ellen yin-wycoff, associate director harkmore lee, msw dir. of training & education calcasa

TRANSCRIPT

Ellen Yin-Wycoff, Associate DirectorHarkmore Lee, MSW

Dir. of Training & EducationCALCASA

1) Overview of workshop2) Group Agreements3) Learning Objectives4) Taking the first steps5) Managing from an anti-oppression

framework 6) Developing a program7) Developing a program budget8) Grant Compliance9) Other areas10) Review

ALL IDEAS AND POINTS OF VIEW HAVE VALUE You may hear something you do not agree with or you think is "silly" or "wrong." Please remember that one of the goals of this meeting is to share ideas. All ideas have value in this setting. Also share YOUR ideas and thoughts and avoid editorials of another colleague’s comments.

SAFE SPACEWhat is shared and discussed with one another should “stay here” – apart from ideas and solutions that will help your own work and agency.

USE COMMON CONVERSATIONAL COURTESY Please don't interrupt; use appropriate language, avoid third party/ side bar discussions, etc.

HUMOR IS WELCOME BUT humor should never be at someone else's expense.

HONOR TIME We have an ambitious agenda, so it will be important to follow the time guidelines for the next two days.

CELL PHONE / TEXTING / E-MAIL COURTESY Please turn cell phones, or any other communication item with an on/off switch to “silent. If you need to respond, kindly step outside

BE COMFORTABLEPlease feel free to take personal breaks as needed

ANY OTHERS AGREEMENTS TO ADD?

• To under the challenges and rewards of becoming a new manager

• To develop a management approach through an anti-oppression lens.

• To be equipped with basic knowledge, skills and tools to become a manager.

1) Understand the role of managers as good stewards of money (“Big Picture”)

2) Understand the reasons why we budget3) Learn a process of developing a program

budget4) Practice formulating a budget.

ACTUAL % BUDGET VARIANCE PRIOR YR ACTUAL % BUDGET VARIANCE PRIOR YR

Contributions: General $ - 0.00% $ 11,000.00

$ (11,000.00) $ 5,179.26 $ 11,516.03 0.31% $ 124,500.00 $(112,983.97) $ 145,965.94

Restricted $ 27,968.17 7.24% $ 8,000.00 $ 19,968.17 $ 2,444.06 $ 94,059.45 2.53% $ 29,000.00 $ 65,059.45 $ 44,985.73

Grants $ 3,690.00 0.95% $ - $ 3,690.00 $ - $ 38,727.66 1.04% $ 33,750.00 $ 4,977.66 $ 14,903.00

Custodial $ 2,350.00 0.61% $ 1,100.00 $ 1,250.00 $ 2,620.00 $ 10,750.00 0.29% $ 11,000.00 $ (250.00) $ 12,200.00

Other $ - 0.00% $ 200.00 $ (200.00) $ - $ - 0.00% $ 2,200.00 $ (2,200.00) $ -

Special Events $ - 0.00% $ 3,400.00 $ (3,400.00) $ 700.00 $ 105,714.60 2.85% $ 125,770.00 $ (20,055.40) $ 96,720.99

Membership Dues $218,751.66 56.61% $209,468.00 $ 9,283.66 $208,683.16 $2,177,928.31 58.63% $2,064,176.00 $ 113,752.31 $1,881,032.90

Program Service Fees $139,474.73 36.09% $155,166.00

$ (15,691.27) $133,634.40 $1,346,398.01 36.25% $1,546,386.00 $(199,987.99) $1,417,194.60

Gross income $392,234.56 101.51% $388,334.00 $ 3,900.56 $353,260.88 $3,785,094.06 101.90% $3,936,782.00 $(151,687.94) $3,613,003.16 Financial Assistance and Discounts $ (16,449.04) -4.26% $ (9,354.00)

$ (7,095.04) $ (13,573.67)

$ (153,056.06) -4.12%

$ (89,641.00) $ (63,415.06) $ (101,443.70)

Insufficient funds $ 1,114.40 0.29% $ (2,100.00) $ 3,214.40 $ 1,760.65 $ (3,093.21) -0.08%

$ (21,000.00) $ 17,906.79 $ (9,383.68)

Total operating income $376,899.92 97.54% $376,880.00 $ 19.92 $341,447.86 $3,628,944.79 97.69% $3,826,141.00 $(197,196.21) $3,502,175.78 Interest and Dividend income $ 2,922.37 0.76% $ 200.00 $ 2,722.37 $ 3,563.33 $ 20,143.77 0.54% $ 2,000.00 $ 18,143.77 $ 16,559.34 Unrealized Gain (loss) Investments $ 6,415.66 1.66% $ 1,200.00 $ 5,215.66 $ 14,335.47 $ 36,278.26 0.98% $ 12,000.00 $ 24,278.26 $ 35,686.99 Realized Gain (loss) Investments $ - 0.00% $ - $ - $ - $ 13,000.00 0.35% $ - $ 13,000.00 $ -

Other income $ 178.38 0.05% $ 1,500.00 $ (1,321.62) $ 205.72 $ 16,280.69 0.44% $ 15,000.00 $ 1,280.69 $ 25,531.99

Total income $386,416.33 100.00% $379,780.00 $ 6,636.33 $359,552.38 $3,714,647.51 100.00% $3,855,141.00 $(140,493.49) $3,579,954.10

Salaries $178,964.44 46.31% $196,654.00 $ 17,689.56 $168,185.28 $1,872,880.04 50.42% $1,985,040.00 $ 112,159.96 $1,729,567.21 Salaries - Capital Campaign $ 871.13 0.23% $ - $ (871.13) $ - $ 3,450.01 0.09% $ - $ (3,450.01) $ -

Retirement $ 4,686.25 1.21% $ 6,252.00 $ 1,565.75 $ 4,854.17 $ 53,396.07 1.44% $ 60,180.00 $ 6,783.93 $ 45,666.46

FINANCEDIRECTOR

Money is a powerful. How it is managed and controlled can result in positive and negative ways.

Must be good stewards of funds. Budget is tool to help us be good stewards

and help us accomplish our objectives

Resource allocation: Budget is a “spending plan,” and is principal mechanism for deciding priorities between programs.

Financial control: One of the principal mechanisms for assuring resources are spent as decided by an agency’s Board of Directors.

Management control: Use budget to help improve efficiency and effectiveness.

Planning tool: Budget can be connected to the strategic plan.◦ “The budget can be thought of as the

continuous improvement plan translated into a performance plan.” Keuren (2002)

Communications device: Budget can be used to communicate goals and objectives of an organization, and how resources are allocated to meet this objectives.

1) Determine timeline to complete the program budget.2) Identify program’s key objectives or target goals.3) Determine the program’s outcomes and the

strategies/tasks needed to achieve the outcomes4) Identify the budget format your agency utilizes for its

fiscal year.5) Identify the expenses associated with these tasks and

estimate the values over the course of the fiscal year.6) Identify potential funds to cover these program costs

and estimate the amounts available.7) Seek preliminary approval by Executive Director and

await final decision by Board of Directors.8) YEA! Board approves. Be ready to execute and monitor

program budget.

Executive Director Finance Director or Manager Other program managers or directors

Have a very clear, written vision of what your program will look like and what it will accomplish.

Familiar with key financial terms Know Microsoft Excel Do not be intimidated. Utilize the

opportunity to be a good steward of money and help advocate and empower survivors and your program staff.

Executive Director, Finance Director and the Board of Directors will determine when the Agency budget must be approved for the next fiscal year.

Then calendar backwards 4 – 6 months and schedule key meetings and deadlines.

Program budgets will feed

December/January•Begin discussions regarding next fiscal year’s programs and identify key objectives, outcomes, and strategies.

•Budget development schedule sent to program managers. General budget guidelines & directions are given to program staff. Program staff begin work.

May•Staff completes final draft of budget

•Finance Committee reviews final version and approves it. Prepares for final Board approval.

March•First draft of agency budget is completed.

February•Program Managers continue to work on their individual program budgets.

•Meet with Finance staff to estimate revenues and expenses.

•First draft of program budgets are done.

April•Finance Committee review first budget draft and makes preliminary recommendations and changes. Send it back to staff.

June•Board of Directors reviews and approved final budget for upcoming fiscal year.

July 1st•Fiscal year begins. New agency budget in place. Programs can begin work for new fiscal year.

Sample Budget Development Timeline

For a July 1st Fiscal Year (F)

It improves planning and budget preparation by providing advance notice of when particular information is required and who is responsible for obtaining the information.

It facilitates gathering opinions/data from key staff, board members, etc. by providing clear timeline on when decisions have to be made.

Helps to assure that legal dates/requirements of the budget process are met.

Facilitates informing staff about the process, and provides staff an opportunity to give input.

Now that you have developed your timeline, begin to identify key objectives of your new program.

Utilize Logic Model Framework sheet Keep it simple: 2 -3 key objectives

Utilizing Logic Model Framework, identify the key outcomes wish to achieve for each objective.

Outcomes must be measurable. Be specific and quantify (e.g. the Hotline Program will provide support to 10 survivors each month)

Keep it simple: 2 -4 key measurable outcomes for each objective or target. Be realistic.

Specifically identify the strategies and tasks need to achieve outcomes (e.g. Program staff will conduct outreach meetings with four different first responders in the area and provide information about the Hotline Program).

Two common ones: 1) Line Item

This is a more traditional method of developing a budget using the previous year's budget as a base and will then require a justification for any increase that is requested for the ensuing year.

2) Zero-basedThe zero based budget is a procedure and system based on a justification for all expenditures of an organization at the time the budget is formulated as it allows management to, in effect, start over and not be influenced by previous budgets.

Example: If you have $300 to budget, you might budget $150 to food, $100 to clothing, $35 to toiletries, and $15 to entertainment. You now have zero dollars left to later spend. If you decide you want $25 for entertainment, then you had better pull $10 from one of those other categories.

It provides an effective means of tracking the effectiveness and impact of a particular expenditure and allows for adjustment based on the analysis.

Determine staffing needs and other program related costs (e.g. material costs, trainings, etc.

Utilize samples Direct vs. Indirect Costs Reasonable, Allocable, and Allowable Costs

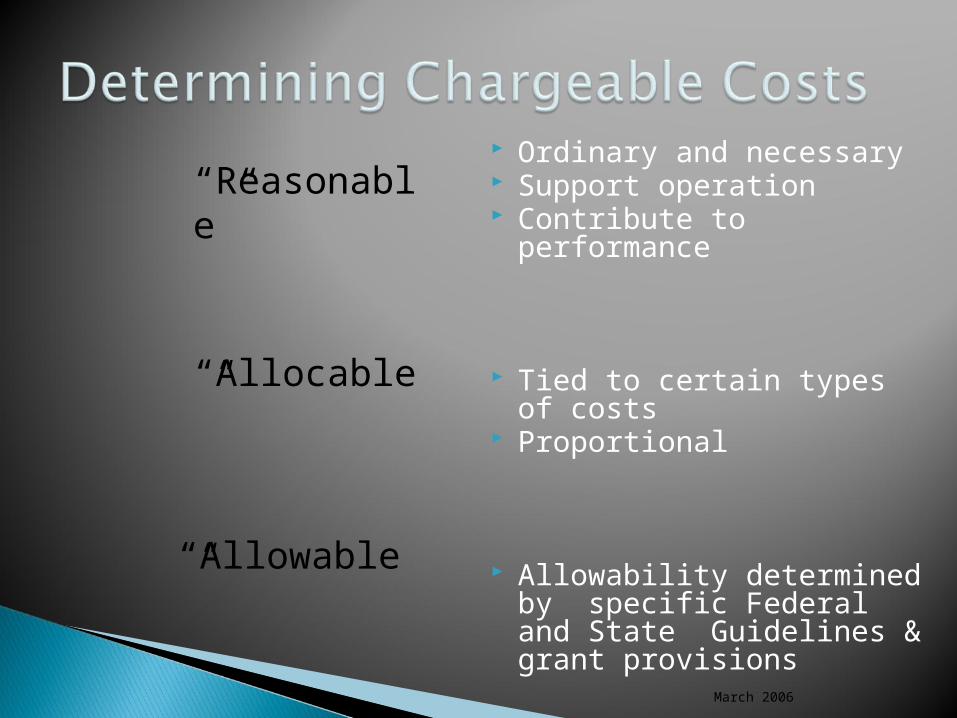

March 2006

Ordinary and necessary Support operation Contribute to performance

Tied to certain types of costs

Proportional

Allowability determined by specific Federal and State Guidelines & grant provisions

“Reasonable”

“Allocable”

“Allowable”

What funds are available to cover these costs (e.g. grants, in-kind donations, etc.)

Work closely with Finance Department. They – along with Executive Director - help determine funding for your program.

Make your case to your Executive Director, so she/he can make the case to the Board of Directors.

If you did your homework, you can make a strong case.

Ultimately, it’s the Executive Director and Board of Directors final decision to approve the entire operating budget of the agency.

Be prepared to inform our entire program staff of program budget approval.

Closely monitor your budget by working closely with the Finance Department.

REMEMBER: Your program budget is a powerful tool which empowers you to be a good steward of funds and – ultimately – to help support the survivors in your community throughout the year.

1) Identify and quantify the budget need2) Research and identify potential funders.3) Carefully read the application and what is

required.4) Make the case. Good writers, good eyes.5) Provide good outcomes and solid data.6) Prepare and attach the proposed budget.7) Copies Signatures Submit Wait

Award!SUBMITTING A PROPOSAL IS A TEAM

PROCESS!

1) Understand what the obligations are for the grant via the award letter and contract.

2) Write down all report deadlines.3) Know how to complete a funder’s

grant report.4) Educate your staff.5) Track all numbers – programmatic

and financial (see sample)

6) Remember what is reasonable, allocable and allowable.

7) Complete the report carefully and submit on-time.

8) Keep good and open communications with your grant manager/monitor.

9) Keep an excellent filing system.10) When in doubt, ask for help.

2010 Recipient Handbook:

http://www.oes.ca.gov/WebPage/oeswebsite.nsf/PDF/2010%20CalEMA%20Criminal%20Justice%20Programs%20Recipient%20Handbook/$file/TOC%20INDEX%201000-14000%20FINAL.pdf