emerging issues in government accounting & auditing€™s agenda • state fiscal outlook •...

TRANSCRIPT

Emerging Issues in Government Accounting & Auditing36th Annual TennesseeGovernment Auditing Training Seminars

1

Today’s Agenda• State Fiscal Outlook• Legislative and Regulatory Issues• Uniform Guidance Implementation• Accounting and Auditing Issues• Other Emerging Issues

2

State Fiscal OutlookCloudy with a Chance of Storms….

3

NATIONAL OVERVIEW

GDP growth: 1.6% in 2016 compared to 2.6% in 2015 (lowest since 2011)Missed projections (1.8% to 2.2%)

Recession: WSJ panel of economists 21% chance in 2017; nearly 60% in next four years

Unemployment rate: 4.5% in March 20174.7% at end of 2016

Jobs:March 2017 – 98,000 (the 78th straight month of positive job creation)2016 – 180,0002015 -230,000

Interest rates:Fed Reserve raised rates .25% in March 2017. Third increase since the Great Recession.

Stock Market:2016 – DJIA up 15%“Trump Bump” – S&P 500 up 6% from election day to inauguration day

Source: NASBO 2017

STATE FISCAL OVERVIEW

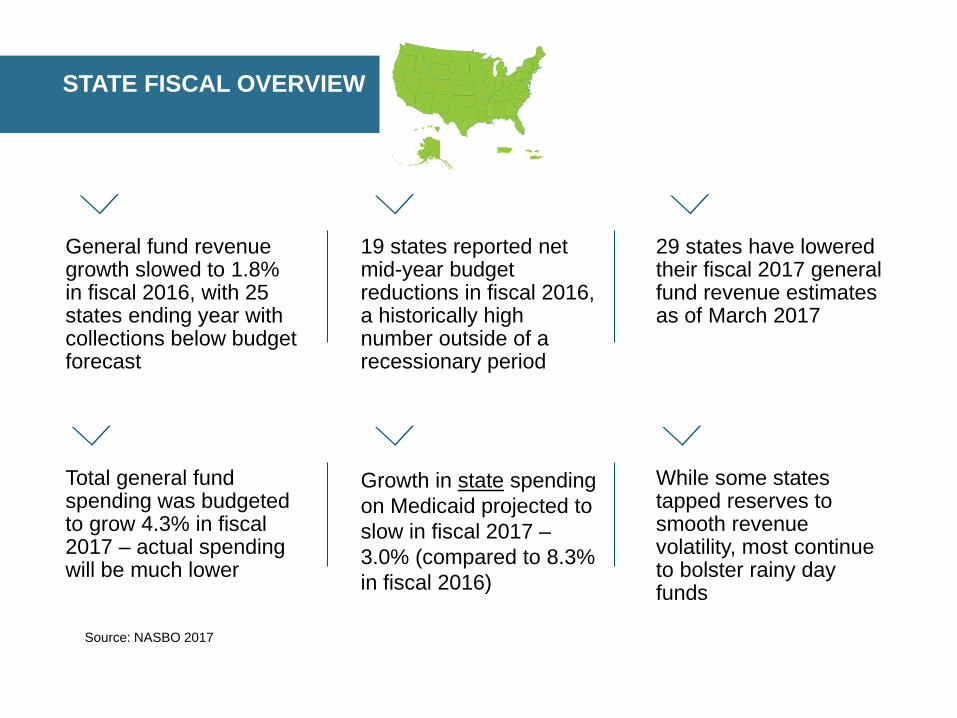

General fund revenue growth slowed to 1.8% in fiscal 2016, with 25 states ending year with collections below budget forecast

29 states have lowered their fiscal 2017 general fund revenue estimates as of March 2017

Total general fund spending was budgeted to grow 4.3% in fiscal 2017 – actual spending will be much lower

Growth in state spending on Medicaid projected to slow in fiscal 2017 –3.0% (compared to 8.3% in fiscal 2016)

While some states tapped reserves to smooth revenue volatility, most continue to bolster rainy day funds

19 states reported net mid-year budget reductions in fiscal 2016, a historically high number outside of a recessionary period

Source: NASBO 2017

FISCAL 2016 GENERAL FUND SPENDINGSTILL BELOW INFLATION-ADJUSTED PRE-RECESSION PEAK

General Fund Spending: FY 2008 – FY 2017

$687

$661

$623$645

$667

$695

$726

$758

$786

$820

$794*

$550

$600

$650

$700

$750

$800

$850

FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017

(in b

illion

s)

Source: NASBO Fiscal Survey of States; Fiscal 2017 figure is based on states’ enacted budgets.*Aggregate spending level would need to total $794 billion in fiscal 2016 to be equivalent with real 2008 spending level.

Enacted Budget Cuts Made After the Budget Passed

20

28

35

22

9 813

72 3 1

16

37 37

18

5 2 4

13

41 39

23

811

814

19

0

10

20

30

40

50

$0

$5

$10

$15

$20

$25

$30

$35

$40

Num

ber o

f Sta

tes

$ In

Billio

ns

Number of states Amount of reduction

Recession ends

Recession ends Recession ends

Source: NASBO Fiscal Survey of States

19 STATES MADE MID-YEAR BUDGET CUTS IN FISCAL 2016, TOTALING $2.8 BILLION

GENERAL FUND REVENUE

8

STATE REVENUE RECOVERED MORE SLOWLY AFTER 2007 RECESSION (ROCKEFELLER INSTITUTE)

REVENUES BELOW PROJECTIONS IN MANY STATES IN FISCAL 2016 AND 2017 General Fund Revenue Collections Compared to Original Budget Projections

36

9 10 7

20

7

25 24

2

9 56

5

4

516

12

32 35 37

25

39

204

0

5

10

15

20

25

30

35

40

45

50

2010 2011 2012 2013 2014 2015 2016 2017*

Num

ber o

f Sta

tes

Fiscal Year

HigherOn TargetLower

Source: NASBO Fiscal Survey of States.*Fiscal 2017 figures are based on data collected early in fiscal year. Not all states were able to report for fiscal 2017.

HOW ARE WE DOING IN 2017?

11

FISCAL 2017 REVENUE GROWTH SO FAR

Fiscal 2017 general fund revenue forecasts increase of 2.2%˃ PIT +3.5%, Sales

+3.1%, and CIT -1.3%

˃ Declines in 9 States

Fiscal 2017 general fund revenues through January increased by 1.7%˃ PIT +3.4%, Sales

+2.9%, and CIT -9.1%

˃ Declines in12 States

• PIT = personal income tax; CIT = corporate income tax Source: 2016 State Expenditure Report & States’ Own Reports

Fiscal 2016 general fund revenues increased by 1.8%˃ PIT +2.9%, Sales

+3.2%, and CIT -5.8%

˃ Declines in 15 States

STATE SAVINGS ACCOUNTS(RAINY DAY FUNDS)

13

STATES CONTINUE TO STRENGTHEN RAINY DAY FUNDS29 STATES REPORTED INCREASES IN FISCAL 2016; 25 STATES PROJECT INCREASES FOR FISCAL 2017

Rainy Day Fund Balances, Fiscal 2008 to Fiscal 2017

*FY2016 totals exclude Georgia, and FY 2017 totals exclude Georgia and Oklahoma. Source: NASBO Fall 2016 Fiscal Survey

$32.9$29.0

$21.0$24.7

$34.3

$41.3

$47.7 $47.8 $48.2 $47.7

$23.0

$13.8

$3.0$6.7

$12.3

$18.8

$25.4$28.9

$31.9 $34.0

$0

$10

$20

$30

$40

$50

$60

2008 2009 2010 2011 2012 2013 2014 2015 2016* 2017*

In b

illio

ns

Blue = Total statesRed = Excluding AK & TX

STATES CONTINUE TO STRENGTHEN RAINY DAY FUNDS SINCE HITTING RECENT LOW IN FISCAL 2010-2011

Median Rainy Day Fund Balance Over Time

Source: NASBO Fall 2016 Fiscal Survey

4.6%

0.7%

4.9%

2.0%

5.1%

0%

1%

2%

3%

4%

5%

6%

Perc

ent o

f Gen

eral

Fun

d Sp

endi

ng

Fiscal Year

STATE SPENDING TRENDS

16

State General Fund Spending Continues to Grow Moderately for Seventh Consecutive Year

Annual General Fund Expenditure Growth (%)

4.4 3.7 4.3

-8

-6

-4

-2

0

2

4

6

8

10

12

%

*Average

*38-year historical average annual rate of growth is 5.5 percent *Fiscal 2017 numbers are enacted.

Source: NASBO Fiscal Survey of States

K-12, 19.4%

Higher Ed, 10.2%

Transp. 7.9%

Corrections 3.0%

Public Assistance,

1.4%

All Other, 29.2%

Medicaid, 29.0%K-12

21.6%

Higher Education

10.2%

Transp. 7.9%

Corrections3.5%Public

Assistance1.7%

All Other34.5%

Medicaid 20.7%

TOTAL STATE EXPENDITURES BY FUNCTION

FISCAL YEAR 2008$1,479 Billion

FISCAL YEAR 2016$1,928 Billion

Source: NASBO State Expenditure Report. Total state expenditures include all federal and state funds. Percentages based on 50-state totals.

FEDERAL OUTLOOK FOR STATES

19

20

1 2

3 4

FEDERAL UNCERTAINTY FOR STATES

The Affordable Care Act, especially Medicaid – Per capita caps, Expansion, Flexibility

Tax Policy Considerations –municipal debt, border-adjusted corporate tax, state/local tax deductibility

Infrastructure The Fiscal 2017 Budget vs. the 2018 Budget

CHALLENGES: LONG TERM BEGINS NOW

• Tighter Resources for Years

• Demographic Changes

• Debt and Pension Liability

• Infrastructure

• Medicaid Changes and Federal Budget Cuts

Legislative and Regulatory Issues

Municipal Disclosures – SEC Proposes Amendments to Rule 15c2-12

• Proposal issued on March 1, 2017– Improves investor protection and enhances

transparency in municipal securities market• Addresses concern about private bank lending

– Comments due by May 15, 2017– 111 pages in length!– Effective date: three months after adoption

• Adds two new event notices under continuing disclosure undertakings– Currently there are 14 listed events– Requires notice within 10 days of the

occurrence

24

Municipal Disclosures – SEC Proposes Amendments to Rule 15c2-12

• Two new events are:– Incurrence of a financial obligation of the

issuer, if material, or agreement to covenants, events of default, remedies, priority rights, or other similar terms of a financial obligation, any of which affect security holders, if material

– Default, event of acceleration, termination event, modification of terms, or other similar events under the terms of the financial obligation of the issuer of obligated person, any of which reflect financial difficulties

25

Municipal Disclosures – SEC Proposes Amendments to Rule 15c2-12

• “Financial Obligation” is defined as:– A debt obligation,– Lease,– Guarantee,– Derivative instrument, or– Monetary obligation resulting from a

judicial, administrative, or arbitration proceeding.

26

Municipal Disclosures – SEC Proposes Amendments to Rule 15c2-12

• What should be disclosed?– A description of the material terms of the

financial obligation, including:• Date of incurrence• Principal amount• Maturity and amortization• Interest rate (or method of computation of the

interest rate)• Default rates

27

Municipal Disclosures – Material Events

• Just a reminder - the current 14 material events:– Principal and interest payment delinquencies– Non-payment related defaults– Unscheduled draws on debt service reserves reflecting financial stress– Unscheduled draws on credit enhancements reflecting financial stress– Substitution of credit or liquidity providers, or their failure to perform– Adverse tax opinions or events affecting the tax-exempt status– Modifications to rights of security holders– Bond calls and tender offers– Defeasances– Release, substitution or sale of property securing security repayment– Rating changes– Bankruptcy, insolvency or receivership– Merger, acquisition or sale of all issuer assets– Appointment of successor trustee

28

High Quality Liquid Assets (HQLA)

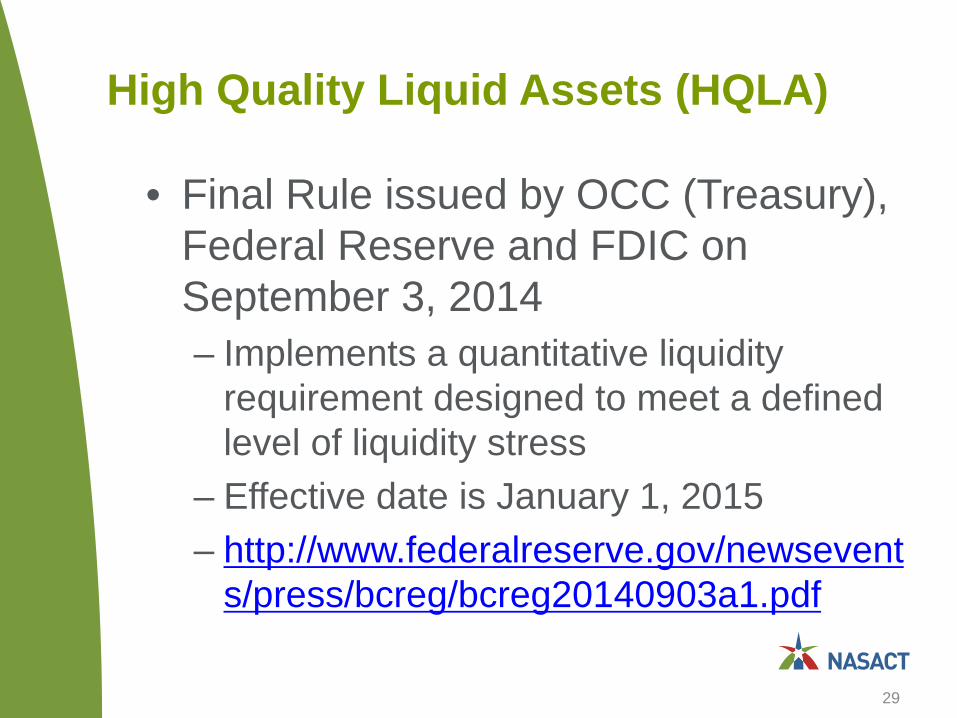

• Final Rule issued by OCC (Treasury), Federal Reserve and FDIC on September 3, 2014– Implements a quantitative liquidity

requirement designed to meet a defined level of liquidity stress

– Effective date is January 1, 2015– http://www.federalreserve.gov/newsevent

s/press/bcreg/bcreg20140903a1.pdf

29

High Quality Liquid Assets (HQLA)

• Concerns:– Excludes municipal securities from the

definition of “High Quality Liquid Assets” (HQLAs)

• Will increase borrowing costs for municipal issuers

• Reduce market liquidity, increase volatility• Disadvantage U.S. municipal securities

relative to foreign governments• Impact collateralization of public funds

30

High Quality Liquid Assets (HQLA)

• Recent developments– Federal Reserve (April 1, 2016)

• Issued final rule that would treat some municipal securities as level 2B liquid assets

– Must be backed by the full faith and credit of a state or municipality– Would still need to meet the “liquid and readily marketable

standard”

• Treasury and FDIC still exclude munis as HQLA– Congress

• HR 1624 introduced in House in March 2017– Treats munis that are investment grade and readily marketable as

level 2A• SB 828 introduced in Senate on April 6, 2017

– Treats munis as level 2B

31

CHOICE Act

• H.R. 5983– Jeb Hensarling (TX-R), Chairman of the

House Committee on Financial Services• Passed in committee on September 13, 2016• Must be reintroduced in 115th Congress

– Proposed legislation would repeal various sections of the Dodd-Frank Act

• Including section 978 (GASB funding!)– State and local government

organizations will monitor this closely!32

DOL – Overtime Expansion

• DOL has finalized its proposal to raise the threshold income level at which workers are exempt from overtime pay– From $23,660 to $47,476 per year (or from$455

to $913 per week) for salaried employees– Effective date is December 1, 2016– Final Rule and State and Local Fact Sheet

https://www.dol.gov/WHD/overtime/final2016

• Federal judge issued nationwide injunction on November 23, 2016– DOL must now formally appeal

33

OMB Uniform Guidance

34

OMB Uniform Guidance

• Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (“Uniform Guidance”)– Final Rule issued on December 26, 2013

• Contained in 2 CFR Part 200 • Effective dates:

– Federal agencies on December 13, 2014– Subpart F audit requirements are applicable to fiscal years

beginning on or after December 26, 2014

– Interim Rule (for agencies) issued on December 19, 2014– Resources:

• http://www.whitehouse.gov/omb/grants_docs/• https://cfo.gov/cofar/

35

Grant Reform Implementation

• OMB continues to work on a series of FAQs to clarify the guidance – Most recent update in September 2015

• Currently 100 FAQs• Next round of FAQs are expected in Spring 2017

• Technical correction issued in September 2015

• OMB has developed metrics to identify if the reforms have achieved the stated purpose of increasing efficiencies and reducing burden

• Rule revision expected for exposure in Spring 2017

36

Implementation Issues

• Risk Assessments for Type B programs (200.518)– All high-risk Type B programs identified through

risk assessment must be tested as major– If you risk assess too many Type B programs,

you will over audit• Example: With 10 low-risk Type A programs, you only

need to select 3 high-risk Type B programs (25%). But, if you conduct risk assessments on 10 Type B programs and 7 are deemed high risk, you will have to audit all 7 as major programs.

• Key: Stop risk assessing Type B programs when the threshold is met!

37

Current Developments: “Smoothing” of Major Programs

• Heavy Audit Burden in Year 3 (2018)– New high-risk criteria will cause more Type

A programs to be deemed low-risk• However, all Type A programs must still be tested

as major at least once every three years– As a result, there will be a heavy audit burden in year

3 due to large number of low-risk Type A programs that must be tested as major

• “Smoothing” of major programs over three-year period is a solution

– 2016 Compliance Supplement allowed “smoothing” technique

• Appendix VII - Other Audit Advisories

38

Current Developments: Pension Plan Costs Allowability

• Section 200.431(g)(3)– “For entities using accrual based

accounting, the cost assigned to each fiscal year is determined in accordance with GAAP”

• GASB 68 calculated pension costs differ from the amounts funded

– HHS DCA is currently disallowing amounts funded in excess of GASB 68 amount (but awaiting OMB guidance)

– OMB will issue a proposed revision in Spring 2017

39

Current Developments: Testing SFA Cluster as Major

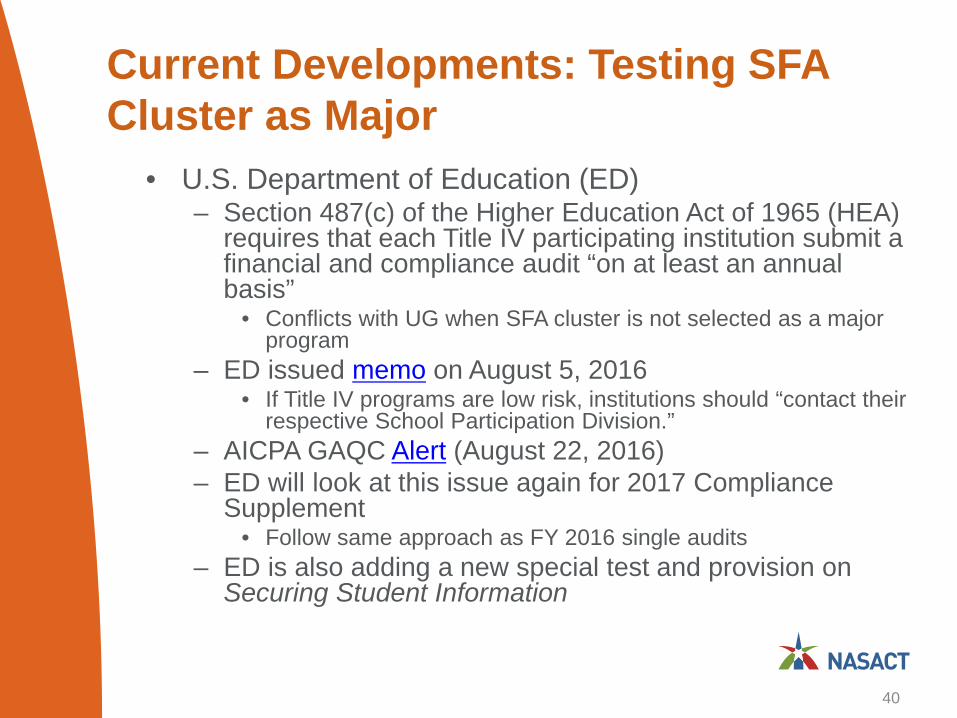

• U.S. Department of Education (ED)– Section 487(c) of the Higher Education Act of 1965 (HEA)

requires that each Title IV participating institution submit a financial and compliance audit “on at least an annual basis”

• Conflicts with UG when SFA cluster is not selected as a major program

– ED issued memo on August 5, 2016• If Title IV programs are low risk, institutions should “contact their

respective School Participation Division.”– AICPA GAQC Alert (August 22, 2016)– ED will look at this issue again for 2017 Compliance

Supplement• Follow same approach as FY 2016 single audits

– ED is also adding a new special test and provision on Securing Student Information

40

CFDA Number – Changes Coming Soon!

• New Schematic– Numbering construct associated with CFDA

numbers will be changed from ##.#### to ###.####

• Prefix will align with 3-digit Common Government-wide Accounting Classification (CGAC) agency code used in the Treasury Account Symbol (TAS) listed in Circular A-11, Appendix C

• Suffix is changed to 4 digits to allow additional space for future entries

– Effective October 1, 2018• CFO Council alert for more information

41

Transparency IssuesFFATA, DATA Act

Increasing Transparency: The Continuing Story

• ARRA (2009)– Final report May 2014

• FFATA (2006)– Monthly reporting of federal awards and

contracts at prime/first-tier sub levels – Ongoing

• DATA (2014)– Amends FFATA

43

DATA Act: Full Disclosure of Federal Funds

• Any funds expended by a Federalagency (or component) must be reported monthly (when practicable) but not less than quarterly– 10 specific items are listed, e.g.,

• amount of budget authority appropriated• amount obligated • accounts from which the appropriations

are obligated, etc.

44

DATA Act: Data Standards

• Government-wide financial data standards shall be established for all federal funds and be used by bothfederal agencies and recipients

• Must include common data elements for financial and payment information– Goal is to improve the usability,

transparency and accountability of financial and performance information

45

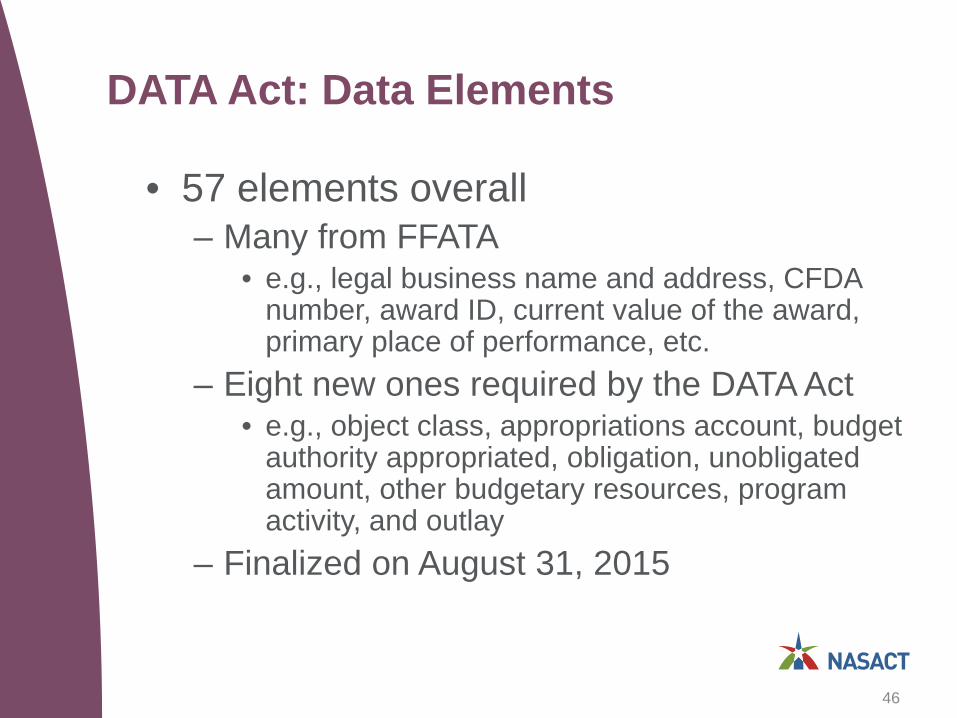

DATA Act: Data Elements

• 57 elements overall– Many from FFATA

• e.g., legal business name and address, CFDA number, award ID, current value of the award, primary place of performance, etc.

– Eight new ones required by the DATA Act• e.g., object class, appropriations account, budget

authority appropriated, obligation, unobligated amount, other budgetary resources, program activity, and outlay

– Finalized on August 31, 2015

46

DATA Act: Section 5 Pilot Program –Current Test Models

• Consolidated Federal Financial Report (FFR, SF 425) – FFR is currently submitted through multiple

entry systems– Hypothesis

• A “single point of entry” would be more efficient than submitting the same data on multiple forms to multiple reporting avenues

– Test• Working with Administration for Children and

Families (ACF) to test ACF’s grant recipient reporting consolidated FFR into the Payment Management System

47

DATA Act: Section 5 Pilot Program –Current Test Models

• Single Audit Reporting (two items)– Combined DCF and SEFA– Common Notice of Award (NOA) Cover Sheet

• Hypothesis– Some data on the DCF and SEFA are

duplicative; burden can be reduced– Standardized NOA would facilitate access to

standardized data needed for SA reports• Testing

– Currently developing “Long Form SF-SAC”– Standardized NOA will be developed by

Grants.gov; focus group will test efficiency gains

48

DATA Act: Timeline/Deadlines

• May 2015– Establish data standards

• May 2017– Federal agencies must report spending data

using data standards• August 2017

– OMB must report Section 5 pilot results• May 2018

– Federal agencies must post spending data in machine-readable formats

49

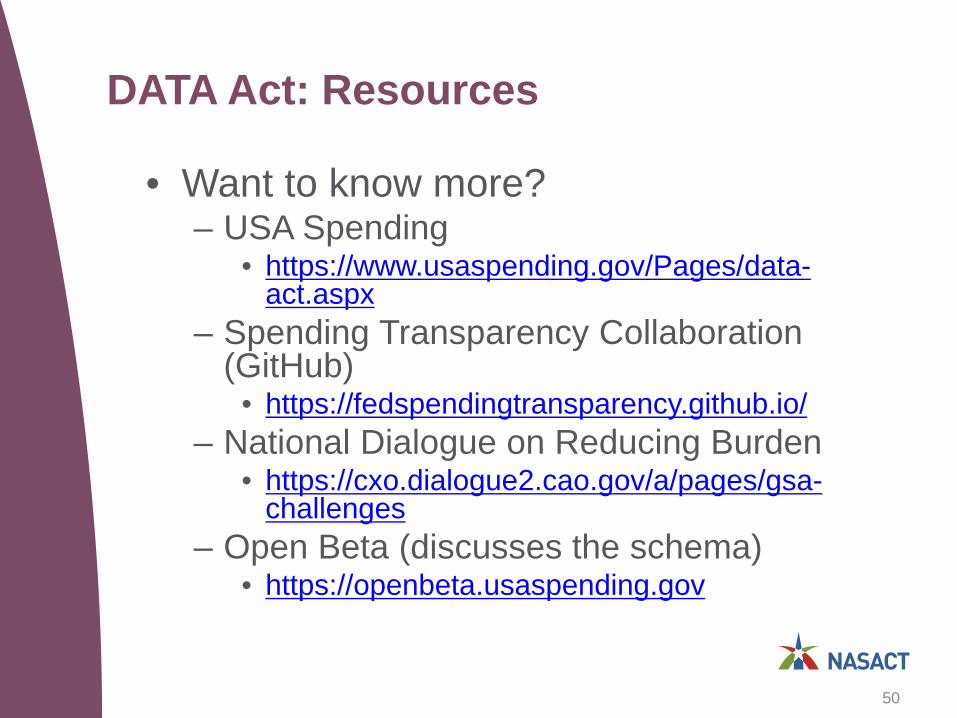

DATA Act: Resources

• Want to know more?– USA Spending

• https://www.usaspending.gov/Pages/data-act.aspx

– Spending Transparency Collaboration (GitHub)

• https://fedspendingtransparency.github.io/– National Dialogue on Reducing Burden

• https://cxo.dialogue2.cao.gov/a/pages/gsa-challenges

– Open Beta (discusses the schema)• https://openbeta.usaspending.gov

50

Accounting Issues

GASB 74 and 75 – Other Postemployment Benefits (OPEB)

• Release and effective dates– Final statements issued in June 2015

• Statement 74 – Plans• Statement 75 - Employers

– Effective dates• Plans – June 2017• Employers – June 2018

52

GASB 74 and 75 – Other Postemployment Benefits (OPEB)

• Built on the new pension standards– Designed to improve OPEB information

for:• decision-making and accountability purposes• comparability across governments• transparency

– Establishes standards for: • liabilities • deferred inflows and outflows of resources• expense/expenditures

53

GASB’s Reexamination of the Reporting Model

• Added to technical agenda on September 1, 2015

• Targeted review (not “wholesale” changes)

• First phase of the project– Financial Reporting Model Improvements

– Governmental Funds– Invitation to Comment (ITC) released

December 7, 2016

54

GASB’s Reexamination of the Reporting Model: Governmental Funds

• ITC addresses potential improvements for financial reporting of governmental funds, including:– Recognition approaches (measurement focus

and basis of accounting)– Format of the governmental funds statement of

resource flows– Specific terminology– Reconciliation to the government-wide

statements– For certain recognition approaches, a statement

of cash flows

55

GASB’s Reexamination of the Reporting Model: Governmental Funds

• ITC introduces three alternative recognition approaches for governmental fund financial statements:– Near-term financial resources– Short-term financial resources, and– Long-term financial resources

• These three approaches fall on a continuum—from a closer-to-cash approach at one end to a closer-to-economic resources approach on the other

56

GASB’s Reexamination of the Reporting Model – What’s Next?

• Items that will be included in the Preliminary Views:– Government-Wide Statement of Activities

• Consider alternatives for the format of the statement of activities.

– Proprietary Fund Financial Statements• Consider reporting alternatives related to the existing

requirement to separately present operating and nonoperating revenues and expenses.

– Budgetary Comparisons• Consider the appropriate method of communication (as a basic

financial statement or required supplementary information) for budgetary comparison information and which budget variances, if any, should be required to be presented.

– Permanent Funds• Consider alternatives for reporting information about permanent

funds.

57

GASB’s Reexamination of the Reporting Model – What’s Next?

• Items that will be included in the Exposure Draft:– Management’s Discussion and Analysis

• Consider alternatives for enhancing financial statement analysis, eliminating boilerplate components that are no longer necessary for understanding the financial reporting model, and

• Clarify guidance for presenting currently known facts, decisions, or conditions that are expected to have a significant effect.

– Debt Service Fund Presentation• Consider alternatives for providing additional information about

debt service funds (either individually or in aggregate).– Extraordinary and Special Items

• Consider alternatives to improve the consistency of application of the guidance for reporting extraordinary and special items.

– Other Issues• Consider alternatives that could permit more timely financial

reporting or that could reduce complexity overall.

58

GASB’s Reexamination of the Reporting Model – What’s Next?

• Timing– Deliberations begin in October 2015– Due process document at end of 2016– July 2018: Preliminary Views– April 2020: Exposure Draft– November 2021: Final Statement– Implementation dates: sometime in 2022,

2023

59

FASB Releases New NFP Accounting Guidance

• FASB issued an Accounting Standards Update (ASU) on August 18, 2016 (Topic 958)– First major change to NFP financial reporting since

FASB 117 (1993)– Key issues addressed:

• Complexity of net asset classifications– Replaces the existing three classes of net assets with two new

classes that focus on donor restrictions• Deficiencies in information about liquidity and availability

of resources• Lack of consistency on expenses and investment return• Enhance the utility of the statement of cash flows

• Visit FASB’s website here for more

60

Auditing Issues

Government Auditing Standards

• “Yellow Book” or• Generally

Accepted Government Auditing Standards (“GAGAS”)

62

GAO’s Government Auditing Standards

• Exposure Draft issued April 6, 2017– First proposed changes since 2011– Comment period ends July 6, 2017– Why Issued?

• Represents a modernized version that takes into account developments in the accounting and auditing professions

• Intended to reinforce principles of transparency and provide a framework for high quality government audits

– Effective date: to be determined– http://gao.gov/yellowbook/overview

63

GAO’s Government Auditing Standards

• Some of the key proposed changes:1. New format and organization of GAGAS2. Independence threats related to

preparing records and financial statements

3. Independence guidance related to three-party arrangements

4. Independence guidance related to professional services in government

5. GAGAS qualification for CPE requirement

64

GAO’s Government Auditing Standards

• Key proposed changes (cont.):6. CPE guidance for 24-hour and 56-hour

requirements7. Peer review requirements8. Internal control: financial audits,

examination engagements, and performance audits

9. New requirements for waste10.Standards for reviews of financial

statements

65

GAO’s Government Auditing Standards

• Formatting Changes and Realignment– Requirements will be differentiated from

application guidance (“clarity format”)• “must” and “should” statements are

highlighted in the requirements– Supplemental Guidance (Appendix from

2011) is either removed or incorporated into individual chapters

66

GAO’s Government Auditing Standards

• Chapter reorganization and realignment– Chapter 1: Foundation and Principles– Chapter 2: General Requirements– Chapter 3: Ethics, Independence, Professional Judgment– Chapter 4: Competence and CPE– Chapter 5: QC and Peer Review – Chapter 6: Standards for Financial Audits– Chapter 7: Standards for Attestation Engagements and

Reviews of Financial Statements– Chapter 8: Fieldwork Standards for Performance Audits– Chapter 9: Reporting Standards for Performance Audits

67

GAO’s Government Auditing Standards

• Independence Threats: Preparing Accounting Records and Financial Statements (3.89)– Any services performed by auditors related to

preparing accounting records and FS, other than those defined as impairments, create significant threats to auditors’ independence

– Auditors should:• Document the threats and safeguards applied to

eliminate and reduce threats to an acceptable level OR

• Decline to perform the service

68

GAO’s Government Auditing Standards

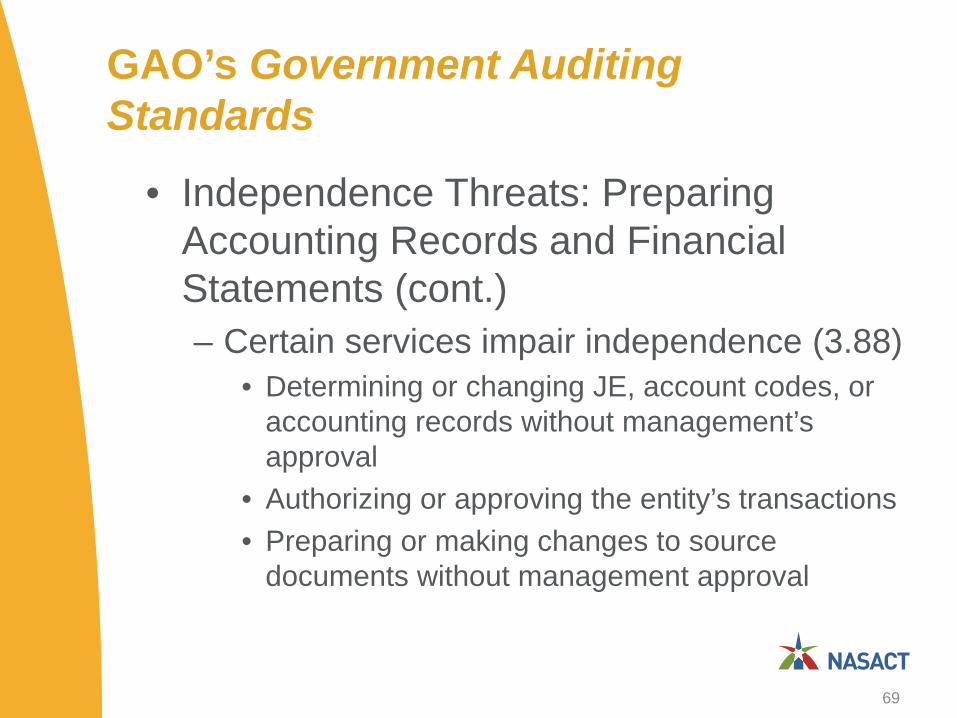

• Independence Threats: Preparing Accounting Records and Financial Statements (cont.)– Certain services impair independence (3.88)

• Determining or changing JE, account codes, or accounting records without management’s approval

• Authorizing or approving the entity’s transactions• Preparing or making changes to source

documents without management approval

69

GAO’s Government Auditing Standards

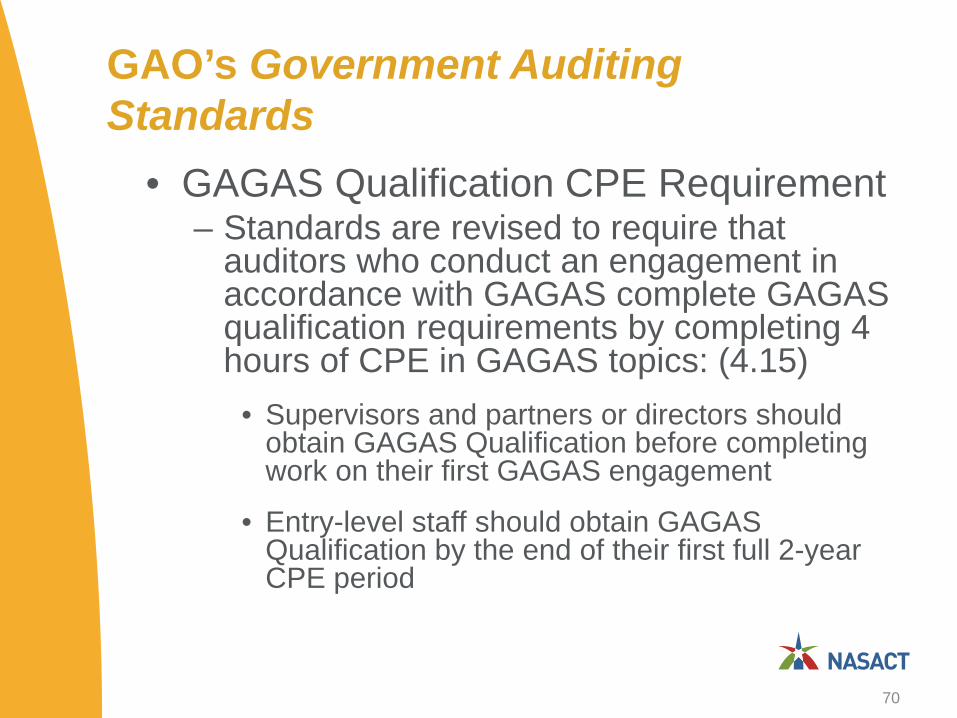

• GAGAS Qualification CPE Requirement– Standards are revised to require that

auditors who conduct an engagement in accordance with GAGAS complete GAGAS qualification requirements by completing 4 hours of CPE in GAGAS topics: (4.15)

• Supervisors and partners or directors should obtain GAGAS Qualification before completing work on their first GAGAS engagement

• Entry-level staff should obtain GAGAS Qualification by the end of their first full 2-year CPE period

70

GAO’s Government Auditing Standards

• GAGAS Qualification CPE Requirement (cont.)– To update their GAGAS Qualification, auditors

should complete at least 4 hours of CPE in GAGAS topics each time the Comptroller General issues a revision of GAGAS (4.17)

• These CPE hours should be completed by the end of each auditor’s next full 2-year CPE period after the GAGAS revision is issued

• CPE Q&A document (2005) is superseded

71

GAO’s Government Auditing Standards

• Peer Review Requirements– The standards for peer review are revised to

differentiate requirements for those audit organizations affiliated with a recognized organization (5.64)

– Standards require that audit organizations affiliated with a recognized organization comply with the respective organization’s peer review requirements and additional GAGAS peer review requirements in areas such as:

1. selection of GAGAS engagements,

2. peer review report ratings, and

3. availability of peer review report to the public

72

GAO’s Government Auditing Standards

• Peer Review Requirements (cont.)– Standards require that audit organizations not

affiliated with a recognized organization comply with GAGAS peer review requirements in areas such as: (5.65)

• Peer review scope• Peer review intervals• Written agreement for peer review• Peer review team• Follow-up on prior peer review• Assessment of peer review risk• Report content• Peer review report ratings• Audit organization’s response to the peer review report• Availability of the peer review report to the public

73

GAO’s Government Auditing Standards

• New Requirements for Waste– For financial audits, examination engagements, and

performance audits, standards are expanded to require that auditors perform audit procedures to ascertain the potential effect on the audit objectives if they become aware of waste (6.16, 7.18, 8.69)

• Auditors are required to report when waste has occurred that is material or has a significant effect on the audit objectives for financial audits, examination engagements, and performance audits (6.35, 7.41, 9.32)

• Auditors are required to communicate in writing waste that does not have a material or significant effect on the audit objectives but warrants the attention of those charged with governance for financial audits, examination engagements, and performance audits (6.39, 7.42, 9.33)

74

GAO’s Government Auditing Standards

• What is Waste? (6.17, 7.19, 8.75)– The act of using or expending resources

carelessly, extravagantly, or to no purpose. – Waste involves the taxpayers not receiving

reasonable value for money in connection with any government-funded activities because of an inappropriate act or omission by parties with control over or access to government resources.

– Waste can include activities that do not include abuse and does not necessarily involve a violation of law. Rather, waste relates primarily to mismanagement, inappropriate actions, and inadequate oversight.

75

GAO’s Government Auditing Standards

• Standards for Reviews of Financial Statements– Statement on Standards for Accounting

and Review Services No. 21, Section 90 (Review of Financial Statements) is incorporated for auditors conducting reviews of financial statements in accordance with GAGAS (7.01)

76

Other Emerging IssuesThings on the radar…

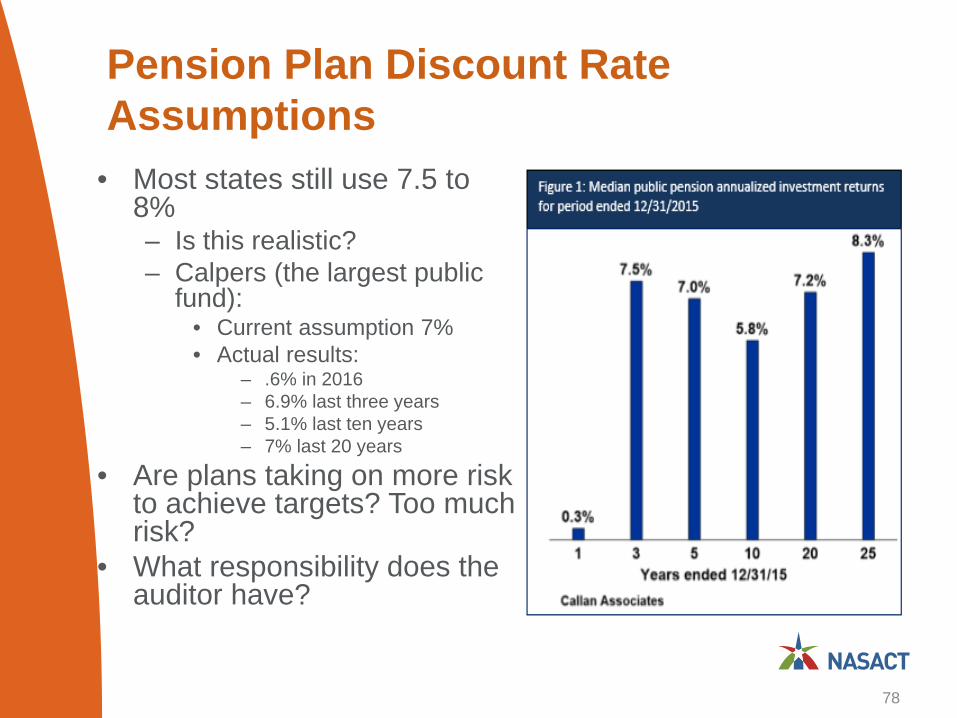

Pension Plan Discount Rate Assumptions

• Most states still use 7.5 to 8%– Is this realistic?– Calpers (the largest public

fund):• Current assumption 7%• Actual results:

– .6% in 2016– 6.9% last three years– 5.1% last ten years– 7% last 20 years

• Are plans taking on more risk to achieve targets? Too much risk?

• What responsibility does the auditor have?

78

Alternatives to Public Financing: Bank Loans and Direct Purchases

• SEC– Increasingly concerned about increased activity

and lack of disclosure• Private placement - $24 billion in 2014

• MSRB, FINRA– Firms must assess whether a financing

instrument is a security or a loan• Many “notes” (loans) should be securities?• www.msrb.org

• GASB– Current research activity

• Debt Disclosures, including Direct Borrowing -Reexamination of Statements 34, 38, and 62

79

These continue to be interesting times…

80