effect of micro and macro economic factors on the

TRANSCRIPT

Published by the Society for Alliance, Fidelity and Advancement (SAFA) 47

Research

Paper

Accepted 17 February, 2019

SAFA1= 0.63

International Journal of Business and Management Science

Chief Editor: Mohammad Safa

www.safaworld.org/ijbms23

Submission: [email protected]

Effect of Micro and Macro Economic Factors on the Financial Health of General Insurance Companies

in Indonesia

aToto Sugiharto,

bNovita Sulistiowati,

cRina Nofiyanti

ac

Faculty of Economics, Gunadarma University, Indonesia bFaculty of Information and Communication Technology, Gunadarma University,

Indonesia

*Corresponding author: [email protected]

Abstract: The objective of the study is to analyze the effect of macro and micro

economic factors on the financial health of general insurance companies in

Indonesia. Macroeconomic factors include economic growth rate, inflation rate, and

interest rate; microeconomic factors include company size, investment

performance, loss ratio, and current ratio. Financial health is represented by risk-

based capital. Automatic linear modeling was performed to test the proposed

hypotheses. It is revealed that the financial health of general insurance companies is

significantly influenced by, respectively, current ratio, reference interest rate,

inflation rate, and company size in different directions and magnitudes.

Keywords: General Insurance Companies; Risk Based Capital; Economic Growth;

Inflation Rate; Interest Rate; Company Size; Investment Performance; Current

Ratio

1SAFA stands for Standardized Acceptance Factor Average which is calculated based on the review scores. If the

obtained SAFA lies between 0.5 and 1 tends to be accepted for publication with the recommended level of

revision, if other requirements are satisfied. 2 Copyright @ 2025, Mohammad Safa: Unless otherwise noted, copyrights for the texts which comprise all issues

of the International Journal of Business and Management Science (IJBMS) are held by the copyright owner.

Items published by IJBMS may be freely shared among individuals, but they may NOT be republished in any medium without written consent from the copyright owner. In order to discuss any relevant issues or acquire

permission for reprint or reuse of data, please contact the editors at [email protected]. 3 Disclaimer: Facts and opinions published in the International Journal of Business and Management Science (IJBMS) express solely the opinions of the respective author(s). Author(s) are responsible for citing sources and

the accuracy of their references. The editors cannot be held responsible for any lacks or possible violations of

third parties’ rights. If any misconduct found in any published items, the relevant party may contact the editors for suggestions.

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

48 International Journal of Business and Management Science, 9(1): 47-65, 2019

INTRODUCTION

In the economic system, financial institutions function as economic support

through the provision of facilities that encourage capital outflows and capital

inflows or capital turnover. As one of the sectors in the financial industry,

insurance companies serve a special role in supporting monetary and investment

activities by providing long-term funds, while increasing risk-taking capabilities.

Additionally, the insurance sector is an integral part of a country's financial

industry whose role cannot be underestimated. Accordingly, if the performance of

this important sector is not encouraging and does not experience substantial

growth, it will influence the economic system in a very unfavorable way.

Insurance companies play an important role for both businesses and individuals

where they compensate for any losses and place them in the same position as

before the loss occurred. The level of the financial health of an insurance company

determines its position within the market, which, in turn, increases market growth.

The diversity in numbers and size of insurance companies, which are closely

related with both internal (microeconomic) factors and external (macroeconomic)

factors, provide an important contribution in determining the financial health as

well as financial performance of insurance companies.

Ghimire (2104) defines insurance as a means of financial protection from

events that result in loss of property (wealth or assets), loss of family head as the

backbone of family breadwinners, and loss of income due to accident, prolonged

illness, and disability permanent. Meanwhile, from a legal point of view,

according to Article 246 of the Commercial Code, insurance or coverage is

defined as an agreement where the insurers bind themselves to the insured by

obtaining a premium, to give him compensation due to a loss, damage, or not

expected benefit, which may be suffered due to an uncertain event. In addition, the

Financial Services Authority of Indonesia (OJK) defines insurance as the

agreement between the insurer and the insured requires the insured to pay a

premium to provide compensation for the risk of loss, damage, death, or loss of

expected profits, which may occur for unexpected events.

In the last decade, insurance companies in Indonesia experienced substantial

growth, particularly in total assets, premium growth rates and the ratio between the

rates of growth of premiums and gross domestic product. Data on these three

attributes over the past five years is presented in Table 1 below.

Table 1: Premium growth rate, premium growth rate to gross domestic product ratio and assets of

insurance companies 2012-2016

Attribute Year

2012 2013 2014 2015 2016

PGR1 (%) 14.90 9.80 28.10 19.50 15.36

PGR/GDP2 (%) 2.13 2.13 2.35 2.56 2.00

Asset (trilion IDR3) 584.02 659.73 807.68 853.42 984.53

Source: Financial Service Authority of Indonesia (Insurance Statistics 2016)

Note: 1Premium Growth Rate (Laju Pertumbuhan Premi); 2Gross Domestic Product (Produk

Domestik Bruto), 3Indonesian Rupiah

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

International Journal of Business and Management Science, 9(1): 47-65, 2019 49

In has been predicted by Rahim (2013) that the insurance industry in Indonesia

in the next five years has the potential to grow quite rapidly. However, there are

three important agendas that must be accomplished to realize these optimistic

projections. Firstly, internal consolidation that includes the consistent

implementation of the principle of risk-based capital (RBC), the implementation of

risk-based pricing (RBP) and the implementation of the principles of good

corporate governance (GCG) in a comprehensive manner. Secondly, the increase

and expansion of business activities through the application of the transfer of risk

concept that is to bear the risk of economic actors in other sectors through

professional asset management practices. Thirdly, improving human resources

(HR) quality, service quality, and the efficiency of corporate management through,

among others, the application of information and communication technology

(ICT) including information systems (Rahim, 2013).

Based on the above-mentioned background to the recent study, this research—

which aims to analyze the influence of macroeconomic and microeconomic

(company specific) factors on the financial health of Indonesian general insurance

companies—is of importance and, therefore, needs to be accomplished. Results of

the study are expected to provide managers or practitioners of insurance industry,

particularly general insurance companies, with information regarding

macroeconomic and microeconomic factors that potentially affect the financial

health of general insurance companies.

The paper is organized as follows. The second section describes the literature

review which consists of the financial health of insurance companies, the

determining factors of the financial health of insurance companies, the

macroeconomic determinants of the financial health of insurance company and research hypotheses. The third section explains the methods of the study which

covers research model and variables, methods of analysis and sampling

procedures. The fourth section consists of results and discussions which include

the descriptive statistical analysis of research variables, the results of the automatic

data preparation and the inferential statistical analysis of research variables.

Finally, we present our conclusions.

LITERATURE REVIEW

Financial Health of Insurance Companies

Similar with other types of business organizations, insurance companies are

established and operate their business activities with the aim of maximizing the

wealth of their shareholders by, among others, maximizing the company's market

value (Necas, 2016). In addition, Dahnel et al. (2005) in Necas (2016) explained

that the relationship between shareholders, insurance companies, and

policyholders (clients) can be illustrated as follows. Shareholders provide

capital—along with its related risks—for insurance companies with the hope of

obtaining revenue along with other requirements, namely the increase in market

value of the funds invested. On the other hand, policyholders (clients) divert risk

to insurance companies with the hope that in the future all obligations contained in

insurance policies are met by the insurance companies. In return, insurance

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

50 International Journal of Business and Management Science, 9(1): 47-65, 2019

companies demand premiums in accordance with the risks faced by clients taken

over by insurance companies.

Shareholders demand high returns - in this case return on assets (ROA) with

low risk. Policy holders (clients) want the maximum guarantee that the insurance

company in the future fulfills all its obligations in accordance with the insurance

policy (insurance policy) agreed upon by both parties. The extent to which the

insurance company is able to fulfill all of its obligations depends very much on

what is referred to as capital endowment or capital support or capital availability.

Meanwhile, the higher the level of capital support — the greater the capital

support that needs to be provided - it will be increasingly difficult for shareholders

to obtain the required or desired income. In uniting or harmonizing the desires of

both parties namely shareholders - who demand high returns (ROA) - and

policyholders (clients), who demand definitive and comprehensive guarantees,

insurance companies can use financial stability as an intermediary or the bridging

aspect between shareholders and policyholders. Chen and Wong (2004) use the

term financial stability and financial health insurance companies alternately or

interchangeably, meaning that they have the same meaning. Financial stability or

financial health of an insurance company acts as a prerequisite for insurance

companies in fulfilling the wishes of shareholders and policyholders (Necas,

2016). This is in line with Vaughan and Vaughan (2008) who states that the

financial stability or financial health of insurance companies is a very important

factor that must be considered in choosing an insurance company.

Chen and Wong (2004) and Necas (2016) in their study found that financial

stability and financial health are closely related to the solvency or solvency of

insurance or reinsurance companies to guarantee fulfillment of obligations

permanently following insurance or reinsurance activities from their own

resources , liquidity — the ability to fulfill its financial obligations at the right

time, without affecting normal operations, and profitability — the ability of

insurance companies to make profits. In Indonesia, based on the Financial Services

Authority (2016), compulsory insurance companies at all times meet financial

health level requirements where the level of financial health company includes: (a)

solvency level; (b) technical reserves; (c) sufficient investment; (d) equity; (e)

guarantee funds; and (f) other provisions relating to financial health.

Determining Factors of the Financial Health of Insurance Companies

Chen and Wong (2004) state that the financial health of insurance company

which is represented by insolvency of the company are influenced by a number of

factors. In general, these factors are classified into two major groups, i.e. micro-

determinants or micro-economic indicators or company-specific determinants and

macro determinants or macro-economic indicators (Chen and Wong, 2004;

Caporale et al., 2017). Micro-economic indicators that have the potential to affect

the health level of insurance companies, both life insurance and general insurance,

are presented in Table 2.

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

International Journal of Business and Management Science, 9(1): 47-65, 2019 51

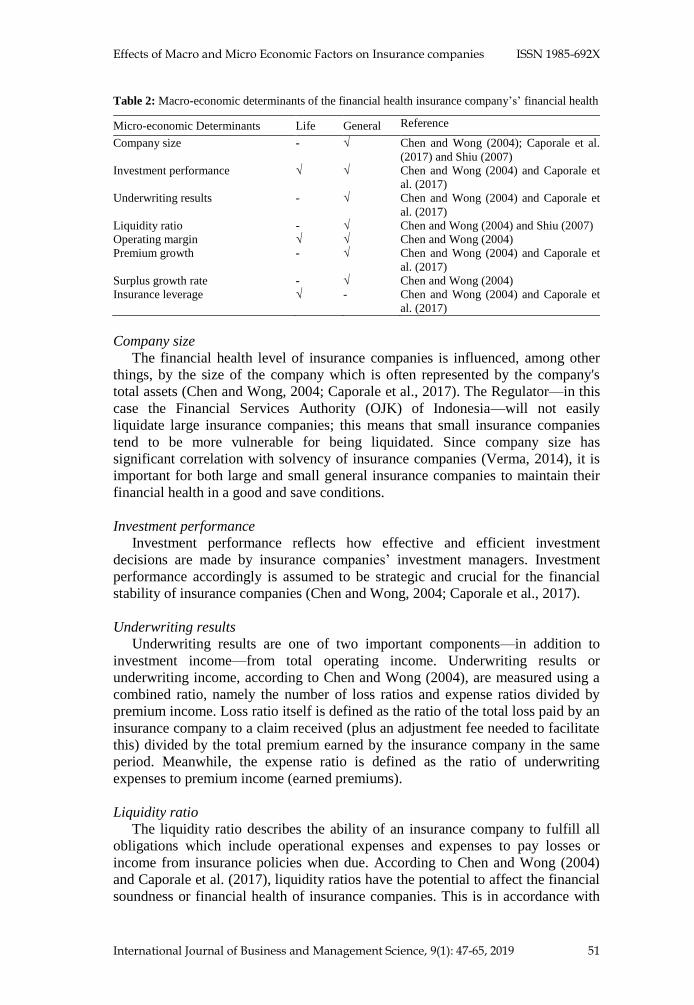

Table 2: Macro-economic determinants of the financial health insurance company’s’ financial health

Micro-economic Determinants Life General Reference

Company size - √ Chen and Wong (2004); Caporale et al.

(2017) and Shiu (2007)

Investment performance √ √ Chen and Wong (2004) and Caporale et

al. (2017)

Underwriting results - √ Chen and Wong (2004) and Caporale et

al. (2017)

Liquidity ratio - √ Chen and Wong (2004) and Shiu (2007)

Operating margin √ √ Chen and Wong (2004)

Premium growth - √ Chen and Wong (2004) and Caporale et

al. (2017)

Surplus growth rate - √ Chen and Wong (2004)

Insurance leverage √ - Chen and Wong (2004) and Caporale et

al. (2017)

Company size

The financial health level of insurance companies is influenced, among other

things, by the size of the company which is often represented by the company's

total assets (Chen and Wong, 2004; Caporale et al., 2017). The Regulator—in this

case the Financial Services Authority (OJK) of Indonesia—will not easily

liquidate large insurance companies; this means that small insurance companies

tend to be more vulnerable for being liquidated. Since company size has

significant correlation with solvency of insurance companies (Verma, 2014), it is

important for both large and small general insurance companies to maintain their

financial health in a good and save conditions.

Investment performance

Investment performance reflects how effective and efficient investment

decisions are made by insurance companies’ investment managers. Investment

performance accordingly is assumed to be strategic and crucial for the financial

stability of insurance companies (Chen and Wong, 2004; Caporale et al., 2017).

Underwriting results

Underwriting results are one of two important components—in addition to

investment income—from total operating income. Underwriting results or

underwriting income, according to Chen and Wong (2004), are measured using a

combined ratio, namely the number of loss ratios and expense ratios divided by

premium income. Loss ratio itself is defined as the ratio of the total loss paid by an

insurance company to a claim received (plus an adjustment fee needed to facilitate

this) divided by the total premium earned by the insurance company in the same

period. Meanwhile, the expense ratio is defined as the ratio of underwriting

expenses to premium income (earned premiums).

Liquidity ratio

The liquidity ratio describes the ability of an insurance company to fulfill all

obligations which include operational expenses and expenses to pay losses or

income from insurance policies when due. According to Chen and Wong (2004)

and Caporale et al. (2017), liquidity ratios have the potential to affect the financial

soundness or financial health of insurance companies. This is in accordance with

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

52 International Journal of Business and Management Science, 9(1): 47-65, 2019

Verma’s (2014) research results which indicate that liquidity ratio significantly

affect the solvency of insurance companies, in particular life insurance companies.

Operating margin

Intuitively, insurance companies that are considered profitable (profitable)

means they obtain more revenues than their expenses (expenses). Operating

margin, thus, is a measure of the proportion of the income of the insurance

company remaining after deduction to pay for all variable costs such as salary,

Premium growth

Premium growth reflects the level of market penetration of insurance

companies. The results of research conducted by Kim et al. (1995) indicate that

high premium growth is one of the numbers of factors that led to a decrease in the

level of financial health of insurance companies which in this study were

represented by insolvency. This indicates that the rate of premium growth that is

too fast and high will result in the phenomenon of self-destruction, especially if

other objectives of the insurance company are ignored (Chen and Wong, 2004).

Surplus growth rate

The surplus growth is closely related to operational margins (Chen and Wong,

2004). Therefore, it can be interpreted that insurance companies that fall into the

category of profitable will have a high surplus growth rate. However, it should be

considered that surplus growth is too fast and too substantial because the

phenomenon indicates that insurance companies will have a high level of

operational risk. This situation—too high an operational risk—will have an impact

on the financial soundness of insurance companies (Lee and Urrutia, 1996).

Insurance leverage

Insurance leverage is defined as a reserve for surplus (Chen and Wong, 2004).

Insurance companies that have a level of insurance leverage or financial leverage

will have a high risk that, among other things, is reflected in their low level of

financial health (Carson and Hoyt, 1995). Furthermore Carson and Hoyt (1995)

explained that the level of financial health of insurance companies can be

predicted from the amount of insurance leverage or financial leverage.

Macroeconomic Determinants of the Financial Health of Insurance Company

According to Browne and Hoyt (1999), there are three reasons for the

importance of understanding macroeconomic conditions for managers of insurance

companies. First, the health level of insurance companies is closely related to

macroeconomic conditions that are influenced by government policies - in this

case the Financial Services Authority (OJK). Second, the effectiveness of the

policies taken by the government (OJK) which have the potential to influence the

level of financial health of insurance companies is closely related to

macroeconomic conditions. Third, the resources needed to carry out supervision

and or control over the level of financial health of insurance companies depend

heavily on the macroeconomic conditions in which the insurance company

operates.

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

International Journal of Business and Management Science, 9(1): 47-65, 2019 53

The macro-economic indicators that are assessed as having the potential to

affect the health level of insurance companies are the inflation rates, economic

growth which are represented by current prices of gross domestic product (GDP),

bank interest rates, and level of competition (competitiveness) which is

represented by the number of insurance companies (Chen and Wong, 2004;

Caporale et al., 2017). The four of the macroeconomic indicators is presented in

the following table.

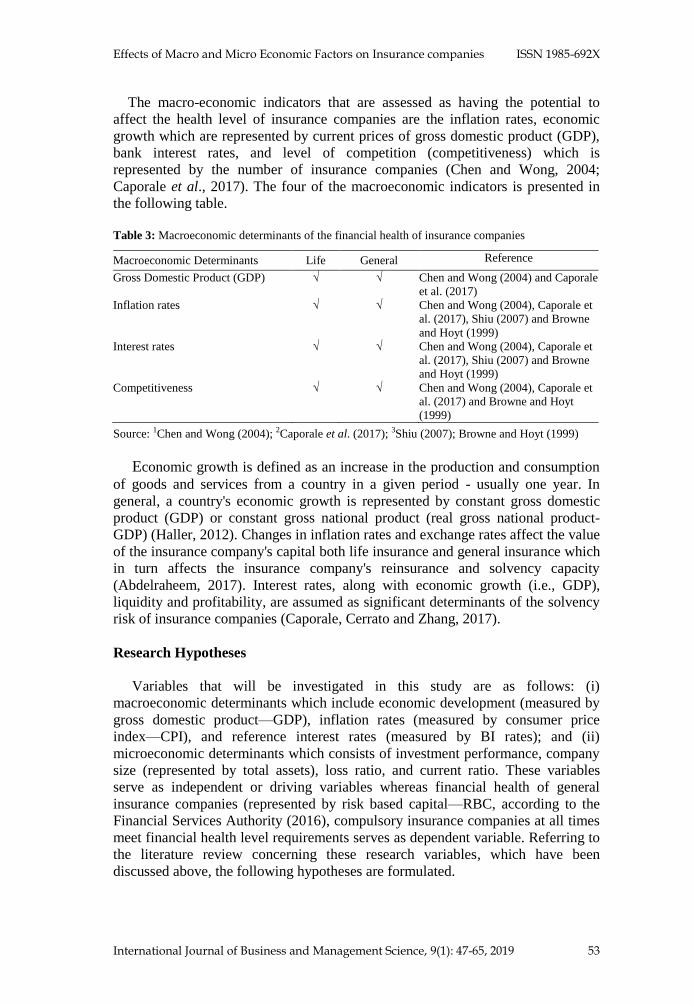

Table 3: Macroeconomic determinants of the financial health of insurance companies

Macroeconomic Determinants Life General Reference

Gross Domestic Product (GDP) √ √ Chen and Wong (2004) and Caporale

et al. (2017)

Inflation rates √ √ Chen and Wong (2004), Caporale et

al. (2017), Shiu (2007) and Browne

and Hoyt (1999)

Interest rates √ √ Chen and Wong (2004), Caporale et

al. (2017), Shiu (2007) and Browne

and Hoyt (1999)

Competitiveness √ √ Chen and Wong (2004), Caporale et

al. (2017) and Browne and Hoyt

(1999)

Source: 1Chen and Wong (2004); 2Caporale et al. (2017); 3Shiu (2007); Browne and Hoyt (1999)

Economic growth is defined as an increase in the production and consumption

of goods and services from a country in a given period - usually one year. In

general, a country's economic growth is represented by constant gross domestic

product (GDP) or constant gross national product (real gross national product-

GDP) (Haller, 2012). Changes in inflation rates and exchange rates affect the value

of the insurance company's capital both life insurance and general insurance which

in turn affects the insurance company's reinsurance and solvency capacity

(Abdelraheem, 2017). Interest rates, along with economic growth (i.e., GDP),

liquidity and profitability, are assumed as significant determinants of the solvency

risk of insurance companies (Caporale, Cerrato and Zhang, 2017).

Research Hypotheses

Variables that will be investigated in this study are as follows: (i)

macroeconomic determinants which include economic development (measured by

gross domestic product—GDP), inflation rates (measured by consumer price

index—CPI), and reference interest rates (measured by BI rates); and (ii)

microeconomic determinants which consists of investment performance, company

size (represented by total assets), loss ratio, and current ratio. These variables

serve as independent or driving variables whereas financial health of general

insurance companies (represented by risk based capital—RBC, according to the

Financial Services Authority (2016), compulsory insurance companies at all times

meet financial health level requirements serves as dependent variable. Referring to

the literature review concerning these research variables, which have been

discussed above, the following hypotheses are formulated.

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

54 International Journal of Business and Management Science, 9(1): 47-65, 2019

H1: Economic growth is assumed to have a positive correlation with financial

health of general insurance companies. General insurance companies operated

within an economic systems with high economic growth will have healthier

financial conditions (i.e., higher risk based capital—RBC).

H2: Inflation is assumed to have a negative correlation with financial health of

general insurance companies. General insurance companies operated within

an economic systems with high rates of inflation will have lower level of

financial health conditions (i.e., lower risk based capital—RBC).

H3: Reference interest rate is assumed to have a negative correlation with

financial health of general insurance companies. General insurance operated

within an economic systems with high rates of reference interest will have

lower financial health level (i.e., lower risk based capital—RBC).

H4: Investment performance is assumed to have a positive correlation with

financial health of general insurance companies. General insurance

companies with higher investment performance will have healthier financial

conditions (i.e., higher risk based capital—RBC).

H5: Company is assumed to have a positive correlation with financial health of

general insurance companies. A bigger general insurance companies will

have healthier financial conditions (i.e., higher risk based capital—RBC).

H6: Loss ratio is assumed to have a negative correlation with financial health of

general insurance companies. General insurance companies with higher loss

ratio will have less healthy financial conditions (i.e., lower risk based

capital—RBC).

H7: Current ratio is assumed to have a positive correlation with financial health

of general insurance companies. General insurance companies with higher

current ratio will have healthier financial conditions (i.e., higher risk based

capital—RBC).

METHODOLOGY

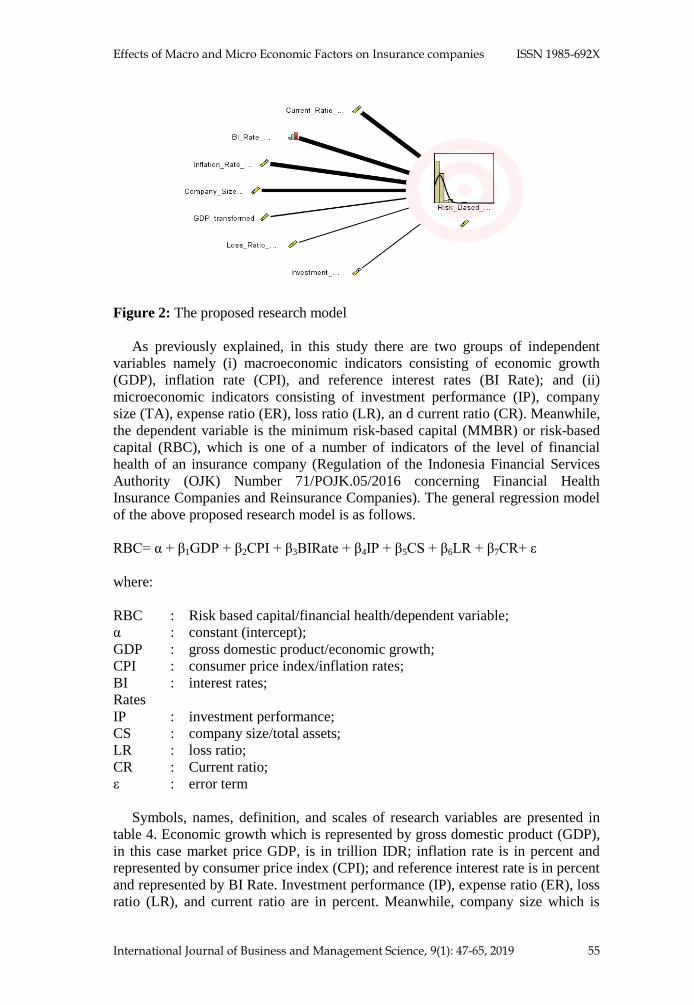

Research Model and Variables

Research model that illustrates the pattern of causal relationships amongst

variables, in this case between independent variables (i.e., economic development

(GDP), inflation rates (CPI), reference interest rates (BI rates), investment

performance, company size, loss ratio, and current ratio) and dependent variable

(i.e., financial health of general insurance companies measured by RBC) is

presented in figure 2 which follows.

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

International Journal of Business and Management Science, 9(1): 47-65, 2019 55

Figure 2: The proposed research model

As previously explained, in this study there are two groups of independent

variables namely (i) macroeconomic indicators consisting of economic growth

(GDP), inflation rate (CPI), and reference interest rates (BI Rate); and (ii)

microeconomic indicators consisting of investment performance (IP), company

size (TA), expense ratio (ER), loss ratio (LR), an d current ratio (CR). Meanwhile,

the dependent variable is the minimum risk-based capital (MMBR) or risk-based

capital (RBC), which is one of a number of indicators of the level of financial

health of an insurance company (Regulation of the Indonesia Financial Services

Authority (OJK) Number 71/POJK.05/2016 concerning Financial Health

Insurance Companies and Reinsurance Companies). The general regression model

of the above proposed research model is as follows.

RBC= α + β1GDP + β2CPI + β3BIRate + β4IP + β5CS + β6LR + β7CR+ ε

where:

RBC : Risk based capital/financial health/dependent variable;

α : constant (intercept);

GDP : gross domestic product/economic growth;

CPI : consumer price index/inflation rates;

BI

Rates

: interest rates;

IP : investment performance;

CS : company size/total assets;

LR : loss ratio;

CR : Current ratio;

ε : error term

Symbols, names, definition, and scales of research variables are presented in

table 4. Economic growth which is represented by gross domestic product (GDP),

in this case market price GDP, is in trillion IDR; inflation rate is in percent and

represented by consumer price index (CPI); and reference interest rate is in percent

and represented by BI Rate. Investment performance (IP), expense ratio (ER), loss

ratio (LR), and current ratio are in percent. Meanwhile, company size which is

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

56 International Journal of Business and Management Science, 9(1): 47-65, 2019

represented by total asset (TA) is in billion IDR. The level of financial health is

represented by risk based capital (RBC) and it is in percent.

Table 4: Symbols, names, definition, and scales of research variables

No. Research Variables

Definition Unit/Scale Symbol Name

Independent variables

1 GDP Economic growth The amount of added value generated

by all business units in a country or

the total value of final goods and

services produced by all economic

units of a country is estimated by

gross domestic product (GDP).

Trillion IDR

2 IR Inflation rates The trend of rising prices of goods and

services continues continuously. Percent

3 BI-Rate Reference interest rates The interest rate reflects the monetary

policy adopted by Bank Indonesia and

announced to the public.

Percent

4 IP Investment

performance

Investment performance illustrates the

effectiveness and efficiency of

investment decisions made estimated

by the ratio of net investment income

to total income.

Percent

5 CS Company size (Total

Assets)

The size of the insurance company

represented by the company's total

assets.

Trillion IDR

6

LR Loss ratio Ratios that describe losses

experienced by insurance companies

as a proportion of premium income

earned during the year.

Percent

7 CR Current Ratio Ratios which reflect the ability of an

insurance company to pay off all its

short-term debt.

Percent

Dependent Variable

8 RBC Risk-based capital. The amount of capital needed for

which the determination is based on

the risks faced.

Percent

Methods of Analysis

Automatic linear modeling (ALM – a procedure of linear regression analysis in

SPSS) is performed to test the proposed hypotheses. In addition, partial classical

assumption tests or model diagnosis (i.e., multicollinearity and autocorrelation) are

performed to analyze data. Different from traditional or conventional regression

analysis (i.e., multiple linear regression analysis), automatic linear modeling

accelerates the data analysis process through a number of automatic mechanisms.

Two of which are automatic variable selection and automatic data preparation

(Yang, 2014).

Automatic variable selection

A data set with a large number of independent variables where each of them

has the potential to serve as determinant of the dependent variable is very often

collected by researcher. Accordingly, deciding which variables will be included in

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

International Journal of Business and Management Science, 9(1): 47-65, 2019 57

multiple linear regression models is very difficult. This is believed to be the most

difficult part in multiple linear regression modeling. In general, researchers want

to choose at least one of the many variables that have the potential to be predictors

that provide accurate predictions with reasonable measurement costs. The

approach that is often used for this purpose is the method of variable selection,

which is one of the methods that is available and commonly used in the data

mining field. With the relevant determinants identified using the method of

selecting these variables, estimates and predictions will be more appropriate. Of

the many methods of selecting variables, the stepwise method and the all-

possibility-subset methods or the best-subset are still the most commonly used

methods. Automatic linear modeling has both all-possible-subsets and phases

ability (i.e., step forward) where both approaches are guided by some optimality

statistics. In this study, the best-subset method of variable selection is performed

where the objective of the linear modeling is to create or build a standard model.

Automatic data preparation

Before a linear modeling is accomplished, in this case a multiple linear

regression, the data to be used must be cleaned and, in turn, ready for use.

Common problems related to data include (i) missing data must that must be

replaced, (ii) data in the form of date/month/hour must be changed to duration

data, (iii) predetermined category predictors, and (iv) identify and handle outliers

correctly. In relation to the above-mentioned issues, automatic linear modeling

provides an automatic data preparation (ADP) platform with which many of data

cleaning procedures can be accomplished.

The automatic data preparation used in this study include the followings (i)

data and time handling, (ii) adjustment of measurement level, (iii) missing and

outlier values handling, and (iv) supervised merging.

Model Diagnostic Test

Results of model diagnostic which include autocorrelation test and

multicollinearity test are summarized in table 7 below.

Table 7: Summary of model diagnostic of research variables

Diagnostic test Method Results Conclusions

Autocorrelation Durbin-Watson 1.572 No autocorrelations

Multicollinearity Variance Inflation Factors (VIF) 1.047-1.468 No multicollinearity

Based on the results of model diagnostic tests, it is clear that the resulting

model is acceptable. Accordingly, the model can be regarded as the best linear

unbiased estimator of risk based capital (financial health) of general insurance in

Indonesia.

Sampling Procedures

Sixty seven general insurance companies in Indonesia (approximately 84

percent of the population) were involved in this study. These companies were

derived from 81 general insurance companies in 2011, 81 in 2012, 80 in 2013, 79

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

58 International Journal of Business and Management Science, 9(1): 47-65, 2019

in 2014, 75 in 2015, 75 and 75 in 2016. General insurance companies that will be

selected and involved in this study as sample should satisfy the following

conditions:

(i) exists in the whole research period (i.e., 2011-2016);

(ii) provides financial reports (i.e., balance sheets and income statements); and

(iii) provides all research variables (i.e., risk based capital, current ratio, loss ratio,

expense ratio, and investment performance).

The selected general insurance companies, which fulfilled all research

conditions, are presented in table 5 which follows.

Table 5: Sampling procedures

Conditions No of companies

Exists in the whole research period (i.e., 2011-2016); 75

Provides financial reports (i.e., balance sheets and income statements 72

Provides all research variables (i.e., risk based capital, current ratio, loss

ratio, expense ratio, and investment performance). 67

The selected general insurance companies 67

As clearly depicted in table 5 above, from 81 general insurance companies in

2011 and 75 general insurance companies in 2016, only 75 general insurance

companies that exist during the whole five years period (i.e., 2011-2016) where 72

of which that satisfy the second research conditions (i.e., provide a complete

financial reports for the whole research period of 2011-2016) and only 67 general

insurance companies which satisfy all research conditions. Accordingly, we have

only 67 general insurance companies that can be selected and involved as samples

in this study.

Panel data set comprising research variables was used in this study. Financial

reports which include balance sheets and income statements of the general

insurance companies covering the period 2011-2016 serve as the primary sources

of data. Therefore, the sample size of this study is 402 (i.e., 67 general insurance

companies x 6 periods). These were obtained from the Financial Services

Authority of Indonesia (OJK). Other data (i.e., regional economic development

and consumer price index) was obtained from Statistics Indonesia.

RESULTS AND DISCUSSION

Descriptive Statistical Analysis of Research Variables

In Table 6, which follows, results of descriptive analysis of dependent and

independent research variables are described. As clearly shown in the table,

general insurance companies’ financial health, which is in this study represented

by risk-based capital (RBC), substantially varied. It ranges from as low as 55

percent to as high as 3,866.24 percent and averages at 343.81 percent. Its

substantial variability is indicated by the value of coefficient of variation (CV)

which is more than 100 percent (i.e., 103.12 percent).

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

International Journal of Business and Management Science, 9(1): 47-65, 2019 59

Table 6: Descriptive statistics of research variables

Variables Descriptive Statistics

Minimum Maximum Mean Stdev* CV**

Risk based capital (percent) 55.00 3,866.24 343.81 354.53 103.12

GDP (trillion IDR) 7,831.73 12,406.81 9,928.56 1,683.70 16.96

Inflation rates (percent) 3.02 8.36 4.52 1.78 39.38

BI-rate (percent) 4.75 7.50 6.37 0.96 15.07

Investment performance

(percent)

0.01 42.59 6.62 4.10 61.93

Company size (billion IDR) 52.88 12,016.87 1,441,51 2,249.06 156.22

Loss ratio (percent) 0.01 12,078.12 230.80 613.20 265.68

Current ratio (percent) (267.10) 412.85 28.91 43.06 148.95

Note: * Standard deviation; ** Coefficients of Variation

Variability in macroeconomic indicators or determinant such as economic

growth (i.e., GDP), inflation rate (i.e., consumer price index), and reference

interest rate (i.e., BI Rate) is relatively low. Their coefficients of variances are,

consecutively, 16.96, 39.38, and 15.07 percent which indicates that the economic

conditions of the nation during the research time span relatively stable.

Significant divergences, meanwhile, are also found in microeconomic

indicators or company specific factors which include company size (ranges from

52.88 to 12,016.87 billion IDR), expense ratio (ranges from -26.77 to 515.77

percent), loss ratio (ranges from 0.01 to 12,078.12 percent), and current ratio

(ranges from -267.10 to 412.85 percent). Substantial variations amongst general

insurance companies’ specific factors also indicated by their related coefficient of

variations which are higher than 100 percent (i.e., their standard deviations are

higher than their mean). These substantial variations indicate that management

quality amongst general insurance companies is varied.

Results of the Automatic Data Preparation

Table 8 provides results of the automatic data preparation facilities available in

the Automatic Linear Modeling.

Table 8: Results of the automatic data preparation within the Automatic Linear

Modeling

Variables Role Action Taken

BI rates Predictor Change measurement level from continuous to ordinal

Merge categories to maximize association with target

Company size Predictor Trims Outliers

Current ratio Predictor Trims Outliers

GDP Predictor Trims Outliers

Inflation rate Predictor Trims Outliers

Investment performance Predictor Trims Outliers

Loss ratio Predictor Trims Outliers

Outliers were identified by procedures where continuous predictor values that

were outside the cutoff value (i.e., three standard deviations from the mean) were

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

60 International Journal of Business and Management Science, 9(1): 47-65, 2019

treated as outliers. As indicated in the table, except BI rate which was converted its

measurement from continuous to ordinal and merge the categories to maximize

association with target (i.e., dependent variable RBC) outliers within all

independent variable were trimmed. In addition, the automatic linear model also

provides diagnostic statistics, i.e., Cook’s Distance, which measures the effect of

each of the identified outliers on the suitable models. There were 23 outliers data

which were identified to have important contribution to the fitted model when they

were taken out from the model. However, only one of 23 data that have Cook’s

Distance greater than 0.5 but, fortunately, less than 1 (i.e., 0.634) which indicates

that the data can be assumed to be less influential. Accordingly, the resulting

model is acceptable.

Inferential Statistical Analysis of Research Variables: Results of the

Automatic Linear Modeling

Results of the Automatic Linear Modeling which represent the magnitudes

(regression coefficients), directions (sign of regression coefficients), significances

(p values), and importance of causal relationship amongst research variables (i.e.,

independent variables and dependent variable), is presented in the figure 3 below

and table 9 which follows.

Figure 3: The effects of independent variables on dependent variable (i.e., risk

based capital—RBC).

Figure 3 clearly shows that risk-based capital (RBC) of general insurance

companies in Indonesia is influenced in different directions and magnitudes by

current ratio, expense ratio, reference interest rate (BI Rate), inflation rate

(consumer price index), company size, and loss ratio. BI rate are presented in two

version of measurements (i.e., continues and ordinal). Both of them have similar

effect direction with slightly different magnitudes.

Risk based capital of general insurance companies, as clearly depicted in figure

3 and shown in Table 8, is significantly affected, consecutively, by current ratio,

reference interest rates (measured using BI Rate), inflation rates (consumer price

index), and company size (measured using total assets) in different magnitudes and

directions.

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

International Journal of Business and Management Science, 9(1): 47-65, 2019 61

Table 9: Regression coefficients (magnitude effects) and significance effect of causal relationships

between independent and dependent variables

Variables Coefficients Significance Importance/Strength

Intercept1 507.947 0.000 -

Current Ratio 1.861 0.000 0.556

BI Rate (continues) -427.844 0.000 0.188

BI Rate (ordinal) -226.576 0.000 0.188

Inflation Rate -78. 695 0.000 0.174

Company Size -0.043 0.000 0.082

Accuracy (R2): 24.30 percent,

F-test: 26.709 (p<0.000)

Current ratio

Current ratio is one of several measures of liquidity ratio of general insurance

companies. This ratio indicates an insurance company’s ability to settle its current

liabilities without prematurely selling long term investments or to borrow money.

If this ratio is less than 100 percent, then the insurance company’s liquidity

becomes sensitive to the cash flow from premium collections. Liquidity and

solvency are essential for insurance companies (D´Oliveira, 2006) in which

deficiency of liquidity means delays in honoring obligations with service

providers. If this situation is sustained over a long period, the market is likely to be

negatively impacted.

Finding of this research which revealed that current ratio significantly affects

the solvency (i.e., RBC) of general insurance companies is in line with D’Oliviera

(2006), Chen and Wong (2004), and Caporale et al. (2017). Current ratio affects

risk based capital in positive ways which means that general insurance companies

with higher current ratio tend to have higher risk based capital or financially

healthier than those of general insurance companies with lower current ratio.

Company size

Other microeconomic indicator or company specific determinant which

significantly affects financial health (RBC) of general insurance companies is

company size which is represented by company’s total assets. Interestingly, it

influences the financial health of general insurance companies in a negative way

meaning that larger general insurance companies tend to have lower RBC or less

healthy financially than those smaller general insurance companies. This finding is

to same extent in accordance with Chen and Wong (2004) as well as Caporale et

al. (2017) who state that financial health of an insurance company is affected by its

size. Since large insurance company tends not to be liquidating easily by the

authority, larger general insurance company tends to have lower RBC.

Reference interest rate (BI rate)

BI rate (reference interest rate) is found to negatively affect risk based capital

of general insurance companies. This implies that general insurance reference

interest rate (BI rate) will have lower risk based capital or financially less healthy.

In other words, the higher the reference interest rates the lower the RBC or the

lower the financial health of the company. In general, this finding is in line with

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

62 International Journal of Business and Management Science, 9(1): 47-65, 2019

those findings of Abdelraheem (2017) and Caporale et al. (2017) where increase in

interest rates tends to reduce the level of financial health of general insurance

companies. Empirical results of Boubaker and Sghaier (2012) support the finding

which shows that the interest rate and the inflation rate have a differentiated

impact on the non-life insurance premiums depending on the value of the inflation

rate. The inflation rate and exchange rate, according to Ahlgrim and D’Arcy

(2012), negatively influence the financial health of insurance companies where

companies which are operated within an economic system characterized by higher

inflation rates tend to have lower financial health condition.

Inflation rate (Consumer price index)

Inflation rate (consumer price index) is revealed to have negative effect on risk-

based capital of general insurance companies. General insurance companies which

is operated within an economic system characterized by higher rate of inflation

(consumer price index) will have lower risk-based capital or financially less

healthy.

This finding is, to some degree, in accordance with Ahlgrim and D‘Arcy (2012)

statement that the effect of inflation rate on financial health insurance companies,

which is in negative way, considered as one of the top risk list for insurers. In

addition, the inflation rate has a direct effect on claims cost and investment

performance as well as assets and liabilities of insurance company.

CONCLUSIONS

The level of financial health of general insurance companies which in this study is

estimated by risk-based capital (RBC) was influenced by reference interest rates

(i.e., BI rates), inflation rates (i.e., consumer price index—CPI), liquidity (i.e.,

current ratio—CR), and company size (i.e., total assets) in different directions and

magnitudes. Macro-economic factors which include reference interest rates and

inflation rates are revealed to significantly affect the financial health of general

insurance companies in negative way. This means that increases in either interest

rates or inflation rates will cause risk-based capital of general insurance companies

to decrease or have lower level of financial health vice verza. This also indicates

that macro-economic environments which are characterized by high rates of

interest and inflation will decrease the financial health of general insurance

companies. Microeconomic indicators which significantly affect the financial

health of general insurance companies are liquidity ratio (i.e., current ratio) and

company size (i.e., total assets). General insurance companies having higher

liquidity ratio tend to have better financial health conditions. Larger general

insurance companies, interestingly, tend to have lower level of financial health

conditions.

LIMITATION OF THE RESEARCH

In the present study financial health of general insurance companies is only

represented by risk-based capital (RBC). Other measures of financial health of

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

International Journal of Business and Management Science, 9(1): 47-65, 2019 63

insurance companies, both general/non-life and life insurance, according to the

Indonesia Financial Authority Regulation No. 71/POJK.5/2016, include technical

reserve, equity, and investment adequacy. For further study, it is recommended to

take these measures into account to examine whether any difference amongst these

measures in relation to their potential driving factors i.e., macroeconomic as well

as microeconomic ones.

ACKNOWLEDGEMENTS

Special appreciation is addressed to the Directorate of Research and Extensions,

Directorate General of Higher Education, Ministry of Research and Higher

Education of the Republic of Indonesia for providing the required research funds.

Gunadarma University Research Center and the Indonesia Insurance Institute

(AAMAI) were of great support for providing supporting data and information for

the study.

REFERENCES

Abiodun, A.J. (2009). Empirical evidence of executives’ perception and scanning of

business environment in Nigeria. Buletinul Universitatii Petrol. 61(3): 12-25.

Adam, M., J. Anderson, L-F. Anderson and M. Lindmaar (2005). The historical relation

between banking, insurance and economic growth in Sweden: 1830 to 1998. Available

from: https://brage.bibsys.no.adams mike 2605.pdf [Accessed 25 October 2017].

Akinlo, T. and O. T. Apanisile (2014). Relationship between insurance and economic

growth in Sub-Saharan African: A panel data analysis. Modern Economy. 2(5): 120-

127.

Akpan, S. S., Mahat, F., Noordin, B-A. and Nassir, A. (2017). Contrasting the effect of

risk- and Non-risk-based capital structure on insurers’ performance in Nigeria, Social

Science, 2(6): 143-148.

Bednarczyk, T. H. (2013). Insurance development as a factor in long-term economic

growth. Insurance Review. 4(23): 29-46.

Bellando, J-L (2006) Assessing the financial health of insurance undertakings to protect

the insured from the risks to which these firms are exposed: Solvency rules. Available

from: www.oecd.org/finance/insurance/1857594 20 [Accessed 14 December 2017].

Brainard, L. (2008). What is the role of insurancein economic development? (The Second

Paper), Zurich, Switzerland: Zurich Government and Industry Affairs.

Burca, A-M. and G. Batrinca (2013). The determinants of financial performance in the

Romanian insurance market, International Journal of Academic Research in

Accounting, Finance and Management Sciences. 4(1): 299–308.

Capital Market and Financial Institution Supervisory Agency (2012). Insurance Statistics

of Indonesia 2011. Jakarta, Indonesia: Capital Market and Financial Institution

Supervisory Agency of the Republic of Indonesia.

Caporale, G.M., Cerrato, M. and Zhang, X. (2017). Analysing the determinants of

insolvency risk for general insurance firms in the UK, Journal of Banking and Finance.

3(84): 107-122.

Cekrezi, A. (2015). Determinants of financial performance of the insurance companies: A

case of Albania, International Journal of Economics, Commerce and Management.

3(4): 1-10.

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

64 International Journal of Business and Management Science, 9(1): 47-65, 2019

Chen, R. and Wong, K. A. (2004). The determinants of financial health of Asian insurance

companies, The Journal of Risk and Insurance. 71(3): 469-499.

Cristea, M., Marcu, N. and. Carstina, S. (2014). The relationship between insurance and

economic growth in Romania compared to the main results in Europe–a theoretical and

empirical analysis. Procedia Economics and Finance. 4(8): 226-235.

Curak, M., Loncar, S. and Poposki, K. (2009). Insurance sector development and economic

growth in transition countries. International Research Journal of Finance and

Economics. 4(34): 29-41.

Delen, D., Kuzey, C. and Uyar, A. (2013). Measuring firm performance using financial

ratios: A decision tree approach, Expert Systems with Applications. 40 (2013): 3970–

3983.

Ege, I. and Bahadir, T. (2011). The relationship between insurance sector and economic

growth: An econometric analysis. International Journal of Economic Research. 2(2): 1-

9.

Financial Service Authority of Indonesia (2013). Insurance statistics of Indonesia 2012.

Jakarta, Indonesia: Financial Service Authority of Indonesia.

Financial Service Authority of Indonesia (2014). Insurance statistics of Indonesia 2013.

Jakarta, Indonesia: Financial Service Authority of Indonesia.

Financial Service Authority of Indonesia (2015). Insurance statistics of Indonesia 2014.

Jakarta, Indonesia: Financial Service Authority of Indonesia.

Financial Service Authority of Indonesia (2016). Insurance statistics of Indonesia 2015.

Jakarta, Indonesia: Financial Service Authority of Indonesia.

Financial Service Authority of Indonesia (2017). Insurance statistics of Indonesia 2016.

Jakarta, Indonesia: Financial Service Authority of Indonesia

Financial Service Authority of Indonesia (2013). Financial Services Authority (OJK)

Regulation Number 71/POJK.05.2016 concerning Insurance and Reinsurance

Companies. Jakarta, Indonesia: Financial Service Authority of Indonesia

Ghimire, R. (2014). Contribution of insurance industries in economic development of

Nepal. Reflection. 3(5): 1-12.

Han, L., D. Li, Moshirian, F. and Tian, Y. (2010). Insurance development and economic

growth. The Geneva Papers 5(35): 183–199.

International Monetary Fund (2107). Financial system stability assessment. (IMF Country

Report No. 17/152). Washington DC. USA: International Monetary Fund.

Joo, B.A. (2013). Analysis of financial stability of Indian non-life insurance companies,

Asian Journal of Finance & Accounting 5(1): 306-319.

Kaur, N. and R. Kapoor (2007). Profitability analysis of public sector banks in India.

Indian Management Studies Journal 7(11): 167-180.

Kyule, J.M (2015). Impact of liquidity and solvency on financial performance of firms

listed at the Nairobi Securities Exchange. Unpublished master’s thesis. University of

Nairobi. Nairobi, Kenya.

Liedtke, P.M. (2007). What’s insurance to a modern economy? The Geneva Papers, 7(32):

211-221.

Maaka, Z.A. (2013). The relationship between liquidity risk and financial performance of

commercial banks in Kenya. Unpublished master’s thesis, University of Nairobi,

Nairobi, Kenya.

Malik, H. (2011). Determinants of insurance companies’ profitability: An analysis of

insurance sector of Pakistan, Academic Research International. 1(3): 2-16.

Moro, O. and Anderloni, L. (2014). Non-life insurance economic performances—An

empirical investigation, Journal of Economics and Management. 3(8): 160-177.

Obudho, A.R. (2014). The relationship between financial risk and financial performance

of insurance companies in Kenya. Unpublished master’s thesis, University of Nairobi,

Nairobi, Kenya.

Effects of Macro and Micro Economic Factors on Insurance companies ISSN 1985-692X

International Journal of Business and Management Science, 9(1): 47-65, 2019 65

Pervan, I. and Kuvek, T. (2013). The relative importance of financial ratios and non-

financial variables in predicting of insolvency, Croatian Operational Research Review

(CRORR), 4(4): 187-198.

Rahim, H. (2013). Indonesian insurance growth optimism: Five-year development

projection (2014-2018). Journal of Insurance and Risk Management. 1(2): 1-21.

Setiawan, S. (2013). Prospects and competitiveness of Indonesia's insurance sector amid

the challenges of integrating ASEAN financial services. In H. Amir (Ed.).

Strengthening International Economic and Financial Relations in Support of National

Development. Jakarta, Indonesia: Naga Media.

Sherris, M. (2007). Risk based capital and capital allocation in insurance (Institute of

Actuaries of Australia Biennial Convention 2007). Canberra, Australia: The Institute of

Actuaries of Australia.

Smith, T.M. and Reece, J.S. (1999). `The relationship of strategy, fit, productivity and

business performance in a service setting, Journal of Operations Management. 2(17):

145-161

Vaughan, E.J. and Vaughan, T. (2008) Fundamentals of risk and insurance. Hoboken, New

Jersey, USA: John Wiley & Sons.

Verma, A. and Bala, R. (2013). The relationship between life insurance and economic

growth: Evidence from India. Global Journal of Management and Business Studies.

3(4): 413-422.