Source: Oxford Economics

2015 2036Change

Annual

Avg (%)

West of England LEP: Local authority comparison

Bath and North

East SomersetBristol North Somerset

South

Gloucestershire

West of England

LEP

Population (000s) 13.6 52.2 20.5 26.8 113.1

Population 16-64 (000s) 9.5 43.8 6.6 12.8 72.7

Net migration (000s) 0.9 1.3 1.5 1.0 4.7

Total employment (000s) 13.3 8.3 20.3 38.0 79.8

GVA (Annual average, %) 2.2 1.4 3.3 3.6 2.3

Source: Oxford Economics

Share of West of England LEP growth (%), 2000-2014

Growth in key indicators: 2000-2014

0

5

10

15

20

25

30

35

40

45

50

Population Employment GVA

Bath and North East Somerset Bristol North Somerset South Gloucestershire(%)

Source: Oxford Economics

West of England LEP comparison: 2013 sector variation

*BRES data for Agriculture, forestry and fishing unavailable

The location quotient (LQ) for each sector is calculated as its proportion of employment relative to the same proportion at

the Great Britain (GB) level. An LQ of 1 signifies the sector has the same concentration in the region as the average in GB.

An LQ above 1 highlights a relatively high concentration of the sector in the region. An LQ below 1 signifies a relatively low

concentration of the sector in the region.

Bath and North

East SomersetBristol North Somerset

South

Gloucestershire

Agriculture, forestry and fishing - - - -

Mining and quarrying 0.2 0.0 0.2 0.4

Manufacturing 0.6 0.5 1.1 1.5

Electricity, gas, steam 0.2 0.7 0.2 0.1

Water supply; sewerage 2.1 0.7 1.5 1.4

Construction 1.0 0.8 1.0 1.3

Wholesale and retail trade 1.0 1.0 1.0 0.9

Transportation and storage 0.5 1.0 1.3 1.0

Accommodation and food service 1.3 0.9 1.1 0.8

Information and communication 1.0 1.0 0.6 1.3

Financial and insurance activities 0.8 1.9 0.5 1.3

Real estate activities 1.3 1.0 1.8 0.7

Professional, scientific and technical 0.9 1.3 0.8 0.9

Administrative and support services 0.5 1.1 1.0 1.0

Public administration and defence 0.6 1.0 1.0 1.9

Education 1.7 1.1 0.8 0.9

Human health and social work 1.4 1.2 1.2 0.8

Arts, entertainment and recreation 1.0 0.9 0.9 0.5

Other service activities 1.1 0.9 1.1 0.7Source: BRES Red shading denotes a location quotient below 0.8. Green shading denotes a location quotient above 1.3

West of England LEP: Local authority outlook

Annual average growth (%), 2015-2036

South Gloucestershire is expected to lead employment growth in the period 2015-2036, growing at a pace of 0.7%

annually, followed by 0.6% in North Somerset. With 54,000 additional jobs created in the LEP over the period,

South Gloucestershire and North Somerset contribute almost two-thirds (35,000 jobs) of the total.

GVA growth follows a similar pattern to employment, with fastest growth forecast within South Gloucestershire

(2.6%) followed by North Somerset (2.5%), each outpacing the LEP average of 2.4%. Though growing at a lesser

rate of 2.3% per annum, Bristol is the largest driver of LEP growth, contributing 1.0% of the total average each

year.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Population Employment GVA

Bath and North East Somerset

Bristol

North Somerset

South Gloucestershire

West of England LEP

(%)

Source: Oxford Economics

LEP comparison: 2013 sector variation

The location quotient (LQ) for each sector is calculated as its proportion of employment relative to the same proportion at

the Great Britain (GB) level. An LQ of 1 signifies the sector has the same concentration in the region as the average in GB.

An LQ above 1 highlights a relatively high concentration of the sector in the region. An LQ below 1 signifies a relatively low

concentration of the sector in the region.

23

*BRES data for Agriculture, forestry and fishing unavailable

West of England

LEP

Greater

Cambridge and

Greater

Peterborough

LEP

Oxfordshire LEPThames Valley

Berkshire LEP

Gloucestershire

LEP

Swindon and

Wiltshire LEP

Agriculture, forestry and fishing - - - - - -

Mining and quarrying 0.2 0.2 0.3 1.7 0.5 0.3

Manufacturing 0.9 1.3 0.9 0.7 1.6 1.1

Electricity, gas, steam 0.4 0.5 0.4 1.1 1.8 0.9

Water supply; sewerage 1.2 1.3 0.8 1.4 1.0 1.3

Construction 1.0 1.0 1.0 0.8 1.1 1.0

Wholesale and retail trade 1.0 1.0 1.0 1.1 1.0 1.1

Transportation and storage 0.9 1.0 0.7 0.9 0.7 1.0

Accommodation and food service 1.0 0.9 1.1 0.9 1.0 1.1

Information and communication 1.0 1.0 1.4 3.4 0.8 0.8

Financial and insurance activities 1.4 0.6 0.4 0.6 0.9 1.5

Real estate activities 1.1 1.0 0.8 0.8 1.1 1.0

Professional, scientific and technical 1.0 1.0 1.4 1.4 0.8 1.1

Administrative and support services 1.0 1.2 0.8 1.0 0.9 0.9

Public administration and defence 1.2 0.8 0.7 0.6 1.1 1.0

Education 1.1 1.2 1.7 0.9 1.0 0.9

Human health and social work 1.1 0.9 0.9 0.6 1.0 0.9

Arts, entertainment and recreation 0.8 0.8 1.1 1.2 0.8 0.8

Other service activities 0.9 0.9 1.1 1.5 1.0 1.0Source: BRES Red shading denotes a location quotient below 0.8. Green shading denotes a location quotient above 1.3

LEP comparison: outlook

24

Key indicators: 2014

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Population growth Employment growth GVA growth

West of England LEP Greater Cambridge and Greater Peterborough LEP

Oxfordshire LEP Thames Valley Berkshire LEP

Gloucestershire LEP Swindon and Wiltshire LEP

(%)

Source: Oxford Economics

Annual average growth (%), 2015-2036

West of England

LEP

Greater Cambridge

and Greater

Peterborough LEP

Oxfordshire LEPThames Valley

Berkshire LEPGloucestershire LEP

Swindon and

Wiltshire LEP

Population (000s) 1,105 1,409 673 884 611 699

Population 16-64 (000s) 712 882 431 569 378 435

Net migration (000s) 6.8 9.6 3.8 1.0 4.8 3.0

Total employment (000s) 634 744 398 558 332 367

GVA (£m 2011) 27,930 32,966 18,324 33,305 13,665 15,605

Source: Oxford Economics

Scenarios

As the economic outlook is uncertain, we have looked at two potential scenarios. Our baseline forecast has a 50%

probability.

Upside scenario assumptions

High growth scenario (5% probability). This scenario assumes that faster growth can be achieved through:

Increased investment and exports performance at the UK level. This provides a significant boost to manufacturing,

information & communications and professional services.

Consumers play a big role in the recovery. The faster growth of the above sectors raises consumer confidence and

produces a multiplier effect through local economies with high concentrations of those sectors, which benefits consumer

led sectors including wholesale & retail trade and accommodation & food services.

No further public spending cuts. Given the improved economic conditions, the government benefits from increased

revenue and is able to ease the austerity program. As a result public sector employment remains relatively flat, rather

than falling.

Medium-high growth scenario (10% probability). This scenario assumes that faster growth can be achieved through:

Increased investment and exports performance at the UK level. This provides a significant boost to manufacturing,

information & communications and professional services.

Consumers play less of a role in the recovery than in the high growth scenario. The faster growth in the above

sectors fails to raise consumer confidence significantly and the multiplier effect on consumer led sectors is dampened.

Public spending cuts remain. Despite the improved economic conditions, the government sticks to the austerity

program outlined in our baseline view.

26

Upside scenarios: summary results

West of England LEP: GVA performance West of England LEP: Total employment performance

In the event of a more robust macroeconomic performance envisaged under the high growth scenario, the West of

England LEP will benefit from a more positive economic outlook over the forecast period. Higher levels of investment

and an improved export performance will help drive growth in construction and manufacturing. Although the West of

England is somewhat underrepresented in these sectors, they provide a catalyst for growth amongst consumer led

sectors. Under the high growth scenario, GVA will grow on average by 3.3% per year in the decade to 2025,

significantly above the baseline forecast of 2.6%. GVA growth is more sustained under the high growth scenario, with

post-2025 growth averaging 3.2% annually compared to 2.2% under baseline assumptions. Employment will also

receive a notable increase under this scenario, rising by 0.9% in the period to 2036, creating 69,000 jobs in addition to

the baseline. The region’s supply-side constraint is likely to be eased against a backdrop of greater economic growth as

the LEP benefits from greater levels of inward net migration

In the medium-high growth scenario, the West of England LEP receives a boost in employment and GVA,

outperforming the baseline forecasts. But with austerity cuts still on the table and dampened consumer confidence,

employment and GVA growth will be restricted on the upside. 27

500

550

600

650

700

750

800

2000 2005 2010 2015 2020 2025 2030 2035

Medium-high High Base

Source: Oxford Economics

ForecastForecast

(000s)

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

2000 2005 2010 2015 2020 2025 2030 2035

Medium-high High Base

Source: Oxford Economics

ForecastForecast

(%)

Scenario comparison

28

West of England LEP: The decade ahead

West of England LEP: Long-term forecasts

When comparing the decade ahead to our long-term forecasts it is evident that the initial period will provide the impetus for

growth. However, the ‘cooling’ of the economy is only marginal in the high growth scenario and limited in the medium-high

growth scenario. The baseline forecasts for the West of England LEP exhibits the most pronounced drag on growth in the long-

term. Most notably shown in total and FTE employment forecasts, with annual average growth expected to average 0.6% per

year until 2025, with the average declining to half this pace in the subsequent years to 2036.

Baseline Medium-high HighEmployment (000s) 32.8 48.2 61.0

Annual average (%) 0.6 0.8 1.0

FTE employment (000s) 27.4 41.0 52.2

Annual average (%) 0.6 0.8 1.0

GVA Annual average (%) 2.6 3.0 3.3

Population (000s) 81.3 83.5 95.3

Annual average (%) 0.7 0.7 0.8

Net Migration Annual average (000s) 3.3 3.5 4.6

Source: Oxford Economics

Change 2015-2025

Baseline Medium-high HighEmployment (000s) 53.5 87.9 122.3

Annual average (%) 0.4 0.7 0.9

FTE employment (000s) 43.9 74.3 104.6

Annual average (%) 0.4 0.6 0.9

GVA Annual average (%) 2.4 2.8 3.2

Population (000s) 141.4 152.1 176.7

Annual average (%) 0.6 0.6 0.7

Net Migration Annual average (000s) 2.6 3.1 4.3

Source: Oxford Economics

Change 2015-2036

Summary

Summary

The global economy is forecast to enter a period of solid growth with the world’s largest economies experiencing an

improved economic outlook. The US looks set to be the driver of the global economy as it experiences robust

growth on the back of high levels of consumer confidence and spending. With the Eurozone returning to growth in

2014, the outlook for Europe looks positive, despite uncertainty surrounding the details of the Greek deal presenting

some downside risk. This is important for the UK and West of England LEP as Europe remains a key trading

partner, with developments on the continent affecting demand, confidence and influencing government policy.

The UK’s economy has experienced a strong recovery with GVA growth reaching 3.0% in 2014. After a soft start to

2015 in Q1, a firming in Q2, underpinned by services, has buoyed growth estimates for the year. UK growth will be

underpinned by a number of factors including: rising household expenditure - driven by rising wages and low

inflation; strong corporate finances supporting investment; and sustained rises in housebuilding.

UK jobs are forecast to rise by 3.2 million between 2015 and 2036, with total employment reaching 37.0 million.

Employment growth is primarily in private services, with 1.7 million additional jobs expected in professional services

and administration & support. Notable exceptions to this trend are construction and healthcare which are forecast to

rise by 1.0 million.

Employment in the West of England LEP is forecast to rise on average by 0.6% per year over the decade ahead to

2025, before halving to around 0.3% per year thereafter. This will increase employment in the LEP to 697,000 by

2036, creating an additional 54,000 jobs. Accounting for the largest rises in employment are professional services

(16,000 additional jobs), administration & support (12,000), construction (9,500) and healthcare (9,100). These gains

will be partially offset by losses in manufacturing (9,700) and public administration (3,700). As a result the

employment structure is likely to become further dominated by services, which will account for 87% of total

employment by 2036.

30

Annex A: Data sources and assumptions

Model overview

This annex provides technical information on the structure of Oxford Economics Local Authority District Forecasting

Model and details of the data sources and definitions of variables within the model. The model should be viewed as

one piece of evidence in making policy decisions and tracking economic and demographic change. As with all

models it is subject to margins of error which increase as the level of geographical detail becomes smaller, and

relies heavily upon published data.

Models, though predominantly quantitative, also require a degree of local knowledge and past experience, or more

generally forecasting art, to make plausible long term projections. To this end the Oxford model has been developed

by a team of senior staff who have a long history in model building and forecasting at both local and regional levels.

The Local Authority District Forecasting Model sits within the Oxford suite of forecasting models. This structure

ensures that global and national factors (such as developments in the Eurozone and UK Government fiscal policy)

have an appropriate impact on the forecasts at a local authority level. This empirical framework (or set of ‘controls’)

is critical in ensuring that the forecasts are much more than just an extrapolation of historical trends. Rather, the

trends in our global, national and sectoral forecasts have an impact on the local area forecasts.

32

Hierarchal structure of Oxford Economics’ suite of models

Oxford Economics

Global model

Oxford Economics

UK industry model

Oxford Economics

UK macro model

Oxford Economics

UK regional model

Oxford Economics

UK LAD forecasting model

33

Local forecasting model

The Local Authority District Forecasting Model produces base forecasts, which can be compared with other

published forecasts (though care should be taken over data definition issues), and as a guide to aid commentary or

analysis of West of England LEP and its local authority economies. These forecasts can in one sense be considered

to provide baseline ‘policy off’ projections with which the actual outturn under policy initiatives could be compared.

However it must be realised that there are inherent difficulties in using the forecasts as a ‘policy-off’ baseline. In

particular the base projections are ‘unconstrained’ in the sense that they make no allowance for constraints on

development which may be greater than in the past.

Our local forecasting model depends essentially upon three factors:

■ National/regional outlooks – all the forecasting models we operate are fully consistent with the broader global

and national forecasts which are updated on a monthly basis.

■ Historical trends in an area (which implicitly factor in supply side factors impinging on demand), augmented

where appropriate by local knowledge and understanding of patterns of economic development built up over

decades of expertise, and

■ Fundamental economic relationships which interlink the various elements of the outlook.

34

Model structure

The main internal relationships between variables are summarised below. Each variable is related to others within

the models. Key variables are also related to variables in the other Oxford Economics models.

Households

Workplace wages

(by sector)

UK macro

trends

House prices

Commuting

(by occupation)

Employment

(residence based)

Resident wages

(total)

Population Unemployed/Inactive Migration

Natural increase

Employment

(workplace based)

GVA by sector

Key

South West trends

35

Data sources and assumptions

Population and migration

Population and migration data are collected from the Mid-Year estimates (MYE) for each area. These have been

revised in line with the 2011 Census results. The latest data available is for 2014.

Oxford Economics produce their own forecasts of population which are economically driven and thus differ from the

official population projections. Official births and deaths projections from 2012-based population projections are used

but we have our own view on UK migration. The chart below sets out the Oxford migration forecast for the UK

compared with the 2012-based population projection. Oxford Economics expect UK net migration to average

157,000 per annum from 2015-2036, compared to 167,000 in the official projections. The latest data suggests that

UK net migration reached 260,000 in 2014, which is already considerably above the official projections (166,000).

36

West of England LEP: Net migration projections UK: Net migration projections

-50

0

50

100

150

200

250

300

350

1992 1997 2002 2007 2012 2017 2022 2027 2032

Oxford Economics Official 2012-based

Source: Oxford Economics

Forecast

(000s)

Source: Oxford Economics

Forecast

(000s)

-2

0

2

4

6

8

10

12

14

1992 1997 2002 2007 2012 2017 2022 2027 2032

Oxford Economics Official 2012-based

Source: Oxford Economics

Forecast

(000s)

Source: Oxford Economics

Forecast

(000s)

Data sources and assumptions

Population and migration (continued)

The divergence reflects stronger economic prospects and displacement affects from the Middle East and North

Africa. Oxford Economics’ population forecasts are derived from an economically driven model whereas official

projections are trend based and do not consider how demand in the economy (and the likely impact on employment

rates) affects migration.

At the local level, migration is linked to the employment rate forecast. If the employment rate within an area is falling

too fast, migration reacts as the model assumes that people would not be attracted into this area to live, given that

the employment prospects are weak. This approach ensures that the relationship between the labour market outlook

and the demographic forecasts is sensible. This series is scaled to be consistent with the migration forecast for the

South West from the UK Regional Model.

The total population forecast is then constructed using the forecast of migration and the natural increase

assumptions. Natural increase for local areas is forecast based upon recent trends in both the historical data and the

official projections.

Working age population

Working age population data is also collected from the Mid-Year estimates (MYE) for each area up to 2014. It is

defined as all people aged 16 to 64.

The share of working age to total population is forecast using both trends in the official projections and trends in the

South West forecast from our UK Regional Model. This is applied to the total population forecast and scaled to be

consistent with the working age population for the South West.

37

Data sources and assumptions

Employees in employment

There are two key sources for the employee jobs data – ONS Workforce Jobs (WFJ) and the Business Register and

Employment Survey (BRES):

The WFJ series is reported on a quarterly basis, providing estimates of employee jobs by sector (based on the 2007

Standard Industrial Classification – SIC 2007) for the UK and its constituent government office regions, over the

period 1981Q3 to 2015Q1.

The BRES is an employment survey which has replaced the Annual Business Inquiry (ABI). Similar to WFJ, BRES

data is based upon SIC 2007, but it is only published for the years 2008-13. Prior to this, ABI and Annual

Employment Survey (AES) data is available for employee jobs data, however this is based on an older industrial

classification (SIC 2003). Data is available at local authority level and more detailed sector definitions. It is worth

noting that the BRES is first and foremost a survey and is therefore subject to volatility, particularly when the level of

detail becomes more refined. The survey is collected in September of each year and not seasonally adjusted.

There are a number of steps in constructing regional employee jobs, due to changes in sectoral classifications

across the various sources, and restrictions on data availability over particular periods of time. Initially, we take

employee jobs data for each sector directly from the BRES over the years 2009-13, which reflects recent

methodological changes to the BRES in accounting for working proprietors. This relates to September figures and is

based upon SIC 2007 sectors. In 2008, levels of employee jobs are constructed by extrapolating back the trend in

the old BRES. Data from the ABI and AES is used to construct the data back to 1991.

This constructed local dataset is then scaled to be consistent with the UK employee jobs series from WFJ, by

applying an adjustment factor to all sectors which converts the data to annual average values (seasonally adjusted).

38

Data sources and assumptions

Employees in employment (forecasts)

The starting point in producing employment forecasts is the determination of workplace-based employees in

employment in each of the broad 19 SIC2007 based sectors consistent with the South West and UK outlooks. At

local authority level some of the sectors are driven predominantly by population estimates, others by total

employment in the area and the remainder relative to the regional performance (largely exporting sectors). All

sectors are also influenced by past trends in the local area. Taken in totality, employment is cross referenced with a

number of variables (including population, relative performance across similar areas, historical cyclical performance

and known policy) for checking and validation purposes. Where necessary, manual adjustments are made to the

projected trends to reflect this validation process. The methods of sectoral projection are as follows, each of which

are forecast based upon recent trends:

Share of the South West: Agriculture; Mining and quarrying; Manufacturing; Electricity, gas & steam; Water

supply; sewerage, waste management; Information and communication; Financial and insurance activities

Location quotient based upon total employment: Construction; Real estate activities; Professional,

scientific and technical activities; Administrative and support service activities

Location quotient based upon consumer spending: Wholesale and retail trade; Transportation and

storage; Accommodation and food service activities; Arts, entertainment and recreation; Other service activities

Location quotient based upon population: Public administration and defence; Education; Human health

and social work activities

These sectors are then split out into their detailed 2 digit sector forecasts using shares from the raw BRES data. The

shares are forecast in line with changes in the detailed sector for South West and then constrained to both the broad

sector forecast within the local area and also to the detailed South West forecasts produced in the UK Regional

Model.

39

Data sources and assumptions

Self-employment

Self-employment data for the South West is taken from Workforce jobs (19 sector detail). The data is broken down

into detailed sectors using both employee trends and the UK data for self-employment by 2 digit SIC2007 sector.

Data for the local authorities is Census based (and scaled to the South West self-employed jobs estimates) and is

broken down using the employees in employment sectoral structure. The sectors are forecast using the growth in

the sectoral employees in employment data and the estimates are scaled to the regional estimate of self-

employment by sector.

Total employment

Total employment includes employees in employment, the self-employed and Her Majesty’s Forces. No specific

forecasting for this measure is required - it is calculated from the forecasted elements discussed above.

Note that this estimate is a jobs and not people measure (i.e. one person can have more than one job and would be

counted more than once in this indicator).

Unemployment

Claimant count unemployment data is taken from ONS, via NOMIS. Annual average values are calculated from the

monthly data. The latest data available is July 2015.

Unemployment (claimant count) is projected based on regional trends and a measure of overall labour market

tightness (relative employment rate) in the local area. It is not at present directly affected by migration though they

do impact indirectly through the employment rate (which has working age population as its denominator).

Unemployment rate is defined as claimant count unemployment as a percentage of the working age population. No

specific forecasting of this measure is required.

40

Data sources and assumptions

Resident employment

Resident employment data is taken from the Annual Population Survey. The latest year of available data is 2014.

Given that this data is survey based and tends to be very volatile, data is ‘smoothed’ by taking a 3 year average.

Residence employment is based on a commuting matrix taken from the 2011 Census. This matrix tells us where

employed residents of an area work. Using this information each available job (see workplace employment people

based above) is allocated to a resident of a given authority. This method assumes the proportions of commuting do

not change over time.

Employment rate is defined as residence employment as a percentage of the population aged 16 plus. No specific

forecasting of this measure is required.

Gross Value Added

GVA forecasts are available for detailed sectors for the South West region from our UK Regional Model. For areas

within the region, data on total GVA is available at NUTS 3 level. This includes counties and former Metropolitan

counties. Our forecasts at local authority level are obtained firstly by calculating an ‘expected’ GVA in each area.

This is calculated by multiplying the South West region’s GVA per employee in each sector by workplace

employment in each sector within each local authority area. An adjustment factor based upon relative earnings is

also applied as areas with higher wages should produce higher levels of GVA. Expected GVA is then scaled to add

the GVA at NUTS 3 level and the South West sectoral forecasts from the UK Regional Model.

41