economics 2010a game theory section notes · •theory: bayesiannashequilibrium •application:...

TRANSCRIPT

Economics 2010a Game Theory Section Notes

Jetlir Duraj(based on an extended version of section notes first produced by Kevin He)∗

December 4, 2018

∗These are an expanded version of the section notes by Kevin He. They contain additional exercises and material from olderproblem sets of Jerry Green, from the Book Game Theory by Maschler, Solan and Zamir and from the graduate book with thesame title of Roger Myerson. Send comments, critique to [email protected]

Economics 2010a . Section 1 : Welcome to Game Theory1 10/23/2018∣∣∣∣ (0) Welcome; (1) Course outline; (2) Normal form games; (3) Extensive form games; (4) Strategies in

extensive form games; (5) Optional: on the absent-minded driver.∣∣∣∣

TF: Jetlir Duraj ([email protected])

0 Welcome

“But I don’t want to go among mad people,” Alice remarked.“Oh, you can’t help that,” said the Cat: “we’re all mad here. I’m mad. You’re mad.”“How do you know I’m mad?” said Alice.“You must be,” said the Cat, “or you wouldn’t have come here.”

— Alice in Wonderland, on mutual knowledge of irrationality.2

1 Course Outline via a Taxonomy of Games

1.1 A taxonomy of games. The second half of Economics 2010a is organized around several types ofgames of interest in economics, paying particular attention to (i) relevant solution concepts in thedifferent settings we will consider, and (ii) some key economic applications belonging to these settings. Tounderstand the course outline, it is helpful to first introduce some non-rigorous binary classification schemesthat give rise to the game types we will consider in this course.Rigorous definitions of the following terminologies are not feasible without first laying down some background,so at this point we will instead appeal to hopefully familiar games to illustrate the classifications.A game may have...

• Simultaneous moves (eg. rock-paper-scissors) or sequential moves (eg. chess)

• Complete information (eg. chess) or incomplete information (eg. poker)

• Chance moves (eg. Backgammon) or no chance moves (eg. Reversi)

• Finite horizon (eg. tic-tac-toe) or infinite horizon (eg. Gomoku on an infinite board)

• Zero-sum payoff structure (eg. poker) or non-zero-sum payoff structure (eg. the usual model ofprisoner’s dilemma)

1.2 Course outline. Roughly, the course can be divided into 4 units. Each unit is focused on one type ofgame, studying first its solution concepts then some important examples and applications.game type 1: simultaneous move games with complete information

• theory: Nash equilibrium and its extensions, rationalizability

• application: Nash implementation

game type 2: simultaneous move games with incomplete information

• theory: Bayesian Nash equilibrium

• application: Global Games, Auctions1These are an expanded version of the Section Notes first compiled by Kevin He. They contain additional exercises and

material from older problem sets of Jerry Green, from the Book Game Theory by Maschler, Solan and Zamir and from thegraduate book with the same title of Roger Myerson. Send comments, critique to [email protected]. Figure 1 is due toHaluk Ergin. Figures for Example 11 and Example 12 are adapted from Maschler, Solan, and Zamir (2013): Game Theory [1].

2And on being accepted to Harvard for grad school.

1

game type 3: sequential move games with complete information

• theory: Subgame perfect equilibrium

• application: Bargaining games, repeated games

game type 4: sequential move games with incomplete information

• theory: Perfect Bayesian equilibrium, sequential equilibrium, strategically stable equilibrium, etc

• application: Signaling games

1.3 About sections. Sections are optional. We will review lecture material and work out additional examples.Questions, remarks or critique related to these notes are very welcome.

2 Normal Form Games

2.1 Interpreting the payoff matrix. Here is the familiar payoff matrix representation of a two-player game.

L R

T 1,1 0,0B 0,0 2,2

Player 1 (P1) chooses a row (Top or Bottom) while player 2 (P2) chooses a column (Left or Right). Eachcell contains the payoffs to the two players when the corresponding pair of strategies is played. The firstnumber in the cell is the payoff to P1 while the second number is the payoff to P2. (By the way, this gameis sometimes called the “game of assurance”.)Two important things to keep in mind:(1) In a normal form game it is usually assumed, that players choose their strategies simultaneously. Thatis, P2 cannot observe which row P1 picks when choosing his column. In this case it is irrelevant when theactual decisions are taken, as long as no player can observe her opponents’ decisions.3

(2) The terminology “payoff matrix” is slightly misleading. The numbers that appear in a payoff matrixare actually Bernoulli utilities, not monetary payoffs. To spell out this point in painstaking details: theset of possible outcomes of the game is X := TL, TR,BL,BR. Each player j has a preference %j over∆(X), the set of distributions on this 4 point set. Assume %j is complete and transitive and satisfies thevNM axioms of Independence and Continuity. Then, due to the vNM representation theorem, we find that%j is represented by a utility function Uj : ∆(X)→ R , given by

Uj(p) = pTL · uj(TL) + pTR · uj(TR) + pBL · uj(BL) + pBR · uj(BR).

We then enter uj(TL), uj(TR), uj(BL), uj(BR) into the payoff matrix cells, which happen to be 1, 0, 0, 2.In particular, in computing the expected utility of each player under a mixed strategy profile, we simply takea weighted average of the matrix entries – there is no need to apply a “utility function” to the entries beforetaking the average as they are already denominated in utils. Furthermore, it is important to remember thatlinearity is only given in probabilities, and in particular it does not imply risk-neutrality of the players. It israther a property of the vNM representation.4Finally, as was just established, we will use the Expected Utility paradigm when modeling Choice underUncertainty throughout this course. This is by far not the only way to model Choice under Uncertainty and

3But note that this statement has a hidden assumption: that players’s preferences are stable and don’t change with time.4In fact, mixed strategies in game theory provided one of the motivations for von Neumann and Morgenstern’s work on

their representation theorem for preference over lotteries. Von Neumann’s 1928 theorem on the equality between maxmin andminmax values in mixed strategies for zero-sum games assumed players choose the mixed strategy giving the highest expectedvalue. But why should players choose between mixed strategies based on expected payoff rather than median payoff, mean payoffminus variance of payoff, or say the 4th moment of payoff? The vNM representation theorem finds sufficient and necessaryconditions on their preference over lotteries, which yield the expected utility representation. Note, that utilities are (1) notobservable and (2) not even scale invariant, but choices indeed are observable. The latter is true at least in principle and inmany cases in reality as well.

2

doing game theory with other classes of preferences remains an open area of research, but Expected Utilityis the standard paradigm and so we stick to it in this introductory course.2.2 General definition of a normal form game. The payoff matrix representation of a game is convenient,but it is not sufficiently general. In particular, it seems unclear how we can represent games in which playershave infinitely many possible strategies, such as a Cournot duopoly. Thus the following, more generaldefinition.

Definition 1. A normal form game G = 〈N , (Sk)k∈N , (uk)k∈N 〉 consists of:

• A finite collection of players5 N = 1, 2, ..., N

• A set of pure strategies Sj for each j ∈ N

• A (Bernoulli) utility function uj : ×Nk=1Sk → R for each j ∈ N

To interpret, the pure strategy set Sj is the set of actions that player j can take in the game. Wheneach player chooses an action simultaneously from their own pure strategy set, we get a strategy profile(s1, s2, ..., sN ) ∈ ×Nk=1Sk. Players derive payoffs by applying their respective utility functions to the strategyprofile.The payoff matrix representation of a game is a specialization of this definition. In a payoff matrix for 2players, the elements of S1 and S2 are written as the names of the rows and columns, while the values of u1and u2 at different members of S1 × S2 are written in the cells. If S1 = sA1 , sB1 and S2 = sA2 , sB2 , thenthe game G = 〈1, 2, (A1, A2), (u1, u2)〉 can be written in a payoff matrix:

sA2 sB2

sA1 u1(sA1 , sA2 ), u2(sA1 , sA2 ) u1(sA1 , sB2 ), u2(sA1 , sB2 )sB1 u1(sB1 , sA2 ), u2(sB1 , sA2 ) u1(sB1 , sB2 ), u2(sB1 , sB2 )

Conversely, the game of assurance can be converted into the standard definition by taking N = 1, 2,S1 = T,B, S2 = L,R, u1(T, L) = 1, u1(B,R) = 2, u1(T,R) = u1(B,L) = 0, u2(T, L) = 1, u2(B,R) = 2,u2(T,R) = u2(B,L) = 0,The general definition has the advantage of allowing us to write down games with infinite strategy sets. Ina duopoly setting where firms choose own production quantity, their choices are not taken from a finite setof possible quantities, but are in principle allowed to be any positive real number. So, consider a game withS1 = S2 = [0,∞),

u1(s1, s2) = p(s1 + s2) · s1 − C(s1)

u2(s1, s2) = p(s1 + s2) · s2 − C(s2)

where p(·) and C(·) are inverse demand function and cost function, respectively. Interpreting s1 and s2 asthe quantity choices of firm 1 and firm 2, this is Cournot competition formulated as a normal form game.

3 Extensive Form Games

3.1 Definition of an extensive form game. The rich framework of extensive form games can incorporatesequential moves, incomplete and perhaps asymmetric information, randomization devices such as dice andcoins, etc. It is one of the most powerful modeling tools of game theory, allowing researchers to formally studya wide range of economic interactions. Due to this richness, however, the general definition of an extensiveform game is somewhat cumbersome. An extensive form game can be thought of as a tree endowed withsome additional structures. These additional structures formalize the rules of the game: the timingand order of play, the information of different players, randomization devices relevant to the game, outcomesand players’ preferences over these outcomes, etc.

5From now on: by convention, players 1, 3, 5, ... are female while players 2, 4, 6, ... are male.

3

Definition 2. A finite-horizon extensive form game Γ has the following components:

• A finite-depth tree with vertices V and terminal vertices Z ⊆ V .

• A set of players N = 1, 2, ..., N.

• A player function J : V \Z → N ∪ c.

• A set of available moves Mj,v for each v ∈ J−1(j), j ∈ N . Each move in Mj,v is associated with aunique child of v in the tree.

• A probability distribution f(·|v) over v’s children for each v ∈ J−1(c).

• A (Bernoulli) utility function uj : Z → R for each j ∈ N .

• An information partition Ij of J−1(j) for each j ∈ N , whose elements are information setsIj ∈ Ij . It is required that v, v′ ∈ Ij ⇒Mj,v = Mj,v′ .

The game tree captures all possible states of the game. When players reach a terminal vertex z ∈ Z ofthe game tree, the game ends and each player j receives utility uj(z). The player function J indicates whomoves at each non-terminal vertex. The move might belong to an actual player j ∈ N , or to chance, “c”.Note that J−1(j) refers to the set of all vertices where player j has the move. If a player j moves at vertexv, she gets to pick an element from the set Mj,v and play proceeds along the corresponding edge. If chancemoves, then play proceeds along a random edge chosen according to f(·|v).An information set Ij of player j refers to a set of vertices that player j cannot distinguish between.6It might be useful to imagine the players conducting the game in a lab, mediated by a computer. At eachvertex v ∈ V \Z, the computer finds the player J(v) who has the move and informs her that the game hasarrived at the information set IJ(v) 3 v. In the event that this IJ(v) is a singleton, player J(v) knows exactlyher location in the game tree. Else, she knows only that she is at one of the vertices in IJ(v), but she doesnot know for sure which one.7 The requirement that two vertices in the same information set must have thesame sets of moves is needed to prevent a player from gaining additional information by simply examiningthe set of moves available to her. Otherwise, the idea that the player supposedly cannot distinguish betweenany of the vertices in the same information set would be defeated. For convenience, we also write Mj,Ij forthe common move set for all vertices v ∈ Ij .There are two conventions for indicating an information set Ij in game tree diagrams. Either all of thevertices in Ij are connected using dashed lines, or all of the vertices are encircled in an oval.

Example 3. Figure 1 illustrates all the pieces of the general definition of an extensive form game.For convenience, let’s name each vertex with the sequence of moves leading to it (and name the root as∅). The set of players is N = 1, 2. The player function J(v) is shown on each v ∈ V \Z in Figure 1,while the payoff pair (u1(z), u2(z)) is shown on each z ∈ Z. The set of moves Mj,v at vertex v is shown onthe corresponding edges. Player 1 moves at two vertices, J−1(1) = ∅, (l, a) . Her information partitioncontains only singleton sets, meaning she always knows where in the game tree she is when called upon tomove. Player 2 moves at three vertices, J−1(2) = (r), (l, b), (m) . However, player 2 cannot distinguishbetween (m) and (l, b), though he can distinguish (r) from the other two vertices. Thus, his informationpartition contains two information sets, one containing just (r), the other containing the two vertices (m)and (l, b). As required by the definition, M2,(m) = M2,(l,b) = x, y, so that player 2 cannot figure outwhether he is at (m) or (l, b) by looking at the set of available moves.

6The use of an information partition to model a player’s knowledge predates extensive form games with incomplete informa-tion. Such models usually specify a set of states of the world, Ω, then some partition Ij on Ω. When a state of the world ω ∈ Ωrealizes, player j is told the information set Ij ∈ Ij containing ω, but not the exact identity of ω. So then, finer partitionscorrespond to better information. To take an example, suppose 3 people are standing facing the same direction. An observerplaces a hat of one of two colors (say color 0 and color 1) on each of the 3 people. These 3 people cannot see their own hat coloror the hat color of those standing behind them. Then the states of the world are Ω = 000, 001, 010, 011, 100, 101, 110, 111.The person in the front of the line has no information, so her information partition contains just one information set with allthe states, I1 = 000, 001, 010, 011, 100, 101, 110, 111 . The second person in line sees only the hat color of the first person,so that I2 = 000, 010, 100, 110, 001, 011, 101, 111 . Finally, the last person sees the hats of persons 1 and 2, so thatI3 = 000, 100, 001, 101, 010, 110, 011, 111 . In the context of extensive form games, one might think of J−1(j) asthe relevant “states of the world” for j’s decision-making and the fineness of her information partition Ij reflects the extent towhich she can distinguish between these states.

7She might, however, be able to form a belief as to the likelihood of being at each vertex in IJ(v), based on her knowledgeof other players’ strategies and the chance move distributions.

4

Chance move distributions: f(a|(l)) = f(b|(l)) = 0.5.Information partitions: I1 = ∅, (l, a) , I2 = (r), (l, b), (m) .

Figure 1: An extensive form game with incomplete information and chance moves.

1

2

(1,1)

L

(0,0)

R

T

2

(0,0)

L

(2,2)

R

B

Figure 2: Game of assurance in extensive form.

The definition of extensive form games given above, allows us to formally characterize games of perfectinformation as well.

Definition 4. An extensive form game is called a game of perfect information if all the informationsets of all players contain one node.

3.2 Using information sets to convert a normal form game into extensive form. Every finite normal formgame G =

⟨N , (Sj)Nj=1, (uj)Nj=1

⟩may be converted into an extensive form game of incomplete information

with 1 +∑NL=1

∏Lj=1 |Sj | vertices. Construct a game tree with N + 1 levels, so that all the vertices at level

L belong to a single information set for player L, for 1 ≤ L ≤ N . Level 1 contains the root. The root has|S1| children, corresponding to the actions in S1. These children form the level 2 vertices. Each of theselevel 2 vertices has |S2| children, corresponding to the actions in S2, and so forth. Each terminal vertex zin level N + 1 corresponds to some action profile (sz1, sz2, ..., szN ) in the normal form game G and is assignedutility uj(sz1, sz2, ..., szN ) for player j in the extensive form game. Figure 2 illustrates such a conversion usingthe game of assurance discussed earlier.

4 Strategies in Extensive Form Games

4.1 Pure strategy in extensive form games. How would you write a program to play an extensive form gameas player j? Whenever it is player j’s turn, the program should take the information set as an inputand return one of the feasible moves as an output. As the programmer does not a priori know thestrategies that other players will use, the program must encode a complete contingency plan for playingthe game so that it returns a legal move at every vertex of the game tree where j might be called upon toplay. This motivates the definition of a pure strategy in an extensive form game.

Definition 5. In an extensive form game, a pure strategy for player j is a function sj : Ij → ∪v∈J−1(j)Mj,v,so that sj(Ij) ∈Mj,Ij for each Ij ∈ Ij . Write Sj for the set of all pure strategies of player j.

In simpler words: a pure strategy for player j returns a legal move at every information set of j.

5

Example 6. In Figure 1, one of the strategies of P1 is s1(∅) = m, s1(l, a) = d. Even though playing m atthe root means the vertex (l, a) will never be reached, P1’s strategy must still specify what she wouldhave done at (l, a). This is because some solution concepts we will study later in the course require us toexamine parts of the game tree which are unreached when the game is actually played. Intuitively, thisis necessary because the optimality of an action for a player at some information set may depend on whatshe/he and her/his opponents would have played on an information set which would be reached only if theplayer chooses differently than the strategy under consideration.One of the strategies of P2 is s2((l, b), (m)) = y, s2(r) = z. In every pure strategy P2 must play the sameaction at both (l, b) and (m), as pure strategies are functions of information sets, not individual vertices.In total, P1 has 6 different pure strategies in the game and P2 has 6 different pure strategies.

4.2 Two definitions of randomization. There are at least two natural notions of ’randomizing’ in an extensiveform game: (1) Player j could enumerate the set of all possible pure strategies, Sj , then choose an elementof Sj at random; this corresponds to picking a probability distribution over Sj . (2) Player j could pick arandomization over Mj,Ij for each of her information sets Ij ∈ Ij . These two notions of randomization leadto two different classes of strategies that incorporate stochastic elements:

Definition 7. A mixed strategy for player j is an element σj ∈ ∆(Sj).

Definition 8. A behavioral strategy for player j is a collection of distributions bIjIj∈Ij ,where bIj ∈ ∆(Mj,Ij ).

Strictly speaking, mixed strategies and behavioral strategies form two distinct classes of objects. Wemay, however, talk about the equivalence between a mixed strategy and a behavioral strategy in the followingway:

Definition 9. Say a mixed strategy σj and a behavioral strategy bIj are equivalent if they generatethe same distribution over terminal vertices regardless of the strategies used by opponents, which may bemixed or behavioral.

Note that in this definition for both the behavioral and the mixed case, opponents of j are assumed to playindependently of each other.

Example 10. In Figure 1, a behavioral strategy for P1 is: b∗∅(l) = 0.5, b∗∅(m) = 0, b∗∅(r) = 0.5, b∗(l,a)(t) =0.7, b∗(l,a)(d) = 0.3. That is, P1 decides that she will play m and r each with 50% probability at theroot of the game. If she ever reaches the vertex (l, a), she will play t with 70% probability, d with 30%probability. Now, consider the following 4 pure strategies: s(1)

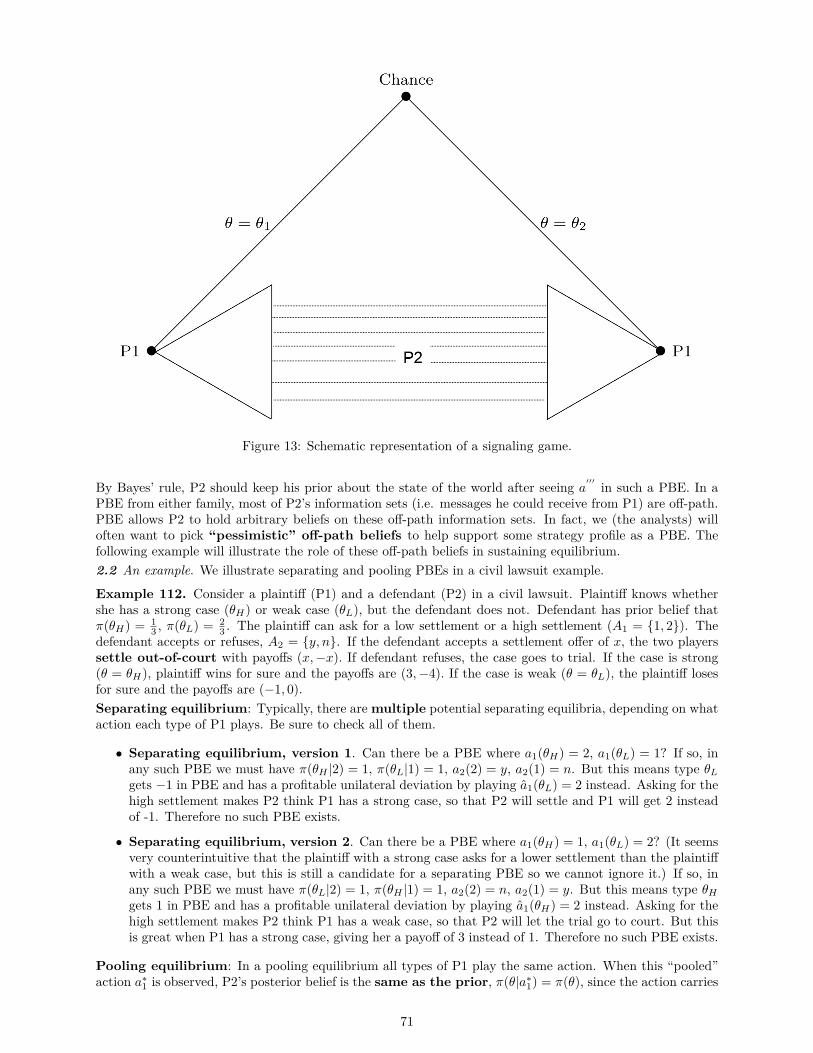

1 (∅) = l, s(1)1 (l, a) = t; s(2)

1 (∅) = l, s(2)1 (l, a) = d;

s(3)1 (∅) = r, s

(3)1 (l, a) = t; s(4)

1 (∅) = r, s(4)1 (l, a) = d and construct the mixed strategy σ∗j so that σ∗j (s(1)

1 ) =0.35, σ∗j (s(2)

1 ) = 0.15, σ∗j (s(3)1 ) = 0.35, σ∗j (s(4)

1 ) = 0.15. Then the behavioral strategy b∗ is equivalent to themixed strategy σ∗j .

It is often “nicer” to work with behavioral strategies than mixed strategies, for at least two reasons. First,behavioral strategies are easier to write down and usually involve fewer parameters than mixed strategies.Second, it feelsmore realistic for a player to randomize at each decision node than to choose a “grand plan”at the start of the game. In general, however, neither the set of mixed strategies nor the set of behavioralstrategies is a “subset” of the other, as we now demonstrate.

Example 11. (A mixed strategy without an equivalent behavioral strategy) Consider an absent-mindedcity driver who must make turns at two consecutive intersections. Upon encountering the second inter-section, however, she does not remember whether she turned left (T ) or right (B) at the first intersection.The mixed strategy σ1 putting probability 50% on each of the two pure strategies T1T2 and B1B2 generatesthe outcome O1 50% of the time and the outcome O4 50% of the time. However, this outcome distributioncannot be obtained using any behavioral strategy. That is, if the driver chooses some probability of turningleft at the first intersection and some probability of turning left at the second intersection, and furthermorethese two randomizations are independent, then she can never generate the outcome distribution of 50% O1,50% O4.

6

Example 12. (A behavioral strategy without an equivalent mixed strategy) Consider an absent-mindedhighway driver who wants to take the second highway exit. Starting from the root of the tree, x1, he wantsto keep left (L) at the first highway exit but keep right (R) at the second highway exit. Upon encounteringeach highway exit, however, he does not remember if he has already encountered an exit before. The driverhas only two pure strategies: always L or always R. It is easy to see no mixed strategy can ever achieve theoutcome O2. However, the behavioral strategy of taking L and R each with 50% probability each time hearrives at his information set gets the outcome O2 with 25% probability.

These two examples are “strange” in the sense that the drivers “forget” some information that they knewbefore. The city driver forgets what action she took at the previous information set. The highway driverforgets what information sets he has encountered. The definition of perfect recall rules out these twopathologies.

Definition 13. An extensive form game has perfect recall if whenever v, v′ ∈ Ij , the two paths leadingfrom the root to v and v′ pass through the same sequence of information sets and take the same actions atthese information sets.

Intuitively, a game of perfect recall makes it impossible for a player who can remember all the informationabout the path of play she gathered in previous stages (i.e. never forgets anything) to find out in which nodeof any non-singleton information set she is located.In the examples above: the city driver game fails perfect recall since taking two different actions from theroot vertex lead to two vertices in the same information set. The highway driver game fails perfect recallsince vertices x1 and x2 are in the same information set, yet the path from root to x1 is empty while thepath from root to x2 passes through one information set.Kuhn’s theorem states that in a game with perfect recall, it is without loss to analyze only behavioralstrategies. Its proof is beyond the scope of this course.

Theorem 14. (Kuhn 1957) In a finite extensive game with perfect recall, (i) every mixed strategy has anequivalent behavioral strategy, and (ii) every behavioral strategy has an equivalent mixed strategy.

5 Optional food for thought: on the absent-minded driver.

The two types of analyses presented here are intuitively nearer to the concepts of Bayesian Nash Equilibriumand Correlated Equilibrium we will cover in later parts of the lecture. They are based on “The absent-mindeddriver”, Aumann et al., Games and Economic Behavior 1997, Vol. 20 pp. 102-116.Consider the absent-minded driver game we saw in the lecture.

7

Y

1

4

continue

exit

Xexit

0

continue

start

We calculated in the lecture, that the optimal behavioral strategy puts probability of p = 23 on Continue.

Here, in the first part we consider another approach to the same problem, which takes beliefs of the driverabout her location within the info set into account, while in the second part we show that with the helpof simple correlating devices it is possible to achieve an even higher payoff than with mixed or behavioralstrategies.

(1) A Bayesian perspective.For the following analysis we assume

1. The driver makes a decision at each intersection through which he passes. Moreover, when at oneintersection, she can determine the action only there, and not at the other intersection–where she isn’t.

2. Since she can’t distinguish between intersections, whatever reasoning obtains at one intersection mustobtain also at the other, and she is aware of this.

This implies the following.

• The optimal decision is the same at both intersections; it is pinned down by the probability of choosingContinue at each intersection. Call it p∗.

• Therefore, at each intersection, the driver believes that p∗ is chosen at the other intersection.

• The driver has a belief over her location within her information set. At each intersection, the driveroptimizes her decision given her beliefs. Therefore, choosing p at the current intersection she is located,must be optimal given the belief that p∗ is chosen at the other intersection. Moreover, her belief mustbe derived from the strategy she chooses.

By the principle of insufficient reason, without any information about the strategy chosen, the prior prob-ability of being at X will be 1

2 . Denote α(p∗) the belief the driver has about being at the intersection X,given her strategy of choosing p∗ at the other intersection. The reasoning above and Bayes rule implies, that

α(p∗) =12

12 + 1

2p∗ .

Given her beliefs about the behavior at the other node, the payoff of choosing p at the current node is

h(p, p∗) = α(p∗)[(1− p) · 0 + p(1− p∗) · 4 + pp∗ · 1] + (1− α(p∗))[(1− p) · 4 + p · 1].

The first part on the r.h.s. of this expression is the probability of being at X times the payoff from strategyp, conditional on being at X, while the second expression is the probability of being at Y times the payofffrom strategy p, conditional on being at Y . p must be chosen optimally, given the belief p∗ and moreover, pmust be equal to p∗, since the agent doesn’t distinguish between the nodes and any beliefs she has must bederived from the strategy chosen in equilibrium. That is, p∗ must fulfill

p∗ ∈ arg maxp∈[0,1]

h(p, p∗). (1)

8

For the function h(p, q) = 11+q [(1 − p) · 0 + p(1 − q) · 4 + pq · 1] + q

1+q [(1 − p) · 4 + p · 1] = (4−6q)p+4q1+q , we

maximize p for fixed q. The solution as a function of q satisfies

p =

0 if q > 2

3any value in [0, 1] if q = 2

31 if q < 2

3 .

This shows that the solution to (1) is unique and equal to p∗ = 23 . The same as for the optimal behavioral

strategy! Recall that the payoff of the optimal behavioral strategy was 43 .

(2)The handkerchief solution. Assume the driver has a handkerchief in her pocket. Whenever she goesthrough an intersection, she ties a knot in the handkerchief, if there was no knot; or she unties the knot, ifthere was one. At the beginning, i.e. at start it is equally probable that the handkerchief had or did nothave a knot. The driver-absent-minded as she is-cannot remember which was the case. Thus, at each one ofthe two intersections, the probability of having a knot in the handkerchief is 1

2 . Therefore, seeing a knot ornot at each intersection does not reveal any information about the intersection.Nevertheless, consider the following strategy for the driver: exit if there is a knot, continue if there is not.The payoff of this simple strategy is 1

2 · 0 + 12 · 4 = 2: with probability 1

2 the handkerchief had a knot, so thatthe driver exits and the payoff is 0 and with probability 1

2 the handkerchief had no knot so that the drivercontinues and ties a knot; at the next node, seeing the knot the driver exits so that the payoff realized is4. Note that the path of play induced by this strategy can not be replicated using a behavioral strategy:the handkerchief has allowed the driver to avoid ever reaching the last node with payoff 1. Note also, that2 > 4

3 , the payoff from the best behavioral strategy. The handkerchief has served as a coordination devicebetween the forgetful selves in the different nodes and has achieved a higher payoff than the best behavioralstrategy!Question to ponder: what is ‘strange’ in this solution ?

Trivia: “Alice’s adventures in Algebra: Wonderland solved”, Bayley, M. in New Scientist, 2009 containsmore about the mathematics which inspired Lewis Carroll’s book.

9

Economics 2010a . Section 2 : Nash Equilibrium and Its Properties 10/29/2018∣∣∣∣ (1) Strategies in normal form games; (2) Nash equilibrium and some properties; (3) Solving for NE;∣∣∣∣

TF: Jetlir Duraj ([email protected])

1 Strategies in Normal Form Games

1.1 Recurring notations. The following notations are common in game theory but usually go unexplained.If X1, X2, ..., XN is a sequence of sets with typical elements x1 ∈ X1, x2 ∈ X2, ..., then:

• X−i means ×1≤k≤N,k 6=iXk

• X is sometimes understood to mean ×Nk=1Xk.

• (xi) refers to a vector8 (x1, x2, ..., xN ). So (xi) is an element in ×Nk=1Xk. The parentheses are used todistinguish it from xi, which is an element of Xi.

• x−i is an element in X−i, i.e. in ×1≤k≤N,k 6=iXk. Confusingly, usually no parentheses are used aroundx−i.

To see an example of these notations, suppose we are studying a three player game

G = 〈1, 2, 3, (S1, S2, S3), (u1, u2, u3)〉

Then “s−2” usually refers to a vector containing strategies from P1 and P3, but not P2. It is an element ofS1 × S3, also written as S−2.1.2 Mixed strategies in normal form games. A player who uses a mixed strategy in a game intentionallyintroduces randomness into her play. Instead of picking a deterministic action as in a pure strategy, amixed strategy user tosses a coin to determine what action to play. Game theorists are interested in mixedstrategies for at least two reasons: (i) mixed strategies correspond to how humans play certain games,such as rock-paper-scissors; (ii) the space of mixed strategies represents a “convexification” of the actionset Si and convexity is required for many existence results.

Definition 15. Suppose G = 〈N , (Sk)k∈N , (uk)k∈N 〉 is a normal form game where each Sk is finite.9 Thena mixed strategy σi is a member of ∆(Si).

Sometimes the mixed strategy putting probability p1 on action s(1)1 and probability 1− p1 on action s(2)

1 iswritten as p1s

(1)1 ⊕ (1− p1)s(2)

1 . The “⊕” notation (in lieu of “+”) is especially useful when s(1)1 , s

(2)1 are real

numbers, as to avoid confusing the mixed strategy with an arithmetic expression to be simplified.Two remarks:

• When two or more players play mixed strategies, their randomizations are assumed to be independent.

• Technically, pure strategies also count as mixed strategies – they are simply degenerate distri-butions on the action set. The term “strictly mixed” is usually used for a mixed strategy that putsstrictly positive probability on every action.

When a profile of mixed strategies (σk)Nk=1 is played, the assumption on independent mixing, together withprevious week’s discussion on payoff matrix entries as Bernoulli utilities in a vNM representation, imply thatplayer i gets utility: ∑

(s′k)∈×kSk

ui(s′

1, ..., s′

N ) · σ1(s′1) · ... · σN (s′N )

We will abuse notation and write ui(σi, σ−i) for this utility, extending the domain of ui into mixed strategies.8Sometimes also called a “profile”.9We can also define mixed strategies when the set of actions Sk is infinite. However, we would need to first equip Sk with

sigma-algebra, then define the mixed strategy as a probability measure on this sigma-algebra.

10

1.3 What does it mean to “solve” a game? A detour into combinatorial game theory. Why are economistsinterested in Nash equilibrium, or solution concepts in general? As a slight aside, you may want to knowthat there actually exist two areas of research that go by the name of “game theory”. The full namesof these two areas are “combinatorial game theory” and “equilibrium game theory”. Despite thesimilarity in name, these two versions of game theory have quite different research agendas. The mostsalient difference is that combinatorial game theory studies well-known board games like chess where thereexists (theoretically) a “winning strategy” for one player. Combinatorial game theorists aim to find thesewinning strategies, thereby ultimately solving the game. On the other hand, no “winning strategies” (usuallycalled “dominant strategies” in our lingo) exist for most games studied by equilibrium game theorists.10

In the Battle of the Sexes, for example, due to the simultaneous move condition, there is no one strategythat is optimal for P1 regardless of how P2 plays, in contrast to the existence of such optimal strategies in,say, tic-tac-toe.If a game has a dominant strategy for one of the players, then it is straight-forward to predict its outcomeunder optimal play. The player with the dominant strategy will employ this strategy and the other playerwill do the best they can to minimize their losses. However, predicting outcome in a game without dominantstrategies requires the analyst to make assumptions. These assumptions are usually called equilibrium as-sumptions and give “equilibrium game theory” its name. One of the most common equilibrium assumptionsin normal form games with complete information is the Nash equilibrium, which we now study.

2 Nash Equilibrium

2.1 Defining Nash equilibrium. A Nash equilibrium11 is a strategy profile where no player can improve uponher own payoff through a unilateral deviation, taking as given the actions of others. This leads to the usualdefinition of pure and mixed Nash equilibria.

Definition 16. In a normal form game G = 〈N , (Sk)k∈N , (uk)k∈N 〉, a Nash equilibrium in pure strate-gies is a pure strategy profile (s∗k)k∈N such that for every player i, ui(s∗i , s∗−i) ≥ ui(s′i, s∗−i) for all s′i ∈ Si.

Definition 17. In a normal form game G = 〈N , (Sk)k∈N , (uk)k∈N 〉, a Nash equilibrium in mixedstrategies is a mixed strategy profile (σ∗k)k∈N such that for every player i, ui(σ∗i , σ∗−i) ≥ ui(s′i, σ∗−i) for alls′i ∈ Si.

In the definition of a mixed Nash equilibrium, we required no profitable unilateral deviation to any purestrategy, s′i. It would be equivalent to require no profitable unilateral deviation to any mixed strategy, dueto the following fact.

Fact 18. For any fixed σ−i, the map σi 7→ ui(σi, σ−i) is affine, in the sense thatui(σi, σ−i) =

∑si∈Si σi(si) · ui(si, σ−i).

That is, the payoff to playing σi against opponents’ mixed strategy profile σ−i is some weighted average ofthe |Si| numbers (ui(si, σ−i))si∈Si , where the weights are given by the probabilities that σi assigns to thesedifferent actions. So, if there is some profitable mixed strategy deviation σ′i from a strategy profile (σ∗i , σ∗−i),then it must be the case that for at least one s′i ∈ Si with σ′i(s′i) > 0, we have ui(s′i, σ∗−i) > ui(σ∗i , σ∗−i).

Example 19. Consider the game of assurance,

L R

T 1,1 0,0B 0,0 2,2

We readily verify that both (T, L) and (B,R) are pure strategy Nash equilibria. Note one of these two NEsPareto dominates the other. In general, NEs need not be Pareto efficient. This is because the definitionof NE only accounts for the absence of profitable unilateral deviations. Indeed, starting from the strategyprofile (T, L), if P1 and P2 can contract on simultaneously changing their strategies, then they would bothbe better off. However, these sorts of simultaneous deviations by a “coalition” are not allowed.

10The one-shot prisoner’s dilemma is an exception here.11John Nash called this equilibrium concept “equilibrium point” but later researchers referred to it as “Nash equilibrium”.

11

But wait, there’s more! Suppose P1 plays 23T ⊕

13B. Suppose P2 plays 2

3L⊕13R. This strategy profile is

also a mixed NE. The reasoning is surprisingly simple. When P1 is playing 23T ⊕

13B, P2 gets an expected

payoff of 23 from playing L and an expected payoff of 2

3 from playing R. Therefore, P2 has no profitableunilateral deviation because every strategy he could play, pure or mixed, would give the same payoff of 2

3 .Similarly, P2’s mixed strategy 2

3L ⊕13R means P1 gets an expected payoff of 2

3 whether she plays T or B,so P1 does not have a profitable deviation either.

2.2 Nash equilibrium as a fixed-point of the best response correspondence. Nash equilibrium embodies theidea of stability. To make this point clear, it is useful to introduce an equivalent view of the Nash equilibriumthrough the lens of best response correspondence.

Definition 20. The individual pure best response correspondence for player i is BRi : S−i ⇒ Si12

whereBRi(s−i) := arg max

si∈Siui(si, s−i).

The pure best response correspondence involves putting the N pure best response correspondencesinto a vector: BR : S ⇒ S where BR(s) := (BR1(s−1) ... BRN (s−N )).Analogously, the individual mixed best response correspondence for player i is BRi :

∏k 6=i ∆(Sk)⇒

∆(Si) whereBRi(σ−i) := arg max

σi∈∆(Si)ui(σi, σ−i).

The mixed best response correspondence involves putting the N mixed best response correspondencesinto a vector: BR :

∏i ∆(Si)⇒

∏i ∆(Si) where BR(σ) := (BR1(σ−1) ... BRN (σ−N )).

To interpret, the individual best response correspondences return the argmax of each player’s utility functionwhen opponents plays some known strategy profile. Depending on others’ strategies, the player may havemultiple maximizers, all yielding the same utility. As a result, we must allow the best responses to becorrespondences rather than functions. Then, it is easy to see that:

Proposition 21. A pure strategy profile is a pure NE iff it is a fixed point of BR. A mixed strategy profileis a mixed NE iff it is a fixed point of BR.

Fixed points of the best response correspondences reflect stability of NE strategy profiles, in the sense thateven if player i knew what others were going to play, she still would not find it beneficial to change her actions.This rules out cases where a player plays in a certain way only because she held the wrong expectationsabout other players’ strategies. We might expect such outcomes to arise initially when inexperienced playersparticipate in the game, but we would also expect such outcomes to vanish as players learn to adjust theirstrategies to maximize their payoffs over time. That is to say, we expect non-NE strategy profiles to beunstable.

2.3. Three properties of Nash equilibria.Property 1: the indifference condition in mixed NEs.In Example 19, we saw that each action that player i plays with strictly positive probability yields the sameexpected payoff against the mixed strategy profile of the opponent. Turns out this is a general phenomenon.

Proposition 22. Suppose (σ∗i ) is a mixed Nash equilibrium. Then for any si ∈ Si such that σ∗i (si) > 0, wehave ui(si, σ∗−i) = ui(σ∗i , σ∗−i).

Proof. Suppose we may find si ∈ Si so that σ∗i (si) > 0 but ui(si, σ∗−i) 6= ui(σ∗i , σ∗−i). In the event thatui(si, σ∗−i) > ui(σ∗i , σ∗−i), we contradict the optimality of σ∗i in the maximization problem arg max ui(σi, σ∗−i),for we should have just picked σi = si, the degenerate distribution on pure strategy si. In the event thatui(si, σ∗−i) < ui(σ∗i , σ∗−i), we enumerate Si = s(1)

i , ..., s(r)i and use the Fact 18 to expand:

ui(σ∗i , σ∗−i) =r∑

k=1σ∗i (s(k)

i ) · ui(s(k)i , σ∗−i)

The term ui(si, σ∗−i) appears in the summation on the right with a strictly positive weight, so if ui(si, σ∗−i) <ui(σ∗i , σ∗−i) then there must exist another s′i ∈ Si such that ui(s′i, σ∗−i) > ui(σ∗i , σ∗−i). But now we have againcontradicted the fact that σ∗i is a best mixed response to σ∗−i.

12The notation f : A⇒ B is equivalent to f : A→ 2B .

12

Property 2: Nash payoffs are greater or equal than the maxmin values of each player.

Definition 23. In a normal form game the maxmin value of a player is defined by

maxσi

minσ−i

ui(σi, σ−i),

while the minmax value of a player is defined by

minσ−i

maxσi

ui(σi, σ−i).

The interpretation of these two values is straightforward:- the maxmin of i is the smallest utility value agent i can ensure if she best responds to the strategies of theother players, while- the minmax of i is the lowest utility the other players can push player i down to, if she best responds totheir strategy.We showed in the lecture, that for two player, zero-sum (or actually constant-sum) games, these two valuesare identical for both players. It turns out that in any game of finite players, any Nash equilibrium payoffof each player is at least as large as his minmax or maxmin value.

Proposition 24. In each normal form game G = (N , (Si)i∈N , (ui)i∈N ) with a finite set of players, for everyNash equilibrium σ∗ = (σ∗1 , . . . , σ∗n) and for every player i it holds

ui(σ∗) ≥ maxσi

minσ−i

ui(σi, σ−i), ui(σ∗) ≥ minσ−i

maxσi

ui(σi, σ−i).

Proof. Note that σ∗ being a Nash equilibrium can be written as

ui(σ∗i , σ∗−i) ≥ ui(si, σ∗−i) (2)

for all si ∈ Si and all players i ∈ N . Due to the properties of Expected Utility this is equivalent to thestatement

ui(σ∗i , σ∗−i) ≥ ui(pi, σ∗−i) (3)

for all pi ∈ ∆(Si): One direction is clear, since pure strategies are a particular case of mixed strategies; theother direction is proven by taking mixtures and noticing that the LHS of both (2) and (3) doesn’t dependon resp. si and pi.(1) Note then, that

ui(σ∗) = maxσi

ui(σi, σ∗−i) ≥ minσ−i

maxσi

ui(σi, σ−i),

where the first equality comes from the definition of Nash equilibrium and the second from the definition ofmin of a function.(2) Furthermore,

ui(σ∗) = maxσi

ui(σi, σ∗−i) ≥ maxσi

minσ−i

ui(σi, σ−i),

because for each fixed σi we have that ui(σi, σ∗−i) ≥ minσ−i ui(σi, σ−i), i.e. we have two functions of σi,where the first always dominates the second at each σi. This implies that the maximum of the first isgreater-equal to the maximum of the second function.These two arguments complete the proof.

Property 3: Never play strictly dominated strategies.

Definition 25. In a normal form game G = (N , (Si)i∈N , (ui)i∈N ) call a pure strategy si ∈ Si of player istrictly dominated if there exists a mixed strategy σi ∈ ∆(Si) so that for every σ−i we have

ui(σi, σ−i) > ui(si, σ−i).

Do not confuse this definition with the one from Nash equilibrium: here, the inequality is strict and shouldhold for every possible play of the other players. It turns out, that recognizing strictly dominated strategiescan help analyze the Nash equilibria of a game, since no player would ever employ them in a Nash equilibriumstrategy.

13

Proposition 26. If σ∗ is a Nash equilibrium of the normal form game G = (N , (Si)i∈N , (ui)i∈N ), then noplayer puts positive probability on a strictly dominated strategy. In other words:

si strictly dominated for i and σ∗ is Nash =⇒ σ∗i (si) = 0.

Proof. Let σ∗ be Nash and assume, that si is strictly dominated by σi for i. This means in particular, that

ui(σi, σ∗−i) > ui(si, σ∗−i).

The definition of Nash equilibrium implies then, that

ui(σ∗i , σ∗−i) > ui(si, σ∗−i),

while the indifference principle implies that if σ∗i (s′i) > 0, then ui(s′i, σ∗−i) = ui(σ∗) > ui(si, σ∗−i). If it were,that σ∗(si) > 0, this would mean that there is some s′i with σ∗i (s′i) > 0 and ui(s′i, σ∗−i) = ui(σ∗) > ui(si, σ∗−i)whose probability σ∗i (s′i) could be increased and which would yield a higher payoff for player i. This wouldbe a contradiction to Nash equilibrium definition! Thus, it has to be σ∗i (si) = 0.

2.4 Mathematical properties of the set of Nash equilibria. The set NE of Nash equilibria of a finite normalform game G is a subset of the product space of strategy profiles ∆(S1)×∆(S2)× · · · ×∆(Sn), where n isthe number of the players. This set is compact, because it is a bounded and closed set of an euclidean space:

• If |S| =∏ni=1 |Si| is the cardinality of the set of pure strategies of the game, then ∆(S1) × ∆(S2) ×

· · · ×∆(Sn) can be mapped uniquely to a bounded set of R|S| and thus is bounded.

• Let σm be a sequence of Nash equilibria of the game such that it converges to a strategy profile σ, i.e.σm→σ as m→∞. We then have

ui(σm,i, σm,−i) ≥ ui(si, σm,−i)

for all players i, strategies si ∈ Si. But the payoff functions are continuous in their arguments, so thatpassing to the limit m→∞ we have

ui(σi, σ−i) ≥ ui(si, σ−i)

for all players i, strategies si ∈ Si. But this is just the definition of σ being a Nash equilibrium profile!This argument shows that the set NE of equilibria is closed.

The set NE of Nash equilibria is in general not convex. Consider as a counterexampe the Battle of the Sexesgame:

Opera Football

Opera 3,2 0,0Football 0,0 2,3

You can check that there are three Nash equilibria for this game: two in pure strategies (Opera,Opera),(Football, Football) and one in mixed strategies ( 3

5Opera ⊕25Football,

25Opera ⊕

35Football).

13 Take themixture with probability 1

2 of the two pure Nash equilibria, i.e. consider ( 12Opera ⊕

12Football,

12Opera ⊕1

2Football). But note that player 1 gets a utility of 32 by playing Opera and a utility of 1 by playing

Football and thus would deviate to playing Opera with probability one. This means, that the set NE ofNash equilibria doesn’t contain ( 1

2Opera⊕12Football,

12Opera⊕

12Football) and thus it is not convex.

Question: Can you think of a (trivial) case where the set of Nash equilibria is indeed convex ?Hint: Think of Prisoner’s Dilemma.

Example 27. Consider the three player game in which every player has two pure strategies; Player 1 choosesa row (T or B), Player 2 chooses a column (L or R) and player 3 chooses the matrix (W or E). The followingmatrices show only the payoff function of player 1.

13Please, please make sure you can indeed find these Nash equilibria on your own – if the concept of Nash equilibria iscompletely new, this is good practice! See also below if you have difficulties characterizing the set of Nash equilibria here.

14

L R

T 0 1B 1 1

matrix W

L R

T 1 1B 1 0

matrix E

What is the maxmin and the minmax value of player 1 in mixed strategies ?

Solution. Assume P1 uses x⊕ (1− x), P2 uses y ⊕ (1− y) and P3 z ⊕ (1− z). Then P1s payoff is

U1(x, y, z) = 1− xyz − (1− x)(1− y)(1− z).

and maxmin-ing this expression leads to

v1 = maxx

miny,z

U1(x, y, z) = 12 .

To see this, note that U1(x, 1, 1) = x ≤ 12 for every x ≤ 1

2 . Also, U1(x, 0, 0) = 1− x ≤ 12 for every x ≥ 1

2 . Itfollows miny,z U1(x, y, z) ≤ 1

2 . But U1( 12 , y, z) ≥

12 for each y.

Next we calculate the minmax of P1.

v1 = miny,z

maxx

U1(x, y, z)

= miny,z

maxx

(1− xyz − (1− x)(1− y)(1− z))

= miny,z

maxx

(1− (1− y)(1− z) + x(1− y − z))

One can see that the (inner) maximum is achieved x = 1 if 1− y − z ≥ 0 and at the extreme point x = 0 if1− y − z ≤ 0. It follows

maxx

(1− (1− y)(1− z) + x(1− y − z)) =

1− (1− y)(1− z), y + z ≥ 11− yz, y + z < 1.

By going case-by-case and using symmetry we see that the (outer) optimum is attained at y = z = 12 . It

followsv1 = 3

4 .

Note that in this example we havev1 = 1

2 <34 = v1.

2.5 Symmetric Games. A game in normal form G = (N , (Si)i∈N , (ui)i∈N ) is called a symmetric game if

• Each player has the same set of strategies: Si = S for all i ∈ N .

• The payoff functions satisfy for each pair of players i, j with i < j

ui(s1, s2, . . . , sn) = uj(s1, . . . , si−1, sj , si+1, . . . , sj−1, si, sj+1, . . . , sn).

Examples of symmetric games are Bertrand duopoly or Cournot duopoly with identical costs, Prisoner’sDilemma, etc. An example of a non-symmetric game is the Battle of the sexes.One can adapt the proof of Nash’s existence Theorem to show that every finite symmetric game has asymmetric Nash equilibrium in mixed strategies: a Nash equilibrium σ = (σi)i∈N satisfying σi = σjfor each i, j ∈ N .This fact can come in handy when solving games. Moreover, the assumption of symmetric play is naturalgiven that symmetric games are so that the players are interchangeable, i.e. their exact identity doesn’tmatter for the game play.

15

3 Solving for Nash Equilibria

The following steps may be helpful in solving for NEs of two-player games.

1. Use iterated elimination of strictly dominated strategies to simplify the problem.14

2. Find all the pure strategy Nash equilibria by considering all cells in the payoff matrix.

3. Look for a mixed Nash equilibrium where one player is playing a pure strategy while the other isstrictly mixing.

4. Look for a mixed Nash equilibrium where both players are strictly mixing.

Example 28. (December 2013 Final Exam) Find all NEs, pure and mixed, in the following payoff matrix.

L R Y

T 2, 2 −1, 2 0, 0B −1,−1 0, 1 1,−2X 0, 0 −2, 1 0, 2

Solution:Step 1: Strategy X for P1 is strictly dominated by 1

2T ⊕12B. Indeed, u1(X,L) = 0 < 0.5 = u1( 1

2T ⊕12B,L),

u1(X,R) = −2 < −0.5 = u1( 12T⊕

12B,R), and u1(X,Y ) = 0 < 0.5 = u1( 1

2T⊕12B, Y ). But having eliminated

X for P1, strategy Y for P2 is strictly dominated by R: u2(T, Y ) = 0 < 2 = u2(T,R), u2(B, Y ) = −2 < 1 =u2(B,R). Hence we can restrict attention to the smaller, 2x2 game in the upper left corner.Step 2: (T, L) is a pure Nash equilibrium as no player has a profitable unilateral deviation. (The deviationL → R does not strictly improve the payoff of P2, so it doesn’t break the equilibrium.) At (T,R), P1deviates T → B, so it is not a pure strategy Nash equilibrium. At (B,L), P2 deviates L → R. At (B,R),no player has a profitable unilateral deviation, so it is a pure strategy Nash equilibrium. In summary, thegame has two pure strategy Nash equilibria: (T, L) and (B,R).Step 3: Now we look for mixed Nash equilibria where one player is using a pure strategy while the other isusing a strictly mixed strategy. As discussed before, if a player strictly mixes between two pure strategies,then they must be getting the same payoff from playing either of these two pure strategies.Using this indifference condition, we quickly realize it cannot be the case that P2 is playing a purestrategy while P1 strictly mixes. Indeed, if P2 plays L then u1(T, L) > u1(B,L). If P2 plays R thenu1(B,R) > u1(T,R).Similarly, if P1 is playing B, then the indifference condition cannot be sustained for P2 since u2(R,B) >u2(L,B).Now suppose P1 plays T . Then u2(T, L) = u2(T,R). This indifference condition ensures that any strictlymixed strategy of P2 pL⊕(1−p)R for p ∈ (0, 1) is a mixed best response to P1’s strategy. However, to ensurethis is a mixed Nash equilibrium, we must also make check P1 does not have any profitable unilateraldeviation. This requires:

u1(T, pL⊕ (1− p)R) ≥ u1(B, pL⊕ (1− p)R)

that is to say,

2p+ (−1) · (1− p) ≥ (−1) · p+ 0 · (1− p)4p ≥ 1

p ≥ 14

14Next section will focus more on IESDS and its properties. Regarding the relation of never best response property to theproperty of being strictly dominated for strategies: these two concepts are equivalent for two-player games. For games withmore than two players, they are in general not equivalent under the assumption that opponents of a player cannot correlatetheir strategies.

16

Therefore, (T, pL⊕ (1− p)R) is a mixed Nash equilibrium where P2 strictly mixes when p ∈ [ 14 , 1).

Step 4: There are no mixed Nash equilibria where both players are strictly mixing. To see this, notice ifσ∗1(B) > 0, then

u2(σ∗1 , L) = 2 · (1− σ∗1(B)) + (−1) · (σ∗1(B)) < 2 · (1− σ∗1(B)) + (1) · (σ∗1(B)) = u2(σ∗1 , R)

So it cannot be the case that P2 is also strictly mixing, since P2 is not indifferent between L and R.In total, the game has two pure Nash equilibria, (T, L) and (B,R), as well as infinitely many mixed Nashequilibria, (T, pL⊕ (1− p)R) for p ∈ [ 1

4 , 1).

Sometimes, iterated elimination of strictly dominated strategy simplifies the game so much that the solutionis immediate after Step 1. The following example illustrates.

Example 29. (Guess two-thirds the average, also sometimes called the beauty contest game15) Considera game of 2 players G(1) where S1 = S2 = [0, 100], ui(si, s−i) = −

(si − 2

3 ·si+s−i

2

)2. That is, each player

wants to play an action as close to two-thirds the average of the two actions as possible. We claim that foreach player i, every action in (50, 100] is strictly dominated by the action 50. To see this, for any opponentaction s−i ∈ [0, 100], we have 2

3 ·50+s−i

2 ≤ 50, so the guess 50 is already too high:

50− 23 ·

50 + s−i2 ≥ 0

At the same time, ddsi

[si − 2

3 ·si+s−i

2

]= 2

3 > 0. Hence we conclude playing any si > 50 exacerbates theerror relative to playing 50,

si −23 ·

si + s−i2 > 50− 2

3 ·50 + s−i

2 ≥ 0

so then −(si − 2

3 ·si+s−i

2

)2< −

(50− 2

3 ·50+s−i

2

)2for all si ∈ (50, 100] and we have the claimed strict

dominance.This means we may delete the set of actions (50, 100] from each Si to arrive at a new game G(2) whereeach player is restricted to using only [0, 50]. The game G(2) will have the same set of NEs as the originalgame. But the same logic may be applied again to show that in G(2), for each player any action in (25, 50]is strictly dominated by the action 25. We may continue in this way iteratively to arrive at a sequenceof games (G(k))k≥1, so that in the game G(k+1), player i’s action set is

[0,( 1

2)k · 100

]. All of the games

G(1),G(2),G(3), ... have the same NEs. This means any NE of G(1) must involve each player playing an actionin

∞⋂k=1

[0,(

12

)k· 100

]= 0

Hence, (0, 0) is the unique NE.

Example 30. Consider the following three player game, where the first player chooses rows, the secondcolumns and the third chooses the matrix.

A L R

T 1,1,1 0,1,3B 1,3,0 1,0,1

C L R

T 3,0,1 1,1,0B 0,1,1 0,0,0

We claim, that there is only one mixed Nash equilibrium and it is in pure strategies: (T, L,A).Solution:Step 1: There is only one Nash equilibrium in pure strategies. Note, that domination argumentsdon’t help here, because no pure strategy of any player is dominated. It is easy to see, that (T, L,A) is a

15The name “beauty contest game” comes from an old newspaper game where readers pick the 6 faces they consider themost beautiful from a set of 100 portraits. The readers who pick the six most popular choices won a prize.

17

pure Nash equilibrium: if players 1, 2 play (T, L), then player 3 is indifferent and so might as well choose A.Note also, that (T, L) is a Nash equilibrium of the two-player game created by taking matrix A and deletingall payoffs of player 3. In this restricted game, there is also the pure Nash where players 1, 2 play (B,L),but then player 3 would like to switch matrix. If we restrict matrix B to the payoffs of players 1, 2 only, wesee that there is only one pure Nash in the two-player induced game: (T,R). but then player 3 would liketo switch matrix to A. In all, there is only one pure Nash and it is (T, L,A).Step 2: There are no Nash equilibria, where two players play pure and the remaining playercompletely mixes.- Assume there is a Nash equilibrium where players 1, 2 play pure and player 3 completely mixes. But wesaw that in A players 1, 2 would then play either (T,L) or (B,L). In the second case, player 3 would liketo switch matrix, so it must be (T, L). But then player 2 would better switch to R, since when matrixA is played he gets 1 in any case and when matrix C is played with positive probability, he gets 1 > 0.Contradiction.- Assume there is a Nash equilibrium where players 1,3 play pure and player 2 completely mixes. Assumefirst, that player 3 plays A. Then any completely mixed strategy of player 2 will induce player 1 to playB, because then she can make sure she gets 1 instead than less than 1. But if player 1 plays B, player 2would want to play L with probability 1, which contradicts the fact that he is completely mixing. Assumethen, that player 3 is playing C. Here player 1 would want to play T with probability 1, because B gives herstrictly less utility, no matter what the strategy of player 2 is. But player 1 playing T would make player 2play L with probability 1, contradicting the hypothesis that he completely mixes.- Assume there is a Nash equilibrium where players 2,3 play pure and player 1 completely mixes. Assumefirst, that player 3 plays A. We know from the induced game between players 1, 2 that then player 1 wouldwant to completely mix only if player 2 is playing L, because otherwise player 1 could increase payoff byplaying B. But then player 3 would want to switch to C to ensure a payoff of 1 contradicting the assumptionthat she plays A. Assume then, that player 3 plays C. Here player 1 would never completely mix, becauseno matter the strategy of player 2 she gets strictly more by playing T rather than B. This contradicts theassumption that player 1 completely mixes and concludes this case.Step 3: There are no Nash equilibria, where one player plays pure and the remaining playerscompletely mix.- Assume it is player 1 who plays pure. Assume first, she plays T . Let p, q ∈ (0, 1) the probabilities withwhich, resp. player 2 plays L and player 3 plays A in equilibrium. Player 3 would choose q ∈ (0, 1) only ifshe is indifferent between the two matrices, i.e. p has to fulfill

p+ 3(1− p) = p+ 0(1− p).

But this implies p = 1, a contradiction. Assume then, that player 1 instead plays B. Let p, q ∈ (0, 1) theprobabilities with which, resp. player 2 plays L and player 3 plays A in equilibrium. Player 2 would wantto completely mix only if he is indifferent between L,R. It follows, that q has to fulfill

3q + 1(1− q) = 0q + 0(1− q),

which is impossible.- Assume now there is a Nash equilibrium where player 2 is the only player who plays pure. Assume heis playing L. Player 1 would want to completely mix only if player 3 was playing A; otherwise, she wouldchoose T with probability 1, which is a contradiction. Assume then, that player 2 is playing R. But thenplayer 3 would play A with probability one, because no matter what the play of player 1 is, she is better offwith A.- Assume finally, for this step, that it is player 3 who plays pure and the other two players completely mix.We can see that it can’t be the case that player 3 plays C because then, player 1 would choose T withprobability 1. So it must be that player 3 plays A. But here again, we know that player 1 would want tocompletely mix if and only if player 2 is playing L, because otherwise by choosing B she can ensure a payoffof 1. This contradicts the assumption that player 2 is completely mixing.Step 4: There are no Nash equilibria, where all players completely mix.16

Assume there is a completely mixed Nash equilibrium where player 1 plays T with probability p, player 2plays L with probability q and player 3 plays A with probability r. Then we must have that players are allindifferent between their resp. pure strategies. For player 1 this means that r, q must fulfill (besides beingin (0, 1))

qr + 0 + 3q(1− r) + (1− q)(1− r) = r + 0.16There are several ways to do this step, this is just one of them.

18

Here, the LHS is player 1 payoff from playing T and the RHS is her payoff from playing B. Simple algebrashows that this indifference condition can be written as

3q(1− r) = (1− q)(2r − 1). (4)

Note that this implies in particular, that r ∈ ( 12 , 1). Similar algebra for players 2 and 3 shows that their

indifference conditions can be written as

3r(1− p) = (1− r)(2p− 1) (5)

for player 2 and3p(1− q) = (1− p)(2q − 1) (6)

for player 3.17 Now multiply equations (4),(5) and (6) side by side to arrive (using that p, q, r ∈ ( 12 , 1)) at

27pqr = (2p− 1)(2q − 1)(2r − 1).

The RHS of this equation is smaller than 1, while the LHS is greater than 278 > 2, so we have a contradiction!

In all, there can’t be a completely mixed Nash equilibrium.

Example 31. Consider the following normal form game and show that there is a unique Nash equilibriumin mixed strategies.

L R

Rr 0,0 1,-1Rf 0.5,-0.5 0,0Fr -0.5,0.5 1,-1Ff 0,0 0,0

Solution: Step 1: Ff is dominated. For this, compare its payoff to any strict mixture of Rr and Rf .IESDS stops here since no more strategies can be deleted for any of the players.Step 2: There are no pure Nash equilibria. This is easily seen by checking the remaining six sells ofthe matrix, once Ff is deleted. By Nash’s existence theorem there is at least one mixed Nash equilibrium.Step 3: There is no Nash equilibrium where P2 doesn’t strictly randomize. Assume that P2 playsL with probability one. Then P1 would best respond by playing Rf with probability 1. But this means we’dhave a pure NE which contradicts Step 2. Assume that P2 plays R with probability 1. Then P1 is indifferentbetween Rr and Fr and thus plays a mixture between the two. But this profile of strategies gives -1 to P2,which he can improve upon by deviating to L (it would give him a positive payoff).Step 4: There is no Nash equilibrium where P1 puts positive probability on Fr. To see this, itsuffices to note that Fr is weakly dominated by Rr. If P2 strictly mixes in a NE (which we established inStep 3), it follows that Rr always gives a better payoff than playing Fr with positive probability.Step 5: Finding the mixed Nash. We know now that any mixed Nash equilibrium has P2 mix betweenL and R. For this, P1 would have to strictly mix between Rr and Rf . This happens only if she is indifferentbetween the two strategies in equilibrium. Let p be the probability that P2 chooses L. The payoff of P1 fromplaying Rr is 1− p, while that of playing Rf is 0.5p. Equalizing these yields p = 2

3 .Let q be the probability that P1 chooses Rr. The payoff of P2 from playing L is 0.5(1− q), while the payofffrom playing R is q. Equalizing these and solving for q yields q = 1

3 .We have showed that any Nash equilibrium has strict mixing between Rr and Rf for P1 and L and R forP2 and we have found unique mixing probabilities by employing the indifference conditions needed for Nashequilibrium. It follows that the unique Nash equilibrium is

(13 ⊕

23 ⊕ 0⊕ 0; 2

3 ⊕13).

17You can also use the symmetry of the game to write down these conditions without going through the algebra.

19

Example 32. Consider the following normal form game and find its unique Nash equilibrium.

L C R

T 0, 0 7, 6 6, 7M 6, 7 0, 0 7, 6B 7, 6 6, 7 0, 0

Solution. It is easy to see that no strategy is strictly dominated and that there are no Nash equilibria whereonly one of the players plays a pure strategy. Assume that P2 randomizes between L and C only. Then thebest response of P1 is to play B with probability one. But then P2 would optimally decide to not randomizeand play C with probability 1. A similar argument, using symmetry of the game, shows that there is nomixed Nash equilibrium where at least one of the players mixes between two pure strategies. Thus all Nashequilibria of the game have to be equilibria where both players strictly mix between all their three strategies.Since this is a symmetric game, it has a symmetric Nash equilibrium, which per above involves strict mixingbetween all pure strategies. It is therefore given by(

(13 ⊕

13 ⊕

13); (1

3 ⊕13 ⊕

13)).

It is easy to see that, under the constraint that the opponent mix between all three strategies, only uniformmixing as here can make a player indifferent between all three of her pure strategies. This finishes the proofthat the symmetric mixed Nash is the unique Nash.

Example 33. (from MWG) Consumers are uniformly distributed along a boardwalk that is 1 mile long.Ice-cream prices are regulated, so consumers go to the nearest vendor because they dislike walking (assumethat at the regulated prices all consumers will purchase an ice-cream even if they have to walk a full mile).If more than one vendor is at the same location, they split the business evenly.(a) Consider a game in which two vendors pick their locations simultaneously. Show that there exists aunique pure Nash equilibrium where both vendors locate at the midpoint of the boardwalk.(b) Show that with three vendors no pure Nash equilibrium exists.Solution. (a) Let x1 be the location of vendor 1 and x2 the location of vendor 2. Thus, we can associate astrategy for Player i with xi ∈ [0, 1]. First, let us find out the payoff function for each of the vendors. Sincethe price of ice-cream is regulated (thus fixed), we can identify the profit of each vendor with the number ofcustomers she gets. Suppose that x1 < x2. In this case, all consumers located to the left (below) x1+x2

2 willpurchase from vendor 1, while all customers located to the right of x1+x2

2 will buy ice-cream from vendor 2.Thus

u1(x1, x2) = x1 + x2

2 , u2(x1, x2) = 1− x1 + x2

2 .

We can derive a similar result for x2 < x1:

u1(x1, x2) = 1− x1 + x2

2 , u2(x1, x2) = x1 + x2

2 .

In the case that x1 = x2 the vendors split the business so that u1(x1, x2) = u2(x1, x2) = 12 .

It is straightforward to check that ( 12 ,

12 ) constitutes a NE (just check that no deviation is strictly profitable).

To show uniqueness, suppose first that x1 = x2 <12 . Then any firm can do better by moving by ε > 0 to the

right, since it will sell almost 1− x1 >12 units rather than 1

2 units. Similarly, one shows that there’s no NEwith x1 = x2>

12 . Suppose now that x1 < x2. Then firm 1 can do better by moving to x2 − ε, with ε > 0,

therefore this could not have been a NE. Similarly it can be shown that x1 > x2 does not constitute a NE.(b) Suppose that an equilibrium exists given by (x∗1, x∗2, x∗3). Suppose first that x∗1 = x∗2 = x∗3. Then eachfirm sells 1

3 . But any firm can increase its sales by moving to the right (if x∗1 = x∗2 = x∗3 <12 ) or the left

(if x∗1 = x∗2 = x∗3 ≥ 12 ), a contradiction. Suppose that two firms locate at the same point, say x∗1 = x∗2. If

x∗1 = x∗2 < x∗3 then firm 3 can do better by moving to x∗1 + ε for ε > 0 small. If x∗1 = x∗2 > x∗3 then firm 3can do better by moving to x∗1 − ε for ε > 0 small enough, a contradiction. Finally, suppose that all three 3firms are located at different points. But then the firm that is located the farthest on the right will be able

20

to increase sales by moving to the left by ε > 0, a contradiction. Thus, there exists no pure strategy NE inthis game.

21

Economics 2010a . Section 3 : Misc. Topics 11/7/2016∣∣∣∣ (1) More actions can be worse; (2) Correlated Equilibrium; (3) Rationalizability;∣∣∣∣

TF: Jetlir Duraj ([email protected])

1 More actions can lower equilibrium payoffs

It is well known that a single rational agent with classical preferences cannot be made worse off by enlargingthe set of possible actions she possesses in a decision problem. The following example shows that this is notthe case anymore in strategic situations, even if we keep the assumption of classical preferences.

Example. Recall the Battle of the Sexes game from last section.

Opera Football

Opera 3,2 0,0Football 0,0 2,3

We showed that it has three Nash equilibria and that all of them have strictly positive payoffs for the agents.Now add a third action: stay home and suppose the game matrix changes into

Opera Football Stay Home

Opera 3, 2 0, 0 −1, 4Football 0, 0 2, 3 −1, 4

Stay Home 4,−1 4,−1 0, 0

Note now that the only Nash is for both players to stay home and it has payoff zero for both players. Addingchoices has led to lower utilities in equilibrium.

2 Correlated Equilibrium

Let’s begin with the definition of a correlated equilibrium in a normal form game.

Definition 34. In a normal form game G = 〈N , (Sk)k∈N , (uk)k∈N 〉, a correlated equilibrium (CE)consists of:

• A finite set of signals Ωi for each i ∈ N . Write Ω := ×k∈NΩk.

• A joint distribution p ∈ ∆(Ω), so that the marginal distributions satisfy pi(ωi) > 0 for each ωi ∈ Ωi.18

• A signal-dependent strategy s∗i : Ωi → Si for each i ∈ N

such that for every i ∈ N , ωi ∈ Ωi, si ∈ Si,∑ω−i

p(ω−i|ωi) · ui(s∗i (ωi), s∗−i(ω−i)) ≥∑ω−i

p(ω−i|ωi) · ui(si, s∗−i(ω−i))

A correlated equilibrium envisions the following situation. At the start of the game, an N -dimensionalvector of signals ω realizes according to the distribution p. Player i observes only the i-th dimension of thesignal, ωi, and plays an action s∗i (ωi) as a function of the signal she sees. Whereas a pure Nash equilibriumhas each player playing one action and requires that no player has a profitable unilateral deviation, in a

18This is without loss of generality since any 0 probability signal of player i may be deleted to generate a smaller signalspace.

22

correlated equilibrium each player may take different actions depending on her signal. Correlatedequilibrium requires that no player can strictly improve her expected payoffs after seeing any of her signals.More precisely, seeing the signal ωi leads her to have some belief over the signals that others must haveseen, formalized by the conditional distribution p(·|ωi) ∈ ∆(Ω−i). Since she knows how these opponentsignals translate into opponent actions through s∗−i, she can compute the expected payoffs of taking differentactions after seeing signal ωi. She finds it optimal to play the action s∗i (ωi) instead of deviating to any othersi ∈ Si after seeing signal ωi.Four important remarks about the definition of correlated equilibria.(1) The signal space and its associated joint distribution, (Ω, p), are not part of the game G, but partof the equilibrium. That is, a correlated equilibrium constructs an information structure under which aparticular outcome can arise.(2) There is no institution compelling player i to play the action s∗i (ωi), but i finds it optimal to do soafter seeing the signal ωi. It might be helpful to think of the traffic lights as an analogy for a correlatedequilibrium. The light color that a player sees as she arrives at the intersection is her signal and imaginea world where there is no traffic police or cameras enforcing traffic rules. Each driver would neverthelessstill find it optimal to stop when she sees a red light, because she infers that her seeing the red light signalmust mean the driver on the intersecting street received the green light signal, and further the other driveris playing the strategy of going through the intersection if he sees a green light. Even though the red light(ωi) merely recommends an action (s∗i (ωi)), i finds it optimal to obey this recommendation given howothers are acting on their own signals.(3) A Nash equilibrium is always a correlated equilibrium. Indeed, if the strategies σ∗i of each player fulfillthe requirements of the Nash equilibrium in the normal form game G = 〈N , (Sk)k∈N , (uk)k∈N 〉 constructΩ = ×k∈NSk,Ωi = Si and p ∈ ∆(Ω) by

p(s1, . . . , sn) = σ1(s1) · σ2(s2) · · · · σn(sn).

Finally, define the signal dependent strategies s∗i : Ωi→Si by s∗i (si) = si.It is trivial to see that this gives a correlated equilibrium. In particular, they always exist.(4) The set of correlated equilibria of a finite normal form game is convex.19 To see this intuitively, considera collection ((Ωli)i∈N , pl, (s∗li )i∈N ) for l = 1, . . . , k, all correlated equilibria of the game and consider weightspl ≥ 0, . . . , pk ≥ 0 with

∑l pl = 1. Construct the new correlated equilibrium by first flipping a ’coin’ or

k-faced dice if you will, which falls on l with probability pl and instruct the players to play the l-th correlatedequilibrium if face l arises as outcome. Once they see the instruction of the dice, the players will play thel-th correlated equilibrium. This is true because of it being a correlated equilibrium in the first place! In all,it is not hard to see then, that this two-stage process gives a correlated equilibrium of the game, which is amixture with weights pl, l = 1, . . . , n of the original correlated equilibria.

Example 35. Consider the usual coordination game, given by the payoff matrix:

L R

L 1,1 0,0R 0,0 1,1

The following is a correlated equilibrium: Ω1 = Ω2 = l, r, p(l, l) = 0.3, p(l, r) = 0.1, p(r, l) = 0.2,p(r, r) = 0.4, s∗i (l) = L and s∗i (r) = R for each i ∈ 1, 2. We can check that no player has a profitabledeviation after any signal. For instance, after P1 sees the signal l, he knows that p(ω2 = l|ω1 = l) = 3

4 ,p(ω2 = r|ω1 = l) = 1

4 . Since s∗2(l) = L, s∗2(r) = R, the expected payoff for P1 to playing L is 3

4 · 1 + 14 · 0 = 3

4 ,whereas the expected payoff to playing R is 3

4 ·0 + 14 ·1 = 1

4 . As such, P1 does not want to deviate to playingR after seeing signal l. Similar arguments can be made for P1 after signal r, P2 after signal l, and P2 aftersignal r.Here’s another correlated equilibrium: Ω1 = Ω2 = l, r, p(l, l) = 0.8, p(r, r) = 0.2, p(l, r) = 0, p(r, l) = 0,s∗i (l) = L and s∗i (r) = R for each i ∈ 1, 2. Note that the signal structures of different correlated equilibrianeed not be the same.In this second equilibrium, the signal structure is effectively a coordination device that picks the (L,L) Nash

19Recall, that this wasn’t true for Nash equilibria.

23

equilibrium 80% of the time, the (R,R) Nash equilibrium 20% of the time. Since each equilibrium chosenis, being Nash, self-enforcing, it is as if the agents are using a randomization device which is public, in thesense, that every player sees the signals of all players. This method to ‘correlate’ among Nash equilibria canbe made more general.

Example 36. (Public randomization device) Fix any normal form game G and fix K of its pure Nashequilibria, E1, ..., EK , where each Ek abbreviates some pure strategy profile (s(k)

1 , ..., s(k)N ). Then, for any

K probabilities p1, ..., pK with pk > 0,∑Kk=1 pk = 1, consider the signal structure with Ωi = 1, ...,K,

p(k, ..., k) = pk for each 1 ≤ k ≤ K, and p(ω) = 0 for any ω where not all N dimensions match. Consider thestrategies s∗i (k) = s

(k)i for each i ∈ N , 1 ≤ k ≤ K. Then (Ω, p, s∗) is a correlated equilibrium. Indeed, after

seeing the signal k, each player i knows that others must be playing their part of the k-th Nash equilibrium,(s(k)

1 , ..., s(k)N ). As such, her best response must be s(k)

i , so s∗i (k) = s(k)i is optimal.

Example 37. (Coordination game with an eavesdropper) Three players Alice (P1), Bob (P2), and Eve (P3,the “eavesdropper”) play a zero-sum game. Alice and Bob win only if they show up at the same location,and furthermore Eve is not there to spy on their conversation. The payoffs are given below. Alice chooses arow, Bob chooses a column, and Eve chooses a matrix.

L R

L -1,-1,2 -1,-1,2R -1,-1,2 1,1,-2

matrix L

L R

L 1,1,-2 -1,-1,2R -1,-1,2 -1,-1,2

matrix R

The following is a correlated equilibrium. Ω1 = Ω2 = Ω3 = l, r, p(l, l, l) = 0.25, p(l, l, r) = 0.25, p(r, r, l) =0.25, p(r, r, r) = 0.25, s∗i (l) = L and s∗i (r) = R for all i ∈ 1, 2, 3. The information structure models asituation where Alice and Bob jointly observe some randomization device unseen by Eve20 and use it tocoordinate on either both playing L or both playing R. Eve’s signals are uninformative of Alice and Bob’sactions. Indeed, after seeing either ω3 = l or ω3 = r, Eve thinks the chances are 50-50 that Alice and Bob areboth playing L or both playing R, so she has no profitable deviation from the prescribed actions s∗3(l) = L,s∗3(r) = R. On the other hand, after seeing ω1 = l, Alice knows for sure that Bob is playing L while Eve hasa 50-50 chance of playing L or R. Her payoff is maximized by playing the recommended s∗1(l) = L. (You cancheck the other deviations similarly.)Eve’s expected payoff in this correlated equilibrium is 1

2 · 2 + 12 · (−2) = 0. However, if Alice and Bob were

to play independent mixed strategies, then Eve’s best response leaves her with an expected payoff ofat least 1. To see this, suppose Alice plays L with probability qA and Bob plays L with probability qB . IfqA · qB ≥ (1 − qA) · (1 − qB), so that it is more likely that Alice and Bob coordinate on L than on R, Evemay play L to get an expected payoff of:

(−2) · (1− qA) · (1− qB)︸ ︷︷ ︸Alice and Bob meet without Eve

+ (2) · [1− (1− qA) · (1− qB)]︸ ︷︷ ︸otherwise