ee overview - 22nd sept 2014 final (3) -...

TRANSCRIPT

CEEOverview, Context & Key Trends09/23/2014

External Presentation: OutlineOutline: Outline

Review

« What’s happened/changed since last year?

« Investment context – if you had spent €500,000 in CEE…..

Looking Ahead: Driving Factors

« Macro-Econ & Market Summary

« Capital Value Indices – room for growth?

« Longer-term: structural shifts - logistic bananas, e-tailing, outsourcing, quality offices

September 2013: Summary

3

« Russia/Ukraine situation…..has changed things.

« Outside of the UK, Eurozone growth is ‘very patchy’

Bank finance conditions gradually improving, slowly spreading to the periphery

Lack of capital market depth – dependence on international investment

Office market trends better than headlines suggest – rents stabilised + growth capacity

Some pockets of retail yet to be tapped into, but challenging for non-dominant centres

Industrial/logistics market has very strong growth potential, esp in CE4 core and Russia

Long-term investment horizon very positive

Short-mid term also positive: capital values below peak/par, compared to Germany

Perception of non-core markets an ongoing concern – some justified, some not.

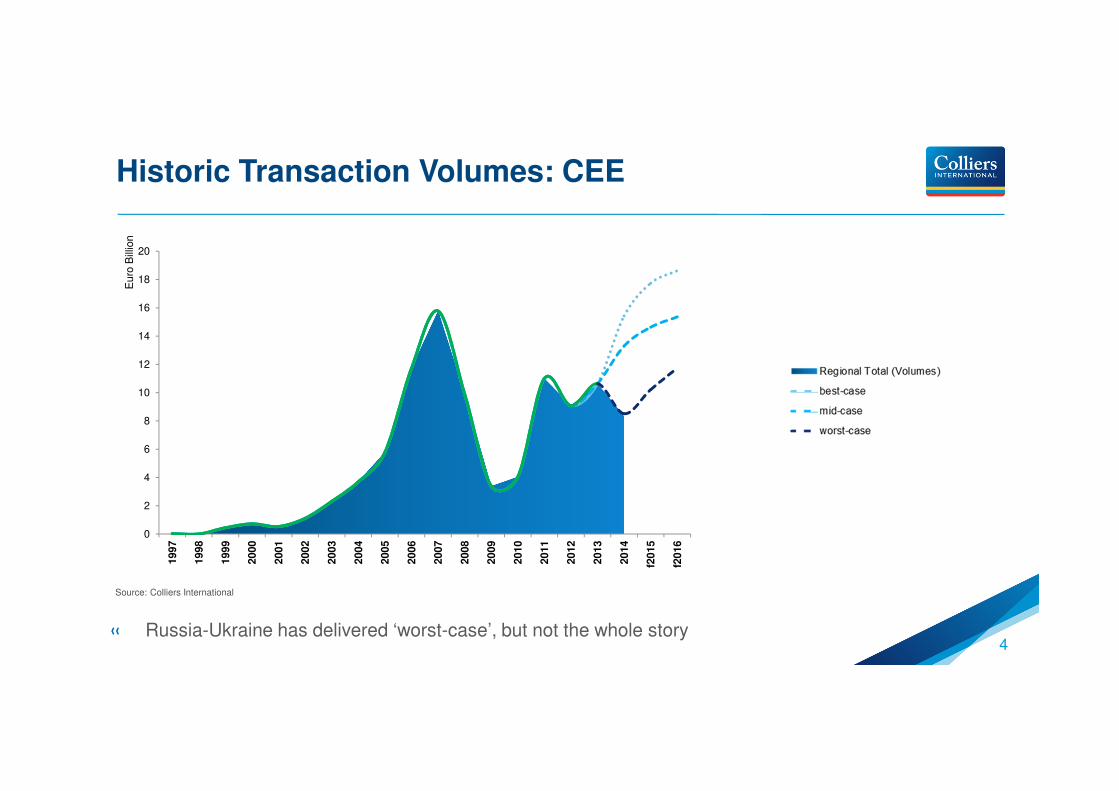

Historic Transaction Volumes: CEE

4

0

2

4

6

8

10

12

14

16

18

20

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

f2015

f2016

Euro

Bill

ion

« Russia-Ukraine has delivered ‘worst-case’, but not the whole story

Source: Colliers International

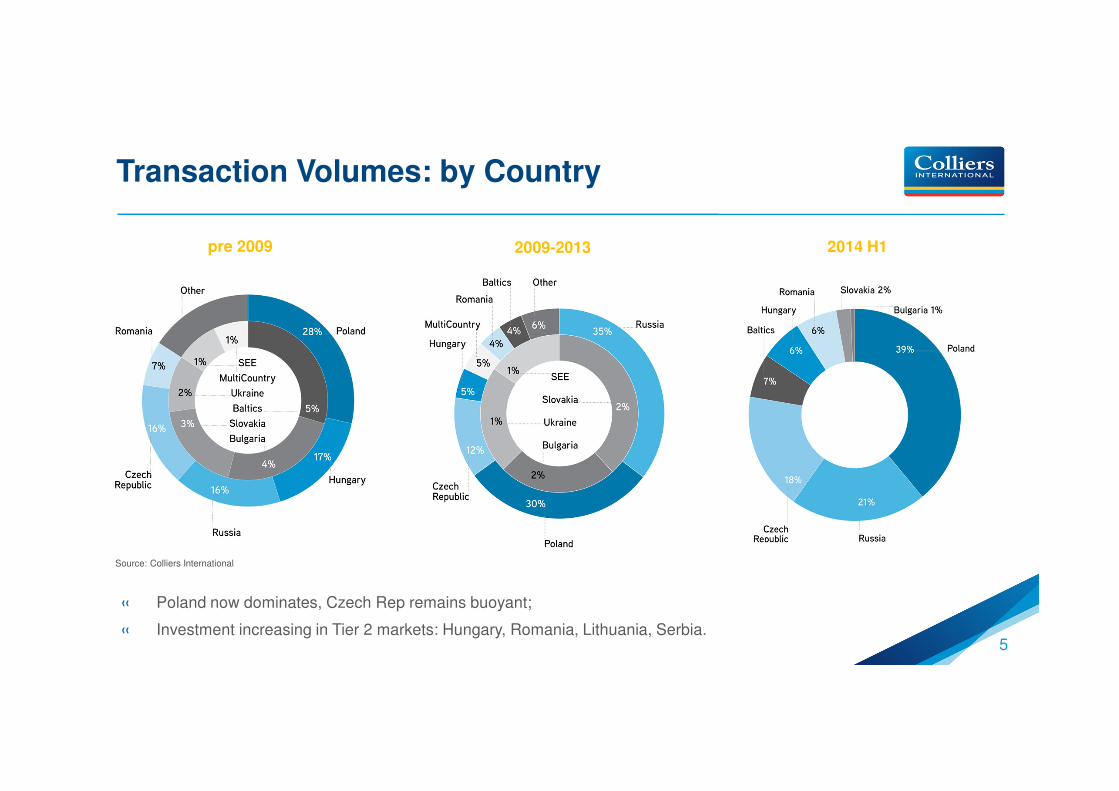

Transaction Volumes: by Country

5

« Poland now dominates, Czech Rep remains buoyant;

« Investment increasing in Tier 2 markets: Hungary, Romania, Lithuania, Serbia.

2014 H1pre 2009 2009-2013

Source: Colliers International

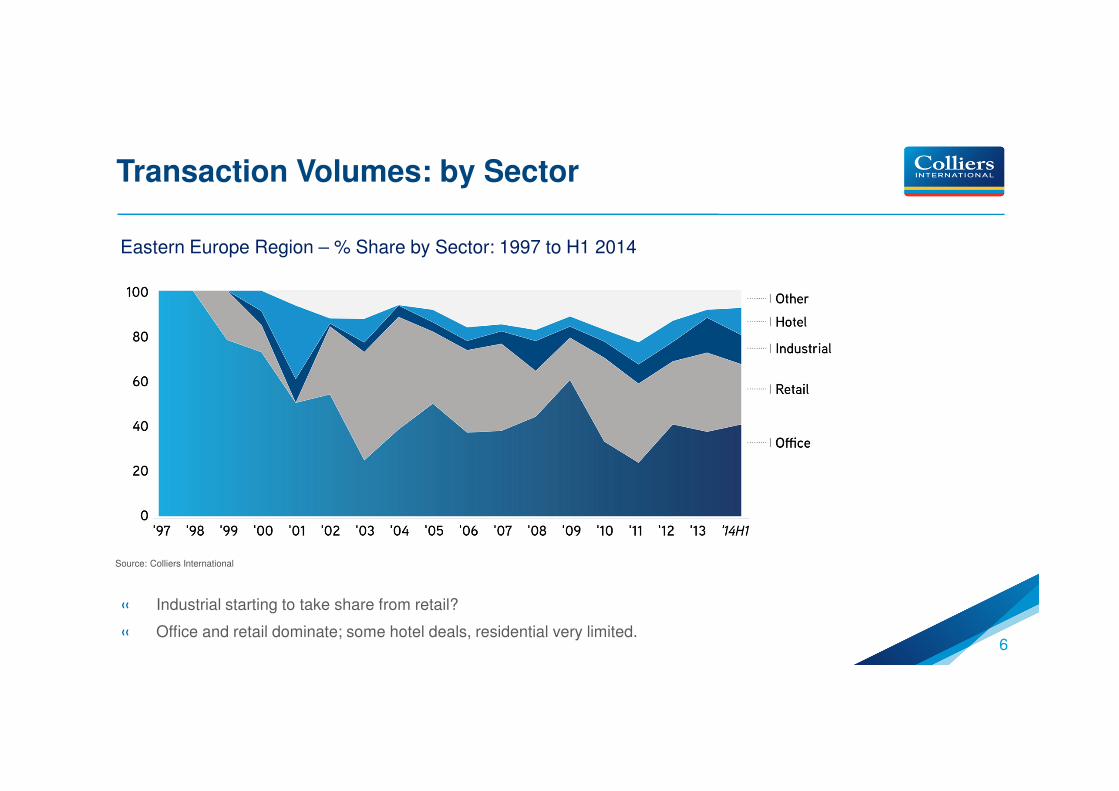

Transaction Volumes: by Sector

6

« Industrial starting to take share from retail?

« Office and retail dominate; some hotel deals, residential very limited.

Eastern Europe Region – % Share by Sector: 1997 to H1 2014

Source: Colliers International

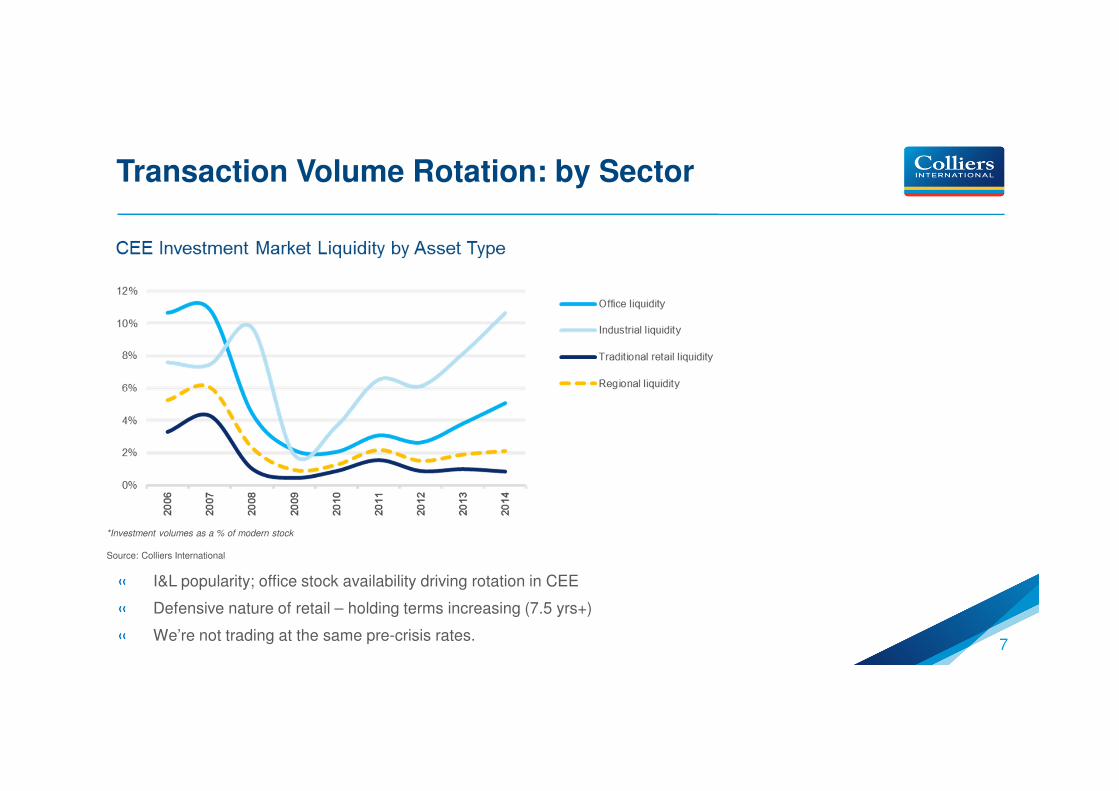

Transaction Volume Rotation: by Sector

7

« I&L popularity; office stock availability driving rotation in CEE

« Defensive nature of retail – holding terms increasing (7.5 yrs+)

« We’re not trading at the same pre-crisis rates.

*Investment volumes as a % of modern stock

Source: Colliers International

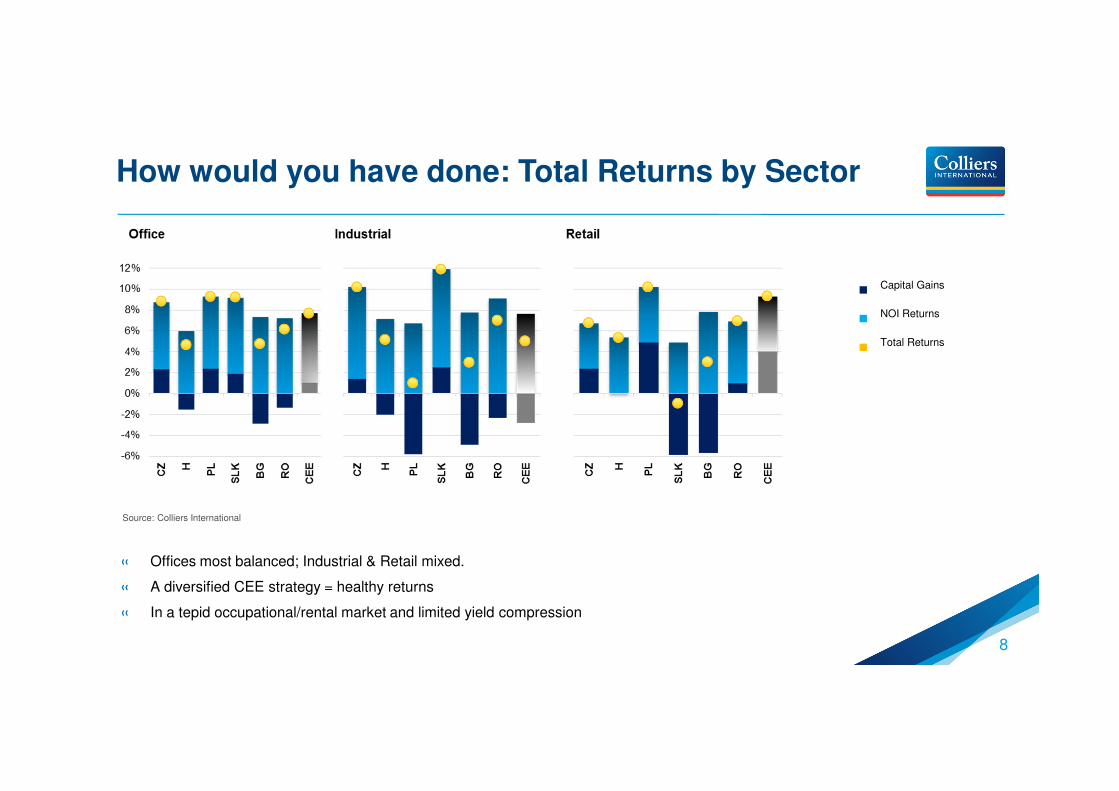

How would you have done: Total Returns by Sector

8

« Offices most balanced; Industrial & Retail mixed.

« A diversified CEE strategy = healthy returns

« In a tepid occupational/rental market and limited yield compression

■Capital Gains

■NOI Returns

■Total Returns

Source: Colliers International

How would you have done: by Country?

9

■ Capital Gains

■ NOI Returns

■ Total Returns

« Poland would have been the best country, retail

the best sector

« Czech the best risk-adjusted returns, vs govnt.

Bonds

« Romania, Slovakia and Hungary, followed by

Bulgaria

« CEE weighted allocation (oriented to core) =

equally positive

■ Country 10 year bonds

■ CRE Premia

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

PL

CE

E

CZ

RO

SL

K

H BG

Source: Colliers International

-15%

-10%

-5%

0%

5%

10%

15%

CE

E

Germ

an

y

Ho

llan

d

Sp

ain

Med

ian

Office

CE

E

Germ

an

y

Ho

llan

d

Sp

ain

Med

ian

Industrial

CE

E

Germ

an

y

Ho

llan

d

Sp

ain

Med

ian

Traditional Retail

How would you have done: CEE vs Europe?

10

« CEE matches Germany, Holland and Spain

« Office & retail best performing sectors.

« CEE industrial NOI comparable with other markets.

■Capital Gains

■NOI Returns

■Total Returns

Source: Colliers International / IPD

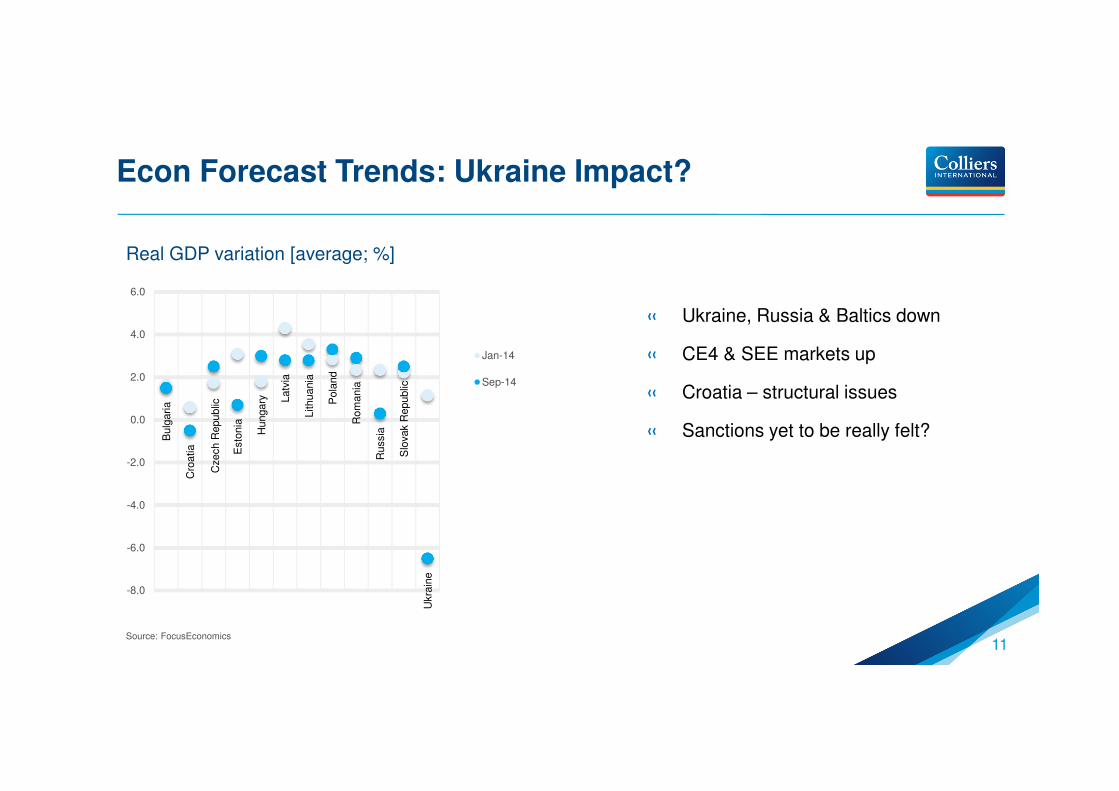

Econ Forecast Trends: Ukraine Impact?

11

« Ukraine, Russia & Baltics down

« CE4 & SEE markets up

« Croatia – structural issues

« Sanctions yet to be really felt?

Source: FocusEconomics

Bulg

aria

Cro

atia

Czech R

epublic

Esto

nia

Hungary L

atv

ia

Lithuania

Pola

nd

Rom

ania

Russia

Slo

vak R

epublic

Ukra

ine

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

Real GDP variation [average; %]

Jan-14

Sep-14

Country Summary: H1 2013 v H1 2014

12

H1 2013 H1 2014

Poor Neutral Good V. Good

• • • •

Market Summary

13

« Market activity likely to see yields compress

« Investment volumes likely to increase in 2014 and 2015

Russian/Ukraine impact localised to date – uncertainty a problem

Development/repositioning is needed – modernisation & investment flows

Clear increase in CRE investment demand elsewhere in the region

Fresh signs of economic (and political) recovery in CE4 and SEE

Investment driven by capital markets more than CRE fundamentals?

Prices/markets remain attractive relative to other ‘Eurozone Tier 2 markets’

Rents have declined/been flat post-crisis, still ‘buying off the bottom’