emerging issues in government accounting & … 2013.pdfemerging issues in government accounting...

TRANSCRIPT

Emerging Issues in Government Accounting & Auditing

AGA Southeast Region PDC

Nashville, Tennessee April 5, 2013

R. Kinney Poynter, Executive Director,

NASACT

1

Today’s Agenda

• State Fiscal Outlook • Legislative and Regulatory Issues • Changing World of Audit Standards • Other Emerging Issues on the Radar

2

State Fiscal Outlook

Improving but Slowly…

3

State Fiscal Outlook For FY 2013

• Fiscal 2013 projections show aggregate expenditures and revenues continue to improve

• For many states, general fund revenues and expenditures still below fiscal 2008

• States recovering, but not recovered 4

State Government Challenges FY 2013

• Improved revenue growth, but not enough

to go around… • Federal government • Health care changes, implementation • Long-term liabilities

5

Federal Overhang…

• Sequester • Debt ceiling • Many program authorizations are set to

expire • “Grand bargain” tax reform?

6

Aaa Municipal Credit Indirectly Linked to U.S. Government

• 4 of 15 Aaa-rated states placed on negative outlook: MD,

MO, NM, VA • 40 of 440 Aaa-rated local governments have similar

vulnerabilities; some also have healthcare-related funding exposure to nursing homes and hospitals. These ratings have also been placed on negative outlook.

• If the US rating were to be placed on review or downgraded, the ratings on the linked entities would be placed on review or downgraded as well.

8

National Economic Indicators

• 4th quarter GDP grows a modest 0.1% – 3rd Quarter GDP increased 3.1% – 14th straight quarter of at least some growth

• Federal Reserve projects 2.3%-3.0% growth in 2013

• Other economic figures: – Unemployment rate at 7.7% in February – Manufacturing grows for 3rd consecutive month in

February – New Home Sales rose 15.6% in January

General Fund Expenditure Growth

-8

-6

-4

-2

0

2

4

6

8

10

12

%

General Fund Expenditure Growth (%)

*35-year historical average rate of growth is 5.6 percent *Fiscal ‘13 numbers are appropriated Source: NASBO Fall 2012 Fiscal Survey of States

* Average

9

Spending Still Below FY 2008

Source: NASBO Fall 2012 Fiscal Survey of States

General Fund Revenue

Source: NASBO Fall 2012 Fiscal Survey of States

State Tax Revenue

» State revenues continue to grow, albeit at a slower pace » Tax collections have increased on a year-over-year basis for eleven straight quarters,

through 4Q2012.

» If states meet their current forecasts for fiscal 2013, they would surpass their pre-recession peak.

» State liquidity has improved, exhibited by a lower number of states borrowing externally for cash flow purposes.

-30

-20

-10

0

10

20

30

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012*

Year-Over-Year Quarterly Percentage Change in State Tax Revenue

Total Tax Collections Personal Income Tax Sales Tax

* 4th Quarter results from 2012 are preliminary

Source: - Moody’s; chart source - Rockefeller Institute of Government

12

States Continue To Rebuild Reserves After Recession

Source: NASBO Fall 2012 Fiscal Survey of States

Minimal Mid-Year Budget Cuts in FY 2012

14

28

35

22

9 8 13

7 2 3 1

16

37 37

18

5 2 4

13

43 39

19

8

0

10

20

30

40

50

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

Num

ber

of S

tate

s

($ in

Mill

ions

)

Budget Cuts Made After the Budget Passed ($ millions)

Number of states Amount of reduction

Recession ends

Recession ends Recession ends

Strategies Used to Reduce or Eliminate Budget Gaps – FY 2013

• Reduce Local Aid: 8 states • Layoffs: 9 states • Furloughs: 3 states • Cuts to Employee Benefits: 9 states • Across-the-Board Cuts: 13 states • Targeted Cuts: 21 states • Rainy Day Fund: 4 states • Reorganize Agencies: 10 states

15

16

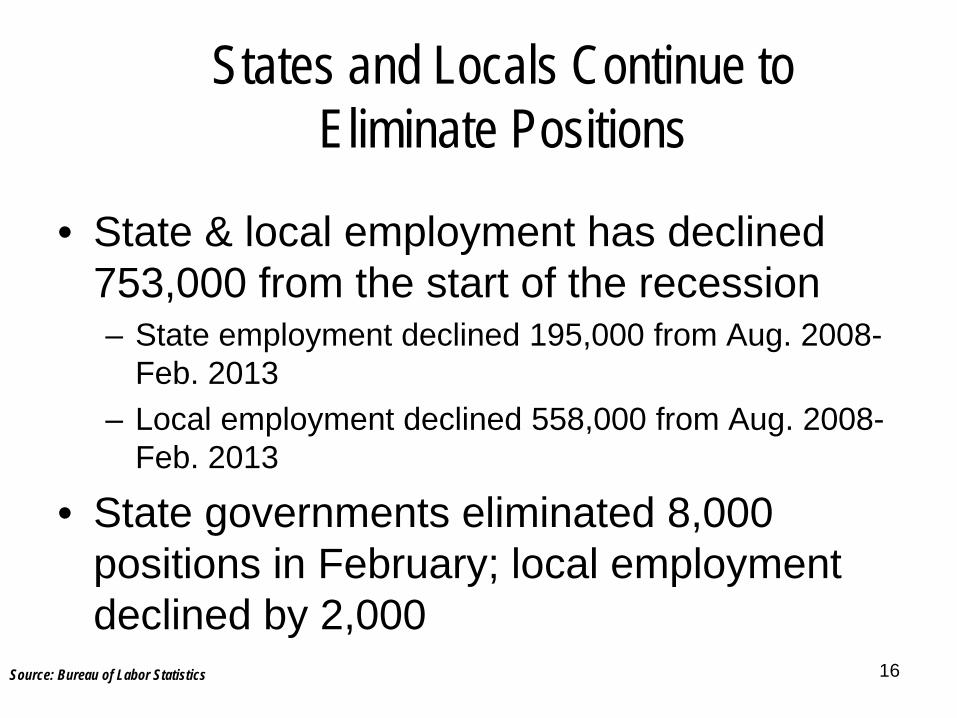

States and Locals Continue to Eliminate Positions

• State & local employment has declined 753,000 from the start of the recession – State employment declined 195,000 from Aug. 2008-

Feb. 2013 – Local employment declined 558,000 from Aug. 2008-

Feb. 2013

• State governments eliminated 8,000 positions in February; local employment declined by 2,000

Source: Bureau of Labor Statistics

Shrinking Public Payrolls

17 Source: Wall Street Journal 3-25-13

19

Spending by Funding Source

General Funds39.8%

Federal Funds31.2%

Other State Funds26.5% Bonds

2.5%

Total State Expenditures By Funding Source, Estimated Fiscal 2012

Source: NASBO State Expenditure Report

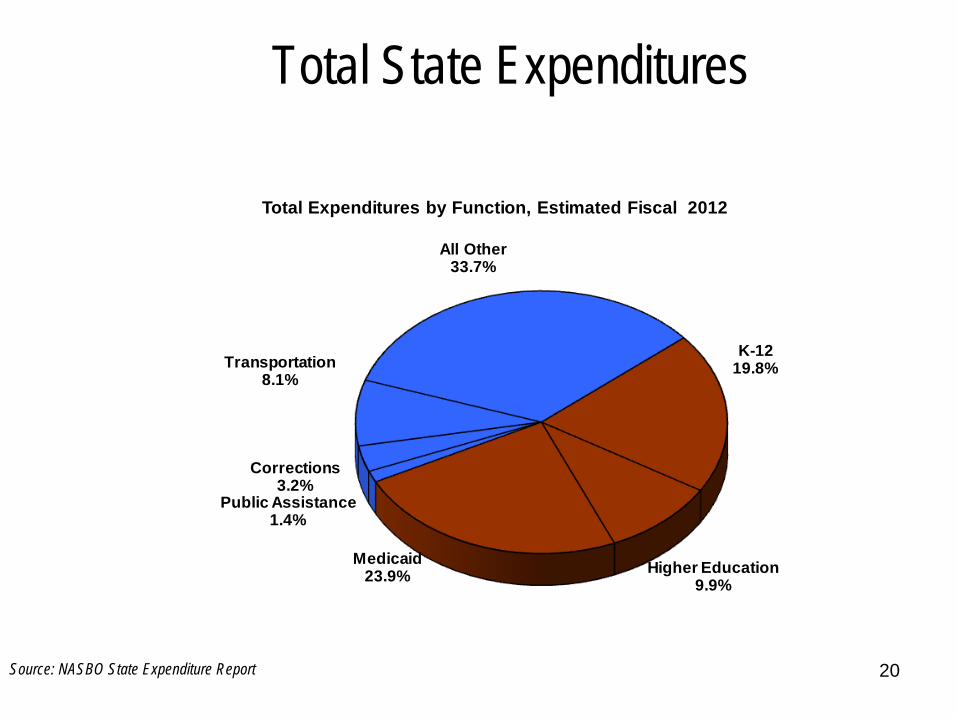

Total State Expenditures

K-1219.8%

Higher Education9.9%

Medicaid23.9%

Public Assistance1.4%

Corrections3.2%

Transportation8.1%

All Other33.7%

Total Expenditures by Function, Estimated Fiscal 2012

Source: NASBO State Expenditure Report 20

21

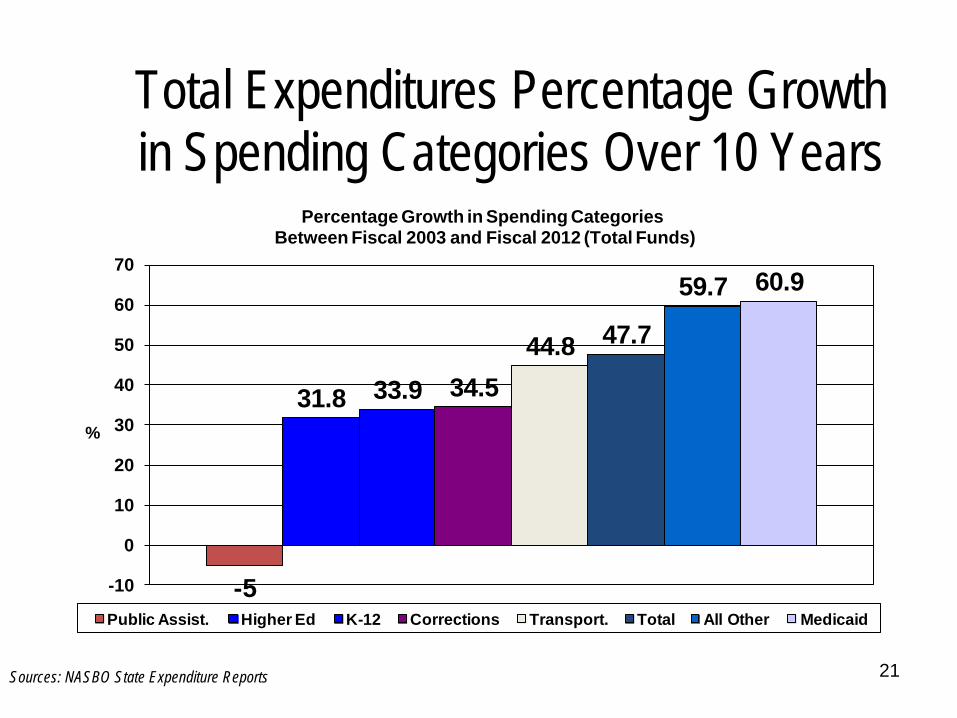

Total Expenditures Percentage Growth in Spending Categories Over 10 Years

-5

31.8 33.9 34.544.8 47.7

59.7 60.9

-10

0

10

20

30

40

50

60

70

%

Percentage Growth in Spending CategoriesBetween Fiscal 2003 and Fiscal 2012 (Total Funds)

Public Assist. Higher Ed K-12 Corrections Transport. Total All Other Medicaid

Sources: NASBO State Expenditure Reports

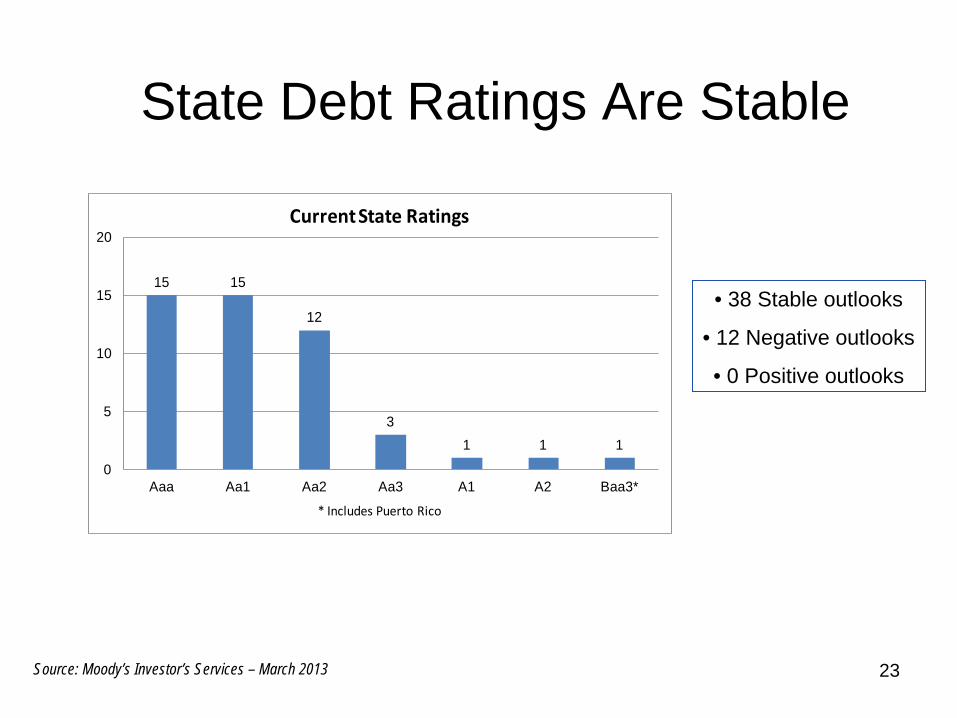

State Debt Ratings Are Stable

• 38 Stable outlooks

• 12 Negative outlooks

• 0 Positive outlooks

15 15

12

31 1 1

0

5

10

15

20

Aaa Aa1 Aa2 Aa3 A1 A2 Baa3*

Current State Ratings

* Includes Puerto Rico

23 Source: Moody’s Investor’s Services – March 2013

24

State Fiscal Outlook

• Below average budgets for at least the next several years

• Health care reform implementation • Tough competition for general funds

and limited federal funds – Wind down of Recovery Funds

• Dealing with long-term liabilities • States will continue to make some

painful choices

Legislative and Regulatory Issues

Things You Need to Know…

25

Dodd–Frank

• Dodd-Frank Wall Street Reform and Consumer Protection Act (Public Law 111-203; signed on July 21, 2010) – Noteworthy provisions include:

• A new mechanism to fund GASB • Regulation and registration of municipal financial

advisors

26

Dodd-Frank

• GASB Funding (§978) – SEC may require a national securities

association (FINRA) to establish a reasonable annual accounting support fee

– FINRA will assess its members based on municipal securities trading volume reported to MSRB

– SEC approved FINRA’s model for GASB support fee on February 23, 2012

• Effective immediately

27

Dodd-Frank

• Regulation of Municipal Financial Advisor (§975) – SEC proposed permanent rules in December

2010 – Created a very sweeping definition that does

not include either an “engaged in business” or a compensation component as a requirement, both of which have been core elements of the existing regulatory scheme

28

Dodd-Frank

• Regulation of Municipal Financial Advisor (§975) (cont.) – Current definition excludes a “municipal entity

or an employee of a municipal entity” – Elected member of a governing body is

considered an “employee” but non-elected members are not

• Very controversial since appointed members must register under current proposed rule

– Still awaiting final rule from the SEC • “Could still be months away” – John Cross, SEC

29

SEC Concerns with the Municipal Market

• Field hearings started in 2010 exploring various aspects of the muni market including: – disclosure and transparency – financial reporting and accounting – investor protection and education

• Final report released on July 31, 2012 – http://www.sec.gov/news/press/2012/2012-

147.htm

30

SEC Concerns with the Municipal Market

• Key recommendations – Legislative:

• Provide the SEC with the authority to set requirements for issuer disclosure including:

– Timeframes, frequency, content (including financial statements and other financial information)

• Amend the Securities Act so that conduit issuers are no longer exempt

– Would subject conduit issuers who use municipal securities to finance their projects to SEC registration and disclosure requirements

31

SEC Concerns with the Municipal Market

• Key recommendations (cont.) – Legislative:

• Provide the SEC with the authority to establish form and content of financial statements, including the authority to recognize standards of a private sector body (presumably GASB) as generally accepted for federal securities laws and provide the SEC with attendant authority over such body

• Provide the SEC with the authority to require issuers to have their financial statements audited whether by an independent auditor or state auditor

32

SEC Concerns with the Municipal Market

• Key recommendations (cont.) – Legislative:

• Provide safe harbor from private liability for forward looking statements

• Provide a mechanism to enforce compliance with continuing disclosure agreements

– Regulatory • SEC could update current interpretative guidance

on disclosure obligations – Would consider areas where improvements are needed

especially related to disclosure of financial statements

33

SEC Concerns with the Municipal Market

• Key recommendations (cont.) – Regulatory

• SEC could amend 15(c)2-12 – Could mandate more specific disclosures related to risks

of municipal securities and disclosures – Could further require that issuers have disclosure

policies in place and increase use of websites

• SEC would continue working with the MSRB to further enhance EMMA

• SEC could encourage the use of industry best practices and promote the development of additional guidelines and best practices

34

SEC Concerns with the Municipal Market

• Next steps at this point are uncertain: – Congress has a lot on its plate currently

• Concerns over the municipal market may not rise to the top

– New SEC chair soon • Confirmation of Mary Jo White is expected soon

– Her interest in the municipal bond market is yet to be determined

– Government organizations will continue to monitor closely 35

Money Market Funds

• Recommendation by the Financial Stability Oversight Council (FSOC) – FSOC created in Dodd Frank to address

threats to U.S. financial system – Money market mutual funds should be valued

on a “floating” basis (current market value) instead of a “stable” net asset value (NAV)

• FSOC issued this recommendation despite the SEC’s rejection of similar proposals

36

Money Market Funds

• Proposal is very controversial since: – Governments purchase MMMFs as part of

their investment portfolios. Changing to a floating would require changes to laws.

– Would be inconsistent with SEC’s definition of 2a7-like investment pools. Changes in some GASB standards would be necessary.

– MMMFs are the largest investors of S-T muni bonds. This change may make MMMFs less attractive to investors, limiting the MMMFs’ purchasing power.

37

OMB Grant Reform Proposals

• Proposed OMB Uniform Guidance: Cost Principles, Audit, and Administrative Requirements – Issued in Federal Register on February 1,

2013 • Builds on past Presidential directives • http://www.whitehouse.gov/sites/default/files/omb/fi

nancial/grant_reform/proposed-omb-uniform-guidance-for-federal-financial-assistance.pdf

• Comment deadline extended to June 2, 2013 • Reforms finalized by the end of 2013

38

OMB Proposals

• Consolidates 8 existing circulars – Designed to reducing burden and target

improper payments, waste, fraud, and abuse • Reform ideas are in three primary areas:

1. Audit requirements (Circulars A-133, A-50) 2. Cost principles (Circulars A-21, A-87, A-122) 3. Administrative requirements (the

government-wide Common Rule implementing Circulars A-89, A-102, A-110)

39

Audit Requirements – Single Audit

• Audit Threshold – Raise threshold from $500,000 to $750,000

• Would reduce audit burden on approx. 5,000 smaller entities while maintaining audit coverage of more than 99% of federal awards

• ANPG’s proposed for a “more focused” single audit for entities expending between $1 - $3 million has been deleted.

40

Audit Requirements – Single Audits

• Major Program Determination (changes impact all four steps in the process) – Increase the minimum threshold for a

program to be Type A from $300,000 to $500,000 (Step 1)

• But, not change the alternative 3% of total federal awards expended.

41

Audit Requirements – Single Audits

• Major Program Determination (cont.) – Refocus the criteria for a Type A program to

qualify as high-risk (Step 2) • Revised criteria would result in a Type A program

being designated as a high-risk only when in the most recent period:

– the program failed to receive an unqualified opinion; – had a material weakness in internal controls; or – had questioned costs exceeding five percent of the

program’s expenditures.

42

Audit Requirements – Single Audits

• Major Program Determination (cont.) – Reduce the burden associated with Type B

programs: • Reduce the number of high risk Type B programs

that must be tested as major programs from at least one-half (50%) to at least one-quarter (25%) of the number of low-risk Type A programs. (Steps 3 and 4)

• Allow the auditor to stop the Type B program risk assessment process after this number of high risk Type B programs are identified. (Steps 3 and 4)

43

Audit Requirements – Single Audits

• Major Program Determination (cont.) – Simplify the calculation to determine relatively

small Type B programs for which the auditor is not required to perform a risk assessment

• Change from the current stepped approach to a flat 25% of the Type A/B threshold. (Step 3)

– This change allows more Type B programs to be classified as relatively small.

44

Audit Requirements – Single Audits

• Major Program Determination (cont.) – Reduce the minimum coverage required from

50% for a regular auditee and 25% for a low-risk auditee to: (Step 4)

• 40% for a regular auditee and • 20% for a low-risk auditee.

45

Audit Requirements – Single Audits

• Questioned Costs – Increase the minimum threshold for reporting

from $10,000 to $25,000 • Will help focus on the audit findings presenting the

greatest risk.

• Streamlining Types of Compliance – Goal is to focus on those requirements

presenting the greatest risk to improper payments, waste, fraud, and abuse

• Would reduce the audit burden

46

Audit Requirements – Single Audits

• Streamlining Types of Compliance (cont.) – The “Keepers” (7)

• Activities Allowed or Unallowed – Including “matching” and “period of availability” to verify

allowability

• Cost Principles • Cash Management • Eligibility • Reporting • Subrecipient Monitoring • Special Tests and Provisions

47

Audit Requirements – Single Audits

• Streamlining Types of Compliance (cont.) – Eliminated (7)

• Davis Bacon • Equipment and Real Property Management • Matching, Level of Effort, and Earmarking • Period of Availability of Federal Funds (except

where tested to verify allowable/unallowable costs) • Procurement and Suspension and Debarment • Program Income • Real Property Acquisition & Relocation Assistance

48

Audit Requirements – Single Audits

• Streamlining Types of Compliance (cont.) – OMB will consider requests from agencies to

add one or more compliance requirements back under Special Tests and Provisions

• Will only be accepted when compliance is required by statute or regulation and

• When the federal agency – makes a strong case of how non-compliance could result

in increased risk – Provides a targeted compliance supplement write-up

identifying improper payment risks and focusing on audit tests to address these risks

49

Audit Requirements – Audit Follow-Up

• The proposal strengthens follow-up by federal agencies by (Circular A-50) – Requiring a senior accountable official to oversee

the overall audit resolution. – Requiring agencies to use audit risk metrics. – Encouraging agencies to engage in cooperative

audit resolution. – Encouraging agencies to be more proactive in

resolving weaknesses and deficiencies. – Digitizing Single Audit reports.

50

Audit Requirements – Pass-Through Entities & Subrecipients

• Cross-agency coordination: – Makes clear that it is the responsibility of the

cognizant or oversight agency to coordinate audits or reviews by other federal agencies that are made in addition to the Single Audit.

– Responsibilities include, among other things, coordination of a management decision for cross-cutting findings.

– Goal is to reduce redundancy and burden.

51

Audit Requirements – Pass-Through Entities & Subrecipients

• Audit follow-up: – For subrecipients receiving the majority of

their awards directly from the federal government, the cognizant or oversight agency are the most appropriate entity to conduct audit follow-up on audit findings that cut across programs.

– Goal is to eliminate duplicative audit follow-up work performed by a pass-through entity without providing significant additional work to federal agencies. 52

Audit Requirements – Pass-Through Entities & Subrecipients

• Audit follow-up (cont.): – Proposal addresses this issue by making

management decisions available through the FAC.

• Cognizant or oversight agency will provide management decisions for all findings in which it has funds directly implicated, and

• Will make those management decisions publicly available so that other federal awarding agencies and pass-through entities may decide to rely on them, or may decide to issue their own decisions, as appropriate.

53

Audit Requirements - Timeliness

• Timeliness – Reduction in the amount of time for audit

submission from nine to six months was suggested by many in the federal agency and audit community

• OMB “supports this idea” but notes that legislative changes would be necessary.

– Current reporting deadline remains nine months (for now)

54

Cost Principles

• Some of the changes are being proposed to reform federal cost principles include: – Consolidate various cost circulars into one. – Introduce a mandatory or optional flat rate

option for indirect cost rate setting. – Direct pilots for exploring alternatives to time-

and-effort reporting for salaries and wages. – Clarify that budgeting for contingency funds

with a federal award of IT systems are okay. – Allow for idle capacity in data centers.

55

Administrative Requirements (Common Rule)

• Reforms to administrative requirements could include: – Consolidate various requirements in A-102

and A-110 into one uniform set. – Require pre-award consideration based on

proposal’s merit and applicant’s financial risk. – Require agencies to provide 90-day notice of

funding opportunities. – Provide a standard format for announcement

for funding opportunities.

56

Transparency Reporting

No Longer a Catchy Phrase…It’s Here to Stay!

57

ARRA

• American Recovery and Reinvestment Act – Signed into law on February 17, 2009

• Public Law 111-5 • Total funding – $862 billion • Approximately $280 billion to the states • Recovery funding from 28 federal agencies

• Required quarterly reporting of ARRA expenditures

• Things have been pretty quiet – Activity is now winding down

58

From ARRA to FFATA

• Federal Financial Accountability and Transparency Act (9/26/06; P.L. 109-282) – Also known as “The Transparency Act” – Requires reporting of federal awards and

contracts at prime/first-tier sub levels – OMB Memorandum Guidance – OMB Compliance Supplement

• Contains a section on Single Audit considerations

59

From FFATA to DATA

• Digital Accountability and Transparency Act (DATA) – H.R. 2146 (June 2011) – Makes several major pro-transparency

reforms, including: • Reporting quarterly expenditures for all grants and

contracts • Creating the Federal Accountability and Spending

Transparency Board (FAST Board) – Bill passed the House on April 25, 2012; Sen.

Warner (VA) currently working with House on companion bill 60

Changing World of Audit Standards

61

New Standards Issued

• Government Auditing Standards – GAO issued new standards in December

2011 – Conceptual framework for independence

• AICPA Clarity Standards – Massive project at the Auditing Standards

Board to reduce complexity of all existing auditing standards

62

Government Auditing Standards

• The new conceptual framework for independence requires that auditors: 1. Identify threats to independence 2. Evaluate the significance of the threats

identified 3. Apply safeguards, when necessary, to

eliminate the threats or reduce them to an acceptable level

4. Determine if the threat level is acceptable 63

AICPA “Clarity Project”

• Massive project to reduce complexity • Major milestone reached with issuance of

SAS No. 122 (October 2011) – Brings together and codifies 39 clarified SASs

that the ASB had finalized, but had not issued – Effective for audits of financial statements for

periods ending on or after December 15, 2012 • Codification issued April 2012 • www.aicpa.org/SASClarity

64

Other Emerging Issues on the Radar

65

COSO Framework

• Established in 1992 by the Committee of Sponsoring Organizations

• ED released in December 2011: – Provides “fresh, modern approach” with

examples for modern business environment – Original five components stay the same but

will now have 17 principles • Final framework expected in May 2013

– www.ic.coso.org

66

Control Environment

Risk Assessment

Control Activities

Information & Communication

Monitoring Activities

Summary of Updates Codification of 17 principles embedded in the Original Framework

1. Demonstrates commitment to integrity and ethical values 2. Exercises oversight responsibility 3. Establishes structure, authority and responsibility 4. Demonstrates commitment to competence 5. Enforces accountability

6. Specifies relevant objectives 7. Identifies and analyzes risk 8. Assesses fraud risk 9. Identifies and analyzes significant change

10. Selects and develops control activities 11. Selects and develops general controls over technology 12. Deploys through policies and procedures

13. Uses relevant information 14. Communicates internally 15. Communicates externally

16. Conducts ongoing and/or separate evaluations 17. Evaluates and communicates deficiencies

67

FAF’s Proposal – GASB Agenda

• Issued February 26, 2013 • Result of the FAF’s independent academic

study examining stakeholders’ views on the scope of GASB’s authority – Two controversial projects:

• SEA and Financial Projections

• Proposal has three groups of information – FAF will determine whether group 2 items are

appropriate for GASB agenda. 68

GASB Projects • Pension Accounting

– GASB recently issued Statements No. 67 (plans) and 68 (employers)

• New standards change from a net pension obligation (NPO) approach to a net pension liability (NPL) approach

• Will clearly separate funding pension plans from employer’s accounting and reporting for such plans

• More liability on the balance sheet is expected • Effective dates

– 67: FYE beginning after June 15, 2013 – 68: FYE beginning after June 15, 2014

69

GASB Projects

• Economic Condition: Financial Projections – PV released December 6, 2011 – Five year projections of:

• Major individual inflows of resources • Major individual outflows of resources • Major individual financial obligations • Annual debt service payments • Narrative discussion of major intergovernmental

service interdependencies – Report in CAFR’s RSI

70

Public Pension Transparency Act

• H.R. 567 introduced by Rep. Nunes (R-CA), Ryan (R-WI) and Issa (R-CA) – Challenges the validity of current state and

local government pension accounting – Mandates federal reporting requirements

regarding their pension costs including use of discount rate based on U.S. obligations

– Penalties include losing tax exempt status – Also prohibits any future federal bailouts

71

Pension Disclosures – Official Statements

• National Association of Bond Lawyers – Provide “considerations” to NABL members in

preparing pension disclosures in O/S – Include portions of core documents (e.g.,

sponsor’s f/s, system’s f/s, actuarial report, etc.) that the issuer considers material

– Additional disclosure may be necessary if issuer believes there are negative trends in unfunded liabilities

– Final version released May 15, 2012 • http://www.nabl.org

72

Pension Funding

• Guide for Elected Officials – March 2013 – Issued by Pension

Funding Task Force (Big 7, GFOA, and NASACT)

– http://www.nga.org/files/live/sites/NGA/files/pdf/2013/1303PensionFundingGuideBrief.pdf

– Key message - Fund the ARC!!

73

Moody’s Evaluation of S&L Government Pension Plans

• Proposal will “bring greater transparency and consistency to the analysis of pension liabilities.” – Final document due in April 2013

• Ratings on states are not likely to change – However, “the proposed adjustments would

nearly triple fiscal 2010 reported unfunded actuarial accrued liability (“UAAL”) for the 50 states and our rated local governments”

74

Moody’s Evaluation of S&L Government Pension Plans

• Four principal adjustments to as-reported pension information: 1. Multiple-employer cost-sharing plan liabilities

will be allocated to specific government employers based on proportionate shares of total plan contributions

2. Accrued actuarial liabilities will be adjusted based on a high-grade long-term corporate bond index discount rate (5.5% for 2010 and 2011)

75

Moody’s Evaluation of S&L Government Pension Plans

• Four principal adjustments to as-reported pension information (cont.): 3. Asset smoothing will be replaced with

reported market or fair value as of the actuarial reporting date

4. Annual pension contributions will be adjusted to reflect the foregoing changes as well as a common amortization period

76

Tax Reform

• Tax reform may impact state and local governments in a variety of ways: – Limiting the tax exemption of municipal bond

interest for high income earners – Eliminating the tax exemption for municipal

bonds all together – Limiting deductibility of state and local income

taxes

77

MD

AK

HI

WA

OR

CA

ID

NV

MT

WY

UT CO

AZ NM

ND

SD

NE

KS

OK

TX

MN

IA

MO

AR

LA

WI

IL

MI

IN

KY

TN

MS AL GA

FL

OH

WV VA

NC

SC DC

DE

PA NJ

NY

CT

RI

MA

VT NH

ME

State Establishing State-Run Exchange State Will Partner with Feds State Will Have Federal Exchange as Default

Source: 2013 NCSL Research and NCSL Health Reform: State Legislative Tracking Database

Health Care Exchanges – Where States Stand

78

These Continue to be Interesting Times…

79