economic trends may 2013

TRANSCRIPT

96

98

100

102

104

106

108

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

Economic Trends May 2013

Annualized Quarterly Growth in Real GDP

4.0

%

1.9

%

1.2

% 3

.1%

0

.4%

2

.5%

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2000q1 2001q1 2002q1 2003q1 2004q1 2005q1 2006q1 2007q1 2008q1 2009q1 2010q1 2011q1 2012q1 2013q1

Darker Bars Represent National Recessions.

MS University Research Center, IHL 2 May 2013

The up-down-up pattern is largely due to technical reasons (Inventory correction, defense spending, Hurricane Sandy)

US Jobs Added (Subtracted) By Month

MS University Research Center, IHL 3

(1,000,000)

(800,000)

(600,000)

(400,000)

(200,000)

0

200,000

400,000

600,000

2007 2008 2009 2010 2011 2012 2013

May 2013

Average Monthly Gain in 2013 is 195,750.

US Nonfarm Employment

100,000

105,000

110,000

115,000

120,000

125,000

130,000

135,000

140,000

Tho

usa

nd

s

May 2013 MS University Research Center, IHL 4

Peak-to-trough loss 8.8 million jobs or 6.4%. Gains since trough 5.7 million jobs. We remain 2.2% below peak.

Institute For Supply Management Indices

30.0

35.0

40.0

45.0

50.0

55.0

60.0

65.0

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

ISM

Ind

ices

: ab

ove

50

is e

xpan

din

g

Manufacturing Index Nonmanufacturing Index

MS University Research Center, IHL 5 May 2013

An ISM Index above 50 says the industry is expanding. Below 50 indicates a contraction.

Both series have declined.

Real US Retail Sales Adjusted for Inflation

$280,000

$290,000

$300,000

$310,000

$320,000

$330,000

$340,000

$350,000

Mo

nth

ly S

ale

s M

illi

on

s o

f 2

00

4 $

MS University Research Center, IHL 6 May 2013

Retail sales remain relatively modest. We are only just now to the pre-recession level of sales. Recent improvement was fueled by

higher gasoline prices and auto sales.

US Light Vehicle Sales

9.0

11.0

13.0

15.0

17.0

19.0

21.0

23.0

Mill

ion

s o

f U

nit

s, S

AA

R

MS University Research Center, IHL 7 May 2013

Light vehicle sales have been a bright spot in the economy with average sales

of 14.4 million units in 2012. April marked the first time since October 2012

the level fell below 15 million units.

Weekly U.S. Regular Retail Gasoline Prices Dollars Per Gallon

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

May 2013 MS University Research Center, IHL 8

Because of limited incomes, high gasoline prices hit Mississippians especially hard and have a dampening

effect on discretionary spending.

US Consumer Sentiment Historically Low

50.0

60.0

70.0

80.0

90.0

100.0

110.0

120.0Ja

n-9

0

Jan

-91

Jan

-92

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Un

iver

sity

of

Mic

hig

an In

dex

, 19

66

= 1

00

MS University Research Center, IHL 9 May 2013

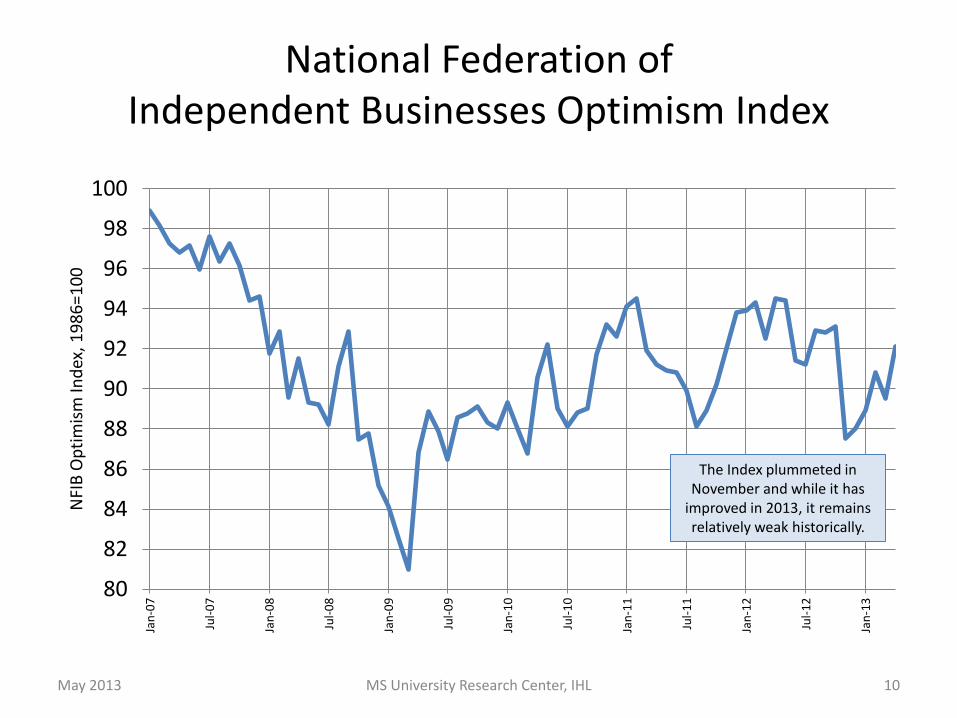

National Federation of Independent Businesses Optimism Index

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

80

82

84

86

88

90

92

94

96

98

100

NFI

B O

pti

mis

m In

dex

, 19

86

=10

0

MS University Research Center, IHL 10 May 2013

The Index plummeted in November and while it has

improved in 2013, it remains relatively weak historically.

Year-Over-Year Growth in Real Personal Income Less Transfer Payments

by Quarter

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Mar

-60

Mar

-62

Mar

-64

Mar

-66

Mar

-68

Mar

-70

Mar

-72

Mar

-74

Mar

-76

Mar

-78

Mar

-80

Mar

-82

Mar

-84

Mar

-86

Mar

-88

Mar

-90

Mar

-92

Mar

-94

Mar

-96

Mar

-98

Mar

-00

Mar

-02

Mar

-04

Mar

-06

Mar

-08

Mar

-10

Mar

-12

May 2013 MS University Research Center, IHL 11

Gray Areas Represent National Recessions.

Declines are characteristic of recessions. Growth trended downward in 2011 and early 2012, but did

not go negative. Growth improved in late 2012.

96

98

100

102

104

106

108

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

Ind

ex 2

00

4=

100

MS Index of Coincident Indicators

12 MS University Research Center, IHL May 2013

The MSCI has risen for 9 consecutive months. But the

momentum has softened in 2013.

The Mississippi Index of Coincident Indicators reflects economic conditions existing in a given month. The index is constructed by the Federal Reserve Bank of Philadelphia and re-indexed to 2004. The Index is based on changes in nonfarm employment, the unemployment rate, average manufacturing workweek length and wage and salary disbursements.

Regional Comparison March Coincident Index as Percentage of Pre-recession Peak

93.4%

96.5%

91.2%

97.4% 98.1%

99.7% 98.9%

98.0% 99.0%

95.5%

101.9%

107.4%

103.4%

80.0%

85.0%

90.0%

95.0%

100.0%

105.0%

110.0%

AL AR FL GA KY LA MS NC OK SC TN TX US

May 2013 MS University Research Center, IHL 13

MS Index of Leading Indicators

80

85

90

95

100

105

110

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

Ind

ex 2

00

4=

100

14 MS University Research Center, IHL

The Index shows a softening of growth during the first quarter.

May 2013

The Mississippi Index of Leading Indicators reflects economic conditions expected for the coming months. The index is constructed by the University Research Center and indexed to 2004. There are 8 components of the Index: MS Initial Unemployment Claims; MS Income Tax Withholdings; MS Value of Residential Building Permits; MS MFG Employment Intensity Index, MS Diesel Fuel Consumption Index; ISM Index of US MFG Activity; US Consumer Expectations Index and US Retail Sales.

MS Nonfarm Employment

800

850

900

950

1,000

1,050

1,100

1,150

1,200

Tho

usa

nd

s

May 2013 MS University Research Center, IHL 15

Jobs have been slow to return to Mississippi following the “Great Recession”.

Growth began to improve in late 2012.

1,162.1

May 00

1,110.9

Jun 03

1,161.9

Feb 08

1,116.6

Mar 13

Employment Index December 2007 = 100

90%

92%

94%

96%

98%

100%

102%

De

cJa

n 0

8Fe

bM

arA

pr

May Jun

Jul

Au

gSe

pO

ctN

ov

De

cJa

n 0

9Fe

bM

arA

pr

May Jun

Jul

Au

gSe

pO

ctN

ov

De

cJa

n 1

0Fe

bM

arA

pr

May Jun

Jul

Au

gSe

pO

ctN

ov

De

cJa

n 1

1Fe

bM

arA

pr

May Jun

Jul

Au

gSe

pO

ctN

ov

De

cJa

n 1

2Fe

bM

arA

pr

May Jun

Jul

Au

gSe

pO

ctN

ov

De

cJa

nFe

bM

arA

pr

US MS

MS University Research Center, IHL May 2013 16

MS Employment Trends By Major Industry

0

50

100

150

200

250

300

Tho

usa

nd

s

Construction MFG Trade, Trans and UtlitiesProfessional Services Education and Health Services Leisure and HospitalityGovernment

May 2013 MS University Research Center, IHL 17

MS Real Income Tax Withholdings Six Month Moving Monthly Average Growth Over Prior Year

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Ja

n-0

0

Ja

n-0

1

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

Ja

n-0

9

Ja

n-1

0

Ja

n-1

1

Ja

n-1

2

Ja

n-1

3

18 MS University Research Center, IHL May 2013

CY 2011 -0.7% CY 2012 3.2%

CY 2013 To Date -1.6%.

Year-Over-Year Growth in MS Real Personal Income Less Transfer Payments

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Mar-00 Mar-01 Mar-02 Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12

May 2013 MS University Research Center, IHL 19

Growth has slowed since early 2011, but remains positive.

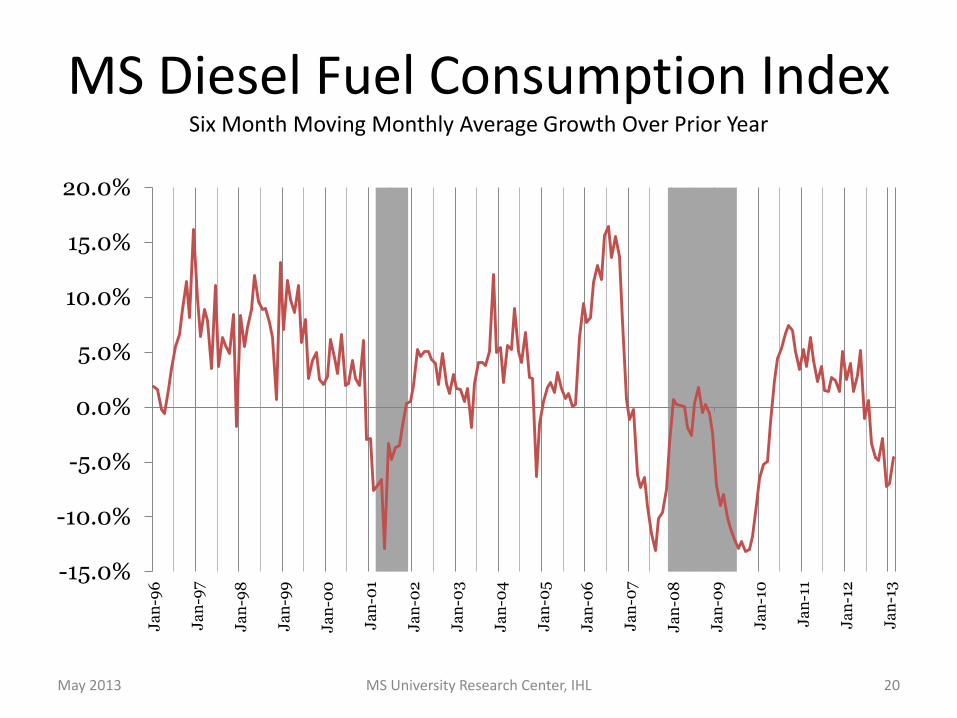

MS Diesel Fuel Consumption Index Six Month Moving Monthly Average Growth Over Prior Year

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

Ja

n-9

6

Ja

n-9

7

Ja

n-9

8

Ja

n-9

9

Ja

n-0

0

Ja

n-0

1

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

Ja

n-0

9

Ja

n-1

0

Ja

n-1

1

Ja

n-1

2

Ja

n-1

3

20 MS University Research Center, IHL May 2013

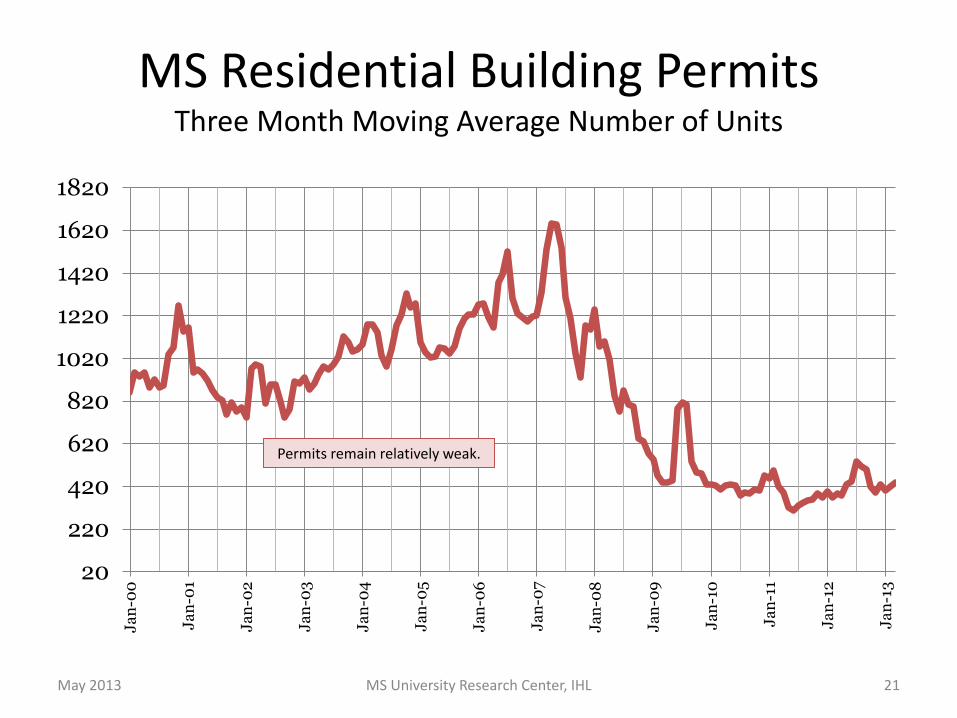

MS Residential Building Permits Three Month Moving Average Number of Units

20

220

420

620

820

1020

1220

1420

1620

1820

Ja

n-0

0

Ja

n-0

1

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

Ja

n-0

9

Ja

n-1

0

Ja

n-1

1

Ja

n-1

2

Ja

n-1

3

21 MS University Research Center, IHL May 2013

Permits remain relatively weak.

MS Construction Employment

20.0

25.0

30.0

35.0

40.0

45.0

50.0

55.0

60.0

65.0

70.0Ja

n-9

0

Jan

-91

Jan

-92

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Tho

usa

nd

s

May 2013 MS University Research Center, IHL 22

MS construction employment remains relatively weak

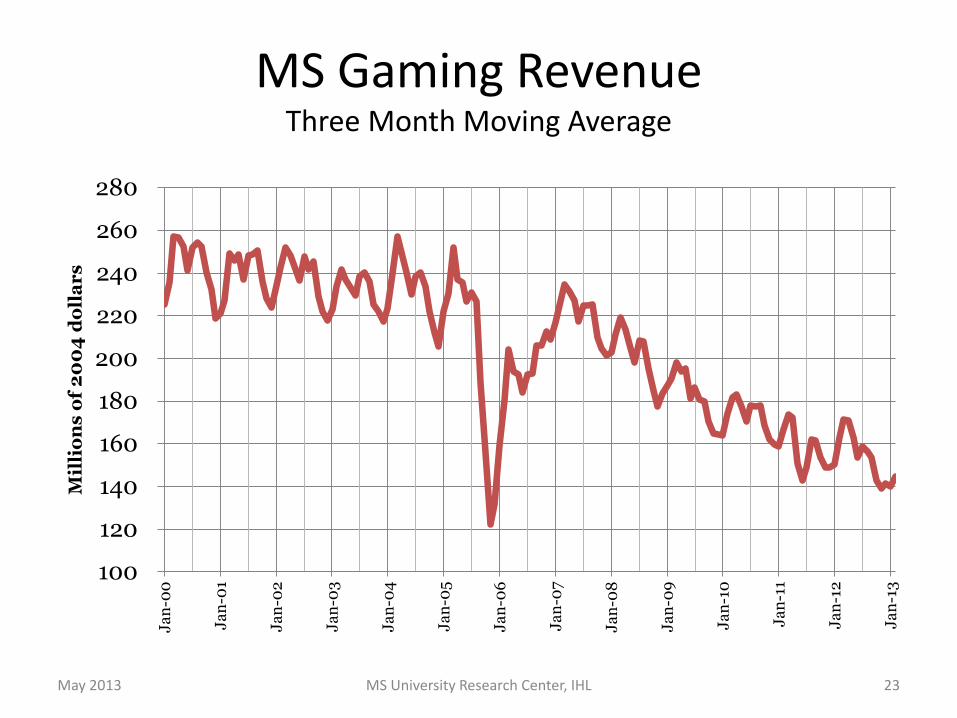

MS Gaming Revenue Three Month Moving Average

100

120

140

160

180

200

220

240

260

280J

an

-00

Ja

n-0

1

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

Ja

n-0

9

Ja

n-1

0

Ja

n-1

1

Ja

n-1

2

Ja

n-1

3

Mil

lio

ns

of

20

04

do

lla

rs

23 MS University Research Center, IHL May 2013

MS Unemployment Claims Three Month Moving Average

0

50

100

150

200

250

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Ja

n-0

0

Ja

n-0

1

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

Ja

n-0

9

Ja

n-1

0

Ja

n-1

1

Ja

n-1

2

Ja

n-1

3

Th

ou

sa

nd

s

Initial Claims Continued Claims

24 MS University Research Center, IHL May 2013

MS Manufacturing Workweek Length Three Month Moving Average

37

38

39

40

41

42

43

44

Ja

n-0

0

Ja

n-0

1

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

Ja

n-0

9

Ja

n-1

0

Ja

n-1

1

Ja

n-1

2

Ja

n-1

3

25 MS University Research Center, IHL May 2013